ia1 lecture 11people.exeter.ac.uk/wl203/beam011/materials/lecture 11/ia1 lecture... · lecture 11...

TRANSCRIPT

1

Investment Analysis 1

BEAM011

Lecture 11

Revision Lecture

Dr Jon Tucker

Xfi Centre for Finance and Investment

University of Exeter

Lecture Objectives

To focus on the topics and component techniques covered in the Investment Analysis 1 module:

1. Financial Statement Analysis 1&2

2. Financial Ratio Analysis

3. Industry Analysis

4. Company Valuation

5. Technical Analysis

6. Creative Accounting

7. Financial Statement Modelling

8. Financial Distress Analysis

9. International Investment Analysis

2

Financial Statement Analysis 1

• Discussion of different types of investor – passive, intuitive, stock screeners

• Conclusion that we should aim to be fundamental analysts – studying a wide range of financial information to determine intrinsic value

• Understanding of key financial statements:

Balance Sheet – financial position

Income Statement – financial performance

Cash Flow Statement – source and application of cash

• What should we understand here?

• Purpose, structure, and component items of each statement

• Accounting conventions governing their preparation

• How we read/interpret each statement

How do we ‘read/interpret’ each of the financial statements?

• Balance Sheet – asset mix, liquidity, financing

• Income Statement – gross profit, expenses, net profit

• Cash Flow Statement – dividend cover from cash, reliance on

outside financing, prudent cash management?

• Process of fundamental analysis:

• Knowing the business

• Analysing information

• Forecasting payoffs

• Converting forecast into valuation

• Investment decision

Financial Statement Analysis 1

3

• Understanding of the other information presented with the Annual Report and how it might be employed by the investment analyst

� Operating and Financial Review – systematic discussion of financial performance (main factors underlying) and position (capital structure, treasury, etc.)

� Chairman’s Statement – unaudited view of current and likely future performance/developments

� Directors’ Report – functional report – includes business review, directors’ shareholdings, various company policies, etc.

� Corporate Governance – governance structures, internal and external control mechanisms, make-up of board, compliance, etc.

� Corporate Social Responsibility – economic, social and environmental policies

Financial Statement Analysis 2

� Segmental Financial Reports – disaggregates key information by line of business, geographical market (as subject to different levels of risk, growth, profitability)

� Statement of Recognised Gains and Losses – looks at all gains and losses (not just those in income statement)

� The Value Added Statement – value added by ‘stakeholders’ in the business (employees, suppliers, government)

� Environmental Reporting – externalities not recorded in financial statements – gives environmental policies and performance

� Inflation Accounting and Reporting – shows impact of inflation on financial position and performance

� Statement of Stockholders’ Equity – shows components of stockholders’ equity or the investment of the owners in the firm(earnings reinvested in the business, various accounting adjustments that reflect selected market value changes in certain investments in securities, etc.)

Financial Statement Analysis 2

4

The Analyst’s Template:

• Key points:

• Generic and needs to be customised

• Narrative is the most important/difficult part

• How does the firm create value (its business model)?

• What are its links with the industry analysis? Macro environment?

• Broad structure:

• ‘Tear-sheet’ – financial market performance summary

• Company profile

• Profitability

• Long and short-term finance (solvency) + efficiency

• Investor ratios

• Risk analysis

• Forecasts + company valuation

• Prospects and conclusions (recommendation)

Financial Statement Analysis 2

Financial Ratio Analysis

Why use financial ratios?

• To gauge financial position and performance

• Can be used for planning, control and evaluation

Nature of financial ratios

• Financial statement and resource variables, gauges relatives rather than absolutes

• The experienced analyst calculates the ratios they need rather than a prescribed list – ‘calculate the ratio needed to do the job’

Comparators

• Range of comparator measures

• Best = past performance, target and/or similar firms

5

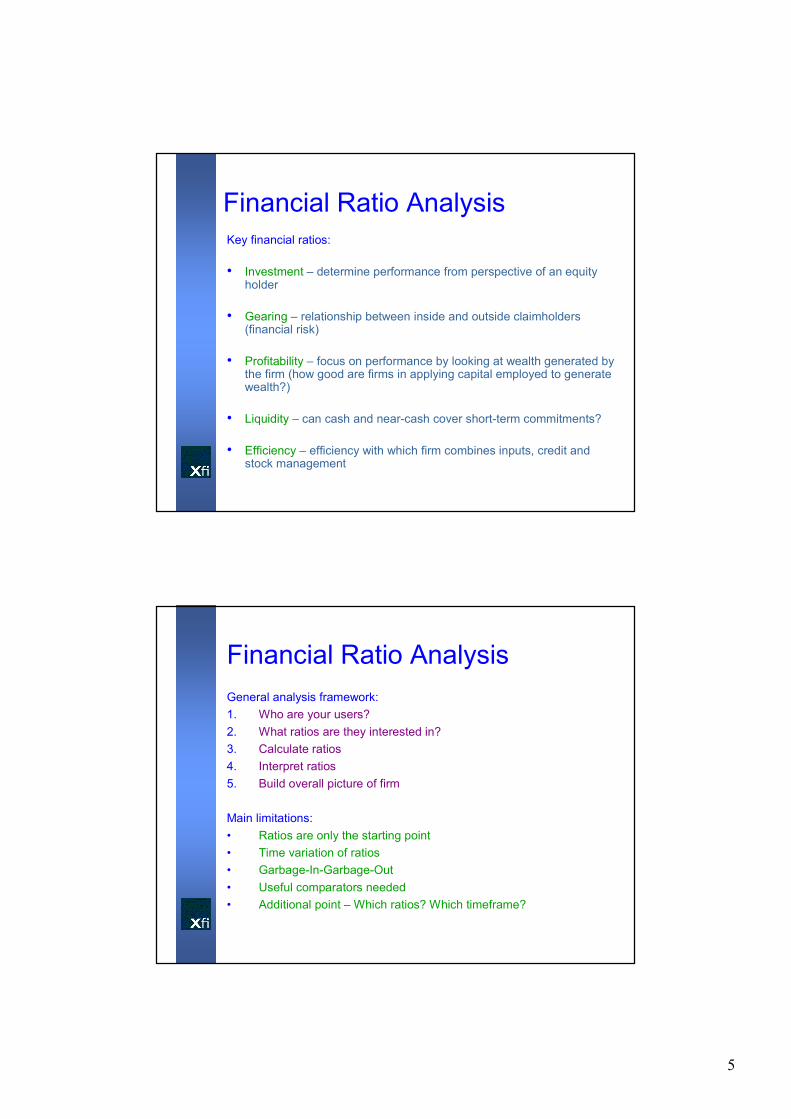

Key financial ratios:

• Investment – determine performance from perspective of an equity holder

• Gearing – relationship between inside and outside claimholders (financial risk)

• Profitability – focus on performance by looking at wealth generated by the firm (how good are firms in applying capital employed to generate wealth?)

• Liquidity – can cash and near-cash cover short-term commitments?

• Efficiency – efficiency with which firm combines inputs, credit and stock management

Financial Ratio Analysis

General analysis framework:

1. Who are your users?

2. What ratios are they interested in?

3. Calculate ratios

4. Interpret ratios

5. Build overall picture of firm

Main limitations:

• Ratios are only the starting point

• Time variation of ratios

• Garbage-In-Garbage-Out

• Useful comparators needed

• Additional point – Which ratios? Which timeframe?

Financial Ratio Analysis

6

Industry Analysis

Industry analysis process – a sensible way for the analyst to place the

firm within its wider context was to analyse the economy, the industry

and then the firm

Macroeconomic analysis – here we briefly reviewed how different key

macro variables (C, I, G, %∆GDP, r, etc.) could exert a potential

impact on companies and their financial statements

PEST analysis helps us do this

Strategy analysis – examines the firm’s profit drivers and key risks,

considers current and potential future performance

Focuses on profit potential (industry choice, competitive positioning,

corporate strategy)

Porter’s Five Forces – important tool to help consider intensity of

competition – considers degree of (actual and potential) competition

and then bargaining power in input and output markets

Industry Analysis

Competitive strategy analysis – is the firm a cost leader or

differentiator? Do resources match its chosen strategy?

Look at lists of characteristics to spot either type

Corporate strategy analysis - what are the economic consequences of

managing all the different businesses under one corporate entity?

Does it make sense to manage them under one firm?

SWOT analysis is helpful here

7

Industry Analysis

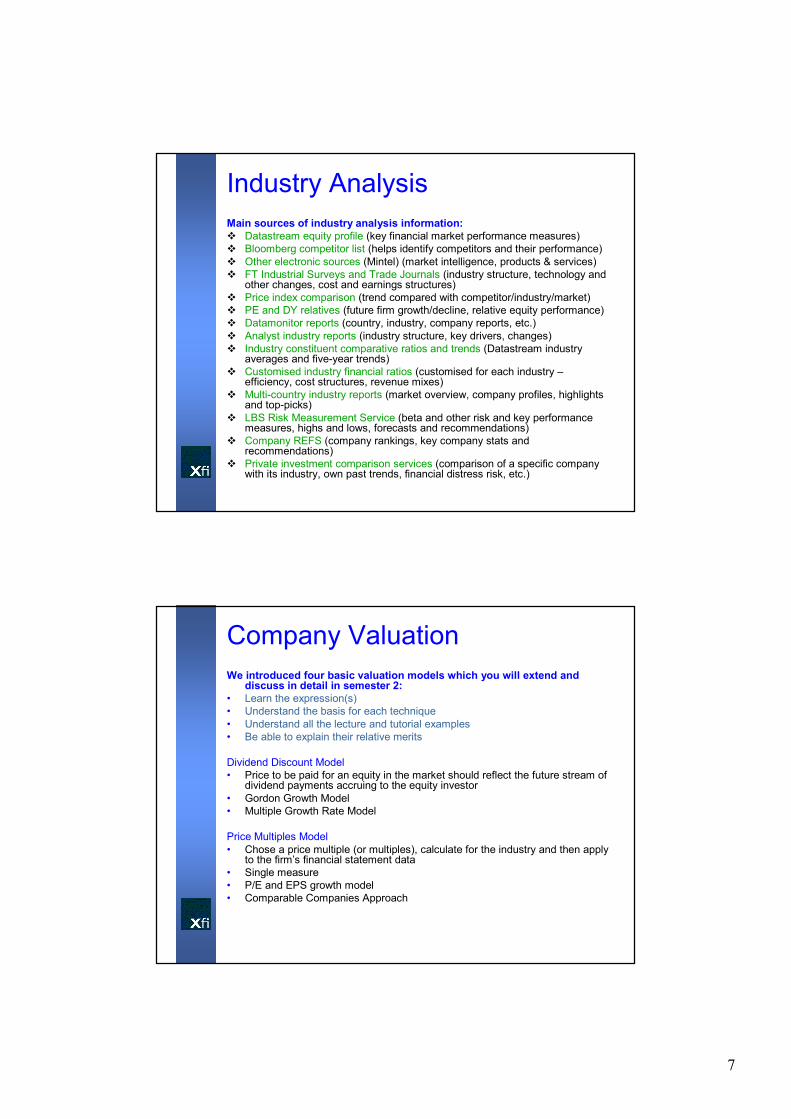

Main sources of industry analysis information:

� Datastream equity profile (key financial market performance measures)

� Bloomberg competitor list (helps identify competitors and their performance)

� Other electronic sources (Mintel) (market intelligence, products & services)

� FT Industrial Surveys and Trade Journals (industry structure, technology and other changes, cost and earnings structures)

� Price index comparison (trend compared with competitor/industry/market)

� PE and DY relatives (future firm growth/decline, relative equity performance)

� Datamonitor reports (country, industry, company reports, etc.)

� Analyst industry reports (industry structure, key drivers, changes)

� Industry constituent comparative ratios and trends (Datastream industry averages and five-year trends)

� Customised industry financial ratios (customised for each industry –efficiency, cost structures, revenue mixes)

� Multi-country industry reports (market overview, company profiles, highlights and top-picks)

� LBS Risk Measurement Service (beta and other risk and key performance measures, highs and lows, forecasts and recommendations)

� Company REFS (company rankings, key company stats and recommendations)

� Private investment comparison services (comparison of a specific company with its industry, own past trends, financial distress risk, etc.)

Company Valuation

We introduced four basic valuation models which you will extend and discuss in detail in semester 2:

• Learn the expression(s)

• Understand the basis for each technique

• Understand all the lecture and tutorial examples

• Be able to explain their relative merits

Dividend Discount Model

• Price to be paid for an equity in the market should reflect the future stream of dividend payments accruing to the equity investor

• Gordon Growth Model

• Multiple Growth Rate Model

Price Multiples Model

• Chose a price multiple (or multiples), calculate for the industry and then apply to the firm’s financial statement data

• Single measure

• P/E and EPS growth model

• Comparable Companies Approach

8

Company Valuation

Free Cash Flow Model

• we project financial statements, use them to calculate free cash flows and

then use these as the basis for equity valuation

Free cash flow = Profit after taxes

+ Depreciation

+ Net after-tax interest payments

- Increase in current assets

+ Increase in current liabilities

- Increase in fixed assets at cost

• financial statement modelling exercise, calculate FCFs, calculate TV, derive

intrinsic value of equity, compute price per share

Residual Income Model

• value of equity = BV equity + PV of expected future residual income

• Understand concept of residual income

• Finite period model

• ROE expression

• Note: you must remember how to calculate the WACC for a firm!

Technical Analysis

What is technical analysis?

• Study of past prices to predict future prices, based in Dow Theory,

understanding of human expectations (behaviour), future can be found in the

past, history repeats itself

• Compare with fundamental analysis – price based on future earnings, price

reflects all available information (EMH)

Technical analysis techniques include:

� Price fields – focus on open, close, high, low, bid, ask, volume

� Charts – line charts for trends, bar charts to pick up intra-day variation,

volume-bar to observe relation between price and volume

� Support and resistance – reversal at S&R levels, problem when breakout

occurs, trader’s remorse, extended breakout if accompanied by large volume,

support becomes resistance

9

� Trends – consistent change in prices, could examine falling or rising support or resistance levels, breakouts etc.

� Moving averages – mean security price at a point in time, buy when price moves above MA and sell when it drops below, smooth erratic series, trader’s remorse effect here too, doesn’t give much advance warning

� Indicators – calculation involving price and/or volume to predict future prices, MACD indicator – 12dayMA-26dayMA – oscillates around zero (above zero bullish, below zero bearish) – give you some advanced warning

� Market indicators - monetary (interest rates), sentiment (buys versus sells amongst analysts) and momentum (MACD of the market index)

� Line studies – trends, S&R levels, arcs, fans etc. – visual pattern spotting but also using maths relations such as Fibonacci arcs

Note: You should be able to explain each technique, illustrate with an example diagram where possible and give its relative merits, would the professional analyst use them (if so, when?), does thetechnique give you advance warning?

Technical Analysis

Creative Accounting

• Nature of creative accounting – making financial statements

show a better picture of the firm’s financial position and

performance in an attempt to mislead investors

• How is this achieved?

1. Revenue recognition methods – bring forward recognition?

2. Equity/cost method for affiliates – show income as dividends or

earnings depending on how investment is treated

3. LIFO effect – FIFO inflates profits and asset values

4. Depreciation – use straight line depreciation and longer lives to

increase profits

5. Amortisation expense – stretch amortisation period to increase

profits

10

6. Exploration costs – the more costs you capitalise, the better your balance sheet and profits

7. Pension costs – more optimistic about future performance then reduce or miss contributions to fund (or even claw-back)

8. Other post-employment contracts – one company may account for future health and life-insurance payments as a long-term liability, another might simply pay when they fall due (balance sheet looksmuch better)

9. Asset impairments – failure to recognise loss on asset impairment then profits look artificially high

10. Compensation – use stock options as compensation to reduce expenses

Creative Accounting

Smith and Hannah – seminal work on creative accounting, discuss:

• Excessive provisions

• Extraordinary items

• Off balance sheet finance

• Capitalised costs

• Non-trading profits

• Brand accounting

• Depreciation rate changes

• Pension fund holidays

• Earn-out commitments

• Foreign exchange mismatch

• Low tax charge

Note studies on frequency of use of these measures

Creative Accounting

11

More general measurement problems in accounting

• Economic versus accounting numbers

• Profit versus cashflow

• Recognition and matching (depreciation, intangible assets, etc.)

• Definition of the firm

• Inflationary distortion (profits overstated, assets understated)

• Number of transactions

These factors sometimes lead to investors being unintentionally misled

Accounting standards in the UK and elsewhere

• Role in the UK as an example (FRC and its component panels) – be able to describe them

• Understand the broad nature of accounting standards

• Movement of UK and other EU countries to IAS from January 2005

• Illustration with the Enron story – some nice examples!

Creative Accounting

Financial Statement Modelling

What should we be able to do?

• Understand and be able to apply the principles of financial

statement modelling

• Compute the free cash flow of a company

• Use free cash flow to compute the value of the company

• Perform sensitivity analyses on the computed value of the

company

Why did we focus on it?

• As a precursor to DCF-based modelling in semester 2 studies

and because you will need to simulate value in your

dissertation if you chose an Investment Analysis dissertation

12

Financial Statement Modelling

• Purpose of the technique – valuing equity, credit analysis, sensitivity

and scenario analyses

• Sales is the driver of such models (measure of activity), but difficult to

forecast

1. Work out year 0 accounts, set up parameter box and project one year

and then five years ahead

2. Set a plug variable to produce a balance sheet equation (and to give

financing policy)

3. Calculate free cash flows – measures cash available to investors

(finance free measure)

4. Calculate terminal value for cash flows

5. Discount, add back initial cash (negative debt), subtract initial debt to

get from enterprise value to equity value

6. Conduct sensitivity analyses to gauge the impact of key variables such

as growth and cost of capital

7. Calculate model cost of capital using CAPM-based WACC

Financial Distress Analysis

What is credit rating used for? Assessing creditworthiness, predicting

corporate failure

• Definition of insolvency/bankruptcy – firm cannot pay its debts as

they fall due, Ch11, Ch7 – understand broad definitions

• Common causes – overtrading, demand changes, diversification,

etc.

• Wide range of information sources used in credit analysis (including

previous credit history, collateral, rating agencies, bond yield, etc.)

• Financial ratios used in credit analysis:

1. Balance Sheet – current ratio, asset protection, gearing

2. Income Statement – profit margins, fixed charge coverage

3. Cash Flow Statement – cash flow/capex, depreciation/cash flow,

capex/depreciation

13

Univariate models

• Beaver’s model:

• Cash flow/total debt

• Net income/total assets

• Total debt/total assets

• Working capital/total assets

• Current ratio

• No-credit interval

• Total assets

• Gearing and profitability were relatively good predictors of failure

Financial Distress Analysis

Multivariate models

• Combine univariate ratios

� Altman’s Model: calculation of a Z-score

• Working capital / Total assets (%)

• Retained earnings / Total assets (%)

• Earnings before interest and taxes / Total assets (%)

• Market value of equity / Total liabilities (%)

• Sales / Total assets (no.of times)

� Taffler’s model for the UK

• Concentrated on returns, working capital, financial risk, liquidity

� Conditional probability models

• Estimate probability of occurrence rather than simply fail or survive

Financial Distress Analysis

14

� Use of capital market data

• Idea that share price contains reactions which are relevant to insolvency

� Inflation accounting and failure prediction

• Inflation accounting makes ratios more economically relevant –models should improve

� The use of non-financial indicators

• Changes in directors shareholdings

• Resignation of directors

• Delay in submitting accounts

� Zeta® Credit Risk Model: Altman (1977)

• Added some new variables to create a better model

Financial Distress Analysis

� KMV Approach

• Uses market-based quantitative techniques to assess credit risk

� Various others studies which extend these models

• Learn these

Financial Distress Analysis

15

Bond ratings

• How are they calculated? Financial ratios (interest cover, cash flow to debt,

gearing) but also competitive position, quality of management, etc.

• Classification of debt ratings – S&P and Moody’s

• Academic research studies of factors driving debt ratings (profitability,

gearing, size, etc.)

• Kaplan-Urwitz models of debt rating – model which performs best includes

financial market variables and financial statement variables, difficult to model

all of variability in debt ratings (need other factor such as assessment of firm

strategy, prospects)

Financial Distress Analysis

International Investment Analysis

• Difficulty in comparing financial statements across countries

• Thus we need to understand main drivers of accounting differences

across countries:

1. External environment and culture – Hofstede’s 4 dimensions of

culture, Gray’s application to accounting practices

2. Legal systems – Common Law (Accounting standards), Roman

Law (Prescriptive rules in Company Law)

3. Providers of finance – bank/family group (financial reporting to

creditors/government, law-driven), shareholder group (financial

reporting to equity holders, GAAP-driven)

4. Taxation – are financial accounts tax accounts?

5. Accounting profession – strength, size and training of accounting

profession?

16

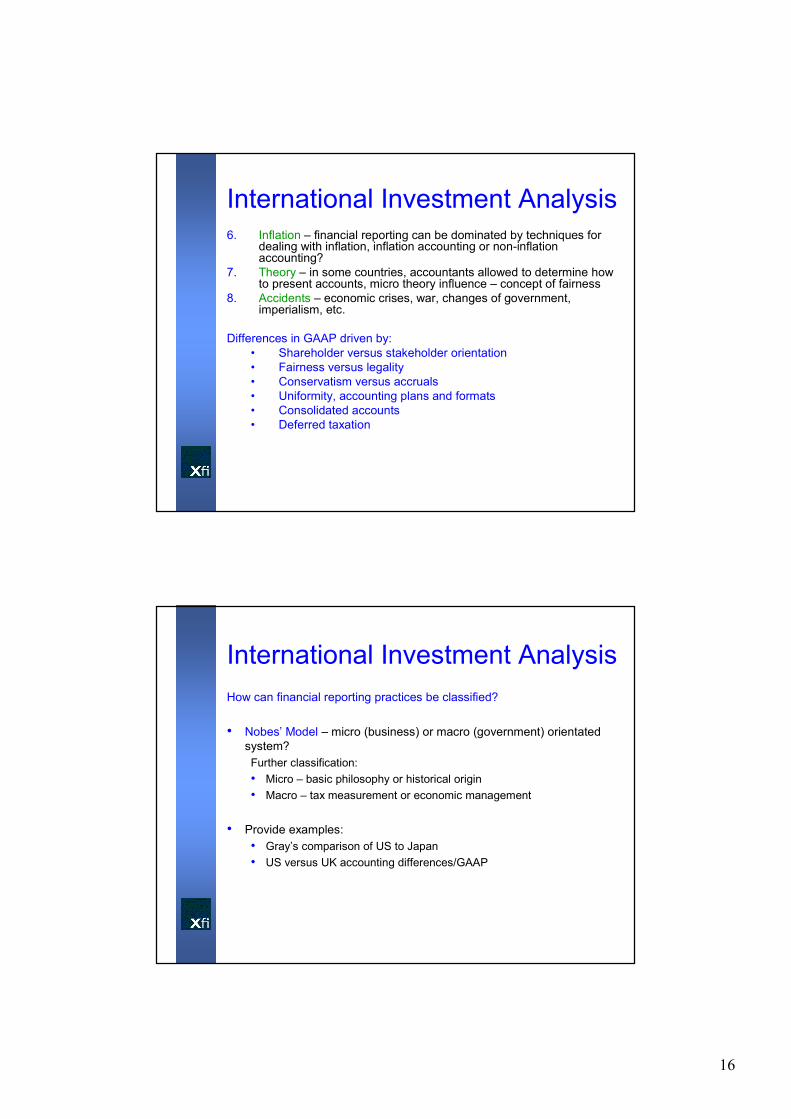

6. Inflation – financial reporting can be dominated by techniques for dealing with inflation, inflation accounting or non-inflation accounting?

7. Theory – in some countries, accountants allowed to determine how to present accounts, micro theory influence – concept of fairness

8. Accidents – economic crises, war, changes of government, imperialism, etc.

Differences in GAAP driven by:

• Shareholder versus stakeholder orientation

• Fairness versus legality

• Conservatism versus accruals

• Uniformity, accounting plans and formats

• Consolidated accounts

• Deferred taxation

International Investment Analysis

How can financial reporting practices be classified?

• Nobes’ Model – micro (business) or macro (government) orientated

system?

Further classification:

• Micro – basic philosophy or historical origin

• Macro – tax measurement or economic management

• Provide examples:

• Gray’s comparison of US to Japan

• US versus UK accounting differences/GAAP

International Investment Analysis

17

What have you learned from Investment Analysis 1?

1. The key tools of an Investment Analyst, advising on equity (and debt) investments

2. A series of simple techniques for calculating and simulating firm value (and their relative merits)

3. The problems inherent in financial statement information (and the alternative technique of technical analysis)

4. The issues facing the analyst when attempting to value a firm and provide a recommendation to your clients

Exam TechniqueEssay questions

• Read the question carefully and make some attempt to answer what is asked for (rather than what you would like the question to ask)

• Structure essay-style questions:

• Introduction

• Outline structure of rest of answer

• Define terms of reference

• Arguments in support of answer to question

• Summary and conclusion – re-address the question and give conclusion based on your most important points

• You must have at least 6 good points to make in an essay answer –don’t focus on one small part of a topic

• Don’t simply list everything you have learned

• You should be able to write at least two pages for an answer in 40 minutes – if you can’t then practice

18

Exam Technique

Calculation questions

• Will often come with discussion elements too – do the calculations first and then the discussion parts

• Always have a go at the discussion parts

• Often discussion parts will ask you about whether you think a particular technique is useful or not (learn relative merits)

• Show your workings – tell the marker what you are doing, keep it tidy

• Remember currency, units, magnitude, UK convention for commas and decimals

• Write out the expression for calculations before you attempt them (not needed so much with ratio analysis)

Exam Technique

Company analysis questions

• Order of your answer:• Read the accounts and write half a page on what you see – sales

growth? Declining profitability? Changing asset structure?

• Calculate the ratios – tell the marker which ratio, which year, what the units and magnitude are (2 or 3 ratios per category maximum)

• Focus ratio analysis on most recent two years ONLY!

• Write some interpretation on each of the ratios calculated –analyse, don’t merely describe – explain ‘why’ the change may have occurred

• Give a conclusion about the financial performance and position –would this be a reasonable investment or not?

Note: change this year → you can attempt only ONE company analysis question! So chose carefully.

19

Exam Technique

General points:

• Instructions on front of paper:You are to answer ONE question from section A and any TWO questions from section B.

Calculators permitted. Closed Note. All questions carry a maximum of 100 marks.

Total marks awarded out of 300 are scaled to 100 per cent.

• Make sure your calculator/pens etc, work before the exam

• Spend 5 minutes (at least) reading through the paper to identify the questions which you wish to answer

• Look at your watch and have a strict cut-off of 40 minutes per question

• If you are running out of time (ONLY) then bullet-point the other things you intended to cover

• Listing points is generally not acceptable as this leads to little analysis

• Spend the first 5 minutes of each question just thinking (for essay questions you could even write a very short essay plan before your answer if you like)

• Answer all three questions you have chosen and all parts to eachquestion

Exam Technique

Good luck and thanks for studying Investment Analysis!