herbalife: a devastatingly perfect storm that could send shares under $30 this year

TRANSCRIPT

Herbalife: A Devastatingly Perfect Storm that

Could Send Shares Under $30

• Quoth the Raven Research continues to believe Herbalife is a strong sell with downside of more

than 46.3% before the end of 2017 and further downside in following quarters

• The potential impact of a coming nation-wide documentary has been significantly underestimated

and may cause an unprecedented public relations nightmare for the company that it may

permanently have trouble recovering from

o For comparison, Blackfish, a similar style of critical documentary, drove SeaWorld’s stock

price down 60% leading up to its release. A critical nationwide 60 Minutes expose on

Lumber Liquidators helped drive its stock price down more than 80% in the months

following the report

• Carl Icahn has a history of selling his stake in companies into buybacks.

o In 2016 he sold $500m in shares into Nuance’s buyback. In 2012, he sold $1.17 billion in

stock back to Motorola Solutions. I believe Mr. Icahn may consider exiting his Herbalife

position before the documentary’s March 17, 2017 release or before the FTC’s sanctions

on Herbalife’s business model take effect in May 2017

• The company’s largest growth market, China, appears to be stalling and a newly disclosed SEC

Foreign Corrupt Practices Act investigation and a new joint venture with a China-based company

raises questions about whether the company is still on solid footing in its largest market

• I believe the company’s true fundamentals continue to deteriorate much more than the company’s

Non-GAAP numbers and accompanying constructed narrative lead on

• I believe the only publicized sell side analyst for the company (who is also an Herbalife distributor)

continues to lead shareholders to the slaughter with an absurd $90 price target

Please carefully read the Disclaimer on the following page

P a g e | 2

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

Disclaimer: The following is for informational purposes only and should not be considered investment advice. Quoth the Raven’s

(“QTR”) articles, Twitter or any other form of dissemination of analysis in person or online are all the sole product of QTR and

his personal, individual opinions. These articles are not associated with, in any way, the opinions, strategies, or works of QTR’s

employer, associates, or entities in any way otherwise related to QTR. QTR is not a registered investment adviser and does not

hold any licenses in any jurisdiction. (i.e. These are solely my personal thoughts and opinions).

You agree that by reading Quoth the Raven’s articles, you are acting at your own risk. In no event should QTR be liable for any

direct or indirect trading gains or losses caused by any information contained in QTR’s articles, StockTalks, Twitter or any other

internet-based dissemination methods. Information in QTR’s articles are not an offer to sell or a solicitation of an offer to buy any

security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under

the securities laws of such jurisdiction. QTR is not suggesting the transacting of any financial instruments and QTR suggests

consulting your personal financial adviser with regards to any and all such financial transactions. Literally, I was serving beer in

an Irish pub five years ago for a living.

QTR makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy,

timeliness, or completeness of any material contained in this site. Again, you should seek the advice of your personal financial

adviser or a financial professional regarding your stock transactions. QTR does not, in any way, guarantee that he is providing all

information that may be available on any topic written. QTR recommends, again, that you do your own due diligence and consult

a registered financial adviser before buying or selling any security.

The information and opinions contained in this article are based on publicly available information about companies and persons.

QTR recognizes that there may be non-public information in the possession of companies or other people that could lead others

to disagree with my analyses and conclusions. Any statements, estimates, projections and opinions may prove to be substantially

inaccurate and are inherently subject to significant risks and uncertainties beyond QTR’s control.

Although QTR believes the statements he makes in this article are substantially accurate in all material respects and do not omit

to state material facts necessary to make those statements not misleading, QTR makes no representation or warranty, express or

implied, as to the accuracy or completeness of those statements or any other written or oral communication it makes with respect

to any company or persons mentioned, and QTR expressly disclaims any liability relating to those statements or communications

(or any inaccuracies or omissions therein). Thus, shareholders and others should conduct their own independent investigation and

analysis of those statements and communications of companies or persons to which those statements or communications may be

relevant.

QTR most always holds a position in any of the securities profiled in his pieces and he constructs his disclosures to the best of his

knowledge in order to maintain transparency and also to uphold and respect pertinent securities laws. QTR may or may not report

when a position is initiated or covered. Each investor must make that decision based on his/her judgment of the market.

I am short Herbalife through owning put options.

I stand to make money if the price of Herbalife stock moves lower.

I am not a stockbroker or financial adviser. I hold no licenses and am not registered with FINRA or any other financial body. I

am a casual investor making casual observations for the purpose of discussion and open communication and analysis of

companies and stocks. Often, I am wrong. I have been wrong in the past and will be wrong in the future.

Again, all articles are my opinion only and are not suggestions to buy or sell any equity, bond, option or other financial

instrument. QTR may have long or short positions in any tickers mentioned at any time and reserves the right to open, close, or

modify positions at all time without notice. My conclusions are the result of my personal due diligence and have been wrong in

the past. Alright, now you kids go have fun out there.

P a g e | 3

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

When I asked [outgoing Herbalife CEO Michael] Johnson how he

felt about all the people who had lost money trying to get rich

through Herbalife, he hesitated. “I’m sorry that it happened,” he

said. “I’m sorry people lost money at a racetrack and at the lottery.

Today’s Herbalife is about hard work and energy. I can’t go and fix

anything in the past.

The New Yorker, 3/5/2017

P a g e | 4

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

$30 Per Share and Under: To Me, It’s Only a Question of “When” and Not “If”

In what will be my only report on Herbalife issued for the rest of this year, and possibly for good, I want

to give the public my firmly held belief on why the stock could easily be $30 or under by the end of 2017.

Obviously, this differs with the "analyst consensus" targeting $90 per share, but I believe my track record

of accuracy and attention to detail thus far with Herbalife should cause readers to carefully examine what

I am going to present in today's article.

I believe coming effects of the Betting on Zero documentary have been vastly understated and

underestimated by the market and I am in a unique position to comment on it, having been one of the few

who has had a chance to view the film prior to its release. I also believe that the company's latest

financing and corresponding buyback could possibly be used to take Carl Icahn out of his position in the

company. The new and growing debt burden that the company now has to deal with and service in an

environment where rates are going up could wind up being devastating, as I predict the core of the

business will continue to deteriorate, eventually giving way only to a balance sheet with a book value of

$2.11 per share.

Also to blame for what I believe will be Herbalife's continued deterioration this year is a reduction in

growth for the company’s largest market, China. In a small informal blog post I put up a week ago, I

pointed out that I thought there was something weird about the company’s new joint venture with China-

based company Tasly. While I believe that the deterioration of growth and this joint venture are likely tied

together one way or another, I have yet to fill in the missing link between the two. What is for certain is

that, across the board, the company's core business is deteriorating. Analyst estimates continue to come

down, the company's guidance continues to get lower, and the GAAP numbers tell a starkly different tale

than the company’s “adjusted” Non-GAAP guidance. It is using these numbers that has helped me arrive

at the belief that Herbalife could very easily be worth a fraction of what it is worth today in just a few

short months.

We have already seen significant selling over the past few trading days, as the stock has moved from

around $60, where it was after earnings, to about $53, where it trades today. I believe this to be the

P a g e | 5

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

beginning of a much larger downtrend that could once and for all wrap up the Herbalife story for the most

part.

Betting on Zero Could Be PR Armageddon

The first thing that needs to be addressed is what I believe to be a vast under-estimation and flippant

attitude towards a coming documentary that will be available nationally, as well as on subscription

services that have millions of international subscribers. Everyone knows that Betting on Zero is going to

be released on March 17 of this year. What everybody doesn't know is exactly how devastating the film

could be for the company.

It has been asserted over the last few years by me that much of Herbalife’s organic internal growth comes

from the confidence of its distributors and the confidence that those distributors have in their ability to

earn from potential new recruits. This film will be the first effective instance of taking what is otherwise a

Wall Street story and boiling it down to a gut wrenching and stomach churning experience that any

average movie watcher can experience. It could wreck the confidence of millions of potential recruits, as

well as potential existing distributors.

I went into the world premiere of Betting on Zero at Tribeca having seen everything that has to do with

Herbalife. Because the company declined to participate in the documentary, much of the story was

produced using financial news clips and publicly available documentation on the company. These

interviews and details I have memorized and seen many times over. The story is nothing new to me, nor

are what I believe to be the harsh and negative effects of the company's business model on a good

majority of its participants.

However, even after my extensive background, I wound up leaving the film in tears because of the

portrayal of several personal accounts that director Ted Braun profiles in the film. The point is that if it is

enough to incite emotion from somebody that knows this situation cold, it is going to be more than

enough to incite real emotion from viewers who are only first familiarizing themselves with the Herbalife

saga. For those that want a little bit more of an in-depth look at the film itself, you can watch the trailer

and then read a review I wrote after the Tribeca Film Festival last year.

P a g e | 6

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

The good news for critics and bad news for the company is that the film has since been amended to

include the results of the FTC’s recent findings, content that will only serve to make the film that much

more devastating for the company.

Let's look at a couple of quick examples as to what mainstream media can do to the public’s perception of

a company. First, there is the obvious comparison in Blackfish, the documentary that critically portrayed

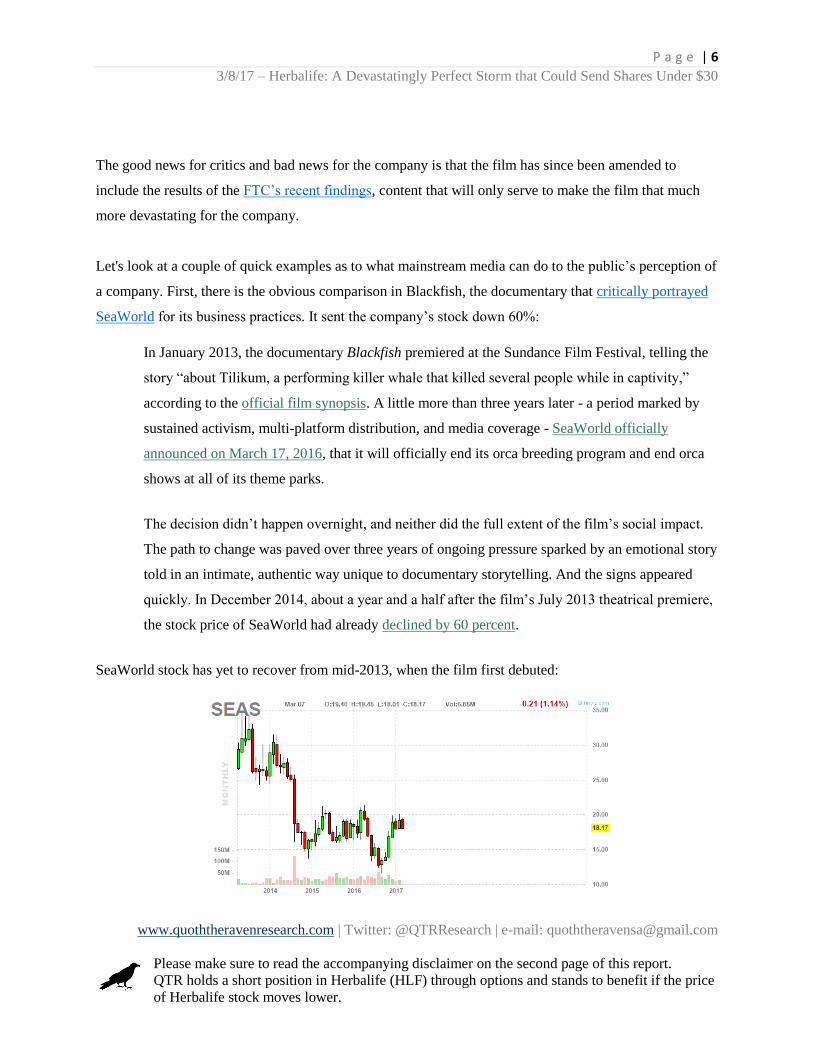

SeaWorld for its business practices. It sent the company’s stock down 60%:

In January 2013, the documentary Blackfish premiered at the Sundance Film Festival, telling the

story “about Tilikum, a performing killer whale that killed several people while in captivity,”

according to the official film synopsis. A little more than three years later - a period marked by

sustained activism, multi-platform distribution, and media coverage - SeaWorld officially

announced on March 17, 2016, that it will officially end its orca breeding program and end orca

shows at all of its theme parks.

The decision didn’t happen overnight, and neither did the full extent of the film’s social impact.

The path to change was paved over three years of ongoing pressure sparked by an emotional story

told in an intimate, authentic way unique to documentary storytelling. And the signs appeared

quickly. In December 2014, about a year and a half after the film’s July 2013 theatrical premiere,

the stock price of SeaWorld had already declined by 60 percent.

SeaWorld stock has yet to recover from mid-2013, when the film first debuted:

P a g e | 7

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

We also have the situation with Lumber Liquidators for comparison. Lumber Liquidators was featured

during one 15 or 20 minute critical segment on 60 Minutes and it subsequently resulted in an immediate

25% drop, followed by a catastrophic loss for shareholders when the stock moved down more than 80%

over the course of the year after the report:

Those that have not seen Betting on Zero or those who are writing it off as a nonevent do not understand

director Ted Braun's knack for grabbing the gut and the heart of the viewers who are watching. Braun

tries to take an objective look at both the company and the entire situation, but Herbalife comes out

looking horrible. I said in my review of the film in April of 2016:

While Betting on Zero is not a decidedly anti-Herbalife movie from the onset, its ability to profile

real victims, the Wall Street story and the simple truth about the company's business practices

could be absolutely devastating to Herbalife if the film is picked up and distributed on a national

scale.

And unlike anything that we have seen throughout the media coverage of the Wall Street story,

Betting on Zero tells us the story of 10 to 15 undocumented Latino immigrants who have lost

hundreds of thousands of dollars as Herbalife distributors. The film follows them in a quest for

justice and reparations, led by LULAC activist Julie Contreras. The film profiles Contreras just as

much as Ackman, explaining her ferocious activist nature as the product of proud Mexican

parents and a gunshot wound that almost left her dead in the early 2000's. A notable scene in the

film is Contreras' reaction to a cease and desist letter sent to her from Herbalife. Contreras, in

tears, swears to never apologize for sticking up for victims of Herbalife.

P a g e | 8

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

The movie has some surprisingly touching and deeply emotional moments. I always knew that

what the company was doing to people who did not understand how the business plan worked

was disingenuous, but seeing on film a group of victims literally praying to God for justice after

many of them severed relationships and spent hundreds of thousands of dollars tugged at the

heartstrings of Ms. QTR and I, who both teared up.

There’s no real better way to sum it up than to say that if you hold shares heading into the national release

of this film, I believe you are playing Russian Roulette with your capital.

Could Carl Icahn Decide to Exit into the New Buyback at Any Time?

This brings us to one of the film’s antagonists, Carl Icahn. Without even bringing up the fact that Mr.

Icahn has petitioned publicly to buy up to 50% of the company and has yet to act on much more than half

of that - and without bringing up the fact that Mr. Icahn may have put out an inaccurate press release after

the FTC settlement announcement, let's talk some basic common sense about why Mr. Icahn could want

to exit his position in the company as soon as this month.

Think about this. You are Mr. Icahn. You hold a $1.3 billion position in Herbalife as of February of this

year and have seen the fundamentals of the business implode before your eyes. The CEO you originally

bet on is stepping down soon, after selling tens of millions of dollars in stock, some of which as recent as

just a couple of days ago. A documentary by an award-winning director is about to hit the national stage

that is going to make you look like a mix between Lex Luther and Gordon Gekko – and, in the process,

will make Herbalife look like it is of extremely questionable moral and ethical standards.

Your good friend, Bill Stiritz, who you possibly got to buy into the stock, has just sold a significant

portion of his stake in the company after reassuring the media and the public just months prior that he had

full confidence you and the in the company. His stake in 2015 was 7.5 million shares, or about $350

million. His stake now is 4.8 million shares, which Matt Stewart writes may even be “closer to 4 million

shares as many of his call options may expire worthless or out of the money”.

If you’re Carl, do you wait around to see what the results of this film ultimately are? If you do, what

about the FTC order that kicks into effect in May of this year? Do you wait for those sanctions to kick in?

P a g e | 9

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

I sure wouldn't, but again, maybe the guy who has consistently displayed a lack of knowledge as to the

fundamentals of the business has some type of inside track lined up that I don't know about. It could

happen – as my disclaimer says, I’m often wrong.

After all, there has been all of this talk about Icahn wanting to make a bid for the company and take it

private. So far, he has done no such thing and we have already gotten one credible report that he was

looking to sell his shares in the company. I'm not the world’s greatest financial analyst, but that seems

like the complete opposite of taking a company private.

A case for a leveraged buyout gets significantly more difficult when you consider that the company just

completely obliterated its balance sheet with this last $1.45 billion credit facility it has taken on.

If he still wants to sell, isn’t it more likely that Carl Icahn would sell into the company’s newly authorized

buyback in order to take himself out of his position instead of trying to make a strategic move for the

company that is levered significantly more than it was just a quarter ago?

If you answered yes, we are on the same page. This option looks to be more and more of a reality as

investors look into Icahn’s track record of selling into buybacks. For instance, in 2016 he sold back $500

million in Nuance shares to the company.

And in 2012, he sold into Motorola Solutions’ buyback:

P a g e | 10

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

“The filing speaks for itself,” Stiritz said when reached by phone.

He declined to comment further.

Matt Townsend, Bloomberg, February 2017

P a g e | 11

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

The Company’s Largest Growth Market is Stalling

In his first presentation on Herbalife back in 2012, one of the terms that Bill Ackman pointed out was the

"pop and drop" that occurs after Herbalife appears in certain geographic locations.

This phenomenon, as shown here, is a result of the company entering a geographic location with steam

and then eventually petering out as new recruits dry up and presumably the reality of the business starts to

set in for participants.

Over the past few years, China has been the growth engine for the company. After CFO John DeSimone

admitted a couple of quarters ago that comps were going to be difficult for China this year, it is now

looking like the rate of growth has turned negative in dramatic fashion in China. This past quarter, the

company experienced negative growth in volume points and net sales in China, indicating that the

company may very well be at the edge of the apex of saturation in China.

P a g e | 12

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

This market doesn't even have to drop further in order for the company to start to really fall apart - it

really only needs to stall or stagnate. As other geographic locations do the same, the size of Herbalife’s

member base only churns in place or reduces slightly, indicating that it is potentially possible that the

company has reached worldwide saturation.

If you are a believer that the company is a pyramid scheme, this is extraordinarily bad news for the

company’s future. For a company that the FTC seems to think survives primarily on recruitment, the lack

of participants to recruit would certainly seem to be a significant barrier to conducting business.

When you put the three of these things together – the coming documentary, China’s growth declines and

the coming FTC sanctions beginning in May - they create a perfect storm for a significant selloff in

Herbalife shares. Do you want to get caught long if Icahn sells prior to the documentary hitting the public,

or do you want to ride it out with little to no visibility as to where the company is heading?

Buyback – Or War Chest?

(Charts and accounting in this section compiled with the help of “Fear and Greed”)

There is also a second, less possible, speculative argument to make that Herbalife may have simply been

raising the capital necessary to create a war chest for itself while it can with its recent $1.45 billion credit

facility. If the company doesn’t buy Icahn out of his shares, this may be the case.

The structure with which the company has put together its buyback and the length of time that it intends

to use to buy back stock, three years, all suggest that the company could possibly be trying to just build a

war chest of cash for itself. Obviously, this would prompt several inquiries. The first of which would be

whether the company feels as though its free cash flow is going to be curtailed in a big way moving

forward. As you can see, the company’s free cash flow continues to decline.

P a g e | 13

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

Another inquiry one may have in this hypothetical situation is whether the company has full and

unrestricted access to its cash that is domiciled overseas.

The Financials Are Just Plain Ugly

(Charts and accounting in this section compiled with the help of “Fear and Greed”)

I believe the financials are very clearly telling a story of a company that's core is in distress.

On top of the company seeing its fundamentals in stagnation or the beginning of real decline, there are

liabilities that aren't talked about in the mainstream and certainly haven't been covered by sell side

analysts that investors need to be aware of.

The Balance Sheet is Loaded with Sub-Par Assets

Investors in Herbalife should take a real close look at the assets that make up just about 1/3 of total assets.

For those unable to read a balance sheet, let’s make the job a little easier:

P a g e | 14

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

Prepaid expenses are cash that has been paid out – but not expensed in the income statement (yet). I

assume their value on liquidation to be $0.

Goodwill and intangibles are the same and have a $0 value at liquidation.

Deferred financing costs (same as prepaid expenses) also have a $0 value at liquidation.

When it comes to deferred tax assets - this one takes a little explanation. These are “receivables” that the

company “expects” will be collected from taxing authorities in the future. In reality, they may not really

be “collected,” but rather they will reduce future tax payments resulting from future generated taxable

income. This means that when the company loses money today (on an income tax basis), they will carry

those losses forward and offset future taxable income, generating a receivable today.

Think about that for a moment - Herbalife expects that it will collect these assets from various

governments in the future. Funny, as it doesn’t seem that Herbalife has a good relationship with various

governments based on disclosed ongoing tax battles the company has been having with various

governments. For instance, the company has what appears to be over $150 million in outstanding tax

liabilities that it doesn't look like it is going to be able to avoid paying. I'm very simply basing this on the

fact that this language has been included in the company’s filings for the last couple of years. We’ll

review more in a second. Back to these deferred tax assets.

The accounting standard for recording these receivables is “more likely than not.” In other words, it

could practically be a coin-toss on whether these assets will have any real value going forward, but we

can assume it’s at least a 51% yes/49% no situation.

This leaves us with “other” long term assets. This is $154 million - or just about 6% of total assets – and

we know virtually nothing about what’s in here, other than that they are “long-term” assets. In my book,

P a g e | 15

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

if you won’t or can’t tell investors what these assets represent – they should be considered virtually

worthless.

Add this all up and you’ve got $871 million of questionable assets. What value should you ascribe to

these assets? This is up to you, but suddenly I’m acquiring a thirst that only Coke Zero can quench.

The Company Could Have Over $200 Million in Tax Liabilities Outstanding

Let’s dive into corporate tax liabilities a little further.

The blue bars above represent the future expected collections (more likely than not) to occur in the future.

The red bars represent amounts actually required to be paid in the short term. The net of these two

amounts represents the net income taxes receviable on the company’s books.

Herbalife expects that it will actually collect more than it will pay in income taxes. Does that make

sense to you at all? If the future was reasonably assured and not just “more likely than not,” then maybe I

P a g e | 16

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

could accept that position. But this is Herbalife, and to me, the future production of taxable income is in

question.

All the while, known income tax exposures due to audits and other examinations by taxing authorities

have become massive.

Herbalife discloses the following tax-related exposures in its 2016 10-K, some of which are still being

contested or are in various stages of appeal:

• Mexican Tax Administration Service - $56 million

o No known recorded liability

• Mexican Tax Administration Service #2 - $14.2 million

o No known recorded liability

• Mexican Tax Administration Service #3 - $44.0 million

o No known recorded liability

• Mexican Tax Administration Service #4 – 2010, UNKNOWN AMOUNT

o No known recorded liability

• Federal Revenue office of Brazil - $7.6 million

o No known recorded liability

• Several Brazilian States - $49.4 million related to 2016 with the company believing it could

receive a similar assessment for 2014

o No known recorded liability

• Indian VAT authorities - $5.1 million

o No known recorded liability

• Korea Customs Service - $29.7 million (held in “other assets” on the balance sheet)

o No known recorded liability

• Greek Social Security Agency - $2.1 million

o No known recorded liability

Add all of that up and you get a potential exposure of nearly $208 million, with $0 recorded as loss

allowances to cover these ongoing, active demands for payment from taxing authorities.

P a g e | 17

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

The company states that it does not believe a loss is “probable” on any of the $114 million in exposure

just from Mexico. Note the difference in accounting treatment between these liabilities (which are not

recognized unless they are probable) and recording the deferred income tax assets on the books only

when it’s “more likely than not” that they will be collected.

Does that make any sense considering the magnitude of these claims?

One must think that not only will these tax liabilities have an impact to the company’s cash balance

eventually, but they are also probably not doing any favors in terms of the company’s relationship with

each corresponding country. If you worked for the Brazilian government, for instance, and Herbalife

owed you – let’s say possibly $98.8 million (10-K, page 97) - that it had been trying to duck out of and

appeal, it obviously is reasonable to assume that Herbalife may not be a company that you give preference

to when it needs favors in the future.

Inventory is Building Up – Will Write-downs Follow?

On-balance sheet inventory has exploded and now stands at 173 days sales. The explosion in inventory

stands in direct contrast to the deterioration in revenue production.

What kind of a company needs nearly half a year of inventory sitting on its books? Does Herbalife just do

a dismal job in managing inventory? Here’s one possible reason: sales have dropped off so fast the

company can’t put the brakes on production fast enough. Let’s see what happens in following quarters

with potential “write downs” of inventory. I predict that we’ll see some fairly significant write-downs in

coming quarters as the company may not be able to move this stagnating inventory.

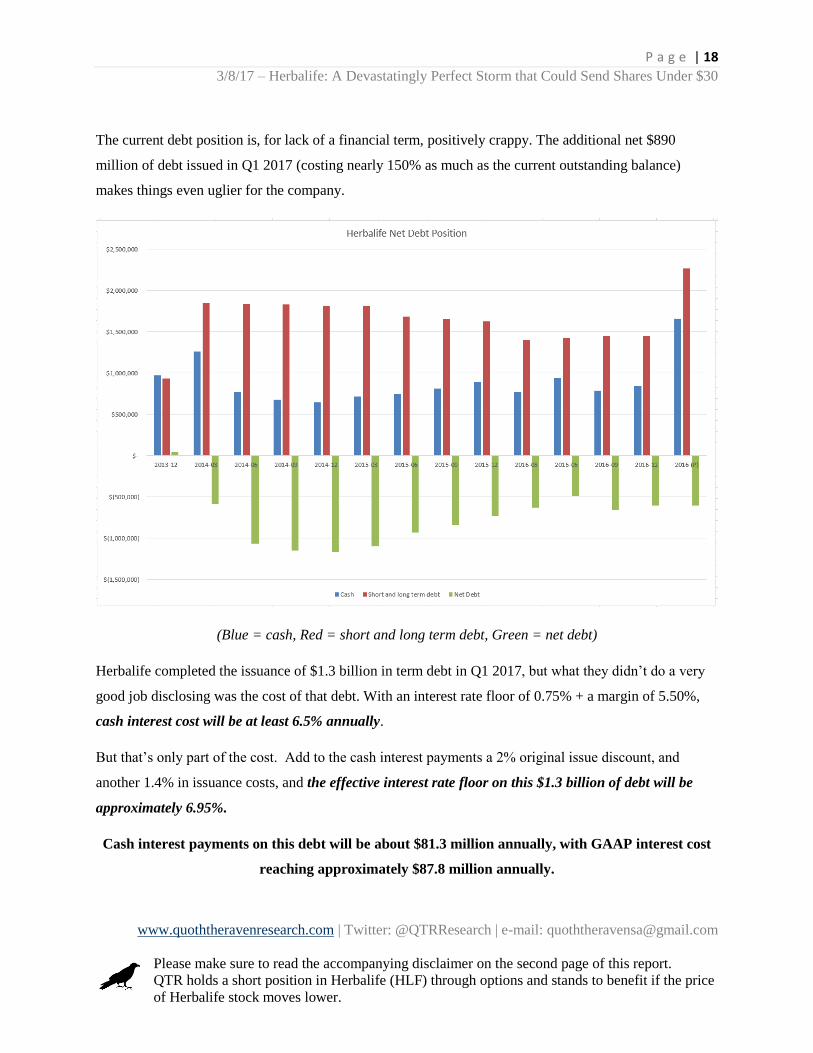

The Debt Situation Has Gotten Significantly Worse

P a g e | 18

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

The current debt position is, for lack of a financial term, positively crappy. The additional net $890

million of debt issued in Q1 2017 (costing nearly 150% as much as the current outstanding balance)

makes things even uglier for the company.

(Blue = cash, Red = short and long term debt, Green = net debt)

Herbalife completed the issuance of $1.3 billion in term debt in Q1 2017, but what they didn’t do a very

good job disclosing was the cost of that debt. With an interest rate floor of 0.75% + a margin of 5.50%,

cash interest cost will be at least 6.5% annually.

But that’s only part of the cost. Add to the cash interest payments a 2% original issue discount, and

another 1.4% in issuance costs, and the effective interest rate floor on this $1.3 billion of debt will be

approximately 6.95%.

Cash interest payments on this debt will be about $81.3 million annually, with GAAP interest cost

reaching approximately $87.8 million annually.

P a g e | 19

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

Get to work analysts - add that interest cost into your models. Offsetting this additional expense will be

savings of interest on $410 million retired debt at an approximate rate of 4.29%, or $17.6 million. That

sounds like a great deal – right? Replace debt at a nearly 162% higher cost?

“Desperation is a stinky cologne”

– Spurbury Police Chief Grady

Cash Flow After Forex Has Collapsed

Let’s go back to the company’s cash flow, which I started to touch on earlier. Remember the good ‘ole

days back in 2013 when the company was a cash flow gushing machine? $600 million in annual free

cash flow was the norm. Well, those days are long gone. Free cash flow after the impact of Forex now

stands at $200 million, or only about 1/3 of what is was only 3 years ago.

This is no longer a growth company. The mounting weight of investigations, sales declines, and a

general collapse in confidnce has wreaked havoc on the company’s ability to produce cash from

operations. This could again be a reason why the 2017 increase in debt may not be used to repurchase

stock (as analysts have hoped) - but may instead be held by the company as a cushion to simply weather

the storm created by the collapse of the company.

Shipping and Handling Collapse Doesn’t Match Revenue Collapse

It appears that shipping and handling revenues declined nearly 19.1% year-over-year, as compared to

reported sales revenue declines of 3.9%. This seems a little suspect.

P a g e | 20

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

Since the company began reporting shipping and handling revenues, they have steadily declined as a

percentage of sales. Why would shipping revenues drop off at a much faster rate than the revenues they

are probably helping to produce? Is it possible that shipping revenues are illustrating the true sales trends

within the company?

(Blue = sequential change in sales, Red = sequential change in S&H)

Net Income – Adjusted or GAAP – Is Getting Ugly

Because a majority of the company’s net income comes from outside of the United States, 32% of

reported GAAP net income was lost due to currency translation adjustments in Q4 2016.

If you thought reported GAAP net income in Q4 2016 was bad enough, you should look at

comprehensive net income – which is really ugly. Comprehensive net income shows the results of the

company after including the accretive or dilutive effects of Forex translation adjustments. Since

Herbalife is so heavily invested in non-USA entities, when the dollar strengthens, these investments lose

value at a very significant rate. In Q4 2016, 32% of reported GAAP net income was “taken back” by

Forex devaluation.

P a g e | 21

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

As President Trump would Tweet: “Sad!”

In the case of new estimates, we have a company whose net income estimates have declined

meaningfully, while EPS estimates push higher. Yet, we are supposed to believe that all is going to be OK

over the course of the long term.

P a g e | 22

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

If you believe the company is a pyramid scheme - or have even entertained the thought - you must have

also learned that at some point, pyramid schemes collapse. When they do, they tend to accelerate on the

way down. If this really is the final act for Herbalife coming up, time is going to be of the essence.

P a g e | 23

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

“The file is closed with the SEC; Raising our PT to $90”

Tim Ramey, June 25, 2015

“There is an ongoing SEC investigation that we suspect resolves

with the closure of the FTC file.”

Tim Ramey, July 2016

“The U.S. Government is investigating dietary supplement maker

Herbalife over whether it violated foreign bribery laws while

conducting business in China…

‘The company is cooperating with the SEC’s investigation and

cannot predict the scope, duration or outcome of the matter at this

time,’ Herbalife said.

Reuters, January 2017

P a g e | 24

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

Despite Everything, Herbalife “Analysts” Remain 100% Clueless

Despite all of this overwhelming analysis to the contrary, the one sell side analyst that gets the most

airtime on CNBC and with "serious investors" maintains his $90 price target on the company. It is an

unfathomable analytical method to seemingly continue to maintain a single price target for 6 months on a

company once it has lowered EPS estimates. Despite the fact that Mr. Tim Ramey has gotten numerous

extremely important things incorrect about the company, namely suggesting on national television that

injunctive relief was off the table and in a research note that the SEC had “closed the file” on the

company, he remains the only analyst that the mainstream media will amplify to the masses.

It is rare that a public counterpoint to his analysis, except for Bill Ackman, is made available. This despite

what I believe to be many misleading statements Ramey has made in the past and the above analysis of

raw data telling a very different story than the one the company and Mr. Ramey would like you to

believe. When a sell side analyst is recommending the stock in says in his disclosure that he is actually an

Herbalife distributor as well, don't you think the media should have the responsibility of assigning a

counterpoint to his statements? How about at least putting this on the screen before Ramey speaks:

(source: Pivotal Research note on Herbalife from January 2017)

If given a platform, a counterpoint to Ramey may want to point out the extremely inconvenient following

facts to him:

• The company’s fundamentals are deteriorating

• The SEC has now opened an investigation into the company for potential FCPA violations in its

biggest market, China

P a g e | 25

3/8/17 – Herbalife: A Devastatingly Perfect Storm that Could Send Shares Under $30

www.quoththeravenresearch.com | Twitter: @QTRResearch | e-mail: [email protected]

Please make sure to read the accompanying disclaimer on the second page of this report.

QTR holds a short position in Herbalife (HLF) through options and stands to benefit if the price

of Herbalife stock moves lower.

• The company has now taken on more leverage, putting more weight on the performance of the

business as a necessity for continued growth and solvency

• The FTC's sanctions kick into effect in just two months

• Bill Stiritz has reduced his stake in the company

• A worldwide global release of what I believe to be a devastating documentary is going to occur in

just two weeks

A bet on the company here is a bet that Carl Icahn and other large shareholders are going to sit around

and wait to see what will happen. That’s a bet that I believe long investors will lose.