how do households finance the purchase of a house?

DESCRIPTION

How do households finance the purchase of a house?. Down payment typically 10% of selling price, but 20% is the magic number Mortgage loan to pay the seller the difference between the purchase price and the down payment Mortgage choices impact the economic cost of a home. - PowerPoint PPT PresentationTRANSCRIPT

How do households finance the purchase of a house?

Down payment typically 10% of selling price, but 20% is the

magic number Mortgage

loan to pay the seller the difference between the purchase price and the down payment

Mortgage choices impact the economic cost of a home

Basic Dimensions of a Mortgage

Loan amount (purchase price minus down payment) = PV

Interest rate per period = r Time period for the loan = n Pre-payment option

Self-amortizing, Fixed Rate mortgage

Interest rate and monthly payment are fixed. Standard, conventional

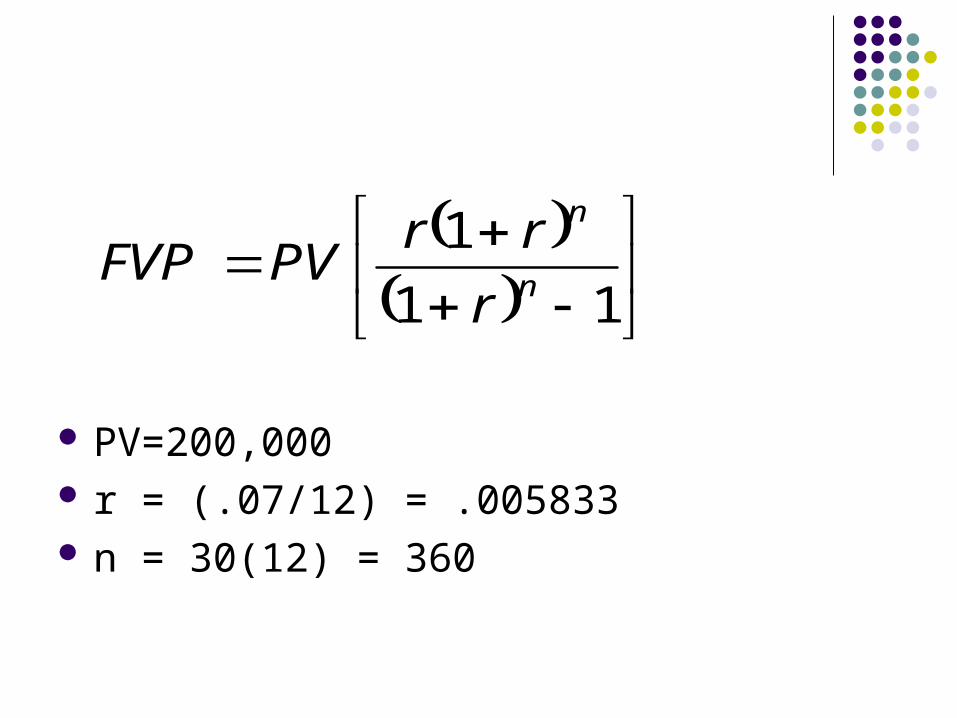

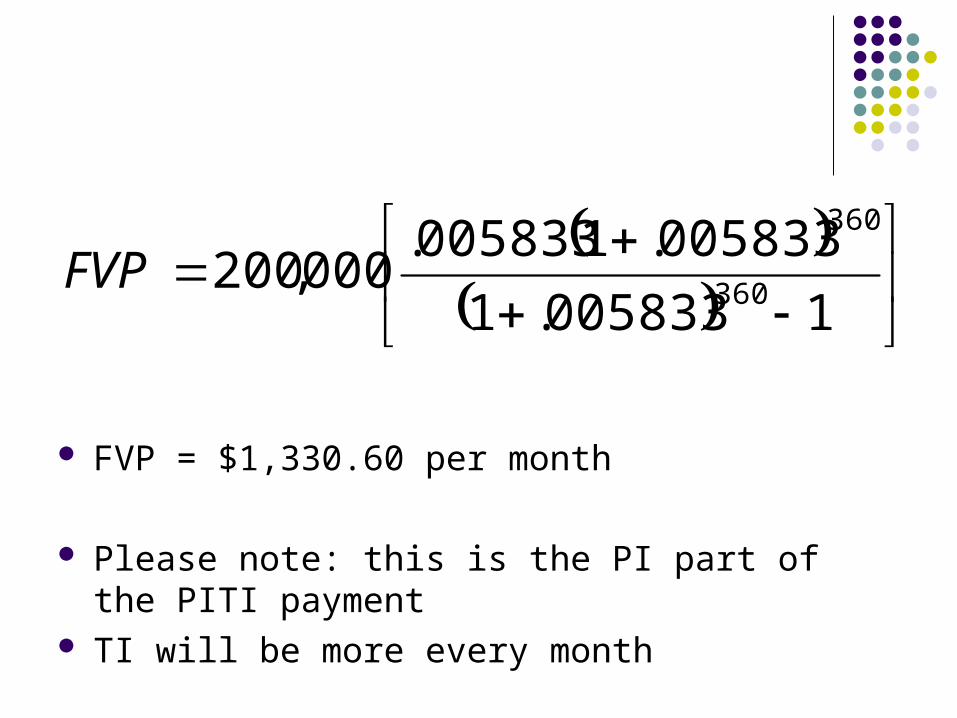

Example (with monthly compounding): loan amount = $200,000 interest rate = 7.0% time period = 30 years

PV=200,000 r = (.07/12) = .005833 n = 30(12) = 360

11

1n

n

r

rrPVFVP

FVP = $1,330.60 per month

Please note: this is the PI part of the PITI payment TI will be more every month

1005833.1

005833.1005833.000,200 360

360

FVP

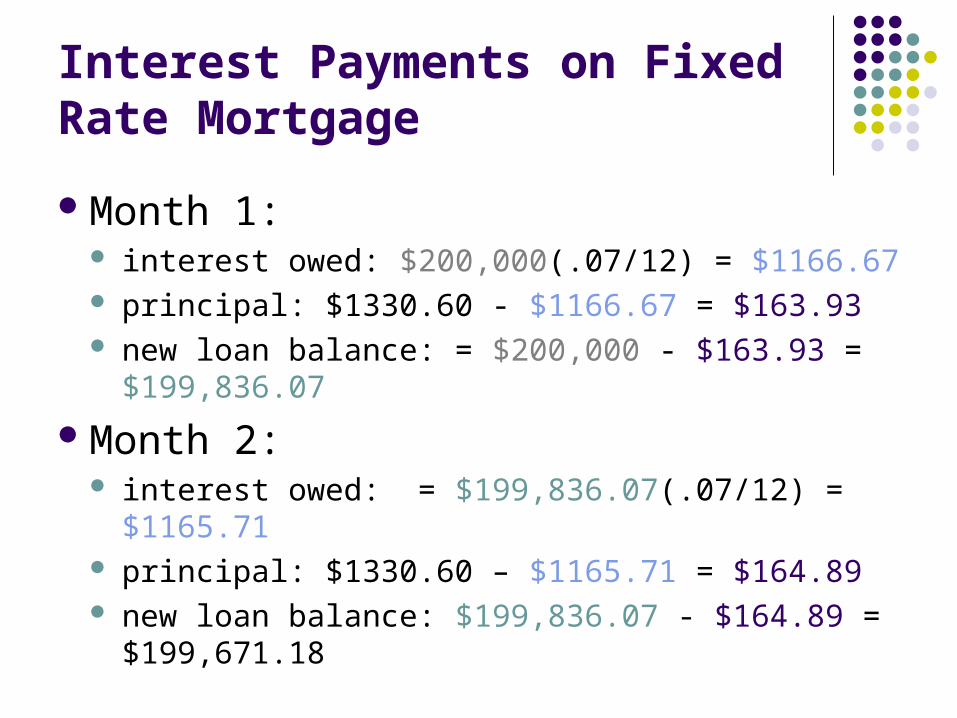

Interest Payments on Fixed Rate Mortgage

Month 1: interest owed: $200,000(.07/12) = $1166.67 principal: $1330.60 - $1166.67 = $163.93 new loan balance: = $200,000 - $163.93 =

$199,836.07

Month 2: interest owed: = $199,836.07(.07/12) = $1165.71 principal: $1330.60 – $1165.71 = $164.89 new loan balance: $199,836.07 - $164.89 =

$199,671.18

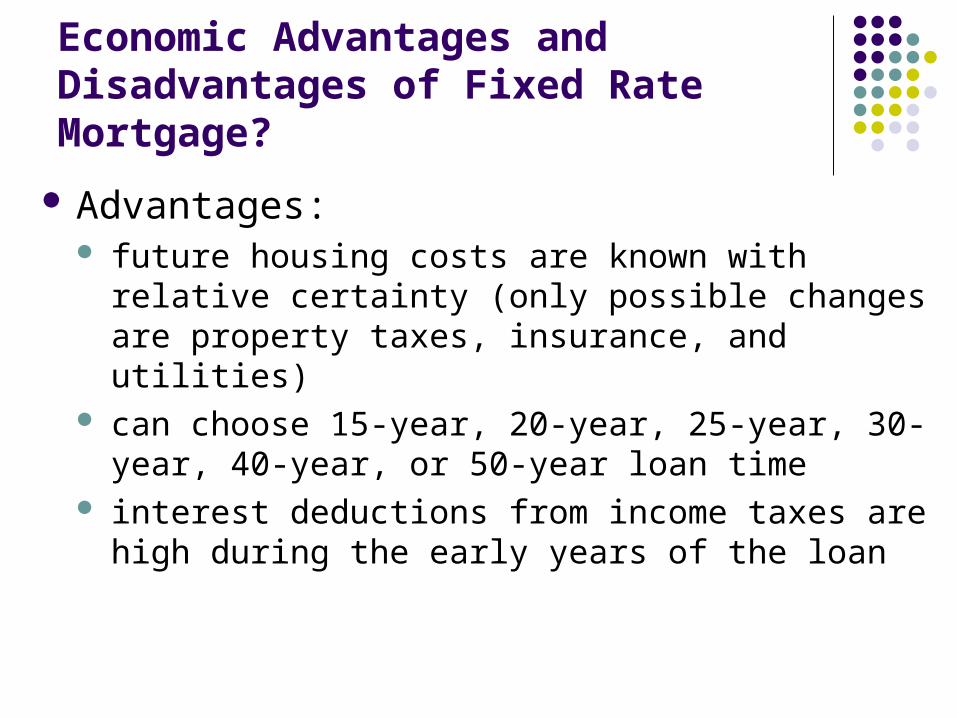

Economic Advantages and Disadvantages of Fixed Rate Mortgage?

Advantages: future housing costs are known with relative certainty

(only possible changes are property taxes, insurance, and utilities)

can choose 15-year, 20-year, 25-year, 30-year, 40-year, or 50-year loan time

interest deductions from income taxes are high during the early years of the loan

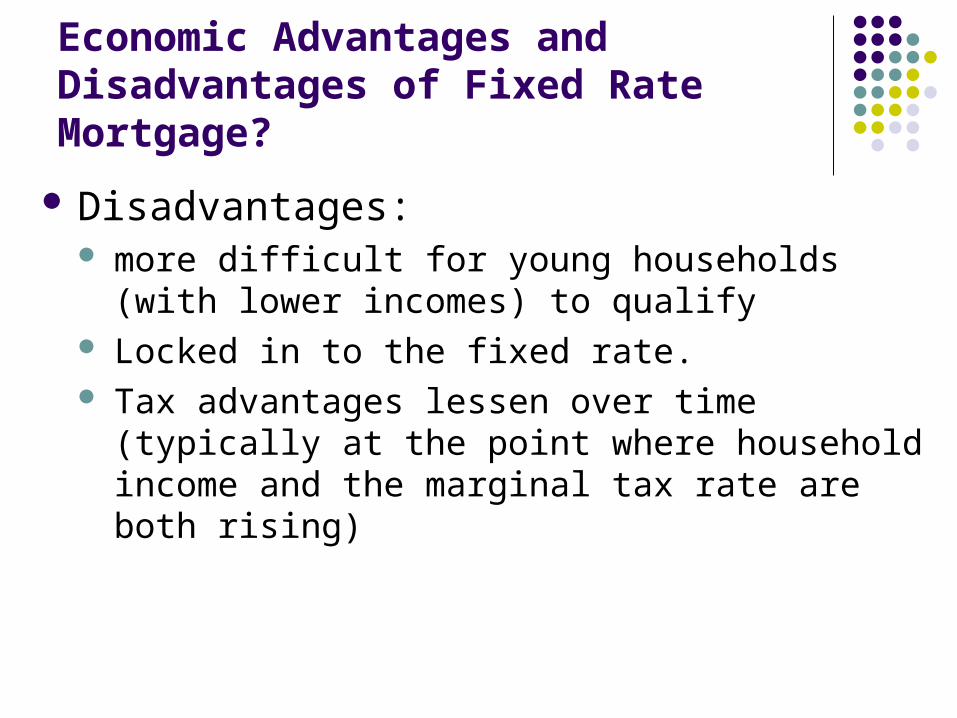

Economic Advantages and Disadvantages of Fixed Rate Mortgage?

Disadvantages: more difficult for young households (with lower

incomes) to qualify Locked in to the fixed rate. Tax advantages lessen over time (typically at the

point where household income and the marginal tax rate are both rising)

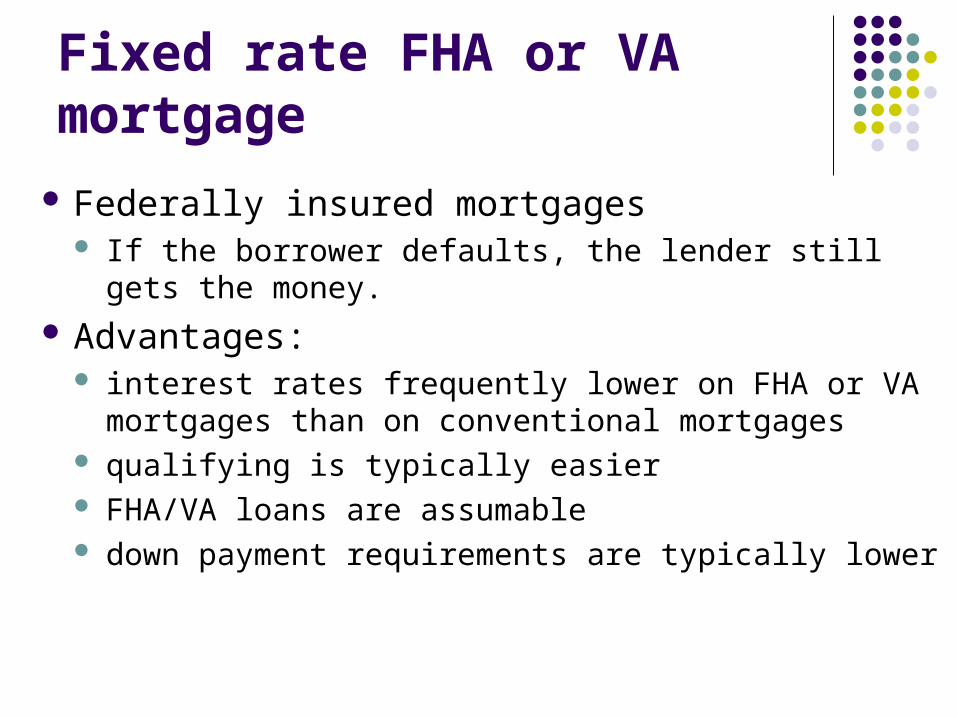

Fixed rate FHA or VA mortgage

Federally insured mortgages If the borrower defaults, the lender still gets the money.

Advantages: interest rates frequently lower on FHA or VA mortgages

than on conventional mortgages qualifying is typically easier FHA/VA loans are assumable down payment requirements are typically lower

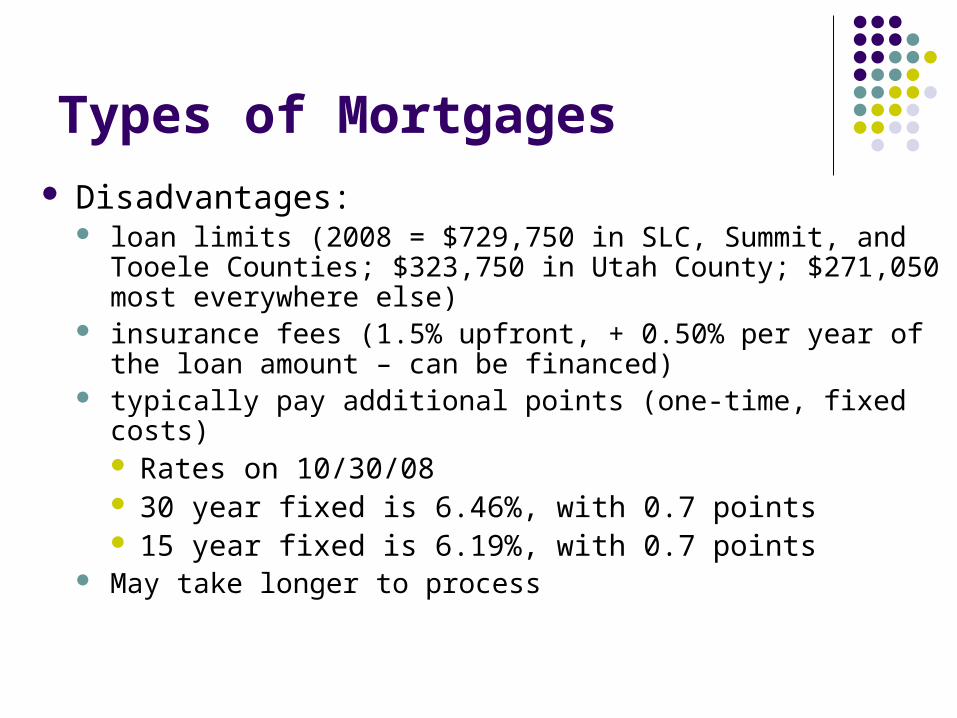

Types of Mortgages Disadvantages:

loan limits (2008 = $729,750 in SLC, Summit, and Tooele Counties; $323,750 in Utah County; $271,050 most everywhere else)

insurance fees (1.5% upfront, + 0.50% per year of the loan amount – can be financed)

typically pay additional points (one-time, fixed costs) Rates on 10/30/08 30 year fixed is 6.46%, with 0.7 points 15 year fixed is 6.19%, with 0.7 points

May take longer to process

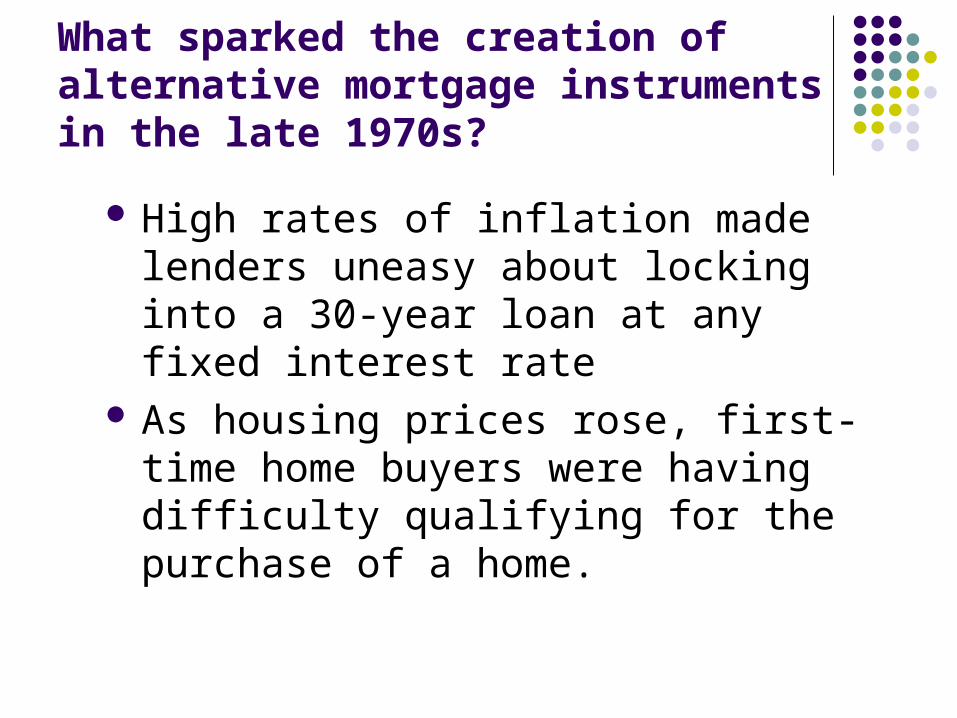

What sparked the creation of alternative mortgage instruments in the late 1970s?

High rates of inflation made lenders uneasy about locking into a 30-year loan at any fixed interest rate

As housing prices rose, first-time home buyers were having difficulty qualifying for the purchase of a home.

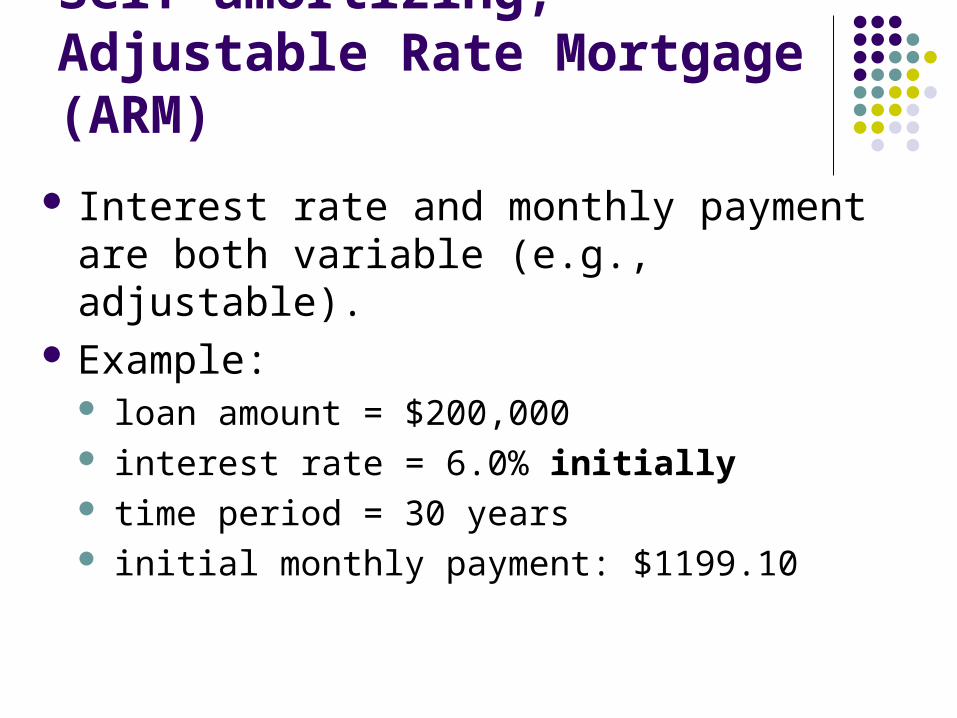

Self-amortizing, Adjustable Rate Mortgage (ARM)

Interest rate and monthly payment are both variable (e.g., adjustable).

Example: loan amount = $200,000 interest rate = 6.0% initially time period = 30 years initial monthly payment: $1199.10

More about the ARM interest rate

Index - market interest rate that is not directly controlled by the lender. It is used to initially set and periodically adjust the interest rate on the loan

Spread - the amount that is added to the index to arrive at the the ARM interest rate.

More about the ARM interest rate

Frequency of rate change - how often the lending institution can change the ARM interest rate.

Rate cap - limitations on either the increase or the decrease in the ARM interest rate that can occur at a point in time.

Frequency of payment change - how often monthly payments can change (typically the same as frequency of rate change -- if not, there is the possibility of negative amortization)

More about the ARM interest rate

When the associated index moves and an adjustment period occurs, the lender changes the interest rate by the amount allowed

(up or down) recalculates the monthly payments based on the

new interest rate and the remaining loan balance.

Economic Advantages and Disadvantages of an Adjustable Rate Mortgage?

Advantages: Initial interest rates are typically lower If you are buying when mortgage rates are high, but

expected to fall in the future Disadvantages:

Greater uncertainty about what future mortgage payments will be

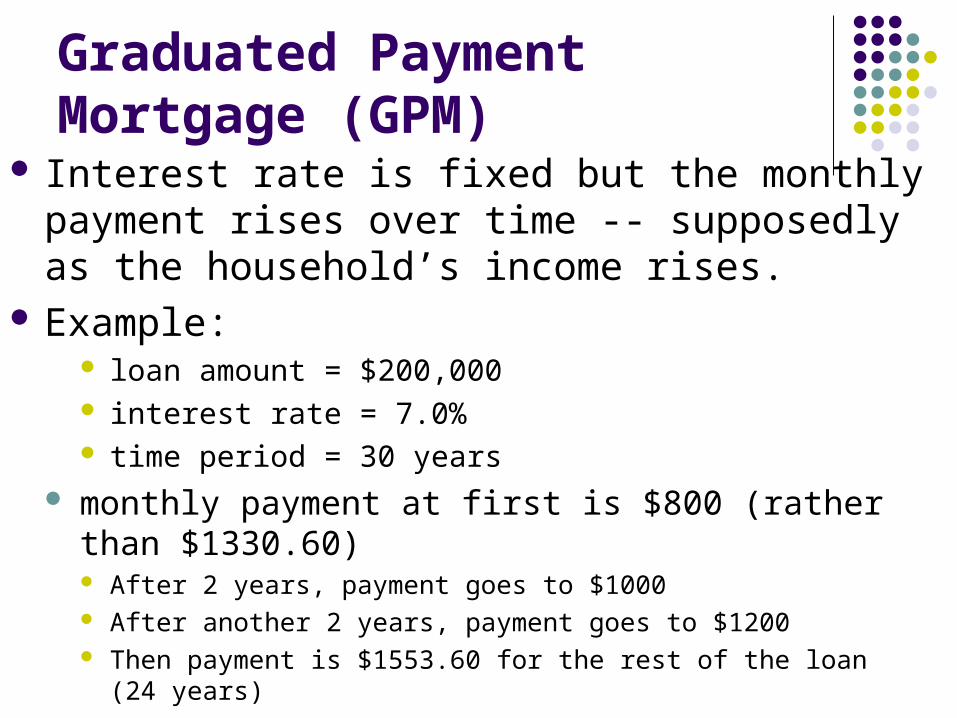

Graduated Payment Mortgage (GPM)

Interest rate is fixed but the monthly payment rises over time -- supposedly as the household’s income rises.

Example: loan amount = $200,000 interest rate = 7.0% time period = 30 years

monthly payment at first is $800 (rather than $1330.60) After 2 years, payment goes to $1000 After another 2 years, payment goes to $1200 Then payment is $1553.60 for the rest of the loan (24 years)

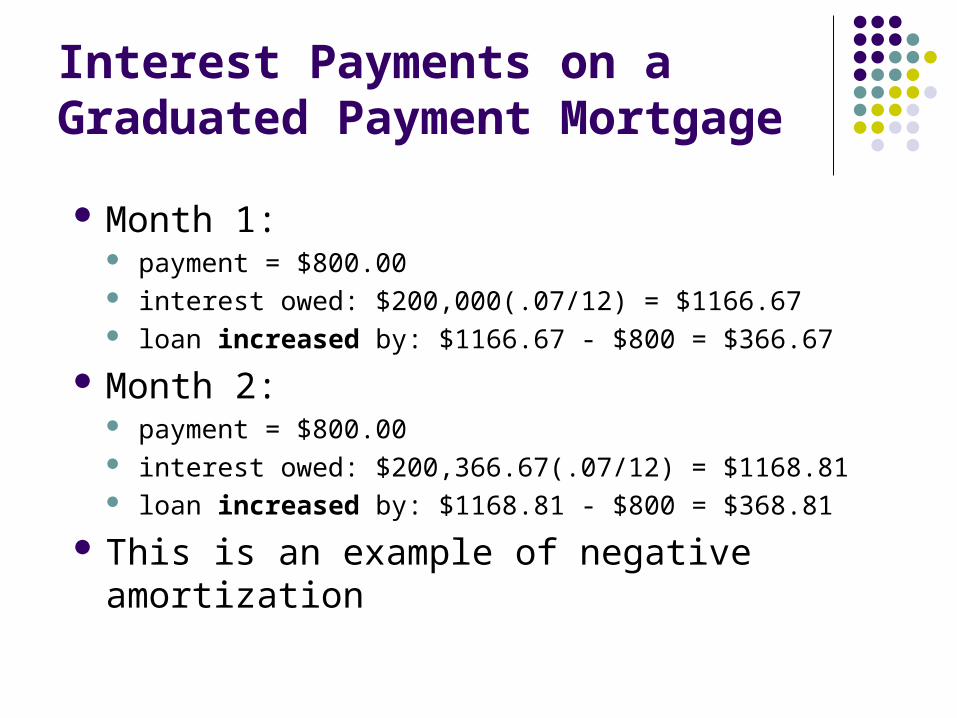

Interest Payments on a Graduated Payment Mortgage

Month 1: payment = $800.00 interest owed: $200,000(.07/12) = $1166.67 loan increased by: $1166.67 - $800 = $366.67

Month 2: payment = $800.00 interest owed: $200,366.67(.07/12) = $1168.81 loan increased by: $1168.81 - $800 = $368.81

This is an example of negative amortization

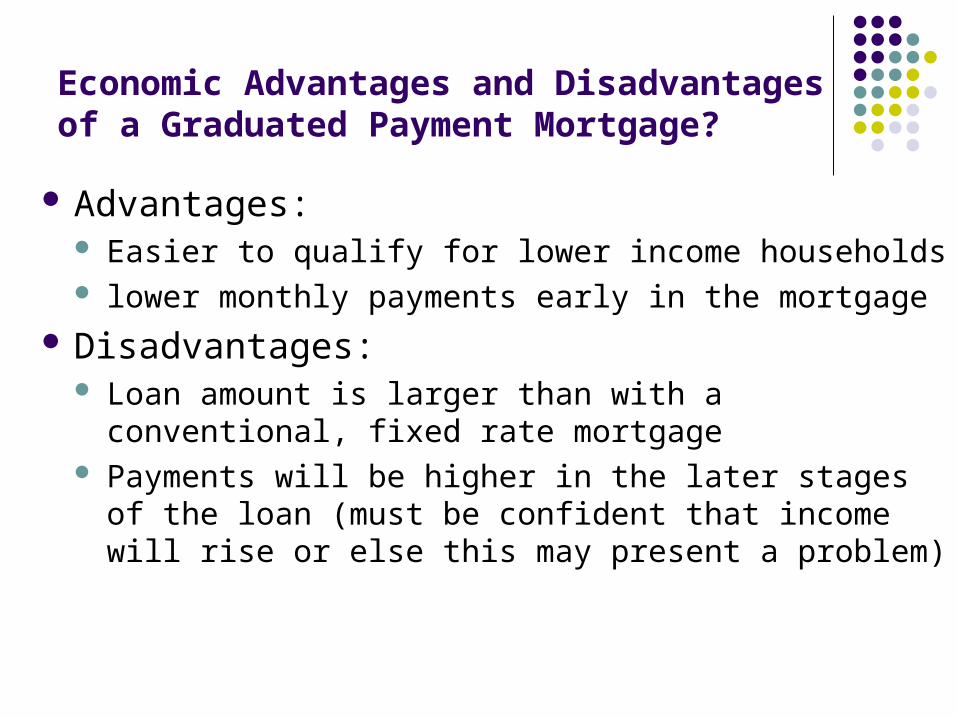

Economic Advantages and Disadvantages of a Graduated Payment Mortgage?

Advantages: Easier to qualify for lower income households lower monthly payments early in the mortgage

Disadvantages: Loan amount is larger than with a conventional, fixed

rate mortgage Payments will be higher in the later stages of the loan

(must be confident that income will rise or else this may present a problem)

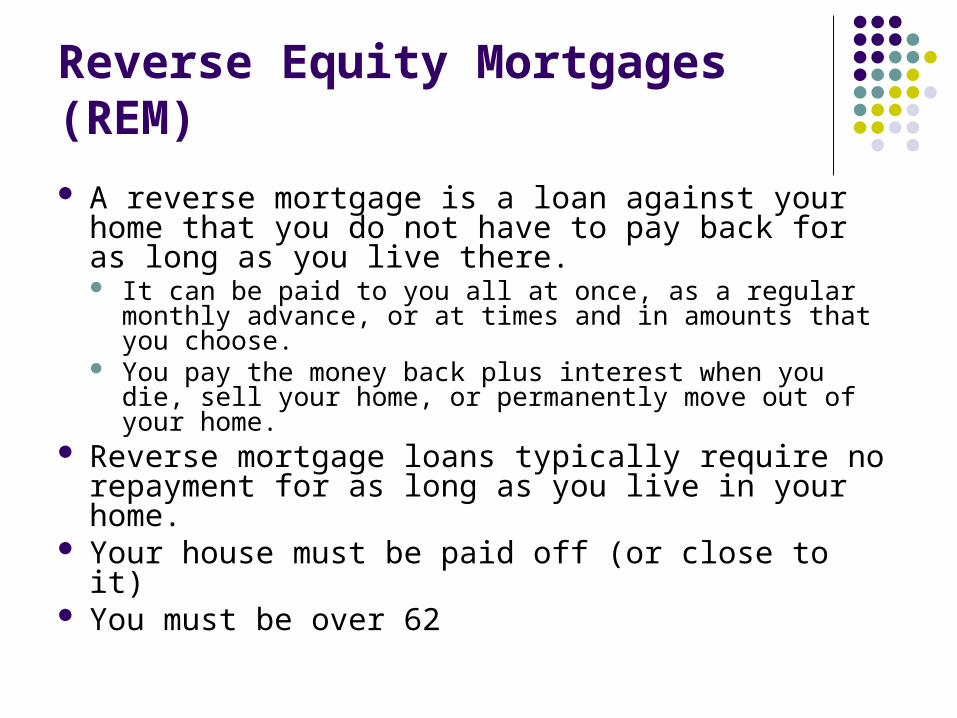

Reverse Equity Mortgages (REM)

A reverse mortgage is a loan against your home that you do not have to pay back for as long as you live there. It can be paid to you all at once, as a regular monthly

advance, or at times and in amounts that you choose. You pay the money back plus interest when you die, sell

your home, or permanently move out of your home. Reverse mortgage loans typically require no

repayment for as long as you live in your home. Your house must be paid off (or close to it) You must be over 62

REMs

Advantages: Way to access your home equity without having

the burden of repayment Creates income

Disadvantages: Reduces the value of your estate Your home must be sold after your death to repay

the REM, if liquid assets are not available to pay off the REM

Interest Only Your payment only covers the interest owed on the loan

Then you have a balloon payment after a specified # of years (e.g. 7 or 12) with the principal balance due

Or your loan will amortize over a shorter amount of time E.g. 40 yr IO – pay IO for 10 years, and then amortized over 30 yrs

Advantages: Lower monthly payments Maybe good for rental properties and/or high-equity growth areas

Disadvantages: Negative amortization may occur No gain in equity from principal reduction Very risky

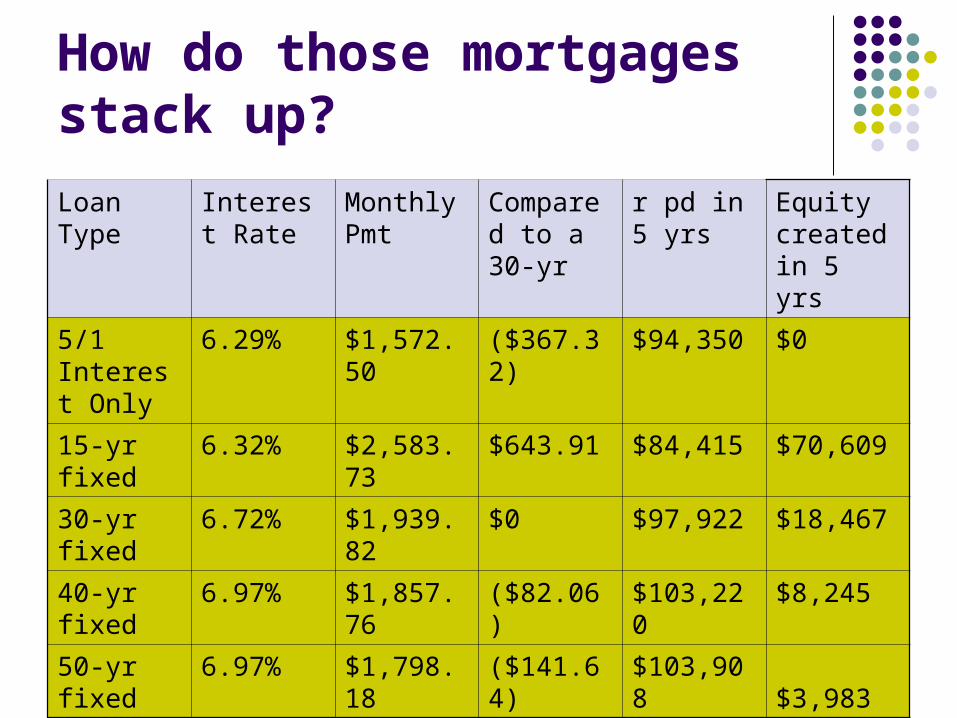

How do those mortgages stack up?

Loan Type

Interest Rate

Monthly Pmt

Compared to a 30-yr

r pd in 5 yrs

Equity created in 5 yrs

5/1 Interest Only

6.29% $1,572.50 ($367.32) $94,350 $0

15-yr fixed 6.32% $2,583.73 $643.91 $84,415 $70,609

30-yr fixed 6.72% $1,939.82 $0 $97,922 $18,467

40-yr fixed 6.97% $1,857.76 ($82.06) $103,220 $8,245

50-yr fixed 6.97% $1,798.18 ($141.64) $103,908$3,983

Summary: Economic Costs and Economic Benefits of Various Mortgage Instruments Depend Upon...

Life cycle stage Business cycle stage Risk tolerance Liquidity needs

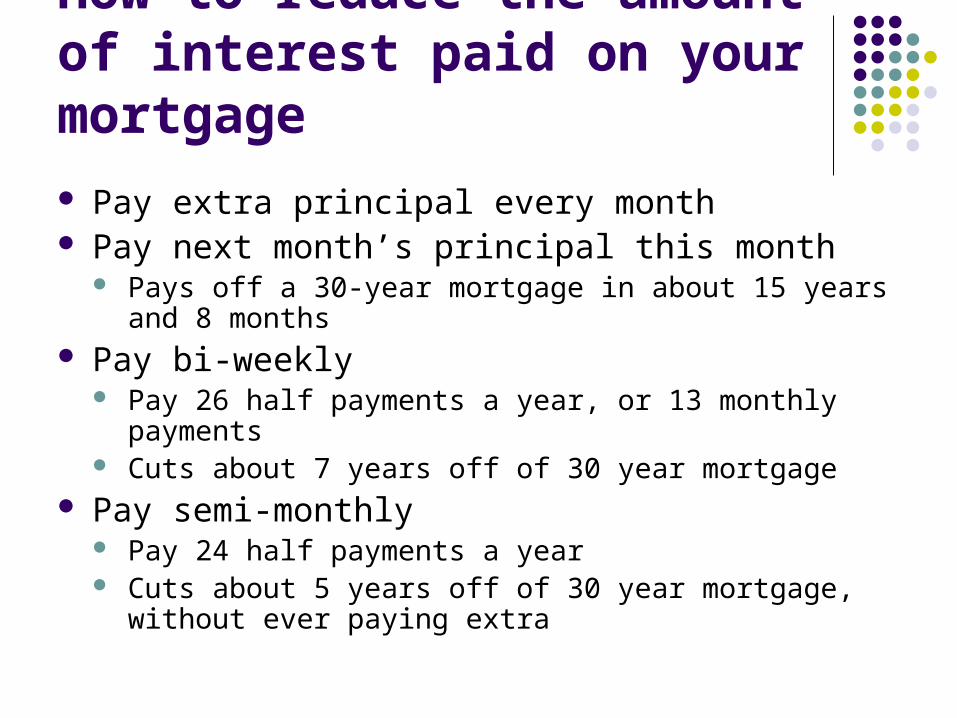

How to reduce the amount of interest paid on your mortgage

Pay extra principal every month Pay next month’s principal this month

Pays off a 30-year mortgage in about 15 years and 8 months

Pay bi-weekly Pay 26 half payments a year, or 13 monthly payments Cuts about 7 years off of 30 year mortgage

Pay semi-monthly Pay 24 half payments a year Cuts about 5 years off of 30 year mortgage, without ever

paying extra

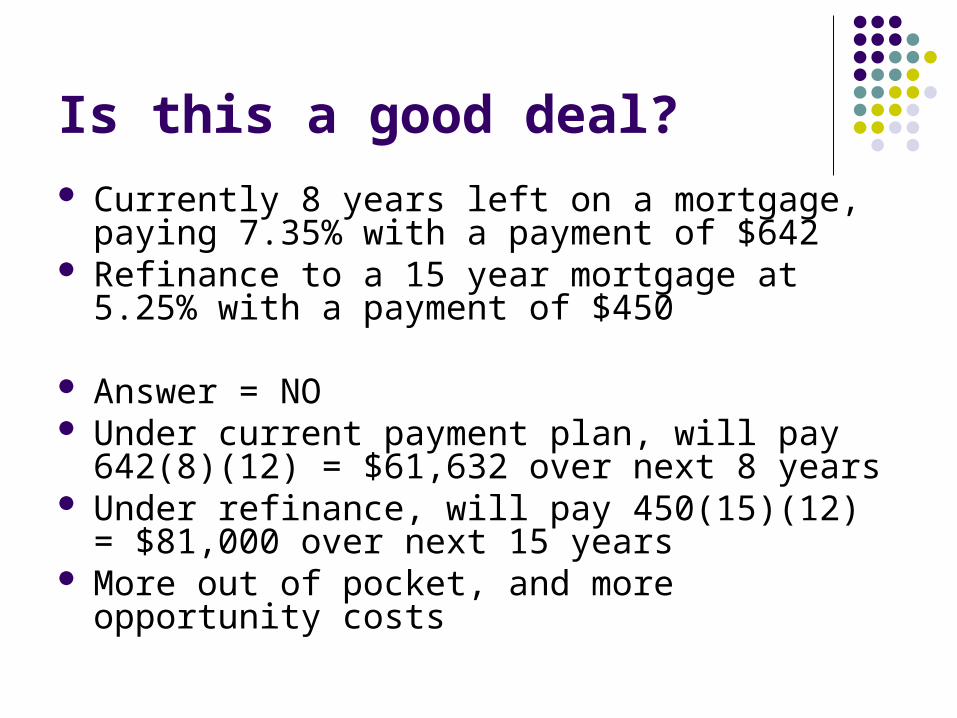

Is this a good deal? Currently 8 years left on a mortgage, paying 7.35%

with a payment of $642 Refinance to a 15 year mortgage at 5.25% with a

payment of $450

Answer = NO Under current payment plan, will pay 642(8)(12) =

$61,632 over next 8 years Under refinance, will pay 450(15)(12) = $81,000

over next 15 years More out of pocket, and more opportunity costs