hot topic: foreign account tax compliance act … handouts/rims 14/lgl011...hot topic: foreign...

TRANSCRIPT

Page 1

Recording of this session via any media type is strictly prohibited.

Page 1

HOT TOPIC: Foreign Account Tax Compliance Act (FATCA)

Overview and Next Steps

Page 2

Recording of this session via any media type is strictly prohibited.

• Denise M Hintzke Global Tax Leader - Foreign Account Tax Compliance Deloitte Tax LLP New York, NY UNITED STATES

Denise works closely with the Global Tax Information and Reporting Practice as well as the Deloitte Member Firms as the Firms deploy cross-functional talent to the global market place in response to the demanding requirements of the provisions of the U.S. Foreign Account Tax Compliance Act. Denise has 30 years of experience advising clients and internal business units on the intricacies of the tax law and assisting organizations in their endeavor to implement the qualified intermediary requirements and put into place best practices with regard to their tax withholding and reporting responsibilities. She has participated on numerous committees and working groups through-out her career, including the Accounting Industry/IRS working group addressing issues regarding the QI Audit procedures. She is a well know speaker on the topic of FATCA as well as on tax withholding and reporting issues and has authored several articles on the topic.

Page 3

Recording of this session via any media type is strictly prohibited.

What to Expect • What is FATCA and how does it apply to your company. • What are the compliance obligations for both incoming and outgoing payments. • What are the implications of these rules, exceptions and frameworks on your business. • What should you do as a Risk Manager to make sure that you are compliant.

Page 4

Recording of this session via any media type is strictly prohibited.

Introduction to FATCA

Page 5

Recording of this session via any media type is strictly prohibited.

What Are We Discussing

Chapter 61 Chapter 3 Chapter 4

• Documentation, withholding and reporting on payments of U.S. source income to non-U.S. persons

• Forms W-8 • Form 1042-S

• Identification of U.S. persons holding accounts at non-U.S. financial institutions or through non-U.S. entities

• Form 8966

• Documentation, withholding and reporting on payments to U.S. persons

• Form W-9 • Form 1099

Page 6

Recording of this session via any media type is strictly prohibited. Foreign Financial Institutions

Equity or Debt in Financial Institutions

Cash value insurance

at

Annuities

U.S. Person

Depository accounts Custodial accounts

FATCA

Holding

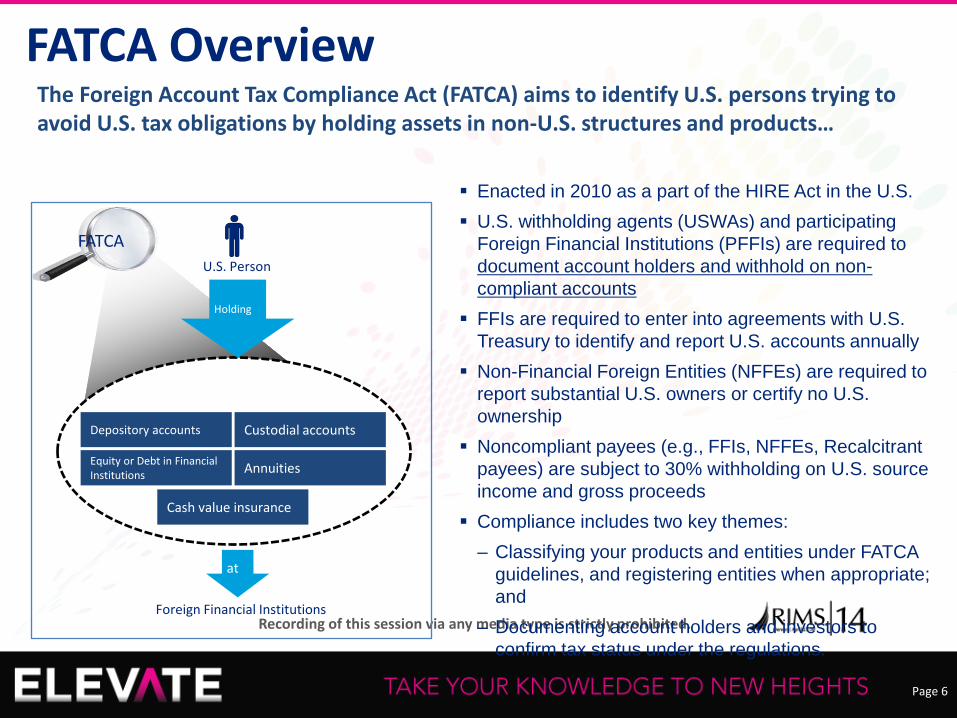

The Foreign Account Tax Compliance Act (FATCA) aims to identify U.S. persons trying to avoid U.S. tax obligations by holding assets in non-U.S. structures and products…

FATCA Overview

Enacted in 2010 as a part of the HIRE Act in the U.S. U.S. withholding agents (USWAs) and participating

Foreign Financial Institutions (PFFIs) are required to document account holders and withhold on non-compliant accounts

FFIs are required to enter into agreements with U.S. Treasury to identify and report U.S. accounts annually

Non-Financial Foreign Entities (NFFEs) are required to report substantial U.S. owners or certify no U.S. ownership

Noncompliant payees (e.g., FFIs, NFFEs, Recalcitrant payees) are subject to 30% withholding on U.S. source income and gross proceeds

Compliance includes two key themes: ‒ Classifying your products and entities under FATCA

guidelines, and registering entities when appropriate; and

‒ Documenting account holders and investors to confirm tax status under the regulations.

Page 7

Recording of this session via any media type is strictly prohibited.

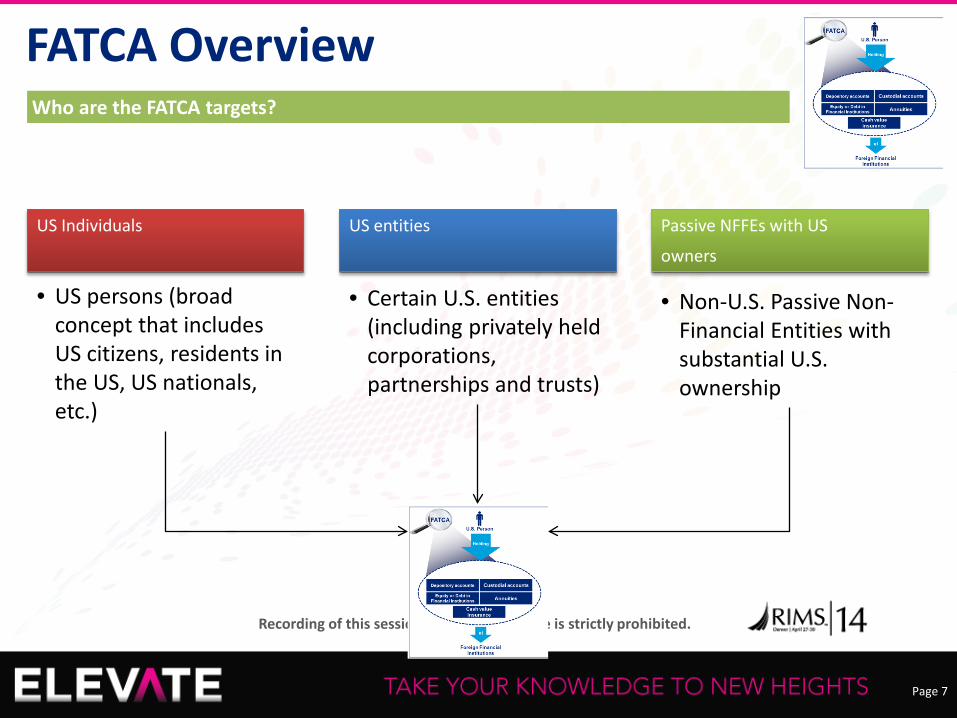

Who are the FATCA targets?

FATCA Overview

US Individuals

US entities

Passive NFFEs with US

owners

• Certain U.S. entities (including privately held corporations, partnerships and trusts)

• Non-U.S. Passive Non-Financial Entities with substantial U.S. ownership

• US persons (broad concept that includes US citizens, residents in the US, US nationals, etc.)

Page 8

Recording of this session via any media type is strictly prohibited.

What FATCA Means

Page 9

Recording of this session via any media type is strictly prohibited.

Companies fall into three categories

Foreign Account Tax Compliance Act (FATCA)

Copyright © 2014 Deloitte Development LLC. All rights reserved.

12

Withholding Agent Foreign Financial Institution (FFI) Non-Financial Foreign Entity (NFFE)

• Foreign or U.S. person that has control, receipt, custody, disposal or payment of any “withholdable payment”

• Not limited to financial services industry • Foreign entity that accepts deposits, holds financial assets for the account of

others as a substantial part of its business, or engages primarily in the business of investing or trading securities, commodities, partnerships or any interests in such positions.

• Includes pension and retirement funds • May include holding companies and treasury centers in certain situations

• Includes any foreign entity that is not a FFI • Excepted NFFEs: • Publicly traded corporation and its corporate affiliates (more than 50% of

vote and value) • Entity organized under the laws of a possession of the U.S. • A foreign government, international organization or any wholly owned

agency thereof • Active NFFEs • Passive NFFEs

Page 10

Recording of this session via any media type is strictly prohibited.

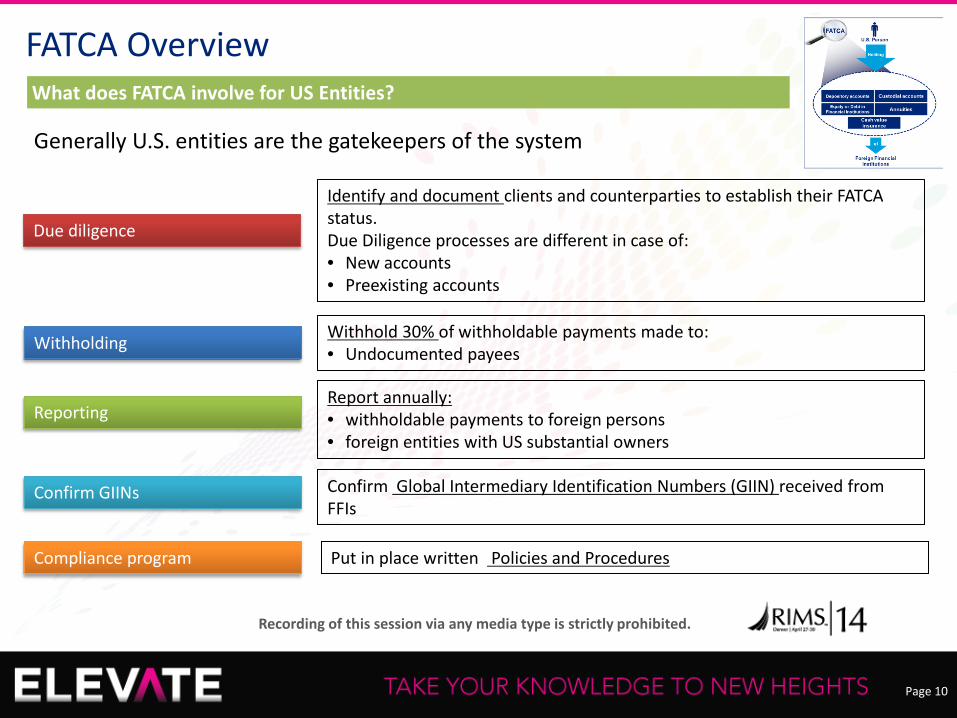

What does FATCA involve for US Entities?

FATCA Overview

Generally U.S. entities are the gatekeepers of the system

Due diligence

Withholding

Reporting

Confirm GIINs

Compliance program

Identify and document clients and counterparties to establish their FATCA status. Due Diligence processes are different in case of: • New accounts • Preexisting accounts

Withhold 30% of withholdable payments made to: • Undocumented payees

Report annually: • withholdable payments to foreign persons • foreign entities with US substantial owners

Confirm Global Intermediary Identification Numbers (GIIN) received from FFIs

Put in place written Policies and Procedures

Page 11

Recording of this session via any media type is strictly prohibited.

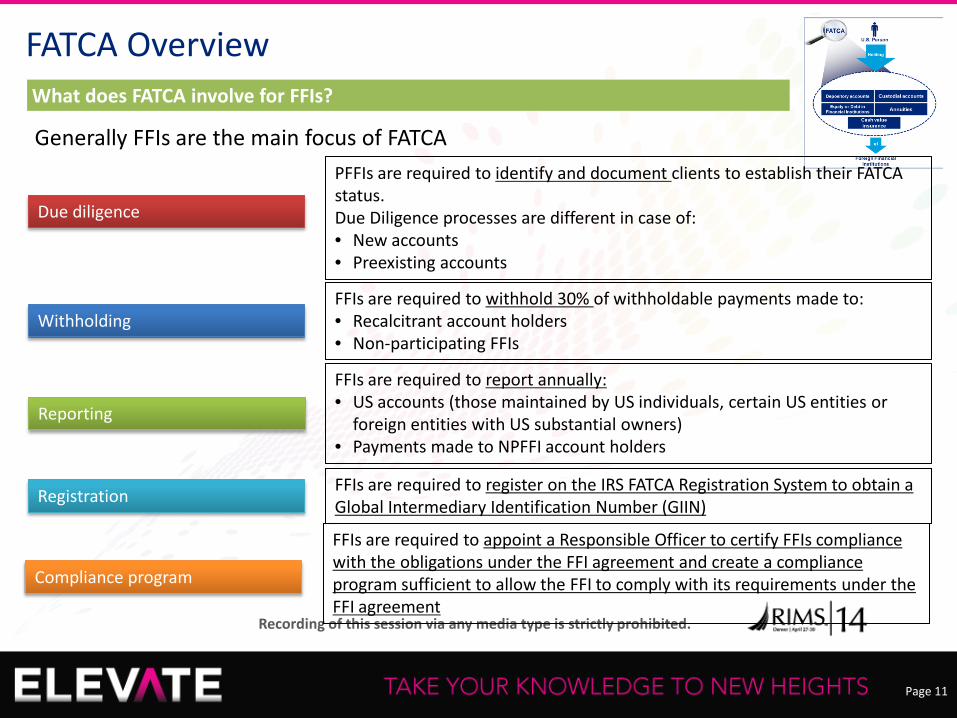

What does FATCA involve for FFIs?

FATCA Overview

Generally FFIs are the main focus of FATCA

Due diligence

Withholding

Reporting

Registration

Compliance program

PFFIs are required to identify and document clients to establish their FATCA status. Due Diligence processes are different in case of: • New accounts • Preexisting accounts

FFIs are required to withhold 30% of withholdable payments made to: • Recalcitrant account holders • Non-participating FFIs

FFIs are required to report annually: • US accounts (those maintained by US individuals, certain US entities or

foreign entities with US substantial owners) • Payments made to NPFFI account holders

FFIs are required to register on the IRS FATCA Registration System to obtain a Global Intermediary Identification Number (GIIN)

FFIs are required to appoint a Responsible Officer to certify FFIs compliance with the obligations under the FFI agreement and create a compliance program sufficient to allow the FFI to comply with its requirements under the FFI agreement

Page 12

Recording of this session via any media type is strictly prohibited.

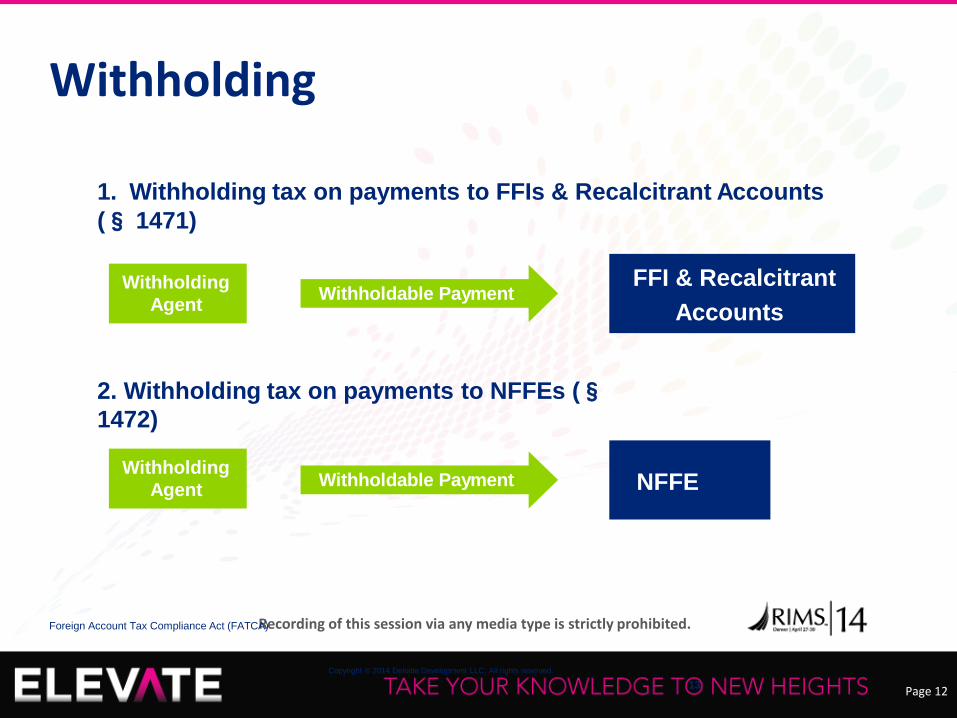

Withholdable Payment Withholding Agent

FFI & Recalcitrant Accounts

1. Withholding tax on payments to FFIs & Recalcitrant Accounts (§ 1471)

2. Withholding tax on payments to NFFEs (§ 1472)

Withholding Agent NFFE Withholdable Payment

Withholding

Foreign Account Tax Compliance Act (FATCA)

Copyright © 2014 Deloitte Development LLC. All rights reserved.

13

Page 13

Recording of this session via any media type is strictly prohibited.

Withholdable Payment

Withholdable Payments

Foreign Account Tax Compliance Act (FATCA)

Copyright © 2014 Deloitte Development LLC. All rights reserved.

14

In general: • U.S. source FDAP income • Gross proceeds from the sale or other disposition of property

of a type that can produce U.S. source interest or dividends – The term “sale or other disposition” includes “retirements and

redemptions of indebtedness” — FATCA withholding on loan principal repayments!

• Interest paid by foreign branch of U.S. bank • Foreign pass thru payments

Page 14

Recording of this session via any media type is strictly prohibited.

Withholdable Payment

Withholdable Payments

Foreign Account Tax Compliance Act (FATCA)

Copyright © 2014 Deloitte Development LLC. All rights reserved.

15

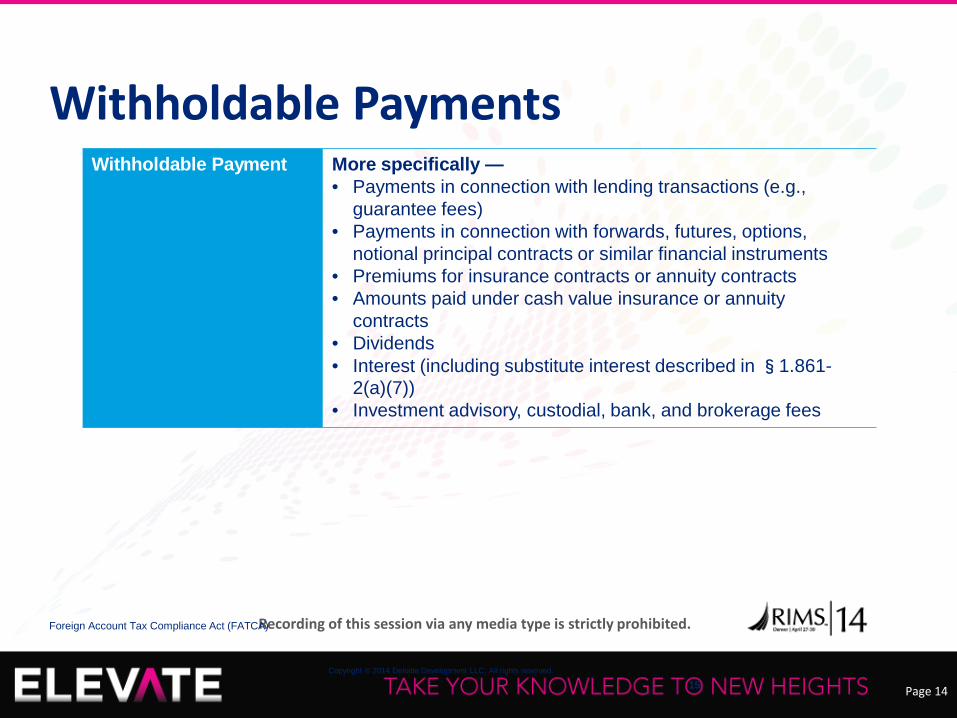

More specifically — • Payments in connection with lending transactions (e.g.,

guarantee fees) • Payments in connection with forwards, futures, options,

notional principal contracts or similar financial instruments • Premiums for insurance contracts or annuity contracts • Amounts paid under cash value insurance or annuity

contracts • Dividends • Interest (including substitute interest described in §1.861-

2(a)(7)) • Investment advisory, custodial, bank, and brokerage fees

Page 15

Recording of this session via any media type is strictly prohibited.

Withholdable Payment

Withholdable Payments – Exceptions

Foreign Account Tax Compliance Act (FATCA)

Copyright © 2014 Deloitte Development LLC. All rights reserved.

16

Exceptions — payments for: • Interest on outstanding accounts payable arising from the

acquisition of goods or services • Services (including wages and other forms of employee

compensation (such as stock options)) • The use of property • Office and equipment leases • Software licenses • Transportation and freight • Gambling winnings, awards, prizes, and scholarships • Effectively connected income • “Grandfathered obligations”

Page 16

Recording of this session via any media type is strictly prohibited.

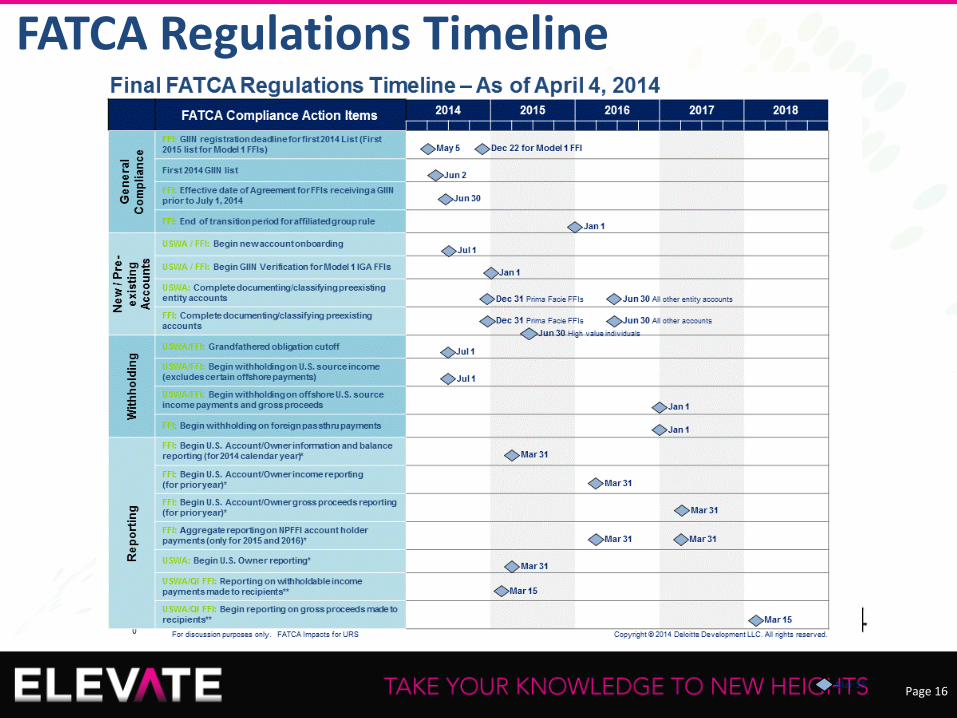

FATCA Regulations Timeline

Mar 15

Page 17

Recording of this session via any media type is strictly prohibited.

FATCA & IGAs

Page 18

Recording of this session via any media type is strictly prohibited.

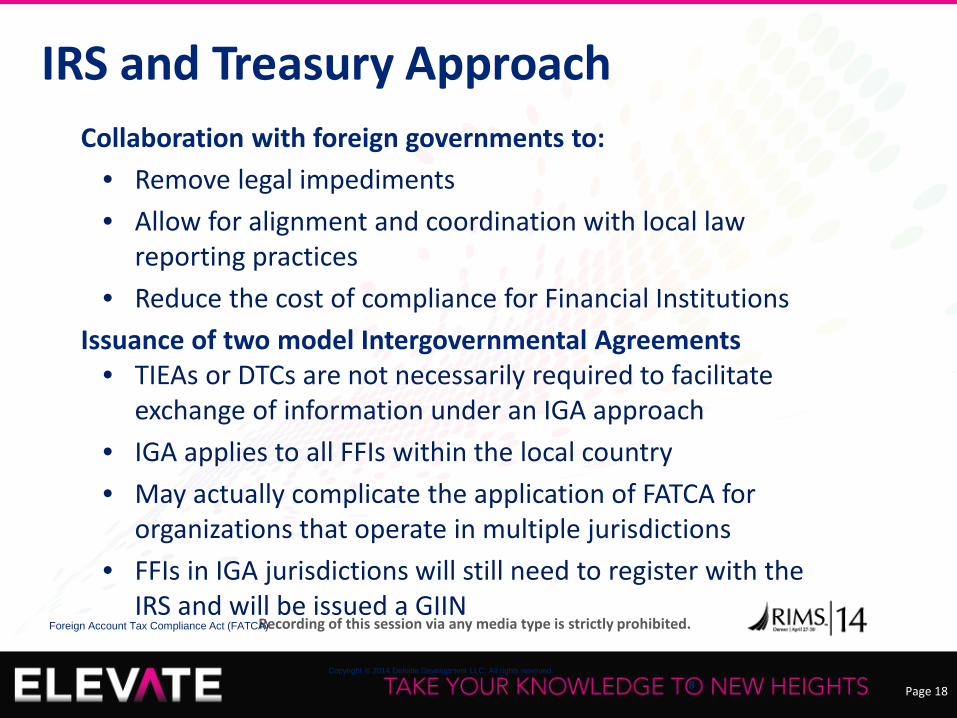

IRS and Treasury Approach

Foreign Account Tax Compliance Act (FATCA)

Copyright © 2014 Deloitte Development LLC. All rights reserved.

8

Collaboration with foreign governments to: • Remove legal impediments • Allow for alignment and coordination with local law

reporting practices • Reduce the cost of compliance for Financial Institutions

Issuance of two model Intergovernmental Agreements • TIEAs or DTCs are not necessarily required to facilitate

exchange of information under an IGA approach • IGA applies to all FFIs within the local country • May actually complicate the application of FATCA for

organizations that operate in multiple jurisdictions • FFIs in IGA jurisdictions will still need to register with the

IRS and will be issued a GIIN

Page 19

Recording of this session via any media type is strictly prohibited.

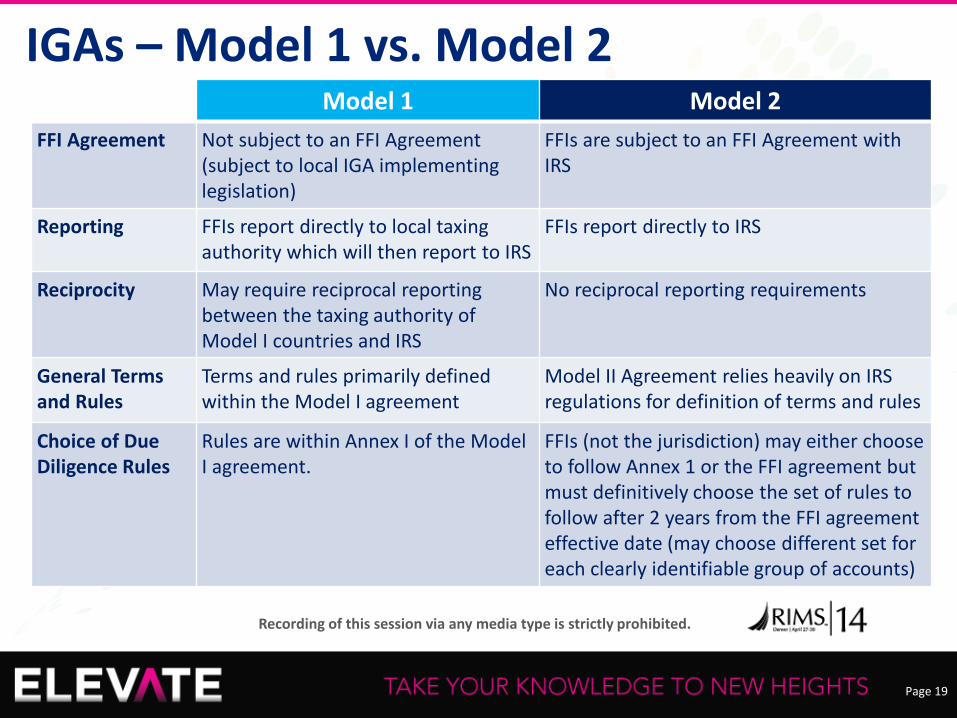

Model 1 Model 2 FFI Agreement Not subject to an FFI Agreement

(subject to local IGA implementing legislation)

FFIs are subject to an FFI Agreement with IRS

Reporting FFIs report directly to local taxing authority which will then report to IRS

FFIs report directly to IRS

Reciprocity May require reciprocal reporting between the taxing authority of Model I countries and IRS

No reciprocal reporting requirements

General Terms and Rules

Terms and rules primarily defined within the Model I agreement

Model II Agreement relies heavily on IRS regulations for definition of terms and rules

Choice of Due Diligence Rules

Rules are within Annex I of the Model I agreement.

FFIs (not the jurisdiction) may either choose to follow Annex 1 or the FFI agreement but must definitively choose the set of rules to follow after 2 years from the FFI agreement effective date (may choose different set for each clearly identifiable group of accounts)

IGAs – Model 1 vs. Model 2

Page 20

Recording of this session via any media type is strictly prohibited.

Generally the same due diligence requirements for non IGA payees • Required to collect updated Forms W-8 • Required to validate GIIN (exception: Model I IGA FFIs have until January 1, 2015 to

provide a GIIN)

More Complicated Due diligence • Local law interpretations may mean that entities are treated differently depending on

where they are located • May need separate documentation for chapter 3 and FATCA

IGAs are still a moving target! • Many new agreements are already in negotiation and will be signed • IGAs open for renegotiation in the future and may be terminated • IGAs may be modified by the contracting authorities (Favored Nation Clause)

What IGAs mean to US Withholding Agents

Page 21

Recording of this session via any media type is strictly prohibited.

Chapter 4 Status: Model I vs. Model II • Model I: Reporting Model I FFI = Registered Deemed-Compliant FFI • Model II: Sign a modified FFI agreement = Participating FFI

Reporting • Model I FFIs report directly to their local taxing authority • Model II FFIs report directly to the IRS

FFIs should be familiar with their specific IGA details • Annexes

– Vary by agreement and include due diligence and reporting standards as well as other significant terms of agreement • e.g. Mexico uses average balances for thresholds and reporting, Model 2 FFIs have a

choice of due diligence rules (those outlined in Annex 1 or those in the FFI agreement)

– Annexes also define what local products are in-scope and exempt

What IGAs mean to FFIs

Page 22

Recording of this session via any media type is strictly prohibited.

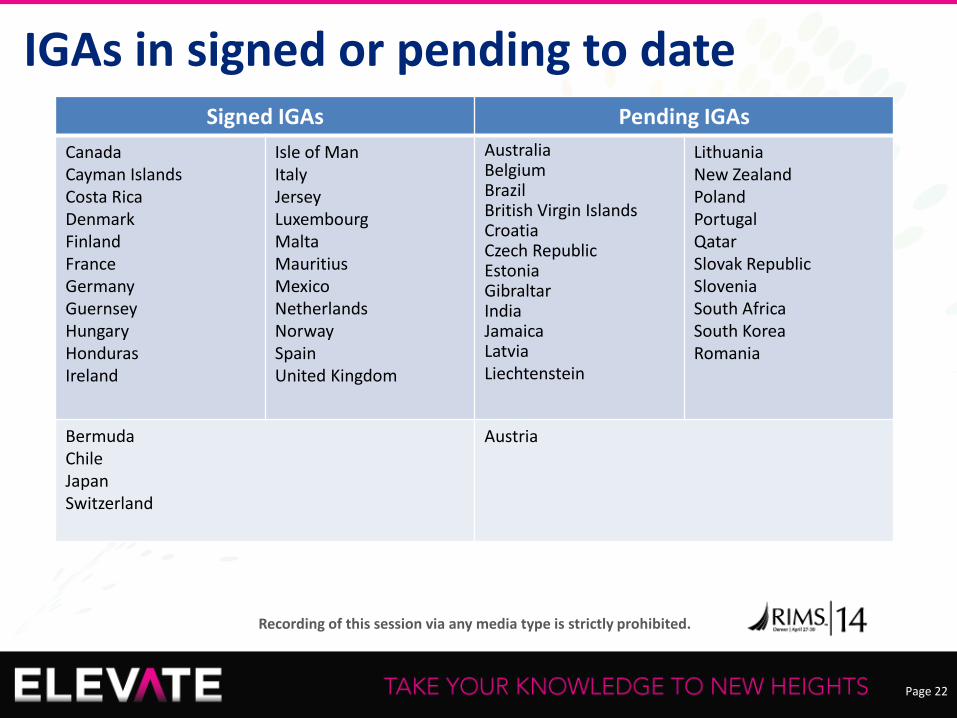

IGAs in signed or pending to date Signed IGAs Pending IGAs

Canada Cayman Islands Costa Rica Denmark Finland France Germany Guernsey Hungary Honduras Ireland

Isle of Man Italy Jersey Luxembourg Malta Mauritius Mexico Netherlands Norway Spain United Kingdom

Australia Belgium Brazil British Virgin Islands Croatia Czech Republic Estonia Gibraltar India Jamaica Latvia Liechtenstein

Lithuania New Zealand Poland Portugal Qatar Slovak Republic Slovenia South Africa South Korea Romania

Bermuda Chile Japan Switzerland

Austria

Page 23

Recording of this session via any media type is strictly prohibited.

FATCA at the OECD Level

Page 24

Recording of this session via any media type is strictly prohibited.

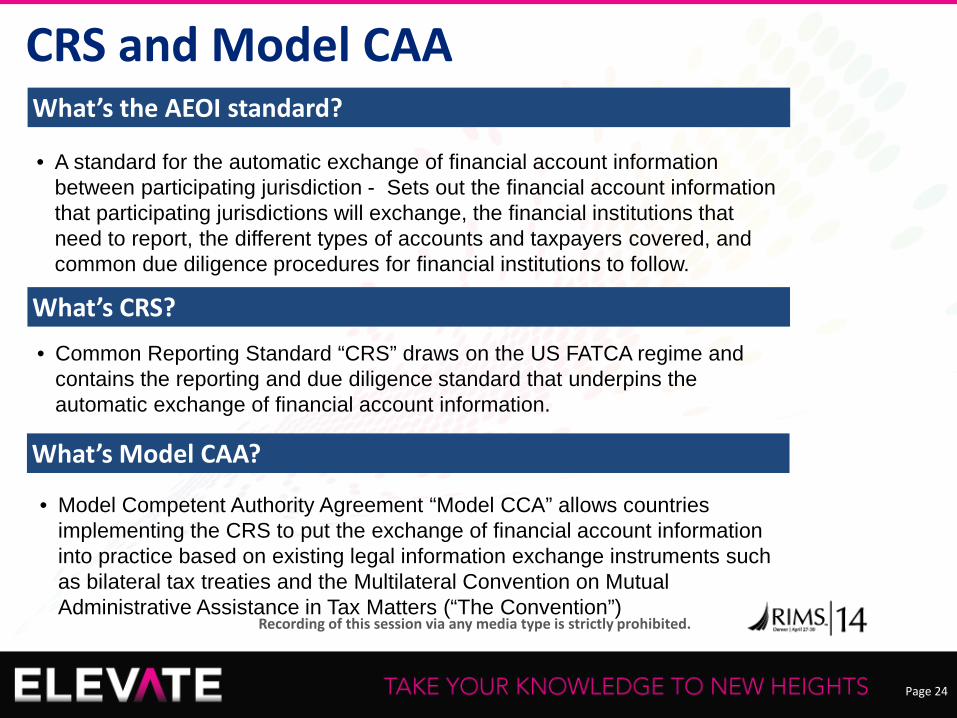

• Model Competent Authority Agreement “Model CCA” allows countries implementing the CRS to put the exchange of financial account information into practice based on existing legal information exchange instruments such as bilateral tax treaties and the Multilateral Convention on Mutual Administrative Assistance in Tax Matters (“The Convention”)

CRS and Model CAA

What’s CRS?

• Common Reporting Standard “CRS” draws on the US FATCA regime and contains the reporting and due diligence standard that underpins the automatic exchange of financial account information.

What’s Model CAA?

What’s the AEOI standard?

• A standard for the automatic exchange of financial account information between participating jurisdiction - Sets out the financial account information that participating jurisdictions will exchange, the financial institutions that need to report, the different types of accounts and taxpayers covered, and common due diligence procedures for financial institutions to follow.

Page 25

Recording of this session via any media type is strictly prohibited. OECD Resident Financial Institutions

Equity or Debt in Certain Financial Institutions

Cash value insurance

at

Annuities

Resident in Signatory country

Depository accounts Custodial accounts

AEOI

Holding

AEOI aims to identify resident persons trying to avoid tax obligations in their countries of residence by holding assets in structures and products…

AEOI Overview

Financial Institutions (FIs) are required to document account holders and establish Due diligence processes to report accounts on signatory countries’ individuals and entities and substantial owners of entities (regardless of the residence of the entity)

Non-Financial Entities (NFEs) are required to report substantial owners or certify residence of ownership

Compliance includes two key themes:

‒ Classifying your products and entities under CRS guidelines, and

‒ Documenting account holders and investors to confirm tax status under the CRS rules.

Big Bang approach – it is recognized that an approach allowing financial institutions to collect information on all or a wider group of non-resident accountholders from a common starting date may be desirable, even where such accountholders are not currently reportable.

Page 26

Recording of this session via any media type is strictly prohibited.

Who are the AEOI targets?

AEOI Overview

Signatory Countries’ Individuals Signatory Countries' entities Controlling persons of NFEs

• Entities that are considered tax residents in the signatory countries

• Resident controlling persons of any passive NFEs, regardless of the place of residence of the NFE

• Individuals that are considered tax residents in the signatory countries

Page 27

Recording of this session via any media type is strictly prohibited.

The timelines and requirements under IGAs and US FATCA Regulations are broadly aligned – “Go-live” dates are the same

27

2016

FATCA

IGAs

OECD FATCA

1 July 2014

1 July 2014

2015???

‘Go live’ date

31 May 2015

Before September 2015

2016???

Timelines for global information reporting compliance

Reporting date

Page 28

Recording of this session via any media type is strictly prohibited.

Considerations for Payments

Page 29

Recording of this session via any media type is strictly prohibited.

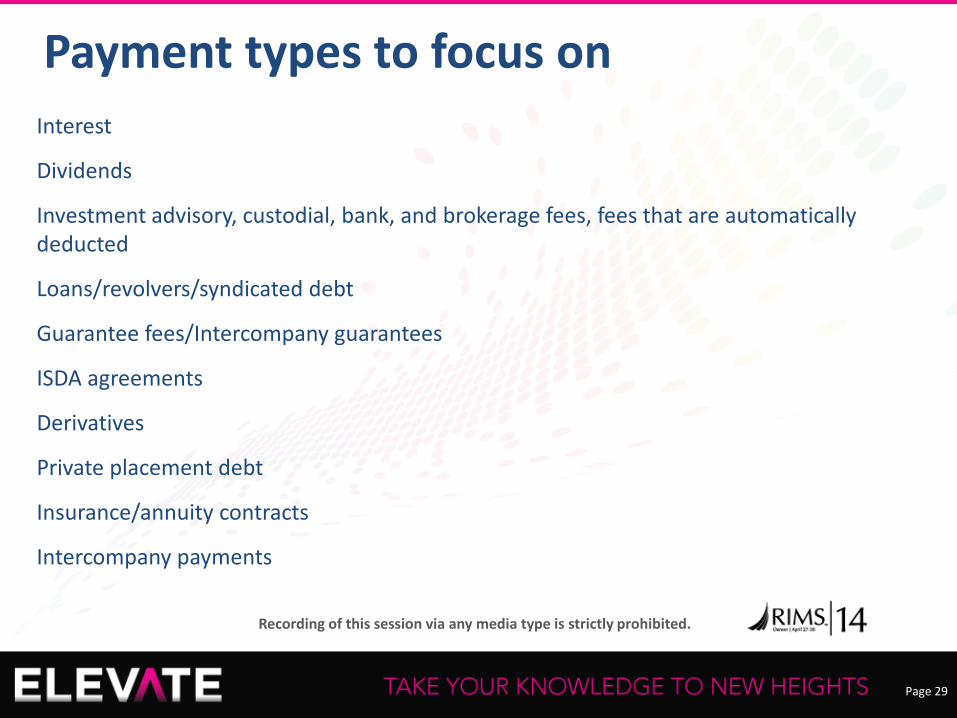

Interest

Dividends

Investment advisory, custodial, bank, and brokerage fees, fees that are automatically deducted

Loans/revolvers/syndicated debt

Guarantee fees/Intercompany guarantees

ISDA agreements

Derivatives

Private placement debt

Insurance/annuity contracts

Intercompany payments

Payment types to focus on

Page 30

Recording of this session via any media type is strictly prohibited.

30

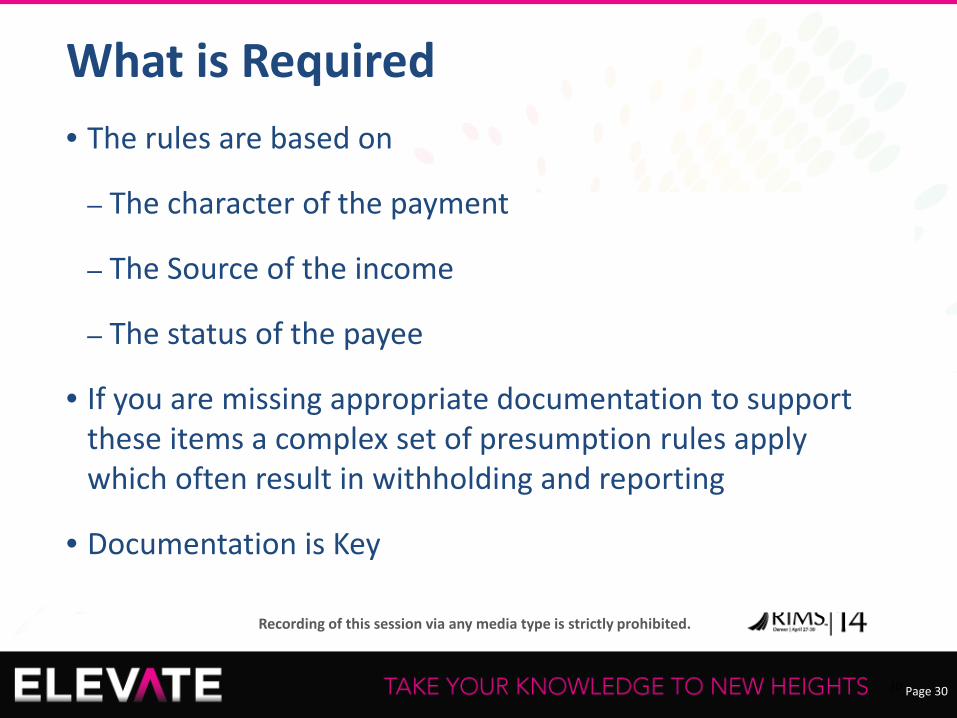

What is Required • The rules are based on

– The character of the payment

– The Source of the income

– The status of the payee

• If you are missing appropriate documentation to support these items a complex set of presumption rules apply which often result in withholding and reporting

• Documentation is Key

Page 31

Recording of this session via any media type is strictly prohibited.

Presumption Rules…

31

• Presumption rule complexity has increased introducing variations based upon the types of income paid as well as the payee.

• Undocumented individuals are presumed to be US persons

• Without a form, a trust or partnership is presumed to be an uncertified U.S. non-exempt payee subject to backup withholding and Form 1099 reporting.

• Without a tax Form, the “Bad 8” entities must be treated as NPFFI subject to 30% FATCA withholding and Form 1042-S reporting. The ‘Bad 8’ include:

– Corporations, foreign governments, international organizations, foreign central banks of issue, financial institutions, brokerage firms, nominees/custodians and swap dealers.

Page 32

Recording of this session via any media type is strictly prohibited.

Presumption Rules…

32

• Without a tax Form, other types of entity payees presumed to be an exempt recipient, but subject to indicia testing (note: added foreign telephone number as type of foreign indicia for accounts opened on or after July 1, 2014).

• ECI Presumption for US branch of foreign bank or insurance company now requires an EIN. If EIN is not provided, the presumption is it is just like any other foreign payee subject to Chapter 4 or Chapter 3 withholding.

• Joint account holders with an undocumented joint payee that does not appear to be an individual are presumed NPFFI.

• If all the joint owners are individuals, and no tax certification form is provided, the account is subject to 28% backup withholding on all Form 1099 reportable payments.

• If all the joint owners are individuals, and any account owner provides a Form W-9, that person must be identified as the primary taxpayer and the account is subject to Form 1099 reporting to that person.

Page 33

Recording of this session via any media type is strictly prohibited.

• FATCA generally applies to financial transactions that entities engage in on a regular basis in support of operations

– Financing – Hedging (e.g., via notional principal contracts)

• Financing: FATCA requires new provisions in credit agreements and other loan documents to address allocation of FATCA risk, including (i) representations and covenants from the parties and (ii) withholding and gross-up provisions for loans that are made (or materially amended) after January 1, 2014

• Special attention must be given to gross-up clauses

– The term “sale or other disposition” includes the retirement or redemption of indebtedness — gross proceeds withholding will make FATCA applicable to BOTH the principal and interest portions of loan payments starting in 2017

Additional areas of focus

Page 34

Recording of this session via any media type is strictly prohibited.

What Should Risk Officers be Considering

Page 35

Recording of this session via any media type is strictly prohibited.

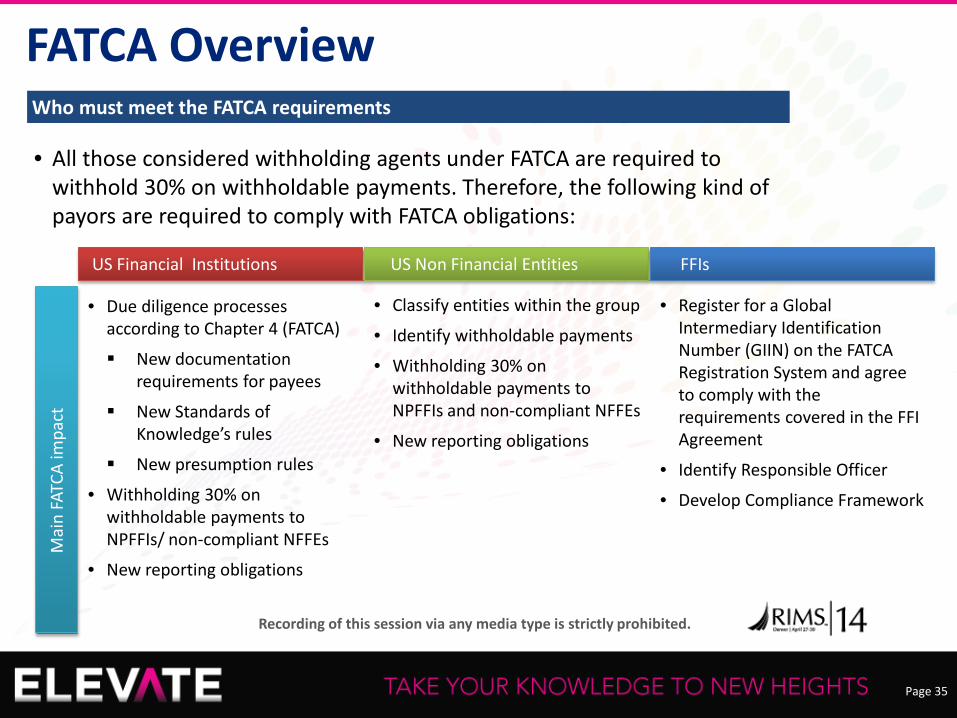

Who must meet the FATCA requirements

FATCA Overview

• All those considered withholding agents under FATCA are required to withhold 30% on withholdable payments. Therefore, the following kind of payors are required to comply with FATCA obligations:

US Financial Institutions US Non Financial Entities FFIs

• Due diligence processes according to Chapter 4 (FATCA)

New documentation requirements for payees

New Standards of Knowledge’s rules

New presumption rules

• Withholding 30% on withholdable payments to NPFFIs/ non-compliant NFFEs

• New reporting obligations

• Classify entities within the group

• Identify withholdable payments

• Withholding 30% on withholdable payments to NPFFIs and non-compliant NFFEs

• New reporting obligations

• Register for a Global Intermediary Identification Number (GIIN) on the FATCA Registration System and agree to comply with the requirements covered in the FFI Agreement

• Identify Responsible Officer

• Develop Compliance Framework

Mai

n FA

TCA

impa

ct

Page 36

Recording of this session via any media type is strictly prohibited.

• What are some risk mitigation strategies you can employ in your organization to limit liability for your organization?

• What are some risk mitigation strategies you can employ in your organization to limit your personal liability?

Risk mitigation strategies

Page 37

Recording of this session via any media type is strictly prohibited.

• Legal Entity Management • Customer Due Diligence • Management and Validation of Customer Tax Documentation • Payments Withholding and Depositing • Reporting (Forms 8966 and 1042/1042-S) • Responsible Officer Certifications • Intergovernmental Agreements Compliance

What areas should a Risk Officer monitor to ensure FATCA compliance?

Page 38

Recording of this session via any media type is strictly prohibited.

A process must be created to manage the classification and registration of new and preexisting legal entities with the EAG. • Review pre-existing legal entities

o Affected lines of business (“LOBs”) must review their legal entities, including special-purpose entities and special-purpose vehicles to determine if the entities should be classified as USWAs, FFIs, or NFFEs.

o LOBs should also identify and review branches (which include disregarded entities) with operations in non-U.S. jurisdictions as they will be included in an FFI’s registration.

• Process for new legal entities o A process must be established for identifying the status of all new legal entities when they

are created. o If a new legal entity is part of a class that requires registration, then notice should be sent to a

responsible officer or a responsible officer may need to be identified.

Legal entity management

Page 39

Recording of this session via any media type is strictly prohibited.

Confirm that appropriate customer due diligence has been performed to collect, verify, validate, and store data on customers (both new and pre-existing) as required by FATCA to classify customers and payees.

These efforts include: • Identification of payments • Performance of due diligence procedures for new and pre-existing accounts, including the

collection of any required documentation • Validating documentation against AML/CDD and other account information • Applying presumption rules when no documentation to classify as recalcitrant, nonparticipating or

noncompliant • Monitoring for U.S. indicia, inconsistencies or inaccuracies in customer data • Obtaining privacy waivers or closing/transferring accounts if not obtained • Verifying GIINs and tracking grace periods • Tracking U.S. ownership in passive NFFE (10%+ owners) accounts

Customer due diligence

Page 40

Recording of this session via any media type is strictly prohibited.

Affected lines of business (“LOBs”) must have procedures to manage and validate Forms W-8, W-9 and associated supporting documentation that must be collected for all accounts. Where discrepancies are identified, we must solicit the documentation or apply the presumption rules. The eyeball test will be limited from July 1, 2014.

At a minimum, the procedures must verify: • That the appropriate form was submitted for an account (including form version) • That the form has not expired • The completeness of the data in the form • The accuracy of the data in the form to ensure no discrepancies • That the form was correctly submitted (original or electronic) • That any modifications to the form (cross-outs, additions, etc.) are initialled and not prohibited

(e.g., crossing out required certifications)

The procedures must be executed whenever a new form is received. Forms may be received due to account opening or a party providing an updated form due to changed circumstances.

Tax documentation

Page 41

Recording of this session via any media type is strictly prohibited.

All withholding agents are required to deduct and remit to the IRS a 30% withholding tax on all “withholdable payments” made to nonparticipating FFIs, recalcitrant account holders, and noncompliant Passive NFFEs, unless otherwise excepted by IGAs. Withholding agents include all persons having the control, receipt, custody, disposal, or payment of any “withholdable payment.”

Notably, FFIs generally are withholding agents under this regulation. However, FFIs are generally only required to conduct withholding in scenarios where they have primary withholding responsibility, such as when acting as the originator of a U.S. source payment or a withholding qualified intermediary to a U.S. source payment.

Additionally, withholding agents will need to establish processes to handle refunds where necessary.

Withholding and depositing

Page 42

Recording of this session via any media type is strictly prohibited.

• Form 1042-S must include chapter 4 reportable amounts made during the year to payees that are: o Recalcitrant account holders o Foreign entities o U.S. persons included in a U.S. payee pool (non-U.S. payors only)

• Chapter 4 reportable amounts generally include U.S. source FDAP payments o Beginning in 2017, this will also include gross proceeds and possibly foreign passthrough

payments subject to FATCA withholding.

• Under the rules of FATCA, FFIs may be required to perform two types of reporting on an annual basis.

• U.S. account and pooled reporting on Form 8966 o FFIs would ordinarily report this information to the IRS under the FATCA regulations, except FFIs

in Model 1 IGA jurisdictions, which would report this information to their local authority • Form 1042-S reporting of chapter 4 reportable amounts

• Participating FFIs that already have Form 1042-S reporting obligations under chapter 3 will continue that reporting and, if the recipient is not subject to FATCA withholding, will just need to reflect the exemption code for payees that are not subject to FATCA withholding.

Reporting

Page 43

Recording of this session via any media type is strictly prohibited.

• The responsible officer (or “RO”) enables FATCA compliance throughout an organization and across a variety of functions.

• He/she has a vested interest in the development and implementation of FATCA compliance policies and procedures.

• The RO determines that governance is in place to provide required supporting documentation and compliance sign-offs.

Responsible officer

Page 44

Recording of this session via any media type is strictly prohibited.

The responsible officer’s duties to the compliance program: • The responsible officer must (either personally or through designated persons) establish a

compliance program that includes policies, procedures, and processes sufficient for the participating FFI to satisfy the requirements of the FFI agreement.

• The responsible officer (or designee) must periodically review the sufficiency of the FFI’s compliance program and the FFI’s compliance with the requirements of an FFI agreement.

• The responsible officer must consider the results of these reviews in making the periodic certifications.

• The responsible officer must also ensure that the participating FFI complies with the IRS’s review of compliance.

A comprehensive compliance program

Page 45

Recording of this session via any media type is strictly prohibited.

Establishing the proper framework for FATCA compliance will be indispensable to mitigating the risks associated with a potential FATCA audit. This FATCA framework should include policies and procedures to comply with the FATCA requirements, as well as procedures for periodic reviews. These policies and procedures should be prepared for a potential audit.

Therefore, it is advisable that financial institutions implement the following: • Written policies and procedures that document the fulfillment of FATCA requirements • Written policies and procedures that verify the FATCA compliance in the financial institution or

compliance group • Testing procedures for the adequacy of the compliance program • Communications/reports to the responsible officer with metrics for assurance in responsible

officer certification sign-off

What will likely need to be developed?

Page 46

Recording of this session via any media type is strictly prohibited.

Written policies and procedures to document the fulfillment of FATCA requirements, including: • The identification processes for payees and account holders • Documentation and due diligence requirements for payees and account holders • How U.S. indicia for payees and account holders are reviewed • Withholding policies • Reporting policies • How the FFI will administer its compliance program and responsible officer certifications

Policies: Fulfillment of FATCA requirements

Page 47

Recording of this session via any media type is strictly prohibited.

Written policies and procedures to verify FATCA compliance in the financial institution or compliance group, including: • Establishing internal audit processes and document them. This will require developing a

methodology, timeframe, and other parameters associated with the internal audit process. • Documenting the findings of each periodic review with written reports that will be presented to

the responsible officer. • Establishing a process for the responsible officer to play an active role in reviewing and managing

the results of the internal audit processes. This active role could consist, for example, of establishing periodic meetings with the internal audit committee, documenting such methodology, and keeping a record of the minutes of committee meetings.

Policies: Compliance measures within the organization

Page 48

Recording of this session via any media type is strictly prohibited.

• Test cases can be developed to challenge any automated or manual processes used to confirm FATCA compliance. o Develop “dummy” legal entities, customers, and transactions. o Identify the desired result for each “dummy” case. o Measure the expected output versus the actual result. o Track the progress at each step within the process to identify weaknesses in the designed process.

• Periodically, review the actual results of a select population once the system is live. o This testing will provide greater confidence for certifications that the results are accurate. o This will also confirm that the system continues to operate as planned in the policies and procedures.

Testing procedures and periodic review

Page 49

Recording of this session via any media type is strictly prohibited.

• Reports from affected areas to measure the level of compliance for each of the various certifications that must be made.

• Internal processes to obtain subordinate certifications throughout the organization. o The main purpose for this process is that the responsible officer can create a chain of accountability

throughout the organization or compliance group. o Obtain and document underlying certifications from other relevant persons within the organization,

including those in each line of business and, in case of compliance groups, in each jurisdiction for each entity.

Measures for testing

Page 50

Recording of this session via any media type is strictly prohibited.

• Governance: Verify that the FATCA program is subject to an appropriate level of governance that includes a clear project sponsor, regular steering committee meetings, progress reports (time, cost and quality), and involvement of risk management and internal audit.

• Risks and issues: Confirm that an appropriate risk and issue management process has been established and that it is reviewed frequently. Key risks inherent in the program plan and the FATCA policy have been captured and are being appropriately managed.

• Plan and scope: Confirm that the scope of the program has been clearly defined. Review the plan to verify that the appropriate workstreams, activities, and tasks have been scheduled to meet FATCA regulation milestones. Confirm scope and plans are subject to a clearly defined change management process.

Areas to develop

Page 51

Recording of this session via any media type is strictly prohibited.

• Assumptions and decisions: Undertake a review of the assumptions and decisions log, including decision-making rationale against relevant guidance to determine that major program decisions are in line with regulations and peers.

• Technical: Assess the program technical requirements and approaches and compare them against the FATCA policy requirements and regulations.

• Controls: Review the controls in place to confirm that they have been designed effectively to address any risks that arise and check whether the controls are operating effectively (i.e., conformance testing).

• Data: Verify that data searches performed are FATCA compliant. Assess the quality of the data outputs that will be used for FATCA reporting.

Areas to develop

Page 52

Recording of this session via any media type is strictly prohibited.

Questions

Page 53

Recording of this session via any media type is strictly prohibited.

Denise Hintzke Tax Director, Global FATCA Tax Leader Deloitte Tax LLP 212.436.4792 [email protected]

Page 54

Recording of this session via any media type is strictly prohibited.

KEEP THIS SLIDE FOR EVALUATION INFORMATION/MOBILE APP ETC.

Please complete the session survey on the RIMS14 mobile application.