government (corporate) governance implementation guide€¦ · · 2009-07-285.4.1 strategic...

TRANSCRIPT

GOVERNMENT (CORPORATE) GOVERNANCE

IMPLEMENTATION GUIDE June 2008

(Commitment to Purpose)

PROVINCIAL TREASURY PROVINCIAL GOVERNMENT

WESTERN CAPE

i

Government (Corporate) Governance Implementation Guide, June 2008

Table of Contents Page

1. INTRODUCTION .......................................................................................................... 1

1.1 Background................................................................................................................... 1

1.2 Purpose ........................................................................................................................ 1

2. DEFINITION OF GOVERNANCE................................................................................. 2

3. WHY IS GOVERNANCE IMPORTANT?...................................................................... 2

4. IMPLEMENTING GOVERNMENT GOVERNANCE..................................................... 3

5. COMPONENTS OF GOVERNMENT GOVERNANCE FRAMEWORK ....................... 3

5.1 Stakeholders................................................................................................................. 3

5.1.1 Voters ........................................................................................................................... 3

5.1.2 Service Delivery............................................................................................................ 3

5.1.3 Partnerships.................................................................................................................. 4

5.1.4 Judiciary........................................................................................................................ 4

5.1.5 Government.................................................................................................................. 4

5.1.6 Prescripts...................................................................................................................... 4

5.1.7 Cluster System ............................................................................................................. 4

5.2 Principles and Values ................................................................................................... 5

5.2.1 Accountability................................................................................................................ 5

5.2.2 Conflict of Interest......................................................................................................... 5

5.2.3 Transparency................................................................................................................ 5

5.2.4 Integrity ......................................................................................................................... 5

5.2.5 Stewardship.................................................................................................................. 6

5.2.6 Leadership .................................................................................................................... 6

5.2.7 Commitment ................................................................................................................. 6

5.2.8 Sustainability................................................................................................................. 6

5.2.9 Fairness ........................................................................................................................ 7

5.2.10 Efficiency, Effectiveness, Economical .......................................................................... 7

ii

Government (Corporate) Governance Implementation Guide, June 2008

5.2.11 Responsibility towards purpose.................................................................................... 7

5.2.12 Honesty......................................................................................................................... 7

5.2.13 Public Service Principles .............................................................................................. 7

5.3 Management Challenges.............................................................................................. 8

5.3.1 Citizen Focus................................................................................................................ 8

5.3.2 Managing for results ..................................................................................................... 8

5.3.3 Responsible spending .................................................................................................. 9

5.3.4 Objectives of Governance Excellence.......................................................................... 9

5.4 Functional Application Areas ........................................................................................ 9

5.4.1 Strategic Leadership..................................................................................................... 9

5.4.2 Management and Stewardship..................................................................................... 9

5.4.3 Performance Measures .............................................................................................. 10

5.4.4 Control ........................................................................................................................ 10

5.5 Governance Specific Activities ................................................................................... 10

5.5.1 Control Environment................................................................................................... 10

5.5.2 Control Activities......................................................................................................... 10

5.5.3 Information and Communication ................................................................................ 10

5.5.4 Enterprise Risk Management ..................................................................................... 11

5.5.5 Monitoring Activities.................................................................................................... 11

5.6 The Governance Universe.......................................................................................... 11

5.6.1 Integration with other processes................................................................................. 11

5.7 Continuous Improvement ........................................................................................... 12

5.7.1 Internal Changes ........................................................................................................ 12

5.7.2 External Changes ....................................................................................................... 12

5.8 Planning Process Monitoring...................................................................................... 12

5.9 Alignment with current budget process ...................................................................... 13

6. WAY FORWARD........................................................................................................ 13

7. CONCLUSION............................................................................................................ 14

APPENDIX A: IMPLEMENTATION GUIDE ........................................................................... 15

iii

Government (Corporate) Governance Implementation Guide, June 2008

Glossary ALO Activity Level Objective

API Activity Performance Indicator

BBBEE Broad Based Black Economic Empowerment

Constitution The Constitution of the Republic of South Africa, Act 108 of 1996

EPI Entity Performance Indicator

EWO Entity – Wide Objectives

Framework Governance Framework

GGF Government Governance Framework

King II King Report on Corporate Governance for South Africa- 2002

KMO Key Measurable Objective

KPI Key Performance Indicator

KRA Key Result Area

MTP Medium Term Plan

NGO Non Governmental Organisation

OECD Organisation for Economic Co-operation and Development

PFMA Public Finance Management Act 1 of 1999 (as amended by Act 29 of 1999)

PGWC Provincial Government Western Cape

PSC Public Service Commission

PPP Provincial Public Partnership

SSC Sihlume Sisonke Consortium

RPI Result Performance Indicator

PGWC GOVERNMENT GOVERNANCE IMPLEMENTATION STRATEGY

1. Introduction 1.1 Background

The PFMA King II on Corporate Governance and the GGF require the

provincial government to continuously strive toward and improve governance

excellence.

In order to meet the above, a departmental roadmap for the implementation of

government governance, based on the GGF was compiled to address specific

issues highlighted in the response strategy document.

1.2 Purpose

The purpose of this implementation guide is to enable management to

implement government governance in their departments. This creates a

situation where current activities can be automatically aligned with

governance practices during the normal cause of the day-to-day operations. It

further enables management to keep track of the level of progress made.

Allow them to use the guide as a reference document to keep track of the

linkages between the various components of the GGF. It would also allow

departments to systematically implement government governance in a

coordinated manner across all the departments.

1

This systematic approach allows the implementation to take place and to

make adjustments when required, without loosing the momentum of

implementation or slowing down the progress made. The differences

between departments are explicitly obvious and it can be assumed that some

departments will be able to proceed at a faster pace with implementation than

other departments. With the implementation guide, it is therefore possible, to

have a coordinated implementation initiative on the one hand and at the same

time allowing those departments that are ready, to continue the

implementation process without being negatively influence by those that

proceed at a slower pace. This enhances a seamless implementation

process.

Government (Corporate) Governance Implementation Guide, June 2008

The implementation guide further allows those responsible for coordinating

the implementation to monitor the progress made by departments in a

standardised manner. The implementation guide also allows the department

to consider various output indicators that can be considered to develop

measuring indicators and performance indicators on throughout the different

plans.

Although “Annexure A” attached does not provide all the detail that can be

applied during the alignment process, it can form the basis to develop

alignment schedules that are uniquely developed to meet the requirement of

individual departments. Therefore, it provides a guide rather that a prescript,

and should be adjusted by individual departments to develop their own

alignment practices.

2. Definition of Governance

Government governance is defines as providing stakeholder assurance that

abilities are applied in such a manner that objectives will be achieved

effectively and efficiently in an agreed ethical environment.

3. Why is Governance important?

The PFMA promotes the objective of good financial management, in order to

maximise delivery through the efficient and effective (economic) use of limited

resources.

Government governance is more than the effective prevention of

irregularities, fraud, financial misconduct, etc. And it is not just about

compliance and control; it is also about a framework of principles that

facilitate the organisations’ ability to achieve its long-term objectives efficiently

and effectively.

It is also about maintaining specific performance over the long-term and it is

about assurance that all these activities are done in an ethical environment.

2

Government (Corporate) Governance Implementation Guide, June 2008

4. Implementing Government Governance

When implementing a government governance culture it is important;

• to recognise the role of the stakeholders;

• define the functional application areas necessary to assist those

responsible to provide assurance of excellence in governance;

• understand the governance environment within which these functional

application areas operate, and

• identify and select the applicable ethical values necessary to ensure

governance excellence in each endeavour.

5. Components of Government Governance Framework

5.1 Stakeholders

PGWC has a variety of stakeholders each with their unique expectations

based on their relationship with government. The choice of who can be a

stakeholder is a limited one for government. By definition the majority

stakeholders is the citizens that can vote for a specific “government” / political

party during an election, an option not available to government who cannot

select citizens to be stakeholders. This section briefly describes some of the

stakeholders government has, to emphasise this diversity and accompanied

complexities.

5.1.1 Voters

The main stakeholders in PGWC are its citizens who have a voting power that

they can exercise every five years

5.1.2 Service Delivery

There are limited resources available for PGWC to deliver adequate service

to the stakeholders. It appears if trend is becoming more apparent where a

yearly decline in resources is experienced whilst at the same time the

requirement for additional services increases

3

Government (Corporate) Governance Implementation Guide, June 2008

5.1.3 Partnerships

Partnerships between the PGWC and others (NGO’s, PPP, BBBEE etc.) in

delivering services bring a specific emphasis to the development of a GGF.

These partnerships are essential in service delivery and it is important that

government exercises care when establishing and maintaining these

relationships.

5.1.4 Judiciary

The media has contributed to the awareness that the majority of the citizens

lack access to the judiciary because of a variety of reasons of which financial

means is but one.

5.1.5 Government

Government consisting of Parliament (Legislator), Cabinet (Executive) and

Administration is responsible at various levels to ensure that services are

provided to citizens as mandated in the Constitution.

5.1.6 Prescripts

As indicated in the GGF’s foreword, the PFMA promotes the objective of good

financial management, in order to maximise service delivery through the

efficient and effective use of limited resources. However, there are a number

of existing legislation and other prescripts also bearing impact on the activities

of a department.

5.1.7 Cluster System

Introducing and implementing the cluster system is aimed at improving the

effectiveness of service delivery by co-ordinating similar projects within the

departments. The co-ordination will be the responsibilities of lead

departments. The system aims to provide coordination to minimise the cost

of service delivery by reducing the duplication of similar services across the

various departments. The aim is also to develop communities by providing a

comprehensive improvement to services compared to the scattered activities

by departments.

4

Government (Corporate) Governance Implementation Guide, June 2008

5.2 Principles and Values

It represents the attitude and spirit with which important and mundane

activities are daily performed by personnel. It is the standard by which

service delivery is conducted both internally and externally and express.

5.2.1 Accountability

Accountability is fundamental to our democratic system of government as it is

embedded in section 195(e) of the Constitution and assigned to the PSC to

ensure compliance.

The GGF require of those involved, to identify and articulate their

responsibilities and their relationships; to consider who is responsible for

what, to whom, and by when; to acknowledge the relationships that exist

between stakeholders and those who are entrusted to manage resources;

and to deliver required outputs and outcomes whilst sharing a common value

system.

5.2.2 Conflict of Interest

As indicated by literature, a person in public service cannot serve two

masters. Government needs to have explicit guidelines about what

constitutes conflicts of interest and what to do about it whenever these occur

or might occur.

5.2.3 Transparency

The Constitution mandates the PSC to ensure that government exercises

transparency by providing the public with timely, accurate and accessible

information. There appears to be consensus globally in the public and private

sectors that transparency is the foundation for ensuring observance of all

governance principles and without such the pressure to adhere to principles

diminishes resulting in difficulties to achieve governance excellence.

5.2.4 Integrity

Integrity is based on honesty and objectivity, and high on the standards in the

stewardship of public funds and the management of a department’s affairs. It

is dependent on the effectiveness of the control framework and on the

personal standards and professionalism of the individuals within the

department. Integrity is reflected in decision-making practices and procedures

5

Government (Corporate) Governance Implementation Guide, June 2008

and in the quality and credibility of its performance reporting. It is a key

element in the development of social capital and the value placed on it should

constantly be made clear to all.

5.2.5 Stewardship

Public officials (ministers, public servants and office holders) exercise their

powers on behalf of the nation. The resources they use are held in trust and

are not privately owned. Officials are therefore stewards of those powers and

resources. This requires that they ensure financial sustainability and the

efficient and effective management of resources, as well as maintaining less

tangible factors, such as the trust placed in government as a whole.

5.2.6 Leadership

Effective public sector governance requires leadership from those entrusted

to govern. This requires clear identification and articulation of responsibility

and a real understanding and appreciation of the various relationships

between the organisation’s stakeholders and those who are entrusted to

manage resources and deliver required outcomes. Leadership is a quality that

excels on education, experience and personal qualities and those entrusted

to lead should be worthy to do so.

5.2.7 Commitment

Public sector governance excellence requires a strong commitment by all

participants to effectively implement all elements of financial governance. The

GGF is very much people oriented, involving better communication; a more

systematic approach to corporate management; a greater emphasis on

corporate values and ethical conduct; risk management; relationships with

citizens and clients; and accentuate quality of service delivery.

5.2.8 Sustainability

The principle of sustainability is especially important within the South African

context where development is paramount and the resources to address the

variety of factors confronting the National Government and Provincial

Government are limited.

6

Government (Corporate) Governance Implementation Guide, June 2008

5.2.9 Fairness

The Constitution assigns to the PSC the responsibility to ensure that the

public service operates in such a manner that it is fair, equitable and without

bias.

5.2.10 Efficiency, Effectiveness, Economical

Section 195 (d) of the Constitution assigns to the PSC the objective to ensure

that the public service operates in such a manner that it is effective and to

standard of professional values. To ensure that resources are applied in an

optimum manner and the maximum results are received from every input that

is made in achieving objectives. It ensures that more services can be

delivered at the same cost and that recourses are optimally used and

progress being monitored.

5.2.11 Responsibility towards purpose

The GGF empowers management to limit unnecessary changes to previously

determined objectives while at the same time sensitising management to

consider the future value of new objectives before including them in the

different plans. It provides the means to sufficiently scrutinise the future role

and value of a specific objective. Once this has taken place, responsibility

towards purpose becomes a reality and one of the cornerstone values that

can ensure the successful achievement of objectives.

5.2.12 Honesty

Honesty is one of the universal values incorporated into the value system of

the GGF that appears to be applicable to all persons in all activities when

performing their duties and / or when they are involved in delivering services.

Honesty is a personal trait and a critical element when development of social

capital is performed. GGF relies on this value especially in circumstance

where funds are limited to implement controls that can sometimes be very

costly.

5.2.13 Public Service Principles

It is important to note four basic sets of principles that are guidance to

departments:

7

Government (Corporate) Governance Implementation Guide, June 2008

Respect for democracy that recognises that authority lies with democratically

elected officials who are accountable to parliament and thereby to the

citizens. A well performing public service takes its democratic responsibilities

seriously, constantly providing ministers.

Deliver Quality Services that require government employees to provide high

quality; impartial advice on policy issues while committing to the design,

delivery and continue an improvement of programmes and services.

Ethical Environment (integrity, trust and honesty etc.) that forms the personal

cornerstone of governance excellence and democracy. They require the

public servants to support the common good at all times and recognise the

need for openness, transparency and accountability in what they do and how

they do it.

Respect for the individual that requires that everyone should be treated with

respect, decency, responsibility and humanity. In a well performing

workplace, they show themselves in respect, civility, fairness and caring.

5.3 Management Challenges

5.3.1 Citizen Focus

The GGF provides mechanisms to consider designing, delivering, evaluating,

reporting on its activities and monitoring when planning service delivery to

citizens.

Initiatives such as Batho Pele, iKapa Elihlumayo, iKapa GDS, AsgiSA have

little value if it does not result in an improved and sustainable service delivery

to its citizens. The GGF equips management with a process so that the

objectives of these initiatives can be achieved successfully.

5.3.2 Managing for results

In developed countries management for results is based on citizens’ concern

for value obtained for taxes paid. Whilst a portion of the citizens are

concerned about the value they receive for taxes paid the majority is

concerned about the service they perceive to be rightly theirs. Whichever

may be the case the fact remains that service delivery is an important issue

and therefore, so is managing for results.

8

Government (Corporate) Governance Implementation Guide, June 2008

5.3.3 Responsible spending

The PGWC needs to strike a balance between investing in service

improvement, maintaining the integrity of existing programs and developing

new programs, whilst coping with budgetary constraints.

5.3.4 Objectives of Governance Excellence

Governance excellence is a shared responsibility, between provincial

departments, private associations, companies, investors and other parties

committed to improving governance practices a requirement for governance

excellence as indicated by OECD principles.

The PGWC needs to rise to the governance challenges that provide real

stakeholder value by focussing on the needs of the citizens, and at the same

time operates within predetermined public service values.

5.4 Functional Application Areas

This section defines functional application areas or managerial processes that

are incorporated by the GGF to enable employees in the province to

discharge their duties in a manner that has been recognised as being an

important cornerstone in governance excellence by public sector agencies

across the globe.

5.4.1 Strategic Leadership

Strategic Leadership refers to the awareness and commitment of managers at

all levels to establish and sustain a “results orientated environment” where

modern management practices are supported by strong and effective

functional advice, corporate planning and resource allocation and reallocation

processes and mechanisms.

5.4.2 Management and Stewardship

Public sector governance as approached in the GGF encompasses how a

department is managed, its functional structures, its culture, its policies and

strategies, and the ways in which it deals with various stakeholders.

Governance often is a combination of legal and organisational structure and

management requirements, aimed at facilitating accountability and improving

performance.

9

Government (Corporate) Governance Implementation Guide, June 2008

5.4.3 Performance Measures

Management must determine the content and frequency of reports regarding

performance in general. Clear criteria can be developed and applied to

measure the performance of staff, relevant stakeholders i.e. suppliers/private

partnerships as well as the progress made towards achieving objectives.

5.4.4 Control

Control is regarded as a process, affected by management designed to

provide reasonable assurance that risks are mitigated to ensure the

achievement of objectives. It assigns the responsibility to all employees to

ensure that controls are operational and effective. However, the ultimate

responsibility and accountability for controls rests with management.

5.5 Governance Specific Activities 5.5.1 Control Environment

Governance takes place within a specific control environment where

management and employees establish and maintain an environment

throughout the department that sets a positive and supportive attitude toward

internal control. This section addresses the “soft issues” in the managerial

processes that are at most times hard to evaluate with regard to influence and

existence, and difficult to control and monitor.

5.5.2 Control Activities

The GGF has as its basis internal control activities, which are expressed in

policies, procedures, techniques, and mechanisms that help ensure that

management's directives to mitigate risks that were identified during the risk

assessment process are carried out. Control activities are an integral part of

the planning, implementing, and reviewing processes. They are essential for

proper stewardship and accountability for government resources and for

achieving effective and efficient program results.

5.5.3 Information and Communication

10

Management must have relevant, reliable information, both financial and non-

financial, relating to external as well as internal events to manage and control

its operations. Information that needs to be identified should be recorded and

communicated to management and others within the department who need it.

Government (Corporate) Governance Implementation Guide, June 2008

It allows management to determine the format and time frame of the

information required to assist them to carry out their internal control and

operational responsibilities.

5.5.4 Enterprise Risk Management

Based on best practices researched, effective risk management that is based

on regular information on which to perform competent judgments is regarded

as mandatory when aiming for governance excellence. It incorporates the

understanding that the precondition to risk assessment is the establishment of

clear, consistent management goals and objectives at both the entity level

and at the activity (program or mission) level.

5.5.5 Monitoring Activities

Monitoring is the final internal control standard incorporated and it ensures

that internal control monitoring assesses the quality of performance over time

and that the findings of audits and other reviews are promptly resolved. This

enables management to consider the degree to which the continued

effectiveness of internal control is monitored, both ongoing monitoring

activities and separate evaluations of the internal control system, or portions

thereof.

5.6 The Governance Universe

The governance universe organises all management activities and processes

into a meaningful whole. It aims to bring about a comprehensive

understanding of the individual aspects and the possible combinations of

choices and strategies management can follow.

5.6.1 Integration with other processes

The financial government governance processes are driven by principles and

values that cannot be limited to pre-selected focus areas. It flows through all

daily activities and it is embedded in the attitude and aptitude of the

employees performing these activities.

11

Government (Corporate) Governance Implementation Guide, June 2008

5.7 Continuous Improvement

It is important that efforts to establish Governance excellence in PGWC are

sustainable by including processes that ensure the GGF is continually

updated with global developments and specific developments within the

Western Cape Province.

5.7.1 Internal Changes

Internal developments based on changes in objectives, potential risk and

recommendations as a result of other investigations needs to be constantly

monitored and acted upon.

Reports received form separate evaluations such as Risk Assessment and

Internal Audit and will be reviewed to identify possible government

governance related issues. If analysis of the reports reflects a shortcoming

related to governance issues processes the specific area or areas i.e.

strategic, structural relationships, performance measures, control assurance

will be addressed.

5.7.2 External Changes

A change management process pertaining to the governance framework was

developed in co-operation with SSC to ensure latest developments occurring

outside the government sector are considered for incorporation into the

Framework and ultimately into the governance processes as daily performed

by the departments within the PGWC.

5.8 Planning Process Monitoring

Governance excellence is determined by how well the planning processes

have been performed. It starts with determining long-term objectives and then

selecting the activities required to achieve these objectives over the

determined time period. In its basic form it means having objectives that are

broken down into the different activities that must be performed to achieve the

objectives.

12

It is important to give thorough consideration to each activity that is required

to achieve an objective. It is when the activities are performed that resources

are required and the manner in which they are performed that will determine

the effectiveness, efficiency and the ethical environment, all of which

culminating in projecting a typical corporate identity.

Government (Corporate) Governance Implementation Guide, June 2008

5.9 Alignment with current budget process

The point of departure in this process is the five years electoral cycle

functioning in the Republic of South Africa.

The overarching goals and objectives of the new government are translated

into strategic goals, strategic objectives and measurable objectives that are

contained in the strategic and performance plan.

These plans are developed within the resource envelope specified by the

current Medium Term Economic Framework (MTEF) An annual performance

plan is developed that reflects the measurable objectives and performance

targets for the current fiscal year and the next two years. Annual performance

agreements of accounting officers are directly linked to the annual

performance plan and the annual budget.

6. Way Forward

In order to address the significant governance issues facing departments, the

key implementation approach is following the above GGF approach to:

• Assess current state by comparing the department to the attached

implementation guide e.g.

o Has stakeholders been identified

o Have the stakeholders relationship been defined

o Review departmental governance environment

o Define and agree on Values

o Align elements of the Strategic Leadership and Planning

o Align elements of Management and Stewardship

o Align elements of Control Assurance

o Align and agree on Governance Related Activities

Elements in Control Environment

Elements in Enterprise Risk Management

Elements in Information Communication

Elements in Control Activities

Elements in Monitoring

• Develop a Response strategy

13 Government (Corporate) Governance Implementation Guide, June 2008

14

Government (Corporate) Governance Implementation Guide, June 2008

• Conduct awareness campaigns

• Develop orientation programs for new employees

• Ensure continuous monitoring and evaluation of implementation.

7. Conclusion

The full implementation of the departmental governance guide together with

the GGF and the Enterprise Risk Management Framework will assist in

ensuring governance excellence within the PGWC and its ability to achieve its

long-term objectives efficiently and effectively.

Appendix A: Implementation Guide

GOVERNANCE IMPLEMENTATION GUIDE & TOOLKIT Development program Critical

Issues Phase 1 Phase 2 Phase 3 Training Complete

Stakeholders: Chapter 2; Pg 15

• Identified

• Nature of relationships determined

• Documented

• Communicated

• Communication responsibility assigned

Principles and values: Chapter 3; Pg 21

Selecting the key values. • Selected

• Documented

• Communicated

• Linked to Relevant Activities

Corporate culture

• Determined

• Communicated

• Monitored Key Values Accountability

• Assigned

• Linked to relevant activities

• Linked with decision making enablement

• Monitored

• Communicated Conflict of interest

• Must be documented

• linked to specific elements

• Monitored

• Communicated

• Acknowledge

15

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

16

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Transparency

• Linked to relevant areas

• Inputs are documented

• Inputs Acknowledge

• Subjected to consideration

• Decisions communicated to all concerned

Integrity • Required Standards

Determined

• Communicated

• Acknowledged

• Monitored Stewardship

• Stewardship determined

• Linked to related activities

• Assigned

• Acknowledge

• Monitored

Leadership

• Determined

• Linked to relevant elements

• Assigned

• Acknowledged

• Monitored

Commitment

• Linked with relevant activities

• Reconciled with existing skills based

• Monitored Sustainability

• Linked to objectives

• linked to activities

• Assigned

• Acknowledged

• Monitored

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

17

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Fairness

• Linked to activities

• Assigned

• Acknowledge

• Monitored Efficiency

• Linked to activities

• Assigned

• Acknowledge

• Monitored

Effectiveness • Linked to activities

• Assigned

• Acknowledge

• Monitored

Economical • Linked to activities

• Assigned

• Acknowledge

• Monitored Responsibility towards purpose

• Linked to objectives

• Assigned

• Acknowledge

• Monitored

Honesty • Linked to relevant

activities

• Assigned

• Acknowledge

• Monitored

Functional application areas STRATEGIC LEADERSHIP Strategic Plan: Chapter 5; Pg 40

• Specific planning process

• Relationship and contents of different plans

• Covers at least 5 Years

• Reflect EWO/ Entity Wide objectives

• Reflects legislative

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

18

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

support for strategic objectives

• Communicated

• Linked to budget

• Linked to existing resources

• Reflects resource requirements

• Reflects lifecycle

• Reflects assumptions

• Reflects risk appetites and strategies

Maintained

• Rolling plan

• Adjustments

• Recorded

• Motivated

• Approved Progress Measured

• Measurable indicators developed

• Entity Performance Indicators EPI

• Linked EWO with EPI

• Assigned

• Acknowledge

• Regularly monitored

Governance environment • Effectiveness regularly

reviewed

• Effectiveness regularly tested

• Compliance ensured

• unexpected results are investigated

• Reflects ethical values

• Reflects predetermined culture

• Reflects management reaction towards violations

• Linked to other plans

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

19

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Annually Reviewed

• Annually Approved

• Feeds into Medium Term Plan

Medium Term Plan: Chapter 5; Pg 41

• Covers at least 3 - 5 Years

• Reflect KRA Key Result Area

• Communicated

• Linked to budget

• Linked to existing resources

• Reflects resource requirements

• Reflects lifecycle

• Reflects assumptions

• Reflects risk appetites and strategies

Maintained

• Rolling plan

• Adjustments

• Recorded

• Motivated

• Approved

Progress Measured

• Measurable indicators developed

• Result Performance Indicators RPI

• Linked KRA with RPI

• Assigned

• Acknowledge

• Regularly monitored

• Governance environment

• Effectiveness regularly reviewed

• Effectiveness regularly tested

• Compliance ensured

• unexpected results are investigated

• Linked to other plans

• Annually Reviewed

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

20

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Annually Approved

• Feeds into Annual Business Plan

Annual Business plan: Chapter 5; Pg 42

• Covers at least 2 - 3 Years

• Reflect KMO Key Measurable Objectives

• Communicated

• Linked to budget

• Linked to existing resources

• Reflects resource requirements

• Reflects lifecycle

• Reflects assumptions

• Reflects risk appetites and strategies

Maintained

• Rolling plan

• Adjustments

• Recorded

• Motivated

• Approved

Progress Measured

• Measurable indicators developed

• Key Performance Indicators KPI

• Link KMO with KPI

• Assigned

• Acknowledge

• Regularly monitored

• Governance environment

• Effectiveness regularly reviewed

• Effectiveness regularly tested

• Compliance ensured

• unexpected results are investigated

• Linked to other plans

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

21

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Annually Reviewed

• Annually Approved

• Feeds into Operational Plan

Operational Business plan: Chapter 5; Pg 42

• Covers at least 1-2 Years

• Reflect ALO Activity Level Objectives

• Communicated

• Linked to budget

• Linked to existing resources

• Reflects resource requirements

• Reflects lifecycle

• Reflects assumptions

• Reflects risk appetites and strategies

Maintained

• Rolling plan

• Adjustments

• Recorded

• Motivated

• Approved Progress Measured

• Measurable indicators developed

• Activity Performance Indicator

• Linked ALO with API

• Assigned

• Acknowledge

• Regularly monitored

• Governance environment

• Effectiveness regularly reviewed

• Effectiveness regularly tested

• Compliance ensured

• unexpected results are investigated

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

22

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Linked to other plans

• Annually Reviewed

• Annually Approved

• Feeds into System of Internal Control

Budget: Chapter 10; pg 77

• Aligned with prescripts

• Documented

• Linked with plans

• Approved

• Accountability assigned and accepted

• Linked with objectives

• Linked with activities

• Linked with measuring indicators

• Monitored

• Maintained

• Reviewed

• Adjusted timely

HR Plan: Chapter 5; Pg 42

• Documented

• Assess human resources need

• Linked with Plans

• Documents skills require

• Reconcile skills requirements with resource demands

• Analyses differences between resource needs supply available

• Document strategy to meet Hr needs of departments

• Monitor and evaluate

Vacancies

• Filled timeously

• Salary levels are market related

• Service delivery not effected by delays

• Filled with right skills

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Job Descriptions & performance Agreements

• Tasks defined linked to objectives

• Reflects Authority assigned

• Reflects key control responsibilities

• Authority & Responsibility based on employee involve

• Authority and responsibility acknowledge by employees

Analysis of knowledge skill & abilities

• Employees selected has the required knowledge and skills

• Job descriptions are up to date

• Task, skill & abilities required are linked to objectives

• Task, skill & abilities required are communicated to employees

HR Policies & Practices

• Hiring policy exist

• Training policy exist

• Counselling policies exist

• Orientation policies exist

• Promotion policies exist

• Performance policies exist

• Evaluation policies exist

• Grievance policies exist

• Exit policy exist

• Position descriptions and qualifications linked to objectives

23

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Performance Management

• Performance appraisals are linked to objectives in strategic plan

• Performance appraisals are linked to operational performance indicators

• Performance appraisals includes assessing ethical values

• Employees receive feedback on performance appraisals

• Disciplinary and or remedial action are taken when violations occur

• HR plan exist to deal with large numbers of vacancies occur

Background checks

• Background check are performed on applications

• Reference are contacted

• Qualifications are confirmed

Training & counselling • Programs exist to

maintain and improve existing competencies

• Training programs meets the career demands of all employees

• Ongoing training are provided

• Candid job counselling are provided

• Supervisor receive skill training to provide constructive job counselling

Personnel turnover • Critical control and key

areas are monitored to detect un acceptable personnel turnover

• Key personnel have e not quit unexpectedly

• No patterns are apparent that relates to excessive focus on control

24

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Management human capital

• HR communicates all relevant information to employees

• Leaders type has been defined

• Focus is place on developing teamwork

• Focus placed on recruiting competent people on all levels

• Compensation system is adequate and market related to retain employees

• Flexible and workplace, work environment, casual dress codes flexi time is provided

IT Plan: Chapter 5; Pg 42

• Assess human resources need

• Linked with Plans

• Documents skills require

• Reconcile skills requirements with resource demands

• Analyses differences between resource needs supply available

• Document strategy to needs Hr needs of departments

• Monitor and evaluate Strategic Assets: Chapter 5; Pg 42

• Documented

• Assess human resources need

• Linked with Plans

• Documents skills require

• Reconcile skills requirements with resource demands

• Analyses differences between resource needs supply available

25

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Document strategy to needs Hr needs of departments

• Monitor and evaluate

Application Area Management & Stewardship: Chapter 5; Pg 44

General Control Activities

• Reflects policies and procedures

• Reflect control needed

• Linked to risk profile

• Proper application monitored

• Periodically reviewed

• Timely action taken when failure occurs

• Improvements considered when appropriate

• Implements exception reports

• Periodically approved

• Linked with purpose of control

• Accountability assigned

• Accomplishment of objectives

Business Processes: Chapter 5; Pg 44

• Process flowcharts

• Reflect Key Control areas

• Reflect Control Objective

• Linked with ALO

• Linked with budget

• Linked with HR

• Linked with IT

• Linked with Strategic Assets

• Reflects relevant governance Environment activities

26

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Linked with operational performance indicator

• Regularly updated with best practices

Structure & Relationship: Chapter 5; Pg 45

• Documented

• Documented relationships

• Documents Authority Assignments

• Documents accountability assignment

• Linked with process flowcharts

• linked Key Control areas

• Reflect Control Objective

• Linked with ALO

• Linked with budget

• Linked with HR

• Linked with IT

• Linked with Strategic Assets

• Reflects relevant governance Environment activities

• Linked with operational performance indicator

• Feeds into Organisational Structure

Organisational structure: Chapter 5; Pg 45

• Documented

• Documents Authority Assignments

• Documents accountability assignment

• linked with Structure and relationship

• Linked with process flowcharts

• Linked Key Control areas

• Linked with ALO

• Linked with budget

• Linked with HR

27

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Linked with IT

• Linked with Strategic Assets

• Reflects relevant governance Environment activities

• Linked with operational performance indicator

• Feeds into Roles and relationships

Governance environment

• Size is appropriate for operations

• size facilitate flow of information

• Key areas of Authority

• Kea areas identified

• Key areas communicated

• Update chart provided to all employees

• Those authorised understand their responsibilities

• Structure periodically reviewed

• Adequate capacity exist

• No excessive overtime

• One employee on job

• Proper Supervision

• On the job training is provided & processing Transactions

• Guidance is provided to enable workflow

• Employees understand their tasks

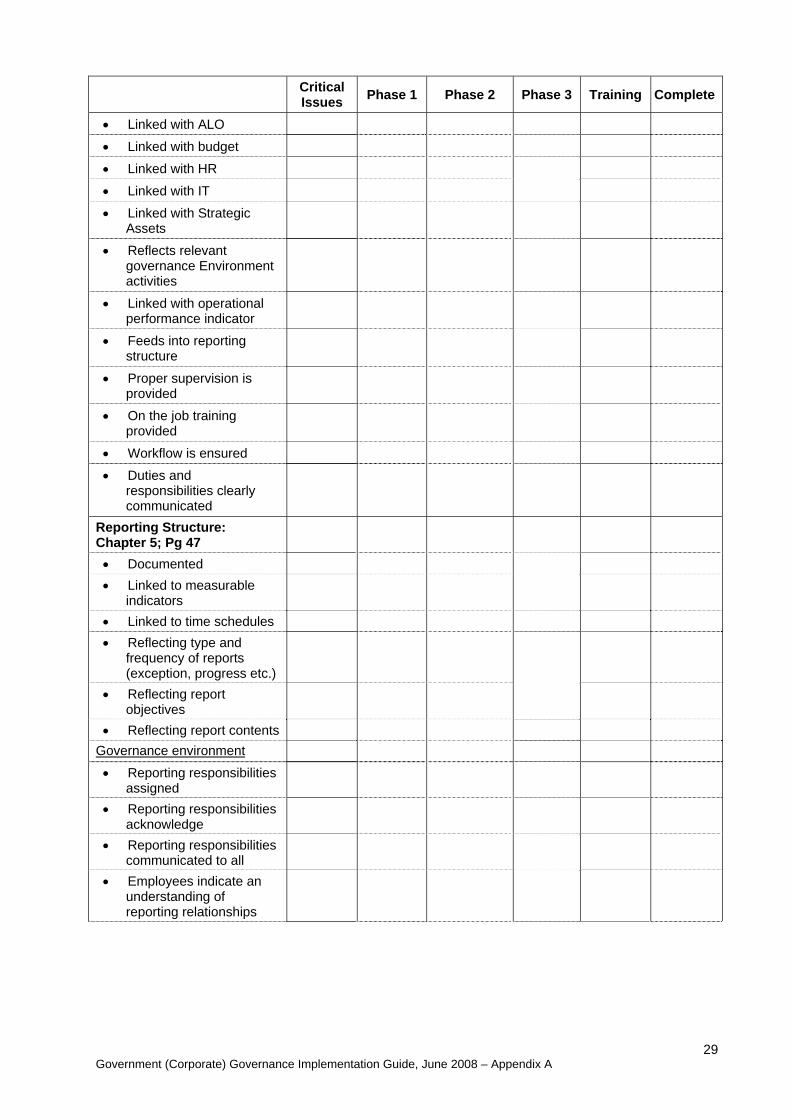

Roles & Relationships: Chapter 5; Pg 46

• Documented

• Including Standards of Behaviour

• linked with organisational structure

• Linked with process flowcharts

• Linked Key Control areas

28

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Linked with ALO

• Linked with budget

• Linked with HR

• Linked with IT

• Linked with Strategic Assets

• Reflects relevant governance Environment activities

• Linked with operational performance indicator

• Feeds into reporting structure

• Proper supervision is provided

• On the job training provided

• Workflow is ensured

• Duties and responsibilities clearly communicated

Reporting Structure: Chapter 5; Pg 47

• Documented • Linked to measurable

indicators

• Linked to time schedules • Reflecting type and

frequency of reports (exception, progress etc.)

• Reflecting report objectives

• Reflecting report contents Governance environment • Reporting responsibilities

assigned

• Reporting responsibilities acknowledge

• Reporting responsibilities communicated to all

• Employees indicate an understanding of reporting relationships

29

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Performance measures: Chapter 5; Pg 47

Governance environment • Applied towards

operational performance measures

• Applied towards individual performance measure

• Link exist between operational performance and individual performance

Regular Financial statements: Chapter 5; Pg 48

• Meeting prescripts

• Documented

• Reflecting reporting information

Governance environment • Attitude towards

functions and operations

• Financial data is linked to objectives and Performance Indicators

• Financial data is used to track progress

• Financial Data is compared with expected results

• Other Financial data is considered during decisions making process

Balance Scorecard: Chapter 5; Pg 48

• Documented

• Reflecting measuring indicators

• Reflecting frequency and intervals

• Reflecting benchmark criteria

• Reflecting scorecard objectives

Performance management individual: Chapter 5; Pg 49

• Documented

• Reflecting rewards system

30

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2

31

Phase 3 Training Complete

• Communicated

• Based on employee participation

• Based on employee acknowledgement

• Linked wit HR strategies

• Linked to objectives

• Linked to expected progress results

• Linked to critical performance indicators

Performance management Operational: Chapter 5; Pg 49

• Documented

• Reflecting measuring indicators

• Reflecting linkages between performance indicators in various strategic plans

• Reflecting timelines and report intervals

• Reflecting expected progress

• Reflecting reconciliation between expected and actual achievements

• Reflecting assigned responsibility

• Reflecting linkages with individual performance indicators

Risk Management: Chapter 5; Pg 50

• To be conducted by Risk Management

• Documented

• Reflecting business risk identified

• Reflecting mitigation strategies of identified risks

• inked with business processes developed

• Reflecting mitigating controls implemented

• Reflecting responsibility assigned

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Documented

• Reflects required internal environment

• Reflects role of ERM during strategic planning

• Reflect Erma requirements on key areas in organisation

• Reflects ERM approach and methodology

Strategic planning

• Objectives

• Assess links with legislation

• Assess links with other plans

• Assess links with budget

• Assess linked with relevant resources/ strategic assets

• Assess link with management practices

• Assess link with performance management

• Assess links with principles & values

• Assess links with measurable indicators

• Assess links between measurable objectives in different plans

• Assess link with budget dental

• Assess critical objectives Risk Management Methodology

• Documented

• Reflects risk Strategy identifications process

• Reflect different methods

• Document risks identified

• Documents mitigation strategies

32

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Assigns responsibility & accountability for mitigation strategies

• Reflects approach to external risks

• Reflect prioritizing criteria

• Reflects approach to external risks

• Downsizing

• Business processes

• Information system

• Reporting structure

• Resource allocations

• Capacity on al levels

• Strategic Assets

• Organisational structure

• Performance management

• Information & communication

• Policies & procedures

• Accountability & Responsibility

• Values &n Principles

• Control activities

• Budget

• Activities

• Analysis of possible effect

• Control design

Governance environment

• Effectiveness of indicators periodically reviewed

• Data continually compared to identify trends

• Unexpected results are timely investigated

33

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Control Activities Application Area Compliance and accountability: Chapter 5; Pg 52

• Documented

• Reflecting Acts, PTR, NTR and prescripts

• Linked to assignment of accountability

• Linked to processes

• Linked to Delegations

• Communicated

• Assignment acknowledge

• Monitoring system exist to exercise Accountability & responsibility

• Governance Environment

• Assignment accompanied by appropriate decision making powers

• Employees how their task relate to Accountability & Responsibility

• Employees how their task relate to internal control

• Assignment reflected in job description

• Assignment of responsibility reflected in Job descriptions

• Assignment empower employees to make decisions & improvements

• Assignments are made on correct levels

Delegations: Chapter 5; Pg 52

• Documented

• Reflecting responsibility assigned

• Linked to objective

• Linked to Performance indicators

• Linked to key controls implemented

34

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Linked to risk mitigation strategies

• linked to business processes

• Reflecting duration

• Reflecting delegated objective

• Delegations is appropriate to ensure workflow

• Aligned with objectives in Plan

Governance Environment

• Over riding internal control

• Key areas identified

• Guidance are documented

• Instances are recorded

• recorded instance are approved

• Over riding prohibited on certain levels

Policies & Procedures: Chapter 5; Pg 53

• Documented

• Reflects legislation, regulations

• Supported by process flow charts

• Reflecting Key controls

• Reflecting assigned delegations

• Reflecting Assigned Accountability

• Linked to objectives

• Linked to performance indicators

• Reflecting policy requirements

• Subjected to regular review

• Reflecting procedures to implement improvements

35

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Reflecting monitoring areas

• Reflecting reporting assignments

• Periodically reviewed

• Periodically updated with changes in Legislation & regulations

• Regularly updated with best practices

Audit Committee: Chapter 5 ; Pg 54

• Responsibility and Authority are clearly define

• AC do not fulfil management role

• Internal Audit

• Function exist

• IA executed in line with IIA Standards

• Internal Auditors are registered with IIA

• IA is Independent

• IA aligned with IIA definition of IA

Documented

• Reflecting Audit Charter / Mandate

• Reflecting roles and responsibilities

• Reflecting reporting relations

• Reflecting training

• Reflecting member requirements

• Reflecting independency

Monitor & review: Chapter 6: pg 64

• Mechanism in place to monitor operations & Programs

• Independent review's are regarded as important

36

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Coordination between the various activities ie Financial, Operations, Compliance, Governance Environment and Report resolutions. Chapter 6; pg 64

• Regular coordination exist

• Good relationships are encourage

• Regular communication exist

CRITICAL TOOLKIT IMPLEMENTATION ACTIVITIES CRITICAL ACTIVITIES TO BE CONSIDERED WHEN DEVELOPING, IMPLEMENTING ACTIVITIES IN THE IMPLEMENTATION TOOLKIT

Development program Application Area

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Control Environment; Chapter 6, page 57

Governance Culture Code of conduct • Formal code exist

• Code is periodically communicated

• Content is linked to specific activities

• Contents are aligned with operational activities

• Code is periodically acknowledge by employees

• Employees indicate their understanding and awareness

• Employees knows what constitute violations

• Employees are familiar with penalties for violations

• Employees indicate peer pressure exist to report violations

• Employees participates in code update

37

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Disciplinary action

• Documented

• Reflected procedures

• Contents subjected to employee participation

• Acknowledge periodically by all

• Action is taken timely when violations occur

• Penalties for violations are periodically communicated to all

Ethical Tone

• Has bee established at the top

• Ethical tone are communicated periodically

• Timely action are taken when violations occur

• Know problems are communicated to the relevant assurance providers

• Errors on all level are timely and appropriately corrected

• Reason for errors are investigated with aim to prevent future occurrences

• Reflects acceptable behaviour

• Reflects unacceptable behaviour

• Reflects value placed on employees concern

• Reflects procedure for dealing with employees concerns

Conduction dealings outside • Documented

• Reflects unacceptable behaviour

• Reflects penalties

• Contents subjected to employee participation

• Report contents are reliable

38

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Changes after the fact are investigated

Temptation & unethical behaviour

• Documented

• Reflects critical areas prone to unethical behaviour

• Reflects management action to remove temptation

• Incentives are not extreme

• Compensation market related

• Performance & promotions are fair

• Commitment to Competence

• Documented

• Responsibility to execute assigned

• Reflects knowledge & skills needed

• Management ensure that competent exist

• Management employees best in position

• Preference is given to existing employees to fill vacancies

• Employee development program exist

• Employees are encourage to improve skills and capabilities

• Employees are encourage to develop careers within organisation

• Purpose

• Documented

• Responsibility to execute assigned

• Employees understand purpose of their tasks

• Employees understand how their task relates to achievement of objectives

39

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Acknowledge by employees

• Capability Management Ability & Experience

• Documented

• Senior management has proven abilities & Experience

Training & Counselling

• Documented

• Responsibility assigned

• Reflect assistance to employees to improve skills

• Reflects counselling to employees

• Contents included participation of employees

• Control exist to ensure training

• Training provided on all levels

• Training includes supervisory skills

• Constructive job evaluations exist

• Control Self Assessment

• Documented

• Performed by senior managers

• Reflects peer review requirements

• Programs are developed base on results of Control Self Assessment

Control Activities: Chapter 6; pg 60

General Application • Documented • Reflects policies and

procedures

• Reflect control needed • Linked to risk profile • Proper application

monitored

• Periodically reviewed

40

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Timely action taken when failure occurs

• Improvements considered when appropriate

• Implements exception reports

• Periodically approved • Linked with purpose of

control

• Accountability assigned • Accomplishment of

objectives

Accomplishment of objectives • Documented

• Reflects areas

• Reflects intervals

• Reflect report requirements

• Reflect link to meeting schedules

• Tract performance against PI in all plans

• Reflects requirements for reliable reports

• Limited number developed and linked with plans

• Progress monitored periodically

• Reflects corrective action when progress not made according to plans

• Reflects reconciliations required

Compliance With laws, regulations & contracts

• Documented

• Changes are implemented

• Compliance controls are implements

• Linked to applicable activities

• Monitoring compliance exist

• Procedures are updated with changes

41

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Register is kept of related laws regulations contract

• Responsibility assigned

• Updates of acts & revaluations are monitored

Safeguarding of Assets

• Access control exist for vulnerable assets

• Access control monitored

• Assets are assigned to relevant employees

• Controls communicated to all

• Difference in reconciliation are appropriately acted on

• Disaster recovery plan exist

• Documented

• Employees acknowledge safeguarding responsibilities

• Physical controls implemented

• Reconciliation between physical assets and register performed periodically

• Reflected access control

• Reflects identification and protection requirements

• Reflects responsibility for assets

• Register kept of assets assigned

• Register kept of unassigned assets

Segregation of duties

42

• Assignments impairment systematically to ensure checks and balances

• Documented

• Flow charts provide serrations overview

• No individual allowed to work alone with cash, payments, or other vulnerable assets

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• No single individual permitted to exercise control over all aspects of activity

• Reflect accountability & custodian assignments

• Reflects authorisation assignments

• Reflects criteria to determine asset vulnerability (Value, portability, exchangeability etc)

• Reflects custodian assignments

• Reflects identified areas where collusion can destroy control effectiveness

• Reflects incompatible key controls

• Reflects key controls to prevent fraud, theft errors 7 waste

• Reflects opening mail assignments

• Reflects review assignments

Access control information systems

• Access to classified information is monitored

• Access violations timely investigated and acted on

• Documented

• Physical and logical controls are implemented to prevents and detect unauthorised access

• Reflect control criteria

• Reflects access assignments

• Register is kept of classified information

• Resource classification communicated to resource owners

• Resource owners apply access criteria to their information

43

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

Reliability of information

• Documented

• Reflects criteria for reports

• Reflects criteria for monitoring reports

• Reflects criteria for information

• Reflects criteria for communications

Criteria based on 4 levels

• Validity

• Timely

• Accurately

• complete

Information processing

• Documented

• Edit checks are used in controlling data

• Transaction performed in numerical sequent

• File totals compared with control accounts

• Exception and violations are timely acted on

• Access to data control

• Transactions and events appropriately classified

• Proper classification take place throughout lifecycle of transaction

• Classification codes exist

• Changes to transactions, codes, numbers etc, monitored with exception reports

Documentation

• Documented

• Internal controls documented with process flow charts

• Written documentation exist t for internal control structures

• IC documentation readily available

44

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Reflects activity level function

• Reflects key controls

• Reflects applicable policies

• Reflects existing annual

• Reflects 4 level criteria required

• Reflect filing criteria

• Reflects management arrangements

• Responsibility assigned Effective & Efficient use of resources

• Documents

• Use of resources is monitored

• Potential output of each resource measured

• Activities performed quantified to compare potential against actual

Information technology Chapter 5; page 42

Documented • Reflects infrastructure

• Reflect capability

• Monitored periodically

• Subjected to assessments

• Reflect maintenance of infrastructure

• Accountability & Responsibility assigned

• Assignments acknowledged

Application software • Prohibits unauthorized

program & System modification

• New software tested for user requirements

• Software libraries exist

• Software libraries protected

• Software libraries maintained

45

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Accountability and responsibility assigned

• Access, change control exercised

• Unauthorized access investigated

• Reflects access criteria

• Software usage monitored

Service continuity

• Documented

• Reflects backup procedures

• Reflects offsite backup requirements

• Reflects hardware requirements

• Reflects virus control strategies

• Reflects contingency plans

Information & communication: Chapter 6; pg 62

• Documented

• Reflects reliability requirements

• Reflects communication means

• Reflect authority of communication various formats

• Reflects purpose of communications

• Based on organisational needs

• Reflects gathering procedures

• Reflects critical information regarding achievement of objectives

• Reflects internal control information required

• Reflects response times

• Information system develop to provide required information timely

46

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Information system integrated with IT

• Information system integrated with culture of organisation

Distribution of information • Documented • Reflects identification

criteria to determine relevant information

• Reflect communications formats

• Provided timely at correct levels

• Reflects type of information required

• Reflects resources of information

• Assigned accountability & responsibility

• Reflects responses required

• Reflects response time allowed

• Reflects purpose of different types of information

Internal communication

• Documented

• Reflect types of internal information required

• Apply to update employees with relevant information

• Reflects the purpose of communications

• Reflects reactions required

• Provide employees with means o of communicating across organisation

• Reflect informal communication lines

• Provides guidance regarding reporting adverse information

47

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

External Communications

• Documented

• Reflecting purpose

• Determine groups that can have severe impact on programs

• Reflecting communication channels with stakeholders

• Reflect communications requirement on communication received

• Reflect requirement for communication regarding complaints received

• Reflect consideration requirements on reports received

• Communication effectiveness monitored

Means forma of communication

• Documents

• reflect communication system

• Reflect communication flowcharts

• Reflect communication forms and means

• Reflect purpose of communication format

• Reflects response requirements

Management of communication

• Documented

• Reflect revision requirements of communication

• Assigns accountability & responsibility

• Reflect links with strategic plans

• Reflects links with performance monitoring

• Reflects links with monitoring requirements

• Reflects mechanisms to detect emerging communication needs

48

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• Monitor advances & best practice in communications

• Update existing communication systems with new developments

Norms & Standards • Documented

• Reflect critical information for decision making

• Reflect links with strategic planning

• Reflect responses require on independent investigation, audit & reports

• Review appropriateness of reporting structure & contents

• Reflects criteria for report content

Separate evaluation

• Documented

• Reflect response criteria on separate evaluations received

Corporate culture

• Documented

• reflect communication strategies

• Reflect evaluations strategies

• Reflect improving strategies

• Reflect desired tone at the top

Monitoring: Chapter 6; pg 64 • Documented

• Reflects ongoing monitoring requirements

• Reflect control areas monitored

• Risk management

• key controls

• Supervision

• Progress indicators

49

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

50

Government (Corporate) Governance Implementation Guide, June 2008 – Appendix A

Critical Issues Phase 1 Phase 2 Phase 3 Training Complete

• operational performance

• Individual performance

• Reconciliation

• Compliance

• Safeguarding of assets

• Accomplishment of objectives

• Effectiveness & efficient use of resources

• Report resolutions

• Separate evaluations

• Recommendation response

• Response time

• Reflect frequency requirements

• Reflect response strategies

• Reflect monitoring purpose in each case

• Assign accountability & responsibility