good timing: ceo stock option awards and company news ... 1997.pdfthis article analyzes the timing...

TRANSCRIPT

http://www.jstor.org

Good Timing: CEO Stock Option Awards and Company News AnnouncementsAuthor(s): David YermackSource: The Journal of Finance, Vol. 52, No. 2, (Jun., 1997), pp. 449-476Published by: Blackwell Publishing for the American Finance AssociationStable URL: http://www.jstor.org/stable/2329486Accessed: 24/06/2008 14:17

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at

http://www.jstor.org/page/info/about/policies/terms.jsp. JSTOR's Terms and Conditions of Use provides, in part, that unless

you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you

may use content in the JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at

http://www.jstor.org/action/showPublisher?publisherCode=black.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed

page of such transmission.

JSTOR is a not-for-profit organization founded in 1995 to build trusted digital archives for scholarship. We work with the

scholarly community to preserve their work and the materials they rely upon, and to build a common research platform that

promotes the discovery and use of these resources. For more information about JSTOR, please contact [email protected].

THE JOURNAL OF FINANCE . VOL. LII, NO. 2 . JUNE 1997

Good Timing: CEO Stock Option Awards and Company News Announcements

DAVID YERMACK*

ABSTRACT

This article analyzes the timing of CEO stock option awards, as a method of inves- tigating corporate managers' influence over the terms of their own compensation. In a sample of 620 stock option awards to CEOs of Fortune 500 companies between 1992 and 1994, I find that the timing of awards coincides with favorable movements in company stock prices. Patterns of companies' quarterly earnings announcements are consistent with an interpretation that CEOs receive stock option awards shortly before favorable corporate news. I evaluate and reject several alternative explana- tions of the results, including insider trading and the manipulation of news an- nouncement dates.

MANY EXECUTIVE COMPENSATION STUDIES find links between the introduction of long-term incentive plans and changes in company performance. Leading examples include Larcker (1983) (accounting-based performance plans) and DeFusco, Johnson, and Zorn (1990) (stock options). However, most evidence in such studies is consistent with two interpretations. Incentive compensation might motivate managers to make superior decisions. Alternatively, managers might have influence over the terms of their own compensation and use this power to obtain more performance-based pay in advance of anticipated stock price increases. Until recently, the limited public data about executive com- pensation has permitted little research that could distinguish between these alternative hypotheses.

Using the dates of stock option awards received by CEOs of major U.S. companies, this article investigates the hypothesis that managers influence the terms of their own compensation. U.S. public corporations began reporting this information in late 1992 pursuant to reformed Securities and Exchange Commission (SEC) regulations for executive compensation disclosure (SEC (1992)). Since nearly all executive stock options are granted with fixed exercise prices equal to the stock price on the date of award, opportunistic timing of

* Stern School of Business, New York University. I have received helpful comments from Edwin Elton, Zsuzsanna Fluck, David Ikenberry, Kose John, Ren6 Stulz (the editor), Michael Weisbach, Karen Wruck, and two anonymous referees. I thank seminar participants at NYU, the National Bureau of Economic Research, the American Finance Association annual meeting, the Utah Winter Finance Conference, and Michigan State University. I appreciate research assistance by Anand Srinivasan and Shlomith Zuta. I gratefully acknowledge the contribution of I/B/E/S Inter- national Inc. for providing earnings per share forecast data, available through the Institutional Brokers Estimate System. This data has been provided as part of a broad academic program to encourage earnings expectations research.

449

450 The Journal of Finance

3.0%

2.0%

f.)

0

0 1.0%

0.0

1 .0%

-20 Award Date 20 40 60 80 100 120

Trading Days Relative to Award Date

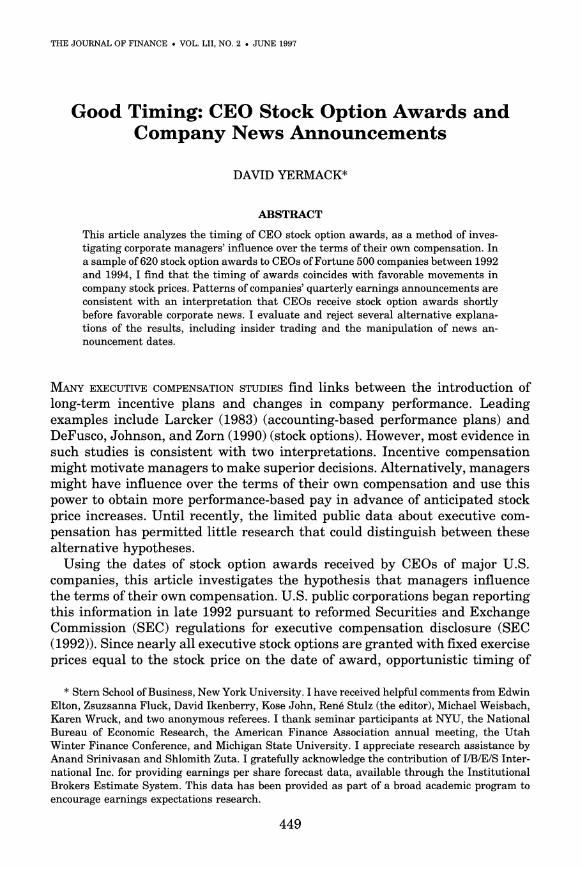

Figure 1. Abnormal stock returns following receipt of stock options by CEOs. Mean cumulative abnormal stock returns (CARs) for Fortune 500 companies awarding stock options to their CEOs between 1992 and 1994. CARs are calculated for an event period around the dates of 620 CEO stock option awards. It is important to recognize that news of option awards almost never becomes public until company proxy statements are filed approximately three months after the fiscal year in which an award occurs. Sample selection and CAR calculations are described more fully in the text, and Table I reproduces the data shown in this figure.

option awards around company news announcements could significantly in- crease CEO wealth for reasons unrelated to the options' purported incentive purpose. If managers influence the structure of their compensation contracts, I expect CEOs to receive stock option awards shortly in advance of favorable news that pushes company stock prices higher.

Results presented herein are consistent with this prediction, and data dis- played in Figure 1 illustrate the main findings. The figure shows mean cumu- lative abnormal stock returns (CARs) for company stocks around the dates of 620 stock option awards to Fortune 500 CEOs between 1992 and 1994 (calcu- lation details appear in Section II below). Companies making stock option awards to their CEOs outperform the market on a risk-adjusted basis by slightly more than 2 percent during the period beginning the day after the award and lasting approximately ten weeks (50 trading days). The abnormal returns level off and remain permanently embedded in company stock prices thereafter. These stock price increases occur even though news of CEO stock option awards remains undisclosed until proxy statements are published ap- proximately three months after the end of company fiscal years-three to fifteen months after the awards. The pattern of abnormal returns is consistent

CEO Stock Option Awards and Company News Announcements 451

with CEOs receiving stock options shortly in advance of favorable news unre- lated to the award. Detailed analysis in Section III of companies' quarterly earnings announcements provides further evidence supporting this interpre- tation.

Many companies characterize stock options as devices for aligning the long- term interests of shareholders and managers. While options and other contin- gent pay instruments undeniably reward managers for long-term success, the results of this article suggest that their role in executive compensation is more complex. Because CEO option recipients benefit from the remarkable good timing of their awards, their compensation appears to increase for reasons that have little to do with managerial skill, effort, or performance.

Section IV considers but rejects a range of alternative explanations for the patterns observed in the data. One possibility is that news of option awards somehow reaches the investing public around the time of the grant date. Investors might then buy shares, either because of the expected value of greater managerial incentives, or, if one believed that managers influenced their own pay, in response to the optimistic signal conveyed by the CEO's receipt of an option award. A similar possibility is that insider trading by CEOs or others accounts for the rise in stock prices just after CEO option awards. While it may be impossible to refute these conjectures completely, I show in Section IV.A that the daily trading volume in company stocks remains un- changed around the time of CEO option awards, which is inconsistent with all of these theories about increased share purchases (Meulbroek (1992)).

Several other theories about the timing of stock option awards are explored in Section IV. Boards of directors may acquiesce in CEOs' manipulation of the dates of stock option awards as an indirect method of permitting insider trading by managers, in line with the controversial recommendations of some theorists. Similarly, the board may award options in advance of anticipated stock price increases as a form of managerial reward. However, granting options in such a pattern without first disclosing the relevant news to share- holders would seem to contravene federal securities laws and possibly expose managers and directors to legal liability. Firms might award stock options shortly before favorable news announcements as an indirect method of grant- ing discount options with in-the-money exercise prices, as recommended by some compensation theorists. However, the availability of less noisy contract- ing alternatives and the paucity of premium options granted out-of-the-money appear to undermine the likelihood of this explanation. Similarly, a company could award stock options in advance of favorable news as a strategy for achieving net tax savings between the firm and the CEO, but related empirical studies have found that tax considerations do not explain cross-sectional patterns of CEO stock option awards. CEOs may manipulate the timing of news disclosures in order to increase the value of their options. However, this strategy would involve delaying favorable news and rushing forward adverse information, even though studies show that managers behave in the opposite way when releasing corporate news. I test this theory using data from com- pany earnings announcements, and the results fail to support this conjecture.

452 The Journal of Finance

The remainder of this article is organized as follows. Section I describes the procedures followed by companies in awarding stock options to CEOs and reviews related literature on opportunistic managerial behavior in response to compensation parameters. Section II presents the basic results showing an association between CEO option award dates and favorable movements in company stock prices. Section III contains an analysis of corporate earnings announcements. Data about these announcements are consistent with the hypothesis that managers' stock option awards are favorably timed relative to releases of good and bad news. Section IV explores possible alternative expla- nations for the results, with close attention to the empirical and theoretical literature on insider trading. Section V concludes.

I. The Stock Option Award Process

Stock options provide the lion's share of performance-based incentive compen- sation received by CEOs in large U.S. companies (Jensen and Murphy (1990)). For most CEOs in major companies, stock options are awarded once each year by a compensation committee of the board of directors, acting under the authority of periodic shareholder votes' (occasionally CEOs receive multiple awards). Compensation committees exercise discretion over the size and tim- ing of stock option awards, and these parameters vary substantially across companies and over time. The increasing size and frequency of CEO option awards over the last decade (Yermack (1995)) has attracted attention from shareholder activists and government authorities such as the SEC, the Finan- cial Accounting Standards Board (FASB), and the U.S. Congress, all of which recently promulgated regulations encouraging shareholder scrutiny of execu- tive pay.

The SEC's expansion of executive compensation disclosure requirements in 1992 (SEC (1992, 1993a, and 1993b)) greatly increased public information about compensation committees and top managers' pay. Among other data, companies' annual proxy statements now report exact dates of managers' stock option awards, the key variable in this article.2 The documents also must include compensation committee reports, which describe the, criteria for top managers' pay and disclose conflicts-of-interest held by committee members. The widely understood intent of these measures has been "to put stockholders in charge of monitoring executive compensation," according to Karmel (1994). With similar motives, Congress in 1993 enacted ?162(m) of the Internal Rev- enue Code, limiting the tax deductibility of executive compensation unless the

1 These votes usually occur every five years at annual shareholder meetings. Little suspense surrounds the outcome: in a sample of 367 incentive compensation plan votes (including stock options) analyzed by Brickley, Bhagat, and Lease (1985), all 367 were approved, and the authors report that the New York Stock Exchange's proxy specialist had no knowledge of an executive compensation plan ever being rejected by stockholders.

2 Although corporations are not specifically required to disclose dates of stock option awards, many report the information voluntarily, and it can always be inferred from required disclosures of awards' expiration dates and durations.

CEO Stock Option Awards and Company News Announcements 453

pay results from a performance-based plan administered by a committee of independent directors.

Board compensation committee reports in annual proxy statements, as well as realignments of compensation committees to comply with the new tax code provision, revealed numerous instances where CEOs appeared to have direct or indirect influence upon the contracting process for their own pay. Many companies openly acknowledged in proxy statements that managers helped structure their own compensation, including the timing of stock option awards, with the role of board committees apparently limited to ratifying management proposals. For example, Intel Corp.'s 1994 proxy statement reported that during the prior year, ". . . stock options for the executive officers were granted upon recommendation of management...." Similarly, Western Digital Corp. described the role of its compensation committee by writing in its 1994 proxy statement, ". . . taking into account the recommendations of management, the Committee determines the employees to whom options will be granted, [and] the timing and manner of the grants of options."

In addition to these acknowledgements of direct management participation in setting the terms of compensation, many proxy statements suggested the presence of conflicts of interest in the contracting process. As discussed below, a handful of Fortune 500 companies reported having CEOs who served as members of their own compensation committees. Some companies had pairs of CEOs who sat on each other's compensation committees-in effect, two people responsible for establishing each other's pay (Cowan (1992)). Scores of corpo- rations reported that outside directors who served on compensation commit- tees benefitted from personal consulting contracts or from the diversion of company business to their principal employers. In addition to these channels for CEOs to bestow favors upon the directors who set their compensation, the process for recruiting and reappointing members of the board itself had long been understood to fall under the CEO's control in most companies.

The central hypothesis of this article is that CEOs exert influence over their compensation committees in these and other ways, and that they exploit this power to increase the value and lower the riskiness of their compensation. The suggestion that managers manipulate the compensation contracting process to appropriate value from stockholders, despite the availability of low-cost pre- ventive measures, is similar to the conclusion of Blanchard, Lopez-de-Silanes, and Shleifer (1994) in their study of the dispositions of cash windfalls realized by 11 public companies. After finding that large fractions of the cash windfalls are diverted to higher executive compensation, the authors argue that failings of corporate governance systems often lead to compensation systems in which "managers grab whatever profits they can get away with."

This research complements a line of articles that have found managers behaving opportunistically, and not necessarily in shareholders' interests, in response to the structure of their compensation. Healy (1985) shows that companies' accounting policies are influenced by managerial compensation, as firms are more likely to accrue discretionary expenses during years in which their operating income exceeds the upper limits or falls below the lower limits

454 The Journal of Finance

of managers' accounting-based bonus plans. Lambert, Lanen, and Larcker (1989) find that firms pay lower dividends than expected after the adoption of executive stock option plans, and Jolls (1996) finds that managers holding large numbers of options tend to substitute stock repurchases for dividend payments as a means of distributing free cash flow. Dechow and Sloan (1991) find that managers reduce research and development spending as they near expected retirement, apparently to maximize bonus payments tied to account- ing earnings.

In all of these studies, the authors find evidence that managers manipulate some parameter of the firm's operating or reporting strategy to increase compensation. Arguably, these actions might be in shareholders' interests or carry small costs, since shareholders choose not to bear the cost of writing and enforcing contract terms to prevent the behavior (Jensen and Meckling (1976)). In contrast, the findings of this study involve no manipulation of strategy, only an opportunistic choice of stock option award dates that transfers wealth from stockholders to managers. Moreover, the practice could be eliminated at al- most no cost, by using off-the-shelf contracting terms that require stock options to be awarded on fixed dates each year, or not within a certain interval around regular corporate news releases (such as earnings announcements).

II. Stock Option Awards and Stock Price Movements

To study whether top managers' stock option awards occur at favorable times, I use data from the first two annual proxy statements filed by Fortune 500 companies in compliance with the SEC's 1992 reformed executive com- pensation disclosure rules. The April 1993 Fortune 500 list serves as the basis for the sample. For each company, I collect information about stock options awarded to the CEO; when more than one person holds the CEO position during a fiscal year, I collect data for the person in office the longest. Excluding a handful of observations with data problems,3 the sample includes 620 CEO stock option awards made in the 1992-93 and 1993-94 fiscal years, with some companies accounting for multiple awards. In 46 cases, companies list a Saturday or Sunday as the stock option award date; I count these awards as having been made on the previous Friday, since that day's stock price must have been the basis for setting the exercise price.

A. Stock Price Increases After CEO Option Awards

A straightforward test of whether CEOs receive stock options at favorable times comes from studying movements in company stock prices around option

3 A small number of companies reported only the month and not the exact date of stock options' expirations, technically violating the SEC's rules. A few other firms made option awards during periods when their stock was not traded, such as initial public offerings, reorganizations, and switches between stock exchanges. I did not gather data for "reload" option awards that some companies automatically make to their CEO when existing options are exercised. I also omit a small number of events involving the repricing or exchange of older options.

CEO Stock Option Awards and Company News Announcements 455

award dates. The hypothesis of this study implies that CEOs receive stock options shortly before favorable news pushes stock prices higher. The corre- sponding null hypothesis is that stock prices exhibit no significant movement after option awards are made.

For each stock option award, I use daily stock return data from the Center for Research in Security Prices (CRSP) database to estimate abnormal stock returns around the award date. Following the widely used event-study meth- odology of Dodd and Warner (1983), I define each day's abnormal return (AR) as

ARit= Rit - Rit = Rit - ai - Pi Markett (1)

where Market is the yield on CRSP's dividend-inclusive, value-weighted index for the Nasdaq or New York Stock Exchange/American Stock Exchange (NYSE/AMEX) file. The subscripts i and t indicate companies and days, re- spectively. The ai and P3i market model parameters are estimated from regres- sions of Rit against Markett using one year of daily trading data prior to the event period surrounding each stock option award.4

I use daily abnormal returns to form cumulative abnormal returns (CARs) over an event period beginning 20 trading days (or approximately one month) prior to each stock option award and lasting until 120 trading days (or approx- imately six months) thereafter. The one-month lead time is used to illustrate that the cumulation of positive CARs begins exactly on the option award date. For the sample of 620 stock option awards, I average together the CARs for each day, testing their significance with t-statistics calculated according to Dodd and Warner (1983). Table I presents average CARs over the course of the event period; the same data are displayed in Figure 1 above. Note that the sample declines from 620 to 613 over the event period, mostly due to the unavailability of 1995 trading data in the CRSP database; these data are necessary to calculate long-term CARs for awards made after mid-1994.

Company stock prices begin rising just after the days on which CEOs receive stock option awards, and companies outperform the market on a risk-adjusted basis by slightly more than 2 percent over the next ten weeks or 50 trading days. Average CARs grow in a steady pattern over this period, suggesting that "good news" events for sample firms occur at an approximately uniform rate over the ten weeks after CEOs receive stock options. According to two-tailed hypothesis tests, the average CAR (calculated relative to day t20) has mag- nitude of + 1.18 percent and is significantly greater than zero at the 5 percent level three weeks or 15 trading days after the award; one week later the magnitude rises to +1.55 percent with significance below 1 percent.

After approximately 50 trading days or ten weeks, the rate of cumulation of abnormal returns slows. The average CAR that is permanently embedded in

4 Some investigators estimate market model parameters with data obtained both before and after the event period. That approach would be problematic with this article because many awards occurred in 1994, and the CRSP database does not yet include the necessary 1995 observations.

456 The Journal of Finance

Table I

Stock Returns Following Receipt of Stock Options by CEOs Cumulative abnormal stock returns (CARs) for Fortune 500 companies awarding stock options to their CEOs in the 1992-93 and 1993-94 fiscal years. Mean and median CARs are displayed for an event period around the dates of 620 CEO stock option awards. CARs and t-statistics are calculated from Dodd and Warner's (1983) market model methodology. The chart also shows the percentage of CARs that have positive values. Z-statistics for whether the distribution of CARs is centered at zero are based on Wilcoxon rank-sum, statistics. The data below are also displayed in Figure 1. The sample includes all firms listed in the 1993 Fortune 500 ranking of U.S. manufacturing and mining companies. Dates for CEO stock option awards are obtained from the first two proxy statements filed by each firm in compliance with the Securities and Exchange Commission (SEC) reformed rules for executive compensation disclosure, which became effective in late 1992. CARs are calculated using the Center for Research in Security Prices (CRSP) database.

Days Relative Sample % CARs Mean To Award Size Positive CAR t-Statistic Median CAR Z-Statistic

-20 620 47.6% -0.03% -0.21 -0.10% -0.99

-10 620 50.3% -0.09% -0.42 0.06% -0.52

AwardDate 620 48.1% 0.02% -0.28 -0.47% -0.40 1 620 48.7% 0.05% -0.17 -0.25% -0.04 2 620 49.8% 0.21% 0.36 -0.02% 0.38 3 620 50.6% 0.34% 0.65 0.10% 0.88 4 620 51.0% 0.36% 0.60 0.26% 0.91 5 620 49.7% 0.47% 0.96 -0.05% 1.15 6 620 50.0% 0.53% 0.99 0.01% 1.29 7 620 51.9% 0.67% 1.22 0.52% 1.46 8 620 51.5% 0.73% 1.31 0.33% 1.60 9 620 51.6% 0.77% 1.39 0.32% 1.61

10 620 51.5% 0.86% 1.55 0.43% 1.80*

15 620 53.1% 1.18% 2.08** 0.84% 2.43**

20 620 54.5% 1.55% 2.71*** 0.73% 2.92***

30 619 55.4% 1.71% 2.81*** 1.98% 3.09***

40 619 55.7% 1.67% 2.70*** 1.92% 2.92***

50 618 57.4% 2.27% 3.42*** 2.16% 3.50***

60 618 55.7% 2.30% 3.14*** 2.30% 3.02***

80 616 53.2% 2.13% 2.68*** 1.30% 2.37**

100 614 51.6% 2.56% 2.68*** 1.27% 2.29**

120 613 54.5% 2.82% 2.47** 1.86% 2.33**

* Significant at 1% level. ** Significant at 5% level.

* Significant at 10% level.

CEO Stock Option Awards and Company News Announcements 457

stock prices levels off between 2.5 percent and 3.0 percent, as shown by the data in Table I and the illustration in Figure 1.

To attribute these abnormal returns to the arrival of unrelated "good news," one must believe that investors remain unaware of CEO stock option awards for some time after the grant date. As discussed, the only official way that companies inform the public about executive option awards occurs in annual proxy statements, which are filed approximately three months after a fiscal year ends. My own experience in reading news stories, press releases, and on-line indices concerned with executive compensation suggests that timely press reports of stock option awards are almost unheard of.5 This claim is supported by the analysis of trading volume in Section IV.A below, which shows essentially no change in typical volume around the dates on which CEOs receive options. While reporters and analysts will occasionally learn that companies have adopted new incentive compensation plans (see, e.g., Dial and Murphy's (1995) account of analysts following General Dynamics Corp.), their dispatches rarely report such details as the dates of individual compen- sation awards, which usually occur intermittently for years after plans are adopted.

B. Stock Price Behavior Before CEO Option Awards

The data in Figure 1 are consistent with stock prices moving upward after CEOs receive options due to the arrival of "good news." However, I do not find a corresponding pattern of stock prices moving downward in advance of option awards, as would be the case if option awards were delayed until after the disclosure of "bad news." Table I indicates that the mean CAR between dates t_20 and the award date is almost exactly zero (t-statistic = -0.28). If the period prior to the award is extended further backward, I find negative and significant CARs before the award date on the order of -0.5 percent to -1.0 percent, with a high frequency of negative abnormal returns between t50 and t_30. Because these CARs stop cumulating six weeks before the option award date, and because they do not have the same magnitude as the positive CARs found immediately after option awards, I do not place great weight upon them.

If CRSP's equal-weighted market index is used instead of the value- weighted index as the proxy for the market portfolio, my results change

'A typical example is Frank's (1996) report that the CEO of Coca Cola Co. had received an award of 1 million stock options in April, 1995. While obviously of interest to investors, this news was not reported by The Wall Street Journal until February, 1996, ten months after the award date, when Coca Cola released a draft version of its proxy statement. In some special cases, investors do learn of CEO stock option awards quickly. Occasionally, news reports describe the compensation packages awarded to new CEOs hired from outside the company (see, e.g., New York Times (1995)). Companies submitting new stock option plans for shareholder approval sometimes describe proposed awards under those plans in documents filed with the SEC, and CEOs' employ- ment contracts sometimes include guarantees of stock option awards in the future. However, all three of these cases occur only rarely, and the latter two require CEO option awards to be disclosed long in advance, which would not account for the pattern of returns in Figure 1.

458 The Journal of Finance

slightly. I find a mean CAR of -0.58 percent (t-statistic = -1.89) between t20 and the award date, giving some evidence that CEO stock option awards occur after the release of adverse news. Positive abnormal returns then begin cu- mulating on the award date, in a pattern similar to that found when the value-weighted index is used as the market portfolio. However, I am reluctant to rely on the equal-weighted index because it does not appear to be well correlated with the price movements of the large companies in my sample. When using the value-weighted index to estimate the a and ,B market model parameters, I obtain mean values across my 620 observations of -0.00003 and 0.99, respectively, very close to the expected values of 0 and 1. In contrast, the mean a and ,B estimates are -0.001 and 1.19, respectively, when the equal- weighted index is used. If this latter a estimate is annualized by multiplying it by the number of trading days in a year, it equals -0.26, a value that seems implausible. This problem probably reflects the widely recognized tendency of large firms to underperform the market, since the equal-weighted index places relatively more weight on the performance of smaller firms.

The use of the equal-weighted indexed appears to reconcile my results with those of Chauvin and Shenoy (1995), who study CARs around stock option awards in an article written contemporaneously with this study. Chauvin and Shenoy, who use CRSP's equal-weighted index as the market portfolio and also have a sample comprised of large firms, report a CAR of -0.57 percent (t-statistic -3.46) between day t-1o and the award date. They do not report results using the value-weighted index, nor do they look at CARs beyond day t+1o.

C. Value to CEOs of Abnormal Stock Returns

To add perspective to the finding that CEOs receive stock options at favor- able times, I calculate the value to the typical CEO of the post-award stock price "bounce." I use a simple method that represents an upper bound on the change in value for each option award: I multiply each award's face value (number of shares under option times market value of stock on the award date) by the company's abnormal stock return in the period following the award date. Allowing for negative values in cases where the CAR is less than zero, I find that the average abnormal increase in option award value is $30,000 after 20 trading days and $48,900 after 50 trading days (median values are $11,100 and $15,600, respectively). All of these numbers are statistically significant at the 1 percent level, although the economic significance may be minor compared to the average cash salary of $632,900 (median $587,000) received by all Fortune 500 CEOs in the 1993-94 fiscal year. However, from shareholders' perspective, one must recognize that the wealth increase realized by the CEO is likely to be matched by similar increases in the value of options awarded to other top managers, since it is common for firms to award options to many executives on a single date.

CEO Stock Option Awards and Company News Announcements 459

D. Predictable and Unpredictable Award Schedules

Most companies grant stock options in predictable patterns, with CEOs receiving awards at approximately the same time each year. I find evidence that this practice helps explain the pattern of stock returns observed after option awards. I segment my sample into two groups. I classify a CEO's stock option awards as "predictable" if the executive receives options in each of the two fiscal years, with the award pair separated by at least 11 months but no more than 13 months; 350 of the 620 awards fall into this category. I treat 27 additional CEO awards as predictable when the CEO receives options in only one of the two years, but at least one of the other top five executives receives an award in the other year with the dates again separated by 11 to 13 months. The subsample of "unpredictable" CEO awards contains the remaining obser- vations, except that I do not classify four awards made by firms that were public companies in only one of the two sample years. I estimate CARs for each subsample over the 50 trading days following the award date. Each subsample exhibits positive and significant mean CARs. The latter subsample, represent- ing awards that appear to have occurred on a less-fixed schedule, has higher average CARs: 3.27 percent versus 1.59 percent, with the difference significant at the 11 percent level (t = 1.63). These results provide some evidence that CEOs receive option awards at more favorable times if their companies have no predictable schedule for granting options. The power of the test probably suffers from the shortness of the time period studied, since some awards classified as unpredictable would likely appear predictable if more years of data were available for analysis.

E. CEO Influence as a Predictor of Postaward CARs

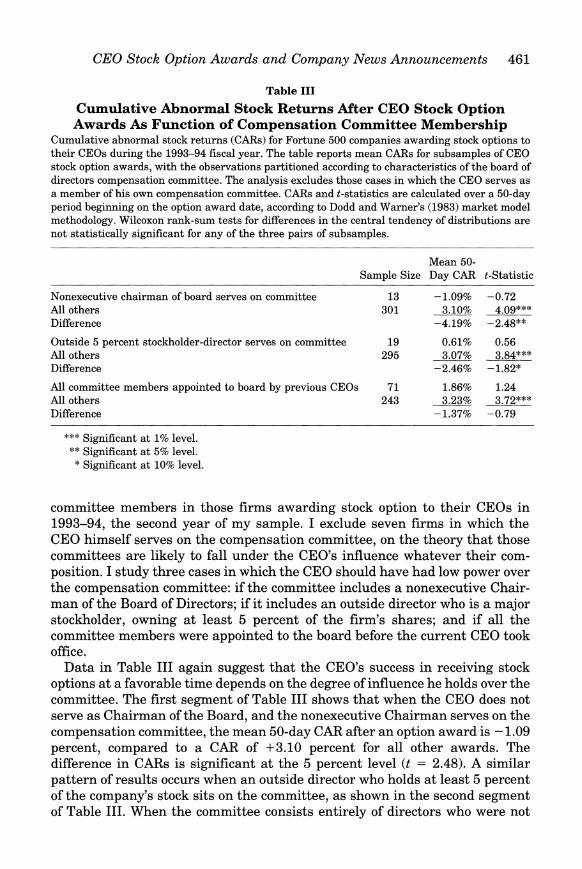

Indirect evidence that CEOs can influence their boards to award stock options at favorable times emerges from analyzing cases in which CEOs should be expected to have unusually great or small influence over members of the compensation committee (or similar group, such as a stock option committee, that has authority to approve option awards).

The most obvious opportunity for CEOs to influence compensation commit- tees should occur when the CEO personally serves as a committee member. I identify 13 option awards in my sample made under these conditions. Since these CEOs have a direct voice in structuring their compensation, one would expect them to receive stock options at especially opportune times. Table II lists the 13 stock option awards made to CEOs serving on their own compen- sation committees, and the table also shows that in many cases, favorable news announcements occur soon after the award. In 10 of 13 cases companies experience positive abnormal stock returns over the subsequent ten weeks (50 trading days). The average 50-day CAR following the awards is a startlingly high 11.2 percent, well above the sample average of 2.2 percent.

Table III reports the results of extending the analysis to certain cases in which CEOs should have low influence over the compensation committee. I gather data on the background and stock ownership of all compensation

460 The Journal of Finance

Table II

Option Awards to CEOs Serving on Their Own Compensation Committees

Stock option awards received by CEOs who serve as members of their own board of directors compensation committees. The table lists the date of each stock option award and significant news announcements that occurred shortly thereafter. In all cases, options were granted with exercise price equal to the stock's market price. The right column lists cumulative abnormal stock returns (CARs) for each company over the 50 trading days beginning with the award date, calculated from the market model approach of Dodd and Warner (1983). The observations represent a subsample of the 620 CEO stock option awards made in the 1992-93 and 1993-94 fiscal years by Fortune 500 companies. CEOs who received stock options while serving on their own compen- sation committees (or similar board of directors groups) are identified from corporate proxy statements, which also serve as the source for dates and exercise prices of each option award. News reports are extracted from the Nexis database, and abnormal stock returns are calculated from the Center for Research in Security Prices (CRSP) database. Several companies published disclaimers about the CEO's role on the compensation committee. Dexter Corp.'s CEO served in an ex-officio, nonvoting capacity. Reliance Electric's CEO resigned from the committee in the middle of the year and purportedly had no role in deliberations over his own pay. Nucor's entire board performed the function of the compensation committee. Total Petroleum delegated CEO compensation issues to the entire board except for the CEO. However, its compensation committee apparently did set the dates for CEO stock option awards, since all other top officers received awards at the same time.

50-Day CAR

Following Company CEO Award Date Subsequent News Award

Dexter Corp. K. Grahame Walker Apr. 24, 1992 Division sold (May 19) 5.9% Great American Mgt. Samuel Zell \ Dec. 16, 1992 None 0.8% Hudson Foods James T. Hudson Oct. 5, 1992 Analyst raises earnings 53.7%

estimate (Nov. 5) Kimball International Douglas A. Habig Aug. 26, 1993 None 4.9% Nucor F. Kenneth Iverson Feb. 28, 1992 Dividend increased -2.8%

(Mar. 16) Aug. 31, 1992 None 23.5% Feb. 28, 1993 Dividend increased -13.9%

(Mar. 12) Aug. 31, 1993 Prices increased; 1.8%

competitors match (Sep. 16)

Reliance Electric John C. Morley Dec. 16, 1993 New product 3.7% demonstration (Jan. 10)

Tandem Computers James G. Treybig Apr. 26, 1993 Division sold (May 10); -4.4% Analyst recommends stock

(May 14) Sep. 8, 1993 Analyst recommends stock 17.1%

(Oct. 4); New product

announcement (Oct. 6) Total Petroleum N. A. Daniel L. Valot Dec. 11, 1992 Analyst recommends stock 43.4%

(Jan. 8) Dec. 11, 1993 Dividend reinstated 11.5%

(Dec. 14) Mean 11.2%

t-Statistic 2.18** Median 4.9%

Wilcoxon Z-Statistic 1.99**

** Significant at 5% level.

CEO Stock Option Awards and Company News Announcements 461

Table III

Cumulative Abnormal Stock Returns After CEO Stock Option Awards As Function of Compensation Committee Membership

Cumulative abnormal stock returns (CARs) for Fortune 500 companies awarding stock options to their CEOs during the 1993-94 fiscal year. The table reports mean CARs for subsamples of CEO stock option awards, with the observations partitioned according to characteristics of the board of directors compensation committee. The analysis excludes those cases in which the CEO serves as a member of his own compensation committee. CARs and t-statistics are calculated over a 50-day period beginning on the option award date, according to Dodd and Warner's (1983) market model methodology. Wilcoxon rank-sum tests for differences in the central tendency of distributions are not statistically significant for any of the three pairs of subsamples.

Mean 50- Sample Size Day CAR t-Statistic

Nonexecutive chairman of board serves on committee 13 - 1.09% -0.72 All others 301 3.10% 4.09*** Difference -4.19% -2.48**

Outside 5 percent stockholder-director serves on committee 19 0.61% 0.56 All others 295 3.07% 3.84*** Difference -2.46% - 1.82*

All committee members appointed to board by previous CEOs 71 1.86% 1.24 All others 243 3.23% 3.72*** Difference -1.37% -0.79

*** Significant at 1% level. ** Significant at 5% level.

* Significant at 10% level.

committee members in those firms awarding stock option to their CEOs in 1993-94, the second year of my sample. I exclude seven firms in which the CEO himself serves on the compensation committee, on the theory that those committees are likely to fall under the CEO's influence whatever their com- position. I study three cases in which the CEO should have had low power over the compensation committee: if the committee includes a nonexecutive Chair- man of the Board of Directors; if it includes an outside director who is a major stockholder, owning at least 5 percent of the firm's shares; and if all the committee members were appointed to the board before the current CEO took offlce.

Data in Table III again suggest that the CEO's success in receiving stock options at a favorable time depends on the degree of influence he holds over the committee. The first segment of Table III shows that when the CEO does not serve as Chairman of the Board, and the nonexecutive Chairman serves on the compensation committee, the mean 50-day CAR after an option award is -1.09 percent, compared to a CAR of +3.10 percent for all other awards. The difference in CARs is significant at the 5 percent level (t = 2.48). A similar pattern of results occurs when an outside director who holds at least 5 percent of the company's stock sits on the committee, as shown in the second segment of Table III. When the committee consists entirely of directors who were not

462 The Journal of Finance

appointed to the board by the CEO, the average CAR is an insignificant + 1.86 percent, compared to +3.23 percent in all other cases, although the difference in these two returns is not significant.

F. Magnitude and Timing of Stock Option Awards

Evidence presented above is consistent with CEOs influencing the timing of stock option awards in order to increase their personal wealth. A related possibility is that CEOs might be able to affect the size of their stock option awards, arranging to receive especially large awards before expected stock price increases. I fail to find evidence of this latter conjecture. I compare the Black-Scholes value of each award with the 50-day CAR following the award date. The sample correlation between these two variables is near zero (-0.04) and not statistically significant. The sample correlations are very similar within the subgroups of predictable (-0.09) and unpredictable (-0.03) awards.

While I do not find evidence that the Black-Scholes value of CEO stock option awards is related to the awards' timing, several statistical issues make me uncertain about the strength of this conclusion. First, if CEOs did influence their boards to vary the size of stock option awards across time, they would choose to receive zero options during periods when they expect their stock prices to fall, effectively postponing a certain volume of options until a more favorable time. These cases of zero awards would be unobservable to research- ers, although one would expect the observed awards to occur at favorable times, as found in this study. Second, an analysis comparing the timing and value of stock option awards is arguably inappropriate, since one really seeks to know the relation between the timing of an award and its abnormal or unexpected component. Estimating each CEO's expected option award would require a Tobit regression model, estimated with numerous regressor variables over a sample that includes CEOs receiving zero options (Yermack, 1995). Such a model is beyond the scope of this article, but even if it were estimated, one would still have to resolve such issues as how to deal with CEOs who receive options more than once a year, and how to estimate the unexpected value of option awards for the large number of CEOs whose Tobit predicted values are less than zero.

ITI. Stock Option Awards and Earnings Announcements

Companies' quarterly earnings announcements provide convenient data for further testing the hypothesis that CEO option awards are timed to anticipate significant corporate news. Unlike some events that might take executives by surprise (such as tender offers or management changes), earnings news is almost certainly known in advance by CEOs, which would appear to be a necessary condition for opportunistically timing stock option awards around news disclosures. Moreover, all public companies must make earnings an- nouncements, which assures that no sample selection bias will arise when studying this type of news.

CEO Stock Option Awards and Company News Announcements 463

8%__ _ _ _

6%

$2

0~~~~~~~~~~~~~~~~~

0%

40 Days Prior -30 20 -10 Award D~ate I10 20 30 40 Days After

Award Date Relative to Nearest Earnings Announcement Date

Figure 2. Timing of CEO stock option awards and earnings announcements. Frequency distribution of CEO) stock option award dates relative to the dates of companies' nearest quarterly earnings announcements. The sample consists of 620 stock option awards to C:EOs of Fortune 500 companies between 1992 and 1994. Dates for CEO stock option awards appear in company proxy statements. Earnings announcement dates are obtained from Bloomberg Financial Markets, The Wall Street Journal Index, and miscellaneous press sources. The data displayed above reflect only those dates when U.S. stock exchanges are open for trading. A small number of awards that occur more than 40 trading days from any earnings announcement are omitted.

For each CEO stock option award, I obtain data about the earnings an- nlouncements that occur before and after the award date from Bloomberg Financial Markets and the Institutional Brokers Estimate System (I/B/E/S). I treat a handful of earnings announcements made during a weekend as having occurred the following Monday, since the first investor reactions would have happened then. Figure 2 illustrates the timing of CEO stock option awards relative to companies) earnings announcements. The most frequent day for CEOs to, receive stock options is one day in advance of earnings announce- ments, and the next-most popular day is the announcement date itself. This pattern may be partly explained by the requirement that boards of directors (or compensation committees) approve stock option awards, as many companies might have practices of announcing earnings just after board meetings. How- ever, the data are also consistent with coordination between option awards and the release of earnings news.

I measure the information content of earnings news in three ways. First, I calculate CARs around each announcement, using the market model method- ology described in Section II. The event period for these stock returns runs from the day before to the day after each announcement; I use a three-day window because of the possibility of advance leakage of earnings news, as well as the practice by some companies of releasing news after the stock market closes. Second, I estimate the surprises" in each earnings announcement as the difference between actual earnings and the mean forecast of a panel of ana-

464 The Journal of Finance

lysts surveyed by I/B/E/S (I use the last monthly I/B/E/S survey before each announcement). I report summary statistics for earnings surprises based on the dollar value of earnings one would have received for investing in an equal-weighted portfolio of the relevant companies' stocks.6 I treat an earnings announcement as a "large surprise" if actual earnings lie more than two standard deviations away from the mean analyst forecast. Finally, I report differences in quarterly earnings minus earnings for the prior quarter, again calculating descriptive statistics from hypothetical equal-weighted portfolios of company stocks.

If CEOs could control the timing of stock option awards around news an- nouncements, one would expect differences in earnings announced before and after CEOs received stock option awards. In particular, favorable earnings announcements should occur after stock option awards. Adverse announce- ments, if they occur at all around the time of stock option awards, should happen before awards are made. Summary statistics in Table IV provide evidence that CEOs receive stock option awards in advance of good earnings news, and weaker indications that awards occur after poor earnings announce- ments (the analysis excludes the 33 cases in which CEOs receive stock option awards on the exact day of earnings announcements).

Abnormal stock return data indicate that earnings announcements after CEOs receive stock options are more favorable than those announcements preceding stock option awards. Mean and median CARs are positive for earn- ings announcements following CEO option awards, while CARs are close to zero and insignificant for announcements preceding awards. The right half of Table IV shows the same data for the subset of earnings announcements occurring around "unpredictable" CEO stock option awards, with the predict- ability of awards determined by the same criteria discussed above. Since a CEO should be more likely to be awarded options at a favorable time if his firm does not follow a predictable schedule, I expect stronger evidence of opportu- nistic timing for unpredictable awards. As expected, both mean and median CARs for earnings announcements following stock option awards are positive, statistically significant, and markedly higher for unpredictable awards com- pared to the sample as a whole.

Data for earnings surprises and earnings changes also support the hypoth- esis. More large positive surprises occur than large negative surprises when earnings are announced after CEOs receive stock options, with the opposite holding for announcements in advance of option awards. While mean earnings surprises are negative for all types of announcements, they are closer to zero

6 I assume that $1,000 is invested in the stock of each company, using the price reported by I/B/E/S for the date of the last monthly analyst survey before each announcement. This approach to calculating descriptive statistics about company earnings avoids problems posed by earnings per share data, which frequently includes negative or outlier values that confound the calculation of percentage changes. The equal dollar approach also assures that all observations contribute evenly to the calculation of descriptive statistics, which is not the case when one forms portfolios by assuming that an equal number of shares of stock are purchased in each company. See Ikenberry and Lakonishok (1993) for references and a fuller discussion.

CEO Stock Option Awards and Company News Announcements 465

Table IV

Earnings Announcements Before and After CEO Stock Option Awards

Descriptive data about company announcements of quarterly earnings, for those announcements preceding and following stock option awards to CEOs. Cumulative abnormal stock returns (CARs) are presented for the period beginning one trading day before and ending one trading day after each earnings announcement. A market model methodology following Dodd and Warner (1983) is used to calculate CARs. Earnings surprises represent the difference between a company's actual earnings and the mean forecast by a panel of analysts surveyed by the Institutional Brokers Estimate System (I/B/E/S). Large positive and negative surprises in earnings are defined to occur when actual earnings are more than two standard deviations from the mean analyst forecast. Descrip- tive statistics for earnings surprises and changes in earnings from the prior quarter are presented on a dollar basis, with statistics calculated from hypothetical equal-weighted portfolios comprised of $1,000 invested in each company's stock. The analysis is based on 620 stock option awards to CEOs of Fortune 500 companies between 1992 and 1994, excluding 33 cases in which CEOs received stock option awards exactly on the days of earnings announcements. The left half of the table shows data for all CEO stock option awards, while the right half presents data for the subsample of awards that are not "predictable." Predictable awards are defined as those made by a company to its CEO in both sample years, with the awards occurring at approximately the same time (within one month) during each year. Earnings data are obtained from I/B/E/S, and some missing values occur due to omissions from the I/B/E/S survey. Stock option award dates are obtained from company proxy statements. Stock return data are obtained from CRSP.

All Earnings Announcements Earnings Announcements Around Around CEO Stock Option Awards Unpredictable Awards

Prior Subsequent Difference Prior Subsequent Difference

Abnormal Stock Returns Observations 587 586 227 226 Mean 0.12% 0.66% 0.54% 0.09% 1.05% 0.96% t-Statistic 0.84 5.05*** 1.85* 0.40 4.79*** 1.83* Median 0.25% 0.38% 0.13% -0.13% 0.55% 0.68% Wilcoxon Z-Statistic 1.30 2.94*** 1.07 -0.16 2.15** 1.48

Earnings surprises, per $1,000 invested Observations 542 552 200 205

Large Positive Surprises 60 83 23 21 33 12

Large Negative Surprises 96 74 (22) 44 37 (7)

Mean ($3.12) ($1.70) $1.42 ($7.33) ($2.67) $ 4.66 t-Statistic - 1.68* -2.19** 0.70 -1.49 -1.40 0.88 Median $0.00 $0.00 $0.00 $0.00 $0.17 $ 0.17 Wilcoxon Z-Statistic -0.95 1.11 1.54 -2.07** 1.32 2.83***

Change in earnings from prior quarter, per $1,000 invested Observations 572 568 211 215 Mean ($2.57) $1.91 $4.48 ($6.75) $6.29 $13.03 t-Statistic -1.34 0.80 1.46 -1.35 1.02 1.64*

Median $0.00 $0.89 $0.89 $0.00 $1.52 $ 1.52

Wilcoxon Z-Statistic -0.41 1.94** 1.83* -1.14 2.82*** 2.88***

*** Significant at 1% level. ** Significant at 5% level.

* Significant at 10% level.

for announcements after CEO option awards. Within the subset of unpredict- able awards, the difference in median earnings surprises is positive and significant. Data for earnings changes relative to the prior quarter exhibit a

466 The Journal of Finance

Table V

Abnormal Stock Returns for Earnings Announcements in Relation To CEO Stock Option Award Date

Cumulative abnormal stock returns (CARs) surrounding company announcements of quarterly earnings, tabulated according to the time between the announcement and the date of a stock option award to the company's CEO. CARs are presented for the period beginning one trading day before and ending one day after each announcement. A market model methodology following Dodd and Warner (1983) is used to calculate CARs and t-statistics. The entire sample consists of 620 stock option awards to CEOs of Fortune 500 companies between 1992 and 1994. Earnings announcement dates are obtained primarily from Bloomberg Financial Markets and The Wall Street Journal Index, while dates of CEO stock option awards are obtained from company proxy statements.

Mean CAR for Median CAR for Award Timing Relative to Sample Earnings Earnings Wilcoxon Z Earnings Announcement Size Announcement t-Statistic Announcement Statistic

6 to 10 days before 20 0.59% 0.41 -0.28% -0.49 2 to 5 days before 25 2.53% 2.90*** 0.85% 1.92* 1 day before 36 2.24% 3.95*** 1.14% 1.79* 1 day after 12 0.68% 0.60 0.49% 0.55 2 to 5 days after 57 -0.36% -0.00 0.15% -0.08 6 to 10 days after 62 -0.20% -0.96 0.04% -0.31

*** Significant at 1% level. ** Significant at 5% level.

* Significant at 10% level.

similar pattern, with more favorable changes being reported after a CEO has received stock options.

Analysis in Table V explores whether the coordination improves between the timing of option awards and earnings announcements when the earnings news is important. Table V presents earnings announcement CARs tabulated ac- cording to the time between the announcement and the date of the CEO's stock option award. Unusually large CARs occur for earnings announcements that are made just after the CEO receives stock options-for example, when the CEO receives an option award one day before an earnings announcement, the mean CAR is +2.24 percent (t-statistic 3.95) while the median is + 1.14 percent (Wilcoxon Z-statistic 1.79). In contrast, no significant pattern of CARs is evident for earnings announcements made just before CEOs receive options. The data appear to support a conjecture that when positive earnings an- nouncements are made very close to the time of a CEO stock option award, the CEO is quite likely to receive his options before the announcement instead of afterwards.

IV. Discussion

The results presented in Sections II and III suggest that CEOs benefit from favorable timing of stock option awards relative to corporate news announce- ments. The results appear more striking when contrasted with studies of legal

CEO Stock Option Awards and Company News Announcements 467

insider stock trades around news announcements. Several investigations have found that executives do not succeed in timing stock trades to exploit contem- poraneous news. Givoly and Palmon (1985) examine insider trading around news announcements by 68 AMEX companies and find no evidence of greater inside purchases before favorable news or greater selling before adverse news. Elliott, Morse, and Richardson (1984) study insider trading around nearly 4,000 news announcements by NYSE/AMEX firms. They also find no consis- tent evidence that executives trade opportunistically around public announce- ments.

While the evidence presented above appears to offer a prima facie case that managers influence the terms of stock option awards to their financial advan- tage, numerous alternative explanations are possible. The following subsec- tions evaluate five such theories, including contemporaneous trading by those with knowledge of CEO stock option awards; acquiescence by directors and shareholders in the opportunistic timing of option awards as a surrogate form of insider trading by executives; deliberate awards of stock options by boards in advance of good news for incentive reasons, or to circumvent investor criticism and accounting costs associated with in-the-money discount options; the use of expected upward movements in option values as a form of tax arbitrage between executives and firms; and the possibility that executives manipulate the timing of news announcements rather than the timing of option awards. For a variety of empirical, institutional, and legal reasons discussed below, none of these alternative theories appears persuasive.

A. Trading on Knowledge of CEO Option Awards

One possible explanation for abnormal stock returns following CEO stock option awards could be news of the awards leaking to some investors around the award dates. If informed investors (including members of the board or CEOs themselves) learned that a CEO had received stock options, they might attempt to capitalize on the news by purchasing stock either legally or ille- gally, thereby pushing prices higher.

A reason to doubt the importance of this trading conjecture is that abnormal stock returns do not begin to cumulate until after the award dates of CEO stock options (see Figure 1 and Table I). Many insiders with access to knowledge of CEO stock option awards would almost certainly know of the awards in advance, and if they considered this knowledge important enough to buy stock, they would undoubtedly buy as soon as possible, causing abnormal returns to experience a "run-up" before the option award date, as is often observed in event studies of investor reactions to significant news.

Nevertheless, the information leakage hypothesis seems compelling enough to warrant further investigation. One cannot reliably test the hypothesis by using standard SEC data about officer and director stock purchases around the dates of CEO stock option awards. As shown above, corporations often release significant news (such as quarterly earnings) very close to the days on which CEOs receive options. Since insiders have at least a ten-day grace period in

468 The Journal of Finance

which to report stock purchases, any significant pattern of insider purchases near the dates of CEO stock option awards could easily be attributed to other news announcements.

An alternative test for the presence of increased trading around the time of important corporate events has been used by Meulbroek (1992), who estimates a market model of trading volume around insider trading episodes. In her study of 131 cases of insider trading, Meulbroek finds that volume in a firm's stock is 93 percent higher than expected on days in which the SEC identifies an insider trading event. Moreover, her study documents a link between this increased volume and the magnitude of abnormal stock price movements.

I follow Meulbroek's approach for analyzing trading volume by using a market model for volume. This regression analysis, an extension of work by Ajinkya and Jain (1989), is similar to the market model for abnormal stock returns:

log(vit) = ai + il0log(vmktt) + 01log(vit-1) + 2lo0g(vit-2) + q,Monit + 2Tueit + 3Wedit + 4Thuit + OlHolidayit + 02Holidayit-l + piEarningsit + 6iDividendit + -yiOption Awardit + Eit (2)

In the specification of the model, vt represents daily trading volume in a company's stock, while vt-l and Vt-2 are lags added to the model to reduce serial correlation of the residuals.7 The Vmkt term is total volume for the New York, American, or Nasdaq exchange, as appropriate. Mon, Tue, Wed, and Thu are day-of-the week dummies, and Holiday is a dummy variable equal to one for days preceding three-day holiday weekends and Fridays following Thanks- givings. Earnings, Dividend, and Option Award are dummy variables equal to one during the event periods surrounding earnings announcements, dividend announcements, and CEO stock option awards, respectively. I estimate the model for a variety of event periods, as discussed below.

I run the market model regression separately for each of the CEO stock option awards, using daily volume data from 50 trading days before until 50 days after each award date as the sample. I drop from the analysis six option awards for which the three events of an earnings announcement, dividend announcement, and CEO stock option award occur simultaneously. I use dummy variables for observations for which the CEO stock option award occurs on the same day as either an earnings or dividend announcement, so that data around those events can contribute to estimates of the coefficients on the Earnings or Dividend dummy variables. Regressions over the sample therefore yield approximately 500 estimates of the p, 6, and y parameters,

7 Because the model is estimated separately for each CEO stock option award and the results then aggregated, it is not straightforward to conduct a hypothesis test for serial correlation. However, it is highly suggestive to observe that in the basic specification of the model, the mean estimated first-order residual autocorrelation coefficient rises from 0.008 to 0.319 if the two lagged volume terms are excluded. The magnitude and significance of coefficient estimates appears unaffected by inclusion of the lagged volume terms.

CEO Stock Option Awards and Company News Announcements 469

Table VI

Abnormal Trading Volume Around CEO Stock Option Awards Coefficient estimates for a model of abnormal trading volume surrounding the dates of CEO stock option awards. Estimates are from a log market model of trading volume similar to that used by Meulbroek (1992). The model includes controls for market volume, two days of lagged company trading volume, days of the week, and holidays. The sample includes daily volume data surround- ing 620 awards of stock options to CEOs of Fortune 500 companies between 1992 and 1994. The market model regression is estimated separately for each award, using 50 leading and 50 trailing days of data. Individual coefficient estimates are averaged to produce the estimates in the table, with standard errors obtained from a method similar to that of Dodd and Warner (1983). Dates on which stock option awards coincide with either earnings announcements or dividend announce- ments do contribute to the estimates below, due to the use of dummy variables in the regression model. The table reports estimated abnormal trading volume for event periods surrounding awards of CEO stock options (for which no public announcements occur), as well as event periods surround- ing quarterly dividend and quarterly earnings announcements. Abnormal volume is reported as an average per day for each event period, and results appear for four alternative sets of event periods. Abnormal volume estimates should be interpreted as percent deviations from normal daily trading volume.

Daily Abnormal

Type of Event Event Period Volume t-Statistic

Event period no. 1 CEO stock option awards event day only - 1.0% -0.27 Dividend announcements event day only 7.1% 3.26*** Earnings announcements event day only 37.5% 18.80***

Event period no. 2 CEO stock option awards [-1, 1] 0.7% 0.83 Dividend announcements [-1, 1] 0.8% 0.87 Earnings announcements [-1, 1] 19.1% 15.22***

Event period no. 3 CEO stock option awards [-10, 10] 1.1% 1.97** Dividend announcements [-1, 1] 0.5% 0.86 Earnings announcements [-1, 1] 20.0% 15.92***

Event period no. 4 CEO stock option awards [-5, 50] -0.7% -3.63*** Dividend announcements [-1, 1] 1.8% 1.58 Earnings announcements [-1, 1] 19.9% 15.80***

*** Significant at 1% level. ** Significant at 5% level.

which measure the abnormal trading volume on days around earnings an- nouncements, dividend announcements, and CEO stock option awards, respec- tively. The arithmetic mean of the individual estimates serves as the overall estimator of each parameter. Standard errors are calculated following Dodd and Warner's (1983) method of aggregating standardized prediction errors.

Table VI presents results of estimating the model with four alternative specifications of the event periods around earnings announcements, dividend announcements, and CEO stock option awards. When each event period is restricted to a single day, abnormal volume is estimated at 37.5 percent on

470 The Journal of Finance

days with earnings announcements, 7.1 percent on days with dividend an- nouncements, and -1.0 percent on days with CEO stock option awards. Only the earnings and dividend announcement abnormal volumes are statistically significant. When the window is widened to include the day before and after each event, abnormal volume is estimated as 19.1 percent, 0.8 percent, and 0.7 percent per day, respectively, with only the earnings-related volume having statistical significance. Other estimates are shown with increasingly wider event periods surrounding CEO stock option awards; these estimates are representative of the results of analyzing numerous event windows around the option award dates. The estimated abnormal trading volume surrounding CEO stock option awards, while sometimes statistically significant, always falls within the approximate range of plus or minus 1.0 percent of usual daily volume. The abnormal volume surrounding CEO option awards never begins to approach the levels needed to explain the abnormal stock returns of more than 2 percent that cumulate after the option award date, according to Meul- broek's (1992) estimates of the association between abnormal volume and abnormal stock returns. I conclude that volume evidence does not support conjectures that increased trading around the dates of CEO stock option awards accounts for the CARs observed during these periods.

B. Shareholder Acquiescence in Surrogate Insider Trading by CEOs

Although the above evidence gives little indication that unusual trading activity takes place around the dates of CEO stock option awards, the profits earned by CEOs due to the favorable timing of these awards makes them resemble a surrogate form of insider trading, albeit without the ordinary requirements of disclosure or risks of detection and prosecution. Some scholars have suggested that shareholders may encourage insider trading by managers for incentive reasons.

Manne (1966) and Carlton and Fischel (1983) are leading exponents of legal insider trading theories, which rest upon assumptions about managerial risk- bearing and the costs of renegotiating compensation contracts. The theories hold that allowing managers to choose secretly when to buy and sell stock will increase their incentives to pursue valuable corporate opportunities and gen- erate positive news on which they can trade. Such arrangements could reduce the costs of writing compensation contracts and protect managers against unfairness in the ex-post settling up process. Further, the willingness of managers to work under such a regime might serve as a valuable signal about their risk preferences.

Many writers have attacked these theories, arguing that permitting insider trading would allow executives to subvert market mechanisms that set wages competitively (Ross (1979)), encourage destructive managerial behavior tied to short-selling, undermine public confidence in the securities markets, and inefficiently reward managers who have fortuitous access to certain informa- tion (see, e.g., Brudney (1979)). This study has relevance for the latter argu- ment, since CEOs appear to receive stock-based compensation shortly in

CEO Stock Option Awards and Company News Announcements 471

advance of stock price increases tied to earnings or other announcements. Even if stockholders acquiesced in the opportunistic timing of CEO stock option awards, considering it an implicit form of compensation, such arrange- ments would contravene the spirit and possibly the letter of the federal secu- rities laws.

Under the "disclose or abstain" doctrine, company executives who have knowledge of significant future news announcements may not acquire stock until the news is disclosed to the public; otherwise they face civil and criminal penalties under Rule 10b-5 of the Securities Exchange Act of 1934. Whether this doctrine covers CEOs who influence their boards to grant stock options at favorable times represents a novel legal issue, since courts would have to decide whether the option award represented the "purchase" of securities for the purposes of Rule 10b-5. However, even though the receipt of a stock option award arguably involves no purposeful action by an executive, it is settled law that these awards represent "purchases" under the closely related Rule 16b- 6(c) prohibition against short-swing profits from insider trading. SEC (1991) directly recognizes the possibility that CEOs could influence their boards to award stock options at favorable times:

[N]ot to treat the employee option ... as a purchase for Section 16 purposes would be to provide a significant opportunity for the short-swing transactions Congress wished to eliminate. For example, an insider could sell employer stock in advance of bad news, and obtain a specially-authorized stock option grant at market after the price drop.

C. Awarding In-the-Money Options for Incentive Reasons

Two theories related to the structure of managerial incentives may cause boards of directors to award stock options to their CEOs shortly before ex- pected increases in the company's stock price. First, boards may want to award discount options with in-the-money exercise prices in order to achieve a larger pay-performance sensitivity than is provided by at-the-money, fair market value options. Second, boards may want to reward executives for their role in generating the favorable news that is expected to increase the stock price.

On a share-for-share basis, discount options provide higher pay-performance sensitivities to CEOs compared to fair market value options (see Lambert, Larcker, and Verrecchia (1991)). Boards of directors may want to obtain these incentive benefits from in-the-money options without bearing the accounting penalties8 and investor criticisms that may accompany the award of discount options. A board could conceivably do so by awarding fair market value options to a CEO at a favorable time, just before the public disclosure of good news that should push the company's stock price higher and move the option into-the-

8 Under current accounting rules, options awarded in-the-money are disfavored relative to fair market value options. Firms must expense the discounted portion of discount options over the vesting period (usually within the first several years after the award date), while fair market value options do not lead to any reported compensation expense.

472 The Journal of Finance

money. The similar possibility that boards may want to reward executives who produce good news by allowing them to profit from the expected "bounce" in the stock price is closely related to Fama's (1980) "expost settling up" theory of compensation.

While these conjectures seem theoretically sound, several institutional re- alities appear to render them unlikely as an explanation for the favorable timing of option awards. First, as discussed above, either practice would seem to violate the "disclose or abstain" principle of the insider trading laws even without purposeful action by the CEO. Second, attempts by boards to award stock options in the expectation that they will move quickly into-the-money would seem to invite unavoidably large errors. Well-known alternatives such as restricted stock or phantom stock could more precisely deliver compensation with the intended value and incentive structure. Third, if companies really did give great thought to the optimal exercise prices of executive options, one would expect a nontrivial fraction of options to be awarded out-of-the-money, although these premium options are rare. Finally, one would have expected to observe at least some lobbying by major companies for the FASB to relax the accounting penalties associated with discount options. However, this issue seems to have drawn no attention at all, even though the accounting treatment of executive stock options has in recent years become a major topic of debate in American business.

D. Minimizing Net Tax Expenses

Most CEO stock options are "nonqualified" for tax purposes, offering a theoretical possibility of net tax savings to an executive and his company compared to the taxes associated with cash compensation. If a firm pays compensation in nonqualified stock options instead of cash, when the options are exercised it obtains a tax deduction equal to the options' in-the-money value. Although this deduction may not have as high a present value as the immediate deduction associated with straight cash pay, overall tax savings between the company and the executive are possible since the executive's personal income tax is also delayed until the exercise date (see Scholes and Wolfson (1992)).9 This net effect, which hinges on the marginal tax rates of the executive and the company, could be increased if both parties were aware that the options were likely to rise in value due to impending good news.

Again, institutional realities appear to render unlikely this explanation for the favorable timing of CEO stock option awards. As noted above, reliance upon the future path of a company's stock price as a means of reducing the tax consequences of compensation appears fraught with uncertainty and is likely dominated by other schemes, such as higher pension benefits or deferred

I This summary explanation does not do justice to the complexities of the tax laws surrounding executive stock options. For example, it is sometimes efficient for an executive to renounce options' tax-favored status before exercising them. For fuller treatments, see Matsunaga et al. (1992) and Scholes and Wolfson (1992).

CEO Stock Option Awards and Company News Announcements 473

compensation.10 Moreover, the importance of tax considerations for stock op- tion awards appears to have diminished markedly in recent decades. While early research such as Holland and Lewellen (1962) attributed the initial spread of stock options to the vast differences in personal tax rates for earned income and capital gains in the 1950s and 1960s, those differences narrowed considerably (and at times disappeared) in the 1980s and 1990s, and they are not necessarily relevant if the CEO's options are nonqualified for tax purposes. Recent cross-sectional studies by Matsunaga (1995) and Yermack (1995) fail to find a relation between firms' relative tax positions and their use of stock options for executive compensation.

E. Managerial Manipulation of News Releases

Much of the preceding text argues that CEOs influence the timing of stock option awards in order to capitalize on movements in stock prices tied to expected news announcements. An equivalent scheme would be for CEOs to manipulate the timing of news announcements in order to increase the value of stock options that they expect to receive from their firms on certain dates. These two explanations do not seem entirely different, as each implies that managers become enriched by controlling some sequence of corporate events. However, the alternative theory does not cast aspersions upon boards' com- pensation committees, since it carries no implication that the committees fall under the influence of the executives whose contracts they negotiate.

Further analysis of the data in this study, as well as the results of other articles, appears to contradict the theory that managers manipulate the dates of news announcements instead of the dates of stock option awards. Such a strategy would require CEOs to delay announcements containing good news until after stock option awards occurred, and rush forward announcements of bad news so that company stock prices fell in advance of (and not after) option awards. A long line of studies has found that managers behave in the opposite way, announcing favorable news quickly and delaying adverse news. See Kross and Schroeder (1984) and Penman (1984) (earnings announcements) as well as Kalay and Lowenstein (1986) (dividends).

I test the conjecture that CEOs delay favorable earnings announcements and rush forward adverse announcements by analyzing the sample of quar- terly earnings announcements gathered for Section III of this study. I assume that the abnormal stock return surrounding an earnings announcement rep- resents the strength of good or bad news conveyed by the announcement. I use this stock return as an explanatory variable in a regression with the dependent

10 Stock option awards do have the advantage of allowing the executive to choose when to exercise the options and incur the tax expense. However, this flexibility is limited to the term of the option, and executives arguably have the same type of discretion over when to recognize pension benefits by choosing their dates of retirement.

474 The Journal of Finance

variable equal to the number of days from the end of a fiscal quarter until each earnings announcement:

days after end of quarter ( to earnings announcementJ

I fiscal quarter + ( quarterly earnings (3) a dummy variables i V announcement CAR/ i i