hedging with plastics futures - the voice of the flexible ... · formally established in 1877 but...

TRANSCRIPT

Hedging with Plastics FuturesHedging with Plastics Futures

Your means to counter price volatilityYour means to counter price volatility

James YongHead of LME Plastics

Natexis Commodity Markets LimitedA Ring Dealing Member of the London Metal Exchange

Authorised and Regulated by The Financial Services Authority

Established in 1976LME Ring Dealing Member since 197810 major languages spoken fluently (English, Spanish, French, Chinese (Mandarin & Cantonese), Italian, German, Swedish, Japanese, Russian & Arabic)

Wholly owned subsidiary of Natexis Banques Populaires (NBP), one of France’s leading commercial banks with net assets >€4.0 billionNBP has Long Term Credit Ratings of A+; A+ and Aa3 from Standard & Poors, Fitch and Moody’s respectively (as at 30 June 2004)

Natexis Commodity Markets Limited

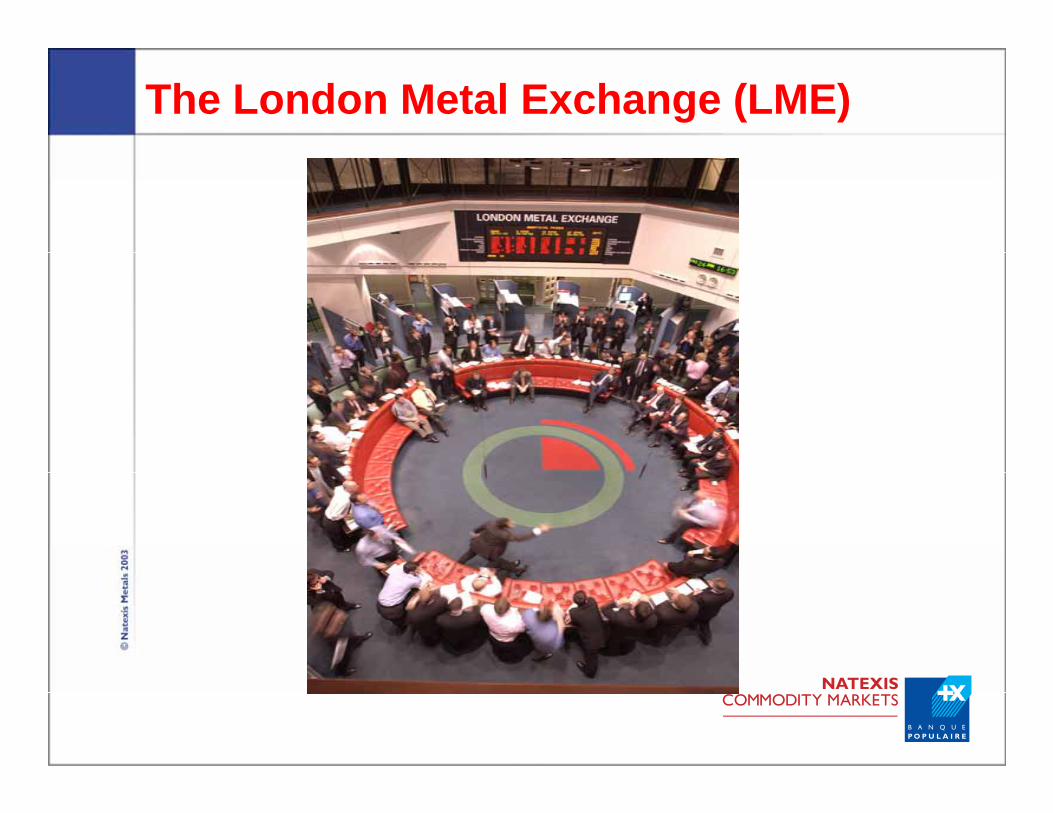

The London Metal Exchange (LME)

Formally established in 1877 but can trace origins to 1571World’s premier non-ferrous metals market with highly liquid contracts in Aluminium, Copper, Lead, Nickel, Tin & ZincLaunching 2 plastics futures contracts (polypropylene & polyethylene) in May 2005LME turnover on the market in excess of $2,500 billion per annumTrading by a combination of open out-cry (the Ring), inter-office telephone and electronic platform (LME Select)

The London Metal Exchange

The London Metal Exchange

24

12

618

2

4

8

1014

16

20

22

1700 - 0700

1510 - 1700

1315 - 15101145 - 1315

0700 - 1145

Late MarketInter Office

RD: ABC: AB

KEY:RD = Ring Dealer

ABC = Associate Broker Clearing

AB = Associate Broker

Ring and KerbTrading: RDInter Office

RD: ABC: AB

Kerb Trading: RD

Inter OfficeRD: ABC: AB

Ring Trading: RDInter Office

RD: ABC: AB

Pre-MarketInter OfficeRD: ABC:

AB

Trading hours (London time)

The London Metal Exchange

LME conducts an orderly market by means of:

The fora (open out-cry in the Ring, inter-office telephone and electronic platform (LME Select))

Transparency – publishing of prices, quotes, etcTrading rulesStandardised contractsApproved brands and warehousesOversight of operations and compliance

The London Metal Exchange

Trading mechanics:

Orders from hedgers, speculators & arbitrageurs placed with brokersBrokers are the customer’s counterparty and assume the credit risk on the customerBrokers can aggregate and match-off ordersRing trading occurs only between Ring Dealing MembersCustomers remain anonymous at all times to the market

Substantial price volatility of raw materialsMajor swings in product demandEver-increasing demand for fixed prices from end usersNo ability to hedge or manage prices and margins

Key issues facing the polymer industry?

A reliable & transparent pricing mechanismPrice risk management simply achieved so benefiting cash flow and earningsRemoves need to manage price risk through inventories and frees-up working capitalAvailable to producers and consumers alikeYour competitors will use them

Why use futures in your business?

Contract to buy or sell a standard quantity of a specified asset at a fixed future date at a price agreed today

Enables you to buy at today’s price but take delivery in the future

Enables you to sell at today’s price but make delivery in the future

Futures contracts – key features

Enforceable legal contracts, but….…. can be closed-out in the marketContract amounts are standardised and the underlying asset clearly specifiedSeries of pre-determined future delivery datesTraded on margin (a fully refundable upfront “good faith” deposit)

Some other features of futures contracts

Tailor your buying and selling to suit your business requirements

Economical use of cash resources

Use futures to get price predictability and protect margins

Cover potential shortfalls in deliveries or sell excess production to the market

Opportunities arising

A futures trade to compensate for a possible adverse price change in the ‘physical’ commodity

Use futures to ‘lock in’ a specific physical price for a pre-determined period of time

Hedge transaction can be closed-out when required

In other words, it’s insurance

So what is hedging?

You have a stock of PE Widgets; a customer will buy 1000 from you in June 2005 and pay the market price then. Widget futures are in lots of 100Your manufacturing cost is $25 per widgetThe market price has ranged from $30-50 recently and is currently $45You want to fix your gross margin now. If there’s no widget futures market this is not possibleLock-in the price now by selling 10 of the June ’05 futures contracts at $45

The basics of a hedge transaction

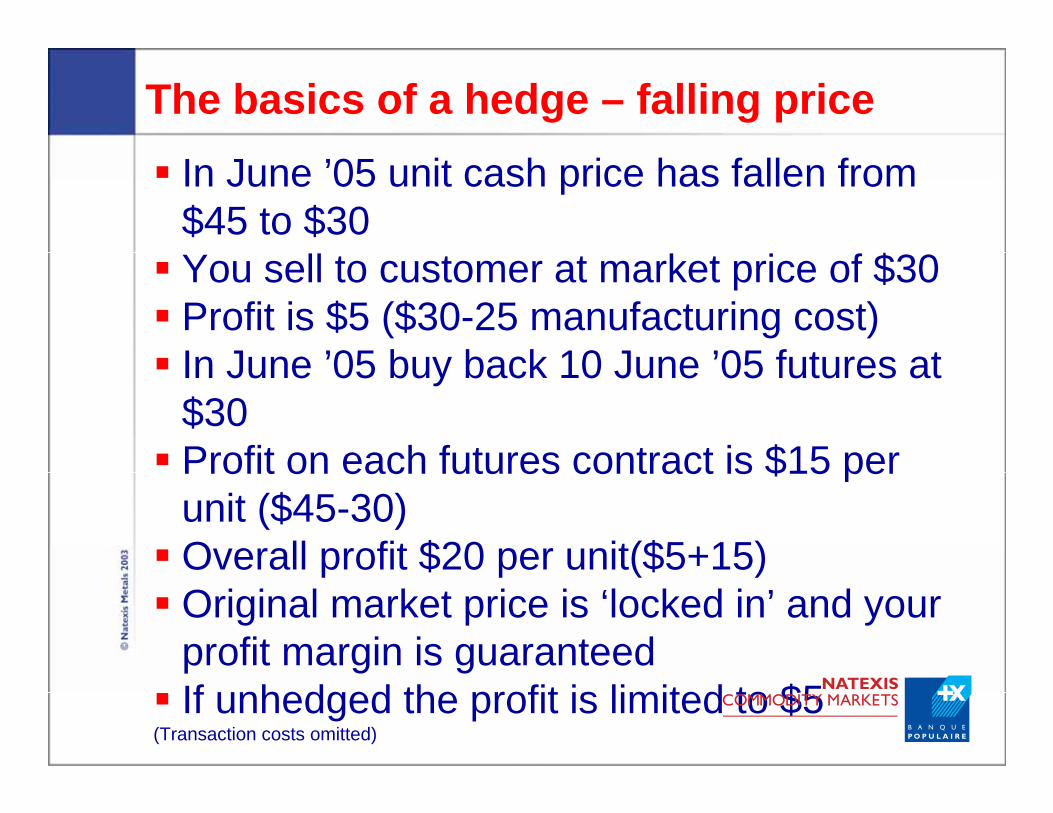

In June ’05 unit cash price has fallen from $45 to $30You sell to customer at market price of $30 Profit is $5 ($30-25 manufacturing cost)In June ’05 buy back 10 June ’05 futures at $30Profit on each futures contract is $15 per unit ($45-30)Overall profit $20 per unit($5+15)Original market price is ‘locked in’ and your profit margin is guaranteedIf unhedged the profit is limited to $5

(Transaction costs omitted)

The basics of a hedge – falling price

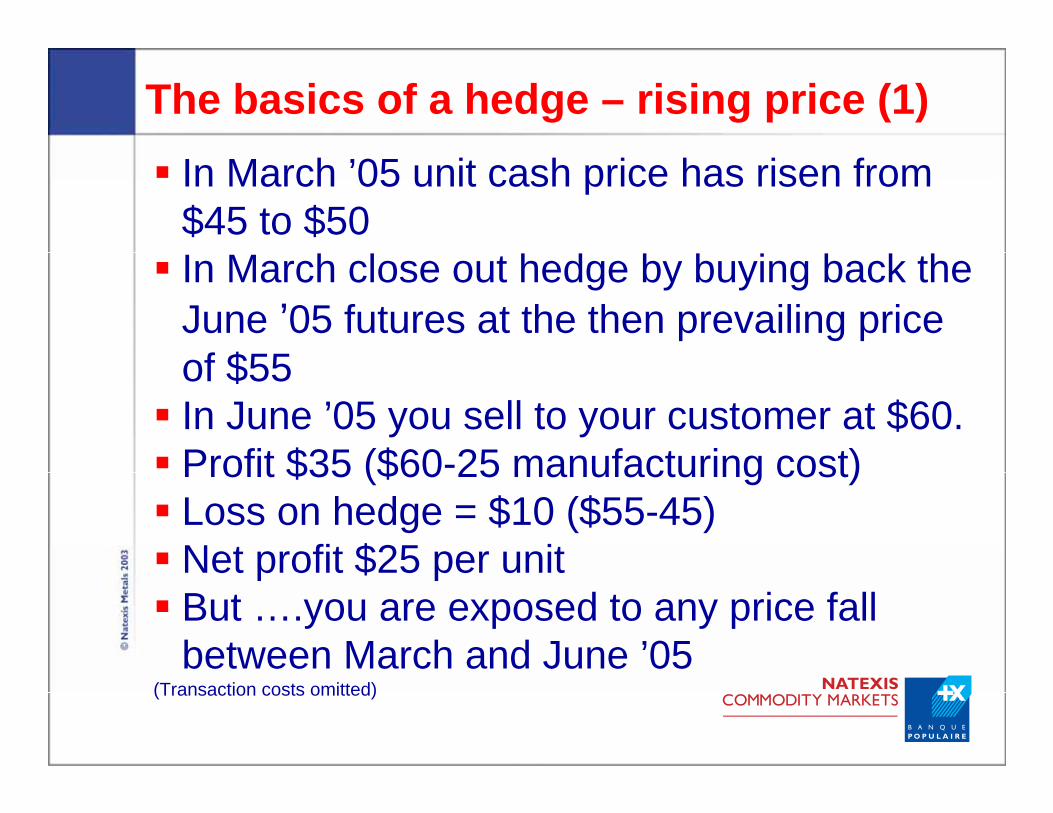

In March ’05 unit cash price has risen from $45 to $50In March close out hedge by buying back the June ’05 futures at the then prevailing price of $55In June ’05 you sell to your customer at $60.Profit $35 ($60-25 manufacturing cost)Loss on hedge = $10 ($55-45)Net profit $25 per unitBut ….you are exposed to any price fall between March and June ’05

(Transaction costs omitted)

The basics of a hedge – rising price (1)

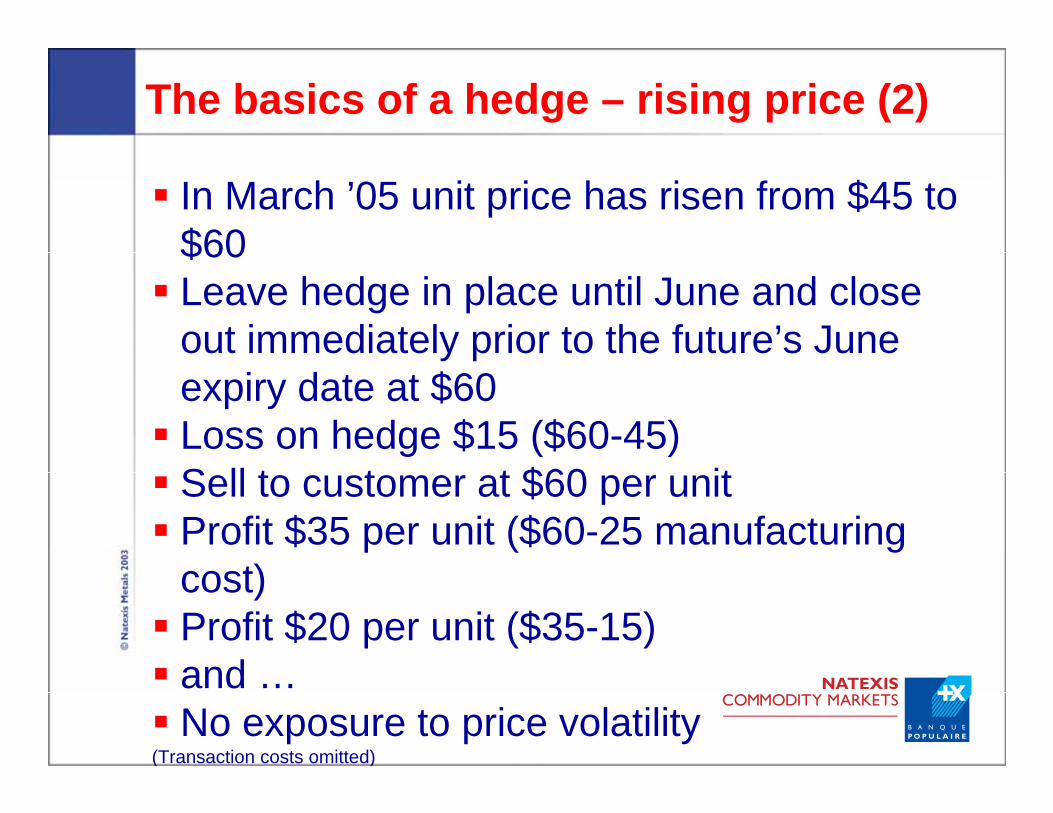

In March ’05 unit price has risen from $45 to $60Leave hedge in place until June and close out immediately prior to the future’s June expiry date at $60Loss on hedge $15 ($60-45)Sell to customer at $60 per unitProfit $35 per unit ($60-25 manufacturing cost)Profit $20 per unit ($35-15)and …No exposure to price volatility

(Transaction costs omitted)

The basics of a hedge – rising price (2)

If product price looks likely to fall you can lock-in a specific price for a specific delivery dateIf, against expectations, the price rises you can either….…. stick with locked-in price, or…. close-out the hedge to benefit from the higher price but ….You leave yourself open to an element of price riskHedging reduces or removes price risk

Opportunities & Implications

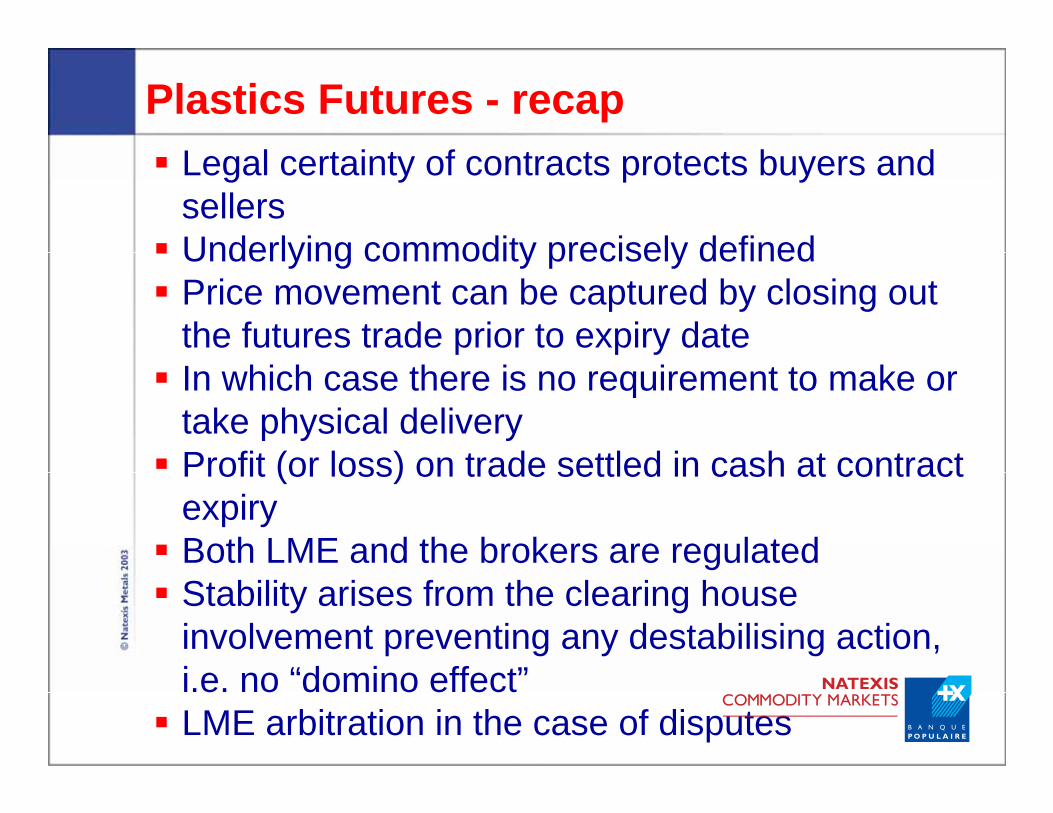

Legal certainty of contracts protects buyers and sellersUnderlying commodity precisely definedPrice movement can be captured by closing out the futures trade prior to expiry dateIn which case there is no requirement to make or take physical deliveryProfit (or loss) on trade settled in cash at contract expiryBoth LME and the brokers are regulatedStability arises from the clearing house involvement preventing any destabilising action, i.e. no “domino effect”LME arbitration in the case of disputes

Plastics Futures - recap

Initial Margin - a fully refundable upfront ‘good faith’ deposit required to secure the performance of the contractInitial Margin is deposited with the brokerInitial Margin is determined by the London Clearing House and is based on a mathematical calculationVariation Margin - derived from the daily marked-to-market valuation of your positionRequirement to pay negative Variation Margin, i.e. if a position moves against youCredit lines for Initial &/or Variation Margin may be available from the broker

Initial and Variation Margin

PP or PE futures contracts can function as proxies if your hedging requirement arises from other grades of PP or PEThere must be a good correlation in the price of your required grade and the LME’s PP or PEThe hedge may not be as precise as the exact grades of PP or PE but ….What other straightforward alternative is there?

Hedging of grades other than LME PE or PP

Physical spot and futures prices move broadly in line, but can differIn a liquid market with no unusual supply or stock constraints the futures’ price will stand at a premium to the cash priceThe premium reflects saving of interest, storage and insurance costs until the future’s expiry date (vis-à-vis purchasing the physical)

Future & spot prices converge as the future’s expiry date approaches

Futures and Physical price correlation

Assumptions: -PE spot price is $1000/mt; each futures contract is for 24.75 tonnes; interest rate is 5% pa; storage and insurance costs (per 24.75 tonnes)

are $2 per day and there are 35 days until expiry of the contractInterest saving is $120.31 (35/360ths x 5% x $1,000 x

24.75)

Storage & insurance costs are $70 (US$2 x 35 days)

Total $190.31 per contract (24.75 metric tonnes)

Equates to $7.69 per tonneFutures price therefore $1007.69 per tonne

Example of Futures premium calculation

2 methods normally seen in the metals market and expected to be replicated for plastics futuresCommission - a percentage per tonne charged on both the opening and closing transactions, orA mark-up/down - a widening (or narrowing) of the market bid/offer prices by a pre-agreed amount (i.e. if the market price is $1005/1010 and the agreed mark-up is $1 the prices applied would be $1004/1011)

Other arrangements may be made by negotiation for large volume trading activity

Hedging commissions & charges

Key risk - adverse variation in the price of the raw materialAim - avoid the effect of PE price risesStrategy - lock in successive monthly requirements by buying futures contracts with matching expiry monthsEither... take delivery via futures contract, or...take the profit (or loss) on the futures transaction and buy at spot price through your usual supplier

Hedging by plastics converter – key issues

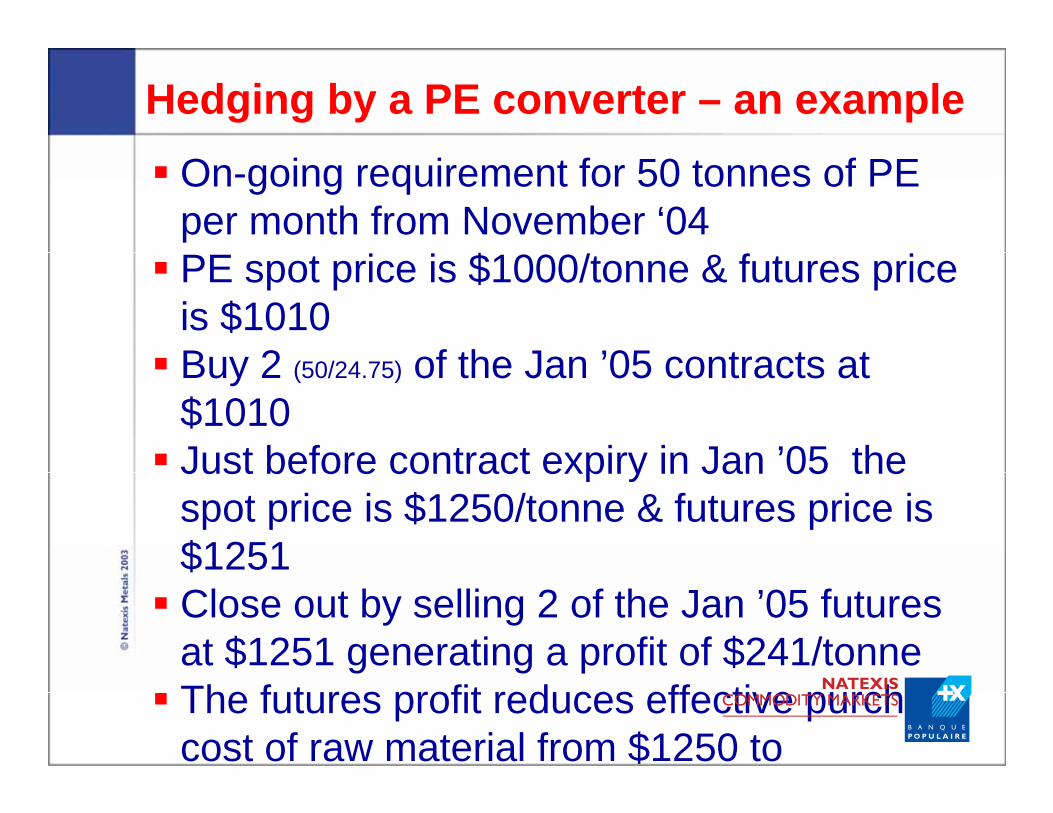

On-going requirement for 50 tonnes of PE per month from November ‘04PE spot price is $1000/tonne & futures price is $1010Buy 2 (50/24.75) of the Jan ’05 contracts at $1010Just before contract expiry in Jan ’05 the spot price is $1250/tonne & futures price is $1251Close out by selling 2 of the Jan ’05 futures at $1251 generating a profit of $241/tonneThe futures profit reduces effective purchase cost of raw material from $1250 to

Hedging by a PE converter – an example

Key risk - adverse variations in the price of the raw materialAim - to secure predictable, profitable selling prices to customersStrategy - lock in forward revenue by selling plastics futures for successive delivery monthsSell production to customers at market pricesClose out futures trades immediately prior to futures contracts expiry date

Hedging by a resin producer – key issues

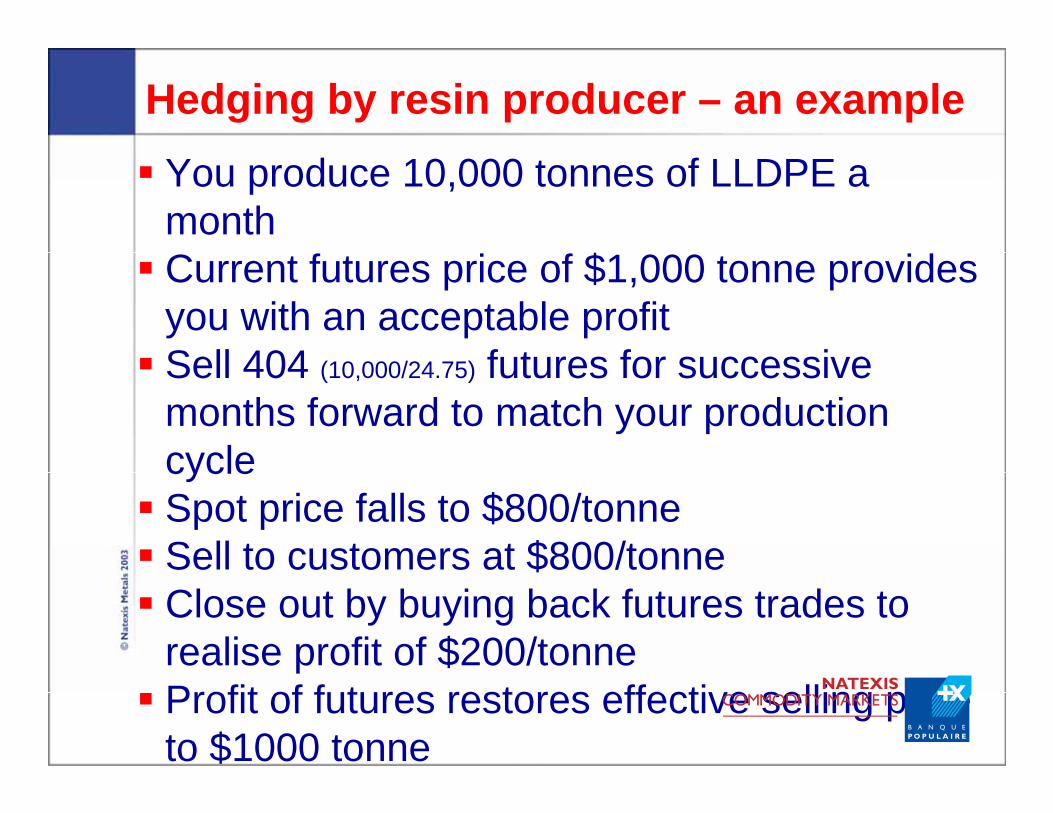

You produce 10,000 tonnes of LLDPE a monthCurrent futures price of $1,000 tonne provides you with an acceptable profitSell 404 (10,000/24.75) futures for successive months forward to match your production cycle Spot price falls to $800/tonneSell to customers at $800/tonne Close out by buying back futures trades to realise profit of $200/tonneProfit of futures restores effective selling price to $1000 tonne

Hedging by resin producer – an example

Cash employed in hedge is the Initial Margin multiplied by the number of contracts openVariation Margin must be paid if future’s price goes the wrong wayBut …credit facilities for Initial &/or Variation Margin may be available from your brokerFutures contracts are in multiples of 24.75 tonnesContracts are denominated in US Dollars, but can be settled in Euros, Pounds Sterling or Japanese Yen

Common issues

Open an account well in advance of the contracts’ launch date of 27th May 2005Contact Natexis Commodity Markets for a discussion on how hedging can help your businessFocus on the key strategies you may want to employArrange for a Natexis Commodity Markets presentation to your key personnel

Next Steps

Natexis Commodity Markets Limited

Mansion Court47-53 Cannon StreetLondon EC4M 5SH

Tel: +44 (0) 20 7648 4950Fax: +44 (0) 20 7248 5262

Email: [email protected]: www.natexiscm.com

Contact