high performance microfinance sam 2015 - plenary session day 2

TRANSCRIPT

High Performance Microfinance

Michael Mithika, Course Director

8th September, 2015

Let’s take a look back on microfinance…

…what do you see?

3 years ago…. 5 years ago… 10 years ago…

…what do you see

In your country and organisation in terms of growth, number of institutions?

What about impact?

more of the same?

a bit of difference?

clients or institutions?

Too much of the same?

…you need to build your ���competitive edge

…and learn from some of the best!

Accenture Institute of High Performance

…from a 3 year study of 6,000 companies

Successful enduring leaders have some things in common.

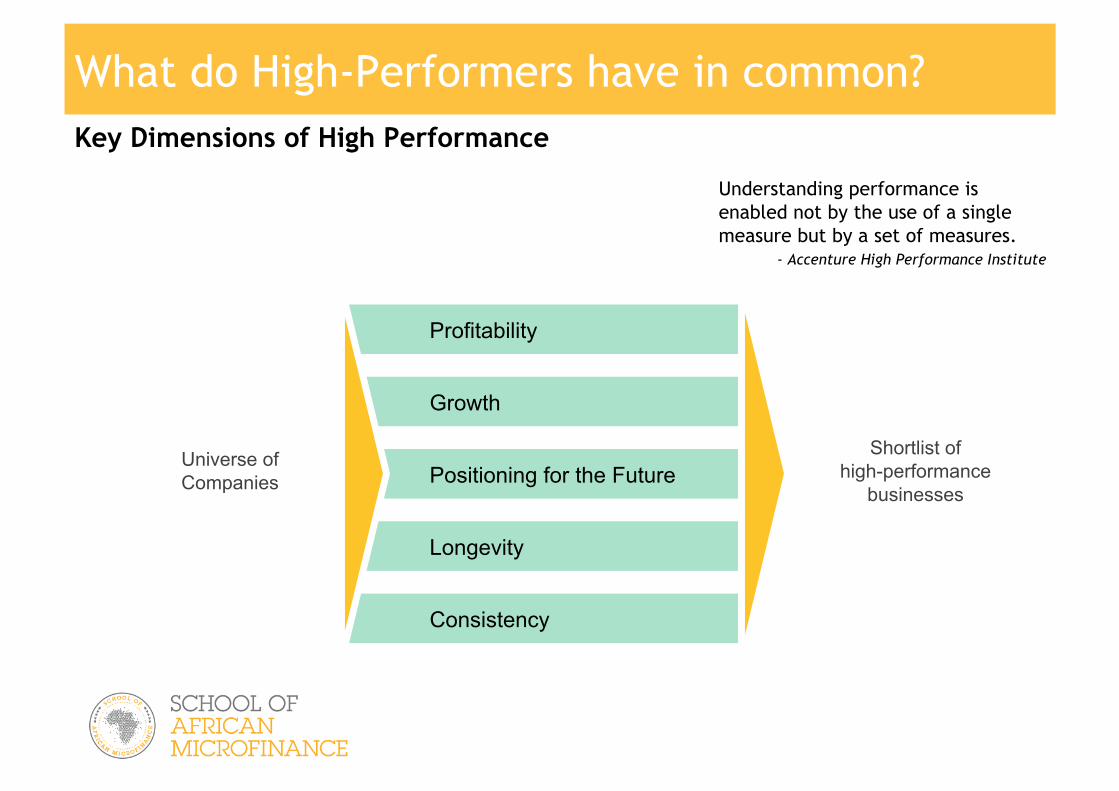

What do High-Performers have in common?

Understanding performance is enabled not by the use of a single measure but by a set of measures.

- Accenture High Performance Institute

Profitability

Growth

Positioning for the Future

Longevity

Consistency

Universe of Companies

Shortlist of high-performance

businesses

Key Dimensions of High Performance

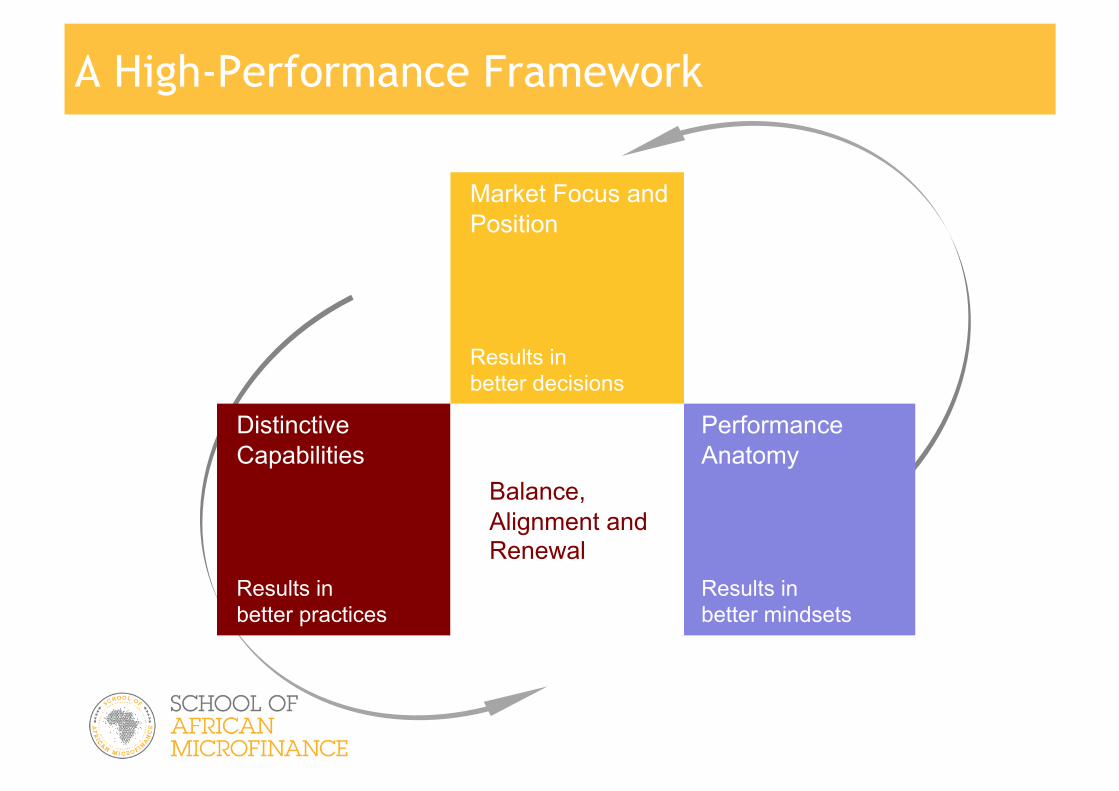

A High-Performance Framework

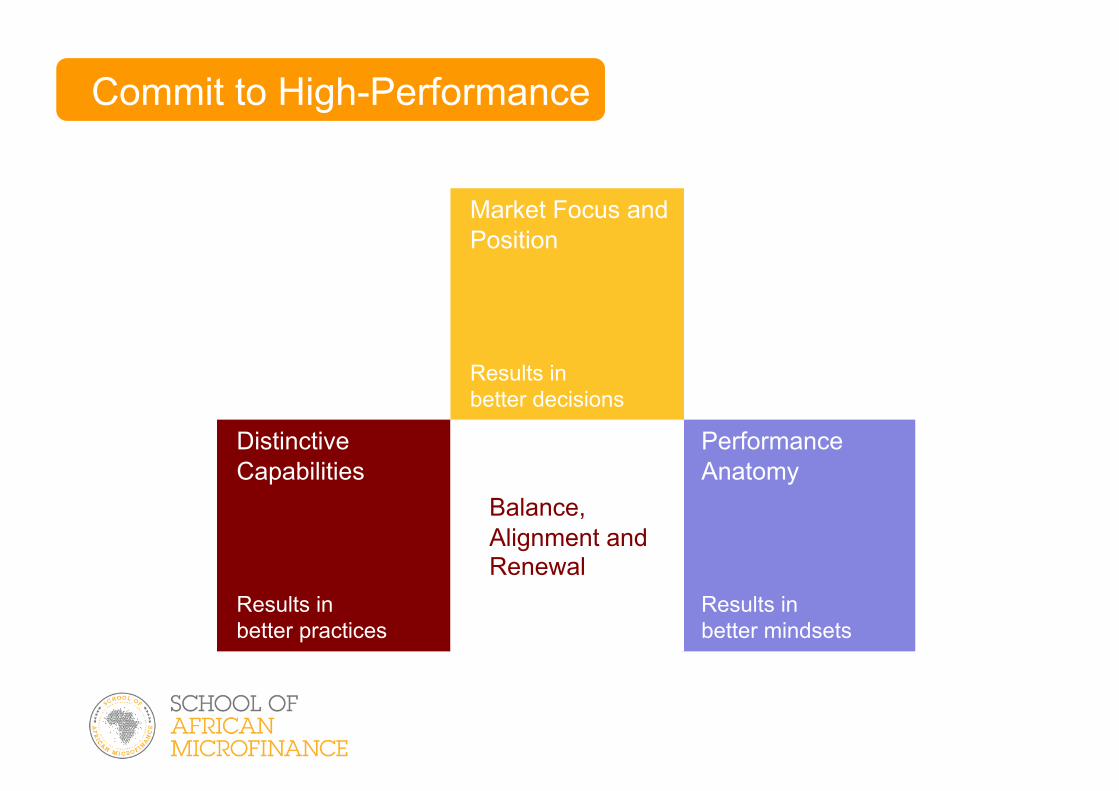

Market Focus and Position

Results in better decisions

Distinctive Capabilities

Results in better practices

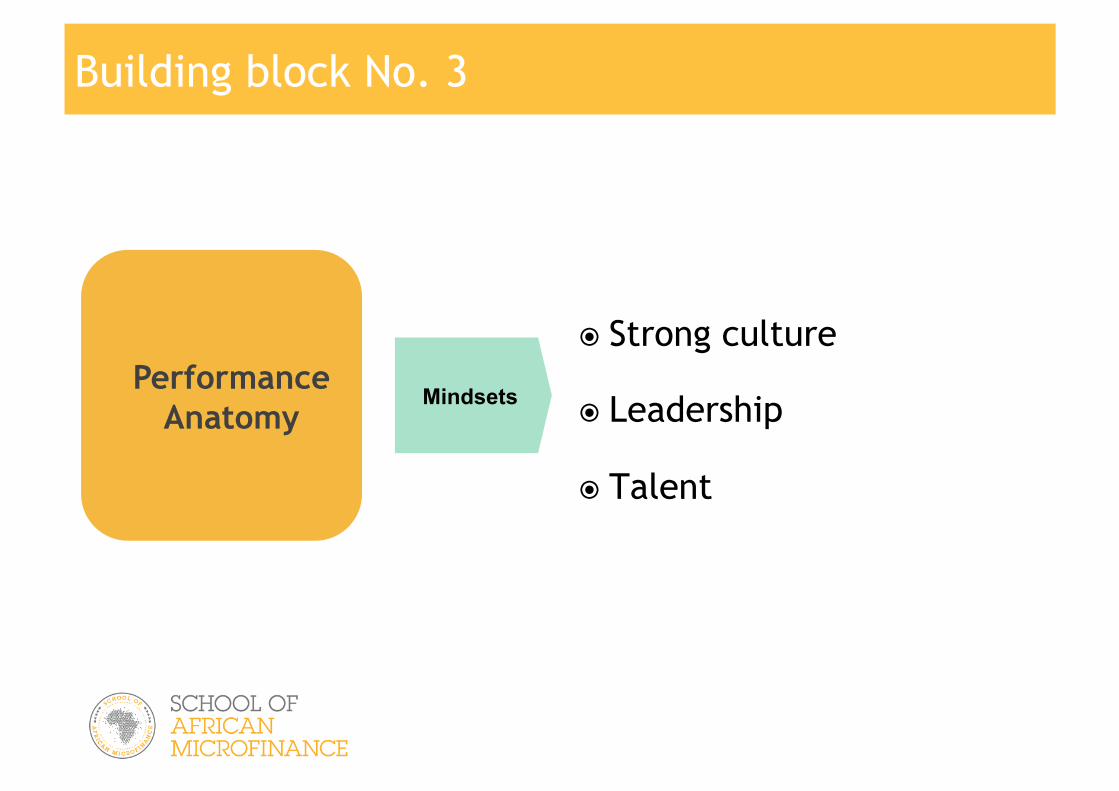

Performance Anatomy

Results in better mindsets

Balance, Alignment and Renewal

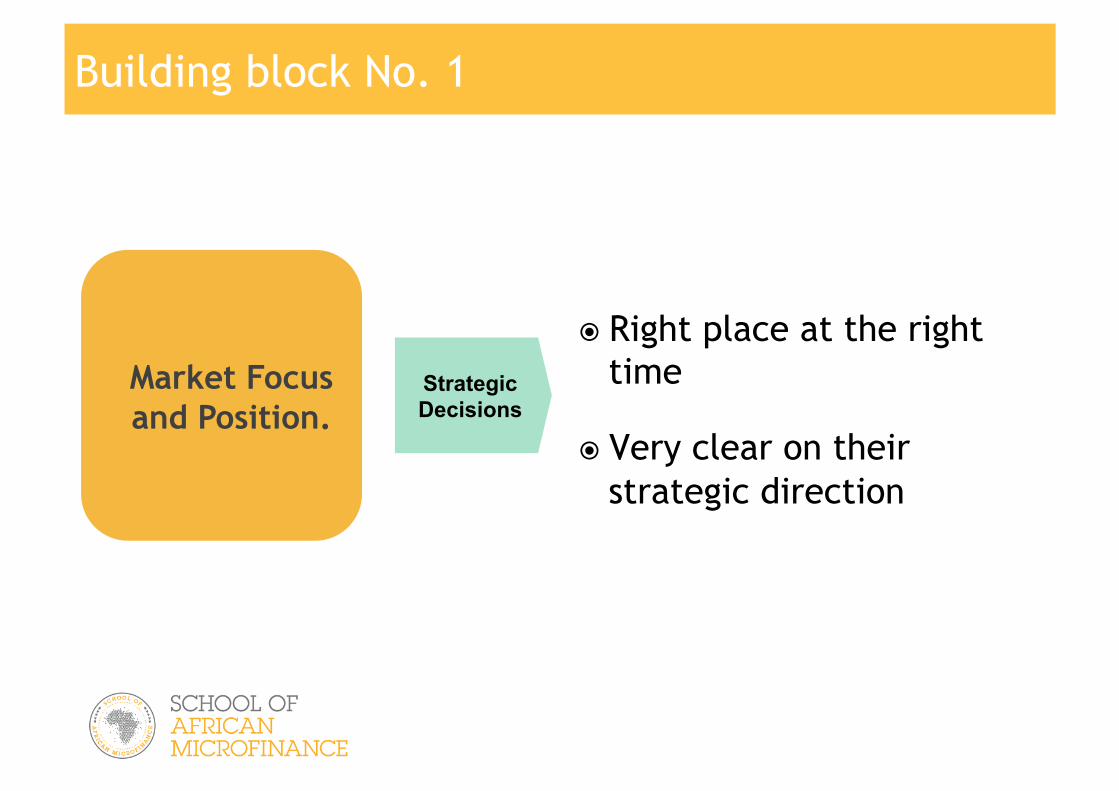

Building block No. 1

! Right place at the right time

! Very clear on their strategic direction

Strategic Decisions

Market Focus and Position.

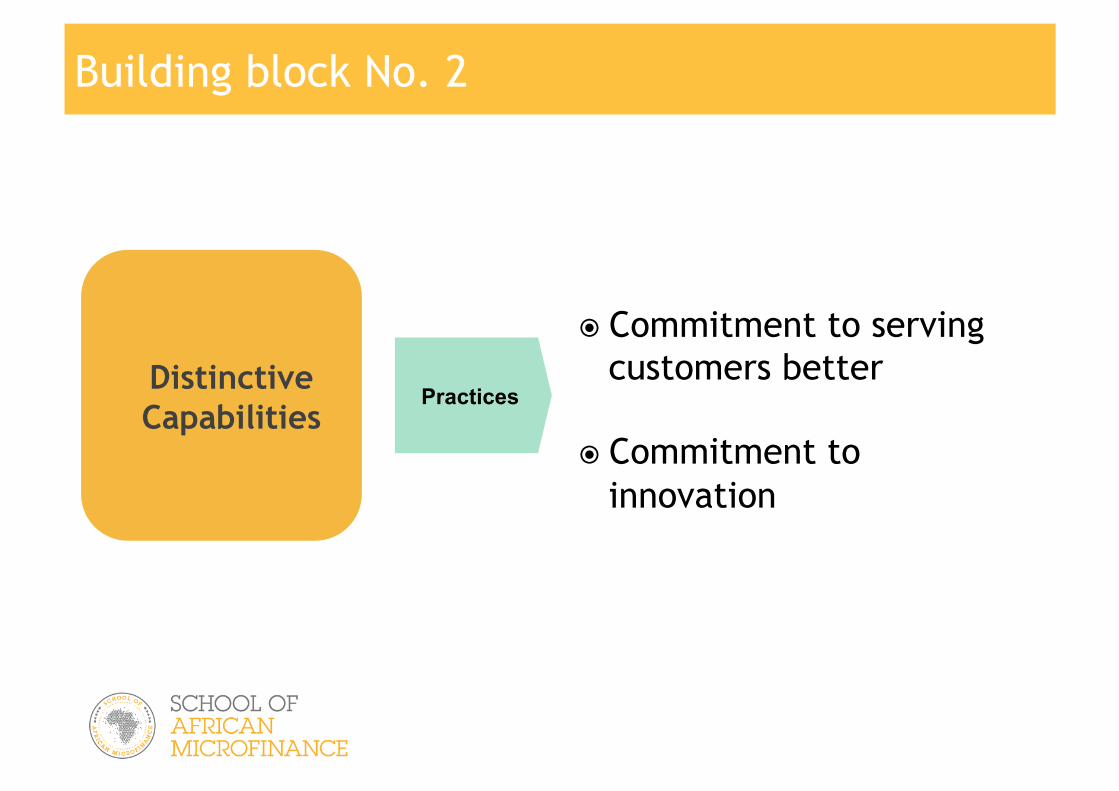

Building block No. 2

! Commitment to serving customers better

! Commitment to innovation

Practices Distinctive Capabilities

Building block No. 3

! Strong culture

! Leadership

! Talent

Mindsets Performance

Anatomy

A Journey we must travel…

Vikram Akula

and the story of

How one man responded…

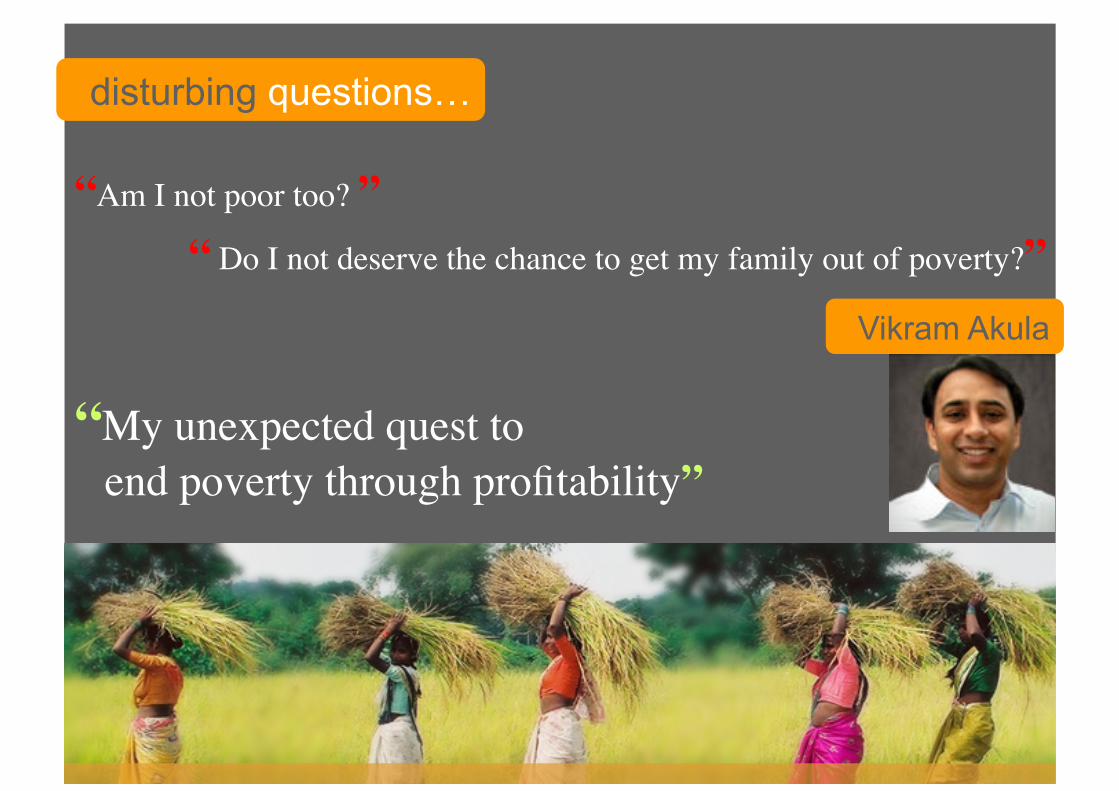

“Am I not poor too? ”“ Do I not deserve the chance to get my family out of poverty?”

“My unexpected quest to ���end poverty through profitability”

disturbing questions…

Vikram Akula

…the result…

…the resolve to empower the poor

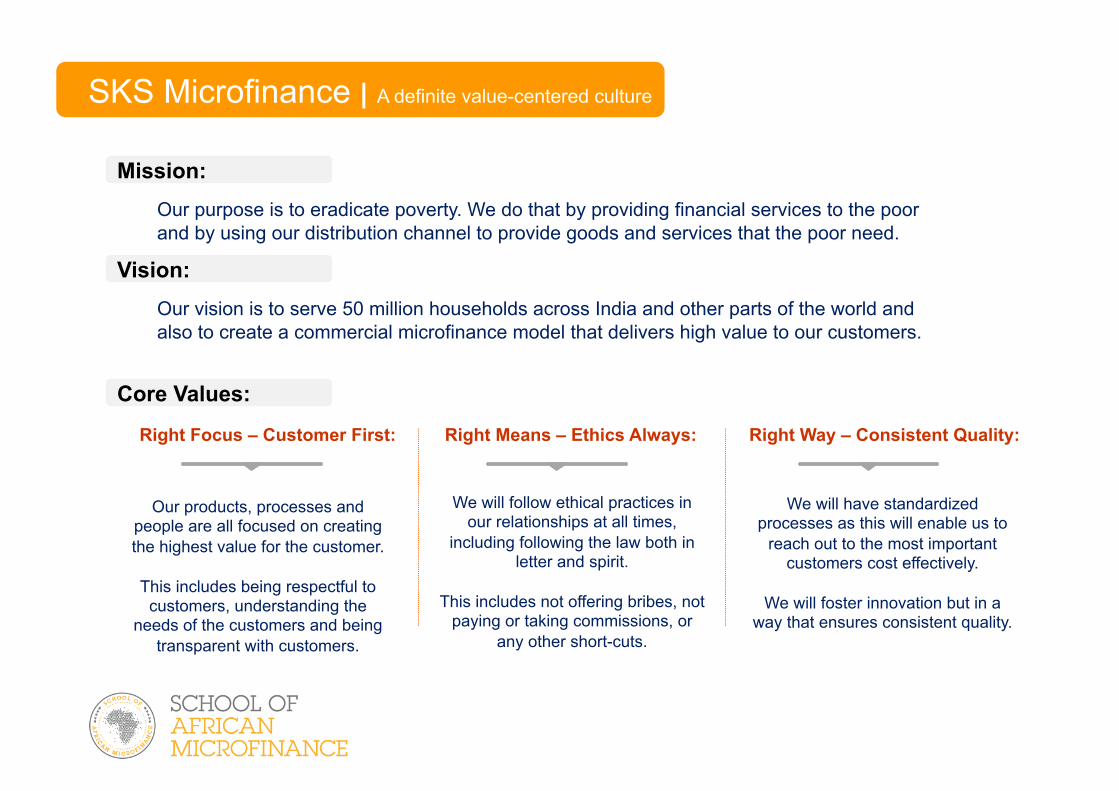

SKS Microfinance | A definite value-centered culture

Mission:

Vision:

Core Values:

Our purpose is to eradicate poverty. We do that by providing financial services to the poor and by using our distribution channel to provide goods and services that the poor need.

Our vision is to serve 50 million households across India and other parts of the world and also to create a commercial microfinance model that delivers high value to our customers.

We will follow ethical practices in our relationships at all times,

including following the law both in letter and spirit.

This includes not offering bribes, not paying or taking commissions, or

any other short-cuts.

Right Means – Ethics Always:

We will have standardized processes as this will enable us to

reach out to the most important customers cost effectively.

We will foster innovation but in a way that ensures consistent quality.

Right Way – Consistent Quality:

Our products, processes and people are all focused on creating the highest value for the customer.

This includes being respectful to customers, understanding the

needs of the customers and being transparent with customers.

Right Focus – Customer First:

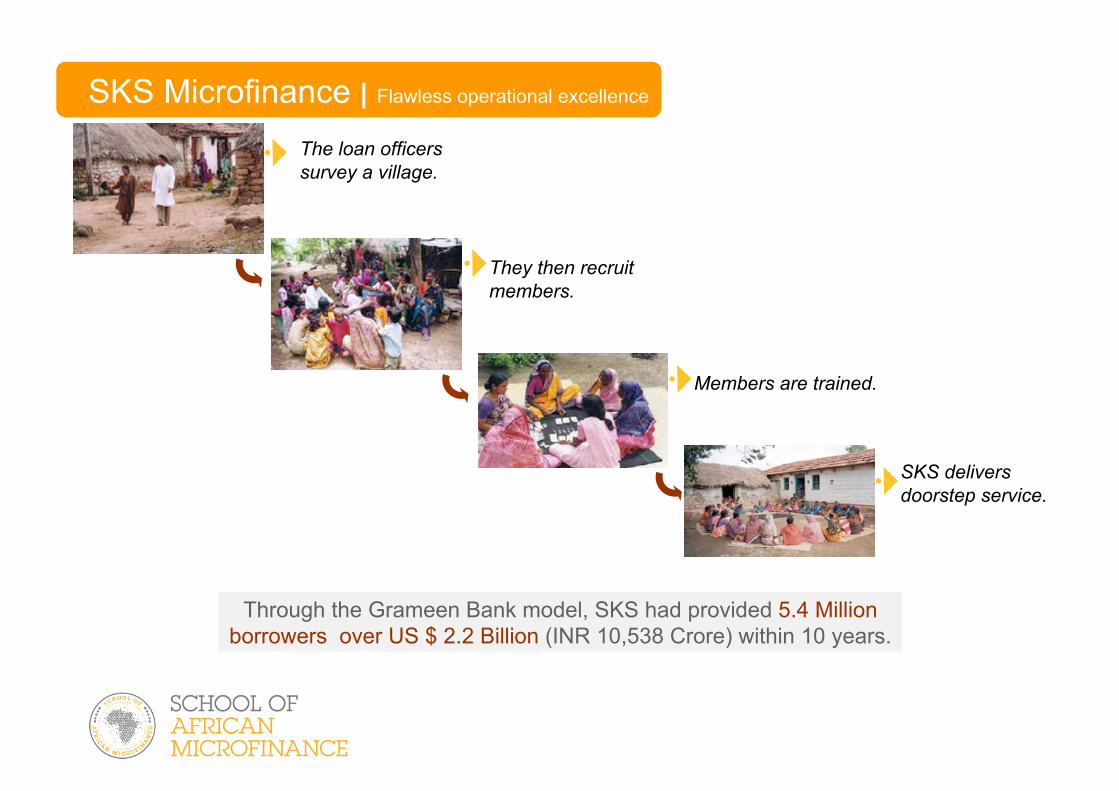

The loan officers survey a village.

They then recruit members.

SKS delivers doorstep service.

Members are trained.

Through the Grameen Bank model, SKS had provided 5.4 Million borrowers over US $ 2.2 Billion (INR 10,538 Crore) within 10 years.

SKS Microfinance | Flawless operational excellence

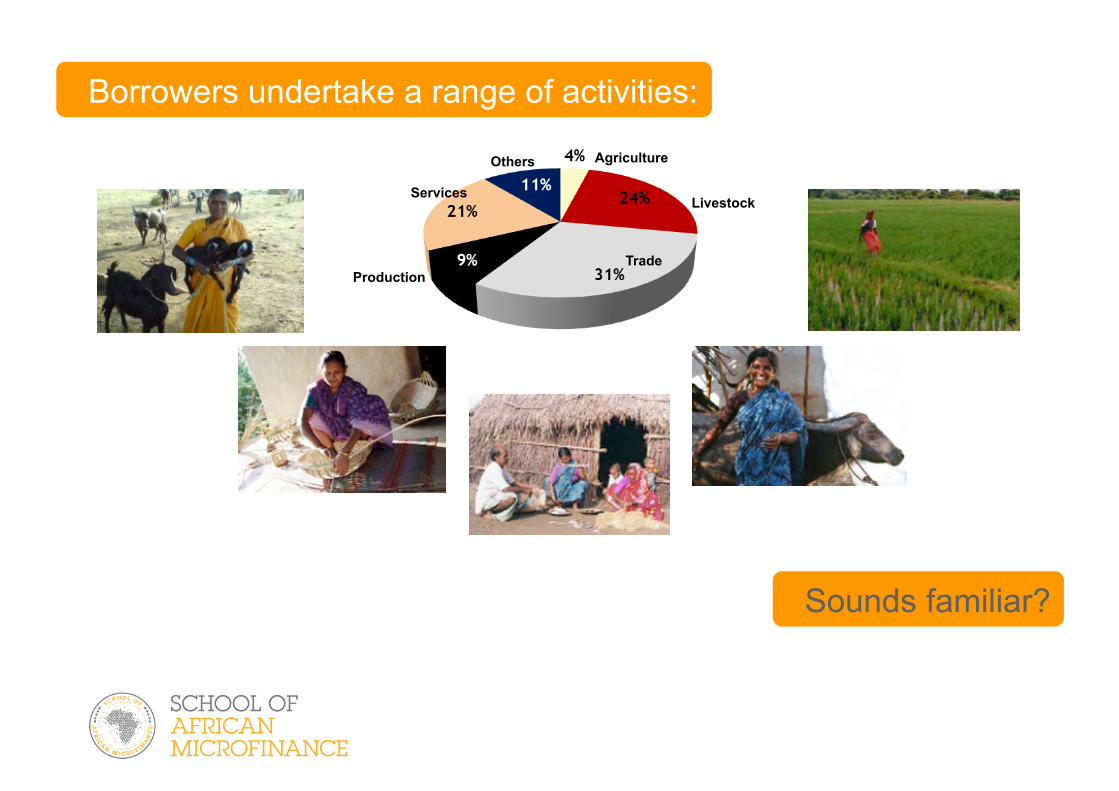

Borrowers undertake a range of activities:

Others Agriculture

Livestock

Trade

Services

Production

Sounds familiar?

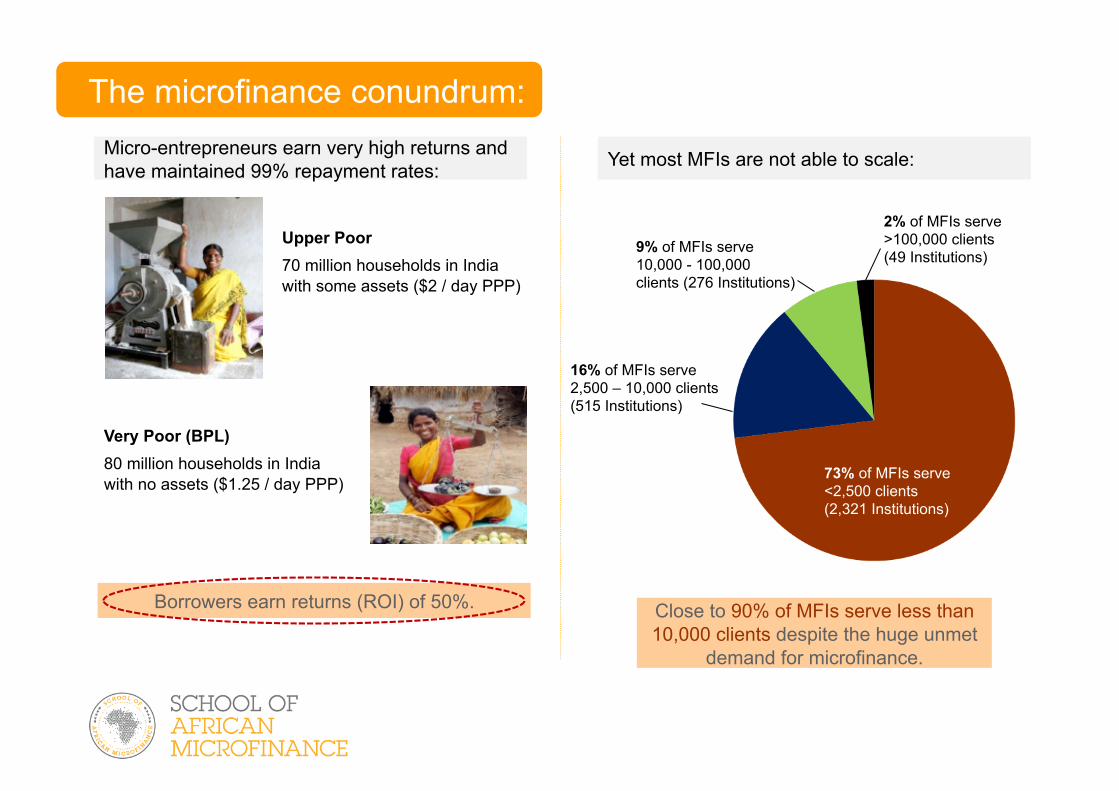

The microfinance conundrum: Micro-entrepreneurs earn very high returns and have maintained 99% repayment rates: Yet most MFIs are not able to scale:

Borrowers earn returns (ROI) of 50%.

Upper Poor 70 million households in India with some assets ($2 / day PPP)

Very Poor (BPL) 80 million households in India with no assets ($1.25 / day PPP)

2% of MFIs serve >100,000 clients (49 Institutions)

9% of MFIs serve 10,000 - 100,000 clients (276 Institutions)

16% of MFIs serve 2,500 – 10,000 clients (515 Institutions)

73% of MFIs serve <2,500 clients (2,321 Institutions)

Close to 90% of MFIs serve less than 10,000 clients despite the huge unmet

demand for microfinance.

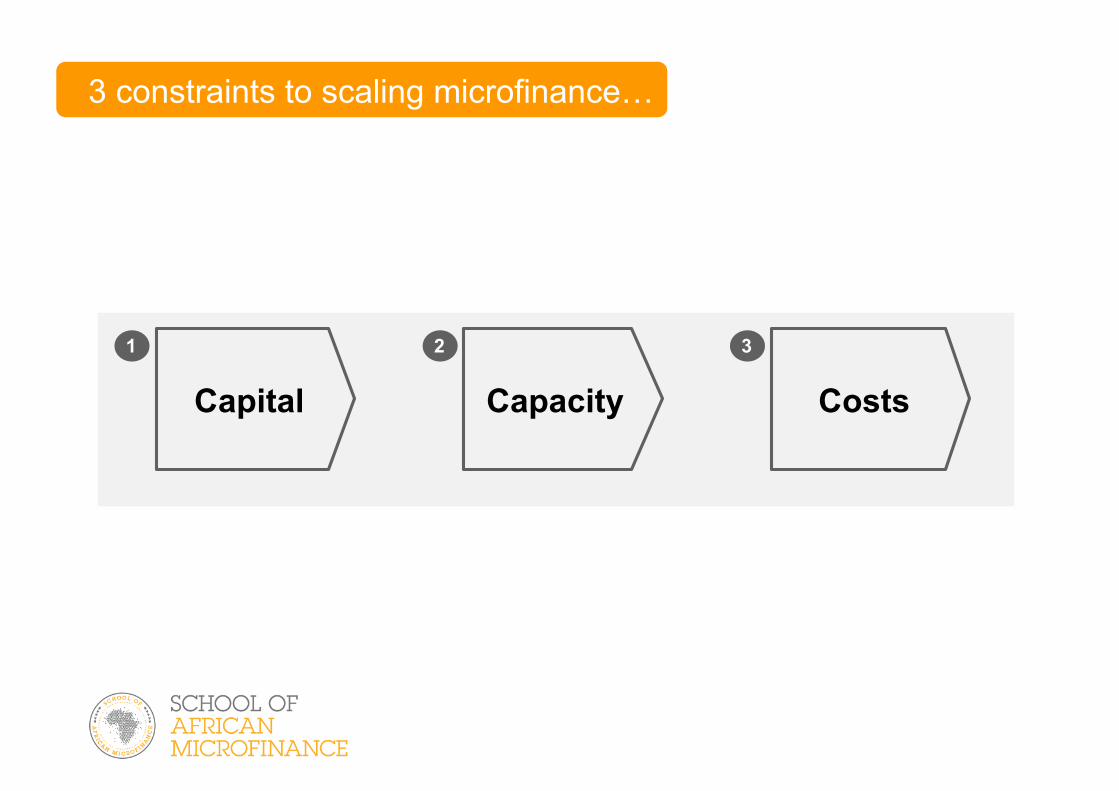

3 constraints to scaling microfinance…

1

Capital

2

Capacity

3

Costs

…and the SKS Solution

1 Capital

Profit model to access commercial capital.

Capacity 2

Scalable processes from the business world.

Costs 3

Technology to automate / lower transaction costs.

1. Profit model to access commercial capital

SKS Members: Indian Equity: Foreign Equity:

$169 Mn (INR 786 Crore) raised in equity:

Loans worth $1 Bn (INR 5,167 Crore) raised in 06-09; and $809 Mn (INR 3,762 Crore) in 08-09 alone:

PSU Banks: Private Banks: MNC Banks:

Capital

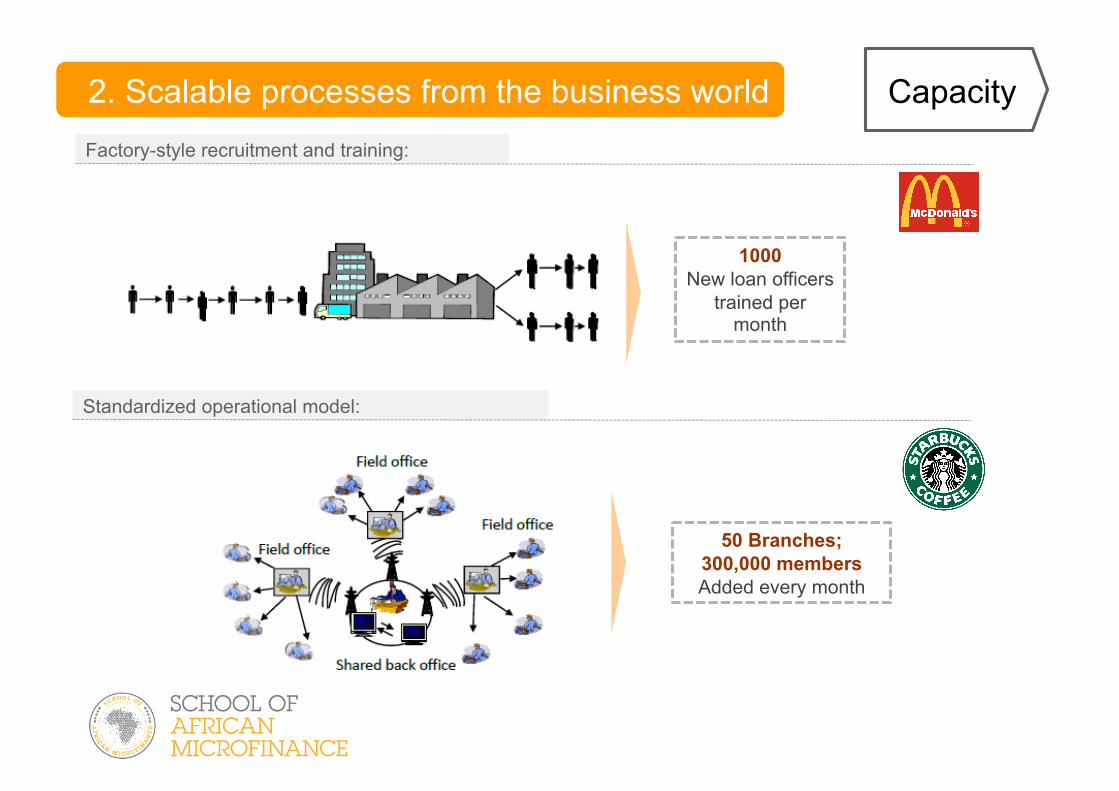

2. Scalable processes from the business world

Standardized operational model:

Factory-style recruitment and training:

1000 New loan officers

trained per month

50 Branches; 300,000 members Added every month

Capacity

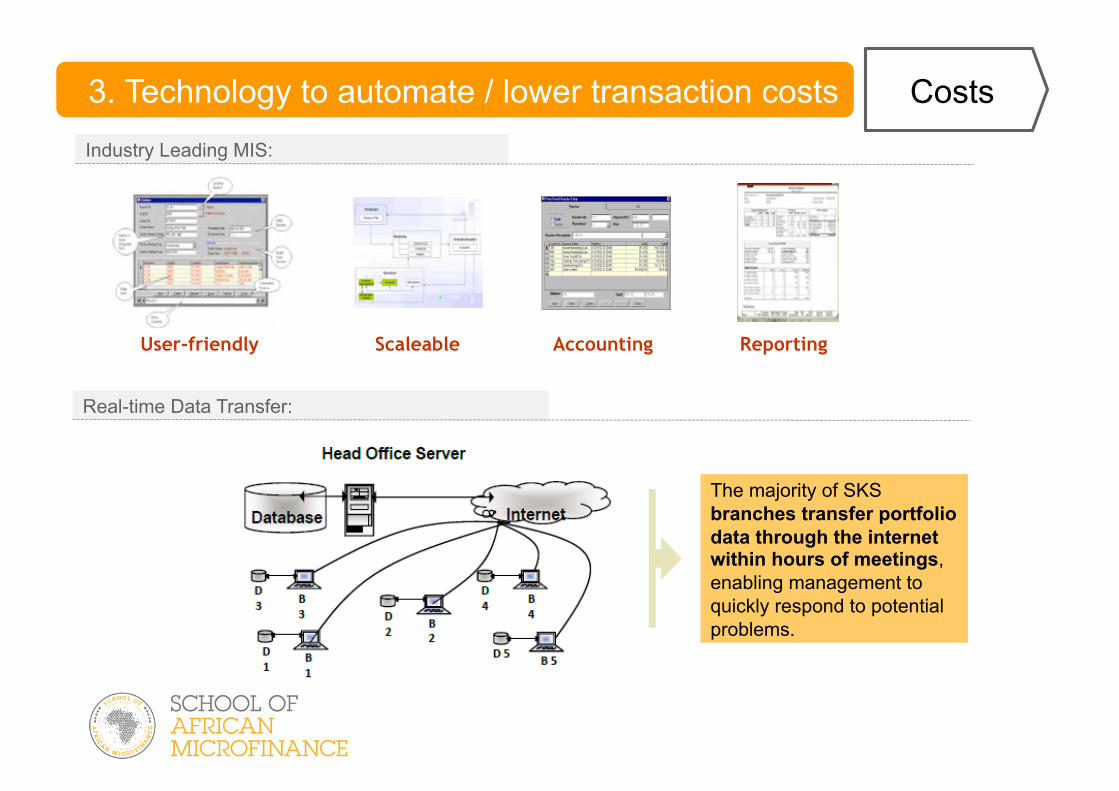

3. Technology to automate / lower transaction costs

Real-time Data Transfer:

Industry Leading MIS:

The majority of SKS branches transfer portfolio data through the internet within hours of meetings, enabling management to quickly respond to potential problems.

User-friendly Scaleable Accounting Reporting

Costs

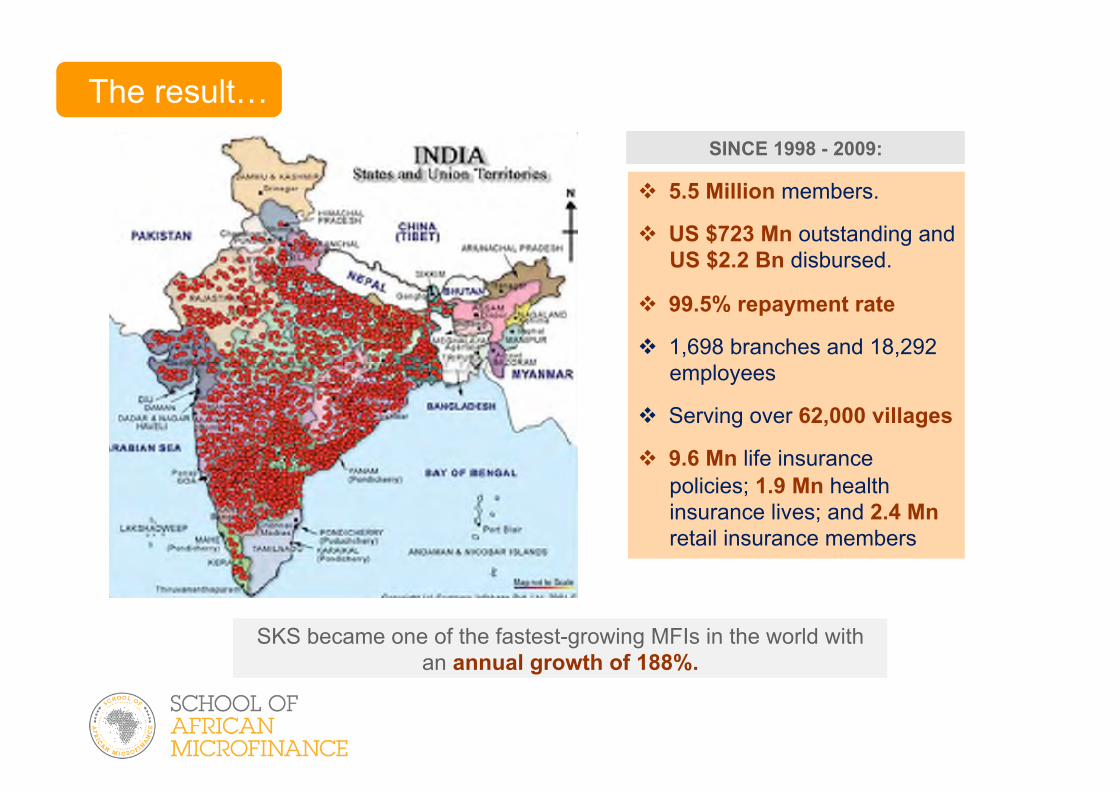

The result…

! 5.5 Million members.

! US $723 Mn outstanding and US $2.2 Bn disbursed.

! 99.5% repayment rate

! 1,698 branches and 18,292 employees

! Serving over 62,000 villages

! 9.6 Mn life insurance policies; 1.9 Mn health insurance lives; and 2.4 Mn retail insurance members

SINCE 1998 - 2009:

SKS became one of the fastest-growing MFIs in the world with an annual growth of 188%.

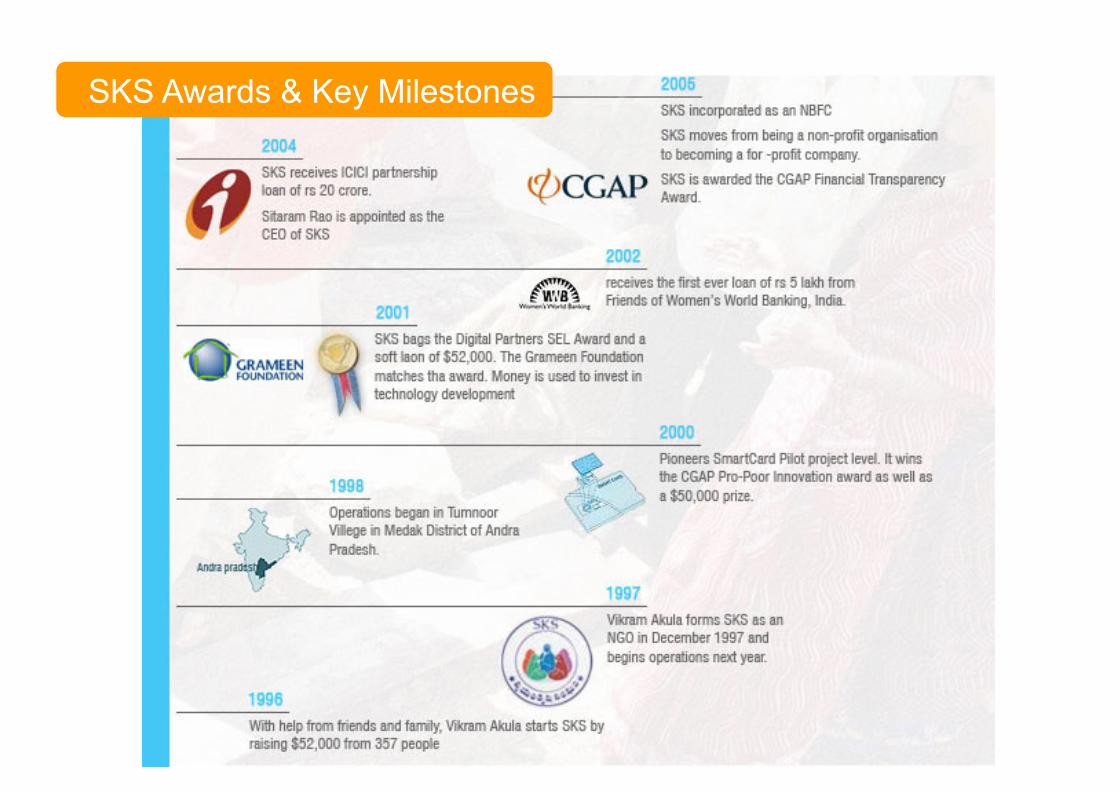

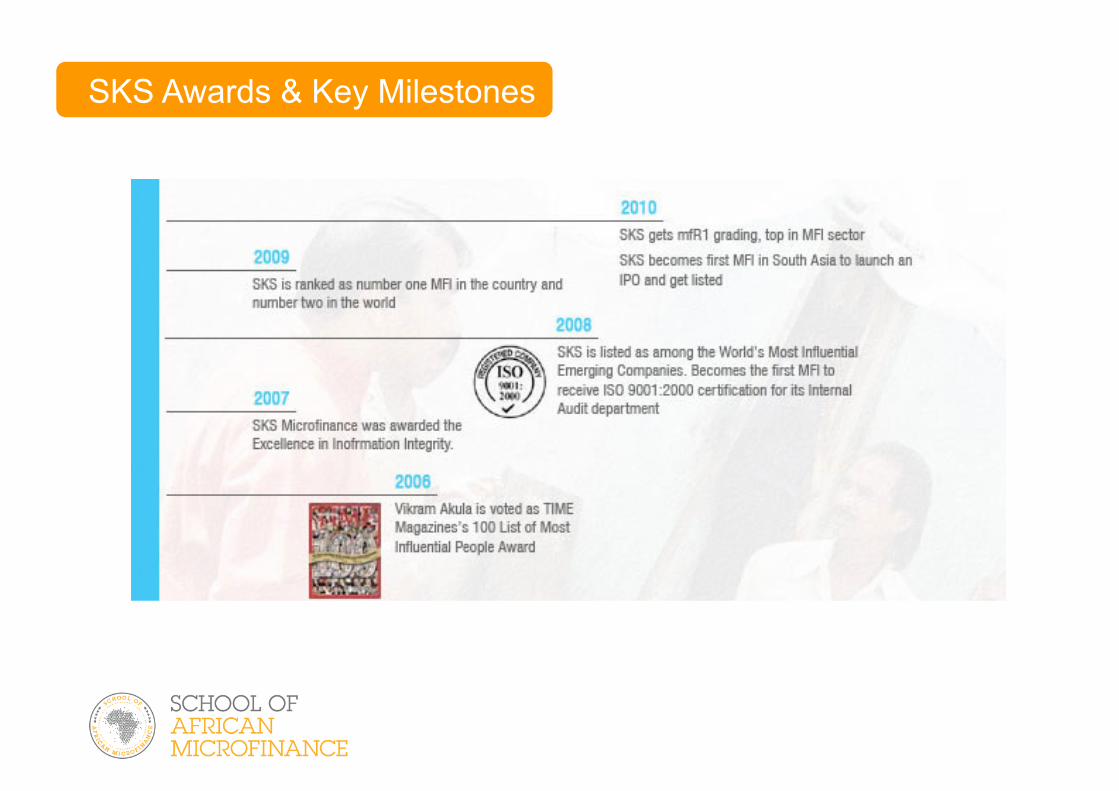

SKS Awards & Key Milestones

SKS Awards & Key Milestones

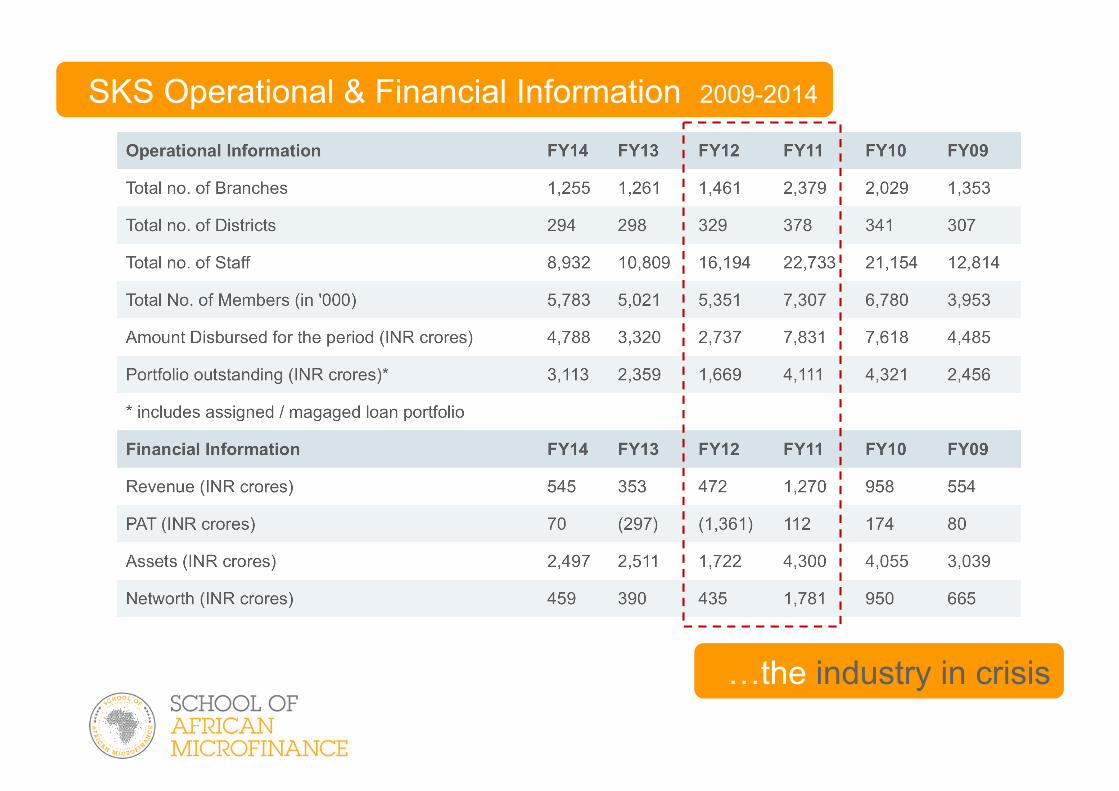

SKS Operational & Financial Information 2009-2014

…the industry in crisis

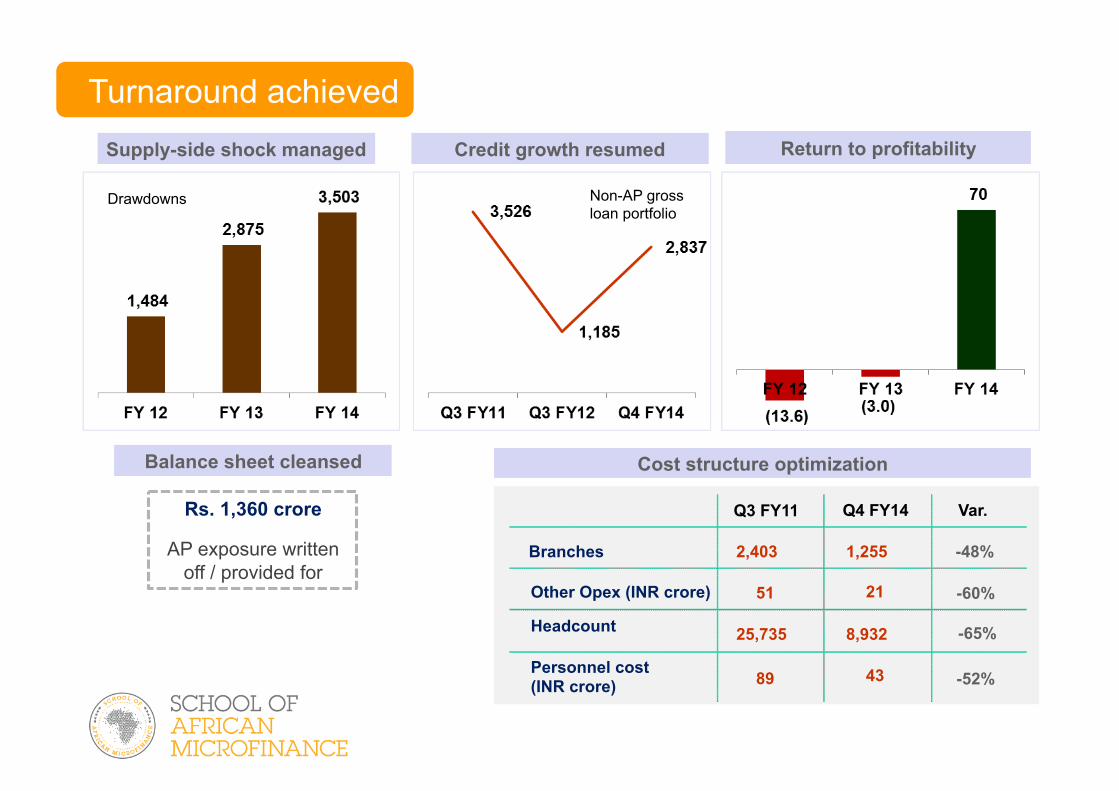

Turnaround achieved Supply-side shock managed Credit growth resumed Return to profitability

Balance sheet cleansed Cost structure optimization

Rs. 1,360 crore

AP exposure written off / provided for

Var. Q4 FY14

Branches

Other Opex (INR crore)

Headcount

Personnel cost (INR crore)

Q3 FY11

2,403 1,255

21 51

25,735 8,932

89 43 -52%

-48%

-60%

-65%

Drawdowns Non-AP gross loan portfolio

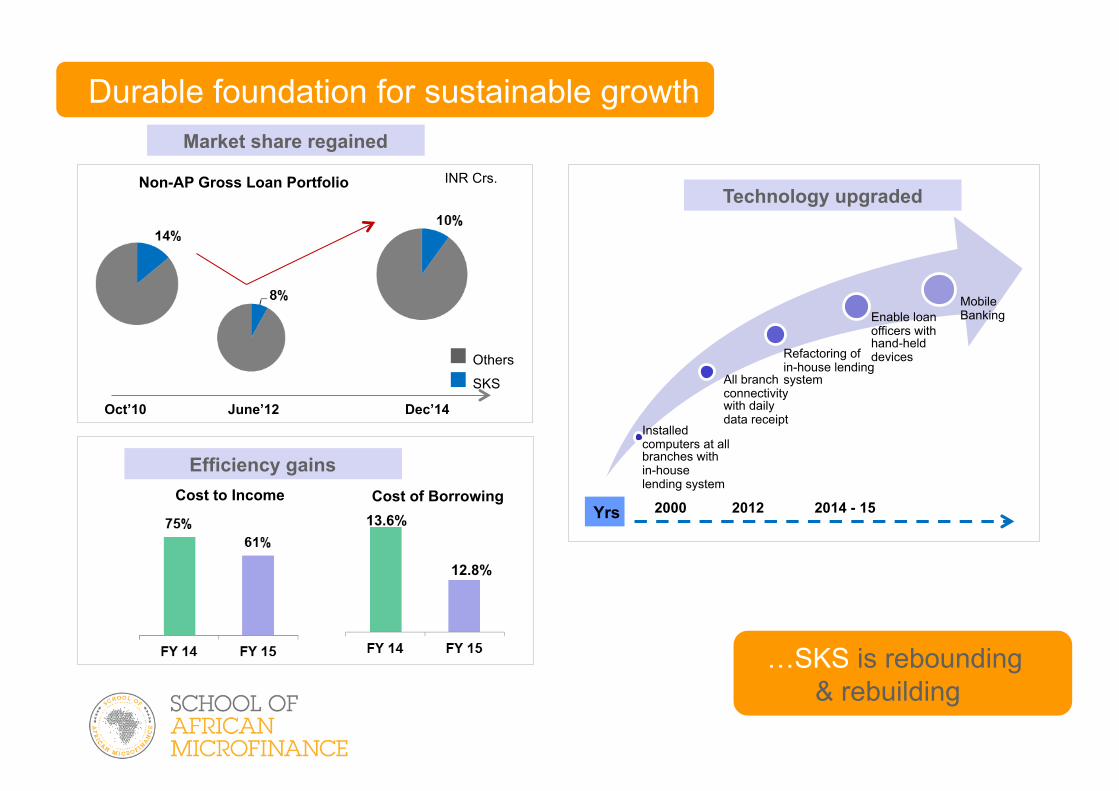

Durable foundation for sustainable growth Market share regained

Non-AP Gross Loan Portfolio INR Crs.

Oct’10 June’12 Dec’14

SKS

Others

Efficiency gains

12.8%

13.6%

Cost to Income Cost of Borrowing

Technology upgraded

Installed computers at all branches with in-house lending system

All branch connectivity with daily data receipt

Refactoring of in-house lending system

Enable loan officers with hand-held devices

Mobile Banking

Yrs 2000 2012 2014 - 15

…SKS is rebounding & rebuilding

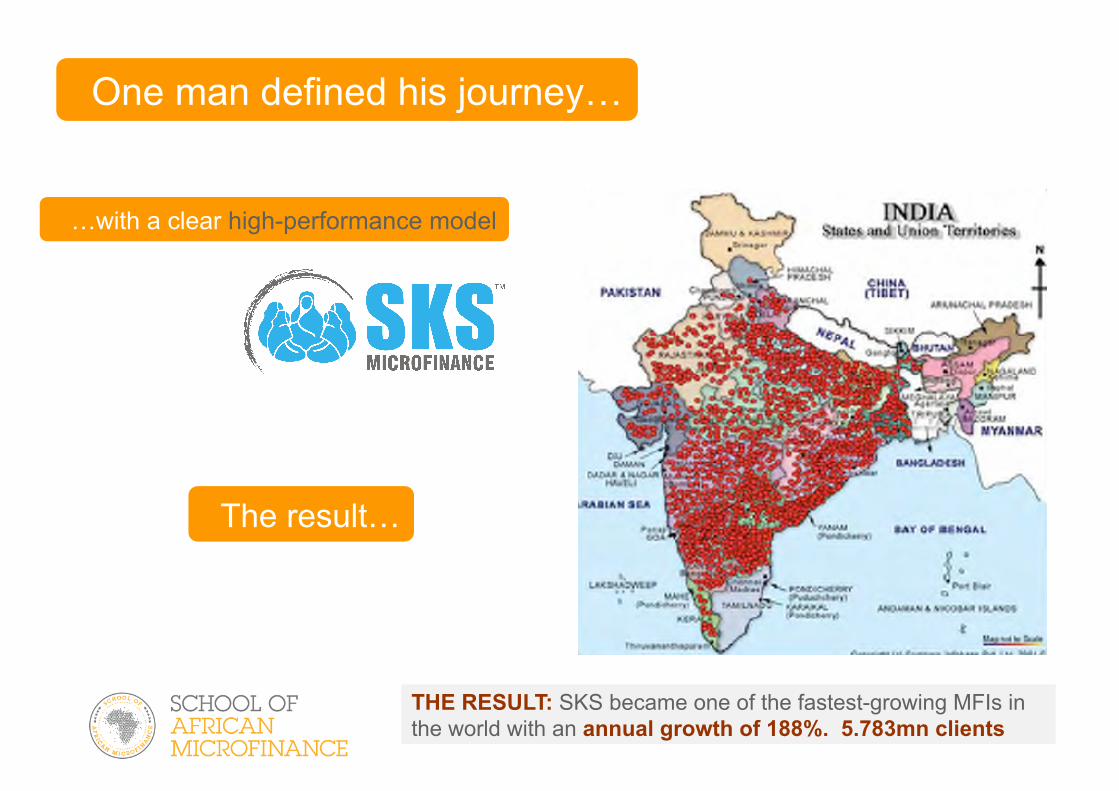

One man defined his journey…

…with a clear high-performance model

The result…

THE RESULT: SKS became one of the fastest-growing MFIs in the world with an annual growth of 188%. 5.783mn clients

Market Focus and Position

Results in better decisions

Distinctive Capabilities

Results in better practices

Performance Anatomy

Results in better mindsets

Balance, Alignment and Renewal

Commit to High-Performance

Questions and Discussions

Thank You