hedgeye restaurants mcd, sbux, dnkn, coffee & the...

TRANSCRIPT

HEDGEYE

RESTAURANTS

MCD, SBUX, DNKN, COFFEE & THE CONSUMER IN 2014

NOVEMBER 12, 2013

HEDGEYE 2 DATA SOURCE

DISCLAIMER Hedgeye Risk Management is a registered investment advisor, registered with the State of Connecticut. Hedgeye

Risk Management is not a broker dealer and does not make investment recommendations. This research does not

constitute an offer to sell, or a solicitation of an offer to buy any security. This research is presented without regard

to individual investment preferences or risk parameters; it is general information and does not constitute specific

investment advice. This presentation is based on information from sources believed to be reliable. Hedgeye Risk

Management is not responsible for errors, inaccuracies or omissions of information. The opinions and conclusions

contained in this report are those of Hedgeye Risk Management, and are intended solely for the use of Hedgeye

Risk Management’s clients and subscribers. In reaching these opinions and conclusions, Hedgeye Risk

Management and its employees have relied upon research conducted by Hedgeye Risk Management’s employees,

which is based upon sources considered credible and reliable within the industry. Hedgeye Risk Management is not

responsible for the validity or authenticity of the information upon which it has relied.

TERMS OF USE This report is intended solely for the use of its recipient. Re-distribution or republication of this report and its

contents are prohibited. For more detail please refer to the appropriate sections of the Hedgeye Services

Agreement and the Terms of Use at www.hedgeye.com

DISCLAIMER

HEDGEYE 3 DATA SOURCE

KEY POINTS

1 GOING AFTER THE COFFEE CONSUMER IN 2014 MCD will make an aggressive push to sell more coffee next year

This may be one of management’s pillars for growth in 2014

2

3

MCCAFE IS A STRONG, PROVEN BRAND Strong national presence and brand awareness

Solid base of core, loyal customers

DRIVING INCREMENTAL COFFEE SALES? An attempt to drive incremental coffee sales may exacerbate service issues

Under this scenario, the core business would likely continue to deteriorate

MCDONALD’S OVERVIEW MCDONALD’S OVERVIEW

HEDGEYE 5 DATA SOURCE

MCDONALD'S OVERVIEW

HEDGEYE 6 DATA SOURCE

2014 ANALYST DAY

HERE’S WHAT WE EXPECT MCDONALD’S TO HIGHLIGHT DURING ITS

ANALYST DAY ON THURSDAY: PUT PEOPLE FIRST - The rise of fast casual suggests there is more competition for hiring. We believe

MCD will refocus their efforts on hiring and retaining the best employees, in an effort to create a better

experience for consumers.

GET IT RIGHT - Along the same lines, we believe MCD plans to emphasize a stronger service platform.

This will require McDonald’s stores to be clean, the crew to be hospitable, and the service to be quick and

accurate.

IMPROVE DRIVE-THRU AND LUNCH - This is vital to the future success of McDonald’s. We believe MCD’s

core lunch business has been declining since 2010, which has been masked by the company’s successful

efforts to sell cold beverages. QSR Magazine recently reported that MCD’s average speed of service was

the slowest in 15 years.

INCREASE COFFEE-DRIVEN BUSINESS - We believe McDonald’s plans to introduce its best practices

from the Canada division into the US, in an effort to go after the coffee consumer in 2014. This strategy

includes selling coffee beans in supermarkets and pairing food with coffee. This will further validate our belief

that McDonald’s is chasing Starbuck’s success.

1

2

3

4

HEDGEYE 7 DATA SOURCE

OBSESSED WITH SBUX, FEAR DNKN?

• The focus of our thesis on MCD is

centered on what we like to call the

company’s “obsession with Starbucks.”

This obsession dates back to 2009, when

McDonald’s used the tag line “four bucks

is dumb,” in what was a clear attempt to

take market share from Starbucks.

• Around the same time, McDonald’s

remodel program began to emulate

Starbucks to a degree, in a failed attempt

to foster a “café” or “third place”

environment.

• We believe McDonald’s plans to reallocate

resources and double down on selling

more coffee in 2014. McDonald’s Remodel Starbucks Café

HEDGEYE 8 DATA SOURCE

OBSESSED WITH SBUX, FEAR DNKN?

SBUX remains

superior, while

DNKN has

separated itself

from MCD over

the past five

quarters.

HEDGEYE 9 DATA SOURCE

OBSESSED WITH SBUX, FEAR DNKN?

MCD’s 2-year

comps have

fallen off a cliff

since 1Q12.

SBUX and DNKN

remain strong.

HEDGEYE 10 DATA SOURCE

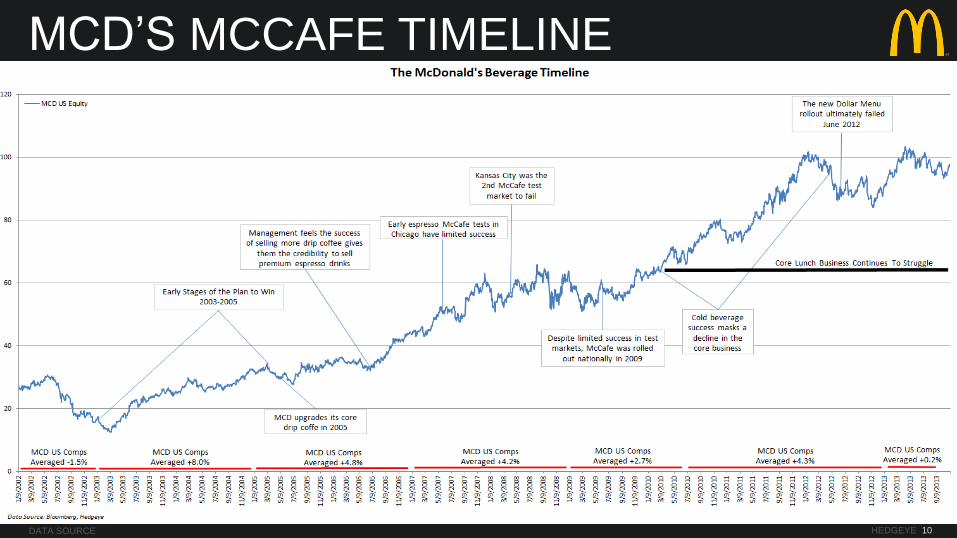

MCD’S MCCAFE TIMELINE

HEDGEYE 11 DATA SOURCE

THIS STRATEGY FAILED IN 2009

ESPRESSO BASED STRATEGY

In 2014, we

believe MCD plans

to reallocate

resources toward

taking market

share in coffee.

MCD began

focusing on

McCafe in April

’09.

Sales suffered for

the balance of the

year. Data Source: Company Filings, Hedgeye

HEDGEYE 12 DATA SOURCE

DETERIORATING LUNCH BUSINESS

Frappes &

Smoothies

accounted for

more than 100%

of SSS.

The success of

cold beverages

masked a

decline in the

core lunch

business.

HEDGEYE 13 DATA SOURCE

FRAPPE & SMOOTHIE SALES WERE STRONG

DETERIORATING LUNCH BUSINESS

We believe the

success of

Frappes &

Smoothies

masked a decline

in the core lunch

business.

Data Source: Company Filings, Hedgeye

HEDGEYE 14 DATA SOURCE

TWO-YEAR TRENDS ARE UGLY

MCD’S GLOBAL WOES

Economic

conditions are

not the cause of

slowing SSS

around the globe.

McDonald’s

issues are not

limited to the

deterioration of

the core lunch

business in the

U.S.

HEDGEYE 15 DATA SOURCE

UNIMPRESSIVE RETURNS

INCREMENTAL RETURNS

MCD’s return on

incremental

invested capital

on a TTM basis

is approaching

levels not seen

since mid-2002.

HEDGEYE 16 DATA SOURCE

KEEP YOUR EYES ON THE FRIES

“I said back then that we had taken our eyes off our

fries, and we paid a price.”

“We’re simplifying our restaurant operations. We’re

using more visual menu boards to make ordering

easier for customers. We’re also eliminating some

sizes and slow-selling items and better organizing

the kitchen, front counter and drive-thru areas to

improve efficiency.”

- Jim Cantalupo, Chairman and CEO Source: 2003 Annual Report

CONSUMER SURVEY

HEDGEYE 18 DATA SOURCE

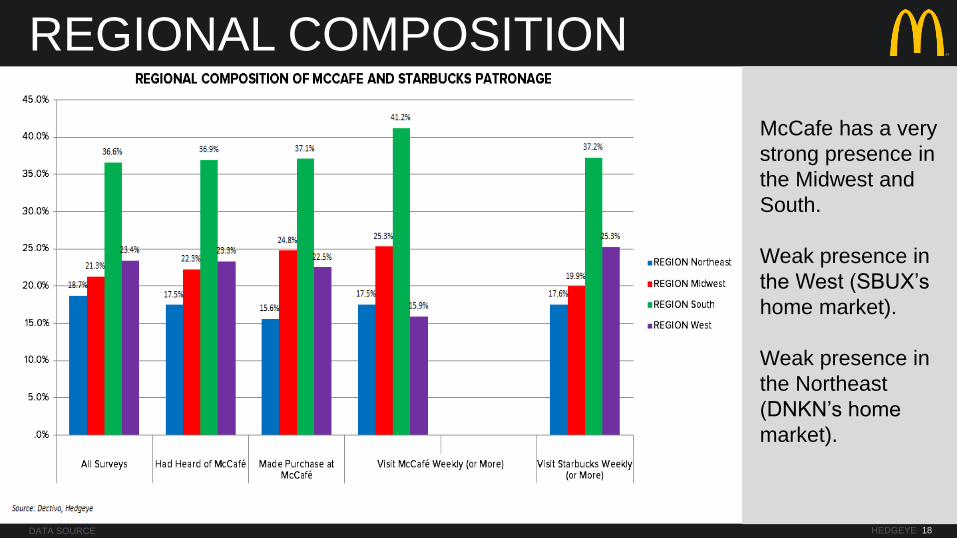

REGIONAL COMPOSITION

McCafe has a very

strong presence in

the Midwest and

South.

Weak presence in

the West (SBUX’s

home market).

Weak presence in

the Northeast

(DNKN’s home

market).

HEDGEYE 19 DATA SOURCE

URBAN SUBURBAN RURAL

McCafe patronage

outstrips SBUX

patronage in rural

areas, while

McCafe patronage

trails Starbucks

patronage in

suburban markets.

HEDGEYE 20 DATA SOURCE

INCOME DISTRIBUTION

As expected, MCD’s

core consumer base

skews toward lower

income individuals.

This makes it difficult

to upsell to premium

espresso beverages.

36.7% of McCafe

customers fall within

the < $39,999 income

cohort, as opposed to

only 29.8% of SBUX

customers.

HEDGEYE 21 DATA SOURCE

EDUCATIONAL ATTAINMENT

Overall, McCafe

consumers have a

lower level of

educational

attainment.

HEDGEYE 22 DATA SOURCE

COFFEE BRAND LOYALTY

59% of SBUX

customers make

coffee purchases at

coffee chains.

Bottom line: among

the people who

patronize McCafe

at least once a

week, 70% are still

buying their coffee

elsewhere.

HEDGEYE 23 DATA SOURCE

COFFEE RATINGS

60% of coffee

consumers like SBUX

coffee “very much.”

This is significant,

considering that the

overall quality and taste

of coffee is the number

one factor coffee

consumers look for.

High brand loyalty

among large brands in

the coffee category

make it very difficult to

take market share.

HEDGEYE 24 DATA SOURCE

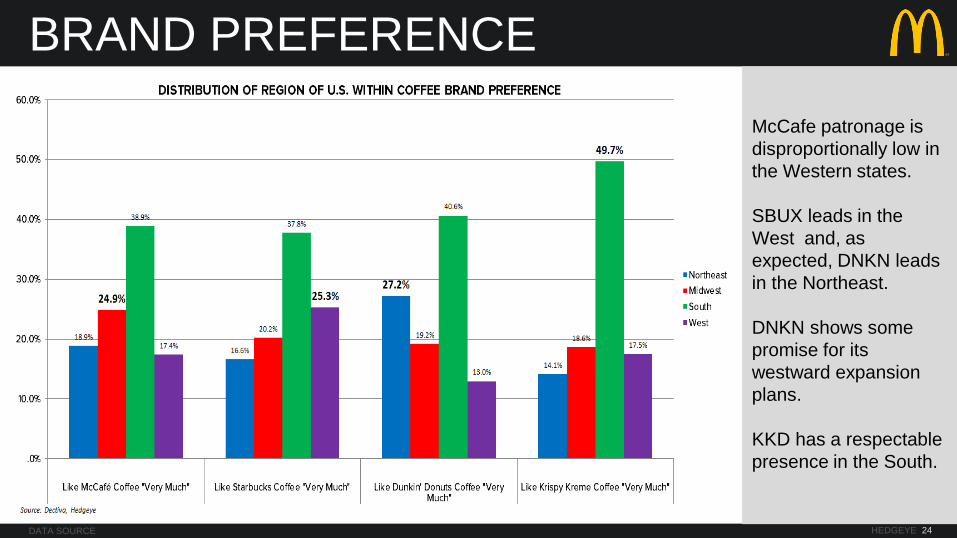

BRAND PREFERENCE

McCafe patronage is

disproportionally low in

the Western states.

SBUX leads in the

West and, as

expected, DNKN leads

in the Northeast.

DNKN shows some

promise for its

westward expansion

plans.

KKD has a respectable

presence in the South.

HEDGEYE 25 DATA SOURCE

BRAND PREFERENCE

Nothing earth-

shattering here.

KKD does resonate

particularly well with

the younger cohorts.

HEDGEYE 26 DATA SOURCE

BRAND PREFERENCE

Housewives and

retirees show up in

disproportionately high

numbers among

McCafe regulars.

When we include ‘like

somewhat,” men are

slightly more likely than

women to be regular

(weekly) customers of

McCafe (in contrast to

SBUX).

HEDGEYE 27 DATA SOURCE

BRAND PREFERENCE

Regular consumers of

specialty coffee drinks

have markedly higher

median income than

the overall sample

mean ($62,500 vs.

$45,000).

Frequent McCafe

customers are slightly

less wealthy than

Starbucks customers.

It would make very little

sense for MCD to

enhance their efforts to

penetrate the specialty

coffee category.

HEDGEYE 28 DATA SOURCE

BRAND PREFERENCE

Starbucks attracts a

higher proportion of

college graduates

among its weekly

clientele than

McCafe.

HEDGEYE 29 DATA SOURCE

DEMAND DRIVERS: ALL CUSTOMERS

• Quality & Overall

Taste of Coffee is

the most important

factor for coffee

customers.

• Cleanliness,

selection of coffee

drinks available,

quality and overall

taste of food, and

the friendliness of

baristas/staff round

out the top 5 most

important factors

for coffee

consumers.

Data Source: Dectiva, Hedgeye

HEDGEYE 30 DATA SOURCE

DEMAND DRIVERS: MCCAFE

• McCafe customers

value a large

selection of coffee

drinks available.

• We think this

presents an issue

for MCD. In our

opinion, any

attempt to expand

the coffee menu

will add complexity

to the back of

house operations.

Data Source: Dectiva, Hedgeye

HEDGEYE 31 DATA SOURCE

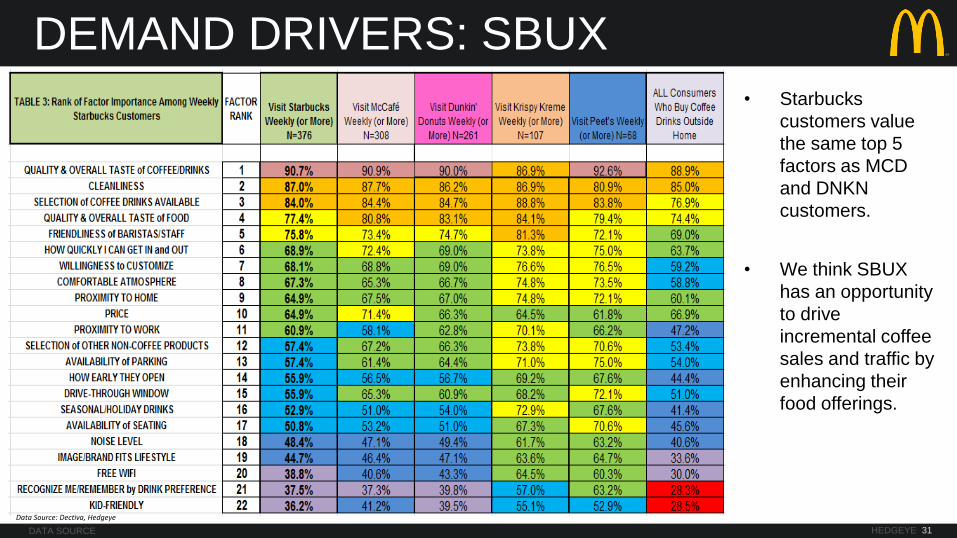

DEMAND DRIVERS: SBUX

• Starbucks

customers value

the same top 5

factors as MCD

and DNKN

customers.

• We think SBUX

has an opportunity

to drive

incremental coffee

sales and traffic by

enhancing their

food offerings.

Data Source: Dectiva, Hedgeye

HEDGEYE 32 DATA SOURCE

DEMAND DRIVERS: DNKN

• DNKN customers

value the same top

5 factors as MCD

and SBUX

customers.

• Surprisingly, price

is well down the list

of most important

factors Dunkin

Donut’s customers

value.

Data Source: Dectiva, Hedgeye

HEDGEYE 33 DATA SOURCE

DEMAND DRIVERS: KKD

• Price is not an

issue for Krispy

Kreme customers.

• What they do favor

is a large selection

of coffee drinks

available.

• We think KKD has

an opportunity to

build upon this, by

offering a larger

selection of coffee

drinks, at a higher

price point.

Data Source: Dectiva, Hedgeye

HEDGEYE 34 DATA SOURCE

DEMAND DIFFERENTIATORS

• McCafe customers value price more

than customization.

• The majority of other customers

value customization more than price.

• MCD’s strategy to take market share

by offering a lower price point will not

work.

• MCD can not match the level of

customization that these other

chains offer.

Data Source: Dectiva, Hedgeye

HEDGEYE 35 DATA SOURCE

KEY HIGHLIGHTS

• Younger individuals, particularly those

with full-time jobs, are the most likely to

purchase coffee-based drinks and to

consume specialty coffee beverages.

Both activities peak in the age group of

25-44.

• Regular consumers of specialty coffee

drinks have markedly higher median

incomes than the overall sample

median ($62,500 vs. $45,000).

• 85% of those surveyed were familiar

with the McCafe name, but only 48%

had made a purchase at a McCafe

location.

HEDGEYE 36 DATA SOURCE

KEY HIGHLIGHTS

• Men are slightly more likely than

women to be regular (weekly)

customers of McCafe (vice versa for

SBUX).

• McCafe’s regular (weekly) customers

skew slightly older than SBUX.

HEDGEYE 37 DATA SOURCE

KEY HIGHLIGHTS

• Frequent McCafe customers

are less wealthy than SBUX

customers (mean incomes:

$58,000 vs. $63,000).

• SBUX attracts a higher

proportion of college graduates

than McCafe among its regular

weekly clientele (44% vs. 36%).

• McCafe patronage is

disproportionately low in the

Western United States.

HEDGEYE 38 DATA SOURCE

KEY HIGHLIGHTS

• McCafe customers are more fickle in

their choice of coffee retailers:

McCafe regulars purchase just 30%

of their coffee-based drinks at fast

food outlets, while SBUX regulars

make 60% of their coffee purchases

at shops that specialize in coffee.

• McCafe customers are more price-

conscious than the average retail

coffee consumer: 32% of McCafe

regulars said that cost was an

“essential” factor in their choice of

coffee retailers.

HEDGEYE 39 DATA SOURCE

LACK OF LOYALTY

• Even among folks who patronize

McCafe at least once a week, they’re

still buying the majority (70%) of their

coffee somewhere else. This means

two things: 1. McCafe customers are not all that loyal.

2. There is an opportunity for MCD to

improve upon this… but, it will come at

the expense of their core business.

HEDGEYE 40 DATA SOURCE

OPERATIONAL ISSUES

• McDonald’s has a number of

operational issues that are irritating

franchisees and turning off consumers.

• To make matters worse, new items are

not resonating with customers.

• The competition in the QSR space has

regrouped and MCD is standing still.

• The menu is too large and too

complex, to efficiently service

customers:

• The Drive-Thru Performance

Study, recently reported that

McDonald’s experienced its

slowest average speed of

service in the history of the 15-

year old study, at 189.49

seconds (QSR Magazine).

HEDGEYE 41 DATA SOURCE

CONCLUSION

In our opinion, MCD needs to readjust its basic store operations.

It is a food destination first and a beverage destination second. • By going after the coffee consumer in 2014, management will only

exacerbate the problems they are currently dealing with.

The coffee category is a crowded space, with dominant players. • In order for MCD’s strategy to pay off in 2014, they will need to “steal”

market share from both SBUX and DNKN.

• Considering the loyal customer base of these two brands, this is

highly unlikely.

1

2

3

HEDGEYE 42 DATA SOURCE

CONCLUSION

In addition to the current competition in the coffee space, smaller brands

such as Krispy Kreme and Peet’s are beginning to penetrate the market.

• This only amplifies the competitive environment.

Fast Casual hamburger chains (Smashburger, etc.) are eroding core lunch.

MCD needs to get “back to the basics.”

• Focus on attracting Millennials by serving fresh, prepared food.

• MCD is losing its relevance in the QSR space.

In 2014, an over-allocation of resources (marketing, etc.) to the coffee

strategy will continue to put undue stress on the core business.

4

5

6

7

HEDGEYE 43 DATA SOURCE

NEW FORMAT CHANGES BEHAVIOR

OLD FORMAT = $800/SQUARE FT NEW FORMAT = $1,300 SQ FT

Insert image

BACK TO THE BASICS

THIS IS WHAT THEY PLAN TO DO They’re targeting coffee consumers at the expense

of their core business. McCafe is already a strong

brand and we believe that the potential upside is

limited.

THIS IS WHAT THEY NEED TO DO They need to get “back to the basics” of serving fresh,

prepared food. At its core, MCD is a food destination.

They must develop a simple, easy-to-operate menu &

produce innovative items that resonate with today’s

consumers.

APPENDIX

HEDGEYE 45 DATA SOURCE

METHODOLOGY AND AUDIENCE

STATISTICALLY SOUND METHODOLOY TARGETTING 1,000 RELEVANT

CONSUMERS ACROSS A VAST DEMOGRAPHIC CROSS SECTION.

HEDGEYE 46 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 47 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 48 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 49 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 50 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 51 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 52 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 53 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 54 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE 55 DATA SOURCE

METHODOLOGY AND AUDIENCE

HEDGEYE

RESTAURANTS

MCD, SBUX, DNKN, COFFEE & THE CONSUMER IN 2014

NOVEMBER 12, 2013