how to read financial statements (powerpoint...

TRANSCRIPT

© Practising Law Institute

CORPORATE LAW AND PRACTICECourse Handbook Series

Number B-2157

How to ReadFinancial Statements

2015

ChairChad Rucker

To order this book, call (800) 260-4PLI or fax us at (800) 321-0093. Ask ourCustomer Service Department for PLI Order Number 58927, Dept. BAV5.

Practising Law Institute1177 Avenue of the Americas

New York, New York 10036

© Practising Law Institute

2

How to Read Financial Statements (PowerPoint slides)

Chad Rucker

Valuation Research Corporation

If you find this article helpful, you can learn more about the subject by going to www.pli.edu to view the on demand program or segment for which it was written.

47

© Practising Law Institute

48

© Practising Law Institute

How

to R

ead F

inancia

l S

tate

ments

1

Ch

air

Ch

ad

Ru

ck

er

Managin

g D

ire

cto

r

Valu

ation R

esearc

h C

orp

ora

tion

500 F

ifth

Avenue

39

th F

loo

r

Ne

w Y

ork

, N

Y 1

0110

Offic

e: 917.3

38.5

613

Cell:

732.8

55.9

241

cru

cker@

valu

ationre

searc

h.c

om

49

© Practising Law Institute

Bala

nce S

heet

2

50

© Practising Law Institute

Asse

ts =

Lia

bili

tie

s &

Eq

uity

3

Asse

ts =

Lia

bili

tie

s +

Bo

ok E

qu

ity

51

© Practising Law Institute

Ba

lan

ce

Sh

ee

t

4

Ba

lan

ce

sh

ee

t -

-Th

e fin

an

cia

l sta

tem

en

t th

at sh

ow

s th

e a

mo

un

ts o

f th

e

co

mp

an

y’s

asse

ts, lia

bili

tie

s, a

nd

ow

ne

rs’ e

qu

ity a

t th

e e

nd

of th

e p

erio

d.

Th

ree

se

ctio

ns o

f a

ba

lan

ce

sh

ee

t:

• A

ssets

--

A r

esourc

e w

ith e

conom

ic v

alu

e that

a c

om

pany o

wns o

r

contr

ols

with the e

xpecta

tion t

hat

it w

ill p

rovid

e futu

re b

enefit.

•L

iab

ilit

ies

--

A c

om

pany's

legal debts

or

oblig

ations that

arise d

uring t

he

cours

e o

f busin

ess o

pera

tions.

Lia

bili

ties a

re s

ettle

d o

ver

tim

e t

hro

ugh t

he

transfe

r of

econom

ic b

enefits

inclu

din

g m

oney,

goods o

r serv

ices.

•B

oo

k E

qu

ity -

- O

n a

com

pany's

bala

nce s

heet, t

he a

mount

of

the f

unds

contr

ibute

d b

y the o

wners

(th

e s

tockhold

ers

) plu

s the r

eta

ined e

arn

ings (

or

losses).

Als

o r

efe

rred t

o a

s s

hare

hold

ers

' equity.

52

© Practising Law Institute

Sam

ple

Bala

nce S

heet

5

CON

SOLI

DA

TED

BA

LAN

CE S

HEE

T - A

BC In

c.(D

olla

rs in

Tho

usan

ds)

20X9

20X8

20X9

20X8

Ass

ets

Liab

iliti

es a

nd S

hare

hold

ers'

Equ

ity

IDID

Ass

ets

Liab

iliti

esCu

rren

t Ass

ets

Curr

ent L

iabi

litie

sA

1Ca

sh a

nd c

ash

equi

vale

nts

$25,

000

$15,

000

B1A

ccou

nts

paya

ble

$60,

000

$57,

000

A2

Acc

ount

s re

ceiv

able

- ne

t of a

llow

ance

for

doub

tful

acc

ount

s of

$6,

000

in 2

0X9

and

$3,0

00 in

20X

8

160,

000

145,

000

B2N

otes

pay

able

51,0

0061

,000

A3

Inve

ntor

ies,

at t

he lo

wer

of c

ost o

r mar

ket

180,

000

185,

000

B3A

ccru

ed e

xpen

ses

30,0

0036

,000

A4

Prep

aid

expe

nses

and

oth

er c

urre

nt a

sset

s4,

000

3,00

0B4

Inco

me

taxe

s pa

yabl

e17

,000

15,0

00B5

Oth

er li

abili

ties

12,0

0012

,000

B6Cu

rren

t por

tion

of l

ong-

term

deb

t6,

000

6,00

0A

5To

tal C

urre

nt A

sset

s$3

69,0

00$3

48,0

00B7

Tota

l Cur

rent

Lia

bilit

ies

$176

,000

$187

,000

Long

-Ter

m A

sset

sLo

ng-T

erm

Lia

bilit

ies

A6

Land

$30,

000

$30,

000

B8D

efer

red

inco

me

taxe

s$1

6,00

0$9

,000

A7

Build

ings

125,

000

120,

000

B9Lo

ng-t

erm

deb

t13

0,00

013

0,00

0A

8M

achi

nery

200,

000

173,

000

B10

Tota

l Lia

bilit

ies

$322

,000

$326

,000

A9

Leas

ehol

d im

prov

emen

ts15

,000

15,0

00A

10Fu

rnit

ure,

fixt

ures

, etc

.15

,000

12,0

00A

11To

tal P

rope

rty,

Pla

nt a

nd E

quip

men

t$3

85,0

00$3

50,0

00Sh

areh

olde

rs' E

quit

yB1

1Co

mm

on s

tock

$75,

000

$72,

500

A12

Less

: acc

umul

ated

dep

reci

atio

n12

5,00

097

,000

B12

Add

itio

nal p

aid-

in c

apit

al20

,000

13,5

00A

13N

et P

rope

rty,

Pla

nt &

Equ

ipm

ent

$260

,000

$253

,000

B13

Reta

ined

ear

ning

s21

4,00

019

2,00

0B1

4To

tal S

hare

hold

ers'

Equ

ity

$309

,000

$278

,000

Oth

er A

sset

sA

14In

tang

ible

s (g

oodw

ill, p

aten

ts) n

et o

f ac

cum

ulat

ed a

mor

tiza

tion

of $

2,00

0 in

20X

9 an

d $1

,000

in 2

0X8

$2,0

00$3

,000

A15

Tota

l Oth

er A

sset

s$2

,000

$3,0

00A

16To

tal A

sset

s$6

31,0

00$6

04,0

00B1

5To

tal L

iabi

litie

s an

d Sh

areh

olde

rs' E

quit

y$6

31,0

00$6

04,0

00

Dec

embe

r 31,

Dec

embe

r 31,

Lin

e #

L

ine #

53

© Practising Law Institute

Sam

ple

Bala

nce S

heet

6

(Dol

lars

in T

hous

ands

)

20X9

20X8

Ass

ets

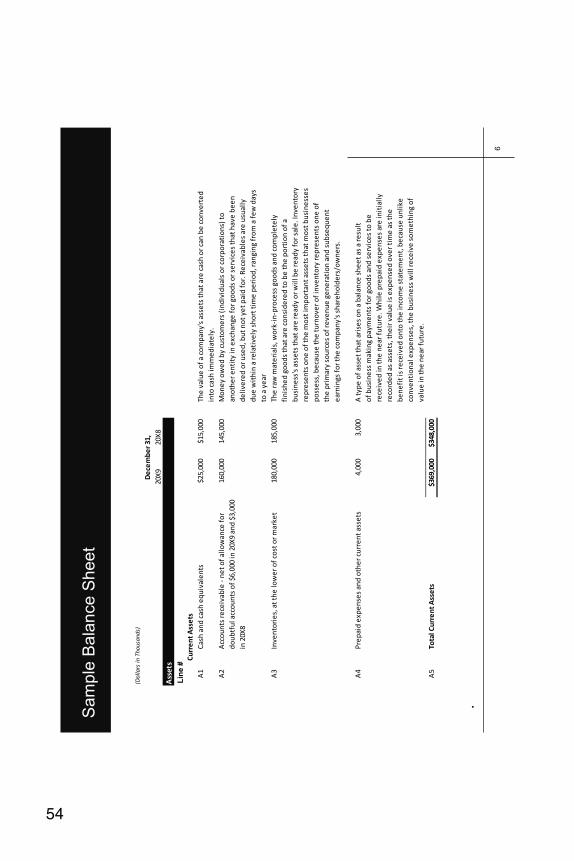

IDCu

rren

t Ass

ets

A1

Cash

and

cas

h eq

uiva

lent

s$2

5,00

0$1

5,00

0Th

e va

lue

of a

com

pany

's a

sset

s th

at a

re c

ash

or c

an b

e co

nver

ted

into

cas

h im

med

iate

ly.

A2

Acc

ount

s re

ceiv

able

- ne

t of a

llow

ance

for

doub

tful

acc

ount

s of

$6,

000

in 2

0X9

and

$3,0

00

in 2

0X8

160,

000

145,

000

Mon

ey o

wed

by

cust

omer

s (i

ndiv

idua

ls o

r cor

pora

tion

s) to

an

othe

r ent

ity

in e

xcha

nge

for g

oods

or s

ervi

ces

that

hav

e be

en

deliv

ered

or u

sed,

but

not

yet

pai

d fo

r. R

ecei

vabl

es a

re u

sual

ly

due

wit

hin

a re

lati

vely

sho

rt ti

me

peri

od, r

angi

ng fr

om a

few

day

s to

a y

ear

A3

Inve

ntor

ies,

at t

he lo

wer

of c

ost o

r mar

ket

180,

000

185,

000

The

raw

mat

eria

ls, w

ork-

in-p

roce

ss g

oods

and

com

plet

ely

fini

shed

goo

ds th

at a

re c

onsi

dere

d to

be

the

port

ion

of a

bu

sine

ss's

ass

ets

that

are

read

y or

will

be

read

y fo

r sal

e. In

vent

ory

repr

esen

ts o

ne o

f the

mos

t im

port

ant a

sset

s th

at m

ost b

usin

esse

s po

sses

s, b

ecau

se th

e tu

rnov

er o

f inv

ento

ry re

pres

ents

one

of

the

prim

ary

sour

ces

of re

venu

e ge

nera

tion

and

sub

sequ

ent

earn

ings

for t

he c

ompa

ny's

sha

reho

lder

s/ow

ners

.

A4

Prep

aid

expe

nses

and

oth

er c

urre

nt a

sset

s4,

000

3,00

0A

type

of a

sset

that

ari

ses

on a

bal

ance

she

et a

s a

resu

lt

of b

usin

ess

mak

ing

paym

ents

for g

oods

and

ser

vice

s to

be

rece

ived

in th

e ne

ar fu

ture

. Whi

le p

repa

id e

xpen

ses

are

init

ially

re

cord

ed a

s as

sets

, the

ir v

alue

is e

xpen

sed

over

tim

e as

the

bene

fit i

s re

ceiv

ed o

nto

the

inco

me

stat

emen

t, b

ecau

se u

nlik

e co

nven

tion

al e

xpen

ses,

the

busi

ness

will

rece

ive

som

ethi

ng o

f va

lue

in th

e ne

ar fu

ture

.A

5To

tal C

urre

nt A

sset

s$3

69,0

00$3

48,0

00

Dec

embe

r 31,

Lin

e #

54

© Practising Law Institute

7

(Dol

lars

in T

hous

ands

)

20X9

20X8

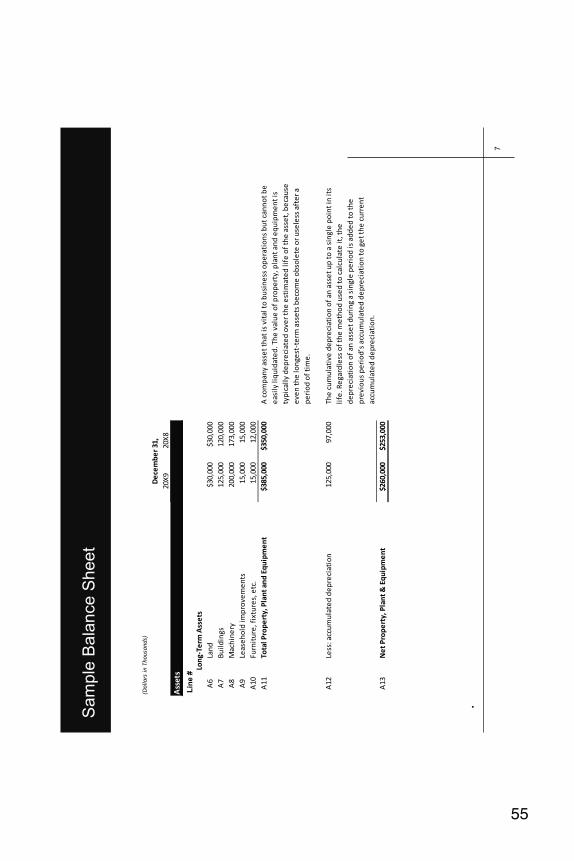

Ass

ets

IDLo

ng-T

erm

Ass

ets

A6

Land

$30,

000

$30,

000

A7

Build

ings

125,

000

120,

000

A8

Mac

hine

ry20

0,00

017

3,00

0A

9Le

aseh

old

impr

ovem

ents

15,0

0015

,000

A10

Furn

itur

e, fi

xtur

es, e

tc.

15,0

0012

,000

A11

Tota

l Pro

pert

y, P

lant

and

Equ

ipm

ent

$385

,000

$350

,000

A c

ompa

ny a

sset

that

is v

ital

to b

usin

ess

oper

atio

ns b

ut c

anno

t be

easi

ly li

quid

ated

. The

val

ue o

f pro

pert

y, p

lant

and

equ

ipm

ent i

s ty

pica

lly d

epre

ciat

ed o

ver t

he e

stim

ated

life

of t

he a

sset

, bec

ause

ev

en th

e lo

nges

t-te

rm a

sset

s be

com

e ob

sole

te o

r use

less

aft

er a

pe

riod

of t

ime.

A12

Less

: acc

umul

ated

dep

reci

atio

n12

5,00

097

,000

The

cum

ulat

ive

depr

ecia

tion

of a

n as

set u

p to

a s

ingl

e po

int i

n it

s lif

e. R

egar

dles

s of

the

met

hod

used

to c

alcu

late

it, t

he

depr

ecia

tion

of a

n as

set d

urin

g a

sing

le p

erio

d is

add

ed to

the

prev

ious

per

iod’

s ac

cum

ulat

ed d

epre

ciat

ion

to g

et th

e cu

rren

t ac

cum

ulat

ed d

epre

ciat

ion.

A13

Net

Pro

pert

y, P

lant

& E

quip

men

t$2

60,0

00$2

53,0

00

Dec

embe

r 31,

Sam

ple

Bala

nce S

heet

Lin

e #

55

© Practising Law Institute

8

(Dol

lars

in T

hous

ands

)

20X9

20X8

Ass

ets

IDO

ther

Ass

ets

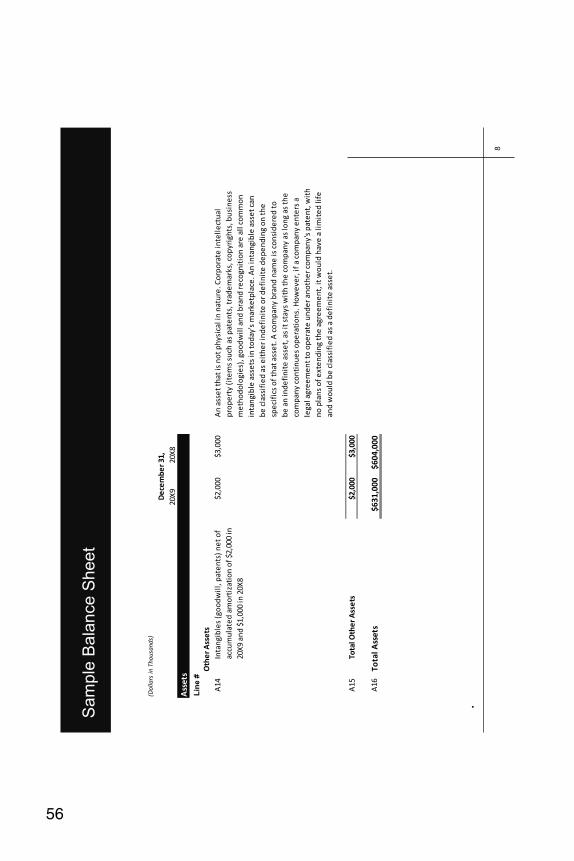

A14

Inta

ngib

les

(goo

dwill

, pat

ents

) net

of

accu

mul

ated

am

orti

zati

on o

f $2,

000

in

20X9

and

$1,

000

in 2

0X8

$2,0

00$3

,000

An

asse

t tha

t is

not p

hysi

cal i

n na

ture

. Cor

pora

te in

telle

ctua

l pr

oper

ty (i

tem

s su

ch a

s pa

tent

s, tr

adem

arks

, cop

yrig

hts,

bus

ines

s m

etho

dolo

gies

), g

oodw

ill a

nd b

rand

reco

gnit

ion

are

all c

omm

on

inta

ngib

le a

sset

s in

toda

y's

mar

ketp

lace

. An

inta

ngib

le a

sset

can

be

cla

ssif

ied

as e

ithe

r ind

efin

ite

or d

efin

ite

depe

ndin

g on

the

spec

ific

s of

that

ass

et. A

com

pany

bra

nd n

ame

is c

onsi

dere

d to

be

an

inde

fini

te a

sset

, as

it s

tays

wit

h th

e co

mpa

ny a

s lo

ng a

s th

e co

mpa

ny c

onti

nues

ope

rati

ons.

How

ever

, if a

com

pany

ent

ers

a le

gal a

gree

men

t to

oper

ate

unde

r ano

ther

com

pany

's p

aten

t, w

ith

no p

lans

of e

xten

ding

the

agre

emen

t, it

wou

ld h

ave

a lim

ited

life

an

d w

ould

be

clas

sifi

ed a

s a

defi

nite

ass

et.

A15

Tota

l Oth

er A

sset

s$2

,000

$3,0

00

A16

Tota

l Ass

ets

$631

,000

$604

,000

Dec

embe

r 31,

Sam

ple

Bala

nce S

heet

Lin

e #

56

© Practising Law Institute

9

Dol

lars

in T

hous

ands

)

20X9

20X8

Liab

iliti

es a

nd S

hare

hold

ers'

Equ

ity

IDLi

abili

ties

Curr

ent L

iabi

litie

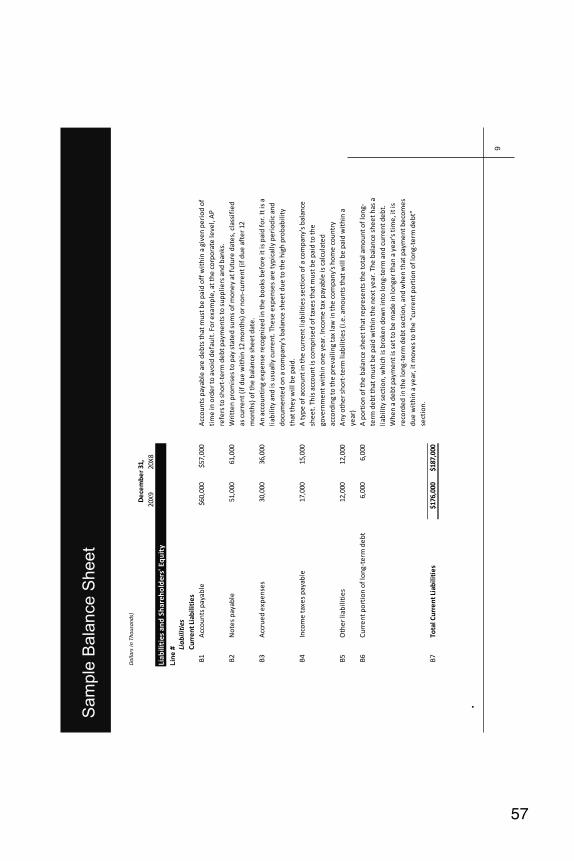

sB1

Acc

ount

s pa

yabl

e$6

0,00

0$5

7,00

0A

ccou

nts

paya

ble

are

debt

s th

at m

ust b

e pa

id o

ff w

ithi

n a

give

n pe

riod

of

tim

e in

ord

er to

avo

id d

efau

lt. F

or e

xam

ple,

at t

he c

orpo

rate

leve

l, A

P re

fers

to s

hort

-ter

m d

ebt p

aym

ents

to s

uppl

iers

and

ban

ks.

B2N

otes

pay

able

51,0

0061

,000

Wri

tten

pro

mis

es to

pay

sta

ted

sum

s of

mon

ey a

t fut

ure

date

s, c

lass

ifie

d as

cur

rent

(if d

ue w

ithi

n 12

mon

ths)

or n

on-c

urre

nt (i

f due

aft

er 1

2 m

onth

s) o

f the

bal

ance

she

et d

ate.

B3A

ccru

ed e

xpen

ses

30,0

0036

,000

An

acco

unti

ng e

xpen

se re

cogn

ized

in th

e bo

oks

befo

re it

is p

aid

for.

It is

a

liabi

lity

and

is u

sual

ly c

urre

nt. T

hese

exp

ense

s ar

e ty

pica

lly p

erio

dic

and

docu

men

ted

on a

com

pany

's b

alan

ce s

heet

due

to th

e hi

gh p

roba

bilit

y th

at th

ey w

ill b

e pa

id.

B4In

com

e ta

xes

paya

ble

17,0

0015

,000

A ty

pe o

f acc

ount

in th

e cu

rren

t lia

bilit

ies

sect

ion

of a

com

pany

's b

alan

ce

shee

t. T

his

acco

unt i

s co

mpr

ised

of t

axes

that

mus

t be

paid

to th

e go

vern

men

t wit

hin

one

year

. Inc

ome

tax

paya

ble

is c

alcu

late

d ac

cord

ing

to th

e pr

evai

ling

tax

law

in th

e co

mpa

ny's

hom

e co

untr

yB5

Oth

er li

abili

ties

12,0

0012

,000

Any

oth

er s

hort

-ter

m li

abili

ties

(i.e

. am

ount

s th

at w

ill b

e pa

id w

ithi

n a

year

)B6

Curr

ent p

orti

on o

f lon

g-te

rm d

ebt

6,00

06,

000

A p

orti

on o

f the

bal

ance

she

et th

at re

pres

ents

the

tota

l am

ount

of l

ong-

term

deb

t tha

t mus

t be

paid

wit

hin

the

next

yea

r. T

he b

alan

ce s

heet

has

a

liabi

lity

sect

ion,

whi

ch is

bro

ken

dow

n in

to lo

ng-t

erm

and

cur

rent

deb

t.

Whe

n a

debt

pay

men

t is

set t

o be

mad

e in

long

er th

an a

yea

r's ti

me,

it is

re

cord

ed in

the

long

-ter

m d

ebt s

ecti

on, a

nd w

hen

that

pay

men

t bec

omes

du

e w

ithi

n a

year

, it m

oves

to th

e "c

urre

nt p

orti

on o

f lon

g-te

rm d

ebt"

se

ctio

n.B7

Tota

l Cur

rent

Lia

bilit

ies

$176

,000

$187

,000

Dec

embe

r 31,

Sam

ple

Bala

nce S

heet

Lin

e #

57

© Practising Law Institute

10

Dol

lars

in T

hous

ands

)

20X9

20X8

Liab

iliti

es a

nd S

hare

hold

ers'

Equ

ity

IDLo

ng-t

erm

liab

iliti

esB8

Def

erre

d in

com

e ta

xes

$16,

000

$9,0

00A

liab

ility

reco

rded

on

the

bala

nce

shee

t tha

t res

ults

from

inco

me

alre

ady

earn

ed a

nd re

cogn

ized

for a

ccou

ntin

g, b

ut n

ot ta

x, p

urpo

ses.

Als

o,

diff

eren

ces

betw

een

tax

law

s an

d ac

coun

ting

met

hods

can

resu

lt in

a

tem

pora

ry d

iffe

renc

e in

the

amou

nt o

f inc

ome

tax

paya

ble

by a

com

pany

. Th

is d

iffe

renc

e is

reco

rded

as

defe

rred

inco

me

tax.

B9Lo

ng-t

erm

deb

t13

0,00

013

0,00

0Lo

ans

and

fina

ncia

l obl

igat

ions

last

ing

over

one

yea

r.B1

0To

tal L

iabi

litie

s$3

22,0

00$3

26,0

00

Dec

embe

r 31,

Sam

ple

Bala

nce S

heet

Lin

e #

58

© Practising Law Institute

11

Dol

lars

in T

hous

ands

)

20X9

20X8

Liab

iliti

es a

nd S

hare

hold

ers'

Equ

ity

IDSh

areh

olde

rs' E

quit

yB1

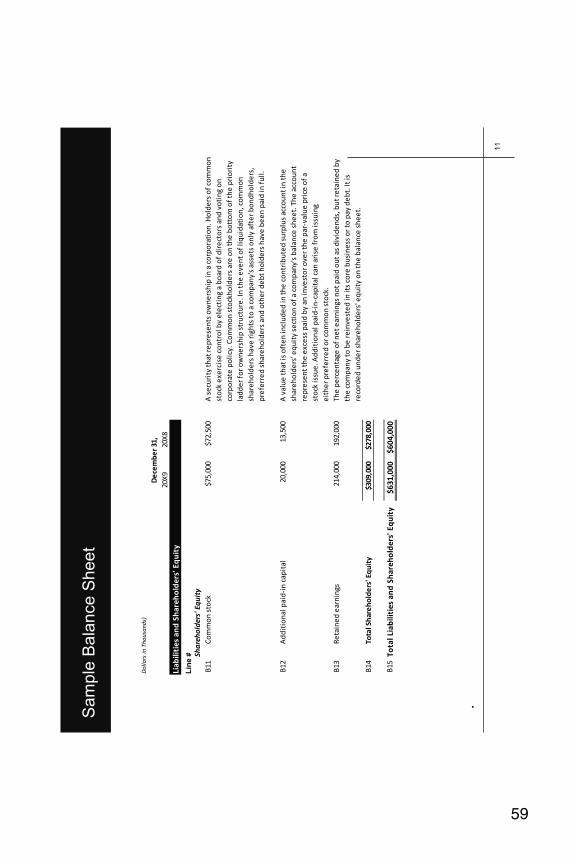

1Co

mm

on s

tock

$75,

000

$72,

500

A s

ecur

ity

that

repr

esen

ts o

wne

rshi

p in

a c

orpo

rati

on. H

olde

rs o

f com

mon

st

ock

exer

cise

con

trol

by

elec

ting

a b

oard

of d

irec

tors

and

vot

ing

on

corp

orat

e po

licy.

Com

mon

sto

ckho

lder

s ar

e on

the

bott

om o

f the

pri

orit

y la

dder

for o

wne

rshi

p st

ruct

ure.

In th

e ev

ent o

f liq

uida

tion

, com

mon

sh

areh

olde

rs h

ave

righ

ts to

a c

ompa

ny's

ass

ets

only

aft

er b

ondh

olde

rs,

pref

erre

d sh

areh

olde

rs a

nd o

ther

deb

t hol

ders

hav

e be

en p

aid

in fu

ll.

B12

Add

itio

nal p

aid-

in c

apit

al20

,000

13,5

00A

val

ue th

at is

oft

en in

clud

ed in

the

cont

ribu

ted

surp

lus

acco

unt i

n th

e sh

areh

olde

rs' e

quit

y se

ctio

n of

a c

ompa

ny's

bal

ance

she

et. T

he a

ccou

nt

repr

esen

t the

exc

ess

paid

by

an in

vest

or o

ver t

he p

ar-v

alue

pri

ce o

f a

stoc

k is

sue.

Add

itio

nal p

aid-

in-c

apit

al c

an a

rise

from

issu

ing

eith

er p

refe

rred

or c

omm

on s

tock

.B1

3Re

tain

ed e

arni

ngs

214,

000

192,

000

The

perc

enta

ge o

f net

ear

ning

s no

t pai

d ou

t as

divi

dend

s, b

ut re

tain

ed b

y th

e co

mpa

ny to

be

rein

vest

ed in

its

core

bus

ines

s or

to p

ay d

ebt.

It is

re

cord

ed u

nder

sha

reho

lder

s' e

quit

y on

the

bala

nce

shee

t.B1

4To

tal S

hare

hold

ers'

Equ

ity

$309

,000

$278

,000

B15

Tota

l Lia

bilit

ies

and

Shar

ehol

ders

' Equ

ity

$631

,000

$604

,000

Dec

embe

r 31,

Sam

ple

Bala

nce S

heet

Lin

e #

59

© Practising Law Institute

Sa

mp

le S

tate

me

nt o

f S

ha

reh

old

ers

’ E

qu

ity

12

CON

SOLI

DA

TED

STA

TEM

ENT

OF

CHA

NG

ES IN

SH

ARE

HO

LDER

S' E

QU

ITY

- ABC

Inc.

(Dol

lars

in T

hous

ands

)

IDCo

mm

onSt

ock

Add

itio

nal

paid

-in

capi

tal

Reta

ined

earn

ings

Tota

l

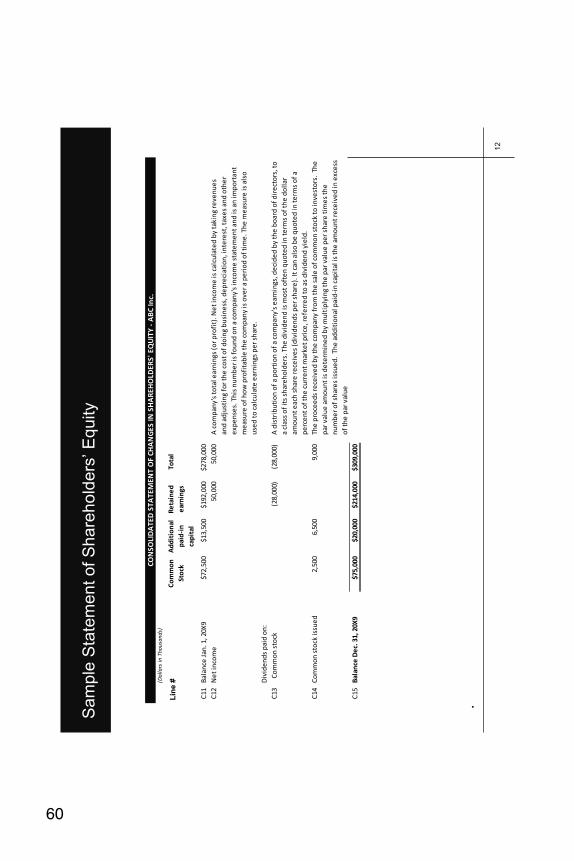

C11

Bala

nce

Jan.

1, 2

0X9

$72,

500

$13,

500

$192

,000

$278

,000

C12

Net

inco

me

50,0

0050

,000

A c

ompa

ny's

tota

l ear

ning

s (o

r pro

fit)

. Net

inco

me

is c

alcu

late

d by

taki

ng re

venu

es

and

adju

stin

g fo

r the

cos

t of d

oing

bus

ines

s, d

epre

ciat

ion,

inte

rest

, tax

es a

nd o

ther

ex

pens

es. T

his

num

ber i

s fo

und

on a

com

pany

's in

com

e st

atem

ent a

nd is

an

impo

rtan

t m

easu

re o

f how

pro

fita

ble

the

com

pany

is o

ver a

per

iod

of ti

me.

The

mea

sure

is a

lso

used

to c

alcu

late

ear

ning

s pe

r sha

re.

Div

iden

ds p

aid

on:

C13

Co

mm

on s

tock

(28,

000)

(28,

000)

A d

istr

ibut

ion

of a

por

tion

of a

com

pany

's e

arni

ngs,

dec

ided

by

the

boar

d of

dir

ecto

rs, t

o a

clas

s of

its

shar

ehol

ders

. The

div

iden

d is

mos

t oft

en q

uote

d in

term

s of

the

dolla

r am

ount

eac

h sh

are

rece

ives

(div

iden

ds p

er s

hare

). It

can

als

o be

quo

ted

in te

rms

of a

pe

rcen

t of t

he c

urre

nt m

arke

t pri

ce, r

efer

red

to a

s di

vide

nd y

ield

.C1

4Co

mm

on s

tock

issu

ed2,

500

6,50

09,

000

The

proc

eeds

rece

ived

by

the

com

pany

from

the

sale

of c

omm

on s

tock

to in

vest

ors.

The

pa

r val

ue a

mou

nt is

det

erm

ined

by

mul

tipl

ying

the

par v

alue

per

sha

re ti

mes

the

num

ber o

f sha

res

issu

ed.

The

addi

tion

al p

aid-

in c

apit

al is

the

amou

nt re

ceiv

ed in

exc

ess

of th

e pa

r val

ueC1

5Ba

lanc

e D

ec. 3

1, 2

0X9

$75,

000

$20,

000

$214

,000

$309

,000

Lin

e #

60

© Practising Law Institute

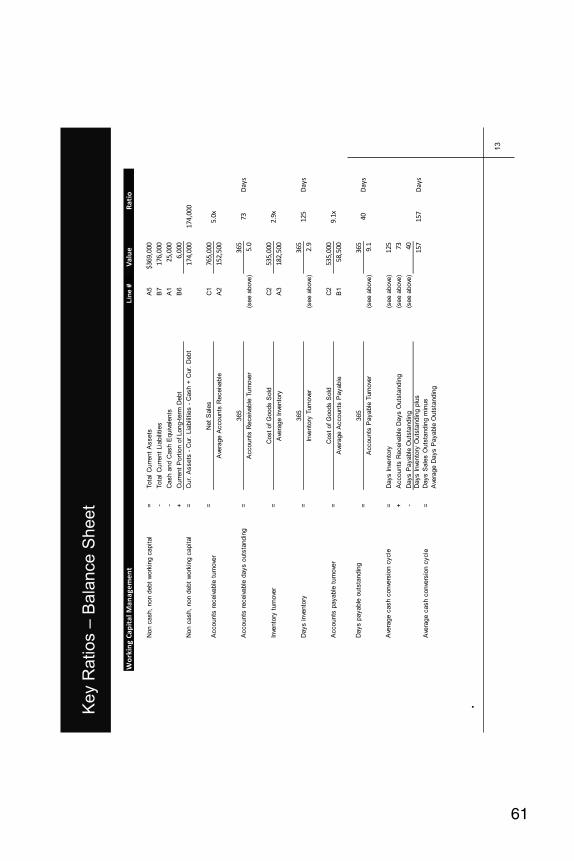

Ke

y R

atio

s –

Ba

lan

ce

Sh

ee

t

13

Wor

king

Cap

ital

Man

agem

ent

IDVa

lue

Rati

o

Non c

ash,

non d

ebt

work

ing c

apital

=Tota

l C

urr

ent

Assets

A5

$369

,000

-Tota

l C

urr

ent

Lia

bili

ties

B7

176,

000

-C

ash a

nd C

ash E

quiv

ale

nts

A1

25,0

00+

Curr

ent

Port

ion o

f Long-t

erm

Debt

B6

6,00

0N

on c

ash,

non d

ebt

work

ing c

apital

=17

4,00

017

4,00

0

=C

176

5,00

0A

215

2,50

0

365

(see a

bove

)5.

0

C2

535,

000

A3

182,

500

365

(see a

bove

)2.

9

C2

535,

000

B1

58,5

00

Days p

ayable

outs

tandin

g36

5(s

ee a

bove

)9.

1

Ave

rage c

ash c

onve

rsio

n c

ycle

=D

ays Inve

nto

ry(s

ee a

bove

)12

5+

Accounts

Receiv

able

Days O

uts

tandin

g(s

ee a

bove

)73

-D

ays P

ayable

Outs

tandin

g(s

ee a

bove

)40

Ave

rage c

ash c

onve

rsio

n c

ycle

=15

715

7D

ays

Day

sA

ccounts

Receiv

able

Turn

ove

r

Inve

nto

ry t

urn

ove

r=

Cost

of G

oods S

old

2.9x

Ave

rage Inve

nto

ry

Cur.

Assets

- C

ur.

Lia

bili

ties -

Cash +

Cur.

Debt

Accounts

receiv

able

turn

ove

rN

et

Sale

s5.

0xA

vera

ge A

ccounts

Receiv

able

Accounts

receiv

able

days o

uts

tandin

g=

365

73

Days inve

nto

ry365

125

Day

sIn

vento

ry T

urn

ove

r=

Accounts

payable

turn

ove

r=

Cost

of G

oods S

old

9.1x

Ave

rage A

ccounts

Payable

=365

40

Days Inve

nto

ry O

uts

tandin

g p

lus

Days S

ale

s O

uts

tandin

g m

inus

Ave

rage D

ays P

ayable

Outs

tandin

g

Day

sA

ccounts

Payable

Turn

ove

r

Lin

e #

61

© Practising Law Institute

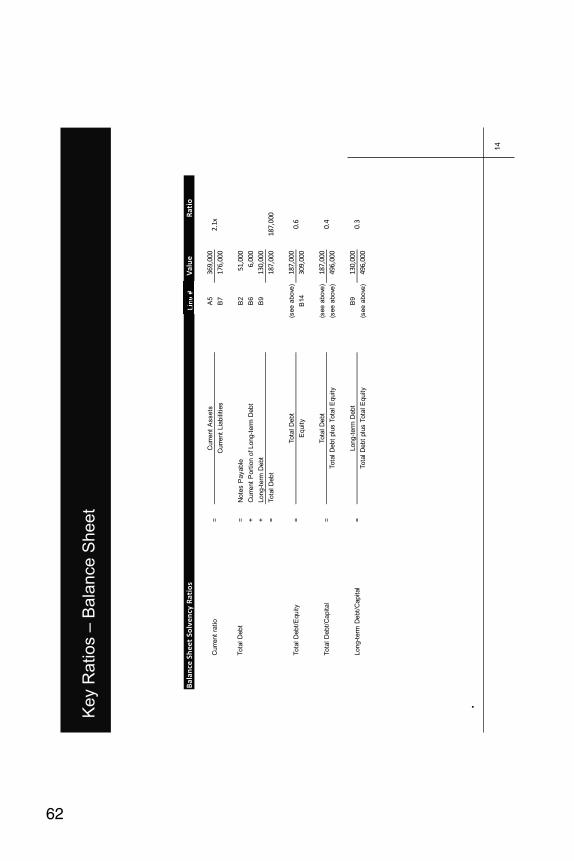

Ke

y R

atio

s –

Ba

lan

ce

Sh

ee

t

14

Bala

nce

Shee

t So

lven

cy R

atio

sID

Valu

eRa

tio

A5

369,

000

B7

176,

000

Tota

l D

ebt

=N

ote

s P

ayable

B2

51,0

00+

Curr

ent

Port

ion o

f Long-t

erm

Debt

B6

6,00

0+

Long-t

erm

Debt

B9

130,

000

=Tota

l D

ebt

187,

000

187,

000

(see a

bove

)18

7,00

0B

14

309,

000

(see a

bove

)18

7,00

0(s

ee a

bove

)49

6,00

0

B9

130,

000

(see a

bove

)49

6,00

0Long-t

erm

Debt/

Capital

=Long-t

erm

Debt

0.3

Tota

l D

ebt

plu

s T

ota

l E

quity

Tota

l D

ebt/

Capital

=Tota

l D

ebt

0.4

Tota

l D

ebt

plu

s T

ota

l E

quity

Curr

ent

ratio

=C

urr

ent

Assets

2.1x

Curr

ent

Lia

bili

ties

Tota

l D

ebt/

Equity

=Tota

l D

ebt

0.6

Equity

IDIIDIDIDDDDDDDDIDDDDDDDDDDDDDDDDDIDIDDDDDDDD

62

© Practising Law Institute

Ke

y R

atio

s –

Ba

lan

ce

Sh

ee

t

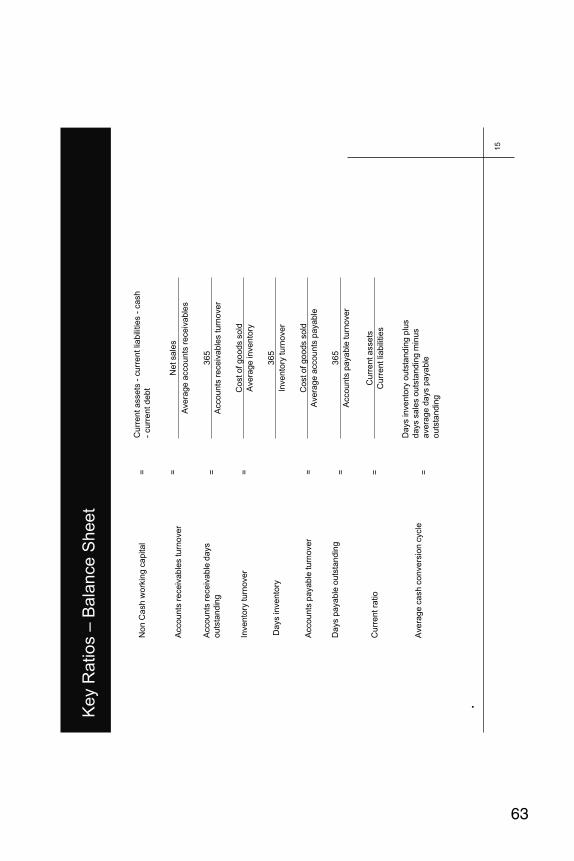

15

No

n C

ash

wo

rkin

g c

ap

ita

l =

C

urr

ent a

sse

ts -

cu

rre

nt lia

bili

tie

s -

ca

sh

- cu

rre

nt d

eb

t

Accounts

re

ce

iva

ble

s tu

rno

ver

=

Ne

t sa

les

Avera

ge a

ccounts

re

ce

ivable

s

Accounts

re

ce

iva

ble

da

ys

ou

tsta

ndin

g

=

36

5

Accounts

re

ce

iva

ble

s tu

rno

ver

Invento

ry turn

over

=

Co

st o

f g

oo

ds s

old

Avera

ge invento

ry

Days invento

ry

36

5

Invento

ry turn

over

Accounts

payable

turn

over

=

Co

st o

f g

oo

ds s

old

Avera

ge a

ccounts

payable

Da

ys p

aya

ble

ou

tsta

ndin

g

=

36

5

Accounts

payable

turn

over

Cu

rre

nt ra

tio

=

C

urr

ent a

sse

ts

Cu

rre

nt lia

bili

tie

s

Ave

rage c

ash

co

nve

rsio

n c

ycle

=

Days invento

ry o

uts

tandin

g p

lus

days s

ale

s o

uts

tandin

g m

inus

ave

rage d

ays p

aya

ble

ou

tsta

ndin

g

63

© Practising Law Institute

Ke

y R

atio

s –

Ba

lan

ce

Sh

ee

t

16

Tota

l D

ebt/E

quity

=

Tota

l D

ebt

Equity

Tota

l D

ebt/C

apital

=

Tota

l D

ebt

Tota

l debt plu

s tota

l equity

64

© Practising Law Institute

Incom

e S

tate

ment

17

65

© Practising Law Institute

Inco

me

Sta

tem

en

t

18

Inc

om

e S

tate

me

nt-

-Th

e fin

an

cia

l sta

tem

en

t th

at sh

ow

s th

e n

et in

co

me

of a

co

mp

an

y fo

r a

pe

rio

d o

f tim

e.

Th

ree

se

ctio

ns o

f a

n in

co

me

sta

tem

en

t:

•R

even

ues -

- A

mounts

earn

ed f

rom

rendering s

erv

ices o

r selli

ng g

oods t

o

custo

mers

.

•E

xp

en

ses -

- T

he e

conom

ic c

osts

that

a c

om

pany incurs

thro

ugh its

opera

tions to e

arn

revenue.

•N

et

Inco

me -

- A

com

pany’s

tota

l re

venues less its

tota

l expenses for

a

period o

f tim

e.

66

© Practising Law Institute

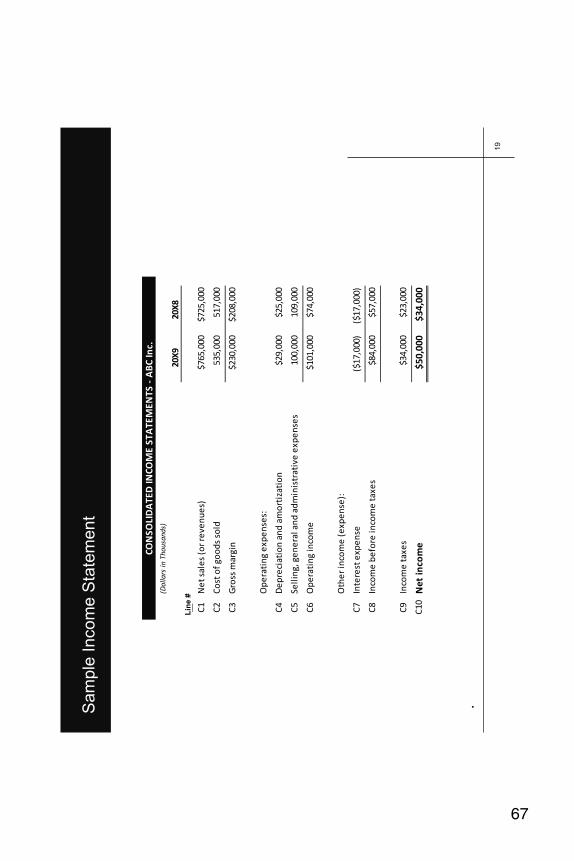

Sam

ple

Incom

e S

tate

ment

19

CON

SOLI

DA

TED

INCO

ME

STA

TEM

ENTS

- A

BC In

c.(D

olla

rs in

Tho

usan

ds)

20X9

20X8

ID C1N

et s

ales

(or r

even

ues)

$765

,000

$725

,000

C2Co

st o

f goo

ds s

old

535,

000

517,

000

C3G

ross

mar

gin

$230

,000

$208

,000

Ope

rati

ng e

xpen

ses:

C4D

epre

ciat

ion

and

amor

tiza

tion

$29,

000

$25,

000

C5Se

lling

, gen

eral

and

adm

inis

trat

ive

expe

nses

100,

000

109,

000

C6O

pera

ting

inco

me

$101

,000

$74,

000

Oth

er in

com

e (e

xpen

se):

C7In

tere

st e

xpen

se($

17,0

00)

($17

,000

)

C8In

com

e be

fore

inco

me

taxe

s$8

4,00

0$5

7,00

0

C9In

com

e ta

xes

$34,

000

$23,

000

C10

Net

inco

me

$50,

000

$34,

000

Lin

e #

67

© Practising Law Institute

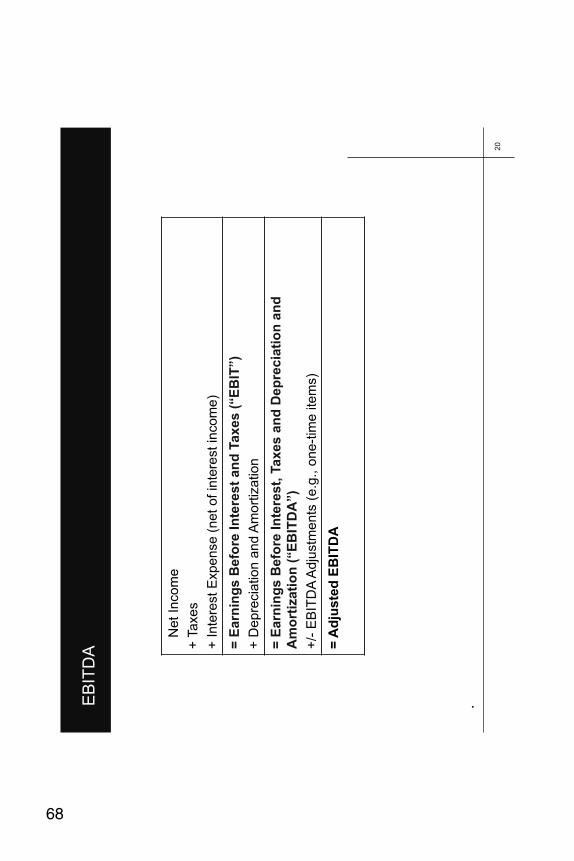

EB

ITD

A

20

N

et

Incom

e

+ T

axe

s

+ Inte

rest

Expense (

net

of

inte

rest

incom

e)

= E

arn

ing

s B

efo

re In

tere

st

an

d T

axes (

“E

BIT

”)

+ D

epre

cia

tion a

nd A

mort

ization

= E

arn

ing

s B

efo

re In

tere

st,

Taxes a

nd

Dep

recia

tio

n a

nd

Am

ort

izati

on

(“E

BIT

DA

”)

+/-

EB

ITD

A A

dju

stm

ents

(e.g

., o

ne-t

ime ite

ms)

= A

dju

ste

d E

BIT

DA

68

© Practising Law Institute

Ke

y R

atio

s –

In

co

me

Sta

tem

en

t

21

Prof

itab

ility

IDVa

lue

Rati

o

20X9

20X9

Gro

ss m

arg

in=

Net

Sale

sC

176

5,00

0-

Cost

of G

oods S

old

C2

535,

000

=C

323

0,00

023

0,00

0

(see a

bove

)$2

30,0

00C

176

5,00

0

EB

IT=

Net

Incom

eC

10

50,0

00+

Incom

e T

axes

C9

34,0

00+

Inte

rest

Expense

C7

17,0

00E

BIT

=E

arn

ings (

i.e,

Net

Incom

e)

befo

re Inte

rest

and T

axes

101,

000

(see a

bove

)10

1,00

0C

176

5,00

0

EB

ITD

A=

Net

Incom

eC

10

50,0

00+

Incom

e T

axes

C9

34,0

00+

Inte

rest

Expense

C7

17,0

00+

Depre

cia

tion a

nd A

mort

ization

C4

29,0

00

EB

ITD

A=

130,

000

130,

000

(see a

bove

)13

0,00

0C

176

5,00

0

C10

50,0

00C

176

5,00

0

C10

50,0

00B

14

293,

500

C10

50,0

00A

16

617,

500

C1

765,

000

A16

617,

500

Net

Sale

s

=N

et

Incom

e17

%A

vera

ge T

ota

l E

quity

Earn

ings (

i.e.,

Net

Incom

e)

befo

re Inte

rest,

Taxes,

Depre

cia

tion,

and A

mort

ization

EB

ITD

A M

arg

in=

EB

ITD

A17

%

Retu

rn o

n e

quity

Retu

rn o

n a

ssets

=N

et

Incom

e8%

Ave

rage T

ota

l A

ssets

Gro

ss M

arg

in

Gro

ss m

arg

in (

%)

=G

ross M

arg

in30

%N

et

Sale

s

Asset

turn

ove

r=

Net

Sale

s1.

2xA

vera

ge T

ota

l A

ssets

Retu

rn o

n s

ale

s=

Net

Incom

e7%

Net

Sale

s

Net

Sale

s

EB

IT M

arg

in=

EB

IT13

%

and A

mort

ization

Lin

e #

69

© Practising Law Institute

Sam

ple

Incom

e S

tate

ment

22

CON

SOLI

DA

TED

INCO

ME

STA

TEM

ENTS

- A

BC In

c.(D

olla

rs in

Tho

usan

ds)

20X9

20X8

ID C1N

et s

ales

(or r

even

ues)

$765

,000

$725

,000

The

amou

nt o

f sal

es g

ener

ated

by

a co

mpa

ny a

fter

the

dedu

ctio

n of

retu

rns,

allo

wan

ces

for d

amag

ed o

r mis

sing

goo

ds a

nd a

ny d

isco

unts

allo

wed

. The

sal

es n

umbe

r rep

orte

d on

a

com

pany

's fi

nanc

ial s

tate

men

ts is

a n

et s

ales

num

ber,

refl

ecti

ng th

ese

dedu

ctio

ns.

C2Co

st o

f goo

ds s

old

535,

000

517,

000

Cost

of s

ales

is th

e am

ount

of m

oney

its

cost

s to

pro

duce

the

good

s or

pro

duct

s of

a

com

pany

. It i

s al

so c

alle

d co

st o

f goo

ds s

old.

The

se c

osts

incl

ude

the

mat

eria

ls a

nd la

bor

need

ed to

pro

duce

the

good

s.C3

Gro

ss m

argi

n$2

30,0

00$2

08,0

00A

com

pany

's to

tal s

ales

reve

nue

min

us it

s co

st o

f goo

ds s

old.

Ope

rati

ng e

xpen

ses:

C4D

epre

ciat

ion

and

amor

tiza

tion

$29,

000

$25,

000

A re

duct

ion

in a

cap

ital

acc

ount

of t

he v

alue

of a

n as

set o

ver t

ime.

C5Se

lling

, gen

eral

and

adm

inis

trat

ive

expe

nses

100,

000

109,

000

The

sum

or a

ll di

rect

and

indi

rect

sel

ling

expe

nses

and

all

gene

ral a

nd a

dmin

istr

ativ

e ex

pens

es o

f a c

ompa

ny.

Dir

ect s

ellin

g ex

pens

es a

re e

xpen

ses

that

can

be

dire

ctly

link

ed

to th

e sa

le o

f a s

peci

fic

unit

suc

h as

cre

dit,

war

rant

y an

d ad

vert

isin

g ex

pens

es. I

ndir

ect

selli

ng e

xpen

ses

are

expe

nses

whi

ch c

anno

t be

dire

ctly

link

ed to

the

sale

of a

spe

cifi

c un

it, b

ut w

hich

are

pro

port

iona

lly a

lloca

ted

to a

ll un

its

sold

dur

ing

a ce

rtai

n pe

riod

, suc

h as

tele

phon

e an

d po

stal

cha

rges

. Gen

eral

and

adm

inis

trat

ive

expe

nses

incl

ude

sala

ries

of

non

-sal

es p

erso

nnel

, ren

t, h

eat a

nd li

ghts

.

C6O

pera

ting

inco

me

$101

,000

$74,

000

Oth

er in

com

e (e

xpen

se):

C7In

tere

st e

xpen

se($

17,0

00)

($17

,000

)Re

ad m

ore:

htt

p://

ww

w.in

vest

oped

ia.c

om/t

erm

s/s/

sga.

asp#

ixzz

1eYi

1TjV

xC8

Inco

me

befo

re in

com

e ta

xes

$84,

000

$57,

000

C9In

com

e ta

xes

$34,

000

$23,

000

A ta

x th

at g

over

nmen

ts im

pose

on

fina

ncia

l inc

ome

gene

rate

d by

all

enti

ties

wit

hin

thei

r ju

risd

icti

on. B

y la

w, b

usin

esse

s an

d in

divi

dual

s m

ust f

ile a

n in

com

e ta

x re

turn

eve

ry y

ear

to d

eter

min

e w

heth

er th

ey o

we

any

taxe

s or

are

elig

ible

for a

tax

refu

nd. I

ncom

e ta

x is

a

key

sour

ce o

f fun

ds th

at th

e go

vern

men

t use

s to

fund

its

acti

viti

es a

nd s

erve

the

publ

ic.

C10

Net

inco

me

$50,

000

$34,

000

Aco

mpa

ny's

tota

lea

rnin

gs(o

rpr

ofit

).N

etin

com

eis

cal

cula

ted

byta

king

reve

nues

and

adju

stin

gfo

rth

eco

stof

doin

gbu

sine

ss,

depr

ecia

tion

,in

tere

st,

taxe

san

dot

her

expe

nses

.Thi

snu

mbe

ris

foun

don

aco

mpa

ny's

inco

me

stat

emen

tan

dis

anim

port

ant

mea

sure

ofho

wpr

ofit

able

the

com

pany

isov

era

peri

odof

tim

e.Th

ism

easu

reis

also

used

to c

alcu

late

ear

ning

s pe

r sha

re.

Lin

e #

70

© Practising Law Institute

Ke

y R

atio

s –

In

co

me

Sta

tem

en

t

23

Inco

me

Stat

emen

t So

lven

cy R

atio

sID

Valu

eRa

tio

C6

101,

000

C7

17,0

00

(see a

bove

)13

0,00

0C

717

,000

(see a

bove

)95

,000

C7

17,0

00

(see a

bove

)18

7,00

0(s

ee a

bove

)13

0,00

0

Net

Debt

=Tota

l D

ebt

(see a

bove

)18

7,00

0-

Cash a

nd C

ash E

quiv

ale

nts

A1

25,0

00=

Net

Debt

162,

000

162,

000

(see a

bove

)16

2,00

0(s

ee a

bove

)13

0,00

0

EB

ITD

A/Inte

rest

=E

BIT

DA

7.6

Inte

rest

EB

IT/Inte

rest

=E

BIT

5.9

Inte

rest

EB

ITD

A

Net

Debt/

EB

ITD

A=

Net

Debt

1.2

EB

ITD

A

(EB

ITD

A -

CA

PE

X)/

Inte

rest

Expense

=E

BIT

DA

- C

AP

EX

5.6

Inte

rest

Expense

Tota

l D

ebt/

EB

ITD

A=

Tota

l D

ebt

1.4

Lin

e #

71

© Practising Law Institute

Ke

y R

atio

s –

In

co

me

Sta

tem

en

t

24

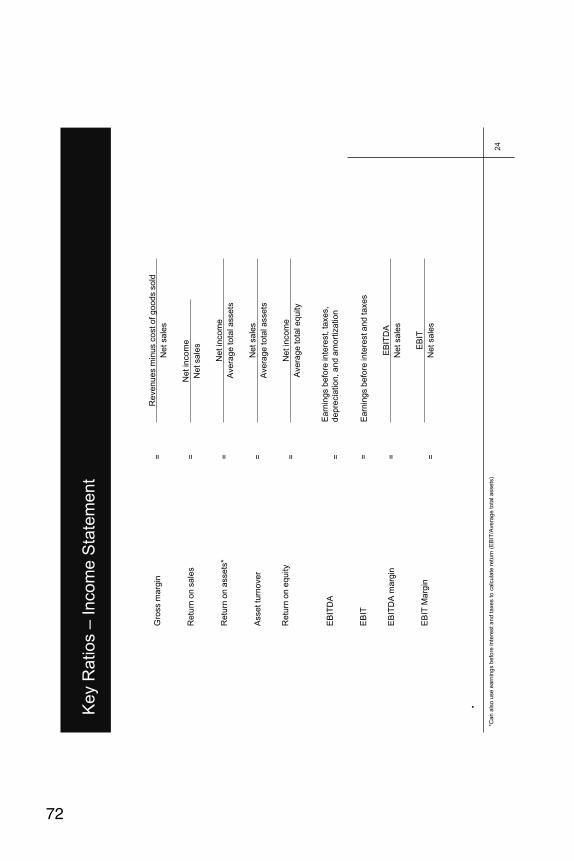

Gro

ss m

arg

in

=

Re

venues m

inus c

ost of goods s

old

Ne

t sa

les

Re

turn

on

sa

les

=

Ne

t in

co

me

Ne

t sa

les

Re

turn

on

asse

ts*

=

Ne

t in

co

me

Avera

ge tota

l assets

Asse

t tu

rno

ve

r =

N

et sa

les

Avera

ge tota

l assets

Re

turn

on

eq

uity

=

Ne

t in

co

me

Avera

ge tota

l equity

EB

ITD

A

=

Earn

ings b

efo

re inte

rest, taxes,

depre

cia

tion, and a

mort

ization

EB

IT

=

Ea

rnin

gs b

efo

re in

tere

st a

nd

ta

xe

s

EB

ITD

A m

arg

in

=

EB

ITD

A

Ne

t sa

les

EB

IT M

arg

in

=

EB

IT

Ne

t sa

les

*Ca

n a

lso

use

ea

rnin

gs b

efo

re in

tere

st a

nd

ta

xe

s t

o c

alc

ula

te r

etu

rn (

EB

IT/A

ve

rag

e to

tal a

sse

ts)

72

© Practising Law Institute

Ke

y R

atio

s –

In

co

me

Sta

tem

en

t

25

EB

IT/Inte

rest

=

EB

IT

Inte

rest

EB

ITD

A/Inte

rest

=

EB

ITD

A

Inte

rest

(EB

ITD

A -

CA

PE

X)/

Inte

rest E

xpense

=

EB

ITD

A -

CA

PE

X

Inte

rest E

xpense

To

tal D

eb

t/E

BIT

DA

=

T

ota

l d

eb

t

EB

ITD

A

Ne

t D

ebt/E

BIT

DA

=

T

ota

l d

eb

t m

inu

s c

ash

EB

ITD

A

73

© Practising Law Institute

Cash F

low

Sta

tem

ent

26

74

© Practising Law Institute

Ca

sh

Flo

w S

tate

me

nt

27

Cash

flo

w S

tate

men

t --

Th

e fin

an

cia

l sta

tem

en

t th

at sh

ow

s th

e c

ash

in

flo

ws

an

d c

ash

ou

tflo

ws fo

r th

e p

erio

d o

f tim

e c

ove

red

by th

e in

co

me

sta

tem

en

t.

Th

ree

se

ctio

ns o

f a

ca

sh

flo

w s

tate

me

nt:

•O

pera

tin

g -

- re

concile

s the n

et

incom

e t

o t

he a

ctu

al cash the c

om

pany

receiv

ed fro

m o

r used in its

opera

ting a

ctivitie

s. A

dju

sts

net

incom

e f

or

any

non-c

ash ite

ms (

such a

s a

ddin

g b

ack d

epre

cia

tion e

xpenses)

and a

dju

sts

for

any c

ash that

was u

sed o

r pro

vid

ed b

y o

ther

opera

ting a

ssets

and

liabili

ties.

•In

vesti

ng

--

The s

econd p

art

of

a c

ash f

low

sta

tem

ent

show

s the c

ash

flow

fro

m a

ll in

vesting a

ctivitie

s, w

hic

h g

enera

lly inclu

de p

urc

hases o

r

sale

s o

f lo

ng-t

erm

assets

, such a

s p

ropert

y, p

lant

and e

quip

ment, a

s w

ell

as investm

ent

securities.

•F

inan

cin

g -

- T

he third p

art

of

a c

ash flo

w s

tate

ment

show

s the c

ash flo

w

from

all

financin

g a

ctivitie

s. Typic

al sourc

es o

f cash flo

w inclu

de c

ash

rais

ed b

y s

elli

ng s

tocks a

nd b

onds o

r borr

ow

ing fro

m b

anks. Lik

ew

ise,

payin

g b

ack a

bank loan w

ould

show

up a

s a

use o

f cash flo

w.

75

© Practising Law Institute

Sa

mp

le C

ash

Flo

w S

tate

me

nt

28

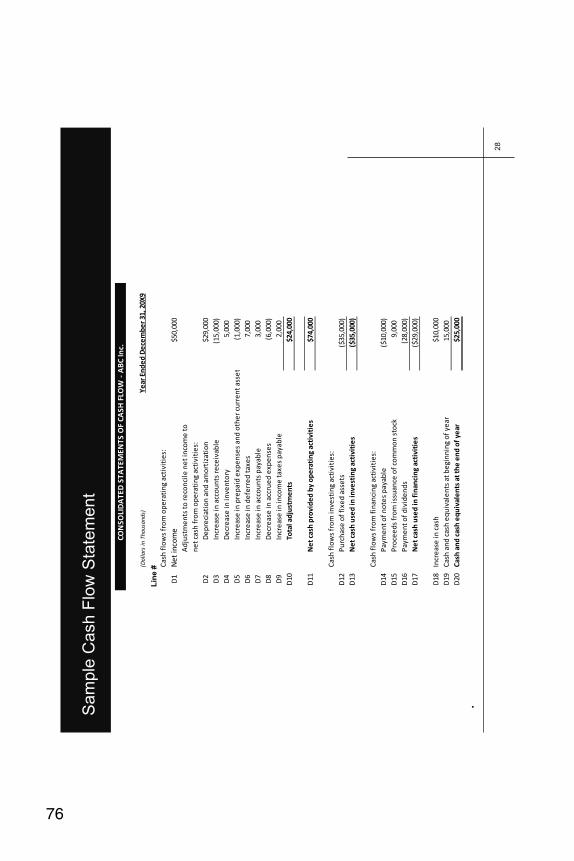

CON

SOLI

DA

TED

STA

TEM

ENTS

OF

CASH

FLO

W -

ABC

Inc.

(Dol

lars

in T

hous

ands

)Ye

ar E

nded

Dec

embe

r 31,

20X

9ID

Cash

flow

s fr

om o

pera

ting

act

ivit

ies:

D1

Net

inco

me

$50,

000

Adj

ustm

ents

to re

conc

ile n

et in

com

e to

net c

ash

from

ope

rati

ng a

ctiv

itie

s:D

2D

epre

ciat

ion

and

amor

tiza

tion

$29,

000

D3

Incr

ease

in a

ccou

nts

rece

ivab

le(1

5,00

0)D

4D

ecre

ase

in in

vent

ory

5,00

0D

5In

crea

se in

pre

paid

exp

ense

s an

d ot

her c

urre

nt a

sset

(1,0

00)

D6

Incr

ease

in d

efer

red

taxe

s7,

000

D7

Incr

ease

in a

ccou

nts

paya

ble

3,00

0D

8D

ecre

ase

in a

ccru

ed e

xpen

ses

(6,0

00)

D9

Incr

ease

in in

com

e ta

xes

paya

ble

2,00

0D

10To

tal a

djus

tmen

ts$2

4,00

0

D11

Net

cas

h pr

ovid

ed b

y op

erat

ing

acti

viti

es$7

4,00

0

Cash

flow

s fr

om in

vest

ing

acti

viti

es:

D12

Purc

hase

of f

ixed

ass

ets

($35

,000

)D

13N

et c

ash

used

in in

vest

ing

acti

viti

es($

35,0

00)

Cash

flow

s fr

om fi

nanc

ing

acti

viti

es:

D14

Paym

ent o

f not

es p

ayab

le($

10,0

00)

D15

Proc

eeds

from

issu

ance

of c

omm

on s

tock

9,00

0D

16Pa

ymen

t of d

ivid

ends

(28,

000)

D17

Net

cas

h us

ed in

fina

ncin

g ac

tivi

ties

($29

,000

)

D18

Incr

ease

in c

ash

$10,

000

D19

Cash

and

cas

h eq

uiva

lent

s at

beg

inni

ng o

f yea

r15

,000

D20

Cash

and

cas

h eq

uiva

lent

s at

the

end

of y

ear

$25,

000

Lin

e #

76

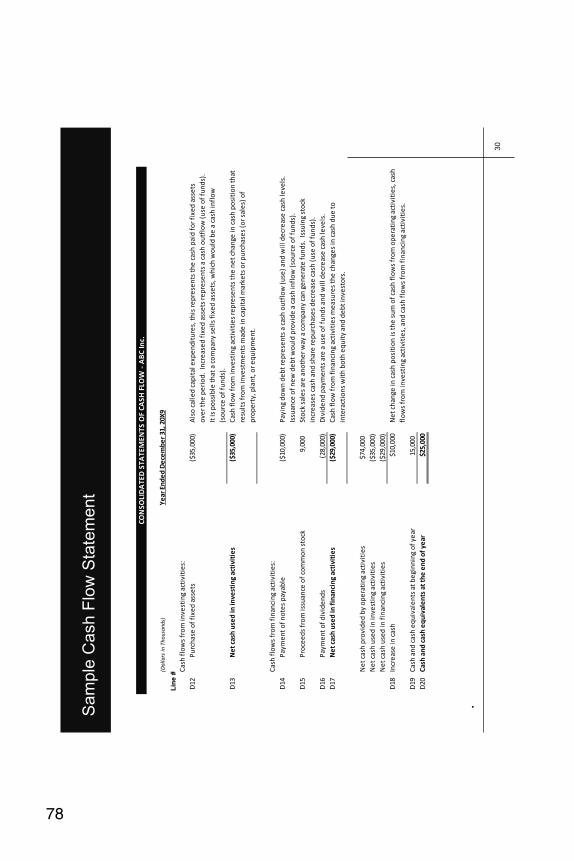

© Practising Law Institute

Sa

mp

le C

ash

Flo

w S

tate

me

nt

29

CON

SOLI

DA

TED

STA

TEM

ENTS

OF

CASH

FLO

W -

ABC

Inc.

(Dol

lars

in T

hous

ands

)Ye

ar E

nded

Dec

embe

r 31,

20X

9ID

Cash

flow

s fr

om o

pera

ting

act

ivit

ies:

D1

Net

inco

me

$50,

000

Adj

ustm

ents

to re

conc

ile n

et in

com

e to

net c

ash

from

ope

rati

ng a

ctiv

itie

s:D

2D

epre

ciat

ion

and

amor

tiza

tion

$29,

000

Add

ed b

ack

as a

non

-cas

h ch

arge

that

was

pre

viou

sly

dedu

cted

to a

rriv

e at

net

in

com

e.D

3In

crea

se in

acc

ount

s re

ceiv

able

(15,

000)

An

incr

ease

(dec

reas

e) in

rece

ivab

les

repr

esen

ts a

use

(sou

rce)

of f

unds

. A

use

of

fund

s is

a c

ash

outf

low

.D

4D

ecre

ase

in in

vent

ory

5,00

0A

n de

crea

se (i

ncre

ase)

in in

vent

ory

repr

esen

ts a

sou

rce

(use

) of f

unds

. A

sou

rce

of fu

nds

is a

cas

h in

flow

.D

5In

crea

se in

pre

paid

exp

ense

s an

d ot

her c

urre

nt a

sset

(1,0

00)

An

incr

ease

(dec

reas

e) in

pre

paid

exp

ense

s or

oth

er c

urre

nt a

sset

s re

pres

ents

a

use

(sou

rce)

of f

unds

. A

use

of f

unds

is a

cas

h ou

tflo

w.

D6

Incr

ease

in d

efer

red

taxe

s7,

000

An

incr

ease

in a

liab

ility

is s

ourc

e of

fund

s an

d re

pres

ents

a c

ash

infl

ow.

By

defe

rrin

g ta

xes,

ABC

will

hav

e ad

diti

onal

fund

s av

aila

ble

for u

se in

ope

rati

ons.

D7

Incr

ease

in a

ccou

nts

paya

ble

3,00

0A

n in

crea

se (d

ecre

ase)

in p

ayab

les

repr

esen

ts a

sou

rce

(use

) of f

unds

. In

crea

ses

in p

ayab

les

may

resu

lt fr

om m

ore

flex

ible

pay

men

t ter

ms

from

ven

dors

and

is a

ca

sh in

flow

(mor

e fu

nds

avai

labl

e fo

r use

in o

pera

tion

s).

D8

Dec

reas

e in

acc

rued

exp

ense

s(6

,000

)A

n de

crea

se (i

ncre

ase)

in e

xpen

ses

accr

ued

is a

use

(sou

rce)

of f

unds

. Pa

ying

off

ex

pens

es is

a c

ash

outf

low

.D

9In

crea

se in

inco

me

taxe

s pa

yabl

e2,

000

Sim

ilar t

o ac

coun

ts p

ayab

le (a

bove

), a

nd in

crea

se in

a p

ayab

le is

a s

ourc

e of

fund

s an

d a

cash

infl

ow.

D10

Tota

l adj

ustm

ents

$24,

000

D11

Net

cas

h pr

ovid

ed b

y op

erat

ing

acti

viti

es$7

4,00

0O

pera

ting

cas

h fl

ow is

the

cash

gen

erat

ed b

y ru

nnin

g th

e bu

sine

ss.

Man

y an

alys

t co

nsid

er c

ash

flow

from

ope

rati

ons

a go

od p

rofi

tabi

lity

mea

sure

as

it is

in

depe

nden

t of i

nves

ting

and

fina

ncin

g de

cisi

ons.

Lin

e #

77

© Practising Law Institute

Sa

mp

le C

ash

Flo

w S

tate

me

nt

30

CON

SOLI

DA

TED

STA

TEM

ENTS

OF

CASH

FLO

W -

ABC

Inc.

(Dol

lars

in T

hous

ands

)Ye

ar E

nded

Dec

embe

r 31,

20X

9ID

Cash

flow

s fr

om in

vest

ing

acti

viti

es:

D12

Purc

hase

of f

ixed

ass

ets

($35

,000

)A

lso

calle

d ca

pita

l exp

endi

ture

s, th

is re

pres

ents

the

cash

pai

d fo

r fix

ed a

sset

s ov

er th

e pe

riod

. In

crea

sed

fixe

d as

sets

repr

esen

ts a

cas

h ou

tflo

w (u

se o

f fun

ds).

It

is p

ossi

ble

that

a c

ompa

ny s

ells

fixe

d as

sets

, whi

ch w

ould

be

a ca

sh in

flow

(s

ourc

e of

fund

s).

D13

Net

cas

h us

ed in

inve

stin

g ac

tivi

ties

($35

,000

)Ca

sh fl

ow fr

om in

vest

ing

acti

viti

es re

pres

ents

the

net c

hang

e in

cas

h po

siti

on th

at

resu

lts

from

inve

stm

ents

mad

e in

cap

ital

mar

kets

or p

urch

ases

(or s

ales

) of

prop

erty

, pla

nt, o

r equ

ipm

ent.

Cash

flow

s fr

om fi

nanc

ing

acti

viti

es:

D14

Paym

ent o

f not

es p

ayab

le($

10,0

00)

Payi

ng d

own

debt

repr

esen

ts a

cas

h ou

tflo

w (u

se) a

nd w

ill d

ecre

ase

cash

leve

ls.

Issu

ance

of n

ew d

ebt w

ould

pro

vide

a c

ash

infl

ow (s

ourc

e of

fund

s).

D15

Proc

eeds

from

issu

ance

of c

omm

on s

tock

9,00

0St

ock

sale

s ar

e an

othe

r way

a c

ompa

ny c

an g

ener

ate

fund

s. I

ssui

ng s

tock

in

crea

ses

cash

and

sha

re re

purc

hase

s de

crea

se c

ash

(use

of f

unds

).D

16Pa

ymen

t of d

ivid

ends

(28,

000)

Div

iden

d pa

ymen

ts a

re a

use

of f

unds

and

will

dec

reas

e ca

sh le

vels

.D

17N

et c

ash

used

in fi

nanc

ing

acti

viti

es($

29,0

00)

Cash

flow

from

fina

ncin

g ac

tivi

ties

mea

sure

s th

e ch

ange

s in

cas

h du

e to

in

tera

ctio

ns w

ith

both

equ

ity

and

debt

inve

stor

s.

Net

cas

h pr

ovid

ed b

y op

erat

ing

acti

viti

es$7

4,00

0N

et c

ash

used

in in

vest

ing

acti

viti

es($

35,0

00)

Net

cas

h us

ed in

fina

ncin

g ac

tivi

ties

($29

,000

)D

18In

crea

se in

cas

h$1

0,00

0N

et c

hang

e in

cas

h po

siti

on is

the

sum

of c

ash

flow

s fr

om o

pera

ting

act

ivit

ies,

cas

h fl

ows

from

inve

stin

g ac

tivi

ties

, and

cas

h fl

ows

from

fina

ncin

g ac

tivi

ties

.D

19Ca

sh a

nd c

ash

equi

vale

nts

at b

egin

ning

of y

ear

15,0

00D

20Ca

sh a

nd c

ash

equi

vale

nts

at th

e en

d of

yea

r$2

5,00

0

Lin

e #

78

© Practising Law Institute

Ke

y R

atio

s –

Ca

sh

Flo

w S

tate

me

nt

31

Cash

Flo

w R

atio

sID

Valu

eRa

tio

D11

74,0

00(s

ee a

bove

)18

7,00

0

Cash F

low

fro

m O

pera

tions -

CA

PE

X=

Net

Cash p

rovi

ded b

y O

pera

ting A

ctivi

ties

D11

74,0

00(F

ree C

ash F

low

s)

-P

urc

hase o

f F

ixed A

ssets

D12

35,0

00=

Fre

e C

ash F

low

s39

,000

39,0

00

EB

ITD

A -

CA

PE

X=

EB

ITD

A(s

ee a

bove

)13

0,00

0-

Purc

hase o

f F

ixed A

ssets

D12

35,0

00=

EB

ITD

A -

CA

PE

X95

,000

95,0

00

D11

74,0

00D

12

35,0

00

D12

35,0

00(s

ee a

bove

)13

0,00

0

D12

35,0

00A

11

385,

000

CA

PE

X/G

ross P

PE

=P

urc

hase o

f F

ixed A

ssets

0.1

Tota

l P

ropert

y,

Pla

nt

and E

quip

ment

CA

PE

X/E

BIT

DA

=P

urc

hase o

f F

ixed A

ssets

0.3

EB

ITD

A

CA

PE

X C

ove

rage

=N

et

Cash p

rovi

ded b

y O

pera

ting A

ctivi

ties

2.1

Purc

hase o

f F

ixed A

ssets

Tota

l D

ebt

Cove

rage

=N

et

Cash p

rovi

ded b

y O

pera

ting A

ctivi

ties

0.4

Tota

l D

ebt

Ave

rag

e o

f T

ota

l P

rop

ert

y,

Pla

nt

an

d E

qu

ipm

en

t 3

67

,50

0

Lin

e #

79

© Practising Law Institute

Ke

y R

atio

s –

Ca

sh

Flo

w S

tate

me

nt

32

To

tal D

eb

t C

ove

rage