hong kong market outlook - implications of the cnh market symposium 2011/01rbs.pdf · -...

TRANSCRIPT

Hong Kong Market Outlook

- Implications of the CNH market

1st ASHK Investment & Risk Management Symposium

19 April 2011

Woon Khien Chia

Head of Local Markets Strategy, Asia

The Royal Bank of Scotland

tel. +65 6518 5169

Duncan Mansfield

Solutions Structurer

The Royal Bank of Scotland

tel. +852 2966 2442

21st ASHK Investment & Risk Management Symposium

The CNH roadmap

China’s market liberalisation (2002-2008) – the early days

2003 2004 2005 2006 2007 2008

Dec 03

HK banks allowed to

take CNY

deposits

Jul 07

CDB issued first CNY-denominated

bond outside

China

Dec 08

PBOC signed

bilateral currency

swap agreement

with Korea (CNY180bn). First

of 8 swap lines

Feb 04

HK became a offshore CNY

clearance

centre

Jan 07

China financial institutions allowed

to issue CNY bonds

in HK

Jul 05

CNY floated

and revalued

by 2%

against USD

31st ASHK Investment & Risk Management Symposium

The CNH roadmap

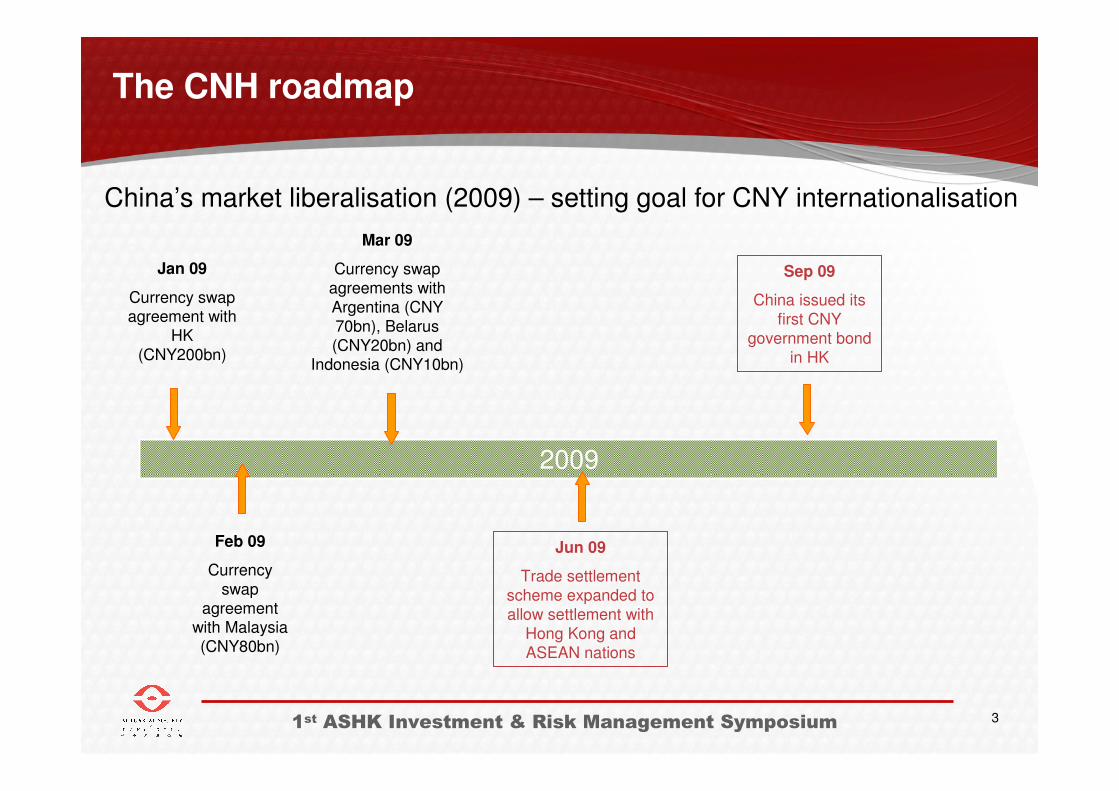

China’s market liberalisation (2009) – setting goal for CNY internationalisation

2009

Feb 09

Currency

swap

agreement with Malaysia

(CNY80bn)

Jun 09

Trade settlement

scheme expanded to

allow settlement with

Hong Kong and

ASEAN nations

Jan 09

Currency swap agreement with

HK

(CNY200bn)

Mar 09

Currency swap

agreements with

Argentina (CNY

70bn), Belarus

(CNY20bn) and Indonesia (CNY10bn)

Sep 09

China issued its

first CNY

government bond

in HK

41st ASHK Investment & Risk Management Symposium

The CNH roadmap

China’s market liberalisation (2010-2011) – the Big Bang

2010 2011

Feb 10

HKMA allowed all

forms of CNY-related fund

raising as long as

funds do not flow

back to mainland

Jun 10

Trade settlement

scheme expanded

to allow settlement

globally

Jul 10

PBOC and HKMA

signed Supplementary

Memorandum of Cooperation – paved

way for setup of CNH

interbank market

Aug 10

Foreign central banks

with CNY swap lines,

clearing & settlement banks for CNY trades

allowed to invest excess

CNY funds in onshore

interbank bond market,

subject to PBOC quota.

Dec 10

Number of onshore

firms eligible for

CNY trade

settlement was increased from 365

to 67359

Jan 11

PBOC launched pilot

programme to allow qualified domestic

firms to use CNY for

outward direct

investments.

Oct 10

HKMA took over

CNY clearing bank

role after BOC (HK)

exhausted its

conversion quota

Jun 10

CNY

returned to appreciation

path, post-

Lehamn

crisis

51st ASHK Investment & Risk Management Symposium

Potential of CNY as a world reserve currency

Share of world reserves – China vs. G3 Share of world trade – China vs. US

0%

10%

20%

30%

40%

50%

60%

48 52 56 60 64 68 72 76 80 84 88 92 96 00 04 08

China US Japan Euro Area

0%

2%

4%

6%

8%

10%

12%

14%

16%

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

China USSource: Bloomberg, RBS

61st ASHK Investment & Risk Management Symposium

0

100

200

300

400

500

600

Jul 09 Sep 09 Nov 09 Jan 10 Mar 10 May 10 Jul 10 Sep 10 Nov 10 Jan 11

0

1

2

3

4

5

6

7

8

CNY deposits in HK (% of deposits in HK, RHS) CNY trade settlement (CNY bn, LHS)

CNY trade settlement scheme huge boost to CNH deposit base

Since initiation in Nov 09, banks have cumulatively settled CNY510bn worth of trade

- roughly 80% attributable to China’s imports, 20% from its exports

- Hong Kong and Singapore probably still key countries of import origins

CNY deposits in Hong Kong poised to reach CNY700-800bn by end-2011

Source: Bloomberg, RBS

71st ASHK Investment & Risk Management Symposium

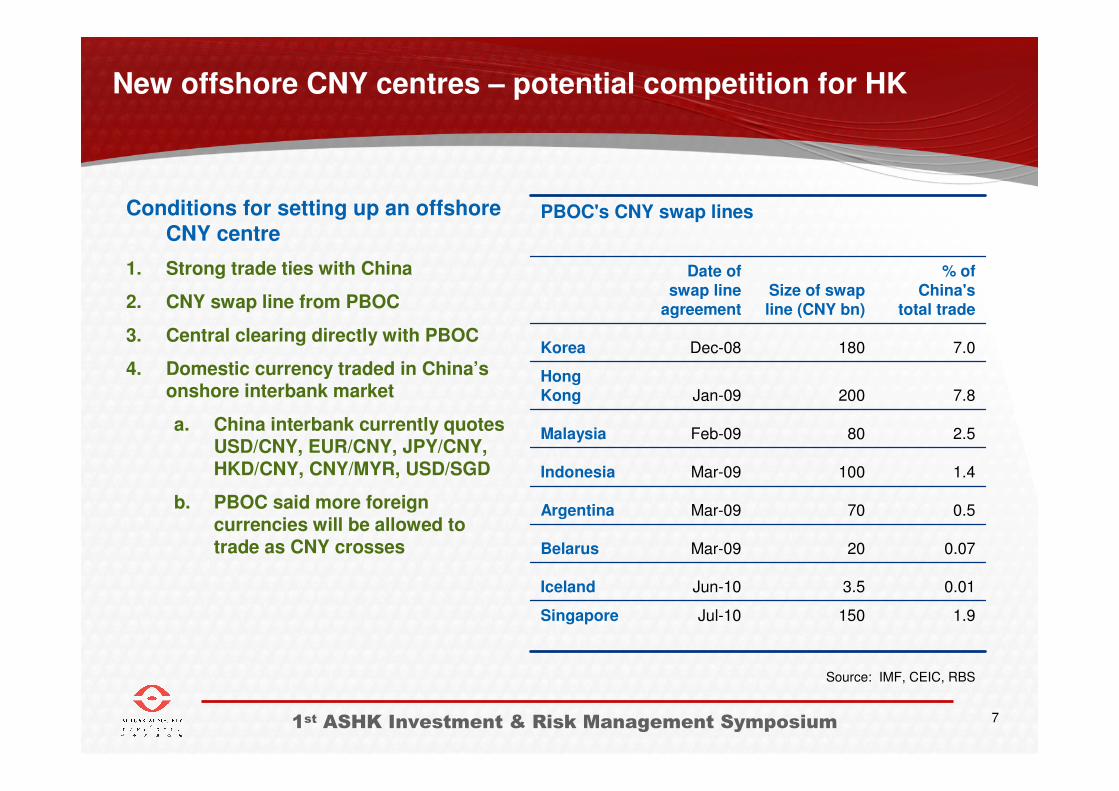

New offshore CNY centres – potential competition for HK

Conditions for setting up an offshore

CNY centre

1. Strong trade ties with China

2. CNY swap line from PBOC

3. Central clearing directly with PBOC

4. Domestic currency traded in China’s onshore interbank market

a. China interbank currently quotes USD/CNY, EUR/CNY, JPY/CNY, HKD/CNY, CNY/MYR, USD/SGD

b. PBOC said more foreign currencies will be allowed to trade as CNY crosses

Source: IMF, CEIC, RBS

1.9150Jul-10Singapore

0.013.5Jun-10Iceland

0.0720Mar-09Belarus

0.570Mar-09Argentina

1.4100Mar-09Indonesia

2.580Feb-09Malaysia

7.8200Jan-09

Hong Kong

7.0180Dec-08Korea

% of China's

total tradeSize of swap line (CNY bn)

Date of swap line

agreement

PBOC's CNY swap lines

81st ASHK Investment & Risk Management Symposium

Market anomaly 1: FX – CNH spot premium over onshore CNY spot…

From peak of 2.5%, CNH spot premium over onshore CNY spot has narrowed to 0.05%

Source: Bloomberg, RBS

6.45

6.50

6.55

6.60

6.65

6.70

6.75

6.80

6.85

23 Aug 10 23 Sep 10 23 Oct 10 23 Nov 10 23 Dec 10 23 Jan 11 23 Feb 11 23 Mar 11

-300

-100

100

300

500

700

900

1100

1300

1500

1700

Spread (pips, RHS) CNY spot CNH spot

91st ASHK Investment & Risk Management Symposium

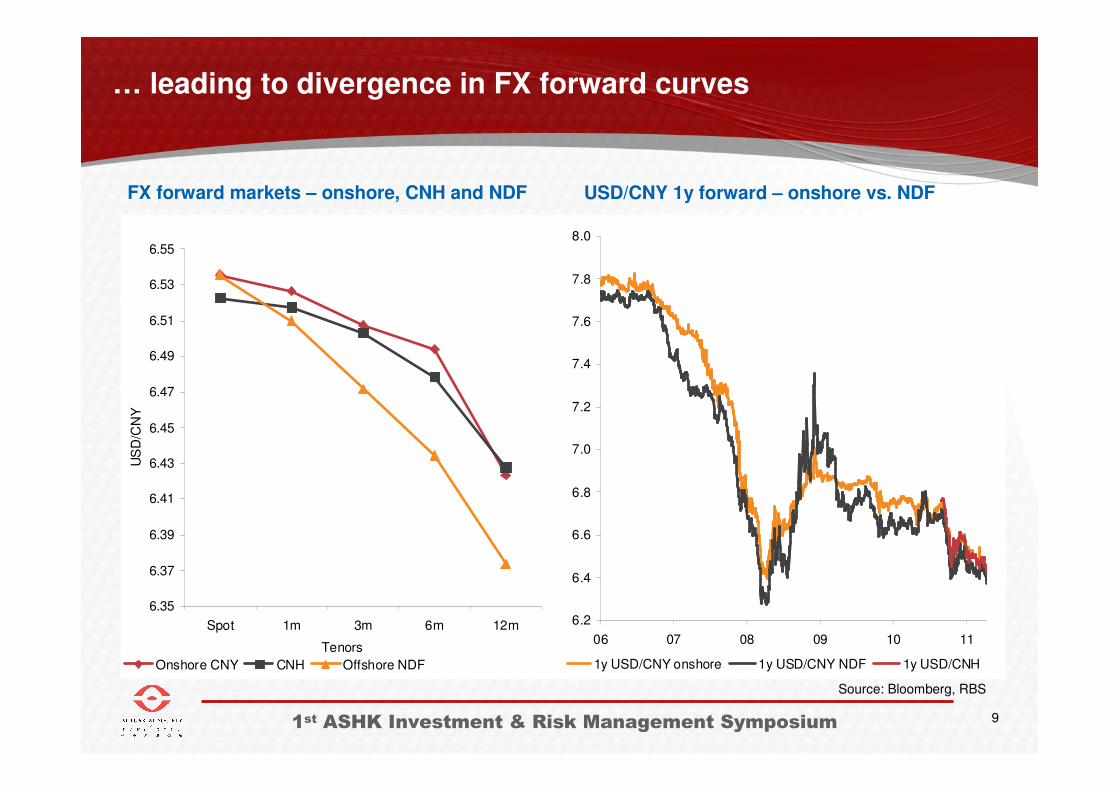

… leading to divergence in FX forward curves

FX forward markets – onshore, CNH and NDF USD/CNY 1y forward – onshore vs. NDF

Source: Bloomberg, RBS

6.2

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

8.0

06 07 08 09 10 11

1y USD/CNY onshore 1y USD/CNY NDF 1y USD/CNH

6.35

6.37

6.39

6.41

6.43

6.45

6.47

6.49

6.51

6.53

6.55

Spot 1m 3m 6m 12m

Tenors

US

D/C

NY

Onshore CNY CNH Offshore NDF

101st ASHK Investment & Risk Management Symposium

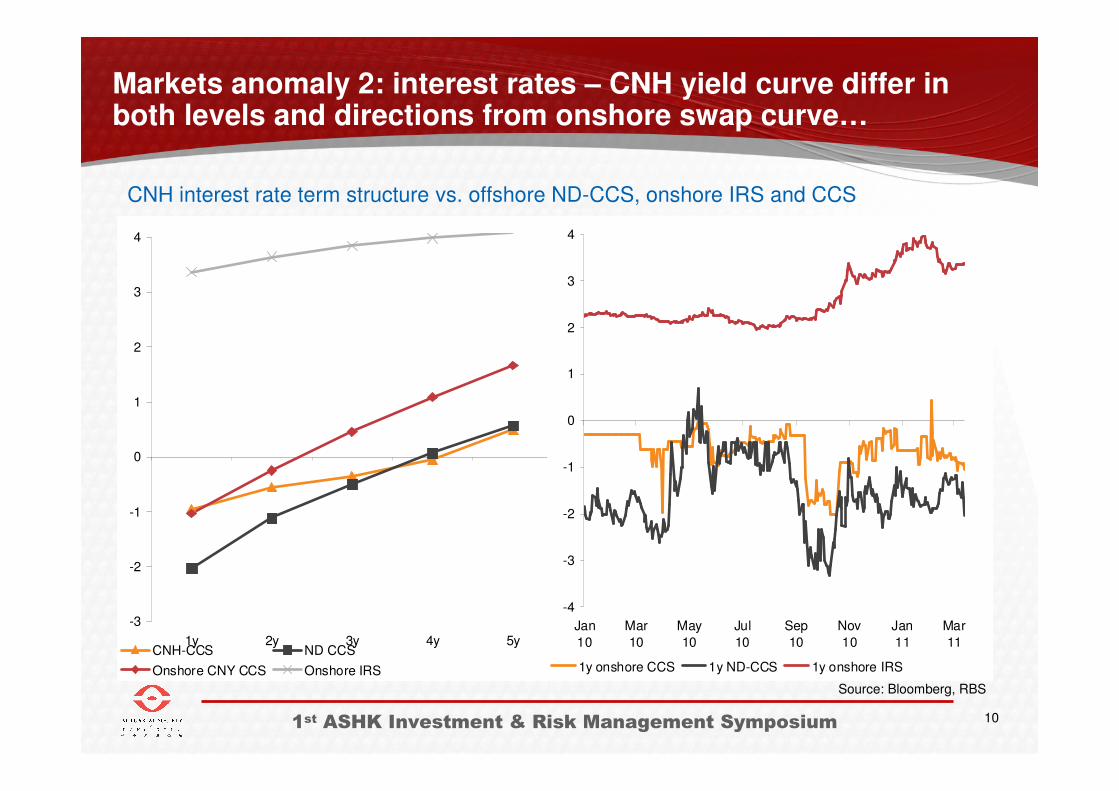

Markets anomaly 2: interest rates – CNH yield curve differ in both levels and directions from onshore swap curve…

CNH interest rate term structure vs. offshore ND-CCS, onshore IRS and CCS

Source: Bloomberg, RBS

-3

-2

-1

0

1

2

3

4

1y 2y 3y 4y 5yCNH-CCS ND CCS

Onshore CNY CCS Onshore IRS

-4

-3

-2

-1

0

1

2

3

4

Jan

10

Mar

10

May

10

Jul

10

Sep

10

Nov

10

Jan

11

Mar

11

1y onshore CCS 1y ND-CCS 1y onshore IRS

111st ASHK Investment & Risk Management Symposium

… which led to huge premium of CNH bond issues over onshore issues, including Chinese government issues

Sovereign benchmark curve set by China MOF CNH issues vs. onshore benchmark curve

Source: Bloomberg, RBS

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

CNH government benchmark Onshore government benchmark

121st ASHK Investment & Risk Management Symposium

The next phase – adding asset classes, expanding geographical coverage

•Mini QFII Scheme

China’s domestic securities houses and fund managers to directly tap into overseas investors to invest in onshore China bonds and equities

•CNY-denominated equity listing in HK

Listing CNY-denominated equities offshore; investors can exchange for CNY via liquidity facility, with profits/ losses to be converted back into HKD

•Inward foreign direct investment settlement

Allowing foreign firms to bring offshore CNY funds into China for direct investments

•More offshore CNY centres

The 4 pre-requisites

a. strong trade flows with China

b. access to PBOC’s CNY swap line

c. CNY central clearing directly with PBOC

d. trading of offshore centre’s domestic currency in China interbank market

131st ASHK Investment & Risk Management Symposium

Implications of CNH on HKD

On HKD’s dollar peg

- A re-peg is not de-peg

- CNH increased chances of HKD re-

pegging to CNY…

- … conditional on CNY becoming fully

convertible (~ 5 years’ time)

- Asset substitution – USD deposit base in

HK being eroded, not HKD deposit base

- Meanwhile, Hong Kong’ strong

fundamentals allow dollar peg

On HKD interest rates

- USD rates remain anchor for HKD rates

until HKD re-pegs

- Re-peg pressure will come from CNH

rates, not onshore CNY rates

- Fortunately, CNH rates are also anchored

by USD rates…

- … as long as China maintain border

control between CNH and onshore CNY

- Bigger uncertainty is in USD rates – when

will Fed starts hiking? when will it unwind

QE?

141st ASHK Investment & Risk Management Symposium

History of HKD dollar peg

7.60

7.65

7.70

7.75

7.80

7.85

7.90

7.95

99 00 01 02 03 04 05 06 07 08 09 10 11

6.4

6.6

6.8

7.0

7.2

7.4

7.6

7.8

8.0

8.2

8.4

USD/HKD spot USD/HKD 1 yr Upper CU Lower CU USD/CNY(RHS)

Source: Bloomberg, RBS

USD/HKD forwards have not priced in resumption of CNY appreciation plus growth of CNH

151st ASHK Investment & Risk Management Symposium

“Asset substitution” underway

CNH deposits are eroding USD deposits, not HKD deposits

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

HKD USD CNY Other fcy

HKD trn

0

10

20

30

40

50

60

70

80

90

100

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

HKD USD CNY Other fcy

% share

Source: Bloomberg, RBS

161st ASHK Investment & Risk Management Symposium

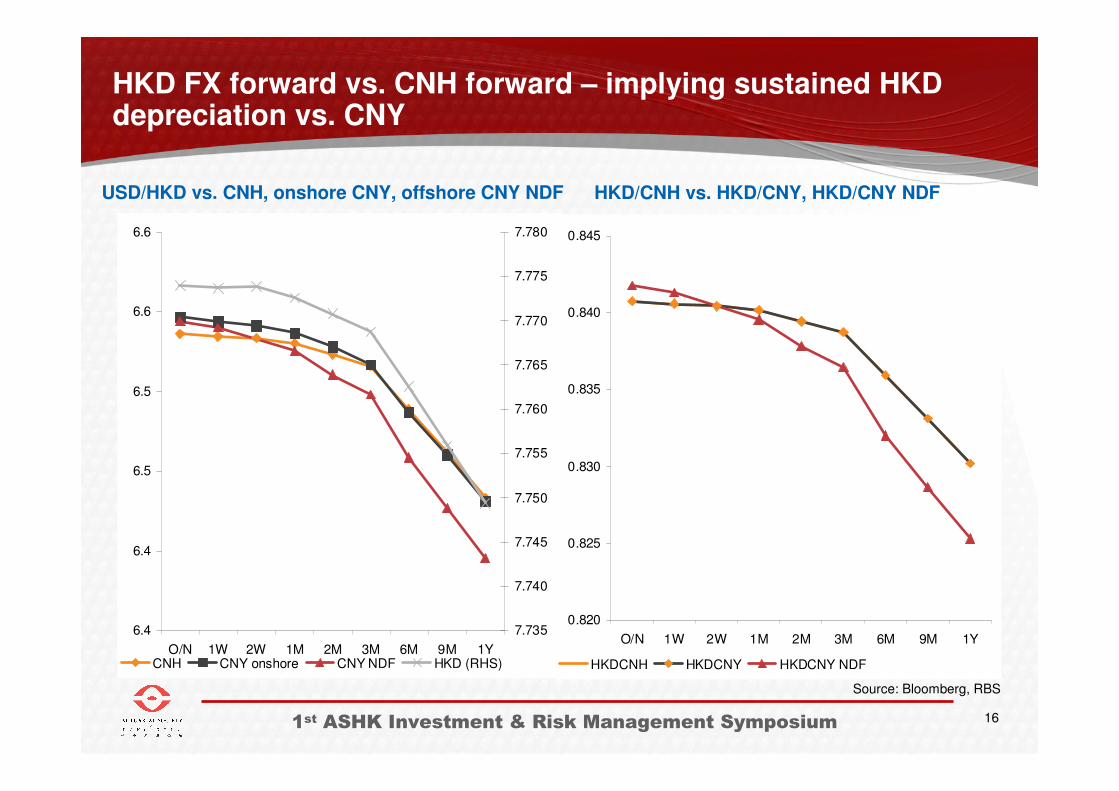

HKD FX forward vs. CNH forward – implying sustained HKD depreciation vs. CNY

USD/HKD vs. CNH, onshore CNY, offshore CNY NDF HKD/CNH vs. HKD/CNY, HKD/CNY NDF

6.4

6.4

6.5

6.5

6.6

6.6

O/N 1W 2W 1M 2M 3M 6M 9M 1Y

7.735

7.740

7.745

7.750

7.755

7.760

7.765

7.770

7.775

7.780

CNH CNY onshore CNY NDF HKD (RHS)

0.820

0.825

0.830

0.835

0.840

0.845

O/N 1W 2W 1M 2M 3M 6M 9M 1Y

HKDCNH HKDCNY HKDCNY NDF

Source: Bloomberg, RBS

171st ASHK Investment & Risk Management Symposium

HKD interest rates vs. CNH rates – anomaly between interbank deposit rates and implied swap offer rates

Interbank rates – hibor vs. CN-hibor, Libor Rates implied from FX forward curves

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

O/N 1W 2W 1M 2M 3M 6M 9M 1Y

CNH USD HKD

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

O/N 1M 2M 3M 6M 9M 1Y

CNH CNY onshore CNY NDF HKD USD Libor

Source: Bloomberg, RBS

181st ASHK Investment & Risk Management Symposium

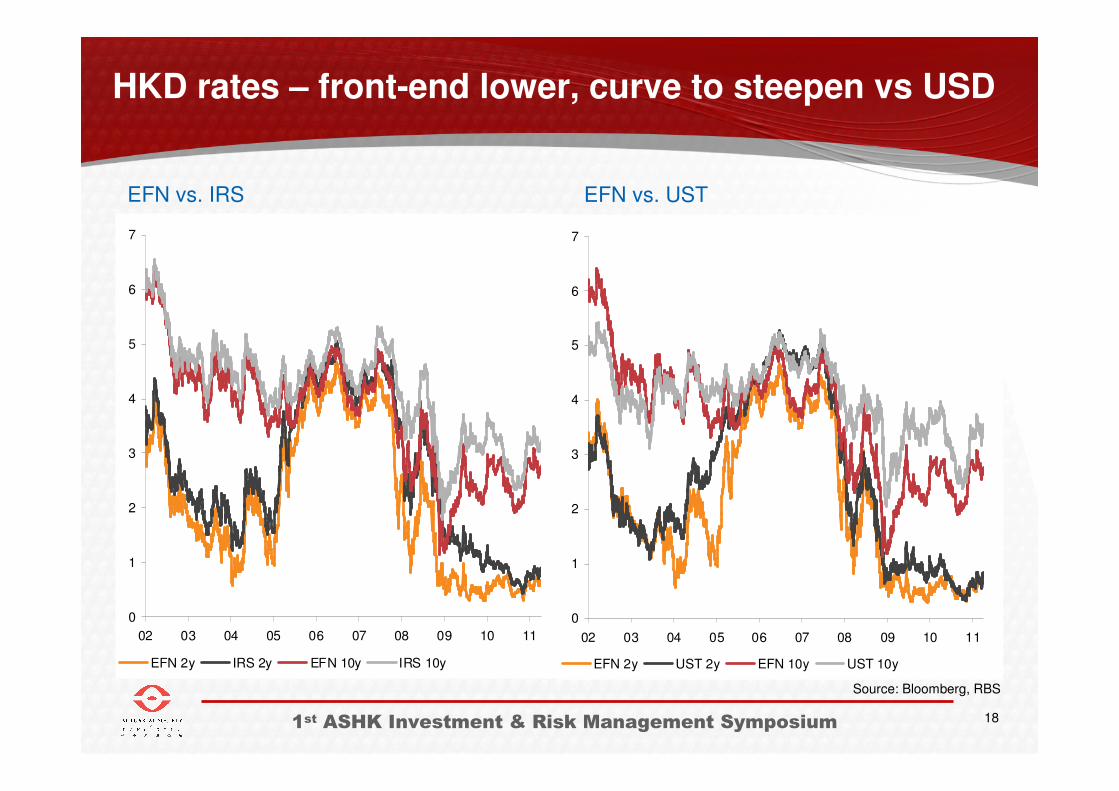

HKD rates – front-end lower, curve to steepen vs USD

EFN vs. IRS EFN vs. UST

0

1

2

3

4

5

6

7

02 03 04 05 06 07 08 09 10 11

EFN 2y IRS 2y EFN 10y IRS 10y

0

1

2

3

4

5

6

7

02 03 04 05 06 07 08 09 10 11

EFN 2y UST 2y EFN 10y UST 10y

Source: Bloomberg, RBS

191st ASHK Investment & Risk Management Symposium

The CNH Market

• Types of CNH products

• CNY, CNH and CNY NDF compared

• CNH market liquidity

• Examples of CNH FX investment products

201st ASHK Investment & Risk Management Symposium

Overview

• CNH market – developing and does not offer the liquidity many need to

hedge their risks

• Onshore CNY – generally not open to Hong Kong investors and

involves CNY/CNH basis risk

• CNY NDF/NDS – better liquidity than CNH but also involves basis risk

• Some structured investment products are available for participants to reduce or increase exposure to CNH/HKD and/or provide better

yields than CNH money markets

211st ASHK Investment & Risk Management Symposium

Snapshot of CNH-denominated product availability

Hong Kong CNH bond market continues to build YesBonds

Fully funded structures so far Not allStructured products

Illiquid YesFX options

CDs launched; structured notes and deposits in early development stage

Yes for CDsCDs/structured notes

Interbank trading relatively thin amid CNH ‘pooling’ in small number of institutions

YesMoney market

IlliquidYesCCS

There are now CNY DF, CNY NDF and CNH DF curves YesForward

USD 500mn interbank volumes YesSpot

Remarks AvailabilityCNH product

221st ASHK Investment & Risk Management Symposium

CNH vs. onshore CNY and offshore CNY NDF

NDF: Out to 1y

NDS: Liquid out to 5 years, some liquidity out to 10

years

Deep Spot and forward to 3 months, modest liquidity at

1 yearDeep Spot and forward to 1yLiquidity

NoneTrade documents for

transfers into/out of China

Trade documents, or PBOC/SAFE approvals for

capital account transactions

Documentation needed

2 business days ahead of maturity

No fixingNo fixingFixing

Forwards and OptionsSpot, Forwards and OptionsSpot, Forwards and OptionsProducts available

Allowed purposes

How is it settled

Remittance into China

Remittance outside China

Freely convertible

Who is allowed to

buy/sell

Location

Current and capital account

with supporting documentation

Delivery

n.a.

No

No

Only companies in China

(with supporting documents)

China onshore

CNY

Trade purposes into China

alone, otherwise restrictions

Delivery

Yes, for trade purposes

n.a.

Yes

Everyone outside China

Abroad,

(Hong Kong for clearing)

CNH

n.a.

Cash settled in USD

n.a.

n.a.

n.a.

Everyone outside China

Abroad

CNY NDF

231st ASHK Investment & Risk Management Symposium

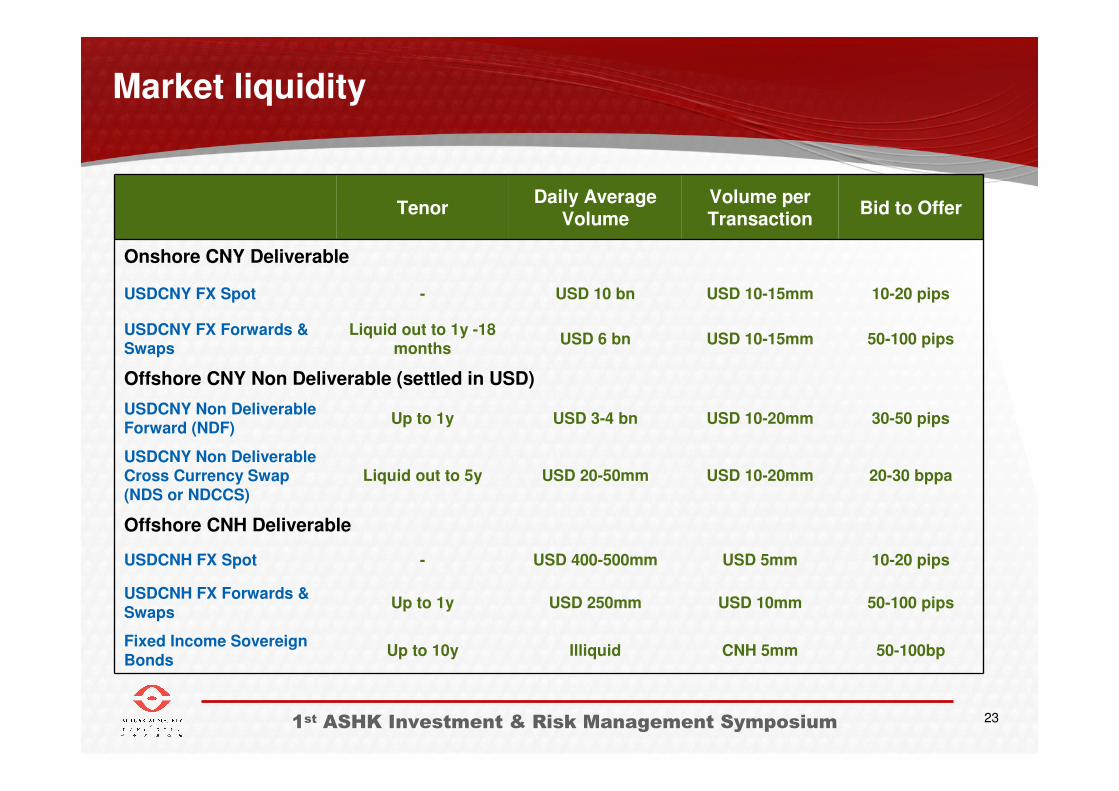

Market liquidity

Offshore CNH Deliverable

Offshore CNY Non Deliverable (settled in USD)

Onshore CNY Deliverable

Up to 10y

Up to 1y

-

Liquid out to 5y

Up to 1y

Liquid out to 1y -18 months

-

Tenor

50-100 pipsUSD 10mmUSD 250mmUSDCNH FX Forwards & Swaps

10-20 pipsUSD 5mmUSD 400-500mmUSDCNH FX Spot

USD 3-4 bn 30-50 pipsUSD 10-20mmUSDCNY Non Deliverable Forward (NDF)

20-30 bppaUSD 10-20mmUSD 20-50mmUSDCNY Non Deliverable Cross Currency Swap (NDS or NDCCS)

10-20 pipsUSD 10-15mmUSD 10 bnUSDCNY FX Spot

50-100 pipsUSD 10-15mmUSD 6 bnUSDCNY FX Forwards & Swaps

50-100bpCNH 5mmIlliquidFixed Income Sovereign Bonds

Bid to OfferVolume per Transaction

Daily Average Volume

241st ASHK Investment & Risk Management Symposium

USD dual currency investment linked to CNH

Indicative Terms & Conditions

� USD Principal : USD 10 million (equivalent to CNH Principal = CNH 65.2 million)

� USD/CNH Spot Reference : 6.5200

� Tenor : 3 Months

� Strike : 6.5200

� Redemption Conditions

- if USD/CNH Spot at expiry is above Strike, Investor receives CNH Principal with 2.0% p.a. interest

- If USD/CNH Spot at expiry is at or below Strike, Investor receives USD Principal with 2.0% p.a. interest

Rationale and Benefits

� This investment is suitable for investors who are sitting on idle USD cash and do not mind converting USD into CNH.

� Allows the investor to take advantage of the implied (from the FX market) and real (from the depo) CNH yield difference as well as access to the CNH option market

� This investment offers higher returns compared to the vanilla money market rates or the sell/buy USD/CNH FX swap plus CNH deposit structure (USD 1.00% p.a.)

Risks

� If there is depreciation on the Renminbi, the investor could be receiving less than his original invested principal in USD terms.

251st ASHK Investment & Risk Management Symposium

CNY Credit Linked Note

Indicative Terms & Conditions

� CNY Principal : CNY 200 million, settled in Settlement Currency

� Reference Obligation : China Sovereign

� Tenor : 5 years

� Coupon : CNY 2.50% p.a. settled in Settlement Currency

� Redemption : 100% at maturity, or in event of default the recovery value after close-out of

hedges, settled in Settlement Currency

� Settlement Currency : USD or HKD (as mutually agreed on Trade Date) using onshore SpotReferences

Rationale and Benefits

� This investment is suitable for investors who are in need of CNY linked assets and who are comfortable with China Sovereign credit risk

� Different reference obligations can be used for a tailored risk/reward profile

� This investment offers higher returns compared to the vanilla CNH money market rates and is available to HK investors

Risks

� Basis risk between CNH and CNY for investors hedging CNH liabilities

� China Sovereign in addition to the usual issuer credit risk

261st ASHK Investment & Risk Management Symposium

Disclaimer

•This material has been prepared for information purposes only. The investments and investment services referred to herein are available only to persons to whom this

material may be lawfully delivered in accordance with applicable securities laws. This material is being distributed only to, and is directed only at, persons who have professional experience in matters relating to investments, falling within Article 19(1) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or to other persons to whom this material may lawfully be communicated. This material is not available to retail customers within the meaning of the rules of the Financial Services Authority (“FSA”). No securities (nor any related securities or other financial instruments or their related derivatives) (together “Securities") discussed herein may be offered or sold in the United States (“US”) except pursuant to an exception from the registration requirements of the Securities Act of 1933. The material should not be

construed as an offer or solicitation to buy or sell any securities or any interest in securities.

•The information contained herein is confidential and is intended for use only by the recipient (the “Recipient”). It should not be reproduced or disclosed to any other personwithout the consent of The Royal Bank of Scotland plc. The material remains the property of The Royal Bank of Scotland plc and/or its affiliates (“RBS”) and must be

returned to RBS on request and any copies the Recipient has made must be destroyed.

•The information contained herein has been prepared by RBS on the basis of information provided by the issuer or one of more of its affiliates to assist interested parties in making a preliminary analysis of this Private Placement transaction and does not purport to be all-inclusive or to contain all of the information that a prospective investor

may require to make a full analysis of the transaction.

•The terms of this presentation are qualified in their entirety by the Information Memorandum, which will be made available by RBS in respect of the transaction described herein, which will supersede the terms hereof.

•This material is distributed on the express understanding that, whilst the information in it is believed to be reliable, it has not been independently verified by RBS. RBS makes no representation or warranty (express or implied) of any nature, nor does RBS accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information in this material. This shall not, however, restrict, exclude or limit any duty or liability to any person under any applicable laws or regulations

of any jurisdiction, which may not lawfully be disclaimed.

•The Recipient of this document should make its own independent evaluation of the transaction and of the relevance and adequacy of the information in this document and should make such other investigations as it deems necessary to determine whether to participate in the transaction.

•RBS, and its connected companies, employees or clients may have an interest in the Securities mentioned in this material. This may involve activities such as dealing in,

holding, acting as market-makers, or performing financial or advisory services, in relation to any of the Securities referred to in this document. RBS may also have acted as a manager or co-manager of a public offering of such Securities, and may also have an investment banking relationship with any of the companies mentioned in this material.

•Any views or opinions (including statements or forecasts) constitute the judgement of RBS as of the date indicated and are subject to change without notice. RBS does not undertake to update this document. The Recipient should not rely on any representation or undertaking inconsistent with the above paragraphs.

•Outside the United States, this material is issued by The Royal Bank of Scotland plc which is authorised and regulated in the United Kingdom by the FSA. In the United

States, this document is issued by RBS Securities Inc. a member of FINRA and an indirect wholly-owned subsidiary of The Royal Bank of Scotland plc. RBS Securities Inc. acts as agent for The Royal Bank of Scotland plc in connection with Securities activities in the United States.

•The Royal Bank of Scotland plc acts in certain jurisdictions as the authorised agent of ABN AMRO Bank N.V.

•The Royal Bank of Scotland plc. Registered in Scotland No. 90312. Registered Office: 36 St Andrew Square, Edinburgh EH2 2YB.

•The daisy device logo, RBS, The Royal Bank of Scotland and Make it happen are trade marks of The Royal Bank of Scotland Group plc.