iffco project

TRANSCRIPT

PROJECT REPORT

ON

“TRANSPORT MANAGEMENT”

OF

IFFCO AONLA”

SUBMITTED IN PARTIAL FULFILMENT OF THEREQUIREMENTS OF THE AWARD OF THE DEGREE OF

BECHLOR OF BUSINESS ADMINISTRATION

SUBMITTED BY:SAURABH TYAGI

1

Expression of sincere gratitude is just a partial acknowledgment. The accomplishment of this project “TRANSPORT MANAGEMENT” I would have not been possible vocabulary falls short of word to express my sincere gratitude to Mr. D R Kundra (Deputy GM, Finance) and Mr. Rajan Kumar Keshri (Sr. Accounts Officer) under whose guidance I had the opportunity to carry out the present work. I am very thankful to Mr. D. Kalia, Chief Manager (Training ) & Mr.

K.K. Pandey, Dy. Manger (Training) who supported me & helped me throughout

the project. I am also thankful to Mr. Yogish Kumar Pundir and Mr. A.K. Mishra,

who provided me with relevant information and spared their precious time with me.

I am thankful to Finance & Account staff & to all the employees of IFFCO

who cooperated with me during my training period.

I OWE A DEEP SENSE OF GRATITUDE TO ALL THE RESPONDENTS

WHO GAVE ME VALUABLE INFORMATION FOR THE PROJECT.

2

42 YEARS OF COOPERATING GLORY

3

LIST OF CONTENTS Page No.

1) Introduction to topic 6

2) Objective of study 7

3) Research Methodology 8

4) Introduction about IFFCO 9-17

5) Objective of the company 18

6) Management 19-21

7) Aim, Vision, Mission 22-23

8) Vision 2010, Approach 24

9) Commitment, Principles 25

10) IFFCO’s Emblem 26

11) Organization chart of IFFCO 27

12) All India share of IFFCO 28

13) Performance highlights 29

14) IFFCO Associates 30

15) Awards galore 31-32

16) Aonla unit 33-38

17) Finance and accounts department 39-43

18) Inventory management 44-46

19) Various sections of inventory 47-52

20) Imported material 53

21) Material coding 54-55

22) Packing & Dispatch 56

23) Document for dispatch of goods. 57-58

24) Accounting of raw material 59-61

4

25) Store section 62

26) Verification of Inventories. 63-66

27) Techniques of Inventory control 67-70

28) Criteria for judging the Inventory system 71-72

29) Inventory software 73

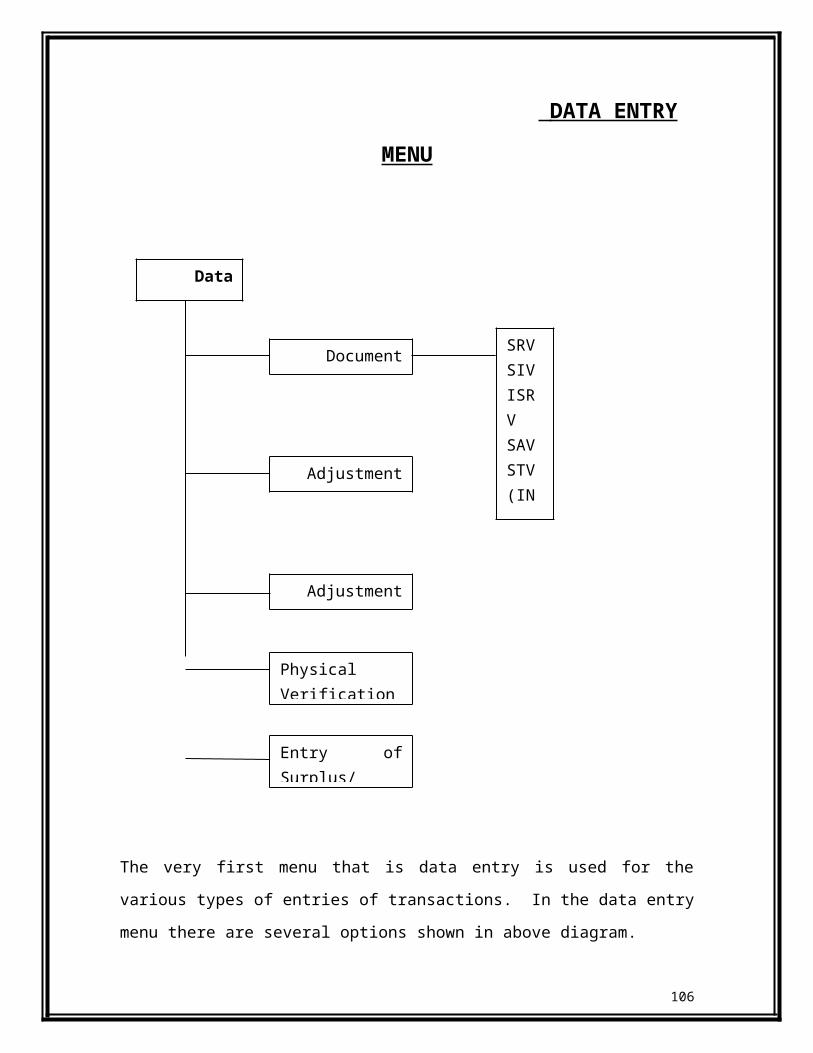

30) Data Entry menu 74-75

31) Reports Menu 76-82

32) Production department 83-86

33) Different vouchers 87-96

34) Rejection/Discreption Report 97-98

35) Tender enquiry 99

36) Performance bank guarantee 100-101

37) Material purchase Requitions 102

38) Store adjustment voucher 103

39) SWOT Analysis & Strategies 104-107

40) Conclusions & Recommendations 108-109

41) Bibliography 110

5

INTRODUCTION TO THE TOPIC

INVENTORY MANAGEMENT

“Managing the level of inventory is like maintaining the level of water in a bath tub with

an open drain. The water is flowing out continuously. If water is let in too slowly, the tub

is soon empty. If the water is let in too fast, the tub overflows.”

The dictionary meaning of inventory is ‘stock of goods’. The investment in inventory is

very high in most of the undertakings engaged in manufacturing. The amount of

investment is sometimes more in inventory than in other assets. About 90 percent part of

working capital is invested in inventories. It is necessary for every management to give

proper attention to inventory management. A proper planning of purchasing, handling,

storing and accounting should form a part of inventory management. By proper planning

it is possible for a company to reduce its levels of inventories to a considerable degree,

without any adverse effect on production and sales, by using simply inventory planning

and control technique. The reduction in excessive inventories carries a favorable impact

on company’s profitability.

An efficient system of inventory management will determine

1) What to purchase

2) How much to purchase

3) From where to purchase

6

4) Where to store, etc.

“Effective inventory management enables an organization to meet or exceed customers’

expectations of product availability while maximizing net profits or minimizing costs”

7

OBJECTIVE OF STUDY

“The main aim of study is to check the efficiency and effectiveness of inventory

management system at IFFCO Aonla.”

Investment in inventory incurs a high cost. Therefore effective management is necessary

to minimize the cost and ultimately increases profitability of an organization.

Apart from our main objective, our other objectives are:

1) To analyze the level of investment in inventory by IFFCO.

2) To study the inventory policy of the company.

3) To analyze the policy adopted by the company.

4) To analyze the financial position of the company.

5) To give suggestion if any, regarding effective inventory management, to ensure

smooth and uninterrupted supply without making unnecessary investment of

funds in inventory.

8

RESEARCH METHODOLOGY

Research covers the search for retrieval of information for a specific purpose.

Basically research is the objective and systematic method of finding solution to a

problem. The steps followed to conduct this study are as follows:-

(1) Formulating research problem – The problem under study viz. how effective are

the measures applied by Iffco, Aonla to control the inventory is basically studied through

analytical research. Material is important for the efficiency of the system. It is a matter of

great importance for inventory department. Inventory department of IFFCO, Aonla is

responsible for efficient inventory control. Thus the whole study is conducted under the

guidance of officers of this department.

(2) Extensive literature survey – Many published studies, books or material on effective

control of inventory were referred to for getting a true direction to research process.

(3) Data collection – The study is conducted through collection of data through surveys,

interviews with officials etc. Personal interviews were conducted where a set of pre-

conceived questions were asked from the officers of inventory department regarding

material control policies adopted by them. Books of accounts of Aonla –I and Aonla – II are

studied thoroughly to details about inventory stock, cost of material consumed, increase and

decrease in stock in the last few years etc.

Sample of material was obtained randomly. ABC analysis was used where sample

of material was graded under three categories: A, B, C.

(4) Analysis and interpretation – The data about inventory is analysed to find out the

effectiveness and efficiency of inventory policy. As regards the financial performance, the

9

data about different financial indicators is analysed to calculate the different ratios and to

draw the graphs.

INTRODUCTION ABOUT IFFCO

During mid- sixties the co-operative sector in India was responsible for

distribution of 70 per cent of fertilisers consumed in the country. This sector had

adequate infrastructure to distribute fertilisers but had no production facilities of its own

and hence dependent on public/private sectors for supplies. To overcome this lacuna and

to bridge the demand-supply gap in the country, a new cooperative society was conceived

to specifically cater to the requirements of farmers. Thus was born IFFCO, the world’s

largest fertiliser cooperative. It was a unique venture in which the farmers of the

country through their own co-operative societies created this new institution to

safeguard their interests. Indian Farmers Fertiliser Cooperative limited, a multi-state

Cooperative has emerged as a role model for cooperatives Over 42 years of its inception,

IFFCO has turned into a true Cooperative – Of the Farmers, By the Farmers and For the

Farmers. IFFCO has steadily grown in strength and stature from a modest membership of

57 societies in 1967-68 to 39564 societies as on 31st March, 2008. The initial equity

capital of Rs.6 lakh contributed by the cooperatives in 1967-68 has also gone upto a paid-

up capital of Rs.426 crore.

Indian Farmers Fertiliser Co-operative Limited (IFFCO) was registered on

November 3, 1967 as a Multi-unit Co-operative Society. On the enactment of the Multi

state Cooperative Societies Act 1984 which was amended in 2002, the Society is deemed

to be registered as a Multi state Cooperative Society. The Society is primarily engaged in

production and distribution of fertilisers. The byelaws of the Society provide a broad

framework for the activities of IFFCO as a Cooperative Society.

10

A pioneer in this field, IFFCO’s growth reflects its belief in the strength of the

farmer. Several prestigious awards stand testimony to the fact that IFFCO is driven by its

values and the dedication of its people. This is an organisation that believes in fair play

and has always followed transparent and professional practices in corporate governance.

PRODUCTION

The largest producer of fertilisers in the country, IFFCO has five state-of-the-art

plants that ensure its special position. These are considered to be among the best

professionally managed fertiliser plants in the world.

IFFCO had set up the KALOL plant for manufacture of Nitrogenous Fertiliser and

KANDLA plant for manufacture of Phosphoric fertiliser. These plants commenced

commercial production in the year 1974-75. . Another ammonia - urea complex was set

up at Phulpur in the state of Uttar Pradesh in 1981. The ammonia - urea unit at Aonla was

commissioned in 1988. As part of the new vision and in order to augment its complex

fertilizer manufacturing capacity, IFFCO acquired DAP/NPK/NP plant in Paradeep,

Orissa in September 2005. This was a historic moment, for it was the first private sector

unit to be acquired by any Indian cooperative. The Paradeep unit was expected to achieve

an optimal production load during 2008-09. During 2007-08, IFFCO’s plants rolled out

68.47 lakh tonne of fertiliser material comprising 39.63 lakh tonne of urea and 28.84 lakh

tonne of NPK/DAP/NP which bears ample testimony to its superlative performance.

IFFCO’s market share in ‘N’ production is 20 percent and 25 percent in P2O5 produced in

the country. IFFCO has initiated energy saving schemes in all its five ammonia plants at a

cost of Rs. 410 crore

11

MARKETING AND DISTRIBUTION

A strong marketing team and a sound distribution network make the bottom line

secure. Backed by this belief, IFFCO has gone all out to extend its reach, resulting in the

highest-ever sales of fertilizer material this year. With the completion of Kalol Expansion

Project, IFFCO is all set to realize the objective of producing 100 lakh tonne of

fertilizers, thereby attaining the distinction of world leader in fertilizer production. Every

fourth bag of fertilizer produced and every third bag of fertilizer sold in the country

belongs to IFFCO.

Around 40,000 cooperative societies and 158 Farmers Service Centres spread

across 29 states and union territories in India make sure that IFFCO’s

products-NPK/NP/DAP/UREA-are easily available to farmers.

These impressive figures have been made possible largely because of the fact

that IFFCO distributes its products through cooperative channels. Though the cooperative

structure may differ from state to state, the goal is to reach out to each district, taluka and

village and hence sell more.

This year, IFFCO has dispatched around 86 lakh tonne of fertilizer material from

its plants and ports by rail and road. With the aim of delivering to the doorstep of the

farmer in all parts of the country, the organisation hired storage space at more than 1,700

locations.

IFFCO’s Farmers Service Centres not only supply material under one roof, they are

used as contact points for providing technical know-how to farmers. These Centres also

organize promotional programmes such as soil test campaigns and farmers’ meetings.

12

. During 2007-08, IFFCO has notched up a record sale of 93.24 lakh tonne of

fertiliser material comprising of 54.29 lakh tonnes of urea and 38.95 lakh tonne of

NPK/DAP/NP witnessing a growth of 8.3% as against 86.10 lakh tonnes in the previous

year. Best ever marketing productivity also sprang to 6158 tonne/head.

FINANCIAL PERFORMANCE

The society recorded an all time high turnover of Rs.12163 crore during 2007-08

while its pre tax profit stood at Rs.380.52 crore and profit after tax at Rs.257.59 crore.

The society declared a dividend of 20% for its shareholders for seventh successive year.

HUMAN RESOURCE – PUTTING PEOPLE FIRST

No vision, however grand, can be fulfilled without the cooperation of its people.

Recognizing this fact, IFFCO has made a sustained investment in its people, creating an

environment that attracts the best talent. At IFFCO, we see teamwork at its best.

Employees at all levels share a common dream, a dream that is understood in IFFCO’s

Vision 2010. Hence, enhancing skills is of great significance for the organisation.

Other initiatives to help the growth of its people included workshops on human

values, leadership and work ethics. There were also many technical activities that led to

development and skill upgradation. Employees were sponsored for participation I

prestigious both in India and abroad.

With the firm belief that Information and Communication Technology (ICT) helps

the people and the organisation to grow together, IFFCO has augmented its workflow

applications. The Corporate Data Centre in New Delhi has been refurbished with the

latest technology. A new VPN was created to provide round-the-clock connectivity in the

plants, zonal office and head office.

13

IFFCO has, over the years, successfully showcased its image in India and overseas.

Its achievements and its contributions to the farming community are highlighted in

various exhibitions and fairs.

Given the fact that IFFCO acknowledge that people are the key drivers in its growth,

there is little wonder, then, that the work environment here is one that encourages

creativity and nurtures success.

A YEAR OF APPRECIATION (2008-09)

It was a moment of pride for every member when the President of India in the year

2007 lauded IFFCO’s efforts at conserving energy and keeping its consumption at the

lowest level. This National Energy Conservation Award 2008 was among many

accolades IFFCO received for its safety and conservation endeavours from FAI, CII and

Government of India. These awards, interalia, include for Best Production Performance,

Energy Conservation and Efficient Water Management to Phulpur Plant; Awards for Best

Technical Innovation, Safety and Environment Management to Aonla Plant; Energy

Conservation and Industrial Safety Award to Kalol Plant; and SUN and NDTV Green IT

Award to Kandla Plant.

In addition IFFCO has pocketed “SMART WORKPLACE AWARD” in the

manufacturing and industrial segment by the prestigious Economic Times, Acer Intel

Smart Workplace Award. At the world communications awards in London its associate

IKSL has been conferred award for Best Content Service and Best Project Management.

Another significant event was the laying of the foundation stone of India’s first-

ever Kisan SEZ (Special Economic Zone) by Dr. Y.S. Rajasekhara Reddy, Chief Minister

of Andhra Pradesh.

Further, IFFCO’s Managing Director, Dr. U.S. Awasthi, received honorary

Doctorate of Science degree from Dr Balram Jakhar, Governor of Madhya Pradesh, at the

Vikram University Campus in Ujjain.

Aonla Unit for the first time has crossed production of 20 lakh MT of urea which is

commendable. Paradeep has achieved greater laurels by producing more than 13 lakh MT

14

of NP/DAP despite shortage of raw material. Society has crossed the landmark sales and

transportation of over 112 lakh MT of fertilizers material registering a sharp rise of 20%

over the last year. With this, IFFCO has now become the largest marketer of process

fertilizers not only in India but in the entire world. Society has already achieved the sales

turnover of about Rs.32800 crore during the financial year 2008-09.

During the year 2008-09, the society has entered into a long term agreement with

LEGEND International for supply of rock phosphate along with equity stake. It has

initialed an MoU with Kazphosphate, a leading chemical and fertilizer manufacturing

company of Kazhakistan. Another agreement of intent has been signed with Qatar for

setting up a Urea plant.

CORPORATE SOCIAL RESPONSIBILITIES

In line with its vision and mission statement, IFFCO has undertaken several

social activities in the areas of education, community development, environment

protection and horticulture, health care/medical facilities etc, all with the intent of

reaching out to those in need and improving the quality of their lives. Adopting a village

is of paramount importance to IFFCO. The programme started with an objective to bring

about overall development in the living standards of rural community through integrated

rural development with particular emphasis on agriculture development, creation of

drinking water facilities, medical and veterinary check up. IFFCO has adopted 439

villages, thus empowering many lives.

Another scheme that benefits the farmers is Sankat Haran Bima Yojana, launched

by IFFCO’s subsidiary, IFFCO-Tokio General Insurance Company Limited (ITGI). Here,

farmers are provided insurance against accidents with the purchase of a 50 kilogram bag

of IFFCO fertiliser. This reaches out to member cooperative societies. The policy has

helped over 7,000 people since its inception in September 2001. ITGI also offers

customized policies for farmers such as Barish Bima Yojana, Mausam Bima Yojana and

Janta Bima Yojana.

IFFCO has initiated several promotional projects to provide greater opportunities to

the farmer by organizing field days, farmers meetings, sales point personnel training,

15

crop seminars, special agriculture campaigns to effect transfer of modern farming trends.

Besides, kits containing seeds, fertilisers, bio-fertilisers and agrochemicals along with

booklets/literature were distributed to farmers. The aim: enhancing crop productivity and

thus improving lives.

In keeping with its intent of empowering the weaker sections of society, including

women, IFFCO presents monthly scholarships to deserving students and also organizes

training programmes for women. The organisation has instituted 17 IFFCO Chairs at

agricultural universities and cooperatives. The emphasis is on current topics in

agriculture. IFFCO uses its 12 storage-cum-community Centres for helping people come

together and share their experiences.

The environment is a major concern with IFFCO. Its units and townships

comprise beautiful landscapes, surrounded by trees. IFFCO is also committed to

improving the safety, health and environment of its manufacturing units, in line with

international norms. The Kalol, Phulpur, Aonla and Kandla units have been awarded the

ISO- 14001 certificate for Environment Management System. Further, the Kalol, Phulpur

and Aonla plants have received the ISO-9001 certification for Quality Management.

IFFCO has contributed Rs 10 crore to set up the IFFCO Kisan Sewa Trust. This

Trust assists farmers in getting medical treatment. Employees also contribute regularly to

it. The Kisan Sewa Trust organizes cancer detection and eye camps and arranges for

blood through the Red Cross Society.

The IFFCO Foundation has been promoted as the think tank of the organisation.

Its objective is to focus on strengthening village level cooperatives in harmony with the

law and culture of the country.

Indian Farm Forestry Development Cooperative Limited (IFFDC), promoted by

IFFCO, was given a certificate of appreciation by the Tata Energy Research Institute for

its efforts towards good corporate citizenship. The Cooperative Rural Development Trust

provides practical training to farmers and has organized 229 programmes in 2008,

benefiting 22,221 farmers.

16

INFORMATION AND COMMUNICATION TECHNOLOGY

IFFCO is taking measures to develop web based services to provide exhaustive

information on agriculture, fertiliser industry, agro-chemicals, and information on

cooperative sector. For this purpose, 108 touch screen monitor based Farmers

Information Kiosks or Cyber Dhabas in 10 languages have been installed in 17 different

states of the country. Besides that, IFFCO has developed and implemented several ERP

solutions and e-commerce solutions for internal use as well as for use in its joint projects.

Some of these solutions have got recognition by Indian as well as by International

Media Groups.

During 2008-09, IFFCO has undertaken enhancement of WAN & Network security

for all the plants and marketing offices across the country. Symantec antivirus server has

been consolidated and clients installed on all the machines across the country for

protection against virus attacks.

In short, we can say that:

IFFCO IS:

1. Largest producer of fertilisers in the country

2. No. of Plant Locations : Five

3. Installed Annual Capacity (‘000 MT)

a. UREA - 4242.2

b. NPK/DAP - 4335.4

c. TOTAL ‘N’ - 2628.2

d. TOTAL ‘P2O5 - 1712.8

17

4. Only Fertiliser Institution in the country to produce 68.47 lakh MT of fertilisers

and 93.24 lakh MT of sales during 2007-08.

5. Contributed about 20% to the total ‘N’ and 25% to the total “P2O5” produced in

the country during the year 2007-08.

6. Fertilisers marketed through 39564 Cooperative Societies and 158 Farmers

Service Centers.

7. Service to the Farmers through a variety of programmes.

18

OBJECTIVES OF THE COMPANY

The broad objectives of setting up this venture:-

1) Producing fertilisers.

2) Promoting the fertilisers distribution system in the co-operative sector.

3) Ensuring availability of fertilisers at the farmer’s doorstep.

4) Creating scientific awareness among farmers.

5) Promoting nation’s growth through modern farming techniques.

6) Improving agricultural productivity through balanced fertiliser application.

7) Strengthening cooperation distribution system.

8) To promote the activity for enriching the life of the rural.

9) To achieve self reliant and self generated economy.

IFFCO has grown steadily since its inception today. It has emerged not only as

the largest fertiliser producing organization in India but also Asia’s largest fertiliser

co-operative.

Prices of IFFCO's Fertilisers (Applicable only within India)

(Indian Rupees Per Tonne w.e.f 31-04-2010)

UREA NPK DAP MOP

N-46% 10-26-26 12-32-16 20:20:00 18-46-0 K-60%

19

M.R.P. 5310 7897 8335 6895 9950 5055

Local Taxes Extra, where ever applicable.

MANAGEMENT The Representative General Body (RGB) which is the General Body forms the

supreme body that guides the various activities of IFFCO. The RGB consists of:

1. Members of the Board of Directors.

2. One delegate from each of the Member Societies holding shares of the value of

Rs.100 thousand and above; such delegate shall be as per the provisions of the

Multi-State Cooperative Societies Act/Rules as amended from time to time;

3. Delegates to be elected from amongst the representatives of Member –Societies

(other than Members holding shares of the value of Rs. 100 thousand and above )

in each State/ Union Territory at the rate of one delegate for every 200 societies or

part thereof. However the maximum number of such delegates from any

State/Union Territory at the rate of one delegate for every 200 societies or part

thereof shall not exceed 25. Such elected delegates shall be as per the provisions

of the Multi-State Cooperative Societies Act/ Rules amended from time to time.

The Board of Directors of IFFCO carry out all functions as specified under the

Multi-state Cooperative Societies Act/Rules. The Board of Directors frame

policies, direct the various activities of the Society and undertake any other

activities conducive to overall growth and development of Societies. The Board is

headed by the Chairman.

The Managing Director is the Chief Executive of the organisation with

responsibilities for general conduct, supervision and management of day to day

20

business and affairs of IFFCO. The The Finance Director oversees the financial

aspects and the Marketing Director looks after the marketing functions of IFFCO.

The Director (Technical) looks after the Techincal aspects, Director (HRD) is

responsible for all the Human Resources, Director (Joint ventures) oversees all the

Joint Venture operations and Director (Coop. Development) looks after Cooperative

Development. These functional directors are assisted by Senior Executives who are

experts in various disciplines.

BOARD OF DIRECTORS

The Directors of IFFCO

Chairperson – Shri Surinder Kumar Jakhar

Vice-Chairperson- Shri N.P. Patel

DIRECTORS

Shri Chandra Prakash

Shri S.L. Dharme Gowda

Shri Kartick Chandra Sarkar

Shri Harminder Singh Jassi

Shri M.Gopal Reddy

Shri Ankushrao R.Tope

Shri Rajhans Upadhyaya

Shri G.C. Maikota

Shri Vithalbhai H. Radadia

Shri Sheesh Pal Singh

Shri Raj Kumar Tripathi

Shri Balvinder Singh Nakai

Shri Ravindra Pratap Singh

Shri K. Srinivasa Gowda

21

Shri K. Somashekhar Rao

Shri Simachal Padhy

Shri Pramod Kumar Singh

Shri R.K.Dhami

Shri B.S.Vishwanathan

Managing Director – Dr. U.S. Awasthi

Joint Managing Director-cum-FD – Shri Rakesh Kapur

Director (Coop. Development) – Dr. G.N. Saxena

Executive Director (HRD) – Shri R. P. Singh

Director (Joint Ventures) – Mr. K.L. Singh

Executive Director (Tech.) – Shri A K Singh

BANKERS

India Overseas Bank

State Bank of India

Bank of Baroda

Standard Chartered Bank

The Maharashtra State Co-operative Bank Ltd.

The West Bengal State Co-operative Bank Ltd.

Madhya Pradesh State Co-operative Bank Ltd.

The Karnatake State Co-operative Bank Ltd.

The Punjab State Co-operative Bank Ltd.

The Hongkong and Shanghai Baking Co-operation Ltd.

ICICI Bank Ltd.

22

IDBI Bank Ltd.

IFFCO’s MAIN AIM

“Strengthening management and participatory character of the Indian Cooperative

Movement by using duly tested and appropriate consultancy, advisory and technological

interventions sourced from within the country and abroad and in accordance of the

Cooperative Principles and in harmony with the law and culture of the land.”

VISION

“To augment the incremental incomes of farmers by helping them to increase their crop

productivity through balanced use of energy efficient fertilisers; maintain the

environmental health; and to make co-operative societies economically and

democratically strong for professionalized services to the farming community to ensure

an empowered rural India.”

MISSION

IFFCO’s mission is “to enable Indian farmers to prosper through timely supply of

reliable, high quality fertilisers and farm inputs and services in an environmentally

sustainable manner and to undertake other activities to improve their socio-economic

status.”

1) To provide to farmers high quality fertilisers in right time and in adequate

quantities with an objective to increase crop productivity.

2) To make plants energy efficient and continually review various schemes to

conserve energy.

23

3) Commitment to health, safety, environment and forestry development to enrich

the quality of community life.

4) Commitment to social responsibilities for a strong social fabric.

5) To institutionalize core values and create a culture of team building,

empowerment and innovation which would help in incremental growth of

employees and enable achievement of strategic objectives.

6) Foster a culture of trust, openness and mutual concern to make working a

stimulating and challenging experience for stakeholders.

7) Building a value driven organization with an improved and responsive customer

focus. A true commitment to transparency, accountability and integrity in

principle & practice.

8) To acquire, assimilate and adopt reliable, efficient and cost effective technologies.

9) Sourcing raw materials for production of phosphatic fertilisers at economical cost

by entering into joint ventures outside India.

10) To ensure growth in core and non-core sectors.

11) A true co-operative society commitment for fostering co-operative movement in

the country.

Emerging as dynamic organization, focusing on strategic strengths, seizing

opportunities for generating and building upon past success, enhancing earnings to

maximize the shareholder’s value.

24

VISION 2010

Having accomplished the objectives envisaged in “vision2000”and”mission-2005”

IFFCO embarked on “vision2010” which focuses on future growth and development of

the society and aims at:

1. Attaining an annual turnover of Rs.15,000 crore by 2010.

2.Installation of Ammonia and Urea plants including acquisition of fertiliser units

3.Backward integration to meet feed stock requirements such as Phosphoric acid,

Natural gas etc.

4. Generation of Power

5.Production and marketing of micro-nutrients, seeds, bio-fertilisers, pesticides etc.

6.Value addition to agri-products and marketing

7.Information technology and IT enabled services

8.Easblishment of retail chain in urban and semi-urban locations.

9.Diversification into new growth areas such as mobile telephony and communication

Technology in the rural areas.

25

Under Vision 2010,IFFCO has set up a power generation company in Chattisgarh and

formed a joint venture to manufacture Phosphoric Acid in Egypt

APPROACH

To achieve our mission, IFFCO as a Cooperative society, undertakes several activities

covering a broad spectrum of areas to promote welfare of member cooperatives and

farmers. The activities envisaged to be covered are exhaustively defined in IFFCO’s Bye-

laws

COMMITMENT

Our thirst for ever improving the services to farmers and member co-operatives is

insatiable, commitment to quality is insurmountable and harnessing of mother earth’s

bounty to drive hunger away from India in an ecologically sustainable manner is the

prime mission.

All that IFFCO cherishes in exchange is an everlasting smile on the face of Indian

Farmer who forms the moving spirit behind this mission.

BUSINESS PRINCIPLES OF THE COMPANY

26

Appreciation of national need of generation upto optimum return of investment.

To fair price of the product manufactured by the company is subsidy to the

farmers.

Total consumer satisfaction as a quality of the product, price of the product and

better service after selling the product.

Effective management information system.

To increase the efficiency of the workers.

To maintain better human relations and discipline among all the employees.

To develop good relation with customers.

IFFCO’S EMBLEM

The Emblem of any organisation i.e. the logo is very important by which the

company is known to everyone or that is identity of the company. After one year of

establishment in 1968, the organisation has decided to make an EMBLEM of IFFCO.

The executive of the company said that which can be easily fit into any place or easily

changeable according to the place and made by simple geometrical method. So the

EMBLEM is made by Mr. M.I. Gupta, Chief Visualiser Developer and looks like

Logo’s ratio is1:2:5 and the color is green. The rectangle shows that the Indian

economy is depend upon the agriculture and green color shows the faith of the farmers,

they believe that after using the urea their fields will always be green, the remaining

27

white color shows that the quality of the IFFCO’s product is very good and oval shape is

meant for the wealth and prosperity.

ORGANISATION CHART OF IFFCO

28

Board of Directors

Chairman & Vice Chairman

Managing Director

Dy.MD-cum- Mkt.

Director

Director

(Technical)

Director

(HRD)

Director.

(Coop. Development)

Dy.MD-cum-

Finance Director

29

Provisional highlights of IFFCO performance during 2008-09.

30

Highest Production of Fertilisers(Previous Best 70.12 lakh MT in 2006-07)

71.68 lakh MT

Highest Production of Urea (Previous Best 39.63 lakh MT in 2007-08)

40.68 lakh MT

Production of NPK/DAP/NP(Best 32.26 lakh MT in 2006-07)

31.00 lakh MT

Highest Sales of Fertilisers(Previous best 93.24 lakh MT in 2007-08)

112.33 lakh MT

Highest Sales of Urea(Previous best 54.29 lakh MT in 2007-08)

58.49 lakh MT

Highest Sales of NPK/DAP(Previous best 38.95 lakh MT in 2007-08)

53.84 lakh MT

Highest Turnover(Previous best Rs.12163 crore in (2007-08)

Rs 32800 crore

Plant Productivity(Best 1669 MT in 2005-06) 1376 MT per employee

Highest Marketing Productivity(Previous best 6158 MT in 2007-08)

7380 MT per employee

Composite Energy ConsumptionLowest 5.907Gcal / MT in 2007-08)

5.9433 Gcal/ MT

IFFCO ASSOCIATES

1. INDUSTRIES CHIMIQUES DU SENEGAL

2. OMAN INDIA FERTILISER COMPANY S.A.O.C.

3. INDIAN POTASH LTD.

4. NATIONAL COMMODITY & DERIVATIVES EXCHANGE LTD.

5. NATIONAL COLLATERAL MANAGEMENT SERVICES LTD.

6. COOPERATIVE RURAL DEVELOPMENT TRUST

7. KISAN SEWA TRUST

8. IFFCO FOUNDATION

9. LEGEND INTERNATIONAL HOLDINGS INC

31

AWARDS GALORE

KALOL UNIT

1) Seven awards received for overall performances from FAI.

2) Two awards for industrial safety from GOI.

3) Award for technical innovation from FAI.

4) Two Rajya Bhasha Shield for promoting Hindi.

5) Award for safety from National Safety Council, Chicago.

6) Indo German greentech environment excellence award.

PHULPUR UNIT

1) Four awards for productivity from NPC.

2) Six national safety’s award from GOI.

3) Two awards for overall performance from FAI.

4) Two awards for technical innovation from FAI.

32

5) FAI’s Award for Best Overall Performance of an operating fertiliser unit for Nitrogen

(Ammonia and Urea) Plant jointly with Zuari Industries Limited, Goa.

6) Three national energy conservation awards.

7) Three awards for best environmental protection from FAI.

8) Best environmental excellence awards from Indo German green tech foundation.

9) Best technical paper award by FAI.

KANDLA UNIT

1) Twelve safety awards from national safety council Bombay GOI.

2) Twenty-three safeties award from Gujarat.

3) Raj Bhasa award for promoting Hindi.

4) Six awards for overall performance from FAI.

AONLA UNIT

1) Award for best implemented project ( 2nd price) from GOI.

2) Award for conservation of energy from GOI

3) National Award for “Excellence in Energy Management”

4) C Indo German and Greentech Environment Excellence Award

5) C Award for Best overall performance from FAI

6) C Two Awards for Excellence in Safety from FAI

7) C Two Safety Awards from National Safety Council of India

8) C Rajiv Ratna National Gold Award 2005 for Best Executive

9) C Excellence Award for papers published on “Safety and Health in

Chemical Industry” and “Hazard Identification & Risk Management

10) National energy conservation award 2006

11) Golden Peacock Environment Management Award 2008

33

ABOUT AONLA UNIT

LOCATION

State Uttar Pradesh

State Capital Lucknow

Distance from Lucknow 280 Km.

Distance from New Delhi 260 Km.

Nearest Airport New Delhi

Railway Station Aonla (10 Km. From the Plant)

Road Plant is In Bareilly–Aonla Bareilly highway.

Area under Plant 260 Hectares

Area under Township 220 Hectares

YEAR OF COMMISSIONING: : 1988

INVESTMENT : Rs.651.6 Crore AONLA- I

34

YEAR OF EXPANSION : 1996

INVESTMENT : Rs.954.7 Crore AONLA- II

YEAR OF DEBOTTLENECKING: 2008

INVESTMENT : Rs.149.2 Crore

PRODUCT CAPACITY TECHNOLOGY

TPD TPA

AMMONIA 3480 11,48,400 HALDOR TOPSOE

UREA 6060 19,99,800 SNAMPROGETTI

‘N’ 2788 9,19,908

The IFFCO AONLA Unit is located in the Gangetic Plains of Uttar Pradesh in

Bareilly district about 28 Km. Southwest on Bareilly-Aonla Road. It was set up on 08

January 1985 and started commercial urea production at 16 July 1988. The infrastructure

of AONLA unit is very big and constructed on 713 acres of land.

IFFCO Aonla unit is the most efficient and quality-wise as well as environmental

oriented unit so that M/s KPMG Peat Marwick, a quality registrar has certified it as ISO:

9002 unit and M/s BVQI London has accredited it as ISO:14001 unit. The Aonla unit, an

35

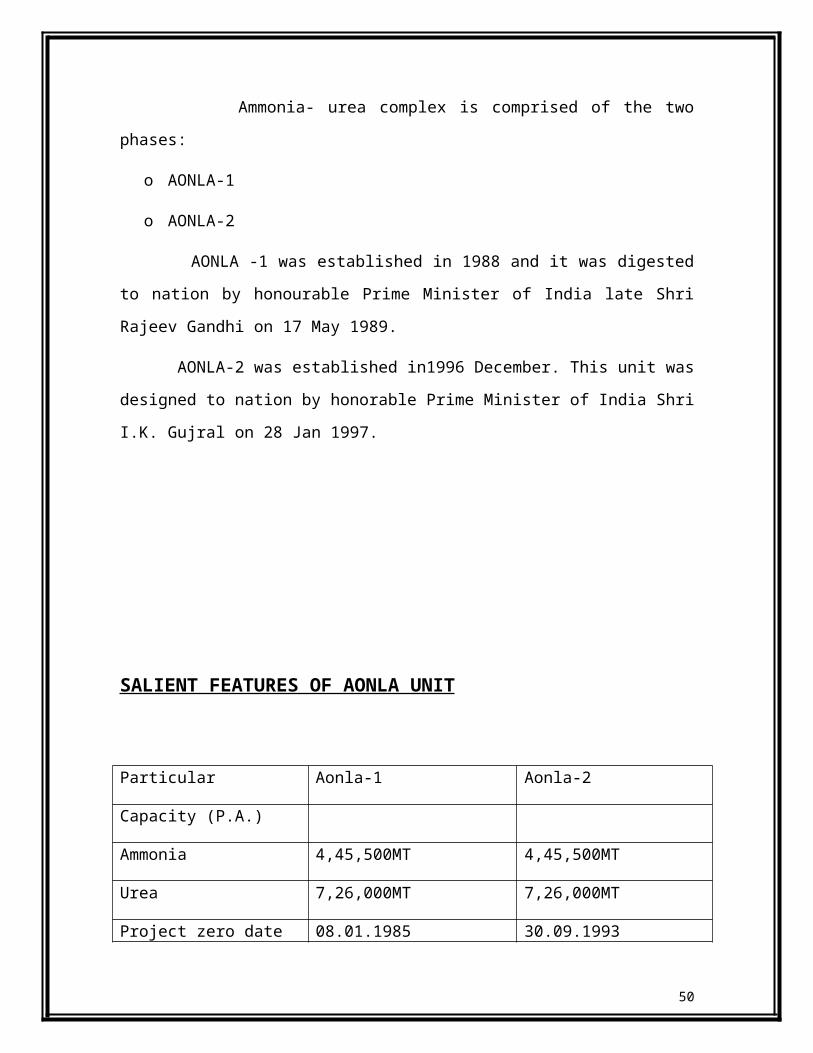

Ammonia- urea complex is comprised of the two phases:

o AONLA-1

o AONLA-2

AONLA -1 was established in 1988 and it was digested to nation by honourable

Prime Minister of India late Shri Rajeev Gandhi on 17 May 1989.

AONLA-2 was established in1996 December. This unit was designed to nation by

honorable Prime Minister of India Shri I.K. Gujral on 28 Jan 1997.

SALIENT FEATURES OF AONLA UNIT

Particular Aonla-1 Aonla-2

Capacity (P.A.)

Ammonia 4,45,500MT 4,45,500MT

Urea 7,26,000MT 7,26,000MT

Project zero date 08.01.1985 30.09.1993

Mechanical completion 08.01.1988 30.11.1996

Ammonia production started

15.05.1988 15.12.1996

Urea production started 18.05.1988 26.11.1996

Feedstock Natural gas Natural gas with Naphtha

36

(Natural Gas from HBJ pipeline being supplied from Bombay high)

Capacity Enhancement of Aonla and Phulpur Units

IFFCO has submitted the Techno-Economic Feasibility Report (TEFR) for

Capacity Enhancement of Aonla and Phulpur Unit to the Department of Fertilisers

(DOF).

Following enhancement in capacity has been envisaged with a total annual increase in

Urea Capacity by 5.115 lakh MT:

Name of Unit Present Capacity

( MTPD)

Proposed

Capacity (MTPD)

Increase in

Capacity (MTPD)

Phulpur-1 1670 2080 410

Phulpur-2 2620 3000 380

Aonla-1 2620 3000 380

37

Aonla-2 2620 3000 380

Total 9530 11080 1550

The installed cost for the Enhanced Capacity is estimated at about Rs. 19 lakh per MTPD

of Urea as against the Rs. 65-70 lakh per MTPD Urea in case of a Grassroots Plant.

Therefore De-bottlenecking of existing Urea Units is the best route to create additional

Urea capacity.

IFFCO has initiated action for De-bottlenecking of its plant at Aonla and Phulpur

Units for Capacity Enhancement. We are awaiting final clearance from DOF. Incidentally

this will also reduce the subsidy to Government vis a vis imported Urea.

PLANTS OF AONLA UNIT

There are mainly four plants in the unit namely:

1. Ammonia Plant

2. Urea plant

3. Product Handling Plant

4. Steam and Power Generation Plant

1. AMMONIA PLANT There are two streams of Ammonia plants having the capacity to produce 2x1520

MTDP of liquid ammonia. The technology is based on Haldor Topsoe, Denmark process

with Natural Gas and Naphtha as main raw material.

38

2. UREA PLANT There are four streams of Urea Plant having the capacity to produce 4x1310 MTPD

OF Urea Fertiliser. The technology is based on Snamprogetti, Italy on Ammonia

stripping process.

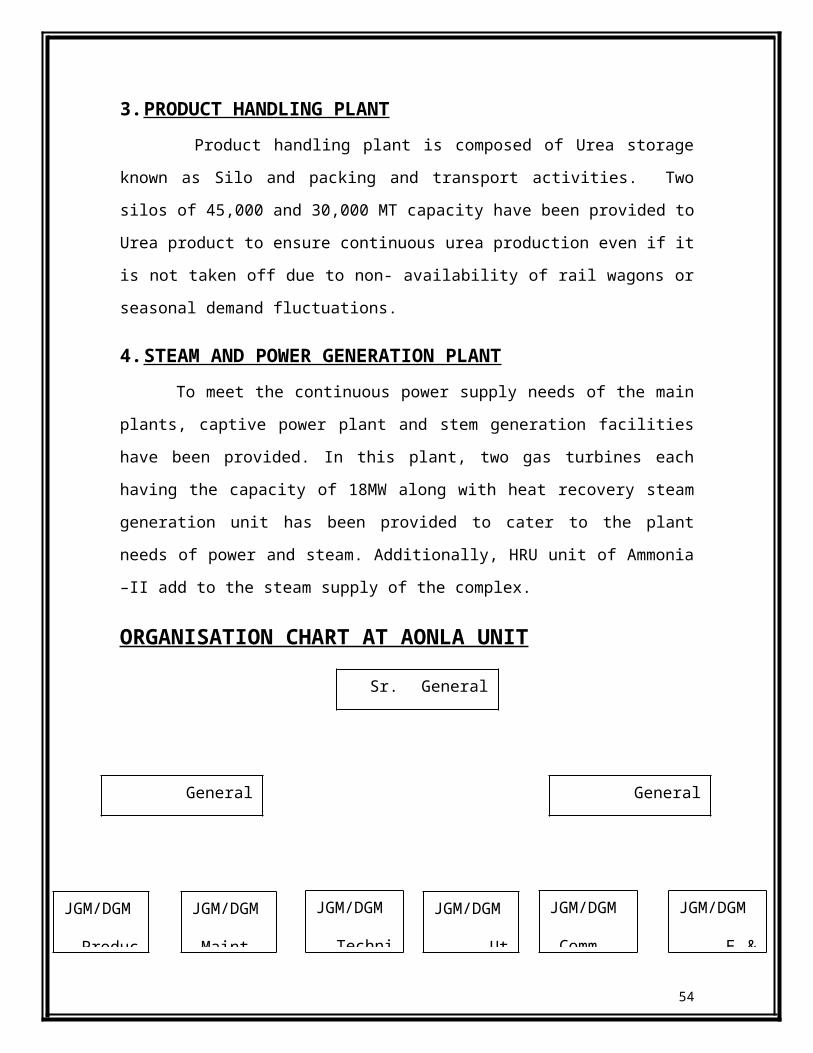

3. PRODUCT HANDLING PLANT Product handling plant is composed of Urea storage known as Silo and packing and

transport activities. Two silos of 45,000 and 30,000 MT capacity have been provided to

Urea product to ensure continuous urea production even if it is not taken off due to non-

availability of rail wagons or seasonal demand fluctuations.

4. STEAM AND POWER GENERATION PLANT To meet the continuous power supply needs of the main plants, captive power plant

and stem generation facilities have been provided. In this plant, two gas turbines each

having the capacity of 18MW along with heat recovery steam generation unit has been

provided to cater to the plant needs of power and steam. Additionally, HRU unit of

Ammonia –II add to the steam supply of the complex.

ORGANISATION CHART AT AONLA UNIT

39

Sr. General Manager

General Manager General Manager

JGM/DGM

Technical

JGM/DGM

Maint.

JGM/DGM

Production

JGM/DGM

Utility

JGM/DGM

Comm.

JGM/DGM

F & A

Ammonia

Plant

Mechanical Process Power Plant Purchase F& A

Finance & Accounts Department At A Glance

The Finance & Accounts Department of IFFCO, Aonla is divided into 5 sections, to

facilitate smooth and easy functioning and control.

Organisation Structure

40

Urea Plant Electrical Design &

Drawing

Offsite Store

JGM/CM

Traffic

Product

Handling

Instrumental

Library &

Document

General

Engg.JGM/CM

Fire & Safety

& Env.

Civil

Laboratory

Training &

Development

FINANCE & ACCOUNT

DEPARTMENT

BOOKS/FICC CELL

FINANCIAL CONCURRENCE

BILL SECTION

PAYROLL & TAXATION SECTION

PSL SECTION

Line of Control in Finance & Account Department

41

Supply Section

Note Sheet Payment

Work Order

HOD

JGM/DGM (F & A)

Chief Manager (F& A)

Sr.Manager (Account)

Manager Account

Work contract

Imported supply

Indigenous supply

Service contract

Chief Manager (F& A)

Sr.Manager (Account)

Sr.Manager (Account)

Sr.Manager (Account)

Manager Account Manager Account Manager Account

Sr. Account Officers

Account officers

Jr. Account Officer

Sr. Accountant

Jr. Accountant

FINANCE AND ACOUNTS DEPARTMENT

Each company is carried with a purpose of earning money. Money or capital

being a scare as well as crucial resource in the working of any organization needs to be

given prime importance. The financial resources have been planned and controlled in a

proper and continuous manner. As among the most crucial decisions of a firm are those

which relate to finance. Finance & accounts from an integral part of any organization.

Proper and smooth functioning of this section is very vital for the organization to survive

and grow.

Finance functions are of two types:

Managerial finance function

Routine finance function

42

Deputy Account Manager

Managerial finance functions are so called because they require skilful planning,

control and execution of financial activities.

Routine finance functions on the other hand, do not require a great managerial

ability to carry them out. They are chiefly and are incidental to the effective handling of

the material finance functions.

The various areas covering under the preview of subsections are as follows

1. BOOKS SECTION

This section basically deals with accounting function, maintenance and keeping of

records.

The various functions include:

Books: Preparing and maintaining balance sheets.

IFCC (Fertiliser Industries Coordination committee)

Costing & Pricing Cells

Reporting

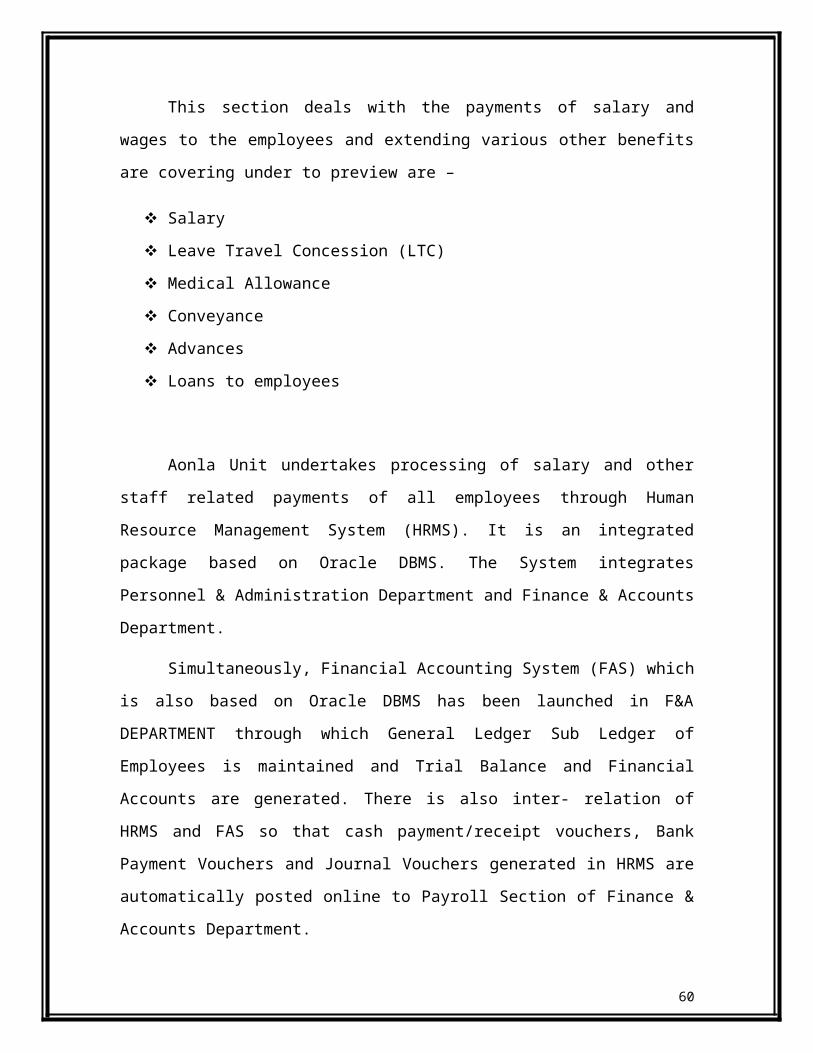

2. PAY ROLL SECTION

This section deals with the payments of salary and wages to the employees and

extending various other benefits are covering under to preview are –

Salary

Leave Travel Concession (LTC)

Medical Allowance

Conveyance

Advances

43

Loans to employees

Aonla Unit undertakes processing of salary and other staff related payments of all

employees through Human Resource Management System (HRMS). It is an integrated

package based on Oracle DBMS. The System integrates Personnel & Administration

Department and Finance & Accounts Department.

Simultaneously, Financial Accounting System (FAS) which is also based on

Oracle DBMS has been launched in F&A DEPARTMENT through which General

Ledger Sub Ledger of Employees is maintained and Trial Balance and Financial

Accounts are generated. There is also inter- relation of HRMS and FAS so that cash

payment/receipt vouchers, Bank Payment Vouchers and Journal Vouchers generated in

HRMS are automatically posted online to Payroll Section of Finance & Accounts

Department.

3. Taxation Section

As per the status and operations of the society, It deals with the following Taxes:-

Central Excise Duty

Income Tax

Service Tax

Sales Tax

Central Excise Duty

As we know that this duty is charged by Central Government on the goods

manufactured. IFFCO mainly produce ammonia and urea at Aonla plant. So duty on

ammonia is charged. In this relation monthly production report is prepared and all

documents and accounts are prepared by the Finance & Accounts Department. The duty

is deposited in the Government bank account on the 5th day of the month.

EXCISE Duty is not charged on production of Urea.

44

CONCEPT OF INVENTORY MANAGEMENT

Dictionary meaning of inventory is “detailed list of movable articles”. The

literary meaning of inventory is stock of goods. According to International Accounting

Standards-2, inventory is a tangible property which is held:

For sale in the ordinary course of business;

In the process of manufacture for such a sale;

For consumption in the process of production of goods and services for sale

including maintenance supplies and consumables other than machinery spares.

Inventory Management involves the control of assets being produced for the

purpose of sale in the normal course of the company's operations. The goal of effective

inventory management is to minimize the total costs - direct and indirect - that are

associated with holding inventories. However, the importance of inventory management

to the company depends upon the extent of investment in inventory.

45

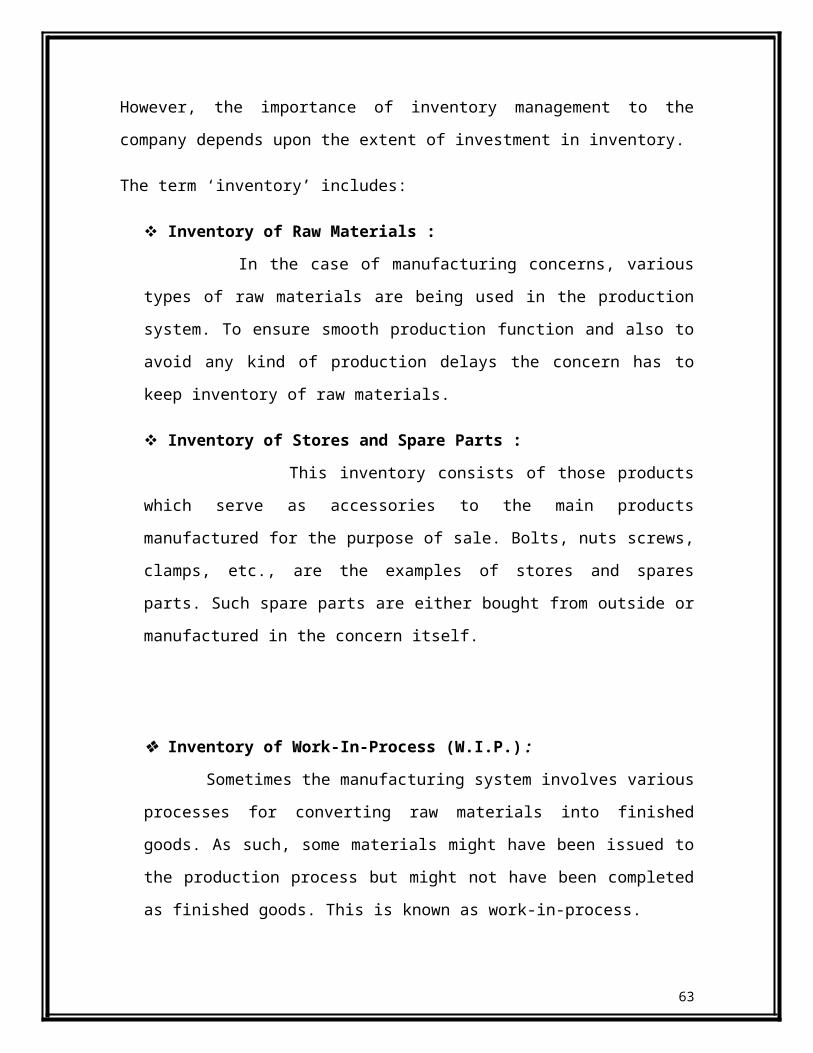

The term ‘inventory’ includes:

Inventory of Raw Materials :

In the case of manufacturing concerns, various types of raw materials are

being used in the production system. To ensure smooth production function and also

to avoid any kind of production delays the concern has to keep inventory of raw

materials.

Inventory of Stores and Spare Parts :

This inventory consists of those products which serve as accessories to the

main products manufactured for the purpose of sale. Bolts, nuts screws, clamps, etc.,

are the examples of stores and spares parts. Such spare parts are either bought from

outside or manufactured in the concern itself.

Inventory of Work-In-Process (W.I.P.) :

Sometimes the manufacturing system involves various processes for

converting raw materials into finished goods. As such, some materials might have

been issued to the production process but might not have been completed as finished

goods. This is known as work-in-process.

Inventory of Finished Goods :

All goods manufactured during a particular period may not be sold

immediately. These are to be kept in warehouse. The idea is to uncouple the

production and sales function so that it is no longer necessary to produce the goods

before a sale can occur.

The application of managerial function on the basis of management principles

in the field of inventory is termed as inventory management. Managerial functions are

performed with respect to inventory; it may be called inventory management.

The objective of inventory management is to plan the optimum size of inventory

which is neither excessive nor deficient and is timely available. For timely availability

46

along with optimum size, there is need for controlling as well. Only on the basis of

various control techniques one can ensures whether inventory would be timely available.

But effective control in itself depends upon organizing and coordination. Thus, inventory

management comprises the functions of planning, controlling and organizing the types of

all goods, quantity, status, flow and time- sequence etc.

Need for inventory management

Inventory management is an integral part of general management. Three important

functional aspects of a business are closely related to inventory management. These are:

1) Production management

2) Marketing management

3) Financial management

Here the production management and marketing management are related to the

physical aspect of inventory management and; financial management is concerned with

the financial aspect of the inventory management.

In production management, production manager will always strive to have a large

inventory of raw materials and of such a good quality as to ensure stable production

operations.

47

In marketing management, marketing manager aims at satisfying ever increasing

demands for improved customers’ service by having large inventory of inside goods.

In financial management, finance manager will effort towards to keep investments

in different types of inventory at a minimum possible level so that the business concern

may earn maximum return.

MATERIAL DEPARTMENT

Material Department is responsible for the proper handling of inputs and

controlling of material inputs. Proper handling of input materials ensures the smooth

running of plant. Material department recognizes the need of the input materials and

arranges them for the plant. It includes the procurement, verification and controls of

materials in right quantity and at right time to facilities the production function.

Material management includes two important functions:

Purchasing

Storing and control of materials

That’s why; it is divided into following sections:

Purchase section ( It is responsible for purchasing of materials )

Store section ( It stores the inputs)

48

These both sections are interrelated and perform their function on coordination.

All purchases are to be made only by the materials department except purchases of petty

item through some vouchers and Department Managers within the limits prescribed in

purchase procedure/power of officer. Material purchase indent should give following

information:

1) Quantity in stores

2) Average monthly consumption since last purchase for stock items

3) Maximum /minimum level

4) Last purchase order reference

5) Reorder level

PURCHASE SECTION

The purchase department is at the interface of internal and external department.

Purchase department do enquiry about the inputs whether it is required or not. This

enquiry is done in two ways that are:

1) Single stage

2) Two stage

After enquiry purchase department invites a tender. After confirmation of all

terms and conditions the department contacts the supplier and orders for the inputs. Thus

it is responsible for purchasing of materials and other raw materials whatever is required

by the organization. Purchase department is responsible for the delivery of right amount

of material at the right time and at the right location to avoid the hampering of the

production.

49

Purchasing is distinct from buying. Purchasing involves the extra knowledge as the

tenders, various vendors, their prices, comparison between them, after sale service,

dispatching follow up and payment terms.

The purchase department considers various things before purchasing the raw materials.

1. Information about the input material

2. Sources of material- vendor

3. Reasonable price of that material

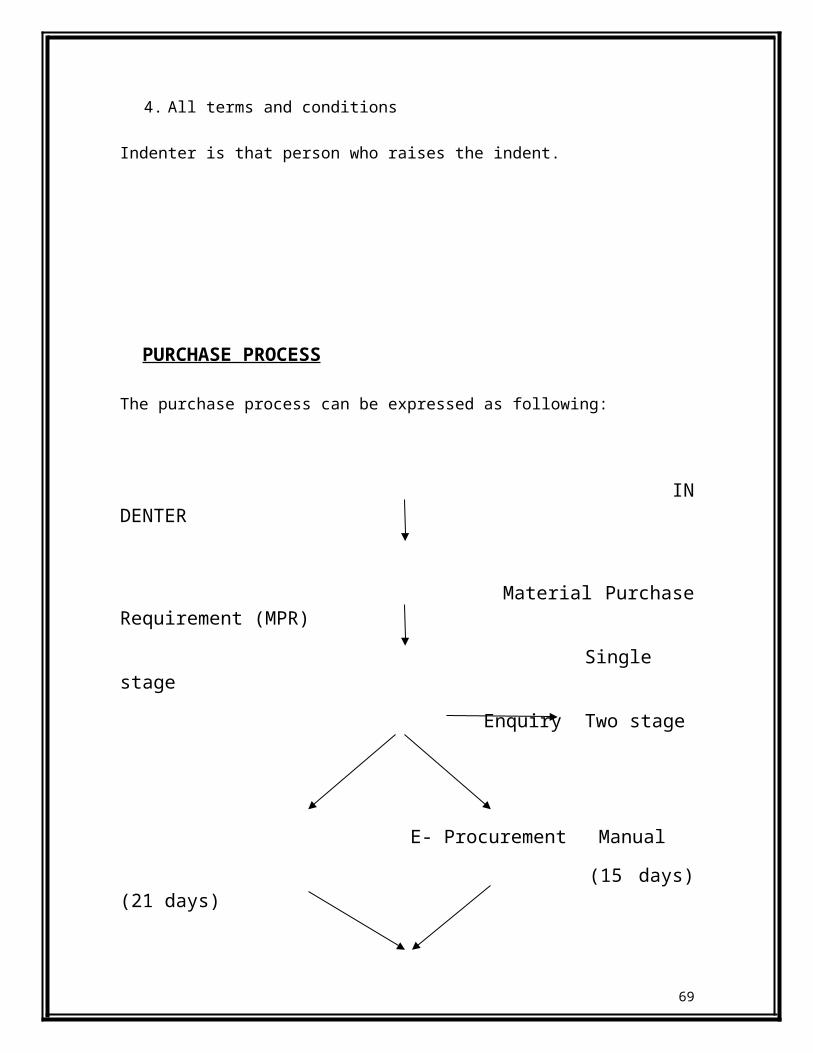

4. All terms and conditions

Indenter is that person who raises the indent.

PURCHASE PROCESS

The purchase process can be expressed as following:

INDENTER

Material Purchase Requirement (MPR)

Single stage

Enquiry Two stage

50

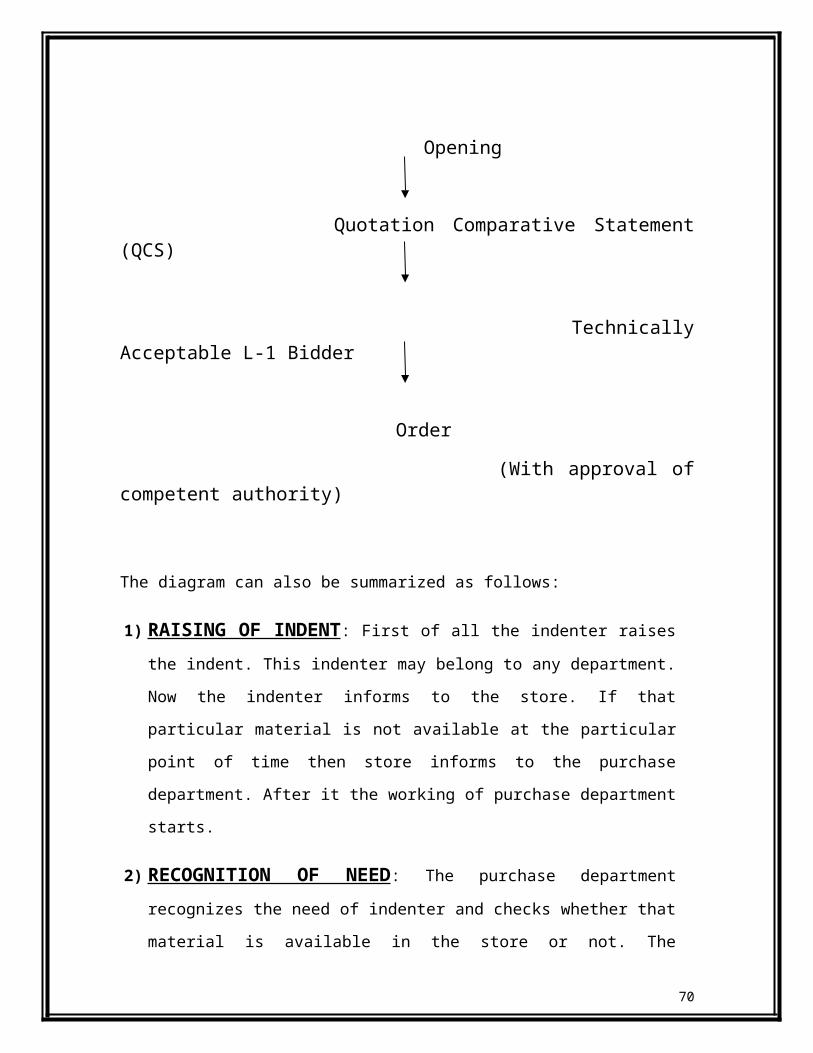

E- Procurement Manual

(15 days) (21 days)

Opening

Quotation Comparative Statement (QCS)

Technically Acceptable L-1 Bidder

Order

(With approval of competent authority)

The diagram can also be summarized as follows:

1) RAISING OF INDENT : First of all the indenter raises the indent. This

indenter may belong to any department. Now the indenter informs to the store. If

that particular material is not available at the particular point of time then store

informs to the purchase department. After it the working of purchase department

starts.

2) RECOGNITION OF NEED : The purchase department recognizes the need

of indenter and checks whether that material is available in the store or not. The

availability of input material at all points of time is the responsibility of purchase

department.

3) REQUISITION TO PURCHASE : This is an intimation to purchase

department by the indenter that he has need of certain materials. He raises indent

by filling a form ‘Material Purchase Requisition’ (MPR). For stock items MPR is

51

raised by store keeping in view maximum, minimum & re-ordering lable. In this

he gives several information like:-

a. Material description/ Proposed Reason

b. Item code/ proposed code

c. Unit

d. Quantity required

e. Value

f. Budget code

g. MPR No.

h. Indenter

PAYMANT AGAINST PURCHASE:

There are various modes of payment through which payment is done:

1. Advance payment to supplier :

If both the parties are agreed upon advance payment that is specifically provided

in the contract order, only then advance payment is given. The advance payment to

contractors shall be made against submission of bank guarantee in the Performa

provided by IFFCO. Advance payment against indemnity bond shall not be released as

provided in the purchase procedure.

2. Full payment / 90% to 95% payment :

52

In case the terms of payment provide for full payment or part payment against

dispatch documents through bank, the supplier will be negotiating the documents through

the bankers. After the documents are received by the bankers, they are forwarding bank

intimation along with a copy of the purchase order to ascertain that the invoice is raised

for the material ordered and conforms to the other terms and conditions of purchase

order.

After the intimation from the bank is received the invoice of the suppliers will be

scrutinized by the Finance and Account Department for the following-

i. Purchase order number

ii. Whether materials supplied are as specified in the purchase

iii. Whether materials supplied are as specified in the purchase order.

iv. Quantity supplied.

v. Price basis whether F.O.R. or Ex-works

vi. Whether excise duty, sale tax and other taxes are as per the order.

vii. Whether bank charges are claimed as per the purchase order.

viii. Other terms and conditions of the purchase order.

ix. Document with bank for retirement should have consignee copy of GR.

Where there is delay in supplying the material and the payment through bank is

90% to 95%. It should be ensured that penalty for delay, as provided in the purchase

order, is recovered before releasing the balance payment. Where payment required to be

made, a clarification is to be sought from materials department and proper approval taken

for waiving of penalty or otherwise before retiring documents.

The payments under the contracts must be regulated as per the expressed terms

and conditions. Any payment not covered by the contractual terms and conditions should

not be released.

3. Full payment / Balance payment after receipt of materials :

53

In case the purchase order provides the 100% payment after receiving of

materials and accepted payment is to be released after the SRV is received from the

stores department. In case 95% or 90% released against document retired from bank then

the balance payment can be released after receipt of SRV from store, which confirms

that the material has been accepted after inspection and taken on charge.

Before released of the payment, the invoices should be scrutinized as the case of

payments released through bank. In addition it should also be verified whether all the

items invoiced have been received, inspected and accepted as per the SRV.

IMPORTED MATERIAL

Materials procured may be either indigenous or imported. For major projects the

foreign contracts are normally finalized at head office level and payment against these

contracts are made by the concerned unit. Orders are also placed by the unit directly.

Payment is made to the foreign party by debiting to the appropriate advance account. If

the payments are made through L/C against documents, the same shall be debited to

advances to foreign suppliers account. On receipt of material at site, project engineer

shall accept the material and initiate for preparation of DCSRV/SRV. After receiving

DCSRV/SRV project accounts will clear the supplier’s advance account for material.

54

Clearing and handling of imported material is the responsibility of material

department on the arrival of ship the materials will be cleared with reference

MATERIAL CODING

It is very typical for the every organization to maintain the stock items in case of

largenumber of items. It will be very typical to identify them at the time of requirement.

So the items are coded to avoid confusion. For the coding of materials the account person

assigns code for every item of store. Thus every item has a code that is called its material

code.

Material coding facilitates the account persons and store manager to maintain the

transactions of the items whether of receiving or of issuing.

Every item maintained by its code in the stock as well as in the store accounting

section. The item/material code remains same in stores and accounting section. Whenever

a transaction is done in store for the inventories the full details of that transaction is send

55

to store accounting section also, because the computers of stores and accounting section

are connected through Local Area Network. (LAN)

In this way it is very comfortable task to maintain the inventories on the inventory

software with the help of material coding.

Advantages of codification

1. Lengthy descriptions are replaced by a simple code.

2. It economizes space in forms and reduces clerical work.

3.Ease in identification of stores.

4. It is comprehensive.

5. It facilitates, mechanized accounting.

6.Secrecy of description can be maintained.

7. It ensures clarity.

CODING

There are different types of coding that are as follows:

a)Numeric : Each item is given a number.

b)Alphabetic : Each item is denoted by a combination of alphabets. If the alphabet

selected indicates the inventory sound when it is pronounced, it is known as

mnemonic system. This helps in remembering the codes.

c)Alphanumeric : It is a combination of alphabets and numeric code.

d)Decimal System: It is basically a numeric system; sub-group may be indicated by

decimals.

In IFFCO 12 digits coding is done.

56

The various codes for the different materials are as follows:

1. Ammonia – 11

2. Urea - 12

3. Offsite - 13

4. Product handling -14

5. Power plant -15

2 digits = for the plant location

3 digits = for the equipment

3 digits = for the material

3 digits = for the size and

1 digit = for the item identification.

Packing & Dispatch

All packing, boxing and protection shall conform to the specification or

requirements of the order. The supplier shall be held liable for the damage or breakage of

the goods due to defective or insufficient packing. It will be according to term and

conditions that are given already in the format.

All goods shall be dispatched by rail/road freight paid and the railway receipt/lorry

receipt shall be posted to the concerned officer of IFFCO.

57

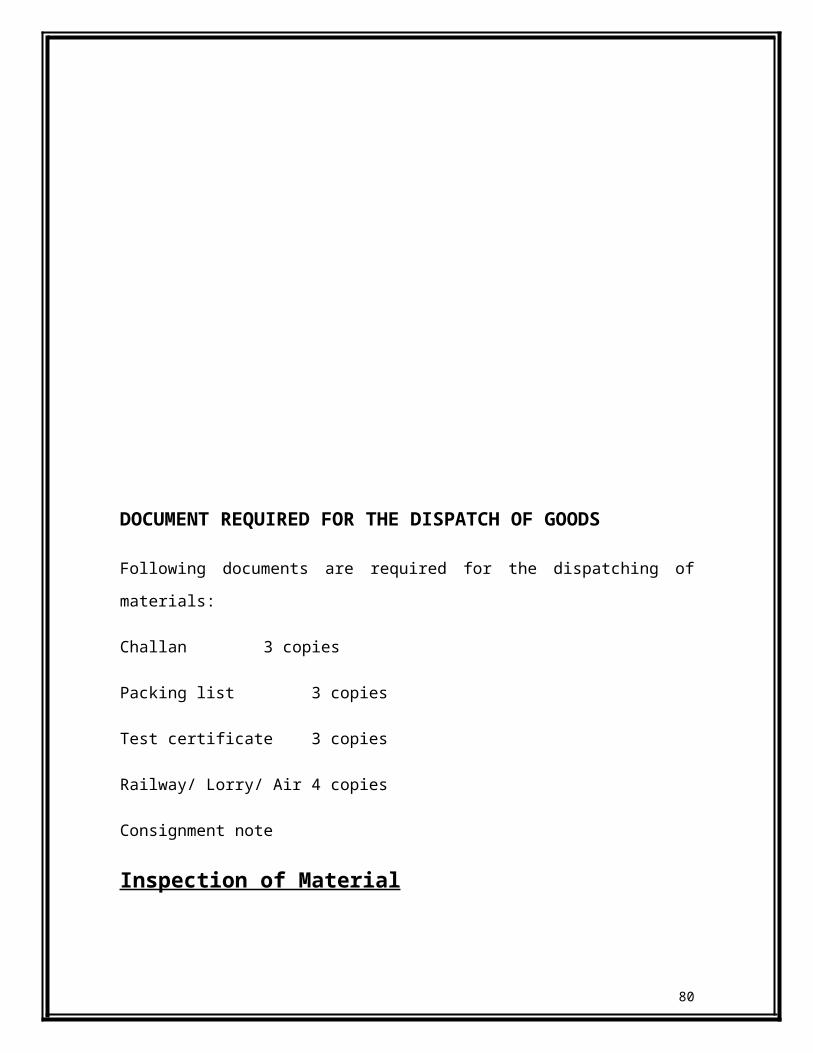

DOCUMENT REQUIRED FOR THE DISPATCH OF GOODS

Following documents are required for the dispatching of materials:

Challan 3 copies

Packing list 3 copies

Test certificate 3 copies

Railway/ Lorry/ Air 4 copies

Consignment note

Inspection of Material

58

The material department shall coordinate with other departments and arrange

inspection of material at vendor’s shop prior to dispatch. Inspection of materials in other

cases shall be carried out on receipt of materials at site. Only materials those cleared by

the inspection will be taken on charge in stores. The person inspecting the material will

sign

on the stores receipt voucher in token of having inspected and accepted the material.

Generally indenter is called upon for the inspection of the material.

Sometimes inspection is done at the gate of IFFCO. Only after inspection material

enters into the store. If there is any damage in the material or they are insufficient in

quantity then rejection report is prepared. Its copies are distributed among all the parties

which are involved in it.

Damaged/Short/Rejected Materials

If the materials are received short or in damaged condition, there are some

conditions in this regard.

In cases where the responsibility for the transit insurance is on IFFCO, a claim should

be lodged with insurance company for the value of material plus incidentals. This

insurance is done by IFFCO TOKIO GENERAL INSURANCE COMPANY. As

soon as the shortage per damage of the materials is noticed the material department

will lodge the provisional claim with the underwriters and pass on the relevant papers

to the finance & accounts department for lodging monetary claim.

In respect of transit insurance claims bill section will pass an adjustment

Entry debiting “claim recoverable account” and credit the “Advance to

Vendors account”. After the adjustments the bill section sent the copy of journal

voucher along with all necessary details such as P.O. No. , MRR No. quantity and

value, name of the supplier to the insurance section for following up the claim with

the insurance company.

59

Where the responsibility for short supply or damages in transit is of the suppliers, the

material department should take up the matter with the supplier for arranging

replacement. A report is prepared in this case. Its copies are sent to the supplier,

purchase department and finance and account department.

Accounting of Raw Materials

Based on the projected consumption requirement of raw materials, the

procurement action is taken by the commercial department at the head office which is in

Delhi.

Described below is the accounting requirement of major raw material.

Imported Phosphoric acid and Ammonia

The consignment of phosphoric acid and Ammonia are received at Kandla and the

material actually received is valued at the contracted cost & freight price.

60

Where free on board (FOB) price is agreed, the ocean freight element is loaded

separately. All connected expenditure like customs duty; handling charges etc. are also

included in inventory valuation.

The valuation of inventory at the month end is to be made on the basis of exchange

rates prevailing on the last day of the month. The difference if any between the

provisional rate and the actual payment rate shall be charged off to the consumption

account, if the material is already consumed.

The account department also ensures that all claim suppliers for shortage are

booked on monthly basis and necessary on quarterly basis for the pending claims.

Indigenous Ammonia

The indigenous ammonia is supplied by KRIBHCO / GNFC to Kandla unit. The

quantity received is accounted at the price payable to the party which is fixed by the

Govt. of India. This price is fixed at par with the landed cost of imported ammonia.

Potash

Potash purchase orders are placed by the commercial department time to time

depending on the material requirement. The material received valued at agreed price plus

local sales tax and freight for transportation of material up to plant site.

The finance department at head office ensure that payment for these raw materials

are released on due dates to avoid interest liability. After releasing the payments the inter

unit debit advice is sent to plant. On receipt of the payment advices the supplier’s account

is adjusted in the plant.

Natural Gas

61

Kalol, Phulpur and Aonla plant consume as feed stock and fuel. As per the contract

with ONGC, gas is supplied to IFFCO at the price fixed by Govt. of India from time to

time.

The meters provided at the inlet point in the plants are the basis for monthly billing.

Meter reading is carried out jointly by ONGC / GAIL and IFFCO representatives. The

unit sends the e-mail to head office for making payment to ONGC / GAIL after due

certification of bill by the head of technical department about quantity of gas received.

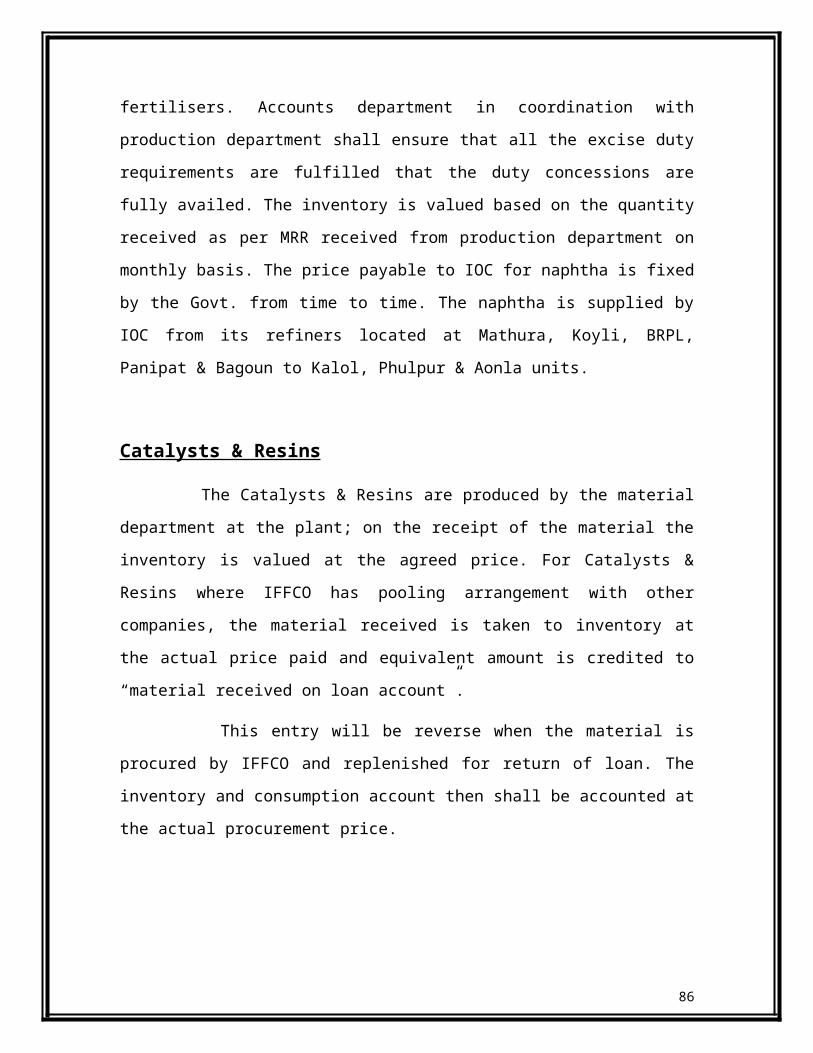

Naphtha

Naphtha is supplied by IOC against advance payment terms. There are excise duty

concessions available for these items provided they are consumed for manufacture of

fertilisers. Accounts department in coordination with production department shall ensure

that all the excise duty requirements are fulfilled that the duty concessions are fully

availed. The inventory is valued based on the quantity received as per MRR received

from production department on monthly basis. The price payable to IOC for naphtha is

fixed by the Govt. from time to time. The naphtha is supplied by IOC from its refiners

located at Mathura, Koyli, BRPL, Panipat & Bagoun to Kalol, Phulpur & Aonla units.

Catalysts & Resins

The Catalysts & Resins are produced by the material department at the plant; on the

receipt of the material the inventory is valued at the agreed price. For Catalysts & Resins

where IFFCO has pooling arrangement with other companies, the material received is

taken to inventory at the actual price paid and equivalent amount is credited to “material

received on loan account”.

This entry will be reverse when the material is procured by IFFCO and replenished

for return of loan. The inventory and consumption account then shall be accounted at the

actual procurement price.

62

63

STORE SECTION

Store of any organization is of vital importance. It is the responsibility of stores to

receive the material required by the organization’s operations to keep it properly & to

issue it as when required. The stores are divided in two subsections for greater flexibility

like receipt and custody section. In IFFCO there are two stores.

a. Store A for Aonla-1( this store contains that spares which are used by Aonla-1)

b. Store B for Aonla-2 unit.( it contains mainly catalysts used by Aonla-2 )

Store has the following warehouses:

Main Store

Cement godown

Petrol Pump

Cable yard

Chemical godown

Paint godown

PDIL store

64

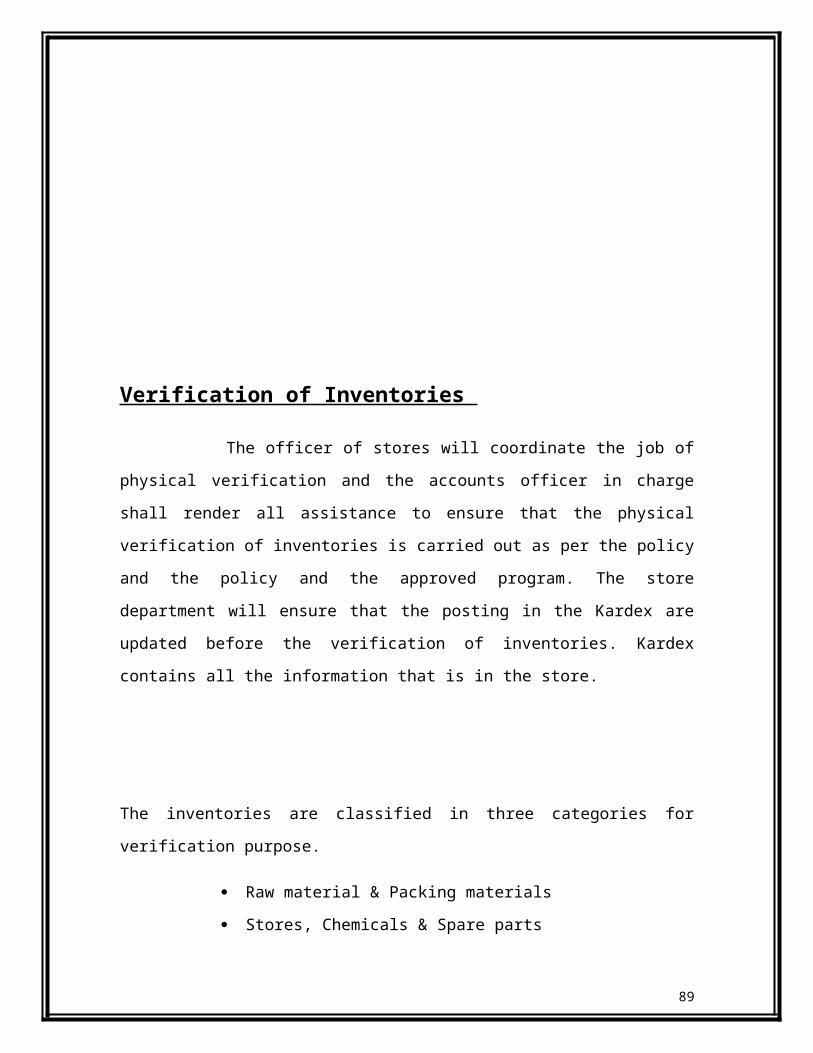

Verification of Inventories

The officer of stores will coordinate the job of physical verification and the

accounts officer in charge shall render all assistance to ensure that the physical

verification of inventories is carried out as per the policy and the policy and the approved

program. The store department will ensure that the posting in the Kardex are updated

before the verification of inventories. Kardex contains all the information that is in the

store.

The inventories are classified in three categories for verification purpose.

Raw material & Packing materials

Stores, Chemicals & Spare parts

Finished products

The stocks of raw materials, packing materials and finished products are to be

verified on quarterly basis by an independent surveyor by the society. No adjustments

need be carried out in the books of accounts unless the discrepancies in liquid raw

materials and solid raw material are in excess of 1% to 5% respectively. This is as per

guidelines issued by the head office.

In case of finished goods also the same principle applied except that no adjustments

in the books of accounts shall be made. However the stock registers shall be adjusted on

the basis of actual stock in order to replace the notional figures of stocks by more

accurate estimate based on physical verification.

The inventories for other items such as stores, spares, construction materials etc. are

also verified every year keeping in view ABC analysis of stock items value and exercise

of verification may be completed by March every year.

65

For the purpose of verification of stores, chemicals & spare parts shall be classified

in to A, B, C categories.

Categories Value (Rs. per unit) Quantum of Verification

A Above Rs. 50,000/- 100%

B 10,001 to 50,000/- 70%

C Below Rs. 10,000/- 25%

A team of stock verifiers shall prepare a stock verification sheet giving the

kardex balance and the physical balance of each item covered in the stock verification.

After filling up the particulars of the value and quality discrepancies with reference to the

priced stores ledger balance, the stock verification sheets shall be forwarded to the

materials department for scrutiny and reconciliation and adjustment in consultation with

finance department accepted shortage shall be processed for the approval of the

competent authority.

RECONCILIATION AND ADJUSTMENT

After each physical verification by the custodians of inventories and suitable

adjustment action has to be taken. It is desirable to complete the physical verification

work by March every year so that reconciliation/adjustment action can be completed

within the year itself.

Internal Check

1) One set of document for receipts, issues and return of materials shall be sent to the

accounting section of finance department. Based on these documents, priced store

ledger shall be prepared for each item for stores. The material code number between

stores and accounts shall be identical. The priced store ledger shall provide value of

each receipt, Issue and return transaction along with quantity ledger. The quantity

balance appearing in priced store ledger shall serve as counter check for accuracy of

66

bin card balance in store which is essential for proper functioning of inventory control

system

2) The priced store ledger shall not be maintained for large number of low value

items such as stationery, medicines, canteen stores etc. in this case the expenditure

shall be charged to the appropriate expense account at time purchase. Quantitative

record shall be kept by the concerned department and shall be produced as and when

required for audit purpose.

Inventory Control

Inventory control is concerned with minimizing the total cost of inventory. The

three main factors in inventory control decision making process are:

a. The cost of holding the stock (e.g., based on the interest rate).

b. The cost of placing an order (e.g., for row material stocks) or the set-up cost of

production.

c. The cost of shortage, i.e., what is lost if the stock is insufficient to meet all

demand.

The third element is the most difficult to measure and is often handled by

establishing a "service level" policy, e. g, certain percentage of demand will be met from

stock without delay.

The Inventory Management system and the Inventory Control Process provides

information to efficiently manage the flow of materials, effectively utilize people and

equipment, coordinate internal activities, and communicate with customers.

Inventory Management and the activities of Inventory Control do not make decisions or

manage operations; they provide the information to Managers who make more accurate

and timely decisions to manage their operations.

67

Inventory control is a systematic control and regulation of purchase and usage of

materials in such a way so as to maintain an even flow of production at the same time

avoiding excessive investment in inventories. Efficient material control reduces losses

and wastage of materials that otherwise pass unnoticed.

Inventory control is the core of material management. The need and importance

of inventories varies in direct proportion to the idle time cost of men and machinery, and

urgency of requirements. If men and machinery in the factory could wait and so could the

customers, materials good not lie in want for them and no inventory need to be carried.

But it is highly uneconomical to keep the men and machine waiting and the requirements

for modern life are so urgent that they can not wait for materials to arrive after the need

for them has arisen.

TECHNIQUES OF INVENTORY CONTROL

68

Reduction of surplus stock is an essential requirement inventory control. Various

techniques are available to solve the various types of problems associated with inventory

control:-

1) Min-Max plan

2) Order cycling system

3) Fixation of various levels

4) Use of control ratios

5) Review of slow and non-moving items

6) The ABC Analysis

1) Min-Max plan:

In this plan analyst lays down a maximum and minimum for each stock item. Minimum

level establishes the reorder point and order is placed for quantity of material, which will

bring it to the maximum level.

2) Order Cycling System:

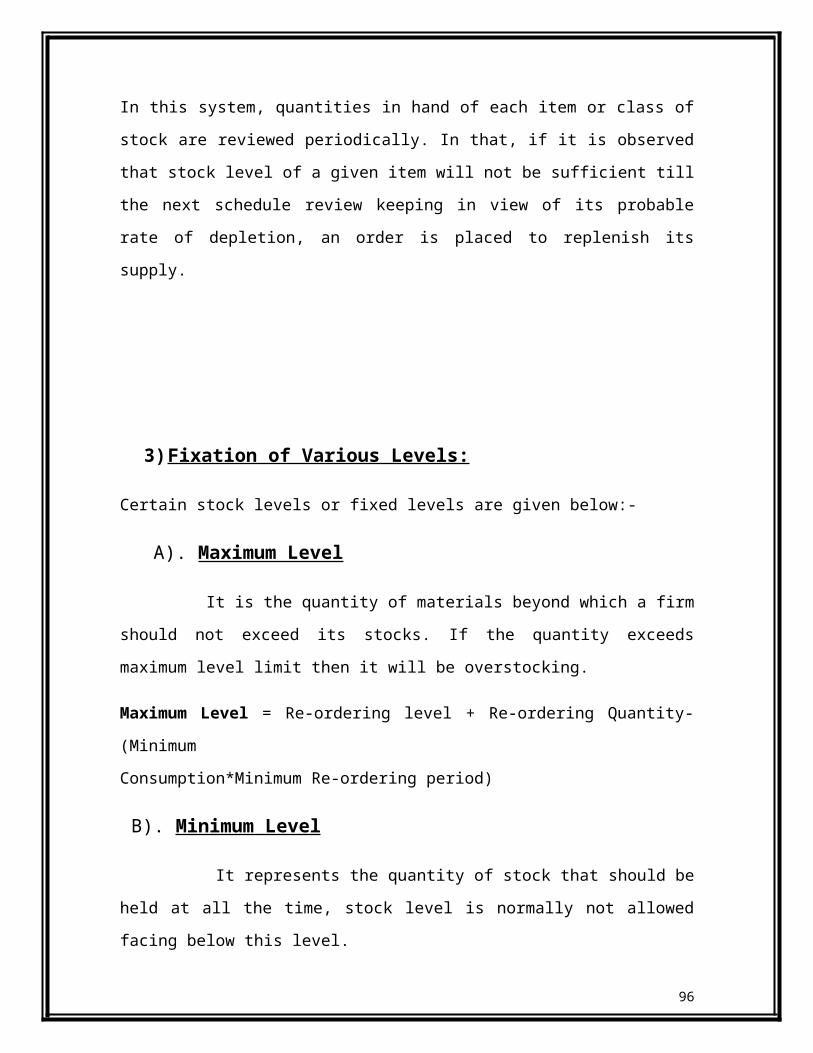

In this system, quantities in hand of each item or class of stock are reviewed periodically.

In that, if it is observed that stock level of a given item will not be sufficient till the next

schedule review keeping in view of its probable rate of depletion, an order is placed to

replenish its supply.

3) Fixation of Various Levels:

69

Certain stock levels or fixed levels are given below:-

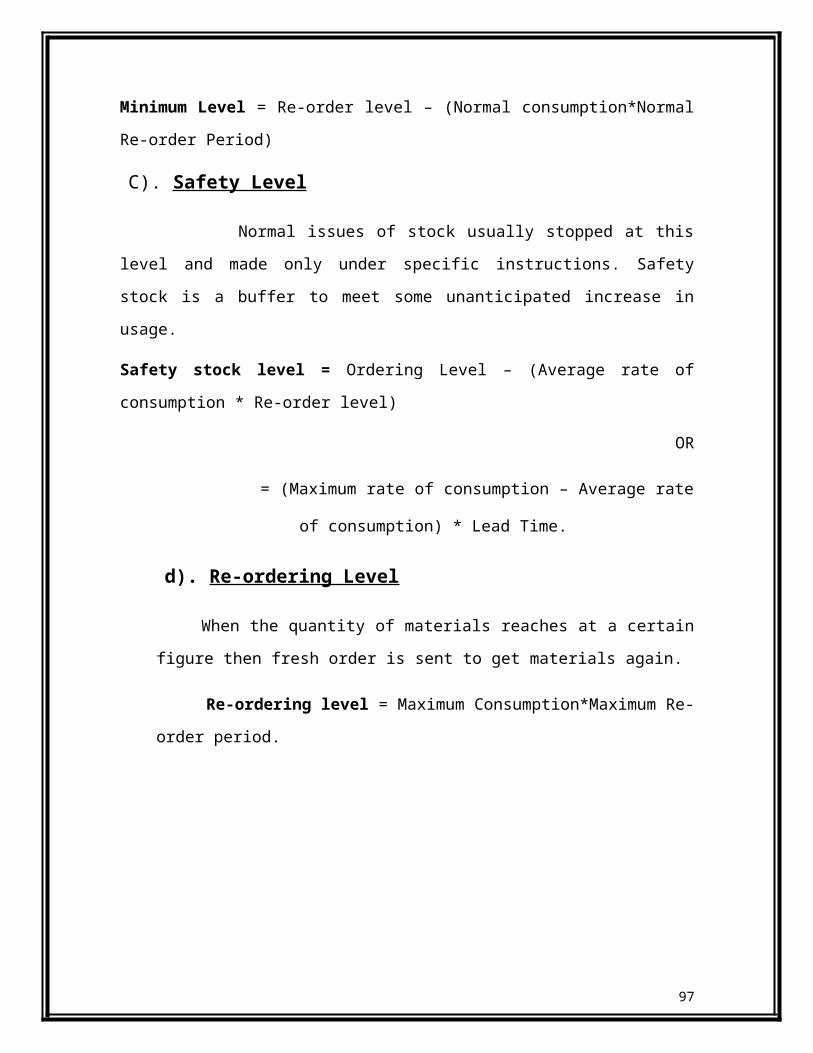

A). Maximum Level

It is the quantity of materials beyond which a firm should not exceed its stocks. If

the quantity exceeds maximum level limit then it will be overstocking.

Maximum Level = Re-ordering level + Re-ordering Quantity-(Minimum

Consumption*Minimum Re-ordering period)

B). Minimum Level

It represents the quantity of stock that should be held at all the time, stock level is

normally not allowed facing below this level.

Minimum Level = Re-order level – (Normal consumption*Normal Re-order Period)

C). Safety Level

Normal issues of stock usually stopped at this level and made only under specific

instructions. Safety stock is a buffer to meet some unanticipated increase in usage.

Safety stock level = Ordering Level – (Average rate of consumption * Re-order level)

OR

= (Maximum rate of consumption – Average rate of consumption) * Lead Time.

d). Re-ordering Level

When the quantity of materials reaches at a certain figure then fresh order is sent to

get materials again.

Re-ordering level = Maximum Consumption*Maximum Re-order period.

70

4) Use of Control Ratios:

Inventory turnover ratio helps management to avoid capital being locked up

unnecessarily. This ratio reveals the efficiency of stock keeping .

Inventory turnover ratio =Cost of materials consumed / Cost of average stock held

during the period

Where,