iea’s medium-term renewable energy - chicago · iea’s medium-term renewable energy ......

TRANSCRIPT

© OECD/IEA 2015© OECD/IEA 2015

The Role of Bioenergy in IEA’s Medium-Term Renewable Energy Market Report 2015

Adam Brown and Pharoah Le Feuvre

Renewable Energy Division

International Energy Agency

tcbiomass2015 - Technology for the Bioeconomy

Chicago 2-5 November 2015

© OECD/IEA 2014

Role of Bioenergy in IEA ETP Scenarios

IEA: Energy Technology Perspectives 2015

Bioenergy is largest primary energy carrier in 2 DS in 2050

© OECD/IEA 2015

The share of non-hydro renewable electricity generation is rising

……. however bioenergy’s share drops due to faster growth of onshore wind and PV.

Renewable electricty generation growing steadily

Renewable generation by technology (2005-20)

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Gene

ratio

n (TWh)

Hydropower Bioenergy Onshore wind Offshore wind Solar PV Geothermal STE Ocean

54%

28%22%

Share of bioenergy in non-hydro

renewable generation

ForecastHistorical

© OECD/IEA 2015

Bioenergy generation by region (2006-20)

As growth slows in some major OECD bioenergy markets, higher levels of generation are anticipated in certain non-OECD countries with abundant resources and policy

drivers.

Medium-term market overview for bioenergy electricity by region

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

TWh

OECD Americas OECD Asia Oceania OECD Europe Africa Asia

China Non-OECD Europe Non-OECD Americas Middle East

© OECD/IEA 2015

Increased competition from other renewables

High levels of incentives are no longer necessary for solar PV and onshore wind in many markets. Support for bio-electricity focussing on the most cost-efficient applications.

Historical and forecast global weighted average generation costs for new

onshore wind and PV plants vs. selected reference bioenergy LCOEs

0

50

100

150

200

250

300

350

400

2010 2015 2020 2010 2015 2020 Dedicated

biomass

Co-firing

(woodchips &

pellets)

Wastes &

residues

Emerging

Technoligies

e.g.

gasification

Aenerobic

Digestion

Onshore wind Solar PV - utility scale Selected bioenergy technologies

USD

2014

/MWh

© OECD/IEA 2015

Notable marketplace adjustments 2014-15

Country Revision Market

Impact

Canada Coal to biomass conversions stimulated by phase out of coal in Ontario. ▲

BrazilRecent renewable energy Power Purchase Agreement (PPA) auctions held over the 2013-

14 period offered more favorable terms to bioenergy projects.▲

KoreaAnnual increase in requirements of Portfolio Standard (RPS) for 13 largest power

companies drives biomass co-firing.▲

Germany

Downward FIT adjustments, removal of some project-specific bonus tariffs, restriction of

new capacity eligible for support to 100 MW per year until 2017, with support then

phased out entirely for new plants above 100 kW.

▼

PolandSupport for biomass will reduced in existing green certificate scheme. Restrictions

increased on volume of certificates awarded for co-firing.▼

United Kingdom

No budget allocated for conversions within the initial Contracts for Difference (CfD)

auction round (besides two coal projects already confirmed), and changes introduced

which alter support for biomass unit conversions under the Renewables Obligation

scheme. Climate Change Levy exemption for renewables removed.

▼

Diverse policy adjustments affect bioenergy prospects in key markets.

© OECD/IEA 2015

Stabilisation of global biofuels production anticipated

World biofuels production by volume 2008-20

Global conventional biofuels production forecast to stabilise over the medium-term.

0.0

0.5

1.0

1.5

2.0

2.5

0

20

40

60

80

100

120

140

160

2005 2007 2009 2011 2013 2015 2017 2019

mb/d

Billion

litres

United States biofuels Brazil biofuels OECD Europe biofuels Rest of the world biofuels

© OECD/IEA 2015

Mandates effectively support global biofuels production

Blending mandates support demand, even with a low oil price environment.

Comparison of global biofuels production and oil prices 2007-20 (indexed)

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2007

= 1

00

MTRMR 2015 global

biofuels production

IEA crude oil import

average price

Forecast

Forward assumption

Historical

© OECD/IEA 2015

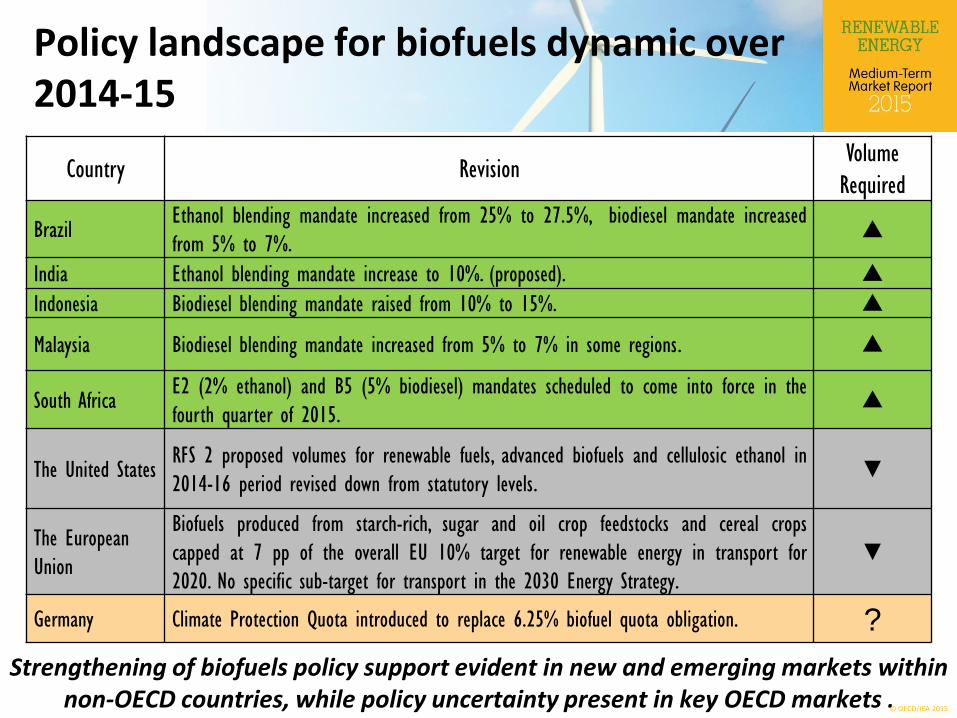

Policy landscape for biofuels dynamic over 2014-15

Country Revision Volume

Required

BrazilEthanol blending mandate increased from 25% to 27.5%, biodiesel mandate increased

from 5% to 7%.▲

India Ethanol blending mandate increase to 10%. (proposed). ▲Indonesia Biodiesel blending mandate raised from 10% to 15%. ▲

Malaysia Biodiesel blending mandate increased from 5% to 7% in some regions. ▲

South AfricaE2 (2% ethanol) and B5 (5% biodiesel) mandates scheduled to come into force in the

fourth quarter of 2015.▲

The United StatesRFS 2 proposed volumes for renewable fuels, advanced biofuels and cellulosic ethanol in

2014-16 period revised down from statutory levels.▼

The European

Union

Biofuels produced from starch-rich, sugar and oil crop feedstocks and cereal crops

capped at 7 pp of the overall EU 10% target for renewable energy in transport for

2020. No specific sub-target for transport in the 2030 Energy Strategy.

▼

Germany Climate Protection Quota introduced to replace 6.25% biofuel quota obligation. ?

Strengthening of biofuels policy support evident in new and emerging markets within non-OECD countries, while policy uncertainty present in key OECD markets .

© OECD/IEA 2015

Early commercialisation in the advanced biofuels sector

Commissioned commercial scale advanced biofuel plants

Advanced biofuels – needed for long-term decarbonisation of the transport sector –are starting to scale up.

© OECD/IEA 2015

Production costs assessment for cellulosic ethanol

Analysis of a breakeven crude oil price for cellulosic ethanol

Production costs for cellulosic ethanol anticipated to be above 2015 oil prices, but significant cost reduction potential identified within the industry.

2014-15 industry focused figures

≤40 50 60 70 80 90 100 110 120 130 140 150 160 170 180 190 200+

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Gasolin

e US

D / Litre

Crude oil price Wholesale gasoline price (USD 10 margin) Advanced biofuel cost estimate (adj. for energy content)

Achievable with

industry expansion?

© OECD/IEA 2015

Further policy support required to accelerate growth in renewable heat

Consumption of modern renewable energy for heat 2008-20

Challenges persist to increasing the contribution of renewables and decarbonising the heat sector, however established renewable heat policies have proved successful.

0

2

4

6

8

10

12

14

16

18

20

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

EJ

Geothermal Solar thermal Modern bioenergy

© OECD/IEA 2015

Lower heating oil prices mean increased competition for domestic biomass systems

3

4

5

6

7

8

9

1Q -

2012

3Q -

2012

1Q -

2013

3Q -

2013

1Q -

2014

3Q -

2014

1Q -

2015Eu

ro cen

t / kW

h

Domestic heating oil Consumer wood pellets

Natural gas

30

50

70

90

110

130

150

170

190

2012 2013 2014 2015 2016 2017 2018 2019 2020

Thou

sand

s

Total installed wood pellet stoves

Domestic <50kW wood pellet boilers

Forecast

Source: AIBIOM

(2015)

Historical

Medium-term forecasted growth in wood pellet system installation (left)

and delivered domestic fuel cost comparison 2012-15 (right) in Austria

Downward movement in heating oil costs has reduced running costs from oil-fired heating systems and closed the fuel price gap to pellets.

© OECD/IEA 2015

Biomass Supply

Source: Adapted from IPCC (2011), and supplemented with IEA data

c. 150 EJ needed to supply transport and heat and power needs (8-11 billion tonnes)Around ½ from residues/wastes, ½ from crops

© OECD/IEA 2015

IEA Biofuel Roadmap - Vision

Biofuel supply grows rapidly and reaches 32EJ in 2050

Diesel/kerosene-type biofuels particularly important to decarboniseheavy transport modes

Large-scale deployment of advanced biofuels will be key

© OECD/IEA 2015

Bioenergy must be part of a broader context?

Source: IEA (2014), Energy Technology perspectives 2014

Integration with

agriculture and forestry

- coproducts and

residues

Coproduction

with biobased

materials Biofuels

Bioenergy heat & power

Environmental

services

(emissions

reductions, wastes)

© OECD/IEA 2015

Conclusions

Renewable growth continues despite low fossil fuel price context and policy uncertainties

The effect of the lower oil price environment is less pertinent for bioenergy for power, but biofuels and heat sectors are impacted in some circumstances

Bio-electricity faces potential competition from lower cost renewables, with opportunities focused on low cost and well integrated projects

Continued policy action is needed for heat and biofuel sectors. Policy uncertainties risk undermining investor confidence and are dampening growth

Good progress in commercialisation of cellulosic ethanol and significant cost reduction potential but long term policy and market framework uncertain

Slow commercialization of thermal processes and energy crops

Integration is the key!

© OECD/IEA 2015

For further insights and analysis…

The Medium-Term Renewable Energy Market Report 2015 was launched on 02 October 2015 and can be purchased online at:

www.iea.org

Thank you for your attention!