hms group acquisition of kazankompressormash...

TRANSCRIPT

HMS Group Acquisition of KazanKompressorMash (KKM)

Investor presentation

12 July 2012

2

Company description

KazanKomressorMash (KKM) at a glance

3

…integrated with leading R&D centre

Modern production facility…

Located in Kazan, Russia (~ 800 km from Moscow)

Overall area 420 ‘000 m2

Production floor 127 ‘000 m2

Developed infrastructure near railway

Dense in & outbound roads network

2300 employees

… focused on a gas stream-control products and technologies…

Centrifugal compressors

Screw compressors

Refrigeration and cooling units (centrifugal compressor-based)

Couplings, gearboxes, multipliers

310 specialists, 3 specialists with doctor degrees, 10 specialists with PhD

35 testing units and 132 patents

One of the largest applied centre for compressor technology in Russia and the CIS

General service (Air)

Refrigeration

Oil and gas production

and transportation

Gas processing

4

Compressor market : applications

• Industrial manufacturing • Construction • Metals & mining • Service (car re- pair, cargo delivery etc) • Airports, sea ports

• Petrochemistry, refining •LNG production • Warehouse terminals • Fishing and refrigerated fleet • Food

• Gas transport • Gas gathering at gas fields • Gas pumping in seams • Gas pumping in underground gas storage

• Oil refining and gas processing • Chemistry and petrochemistry • Power generation • Metallurgy and mineral dressing, coal mining • Cellulose • Food

Compressors by end-user applications

KKM at a glance

5

Product offering for associated gas, natural gas and basic industries in Russia and CIS

Russia; 92%

CIS; 8%

Revenue by end-markets (2011): Revenue by geography (2011):

Steady revenue growth with moderate debt, mln Rub Backlog structure, mln Rub

Rub

2,236

million

As of June 01, 2012

Rub

2,801

million

Rub

2,801

million

6

Market environment and prospects

Industry Project Total CAPEX, bln USD

Oil industry Vancor (Rosneft) Talakan and Alinsk (Surgutneftegaz) Samotlor (TNK-BP) Sakhalin Island (Rosneft, Gazprom)

12.3 (2017) 7.7 (2014) 5.5 (2020) 210 (2030)

Gas industry: Liquefied Natural Gas (LNG)

Kharasavey LNG Plant (Gazprom) Yamal LNG Plant (Novatek) Shtokman LNG Plant (Shtokman Development AG) Pechora LNG Plant (Surgutneftegas):

25.7 17.2 (2018) 20.7 (2017-2018) 4.3

Gas Industry: Gas Exploration and Extraction

Kirinsky block Sakhalin-3 (Gazprom); Gydansky Peninsula (Lukoil); Karsky Sea Shelf (Gazprom); Yamal Peninsula (Gazprom); Yamal (Rospan)

51 (2020); 41.2 (2020); 20.8 (2020) 79.4 (2020) 1.0 billion

Gas Industry: Transportation

Gaz pipeline Bovanenkovo - Ukhta: Gas pipeline Sakhalin – Khabarovsk – Vladivostok Ukhta - Torzhok SPTO Torzhok Eastern Siberia and Far East Gas Pipeline System Development (Phase II):

33 (2015) 15.6 (2020) 7.8 (2013) 1.0 (2015) 15.0 (2020)

Oil refining and pertochemicals

Ust-Luga Refining Plant Ltd (operator company of the refinery) Nakhodka oil refinery (Rosneft, construction) Kirishi refinery (Surgutneftegaz, upgrading) Murmansk refinery (Gazpromneft construction and upgrading)

11.4 (2016) 9.0 (2017) 6.6 (2020) 8.3

Market size by end-markets, mln USD

7

Market outlook

Refrigeration 2%

General service (air) 13%

Oil & Gas production

and transportat

ion, 73%

Gas processing

12%

USD

2,074

million

Market size in 2010 according to Frost and Sullivan report

Russian compressor market growth, mln USD

Source: Frost and Sullivan research

Selected projects to drive industry growth, %

5673

1847 1781

2074

2505

Source: Frost and Sullivan research, CAGR 2011-2016:

17.8%

8

End-markets and competition

Iskra Turbogaz 33%

KMPO 15% Sumy Frunze

NPO 13%

Saturn 10%

KKM 7%

Iskra Avigaz 5%

Others 17%

Gea Grasso 33%

KKM 10% Johnson

Controls 21%

Others 12%

Bitzer 13%

MYCOM 11%

Top-10 selected market share, % (2010)

O&G production and transportation:

Refrigeration:

According to Frost and Sullivan research

Revenue breakdown by end-markets (2011):

Blue-chip customer base with good prospects for sales growth

Oil

an

d g

as

O

the

r in

du

str

ies

Top existing customers Potential sales expansion

Rub

2,801

million

Strong gas market

prospects

Total CAPEX of around USD 200 bn in 2012-2016 Strategic importance of Russian gas for domestic and overseas markets Further deregulation of the market, development of independent gas producers

and growing activity of VIOC in gas extraction along with new project initiatives in existing brown field installations

Compressors –

core and mission

critical equipment

Compressors – main equipment widely used across all technological processes in oil and gas industry – production, transportation, processing and technologies for liquefied gas production

Sound synergies

and integration

simplicity

Compressors are technologically close to pumps: Similar production technology (casting, mechanical processing) Same raw materials and components(bearings, electromotors, shafts etc)

Equal client base and sales channels - VIOCs are the largest customers of pumps and compressors with unified procurement systems

Rationale for HMS entrance to the gas equipment market

9

Current HMS

expertise in the

gas projects

HMS is currently a contractor for Gazprom and Novatek (around 5% of revenue in 2010-2011) and keen to further expand cooperation

HMS entrance to the compressor market through the acquisition will allow to gain 7% market share

10

Transaction rationale

Transaction rationale

1. Access to the new adjacent markets thanks to

combined offering

3. Strengthening of presence in the core markets

2. Attractive compressor market fundamentals

* - According to Frost and Sullivan Research

Strong and renowned brand of KKM will enable entering the market of compressors for oil and gas production and transportation with 7% market share

HMS footprint and engineering capabilities will be deployed to leverage sales of compressors

Combined offering driven by compressors sales will strengthen HMS presence in the oil upstream, gas processing, metals and mining and general chemistry markets

The total Russian compressor market was valued at USD 2.1 billion in 2010. The market to grow at a CAGR of 17.8% over the forecast period (2011-2016)*

The largest and the most profitable segment of the compressor market is oil and gas production and transportation, which accounted for 76% of the total market revenues. Gas processing applications is expected to offer high growth opportunities in the future

Moderate competition due to limited number of local players, high entry barriers in the KKM’s core markets due to advanced technical specialization

Large customer base intersection Broadening the product offering of HMS for oil and gas

companies will give us new competitive advantages in oil and gas industry

Centrifugal compressor

Screw compressor

Refrigerating unit

11

Centrifugal pump

Twin screw pumps

Reactor cooling pump

12

Combined product offering will cover the whole technological chain in the main target industries

Production

Transportation

Processing

Production

Transportation

Processing

Gas-based chemistry

Petrochemistry

General chemical applications

KKM coverage

HMS coverage

Natural gas production and transportation

Associated gas production

Chemicals and petrochemicals

Visible synergies and low integration costs

13

1. Procurement

Consolidation of procurements systems leads to cost saving for maintenance supply due to similar base of key suppliers owing to the same raw materials (ferrous and non-ferrous metals) and spare parts (bearings and electric motors)

2. Production

Production cooperation and specialization in production of major units and components at those operating facilities with higher efficiency (more productive utilization of technological capacity)

3. Sales

4. Service

Growth of compressor sales to VOIC owing to HMS’ strong established relationships with most of the market players

Growth of HMS products sales (pumps and oil and gas equipment) to gas producers, gas processing plants, petro- and gas chemical companies owing to relationships with KKM’s traditional customer base

Growth thanks to integrated solutions and combined offering

Increase in efficiency of service network due to consolidation pumps and compressors service platforms for gas, oil, petrochemical and gas chemical industries

Rotary (Screw) compressor

Centrifugal compressor

Centrifugal pump

5. Low integration costs

Production, procurement and research & design processes are similar to those HMS implemented

Screw pump

14

Business model

15

Acquisition will provide a more diversified industry exposure

HMS and KKM, pro forma

Currently KKM has a limited presence in the market of natural gas, primarily focusing on business development with VOICs.

HMS sets a target to penetrate to the natural gas market with mission-critical core compressor technology and expand current HMS presence in the industry

Offering of integrated solutions and project management capabilities will allow to shift KKM strategy from bare compressors sale to technologically demanding integrated projects

Oil upstream,

45.3%

Oil midstream,

30.2%

Water, 8.4%

Oil Downstream, 3.6%

Thermal power, 2.2%

Metals and mining, 1.0%

Nuclear power, 0.4%

Gas, 5.0% Other, 3.9%

HMS, pre-acquisition, 2011 KKM, pre-acquisition, 2011

Gas segment – the most promising segment given

special focus of HMS and strong growth potential

16

Well-aligned with HMS strategy: focus on integrated compressor-based solutions

Depending on end-user requirements, the level of complexity can vary from bare shaft compressors or delivery to complete integrated solution with commissioning at the customer’s site. Having relevant competence, expertise and equipment production facilities, HMS is well positioned to deliver

integrated solutions to existing customer base (VIOC) and main gas producers:

Bare shaft compressor

Integrated solution

Key advantages

Size Small-to-medium

Medium and large-scale

Successful implementation of large-scale integrated projects

R&D contribution

Middle High KKM has very close ties and deep integration with the leading R&D centre focused on the compressor-based solutions

Aftermarket demand

Average High Strong position for aftermarket sales

EBITDA margin

7-12% 24-26%

Share of compressors in total revenue

100% 15-40%

Key points of concept: -Value of one gas pumping station (integrated solution) for the trunk gas pipeline is similar to current annual revenue of KKM (around Rub 3bn) - There is no “one-stop shop” providers of integrated solutions in Russia with experience similar to HMS (ESPO-1, ESPO-2) - If HMS succeed, revenue of KKM can double based on 1 successful contract for 1 gas pumping station

4

1 - intake tank with air filter 2 - oil cooler assembly 3 - air gearing 4 - exhaust arrangement

1

2

3

5

6

5 - compressor 6 - oil tank 7 - power turbine 8 - bed frame

8

7

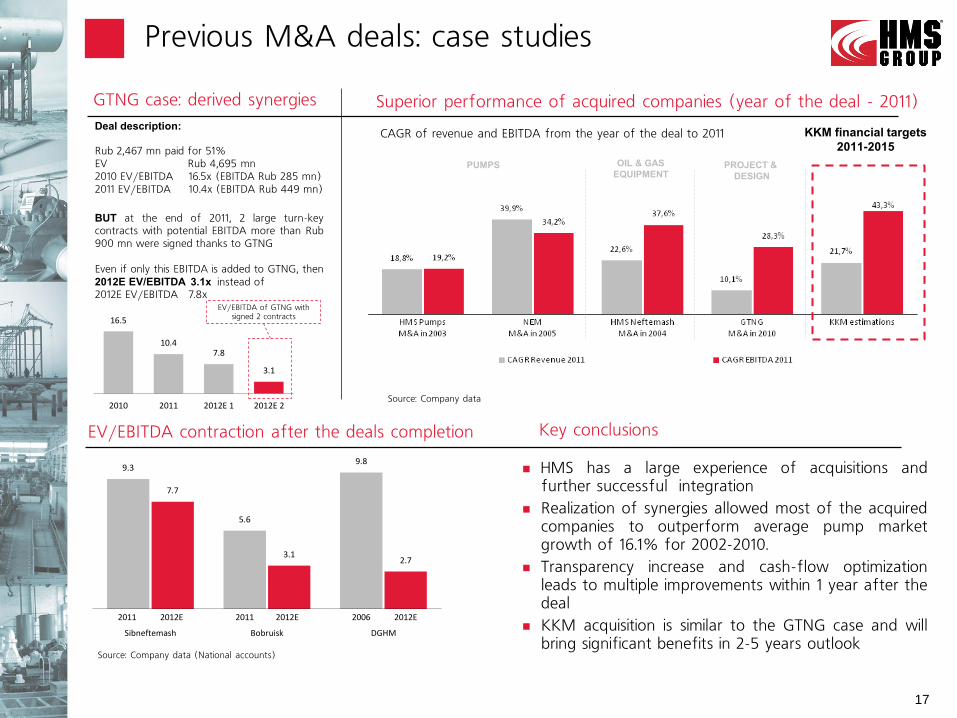

16.5

10.47.8

3.1

2010 2011 2012E 1 2012E 2

9.3

5.6

9.8

7.7

3.12.7

Sibneftemash Bobruisk DGHM

EV/EBITDA contraction after the deals completion

GTNG case: derived synergies

Previous M&A deals: case studies

17

Source: Company data (National accounts)

HMS has a large experience of acquisitions and further successful integration

Realization of synergies allowed most of the acquired companies to outperform average pump market growth of 16.1% for 2002-2010.

Transparency increase and cash-flow optimization leads to multiple improvements within 1 year after the deal

KKM acquisition is similar to the GTNG case and will bring significant benefits in 2-5 years outlook

Source: Company data

Superior performance of acquired companies (year of the deal - 2011)

PUMPS OIL & GAS

EQUIPMENT PROJECT &

DESIGN

Deal description: Rub 2,467 mn paid for 51% EV Rub 4,695 mn 2010 EV/EBITDA 16.5x (EBITDA Rub 285 mn) 2011 EV/EBITDA 10.4x (EBITDA Rub 449 mn)

BUT at the end of 2011, 2 large turn-key contracts with potential EBITDA more than Rub 900 mn were signed thanks to GTNG Even if only this EBITDA is added to GTNG, then 2012E EV/EBITDA 3.1x instead of 2012E EV/EBITDA 7.8x

2011 2012E 2012E 2012E 2011 2006

EV/EBITDA of GTNG with signed 2 contracts

Key conclusions

KKM financial targets

2011-2015 CAGR of revenue and EBITDA from the year of the deal to 2011

Deal’s structure

HMS will hold the control of 77.8% of voting shares (74.47% of KKM’s share capital)

The offer value is Rub 5 524 mn

Financing

3Y bonds of Rub 3 bn issued in Feb 2012 3Y Rub 1.2 bn and short-term Rub 1.3 bn debt facility issued by Sberbank HMS balance sheet remained strong after the deal completion

Deal‘s description

18

Financial impact in

2012

Consolidated revenue is projected to be within Rub 31.5-35.5 bn range Consolidated EBITDA of RUB 5.7-6.3 bn Net Debt/EBITDA of approx. 2.0 (within internal and external covenants)

Deal’s schedule

Federal Antimonopoly service approval received on 6 July 2012 The deal has been closed on 11 July 2012 KKM integration into HMS Group: July-June 2013

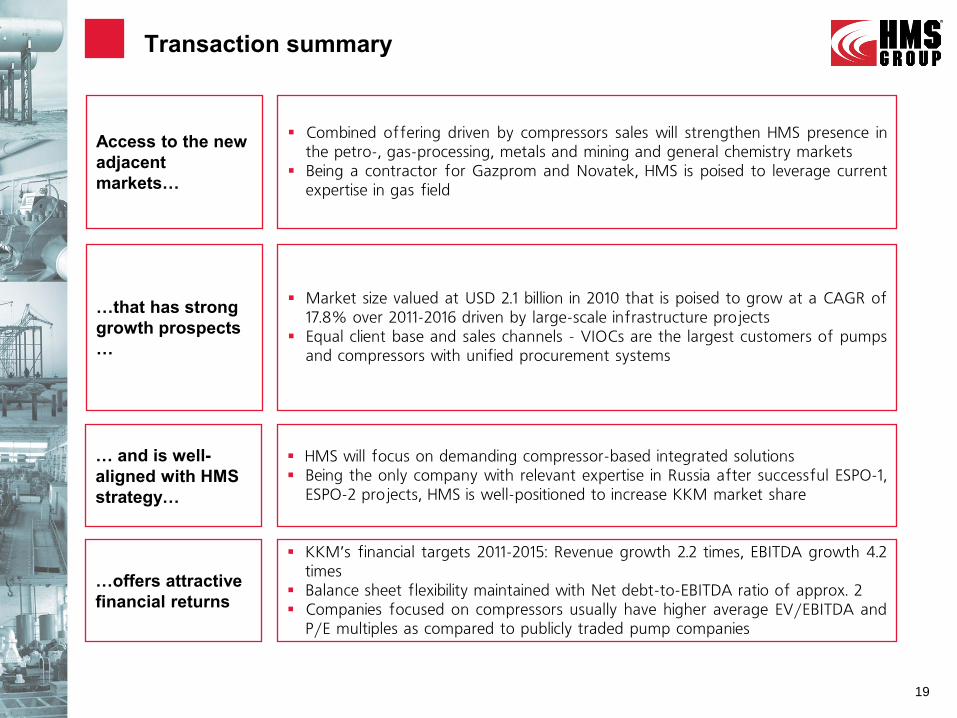

…offers attractive

financial returns

KKM’s financial targets 2011-2015: Revenue growth 2.2 times, EBITDA growth 4.2 times

Balance sheet flexibility maintained with Net debt-to-EBITDA ratio of approx. 2 Companies focused on compressors usually have higher average EV/EBITDA and

P/E multiples as compared to publicly traded pump companies

Access to the new

adjacent

markets…

Combined offering driven by compressors sales will strengthen HMS presence in the petro-, gas-processing, metals and mining and general chemistry markets

Being a contractor for Gazprom and Novatek, HMS is poised to leverage current expertise in gas field

…that has strong

growth prospects

…

Market size valued at USD 2.1 billion in 2010 that is poised to grow at a CAGR of 17.8% over 2011-2016 driven by large-scale infrastructure projects

Equal client base and sales channels - VIOCs are the largest customers of pumps and compressors with unified procurement systems

Transaction summary

19

… and is well-

aligned with HMS

strategy…

HMS will focus on demanding compressor-based integrated solutions Being the only company with relevant expertise in Russia after successful ESPO-1,

ESPO-2 projects, HMS is well-positioned to increase KKM market share