isi investor slides feb 18, 2013 final wo...

TRANSCRIPT

OSK Investor Slides March 2013

Oshkosh Corporation ISI Industrial Conference

March 2013

OSK Investor Slides March 2013

Forward-Looking Statements

2

This presentation includes statements that the Company believes to be “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact, including, withoutlimitation, statements regarding the Company’s future financial position, business strategy, targets, projected sales, costs,earnings, capital expenditures, debt levels and cash flows, and plans and objectives of management for future operations, areforward-looking statements. When used in this presentation, words such as “may,” “will,” “expect,” “intend,” “estimate,” “anticipate,” “believe,” “should,” “project” or “plan” or the negative thereof or variations thereon or similar terminology are generally intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance and are subject to risks, uncertainties, assumptions and other factors, some of which are beyond the Company’s control, which could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These factors include the cyclical nature of the Company’s access equipment, commercial and fire & emergency markets, especially in the current environment where there are conflicting signs regarding the global economic outlook and the ability of the U.S. government to resolve budgetary and debt issues; the expected level and timing of the U.S. DoD procurement of products and services and funding thereof including the impact of sequestration; risks related to reductions in government expenditures in light of U.S. defense budget pressures and an uncertain DoD tactical wheeled vehicle strategy; the ability to comply with laws and regulations applicable to U.S. government contractors; the ability to increase prices to raise margins or offset higher input costs; increasing commodity and other raw material costs, particularly in a sustained economicrecovery; risks related to the Company’s exit from its ambulance business, including the amounts of related costs and charges; risks related to facilities consolidation and alignment, including the amounts of related costs and charges and that anticipatedcost savings may not be achieved; the duration of the ongoing global economic weakness, which could lead to additional impairment charges related to many of the Company’s intangible assets and/or a slower recovery in the Company’s cyclical businesses than Company or equity market expectations; the potential for the U.S. government to competitively bid the Company’s Army and Marine Corps contracts; risks related to the collectability of receivables, particularly for those businesseswith exposure to construction markets; the cost of any warranty campaigns related to the Company’s products; risks related toproduction or shipment delays arising from quality or production issues; risks associated with international operations and sales, including foreign currency fluctuations and compliance with the Foreign Corrupt Practices Act; risks related to actions of activist shareholders; and risks related to the Company’s ability to successfully execute on its strategic road map and meet its long-term financial goals. Additional information concerning these and other factors is contained in the Company’s filings with the Securities and Exchange Commission, including the Form 8-K filed January 25, 2013. All forward-looking statements speak only as of January 25, 2013. The Company assumes no obligation, and disclaims any obligation, to update information contained in this presentation. Investors should be aware that the Company may not update such information until the Company’s next quarterly earnings conference call, if at all.

OSK Investor Slides March 2013

Framing the Opportunity

OSK Investor Slides March 2013

Oshkosh Corporation

• Incorporated in 1917

• Listed on NYSE (Ticker: OSK)

• Employees: 13,200

• FY12 Revenue: $8.18 billion

• FY12 Adjusted EPS (1): $2.27

• Market Capitalization (2): $3.4 billion

• 12/31/2012 Net Debt (3): $499 million

(1) Non-GAAP results. See Appendix for reconciliation to GAAP results.(2) As of February 27, 2013.(3) Net debt is total debt less cash. Source Oshkosh Form 10-Q: January 25, 2013

4

OSK Investor Slides March 2013

Moving the World at Work

• Our vehicles move people and materials at work– Most protect people or property– Many lift people or property– All do so safely and efficiently

• Often share common customers/ distribution channels– JLG, Jerr-Dan, IMT, McNeilus and Pierce sell

into rental channel– Every segment sells to the U.S.

federal government• Share common components/suppliers,

technologies and manufacturing processes• Scale is important to be competitive

5

OSK Investor Slides March 2013

Poised to Deliver Results

• MOVE strategy expected to deliver higher margins throughout cycle• Market recovery from deep cycle has commenced

– Expected to overcome defense downturn • Oshkosh processes and team support execution of MOVE

FY12 FY15E

Industry Leading Brands (1)

Access Equipment #1 Global

Fire Apparatus #1 Global

Airport Products #1 Global

Defense TWV (2) #1 Global

Concrete Mixers #1 Americas

Refuse Collection #1 Americas

6

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

(1) Based on Company estimates.(2) Oshkosh Defense is the leading supplier of heavy and medium tactical

wheeled vehicles for the U.S. Armed Services.

OSK Investor Slides March 2013

MOVE – The Right Strategy

• Focuses on drivers that create highest shareholder value• Recognizes constraints of markets, balance sheet and

business valuations• Expected to drive higher incremental margins across non-Defense

businesses over cycle

7

OSK Investor Slides March 2013

Leveraging a Common Structure: Oshkosh Operating System

• Customer-centric application of lean principles– Sets guiding principles for

relationships with customers

• Improves processes needed todeliver key elements of MOVE

• Supports drive to improve cash flow

• Implementation gaining momentum

• Company-wide foundation for building shareholder value

8

OSK Investor Slides March 2013

MOVE Delivered in FY12

9

Oshkosh Corporation

Full Year

Revenue $8.18BAdjusted Operating Income* $402M

Adjusted Operating Income Margin* 4.9%Adjusted EPS* $2.27Total Debt $955MNet Debt(Total debt less cash) $414M

• Achieved Adjusted EPS* of $2.27– September 14, 2012 Analyst Day

estimate range: $2.05 - $2.15– Raised expectations several times

throughout the year

• Generated $215 million offree cash flow*

• International sales increased to 22% in FY12 from 17% in FY11

• Significant wins for Defense– 750 M-ATVs for U.A.E.– JLTV engineering and manufacturing

development contract award

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

OSK Investor Slides March 2013

Building Momentum:Q1 FY13 Results

• Adjusted EPS* of $0.60– Results exceeded

expectations• Margins expanded in all non-

defense segments– Exceeded expectations in

defense• Generated $39 million in free

cash flow*• Repurchased 4.25 million

shares• Increased FY13 Adjusted

EPS* estimates to a range of $2.80 to $3.05

Net

Sal

es(m

illio

ns)

Adjusted EPS*

OSK Fiscal Q1 Performance

$1,761 $1,876

$0.60

$0.39

$0.00

$0.25

$0.50

$0.75

$1.00

$0

$500

$1,000

$1,500

$2,000

$2,500

FY13 FY12Net Sales EPS

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

10

OSK Investor Slides March 2013

MOVE Highlights

OSK Investor Slides March 2013

Market Recovery and Growth

12

~$220M(2)

Opportunity(FY12-FY15)

FY11 FY15EFY12

~10% CAGR(FY12-FY15)

FY11 FY15EFY12

Non-Defense Operating Income (1) ($ in Millions)

(1) Reflects estimated benefits of market recovery captured in financial estimates. Does not include benefits of other MOVE initiatives. Market recovery operating income growth opportunity from FY11 to prior peak sales levels for non-Defense segments estimated at ~$500 million.

(2) Based on September 14, 2012 Analyst Day estimate for FY12 non-Defense segments operating income, which excluded costs to exit ambulance and European mobile medical businesses.

OSK Investor Slides March 2013

Optimize Cost and Capital Structure

0

50

100

150

200

250

FY12 FY13E FY14E FY15E

8 bps

~75 bps

~130 bps

~250 bps

Targeted Operating Income Margin Impact(Basis Points Operating Income/Sales)

• Targeted margin improvements driven by reductions in product, process and overhead costs

13

OSK Investor Slides March 2013

Value InnovationDriving ~$350 million incremental annual revenue by FY15

(1)

• Disciplined, resourced execution of multi-generational product and technology plans in all segments

• Integrated project teams charged with improving product launch processes and adherence to project KPIs

• Customer First focus driving all innovation

14

(Mill

ions

of D

olla

rs)

(1) Compared with FY12

OSK Investor Slides March 2013

Emerging Market ExpansionTargeting > 25% of revenues by FY15 (30% by FY16)

• Expanding sales, service and manufacturing operations • Forward deploying business development professionals for Defense• Developing products for global markets• Leveraging international facilities across segments

15

17%

~20%>25%

Sales Outside the U.S.

~10%-15% CAGR (FY12-FY15)

FY11 FY15EFY12(1)

(Per

cent

of R

even

ue)

(1) Based on September 14, 2012 Analyst Day estimate.

OSK Investor Slides March 2013

Business Outlook

OSK Investor Slides March 2013

The Access Equipment Advantage

17

JLG is positioned for sustained industry leading performance

Global Leader in Access Equipment

Industry Leading

Innovation

Superior Product Range

Full Spectrum Parts, Service, and Support

Flexible Manufacturing

and Supply Chain

Global Market Presence

OSK Investor Slides March 2013

North American Rental Companies are Refreshing Their Fleets, Increasing Market Penetration

18

Total Construction Spending(Y-O-Y % Change)

NA Rental Equipment Access - Fleet Age(AWP and TMH)

NA Rental Equipment Company Fleet Utilization

‐20

‐10

0

10

20

2006 2007 2008 2009 2010 2011 2012E 2013E 2014E 2015EUnited States Canada

NA Rental Equipment Company CapEx (Y-O-Y % Change)

Source: IHS Global data/projections

Based on International Rental News/Dan Kaplan sample of medium to large NA rental equipment companies (United Rental, RSC, H&E, HERC).

‐90

‐60

‐30

0

30

60

90

120

150

2004 2005 2006 2007 2008 2009 2010 2011

CapEx

Based on International Rental News/Dan Kaplan sample of medium to large NA rental equipment companies (United Rental, RSC, H&E, HERC).

(% C

hang

e)(%

Tim

e U

tiliz

atio

n)

(% C

hang

e)

50

55

60

65

70

75

1Q'10 2Q'10 3Q'10 4Q'10 1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12 3Q'12

Ind. Avg.

40

45

50

55

60

2009 2010 2011 2012

(AgeinMonths)

Age(months)

Source: Rouse Rental Report. Calendar year-end data for 2009-11 and January 2013.

OSK Investor Slides March 2013

Positive North America Leading Indicators

19

Source: Rouse Asset Services, February 2013.

AWP – Articulating Boom 52.1

Average Age(in months)

Used Equipment Value Trends(OLV)

U.S. Housing Starts

Seasonally Adjusted Rate 2013 2012 Change

January 890,000 720,000 +23.6%Source: U.S. Census Bureau, February 2013.

AWP – Scissor Lifts 57.2

AWP – Telescopic Boom 55.6

39.7% 39.4%

35.0

40.0

45.0

Jul Aug Sep Oct Nov Dec Jan

OLV

(% o

f Cos

t

38.4%39.5%

35

37

39

Jul Aug Sep Oct Nov Dec JanOLV

(% o

f Cos

t

30.9% 30.4%30

32.5

35

Jul Aug Sep Oct Nov Dec JanOLV

(% o

f Cos

t

OSK Investor Slides March 2013

Mixed International Markets

20

• Europe– Agriculture providing growth– Strength in eastern and Nordic

markets– Continued softness in western and

southern Europe• Emerging areas of opportunity

– Rental concept advancing in Brazil& Russia; lagging in China

– Latin American infrastructure driving near term demand

– Energy, mining and agriculture attractive for long-term

• Australia Robust market Delayed projects impacting

2013 demand

OSK Investor Slides March 2013

The Oshkosh Defense Advantage

21

Defense Engineering & Product

Development

Scalable Manufacturing & Operations

Vertical Integration of Specialized

Components

Defense Program

Management

Vehicle Fleet Modernization

Service, Lifecycle

Sustainment

Defense industry expertise that leverages thefull capabilities of Oshkosh Corporation

OSK Investor Slides March 2013

Adapting to the Domestic Defense Spending Downturn

22

Current Operations Profile

New Vehicle Production Aftermarket &

Modernization

Tech & Product Development

Future Operations Profile

New Vehicle Production

Aftermarket & Modernization

Tech & Product Development

HEAVY, MEDIUM & MRAP VEHICLES MEDIUM, MRAP & LIGHT VEHICLES

– Compete to win in Light vehicle segment– Optimize our cost structure

OSK Investor Slides March 2013

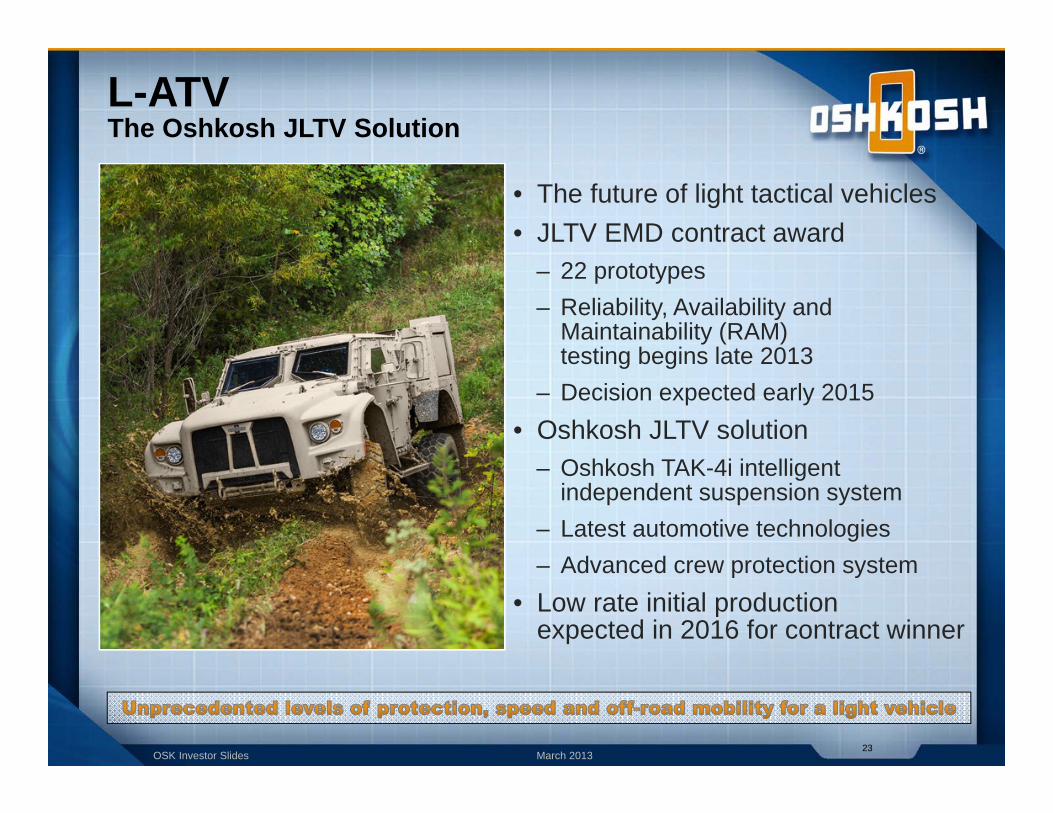

L-ATVThe Oshkosh JLTV Solution

• The future of light tactical vehicles• JLTV EMD contract award

– 22 prototypes– Reliability, Availability and

Maintainability (RAM)testing begins late 2013

– Decision expected early 2015• Oshkosh JLTV solution

– Oshkosh TAK-4i intelligent independent suspension system

– Latest automotive technologies– Advanced crew protection system

• Low rate initial production expected in 2016 for contract winner

23

OSK Investor Slides March 2013

The Fire & Emergency Advantage

24

InnovationLeader

PremierDistribution and Service

Unrivaled Product

Performance

#1 Brands

Leading global provider of specialty vehicles that serve, protect and save lives

OSK Investor Slides March 2013

Domestic Fire Market Drivers Stabilizing

25

• Housing prices and property taxes appear to have bottomedRecent Headlines

Housing starts climb to highest rate since June 2008- Reuters, January 17, 2013

Housing starts projected to rise significantly over next 3 years- Moody’s

Firefighters feel the squeeze of shrinking budgets- Governing magazine

Municipal-debt defaults will remain infrequent and isolated events…- Moody’s

HOUSING PRICES & LOCAL PROPERTY TAXES

• Municipal market has bottomed, expect modest recovery in FY14• Federal funding likely to remain weak through FY14

OSK Investor Slides March 2013

International Market Growth Opportunities• Expect continued growth in

developing countries– Investing in safety and security– Expanding infrastructure

• World air traffic projected to continue growing– Middle East and Asia Pacific

expected to increase 8%-10% per year through 2014

– Driving increased demand for Oshkosh Airport Products

• International customers seeking technologically superior products

26

Pierce Industrial Pumper, Liaoning Province, China

(1)

(1) Source: Air Traffic Growth (regional growth in passenger kilometers) per International Civil Aviation Organization.

OSK Investor Slides March 2013

The CommercialAdvantage

27

Broadest Product Line

Direct Distribution,

Customer Intimacy

Scalable, Flexible

Manufacturing & Operations

Access to Technology, Alternative

Fuels Leadership

Innovation and New Product Development

Best in Class Aftermarket Service and

Support

Integrated factory

Refuse collection vehicle product line

Alternative fuel technology

Street Smart, Street Tough

OSK Investor Slides March 2013

U.S. Mixer Market Unit Growth Analysis

• U.S. housing starts assumptions: 0.8 million in FY13; 1.2 million in FY14; and 1.4 million in FY15

• Concrete mixer parts demand was up 20% in FY12 vs. FY11 and up >100% from the recessionary low

• January 2013 housing starts* at 890,000

28

< 50% of FY06

Volume

0.00.20.40.60.81.01.21.41.61.82.0

2011 2012E 2013E 2014E 2015E

Hou

sing

Sta

rts

In M

illio

ns

U.S. Housing Starts Forecast

Moodys Portland Cement AssociationGlobal Insight Average Analyst Estimate

Assumed one year delay in

mixer demand vs. starts correlation!

* U.S. Census Bureau

Source: 2012 OSK Analyst Day; Rear Discharge Market

OSK Investor Slides March 2013

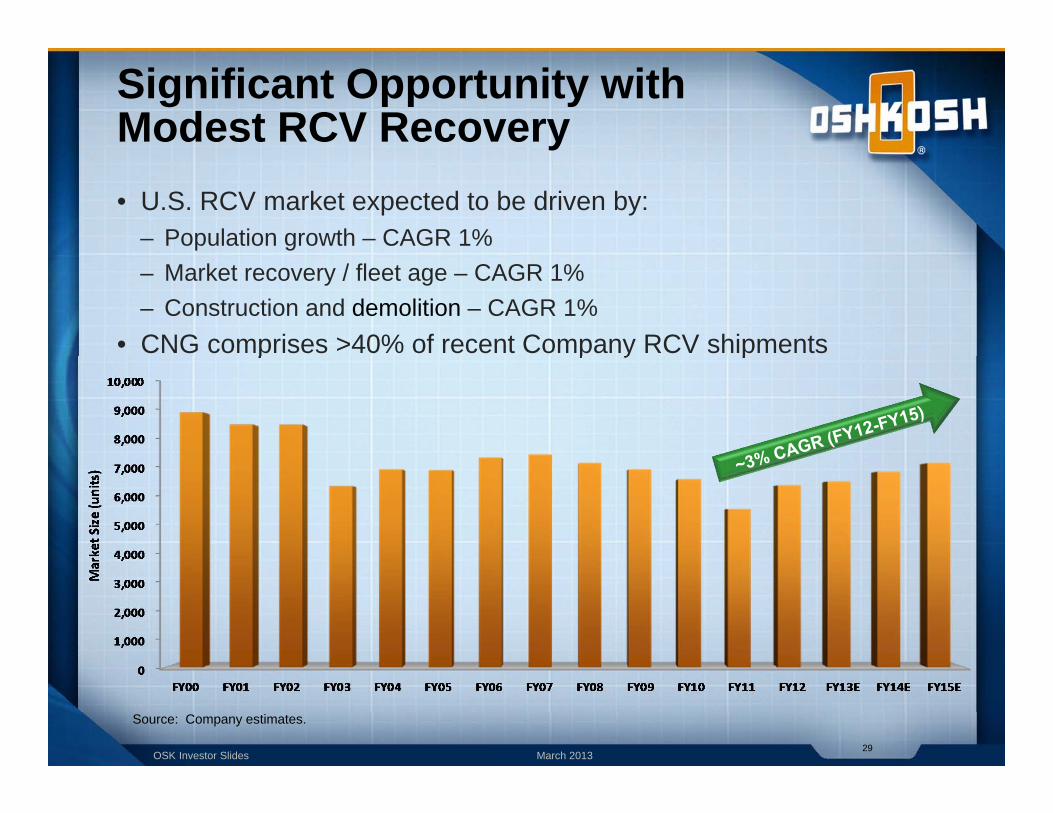

Significant Opportunity with Modest RCV Recovery• U.S. RCV market expected to be driven by:

– Population growth – CAGR 1%– Market recovery / fleet age – CAGR 1%– Construction and demolition – CAGR 1%

• CNG comprises >40% of recent Company RCV shipments

29

Source: Company estimates.

OSK Investor Slides March 2013

Expectations for FY13*

30

Additional expectations• Adjusted corporate expenses ~$130 - $135 million

(share-based compensation and higher IT investment)

• Tax rate of ~32%; including R&D credit reinstatement benefit

• CapEx of ~$60 million• Free cash flow $100 - $125 million• Share count** of ~89 million

Segment information

Measure Access Equipment Defense Fire &

Emergency Commercial

Sales(billions) $2.8-$3.0 $3.2-$3.3 $0.72-$0.75 $0.72-$0.75

Operating Income Margin ~10.5% ~6.5% 2.0%-2.5% 4.5%-5.0%

• Revenues of $7.4 billion to $7.7 billion• Adjusted operating income of $420 million to $455 million• Adjusted EPS from continuing operations of $2.80 to $3.05

Comments on Second Quarter• Expect to benefit from seasonally

driven construction demand andU.A.E. M-ATV sales

* FY13 expectations exclude certain non-GAAP adjustments (see Appendix) and are current as of January 25, 2013

** Excludes impact of any repurchases after December 31, 2012

OSK Investor Slides March 2013

Our Commitment to Shareholders

• Aggressively drive to achieve MOVE targets

• Attack product, process and overhead costs to raise margins

• Apply disciplined capital allocation strategy

• Sustain active shareholder outreach

• Periodically assess strategic options

• Attract highly talented directors and managers

• Deploy Oshkosh Operating System globally to sustain lean culture

31

OSK Investor Slides March 2013

Poised to Deliver Results

• MOVE strategy expected to deliver higher margins throughout cycle• Market recovery, from deep cycle, has commenced

– Is expected to overcome defense downturn • Oshkosh processes and team support execution of MOVE

32

FY12 FY15E

Industry Leading Brands (1)

Access Equipment #1 Global

Fire Apparatus #1 Global

Airport Products #1 Global

Defense TWV (2) #1 Global

Concrete Mixers #1 Americas

Refuse Collection #1 Americas

* Non-GAAP results. See Appendix for reconciliation to GAAP results.

(1) Based on Company estimates.(2) Oshkosh Defense is the leading supplier of heavy, medium and tactical

wheeled vehicles for the U.S. Armed Services.

OSK Investor Slides March 2013

For more information contact:

Patrick N. DavidsonVice President, Investor Relations(920) [email protected]

OSK Investor Slides March 2013

Appendix

OSK Investor Slides March 2013

North America – Strong Rental and Market Conditions, Sustained Growth Cycle• Favorable construction spending outlook• Rental industry robust

– Fleet age 55+ months (near peak)– Utilization near 70% (trending up)– Strong CapEx plans

• Rental penetration continues upward trajectory• Energy projects, industrial retooling driving demand

35

FY15E still well short of

prior peak unit volume

Source: Company estimates

OSK Investor Slides March 2013

EAME – Some Bright Spots Despite Economic Uncertainty• Nordics, Benelux and Germany• Russia (infrastructure), South Africa (mining)

and Middle East (energy and infrastructure)• Relative stability in agriculture• Economic uncertainty in Southern Europe

36

FY15E AWP volume ~50% of peak;

Telehandler volume higher as 60% of demand comes

from Ag

JLG primarily serves the AWP market in EAME

Source: Company estimates

OSK Investor Slides March 2013

Latin America – Brazil Remains Attractive, Construction Strengthening Throughout

• Major projects with over $500 billion in investment expected in Brazil

• Rental concept strengthening• Product adoption increasing in Mexico, Chile and

Panama• Inconsistent supply of capital

37

Demand driven by Olympics,

FIFA World Cup and mining

Source: Company estimates

OSK Investor Slides March 2013

Asia Pacific – Australia Steady, China in Early Phase of Adoption• Australia energy, mining and supporting infrastructure• Rental concept emerging in China• Vietnam, Indonesia and Malaysia showing potential• Singapore adoption growing• Slow recovery in Japan and South Korea

38

Product adoption drives growth

faster than GDPincrease

JLG – Led Formation of

China Work Safety Committee (WSC)

Source: Company estimates

OSK Investor Slides March 2013

Baseline Defense Revenue

39

JLTV EMDGMV 1.1

HMMWV UpgradesInt’l M-ATV

MSVSP-19R, and More

Family of Heavy Tactical Vehicles (FHTV)

M-ATV

Family of Medium Tactical Vehicles (FMTV)

Medium Tactical Vehicle Replacement (MTVR)

Logistics Vehicle System Replacement (LVSR)

Vehicle Support, Aftermarket and Lifecycle Sustainment Services

SandCat

Int’l M-ATV and Other

(1) Baseline assumed in Oshkosh’s EPS outlook

(1)

$1.5-$2.0$0.8-$1.5

OSK Investor Slides March 2013

Non-GAAP to GAAP Reconciliation The table below presents a reconciliation of the Company’s presented Non-GAAP measures to the most directly comparable GAAP measures (in millions, except per share amounts):

40

Fiscal Year Ended Three Months EndedSeptember 30, December 31,

2012 2012 2011Non-GAAP earnings per share attributable to Oshkosh Corporation from continuing operations-diluted 2.27$ 0.60$ 0.39$ Restructuring-related charges, net of tax (0.13) - (0.01) Performance share valuation adjustment, net of tax (0.05) - - Curtailment expense, net of tax (0.02) - - Tender offer and proxy contest costs, net of tax (0.05) (0.11) (0.02) Discrete tax benefits 0.49 0.02 0.07 GAAP earnings per share attributable to Oshkosh Corporation from continuing operations-diluted 2.51$ 0.51$ 0.43$

Net cash flows provided by operating activities 268.3$ 45.1$ Additions to property, plant and equipment (55.9) (8.3) Additions to equipment held for rental (8.4) (1.1) Proceeds from sale of property, plant and equipment 7.6 - Proceeds from sale of equipment held for rental 3.7 3.5 Free cash flow 215.3$ 39.2$

Non-GAAP operating income margin 4.9%Non-GAAP operating income 401.6$ Restructuring-related charges (18.6) Performance share valuation adjustment (7.0) Curtailment expense (3.4) Tender offer and proxy contest costs (6.6) GAAP operating income 366.0$ GAAP operating income margin 4.5%

OSK Investor Slides March 2013

Non-GAAP to GAAP Reconciliation

41

• The table below presents a reconciliation of the Company’s presented non-GAAP measures to the most directly comparable GAAP measures (in millions, except per share amounts):

Low HighCorporateNon-GAAP operating expenses (130.0)$ (135.0)$ Tender offer and proxy contest costs (16.3) (16.3) GAAP operating expenses (146.3)$ (151.3)$

ConsolidatedNon-GAAP operating income 420.0$ 455.0$ Restructuring-related benefits 0.3 0.3 Curtailment expense (0.9) (0.9) Tender offer and proxy contest costs (16.3) (16.3) GAAP operating income 403.1$ 438.1$

Non-GAAP earnings per share attributable to Oshkosh Corporation from continuing operations-diluted 2.80$ 3.05$ Restructuring-related benefits, net of tax - - Curtailment expense, net of tax - - Tender offer and proxy contest costs, net of tax (0.11) (0.11) Discrete tax benefits 0.02 0.02 GAAP earnings per share attributable to Oshkosh Corporation from continuing operations-diluted 2.71$ 2.96$

Net cash flows provided by operating activities 175.5$ 200.5$ Additions to property, plant and equipment (60.0) (60.0) Additions to equipment held for rental (19.0) (19.0) Proceeds from sale of equipment held for rental 3.5 3.5 Free cash flow 100.0$ 125.0$

Fiscal 2013 Expectations

OSK Investor Slides March 2013

Commonly Used Acronyms

42

ARFF Aircraft Rescue and Firefighting M-ATV MRAP All-Terrain Vehicle

AWP Aerial Work Platform MECV Modernized Expanded Capability Vehicle

CNG Compressed Natural Gas MRAP Mine Resistant Ambush Protected

DoD Department of Defense MSVS Medium Support Vehicle System (Canada)

EAME Europe, Africa & Middle East MTT Medium Tactical Truck

EMD Engineering & Manufacturing Development NPD New Product Development

FHTV Family of Heavy Tactical Vehicles OI Operating Income

FMS Foreign Military Sales PLS Palletized Load System

FMTV Family of Medium Tactical Vehicles PUC Pierce Ultimate Configuration

HEMTT Heavy Expanded Mobility Tactical Truck RCV Refuse Collection Vehicle

HET Heavy Equipment Transporter RFP Request for Proposal

HEWATT HEMTT-Based Water Tender ROW Rest of World

HMMWV High Mobility Multi-Purpose Wheeled Vehicle SMP Standard Military Pattern (Canadian MSVS)

JLTV Joint Light Tactical Vehicle TACOM Tank-automotive and Armaments Command

JPO Joint Program Office TDP Technical Data Package

JROC Joint Requirements Oversight Council TFFT Tactical Fire Fighting Truck

JUONS Joint Urgent Operational Needs Statement TPV Tactical Protector Vehicle

KPIs Key Performance Indicators TWV Tactical Wheeled Vehicle

L-ATV Light Combat Tactical All-Terrain Vehicle UCA Undefinitized Contract Action

LVSR Logistic Vehicle System Replacement UIK Underbody Improvement Kit (for M-ATV)