grain transportation report - agricultural marketing … 12-08-16.pdfgrain transportation indicators...

TRANSCRIPT

A weekly publication of the Agricultural Marketing Service

www.ams.usda.gov/GTR

December 8, 2016

Contents

Article/

Calendar

Grain

Transportation

Indicators

Rail

Barge

Truck

Exports

Ocean

Brazil

Mexico

Grain Truck/Ocean

Rate Advisory

Data Links

Specialists

Subscription

Information

--------------

The next

release is Dec 15, 2016

Preferred citation: U.S. Dept. of Agriculture, Agricultural Marketing Service. Grain Transportation Report. December 8, 2016.

Web: http://dx.doi.org/10.9752/TS056.12-08-2016

Grain Transportation Report

WEEKLY HIGHLIGHTS

Grain Vessel Loading Activity Remains Strong as Ocean Freight Rates Tick Up

Ocean-going grain vessel loading activity remained strong in the U.S. Gulf (Gulf) and the Pacific Northwest (PNW) despite an

increase in the ocean freight rates for shipping bulk commodities, including grains. During the 4-week period beginning November 10

and ending December 1, an average of 50 vessels were loaded in the Gulf, with 77 vessels expected within the next 10 days. During

the same period, 21 vessels were at berth in the PNW. Meanwhile, the ocean freight rate for shipping bulk grain from the Gulf to

Japan was $37 per metric ton (mt) during the week ending December 1, a 16 percent increase over the week ending November 10. The

cost of shipping from the PNW to Japan was $20 per mt, a 13 percent increase compared to November 10. According to a December 1

Transportation and Export report by O’Neil Commodity Consulting, increased iron ore and coal shipments to China caused the rate

increase. Those imports have both increased 9 and 12 percent year to year, respectively. However, it is unlikely that the rate hike is

sustainable, as excess vessel supply still exists in the market.

STB Final Decision on Performance Data Reporting On November 30, the Surface Transportation Board (STB) adopted a final rule requiring all Class I railroads to report certain service

performance metrics on a weekly, semiannual, and occasional basis. STB first opened the proceeding (EP 724) with a public hearing

in April 2014 to understand issues pertaining to the rail service problems emerging in late 2013. In October 2014, STB issued an

interim data collection order and then examined new regulations for permanent reporting over the next 2 years. As described in the

recent decision, “The primary purpose of this rulemaking has been to develop a set of performance data that will allow the agency to

monitor current service conditions in the industry and to identify trends or aberrations, which may indicate problems. … A corollary

benefit is that shippers and other stakeholders will have access to the reported data to assist in their business decisions and supply-

chain planning.” The rule becomes effective January 29, 2017, with reporting to begin February 8.

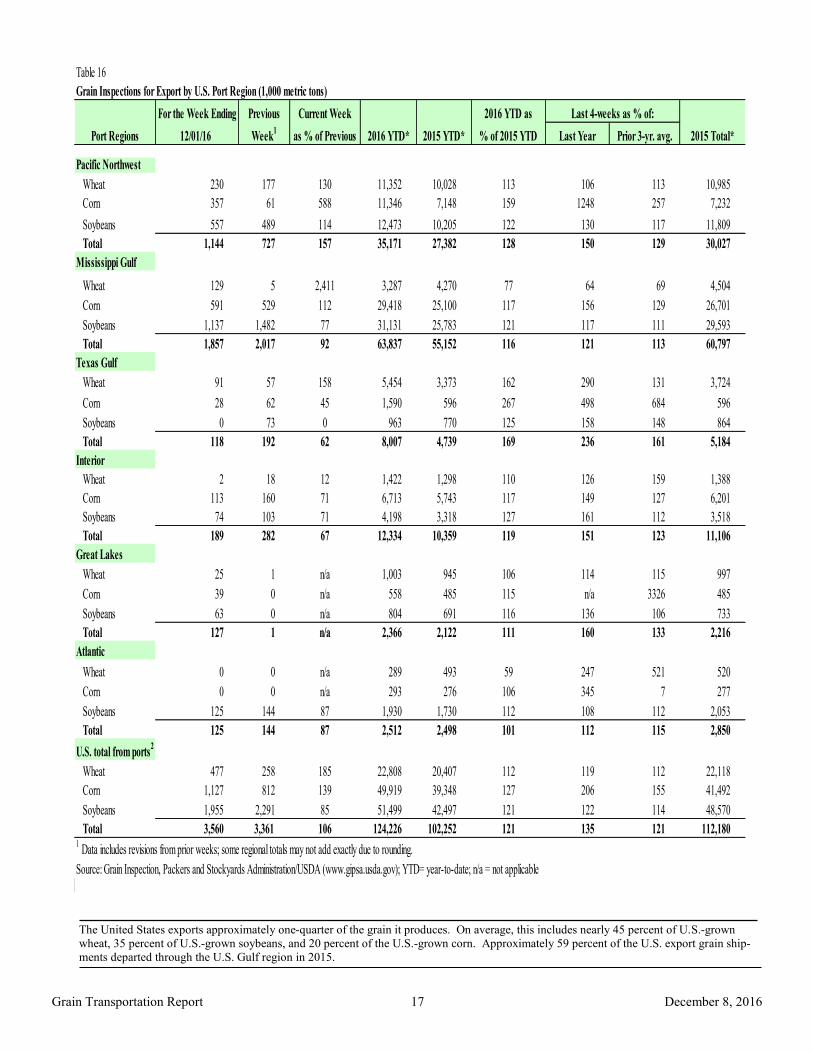

Boost in Pacific Northwest Grain Inspections Help Total For the week ending December 1, total inspections of grain (corn, wheat, and soybeans) for export from major U.S. export regions

reached 3.56 million metric tons (mmt), up 6 percent from the previous week, up 41 percent from last year, and 16 percent above the

3-year average. Inspections of wheat and corn jumped 85 and 39 percent from the previous week, but soybean inspections dropped 15

percent from the past week. PNW grain inspections increased 57 percent from the previous week as shipments increased to China,

Japan, and the Philippines. Mississippi Gulf inspections, however, decreased 8 percent from the previous week. Outstanding export

sales (unshipped) were up for wheat but down for corn and soybeans.

Snapshots by Sector

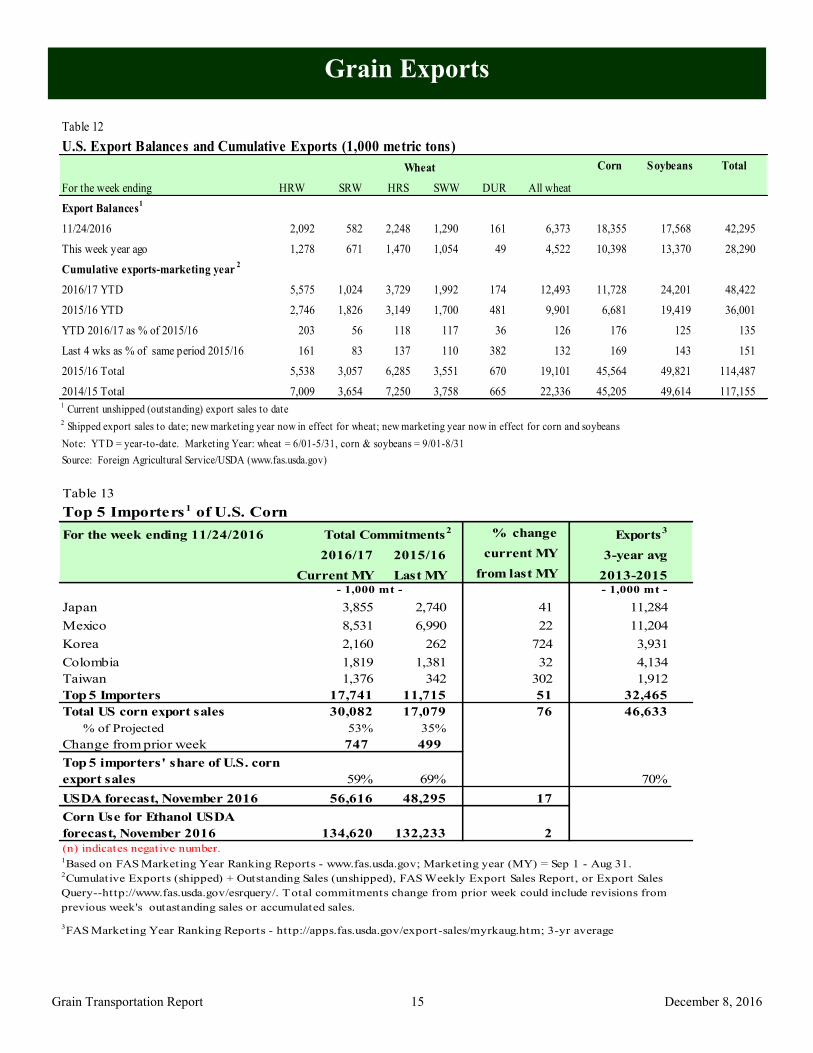

Export Sales

During the week ending November 24, unshipped balances of wheat, corn, and soybeans totaled 42.3 mmt, up 50 percent from the

same time last year. Net weekly wheat export sales were .482 mmt, down 32 percent from the previous week. Net corn export sales

were .747 mmt, down 55 percent from the previous week, and net soybean export sales were 1.40 mmt, down 25 percent from the

past week.

Rail

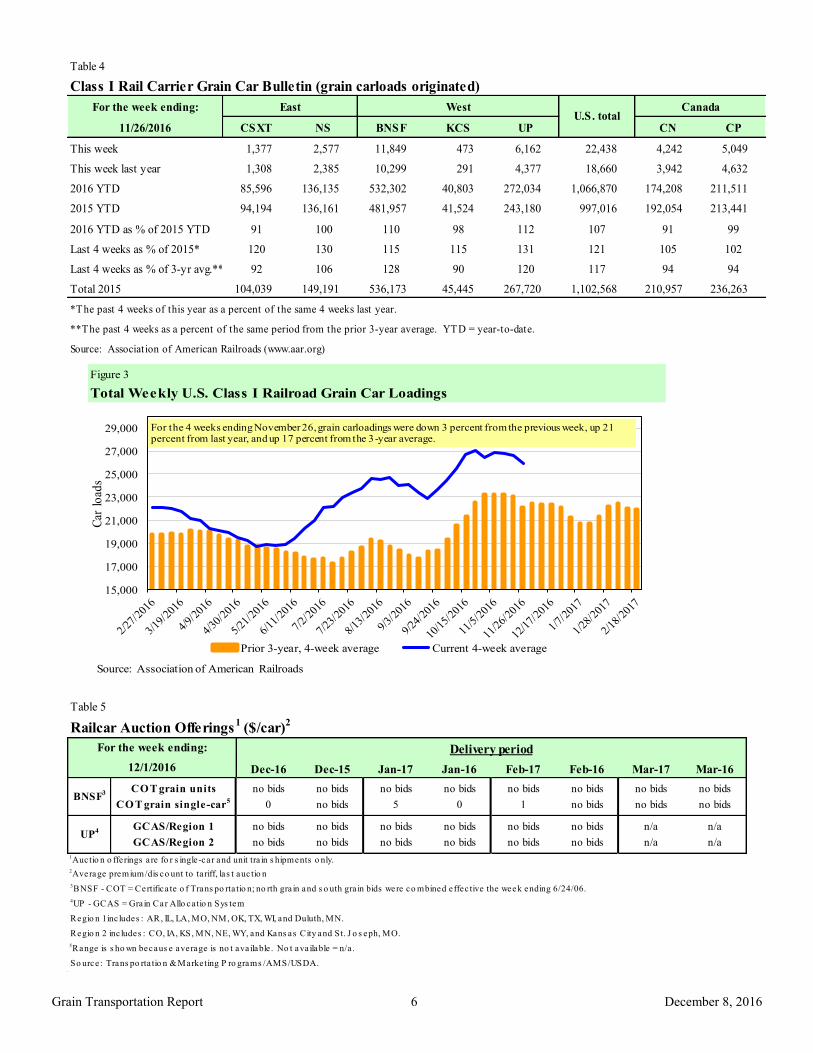

U.S. Class I railroads originated 22,438 grain carloads for the week ending November 26, down 13 percent from the previous week,

up 20 percent from last year, and up 10 percent from the 3-year average.

Average December shuttle secondary railcar bids/offers per car were $33 below tariff for the week ending December 1, up $18 from

last week, and $192 higher than last year. Average non-shuttle secondary railcar bids/offers per car were $109 below tariff, down $26

from last week, and $28 higher than last year.

Barge For the week ending December 3, barge grain movements totaled 1,058,591 tons, 15 percent lower than last week, and up 35 percent

from the same period last year.

For the week ending December 3, 683 grain barges moved down river, down 15 percent from last week, 1,007 grain barges were

unloaded in New Orleans, down 3 percent from the previous week.

Ocean

For the week ending December 1, 50 ocean-going grain vessels were loaded in the Gulf, 19 percent more than the same period last

year. Seventy-five vessels are expected to be loaded within the next 10 days, 9 percent more than the same period last year.

For the week ending December 1, the ocean freight rate for shipping bulk grain from the Gulf to Japan was $37 per metric ton, 4

percent more than the previous week. The cost of shipping from the PNW to Japan was $20 per metric ton, 4 percent more than the

previous week.

Fuel

During the week ending December 5, U.S. average diesel fuel prices were up 6 cents from the previous week at $2.48 per gallon, 10

cents higher than the same week last year.

Contact Us

December 8, 2016

Grain Transportation Report 2

Feature Article/Calendar

Transportation of Fertilizer: 2016 Update

Fertilizer is an essential input for profitable agricultural production that relies upon a vast transportation system for

farmers to get the fertilizer they need, when and where they need it. Fertilizer is transported in solid or liquid form

from its point of origin or production location. Before arriving at the farm, fertilizer products will likely have been

transported by more than one mode of transportation. It is transported by rail cars, river barges, trucks, or as gas or

liquid in pipelines. This article updates the data and analysis of fertilizer movements by rail and barges from a

previous article published in April 18, 2013 edition of the Grain Transportation Report.

The United States is one of the world’s largest importers of fertilizers, which helps supplement its domestic use of

nitrogen and potash.1 Canada has been the largest originating country for U.S. fertilizer imports for more than 20

years. In 2012, the value of major U.S. fertilizer products imported was about $13 billion. About $5 billion that total

were imported from Canada. The United States also imports from Egypt, Chile, Kuwait, and China.2

Rail

Table 1 shows railroads hauled an annual average of 58 million tons of fertilizer and fertilizer ingredients per year

from 2005 to 2014. Over the 10-year period, total fertilizer shipments fluctuated between 49 million and 66 million

tons annually, with a slight downward trend. Fertilizer ingredient shipments increased from 54 percent of the total in

2005 to 58 percent in 2014. Liquid fertilizer shipments increased from 19 percent of the total in 2005 to 22 percent

in 2014. On the other hand, rail movements of anhydrous ammonia, a toxic-by-inhalation hazardous material,

decreased from

3.7 million tons

to 1.4 million

tons (6 percent

to 2 percent of

the total) during

the same time

period. Dry

fertilizer

shipments also

dropped from

13.8 million

tons (22 percent

of the total) in

2005 to 9.9

million tons (17

percent) in

2014.

Barge

Table 2 (see next page) shows 2005-2014 fertilizer barge traffic by month and year, based on delivery date of the

shipment. On average, railroads handled almost five times as much in fertilizer movements as barges. However,

while fertilizer shipments by barge have increased since 2010, shipments by rail have been stable (around 57.5

million tons) during the same time (tables 1 and 2). Overall, March through May is the busiest period for delivering

fertilizer by barges. This corresponds to the typical planting window for corn in many States.3 April usually has the

highest volume of shipments, with a 10-year average shipment of 1.5 million tons. Annual total shipments have

continuously increased since 2010 and reached 16.8 million tons in 2014 (about a 30 percent increase).

The leading origin of barged fertilizers is the Baton Rouge-New Orleans area, which accounts for 79 percent of

barged fertilizer for all U.S. inland waterways from 2005 to 2014.

1 USDA/ERS, Fertilizer Imports/Exports, https://www.ers.usda.gov/data-products/fertilizer-importsexports/summary-of-the-data-findings.aspx. 2 See fertilizer product selection here: https://www.ers.usda.gov/data-products/fertilizer-importsexports.aspx. 3 USDA/NASS, Field Crops: Usual Planting and Harvesting Dates, October 2010.

Table 1: Fertilizer shipped by rail, 2005-2014 (1,000 tons)

Year Dry

fertilizer

Fertilizer

ingredients

Anhydrous

ammonia

Liquid

fertilizer

Total

2005 13,773 34,770 3,662 11,926 64,131

2006 11,489 32,177 3,836 12,019 59,521

2007 12,242 37,333 3,523 13,203 66,301

2008 10,074 31,242 2,902 12,776 56,995

2009 9,760 25,985 1,831 11,460 49,036

2010 11,128 31,778 1,992 12,373 57,271

2011 11,533 31,170 1,791 13,142 57,637

2012 10,530 30,761 1,564 13,536 56,391

2013 10,446 33,952 1,557 13,003 58,959

2014 9,910 33,674 1,416 12,925 57,925

10-Yr Avg. 11,089 32,284 2,408 12,636 58,417 Source: USDA analysis of Surface Transportation Board Confidential Waybill Samples

December 8, 2016

Grain Transportation Report 3

Baton Rouge-New Orleans often receives fertilizers via Florida, which are either domestically produced or imported

to Florida from foreign origins. Also, Baton Rouge-New Orleans receives imports directly from foreign origins.

The leading fertilizer shipped up-bound from New Orleans by barge is urea (about 41 percent). About 20 percent of

barged fertilizers are delivered to the Upper Mississippi River (above St. Louis, MO), which is the leading

destination for barged fertilizer. Fertilizers can use the same barge as down-bound grain and are often a backhaul

commodity instead of sending an empty barge up-bound. The second leading river area for fertilizer deliveries is the

Ohio River, with about 19 percent of all deliveries. Other important delivery points are the McClellan-Kerr

Arkansas River System, and the Lower Mississippi (e.g., Cairo, IL, and other points south).

Table 2: Average monthly barge fertilizer movements, by month, 2005-2014, 10-year average (1,000 tons)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 10-Yr. Avg.

Jan 888 1,028 919 963 754 822 1,073 1,072 1,174 1,049 974

Feb 791 809 785 867 944 895 700 1,087 1,171 1,061 911

Mar 1,350 1,158 1,451 1,005 956 1,040 1,386 1,547 1,462 1,538 1,289

Apr 1,510 1,362 1,465 1,154 1,178 1,624 1,553 1,709 1,696 2,023 1,527

May 1,395 1,191 1,472 1,333 900 1,124 1,337 1,383 1,745 2,175 1,405

Jun 969 806 911 1,039 841 907 1,189 759 1,082 1,003 951

Jul 766 672 816 997 734 714 897 758 924 768 805

Aug 771 590 858 989 750 893 998 842 955 1,183 883

Sep 702 796 918 782 779 888 931 1,106 1,021 1,563 949

Oct 761 846 1,231 948 739 1,381 1,389 1,641 1,489 1,780 1,220

Nov 1,099 913 1,061 719 987 1,349 1,280 1,420 1,583 1,429 1,184

Dec 816 717 952 523 867 1,258 937 1,155 1,039 1,280 954

Annual 11,816 10,887 12,838 11,319 10,429 12,896 13,671 14,480 15,341 16,850 13,053

Source: Detailed Origin-Destination Waterborne Commerce Statistics, U.S. Army Corps of Engineers

Figure 1 shows 10-year monthly average tonnages for fertilizer by rail and all barges. On average, rail moved about

5 million tons of fertilizer every month and barges moved about 1 million tons. Both barge and rail movements

demonstrated peaks in

spring and fall months.

The primary peak was in

April, as many farmers are

getting ready to plant corn

and soybeans, with an

average tonnage of 5.8

million tons for rail and

1.5 million tons for

barges. The second peak

was in October with an

average of 5.5 million tons

for rail and 1.2 million for

barge movements.

[email protected]; [email protected]; [email protected];

Figure 1: Average monthly barge and rail fertilizer movements, 2005-2014

Source: U.S. Army Corps of Engineers, STB Waybill Samples

December 8, 2016

Grain Transportation Report 4

Grain Transportation Indicators

The grain bid summary illustrates the market relationships for commodities. Positive and negative adjustments in differential be-

tween terminal and futures markets, and the relationship to inland market points, are indicators of changes in fundamental market

supply and demand. The map may be used to monitor market and time differentials.

Table 2

Market Update: U.S. Origins to Export Position Price Spreads ($/bushel)

Commodity Origin--Destination 12/2/2016 11/23/2016

Corn IL--Gulf -0.50 -0.49

Corn NE--Gulf -0.79 -0.82

Soybean IA--Gulf -1.13 -0.99

HRW KS--Gulf -1.81 n/a

HRS ND--Portland -2.14 n/a

Note: nq = no quote

Source: Transportation & Marketing Programs/AMS/USDA

Table 1

Grain Transport Cost Indicators1

Truck Barge Ocean

For the week ending Unit Train Shuttle Gulf Pacific

12/07/16 166 255 207 129 165 1422 % 3 1% - 3 % 4 % 4 %

11/30/16 162 256 205 133 159 137

1Indicator: Base year 2000 = 100; Weekly updates include truck = diesel ($/gallon); rail = near-month secondary rail market bid and monthly tariff rate

with fuel surcharge ($/car); barge = Illinois River barge rate (index = percent of tariff rate); and ocean = routes to Japan ($/metric ton)

Source: Transportation & Marketing Programs/AMS/USDA

Rail

Figure 1

Grain bid Summary

December 8, 2016

Grain Transportation Report 5

Rail Transportation

Railroads originate approximately 24 percent of U.S. grain shipments. Trends in these loadings are indicative of

market conditions and expectations.

Figure 2

Rail Deliveries to Port

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

07/0

3/1

3

08/2

8/1

3

10/2

3/1

3

12/1

8/1

3

02/1

2/1

4

04/0

9/1

4

06/0

4/1

4

07/3

0/1

4

09/2

4/1

4

11/1

9/1

4

01/1

4/1

5

03/1

1/1

5

05/0

6/1

5

07/0

1/1

5

08/2

6/1

5

10/2

1/1

5

12/1

6/1

5

02/1

0/1

6

04/0

6/1

6

06/0

1/1

6

07/2

7/1

6

09/2

1/1

6

11/1

6/1

6

01/1

1/1

7

03/0

8/1

7

Carl

oa

ds

-4

-we

ek

ru

nn

ing a

vera

ge

Pacific Northwest: 4 wks. ending 11/30--up 22% from same period last year; up 29% from 4-year average

Texas Gulf: 4 wks. ending 11/30--up 63% from same period last year; up 88% from 4-year average

Miss. River: 4 wks. ending 11/30--up 165% from same period last year; up 14% from 4-year average

Cross-border: 4 wks. ending 11/26--up 36% from same period last year; up 36% from 4-year average

Source: T ransportation & Marketing Programs/AMS/USDA

Table 3

Rail Deliveries to Port (carloads)1

Mississippi Pacific Atlantic & Cross-Border

For the Week Ending Gulf Texas Gulf Northwest East Gulf Total Week ending Mexico3

11/30/2016p

977 2,559 7,813 1,083 12,432 11/26/2016 1,934

11/23/2016r

1,336 1,870 7,926 1,102 12,234 11/19/2016 2,916

2016 YTDr

33,908 78,771 274,677 24,885 412,241 2016 YTD 100,070

2015 YTDr

28,007 54,935 218,760 24,363 326,065 2015 YTD 90,697

2016 YTD as % of 2015 YTD 121 143 126 102 126 % change YTD 110

Last 4 weeks as % of 20152

265 163 122 127 137 Last 4wks % 2015 136

Last 4 weeks as % of 4-year avg.2

114 188 129 115 133 Last 4wks % 4 yr 136

Total 2015 29,054 60,819 239,029 26,730 355,632 Total 2015 97,736

Total 2014 44,617 83,674 256,670 32,107 417,068 Total 2014 98,4221 Data is incomplete as it is voluntarily provided2 Compared with same 4-weeks in 2015 and prior 4-year average.

3 Cross-border weekly data is approximately 15 percent below the Association of American Railroads' reported weekly carloads received by Mexican railroads

to reflect switching between KCSM and FerroMex.

YTD = year-to-date; p = preliminary data; r = revised data; n/a = not available

Source: Transportation & Marketing Programs/AMS/USDA

December 8, 2016

Grain Transportation Report 6

Table 5

Railcar Auction Offerings1

($/car)2

Dec-16 Dec-15 Jan-17 Jan-16 Feb-17 Feb-16 Mar-17 Mar-16

CO T grain units no bids no bids no bids no bids no bids no bids no bids no bids

CO T grain single-car5 0 no bids 5 0 1 no bids no bids no bids

GCAS/Region 1 no bids no bids no bids no bids no bids no bids n/a n/a

GCAS/Region 2 no bids no bids no bids no bids no bids no bids n/a n/a

1Auctio n o fferings a re fo r s ingle-car and unit tra in s hipments o nly.2Average premium/dis co unt to ta riff, las t auc tio n

3BNSF - COT = Certifica te o f Trans po rta tio n; no rth gra in and s o uth gra in bids were co mbined effec tive the week ending 6/24/06.

4UP - GCAS = Grain Car Allo ca tio n Sys tem

Regio n 1 inc ludes : AR, IL, LA, MO, NM, OK, TX, WI, and Duluth, MN.

Regio n 2 inc ludes : CO, IA, KS, MN, NE, WY, and Kans as City and St. J o s eph, MO.

5Range is s ho wn becaus e average is no t ava ilable . No t ava ilable = n/a .

So urce : Trans po rta tio n & Marketing P ro grams /AMS/USDA.

UP4

Delivery period

BNSF3

For the week ending:

12/1/2016

Table 4

Class I Rail Carrier Grain Car Bulletin (grain carloads originated)

For the week ending:

11/26/2016 CSXT NS BNSF KCS UP CN CP

This week 1,377 2,577 11,849 473 6,162 22,438 4,242 5,049

This week last year 1,308 2,385 10,299 291 4,377 18,660 3,942 4,632

2016 YTD 85,596 136,135 532,302 40,803 272,034 1,066,870 174,208 211,511

2015 YTD 94,194 136,161 481,957 41,524 243,180 997,016 192,054 213,441

2016 YTD as % of 2015 YTD 91 100 110 98 112 107 91 99

Last 4 weeks as % of 2015* 120 130 115 115 131 121 105 102

Last 4 weeks as % of 3-yr avg.** 92 106 128 90 120 117 94 94

Total 2015 104,039 149,191 536,173 45,445 267,720 1,102,568 210,957 236,263

*The past 4 weeks of this year as a percent of the same 4 weeks last year.

**The past 4 weeks as a percent of the same period from the prior 3-year average. YTD = year-to-date.

Source: Association of American Railroads (www.aar.org)

East WestU.S. total

Canada

Figure 3

Total Weekly U.S. Class I Railroad Grain Car Loadings

15,000

17,000

19,000

21,000

23,000

25,000

27,000

29,000

Car

lo

ads

Prior 3-year, 4-week average Current 4-week average

For the 4 weeks ending November 26, grain carloadings were down 3 percent from the previous week, up 21 percent from last year, and up 17 percent from the 3-year average.

Source: Association of American Railroads

December 8, 2016

Grain Transportation Report 7

The secondary rail market information reflects trade values for service that was originally purchased from the railroad carrier as

some form of guaranteed freight. The auction and secondary rail values are indicators of rail service quality and demand/

supply.

Figure 4

Bids/Offers for Railcars to be Delivered in December 2016, Secondary Market

-500

0

500

1000

1500

2000

2500

4/2

8/2

016

5/1

2/2

016

5/2

6/2

016

6/9

/201

6

6/2

3/2

016

7/7

/201

6

7/2

1/2

016

8/4

/201

6

8/1

8/2

016

9/1

/201

6

9/1

5/2

016

9/2

9/2

016

10/1

3/2

016

10/2

7/2

016

11/1

0/2

016

11/2

4/2

016

12

/8/2

016

Aver

age

pre

miu

m/d

isco

unt

to tar

iff

($/c

ar)

Shuttle Non-Shuttle

Shuttle prior 3-yr avg. (same week) Non-Shuttle prior 3-yr avg. (same week)12/1/2016

Non-shuttle bids include unit-train and single-car bids. n/a = not available.Source: Transportation & Marketing Programs/AMS/USDA

-$106

UPBNSF

$83

-$113

-$150Shuttle

Non-Shuttle

Average Non-shuttle bids/offers fell $26 this week, and are $109 below the peak.Average Shuttle bids/offers rose $18 this week and are $233 below the peak.

Figure 5

Bids/Offers for Railcars to be Delivered in January 2017, Secondary Market

-400

-200

0

200

400

600

800

1000

1200

1400

6/2

/201

6

6/1

6/2

016

6/3

0/2

016

7/1

4/2

016

7/2

8/2

016

8/1

1/2

016

8/2

5/2

016

9/8

/201

6

9/2

2/2

016

10

/6/2

016

10/2

0/2

016

11

/3/2

016

11/1

7/2

016

12

/1/2

016

12/1

5/2

016

12/2

9/2

016

1/1

2/2

017

Aver

age

pre

miu

m/d

isco

unt

to tar

iff

($/c

ar)

Shuttle Non-Shuttle

Shuttle prior 3-yr avg. (same week) Non-Shuttle prior 3-yr avg. (same week)12/1/2016

Non-shuttle bids include unit-train and single-car bids. n/a = not available.Source: Transportation & Marketing Programs/AMS/USDA

n/a

UPBNSF

n/a

n/a

-$100Shuttle

Non-Shuttle

There were no Non-Shuttle bids/offers this week.Average Shuttle bids/offers are unchanged this week and are $150 below the peak.

December 8, 2016

Grain Transportation Report 8

Figure 6

Bids/Offers for Railcars to be Delivered in February 2017, Secondary Market

-200

0

200

400

600

800

1000

1200

1400

1600

18006/3

0/2

016

7/1

4/2

016

7/2

8/2

016

8/1

1/2

016

8/2

5/2

016

9/8

/201

6

9/2

2/2

016

10

/6/2

016

10/2

0/2

016

11

/3/2

016

11/1

7/2

016

12

/1/2

016

12/1

5/2

016

12/2

9/2

016

1/1

2/2

017

1/2

6/2

017

2/9

/201

7

Aver

age

pre

miu

m/d

isco

unt

to tar

iff

($/c

ar)

Shuttle Non-Shuttle

Shuttle prior 3-yr avg. (same week) Non-Shuttle prior 3-yr avg. (same week)12/1/2016

Non-shuttle bids include unit-train and single-car bids. n/a = not available.Source: Transportation & Marketing Programs/AMS/USDA

n/a

UPBNSF

n/a

n/a

n/aShuttle

Non-Shuttle

There were no Non-Shuttle bids/offers this week.There were no Shuttle bids/offers this week.

Table 6

Weekly Secondary Railcar Market ($/car)1

Dec-16 Jan-17 Feb-17 Mar-17 Apr-17 May-17

BNSF-GF (106) n/a n/a n/a n/a n/a

Change from last week (63) n/a n/a n/a n/a n/a

Change from same week 2015 19 n/a n/a n/a n/a n/a

UP-Pool (113) n/a n/a n/a n/a n/a

Change from last week 12 n/a n/a n/a n/a n/a

Change from same week 2015 38 n/a n/a n/a n/a n/a

BNSF-GF 83 n/a n/a n/a n/a n/a

Change from last week 27 n/a n/a n/a n/a n/a

Change from same week 2015 283 n/a n/a n/a n/a n/a

UP-Pool (150) (100) n/a n/a n/a n/a

Change from last week 8 0 n/a n/a n/a n/a

Change from same week 2015 100 n/a n/a n/a n/a n/a

1Average premium/dis co unt to ta riff, $ /car-las t week

No te : Bids lis ted are market INDICATORS o nly & are NOT guaranteed prices ,

n/a = no t ava ilable ; GF = guaranteed fre ight; P o o l = guaranteed po o l

So urces : Trans po rta tio n and Marketing P ro grams /AMS/USDA

Data fro m J ames B. J o iner Co ., Tradewes t Bro kerage Co .

No

n-s

hu

ttle

For the week ending:

12/1/2016

Sh

utt

le

Delivery period

December 8, 2016

Grain Transportation Report 9

Table 7

Tariff Rail Rates for Unit and Shuttle Train Shipments1

Percent

Tariff change

December, 2016 Origin region* Destination region* rate/car metric ton bushel2

Y/Y3

Unit train

Wheat Wichita, KS St. Louis, MO $3,770 $40 $37.84 $1.03 4

Grand Forks, ND Duluth-Superior, MN $4,143 -$3 $41.11 $1.12 16

Wichita, KS Los Angeles, CA $6,950 -$15 $68.86 $1.87 0

Wichita, KS New Orleans, LA $4,408 $71 $44.48 $1.21 4

Sioux Falls, SD Galveston-Houston, TX $6,486 -$13 $64.28 $1.75 0

Northwest KS Galveston-Houston, TX $4,676 $78 $47.21 $1.28 3

Amarillo, TX Los Angeles, CA $4,875 $109 $49.49 $1.35 3

Corn Champaign-Urbana, IL New Orleans, LA $3,681 $80 $37.35 $0.95 0

Toledo, OH Raleigh, NC $6,061 $0 $60.19 $1.53 0

Des Moines, IA Davenport, IA $2,258 $17 $22.59 $0.57 4

Indianapolis, IN Atlanta, GA $5,191 $0 $51.55 $1.31 4

Indianapolis, IN Knoxville, TN $4,311 $0 $42.81 $1.09 0

Des Moines, IA Little Rock, AR $3,534 $50 $35.59 $0.90 2

Des Moines, IA Los Angeles, CA $5,202 $146 $53.11 $1.35 3

Soybeans Minneapolis, MN New Orleans, LA $3,639 $45 $36.58 $1.00 -2

Toledo, OH Huntsville, AL $5,051 $0 $50.16 $1.37 0

Indianapolis, IN Raleigh, NC $6,178 $0 $61.35 $1.67 0

Indianapolis, IN Huntsville, AL $4,529 $0 $44.98 $1.22 0

Champaign-Urbana, IL New Orleans, LA $4,495 $80 $45.44 $1.24 2

Shuttle Train

Wheat Great Falls, MT Portland, OR $3,953 -$9 $39.17 $1.07 0

Wichita, KS Galveston-Houston, TX $3,871 -$7 $38.37 $1.04 -2

Chicago, IL Albany, NY $5,492 $0 $54.54 $1.48 0

Grand Forks, ND Portland, OR $5,611 -$15 $55.57 $1.51 -1

Grand Forks, ND Galveston-Houston, TX $5,931 -$16 $58.74 $1.60 -1

Northwest KS Portland, OR $5,643 $128 $57.31 $1.56 3

Corn Minneapolis, MN Portland, OR $5,000 -$19 $49.47 $1.26 -1

Sioux Falls, SD Tacoma, WA $4,960 -$17 $49.09 $1.25 -1

Champaign-Urbana, IL New Orleans, LA $3,481 $80 $35.37 $0.90 0

Lincoln, NE Galveston-Houston, TX $3,700 -$10 $36.64 $0.93 2

Des Moines, IA Amarillo, TX $3,895 $63 $39.30 $1.00 2

Minneapolis, MN Tacoma, WA $5,000 -$18 $49.47 $1.26 -1

Council Bluffs, IA Stockton, CA $4,740 -$19 $46.88 $1.19 1

Soybeans Sioux Falls, SD Tacoma, WA $5,600 -$17 $55.44 $1.51 1

Minneapolis, MN Portland, OR $5,650 -$19 $55.92 $1.52 2

Fargo, ND Tacoma, WA $5,500 -$15 $54.47 $1.48 2

Council Bluffs, IA New Orleans, LA $4,525 $93 $45.86 $1.25 2

Toledo, OH Huntsville, AL $4,226 $0 $41.97 $1.14 0

Grand Island, NE Portland, OR $5,460 $131 $55.52 $1.51 2

1A unit train refers to shipments of at least 25 cars. Shuttle train rates are available for qualified shipments of

75-120 cars that meet railroad efficiency requirements.

2Approximate load per car = 111 short tons (100.7 metric tons): corn 56 lbs./bu., wheat & soybeans 60 lbs./bu.

3Percentage change year over year calculated using tariff rate plus fuel surchage

Sources: www.bnsf.com, www.cpr.ca, www.csx.com, www.uprr.com

*Regional economic areas defined by the Bureau of Economic Analysis (BEA)

Tariff plus surcharge per:Fuel

surcharge

per car

The tariff rail rate is the base price of freight rail service, and together with fuel surcharges and any auction and secondary rail

values constitute the full cost of shipping by rail. Typically, auction and secondary rail values are a small fraction of the full

cost of shipping by rail relative to the tariff rate. High auction and secondary rail values, during times of high rail demand or

short supply, can exceed the cost of the tariff rate plus fuel surcharge.

December 8, 2016

Grain Transportation Report 10

Table 8

Tariff Rail Rates for U.S. Bulk Grain Shipments to MexicoDate: Percent

Tariff change4

Commodity Destination region rate/car1

metric ton3 bushel

3Y/Y

Wheat MT Chihuahua, CI $7,459 $0 $76.21 $2.07 0

OK Cuautitlan, EM $6,596 $56 $67.97 $1.85 1

KS Guadalajara, JA $7,077 $143 $73.77 $2.01 1

TX Salinas Victoria, NL $4,197 $32 $43.21 $1.17 1

Corn IA Guadalajara, JA $8,187 $127 $84.95 $2.16 -2

SD Celaya, GJ $7,580 $0 $77.45 $1.97 -4

NE Queretaro, QA $7,909 $105 $81.89 $2.08 0

SD Salinas Victoria, NL $6,635 $0 $67.79 $1.72 1

MO Tlalnepantla, EM $7,268 $102 $75.31 $1.91 0

SD Torreon, CU $7,180 $0 $73.36 $1.86 -1

Soybeans MO Bojay (Tula), HG $8,647 $131 $89.69 $2.44 0

NE Guadalajara, JA $8,942 $136 $92.75 $2.52 -2

IA El Castillo, JA $8,960 $0 $91.55 $2.49 -6

KS Torreon, CU $7,489 $96 $77.49 $2.11 1

Sorghum NE Celaya, GJ $7,164 $117 $74.39 $1.89 -3

KS Queretaro, QA $7,608 $70 $78.44 $1.99 0

NE Salinas Victoria, NL $6,213 $56 $64.05 $1.63 0

NE Torreon, CU $6,607 $90 $68.43 $1.74 -31Rates are based upon published tariff rates for high-capacity shuttle trains. Shuttle trains are available for qualified

shipments of 75--110 cars that meet railroad efficiency requirements.2Fuel surcharge adjusted to reflect the change in Ferrocarril Mexicano, S.A. de C.V railroad fuel surcharge policy as of 10/01/20093Approximate load per car = 97.87 metric tons: Corn & Sorghum 56 lbs/bu, Wheat & Soybeans 60 lbs/bu4Percentage change calculated using tariff rate plus fuel surchage

Sources: www.bnsf.com, www.uprr.com, www.kcsouthern.com

Fuel

surcharge

per car2

Tariff plus surcharge per:Origin

state

December, 2016

Figure 7

Railroad Fuel Surcharges, North American Weighted Average1

-$0.10

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

Dollar

s p

er r

ailc

ar m

ile

3-Year Monthly Average

Fuel Surcharge* ($/mile/railcar)

December, 2016: $0.02, unchanged from last month's surcharge of $0.02/mile; down 2 cents from the December 2015 surcharge of $0.04/mile; and down 19 cents from the December prior 3-year average of $0.21/mile.

1 Weighted by each Class I railroad's proportion of grain traffic for the prior year. * Beginning January 2009, the Canadian Pacific fuel surcharge is computed by a monthly average of the bi -weekly fuel surcharge.**CSX strike price changed from $2.00/gal. to $3.75/gal. starting January 1, 2015.

Sources: www.bnsf.com, www.cn.ca, www.cpr.ca, www.csx.com, www.kcsi.com, www.nscorp.com, www.uprr.com

December 8, 2016

Grain Transportation Report 11

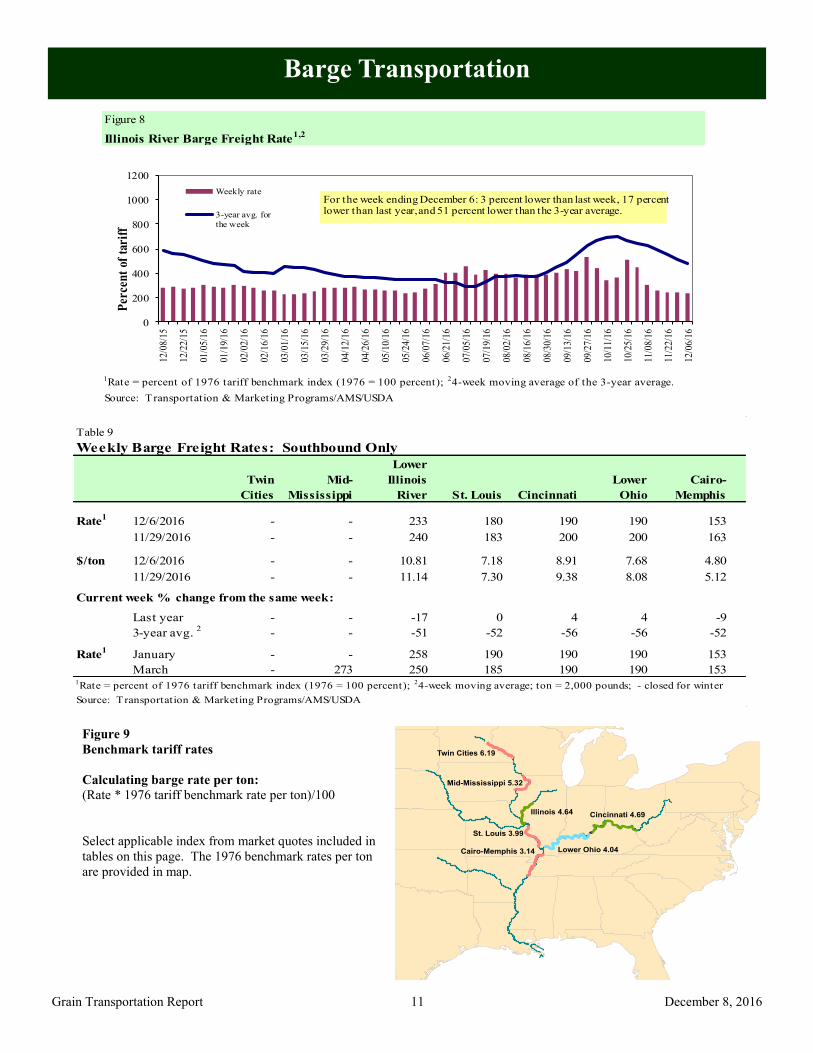

Barge Transportation

Figure 8

Illinois River Barge Freight Rate1,2

1Rate = percent of 1976 tariff benchmark index (1976 = 100 percent); 24-week moving average of the 3-year average.

Source: Transportation & Marketing Programs/AMS/USDA

0

200

400

600

800

1000

1200

12/0

8/15

12/2

2/15

01/0

5/16

01/1

9/16

02/0

2/16

02/1

6/16

03/0

1/16

03/1

5/16

03/2

9/16

04/1

2/16

04/2

6/16

05/1

0/16

05/2

4/16

06/0

7/16

06/2

1/16

07/0

5/16

07/1

9/16

08/0

2/16

08/1

6/16

08/3

0/16

09/1

3/16

09/2

7/16

10/1

1/16

10/2

5/16

11/0

8/16

11/2

2/16

12/0

6/16

Per

cen

t of

tar

iff

Weekly rate

3-year avg. for

the week

For the week ending December 6: 3 percent lower than last week, 17 percent lower than last year,and 51 percent lower than the 3-year average.

Table 9

Weekly Barge Freight Rates: Southbound Only

Twin

Cities

Mid-

Mississippi

Lower

Illinois

River St. Louis Cincinnati

Lower

Ohio

Cairo-

Memphis

Rate1

12/6/2016 - - 233 180 190 190 153

11/29/2016 - - 240 183 200 200 163

$/ton 12/6/2016 - - 10.81 7.18 8.91 7.68 4.80

11/29/2016 - - 11.14 7.30 9.38 8.08 5.12

Current week % change from the same week:

Last year - - -17 0 4 4 -9

3-year avg. 2

- - -51 -52 -56 -56 -52-2 6 6

Rate1

January - - 258 190 190 190 153

March - 273 250 185 190 190 153

Source: Transportation & Marketing Programs/AMS/USDA

1Rate = percent of 1976 tariff benchmark index (1976 = 100 percent);

24-week moving average; ton = 2,000 pounds; - closed for winter

Figure 9

Benchmark tariff rates

Calculating barge rate per ton:

(Rate * 1976 tariff benchmark rate per ton)/100

Select applicable index from market quotes included in

tables on this page. The 1976 benchmark rates per ton

are provided in map.

Twin Cities 6.19

Mid-Mississippi 5.32

St. Louis 3.99

Cairo-Memphis 3.14

Illinois 4.64 Cincinnati 4.69

Lower Ohio 4.04

December 8, 2016

Grain Transportation Report 12

Figure 10

Barge Movements on the Mississippi River1 (Locks 27 - Granite City, IL)

1 The 3-year average is a 4-week moving average.

Source: U.S. Army Corps of Engineers

0

200

400

600

800

1,00006

/13/1

5

06

/27/1

5

07

/11/1

5

07

/25/1

5

08

/08/1

5

08

/22/1

5

09

/05/1

5

09

/19/1

5

10

/03/1

5

10

/17/1

5

10

/31/1

5

11

/14/1

5

11

/28/1

5

12

/12/1

5

12

/26/1

5

01

/09/1

6

01

/23/1

6

02

/06/1

6

02

/20/1

6

03

/05/1

6

03

/19/1

6

04

/02/1

6

04

/16/1

6

04

/30/1

6

05

/14/1

6

05

/28/1

6

06

/11/1

6

06

/25/1

6

07

/09/1

6

07

/23/1

6

08

/06/1

6

08

/20/1

6

09

/03/1

6

09

/17/1

6

10

/01/1

6

10

/15/1

6

10

/29/1

6

11

/12/1

6

11

/26/1

6

12

/10/1

6

12

/24/1

6

1,0

00

to

ns

Soybeans

Wheat

Corn

3-Year Average

For the week ending December 03: up 43 percent from last yearand up 69 percent from the 3-yr avg.

Table 10

Barge Grain Movements (1,000 tons)

For the week ending 12/03/2016 Corn Wheat Soybeans Other Total

Mississippi River

Rock Island, IL (L15) 151 11 99 0 260

Winfield, MO (L25) 359 15 266 2 642

Alton, IL (L26) 539 17 320 2 878

Granite City, IL (L27) 558 18 343 2 922

Illinois River (L8) 105 0 16 0 121

Ohio River (L52) 18 4 76 0 97

Arkansas River (L1) 0 0 40 0 40

Weekly total - 2016 576 22 459 2 1,059

Weekly total - 2015 347 3 425 12 786

2016 YTD1

22,624 1,917 15,084 317 39,942

2015 YTD 18,183 1,609 12,380 339 32,511

2016 as % of 2015 YTD 124 119 122 93 123

Last 4 weeks as % of 20152

152 127 128 20 136

Total 2015 19,215 1,686 14,191 359 35,451

2 As a percent of same period in 2015.

Source: U.S. Army Corps of Engineers

Note: Total may not add exactly, due to rounding

1 Weekly total, YTD (year-to-date) and calendar year total includes Miss/27, Ohio/52, and Ark/1; "Other" refers to oats, barley,

sorghum, and rye.

December 8, 2016

Grain Transportation Report 13

Figure 11

Source: U.S. Army Corps of Engineers

Upbound Empty Barges Transiting Mississippi River Locks 27, Arkansas River

Lock and Dam 1, and Ohio River Locks and Dam 52

0

100

200

300

400

500

600

700

1/3

0/1

6

2/6

/16

2/1

3/1

6

2/2

0/1

6

2/2

7/1

6

3/5

/16

3/1

2/1

6

3/1

9/1

6

3/2

6/1

6

4/2

/16

4/9

/16

4/1

6/1

6

4/2

3/1

6

4/3

0/1

6

5/7

/16

5/1

4/1

6

5/2

1/1

6

5/2

8/1

6

6/4

/16

6/1

1/1

6

6/1

8/1

6

6/2

5/1

6

7/2

/16

7/9

/16

7/1

6/1

6

7/2

3/1

6

7/3

0/1

6

8/6

/16

8/1

3/1

6

8/2

0/1

6

8/2

7/1

6

9/3

/16

9/1

0/1

6

9/1

7/1

6

9/2

4/1

6

10/

1/1

6

10/

8/1

6

10/

15/

16

10/

22/

16

10/

29/

16

11/

5/1

6

11/

12/

16

11/

19/

16

11/

26/

16

12/

3/1

6

Nu

mb

er o

f Ba

rges

Miss. Locks 27 Ark Lock 1 Ohio Locks 52

For the week ending December 03: 678 total barges, down 49 from the previous week, and 17 percent higher than the 3-

year avg.

Figure 12

Grain Barges for Export in New Orleans Region

Source: U.S. Army Corps of Engineers and GIPSA

0

200

400

600

800

1000

1200

8/1

5/1

5

8/2

9/1

5

9/1

2/1

5

9/2

6/1

5

10

/10

/15

10

/24

/15

11/7

/15

11

/21

/15

12/5

/15

12

/19

/15

1/2

/16

1/1

6/1

6

1/3

0/1

6

2/1

3/1

6

2/2

7/1

6

3/1

2/1

6

3/2

6/1

6

4/9

/16

4/2

3/1

6

5/7

/16

5/2

1/1

6

6/4

/16

6/1

8/1

6

7/2

/16

7/1

6/1

6

7/3

0/1

6

8/1

3/1

6

8/2

7/1

6

9/1

0/1

6

9/2

4/1

6

10/8

/16

10

/22

/16

11/5

/16

11

/19

/16

12/3

/16

Downbound Grain Barges Locks 27, 1, and 52

Grain Barges Unloaded in New Orleans

Nu

mb

er o

f b

arges

For the week ending December 03: 683 grain barges moved down river, down 15 percent from last week, 1,007 grain barges were unloaded in New Orleans, down 3 percent from

the previous week.

December 8, 2016

Grain Transportation Report 14

The weekly diesel price provides a proxy for trends in U.S. truck rates as diesel fuel is a significant expense for truck grain move-

ments.

Truck Transportation

Figure 13

Weekly Diesel Fuel Prices, U.S. Average

Source: Retail On-Highway Diesel Prices, Energy Information Administration, Dept. of Energy

1.5

2.0

2.5

3.0

3.5

4.0

06/0

6/1

6

06/1

3/1

6

06/2

0/1

6

06/2

7/1

6

07/0

4/1

6

07/1

1/1

6

07/1

8/1

6

07/2

5/1

6

08/0

1/1

6

08/0

8/1

6

08/1

5/1

6

08/2

2/1

6

08/2

9/1

6

09/0

5/1

6

09/1

2/1

6

09/1

9/1

6

09/2

6/1

6

10/0

3/1

6

10/1

0/1

6

10/1

7/1

6

10/2

4/1

6

10/3

1/1

6

11/0

7/1

6

11/1

4/1

6

11/2

1/1

6

11/2

8/1

6

12/0

5/1

6

Last year Current Year

$ p

er

gall

on

For the week ending December 5: fuel prices increased 6 cents from theprevious week, 10 cents above the same week last year.

Table 11

Change from

Region Location Price Week ago Year ago

I East Coast 2.499 0.053 0.086

New England 2.526 0.054 0.011

Central Atlantic 2.602 0.053 0.060

Lower Atlantic 2.415 0.054 0.120

II Midwest2 2.431 0.075 0.083

III Gulf Coast3

2.361 0.071 0.129

IV Rocky Mountain 2.457 0.007 0.047

V West Coast 2.770 0.043 0.167

West Coast less California 2.679 0.044 0.202

California 2.843 0.043 0.139

Total U.S. 2.480 0.060 0.1011Diesel fuel prices include all taxes. Prices represent an average of all types of diesel fuel.

2Same as North Central 3Same as South Central

Source: Energy Information Administration/U.S. Department of Energy (www.eia.doe.gov)

Retail on-Highway Diesel Prices1, Week Ending 12/5/2016 (US $/gallon)

December 8, 2016

Grain Transportation Report 15

Grain Exports

Table 12

U.S. Export Balances and Cumulative Exports (1,000 metric tons)

Wheat Corn Soybeans Total

For the week ending HRW SRW HRS SWW DUR All wheat

Export Balances1

11/24/2016 2,092 582 2,248 1,290 161 6,373 18,355 17,568 42,295

This week year ago 1,278 671 1,470 1,054 49 4,522 10,398 13,370 28,290

Cumulative exports-marketing year 2

2016/17 YTD 5,575 1,024 3,729 1,992 174 12,493 11,728 24,201 48,422

2015/16 YTD 2,746 1,826 3,149 1,700 481 9,901 6,681 19,419 36,001

YTD 2016/17 as % of 2015/16 203 56 118 117 36 126 176 125 135

Last 4 wks as % of same period 2015/16 161 83 137 110 382 132 169 143 151

2015/16 Total 5,538 3,057 6,285 3,551 670 19,101 45,564 49,821 114,487

2014/15 Total 7,009 3,654 7,250 3,758 665 22,336 45,205 49,614 117,1551 Current unshipped (outstanding) export sales to date

2 Shipped export sales to date; new marketing year now in effect for wheat; new marketing year now in effect for corn and soybeans

Note: YTD = year-to-date. Marketing Year: wheat = 6/01-5/31, corn & soybeans = 9/01-8/31

Source: Foreign Agricultural Service/USDA (www.fas.usda.gov)

Table 13

Top 5 Importers 1 of U.S. Corn

For the week ending 11/24/2016 % change Exports3

2016/17 2015/16 current MY 3-year avg

Current MY Last MY from last MY 2013-2015 - 1,000 mt -

Japan 3,855 2,740 41 11,284

Mexico 8,531 6,990 22 11,204

Korea 2,160 262 724 3,931

Colombia 1,819 1,381 32 4,134

Taiwan 1,376 342 302 1,912

Top 5 Importers 17,741 11,715 51 32,465

Total US corn export sales 30,082 17,079 76 46,633

% of Projected 53% 35%

Change from prior week 747 499

Top 5 importers' share of U.S. corn

export sales 59% 69% 70%

USDA forecast, November 2016 56,616 48,295 17

Corn Use for Ethanol USDA

forecast, November 2016 134,620 132,233 2

1Based on FAS Marketing Year Ranking Reports - www.fas.usda.gov; Marketing year (MY) = Sep 1 - Aug 31.

Total Commitments2

- 1,000 mt -

3FAS Marketing Year Ranking Reports - http://apps.fas.usda.gov/export-sales/myrkaug.htm; 3-yr average

2Cumulative Exports (shipped) + Outstanding Sales (unshipped), FAS Weekly Export Sales Report, or Export Sales

Query--http://www.fas.usda.gov/esrquery/. Total commitments change from prior week could include revisions from

previous week's outastanding sales or accumulated sales.

(n) indicates negative number.

December 8, 2016

Grain Transportation Report 16

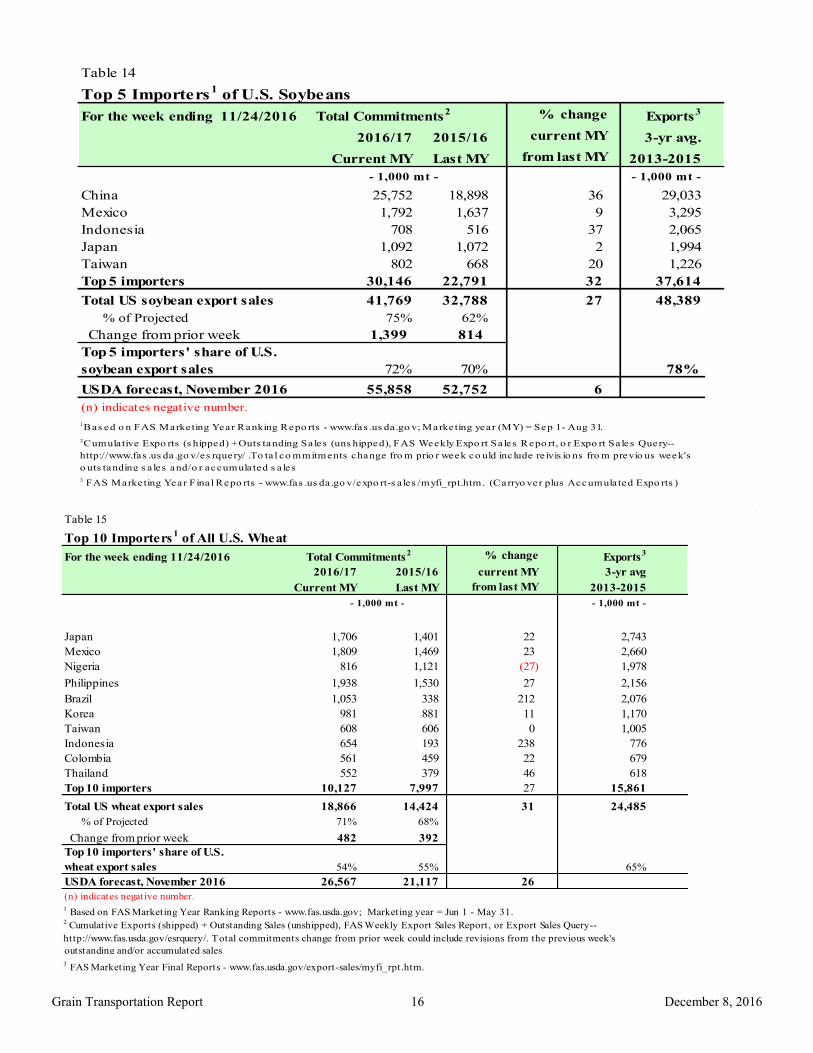

Table 15

Top 10 Importers1 of All U.S. Wheat

For the week ending 11/24/2016 % change Exports3

2016/17 2015/16 current MY 3-yr avg

Current MY Last MY from last MY 2013-2015

- 1,000 mt -

Japan 1,706 1,401 22 2,743

Mexico 1,809 1,469 23 2,660

Nigeria 816 1,121 (27) 1,978

Philippines 1,938 1,530 27 2,156

Brazil 1,053 338 212 2,076

Korea 981 881 11 1,170

Taiwan 608 606 0 1,005

Indonesia 654 193 238 776

Colombia 561 459 22 679

Thailand 552 379 46 618

Top 10 importers 10,127 7,997 27 15,861

Total US wheat export sales 18,866 14,424 31 24,485

% of Projected 71% 68%

Change from prior week 482 392

Top 10 importers' share of U.S.

wheat export sales 54% 55% 65%

USDA forecast, November 2016 26,567 21,117 26

1 Based on FAS Marketing Year Ranking Reports - www.fas.usda.gov; Marketing year = Jun 1 - May 31.

outstanding and/or accumulated sales

Total Commitments2

3 FAS Marketing Year Final Reports - www.fas.usda.gov/export-sales/myfi_rpt.htm.

(n) indicates negative number.

2 Cumulative Exports (shipped) + Outstanding Sales (unshipped), FAS Weekly Export Sales Report, or Export Sales Query--

http://www.fas.usda.gov/esrquery/. Total commitments change from prior week could include revisions from the previous week's

- 1,000 mt -

Table 14

Top 5 Importers1 of U.S. Soybeans

For the week ending 11/24/2016 % change

Exports3

2016/17 2015/16 current MY 3-yr avg.

Current MY Last MY from last MY 2013-2015

- 1,000 mt -

China 25,752 18,898 36 29,033

Mexico 1,792 1,637 9 3,295

Indonesia 708 516 37 2,065

Japan 1,092 1,072 2 1,994

Taiwan 802 668 20 1,226

Top 5 importers 30,146 22,791 32 37,614

Total US soybean export sales 41,769 32,788 27 48,389

% of Projected 75% 62%

Change from prior week 1,399 814

Top 5 importers' share of U.S.

soybean export sales 72% 70% 78%

USDA forecast, November 2016 55,858 52,752 6

1Bas ed o n FAS Marketing Year Ranking Repo rts - www.fas .us da .go v; Marketing year (MY) = Sep 1 - Aug 31.

Total Commitments2

- 1,000 mt -

3 FAS Marketing Year Fina l Repo rts - www.fas .us da .go v/expo rt-s a les /myfi_rpt.htm. (Carryo ver plus Accumula ted Expo rts )

(n) indicates negative number.

2Cumula tive Expo rts (s hipped) + Outs tanding Sales (uns hipped), FAS Weekly Expo rt Sa les Repo rt, o r Expo rt Sa les Query--

http://www.fas .us da .go v/es rquery/ .To ta l co mmitments change fro m prio r week co uld inc lude re ivis io ns fro m previo us week's

o uts tanding s a les and/o r accumula ted s a les

December 8, 2016

Grain Transportation Report 17

The United States exports approximately one-quarter of the grain it produces. On average, this includes nearly 45 percent of U.S.-grown

wheat, 35 percent of U.S.-grown soybeans, and 20 percent of the U.S.-grown corn. Approximately 59 percent of the U.S. export grain ship-

ments departed through the U.S. Gulf region in 2015.

Table 16

Grain Inspections for Export by U.S. Port Region (1,000 metric tons)

For the Week Ending Previous Current Week 2016 YTD as

12/01/16 Week1

as % of Previous 2015 YTD* % of 2015 YTD Last Year Prior 3-yr. avg.

Pacific Northwest

Wheat 230 177 130 11,352 10,028 113 106 113 10,985

Corn 357 61 588 11,346 7,148 159 1248 257 7,232

Soybeans 557 489 114 12,473 10,205 122 130 117 11,809

Total 1,144 727 157 35,171 27,382 128 150 129 30,027

Mississippi Gulf

Wheat 129 5 2,411 3,287 4,270 77 64 69 4,504

Corn 591 529 112 29,418 25,100 117 156 129 26,701

Soybeans 1,137 1,482 77 31,131 25,783 121 117 111 29,593

Total 1,857 2,017 92 63,837 55,152 116 121 113 60,797

Texas Gulf

Wheat 91 57 158 5,454 3,373 162 290 131 3,724

Corn 28 62 45 1,590 596 267 498 684 596

Soybeans 0 73 0 963 770 125 158 148 864

Total 118 192 62 8,007 4,739 169 236 161 5,184

Interior

Wheat 2 18 12 1,422 1,298 110 126 159 1,388

Corn 113 160 71 6,713 5,743 117 149 127 6,201

Soybeans 74 103 71 4,198 3,318 127 161 112 3,518

Total 189 282 67 12,334 10,359 119 151 123 11,106

Great Lakes

Wheat 25 1 n/a 1,003 945 106 114 115 997

Corn 39 0 n/a 558 485 115 n/a 3326 485

Soybeans 63 0 n/a 804 691 116 136 106 733

Total 127 1 n/a 2,366 2,122 111 160 133 2,216

Atlantic

Wheat 0 0 n/a 289 493 59 247 521 520

Corn 0 0 n/a 293 276 106 345 7 277

Soybeans 125 144 87 1,930 1,730 112 108 112 2,053

Total 125 144 87 2,512 2,498 101 112 115 2,850

U.S. total from ports2

Wheat 477 258 185 22,808 20,407 112 119 112 22,118

Corn 1,127 812 139 49,919 39,348 127 206 155 41,492

Soybeans 1,955 2,291 85 51,499 42,497 121 122 114 48,570

Total 3,560 3,361 106 124,226 102,252 121 135 121 112,1801 Data includes revisions from prior weeks; some regional totals may not add exactly due to rounding.

Source: Grain Inspection, Packers and Stockyards Administration/USDA (www.gipsa.usda.gov); YTD= year-to-date; n/a = not applicable

Last 4-weeks as % of:

Port Regions 2015 Total*2016 YTD*

December 8, 2016

Grain Transportation Report 18

Figure 14

U.S. grain inspected for export (wheat, corn, and soybeans)

Source: Grain Inspection, Packers and Stockyards Administration/USDA (www.gipsa.usda.gov)

Note: 3-year average consists of 4-week running average

0

20

40

60

80

100

120

140

160

180

200

4/1

6/20

15

5/1

4/20

15

6/1

1/20

15

7/9

/201

5

8/6

/201

5

9/3

/201

5

10/1

/20

15

10

/29/2

015

11

/26/2

015

12

/24/2

015

1/2

1/20

16

2/1

8/20

16

3/1

7/20

16

4/1

4/20

16

5/1

2/20

16

6/9

/201

6

7/7

/201

6

8/4

/201

6

9/1

/201

6

9/2

9/20

16

10

/27/2

016

11

/24/2

016

12

/22/2

016

1/1

9/20

17

2/1

6/20

17

3/1

6/20

17

Mil

lion

bu

shels

(m

bu

)

Current week 3-year average

For the week ending Dec. 01: 133.8 mbu, up 6 percent from the previous week, up 41 percent from same week last year, and up 16 percent from the 3-year average.

Figure 15

U.S. Grain Inspections: U.S. Gulf and PNW1 (wheat, corn, and soybeans)

-

20

40

60

80

100

120

4/1

6/15

5/1

6/15

6/1

6/15

7/1

6/15

8/1

6/15

9/1

6/15

10/1

6/1

5

11/1

6/1

5

12/1

6/1

5

1/1

6/16

2/1

6/16

3/1

6/16

4/1

6/16

5/1

6/16

6/1

6/16

7/1

6/16

8/1

6/16

9/1

6/16

10/1

6/1

6

11/1

6/1

6

12/1

6/1

6

1/1

6/17

2/1

6/17

3/1

6/17

Mil

lion

bu

shel

s (m

bu

)

Miss. Gulf 3-Year avg - Miss. Gulf

PNW 3-Year avg - PNW

Texas Gulf 3-Year avg - TX Gulf

Source: Grain Inspection, Packers and Stockyards Administration/USDA (www.gipsa.usda.gov)

Last Week:

Last Year (same week):

3-yr avg. (4-wk. mov. Avg):

MS Gulf TX Gulf U.S. Gulf PNW

down 8

up 23

up 7

down 39

up 30

down 12

down 10

up 23

up 6

up 60

up 100

up 48

Percent change from:Week ending 12/01/16 inspections (mbu):

Mississippi Gulf:

PNW:

Texas Gulf:

69.8

43.0

4.4

December 8, 2016

Grain Transportation Report 19

Ocean Transportation

Table 17

Weekly Port Region Grain Ocean Vessel Activity (number of vessels)

Pacific Vancouver

Gulf Northwest B.C.

Loaded Due next

Date In port 7-days 10-days In port In port

12/1/2016 47 50 75 27 n/a

11/24/2016 39 51 79 n/a n/a

2015 range (25..54) (28..54) (36..80) (3..26) n/a

2015 avg. 42 38 56 11 n/a

Source: Transportation & Marketing Programs/AMS/USDA

Figure 16

U.S. Gulf Vessel Loading Activity

0

10

20

30

40

50

60

70

80

90

100

7/1

4/2

016

7/2

1/2

01

6

7/2

8/2

01

6

8/0

4/2

016

8/1

1/2

016

8/1

8/2

016

8/2

5/2

01

6

9/0

1/2

016

9/0

8/2

016

9/1

5/2

016

9/2

2/2

016

9/2

9/2

01

6

10

/06

/20

16

10

/13

/20

16

10

/20

/20

16

10

/27

/20

16

11

/03

/20

16

11

/10

/20

16

11

/17

/20

16

11

/24

/20

16

12

/01

/20

16

Nu

mb

er

of

ve

ssel

s

Loaded Last 7 Days Due Next 10 days Loaded 4 Year Average

Source:Transportation & Marketing Programs/AMS/USDA1U.S. Gulf includes Mississippi, Texas, and East Gulf.

For the week ending December 1 Loaded Due Change from last year 19.0% 8.7%

Change from 4-year avg. 15.6% 23.5%

December 8, 2016

Grain Transportation Report 20

Figure 17

Grain Vessel Rates, U.S. to Japan

Data Source: O'Neil Commodity Consulting

0

5

10

15

20

25

30

35

40

45

50

Nov

. 14

Jan.

15

Mar

. 15

May

15

July

15

Sep

t. 1

5

Nov

. 15

Jan.

16

Mar

. 16

May

16

July

16

Sep

t. 1

6

Nov

. 16

US

$/m

etri

c to

n

Spread Gulf vs. PNW to Japan Rate Gulf to Japan Rate PNW to Japan

Gulf PNW Spread Ocean rates for November '16 $33.69 $18.69 $15.00 Change from November '15 11.4% 14.5% 7.8%

Change from 4-year avg. -23.1% -22.2% -24.1%

Table 18

Ocean Freight Rates For Selected Shipments, Week Ending 12/03/2016

Export Import Grain Loading Volume loads Freight rate

region region types date (metric tons) (US$/metric ton)

U.S. Gulf China Heavy Grain Dec 14/20 53,000 34.00

U.S. Gulf China Heavy Grain Dec 12/20 63,000 36.00

U.S. Gulf China Heavy Grain Dec 10/20 63,000 35.75

U.S. Gulf China Heavy Grain Dec 5/15 60,000 35.75

U.S. Gulf China Heavy Grain Dec 1/10 60,000 35.35

U.S. Gulf China Heavy Grain Nov 20/30 50,000 31.00

U.S. Gulf China Heavy Grain Nov 15/25 50,000 29.00

U.S. Gulf China Heavy Grain Oct 20/30 65,000 27.50

U.S. Gulf China Heavy Grain Oct 10/20 60,000 28.25

U.S. Gulf China Heavy Grain Oct 5/15 66,000 28.00

U.S. Gulf China Heavy Grain Sep 20/25 60,000 27.75

PNW Bangladesh Wheat Dec 1/10 12,500 160.33*

Vancouver China Heavy Grain Nov 1/10 50,000 31.50

PNW Bangladesh Wheat Nov 1/10 12,500 163.55*

PNW Taiwan Wheat Sep 8/22 54,000 21.10

Black Sea Spanish Mediterranean Heavy Grain Oct 14/18 60,000 9.35

River Plate South Africa Soybeans Nov 1/14 25,000 24.00

River Plate Algeria Corn Sep 24/28 40,000 19.50

Ukraine Iran Wheat Oct 10/17 60,000 22.25

Rates shown are per metric ton (2,204.62 lbs. = 1 metric ton), F.O.B., except where otherwise indicated; op = option

*50 percent of food aid from the United States is required to be shipped on U.S.-flag vessels.

Source: Maritime Research Inc. (www.maritime-research.com)

December 8, 2016

Grain Transportation Report 21

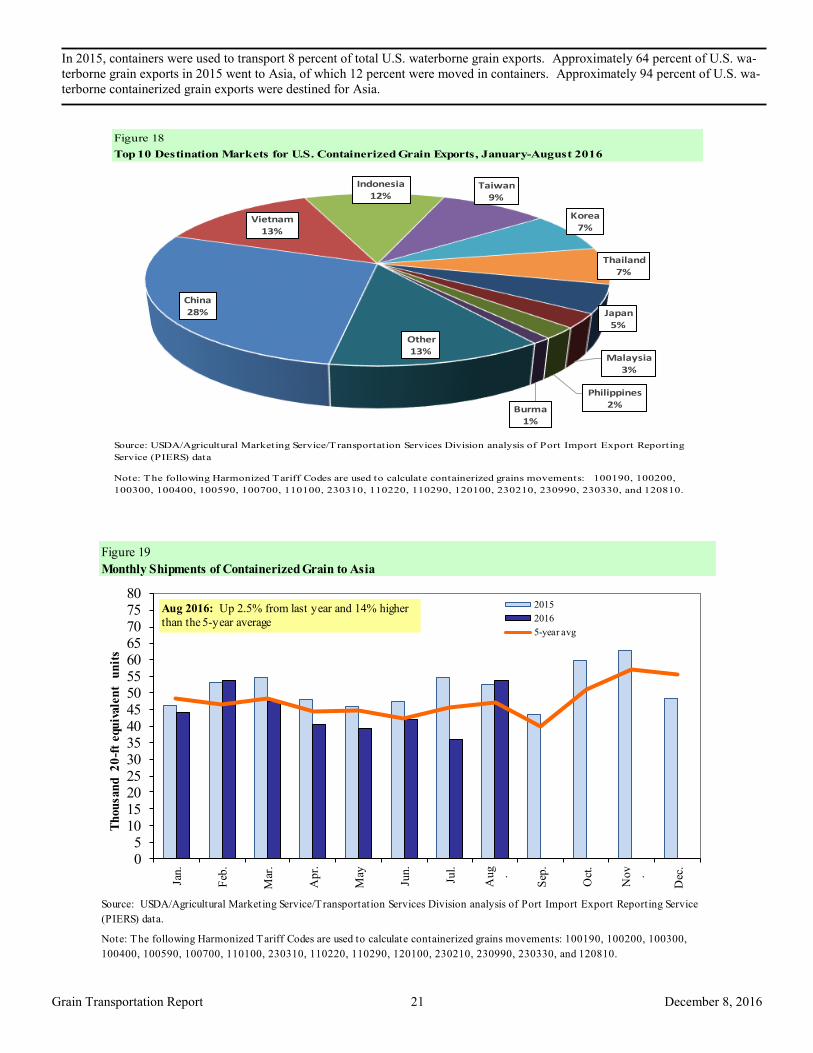

In 2015, containers were used to transport 8 percent of total U.S. waterborne grain exports. Approximately 64 percent of U.S. wa-

terborne grain exports in 2015 went to Asia, of which 12 percent were moved in containers. Approximately 94 percent of U.S. wa-

terborne containerized grain exports were destined for Asia.

Figure 18

Top 10 Destination Markets for U.S. Containerized Grain Exports, January-August 2016

Source: USDA/Agricultural Marketing Service/Transportation Services Division analysis of Port Import Export Reporting

Service (PIERS) data

Note: The following Harmonized Tariff Codes are used to calculate containerized grains movements: 100190, 100200,

100300, 100400, 100590, 100700, 110100, 230310, 110220, 110290, 120100, 230210, 230990, 230330, and 120810.

China28%

Vietnam13%

Indonesia12%

Taiwan9%

Korea7%

Thailand7%

Japan5%

Malaysia3%

Philippines2%Burma

1%

Other13%

Figure 19

Monthly Shipments of Containerized Grain to Asia

Source: USDA/Agricultural Marketing Service/Transportation Services Division analysis of Port Import Export Reporting Service

(PIERS) data.

Note: The following Harmonized Tariff Codes are used to calculate containerized grains movements: 100190, 100200, 100300,

100400, 100590, 100700, 110100, 230310, 110220, 110290, 120100, 230210, 230990, 230330, and 120810.

05

101520253035404550556065707580

Jan

.

Feb

.

Mar

.

Ap

r.

May

Jun

.

Jul.

Aug

.

Sep

.

Oct

.

Nov

.

Dec

.

Th

ou

san

d

20

-ft

equ

ivale

nt

un

its

2015

2016

5-year avg

Aug 2016: Up 2.5% from last year and 14% higher

than the 5-year average

December 8, 2016

Grain Transportation Report 22

Coordinators

Surajudeen (Deen) Olowolayemo [email protected] (202) 720 - 0119

Pierre Bahizi [email protected] (202) 690 - 0992

Weekly Highlight Editors

Surajudeen (Deen) Olowolayemo [email protected] (202) 720 - 0119

April Taylor [email protected] (202) 720 - 7880

Nicholas Marathon [email protected] (202) 690 - 4430

Grain Transportation Indicators

Surajudeen (Deen) Olowolayemo [email protected] (202) 720 - 0119

Rail Transportation

Johnny Hill [email protected] (202) 690 - 3295

Jesse Gastelle [email protected] (202) 690 - 1144

Peter Caffarelli [email protected] (202) 690 - 3244

Barge Transportation

Nicholas Marathon [email protected] (202) 690 - 4430

April Taylor [email protected] (202) 720 - 7880

Matt Chang [email protected] (202) 720 - 0299

Truck Transportation

April Taylor [email protected] (202) 720 - 7880

Grain Exports

Johnny Hill [email protected] (202) 690 - 3295

Ocean Transportation

Surajudeen (Deen) Olowolayemo [email protected] (202) 720 - 0119

(Freight rates and vessels)

April Taylor [email protected] (202) 720 - 7880

(Container movements)

Contributing Analysts

Sergio Sotelo [email protected] (202) 756 - 2577

Subscription Information: Send relevant information to [email protected] for an electronic copy

(printed copies are also available upon request).

Preferred citation: U.S. Dept. of Agriculture, Agricultural Marketing Service. Grain Transportation Report.

December 8, 2016. Web: http://dx.doi.org/10.9752/TS056.12-08-2016

Contacts and Links

In accordance with Federal civil rights law and U.S. Department of Agriculture (USDA) civil rights regulations and policies, the USDA, its

Agencies, offices, and employees, and institutions participating in or administering USDA programs are prohibited from discriminating based on

race, color, national origin, religion, sex, gender identity (including gender expression), sexual orientation, disability, age, marital status, family/

parental status, income derived from a public assistance program, political beliefs, or reprisal or retaliation for prior civil rights activity, in any

program or activity conducted or funded by USDA (not all bases apply to all programs). Remedies and complaint filing deadlines vary by pro-

gram or incident.

Persons with disabilities who require alternative means of communication for program information (e.g., Braille, large print, audiotape, American

Sign Language, etc.) should contact the responsible Agency or USDA's TARGET Center at (202) 720-2600 (voice and TTY) or contact USDA

through the Federal Relay Service at (800) 877-8339. Additionally, program information may be made available in languages other than English.

To file a program discrimination complaint, complete the USDA Program Discrimination Complaint Form, AD-3027, found online at How to

File a Program Discrimination Complaint and at any USDA office or write a letter addressed to USDA and provide in the letter all of the infor-

mation requested in the form. To request a copy of the complaint form, call (866) 632-9992. Submit your completed form or letter to USDA by:

(1) mail: U.S. Department of Agriculture, Office of the Assistant Secretary for Civil Rights, 1400 Independence Avenue, SW, Washington, D.C.

20250-9410; (2) fax: (202) 690-7442; or (3) email: [email protected].

USDA is an equal opportunity provider, employer, and lender.