how it works. - cloud object storage | store & retrieve...

TRANSCRIPT

How it works.

A Guaranteed Lifetime Withdrawal Benefit

For many, the key to retirement success is matching your retirement income to the lifestyle you desire. The New York Life Clear Income Fixed Annuity can provide the income you need for a more robust retirement. At the core of this product is a Guaranteed Lifetime Withdrawal Benefit1 (GLWB) Rider. So, how does it work? It’s simple...

1. Build your base. Your Income Base, a value separate from your

Accumulation Value, will increase for up to 10 years at a rate referred to as your annual increase rate (determined at issue). Your Income Base is only used to calculate your guaranteed lifetime withdrawal benefit amount.

A clear path to retirement.

End of policy year Income Base

0 $100,000

1 $105,000

2 $110,250

3 $115,763

4 $121,551

5 $127,628

6 $134,010

7 $140,710

8 $147,746

9 $155,133

10 $162,889

11 $162,889

12 $162,889

Assumption: 5% compounded annual increase rate locked in for the first 10 years with no withdrawals or surrenders of the Accumulation Value.

End of policy year Accumulation Value

0 $100,000

1 $101,527

2 $102,884

3 $104,259

4 $105,652

5 $107,064

6 $108,495

7 $109,944

8 $110,213

9 $110,483

10 $110,753

11 $111,024

12 $111,296

Assumption: 2.10% crediting rate years 1-7 and 1.0% thereafter with no withdrawals or surrenders; 0.75% annual rider fee taken quarterly.

1 All guarantees are dependent on the claims-paying ability of the issuer, New York Life Insurance and Annuity Corporation (NYLIAC), A Delaware Corporation, a wholly owned subsidiary of New York Life Insurance Company. Surrender charges will not be deducted from death benefit proceeds. May not be available in all jurisdictions. Rider fee applies.

2. Steadily accumulate. Make your premium payment, and watch it grow at

a fixed rate.

This is a hypothetical example of how the Income Base, from which your guaranteed lifetime withdrawals are calculated, can grow in comparison to a policy’s Accumulation Value and is based on the stated assumptions. Actual crediting rates may be higher or lower than stated and are determined when the annuity contract is issued.

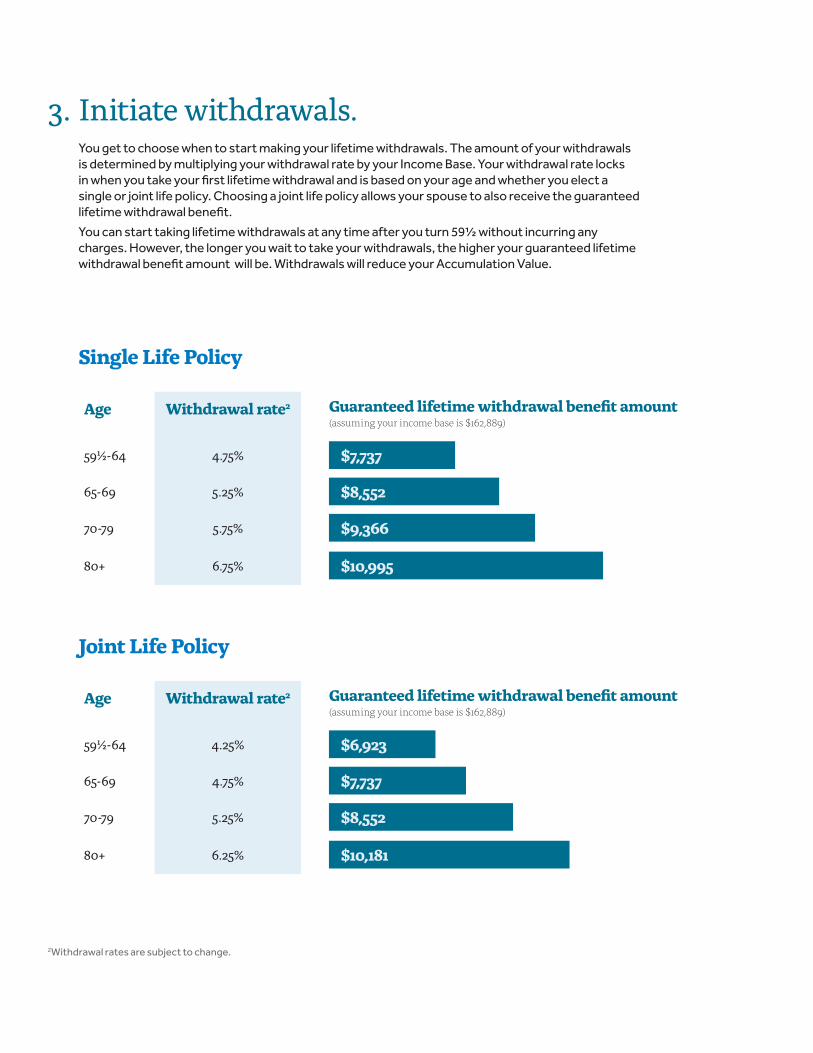

Single Life Policy

Age Withdrawal rate2 Guaranteed lifetime withdrawal benefit amount (assuming your income base is $162,889)

59½-64 4.75% $7,737

65-69 5.25% $8,552

70-79 5.75% $9,366

80+ 6.75% $10,995

3. Initiate withdrawals. You get to choose when to start making your lifetime withdrawals. The amount of your withdrawals

is determined by multiplying your withdrawal rate by your Income Base. Your withdrawal rate locks in when you take your first lifetime withdrawal and is based on your age and whether you elect a single or joint life policy. Choosing a joint life policy allows your spouse to also receive the guaranteed lifetime withdrawal benefit.

You can start taking lifetime withdrawals at any time after you turn 59½ without incurring any charges. However, the longer you wait to take your withdrawals, the higher your guaranteed lifetime withdrawal benefit amount will be. Withdrawals will reduce your Accumulation Value.

2Withdrawal rates are subject to change.

Joint Life Policy

Age Withdrawal rate2 Guaranteed lifetime withdrawal benefit amount (assuming your income base is $162,889)

59½-64 4.25% $6,923

65-69 4.75% $7,737

70-79 5.25% $8,552

80+ 6.25% $10,181

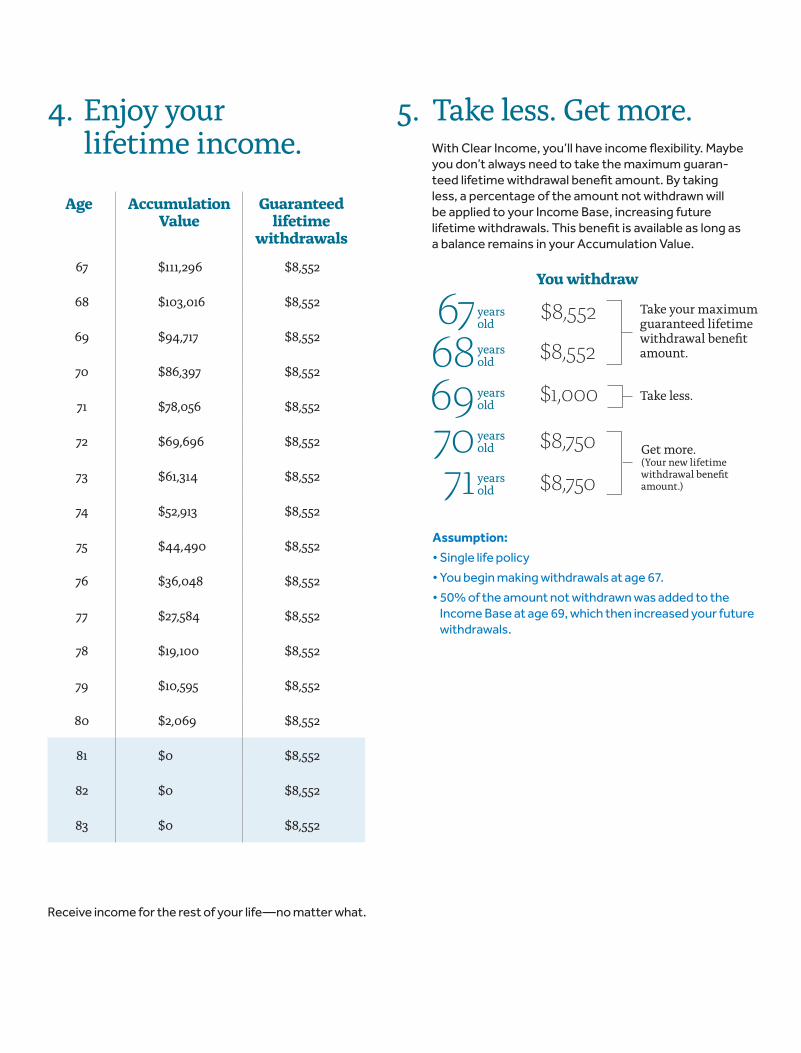

4. Enjoy your lifetime income.

Age Accumulation

ValueGuaranteed

lifetime withdrawals

67 $111,296 $8,552

68 $103,016 $8,552

69 $94,717 $8,552

70 $86,397 $8,552

71 $78,056 $8,552

72 $69,696 $8,552

73 $61,314 $8,552

74 $52,913 $8,552

75 $44,490 $8,552

76 $36,048 $8,552

77 $27,584 $8,552

78 $19,100 $8,552

79 $10,595 $8,552

80 $2,069 $8,552

81 $0 $8,552

82 $0 $8,552

83 $0 $8,552

5. Take less. Get more. With Clear Income, you’ll have income flexibility. Maybe

you don’t always need to take the maximum guaran-teed lifetime withdrawal benefit amount. By taking less, a percentage of the amount not withdrawn will be applied to your Income Base, increasing future lifetime withdrawals. This benefit is available as long as a balance remains in your Accumulation Value.

You withdraw

$8,552

$1,000

$8,750

$8,750

$8,552

Take your maximum guaranteed lifetime withdrawal benefit amount.

years old

years old

6768697071

years old

years old

years old

Get more. (Your new lifetime withdrawal benefit amount.)

Take less.

Assumption:

• Single life policy

• You begin making withdrawals at age 67.

• 50% of the amount not withdrawn was added to the Income Base at age 69, which then increased your future withdrawals.

Receive income for the rest of your life—no matter what.

Terms to know.A glossary to help you understand your Clear Income Guaranteed Lifetime Withdrawal Benefit.

Guaranteed Lifetime Withdrawal Benefit (GLWB) A rider on a deferred annuity that allows withdrawals based on your Income Base to be taken as income from the Accumulation Value of a policy. The withdrawals—or income payments—are guaranteed to continue for life.

Guaranteed Lifetime Withdrawal Benefit Amount The maximum amount of annual income you can withdraw from your policy while still ensuring the income can be sustained for the rest of your life.

Accumulation Value Your initial premium payment and all credited interest makes up your Accumulation Value. You have access to this money at any time (subject to surrender charges or adjustments).

Initial Guaranteed Fixed Interest Rate The fixed rate at which your Accumulation Value will grow for the first seven years of your policy. After seven years, your policy will renew annually with a one-year interest rate that is based on the interest rate set by the company.

Income Base A value in the policy upon which your guaranteed lifetime withdrawal benefit amount is calculated. The Income Base has no cash value.

Annual Increase Rate (also referred to as the roll-up rate) The rate at which your Income Base grows over time (for up to 10 years). The rate is determined at the time your policy is issued and is compounded each year.

Compounding Calculating growth not only on the initial value of an account but also on the account’s growth itself.

Single Life Policy A policy that provides a guaranteed lifetime withdrawal benefit for one person. If that person should die, the named beneficiaries will receive the remaining Accumulation Value.

Joint Life Policy A policy that provides a guaranteed lifetime withdrawal benefit for both you and your spouse. If one mem-ber of the couple should die, the living spouse will continue to receive income payments for the remainder of his or her life.

Withdrawal Rate A percentage used to calculate how much your income payments will be for the rest of your life. The percentage is determined by your age at the time you make your first lifetime withdrawal and whether you elect a single or joint life policy.

New York Life Insurance Company

New York Life Insurance and Annuity Corporation (NYLIAC) (A Delaware Corporation)

51 Madison Avenue New York, NY 10010

www.newyorklife.com

14848.112014 SMRU1624060 (Exp.08.12.2016)

New York Life fixed annuities are issued by New York Life Insurance and Annuity Corporation (NYLIAC), A Delaware Corporation, a wholly owned subsidiary of New York Life Insurance Company, 51 Madison Avenue, New York, NY 10010. Guarantees are based on the claims-paying ability of the issuer. Products are available in jurisdictions where approved.

In most jurisdictions, the policy form numbers for the New York Life Clear Income Fixed Annuity are ICC14-P100 (book value) and ICC14-P120 (MVA); in some states they may be 214-P100 (book value) and 214-P120 (MVA), and state variations may apply. In most jurisdictions, the rider form numbers for the Guaranteed Lifetime Withdrawal Benefit Rider are ICC14-R101 (book value) and ICC14-R102 (MVA), in some states they may be 214-R101 (book value) and 214-R102 (MVA), and state variations may apply.