gorham pma & der conference san diego, ca · 2017-03-22 · gorham pma & der conference san...

TRANSCRIPT

0

Market Outlook & Industry Trends

Presented by:Presented by:

Hal ChrismanVice President [email protected]

Hal ChrismanVice President [email protected]

Gorham PMA & DER ConferenceSan Diego, CA21 March 2017

Gorham PMA & DER ConferenceSan Diego, CA21 March 2017

11

Today’s Agenda

State of the Airline Industry

Fleet & MRO Market Overview

Alternative Materials

Key Industry Trends

22

Driven by low fuel costs and consolidation, the global airline industry achieved record profitability of over $35B USD in 2016

Source: IATA, ICF analysis

2016 was an historic year for airline profitability…

Global Airline Profitability, 1997 - 2017F

-$30

-$20

-$10

$0

$10

$20

$30

$40

$USD Billions

Asia Pacific, $6.3B

North America, $18.1B

Europe, $5.6B

Middle East, $0.3B

Latin America, $0.2B

Africa, ($0.8B)$35.6B

33

However, record profitability has been largely limited to carriers in North America

Source: IATA, ICF Analysis

-1.8%

-4.7%

0.1%

2.3%

1.0%

-0.9%

3.4%

4.7%

0.7%1.5%

3.0%

-0.4%

12.9%

5.2%4.5%

2.9%

0.7%

-3.6%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2008

2012

2017F

Global Airline EBIT Margin by Region

…but many airlines continue to struggle

44

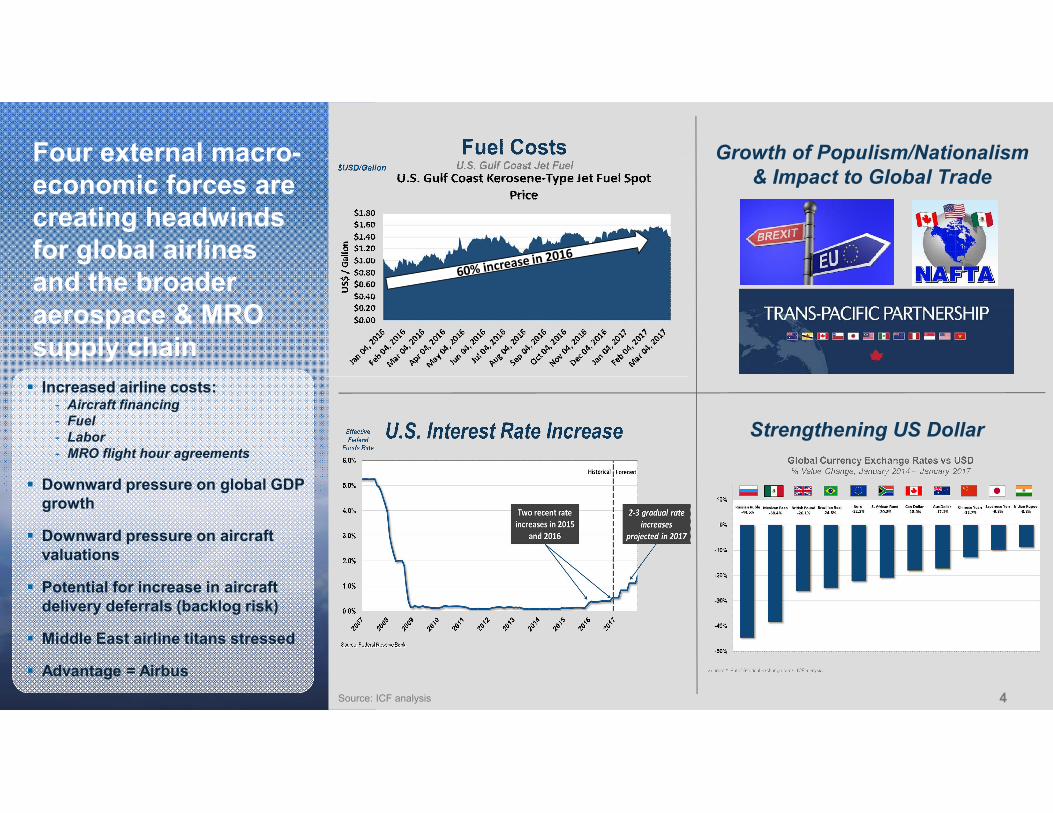

Four external macro-economic forces are creating headwinds for global airlines and the broader aerospace & MRO supply chain

Source: ICF analysis

Strengthening US Dollar

Growth of Populism/Nationalism& Impact to Global Trade

Increased airline costs:- Aircraft financing- Fuel- Labor- MRO flight hour agreements

Downward pressure on global GDP growth

Downward pressure on aircraft valuations

Potential for increase in aircraft delivery deferrals (backlog risk)

Middle East airline titans stressed

Advantage = Airbus

55

Today’s Agenda

State of the Airline Industry

Fleet & MRO Market Overview

Alternative Materials

Key Industry Trends

66

The current commercialair transport fleet consists of almost 28K aircraft; over half are narrowbodyaircraft

Source: CAPA 2016

NarrowbodyJet

WidebodyJet

Turboprop

Regional Jet

27,957Aircraft

13%

54%14%

19%

By Aircraft Type By Global Region

27,957Aircraft

5%

28%

25%5%

30%

7%

Latin America

Africa

NorthAmerica

Asia Pacific

EuropeMiddle East

2016 Global Commercial Air Transport Fleet

77

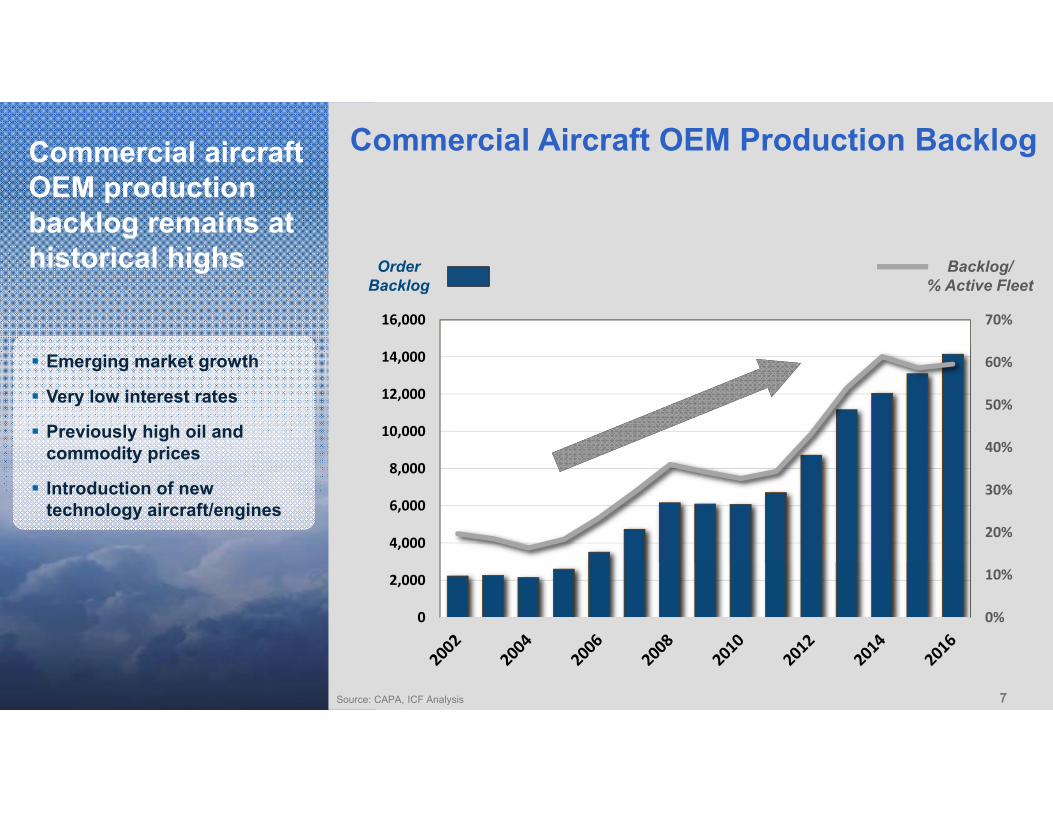

Commercial aircraft OEM production backlog remains at historical highs

Source: CAPA, ICF Analysis

0%

10%

20%

30%

40%

50%

60%

70%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Order Backlog

Backlog/% Active Fleet

Emerging market growth

Very low interest rates

Previously high oil and commodity prices

Introduction of new technology aircraft/engines

Commercial Aircraft OEM Production Backlog

88

Lower fuel costs appear to be reversing aircraft retirements trends

Source: CAPA, Airline Monitor, ICF analysis

Industry Impact:

MRO Suppliers - Positive: Increased spend on older airframes & engines

Surplus Market - Negative: Reduced part-out “feed stock”- OEMs: Improved new

part sales- Distributors: Improved

used part values / pricing

- Operators: Increased material costs

- PMA Suppliers: Very Positive

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

0

200

400

600

800

1,000

1,200

# Retirements

Retirement as % of installed fleet

% Installed Fleet

1991-1999 Average: 203

2000-2009 Average: 473

Commercial Air Transport Annual Aircraft Retirements

99

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2016 2026

AfricaMiddle EastLatin AmericaEuropeAsia PacificNorth America

The combination of strong air travel demand and the need to replace ageing aircraft will drive fleet growth at a healthy 3.2% annually

Source: ICF analysis: CAPA 2016

28,000

30% 25%

38,100

28%

25%

8%

33%

23%

8%

# Aircraft

3.4%

2.4%

1.3%

4.8%

5.0%

4.1%

CAGR

3.2% Avg.

5%

6%

10 Year Global Air Transport Fleet Growth

1010

Current commercial air transport MRO demand is $67.6B; Asia is now larger than North America and Europe in market size

Source: ICF analysis; Forecast in 2016 $USD, exclusive of inflation

Engines

Components

Line

Airframe

Modifications

14%

17%

22%

40%

8%North

America

Asia Pacific

Europe

Middle East

Latin America

Africa

27%

30%

26%

8%

6%4%

$67.6B$67.6B

By MRO Segment By Global Region

2016 Commercial Air Transport Global MRO Demand

1111

The global MRO market is expected to grow by 4.1% per annum to over $100B by 2026

Source: ICF analysis; Forecast in 2016 $USD, exclusive of inflation

Engine and component MRO markets remain the largest segments

Modifications market will see the strongest growth (e.g. interiors, connectivity)

Airframe market slows due to reduced man-hour intensity and increased check intervals as new fleets are introduced

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2016 2026

Modifications

Airframe

Line

Component

Engine

40%

22%

14%

17%

$67.6B

$100.6B

2.8%

3.2%

4.2%

4.5%

CAGR

4.1% Avg.

5.2%

41%

22%

16%

12%

$USDBillions

10 Year Global Commercial Air Transport MRO Demand Growth

1212

Today’s Agenda

State of the Airline Industry

Fleet & MRO Market Overview

Alternative Materials

Key Industry Trends

1313

There two primary reasons operators are aggressively seeking non-OEM supplied parts …

… And we traditionally focus our discussion around three alternatives OEM-supplied parts:

1. Cost savings

2. Part availability

Source: ICF analysis

PMA

PMA (Parts Manufacturer Approval) is approval granted by the FAA to a non-OEM manufacturer of aircraft parts

Two types of PMA:

1. Licensed

2. Competitive

DER Repair

DER (Designated Engineering Representatives), FAA approved engineers who can approve technical data for repairs and modifications outside the CMM

Design Organization Approval (DOA), a blanket approval for an MRO organization to develop internal repairs

Surplus

Three types of surplus material:

1. Used Serviceable Material (USM)

2. New Material

3. Used, unserviceable material

Lower HigherPerceived Risk

1414

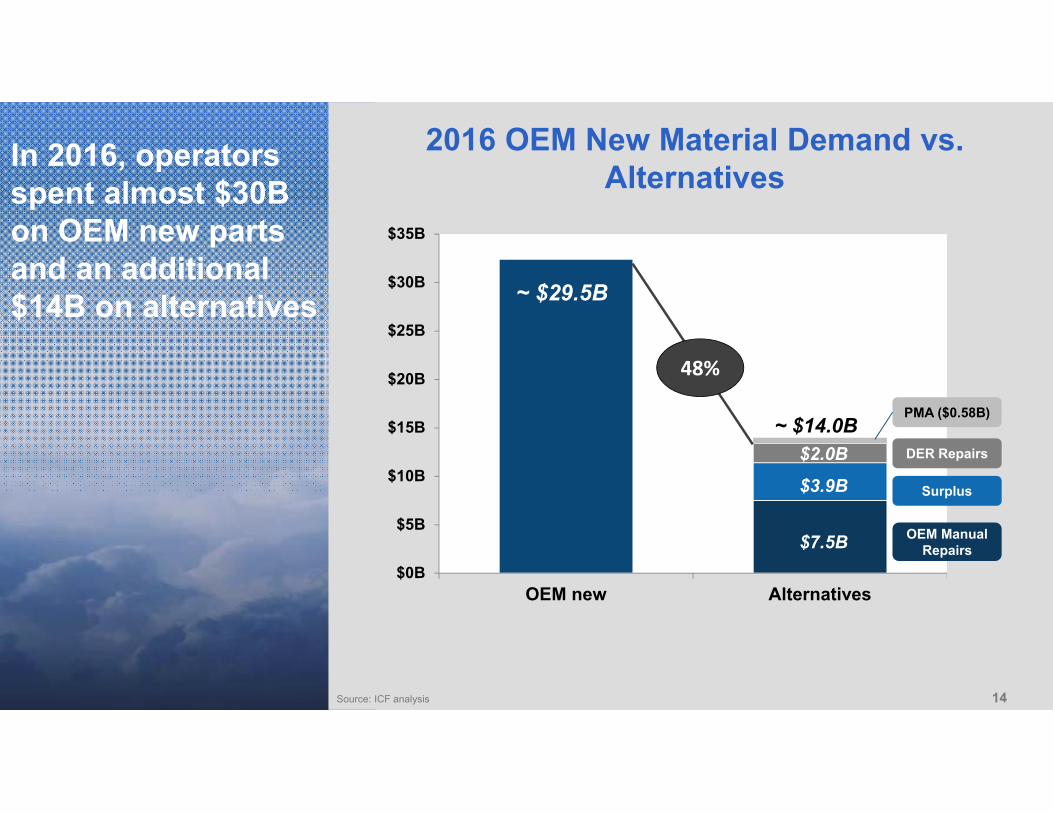

In 2016, operators spent almost $30B on OEM new parts and an additional $14B on alternatives

$0B

$5B

$10B

$15B

$20B

$25B

$30B

$35B

OEM new Alternatives

OEM ManualRepairs

DER Repairs

PMA ($0.58B)

Source: ICF analysis

~ $14.0B

~ $29.5B

$2.0B

$3.9B Surplus

$7.5B

48%

2016 OEM New Material Demand vs. Alternatives

1515

The volume of PMA approvals has been steadily growing since 1990, with over almost 525,000 new approvals granted since 2011 … however, the pace in 2016 and 2017 appears to have dropped significantly

Source: Federal Aviation Administration – PMA Database extract 19 March 2017

36,202

61,439

220,074

356,683

468,689

56,524

0

100,000

200,000

300,000

400,000

500,000

FAA Approved PMA Part Numbersby Year Approved

1616

There are over 1.2 million total PMA parts that are FAA approved, of which over 75% are for Boeing aircraft

Source: Federal Aviation Administration – PMA Database extract 19 March 2017

Boeing76%

Airbus15%

Bombardier3%

P&W1%

Other5%

1,209,415

FAA Approved PMA Part Numbersby OEM

1717

PMA growth is has declined from the “good old years” but is healthy at 4.7%

Source: ICFForecast in 2016 USD, exclusive of inflation

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

-

100

200

300

400

500

600

700

800

2016 2017 2018 2019 2020 2021

Component

Engine

Airframe

Total

Penetration (%)

2016 - 2021CAGR:

% of total MRO material

$ millions

6.0%

2.3%

5.4%

4.7%

Air Transport PMA Market Forecast In $ Millions (2016-2021)

1818

The DER method is an alternative repair process to the OEM component maintenance manual (CMM)

With over 500 Company and 1000+ Consultant DERs in the US, DER repairs are an increasingly important alternative

Broken Part

Repair

CMM

DER

Replace

New

Surplus

PMA

Source: FAA, Gorham

1,034 Consultant

DERs

502 Company

DERs

There are 502 Company and 1,034 Consultant certified DERs in the U.S., with some overlap due to

multiple certifications

1919

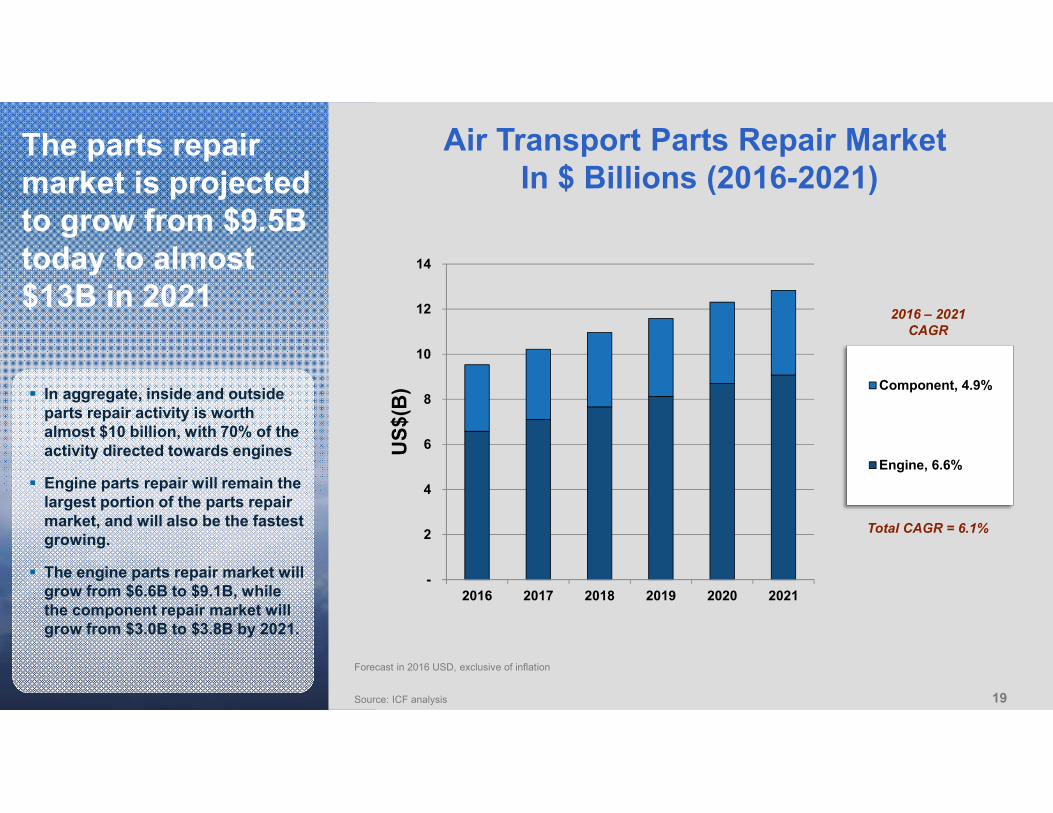

The parts repair market is projected to grow from $9.5B today to almost $13B in 2021

Forecast in 2016 USD, exclusive of inflation

Source: ICF analysis

-

2

4

6

8

10

12

14

2016 2017 2018 2019 2020 2021

US

$(B

) Component, 4.9%

Engine, 6.6%

Total CAGR = 6.1%

2016 – 2021CAGR

In aggregate, inside and outside parts repair activity is worth almost $10 billion, with 70% of the activity directed towards engines

Engine parts repair will remain the largest portion of the parts repair market, and will also be the fastest growing.

The engine parts repair market will grow from $6.6B to $9.1B, while the component repair market will grow from $3.0B to $3.8B by 2021.

Air Transport Parts Repair Market In $ Billions (2016-2021)

2020

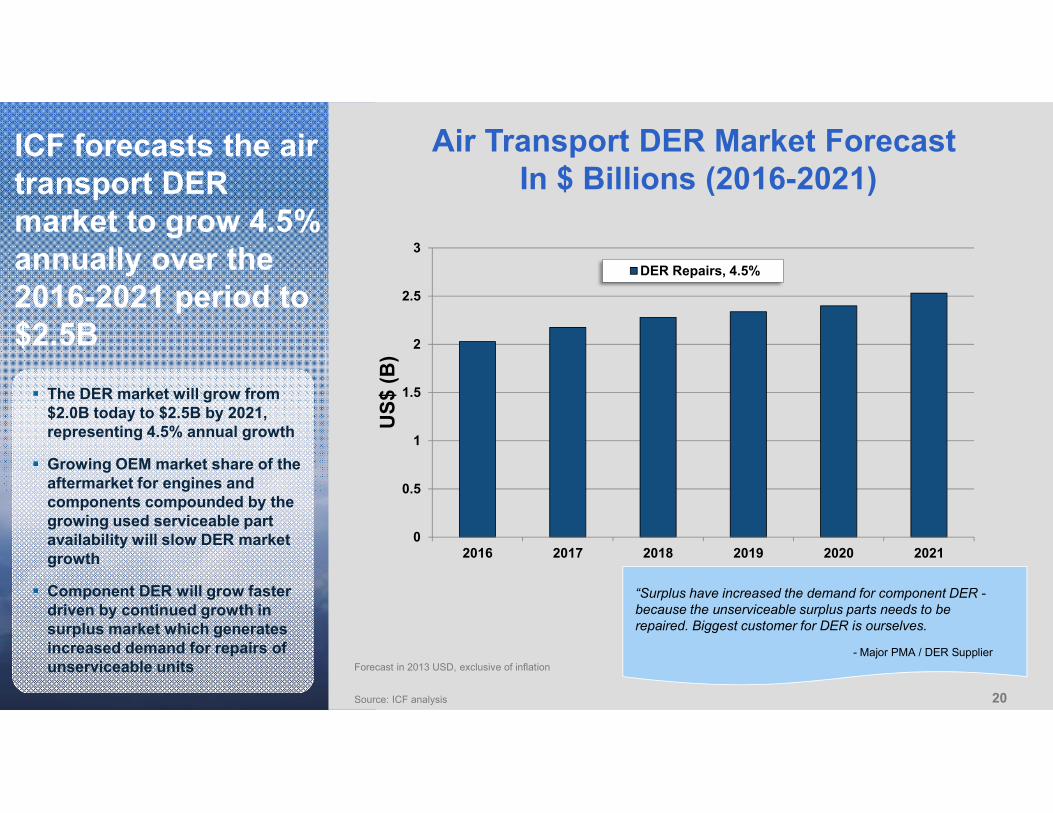

ICF forecasts the air transport DER market to grow 4.5% annually over the 2016-2021 period to $2.5B

Forecast in 2013 USD, exclusive of inflation

Source: ICF analysis

0

0.5

1

1.5

2

2.5

3

2016 2017 2018 2019 2020 2021

US

$ (

B)

DER Repairs, 4.5%

“Surplus have increased the demand for component DER -because the unserviceable surplus parts needs to be repaired. Biggest customer for DER is ourselves.

- Major PMA / DER Supplier

The DER market will grow from $2.0B today to $2.5B by 2021, representing 4.5% annual growth

Growing OEM market share of the aftermarket for engines and components compounded by the growing used serviceable part availability will slow DER market growth

Component DER will grow faster driven by continued growth in surplus market which generates increased demand for repairs of unserviceable units

Air Transport DER Market Forecast In $ Billions (2016-2021)

2121

While we often focus on PMA, Surplus & DER; we need to keep the full spectrum of alternatives in mind

Source: ICF Research

Operators & MROs can choose from at least eight alternatives to fulfill their material demand

Surplus

DER

PMA

Licensed PMA

EASA EPA

CAAC PMA

CRM Repairs

OEM New Parts

Air Transport Material Demand

2222

Today’s Agenda

State of the Airline Industry

Fleet & MRO Market Overview

Alternative Materials

Key Industry Trends

2323

There are four key constraints to PMA/DER market growth

Source: ICF analysis

Operator Technical

Capability & Capacity Availability of

Surplus Parts

Lessor Restrictions

1. Lessor Restrictions

2. OEM Strategies

3. Availability of surplus parts

4. Operator’s technical capability & capacity

OEM

Strategies

2424

While airlines are performing well as a whole, profits are focused primarily on North American operators, so cost reduction remains a priority

In order to control and reduce material spend, airlines must have a comprehensive OEM alternative strategy

PMA parts, DER repairs, and surplus material are valuable material sourcing solutions that drive tangible cost savings and improve part availability

As long as certain airlines continue to have restrictive PMA policies, Lessors will continue to include conservative language in their lease agreements

Education is the only solution

In Summary…

25

For questions regarding this presentation, please contact:

Hal ChrismanVice President Aerospace & MRO Advisory

[email protected] +1 734.277.6710

THANK YOU!

Gorham PMA & DER ConferenceSan Diego, CA21 March 2017

Gorham PMA & DER ConferenceSan Diego, CA21 March 2017

2626

Market Research & Analysis

Airline Maintenance Benchmarking, Operational Improvement, and MRO Strategy

M&A Commercial and Operational Due Diligence

OEM Aftermarket Strategy

Aviation Asset Valuations & Appraisals

MRO Information Technology (IT) Advisory

Strategic Sourcing & Supply Chain Mgt.

LEAN Continuous Process Improvement

Military Aircraft Sustainment Market Analysis and Strategy

ICF provides a full range of Aerospace & MRO advisory services

2727

ICF is one of the world’s largest and most experienced aviation and aerospace consulting firms

Airports • Airlines • Aerospace & MRO • Aircraft Finance

53 years in business (founded 1963)

80+ professional staff

− Dedicated exclusively to aviation and aerospace

− Blend of consulting professionals and experienced aviation executives

Specialized, focused expertise and proprietary knowledge

Broad functional capabilities

More than 10,000 private sector and public sector assignments

Backed by parent ICF International (2016 revenue: 1.2 billion USD)

Global presence –– offices around the world

joined in 2011joined in 2007 joined in 2012 joined in 2014

New York • Boston • Washington DC • London • Singapore • Beijing