hungary stabilization and economic reform - world … · report no. 718-tu hungary stabilization...

TRANSCRIPT

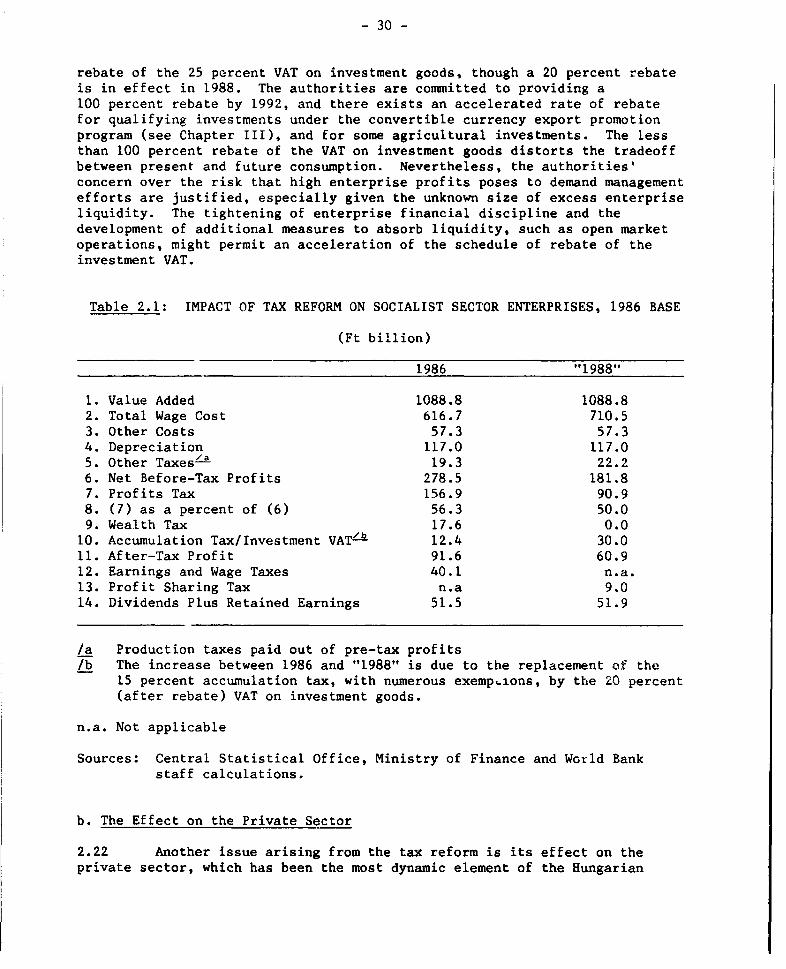

Report No. 718-tU

HungaryStabilization and Economic Reform

May 31,1988

Country Operations Department IVEurope, Middle East and North Africa Region

FOR OFFICIAL USE ONLY

Document of the World 3ank

This document has :- restricted distribution and may be used by recipientsonly in the performan-ce of thieir official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FISCAL YEARJanuary 1 to December 31

CURRENCY EQUIVALENTS(Forints per US$1.00)

Period End-PeriodAverage (Dec. 31)

1980 32.53 32.211981 34.31 34.431982 36.63 39.611983 42.67 45.191984 48.04 51.201985 50.12 47.351986 45.83 45.931987 46.97 46.39

LIST OF ABBREVIATIONS

CMEA = Council for Mutual Economic CooperationCSO Central Statistical OfficeERP = Effective Rate of ProtectionNBH = National Bank of HungaryNPO = National Planning OfficeNSB National Savings BankPIT = Personal Income TaxPPP = Purchasing Power ParitySDI = State Development InstituteTFP = Total Factor ProductivityVAT = Value Added Tax

FM OFFICIAL uw OWLY

BSTRACT

This report analyzes developments in the Hungarian economy si'.e1985. After surveying recent economic developments (Chapter I), the reporteramines the framework of domestic and external regulatory policies andincentives for industrial development and exports (Chapters II and III).One lesson that has emerged from the Hungarian experience is that asupportive macroeconomic en-vironment that keeps domestic demand under tightcontrol is needed to get the desired supply response from economic reform.A parallel lesson is that reform measures can make macroeconomic policymakingmore difficult, at least in the short-run. To lessen this possibility it isimportant to increase financial discipline, which in the Hungarian contextmeans a reduction in the amount of financial subsidies and supports fromthe State to enterprises. The effects of recent reforms to the regulatoryenvironment are analyzed, and ways of increasing their effectiveness oresuggested. Economic reform also places greater reliance on markets, andit is important that markets send signals that encourage a strong supplyresponse, especially of nonruble exports. The failure of this to occurin 1985-86 is analyzed, and measures to avert this outcome in the futureare suggested. Chapter IV analyzes the authorities' medium-termstabilization/reform program. The program represents a consistent andfeasible strategy for stabilizing the economy and stopping the growth ofexternal debt. The success of the program depends on a marked reduction inthe convertible currency current account deficit in 1988 and a consistentand vigorous implementation of the economic reform.

This report was written by Timothy Condon (EM4), using contributions frc..Sadao Nagaoka (PPR), Martin Schrenk (EM4), David Newbery and Mario deZamaroczy (Consultants), and Carlos Hinayon (EM4). Maria Luisa de la Puentewas responsible for the production of the document. The main miPsion visitedHungary in June-July 1987. Its findings were supplemented through visits inOctober 1987 and March 1988. The initial draft of this report was presentedto the authorities in October 1987, and discussed with them in January 1988.This report incorporates the results of the discussions. Final discussionswith the authorities took place in May 1988.

This document has a restricted distribution and may be used bv recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

HUNGARY: STABILIZATION AND ECONOMIC REFORM

Table of ContentsPage No.

COUNTRY DATA

SUMMARY AND CONCLUSIONS . . . . . . . . . . . . i-v

CHAPTER I: Recent Economic Developments . . . . . . . . 1

A. Output and Productivity Trends .. . . . . . . .

B. Macroeconomic Balances . . . . . . . . . . 5C. Consumption and Investment . . . . . . . . . . 7D. Public Finance . . . . . . . . . . . . . . 12E. Money and Credit . . . . . . . . . . 13F. Inflation . . . . . . . . . . . . 15G. Current Account . . . . . . . . . . . . . 17H. External Debt and Creditworthiness . . . . . . . . 19I. Summary . . . . . . . . . . . . . 22

CHAPTER II: Domestic Policies and Competition . . . . . . . 23

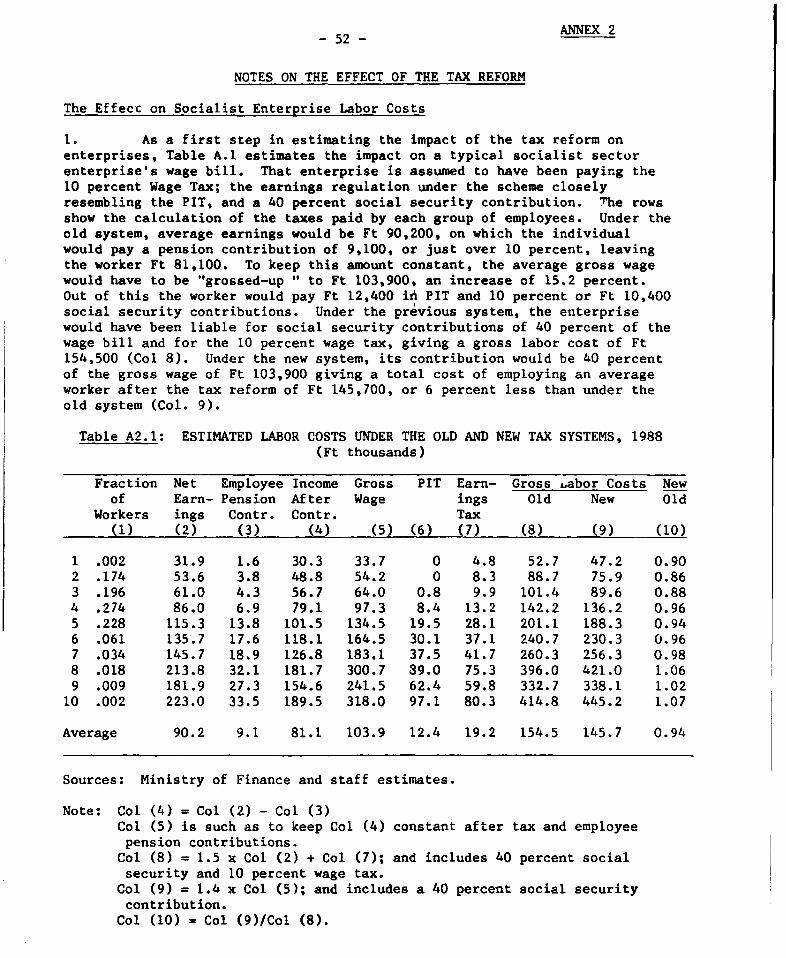

A. Establishing Financial Discipline . . . . . . . . 23a. Regulatory Environment . . . . . . . . . . . 25

B. The Hungarian Tax Reform . . . . . . . . . . 28a. The Impact of the Tax Reform on Socialist Sector Enterprises . 29b. The Effect on the Private Sectcr . . . . . . . .

c. The Revenue Impact of the Tax Reform . . . . . . . 31d. Conclusions . . . . . . . . . . . . . . 33

C. The Domestic Pricing System . . . . . . . . . . 33a. Recent Developments . . . . . . . . . . 34b. Future Reform of the Pricing System . . . . . . . . 34

CHAPTER III: External Policies and Competition . . . . . . . 36

A. Expor' Policies and Incentives . . . . . . . . . . 36a. Recent Trends in Competitiveness . . . . . . . . 36b. Investment Incentives . . . . . . . . . . . 38c. Other Export Promotion Measures . . . . . . . . 38

B. Nonruble Impcrt Policies and Incentives . . . . . . . 39a. Recent Trends in Tariffs and Effective Protection . . . . 39b. Nor.tariff Import Barriers . . . . . . . . . . 40

C. Recommendations . . . . . . . . . . . . . 40

CHAPTER IV: Medium-Term Prospects . . . . . . . . . . 42

A. The Economic Stabilization and Structural Reform Program . . . 42B. Risks to the Scenario . . . . . . . . . . . . 45

ANNEX 1: Notes on Enterprise Subsidies . . . . . . . . . 49

ANNEX 2: Notes on the Effect of the Tax Reform . . . . . . . 52

STATISTICAL APPENDIX. . . . . . . . . . . . . . 53

MAP

Page of 2 pagsCOUTRV OATA: jUj#KY

93.036 sq km 10.63 million (mid-1986) 11S.0 per sq kmAnnual growth rate 0.19% (from 1970 to 1956) 2286S per sq km of arable land

POPULATIm CI4AhErTERiSTIC5 LloAll MELIICrude birth rate (per 1.OO) 11.9 Population per physician (§90) 347Crude death rate (per 1.000) 13.9 Population per hospital bed (1901) 110Infant mortality iper 1.000 live births) 19.0

IKuCm Dh5TftLRMTIL L9771X of private incom. highest 20 percent 32.3 3I

lowest 40 percent 26.2 X owe"d by top 1f of owersS owned by smallest 101 of owners

ACCESS TO PIPED bA1TER 91a1 ACCESS TO FLECTRICITY 119A01X of population - urban 63.0 I/ X of population - urban 99.2

- rural 43.1 J/ - rural 97.6

NUTEITION 19231 EDUCATIONCalorie intake as X of requirements 134.0 Adult literacy rate X (1982) 98.9Per capita protein intake (gns.) 105.3 Primary school enrollment X (1981) 97.0

GUP PER CAPITA IN 1oAa 2/: UIS 2-020

ANNLUAL RATE OF GROWNTH M. eonstant grices)

US *ln. S 1970-75 1°75-0L !980-iM 1m 198

GOP at Market Prices 26.0 100.0 6.2 3.2 1.8 I.$ 3.4Gross Domestic Investment 6.9 26.8 6.9 2.2 -3.8 6.5 SSGross Domestic Saving 6.4 24.6 10.8 5.7 2.4 -6.3 7.9Resource Balance 0.1 0. Exports of Goods. NFS 9.9 37.9 9.6 6.9 5.S -2.2 4.2Imports of Goods. NFS 10.0 38.4 7.S 3.9 1.5 2.7 3.1

0OuTPUT. LABOR FORCE ANDPRODUCTIVITY IN lgf6

Gross Value Added Labor Foree 3_ G.V.A. Per WorkerFt Bln. USS; Ern. % dinu I usi -t

Agriculture 179.0 3.9 16.5 986.2 20.2 3.955 89.6Industry (ncl. constr.) 439.5 9.6 40.6 1.884.0 38.5 5.096 115.4Services 372.1 8.1 34.2 2.022.3 41.3 4.005 90.7Unallocated 4/ 923 LA 2 -8 _**

Total/Average 1084.5 23.6 100.0 4.892.5 100.0 4.415 I/ 100.0 /

GOVER IIENT FINANCE

Consolidated Central Gover_n_nt id"Ft Cln .1 of GAP1987 1 m72--M

Current Receipts 637.3 52.6 58.7Current Expenditures 613.4 50.6 52.8Current Surplus 23.9 2.6 5.8Capital Expenditures 47.9 4.0 6.9External Assistance (net)

1/ Percentage of occupied dwellings.Z/ World Bank Atlas methodology. All other conversions to dollars in this table are at the

average comnercial c-change rate prevailing during the period covered.I/ Active earners.A/ Customs duties, valuation differences commodity and indirect taxes are not allocated by sector.5/ Excluding unallocated.

Not applicableNot available

EH4COMay 19882496G

Page 2 of 2 pagesQgl,ITRY DATA: HUNGARY

MQb CREDIT AND PRICES1211. 1%21 1211 1J84 JiMla 1987

(Ft billions)

Domestic credit 659.6 700.4 729.5 76?.8 825.9 961.6 1071.9Central Government (net) 20.0 30.1 29.7 11.8 21.7 92.0 126.1Local Government 4.3 4.1 5.2 4.6 6.' 7.3 10.4Credit to Non-government 635.5 665.1 695.2 750.9 798A 862.3 935.4

Money and quasimoney 380.2 405.6 421.2 443.1 487.8 556.5 595.1

(percentage growth rates)

Money and quasimoney 7.9 6.7 3.8 5.2 10.1 14.1 7.9Domestic credit 8.8 6.2 4.2 5.3 7.6 16.4 11.5Central Government (net) 80.2 5O.S -1.3 -60.3 83.9 324.^ 37.4Enterprise working capital S.5 5.2 5.2 9.0 12.8 10.S 1.4Household 7.9 1l.S 1S.S 16.4 14.1 14.7 15.7

Memorandum items:M2/GOP (percent) 48.8 47.8 46.9 45.2 47.2 51.1 48.6CPI inflation (percent) 4.6 6.9 7.3 8.3 7.0 5.3 8.6

BALANCE OF PAYMENTS MERCHANDISE EXPORTS (AVERAGE 1980-8613.22 1211 1JM lii l186 1987/n Trade in Trade in

_2Rubes Nonrubles(Millions US$) Fuels. electric S mln % $ mln X

energy 27.1 0.7 452.1 9.4Exports of Goods & NFS 10315.2 10143.9 10270.7 10162.9 10713.1 11696.0 Raw materials. semi-Merchandise (FOB) 9056.6 8879.8 8836.7 8930.3 9147.7 9892.0 finished products.Non-Factor Services 1258.6 1264.1 1434.0 1232.6 1565.4 1804.0 spare parts 911.9 23.2 1674.5 34.8

Machinery, transportImports of Goods & NFS 9843.6 9498.5 9305.7 9536.o 11219.8 11436.0 equipment. otherMerchandise (FOB) 8578.8 8452.4 8022.6 8323.6 9670.6 9787.0 capital goods 1751.0 44.5 606.1 12.6Non-Factor Services 1264.8 1046.1 1283.1 1213.2 1549.2 1649.0 Manufactured

consumer goods 677.0 17.2 657.4 13.7Resource Balance 471.6 645.4 965.0 626.1 -306.7 260.0 Agricultural goods S6.7 14.4 1424.0 g2_.6

Total 3935.6 100.0 4814.1 100.0Net Factor Income -963.2 -666.2 -759.7 -750.5 -857.1 -95S.0(inte est payment) 1128.1 812.8 945.9 989.6 1121.8 1169.0 EXTERNAL DEBT. DECEMBER 31. 1987Net Current Trdnsfers 62.7 56.0 66.0 68.8 77.8 106.0 USS Billignn(workers remittances) .. .. .. .. .. .. (Convertible currency)

Public debt incl. guaranteed 15.8Current A:count Balance -428.9 35.2 271.3 -55.6 -1286.0 -558.0 Non-guaranteed private debt

Total outstanding and disbursed 1S.8Long-Term Capital Inflow 118.3 81.2 860.1 1714.4 652 S .545.0Direct Investment 0.0 0.0 0.0 0.0 0.o 0.0 OEBT SERVICE RATIO FOR 1987 %Official Capital Grants 0.0 0.0 0.0 0.0 0.0 0.0Net LT Loans 202.2 161.3 1016.0 1904.8 1028.0 722.0 (Convertible Currency)Othe, LT Inflows (Net) -83.9 -30.1 -155.9 -190.4 -375.5 -177.0 Public debt. ncl. guaranteed 47.5

Non-guaranteed private debtTotal 47.5

Total Other Items (Net) -386.7 388.5 -825.8 -395.5 606.6 -1155.0Net Short Term Capital -968.5 346.6 -944.6 -488.0 476.9 .. IBRD/IDA LENDING (December 19871 (Mln. USSICapital Flows N.E.I. 0.0 0.0 0.0 0.0 0.0Errors and Omissions S81.8 41.9 118.8 92.S 129.7 .. IBRD IDA

Change in Net Reserves 697.3 -504.9 -305.6 -1263.3 26.9 1198.0 Outstanding and disbursed 722.2Net Credit from the IMF 239.1 356.7 433.9 -95.3 -49.5 -300.0 Undisbursed S62.0Other Reserve Changes 458.2 -861.6 -739.5 -1168.0 76.4 1498.0 Outstanding. incl.(- indicates increase) undisbursed 1284.2

Exchange Rate Adjustment 254.9RATE OF EXCHANGE

1987 (averageL 1986 (averaaelUS$ 1.00 = 46.97 USS 1.00 = 45.83Ft. 1.00 = $0.021 Ft. 1.00 = $0.022

. Not applicable .. Not availableL Preliminary

EM4COMay 1988 (2496G)

-1i -

SUMMARY AND CONCLUSIONS

(i) Hungary's economic reform program involves increasing reliance onmarket forces, improving factor productivity, increasing the flexibility ofthe economic system, shifting production capacity toward activities more inline with Hungarian dynamic comparative advantage, and increasing convertiblecurrency exports. Since 1983, the World Bank has supported Hungary's reformprogram, directly through its assistance program, which has included twoindustrial restructuring loans, and indirectly by increasing Hungary'sparticipation in the international capital markets. Visible progress inestablishing a sustainable supply response has been lacking, and the balanceof payments began to deteriorate in 1985, necessitating a substantialincrease in debt. In 1987, the authorities developed a program designed tostabilize the economy and promote economic restructuring. This reportreviews economic developments in 1986-87, analyzes key aspects of theincentive system as well as the program for stabilization and restructuring.That program embodies improvements in the economy's supply response,particularly compared with the 1985-86 period. This report makes a number ofrecommendations in this regard.

A. Recent Economic Developments and Follow-Up Needs

(ii) After a successful stabilization in 1982-84, Hungary's economicperformance deteriorated in 1985-86. GDP growth fell by 0.3 percent in 1985and nonruble exports declined by 6.6 percent. In 1986, GDP growth increasedby 1.5 percent but there was a further 3.8 percent decline in nonrubleexports. The combination of a poor supply response, growing domestic demandand declining terms of trade led to growing macroeconomic imbalances. By1986, the current account deficit in convertible currencies reached6.0 percent of GDP and the State budget deficit 4.3 percent. The currentaccount deficits were financed by external borrowing, but the total increasein external debt, measured in U.S. dollars, also reflected the effects ofcross exchange rate changes and a compositional shift in the structure ofdebt toward currencies that were appreciating against the dollar.

(iii) The authorities responded to the deterioration in the economy byimplementing measures in 1987 to reduce the current account and fiscaldeficits. These measures were partly effective, and the deterioration in themacroeconomic balances was reversed. GDP growth was 3.4 percent, andnonruble exports grew by 5.0 percent. Moreover, there was no decline in thenonruble terms of trade. There was, however, another large increase inexternal debt, most of it due to the effect of the depreciation of the dollarin the fourth quarter of the year. In early 1988, the most pressingmacroeconomic problem is the need to sustain the turnaround in economicperformance that began in 1987 in a situation where the heavy debt serviceburden reduces the room for maneuver.

(iv) A principal shortcoming of economic policymaking in 1987 was theinability to implement a sufficiently contractionary aggregate demand

- ii -

policy. Real household consumption, rather than declining by 0.5-1.0 percentas planned, grew by 2.8 percent. Investment also recorded stronger thanplanned growth. The unexpected strength of domestic demand had severalcauses. Anticipatory buying developed in the second half of the year as newsof price increases that would take effect in January 1988 with theintroduction of a major tax reform became known. Loose monetary policy in1985-86 also may have created a liquidity overhang that frustrated efforts toreduce demand in 1987. Interest rate policy may not have been -ufficientlyactive to reduce the shift out of deposits into cash, which could be readilyspent. Enterprise liquidity, following two years of rapid growth of Statefinancial subsidies and supports, was high, and monetary policy was notsufficient.y tight for the enterprise sector.

(v) In combination with the measures introduced in 1987 to stabilizethe economy, the authorities elaborated a Stabilization and Economic ReformProgram for 1988-90. A main element of the program is the implementation ofa tight aggregate demand policy in 1988. The experience of 1987 indicatesthat several policy several measures are called for, the first one being atight fiscal policy. Developments in 1987 Oemonstrate that the authoritiesare able to introduce deficit reducing measures in a quick and flexiblemanner. A stronger commitment to improve the fiscal b-alance will benecessary in order to attain the planned reduction in the 1988 State budgetdeficit from 2.9 to 0.8 percent of GDP. Monetary policy for both householdsand enterprises must also be tightened. For the enterprise sector, thetightening of short-term refinancing credit limits is the main tool ofmonetary policy. To permit greater short-term management, open marketoperations are also needed. These would enable ti,s monetary authorities tointervene at the first sign of excess enterprise liquidity. For thehousehold sector, an active interest rate policy is needed to encouragesavings and discourage a flight from savings deposits into cash holdings.

(vi) An improvement in the efficiency of investment, which has been lowin Hungary, is also necessary. A continuation of the recen. trend of scalingback low yielding public investments is needed. Better enterprise investmentdecisions are also needed. A tightening of enterprise financial disciplinethrough a multi-year, pre-announced and front-loaded program of reductions inState financial supports to enterprises is an important step. The reductionin enterprise financial supports is also important because the supports fueldomestic demand, which crowds out nonruble export demand. Strict enforcementof the new bankruptcy law as well as measures to reduce the scope for bankruptenterprises to be refloated would also send an unambiguous signal toenterprises that they will bear the cost of imprudent investment decisions.Reforms to integrate the capital market, especially the planned integrationof the household and enterprise financial systems are also necessary. Suchreforms would increase the competition for long-term investment resources,which, provided financial discipline is tight, would lead naturally to animprovement in the allocation of investment resources. In addition, fullintegration would increase the interest sensitivity of the financial system,which would improve the effectiveness of monetary policy. Finally, in a moreintegrated financial system, State support for subsidized credit schemesshould be minimized. The authorities' intentions are in line with theserecommendations.

- iii -

(vii) An important develoDment in 1987 was the 5 percent growth innonruble exports after two years of falling exports. The growth appearsrelated to an improvement in the incentive to export to the nonruble areacompared with selling on the domestic market and in the ruble area. Thecontinuation of an active exchange rate policy is needed to sustain and buildon the gains of 1987. Moreover, an active exchange rate policy thatsustained the incentive for nonruble exports would promote investment inefficient exports and permit Hungary to dispense with subsidized investmentcredit as an export promotion measure. Finally, it may be possible toimprove debt management in Hungary to avoid large increases in the growth ofexternal debt, measured in U.S. dollars, resulting from cross exchange ratemovements and compositional shifts in debt structure.

B. Domestic Policies and Competition

(viii) Hungary has made significant progress in reforming the regulatoryenvironment to encourage profit maximizing behavior by enterprises. Abankruptcy law was enacted in September 1986, and a major tax reformimplemented in January 1988. These measures have the potential to increasethe efficiency of resource usc in the economy but several additional measuresare needed. The program for reducing state financial supports to enterprisesis a key to establishing financial discipline. The bankruptcy law wi 1 bemuch more effective in discouraging imprudent enterprise decisions i. anenvironment of tight financial discipline. An increase in provisioningagainst doubtful loans by commercial banks will increase the banks' interestin the soundness of their portfolios.

(ix) The introduction of the Value Added Tax and the Personal Income Taxin January 1988, simultaneously with the elimination of several distortionarytaxes, has simplified the tax system and removed many distortions. Someshort-run transitional problems have arisen, however, which require somemodifications. First, permitting private sector entrepreneurs to deduct thecost of their own labor from pre-tax profits would promote neutrality of taxtreatment across enterprises and elicit a stronger supply response from thedynamic private sector. Second, factor price changes accompanying the taxreform may not correspond to the authorities' original intentions. Expectedfactor market reforms, especially granting enterprise managers the freedom todetermine individual employee earnings (subject to a ceiling on the overallenterprise wage bill related to performance) will help promote more efficientuse of labor and capital. Finally, given the need for a sharp improvement inthe public sector's net financial position in 1988, a contingency package ofexpenditure reductions is called for to guard against the possibility of arevenue shortfall in the first year of the tax reform.

(x) Domestic pricing policy aims to shift larger numbers of goods intothe category of freely determined prices. This commendable policy would befurther strengthened by the trade measures, discussed below, to stimulateimport competition. Also, domestic competition would be increased. Inaddition, as noted in various points in this report, distortions arising fromthe system of administered prices are costly to the economy. There is a need

- iv-

to study the levels and manner of setting of the administered prices inHungary to see if the goals of the pricing policy could be met moreefficiently and at a lower fiscal cost.

C. External Policies and Competition

(xi) Policies to promote exports in Hungary are generally well focusedand sustainable in the long-run. It is recommended that the authoritiescontinue to pursue an active exchange rate policy as a principal instrumentof export promotion. There has been less progress in reforming the importregime. Two non-tariff barriers, the import licensing system and the globalquota on consumef goods, effectively close off significant import competitionand artificially reduce the equilib-ium level of the real exchange rate(defined as the price of cradable goods relative to the price of nontradablegoods). The report recommends that the reform program include reform of thelicensing system to increase its automaticity, and the pre-announcedelimination of the consumer goods quota over a period of time. Given thepressure cn the balance of payments, temporary tariff surcharges may beneeded as a transitional measure to minimize the risks of a substantialdeterioration in external balances.

D. Medium-Term Prospects

(xii) The main goals of the Stabilization and Economic Reform Program areto halt the growth of external debt by the end of the period and toaccelerate the restructuring of the economy. The authorities have requestedthe support of the IMF and the World Bank for their program. A main elementof the program is a sharp contraction in domestic demand in 1988 in order toproduce significant improvements in internal and external balance. Theconvertible currency account deficit is projected to fall from $847 millionin 1987 (3.2 percent of GDP) to $500 million in 1988 (1.9 percent of GDP),and the fiscal deficit from the 1987 level of Ft 35 billion (2.9 percent ofGDP) to Ft 10 billion (0.8 percent of GDP). To analyze the implications andthe feasibility of this program, scenarios were developed using a model thatcaptures the links between growth and external constraints. The Governmentwill need to take measures to reduce domestic demand. Nonruble imports areprojected to contract sharply in 1988, while nonruble exports expand by anaverage of 5 percent in 1988-90. Consumption is expected to fall by2-2.5 percent in 1988 in a reversal of the policy that has kept it fromfalling for over thirty years. Policies to reduce domestic demand must bebalanced with the need to raise domestic savings by the equivalent of2.6 percent of GDP in 1988.

(xiii) The economic reforms, especially the reduction in enterprisesubsidies and other financial support and the measures to improve the use ofcapital and labor, are expected to raise productivity growth. While only amodest increase in the investment rate is projected, the measures discussedabove are expected to increase investment efficiency and improve the supplyresponse. GDP growth is expected to be low for the rest of the decade; in1991-95, however, growth is expected to exceed 3 percent.

v

(xiv) The authorities' medium-term adjustment program represents afeasible and consistent path for the economy to grow out of its currentproblems. The path is not an easy one, however. In addition there are realrisks to the program, starting with the uncertainty surrounding the economy'sresponse to the sta;ilization and reform measures. The report argues thatthe authorities can reduce the risks through a vigorous and consistentimplementation of the economic reform. If there is visible progress instabilizing the economy and in implementing the reform, it is likely thatthere would be some flexibility in the financing plan. If the authorities'commitment to the stabilization and reform effort is perceived to waver,however, it is likely that resistance would develop on the part ofinternational lenders, and Hungary could face financing gaps that would beimpossible to fill at reasonable terms or at all.

CHAPTER I

RECENT ECONOMIC DEVELOPMENTS

1.01 By end-1984 Hungary had, with the help of twn IMF Stand-ByArrangements, successfully stabilized its economy following the severeliquidity crisis of 1982. The current account was in surplus, as was theState budget. The successful stabilization was mainly due to tight demandmanagement during 1982-84, which included administrative restrictions toreduce imports but created pent-up demand by 1985. In 1985 a renewal of theeconomic reform was initiated with Bank assistance. Reforms to increasedecentralization, enterprise autonomy and reliance on "indirect regulators",or market-based signals, to guide economic actions were instituted. Inaddition, the authorities judged that, following the stabilization period amore expansionary demand management policy was justified. The economy'sresponse in 1985 and 1986 was poor. The supply side of the economy stagnatedwhile domestic demand expanded. The macroeconomic balances deteriorated inboth years, and there was a dramatic increase in external debt. During 1987,the authorities took measures to halt the deterioration and these measureswere partly effective. There was, however, a further significant increase innet external indebtedness. In early 1988, the most pressing macroeconomicproblem is the need to service the large external debt and make substantialprogress toward eliminating the current account deficit.

1.02 This chapter reviews developments in the economy in 1986 and 1987.It is possible to make the case that, in 1987, Hungary turned the situationarotnd and one can now expect a period of improved economic performance. Themeasures responsible for the turnaround are discussed and the reasons theimprov3ment fell short of expectations are also analyzed. The need toimprove the implementation of the reform, broadly defined to include themaintenance of a sound macroeconomic environment, is identified as a keyingredient in a sustained improvement in economic performance. Severalmeasures are discussed in this regard.

A. Output and Productivity Trends

1.03 A comparison of the five-year intervals, 1976-81 and 1981-86,reveals a near uniform deceleration in sectoral value added growth(Table 1.1). The figures also suggest that a principal cause for theslowdown was the fall in the growth of total factor productivity (TFP). Therate of decline in the labor force did not change much, reflecting a trendthat began in the mid-1970s. Capital stock growth was slower in 1981-86, butthe rapid growth during the earlier period led to an overblown investmentprogram that could not be sustained. While the causes of the productivityslowdown remain a puzzle, by 1985-86 the cumulative effect of slower TFPgrowth, exy)ansionary aggregate demand policy and adverse terms of tradeshocks led to economic stagnation.

1.04 Industry, which in 1986 accounted for 34 percent of GDP and 31percent of total employment, grew at an average annual rate of 1.7 percent in1981-86. Employment fell by 1.5 percent per year, nearly the same rate asduring 1976-81. Gross capital-stock growth was 4.8 percent per year, however,

-2-

much slower than the 7.3 percent average for 1976-81. The deceleration ofcapital stock growth was accompanied by a compression of nonruble capitalgoods imports, which may have slowed the accumulation of technologicalcapability and reduced technical efficiency. Another factor that contributedto the fall in TFP was the failure to improve the allocation of investment,the effects of which were less visible when the capital stock was growingmore rapidly. Allocative efficiency was adversely affected by traderestrictions, which were introduced to improve external balance, andpolicy-induced barriers to mobility, which slowed down structural changewithin firms and industries. In addition, the lack of competition in thedomestic and CMEA markets had a negative effect on the quality of enterprisemanagement. Weak management partly explains the loss of export market sharein 1980-85 in non-CMEA markets, where quality and servicing are important.While these technical, allocative and other inefficiencies are difficult todisentangle, their joint effect is reflected in the decline in theproductivity of Hungarian industry.

Table 1.1: FIVE YEAR GROWTH RATES

(percent per year)

TFP Labor Force Capital Stock Value Added1976-81 1981-86 1976-81 1981-86 1976-81 1981-86 1976-81 1981-86

Industry 0.2 -0.6 -1.4 -1.5 7.3 4.8 4.0 1.7Agriculture &forestry 3.2 2.2 -1.7 -0.8 5.6 3.3 3.7 2.6

Construction 0.4 -1.0 -1.5 -2.4 11.1 1.4 3.7 -1.9Transportation

& communic. 1.6 -0.5 -0.1 0.0 3.5 2.6 3.5 1.0Trade & materialservices -2.3 -0.9 0.8 0.8 5.8 4.8 1.2 2.1

Nornuaterialservices 1.5 0.8 1.9 1.3 4.8 4.6 4.0 2.6

Total 0.8 0.1 -0.6 -0.5 5.4 4.1 3.5 1.7

Source: Central Statistical Office, Statistical Yearbook, and Work Bank Staffcalculations.

Notes: Growth rates are computed between period end points. Capital stocks aregross capital stocks at ronstant prices. TFP is computed as theresidual of a Cobb-Douglas production function for each sector.

1.05 In 1986, value-added in industry fell by 0.5 percent, not as bad asthe 2.1 percent decline in 1985 but far short of the annual Plan target of2.0-2.5 percent growth. Part of the shortfall is attributable to the poorexport performance. The sector is export-oriented, with half of final sales

- 3 -

directed to export markets, split roughly in half between ruble and nonrublemarkets. In 1986, the volume of ruble exports rose by only 0.8 percent whilenonruble exports fell by 4.0 percent. The major factors responsible for thefall in nonruble exports were crowding out by unrestrained domestic demand,deteriorating profitability (discussed in Chapter II), weak demand conditionsin some developing country markets, especially in the Middle East, as well asproblems of quality and servicing.

1.06 Industrial value added grew by 4.1 percent in 1987, a markedimprovement over 1985-86. Within industry, the chemical, electric energy,engineering and machinery, and construction materials sectors recorded betterthan average growth. Part of the improvement is attributable to the6.0 percent increase in nonruble exports, with particularly strong growth inthe chemicals and light industry subsectors. The growth of tne buildingraterials subsector can be traced to the buying spree that was triggered bythe announcemnent of large price increases to take effect in 1988(para. 1.23). For a second consecutive year, a cold winter led to higherdomestic demand for electricity.

1.07 The poor performance of the industry sector, particularly innonruble exports, in 1985 and 1986 increased pressure on the agriculture andforestry sector to find new markets and products. The agriculture andforestry sector, which accounted for 16.7 percent of GDP and 20.4 percent ofemployment in 1986, contributed together with food industry 31 percent ofnonruble export earnings. Despite the relatively high TFP and value-addedgrowth shown in Table 1.1, the sector's recent performance has been mixed.The value of agricultural production is split roughly equally between animalhusbandry and crop production. Declining world prices for livestock led toreductions in the numbers of pigs, poultry and cattle between 1984 and 1986and production of animals for slaughter fell in 1985 and 1986. Procurementprices were raised in 1985 to compensate for some of the decline in worldprices. At the beginning of 1987, the pig and poultry populations werehigher than the year earlier partly as a result of the subsidies. In 1987sales of live animals and animal products grew by 2.4 percent.

1.08 The 1988 Plan budget contains a reduction in agricultural subsidiesand livestock producers will have to look for ways of increasing efficiencyto improve profitability. The depressed condition of world markets haseroded profitability and resulted in some scaling back of production. Theconditions that contributed to this situation--world production outpacingconsumption, weak developing country markets, competition from theEEC--cannot be expected to disappear in the short-term, making the search forefficiency improvements even more urgent. Improving the quality of feed isan important area for further work in improving the efficiency of thelivestock sector (see para. 1.09).

1.09 Cereal production plays a key role in the agricultural sector fortwo reasons: the livestock sector depends on grain inputs, and cereal is amajor foreign-exchange earner. Wheat and maize make up 90 percent of totalcereal production and account for 34.0 percent of the value ot total cropproduction. In 1985 and 1986, drought caused wheat production to fall

- 4 -

sharply. The drought continued in 1987, and in 1987 wheat sales were9.9 percent below the 1986 level. Poor weather since 1985 has adverselyaffected wheat production, and higher corn production has been unable to keeptotal cereal production from falling steadily since 1984. Domestic pricesfor wheat and corn have been substantially below world prices (seeTable 1.7). The domestic pricing policy, which includes a relatively highprice of high protein soybean meal, has given rise to a number ofdistortions. The large proportion of cereal (44 percent of wheat andvirtually all corn) used as animal feed effectively subsidizes livestockproduction. Technically suboptimum feeding regimes have also developed.There is a need to develop a systematic approach to administered pricesetting using international prices as an efficiency standard.

1.10 Output of the Constructiou sector makes up about 40 percent ofthe capital stock, so chaluges in construction closely follow changes ininvestment demand. In 1985, the index of the volume of construction-installation activity was only 77 percent of the 1980 level. The largedrop in the demand for construction was due principally to the stabilizationpolicy in 1982-84, which led to a sustained fall in real investment. Thedeclining TFP for the construction sector shown in Table 1.1 suggests thatthe fall in investment left excess capacity in the construction sector.Restructuring plans exist for some state construction companies, but therewould be advantages to formulating and implementing a sectoral restructuringplan, particularly since the adjustment scenario discussed in Chapter IVdoes not project a large increase in the investment rate. One element of arestructuring plan could be the shift of activity from state enterprises tothe private sector, which doubled its share of construction-installationactivity from 13.4 percent in 1980 to 26.3 percent in 1985.

1.11 In the energy sector, Hungary has large reserves of lignite andbrown coal and modest reserves of coal and natural gas. The share of solidfuel in use has fallen from 62 percent in 1970 to 34 percent in 1985, whilehydrocarbons accounted for the largest share increase. Hungary producesnearly 90 percent of its coal needs but imports nearly 80 percent of itscrude oil needs. The large investments in oil-refining capacity undertakenduring the three Five-Year Plans between 1971 and 1985, however, have leftHungary virtually self-sufficient in the production of refined petroleumproducts. Although Hungary imports most of its crude oil from the SovietUnion, sizable spot purchases from the USSR, which are paid for inconvertible currencies, occur occasionally. In addition, Hungary exportsrefined petroleum products, almost all of which are sold to the nonruble area.

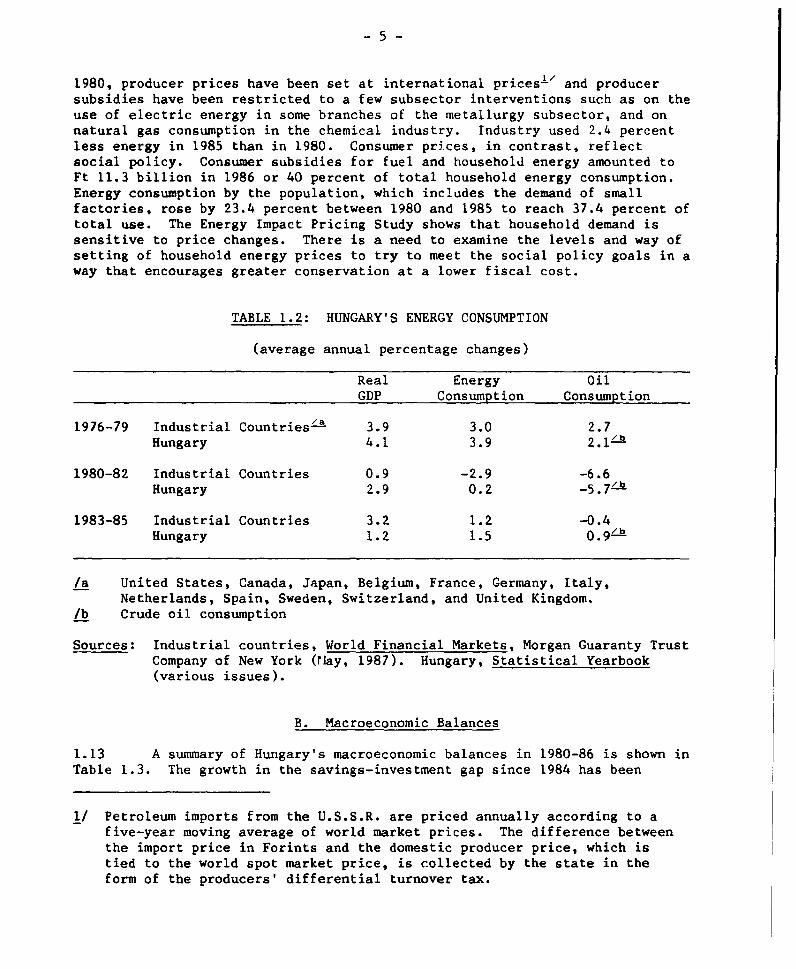

1.12 Energy conservation policy aims to reduce the energy elasticity ofGDP from 1.25 in 1983-85 to 0.35-0.4 by curbing production in energy-intensivesectors (metallurgy, and chemical fertilizers) and promoting energy-savinginvestments through subsidized credit. Efforts to conserve energy have beenless effective in slowing consumption in Hungary than in the industrialcountries (Table 1.2). Part of the reason for the poor record on energyconservation may be the subsidization of household energy prices. Since

- 5 -

1980, producer prices have been set at international prices-I and producersubsidies have been restricted to a few subsector interventions such as on theuse of electric energy in some branches of the metallurgy subsector, and onnatural gas consumption in the chemical industry. Industry used 2.4 percentless energy in 1985 than in 1980. Consumer prices, in contrast, reflectsocial policy. Consumer subsidies for fuel and household energy amounted toFt 11.3 billion in 1986 or 40 percent of total household energy consumption.Energy consumption by the population, which includes the demand of smallfactories, rose by 23.4 percent between 1980 and 1985 to reach 37.4 percent oftotal use. The Energy Impact Pricing Study shows that household demand issensitive to price changes. There is a need to examine the levels and way ofsetting of household energy prices to try to meet the social policy goals in away that encourages greater conservation at a lower fiscal cost.

TABLE 1.2: HUNGARY'S ENERGY CONSUMPTION

(average annual percentage changes)

Real Energy OilGDP Consumption Consumption

1976-79 Industrial Countries/a 3.9 3.0 2.7Hungary 4.1 3.9 2.1/b

1980-82 Industrial Countries 0.9 -2.9 -6.6Hungary 2.9 0.2 _5.7/b

1983-85 Industrial Countries 3.2 1.2 -0.4Hungary 1.2 1.5 0.9/b

/a United States, Canada, Japan, Belgium, France, Germany, Italy,Netherlands, Spain, Sweden, Switzerland, and United Kingdom.

/b Crude oil consumption

Sources: Industrial countries, World Financial Markets, Morgan Guaranty TrustCompany of New York (rlay, 1987). Hungary, Statistical Yearbook(various issues).

B. Macroeconomic Balances

1.13 A summary of Hungary's macroeconomic balances in 1980-86 is shown inTable 1.3. The growth in the savings-investment gap since 1984 has been

1/ Petroleum imports from the U.S.S.R. are priced annually according to afive-year moving average of world market prices. The difference betweenthe import price in Forints and the domestic producer price, which istied to the world spot market price, is collected by the state in theform of the producers' differential turnover tax.

-6-

Table 1.3: MACROECONOMIC BALANCES, 1981-87

(percent of GDP)

1981 1982 1983 1984 1985 1986 1987

Current account balance -3.5 -1.5 0.2 1.4 -0.3 -5.4 -2.2

Private and Enterprise Sectors

Gross fixed investment 17.5 17.5 16.0 16.0 15.5 18.8 19.0Fixed investment 14.3 14.3 14.1 13.3 12.9 16.0 16.2Households 3.1 3.3 3.6 3.7 3.7 4.9 4.6Enterprises 11.2 10.9 10.5 9.6 9.2 11.0 11.6Change in stocks 3.2 3.3 1.9 2.7 2.5 2 9 2.8

National savings 16.9 18.2 17.3 16.2 17.9 16.6 19.1Households 3.5 3.5 4.9 4.7 4.3 4.6 3.7Enterprises 13.4 14.7 12.4 11.6 13.6 12.0 15.4

Savings-Investment gap -0.5 0.6 1.3 0.2 2.5 -2.3 -0.1Households 0.4 0.2 1.3 0.9 0.6 -0.3 -0.9Enterprises -1.0 0.4 -0.0 -0.7 1.8 -1.9 1.0

Public Sector /a

Gross domestic investment 12.2 11.0 10.5 9.7 9.5 8.0 7.8Fixed investment 12.2 11.0 10.5 9.7 9.5 8.0 7.9Change in stocks 0.0 0.0 0.0 0.0 0.0 0.0 0.0

National savings 9.3 8.9 9.3 10.9 6.8 4.9 5.5Current revenues 67.1 65.4 67.8 67.7 64.9 71.3 65.9Current expenditures 57.9 56.5 58.4 56.7 58.1 66.4 60.4

Savings-investment gap -2.9 -2.1 -1.1 1.2 -2.8 -3.1 -2.3

Public and Private

Savings-investment gap -3.5 -1.5 0.2 1.4 -0.3 -5.4 -2.2

Memorandum items:

Share of domestic investmentfinanced by foreign savings 11.7 5.1 -0.7 -5.5 1.1 20.1 8.2

/a Public sector refers to the consolidated state and local governments.

Sources: Central Statistical Office, Ministry of Finance, and NationalPlanning Office, Government Financial Statistics (various issues).

filled by external borrowing. Stopping the growth of external debt requiresthat Hungary raise its saving rate relative to its investment rate. Thestabilization of 1982-84 relied on reducing the investment rate. That policy

-7-

may have hit diminishing returns in light of the apparent reduction in theeconomy's growth potential in the 1980s, and it cannot be pursued muchfurther without jeopardizing the goal of restructuring and technologicaladvance. The authorities' medium-term program indicates a small increase inthe investment rate, which was 26.8 percent in 1987. Enterprise investmentwill be the main source of increase as household demand is expected to bedepressed by the stabilization program and the public sector investmentprogram continues to be scaled back. A marked improvement in the efficiencyof investment also is a key to a successful adjustment scenario. Inaddition, macroeconomic policy should aim to increase the ratio of nationalsavings to GDP. Household sector savings are likely to be depressed in thenext two years as households seek to maintain consumption as real incomesdecline and the tax reform shifts tax burdens from the enterprise sector tothe household sector. That shift, however, is projected to lead to anincrease in enterprise savings. A significant increase in Central Governmentsavings also is needed to achieve the current account target.

C. Consumption and Investment

1.14 Household consumption has not fallen in Hungary since the early1950s. Following four years of modest growth, household consumption grewrapidly in 1986 (Figure 1.1). The principal causes were: the acceleration ofaverage real wages from 1.3 percent growth in 1985 to 1.9 percent in 1986(this followed the declines of 1982-84), a marked increase in income from thesale of farm products, and continued rapid growth of earnings from privatesector activities (Table 1.4). Following the appearance of higher thanplanned fiscal and current account deficits in 1986, the authorities aimed topromote stabilization of the economy by reducing real household consumptionby 0.5-1.0 percent in 1987.

1.15 Two major policy measures were implemented to reduce consumption.First, administrative price increases were announced (para. 1.23) to erodehousehold purchasing power through inflation. The other main policy measurewas a tightening of wage regulations. The stricter wage policy included:(a) increased taxes on wage increases; (b) elimination of the wage regulationscheme that permitted wage increases even if the enterprise was unable to payearnings taxes; (c) where central wage regulation applied, wage increaseswere reduced to 2 percent from 4 percent in 1986; (d) replacement of theaverage earnings-increase regulation scheme by control of the wage bill; and(e) strengthening the link between wage increases and value-added growth.As shown in Table 1.4, the growth of wage income in the first ten months of1987 was reduced to 6.4 percent. This was a 1.8 percentage point below theCPI increase during the same period, but still faster than planned. Thesepolicies were not sufficient to meet the target, however, and as a resultconsumption grew by 2.8 percent in 1987.

1.16 The failure of demand management can be traced to several factors.First, anticipatory buying occurred as information about the tax reform wasdisseminated and people became aware that the introduction of the VAT wouldincrease consumer prices by about 15 percent in 1988 through furtherreductions in consumer price subsidies. The anticipatory buying overwhelmed

- 8 -

Table 1.4: CASH RECEIPTS OF THE POPULATION(FT billions)

Earnings Other Sales of Social Totalin Farm Labor Farm Benefits Other Cash

Wages Cooperatives Income Products in Cash Receipts /a Receipts

1984 207.0 35.9 11.9 47.9 115.9 110.5 528.61985 222.2 36.3 12.6 49.6 125.8 129.3 575.81986 238.1 38.0 14.4 54.5 136.8 147.9 629.71987 261.6 39.5 16.4 59.9 150.5 175.7 703.6

(Annual percentage changes)

1977 8.1 8.3 -0.8 24.6 9.8 14.4 10.31978 9.8 6.7 4.4 6.6 7.4 11.3 8.61979 6.4 5.9 -3.8 6.6 16.7 17.5 9.11980 2.6 4.7 5.7 11.4 15.7 25.4 9.51981 4.4 11.6 5.7 3.6 8.4 17.1 7.41982 5.0 11.0 5.0 11.4 8.5 14.2 8.11983 3.0 4.5 3.2 10.0 9.1 23.0 8.11984 5.2 -1.0 7.9 7.1 12.1 35.7 11.71985 7.3 1.2 5.3 3.7 8.5 17.5 8.91986 7.3 3.5 18.1 9.9 7.6 14.4 9.51987 7.7 3.9 13.8 9.8 9.6 18.8 10.8

/a Mainly receipts from private economic activities, and insurance receiptsother than social benefits.

Source: Monthly Bulletin of Statistics

the impact of administrative price increases that occurred in the first halfof 1987 and led to greater household consumption. Second, monetary policywas ineffective in draining excess liquidity from the enterprise sector,which permitted faster than planned wage increases. Monetary policy was alsounable to halt a decline in household savings. By drawing down their savingsdeposits, consumers were able to increase consumption despite the reductionin real income from wages. It is also likely that a liquidity overhangexisted at end-1986 (para. 1.26). An increase in interest rates on householdloans and deposits would have been an appropriate monetary policy. InSeptember, a 3 percentage point premium was added to long-term deposit ratesto try to reduce the flow from savings deposits, but by then much of thedamage was done. During the third quarter of 1987, household savingsdeposits declined by Ft 5 billion (about 2 percent), while currency holdingsincreased by Ft 6 billion more than planned. Total household savings areestimated to have fallen by 19 percent in 1987. Stabilization policy in 1988calls for a 2.0-2.5 percent reduction in household consumption. The needremains to develop flexible instruments of monetary control that can be usedto support a contractionary aggregate demand policy, and to use a more activeinterest rate policy.

-9-

1.17 Real gross fixed investment declined in each year during 1980 to1985 (Figure 1.1), the result of a stabilization policy that aimed to reducedomestic demand but protect household consumption levels. That trend wasreversed in 1986 when gross fixed investment grew by 6.5 percent. The fallin the investment rate resulted in an across-the-board fall in the growthrate of the capital stock (Table 1.1). Capital productivity has beennegative in Hungary since the mid-1970's_' but the effects of the lowproductivity on overall growth may have been less apparent when the capitalstock was growing more rapidly. The authorities' medium-term program callsfor a substantial improvement in the efficiency of investment. An improvedallocation of investment, favoring the manufacturing industries where Hungaryin potentially competitive, would help.

1.18 In 1986 there was a shift in investment composition toward themanufacturing industries and away from the basic materials and electricenergy subsectors. Investment in mining and electric energy (over 50 percentGovernment financed) fell by 7.2 percent and 4.7 percent respectively, andinvestment in metallurgy, another sector identified as needing restructuring,

Fisure 1.1: SOURCES OF GROWTH

(billions of 1981 Forint)

15~~~~~~~~~~~~~~~~~~~~~~~~~~~~0

10

5 <.

0~ ~~~~t

1911 192 193 1914 1965 19_5 1961

YearS wtncSMtIastastleM &W 1.

2/ The Economic Survey of Europe in 1986, U.N. Economic Commission forEurope discusses trends in factor and total productivity at the aggregatelevel through 1985. Report No. 6124-HU, Hungary: Industrial Policy,Performance, and Prospects for Adjustment, also discusses developmentsin factor and total productivity in Hungarian industry through 1983.

- 10 -

fell by 10.0 percent. Investment results for 1987 indicate that some of thefavorable developments observed in 1986 continued. Fixed investment grew by6.9 percent. Mining's share dropped again, but electric energy's, reflectingthe heavy burden of the construction of the Paks nuclear power plant, grew.The 1988 Plan contains a reduction in Government supported investments inelectric energy.

1.19 The authorities' efforts to improve the structure of investmentinvolve reducing investments financed by the Central and Local Governmentbudgets. The public investment program, which accounted for 38.5 percent ofsocialist sector investment in 1987 (Table 1.5) has several components.First, there are the large Central Government projects, generally exceedingFt 500 million ($10 million). In 1987 there were eight projects- , downfrom 13 in 1984. The authorities envision no new projects for the remainderof the Plan. By end-1987 only two were less than 80 percent completed: theBos-Nagymaros barrage system (29 percent completed) and production of cokingcoal at Mecsek (18 percent). The authorities have stated their intention totry to reduce total spending on Mecsek to less than the planned amount. In1988, planned spending on the large projects group is projected to fall by15 percent, which would imply a cut of nearly 50 percent since 1983. Asecond category of public investment, the Central Target investments, aregenerally smaller in size but require some state coordination. Spending ontarget investments was mainly for investments in petroleum and gas mining,development of the electricity network, rail and road transport, and thecommunications system. Nominal spending on the target group investments hasfallen only slightly from the 1983 level. The Plan for 1988 shows higherspending on mining and communications and lower spending on the others, withtotal target investment spending rising slightly. A third group of publicinvestment projects, the Other Central investments, are concentrated in thenon-productive services: public health, social services, education, cultureand others. Spending on this group has fallen sharply since the early partof the decade.

1.20 Subsidized credit in the form of equity allocations4- is alsoprovided to enterprises investing in certain preferred investment categories.In 1987 there were 18 categories though four of them, support to coal mining,energy saving, agriculture and food processing, and convertible currencyexport development accounted for 80.7 percent of the total. Subsidized

3/ In order of total investment cost they are: the Paks nuclear station(Ft 96.4 billion), the Bos-Nagymaros barrage system (Ft 35.7 billion),production of coking coal at Mecsek coal minvs (Ft 29.9 billion), theBudapest metro (Ft 10.9 billion), the coking plant at the Duna Iron Works(Ft 9.3 billion), ore mining in Mecsek mountain (Ft 4.6 billion),reconstruction of the Royal Palace in Budapest (Ft 2.5 billion), and theFerihegy Airport (Ft 1.1 billion).

4/ Equity allocations, which are administered by the State DevelopmentInstitute, are granted for a fixed annuity, and in some cases a variable"dividend", both treated as costs. Annuities are usually paid over15 years and are sufficient to repay the nominal value of the equityallocation.

- 11 -

Table 1.5: SOCIALIST SECTOR'' INVESTMENT, 1987

(Ft billions)

Councils,State State Bank Enterprises,Budget Loans Loans other sources Total

Central Government 19.8 11.9 - 23.4 55.1of which:-Large 2.4 7.0 - 4.2 13.6-Target 8.9 4.4 - 13.5 26.8-Other 8.5 0.5 - 5.7 14.7Loc&. Government 7.0 - - 27.8 34.8Enterprises 7.1 9.8 33.9 97.9 148.7Total 33.9 21.7 33.9 149.1 238.6

/a Socialist sector investmer.t comprises total investment less privatesector investment. In 1987 it was 81.1 percent of the total.

Source: National Planning Office

credit is administered by the State Development Institute (SDI) which borrowsfrom the National Bank of Hungary at a rate 0.5 percentage points below therate on long-term refinancing credit for commercial banks. A grant from theCentral Government covers the difference between SDI's earnings and its costof funds.

1.21 Local Government (Council) investments are the final component ofpublic investment. They are roughly equal in amount to central targetinvestments but are concentrated in infrastructure. Financing for Councilinvestments is mainly out of the grant from the Central Government budget,municipal taxes and user fees, and bond issues. Council investments areprojected to decrease by 22 percent in 1988 because of the failure of Councilrevenues, especially the grant from the Central Government, to increasesufficiently to offset higher current spending requirements.

1.22 As the role of the public sector has diminished, enterprises haveassumed a greater role in determining the allocation of investment. As thefigures from Table 1.5 indicate, only 29 percent of enterprise investment wasfinanced by loans, either from the State (through the SDI) or from commercialbanks. Retained earnings financed two-thirds of enterprise investment. Withsuch a large proportion financed by retained earnings, strict financialdiscipline is needed to ensure that enterprise investment decisions aresound. The reduction of State subsidies and financial supports toenterprises will help. The introduction of greater competition in theallocation of investment credit would help increase the efficiency ofenterprise investment. In the short-term, competition would be stimulated byforcing commercial banks to compete for long-term investment throughcompetitive bidding. In the medium-term, the continued development and

- 12 -

integration of the financial system should permit the use priority areas tobe phased out and the SDI to become better integrated into the financialsystem. The elimination of the requirement that long-term loans be matchedby long-term deposits, which restricts capital mobility, would also helpimprove the allocation of investment resources.

D. Public Finance

1.23 This section discusses trends in public-sector savings. Other keyaspects of the fiscal system--the effects of the tax reform and financialsupports to enterprises--are discussed separately in Chapter II. Public-sector savings have fallen sharply since 1984 (Table 1.3). Current revenueshave remained at about two-thirds of GDP since 1983 (capital revenue isnegligible), but expenditures grew stubstantially, particularly in 1986.Government capital expenditures have declined in the 1980s, so the worsenedfinancial position is attributable to growing current expenditures. By 1986,current expenditures had risen to 65 percent of GDP, a share that appears atodds with the goaLs of increasing decentralization and allowing market forcesto play a greater role in the allocation of resources. Within currentexpenditures, subsidies and other current transfers and transfers to localgovernment have shown the largest increases.

1.24 The State budget deficit hit Ft 46.9 billion in 1986, ' more thandouble the Plan figure, and representing 4.3 percent of GDP. Three factorscan be singled out. First, the decline in world oil prices contributed to areduction in revenues from the producers' differential turnover tax (a taxpaid by oil users on the difference between the forint price of oil importedfrom the Soviet Union and the world market price converted to forints).Second, consumer price subsidies exceeded the Plan level. Finally, there wasa deficit in the Intervention Fund, an extra-budgetary fund originallyintended to offset the effects of negative terms of trade shocks onenterprises. Lower enterprise tax revenues were offset by higher thananticipated household taxes, and total revenue met the Plan target. Creditto the Central Government expanded by Ft 67.4 billion, which included theState budget deficit plus Ft 20.5 billion of credit extended for the purposeof writing-off non-performing enterprise debt in advance of the transfer ofcredit accounts from the NBH to the commercial banks. The increase inCentral Government credit represented 6.2 percent of GDP.

1.25 In 1987, the Government approved a State budget deficit ofFt 43.8 billion. The unanticipated increase in the convertible currencycurrent account deficit in the fourth quarter of 1986, however, prompted theauthorities to re-assess the consistency of the Plan budget deficit with therequired increase in national savings implied by the target $700-800 million

5/ The figures in Table 1.3 are for the Consolidated Central Government,which differs from the State budget by treating amortization payments asa (negative) financing item rather than an expenditure.

- 13 -

current account deficit. As a result, the State budget deficit target wasreduced to Ft 30-35 billion. New measures necessary to support the lowerdeficit target were approved in April. The most important measure was anincrease in the ceiling on consuler price inflation to 9 percent from theinitial 7 percent level, which permitted consumer price subsidies to belowered. A series of price increases occurred in April, with the mostimportant being a 16-22 percent meat price increase. There was also an8 percent devaluation of the forint against the convertible currency basket.Finally, there was a 3.6 percent appreciation of the forint against thetransferable ruble, which was designed in part to raise revenue from theproducers' differential turnover tax. In July, another series of priceincreases occurred. These included a 20 percent increase in the prices ofhousehold energy, tobacco, and flour and bakery products, and a 10 percentincrease in gasoline and diesel oil prices. This combination of measuresreduced the State budget deficit to Ft 35 billion in 1987. Nevertheless,given the fall in the household savings rate during 1987, (para. 1.15) thereduction in the fiscal deficit was inadequate for a $700-800 million currentaccount deficit.

E. Money and Credit

1.26 The years 1982-84 were marked by tight credit and monetary policiesto support the goal of a current account surplus in the convertible currencybalance of payments. With the appearance of a $329 million surplus in 1984,credit target.: were relaxed and the growth of monetary and credit aggregatesaccelerated (Table 1.6). Plan targets for the growth of credit were overshotin 1985 and 1986. Much of the excessive growth of credit was credit to theCentral Government that resulted from the increasingly loose fiscal stanceBroad money also expanded rapidly in 1985 and 1986. Rapid growth of the realmoney supply may have created a liquidity overhang by end-1986. (A liquidityoverhang occurs when agents are forced to hold real money balances in excessof the desired amount. Limited possibilities for diversification of assetsand chronic excess demand for some consumer goods create the conditions for aliquidity overhang.) A sudden attempt to use these excess real balances putsadditional demand pressure on the domestic goods market, and could spill overinto the balance of payments, confounding efforts to implement an effectivemonetary policy. Developments in household consumption in 1987 wereconsistent with the existence of a liquidity overhang.

1.27 In January 1987, the two-tier banking system was created byseparating the commercial credit departments from the NBH. The authoritiesintended to pursue a tight monetary policy and target growth rates of M2, anddomestic credit were reduced consistent with a change in net foreignliabilities associated with a $700-&00 million convertible currency currentaccount deficit. After two years of excessive credit growth, however, the1987 targets were too loose. When data for the first half of 1987 revealedno significant slowing down in the rate of credit expansion--principally dueto continued rapid growth of credit to households and the Central Government--the monetary authorities reduced the refinancing limits that commercial bankscould extend for working capital credits. Combined with the measures to

- 14 -

contain the fiscal deficit, the tightening of short-term refinancing limitsslowed the growth of credit expansion at the end of 1987, though for the yearboth broad money growth and domestic credit growth exceeded their plantargets. The National Bank's lack of experience in conducting monetarypolicy may also have contributed to the faster than planned growth.

1.28 The credit plan for 1988 indicates a sharp contraction in domesticcredit growth and broad money growth (Table 1.6). Central Government creditgrowth is projected to slow to 0.6 percent, consistent with a fiscal deficitof Ft 10.4 billion of which Treasury bills sales to households and enterpriseswill finance Ft 3 billion. Household credit expansion, 80 percent of whichfinances housing, is projected to be 10.3 per.ent. The brunt of the creditcontraction wAl1 be borne by enterprises in the form of scarcer, moreexpensive short-term working capital. The income velocity of M2 is projectedto increase from 2.06 in 1987 to 2.31. The large increase in velocityreflects not only the tighter monetary policy, but also the effects offinancial innovations--including the introduction of treasury bills and thefurther development of the money market--and higher inflationary expectations.These would tend to lead households and enterprises to economize on the useof cash balances. The tight monetary policy is further justified by theunknown size of excess liquidity in the economy. There is a risk that,despite the anticipatory buying in 1987, household liquidity remainsexcessive. Excess enterprise liquidity also poses a danger because the

Table 1.6: MONETARY AND FINANCIAL DATA

(percentage growth rates)

1982 1983 1984 1985 1986 1987 1988/P

Money and quasimoney(M2) 6.7 3.8 5.2 10.1 14.1 7.9 1.7

Domestic credit 6.2 4.2 5.3 7.6 16.4 11.5 6.0Central Government(net) 50.5 -1.3 -60.3 83.9 324.0 37.4 0.6

Enterprise workingcapital 5.2 5.2 9.0 12.8 10.5 1.4 -1.8

Household 11.5 15.5 16.4 14.1 14.7 15.7 10.3

Memorandum items:Income velocityof M2 2.09 2.13 2.21 2.12 1.96 2.06 2.31

CPI inflation(percent) 6.9 7.3 8.3 7.0 5.3 9.0 15.0

/P Plan

Sources: Central Statistical Office, National Bank of Hungary.

- 15 -

household spending in the third and fourth quarters of 1987 may havetranslated into greater liquid asset holdings of enterprises. In 1988 theneed remains to develop instruments for short-term monetary management. Openmarket operations, for example, would allow more flexible monetary managementthan the current instruments, short term refinencing credit limits andreserve requirements. Implementing a treasury bill auction would create theconditions for open market operations, as well as develop the capitalmarket. A tight monetary policy will also help develop the capital market bypromo'-ing competition in the financial sector and increasing enterprisefinancial discipline.

1.29 At present, interest rate policy differentiates between thehousehold sector and the enterprise sector. Borrowing and lending rates forthe household sector are negative in real terms (Table 1.7), though the3 percentage point increase in long-term deposit rates inttoduced inSeptember 1987 (para. 1.16) should compensate for the accelesation ofconsumer price inflation in 1987. Housing loans, the bulk of householdcredit, carry a 1-3 percent nominal interest rate and a maximum maturity of35 years. Because of the low average yield of the National Savings Banks'(NSB) loan portfolio, increases in household deposits generate losses thstmust be covered by transfers from the Central Government budget. This couldlead the authorities to be overly cautious in raising household depositrates. Borrowing and lending rates for enterprises are in principle freelydetermined, but in practice the NBH continues to exert influence on theinterest rate structure through the interest rate on refinancing credit.This influence is likely to diminish as the interbank money market and openmarket operations develop.

1.30 The Hungarian financial system is being rapidly transformed. Thesegmentation of the household and enterprise financial markets persists,however, with full integration planned for 1989-90. Resolution of the housingfinance issue is blocking complete integration. Two main problems must beaddressed: the need to ensure that housing finance does not become starvedfor funds when financial institutions are free to compete for householddeposits; and the need to safeguard the social policy goal of providingassistance in hcusing finance. There is some urgency to resolving theseproblems. The solvency of the NSB would be threatened if disintermediationwere to occur. Integration of the two financial sectors also would increasecompetition in the banking system as commercial banks compete for housingdeposits. This could increase the interest sensitivity of the financialsystem, and enhance monetary policy. In addition, as competition develops,interest rates could play a larger role in the allocation of credit, whichcould improve the efficiency of investment.

F. Inflation

1.31 Maintaining relatively low inflation has been an important goal ofHungarian macroeconomic policy, and, as shown in Table 1.7 and StatisticalAppendix Table 5.2, inflation has been relatively low and stable. Thesuccessful anti-inflation policy has been an important factor in the heavy

- 16 -

Table. L7: KEY ECONOMIC VARIABLES, 1980-66

(percent)

1980 1981 1982 1983 1984 1985 1986 1987/Y

INCENTIVE INDICATORS

1. Real Effective Exchange Rate1.1 Index 1980=100 100.0 84.8 78.7 84.7 84.0 85.6 101.2 121.21.2 Annual Change (an increase

represents a depreciation) - -15.2 -7.2 7.6 -0.8. 1.9 18.2 19.8

2. Real Interest Rates2.1 One-year savings notes

(households) -4.6 1.S -3.6 -3.1 -'.0 -2.8 -1.2 -2.92.2 Long-term lending rate

(households) -5.6 -1.5 -3.6 -4.0 -4.9 -3.7 -2.2 -5.22.3 12-month time deposit rate

(enterprises) 1.0 0.7 -0.3 1.9 3.3 0.02.4 Long-term investment rate

(enterprises) 6.6 6.2 6.4 S.0 4.1 3.1

Memo Item: Change in the CPI 9.1 4.6 9 7.3 8.3 7.0 5.3 8.6

3. Index of Real Wages3.1 Real wage index (1980=100) 100.0 101.1 ;OJ.4 97.2 94.9 96.1 97.6 97.93.2 Annual change -1.7 1.1 -0.7 -3.2 -2.4 1.3 1.6 0.3

4. Ratios of Domestic AgriculturalPrices to International Prices

4.1 Soymeal 83.0 94.0 66.0 90.0 91.0 116.0 110.04.2 Wheat 39.0 41.0 40.0 46.0 42.0 56.0 66.04.3 Corn 56.0 57.0 65.0 66.0 47.0 59.0 94.0

EXTERNAL TRAOE INDICATORS

5. Volume Index of Exports (1980=100)5.1 Fuels. electric energy 100.0 87.2 140.1 212.7 211.6 121.7 159.0 161.05.2 Materials, semi-finished

products, spare parts 100.0 99.3 97.9 112.1 121.3 120.5 119.4 128.05.3 Machinery, transport equipment.

other capital goods 100.0 100.6 111.8 115.6 120.3 133.0 129.6 132.05.4 Industrial consumer goods 100.0 113.6 104.0 107.0 112.5 118.0 116.7 123.05.5 Materials for the food industry,

live animals. processed foodproducts 100.0 111.6 121.6 126.1 135.3 134.2 126.7 127.0

5.6 TOTAL 100.0 102.6 110.0 121.0 127.0 127.0 124.0 129.0

6. Export Shares World Trade6.1 Food 0.93 1.06 1.15 1.07 1.03 1.11 1.086.2 Metals and minerals 0.42 0.45 0.42 0.41 0.49 0.44 0.546.3 Total primaries 0.39 0.43 0.52 0.52 0.64 0.66 0.756.4 Chemicals 0.59 0.67 0.70 0.67 0.66 0.70 0.616.5 Machinery and transport equipment 0.58 0.54 0.58 0.55 0.49 0.53 0.496.6 Other manufacturers 0.SO 0.52 0.53 0.53 0.50 0.54 0.496.7 Total manufacturers 0.54 0.53 0.56 0.54 0.50 0.53 0.496.8 Total merchandise 0.47 0.49 0.54 0.54 0.54 0.57 0.54

7. Manufactured Exports (Ruble and Nonruble)7.1 Real growth rates 0.5 0.6 11.1 3.4 4.0 10.S -2.6 1.87.2 Value as share of total exports 26.2 25.3 26.9 25.8 25.4 28.8 30.1 30.0

8. Comodity Terms of Trade (X/M)8.1 Index 1980=100 (total) 100.0 99.2 97.0 94.5 92.6 91.6 88.4 89.0

8.1.1 Ruble 100.0 96.1 93.2 90.7 88.9 88.3 88.2 90.98.1.2 Nonruble 100.0 102.2 101.1 98.6 96.3 95.2 88.6 88.6

8.2 Annual change (total) 0.3 -0.8 -2.3 -2.5 -2.1 -1.0 -3.5 0.78.2.1 Ruble -1.1 -3.9 -3.1 -2.6 -2.0 -0.7 -0.1 3.08.2.2 Nonruble 1.7 2.2 -1.1 -2.4 -2.4 -1.1 -6.9 0.0

La Preliminary

Sources: Central Statistical Office, National Bank of Hungary, Statistical Yearbook (various issues),Efficiency Studies, Research Institute of Agricultural Economics. Budapest. 1986.

- 17 -

subsidization of both consumer and producer prices, which has led to pricedistortions, some of which have been mentioned. Policy induced distortionsare inevitably costly, and the cost is borne by the budget. The negativecorrelations between changes in credit to the government and changes innational accounts deflators, shown in Table 1.8, suggest than one of thereasons for growth in the fiscal deficit is spending on price subsidies tocontrol inflation. Consumer price inflation decelerated from 7 percent in1985 to 5.3 percent in 1986. The authorities relaxed the inflation ceilingin 1987, raising it to 9 percent in order to contain the fiscal deficit. Theconsumer price index is expected to increase by 15-16 percent in 1988 whenthe Value Added Tax is introduced. The authorities intend to reduce thenumber of subsidized commodities to a few basic ones including milk, householdheating, and public transportation and to implement a social benefits packageto compensate especially affected groups for the higher prices.

Table 1.8: CORRELATION COEFFICIENTS BETWEEN GOVERNMENT CREDIT EXPANSIONAND CHANGES IN NATIONAL ACCOUNTS DEFLATORS, 1981-86

Deflator forPrivate Public Gross fixed

GDP Consumption Consumption Consumption Investment

-.37 -.34 -.33 -.25 -.44

Source: National Bank of Hungary, Fobb nepgazdasagi folyamatok, 1986 andstaff calculations.

G. Current Account

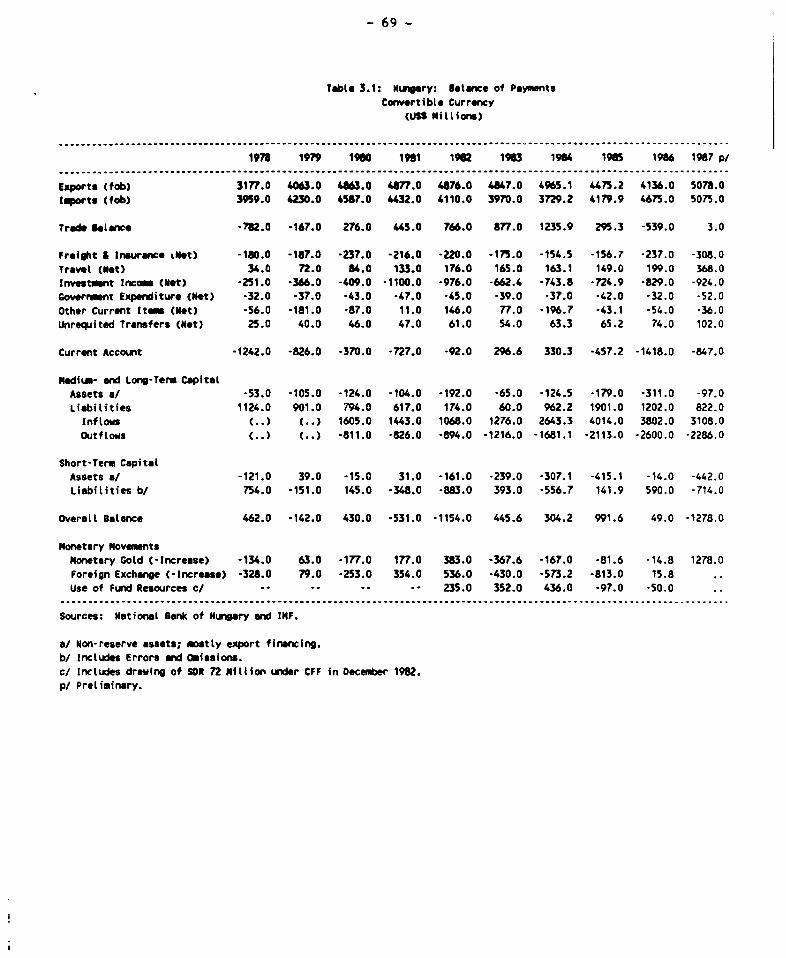

1.32 A detailed look at the balance of payments from 1980 to 1987 ispresented in Tables 3.1 and 3.2 of the Statistical Appendix. Text Table 1.9summarizes recent developments in convertible currency transactions. Theprimary cause of the deterioration in the current account in 1985-86 was thetrade balance, which declined by $1.7 billion in 1985-86. Nonruble importvolumes grew by 2.6 percent in 1985 and 0.8 percent in 1986, while nonrubleexports declined by 6.6 percent and 3.8 percent. The 6.9 percent fall in thenonruble terms of trade in 1986 (Table 1.7), which cost the economy$350-400 million also contributed to the worsening trade balance. Thedepreciation of the dollar and declining commodity prices were the maincauses of the terms of trade loss. Hungary is adversely affected by adepreciation of the dollar because about 50 percent of its nonruble exportsare denominated in dollars, compared with only 30 percent of nonrubleimports. Hungarian organizations were not efficient in using forwardcontracts to hedge against exchange rate risk.

1.33 Partly to increase the effectiveness of the active exchange ratepolicy, in March 1987 the authorities canceled the Competitive Pricing Rule,which aimed at linking domestic price changes to world price changes for

- 18 -

Table 1.9: CONVERTIBLE CURRENCY CURRENT ACCOUNT, SELECTED ITEMS

(US$ millions)

1984 1985 1986 1987

Current Account 329 -457 -1419 -847Merchandise exports (fob) 4965 4475 4136 5078Merchandise imports (fob) 3729 4179 4675 5075Trade balance 1236 296 -539 3Tourism receipts (net) 163 149 199 368Current account/GDP ( percent) 1.7 -2.2 -6.0 -3.2

Source: National Bank of Hungary

about 80 percent of manufacturing turnover but had the effect of permittingincreases in export profitability to be translated into increases in domesticscales profitability. As a result of this and other measures, which arediscussed in Chapter II, in the first nine months of 1987, nonruble salesprices grew faster than domestic sales prices. In the light industrysubsector, for example nonruble sales prices grew by 10.5 percent, anddomestic sales prices by only 3.0 percent. Export performance alsoimproved. During 1987, the volume of nonruble exports grew by 5.0 percentand their value by 11.7 percent. Firmer commodity prices also helped Hungaryavoid a terms of trade loss in 1987. The increase in the volume of nonrubleexports and stable terms of trade compensated for the faster than Plannedgrowth of nonruble imports and contributed to the $542 million improvement inthe 1987 trade balance.

1.34 The balance of ruble trade continued to improve in 1987, recordinga trade surplus of $117 million, up from $17 million in 1986. Part of thelarger-than-expected improvement is attributable to a 2.8 percent terms oftrade gain, which is mainly due to the fall in oil prices as determined bythe Bucharest formula. Export volumes increased by 2.5 percent and importvolumes by 3.7 percent. The bulk of ruble trade is conducted throughbilateral agreements between CMEA member governments. In principle, theagreements maintain balance, and the appearance of a larger-than-expectedtrade surplus is awkward because the transferable ruble, which wasestablished in 1963 for the purpose of bilateral clearing of inter-CMEAtrade, has no "commodity convertibility" so that in practice it has failed tocreate the conditions for multilateral clearing. In addition to thedifficulty of clearing accounts, larger-than-planned ruble exports may be adrain on convertible currency. The Hungarian authorities' response to theaccumulation of a larger-than-expected trade surplus in 1987 was to try toreduce the attractiveness of ruble exports. In March 1987, the forint wasappreciated by 3.6 percent against the transferable ruble. The 2 percentprofit guarantee on ruble exports was eliminated in 1988, and onJanuary 1, 1988 a further 3.7 percent revaluation occurred.

- 19 -

H. External Debt and Creditworthiness

1.35 Hungary overcame a severe liquidity crisis in 1982, and, with thehelp of two IMF Stand-By Arrangements, in 1983-84 succeeded in producing acurrent account surplus, restructuring its debt and restoring itsinternational credit standing. Developments since 1985, however, have causedincreasing concern. The deteriorating macroeconomic performance was financedby relatively large amounts of external borrowing, and Hungary's debt anddebt service ratios grew sharply in 1985-86, as shown in Table 1.10 andFigure 1.2. In 1987, apprehension among lenders was reflected in a hardeningof the terms on Hungary's syndicated loans. The current situation requiresskillful macroeconomic management. Above all, it requires a soundmedium-term program showing progress in economic restructuring that willimprove Hungary's competitiveness, bring about a decline in the debt burdenand an improvement in long-term creditworthiness. Elements of such a programare discussed in Chapter IV.

1.36 Total external liabilities 1n convertible currencies, includingshort-term debt and outstanding IMF purchases, rose from $8.8 billion at theend of 1984 to $17.7 billion in 1987. Net external liabilities, measured asgross liabilities less the external assets of Hungary, rose even faster thangross debt, from $4.4 billion at end-1984 to an estimated $10.9 billion atthe end of 1987. At least half of the recent increase in Hungary's debtmeasured in dollars is explained by changes in cross exchange rates of majorcurrencies since 1985. By end-1986, 60 percent of Hungary's medium to longterm debt was repayable in currencies other than the dollar, up from20 percent at end-1984. Yen and Deutschemark denominated loans accounted for19 percent and 12 percent respectively of the total, though these figureswere probably lower bounds because loans repayable in multiple currenciesmade up 18 percent of the 1986 total.

1.37 The change in the ratio of net debt to exports (Figure 1.2), bothmeasured in dollars, measures the growth in the burden of Hungary's externaldebt. The ratio is less affected by the change in the value of the dollarthan is the total debt figure, since both numerator and denominator arecalculated in dollars. Hungary's net debt relative to exports of goods andservices rose from 66 percent in 1984 to an estimated 152 percent in 1987.Net debt relative to GDP, both measured in dollars, is a better measure ofthe long-term creditworthiness of an economy because, over time, resourcescan be shifted to foreign exchange earning or saving activities. Hungary'snet external debt relative to GDP, which was 20 percent in 1984, rose to33 percent in 1986 and to 42 percent in 1987.

1.38 The maturity distribution of Hungary's external debt indicates achange in borrowing strategy. Short-term debt fell to $1.9 billion or11.0 percent of total convertible currency debt in 1987, whereas in 1980,short-term debt accounted for 36.8 percent of the total. Table 1.11 showsHungary's debt service for 1984-87, as well as projections for 1988-90. Theimplications of the projections are discussed in Chapter IV. The $2.6 billionin 1986 amortization payments included prepayment of $523 million of of loanscontracted at relatively high interest rates. By prepaying such loans,

- 20 -

Table 1.10: CONVERTIBLE CURRENCY EXTERNAL DEBT(US$ millions)

1980 1981 1982 1983 1984 1985 1986 1987

Total debt 9090.0 8699.0 7715.0 8250.0 8835.6 11760.2 15085.6 17739.0of which:Long term 5743.0 5850.0 5951.0 6127.0 7414.8 10005.5 12663.9 15785.0Short term 3347.0 2849.0 1764.0 2123.0 1420.8 1705.2 2421.7 1954.0

Internationalreserves 2558.0 2033.0 1233.0 1862.0 2556.0 3543.0 3638.8 2478.0Other foreignassets 1256.0 1219.0 1539.0 1792.0 2196.7 3199.0 3656.8 4357.0Total foreignassets 3814.0 3252.0 2772.0 3654.0 4752.0 6742.0 7295.6 6835.0

Net externaldebt 5276.0 5447.0 4943.0 4596.0 4082.9 5018.2 7790.0 10904.0

(percent)Net debt/exports/a 87.6 89.2 76.9 74.0 66.1 81.7 117.6 151.8