health insurance: what it actually does -...

TRANSCRIPT

Health Insurance: What it Actually Does

Andrew FriedsonAssistant Professor of EconomicsUniversity of Colorado Denver

DABE LuncheonNovember 15, 2017

Health Insurance

Health Insurance is a big deal in the United States at the moment

2

80

82

84

86

88

90

92

2008 2009 2010 2011 2012 2013 2014 2015 2016

Percent of U.S. Population with Any Health Insurance (U.S. Census Bureau ‐ ACS)

We have just gone through a period of historic change in the U.S. health insurance market

The goal of this talk is to orient you to the big concepts needed to understand where we are going and why

A Brief History of Health Insurance in the U.S.

Around 1900 there was no such thing as health insurance – hospitals were places you went to die if you were poor

Soon after hospital care began to change and become much more effective – but care was incredibly expensive

Late 1920’s/Start of the Great Depression Baylor University Hospital and Blue Cross was the first true health insurance

3

A Brief History of Health Insurance

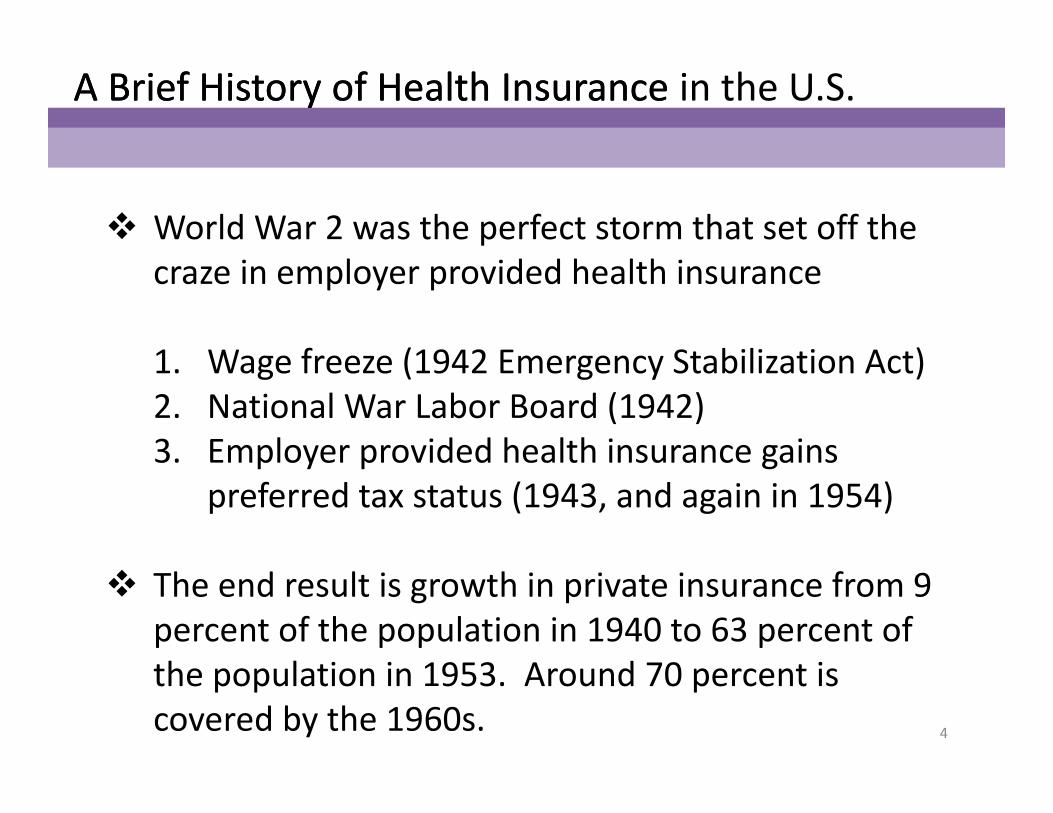

World War 2 was the perfect storm that set off the craze in employer provided health insurance

1. Wage freeze (1942 Emergency Stabilization Act)2. National War Labor Board (1942)3. Employer provided health insurance gains

preferred tax status (1943, and again in 1954)

The end result is growth in private insurance from 9 percent of the population in 1940 to 63 percent of the population in 1953. Around 70 percent is covered by the 1960s. 4

A Brief History of Health Insurance in the U.S.

A Brief History of Health Insurance

By the end of the war, the U.S. had a well developed private health insurance sector

Contrast this with the British Experience: wages were not capped, but the cost of living was kept in check by rationing and price controls on food.

At the end of the war, health insurance was almost completely absent from the U.K., and in 1946 the National Health Service was started with little private pushback.

5

A Brief History of Health Insurance in the U.S.

A Brief History of Health Insurance

The U.S. is very much an anomaly in world health insurance systems. Most countries rolled out a public health insurance system into a world with little private market

The U.S. had a private health insurance market develop early, and has to‐date provided government coverage for only select subpopulations: i.e. the elderly, disabled, poor, or the military

6

A Brief History of Health Insurance in the U.S.

What does Health Insurance Really Cover?

The biggest misconception about health insurance is that it is insurance for your health

To make my point – let us consider CAR insurance

7

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

8

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the damage to the car• The current value of the car

9

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the damage to the car• The current value of the car

Insurance covers the risk of loss, and restores you to “whole”

10

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the

damage to the car• The current value of the car

Insurance covers the risk of loss, and restores you to “whole”

11

Health Insurance

1. Pay a premium for an insurance policy

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the

damage to the car• The current value of the car

Insurance covers the risk of loss, and restores you to “whole”

12

Health Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you • The cost of obtaining treatment

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the

damage to the car• The current value of the car

Insurance covers the risk of loss, and restores you to “whole”

13

Health Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you • The cost of obtaining treatment

3. Also pays for routine maintenance and upgrades

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the

damage to the car• The current value of the car

Insurance covers the risk of loss, and restores you to “whole”

14

Health Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you • The cost of obtaining treatment

3. Also pays for routine maintenance and upgrades

Insurance covers the risk of loss, and other things, does not guarantee restoring you to “whole”

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the

damage to the car• The current value of the car

Insurance covers the risk of loss, and restores you to “whole”

15

Health Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you • The cost of obtaining treatment

3. Also pays for routine maintenance and upgrades

Insurance covers the risk of loss, and other things, does not guarantee restoring you to “whole”

This does not seem like good insurance for your health

What does Health Insurance Really Cover?

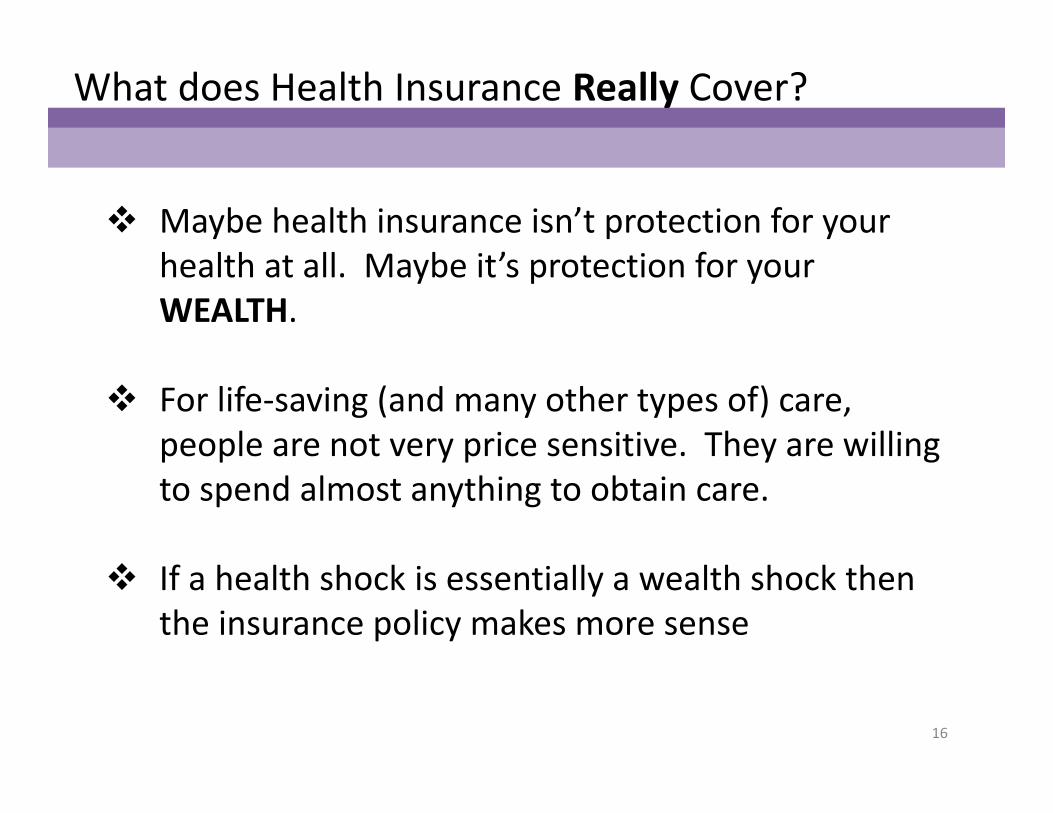

Maybe health insurance isn’t protection for your health at all. Maybe it’s protection for your WEALTH.

For life‐saving (and many other types of) care, people are not very price sensitive. They are willing to spend almost anything to obtain care.

If a health shock is essentially a wealth shock then the insurance policy makes more sense

16

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the

damage to the car• The current value of the car

Insurance covers the risk of loss, restores you to “whole”

17

Health Wealth Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you • The cost of fully repairing the

financial damage

Insurance covers the risk of loss, restores you to “whole”

What does Health Insurance Really Cover?

Car Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you the lesser of• The cost of fully repairing the

damage to the car• The current value of the car

Insurance covers the risk of loss, restores you to “whole”

18

Health Wealth Insurance

1. Pay a premium for an insurance policy

2. In the case of an adverse event insurance pays you • The cost of fully repairing the

financial damage

Insurance covers the risk of loss, restores you to “whole”

Now this looks like an insurance policy!

Health Insurance as Wealth Insurance

This concept is central to health insurance, and is often overlooked in current policy discussions. This was not always the case:

“No longer will illness crush and destroy the savings that theyhave so carefully put away over a lifetime so that they mightenjoy dignity in their later years. No longer will young families seetheir own incomes, and their own hopes, eaten away simplybecause they are carrying out their deep moral obligations totheir parents, and to their uncles, and their aunts.”

‐President Lyndon B. Johnson, remarks when signing Medicareinto law, July 30, 1965

19

Health Insurance as Wealth Insurance

For the bulk of the population health insurance is not life or death, but it’s close. We are avoiding a state of the world where you have two choices:

1. Live the rest of your life in crushing debt or poverty

Or

2. You or a loved one live in horrible agony, die, or possibly both

20

Health Insurance as Wealth Insurance

For the bulk of the population health insurance is not life or death, but it’s close.

HOWEVER, for a subset of the population, health insurance is life or death. These are the very poor, who have no resources and often no access (beyond the ER). For them insurance can be equivalent to access.

21

Evidence

These claims are not controversial within Health Economics, as they have been tested and re‐tested. The most important study was the RAND Health Insurance Experiment

• The largest Randomized Control Trial in social science history ($136 million in 1984)

• Randomly assigned health insurance plans to households

• Little to no impact on health outcomes from insurance (UNLESS you’re low income)

• Big impacts on the amount of care you use, and out of pocket spending 22

Insurance Distorts the Price Signal

The next important thing to understand about health insurance is how it impacts patients decisions with regards to health care

If we believe that medical care is a well functioning market in the absence of health insurance, then adding insurance will scramble the price signal, undermining a market’s ability to operate efficiently

The price a patient feels becomes unhooked from the cost of care, incentivizing patients to overconsume

23

Insurance Distorts the Price Signal

The price a patient feels becomes unhooked from the cost of care, incentivizing patients to overconsume

• Insurers understand this and may try to steer patients to “effective” care and away from waste

• But, as long as coverage lowers the price patients feel, there will be overconsumption

24

Insurance Distorts the Price Signal

The law of demand: lower price, people buy more

Types of ways to pay for care when you have insurance• Flat copay• Co‐insurance• Deductibles• Health Savings Account

Prices via insurance are different than prices without insurance

25

Insurance Companies

Insurers are paid premiums, and pay out claims throughout the year. So to figure out how much an insurer needs to take in:

Some patients have more expenses, some have less, but on average this is what needs to be paid in

Premiums are paid in before the coverage starts, and paid out over time, so make a profit by investing in the interim

26

Insurance Companies

This works because insurers are able to cover a large number of people and pool the risk. This is the same idea as portfolio diversification, or a central limit theorem. The more people with uncorrelated risk, the lower the variance in total payouts and money in will equal money out.

27

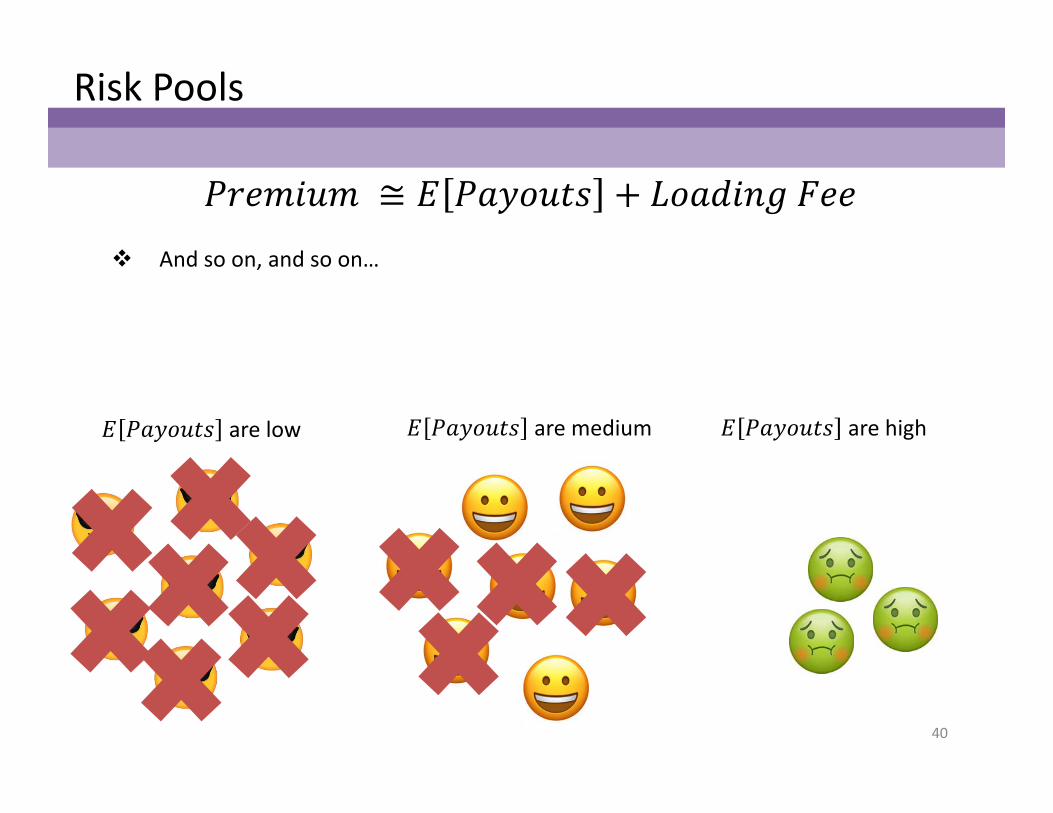

Risk Pools

BUT a problem arises when the population as a whole has different groups with different levels of risk. i.e. some groups that on average need a lot of payouts and and some groups that need very little.

Presumably the high risk group is willing to pay more for coverage than the low risk group

28

Risk Pools

29

are low are medium are high

One thing we can do is EXPERIENCE RATING and charge people based on their risk. This is what we do with car insurance.

Risk Pools

30

are EXTREMELY high

One thing we can do is EXPERIENCE RATING and charge people based on their risk. This is what we do with car insurance.

But, for a subset of the population this would be impossibly unaffordable. AND for many of these people, their conditions are no fault of their own.

For a long time we did this in the U.S. – we either denied people coverage due to “pre‐existing conditions” or made their insurance incredibly expensive. There was a class of “uninsurable” people

Risk Pools

31

are EXTREMELY high

One thing we can do is EXPERIENCE RATING and charge people based on their risk. This is what we do with car insurance.

Also, as prices have grown ‐ in part due to better and more expensive treatments covering a wider variety of diseases – the group of “uninsurable” has expanded

are still pretty darn high

Risk Pools

32

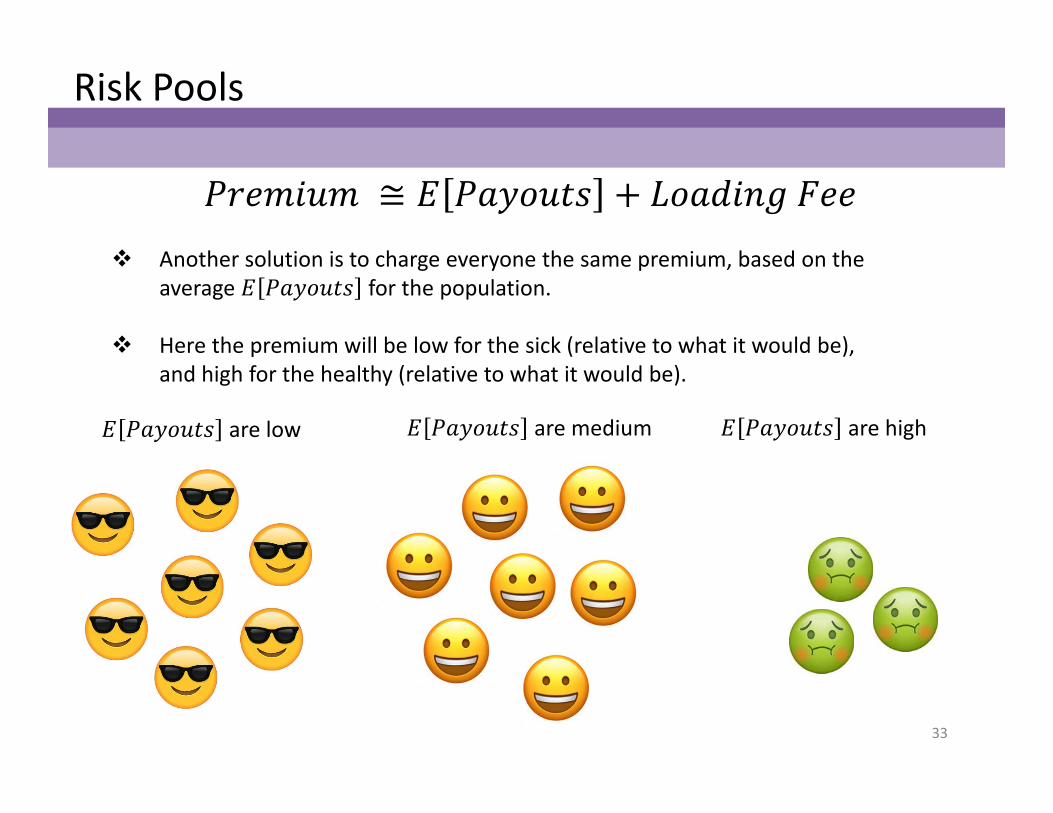

are low are medium are high

Another solution is to charge everyone the same premium, based on the average for the population.

Risk Pools

33

are low are medium are high

Another solution is to charge everyone the same premium, based on the average for the population.

Here the premium will be low for the sick (relative to what it would be), and high for the healthy (relative to what it would be).

Risk Pools

34

are low are medium are high

If for some patients (the healthiest) premium > willingness to pay then those patients will choose to go without insurance

Risk Pools

35

are low are medium are high

If for some patients (the healthiest) premium > willingness to pay then those patients will choose to go without insurance

Risk Pools

36

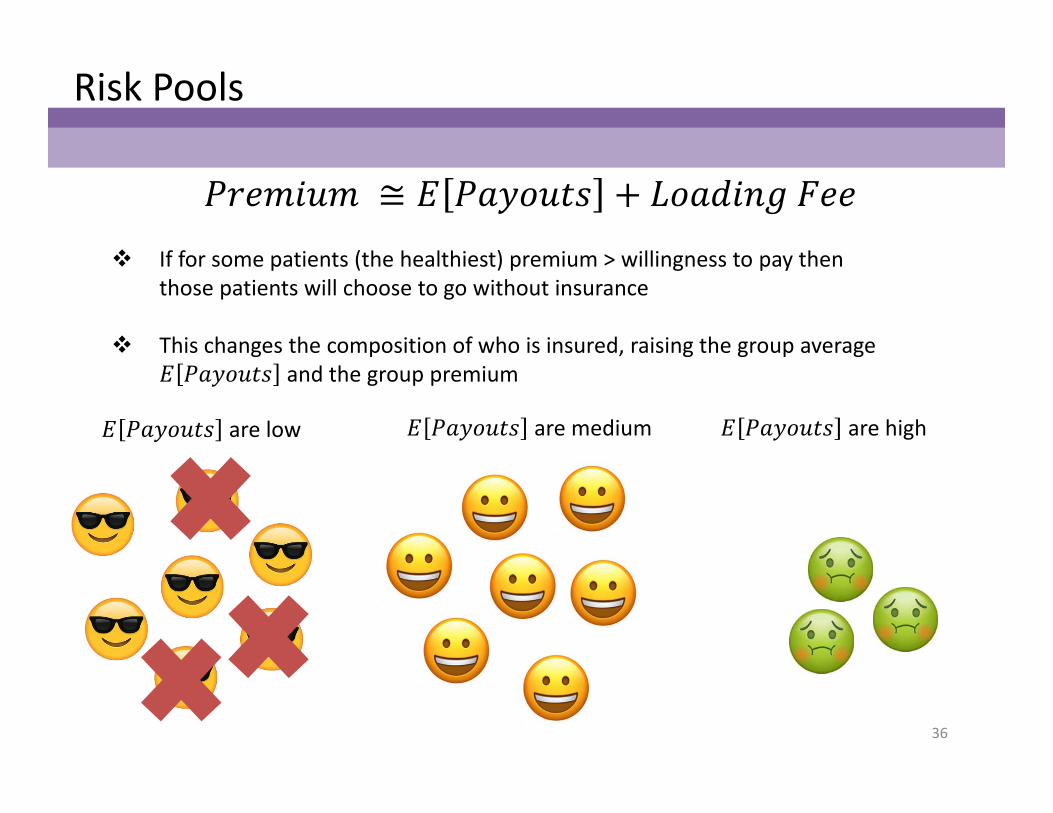

are low are medium are high

If for some patients (the healthiest) premium > willingness to pay then those patients will choose to go without insurance

This changes the composition of who is insured, raising the group average and the group premium

Risk Pools

37

are low are medium are high

At the new premium, a new group of people will find that premium > willingness to pay and choose to go without insurance

This changes the composition of who is insured, raising the group average and the group premium

Risk Pools

38

are low are medium are high

At the new premium, a new group of people will find that premium > willingness to pay and choose to go without insurance

This changes the composition of who is insured, raising the group average and the group premium

Risk Pools

39

are low are medium are high

And so on, and so on…

Risk Pools

40

are low are medium are high

And so on, and so on…

Risk Pools

41

are low are medium are high

And so on, and so on…until only the riskiest people are left in the market. And they face the same incredibly high premiums as under experience rating!

This is referred to as an “adverse selection problem” or a “death spiral”

Stopping the Death Spiral

How to avoid this unpleasant outcome?

1. Go back to experience rating. Feel sorry for sick people

2. Break off the sick people into their own market and subsidize. Very Expensive market, still paid for by the healthy. May get mini‐death‐spirals

3. Convince healthy people to stay in the market

42

Stopping the Death Spiral

3. Convince healthy people to stay in the market

This is the approach most countries have taken

a) “Single Payer” ‐ everyone is on government insurance by law, then premiums (i.e. taxes) can’t spiral

b) “Market Based Solutions” – ACA

• AHCA, Various Senate Bills – split the difference between this and experience rating

43

Premise of the Current Plan

The ACA, or Jon Gruber’s 3‐legged stool

1. No more experience rating (touch off death‐spiral)

2. Mandate health insurance or pay penalty (throw the poor and self‐employed under the bus)

3. Expand insurance for the poor, roll out exchanges

Needs all 3 legs to stand

44

Expanding Insurance: The Good

45

Insurance as a “Merit Good”

Better financial stability• The early ACA‐Medicaid expansion cut payday loan usage

in California by over 1/3 among the young and working‐aged

• Better credit scores, less likely to go into collections, or into bankruptcy

Increased use of primary care, decreased use of ER with the Massachusetts Expansion

Job‐lock and Marriage‐lock

Expanding Insurance: The Bad

46

Taxes and regulatory frictions on business? Unemployment? Not much evidence of this happening

Moral Hazard

• Take worse care of yourself when you’re insured –for example more likely to get flu shot after losing Medicaid

• Care overuse – flat of the curve, and congestion

Expanding Insurance: The Bad

47

‐20

0

20

40

60

80

100

120

140

160

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

2016Q1

2016Q2

Percen

t Growth Relative to 201

3 Q4

Non‐Minor Injury Minor Injury

Ambulance Call Volume in NYC

The average U.S. county saw a slowdown in ambulance response times of 1.8 minutes

Expanding Insurance: The Uncertain

48

Insurers and Bargaining Power

The insurance, drug, and care markets are all highly consolidated. A large influence on the prevailing prices is the relative size and bargaining power of an entity

Expanding insurance changes these power dynamics, but it can be hard to parse out who wins.• A bigger insurer will bargain better with a hospital and

lower payouts• At the same time they will bargain better with employers

and raise premiums

These markets continue to consolidate (CVS‐Aetna), it is unclear who this helps

In Summary

49

1. Blame WW2 for our situation

2. Health insurance is wealth insurance

3. The death spiral looms ever present (unless you go single payer)

4. Insurance expansion does a lot of different things, some good, some bad

5. I did not (and could not) cover it all…questions?