home loan market: consumer analysis

TRANSCRIPT

1

“HOME LOAN MARKET: CONSUMER

ANALYSIS”

Submitted by :(CR-3)

Divya Khunt (30301280)

Divyesh Lakhani (30301322)

Submitted to:

Unitedworld School of Business

Karnavati knowledge village, A/907, Uvarsad, Gandhinagar Highway,

Ahmedabad 382422

2

DICLARATION

We hereby declare that this project submitted to UnitedWorld School of

Business, Ahmedabad. Under the guidance of Dr.Kishor Bhanushli.In the

partial fulfillment of the requirement for the degree of PGDM.This is a result

of our team work carried out during January to march 2014.

This report is entirely an outcome of our team effort and has not been

previously submitted to any other institute or university for any other

examination and for other purpose by any other person.

DATE:

PLACE: Ahmadabad

3

ACKNOWLEDGMENT

"Gratitude is not a thing of expression; it is more matter of feeling."

There is always a sense of gratitude which one express towards others for

their help and supervision in achieving the goals. This formal piece of

acknowledgement is an attempt toexpress the feeling of gratitude towards

people who helpful us in successfully completing of our report. We would

like to express our deep gratitude toUNITEDWORLD SCHOOL OF

BUSINESS.

We feel great pleasure to express our feeling of guidance to our academic

guide Dr. Kishor Bhanushalifor giving the valuable guidance and

suggestion for successful completion of this dissertation. He is always with

us for his competent guidance and valuable suggestion throughout the

pursuance of this research project. And also thanks to all team member

without them support this project can not complete.

In this project the great emphasis is given to home loan. We wish and

express our heart full gratitude to the project guide manager of HDFC bank.

His guidance and suggestion throughout the project, without which would

not have been able to complete this project.

Last but not least we would also like to place of appreciation to allthe

respondents whose responses were of utmost importance for the

project. Thankful to all the respondents whose cooperation& support has

helped us a lot in collecting necessary information.

This project is very challenging opportunity for us to update ourselves. So, I

would like to give thanks to everyone who help us directly and indirectly in

preparing this project.

4

EXECUTIVE SUMMERY

Home loan is dream of person that show the quantity of effort, sacrifices

luxuries and above all gathering funds little to afford one‟s dream. Home is

one of the things that covered everyone want to own. Home is shelter to

person where he rests and feels comfortable. The housing sector plays an

important role in economic development of the country.

Our project title is “Marketing of home loan”. We selected this topic because

Indian housing finance industry has grown by leaps and bound in few years.

A total home loan disbursement by bank hasrisen which witness phenomenal

growth from last 5 years. There are greater number of borrows home loan.

Our objective this study is to know the Customers perceptions about home

loans.

The introduction part includes all the information about home loan and the

history of the home loan. And process of home loan and disbursement of

home loan. In the research methodology we have taken both primary data as

well secondary data, in the primary data we had make a questionnaire to

check the satisfaction level of customer about home loan. In the secondary

data we had studied the annual report of RBI, commercial bank and HDFC

bank.

At the end it illustrates the suggestion and findings based on the analysis

done in the previous section finally deal with the conclusion part.

5

LIST OF TABLE

SR. NO TABLE NAME P.NO.

1 Selection Of Bank 12

2 Criteria Considering While Taking Loan 13

3 Interest Rate 14

4 Satisfaction Level 15

5 Loan Amount 16

6 Facing Problem While Taking Loan 17

7 Age Of Respondent 18

8 Gender Of Respondent 19

9 Occupation Of Respondent 20

10 Income Of Respondent 21

11 Satisfaction level and gender 22

12 Gender and loan amount 23

13 Problem and occupation 24

14 Income level and Interest rate 25

15 Income level and loan amount 26

16 Satisfaction level and gender 27

18 Gender and loan amount 28

19 Occupation and problem 29

20 Income level and interest rate 30

21 Income level and loan amount 31

6

LIST OF FIGURE

SR.NO Name of figure P.NO

1 Selection of bank 12

2 Interest Rate 14

3 Satisfaction Level 15

4 Loan Amount 16

5 Problems 17

6 Age 18

7 Gender 19

8 Occupation 20

9 Income 21

10 Satisfaction Level And Gender 22

11 Gender And Loan Amount 23

12 Problems And Occupation 24

13 Income Level And Interest Rate 25

14 Income Level And Loan Amount 26

7

TABLE OF CONTENT

CHAPTER TITLE PAGE NO

TITLE PAGE I.

DECLARATION II.

ACKNOWLEDGEMENT III.

EXECUTIVE SUMMARY IV.

LIST OF TABLE V.

LIST OF FIGURE VI.

1 INTRODUCTION 1

1.1 Introductions of home loan

1.2 Advantages of home loan

1.3 Disadvantages of home loan

1.4 Disbursement of home loan

2 LITERATURE REVIEW 6

3 RESEARCH METHODOLOGY 9

3.1 Research statement

3.2 Research objective

3.3 Research design

3.4 Sources of data

3.5 Sample design

3.6 Tools used for data analysis 11

4 DATA ANALYSIS 12

5.1 Univariat analysis

5.2 Bi-variat analysis

5.3 Hypothesis testing

5 FINDINGS 32

6 CONCLUSION 33

7 REFERENCE 34

8 ANNEXURE 35

8

CHEPTER 1

INTRODUCTION

9

10

1.1. INTRODUCTION TO HOME LOANS

Home is a dream of a person that shows the quantity of efforts, sacrifices luxuries and

above all gathering funds little by little to afford one‟s dream. Home is one o f the

things that eve ryone one wants to own. Home is a she lte r to pe rson where he

rests and fee ls comfortab le. Many banks provid ing home loans whe ther

commerc ia l banks or financ ia l inst itut ion to the peop le want to have a home.

HDFC- (Hous ing Deve lopment and F inance Corpora t ion) home loan, Ind ia

have been serving the peop le for around three decades and provid ing var ious

hous ing loan accord ing to the ir va r ied need a t at trac t ive & reasonab le interest

rate. Owing to the ir ne twork o f financ ing, HDFC hous ing loans provides

service at your door step and he lps you find a home as pe r your requirements.

Many banks are providing home loans at cheapest rate to attract consumers towards

them.

The more customer fr iend ly at t itude o f these banks, currently o ffer to

consumers cheapest loan over homes. In view o f acute hous ing sho rtage in

the country, and keep ing in mind the soc ia l, economic ro le o f commerc ia l

bank in the present t ime, t he RB I ad v ised ba nk s to encourage the flow of

credit for housing finance. With the RBI reduc ing bank ra te, the home loan

market rate s nose-d iving by 50 bas is po ints.

The HDFC Bank and Standard cha rte red bank has become the firs t p layer

inthis sec tor to announce a hous ing loan for a 20 yea rs per iod. No doubt

it wil l enhance theend cost peop le to p lan the ir house over longer dura t ion

now; it has been made easy for a person to buy tha t dream house which the

dreamt o f long ago.

11

1.2. ADVANTAGES OF HOME LOANS:-

The various benefits of home loans arising to the customers are:-

Attractive interest rate:

The various banks offer attractive interest rates to boost and help their customers. Many

banks provide loans on fixed or floa t ing ra tes to fac il ita te consumers as per

the ir needs.

Help in owning a home:

The home availed by a person with the help of banks because they provide technical and financial

assistance to customer for owing their dream home.

No requirement of guarantor:

The commercial banks now a day liberalize their laws regarding home loans. Some of

banks don‟t even require the guarantor to grant loan to their consumers. They also make

consumers free by reliving him to find a guarantor to complete the proceedings of

availing loan.

Door-step services:

These doors to step services are provided from enquiry stage to the final disbursement

takes place such services are beneficial for customers in present busy life. Banks like

ICICI bank and standard cha rte red bank provide door to s tep se rvices to

cus tomers to bo rrow loan.

Loan period:

There are many banks which provide maximum loan tenures up to 15-20 years based on

the loan amount and the credibility of customers. This relieves the customers to repay

loan amount till a long period

For accidental death insurance:-

Some banks provide free accidental death insurance with housing loan which is

also beneficial for the customers. These benefits o r advantages o f home loans are

respons ib le for mak ing than so popular among customer that a person who doesn‟t

have their home and want to buy, they do it with home loan. Home loans help such

persons in making their dream home.

12

1.3. DISADVANTAGES OF HOME LOANS:-

The main disadvantages of home loans are high lightened as below:

Delays in processing:-

Many t imes, the re a re huge de lays in process ing o f provid ing home loans

because var ious formula t ions to be fulf il led in this process. Due to these

de lays cus tomers fee l mentally as well as financially weak.

Fluctuating interest rates:

Some banks give home loans at floating rates, which fluctuate at Different intervals due

to some reasons. These changes sometimes, may lead to increase in interest rate which

will increase the cost of home loans to the customers.

High cost:

The pub lic secto r banks cha rge high process ing cost for home loan‟s

sanc t ioning. They are forced to pay serious charges at various stages to fulfill the

requirements. Some consumers are no t ab le to pay such charges so such peop le

could not ava il the benefits o f home loan schemes.

Problems in disbursement:

There are many prob lems in d isbursement o f home loan amount. There is

some de lay in disbursement of loan amount to the customers due to legal formalities.

This causes problems to the customers. These are limitations or disadvantages of home

loans. But sometimes some banks charges high insta llments to repay loan amount.

13

1.3. DISBURSEMENT OF HOME LOANS:-

The every bank has its own procedure to disburse the loan amount among customer. After choosing your

right home, the next step is disbursements of home loans. The loan amount is disbursed after identifying

and selecting the property or home that are purchased and submit the requisite legal documents. In the

disbursement of home loans a clear title and full verification to ensure that a person has full rights on his

house. The 230A clearance of seller and 371 clearances from the appropriate authority of income tax is

also needed.

1.3.1. Eligibility criteria:-

However, if one is a resident or non-resident individual who is planning to buy a house in India, one can

apply for a home loan. If a person has decided to buy a property in the near future, he can apply for a loan

before even selecting the property. Once them maximum amount onto put into property has been

decided, the housing finance intuition or banks will let the customer know that how much he is eligible for

and this helps to plan out budget.

1.3.2. Conditions regarding co-applicants: -

All Housing Finance Institutions lay down conditions on who can be co-applicants. All

co-owners to the property. Need to be co-app licants to the loan necessar ily.

These institutions do not permit minors to join in as either co-owner or as co-applicants

because a minor is not eligible to enter into a contact as per law. They do not permit even

friends or relatives who are not blood relatives to take a property jointly. However,

Income of co-applicants can be clubbed together to get higher loan eligibility. Given

information are throws light on acceptable relationship of a co-applicant for clubbing of

income. Income Clubbing of Co-applicants:

Husband-Wife: -

Income of husband-wife can be clubbed.

Parent - son:

It can be clubbed if only son is there but not if any male sibling exists.

Brother-Brother:

If they are currently staying together and intend to stay together inthe new

property, then only, their income-can be clubbed for above purposes.

Brother-Sister:

No clubbing- is possible.

Sister-Sister : -

No clubbing is possible.

Parent-Minor- Child:

No clubbing is possible in this case also.

14

1.3.3. General Terms and Conditions: -

T he fo l lo w ing a re t he te r ms a nd co nd it io ns applicable to the basic home loan

product only. These are likely to change on the basis of the var iat ions o f the home

loan product. Typ ica lly, in genera l home loans, the fo llowing conditions are

applicable.

The loan to value ratio (LTV) cannot exceed a particular percentage. This differs

from product to product and from one hosing finance institution bank to another.

The components of the value of the property calculated here are covered under

cost of property.

The maximum tenure of the bank is nominally fixed by HFI/Bs. However,

HFls/Bs do provide for different tenures with different terms and conditions.

The installment that one pay is normally restricted to about-50-per cent of the

monthly-gross income of the candidate.

The total monthly outflow towards all the loans that have been availed of,

including the current loan is normally restricted to 50% of the

gross monthly income.

One will be eligible for a loan amount which is the lowest as per one's eligibility.

This is calculated as per the LTV norms, the HR, norms and the FOIR norms as

mentioned above.

15

CHAPTER 2

LITERATURE REVIEW

16

LITERATURE REVIEW

Rao K. N. conducts a research on “Retail Banking – Emerging Issue in Home Loan”

in the year 2005. In this research the researcher revealed that during 2002-03 housing

loans by banks grew at a hefty growth rate of more than 100%. The factors that

contributed to this aggressive growth in the portfolio of housing loans of banks and HFC

are: Tax intensives on repayment of principal and interest, rising income level of middle

class, falling interest rate, stable real estate prices, easy availability of housing loans, low

returns on the investment opportunities available in the market. They also concluded that

although there is strong growth in housing loans by financial situations in India, we are

still behind the developed countries in terms of housing loans to GDP ratio.

BrarJasmindeep conducts a research on a “Performance of Housing Finance

Companies” in the year 2005.The main objectives of this research was to study the

operational performance, and the financial performance of the selected institutions. The study

covers three institutions viz. HDFC, LIC & PNB. The study is based on secondary data that

have been collected from the annual reports and web sites of the institutions selected under

study. It covers the period from 1990-91 to 2002-03. The performance of the selected

institutions has been studied by using percentages, compound growths rates and various

ratios.

LallVinay conducts a research on “Housing credit situation in eighties “in the year 1984.

The main objective was attention upon „formal factor‟ (Permanent Construction) which served

mainly to the HIG and MIG, the loan meets only 47% of the price of the house, forcing the

borrowers to make very large down payments. Also the price of a typical house was above 3

times the annual families‟ income of the borrowers. In spite of, the entire system of housing

allocation and credit the supply of affordable funds was much smaller than demand. Thus,

large growth in urban population and the historically low priority given to housing, supply

falls very short of demand and need.

Vandell, Kerry D Analysis in the Year 2008 And He Analysis the Sharpe rise and then suddenly drop down

home price from the period 1998-2008. Changes in prices are for the reasons as such economic fundamentals,

the problem was not subprimelending, but the dramatic reduction, then increases in interest rates during the

early mid-2000,the hosing – boom was concentrated in those market with significant supply side restriction,

which tend to be more price- volatile; and the problem was not excess supply of credit in aggregate, or increase

in subprime percentage but rather in the increased or reduced presence of certain another Mortgage products.

17

M.Mahadeva conducts a research article on “Housing Problem and Incompatibility

Experience from a South Indian State” in the year 2004.In this article, the author has

analyzed the nature and distribution of the housing problem in Karnataka and examined how the

state has addressed this issue. In particular, it considers the strategies adopted during the 90s and

identifies a number of failures including the task force on housing. Some of the major

weaknesses, pertaining to 51 incidences by type and by rural-urban areas, on approaches, on

financial requirements and issue of development and redevelopment are examined to propose

alternative policy strategies to effectively address the housing problem in the state. From the

analysis it is found that Karnataka is not an exception to the general rule that housing strategies,

which were evolved over decades, have not taken the direction expected.

Mr.Krishnamachari conducts a research on “problem of the national housing policy” in

year 1980. The research stated that shelter is a basic human need and as an intrinsic part of

human settlement, is closely linked with the process of overall socioeconomic development.

Though a house is essentially a place of dwelling, it also fulfills many important social needs of

the household. Besides providing shelter, it creates employment, generates voluntary salving and

creates a conducive condition needed for achieving crucial goals”

Berstain David (2009) examined in his study taken from 2001 to 2008 that in this period there is

increased use of home loans as compared to private mortgage insurance (PMI).he have divided

his study into four sections. Section 1 describes why people are going more for home loans than

PMI. the main reason for this that now home loans market provide Piggybank loans for those

people who don‟t have 20% of down payment. Section2 tells the factors responsible for the

growth of home loans and the risks on shifting toward home equity market without any PMI

coverage. PMI can protect lenders from most losses up to 80% of LTV and the absence of PMI

will result in considerable losses in an environment. Section 3 tells the measures in changes of

type of loans. For this he have taken the data from the 2001 and 2007 AHS a joint project by

HUD and Census The results of this analysis presented in Table One reveal a sharp increase in

the Prevalence of owner-occupied properties with multiple mortgages among properties with

firstmortgages. Section 4 describe the Financial status of singlelien and multiple- lienhouseholds

and for this he have taken the survey of consumer finance and show that financial position is

more weaker in multiple loans than the single loans.

18

La cour Micheal (2006) examined the home purchase mortgage product preferences of LMI

households. Objectives of his study to analysis the factors that determined factors their choice

of mortgage product is different income groups have some specified need to meet particular

product. The role pricing and product substitution play in this segment of the market and do

results vary when loans are originated through mortgage brokers? For this they have use the

regression analysis and the results are high interest risk reduce loan value. Self-employed

borrower chooses reduce documented loans than salaried workers Use of this product type

seems to be more prevalent among borrowers with substantial funds for down payment and

better credit scores. In case of pricing Multi families requires price premium and larger loans

carry lower rate. And the role of time, particularly, the time required for the loan to proceed

From application to closing. It is find that government lending taking the longest time and

Nonprime loans the shortest time.Multi family properties take longer time in closing. And

during peak season take longer time to close. And for last objective it is find that broker

originated loans close faster. The effect of mortgage brokers on pricing and other market

outcomes is fertile ground for additional research

Haavio, Kauppi (2000) stated that countries where a large proportion of the population lives

in owner – occupied housing are experiencing higher unemployment rates. Than countries

where the majority of people live in private rental housing, which might suggest that rental

housing enhances labor mobility. In this paper, they develop a simple inter temporal two

region model that allow us to compare owner occupied housing markets to rental markets and

to analyze how these alternative arrangements allocate people in space and time. Announced

that it will offer loans for Rs. 2-10 lakh at 12.5 percent the lowest rate offered by any housing

finance provider, big brother SBI has taken the rate war in the home loans category to new

heights. This is because, apart from the low rate, the interest on these loans is calculated on

principal, which is reduced every month unlike other housing finance companies which

calculate interest on annually reducing basis

19

CHAPTER 3

RESEARCH METHODOLOGY

20

RESEARCH METHODOLOGY

Research methodo logy is a way to systematica lly show the research prob lem. it

may be understood as a sc ience o f studying how research is done sc ientifica lly. It

is necessary for the researcher to know not only re search methods but a lso the

methodo logy. This Section includes the methodology which includes. The research design,

objectives of study, scope of study along with research methodology.

3.1. NEED FOR RESEARCH:

Need of this research is help to know the ideas of customers about home loan products

and services. And how to do marketing of home loan product to the customer in the

market. And also learn about various aspect of HDFC home loan ltd. It also provide

knowledge about understating bank statement, income statement, KYC terms, loan

eligibility, borrower‟s contribution, EMI, rate of interest, introduction to property market,

ownership & transfer of title, property costs etc.

3.2. PROBLEM STATEMENT:

This research is conducted to study on“Marketing of Home loans”

3.3 OBJECTIVES OF RESEARCH:

3.3.1. Primary objective:

The main objective of this study is to know the Customers perceptions about home loans.

To know the ideas of customers about home loan products and services.

To make comparative study of Disbursement of home loans by

Commercial banks.

To analyze the history of home loan.

21

3.3.2. Secondary objectives:

To know the current scenario of the home loan products of different bank in the market.

To get knowledge about “ Indian hosing finance such as operation

perform by banks, different type of bank product, service”

3.4. RESEARCH DESIGN:

3.4.1 Type of research: There are mainly three types of research design:

Exploratory research design

Descriptive research design

Causal research design

This project is based on exploratory study. It was an exploratory study when the know the

scenario of marketing of home loan in market. And also study was made for comparison of disbursement of home loan by commercial banks.

3.5. SOURCE OF DATA:

There are mainly two sources of data to be collected:

Primary data

Secondary data

To fulfill the information need of the study. The data is collected from primary as well as secondary sources.

Primary data are collect from the survey method and I conduct the 50 sample of survey in the project to know the marketing of home loan from the customer.

Secondary data are collect from internal sources. The secondary data was

collected on the basis of organization file, official records, newspapers, magazines, management book and website of the company.

3.6. SAMPLE DESIGN:

3.6.1. Sampling Design: Here, non-probability convenience sampling method has been used.

3.6.2. Sample size: For the questionnaire wehave taken the sample size 50 of respondent who have

taken home loan.

22

3.7. TOOLS USED FOR DATA COLLECTION:

The study based on secondary data. The relevant sources of Secondary Data are

use like:

www.HDFCbank .com

www.shodhganga.com

www.canstar.com

With the help of these sources we find the rate of home loan of different banks.

3.7.1. Data collection period: Datacollection period for this project is 15 days.

3.8. TOOLS USED FOR DATA ANALYSIS:

Data has been presented with the help of bar graph, pie charts, and line graphs etc. and, in SPSS frequencies and used pie charts and bar charts and cross tabulation. And more important is hypothesis testing.

23

UNI VARIATE ANALYSIS

SELECTION OF BANK

Table 1

Figure 1

From the above graph it interpret that 32% people taken loan from the sbi, while 20%

people taken loan from the HDFC bank. And 2% people took loan from UTI, IDBI,

TATA capital, PNB home finance. And 6 % people have taken loan from Kotak. So, we

can say that more than 50% people taken loan from the SBI and HDFC so, both the bank

covered more than half the market of home finance.

ICICI8%

HDFC20%

UTI2%

Tata capital2%

IDBI2%

Bank of baroda

12%

SBI32%

Axis bank4%

Kotak6%

PNB home finance

2% other10%

Selection of Bank

Bank Respondent Percenage

ICICI 4 8

HDFC 10 20 UTI 1 2 Tata capital 1 2 IDBI 1 2 Bank of baroda 6 12 SBI 16 32 Axis bank 2 4 Kotak 3 6 PNB home finance 1 2 Other 5 10 Total 50 100

24

CRITERIA CONSIDER WHILE TAKING LOAN

Table 1

From the above table It Interpret highest mean is 6.6. Of loan tenure and second highest

is 5.1.so, we can say that highest number of people gives more important to loan tenure

and followed by margin amount and then loan eligibility.

List Of Criteria Mean

Faster processing 3.2000 Interest rate 2.9600

Brand Image of Bank 4.0800 Margin Amount 5.1000 Pay Back Period 4.4800 Schemes 4.9600 Loan Tenure 6.6000

Loan eligibility 4.7000 Other 8.8800

25

INTEREST RATE

Table 2

Figure 2

From the above graph it interpret two types of rate are fixed and floating rate from which

58 % people pay fixed rate for their home loan while 38% people pay floating rate for the

home loan and remaining are pay other interest rate. So we can say that more number of

people preferred fixed rate for their home loan.

Fixed rate58%

Floating rate38%

other4%

Intrest Rate

Type of Interest Rate Respondent Percentage

Fixed rate 29 58 Floating rate 19 38 Other 2 4

Total 50 100

26

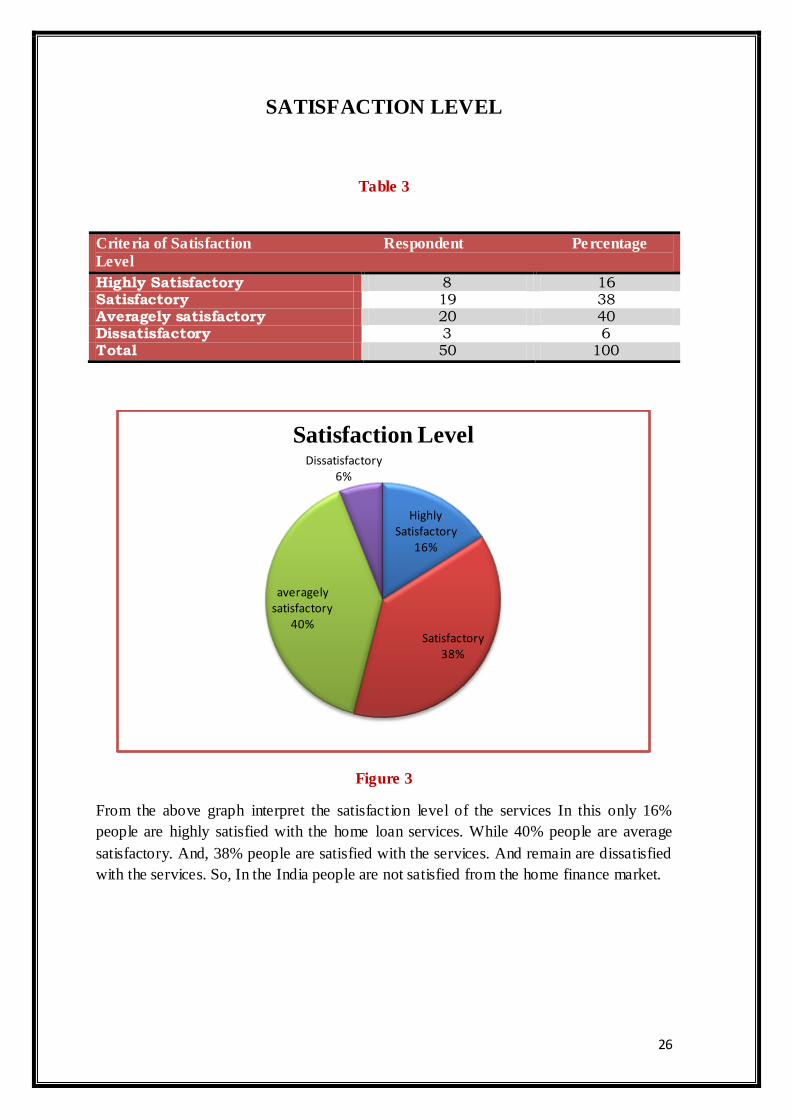

SATISFACTION LEVEL

Table 3

Figure 3

From the above graph interpret the satisfaction level of the services In this only 16%

people are highly satisfied with the home loan services. While 40% people are average

satisfactory. And, 38% people are satisfied with the services. And remain are dissatisfied

with the services. So, In the India people are not satisfied from the home finance market.

Highly Satisfactory

16%

Satisfactory38%

averagely satisfactory

40%

Dissatisfactory6%

Satisfaction Level

Criteria of Satisfaction Respondent Percentage

Level

Highly Satisfactory 8 16 Satisfactory 19 38 Averagely satisfactory 20 40 Dissatisfactory 3 6 Total 50 100

27

LOAN AMOUNT

Table 4

Figure 4

From the above graph It Interpret about loan amount from its 48% people are taking 5 -10

lakh amount of home loan and 42% people are take 1-5 lakh loan amount.so, most of the

people take 5-10 lakh loan amounts from the bank.

less than 1 lakh6%

1-5 lakh42%5-10 lakh

48%

more than 10 lakh4%

Loan Amount

Loan amount Respondent Percentage

Less than 1 lakh 3 6 1-5 lakh 21 42

5-10 lakh 24 48 More than 10 lakh 2 4 Total 50 100

28

PROBLEM FACING WHILE TAKING LOAN

Table 5

Figure 5

From the above graph It Interpret what are the problem facing by the respondent so, 58%

people facing problem of lack of knowledge i.e. awareness of the services and 26%

people face the problem of procedural delay means that the process of the loan passing is

very time consuming and complex. So, we can say that more number of people are not

aware about facility provided by the bank because of lack of knowledge.

lack of knowledge

58%procedural delay and non-

corporetion

26%

other16%

Problem Facing While Taking Loan

Problem Respondent Percentage

Lack of knowledge 29 58 Procedural delay and non-Corporetion 13 26 Other 8 16 Total 50 100

29

AGE OF RESPONDENT

Table 6

Figure 6

From the above graph it interprets that age of respondent from them 38% people‟s age is

between 35-45. 28% people‟s age is between 25-35.and 26% people‟s age is 45-55 and

remaining age is above 55.so, we can say that more number people‟s age is between 35-

45.

25-3528%

35-4538%

45-5526%

above 558%

Age

Age No. of Respondent Percentage

25-35 14 28

35-45 19 38

45-55 13 26

above 55 4 8

Total 50 100

30

GENDER OF RESPONDENT

Table 7

Figure 7

From the above graph it interprets that gender of the respondent from that 72% people are

male and 28% people are female. So we can say that highest number of people is male.

male72%

female28%

Gender

Gender Respondent Percentage

Male 36 72 Female 14 28 Total 50 100

31

OCCUPATION OF THE RESPONDENT

Table 8

Figure 8

From the above graph it interpret that occupation of the respondent from

that 50%people are salaried i.e. they are doing job. 26% people are self-

employed and 16% are professional and remaining 8 % are in other

occupation. So, we can say that who are doing job and salaried those all

person preferred home loan.

professional16%

self-employed

26%salaried50%

other8%

Occupation

Occupation Respondent of occupation

Percentage

Professional 8 16 Self-employed 13 26 Salaried 25 50 Other 4 8

Total 50 100

32

INCOME OF RESPONDENT

Table 9

Figure 9

From the above graph it interpret the income level of the respondent from

that 50% people’s income is between 2-4 lakh and 24% people’s income

is 4-6- lakh, 16% people’s income is more than 6 lakh and remaining

10% income is below 2 lakh. So we can say that person taken loan that

all people’s income is between 2-4 lakh and less number of people that

income is below 2 lakh.

below 2 lakh10%

2-4 lakh50%

4-6 lakh24%

6 lakh and above16%

Income

Income Respondent Percentage

Below 2 lakh 5 10 2-4 lakh 25 50 4-6 lakh 12 24

6 lakh and above 8 16 Total 50 100

33

BI-VARIANT ANALYSIS

SATISFACTION LEVEL AND GENDER

Table 13

Figure 10

The above graph is interpreting it relationships between two variable gender and

satisfaction level. So, in average satisfactory level male are 17 and female are only 3 so

high level of difference in average satisfactory level between male and female. And in

dissatisfactory male are 2 and female are only 1 so very less difference in

dissatisfactory.so very less number of people are dissatisfied with the services.

0

2

4

6

8

10

12

14

16

18

Highly Satisfactory

Satisfactory averagely satisfactory

Dissatisfactory

male female

Highly

Satisfactory

Satisfactory Averagely

satisfactory

Dissatisfactory Total

Male 7 10 17 2 36 19.4% 27.8% 47.2% 5.6% 100.0%

Female 1 9 3 1 14 7.1% 64.3% 21.4% 7.1% 100.0%

Total 8 19 20 3 50

16.0% 38.0% 40.0% 6.0% 100.0%

34

GENDER AND LOAN AMOUNT

Table 12

Figure 11

Above graph is interpret that the relationship between loan amount and gender. 18

male and 6 female have took loan of Rs. 5-10 lakh. While 14 male and 7 female have

took loan of Rs. 1-5 lakh. And only 2 male has took loan of Rs. More than 10 lakah.so we

can say that more number of male take loan of rs.5-10 lakh.

0

2

4

6

8

10

12

14

16

18

less than 1 lakh 1-5 lakh 5-10 lakh more than 10 lakh

male female

LOAN

AMOUNT/GENDER

Male Female Total

Less than 1 lakh 2 1 3 66.7% 33.3% 100.0%

1-5 lakh 14 7 21 66.7% 33.3% 100.0%

5-10 lakh 18 6 24 75.0% 25.0% 100.0%

More than 10 lakh 2 0 2

100.0% 0.0% 100.0% TOTAL 36 14 50

72.0% 28.0% 100.0%

35

PROBLEM WHILE TAKING LOAN & OCCUPATION

Table 13

Figure 12

From the above graph interpret it relationship between occupation and facing problem while

taking loan. 16 salaried person facing problem of lack of knowledge. While 3 salaried person

facing problem procedural delay and non-cooperation. 9 self-employed people facing problem

of lack of knowledge and 4 self-employed people facing problem of procedural delay. So we can

say that salaried person face problem of lack of knowledge more than the professional person.

And only 4 self-employed people face the problem of procedural delay.

0

2

4

6

8

10

12

14

16

professional self-employed salaried other

lack of knowledge proceduraldelay and non-corporetion other

PROBLEMS Professional Self-

employed

Salaried Other TOTAL

Lack of knowledge 3 9 16 1 29

10.3% 31.0% 55.2% 3.4% 100.0%

Procedural delay and

non-corporation

4 4 3 2 13 30.8% 30.8% 23.1% 15.4% 100.0%

Other 1 0 6 1 8

12.5% 0.0% 75.0% 12.5% 100.0%

TOTAL 8 13 25 4 50 16.0% 26.0% 50.0% 8.0% 100.0%

36

INCOME LEVEL AND INTEREST RATE

Table 14

Below 2 lakh 2-4 lakh 4-6 lakh 6 lakh and

above

TOTAL

Fixed

rate

4 12 7 6 29

13.8% 41.4% 24.1% 20.7% 100.0% Floating

rate

1 13 4 1 19

5.3% 68.4% 21.1% 5.3% 100.0% Other 0 0 1 1 2

0.0% 0.0% 50.0% 50.0% 100.0%

TOTAL 5 25 12 8 50 10.0% 50.0% 24.0% 16.0% 100.0%

Figure 13

Above graph interpret it the relationship between income level and interest rate. 12 person

are pay fixed rate whose income is 2-4 lakh, while 13 people pay floating rate whose

income is 2-4 lakh.so there is little difference. Whose income above 6 lakh those people

preferred fixed rate.7 person pay fixed rate whose income is 4-6 lakh.

0

2

4

6

8

10

12

14

Below 2 lakh 2-4 lakh 4-6 lakh 6 lakh and above

Fixed rate Floating rate other

37

INCOME LEVEL AND LOAN AMOUNT

Table 15

Below 2 lakh 2-4

lakh

4-6 lakh 6 lakh

and

above

TOTAL

less than 1 lakh 1 1 1 0 3 33.3% 33.3% 33.3% 0.0% 100.0%

1-5 lakh 2 14 4 1 21 9.5% 66.7% 19.0% 4.8% 100.0%

5-10 lakh 2 9 7 6 24

8.3% 37.5% 29.2% 25.0% 100.0% more than 10 lakh 0 1 0 1 2

0.0% 50.0% 0.0% 50.0% 100.0% TOTAL 5 25 12 8 50

10.0% 50.0% 24.0% 16.0% 100.0%

Figure 14

Above graph interpret the relationship between loan amount and income level. 14 people

havetook loan of rs.1-5 lakh whose income is 2-4 lakh.

0

2

4

6

8

10

12

14

below 2 lakh 2-4 lakh 4-6 lakh 6 lakh and

above

less than 1 lakh 1-5 lakh 5-10 lakh more than 10 lakh

38

SATISFACTION LEVEL AND GENDER

H0: satisfaction level and gender are Independent.

H1: satisfaction level and gender are not Independent.

Level of signification is 5%.

Degree of freedom is (4-1) * (2-1) = 3

Table 16

Calculated2is6.2077

Tabulated 2is 7.815

Since calculated value is lower than the tabulated value so, null hypothesis is

accepted.so, we can conclude that gender and satisfaction level are independent.

Table 16.1

Observed

frequencies

Expected

frequncies

(O-E) (O-E)2 (O-E)2/E

7 5.76 1.24 1.5376 0.266944

10 13.68 -3.68 13.5424 0.989942

17 14.4 2.6 6.76 0.469444

2 2.16 -0.16 0.0256 0.011852

1 2.24 -1.24 1.5376 0.686429

9 5.32 3.68 13.5424 2.545564

3 5.6 -2.6 6.76 1.207143

1 0.84 0.16 0.0256 0.030476

TOATL 6.207794

Value Df

Pearson Chi-Square 6.208 3 Likelihood Ratio 6.253 3

Linear-by-Linear Association 0.157 1

39

GENDER AND LOAN AMOUNT

H0: gender and loan amount are Independent.

H1: Gender and loan amount are not Independent.

Level of signification is 5%.

Degree of freedom is (2-1) * (4-1) = 3

Table 17

Observed

frequncies

expected (O-E) (O-E)2 (O-E)2/E

2 2.16 -0.16 0.0256 0.0118

1 0.84 0.16 0.0256 0.0304

17 15.12 1.88 3.5344 0.2337

7 5.88 1.12 1.2544 0.2133

18 17.28 0.72 0.5184 0.0300

6 6.72 -0.72 0.5184 0.0771

2 1.44 0.56 0.3136 0.2177

0 0.56 -0.56 0.3136 0.5600

TOATL 1.3743

Calculated2is1.3743

Tabulated 2is 7.815

Since calculated value is lower than the tabulated value so, null hypothesis is

accepted. So, we can conclude that gender and loan amount is independent.

Table 17.1

Value df

Pearson Chi-Square 1.224 3

Likelihood Ratio 1.751 3 Linear-by-Linear Association 0.864 1

40

OCCUPATION AND PROBLEMS

H0: Occupation and problems are Independent.

H1: Occupation and problems are not Independent.

Level of signification is 5%.

Degree of freedom is (4-1) * (3-1) = 6

Table 18

Observed

Frequencies

Expected

Frequencies

(O-E) (O-E)2 (O-E)2/E

3 4.64 -1.64 2.6896 0.57965

9 7.54 1.46 2.1316 0.28270

16 14.5 1.5 2.2500 0.15517

1 2.32 -1.32 1.7424 0.75103

4 2.08 1.92 3.6864 1.77230

4 3.38 0.62 0.3844 0.11372

3 6.5 -3.5 12.25 1.88461

2 1.04 0.96 0.9216 0.88615

1 1.28 -0.28 0.0784 0.06125

0 2.08 -2.08 4.3264 2.0800

6 4 2 4 1

1 0.64 0.36 0.1296 0.2025

TOTAL 9.7691

Calculated2is9.7691

Tabulated 2is 12.592

Since calculated value is lower than the tabulated value so, null hypothesis is

accepted.so, we can conclude that occupation and problems are independent.

Table 18.1

Value df

Pearson Chi-Square 9.769 6

Likelihood Ratio 11.856 6 Linear-by-Linear Association 0.298 1

41

INCOME LEVEL AND INTEREST RATE

H0: Income level and interest rate are Independent.

H1: Income level and interest rate are not Independent.

Level of signification is 5%.

Degree of freedom is (4-1) * (3-1) = 6

Table 19

Calculated2is6.3523

Tabulated2is 12.592

Since calculated value is lower than the tabulated value so, null hypothesis is

accepted.so, we can conclude that gender and satisfaction level are independent.

Table 19.1

Observed Expected (O-E) (O-E)2 (O-E)2/E

4 2.9 1.1 1.21 0.4172

12 14.5 -2.5 6.25 0.4310

7 6.96 0.04 0.0016 0.0002

6 4.64 1.36 1.8496 0.3986

1 1.9 -0.9 0.81 0.4263

13 9.5 3.5 12.25 1.2894

4 4.56 -0.56 0.3136 0.0687

1 3.04 -2.04 4.1616 1.3689

0 0.2 -0.2 0.04 0.2000

0 1 -1 1 1

1 0.48 0.52 0.2704 0.5633

1 0.32 0.68 0.4624 1.4450

TOTAL 7.60896

Value Df Asymp. Sig. (2-

sided)

Pearson Chi-Square 7.609 6 0.268

Likelihood Ratio 8.542 6 0.201

Linear-by-Linear

Association

0.014 1 0.907

42

INCOME LEVEL AND LOAN AMOUNT

H0: Income Level and Loan Amount are Independent.

H1: Income Level and Loan Amount are not Independent.

Level of signification is 5%.

Degree of freedom is (4-1) * (4-1) = 9

Table 20

Observed

Frequencies

Expected

frequencies

(O-E) (O-E)2 (O-E)2/E

1 0.3 0.7 0.4900 1.6333

1 1.5 -0.5 0.2500 0.1666

1 0.72 0.28 0.0784 0.1088

0 0.48 -0.48 0.2304 0.4800

2 2.1 -0.1 0.0100 0.0047

14 10.5 3.5 12.250 1.1666

4 5.04 -1.04 1.0816 0.2146

1 3.36 -2.36 5.5696 1.6576

2 2.4 -0.4 0.1600 0.0666

9 12 -3 9 0.7500

7 5.76 1.24 1.5376 0.2669

6 3.84 2.16 4.6656 1.2150

0 0.2 -0.2 0.0400 0.2000

1 1 0 0 0

0 0.48 -0.48 0.2304 0.4800

1 0.32 0.68 0.4624 1.4450

TOTAL 9.8561

Calculated2is9.8561

Tabulated 2is 16.919

Since calculated value is lower than the tabulated value so, null hypothesis is

accepted.so, we can conclude that Income level And Loan Amount Are Independent.

Table 20.1

Value df

Pearson Chi-Square 9.856 9

Likelihood Ratio 10.298 9

Linear-by-Linear Association 5.116 1

43

CHEPTER 5

FINDINGS

44

FINDINGS

1. Majority of the people got loans from SBI and HDFC bank.

2. Most of the people are given important to loan tenure while choosing

loan and followed one is loan eligibility.

3. Most of the customers are facing problem of lack of knowledge because

of they are not aware about different type of facility.

4. Majority of the people pay fixed rate of interest.

5. Most of the people felt that the interest rates are somewhat high and majority of people are satisfied with the services.

6. From the research most of people are male who have taken loan.

7. Most of the people felt that HDFC provide good service compare to other banks.

45

CHEPTER 6

CONCLUSION

46

CONCLUSION

In our study we came to know that many people taken loan and most of

the people have taken loan from the SBI. Home loans have long period

when compare to other personal loans and other loans. So peoples are

confused to take a home loan. Even though the interest rates are high

peoples are willing to take a loan from SBI banks. For disbursement

process is also it will take long time so, many people face the problem of

procedural delay. Finally the whole research was carried out in a

systematic way to reach at exact results. The whole research and findings

were based on the objectives. However, the study had some limitations

also such as lack of time, lack of data, non-response, and reluctant

attitude and illiteracy of respondents, which posed problems in carrying

out the research. But proper attention was made to carry out research in

proper way and to make accurate conclusion for the home loan which

may beneficial for banks to enhance their customer base.

47

CHEPTER 7

REFERANCE

48

REFERENCE

WEBSITE:

www.shodhganga.com

www.starcum.com

www.thinkinvest.com

www.loansnews.com

www.scribed.com

REPORT:

Retail Banking – Emerging Issue in Home Loan” in the year 2005.

Performance of Housing Finance Companies” in the year 2005.

Housing credit situation in eighties “in the year 1984.

Housing Problem and Incompatibility Experience from a South Indian

State” in the year 2004.

Problem of the national housing policy” in year 1980.

49

CHEPTER 7

ANNEXURE

50

QUESTIONNAIRE

1. From which Bank have you taken loan?

1) ICICI 2) HDFC 3) UTI

4) Tata capital 5) IDBI 6) Bank of Baroda

7) SBI 8) Axis Bank 9)Kotak

10) PNB home fin. 11) Others

2. What are the criteria consider while taking a loan? (Give ranking)

Faster Processing Interest Rates Brand image of the Bank

Margin Amount payback period Schemes

Loan tenure Loan eligibility others

3. Which type of interest rate paid by you?

1) Fixed rate 2) Floating rate 3) Other

4. Are you satisfied with the services provided?

1) Highly Satisfactory 2) Satisfactory

3) Averagely Satisfactory 4) Dissatisfactory

5) Highly Dissatisfactory

5. How much loan amount you took?

1) Less than 1 lakh 2) 1-5 lakh

3) 5-10 lakh 4) More than 10 lakh

6. What problems did you face while getting home loans?

1) Lack of knowledge 2) Procedural delays and non-cooperation

3) Any other (please specify) ………………

51

PERSONAL DETAILS

Name: …………………………………………………………………………………...

Age: …………………………………..............................................................................

Gender: …………………………………………………………………………………

Occupation:

1) Professional 2) Self-employed 3) Salaried 4) Other

Which income group do you belong? (Per annum)

1) Below 2 lakh 2) 2-4 lakh

3) 4-6 lakhs 4) 6 lakh and above