globalization. topics what is globalization? is it something new? historical perspectives what are...

TRANSCRIPT

Globalization

Topics

• What is globalization?

• Is it something new? Historical perspectives

• What are the causes?

• Do developing countries benefit from globalization?

• Role for Ukraine in the globalized world?

References• Bordo, M., Eichengreen, B., and Irwin, D., 1999, Is Globalization Today Really

Different than Globalization a Hundred Years Ago?, NBER Working Paper No. 7195• Edwards, S., 1999. How Effective are Capital Controls?, Journal of Economic

Perspectives Vol. 13 (Fall): 65–84.• Obstfeld, M. and Taylor, A. 2002, Globalization and Capital Markets, NBER Working

Paper No.8846.• Edwards, S,

“Capital controls sudden stops and current account reversals,” 2005, NBER Working Paper No. 11170

• Kose, Prasad, Rogoff, and Wei, (2006), Financial Globalization: a reappraisal, NBER Working paper No. 12484

• Stultz, R, (2006), Financial Globalization, Corporate Governance, and Eastern Europe, NBER Working Paper No. 11912

• Martin and Rei (2006), Globalization and Emerging Markets: With or without crash?, American Economic Review, Vol. 96, No.5

• Schmukler,S. and Zoido-Lobaton, P.,2001, Financial Globalization: Opportunities and Challenges for Developing Countries, The World Bank, mimeo.

• Frankel, J., 1992, Measuring International Capital Mobility: A Review, American Economic Review Vol. 82(2): 197-202

• Thomas Friedman, “The World is Flat”

What is globalization?

• Growth in international trade in goods and services

• Increasing role of multinational corporations (MNC), surge of foreign direct investment (FDI)

• Higher integration of the financial markets

• Increase in labor mobility, outsourcing of jobs and migration

The world is flat

• T. Friedman, NY Times columnist, the author of “The World is Flat”– competitive playing fields between industrial

and emerging market countries are leveling– creates opportunities for labor force in

emerging economies to join global markets– examples: Shanghai, China; Bangalore, India

Historical Perspective: 1870 - 1914

• Gold standard as a dominant monetary system (fixed-exchange rate regimes)

• Global capital market centered in London

• Increasing globalized capital market, with surging capital flows

Historical Perspective: 1914 - 1945

• Destruction of global economy with increasing non-cooperative economic policy-making

• Broken credibility on the gold standard and adoption of floating rates

• Monetary policy became subject to domestic goals to help finance wartime deficits

• Capital controls to protect gold and avoid currency crises

• Capital flows were minimal • International prices and interest rates were out

of synchronization

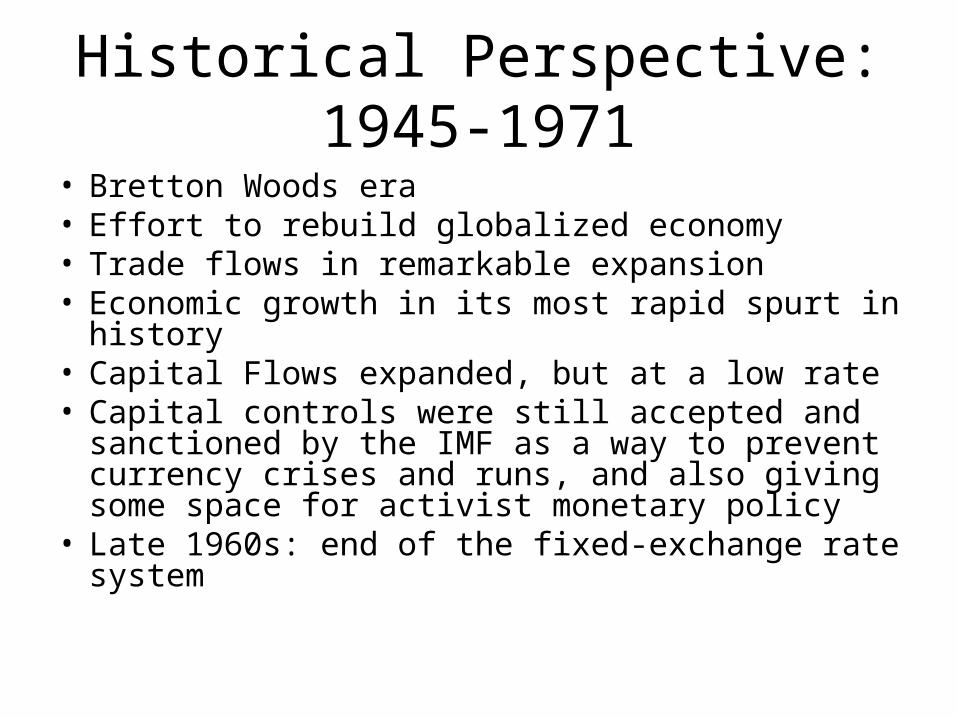

Historical Perspective: 1945-1971

• Bretton Woods era• Effort to rebuild globalized economy• Trade flows in remarkable expansion• Economic growth in its most rapid spurt in history• Capital Flows expanded, but at a low rate• Capital controls were still accepted and

sanctioned by the IMF as a way to prevent currency crises and runs, and also giving some space for activist monetary policy

• Late 1960s: end of the fixed-exchange rate system

Historical Perspective: Post 1971

• Post-Bretton Woods floating era• Still some fixed-exchange rate regimes• Increasing capital mobility • Decreasing capital controls• In peripheral countries: economic reforms

reduced transaction costs and risks of foreign investments

• Small developing countries tended to adopt fixed exchange rates (dollarization and currency boards) while larger ones tended to adopt floating exchange rates with inflation targeting

U-Shape Curve – Stylized Fact

Comparison of integration today and pre 1914 for trade and finance in the US

Bordo et al (1999):“…trade today is strikingly more important than a century ago. Three indicators sustain this view:

• a higher share of trade in tradeables production• the growth of trade in services • the rise of production and trade by multinational

firms.”

Trade in good and services

• Trade is now much larger as a share of tradeable goods production.

• The value of U.S. service exports (excluded from the merchandise trade figures considered above) now amount to about 40 percent of the value of merchandise exports.

The Role of Multinational Trade and Production

• Multinational enterprises existed in the late nineteenth century, but they were exceptional (i.e. East India Company, Standard Oil of New Jersey, Singer Sewing Machine)

• The value of direct investments has soared since the early-1980s and is now a quantum leap above a century ago

Measures of Financial Integration

• Feldstein-Horioka condition

• Real Interest Rate Parity

• Uncovered Interest Rate Parity

• Covered Interest Rate Parity

• Gross Stock of Foreign Capital

• Equity and Bond Prices

Real Interest Parity since 1870 Long-Term Real Interest Differentials

Source: Obstfeld and Taylor (2002)

Real Interest Parity since 1870

• Differentials have varied widely over time

• But have stayed relatively close to a zero mean – The series appear to be to have been

stationary over the very long run, and even in shorter sub-periods.

• Krugman, Paul (1995), “Growing World Trade: Causes and Consequences,” Brookings Papers on Economic Activity 1, pp.327-362:

• “…the general picture of world integration that did not exceed early twentieth century levels until sometime well into the 1970s is thus broadly confirmed. In the last decade or so, the share of trade in world output has finally reached a level that is noticeably above its former peak.”

What are the causes

• lower transportation costs

• lower trade barriers

• development of new telecommunication technologies

Transportation costs

• increasing role of air transportation

• improvements in traditional transportation– better technology, MNC in transportation

(UPS, FedEx)– more developed infrastructure (roads, ports

etc)

Lower trade barriers

Role of Information• First wave of globalization coincided with the invention of the

telephone and radio– transatlantic cable was laid in the 1860s, coming into operation in 1866– Prior to its opening, it could take as long as three weeks for information

to travel from New York to London– With the inauguration of the cable, this delay dropped to one day

• Garbade and Silber (1978) compare the London and New York prices of US bonds four months before and four months after the cable and find a significant decline in the mean absolute difference.

• Information asymmetries can explain the disproportionate importance of family groups in the pre-globalization period (the foreign branches of the Rothschild and Morgan families, for example)

Factors Behind Globalization – Potential Benefits

• Development of the financial sector– More and new type of capital is available

• Deeper and more sophisticated markets• Increased market discipline

– Better financial infrastructure• Insurance• Smoothing of socks• More transparent, competitive, and efficient

financial system – capital seeks its highest rewards

Factors Behind Globalization – Potential Costs

• Inconsistency of some policy goals and the free flow of capital across international boundaries

• Risk of financial and balance of payments crises– More market discipline– Imperfections in international markets

• Contagion– Higher exposure to foreign shocks– Fundamental Contagion: real or financial– Non-fundamental contagion: herding behavior

Costs of Financial Liberalization

Gcrises is the annual growth rate of real GDP at the crises year. G(N) is the annual growth rate of real GDP N years before/after the crises.

Source: Bordo, Eichengreen, and Irwin (1999)

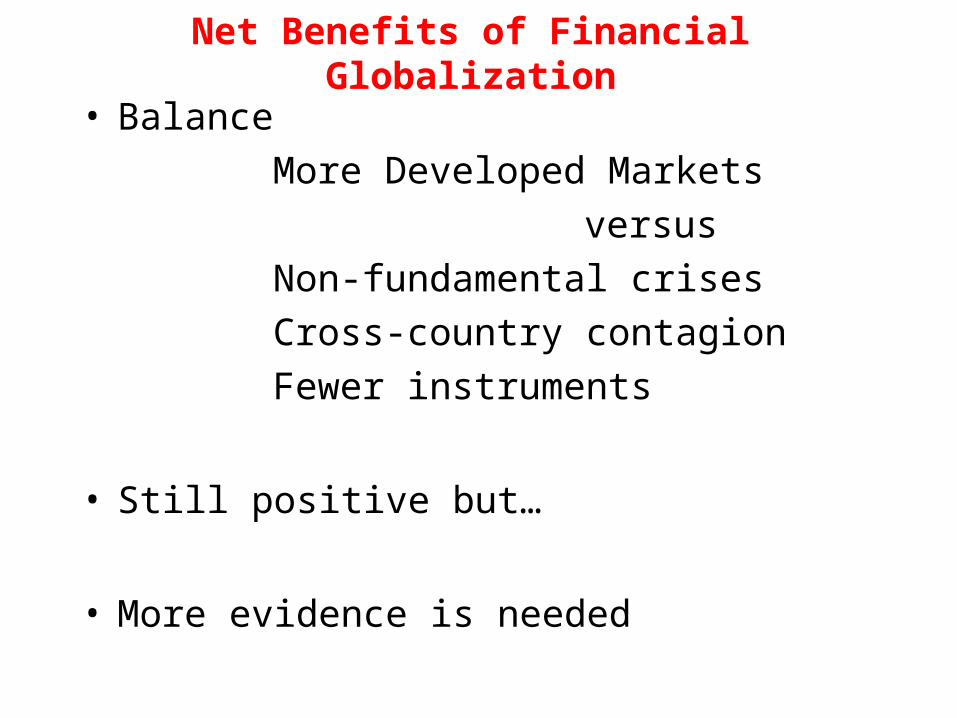

Net Benefits of Financial Globalization

• Balance

More Developed Markets

versus

Non-fundamental crises

Cross-country contagion

Fewer instruments

• Still positive but…

• More evidence is needed

Policy Options

What explains the long stretch of high capital mobility that prevailed before 1914, the

subsequent breakdown in the interwar period, and the very slow postwar reconstruction of the world

financial system ?

The Choice of an Exchange Rate Regime

The Choice of an Exchange Rate Regime

• The Macroeconomic Policy Trilemma for Open Economies - “Inconsistency Trinity”A country cannot simultaneously determine:– Exchange rate– Interest rate– Monetary policy oriented towards domestic

objectives

• In a world with full freedom of cross-border capital movements:– fixed exchange rates and independent domestic-

oriented monetary policy are incompatible choices

The Impossible Trinity

Source: Frankel (1999)

The Trilemma and Major Phases of Capital Mobility

Does capital flow to poor countries?

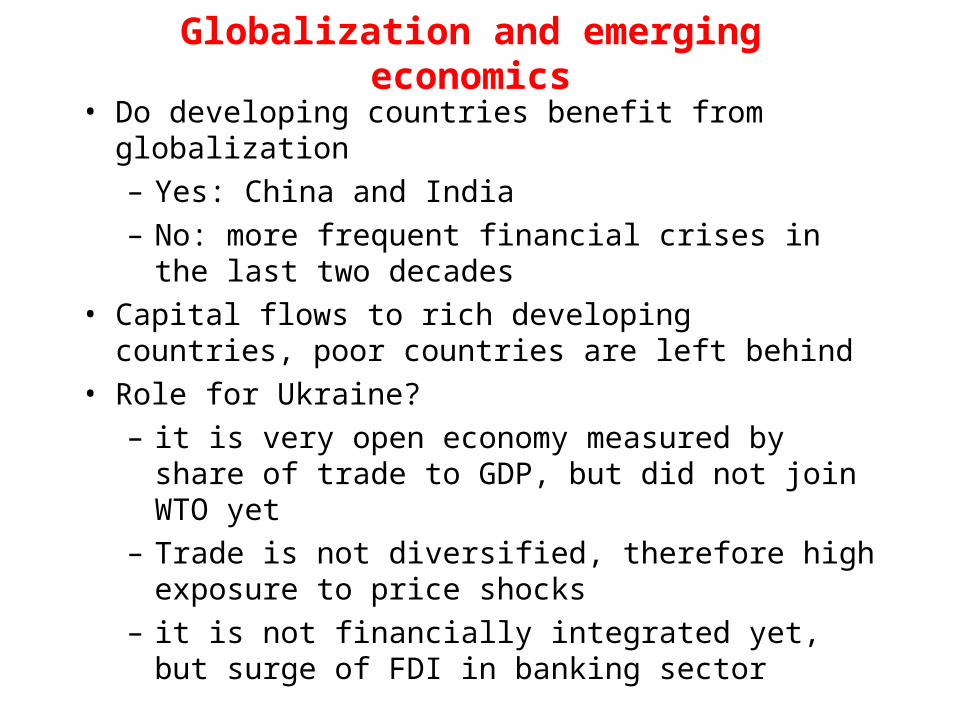

Globalization and emerging economics

• Do developing countries benefit from globalization

– Yes: China and India

– No: more frequent financial crises in the last two decades

• Capital flows to rich developing countries, poor countries are left behind

• Role for Ukraine?

– it is very open economy measured by share of trade to GDP, but did not join WTO yet

– Trade is not diversified, therefore high exposure to price shocks

– it is not financially integrated yet, but surge of FDI in banking sector