global oil market outlook - prism.pttgrp.com (7)_2.pdf · chapter 1: global economic growth key...

TRANSCRIPT

1

9th March 2018

Global Oil Market Outlook

2

Agenda

Oil Demand

Oil Supply

Conclusions

3

Agenda

Oil Demand

Oil Supply

Conclusions

4

Global economic growth

Technology & Environmental Policy

Chapter 2:

Chapter 3:

Chapter 1:

Refinery Overview

Oil Demand

Advanced Economies Developing Economies

3.9%

GDP Growth

2.0% +0.2 MMBDDemand Growth GDP Growth

4.9%

Global GDP Growth

+1.2 MMBD

Demand Growth

Sources: IEA, EIA, OPEC (Jul’17), IMF (Jan’18)

2018 GLOBAL ECONOMY DRIVEN BY DEVELOPING ECONOMIES

CHAPTER 1: GLOBAL ECONOMIC GROWTH

5

CHAPTER 1: GLOBAL ECONOMIC GROWTH

KEY PLAYERS TAKE UP HALF OF DEMAND

4 MAJORPLAYERS

U.S.

Europe

China

India

Developing Economies

Advanced Economies

47%% Share of 2018 Demand

6

53%

CHAPTER 1: GLOBAL ECONOMIC GROWTH

U.S. ECONOMY AND DEMAND GROWTH IN 2018

123210 223

1.5%

2.3%

2.7%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

200

400

600

800

1000

1200

2016 2017 2018Demand Growth GDP

Sources: IEA, EIA, OPEC (Jul’17), IMF (Jan’18)

GDP & Demand Growth

2008 2011 2014 2017

(KBD) (%YoY)2008 2011 2014 2017

2016-2017 (6 M)+1-2%

Miles traveled

Trump’s tax cut plan

35%

21%

Corporations

39.6%37%

Individual

TrumpProposal

Current

4.2% (16-year low in Sep’17)

Unemployment rate

fallen to FACTORS TO WATCH

Solid demand propelling robust economic recovery

7

The next FED chair?Jerome Powell

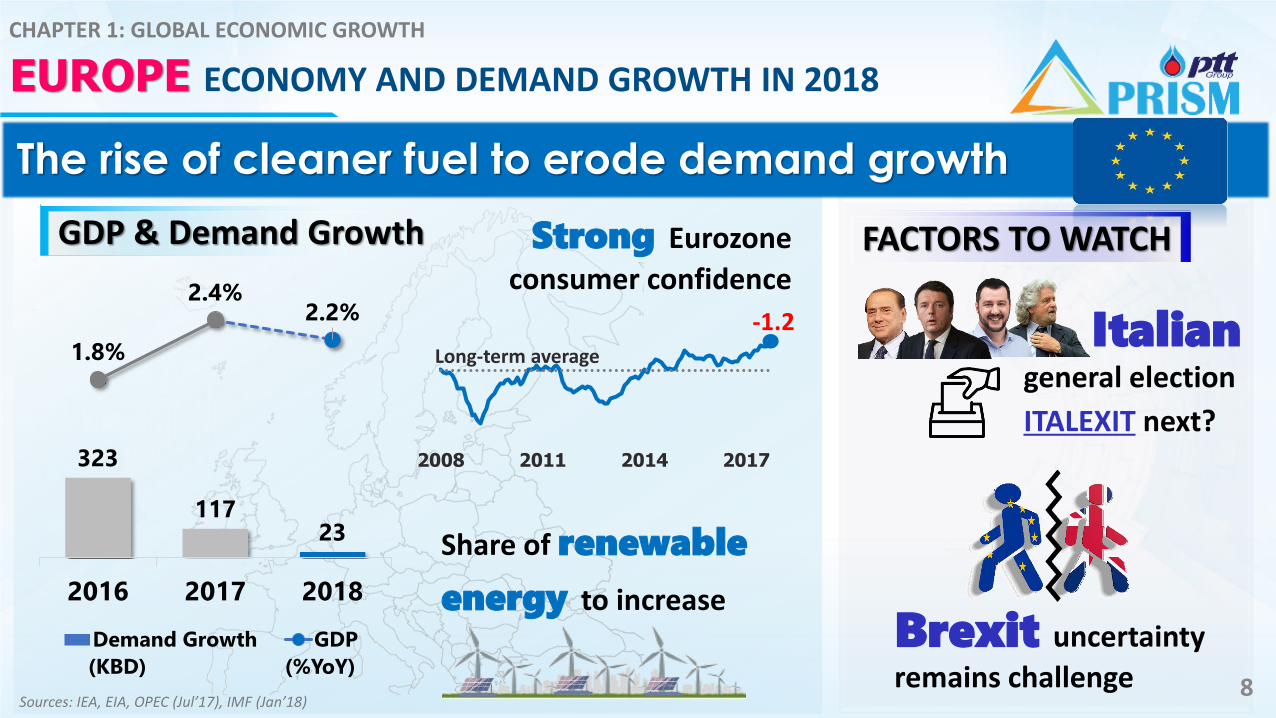

EUROPE ECONOMY AND DEMAND GROWTH IN 2018

Sources: IEA, EIA, OPEC (Jul’17), IMF (Jan’18)

(KBD) (%YoY)

323

11723

1.8%

2.4%2.2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

200

400

600

800

1000

1200

2016 2017 2018

Demand Growth GDP

2008 2011 2014 2017

-1.2Long-term average

Strong Eurozone

consumer confidence

Brexit uncertainty

remains challenge

general election

ITALEXIT next?

GDP & Demand Growth FACTORS TO WATCH

The rise of cleaner fuel to erode demand growth

Italian

Share of renewable

energy to increase

8

CHAPTER 1: GLOBAL ECONOMIC GROWTH

CHINA ECONOMY AND DEMAND GROWTH IN 2018

Sources: IEA, EIA, OPEC (Jul’17), IMF (Jan ’18)

(KBD) (%YoY)

463350 333

6.7% 6.9% 6.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

200

400

600

800

1000

1200

2016 2017 2018

Demand Growth GDP

Shift in China’s economy

from manufacturing to service

Car sales growth by 4-5% in 2017

mainly driven by

SUVsSource: CAAM (Oct’17)

China’s debt

Growth in

“BELT ROAD

INITIATIVE”

30%

40%

50%

60%

2006 2008 2010 2012 2014 2016

Service

Manufacturing

% of GDP

FACTORS TO WATCH

Economic transition towards the

GDP & Demand Growth

“New Normal”

China Globalization Policy

9

CHAPTER 1: GLOBAL ECONOMIC GROWTH

CHAPTER 1: GLOBAL ECONOMIC GROWTH

INDIA ECONOMY AND DEMAND GROWTH IN 2018

Sources: IEA, EIA, OPEC (Jul’17), IMF (Oct’17)

(KBD) (%YoY)

317173 227

7.1%6.7%

7.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

200

400

600

800

1000

1200

2016 2017 2018

Demand Growth GDPExpanding in

middle class

“Make In India”

Transforming India

into a manufacturing magnet

Robust car sales +7% YoY

2018

Strong government

spending, aiming toconstruct

40 km of highway roads per day

FACTORS TO WATCH

2017

Continuous economic growth to drive demand

GDP & Demand Growth

10

Europe : Better-than-

Expected Growth Continued, but Political Risks Persist

China : Slow Down

but Enters New Chapter of “Quality” Growth

India : The Fastest

Growing Country among Emerging Economies.

11

53%

1.5

2.32.7

2016A 2017E 2018F US : Strong Economic

Fundamentals will be Key Growth Drivers in 2018

1.8

2.42.2

2016A 2017A 2018F

7.1

6.7

7.4

2016A 2017E 2018F

6.7 6.96.6

2016A 2017E 2018F3.9%

Global GDP Growth

STRONG ECONOMIC GROWTH GLOBALLY!

CHAPTER 1: GLOBAL ECONOMIC GROWTH

CHAPTER 2: TECHNOLOGY & ENVIRONMENTAL

DISRUPTIVE TECHNOLOGY TO RESHAPE OIL MARKET

Internal Combustion Engines (ICE)

Battery-Powered Cars

2016 Car Fleet

2 Million 0.2 %

% Market Share2016 Car Fleet

1,000 Million 99.8 %

% Market Share

Sources: IEA (Jun’17) and Bloomberg (Jul’17)12

IMPLICATIONS OF THE PARIS AGREEMENT

CHAPTER 3: ENVIRONMENTAL POLICY

Risks over bailing on the Paris climate deal as

No defined “Punishment“ for breaking it

No clear “Detail” on how these countries should do

“WELL BELOW 2⁰C”

195 Nations Agreed to Fight CO2

Keep Global Temperature Increase

By 2100

13

CHAPTER 3: REFINERY OVERVIEW

14Sources: FGE Energy Semi Annual Reports, Fall 2017, Reuters (Feb’18) , IEA Medium Term Outlook (Mar’17)

Asia Pacific and Middle East Refinery Addition

454562

5

474 565

1207

-1000

0

1000

2000

2015 2016 2017 2018 2019 2020

KBD

AP & ME Demand Growth Middle East China

Other AP Japan India

Vietnam Teapot Net Addition

Demand surge + refinery cancellations/deferrals/closures tighten balance.

Global refinery capacity additions UNDER OIL DEMAND

GDP 3.9 %driven by developing economies

Small impactdue to little EVs adoption and uncertainty in policy

OutpaceGlobal oil demand outstrip refinery addition

CONCLUSION: GLOBAL OIL DEMAND

CONCLUSION : OIL DEMAND GROWTH

15

16

Agenda

Oil Demand

Oil Supply

Conclusions

17

“OPEC POWERFULIN THE PAST”

18

OPEC POWER IN THE PAST

85.488.4 89.0 90.6 91.9 93.2 95.0

0

10

20

30

40

50

60

70

80

90

100

2009 2010 2011 2012 2013 2014 2015

Other OPEC Saudi Other non-OPEC Russia U.S. Global Demand

Note: OPEC: Organization of Petroleum Exporting CountrySources: IEA

GLOBAL OIL SUPPLY = OPEC + NON-OPEC

Non-OPEC supply

60%

OPEC supply

40%

GLOBAL OIL SUPPLY AND DEMAND

World’s Major Exporters!

Saudi Arabia

U.S.

Russia

MMBD

19

WHY OPEC IS IMPORTANT?

0

20

40

60

80

100

120

140

160

1990 1993 1996 1999 2002 2005 2008 2011 2014

USD/bbl

1990 : 1st gulf war

2003 : 2nd gulf war

2008 : “Financial Crisis”

OPEC Cut 2 MMBD

1997 : “Asian Crisis”

OPEC Cut 1.2 MMBD2014 : Price War

“EVERY OPEC’S ACTION MOVES OIL PRICE”

20

2

3

4

5

6

7

8

9

10

11

12

2014 2015 2016

MMBD

Saudi’s flooding strategy

S h o c k !Iran sanction was lifted

and unlock 0.8-1.0 MMBD to market

Iraq kept increasing production

KEY OPEC CRUDE OIL PRODUCTION

PRICE WAR STARTED!

21

PRICE WAR LED BLEEDING

50

52

54

56

58

60

26

28

30

32

34

36

2012 2013 2014 2015 2016

MMBD MMBD

Sources: IEA, IMF

“Long period of low oil price hurts oil producing countries”

-30-25-20-15-10

-50

Ira

n

Qa

tar

Nig

eri

a

An

go

la

UA

E

Sa

ud

i A

rab

.

Ku

wa

it

Alg

eri

a

Om

an

Ve

ne

zu

ela

% o

f G

DP

MAJOR OIL EXPORTER BUDGET DEFICIT

-15%

USD/bbl

10

50

90

130

2014 2015 2016

Painful

CRUDE OIL PRICES OPEC & NON-OPEC PRODUCTION

Non-OPEC (RHS)

OPEC (LHS)

22

OUTCOME OF PRICE WAR CREATES “OIL GLUT”

O I L G L U T2,200

2,500

2,800

3,100

3,400

1999 2002 2005 2008 2011 2014

200

300

400

500

600

1999 2002 2005 2008 2011 2014

MMB

MMB

Note: US Commercial Crude oil stock Sources: EIA, Reuters, Bloomberg

U.S. CRUDE OIL INVENTORY

OECD LIQUID FUELS INVENTORY

350

485

2,500

3,000

23

RUSSIA BECAME THE LARGEST OIL PRODUCER

in October 2016High record at 11.2 MMBD

RUSSIA OIL OUTPUT (MMBD) NEW PROJECTS START UP PIPELINE

“RUSSIA was Non-OPEC leader to join

in joint production curb and called on other oil exporters to do the same.”

24

OPEC/RUSSIA AIMED TO CUT AND PUSHED PRICE HIGHER

0

20

40

60

80

100

120

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Nov. 2014: OPEC UNCUT

Nov. 2016: OPEC CUT

Oil price (USD/BBL)

2015-2016: Oil Oversupply

2008: Shale Oil Developed

2014: Shale Boom

Jan-18

Price Recovery

TIME TO STOP

BLEEDING !

25

OPEC & NON-OPEC COMMITS TO “CUT THE GLUT”

Source: OPEC Monthly Report, Oct. 2017

2,500

2,600

2,700

2,800

2,900

3,000

3,100

3,200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5yr-range 2017 2017F (Nov'17) 5-yr Average

OECD Oil Inventories MMB

Target Level

26

HIGH COMPLIANCE FROM PRODUCERS

Sources: OPEC (Jan’18) and IEA (Jan’18)

0

20

40

60

80

100

120

140

160

Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17

OPEC Cut Non-OPEC Cut

%

Compliance Rates of Output Cut

27

OPEC WILDCARDS FROM LIBYA, NIGERIA & VENEZUELA

Libya and Nigeria Output Changes*MMBD

Venezuela Production forecast

Govt. Unrest

Kurdish Independent

28

“NEW ERA OF U.S. POWER”

29

POWER OF U.S. SHALE AND ITS OWN DESTINY

1970 1977 1985 1993 2001 2009 2014

1970s : Witnessed advances in horizontal drilling technologies

1980 : Govt. sponsored research to make hydraulic

fracturing economic

1980s-1990sCommercial success of Shale gas production in Texas

Mid-2000sApplying to oil deposits in Bakken shale

Crude oil price*USD/bbl

2014 : Shale Boom!

*Nominal Oil Price

30

SHALE IS PRODUCED DIFFERENTLY FROM OLD WAY

SHALE OIL WAY:TIRAMISU

OLD WAY: JELLY DONUT

Sources: James Scherrer

VERTICAL DRILLING HORIZONTAL DRILLING

31

NEW TECHNOLOGY INCREASING PRODUCTIVITY

IranMORE LAYERS

Source: EIA

LONGER

0

400

800

1,200

2010 2012 2014 2016

Barrel Per Day

Permian Bakken Eagle Ford Niobrara

OIL PRODUCTION PER RIG IN NEW WELLS

Higher Productivity (2010-2016)

3-4 Times

32

OPEC LOST MARKET SHARES AFTER SHALE BOOM

21%40% 35%

19%

27%15%

60%33% 50%

1973 2011 2015

Others OPEC U.S. Crude

0

2

4

6

8

10

12

1965 1975 1985 1995 2005 2015

MMBD

Sources: EIA

U.S. CRUDE OIL PRODUCTION

U.S. CRUDE SUPPLY BY SOURCE

SHALE BOOM

33

OPEC & US SHALE – TUG OF WAR

0

20

40

60

80

100

120

140

160

1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013 2016

USD/bbl Oversupply (Shale Oil)

“PRICE WAR”

1985 Oversupply (North Sea)

“PRICE WAR”

34

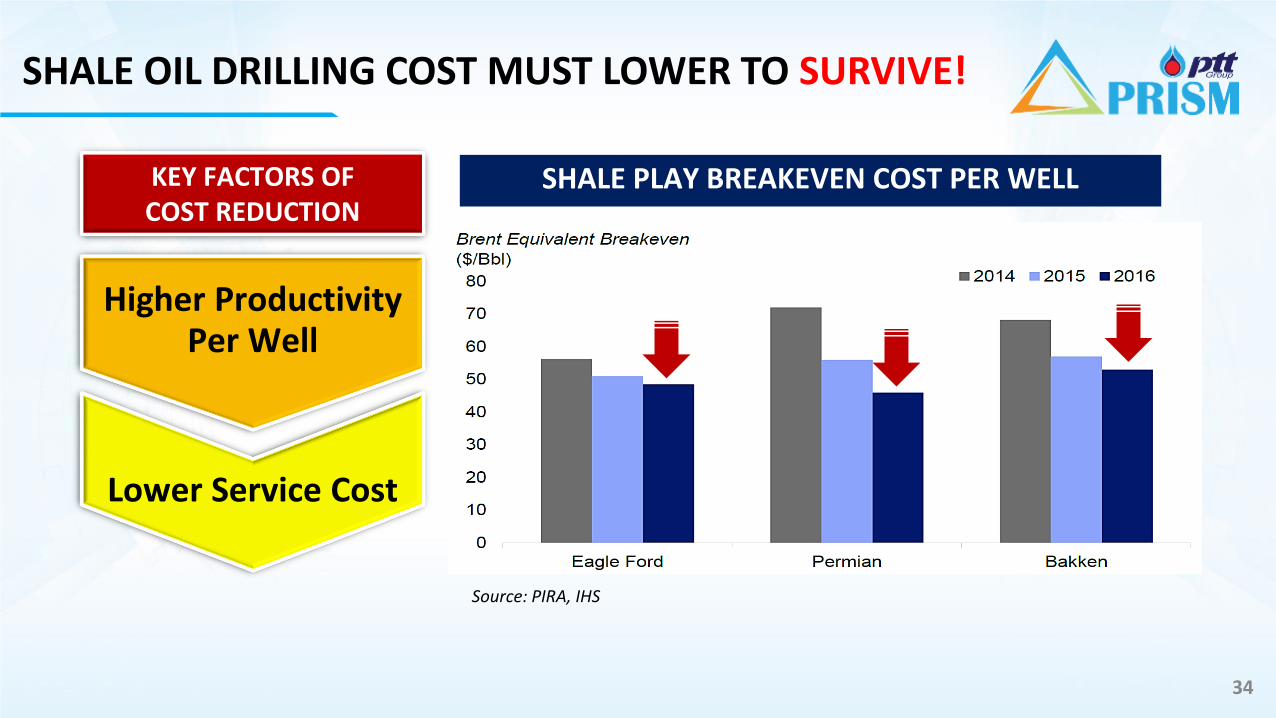

SHALE OIL DRILLING COST MUST LOWER TO SURVIVE!

Source: PIRA, IHS

SHALE PLAY BREAKEVEN COST PER WELLKEY FACTORS OFCOST REDUCTION

Higher Productivity Per Well

Lower Service Cost

35

U.S. SHALE OIL QUICKLY RESPONDS TO THE CUT

0

20

40

60

80

100

120

140

4

5

6

7

8

9

10

11

12

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

US Crude Oil Production (LHS) WTI (RHS)

MMBD USD/BBLUS oil production

Source: EIA (Aug. 2017)

“Pump up faster when oil price’s UP”

36

SUPPLY CONCLUSION

• Respond very quickly to increased oil prices

• At oil price $55/bbl, up to 70% of shale producers can survive

OPEC

NON-OPEC

U.S.

Outlooks

• Become a major spring producer• SOON become the largest oil producers in the

world!

• Lost power of swing producer • Suffered by price war due to countries’

budget deficit • Production cut mainly from disruptions in

Venezuela, Nigeria, and Libya

Recent• Disruptions still carry on, especially in Venezuela,

while others likely to increase• Saudi Arabia is diversifying roles to play more in

refinery business

• Russia became Non-OPEC leader for joint production cut with OPEC

• New projects are queuing to the market

• If without joint production cut, oil output will glut

37

Agenda

Oil Demand

Oil Supply

Conclusions

GLOBAL OIL MARKET

38

CHAPTER 1 : THE PRESENT MARKET & OUTLOOK

CHAPTER 2 : LOOKING FORWARD

GLOBAL OIL MARKET

39

CHAPTER 1 : THE PRESENT MARKET & OUTLOOK

CHAPTER 2 : LOOKING FORWARD

OIL STILL DOMINATES IN ENERGY SECTOR

40

Demand in 2018

• Global economic growth : 3.9%

• Global oil demand growth : 1.4-1.6 MMBD

Alternative Energy

• Keep growing with minor effect in 2018

CHAPTER 1 : THE PRESENT MARKET

41

36%

44%

18%

2%

Petroleum Products Natural Gas

Coal and Lignite Hydro & Imported Elec.

2.05 MMBoED

Thailand Primary Energy Consumption by Type of Energy in 2014

World Primary Energy Consumption by Type of Energy in 2014

31%

29%

21%

10%

5%2% 1%

Oil

Coal

Gas

Bioenergy

Nuclear

Hydro

Other Renewable

273.6MMBoED

FOSSIL FUEL CONTRIBUTE 80% OF WORLD ENERGYCHAPTER 1 : THE PRESENT MARKET

BATTLE OF INFLUENCER : OPEC, RUSSIA AND U.S. SHALE OIL

0

40

80

120US Output Revolution

UNIT : USD/BBL

OPECNo-Ceiling &

Increase Production

< 50

< 30

OIL PRICE WAR

OPEC & Non-OPECOutput Cut Deal

1.8 MMBD until June 17

Output CutExtensionto March 18

> 50

OUTPUT CUT DEAL

Second extensionto end of 2018

3

CHAPTER 1 : THE PRESENT MARKET

OIL SUPPLY GROWTH

+1.1-1.4

Come back to make profit at high prices

Grow from the legacy projects with lower cost

Maintain production cuts through 2018

+0.6

OPECNON-OPECU.S.

0.0

OIL SUPPLY GROWTH

1.7-2.0 MMBD

2018

43

CHAPTER 1 : THE PRESENT MARKET

PRISM PRICE OUTLOOK : DUBAI PROJECTION

44

20

25

30

35

40

45

50

55

60

65

70

Dubai Price : USD/BBL

20162017

2018

65 $

60 $

CHAPTER 1 : THE PRESENT MARKET

45

CHAPTER 1 : THE PRESENT MARKET

STIRRING UP GLOBAL POLICY…

EXAMPLE RISKS ON A SUPPLY DISRUPTION

46

CHAPTER 1 : THE PRESENT MARKET

Unplanned Outage:North Sea’s Forties Pipeline System (FPS)

leakage

Natural DisasterHurricane Harvey hit U.S. Gulf of Mexico, the critical region for both crude production and

refinery. Armed-Force Attacks: Libya’s oil terminals and fields shutdown

PRISM PRICE OUTLOOK : DUBAI PROJECTION

47

20

25

30

35

40

45

50

55

60

65

70

Dubai Price : USD/BBL

2018

20162017

65 $

60 $

CHAPTER 1 : THE PRESENT MARKET

2018 FACTORS TO WATCH

• Geopolitical Tensions • Compliance Concerns

• Global Policy • Financial Tightening

• Shale Oil Production • Technology and

Competitiveness

GLOBAL OIL MARKET

48

CHAPTER 1 : THE PRESENT MARKET & OUTLOOK

CHAPTER 2 : LOOKING FORWARD

49

THE OIL KILLER? - ELECTRIC VEHICLES

New Player From Other SectorAccelerator

Market Owner

“The sound is a very crucially important characteristic of a Ferrari”

Conservationist

Sources: Company’s logo

CHAPTER 2 : LOOKING FORWARD

Ferrari will make a battery-powered supercar to challenge Tesla Inc. at the high end of the electric-auto market, Chief Executive Officer Sergio Marchionne said.

WHY EVs MATTER?

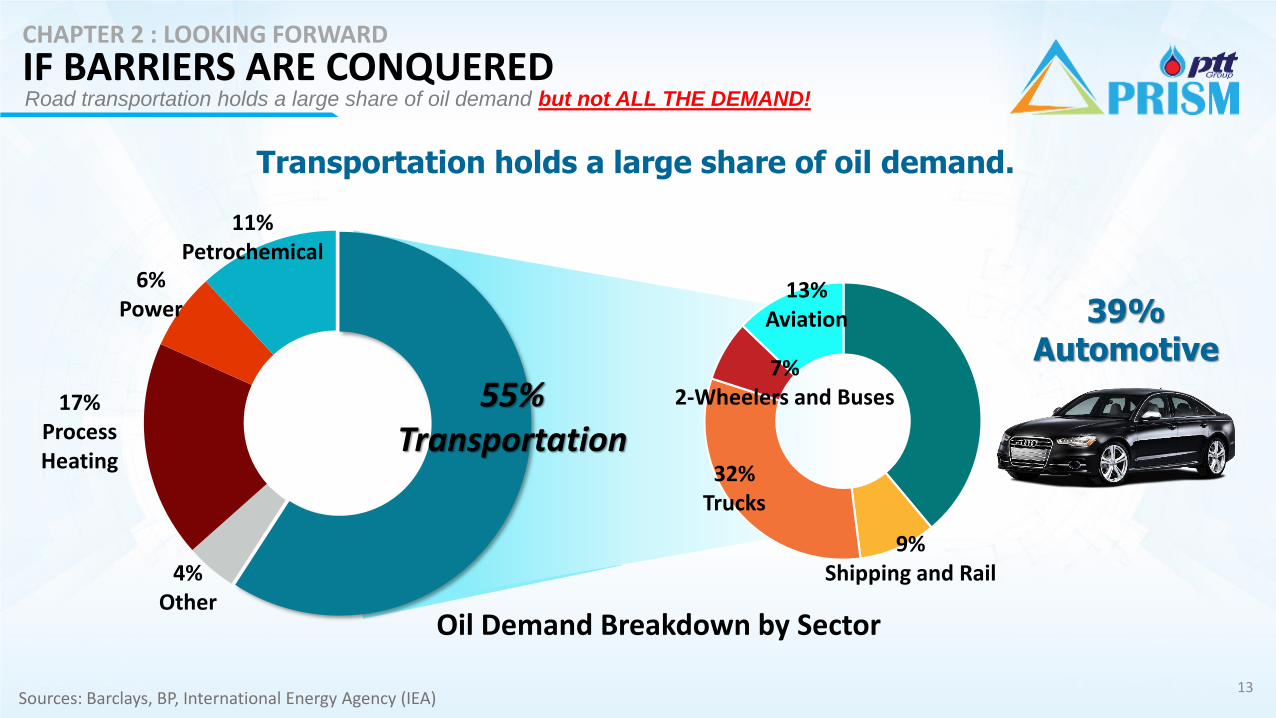

11

Oil Demand Breakdown by Sector

4%Other

17% Process Heating

6%Power

11%Petrochemical

55%Transportation

Transportation holds a large share of oil demand.

39%Automotive

9%Shipping and Rail

32%Trucks

7% 2-Wheelers and Buses

13%Aviation

Sources: Barclays, BP, International Energy Agency (IEA)

Road transportation holds a large share of oil demand

CHAPTER 2 : LOOKING FORWARD

51

Purchase Price

25%

Charging Availability

13%

Note: the rest of 20% are maintenance costs, reliability, and etc.

MANY BARRIERS…

Source: McKinsey & Company (Jan’17)

Brand Availability

18%Driving Range

24%

However, two major challenges await!

Purchase Price

25%

Charging Availability

13%

HAVE BEEN OVERCOMECHAPTER 2 : LOOKING FORWARD

IF BARRIERS ARE CONQUERED

13

Oil Demand Breakdown by Sector

4%Other

17% Process Heating

6%Power

11%Petrochemical

55%Transportation

Transportation holds a large share of oil demand.

39%Automotive

9%Shipping and Rail

32%Trucks

7% 2-Wheelers and Buses

13%Aviation

Sources: Barclays, BP, International Energy Agency (IEA)

Road transportation holds a large share of oil demand but not ALL THE DEMAND!

CHAPTER 2 : LOOKING FORWARD

53

CONCLUSION

This year, crude fundamental is considering less tight than 2017 as surging shale

production will cap an extreme price hike.

For the upside, the “Declare of Corporation” between OPEC & Non-OPEC (Russia)

producers and robust demand resulting from improved global economies will prevent a

price collapse as experienced earlier.

In addition, unexpected “Supply Disruption” from geopolitical risks and emergency

shutdown of producing fields/ refineries remain an upside risk to our price forecast.

While short term bearish impact can be attributed to the increasing production of U.S.

shale oil, in medium to long term, Electric Vehicles penetration will be a factor to watch

for future oil demand disruption.

Q&A