cnh market guide - qtxasset.com

TRANSCRIPT

rbs.com/mib

CNH Market Guide

Vol. 2

How did the offshore renminbi (CNH) market come to wield such influence on the onshore foreign exchange (FX) market?

Since May 2012, USD/CNY trading onshore has consistently pulled away from the People’s Bank of China (PBOC) daily fixing rate towards

the direction of the offshore deliverable USD/CNH.

How did the CNH bond market turn from a seller’s market to a buyer’s market recently? As investors’ expectations switch from FX to bond

gains, issuers have aligned coupons to onshore yields. Higher yields in turn have boosted investors’ appetite for longer tenors. The market

now offers bonds up to 20-year maturity.

A confluence of factors – FX and monetary policy reforms, market deregulation, private sector initiatives, and

global politico-economic events – brought about a spectacular transformation of the CNH market in its first five years.

How will the next five years look?The next phase will be a steeper climb as China attempts to globalise

its offshore CNH franchise before it can reach the final goal of becoming a world reserve currency.

This guide is a sequel to the CNH Market Guide – A precursor to internationalisation of the Chinese renminbi, which was first published

in March 2011. It addresses the various facets of a market that still stands the chance of becoming the world’s next reserve currency,

with a focus on the FX, interest rate and bond markets.

This guide provides a review of the developments in the first five years of the CNY internationalisation. It contains details of regulations,

products types, market depth and market participants. It also contains analysis of how reforms have influenced market

trends that have led to the convergence between the onshore and offshore FX, interest rate and bond markets.

Content

The Roadmap 2

The first five years 3

Market size 3

Market liquidity 6

Market depth 7

PBOC’s CNY swap lines 8

Onshore market access 10

Offshore-onshore market convergence 13

The next five years 14

Becoming fully convertible 14

Internationalising the CNY 15

FX Market 17

Evolution of the market 17

Spot 19

Forwards 20

Cross currency swaps 21

Options and futures 21

Interest Rate Market 22

Evolution of the market 22

Money market 24

Interest rate swaps 24

Sovereign benchmark curve 25

Repo market 25

Bond Market 26

Evolution of the market 26

Issuer Base 29

Types of issuers 29

Motivations and objectives 33

Issuance outlook 35

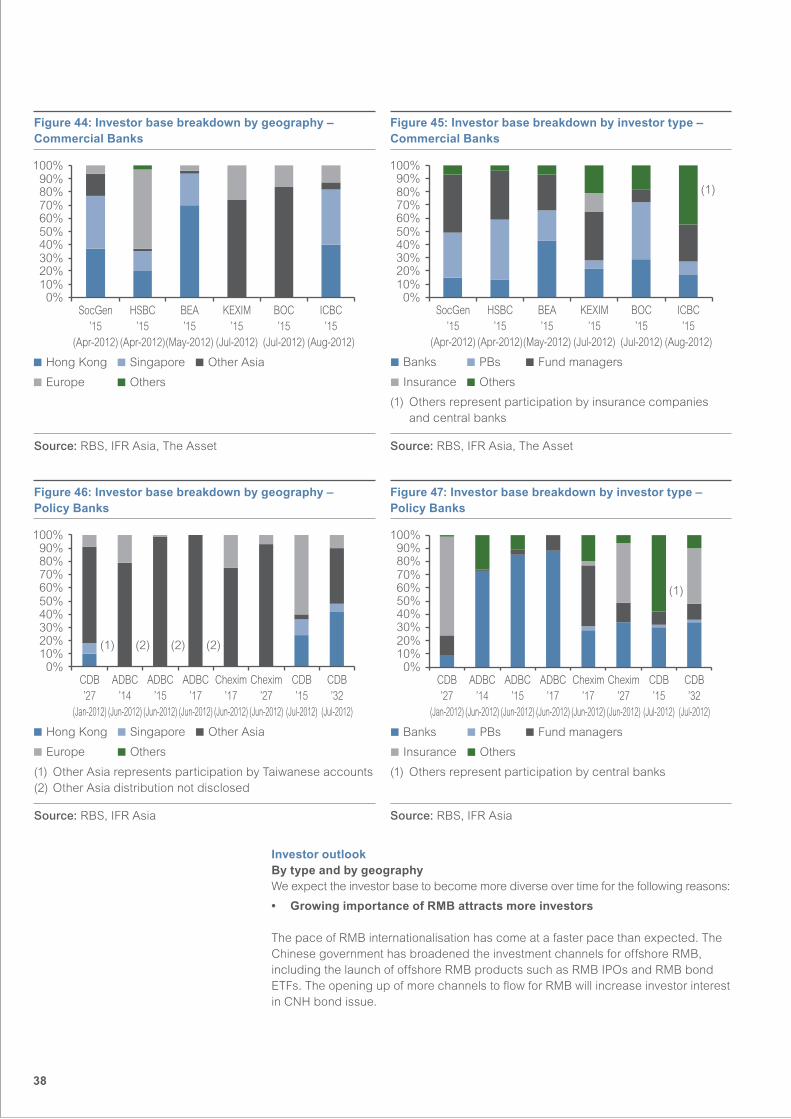

Investor base 36

Types of investors 36

Investor outlook 38

Documentation requirements 39

Listing practice 40

Reg S is the current norm 40

More rated issuers coming to the market 41

Governing law 41

Repatriation rules 42

MOFCOM vs SAFE routes 42

Other RMB schemes 44

Market Trends 44

Globalising the Franchise 46

Building on Asia’s strengths 46

Global vs regional hubs 49

Singapore as second CNY clearing centre 49

Hong Kong-London partnership 50

Self-service centres in Taipei, Tokyo, Sydney 50

Shanghai as the ultimate global CNY pricing centre 50

Multilateral platforms 51

Appendix A 52

Chronology of Regulatory Changes and Events 51

Appendix B 54

Cross-border Payments on Current Account 54

Appendix C 56

List of Abbreviations 56

Appendix D 57

List of Government Agencies 57

The RoadmapFive years after embarking on internationalising the Chinese Yuan (CNY), it is clear that the Chinese government now has a full roadmap for realising it plans. Deliverable CNY is now commonly referred to as CNH.

The first CNH bond was issued in Hong Kong, receiving mixed responses from market participants. Some saw this as an experiment by the Chinese government to gauge market acceptance of the CNY. A common area of concern was the huge price premium of the so-called “dim sum” bonds on onshore bonds. At that time, yields were benchmarked against the USD/CNY non-deliverable forward (NDF) market.

The NDF curve reflected market expectations for the CNY, which was very strong then. The curve translated into CNY interest rate levels that were well below both the USD and onshore CNY interest rates. Proving sceptics wrong, the Chinese government has opened up the market at a rapid pace in a sequence resembling a roadmap (see Figure 1):

• 2007-2008:MadeCNYdeliverable Launched CNH bonds; signed swap lines with selected central banks

• 2007-2010:ExpandedCNHliquiditypool Launched trade settlement scheme; liberalised bond issuance rules; launched

CNH interbank market

• 2011:Loopedbacktoonshore Launched CNH equities; CNY inward investment flows allowed

• 2012:Goglobal Partnering Hong Kong and London; setting up second CNY clearing centre in

Singapore; setting up dedicated lines for other key markets

Figure1:RoadmaptointernationalisationoftheRMB

Source: RBS

2003-2006Laying the ground in HK

2007-2008MakingCNYpartially deliverable

2007-2010Expanding offshore CNYliquiditypool

2011Forming a circular loop back onshore

2012Going global

• BringingCNYtoHKresidents

• FloatingtheCNY

• IntroducingCNY– denominated investment assets (bonds issued by policy banks)

• SigningCNYswap lines with strategically-targeted central banks

• LaunchingCNYtrade settlement scheme

• LiberalisingCNHbond issuance rules

•Makingitwholesale– setting up CNH interbank market

• IntroducingCNY–denominated equity IPO

• Allowing outward FDI

• Launching Renminbi QFII

• Allowing inward FDI

• PromotingLondonas global offshore RMB centre

• PromotingCNYasreserve currency to cash-rich central banks

• SettingsecondCNYclearing centre in Singapore

2

Growing liquidity pool, deepening the markets, expanding the geographical reach

The first five years

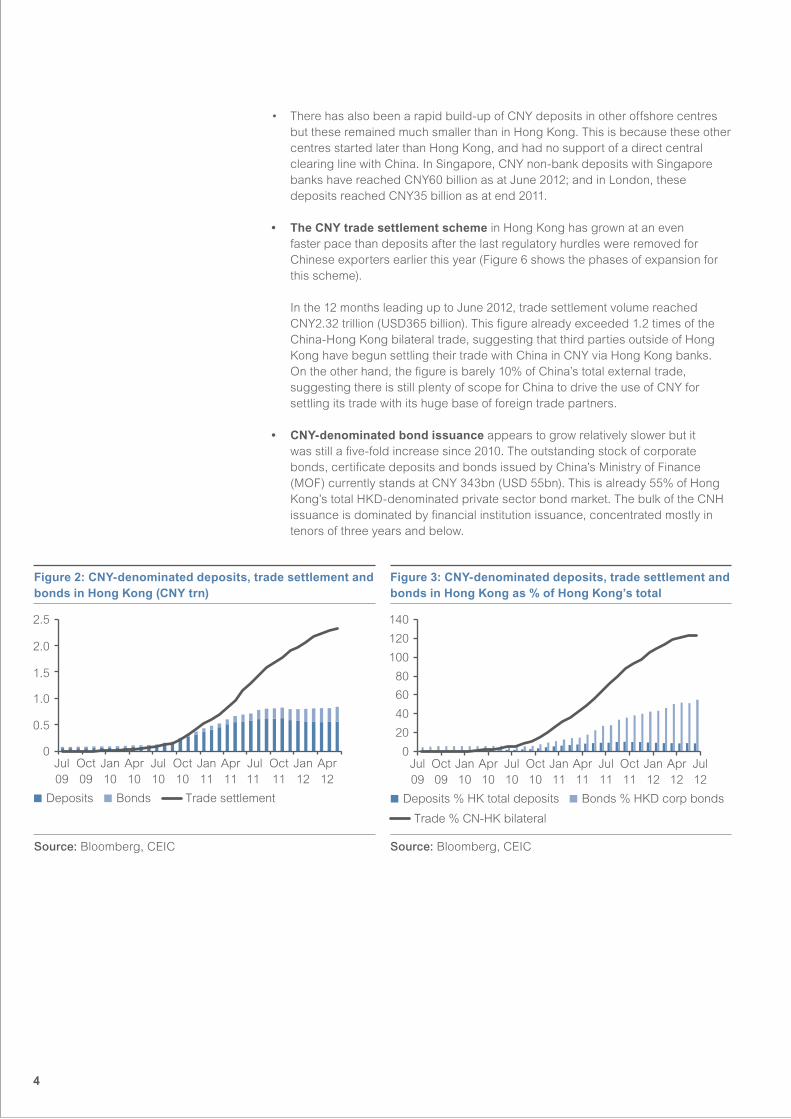

The first five years of the CNH market focused mainly on growing the liquidity pool in Hong Kong, and deepening the FX and bond markets. It was only in 2011 that the focus switched to expanding the market outside of Hong Kong – starting within Asia, notably Singapore and Japan, and more recently further afield to London. The market has grown multi-fold since its launch in 2007, measured in deposits, trade settlement volume and bond issuance (see Figures 2 and 3).

Market size• CNYdepositsinHongKonghavegrownten-foldsincelate2009.Withresident

deposits at CNY558 billion (USD88 billion) as of June 2012, deposits account for 8.8% of Hong Kong banks’ total deposit base or 17.5% of their foreign currency deposit base. However, these account for a mere 0.6% of China’s total deposits.

There are four basic channels through which CNY cash can flow from onshore into Hong Kong banks:

− HongKongresidents’conversionofHKDtoCNY, subject to a CNY20,000 daily limit. Banks clear the HKD/CNY exchange under a special clearing agreement set up in 2005. On 25 Jul 2012, non-Hong Kong residents are allowed to open CNY account in Hong Kong with unlimited limit. However, banks are not allowed to clear their HKD/CNY transactions through this special clearing agreement, the Shanghai conversion window or the cross-border remittance channels. Effectively, the non-Hong Kong resident accounts would not contribute to the build-up of CNY liquidity offshore.

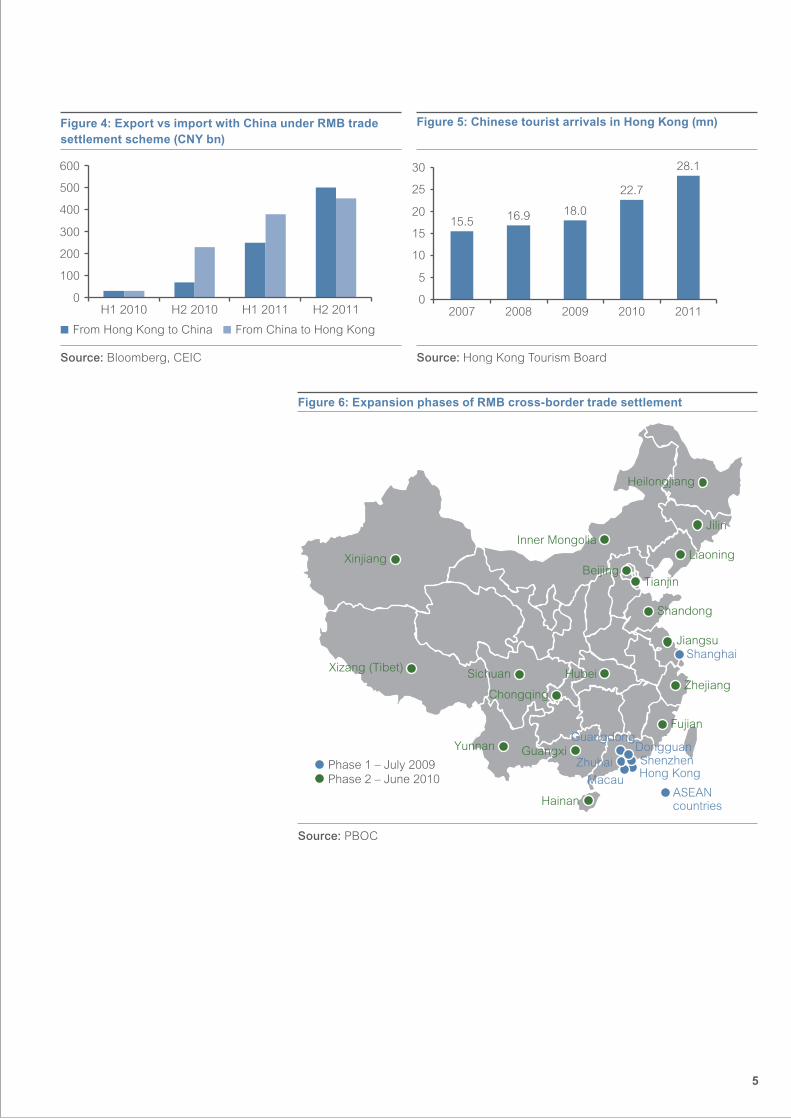

− ExportstoChinasettledinCNY. This is subject to an aggregate clearing limit of +/-CNY8 billion at the Bank of China (Hong Kong) Limited for the net total of exports and imports. Over the past two years, the flows between exports and imports have also become more balanced from an earlier 3:1 ratio between Chinese imports and exports (see Figure 4).

− Chinesecorporates’outwarddirectinvestments. This is subject to individual quotas.

− Chinesetourists’overseasspending. Since the launch of the Individual Visit Scheme in 2003 by the Hong Kong SAR government, which enabled residents of 49 cities in China to visit Hong Kong in their individual capacity, tourists from the mainland have soared 45% on a compounded annual basis from 2007-2011 (see Figure 5).

The first five years of the CNH market focused mainly on growing the liquidity

pool in Hong Kong, and deepening the FX and bond markets.

3

Figure2:CNY-denominateddeposits,tradesettlementandbondsinHongKong(CNYtrn)

Figure3:CNY-denominateddeposits,tradesettlementandbonds in Hong Kong as % of Hong Kong’s total

Source: Bloomberg, CEIC Source: Bloomberg, CEIC

• Therehasalsobeenarapidbuild-upofCNYdepositsinotheroffshorecentresbut these remained much smaller than in Hong Kong. This is because these other centres started later than Hong Kong, and had no support of a direct central clearing line with China. In Singapore, CNY non-bank deposits with Singapore banks have reached CNY60 billion as at June 2012; and in London, these deposits reached CNY35 billion as at end 2011.

• TheCNYtradesettlementscheme in Hong Kong has grown at an even faster pace than deposits after the last regulatory hurdles were removed for Chinese exporters earlier this year (Figure 6 shows the phases of expansion for this scheme).

In the 12 months leading up to June 2012, trade settlement volume reached CNY2.32 trillion (USD365 billion). This figure already exceeded 1.2 times of the China-Hong Kong bilateral trade, suggesting that third parties outside of Hong Kong have begun settling their trade with China in CNY via Hong Kong banks.

On the other hand, the figure is barely 10% of China’s total external trade, suggesting there is still plenty of scope for China to drive the use of CNY for settling its trade with its huge base of foreign trade partners.

• CNY-denominatedbondissuance appears to grow relatively slower but it was still a five-fold increase since 2010. The outstanding stock of corporate bonds, certificate deposits and bonds issued by China’s Ministry of Finance (MOF) currently stands at CNY 343bn (USD 55bn). This is already 55% of Hong Kong’s total HKD-denominated private sector bond market. The bulk of the CNH issuance is dominated by financial institution issuance, concentrated mostly in tenors of three years and below.

Jul09

Oct09

Jan10

Apr10

Jul10

Oct10

Jan11

Jan12

Apr11

Jul11

Oct11

0

0.5

1.0

1.5

2.0

2.5

Apr12

Bonds Trade settlementDeposits

Jul09

Oct09

Jan10

Apr10

Jul10

Oct10

Jan11

Jan12

Apr11

Jul11

Jul12

Oct11

Apr12

Bonds % HKD corp bondsDeposits % HK total deposits

Trade % CN-HK bilateral

0

20

40

60

80

100

120

140

4

Phase 1 – July 2009 Phase 2 – June 2010

Guangdong

Hong Kong

Shanghai

ShenzhenZhuhaiDongguan

BeijingTianjin

Inner MongoliaLiaoning

Jiangsu

Zhejiang

Fujian

Shandong

Hubei

Guangxi

Hainan

Chongqing

Sichuan

Yunnan

Jilin

Heilongjiang

Xizang (Tibet)

Xinjiang

MacauASEAN countries

Source: PBOC

Figure4:ExportvsimportwithChinaunderRMBtradesettlementscheme(CNYbn)

Figure5:ChinesetouristarrivalsinHongKong(mn)

Source: Bloomberg, CEIC Source: Hong Kong Tourism Board

Figure6:ExpansionphasesofRMBcross-bordertradesettlement

0

100

200

300

400

500

600

H1 2010 H1 2011 H2 2011H2 2010

From Hong Kong to China From China to Hong Kong

15.5 16.9 18.0

22.7

28.1

0

5

10

15

20

25

30

2007 2008 2009 2010 2011

5

Liquidity strained by opening of investment avenues back into China

Market liquidityTo a large extent, the liquidity situation of the CNH market is demand-driven. The demand for CNY liquidity is in turn driven by the relative strength of the CNY against USD and other foreign currencies. The measure of the offshore CNY liquidity pool should be the same as the measure of monetary aggregates. The broad liquidity pool should thus comprise of both non-bank deposits and bonds. As such, the drop in deposits in Hong Kong banks from December 2011 to May 2012 did not reflect a shrinking CNH liquidity pool in Hong Kong as bond issuance continued to rise (see Figures 2 and 3 again). Still, the pace of liquidity growth has slowed since fourth quarter 2011. There are three factors behind this:

1. An increase in CNY trade settlement volume for importing Chinese goods since the lifting of restrictions on Chinese exporters to settle in CNY

2. An increase in Hong Kong settlement banks’ investments into the onshore bond market as more of them get special quotas from PBOC to do so

3. An outflow of non-Hong Kong resident CNY deposits to other offshore centres begin to compete for these deposits

In response to the third point above, the Hong Kong Monetary Authority (HKMA) has liberalised previously punitive rules on Hong Kong banks’ risk limits for CNH from the beginning of 2012. More recently, the HKMA also allowed non-residents to set up CNY deposit accounts in Hong Kong with no daily conversion limits. See Figure 7 for a list of rule changes by the HKMA since the start of 2012.

Figure7:HKMAregulatorychangestoimproveRMBliquidity

Allow non-residents to convert unlimited daily amount of RMB

• AIs*canofferRMBservicestonon-HongKongresidentpersonalcustomers,andcurrencyconversionisnotsubjecttocorresponding limits for Hong Kong residents (25 Jul 2012)

Replace RMB limit with RMB liquidity ratio to include more RMB liquid assets

• AIsarerequiredtomaintainaRMBliquidityatnolessthan25%computedonthesamebasisasstatutoryliquidityratio.• ThisupdateincreasesflexibilityfortheinclusionofmoreRMBliquidassets,andaccuracyofmatchingRMBliquidassets

and short-term liabilities (14 June 2012)

Introduce a facility to provide RMB liquidity to AIs participating in HK RMB business

• ThefacilityusesthecurrencyswaparrangementbetweentheHKMAandthePeople’sBankofChina.• Thisfacilityincreasesshort-termRMBliquidity,reducespotentialmarketdisruptionsandincreasesmarketconfidence(14

June 2012)• ToenableAIstobetterassesstheirRMBneeds,theHKMAmovedbackthetimebywhichAIsmaysubmittheirrequests

for funds from 10am to 1.30pm (25 Jul 2012)

Replace RMB Net Open Position (NOP) standard with AIs’ self-determined mechanism

• The20%standardRMBNOPisreplacedbyamechanismwherebyAIsareallowedtosetuptheirowninternalRMBNOPinconsultation with the HKMA. AIs should consider the nature and scale of their RMB business.

• ThismeasurecouldfurtherincreaseRMBliquidityandrecogniseAIs’effectiveRMBexchangeandliquiditymanagementpractices (22 May 2012)

Require AIs to ascertain the genuineness of underlying cross-border merchandise trade transactions

• Thisincludesknow-your-customer(KYC)processes,duediligenceprocedures.andreviewingsupportingdocumentsfromclients ( 2 April 2012)

*AuthorisedInstitutionsorbanksinHongKong.Source: HKMA, Bloomberg

6

Market depthThe launch of the interbank market in October 2010 provided a huge boost to trading volumes of FX spot and forward market. The introduction of the FX option market which followed then gradually led to the innovation of structured products. Figure 8 shows the types of FX and rates products, the maturity range and turnover volume for each product type.

USD/CNH spot and forward daily turnover is now USD5-6 billion, broadly on par with the USD/CNY NDF market which started to see some slight slowdown in trading volume since 2011.

The USD/CNY cross currency swap curve is available up to a 10-year tenor but it is only liquid up to a three-year tenor at the moment. USD/CNH options are also available up to a two-year tenor.

In the bond market, the maturity has stretched to a 20-year tenor by a Chinese policy bank in July 2012. In early 2012, a 15-year tenor was tapped by two Chinese policy banks and China’s MOF with their respective inaugural 15-year issues. The most traded part of the curve remains in three-year tenor and below.

CNH FX trading volume now on par with NDF market

Figure8:RangeofCNHfinancialproducts

Product Tenors Turnover Remarks

Spot T+2 value spot USD1-2bn

Forward O/N - 12m, 18m, 24m

USD2-3bn

CCS 6m – 5y USD300mn

FX Options 1m – 2y USD70-120mn Illiquid relative to other FX productsBetter liquidity in shorter tenors

FX Futures 1m – 1y n.a. To begin trading from 17 September

Money Market O/N to 1y CNY2-4 bn

Repo n.a. n.a. Tripartite platform operated by Euroclear, J.P. Morgan and HKMA

CDs/Notes 3m to 3y n.a

Equities n.a. n.a. First and only IPO in April 2011

Structured Products

Up to 3y n.a.

Bonds Up to 15y for sovereign; up to 20y for FIs/corporates

CNY50mn

Mutual Funds n.a. n.a.

Source: RBS

7

The biggest use of the swap lines so far is from foreign central banks diversifyingreservesintoCNY

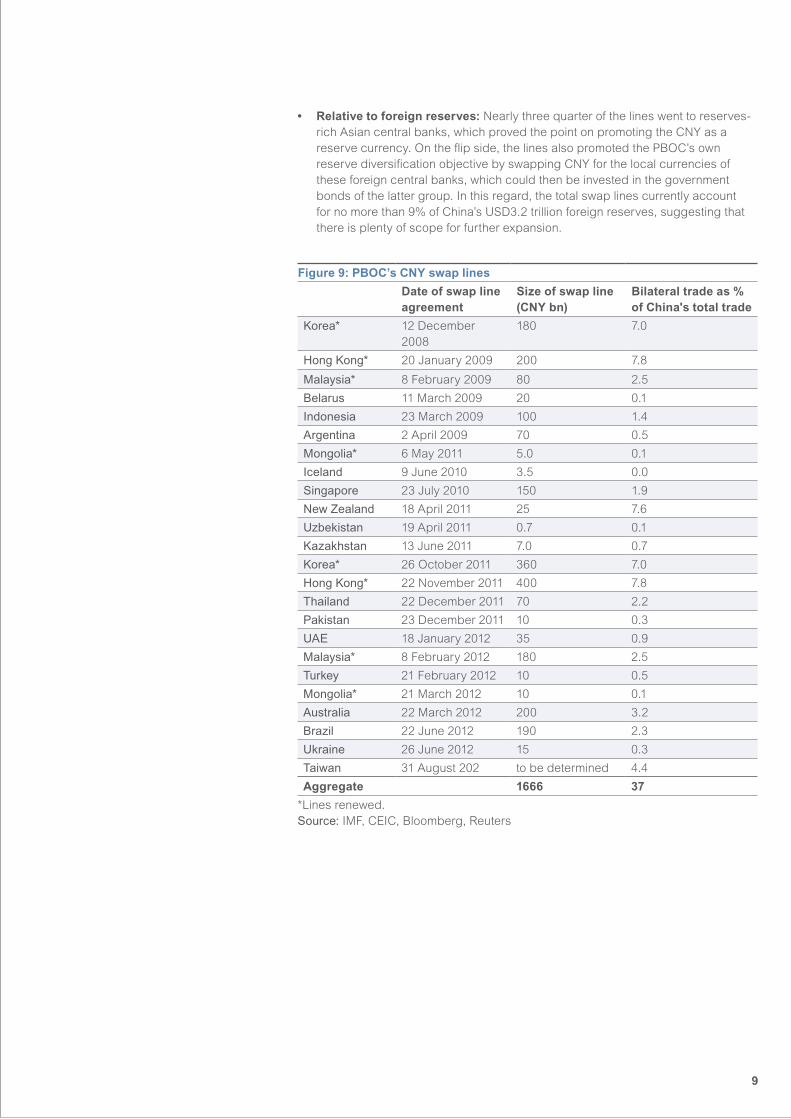

PBOC’sCNYswaplinesSince signing the first CNY swap line in December 2008, the PBOC has signed a total of 20 such lines with foreign central banks. Four of these lines have been renewed before expiry in 2012 while another three have expired. All the lines cover a three-year period. The four renewed lines had the quotas increased by at least double from the original amounts for a three-year extension.

These swap lines serve multiple purposes which evolved with the expansion of the CNH market.

• Standbycreditfacility:WhenthefirstlinewasofferedtotheBankofKorea(BOK), the purpose was to provide a standby credit facility for the BOK with no conditions attached, unlike the facilities offered by the IMF, multilateral agencies or the Fed during the height of the Lehman crisis.

• CNYtradesettlementscheme: The lines that came after the CNY trade settlement scheme was expanded in 2009 were aimed at promoting the use of CNY in bilateral trade and investments between China and these countries.

• CNYasreservecurrency: A year later in August 2010, the PBOC started allowing recipient central banks to partially activate these swap lines for them to obtain CNY to invest in China’s domestic bond market. This move was designed to promote the holding of CNY in the foreign reserves of other central banks. Since then, several central banks have partially converted their CNY swap lines into investment quotas from the PBOC. Otherwise, these swap lines have never been activated to support any credit event.

The total sum of the current 16 CNY swap lines comes to CNY1.67 trillion (USD265 billion). Figure 9 shows the list of recipient central banks and the size of their respective lines and each country’s market share of China’s total trade.

• Relativetoexternaltrade: The total bilateral trade of the 16 recipient countries with China account for 37% of China’s total external trade. The swap quota given to each central bank is not proportionate to the country’s relative market share of China’s trade. This proved the point that these lines are designed to more than just promote the CNY trade settlement scheme.

The introduction of the FX option market which followed then gradually led to the

innovation of structured products.

8

Figure9:PBOC’sCNYswaplines

Date of swap line agreement

Size of swap line (CNYbn)

Bilateral trade as % of China's total trade

Korea* 12 December 2008

180 7.0

Hong Kong* 20 January 2009 200 7.8

Malaysia* 8 February 2009 80 2.5

Belarus 11 March 2009 20 0.1

Indonesia 23 March 2009 100 1.4

Argentina 2 April 2009 70 0.5

Mongolia* 6 May 2011 5.0 0.1

Iceland 9 June 2010 3.5 0.0

Singapore 23 July 2010 150 1.9

New Zealand 18 April 2011 25 7.6

Uzbekistan 19 April 2011 0.7 0.1

Kazakhstan 13 June 2011 7.0 0.7

Korea* 26 October 2011 360 7.0

Hong Kong* 22 November 2011 400 7.8

Thailand 22 December 2011 70 2.2

Pakistan 23 December 2011 10 0.3

UAE 18 January 2012 35 0.9

Malaysia* 8 February 2012 180 2.5

Turkey 21 February 2012 10 0.5

Mongolia* 21 March 2012 10 0.1

Australia 22 March 2012 200 3.2

Brazil 22 June 2012 190 2.3

Ukraine 26 June 2012 15 0.3

Taiwan 31 August 202 to be determined 4.4

Aggregate 1666 37

*Linesrenewed.Source: IMF, CEIC, Bloomberg, Reuters

• Relativetoforeignreserves: Nearly three quarter of the lines went to reserves-rich Asian central banks, which proved the point on promoting the CNY as a reserve currency. On the flip side, the lines also promoted the PBOC’s own reserve diversification objective by swapping CNY for the local currencies of these foreign central banks, which could then be invested in the government bonds of the latter group. In this regard, the total swap lines currently account for no more than 9% of China’s USD3.2 trillion foreign reserves, suggesting that there is plenty of scope for further expansion.

9

Onshore market accessUltimately, the CNH market should be seen as a conduit into the onshore market. Otherwise, the market would never take off, proving the sceptics right – that the experiment at making the CNY partially deliverable/ convertible would end nowhere. And the sceptics were proven wrong so far.

The rapid deregulation of cross-border trade and investments has now made the CNY fully convertible on current accounts. The bulk of the capital account is partially convertible, guarded by quotas and/or application procedures. Figure 10 distinguishes the currency denomination – USD/ foreign currency, offshore deliverable CNH or onshore CNY – in which the different current and capital account itemsareallowedtobesettled.Webrieflydescribedthembelow.

Oncurrentaccounts(moredetailscanbefoundintheAppendix):

• Merchandisegoods: All goods trades can be settled using the onshore CNY exchange rate. Chinese exporters also have the choice to exchange their foreign currency export proceeds in the offshore CNH market before repatriating funds. However, Chinese importers can only use the onshore exchange rate for making payments to offshore counterparties.

• Services,interestincomeandtransfers: Transactions settled in CNY can only be dealt using the offshore CNH exchange rate. This implies that to settle CNY-denominated payments, onshore Chinese entities must remit foreign currency offshore to exchange into CNH for the payments.

Oncapitalaccounts:

• Foreigndirectinvestments: CNY funding is allowed both ways. Inward direct investments are funded through the offshore CNH market, while outward direct investments are funded through the onshore CNY market.

• Portfolioinvestments: CNY funding is allowed only one way, by foreign investors through the Renminbi Qualified Foreign Institutional Investor (RQFII) scheme which was introduced in August 2011. This is a counterpart of the QFII scheme and mini QFII scheme which allowed foreign portfolio investments to enter China in foreign currency denomination. The difference between the regular QFII and mini QFII is that the latter is open specifically for onshore fund managers to directly tap retail investors overseas. The reverse scheme – Qualified Domestic Institutional Investors (QDII), which allows onshore institutions to invest overseas – does not have the equivalent CNY counterpart.

• Loans,tradefinanceanddeposits: Onshore corporations were permitted in June 2010 to borrow CNH from the offshore market for longer-term trade finance and project financing. They are only allowed to extend trade credit in CNY terms for periods of 90 days or less.

• Specialaccess: This pipeline is open to central banks, sovereign wealth funds and CNY trade settlement banks in Hong Kong to invest directly in the onshore interbank bond market. All the quotas are set by the PBOC on a case-by-case basis. In the central banks’ case, the quotas are activated from the CNY swap lines offered by the PBOC and hence, only the central banks which have signed such lines are eligible. As at end 2011, a total CNY255 billion of such quotas has been allocated through this pipeline, of which CNY185 billion went to the first two groups, including CNY65 billion to Japan alone.

Current account fully open/ convertible, capital account still partially convertible

10

Figure10:LevelofopennessofChina’sborders

Current Account Capital Account

Offshore Onshore Offshore Onshore

*Long-term(LT)tradecreditreferstoabove90dterm.Short-termrefersto90dtermand below. Source: RBS

Goods

Foreign Direct

Investment

Portfolio Investment

Loans, LT Trade Credit*

Short-term TradeCredit*

Foreign currency deposits

Trade settlement

banks, foreign CBs,SWFs

Services, Interest Income, Transfers

Goods

Overseas Direct

Investment

Portfolio Investment

Loans, LT Trade Credit*

Short-term TradeCredit*

Foreign currency deposits

PBOC

Services, Interest Income, Transfers

USD

(QFII, min QFII)

(QDII)

(RQFII)

(foreign debt quota)

(foreign debt quota)

(foreign debt quota)

(CNY swap line & special quotas)

CNH

CNY

11

Recent deregulation on investments favoured domestic bonds

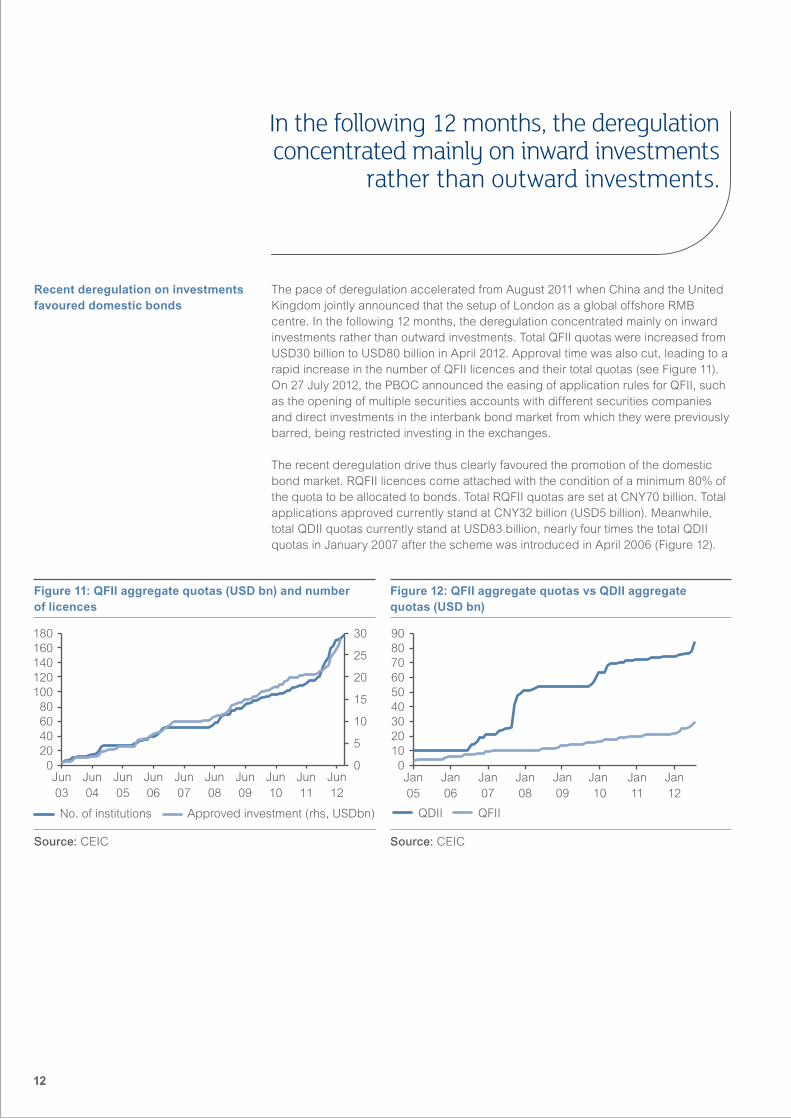

The pace of deregulation accelerated from August 2011 when China and the United Kingdom jointly announced that the setup of London as a global offshore RMB centre. In the following 12 months, the deregulation concentrated mainly on inward investments rather than outward investments. Total QFII quotas were increased from USD30 billion to USD80 billion in April 2012. Approval time was also cut, leading to a rapid increase in the number of QFII licences and their total quotas (see Figure 11). On 27 July 2012, the PBOC announced the easing of application rules for QFII, such as the opening of multiple securities accounts with different securities companies and direct investments in the interbank bond market from which they were previously barred, being restricted investing in the exchanges.

The recent deregulation drive thus clearly favoured the promotion of the domestic bond market. RQFII licences come attached with the condition of a minimum 80% of the quota to be allocated to bonds. Total RQFII quotas are set at CNY70 billion. Total applications approved currently stand at CNY32 billion (USD5 billion). Meanwhile, total QDII quotas currently stand at USD83 billion, nearly four times the total QDII quotas in January 2007 after the scheme was introduced in April 2006 (Figure 12).

In the following 12 months, the deregulation concentrated mainly on inward investments

rather than outward investments.

Figure11:QFIIaggregatequotas(USDbn)andnumber of licences

Figure12:QFIIaggregatequotasvsQDIIaggregate quotas(USDbn)

Source: CEIC Source: CEIC

0102030405060708090

Jan05

Jan06

Jan07

Jan08

Jan09

Jan 10

Jan11

Jan12

QDII QFII

0

5

10

15

20

25

30

020406080

100120140160180

Jun03

Jun04

Jun05

Jun06

Jun07

Jun08

Jun09

Jun10

Jun11

Jun12

No. of institutions Approved investment (rhs, USDbn)

12

Following are the key regulatory changes affecting onshore market access made since August 2011 (a full history and details of regulatory changes can be found in the Appendix):

• August2011 – The PBOC launched Renminbi QFII and pilot scheme for foreign banks to tap CNH to recapitalise mainland operations. Onshore non-FIs/ corporates were allowed to issue CNH bonds subject to quotas.

• December2011 – The Chinese government launched the RMB Qualified Foreign Institutional Investors (RQFII) scheme on a trial basis for foreign investors to enter the onshore market. An initial target of CNY20 billion was set for the quotas to be awarded under the scheme. A minimum 80% floor was set for the funds to be invested in bonds.

• January2011 – Ten investment firms in Hong Kong were granted RQFII licences to invest in China’s securities market with a total CNY10.7 billion of quotas. The firms planned to develop RMB wealth management products onshore.

• April2012 – China announced the expansion of USD50 billion investment quota to both the Qualified Foreign Institutional Investors (QFII) and the Renminbi QFII (RQFII) pilot programmes. This brought the total quota to USD80 billion from USD30 billion for the QFII, and to CNY70 billion from CNY20 billion for RQFII. It will also allow the pilot institutions to use the quota in issuing RMB A-share ETF product, to invest in the A-share index shares and list them in the Hong Kong Exchange (HKEx).

• July2012 – China and Singapore jointly announced that a second offshore CNY clearing centre will be set up in Singapore, to be operated by the full branch of a Chinese bank in Singapore. This agreement is part of a China-Singapore Free Trade Agreement (FTA) signed on 6 July 2012.

• July2012 – China released new rules for foreign investors, lowering minimum qualification requirement and simplifying the approval process for applicants under the Qualified Foreign Institutional Investor (QFII) programme. The changes allowed QFIIs to invest in China’s interbank bond market. The new rules also allowed foreign private equity investment entities to apply for QFII licenses

Offshore-onshore market convergence The wave of rapid regulatory changes from late 2011 paved the way for the convergence between the offshore and onshore markets. In the initial one to two years of its existence until late 2011, the USD/CNH FX market was directionally driven by USD/CNY NDF to the extent that some market participants started mulling over the idea of introducing a NDF version of the CNH market.

Since late 2011, the pull of forces has reversed. The NDF market is now driven by the CNH market such that it behaves like a semi-deliverable market with the forward curve tilting upwards to reflect the positive interest rate premium of CNY interest rates over USD rates. Since April 2012, just prior to the PBOC expanding the intra-day trading band, the onshore USD/CNY market has also started to follow the offshore USD/CNH market, deviating from the direction set by the PBOC every morning through its fixing (Figure 13).

WiththeconvergenceintheFXmarkets,thebondmarketsonshoreandoffshorealsobegan to converge. The yield discount of the offshore issues to the onshore issues is now found mainly in the shorter-dated bonds of three-year tenor and below and has compressed to no more than 50 basis points (see Figure 14). The pressure for the yield convergence is also coming from the subtle shift in FX policy direction by the PBOC – from a strong and stable CNY to a weaker and more volatile CNY. Investors’ expectations on returns from the CNH bond market have thus shifted from FX gains to yield and/or bond gains.

Key deregulations on investments in the past year

Offshore CNH FX has become leader for NDF and even onshore CNYFXmarket

13

Figure13:OffshoreUSD/CNHspotvsonshore USD/CNYspot

Figure14:OffshoreChinaMOF3ybondvsonshore MOF 3y bond (%)

Source: Bloomberg Source: Bloomberg

The next five years

Becoming fully convertible Taking a very long perspective, the CNY is just two steps short of becoming fully convertible and three steps away from becoming an international currency. The steps are:

1. Allow all capital account items to be settled freely in CNY both ways – inwards and outward of China

2. Lift all quotas and streamline application and approval processes

3. Increase the use of CNY for international trade and investments

This is a simplification as the last giant step involves multiple facets. The qualifications of an international currency are much broader than this one-line description (see next section). Logically, one would expect China to make the CNY fully convertible before embarking on the ultimate goal of internationalising the CNY. But China has put the proverbial horse before the cart by creating an offshore CNY market to promote the use of the CNY in international trade and investments before the currency is fully convertible.

China’s actions seem to suggest some degree of time consideration to achieve the goal of internationalising the CNY. The government appears to have its sight for the CNY to be included in the IMF’s Special Drawing Rights (SDR) basket by the end of 2015 when the IMF reviews its basket. The current global climate favours the CNY as both the USD and EUR are under pressure and global investors are looking for an alternative reserve currency. In working towards this goal, the Shanghai municipal government released a blueprint in March 2012, setting a goal of making Shanghai the global pricing centre for both onshore and offshore CNY financial products by 2015, and a global financial centre by 2020.

Partial convertibility at best leads to partial internationalisation

Inclusion in IMF SDR basket will be a strong endorsement

Jun11

Sep11

Nov11

Jan12

Mar12

May12

Jul12

0

1

2

3

4

5

050100150200250300350400

Spread (rhs,bp) CNY 3y bmkCNH 3y bmk

Aug10

Oct10

Jun11

Aug11

Oct11

Dec11

Feb12

Apr12

Jun12

Aug12

Dec10

Feb11

Apr11

Offsh-onsh (% onsh fix, rhs)

Offshore spotOnshore spot

6.2

6.3

6.4

6.5

6.6

6.7

6.8

6.9

-2.5-2.0-1.5-1.0-0.500.51.01.52.02.53.0

14

BIS’s seven criteria to qualify as an international currency

In the next few years, we can thus expect to see more of the following:

• Expansionofthetradesettlementscheme: Trade in goods and services is the smoothest or most consistent way to grow the global CNY liquidity pool, considering especially China’s status as one of the world’s largest trade partner.

• Settingupofmoredirectclearinglines: This will be targeted at strategic trade partners. Jointly with China, Singapore has announced that it will set up an offshore CNY clearing centre, while Taiwan and Japan are believed to be in negotiations with China for their own dedicated clearing lines.

• Jointventureswithinternationalfinancialcentres: London was announced as the global offshore CNY centre and this is in partnership with Hong Kong. Getting the second CNY clearing line will make Singapore a regional satellite centre. Getting Hong Kong to partner with London may thus be China’s assurance to Hong Kong that it retains the lead as the main offshore CNH centre above Singapore and London. In the background, Shanghai is preparing to become the global pricing centre for all CNY financial products onshore and offshore by 2015, as spelt out in its blueprint which names Hong Kong as a partner in achieving this goal. Can Shanghai achieve this goal without the CNY becoming fully convertible?

InternationalisingtheCNYThere are many shades of the definition of an international currency. A short definition is a currency that is widely held as a reserve currency. The US dollar and the euro fit this definition as they currently account for 62.2% and 24.9% of world foreign reserves (see Figure 15). By far the most concise definition of an international currency are the following seven criteria1:

1. Freelytraded: Removal of all restrictions on trading the currency

2. Internationaltradeinvoicing: Ability for both foreign and domestic firms to invoice trades in the currency

3. Readilyaccessible: Ability of domestic and foreign institutions to hold currency in amounts they deem fit

4. Usedforsecuritisationbyprivatesector: Both domestic and foreign institutions are able to issue marketable securities in the currency

5. Usedforsecuritisationbymultilateralagencies: International financial institutionssuchastheWorldBankareabletoissuedebtinstrumentsinthecountry’s market and use the currency in their financial operations

6. Reservecurrency: Currency may be included in currency baskets of other countries

7. Internationalconfidence in the issuing country

1 Peter Kenen, Princeton University, “Currency internationalisation: an overview”, BIS Papers No. 61, December 2011

15

Based on the above criteria, only the USD and the EUR are fit to be called an international currency while none of the other G7 currencies could. The key criterion which most currencies are unable to fulfil is that on international trade invoicing.

The CNY currently falls short of more than half the criteria above. The CNY currently ranks 15th as a payments currency globally with a market share of 0.45%. To be part of the top five payments currencies, the CNY market share has to reach at least 2%. EUR and USD’s market shares are 43% and 31% respectively. Hence, the ultimate goal to become an international reserve currency is still a giant step away.

The USD took about 30 years to achieve the status of an international currency – fromtheendoftheWorldWarIIinthemid-1940stotheearly1970s.ThecollapseoftheBrettonWoodsAgreementsawcentralbanksaroundtheworldswitchfromholding gold reserves to holding USD as their reserve currency. In 1975 when OPEC accepted USD as the sole pricing and settlement currency for oil, this propelled the USD to become the currency denomination for all other major commodities, sealing its status as a world reserve currency.

TheEURwasintroducedin1999.Withthecombinedstrengthofits12foundingmembers, its share of world reserves was set at 18% from the start. As the Euro zone expanded, its share of world reserves has grown, reaching about 28% by third quarter 2009. The EUR’s ascent as an international currency was also bolstered during this period by the bursting of the dot.com bubble and the September 11 terrorist attacks on the US which shook international confidence in the US economy and the dollar.

The last chapter of this guide discusses the chances for China achieving the international currency status for the CNY. The conclusion is that current efforts to globalising the offshore CNH market franchise will lead at best to partial internationalisation without full convertibility.

CNYcurrentlyranksas15th most used payments currency globally

USDtook30yearstobeacceptedas international currency through economics and politics

EURtooklessthan10yearsthrougheconomic union

Figure15:Distributionofworldforeignreserves(%)

Source: IMF

55

60

65

70

75

0

5

10

15

20

25

30

I II III1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EUR GBP JPY Other USD (RHS)

IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

16

Evolution of the market

The CNH FX market officially came into existence in July 2010 when the PBOC and the HKMA signed a Supplementary Memorandum of Cooperation that allows Hong Kong banks to directly settle CNY trades among each other. This led to the creation of the CNH interbank market. In its brief history, the market evolved from one that is purely driven by regulations to one that is increasingly driven by flows from foreign multinational corporations (MNCs) and Chinese corporations.

There were major regulatory changes by both the PBOC and HKMA to directly deepen the FX market.

• Expandingthecentralclearingline: The CNH FX market had a rather turbulent first two years, caused primarily by the tight cap imposed on the Bank of China (Hong Kong) Limited for centrally clearing any long/short CNY positions offshore. Also, the build-up of liquidity through the trade channel was not fast enough to cope with a rapidly growing demand from bond investors.

The central clearing limit was breached twice – the first time on 28 October 2010 from the short side and the second time on 23 September 2011 from the long side. Both times caused huge dislocations between the CNH and onshore markets. In the first episode, the HKMA stepped in to assure the market that it was standing by to activate its CNY swap line with PBOC. In the second episode, the PBOC eventually had to temporarily double the quota. A second central clearing line is on the way to be set up in Singapore, as announced in July 2012.

• IntroducingadailyUSD/CNHspotfixing: The introduction of a daily USD/CNH spot fixing at 11.15am by the Hong Kong Treasury Markets Association (TMA) in June 2011 was an important turning point. This was a boost to the FX derivative and option markets as the fixing provides transparency and also a pricing source for switching to USD settlement in the event of any market disruption that renders the CNH non-deliverable. This was formalised in October 2011 by a working group of banks and the International Swaps and Derivatives Association (ISDA) to include a standard fall-back clause for CNH FX OTC products. However, other products including CNH bonds have yet to standardise the choice of FX fixing and/ or the adoption of a market disruption clause.

• IncreasingHongKongbanks’risklimits: In January 2012, the HKMA increased banks’ CNY net open positions from the 10% cap imposed since July 2011 to 20%. In May 2012, the cap was lifted. Banks’ statutory liquidity requirement on CNY deposits was also liberalised twice, in February and June 2012.

• Wideningtheonshoreintra-daytradingband: In April 2012, the PBOC widened the intra-day trading band on USD/CNY spot from +/-0.5% to +/-1% and lifted the short-selling ban on USD by onshore banks. This easing of FX rules onshore further deepened the offshore market as it broadened the scope for Chinese companies to arbitrage between the two markets.

FX MarketCNH FX market is now driven by corporate flows

17

Other deregulation steps which indirectly helped boost the FX market trading volume included those which opened up the inward investment routes into China, and the lifting of restrictions for Chinese exporters to settle in CNY.

On 27 April 2012, the HKMA extended the real time gross settlement (RTGS) system by an additional five hours to close at 11.30pm. The aim is to facilitate the settling of trades as a step to help deepen the market in London. However, the extended RTGS hours may have limited use as banks are still unable to access their fiduciary accounts at the PBOC Shenzhen branch whose hours have not been extended. The fiduciary account channel was set up in early 2011 after the first breach on the central clearing cap in October 2011 so as to reduce banks’ counterparty risks with the sole central clearing bank, BOC (Hong Kong) Limited. Clearly, banks would favour the PBOC counterparty risk to the BOC risk.

Figure16:TypesofFXmarketsintheoffshoredeliverable,offshorenon-deliverableforwardandonshore deliverable markets

Offshore CNH Offshore NDF OnshoreCNY

Fx Spot

Tenors T+2 value spot n.a. T+2 value spot

Daily volume (USD bn) 1-2 n.a. 20

Ticket size (USD mn) 5-15 n.a. 10-20

Bloomberg/ Reuters CNH TMAF/ CNHFIX= n.a. CNY/ CNY=CFXS

FX forward

Tenors O/N - 12m, 18m, 24m T/N - 12m O/N - 12m, 24m, 36m

Daily volume (USD bn) 2-3 4-5 10

Ticket size (USD mn) 10-20 10-50 10-20

Bloomberg/ Reuters CNH+1M/ CNH1MOR= CCN+1M/ CNY1MNDFOR= CCO+1M / CNY1MOR=

Cross currency swap

Tenors 6m - 5y 1y - 5y 1y - 5y

Daily volume (USD mn) 50-100 20-50 inactive

Ticket size (USD mn) 10-20 10-20 inactive

Bloomberg/ Reuters CGUSSW2/CNHUSCS=TRHK CCSWN2/CNUSNDS2Y= CGYSSW2/CNUSCS

FX option

Tenors O/N-2y O/N-3y O/N-2y

Daily volume (USD mn) 70-300 250-300 Illiquid

Ticket size (USD mn) 10-20 50 n.a.

Bloomberg/ Reuters USDCNHV1Y / CNH1Y0=BRKR USDCNYV1Y/CNY1YO=W USDCNYOV1Y / CNY1YO=CN

FX futures

Tenors 1m-1y (to start on 17 Sep 2012) 1m-1y (CNYUSD)1m-3y (USDCNY)

n.a.

Daily volume n.a. Illiquid n.a.

Ticket size (USD mn) n.a. 0.1mn per contract n.a.

Bloomberg/ Reuters n.a. n.a. n.a.

Source: Bloomberg, RBS

18

OffshoreCNHandonshoreCNYspotrates have converged although the two fixings continue to diverge

DeliverableCNY/JPYcrossnowquoted in Tokyo; expect more crosses to follow

Figure17:USD/CNHfixingvsPBOCUSD/CNYfixingandPBOC intra-day band

Figure18:USD/CNHspotvsUSD/CNYspotandPBOCintra-day band

Source: Bloomberg Source: Bloomberg

Spot

• Marketvsfixings

Spot market liquidity has picked up significantly since its inception. Daily volumes for CNH spot are now about USD2 billion, more than a ten-fold increase from inception. In comparison, the onshore CNY daily trading volume is about USD10 billion. The average transaction size is around USD10 million (see Figure 16).

The direction of USD/CNH is ultimately set by the PBOC’s FX policy through its daily fixing. However, there are still long stretches of deviations from the onshore market for which the comparison can be made in terms of two spot fixings and the real-time trading.

Prior to the recent deregulations which allowed more two-way flow of funds for trade and investments, the deviations between USD/CNH and the onshore market were in both the fixings and real-time trading (Figure 17). Since May 2012, the deviations in the fixings on both sides continue to deviate. However, real-time spot trading of the two markets has converged (Figure 18). This has come about with the onshore real-time spot rate converging to the offshore deliverable CNH rate rather than its own onshore fixing set by the PBOC. In other words, the CNH market has taken the lead over the onshore market.

One can say that the PBOC’s widening of the intra-day trading band in April 2012 from +/-0.5% to +/-1% marked the turning point for market convergence between offshore and onshore. At about the time of the PBOC’s move, the country’s top leaders and the PBOC governor issued statements on allowing the CNY to be more freely trading so as to see more two-way fluctuations on the basis that the currency is fair-valued and the country’s exports have come under pressure. This seems like a subtle message for a switch from a strong FX policy to a neutral or even slightly weak FX policy. The PBOC’s fixing for USD/CNY has risen by 0.8% since the band widening. The offshore USD/CNH fixing has risen by 1.1% during the same period.

On 1 June 2012, the Tokyo interbank market started directly quoting the deliverable CNY/JPY cross rate with the PBOC endorsement. As upcoming offshore CNY centres, we believe that London and Singapore will launch more of the deliverable CNY crosses, starting with crosses against their own respective local currency units.

Jun11

Aug11

Oct11

Dec11

Feb12

Apr12

Jun12

Aug12

6.2

6.3

6.3

6.4

6.4

6.5

6.5

6.6

Intra-day band CNY spot CNH spot

Jun11

Aug11

Oct11

Dec11

Feb12

Apr12

Jun12

Aug12

6.2

6.3

6.3

6.4

6.4

6.5

6.5

6.6

Intra-day band CNY fix CNH fix

19

Figure19:USD/CNH12mnoutrightvsUSD/CNYNDF12moutrightandonshoreUSD/CNY12mnoutright

Figure20:Implied12mnCNYappreciationbyUSD/CNHforwardvsUSD/CNYNDFandonshoreUSD/CNYforward

Source: Bloomberg Source: Bloomberg

Forwards

The daily volume for CNH FX swaps and forwards is estimated at USD3 billion. Tenors are available up to three years, with liquid better in one year and below. CNY NDF daily transaction volume is estimated at USD6.5 billion. Combining spot and forwards, the deliverable CNH FX market is now broadly on par with the NDF market. Onshore, the daily volume of CNY FX swaps and deliverable forwards is estimated at USD10 billion. Combined with spot trading, the total trading volume of the onshore FX market is about USD20 billion (see Figure 19).

There is increasing pressure for the onshore market to trade in line with the offshore deliverable market and away from the onshore fixing. Given this, we expect market participants to increasingly migrate to the deliverable CNH market from the NDF market which takes an onshore fixing. In fact, the behaviour of the USD/CNY NDF market has long stopped behaving like a normal NDF market, behaving more like adeliverablemarket.WellbeforethePBOC’ssubtleshifttoaweakerFXpolicy,the NDF curve has moved upwards steeply. It was dragged up by the steepening pressure from the deliverable USD/CNH forward curve (see Figure 20). As a typical NDF market reflects market expectation for the strength or weakness of the currency to USD, USD/CNY NDF had been inverted to reflect market expectation of a strong CNY before the deliverable CNH market became deep and active.

Combining spot and forwards, the CNH FX market is broadly on par with the NDF market

Market participants are increasingly migrating from NDF to deliverable CNH forwards

Jan11

Mar11

May11

Jul11

Sep11

Nov11

Jan12

Mar12

May12

Jul12

6.206.256.306.356.406.456.506.556.60

CNH 1y NDF 1y CNY 1y

Jan11

Mar11

May11

Jul11

Sep11

Nov11

Jan12

Mar12

May12

Jul12

-3

-2

-1

0

1

2

3

4

CNH 1y NDF 1y CNY 1y

20

Cross currency swaps

Cross currency swaps are offered by major interbank players with tenors from six months to five years, although liquidity is poor above three years. The daily turnover is reasonably big at around USD50-100 million, with an average ticket size of USD10-20 million. Liquidity has been gradually improving as market participants increasingly switch from ND-CCS to the deliverable CCS for hedging trade and investments. For trade, transactions are mainly confined to tenors one-year and below.

On the investment channel, the flows currently tend to come from investors paying CNY CCS rather than issuers receiving CNY CCS. However, as the CNY CCS basis becomes less negative (see Figure 21) and the market gets deeper, USD-based issuers might be increasingly attracted to come to the CNH bond market to raise funds and swap them into USD.

Options and futures

Still in a relatively nascent stage of development, the CNH options market is growing at a brisk pace. The first OTC RMB option was traded in November 2010. The liquidity has since picked up, averaging around USD70 -120 million, reaching USD300 million on busier days. Tenors of up to 12 months are fairly liquid (see Figure 22). Two year options are not as liquid but not uncommon.

On 22 August 2012, the Hong Kong Exchanges and Clearing Limited announced that it will introduce the first deliverable CNY currency futures on 17 September 2012. The USD/CNH contract would be the first deliverable CNY currency future. The final settlement price will be based on the spot USD/CNH fixing published by the Treasury Markets Association at 11.15 am. The first batch of contract months that will become available are October 2012, November 2012, December 2012, January 2013, March 2013, June 2013 and September 2013.

Figure21:1yCNHCCSvsCNYND-CCSandonshore CNYCCS

Figure22:3mUSD/CNHvolvsUSD/CNYNDFvol(%)

Source: Bloomberg Source: Bloomberg

Futures to be available from September 2012

CNH options now trade up to 2-years

Jan10

Apr10

Jul10

Oct10

Jan11

Apr11

Jul11

Oct11

Jan12

Apr12

Jul12

1y CNH CCS 1y CNY ND-CCS 1y CNY CCS

-4-3

-2-10

1234

0123456789

Mar11

May11

Jul11

Sep11

Nov11

Jan12

Mar12

May12

Jul12

CNY NDF vol CNY vol

21

Evolution of the market

Until the end of 2011, the CNH interest rate market comprised only a thinly traded deposit market and a vibrant bond market (see Figure 23). Since January 2012, Hong Kong banks have started to activate a money market by providing a daily fixing on a CNY Hibor curve.

There are three reasons which remain today as to why Hong Kong banks struggled to activate an interest rate swap curve in the CNH market:

• Lackofapolicyinterestratetarget: The PBOC’s interest rate policy targets are Chinese banks’ commercial deposit and lending rates. Hence, the onshore money market of repo and Shibor are driven entirely by liquidity factors, including the PBOC’s open market operations (bills, repos and reverse repos), required reserve ratio (RRR) moves and FX fund moves. Given the vastly different liquidity condition in the CNH market from the onshore market, the onshore Shibor is thus highly inappropriate for setting the CNH interest rate swap market.

• LackofaccesstoonshoreShibor: As the CNH IRS is a deliverable market – similar to the FX market, market makers for the IRS curve would require access to the short-end fixing to be able to manage their interest rate risks. However, there is no access to the onshore Shibor market.

• Onshoremarketishighlyspeculative: There are several different IRS markets onshore, the most heavily traded being that fixed on the seven-day repo rate with a daily turnover of CNY3-4 billion. The Shibor-fixed market is the second most traded market with daily volume barely half of the former. Other IRS curves have fixings on the PBOC’s one-year lending and one-year deposit rates, These are used by corporate borrowers on a case-by-case basis. Until recently, the onshore seven-day-fixed and Shibor-fixed IRS market is highly speculative as both borrowers and investors do not use the market for hedging interest rate risks. More recently, corporate bond issuers have begun using the IRS curve to do hedging.

For all the above points, it is clear that the offshore market cannot use the onshore money market to start an offshore interest rate swap market. This was the reason why Hong Kong banks have come together to start an interbank CNY Hibor curve in January this year. Meanwhile, the PBOC has started managing interest rate policy changes.

• OMObecomestwo-waywithregularreverserepos: Firstly, the PBOC has replaced the use of RRR tool with reverse repurchase operations, regularising the reverse repos in the twice-weekly open market operations (OMO) since the beginning of June 2012. Previously, the OMO comprised only repos and the central bank bill auctions while reverse repos were conducted on a discretionary and bilateral basis with banks in need of liquidity.

Interest Rate MarketStarting a money market, IRS still non-existent

PBOC monetary policy overhaul underway

22

• Subtlyderegulatingcommerciallendinganddepositrates: Secondly, the PBOC has started to use the interest rate tool more frequently, cutting the policy targets on banks’ commercial lending and deposit rates twice on 7 June and 5 July 2012 (see Figure 24). These cuts were accompanied by a softening of the hard corridor by allowing banks to give discounts to their lending rates below the policy targets and premiums to their deposits rates above the policy targets. In the last move, the discount on lending rates is allowed up to 30% while the premium on deposit rates is allowed up to 10%.

The second move clearly reduced banks’ protected interest rate profit margin. Whileintendingtomakebanksmorecompetitive,itispossiblethatthePBOCis also looking at changing its interest rate policy targets.

Specifically, we believe the central bank might introduce a repo and reverse repo corridor target as its interest rate policy and move away from targeting banks’ commercial lending and deposit rates. The country’s top leaders and the central bank governor have openly talked about interest rate reforms at about the same time they have spoken about FX reforms. Hence, a regime shift could be underway which will switch the PBOC’s monetary policy from an active quantity-based approach using the RRR tool to a price-based approach using market interest rate tools. If so, this would create a more policy-driven and deeper Shibor market onshore from one that is currently liquidity-driven and often speculative.

Possible switch in interest rate targets coming up

Figure23:Typesofinterestratesmarketsintheoffshoredeliverable,offshorenon-deliverableforwardandonshoredeliverable markets

Offshore CNH NDF OnshoreCNY

Interbank borrowing

Tenors O/N, T/N, term deposits (to 1y) n.a. O/N, T/N, term deposits to 1y

Daily volume CNY2-4bn n.a. CNY500-800 bn

Ticket size CNY50-500 mn n.a. CNY300 mn

Bloomberg/ Reuters CGDR1 / CNHIBOR n.a. CCDR1 / SHIBOR

Interest rate swaps

Tenors inactive 1y-10y 1y-10y

Daily volume inactive CNY1-2bn. CNY3-4 bn

Ticket size inactive CNY50-300 mn CNY100-300 mn

Bloomberg/ Reuters CGSW1/CNHIRS=BRKR CCSWNI1/CNNDIRS= CCSWO1/CNYIRS7R=CNorCNYIRS3S-CN

MOF bonds

Tenors 2y, 3y, 5y, 10y, 15y n.a. 1y, 3y, 5y, 7y, 10y, 20y (longest 50y, not benchmark)

Daily volume CNY50-200 mn n.a. CNY300 bn

Ticket size CNY5-10 mn n.a. n.a.

Bloomberg/ Reuters n.a. n.a. GCNY2YR / CN2YT=RR

Source: Bloomberg, RBS

23

Figure24:PBOCone-yeardeposit-lendingratepolicycorridor, seven-day repo rate and 3m Shibor rate

Figure25:3mCNHHiborvsCNHFXimpliedrate,CNHdeposit rate and onshore Shibor (%)

Source: Bloomberg Source: Bloomberg

Money market

The daily transaction volume of CNH deposits and loans is estimated to be CNY2-3 billion. For overnight (O/N) and tomorrow-next (T/N) deposits, the size per transaction is around CNY100 million-1 billion while the size for term deposits is usually smaller around CNY50-200 million (See Figure 23).

On 3 January 2012, Hong Kong TMA announced it would establish a CNH Hibor curve by getting three banks to commit to publishing their interbank offered rates at 11am daily. Based on their customer flows, the rates from the three banks were initially wide apart from each other. More members were added subsequently. The number of contributing banks stands at 13 as of August 2012.

Although the rates posted by banks have become less disperse, the curve remains illiquid and is hardly traded. From overnight to three months, the rates are fixed at about the same levels as the rates implied from the USD/CNH FX forward curve (see Figure 25). For the longer tenors, the rates vary according to the fixing and banks’ funding requirements.

Interest rate swaps

As said above, the CNH interest rate swap market practically does not exist at all. The rates posted by Hong Kong banks basically are taken from the onshore market and there seems to be a tacit agreement among interbank market players not to trade the curve.

The best alternative is to create a new IRS curve using the CNY Hibor as fixing once the latter becomes more tradable. An IRS curve would help to deepen the CNH bond market, especially for secondary trading of the bonds, by allowing issuers and investors to hedge their interest rates.

Jan11

Mar11

May11

Jul11

Sep11

Nov11

Jan12

Mar12

May12

Jul12

CNH Hibor CNH FX implied CNH depo

Shibor

-2-1012345678

0123456789

10

Jan07

Jul07

Jan08

Jul08

Jan09

Jul09

Jan10

Jul10

Jan11

Jul11

Jan12

Jul12

1y deposit-lendingrate corridor

7d repo 3m Shibor

24

Sovereign benchmark curve

Only the Chinese government can set the sovereign CNH bond benchmark curve as the CNY is the sovereign currency of China. China’s MOF launched its first bond issuance in September 2009 in tenors of two-years, three-years and five-years, with tranches for retail and institutional investors. Since then, it has issued three more batches of bonds, with roughly six to nine-month frequency in December 2010, August 2011 and most recently in June 2012. In the last issuance, the MOF extended the duration of the sovereign benchmark curve from 10 years to 15 years.

Similar to the CNH corporate bond market, the MOF’s bonds in the offshore CNH market used to command significant coupon discounts over the onshore bonds. In fact, the yield discounts were wider than those issued by regular Chinese bank issuers. These premiums have since evaporated as investors’ expectations have switched from FX gains to bond gains (see Figures 26 and 27).

Repo market

One of the initiatives which emerged from the Hong Kong-London RMB Forum was a tripartite repo arrangement jointly set up by the HKMA central money market unit, Euroclear and J.P. Morgan in late June 2012. The system is designed to facilitate CNH repurchase transactions involving a wider choice of international securities through the Euroclear and J.P. Morgan platform. It can be a start to a full repo market for CNH bonds which would help to boost the extension of bank lending using the limited pool of CNH liquidity. The system also helps to reduce the settlement risks among banks.

Figure26:OffshoreMOFbenchmarkcurvevsonshorebenchmark curve as at 1 Sep 2012 (%)

Figure27:3yMOFoffshoreCNHbondvsonshorebond(%)

Source: Bloomberg Source: Bloomberg

00.51.01.52.02.53.03.54.0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

CNH governmentbenchmark

Onshore governmentbenchmark

Jun11

Sep11

Nov11

Jan12

Mar12

May12

Jul12

Spread (rhs,bp) CNY 3y bmkCNH 3y bmk

0

1

2

3

4

5

050100150200250300350400

25

Evolution of the market

There are broadly three phases of development in the CNH bond market over the past five years: 2007-2009 – a sellers’ market; 2010-2011 – the Big Bang paving way forglobalissuersandinvestors;and2012–abuyers’market.Webrieflydocumentbelow the important milestones in each phase.

The expansion outside of Hong Kong took off from 2010 after the central banks, investors and corporations increasingly showed support for CNY trade settlement and investment. It became a case of supply creating its own demand – the issuance of CNH bonds by global MNCs attracted global investors outside of Hong Kong and Asia.Webrieflydocumenttheimportantmilestonesinthesethreephases.

• 2007-2009:Sellers’market

In January 2007, the PBOC and the National Development and Reform Commission (NDRC) jointly announced that the country’s banks would start to issue CNY-denominated bonds outside of the mainland, specifically in Hong Kong. In June 2007, China Development Bank (a state-owned policy bank) became the first issuer, followed by other state-owned commercial banks. In the beginning, these issuances were primarily targeted to absorb the excess offshore RMB in circulation in Hong Kong and route them back into China.

The playing field was confined largely to the Hong Kong marketplace. Motivated by FX gains rather than yields, Hong Kong-based investors facing a weak USD currency peg and low USD interest rates were willing to accept yields as much as 250-300 basis points below the yields of bonds issued by the same banks onshore. This made the market very much in favour of sellers or issuers. The trade-off was that the maturity of the bonds was mostly capped at a three-year tenor because of the investors’ motivation for FX rather than yield gains.

In September 2009, China’s MOF issued its first offshore bonds in three tranches for both retail and institutional investors. This further spurred issuance from bank issuers, which had by then broadened to China-incorporated foreign banks’ subsidiaries, namely HSBC Bank (China) Company Limited and Bank of East Asia (China) Limited as the first two non-Chinese bank issuers. The MOF bonds also extended the CNH bond curve from three to five years, setting a sovereign benchmark.

This period also marked a critical phase of the RMB internationalisation process, which involved two important developments. First was the signing of bilateral CNY swap lines between the PBOC and the central banks from China’s strategic trade partners. These lines were designed to promote confidence in the use of CNY for trade settlement. Another critical development was the launch of the CNY trade settlement scheme on a pilot basis in July 2009 for selected Chinese coastal cities with Hong Kong and ASEAN member countries. Although the limitation of the scheme did not help much to boost CNY liquidity or deposits in Hong Kong (not fast enough to cope with the increasing demand for the CNH bonds), it signalled Chinese government’s efforts to facilitate the RMB internationalisation process by developing the offshore RMB bond market.

Bond Market

Jun2007–firstCNHbondissued by CDB

Dec2008–firstCNYswaplinesignedwith Korea

Jul2009–CNYtradesettlementpilotscheme launched

26

• 2010-2011:BigBang–issuersandinvestorsgoglobal

This period was marked by rapid liberalisation steps by China, paving way for Hong Kong to aggressively promote the market to global issuers, drawing in global investors. The first step came in February 2010 with the HKMA announcing that all forms of CNH fundraising by any Hong Kong or non-Chinese entities are allowed without prior approval in the Special Administrative Region (SAR) if the proceeds are not to be repatriated into China. In the latter event, repatriation would require the Chinese regulators’ approval. This was followed by the signing of a Memorandum of Cooperation between PBOC and HKMA in July 2010 that allows the Hong Kong banks to set up an interbank market for CNH FX and interest rates.

Hopewell was the first non-Chinese corporate issuer in July 2010. This was followed by the McDonald’s issue in August 2010 which became the first MNC issue. The McDonald’s issue set the precedent for MNCs with substantial business in China to look at the CNH market as an alternative funding source for their Chinese operations.

By this time, the market had grown four-fold since its launch in 2007 to CNY41 billion at the end of 2010. The demand for CNY liquidity to invest in the bond market became so great that it breached the central clearing quota managed by Bank of China (Hong Kong) Limited in October 2010. This activated the HKMA to announce that it would tap the CNY swap line facility from PBOC to ease the market pressure (see FX section).

The October 2010 episode prompted the Hong Kong TMA to start its own USD/CNH daily spot fixing at 11am in June 2011. This indicated China’s commitment to allow market forces to play a greater role in determining CNH exchange rate, without being pressured by the PBOC’s onshore daily fixing for the CNY. In addition to improving the stability of the CNH FX market, it reduces the FX spot basis risk for CNH-denominated products and in turn, provided more comfort for bond investors.

InSeptember2011,China’sVicePremierWangQishanvisitedLondontopromoteLondon as a global offshore RMB centre. Preceding that visit, in August 2011, Chinese corporates which had been kept out of the CNH bond market were allowed to tap the market. The PBOC launched the RMB QFII scheme and a pilot scheme to allow foreign banks to use CNH funds for recapitalising their Chinese operations.

In 2011, the market reached CNY225 billion, which was nearly a 23-fold increase since end 2007.

Despite the market opening up, the supply and demand imbalance remained in this phase. The low yields on CNH bonds reflected strong investor demand and showed that investors’ investment decisions were motivated by FX gains rather than returnfromyields.WiththeshiftinRMBappreciationexpectations,wehaveseenthat investment in RMB bonds has come under greater scrutiny and requires more rigorous credit analysis.

February2010–allformsofCNHfundraising allowed in Hong Kong

July2010–CNHinterbankmarketlaunched

October2010–firstsupranationalissue by ADB, also first 10-year issue and first bond traded on the Hong Kong Stock Exchange

December2010–firstnon-AsianEMissuer, VTB Bank

June2011–HKTMAstarteddaily11amfixingforUSD/CNH

September2011–ChineseVicePremier visited London to promote London as a RMB centre

27

• 2012:buyers’market

The concerns on China’s growth and the subtle shift in the PBOC’s FX policy stance from the beginning of this year combined to turn this market from a sellers’ market to a buyers’ market. The yield premium has now almost completely closed up. Considering that onshore and offshore CNY bond markets have their inherent risks, the question now is whether there should be any yield differentials between the two markets.

For the onshore market, the basic issue is market access and the risk of capital controls. For the offshore market, the issue is currency convertibility. Until the CNY becomes fully convertible, there is still a chance, however remote, that China decides to backtrack to a full non-convertibility status. In a way, the risks onshore and offshore are in fact not dissimilar, stemming from the FX angle.

Moreover, the CNH DF market has priced in the shift in RMB appreciation expectations, and has moved the basis swaps in favour of foreign issuers who would issue CNH bonds and swap the proceeds into other major currencies like USD. These market developments have provided favourable arbitrage opportunities for issuers who do not have imminent needs in RMB.

Despite market pressure, issuance volume continues to go up and investors’ interests remain sturdy as issuers were willing to adjust to higher yields. To a large extent, this was aided by further market reforms and liberalisation of rules. In January 2012, the HK TMA launched CNY Hibor fixing. In January and February 2012, the HKMA consecutively eased Hong Kong banks’ risk limits and statutory liquidity requirements (SLR) on their CNY exposure. Onshore, reforms took the form of a widening of the USD/CNY intra-day trading band in April 2012, and two rounds of rate cuts in June and July 2012 which came with a softening of the corridor on banks’ interest rate margin. The rate cuts in particular helped to further tighten the yield premiums of the onshore bonds to the offshore CNH market.

Two other developments also surfaced in parallel. In February 2012, the Shanghai municipal government released a blueprint, setting a 2015 target for the city to become the global pricing centre for all CNY-denominated financial products onshore and offshore. In April 2012, the City of London followed up on the Chinese Vice Premier’s visit in September 2011 to London by launching a London-Hong Kong forum on the global offshore RMB market. These are very subtle manoeuvres going on here which we will discuss in a later chapter.

WhileShanghaihasitslong-termambitiontobecomethecountry’skeyfinancialcentre, including taking over the current role of Hong Kong as the main offshore RMB pricing centre, Hong Kong has been given the chance to tap on the global financial centre strengths of London to advance its RMB business in the interim. How the future of the two cities pan out would be something to watch out for.

Meanwhile, in the pipeline, a second central clearing line will be set up in Singapore, to be operated by a Singapore branch of a Chinese bank. Tokyo and Taipei are also separately discussing their own respective direct clearing lines into China. All these clearing lines would bypass Hong Kong, which as we said in the last chapter, has now become a more mature market in our opinion.

Euro crisis and subtle shift in PBOC’s FX policy

January2012–HKTMAlaunchedCNYHibor fixing

January2012–HKMAeasedbanks’CNYopenrisklimits

February2012–HKMAeasedbanks’SLRforCNYdeposits

February2012–Shanghaisets2015targettobeglobalCNYpricingcentre for both onshore and offshore markets

April2012–PBOCwidenedonshoreUSD/CNYintra-daytradingband

April2012–CityofLondonlaunchedLondon-Hong Kong forum

JuneandJuly2012–PBOCcutinterest rates twice and softened policy rate corridor

28

At this point, we see the market has evolved from a seller’s market, where investors continuously seek returns on FX appreciation, to a buyer’s market, where investors would treat CNH bonds as a credit product and begin to evaluate the credit-worthiness of the bond and not only the FX gains. The imbalance between demand and supply has improved but not quite yet to demand-supply equilibrium, as shown by the narrowing of the offshore/onshore premiums/discounts. The biggest uncertainty now is the PBOC’s FX policy direction as investors adjust their expectations from chasing FX gains to chasing yield or bond gains.

Issuer Base

The CNH market has experienced an exponential growth since 2010. As of August 2012, total new issues (including CDs) in 2012 amounted to CNY199 billion. Issue volume for financial institutions (FIs) grew at a CAGR of 155% from 2010 to August 2012 while the issue volume for corporates increased at a CAGR of 54% in the same period.

In its early stages of development, CNH issuance was dominated by Chinese government (Ministry of Finance), Quasi-government (policy banks) and China/ Hong Kong FIs. Since the landmark reforms in July 2010, which paved the way for offshore entities to issue CNH bonds in Hong Kong, the issuer base has expanded greatly in terms of issuer type, credit quality, geography, sector and tenor.

Types of issuersCNH bond issuers consist of state-owned enterprises, MNCs, Hong Kong branches of Chinese and foreign banks, and onshore banks direct issuance banks. The CNH market is still dominated by Chinese FIs (both policy banks and commercial banks), which accounts for 70% of total market share as of August 2012. China/Hong Kong corporates represents the second largest category of issuers (apart from MOF issuance), accounting for 8% of total market share as of August 2012.

From 2010 to August 2012, non-Chinese issuers accounted for over 14% of total CNH issue volume, of which corporates made up 50% of the issuer base and FIs took up 47% of the market share.

Chinese FI are the leading issuers in the CNH market; foreign FIs and corporates gained market share since the opening of CNH bond market to offshoreentitiesinJuly2010

Figure28:Issuancebyissuertype(CNYbn)

Source: Bloomberg; includes both bonds and CDs issuance

Shift in investors’ expectations from FX gains to yield or bond gains

Chinese Corp Chinese FI Foreign Corp Foreign FI China MOF

10 10 1641

199191

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012

29

Figure29:Increasingparticipationbynon-Chineseissuer(CNYbn)

Source: Bloomberg; includes both bonds and CDs issuance but excludes China MOF issuance

Figure30:IssuancebyChineseissuers(CNYbn)

Figure31:Issuancebynon-Chineseissuers(CNYbn)

Source: Bloomberg; includes both bonds and CDs issuance

Source: Bloomberg; includes both bonds and CDs issuance

Non Chinese Chinese

2007 2008 2009 2010 2011 20120

40

80

120

160

200

Corp FI China MOF

0

30

60

90

120

150

180

2007 2008 2009 2010 2011 2012

Corp FI Supranationals

0

5

10

15

20

25

2010 2011 2012

30

Figure33:Issuancebycountry(2011)

The geographical composition of the issuer base has also changed over time. Since the first MNC issuance by McDonald’s in August 2010, we have seen a growth in issuance by non-Chinese companies, notably Europe, North America and other parts of Asia. In particular, CNH bond issuance by European issuers increased from a share of only 1% in 2010 to 7% and 6% in 2011 and August 2012 YTD respectively.

Wehavealsoseenanissuertestingthenewmarketwithalternativeissuingstructure,namely Khazanah Nasional, as the first issuer to sell an Islamic bond in the offshore RMB market. The success of this transaction demonstrates the readiness of the market to accept innovation.

In addition, Korean frequent issuers have also accessed the market leveraging on the window in the swap market.

Figure32:Issuancebycountry(2010)

Figure34:Issuancebycountry(2012)

Source: Bloomberg; includes both bonds and CDs issuance but excludes China MOF issuance

Source: Bloomberg; includes both bonds and CDs issuance but excludes China MOF issuance

Source: Bloomberg; includes both bonds and CDs issuance but excludes China MOF issuance

88%

1% 4% 4% 3%

HK/China Europe

Korea US

Southeast Asia Japan

Supranationals Others

HK/China Europe

Korea US

Southeast Asia Japan

Supranationals Others

88%

6% 3%

1% 1% 1%

0.4%

HK/China Europe

Korea US

Southeast Asia Japan

Supranationals Others

83%

7% 2% 2%

3% 1% 0.4%

1%

31

In terms of tenor, the majority of the issuances are concentrated in the shorter end of the curve – three years or less where issuers enjoyed the deepest investor pool. Traditionally, investors’ involvement was driven by an anticipation of RMB appreciation and investors tended to have a directional view in the shorter maturities. As the market evolves further where there are new entrants to the market, issuers were successful in closing transactions with longer maturities. The most notable was when China Development Bank raised CNY1.5 billion for the first 15-year CNH offering in January 2012 where insurance companies supported the transaction. China Development Bank did another CNY1 billion 20-year trade in July 2012.

Figure35:Issuancebytenor

Figure37:Issuancebyissuesize

Figure36:Issuancebytenor

Figure38:Issuancebyissuesize

Source: Bloomberg; includes both FI and Corp bonds and CDs issuance but excludes China MOF issuance

Source: Bloomberg; includes both FI and Corp bonds and CDs issuance but excludes China MOF issuance

Source: Bloomberg; includes only Corp bonds

Source: Bloomberg; includes only Corp bonds

Size-wise, 33% of CNH issuance has an issue size of CNY500 million-1 billion, reflecting investors’ preference for liquidity. As of to date, the record of the largest single issue volume is kept by the China Development Bank (CNY5 billion issue) intheFIspace,andtheNewWorldChinaLand’sCNY4.3billionissueinthecorporates space.

61%

6% 0.4% 2%

<=2 yrs 3yrs

5yrs 7yrs

7-15yrs >15yrs

31%

0.2%

75%

7% 1% 2%

14%

0.7%

<=500m >500m - <=1bn

>1bn - <=1.5bn >1.5bn - <=2bn

>2bn - <=3bn >3bn

33%

2.9%

18%

29%