ias 7 cash flow statements

TRANSCRIPT

05/02/2023IAS 7 1

IAS 7CASH FLOW STATEMENTS

05/02/2023IAS 7 2

Objective Classify historic cash flows during a

period into operating, investing and financing activities

Basis to assess ability to generate cash Assess needs to utilise cash Assess timing and certainty of

generation of cash

05/02/2023IAS 7

3ScopeAll entities must present a cash flow statement as part of financial statements for each period for which financial statements are prepared under IFRS

05/02/2023IAS 7 4

Benefits of cash flow information

Evaluate › how net assets have changed› financial structure, liquidity and solvency› ability to affect amounts, timing and certainty of cash flows› ability to adapt to changing circumstances and opportunities› ability to generate cash› accuracy of past assessments› relationship between profit and cash flow› impact of changing prices

Develop models to assess and compare present value of future cash flows of different entities (in order to perform business or project valuations)

Enhance comparability of operating performance Eliminates effects of differences in accounting treatment

between entities

05/02/2023IAS 7 5

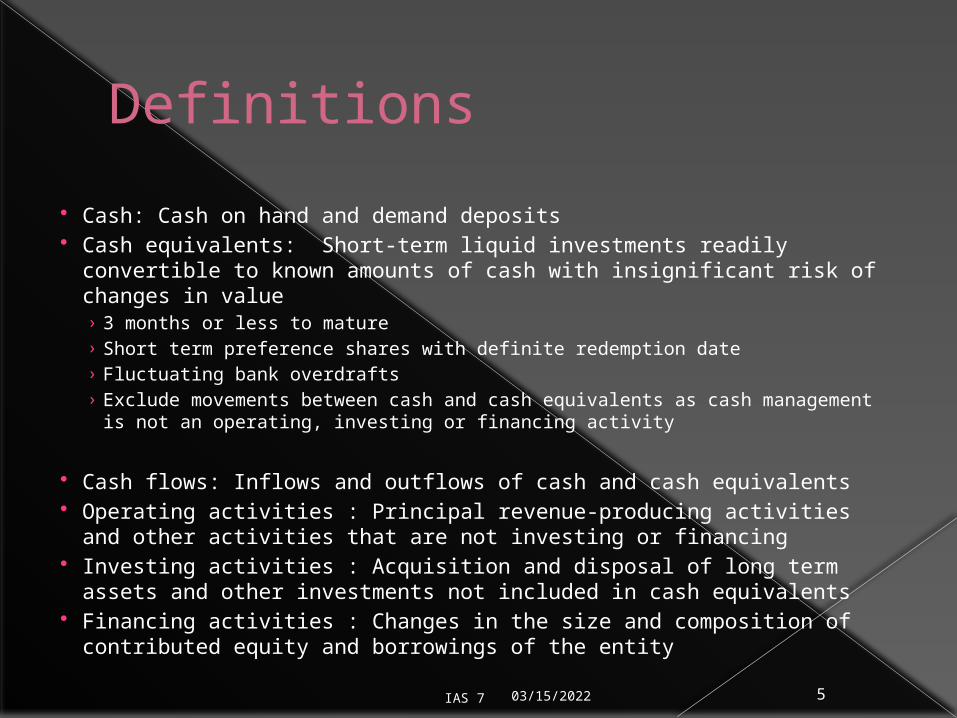

Definitions Cash: Cash on hand and demand deposits Cash equivalents: Short-term liquid investments readily convertible

to known amounts of cash with insignificant risk of changes in value › 3 months or less to mature› Short term preference shares with definite redemption date› Fluctuating bank overdrafts› Exclude movements between cash and cash equivalents as cash

management is not an operating, investing or financing activity

Cash flows: Inflows and outflows of cash and cash equivalents Operating activities : Principal revenue-producing activities and other

activities that are not investing or financing Investing activities : Acquisition and disposal of long term assets and

other investments not included in cash equivalents Financing activities : Changes in the size and composition of

contributed equity and borrowings of the entity

05/02/2023IAS 7 6

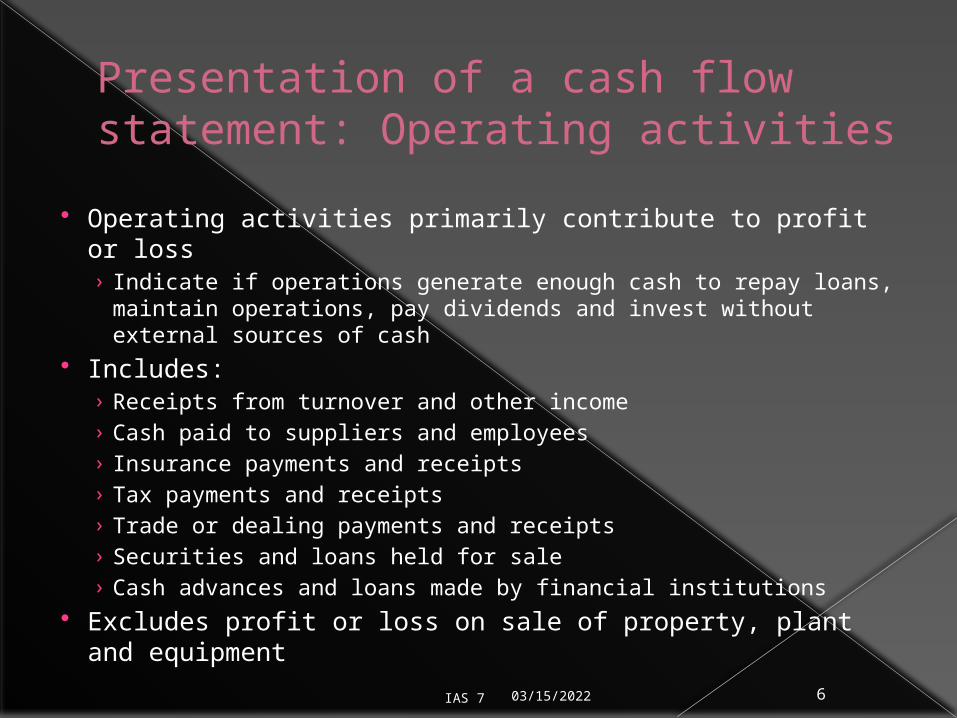

Presentation of a cash flow statement: Operating activities

Operating activities primarily contribute to profit or loss› Indicate if operations generate enough cash to repay loans,

maintain operations, pay dividends and invest without external sources of cash

Includes:› Receipts from turnover and other income› Cash paid to suppliers and employees› Insurance payments and receipts› Tax payments and receipts› Trade or dealing payments and receipts› Securities and loans held for sale› Cash advances and loans made by financial institutions

Excludes profit or loss on sale of property, plant and equipment

05/02/2023IAS 7 7

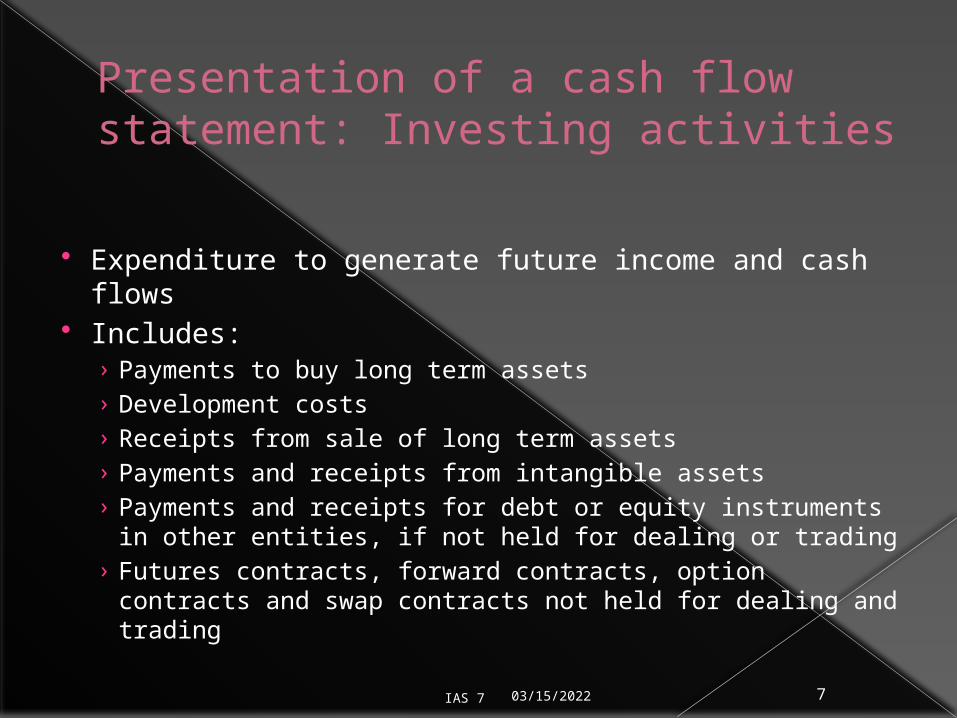

Presentation of a cash flow statement: Investing activities

Expenditure to generate future income and cash flows

Includes:› Payments to buy long term assets › Development costs› Receipts from sale of long term assets› Payments and receipts from intangible assets› Payments and receipts for debt or equity instruments

in other entities, if not held for dealing or trading› Futures contracts, forward contracts, option contracts

and swap contracts not held for dealing and trading

05/02/2023IAS 7 8

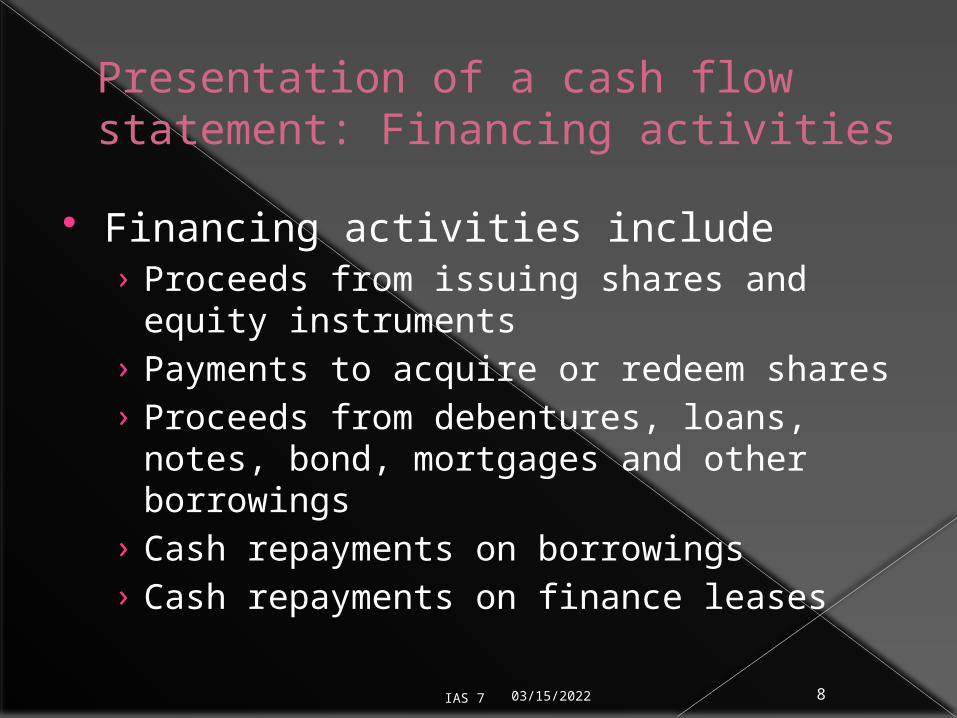

Presentation of a cash flow statement: Financing activities

Financing activities include› Proceeds from issuing shares and equity

instruments› Payments to acquire or redeem shares› Proceeds from debentures, loans, notes,

bond, mortgages and other borrowings› Cash repayments on borrowings› Cash repayments on finance leases

05/02/2023IAS 7 9

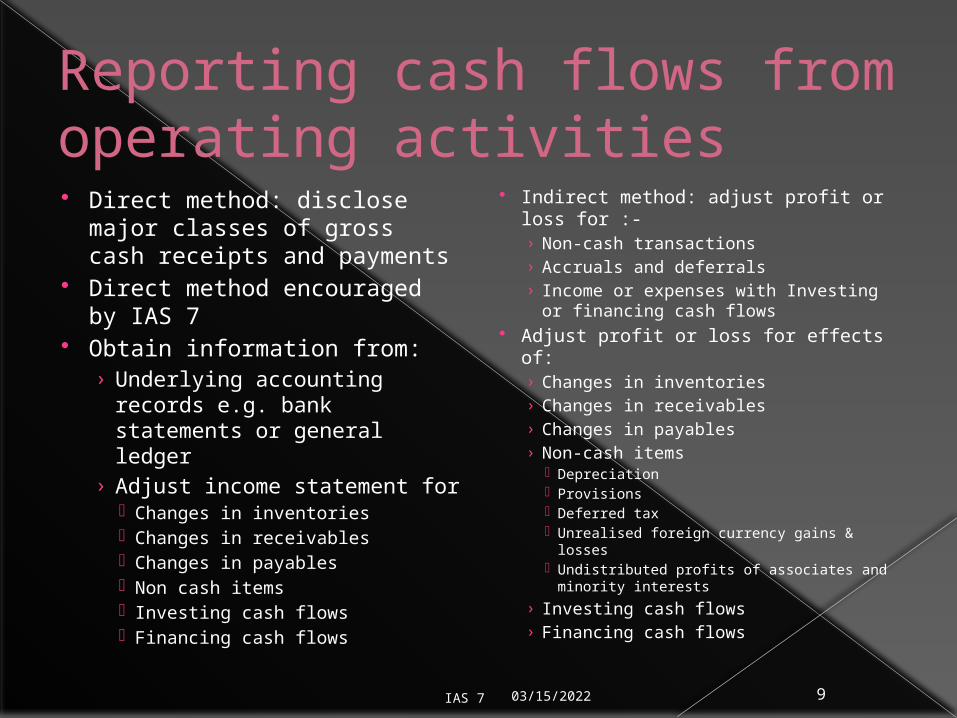

Reporting cash flows from operating activities Direct method: disclose major

classes of gross cash receipts and payments

Direct method encouraged by IAS 7

Obtain information from:› Underlying accounting

records e.g. bank statements or general ledger

› Adjust income statement for Changes in inventories Changes in receivables Changes in payables Non cash items Investing cash flows Financing cash flows

Indirect method: adjust profit or loss for :-› Non-cash transactions› Accruals and deferrals› Income or expenses with Investing

or financing cash flows Adjust profit or loss for effects of:

› Changes in inventories› Changes in receivables› Changes in payables› Non-cash items

Depreciation Provisions Deferred tax Unrealised foreign currency gains &

losses Undistributed profits of associates and

minority interests› Investing cash flows› Financing cash flows

05/02/2023IAS 7 10

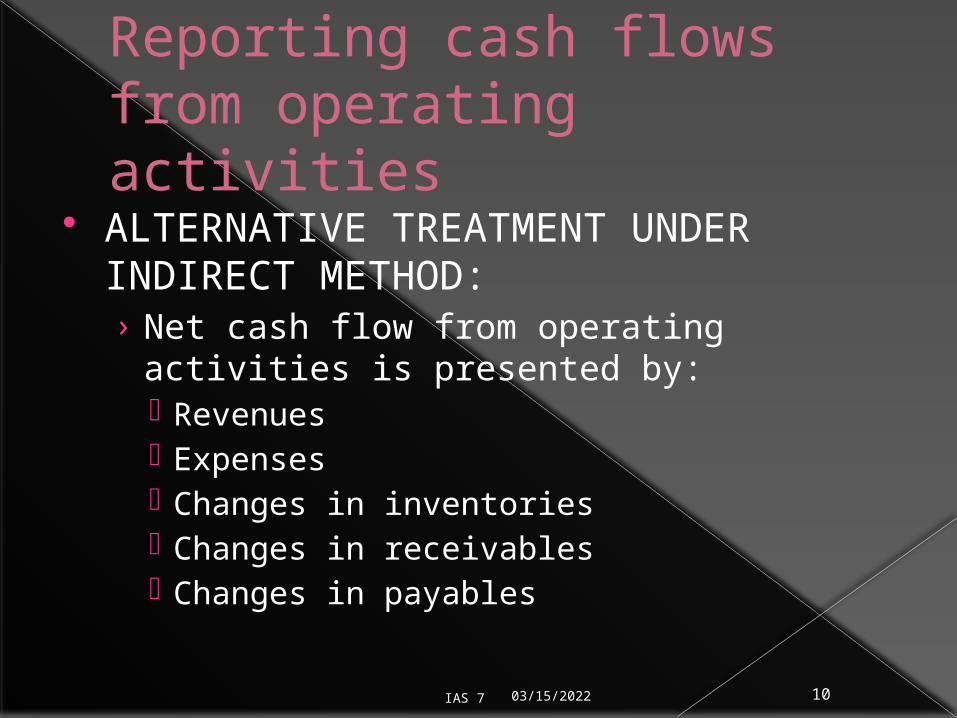

Reporting cash flows from operating activities

ALTERNATIVE TREATMENT UNDER INDIRECT METHOD:› Net cash flow from operating activities is

presented by: Revenues Expenses Changes in inventories Changes in receivables Changes in payables

05/02/2023IAS 7 11

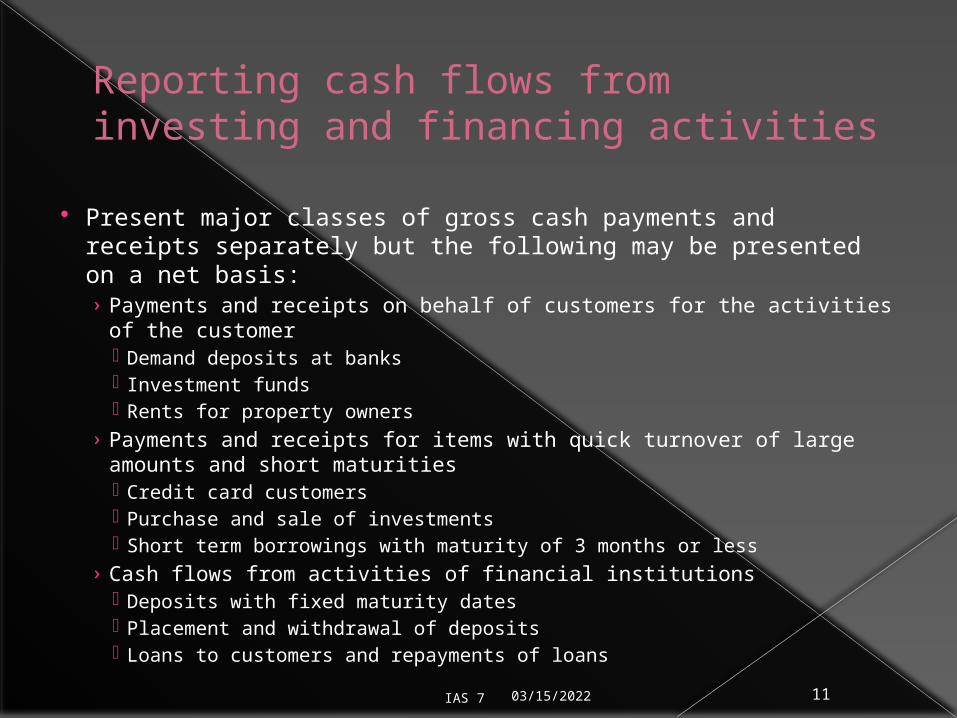

Reporting cash flows from investing and financing activities

Present major classes of gross cash payments and receipts separately but the following may be presented on a net basis:› Payments and receipts on behalf of customers for the activities of the

customer Demand deposits at banks Investment funds Rents for property owners

› Payments and receipts for items with quick turnover of large amounts and short maturities Credit card customers Purchase and sale of investments Short term borrowings with maturity of 3 months or less

› Cash flows from activities of financial institutions Deposits with fixed maturity dates Placement and withdrawal of deposits Loans to customers and repayments of loans

05/02/2023IAS 7 12

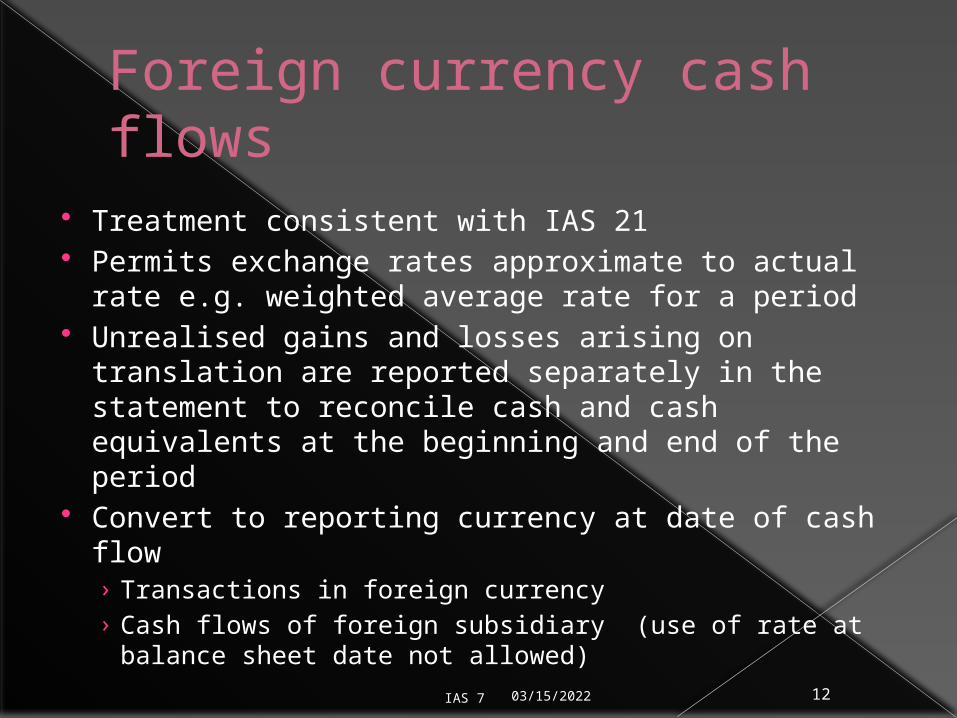

Foreign currency cash flows Treatment consistent with IAS 21 Permits exchange rates approximate to actual rate

e.g. weighted average rate for a period Unrealised gains and losses arising on translation

are reported separately in the statement to reconcile cash and cash equivalents at the beginning and end of the period

Convert to reporting currency at date of cash flow› Transactions in foreign currency› Cash flows of foreign subsidiary (use of rate at balance

sheet date not allowed)

05/02/2023IAS 7 13

Interest and dividends Cash flows from interest and dividends

received and paid are› Disclosed separately

Whether interest is expensed or capitalised› Classified in a consistent manner from period

to period as Operating (e.g. for financial institutions) Investing (cost or returns on investments) Financing activities (cost of obtaining finance) There is no consensus for entities other than

financial institutions

05/02/2023IAS 7 14

Taxes on income Disclose cash flows separately under

operating activities If specifically identified with financing or

investing activities, classify as appropriate (usually difficult to identify as cash flows of tax and transactions arise in different periods)

When tax cash flows are allocated over more than one class, the total amount of taxes paid is disclosed

05/02/2023IAS 7 15

Investments in subsidiaries, associates and joint ventures

Only report cash flows between the entity and investee e.g. dividends and advances

Joint ventures› Proportionate consolidation method:

proportionate share of jointly controlled cash flows are reported in consolidated CFS

› Equity method: disclose cash flows representing investment in the entity, distributions and other payments and receipts between entity and jointly controlled entity

05/02/2023IAS 7 16

Acquisitions and disposals of subsidiaries and other business units

Present aggregate cash flows of the following in separate line items and classify as investing activities› Cash flow effect of disposals versus acquisitions (not

deducted from each other)› Cash paid or received as purchase or sale consideration net

of cash and cash equivalents acquired or disposed of Disclose

› Total purchase and disposal consideration› Cash and cash equivalent portion of total consideration › Cash and cash equivalents in the business unit acquired or

disposed of› Other assets and liabilities in the subsidiary acquired or

disposed of, summarised by each major category

05/02/2023IAS 7 17

Non-cash transactions Exclude non cash investing and

financing transactions from cash flow statement e.g.› Assets purchased with loans or finance

leases› Acquisition of shares in another entity› Conversion of debt to equity

05/02/2023IAS 7 18

Components of cash and cash equivalents

Reconcile cash and cash equivalents in the cash flow statement with cash and cash equivalents in the balance sheet

Disclose the accounting policy to determine cash and cash equivalents

Report changes in accounting policy in accordance with IAS 8

05/02/2023IAS 7 19

Other disclosures Significant cash and cash equivalent balances held

but not available for use by the group› E.G. cash held by a subsidiary in a country with

exchange controls Information about financial position and liquidity of

an entity› Undrawn borrowing facilities and restrictions on use› Cash flows of joint ventures reported using proportionate

consolidation› Cash flows that increase operating capacity vs cash

flows that maintain operating capacity› Segmental cash flows by industry and geographical

segment

05/02/2023IAS 7 20

Summary All IFRS financial statements must contain a cash

flow statement Cash flows are presented using the direct

method or the indirect method Non-cash transactions are excluded Cash flows are classed as operating activities,

investing activities or financing activities Cash flows are reconciled to movements of cash

and cash equivalents in the balance sheet Accounting policy and major restrictions on cash

flow are disclosed

05/02/2023IAS 7 21

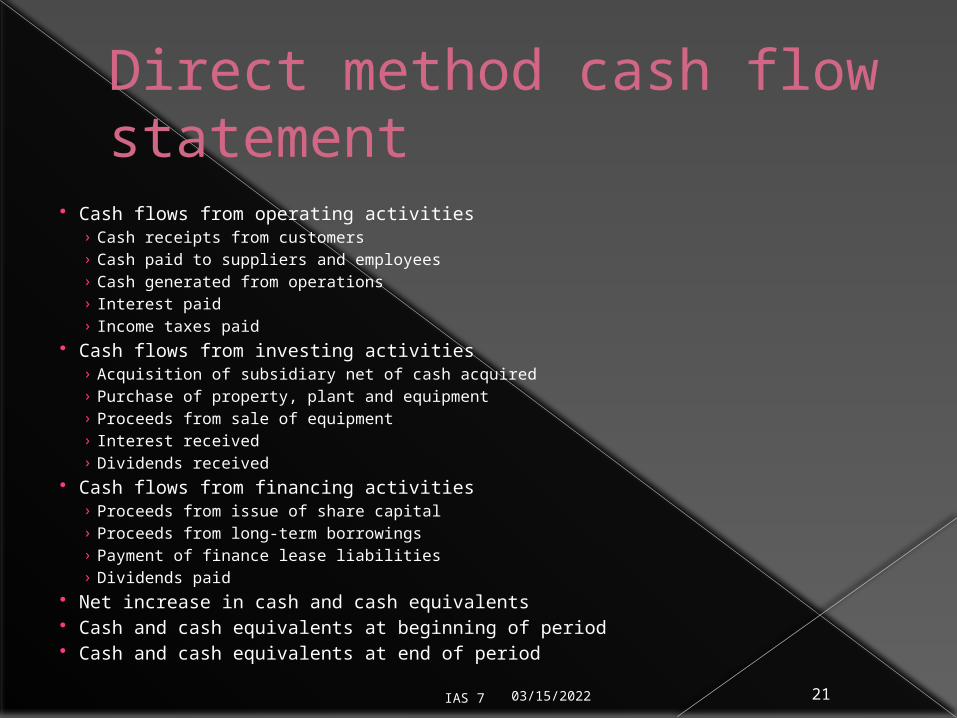

Direct method cash flow statement

Cash flows from operating activities› Cash receipts from customers› Cash paid to suppliers and employees› Cash generated from operations› Interest paid› Income taxes paid

Cash flows from investing activities› Acquisition of subsidiary net of cash acquired› Purchase of property, plant and equipment› Proceeds from sale of equipment› Interest received› Dividends received

Cash flows from financing activities› Proceeds from issue of share capital› Proceeds from long-term borrowings› Payment of finance lease liabilities› Dividends paid

Net increase in cash and cash equivalents Cash and cash equivalents at beginning of period Cash and cash equivalents at end of period

05/02/2023IAS 7 22

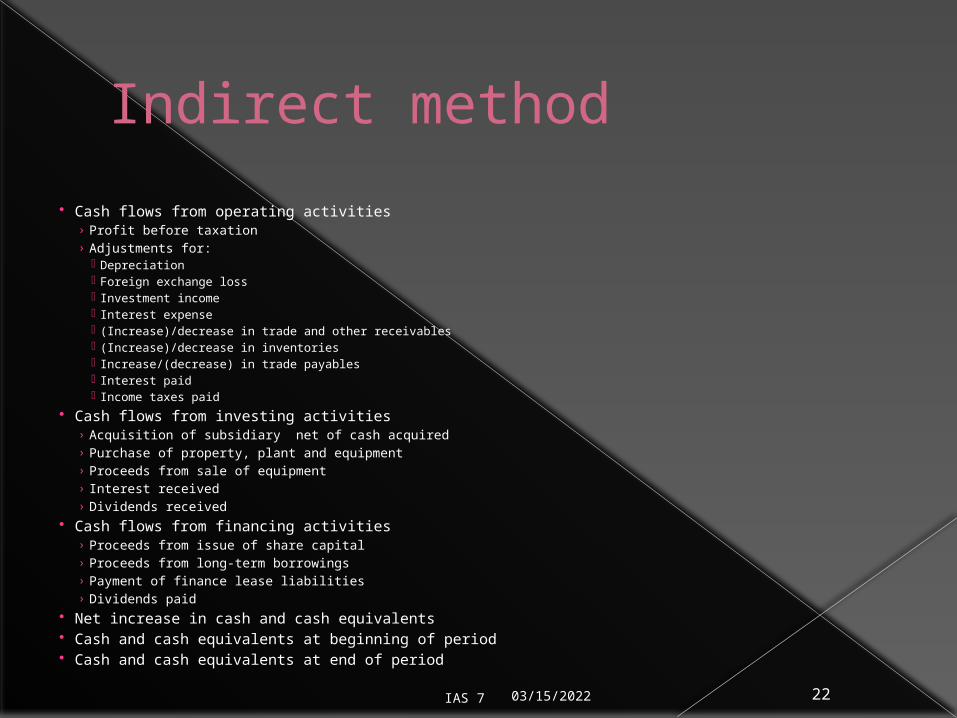

Indirect method Cash flows from operating activities

› Profit before taxation› Adjustments for:

Depreciation Foreign exchange loss Investment income Interest expense (Increase)/decrease in trade and other receivables (Increase)/decrease in inventories Increase/(decrease) in trade payables Interest paid Income taxes paid

Cash flows from investing activities› Acquisition of subsidiary net of cash acquired› Purchase of property, plant and equipment› Proceeds from sale of equipment› Interest received› Dividends received

Cash flows from financing activities› Proceeds from issue of share capital› Proceeds from long-term borrowings› Payment of finance lease liabilities› Dividends paid

Net increase in cash and cash equivalents Cash and cash equivalents at beginning of period Cash and cash equivalents at end of period