an industry in crisis, facing reality sam 2015 - plenary session day 5

TRANSCRIPT

An Industry in Crisis | Facing Reality Michael Mithika, SAM Course Director 11th September, 2015

2

Any progress

Percentage of people in Sub-Saharan Africa and South Asia who live on less than $2 a day… compared to only 14% in MENA.

Source: World Bank

70%

A short history…

Looking back

4

History of Microfinance

Informal credit and savings

Formal state-dominated banks; directed credit

Credit and Savings Cooperatives and People’s banks – 1800s

Inclusive financial systems

“Microcredit” institutions – experimentation in 70’s

1720’s England – Irish Loan Fund

5

Recent Evolution of Microfinance

Agriculture credit

Donor projects

Microfinance Institutions and

sustainability

1990s

Inclusive Financial Systems

1980s

1970s

Directed Credit

Financial Systems

Private investors, new players

emerge; technology leads

innovation

2000s

Vision

Shaping the industry…

Funders

7

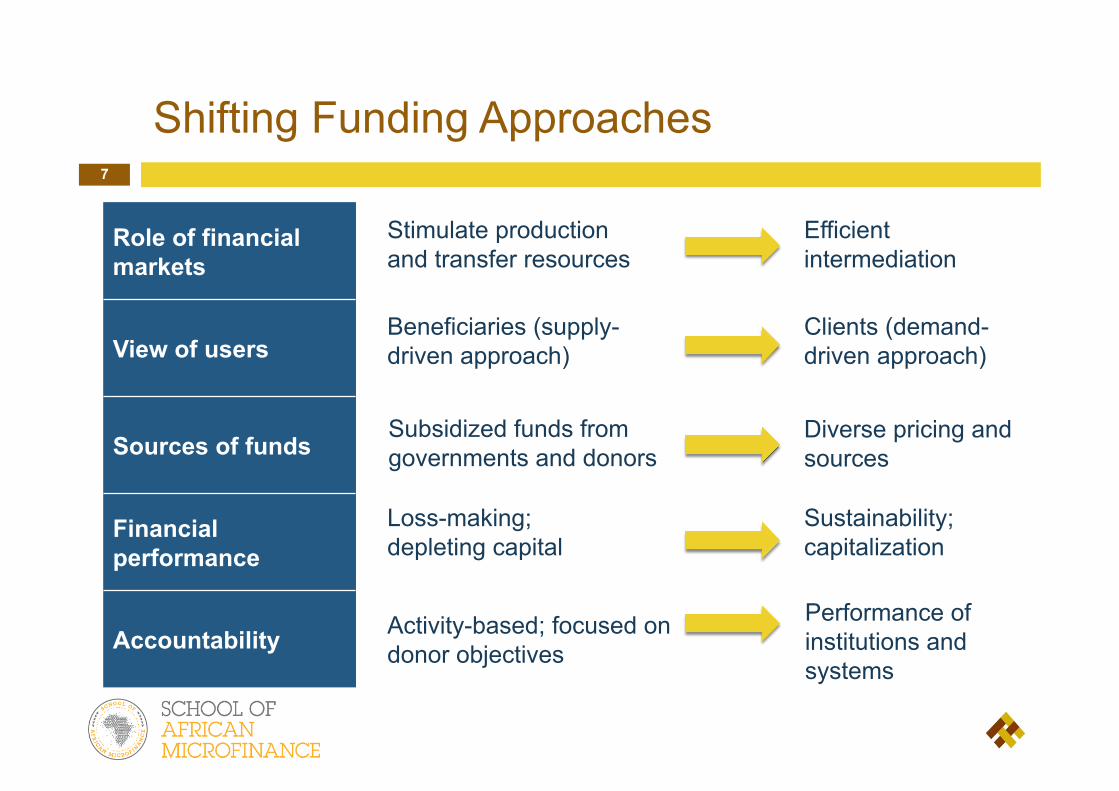

Shifting Funding Approaches

Role of financial markets

View of users

Sources of funds

Financial performance

Accountability

Stimulate production and transfer resources

Efficient intermediation

Beneficiaries (supply-driven approach)

Clients (demand-driven approach)

Subsidized funds from governments and donors

Diverse pricing and sources

Loss-making; depleting capital

Sustainability; capitalization

Activity-based; focused on donor objectives

Performance of institutions and systems

8

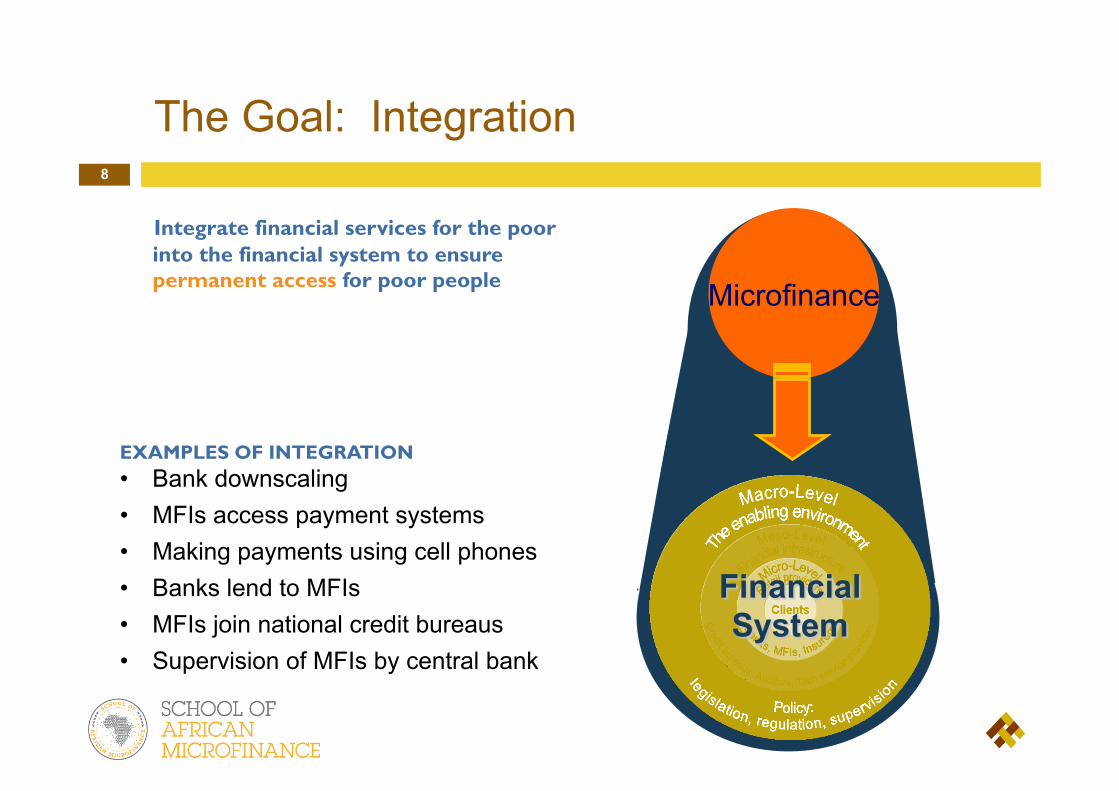

The Goal: Integration

Integrate financial services for the poor into the financial system to ensure permanent access for poor people Microfinance

EXAMPLES OF INTEGRATION • Bank downscaling • MFIs access payment systems • Making payments using cell phones • Banks lend to MFIs • MFIs join national credit bureaus • Supervision of MFIs by central bank

9

International funding for financial inclusion is still on the rise…

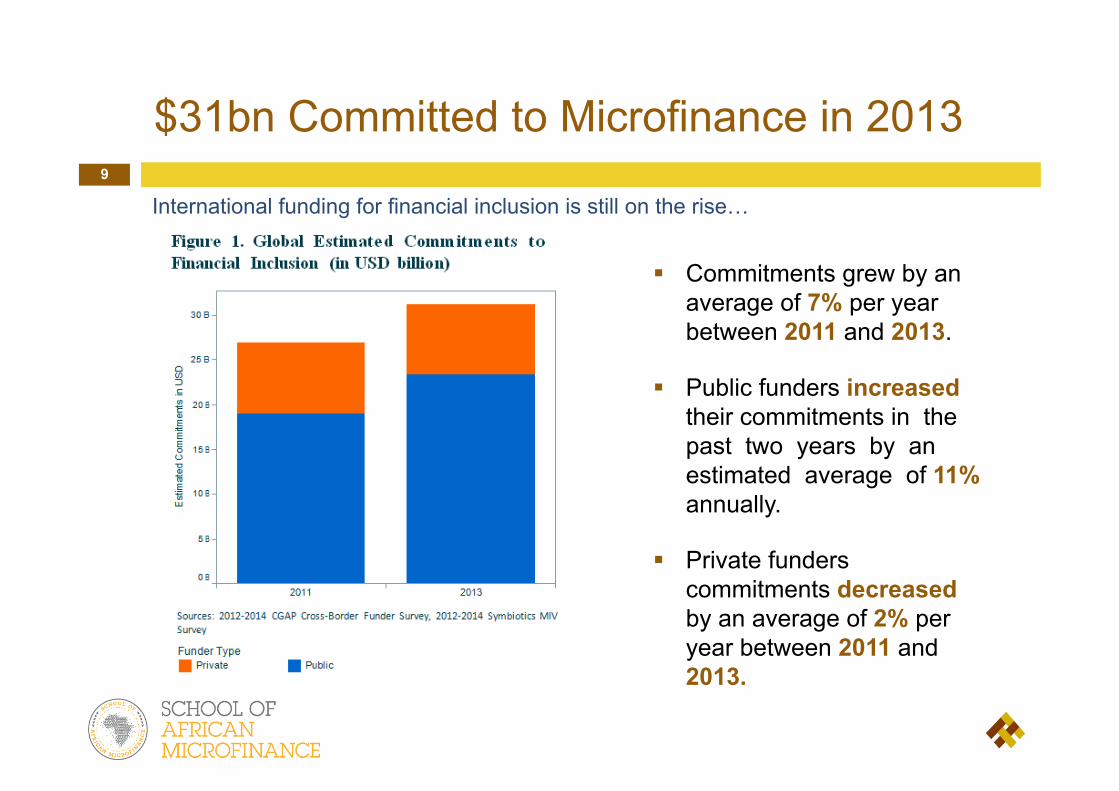

$31bn Committed to Microfinance in 2013

! Commitments grew by an average of 7% per year between 2011 and 2013.

! Public funders increased their commitments in the past two years by an estimated average of 11% annually.

! Private funders commitments decreased by an average of 2% per year between 2011 and 2013.

10

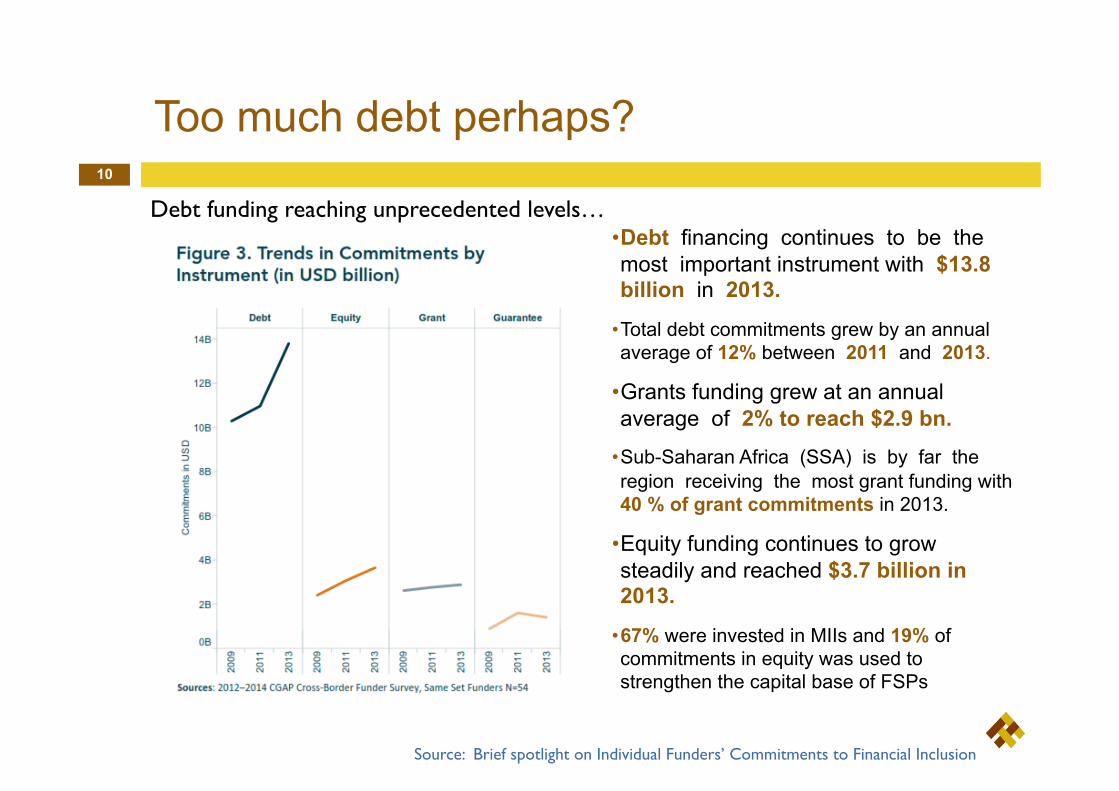

Too much debt perhaps?

Source: Brief spotlight on Individual Funders’ Commitments to Financial Inclusion

Debt funding reaching unprecedented levels… • Debt financing continues to be the most important instrument with $13.8 billion in 2013.

• Total debt commitments grew by an annual average of 12% between 2011 and 2013.

• Grants funding grew at an annual average of 2% to reach $2.9 bn.

• Sub-Saharan Africa (SSA) is by far the region receiving the most grant funding with 40 % of grant commitments in 2013.

• Equity funding continues to grow steadily and reached $3.7 billion in 2013.

• 67% were invested in MIIs and 19% of commitments in equity was used to strengthen the capital base of FSPs

11

Where is the money going?

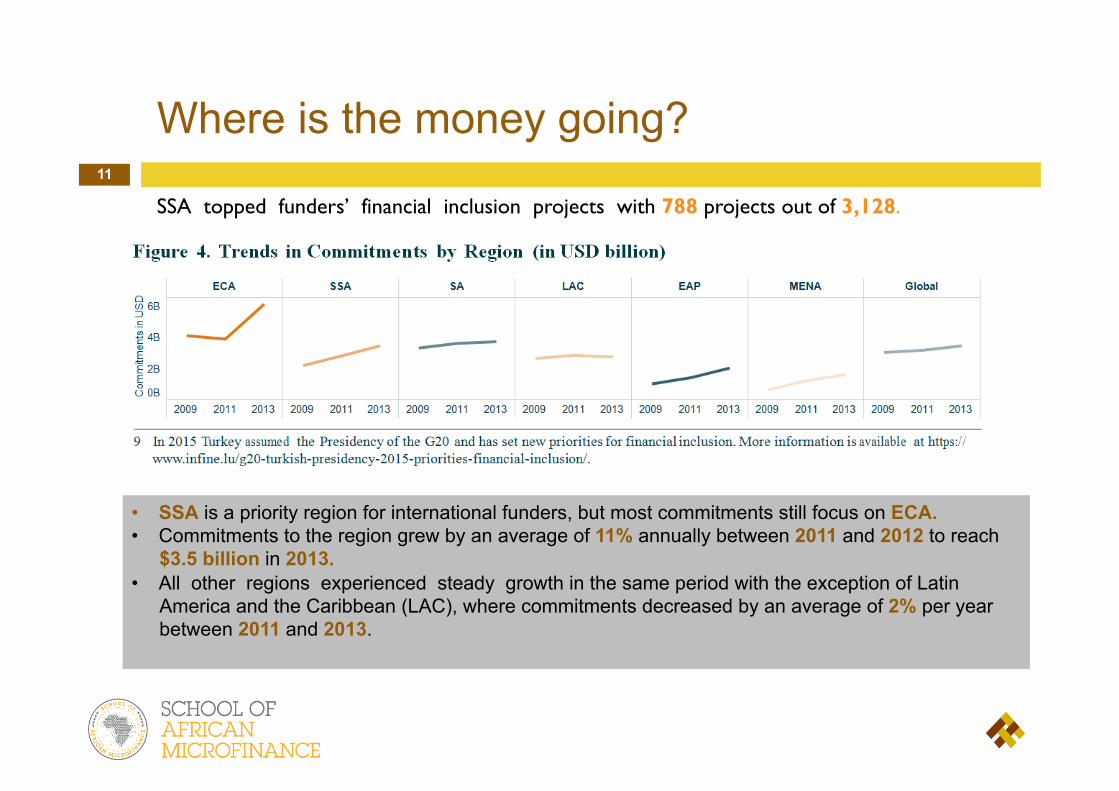

SSA topped funders’ financial inclusion projects with 788 projects out of 3,128.

• SSA is a priority region for international funders, but most commitments still focus on ECA. • Commitments to the region grew by an average of 11% annually between 2011 and 2012 to reach

$3.5 billion in 2013. • All other regions experienced steady growth in the same period with the exception of Latin

America and the Caribbean (LAC), where commitments decreased by an average of 2% per year between 2011 and 2013.

12

More funding…

Has this helped alleviate poverty?

The new face of microfinance?

Commercial Microfinance

14

One man’s determination

“My unexpected quest to end poverty through [extreme] profitability”

Vikram Akula,

Founder, SKS Microfinance 2010

15

The SKS Acceleration Model

CAPITAL

CAPACITY

COSTS

16

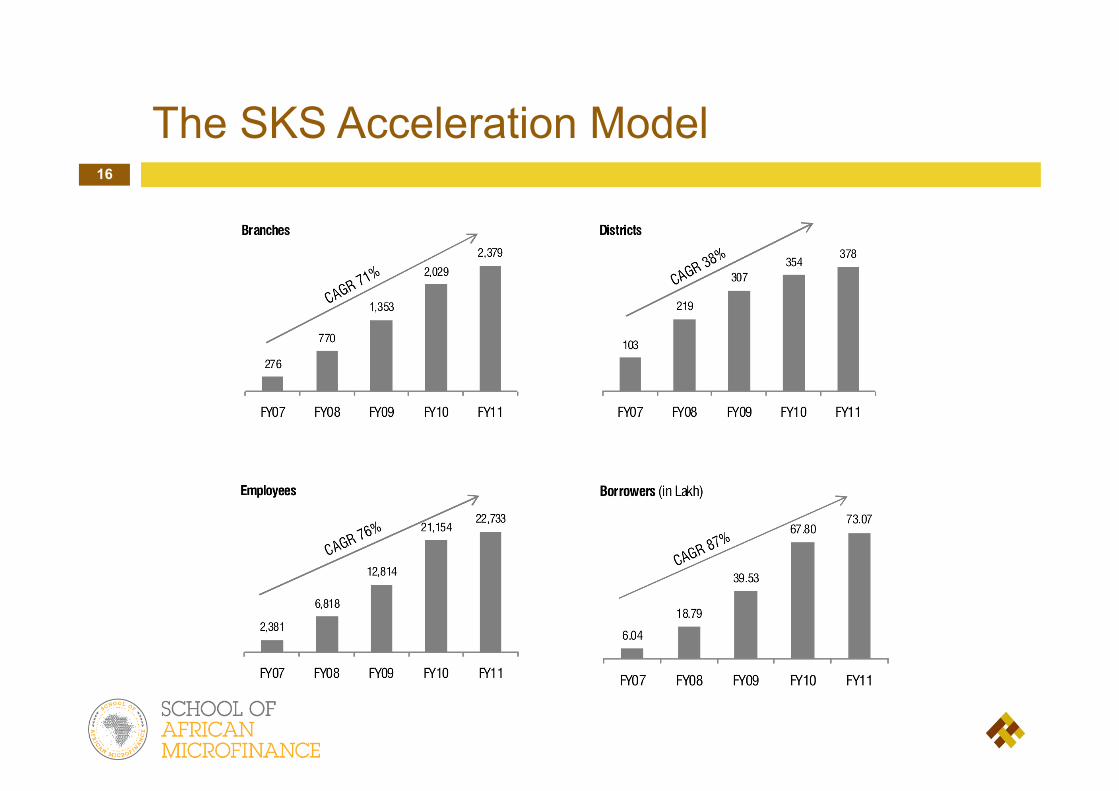

The SKS Acceleration Model

17

Are clients better off…

…because of increased investment in microfinance?

18

Reaching millions… but?

Distress…

19

New Risks emerging…

Banana Skins Report 2012-2014

2012 Biggest Risks NEW RISKS 2014 Biggest Risks(‘12)

Over-indebtedness Strategy (6) Over-indebtedness (1)

Corporate Governance Financial capability (11) Credit risk (4)

Management Quality Product risk (12) Competition (8)

Credit risk Risk Management (6)

Political interference Governance (2)

Compelling research claims…

The critics

21

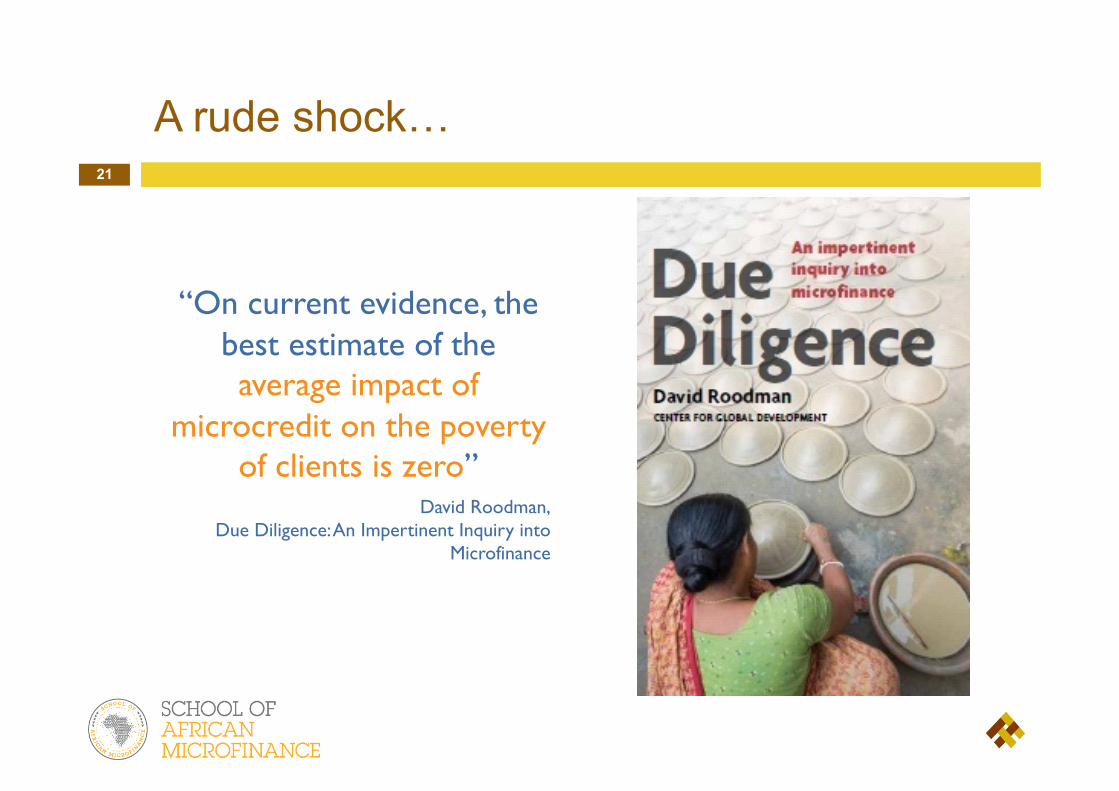

A rude shock…

“On current evidence, the best estimate of the average impact of

microcredit on the poverty of clients is zero”

David Roodman, Due Diligence: An Impertinent Inquiry into

Microfinance

22

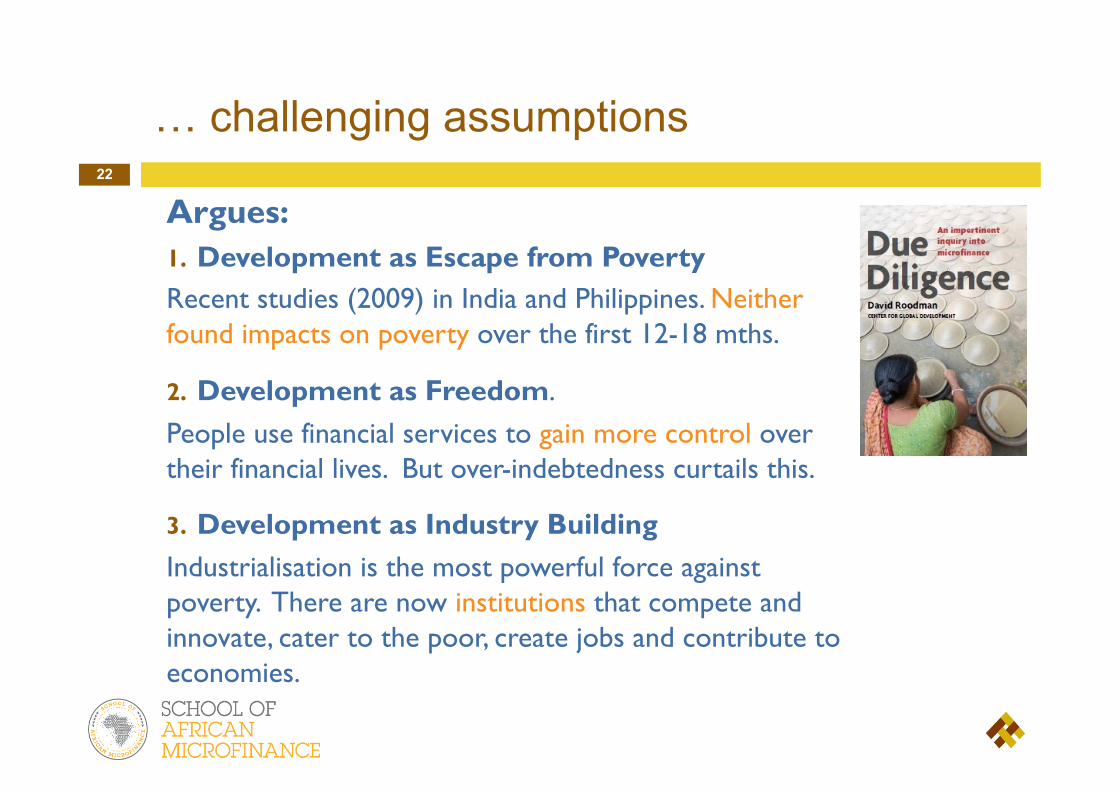

… challenging assumptions

Argues: 1. Development as Escape from Poverty Recent studies (2009) in India and Philippines. Neither found impacts on poverty over the first 12-18 mths.

2. Development as Freedom. People use financial services to gain more control over their financial lives. But over-indebtedness curtails this.

3. Development as Industry Building Industrialisation is the most powerful force against poverty. There are now institutions that compete and innovate, cater to the poor, create jobs and contribute to economies.

23

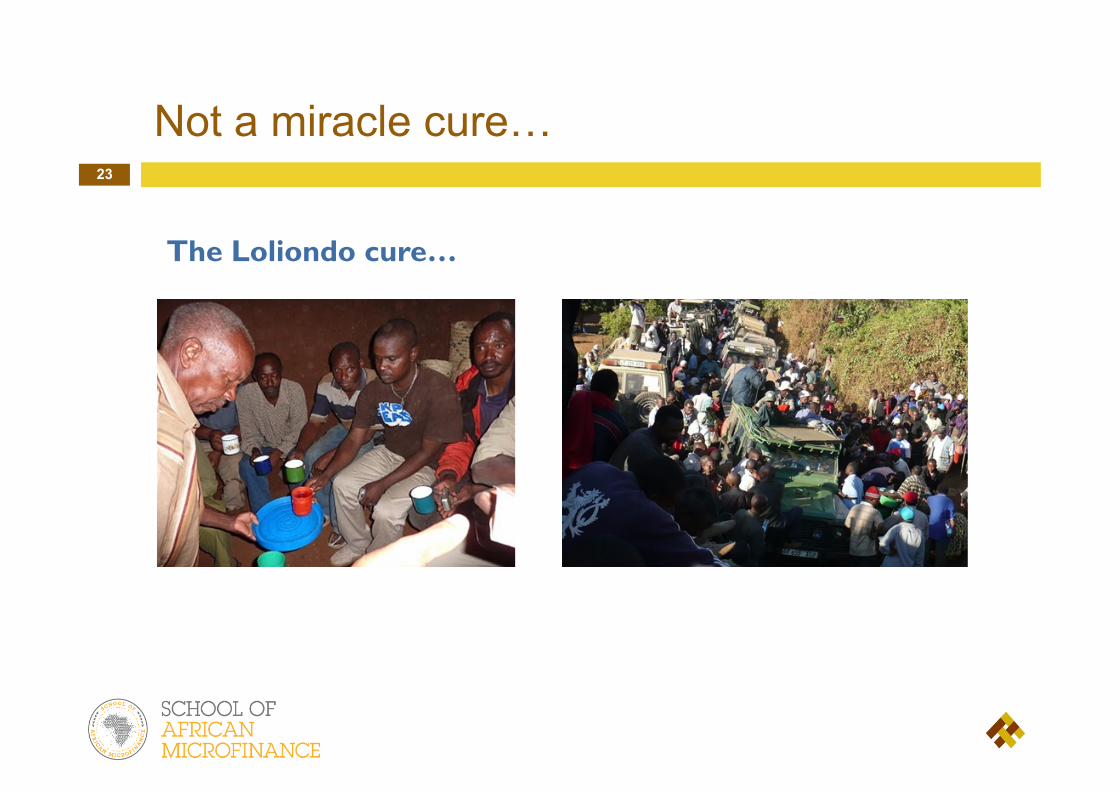

Not a miracle cure…

The Loliondo cure…

24

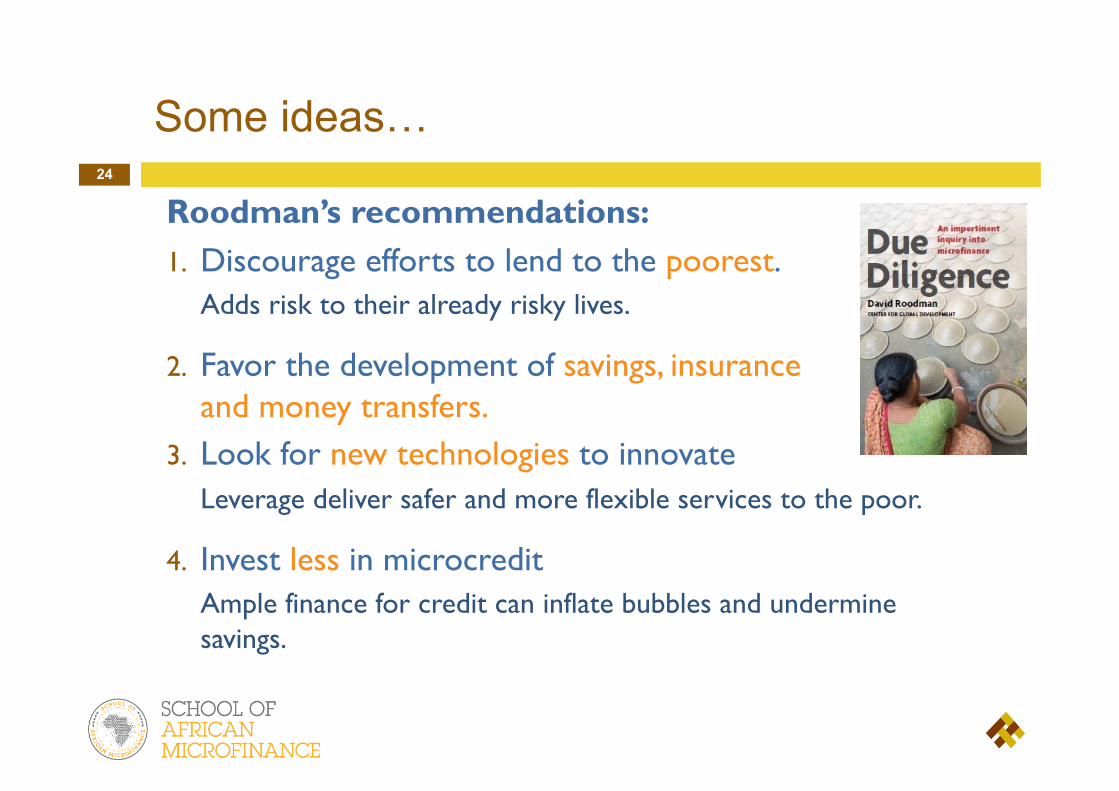

Some ideas…

Roodman’s recommendations: 1. Discourage efforts to lend to the poorest.

Adds risk to their already risky lives.

2. Favor the development of savings, insurance and money transfers.

3. Look for new technologies to innovate Leverage deliver safer and more flexible services to the poor.

4. Invest less in microcredit Ample finance for credit can inflate bubbles and undermine savings.

25

… challenging assumptions

Argues: …that there is no proof that Microfinance does anything at all for poverty reduction.

…it worsens poverty.

…if he is at all right, this huge industry with billions of USD, could in fact be a huge opportunity cost for better ways of reducing poverty.

26

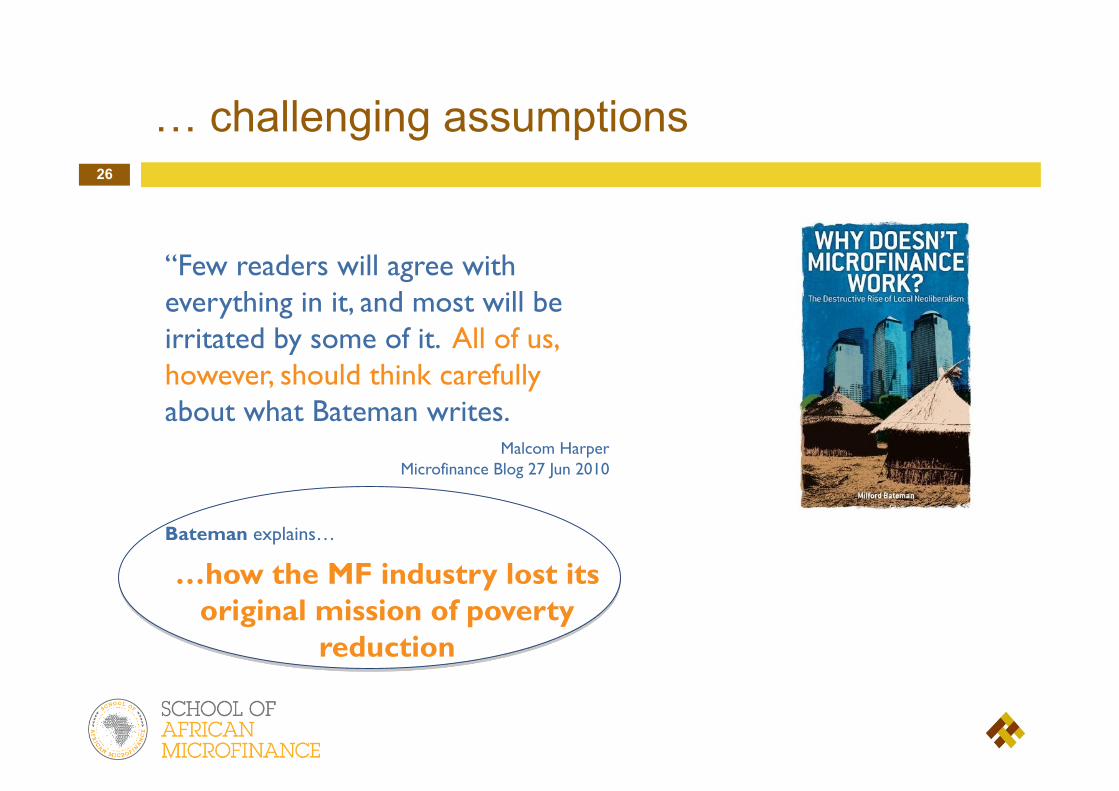

… challenging assumptions

“Few readers will agree with everything in it, and most will be irritated by some of it. All of us, however, should think carefully about what Bateman writes.

Malcom Harper Microfinance Blog 27 Jun 2010

Bateman explains…

…how the MF industry lost its original mission of poverty

reduction

27

… the root cause?

…for these dismal side-effects

“NEW WAVE MICROFINANCE”

…commercial MFIs like Compartamos, BancoSol, Grameen Bank (new style), Accion and others.

Microfinance is now a profit making business that wants to do without subsidies. Commercial

institutions seeking high profits, making millionaires.

28

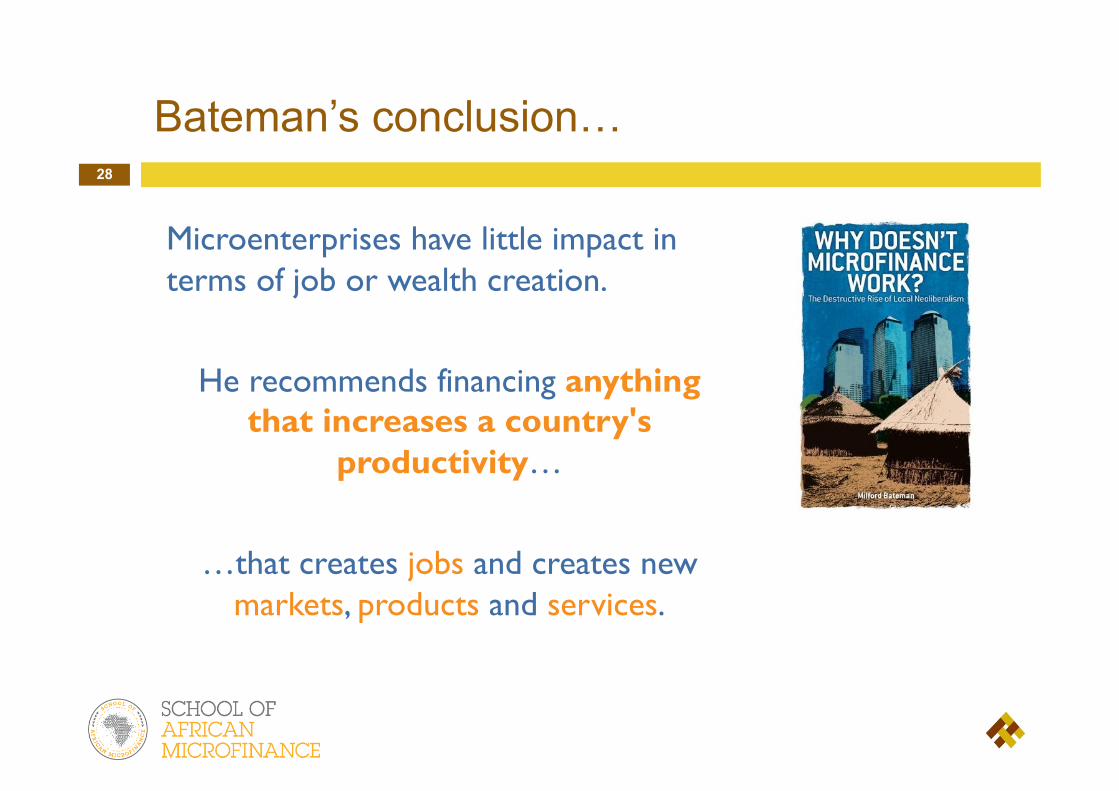

Bateman’s conclusion…

Microenterprises have little impact in terms of job or wealth creation.

He recommends financing anything that increases a country's

productivity…

…that creates jobs and creates new markets, products and services.

29

…challenging assumptions

“If we expand our view to encompass the actual causes of poverty, it becomes clear that

microfinance just won’t do.”

“The only consistent winners in the microfinance game are the lenders…”

Microfinance loans are often used to fund consumption and when used to fund budding businesses, most fail or encounter a lack of

consumer demand.

Structural problems require structural solutions…

THE MICROFINANCE DELUSION

Who Really Wins

- By Jason Hickle, 10 June, 2015

30

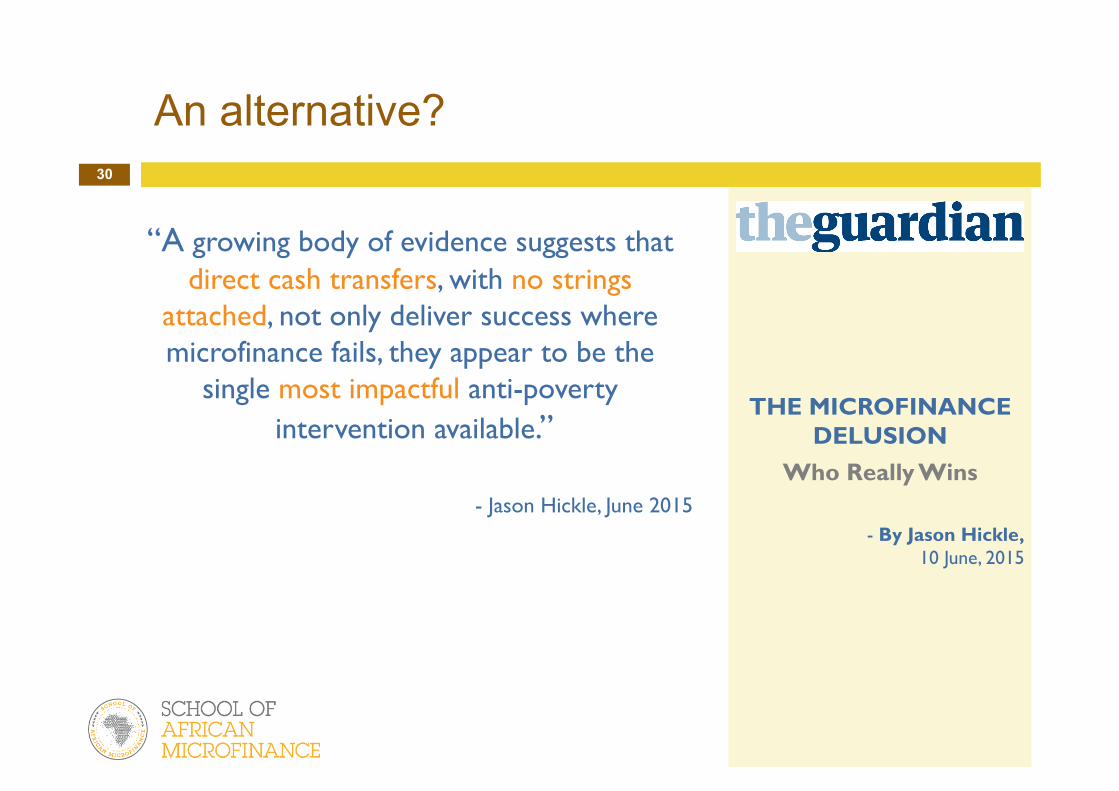

An alternative?

“A growing body of evidence suggests that direct cash transfers, with no strings

attached, not only deliver success where microfinance fails, they appear to be the

single most impactful anti-poverty intervention available.”

- Jason Hickle, June 2015

THE MICROFINANCE DELUSION

Who Really Wins

- By Jason Hickle, 10 June, 2015

31

The revolution…

! At least 45 countries in the Global South now give CTs (cash transfers) to more than 110 million families.

! The size of public spending on cash transfers varies from 0.1% of GDP to 4%, although most programs fall in the range of 0.4% to 1.5%.

! Every program is different, from universal child benefits in Mongolia to pensions in Africa to family grants in Latin America.

Just Give Money to the Poor: The Development Revolution From the Global South By Armando Barrientos and David Hulme

32

Hickle’s conclusion…

We should not abolish microfinance altogether, but microfinance will never work until we address the background conditions

that produce poverty in the first place

…set up the right systems for small businesses to succeed – strong subsidies, state assistance and welfare support to prop up entrepreneurs when they fail

THE MICROFINANCE DELUSION

Who Really Wins

- By Jason Hickle, 10 June, 2015

33

Case Study: South Africa

Self employment income dropped dramatically between 1997-2003,

falling by more than 11% per annum.

40% of income of the South African workforce is spent on

repaying debt

“The programmed diversion of funds into microcredit applications has been a first-order development disaster in the post-apartheid era. ”

- Milford Bateman

% of active credit users in South Africa

defined as over-indebted in 2012.

60%

Commitment to mission

A new model

35

Who does MF Reach?

The extreme poor are rarely reached by microfinance. Social safety net programs are often more appropriate for the destitute and extreme poor.

Destitute Extreme Poor

Moderate Poor

Vulnerable Non-poor

Non-poor Wealthy

P O V E R T Y

L I N E

Most microfinance clients today fall in a band around the poverty line

36

Poverty vs. Prosperity

“No society can surely be flourishing and happy, of which the far greater part of the members are poor

and miserable” Adam Smith,

The Wealth of Nations

37

How many are excluded?

Half of the world’s adult population (about 2.5 billion people) has an account at a formal financial institution:

23% of adults in Africa have an account, however, there is a large variation in account ownership across the different regions.

38

Back to basics…

What the New Philanthropists like Bill &Melinda Gates Foundation are focused on:

! The root causes of poverty…

“lack of access to productivity”

! Poor people can neither create nor seize opportunities if they don’t have basic necessities like nourishment, health, and education

“THE ULTIMATE AIM”

Productivity = Value per unit of Capital | Resource | People

39

Material deprivation (low food consumption, poor housing)

Low human development (education, health)

Lack of voice and ability to influence decisions

Acute vulnerability to adverse shocks (illness, economic crises, natural

disasters)

Poverty is Multidimensional

40

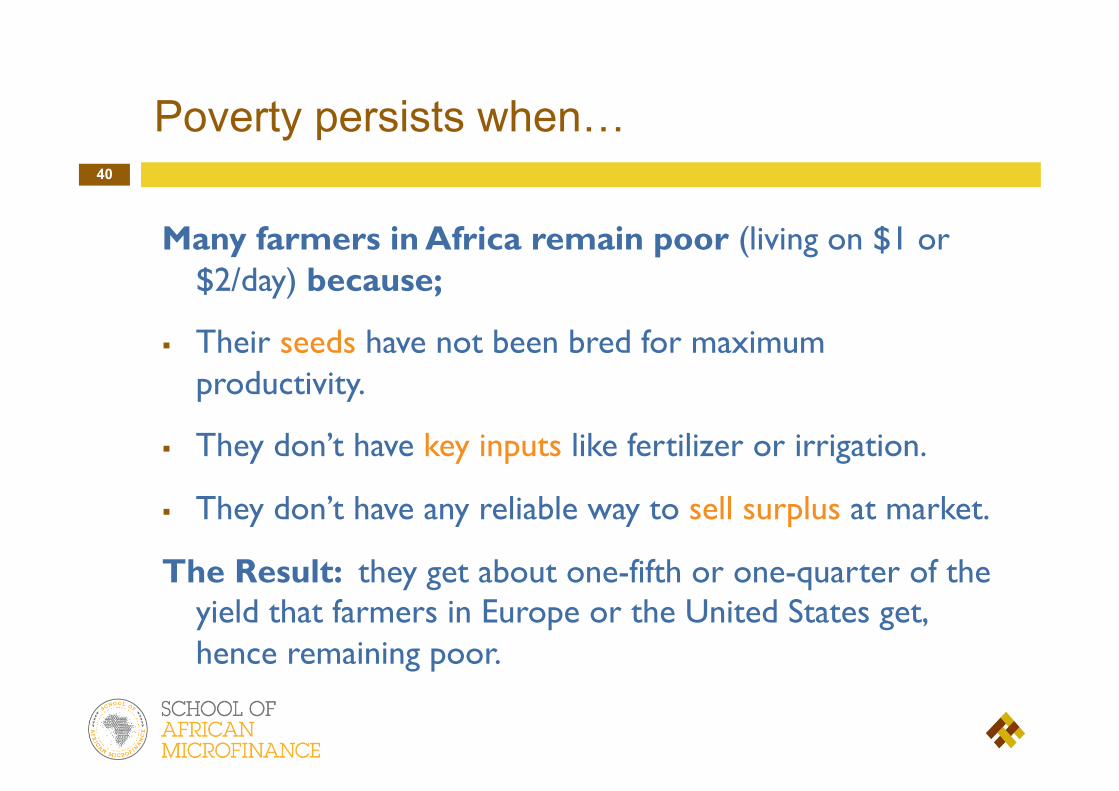

Poverty persists when…

Many farmers in Africa remain poor (living on $1 or $2/day) because;

! Their seeds have not been bred for maximum productivity.

! They don’t have key inputs like fertilizer or irrigation.

! They don’t have any reliable way to sell surplus at market.

The Result: they get about one-fifth or one-quarter of the yield that farmers in Europe or the United States get, hence remaining poor.

41

Access to productivity

Examples:

! GAVI matching funds – they develop new vaccines but also deliver the vaccines already available.

! The Gates Foundation – fund Technoserve in Uganda to work with 50,000 farmers to increase their productivity and quality. The Coca-Cola Company then sources mangoes and passion fruit from these farmers for their fruit juice products.

42

More than basics…

The goal must be more than Financial Inclusion…

Financial Inclusion + other Aspects

…like health, empowerment, business & financial literacy training

…ultimately support productivity levers. e.g. Value-chains

43

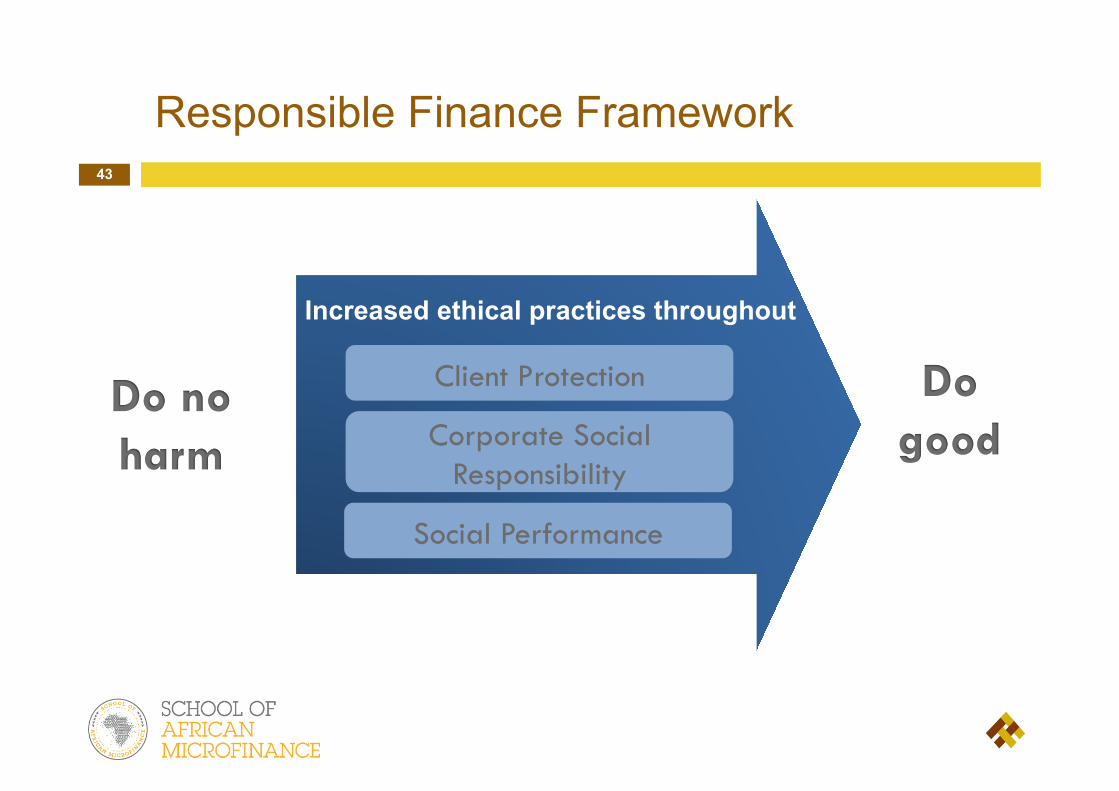

Do good

Responsible Finance Framework

Do no harm

Client Protection

Increased ethical practices throughout

Social Performance

Corporate Social Responsibility

44

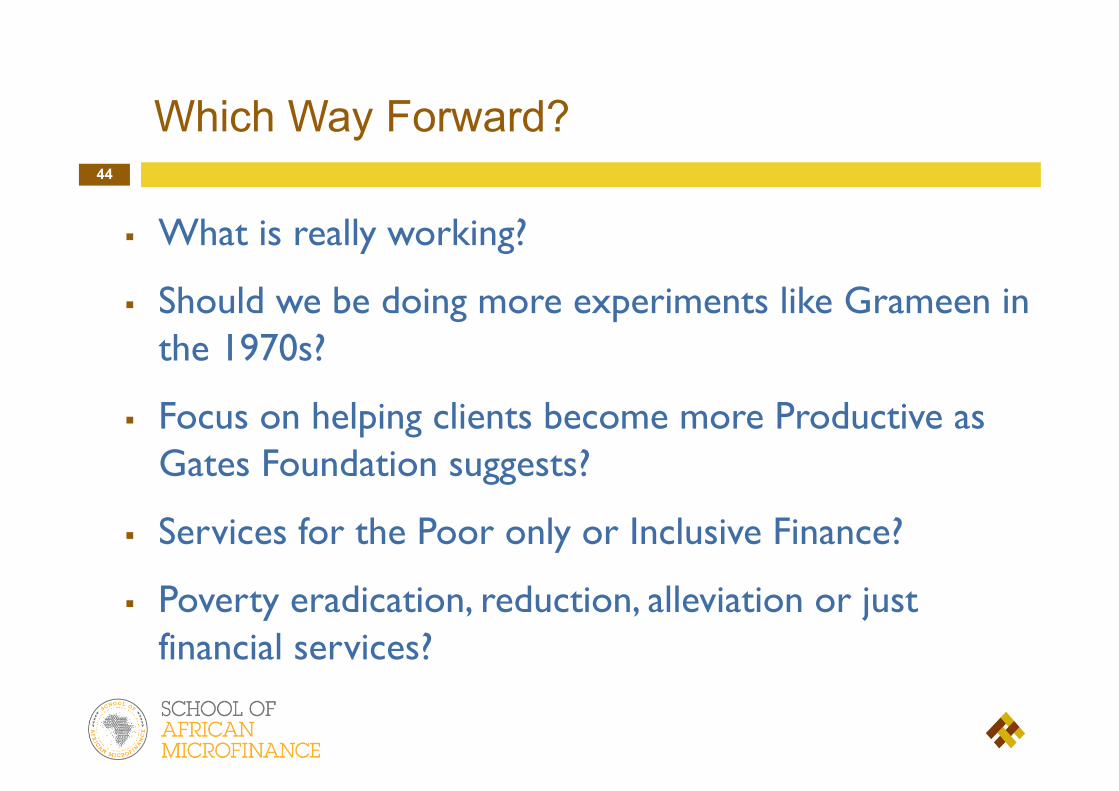

Which Way Forward?

! What is really working?

! Should we be doing more experiments like Grameen in the 1970s?

! Focus on helping clients become more Productive as Gates Foundation suggests?

! Services for the Poor only or Inclusive Finance?

! Poverty eradication, reduction, alleviation or just financial services?

45

The Way Forward…

Finance ++ + other Aspects

…like health, empowerment, business & financial literacy training

…ultimately support productivity levers. e.g. Value-chains

Thank you

We must face reality…