global construction markets trends & prospects · pdf filefirst for global construction...

TRANSCRIPT

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

GLOBAL CONSTRUCTION MARKETS –

TRENDS & PROSPECTS

Chris Sleight,

Editor

International Construction

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

CONTENTS

• Global economic picture

• Global construction outlook

• Global industry ‘health’

• Europe in depth

• Summary

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

ECONOMIC FORECASTS – WHY BOTHER?

• The numbers are never right!

• Hard to interpret

• Can’t take account of unexpected events

– Lehman Bros., European debt crisis, Arab Spring

• Can be politicised/biased

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

BUT...

• Do we expect too much from forecasters?

– No-one predicted the Lehman collapse etc.

– Some things you just can’t forecast for

• The trend is often right, even if the details are inaccurate

• What are the alternatives?

– Poor forecasts are better than no forecasts

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

HOW TO USE FORECASTS

• Pick sources that are reputable & have a good track record

• Work out what is relevant to you

• Don’t rely on just one source

• Plan for different outcomes

• Form your own opinion

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

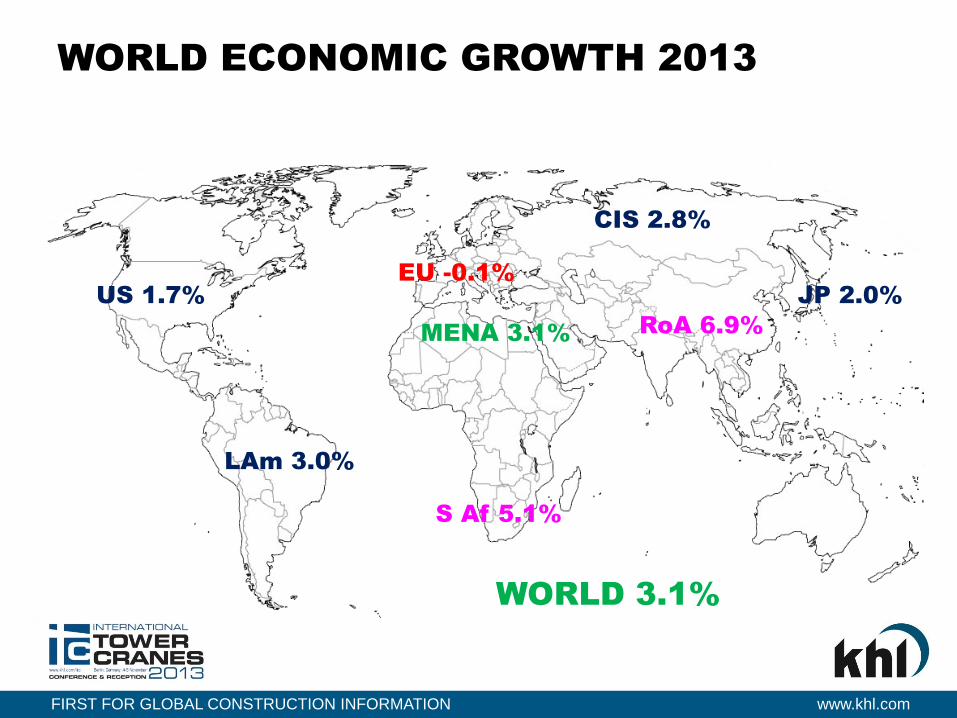

WORLD ECONOMIC GROWTH 2013

EU -0.1%

US 1.7%

LAm 3.0%

MENA 3.1%

S Af 5.1%

CIS 2.8%

JP 2.0%

RoA 6.9%

WORLD 3.1%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

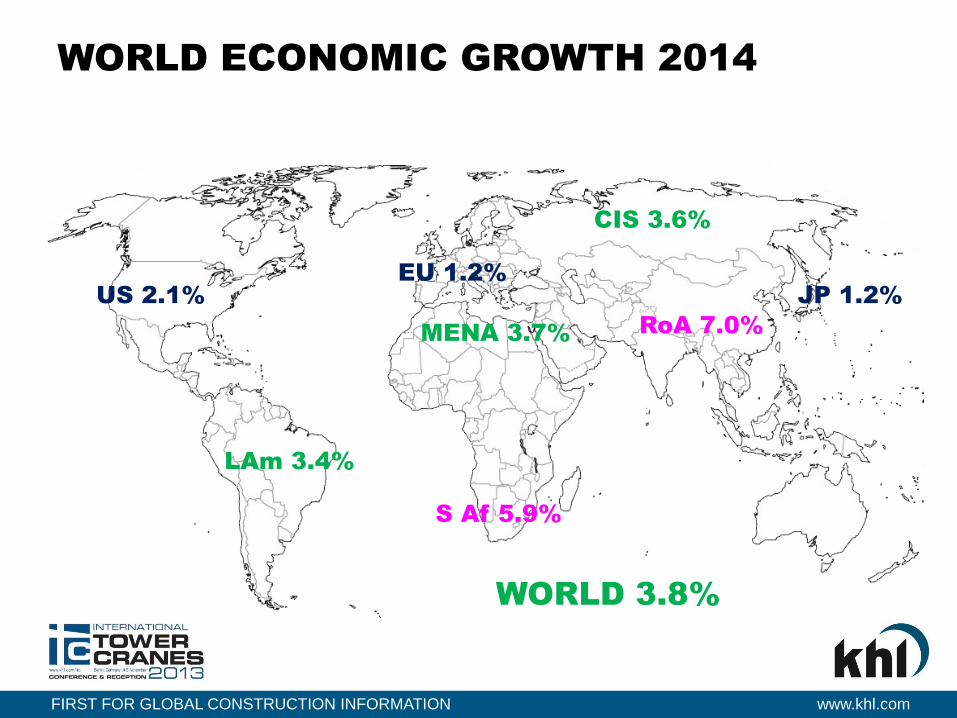

WORLD ECONOMIC GROWTH 2014

EU 1.2%

US 2.1%

LAm 3.4%

MENA 3.7%

S Af 5.9%

CIS 3.6%

JP 1.2%

RoA 7.0%

WORLD 3.8%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

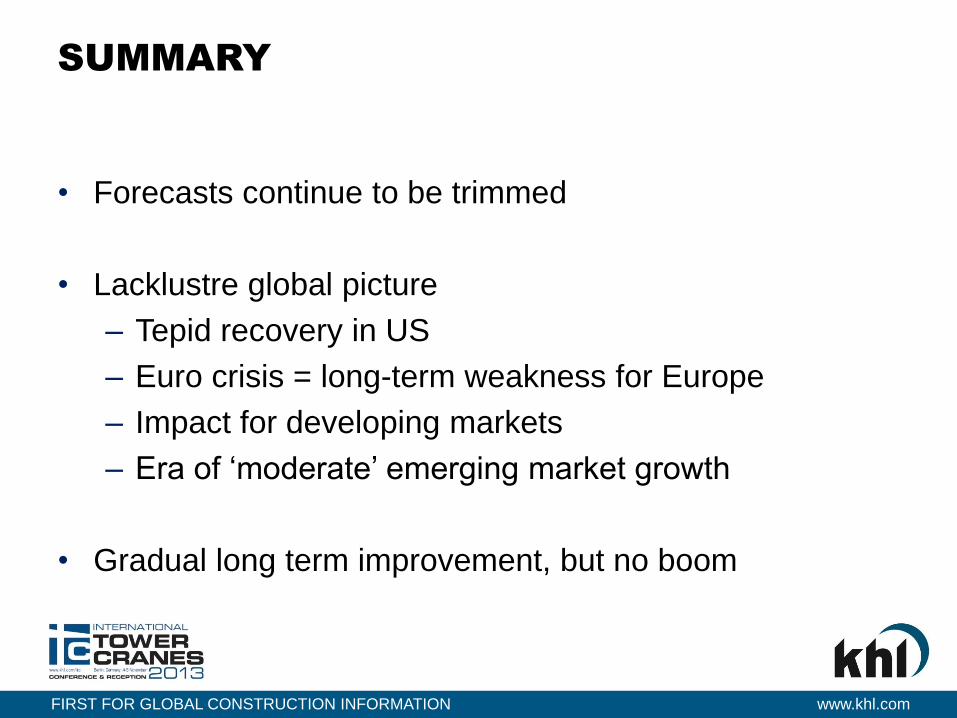

SUMMARY

• Forecasts continue to be trimmed

• Lacklustre global picture

– Tepid recovery in US

– Euro crisis = long-term weakness for Europe

– Impact for developing markets

– Era of ‘moderate’ emerging market growth

• Gradual long term improvement, but no boom

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

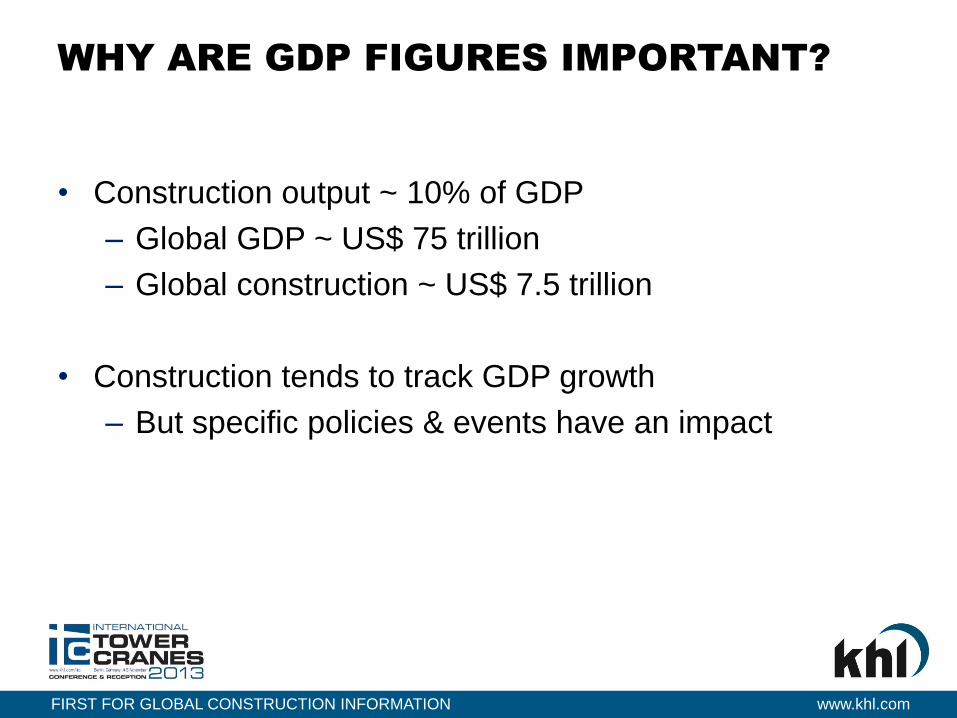

WHY ARE GDP FIGURES IMPORTANT?

• Construction output ~ 10% of GDP

– Global GDP ~ US$ 75 trillion

– Global construction ~ US$ 7.5 trillion

• Construction tends to track GDP growth

– But specific policies & events have an impact

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

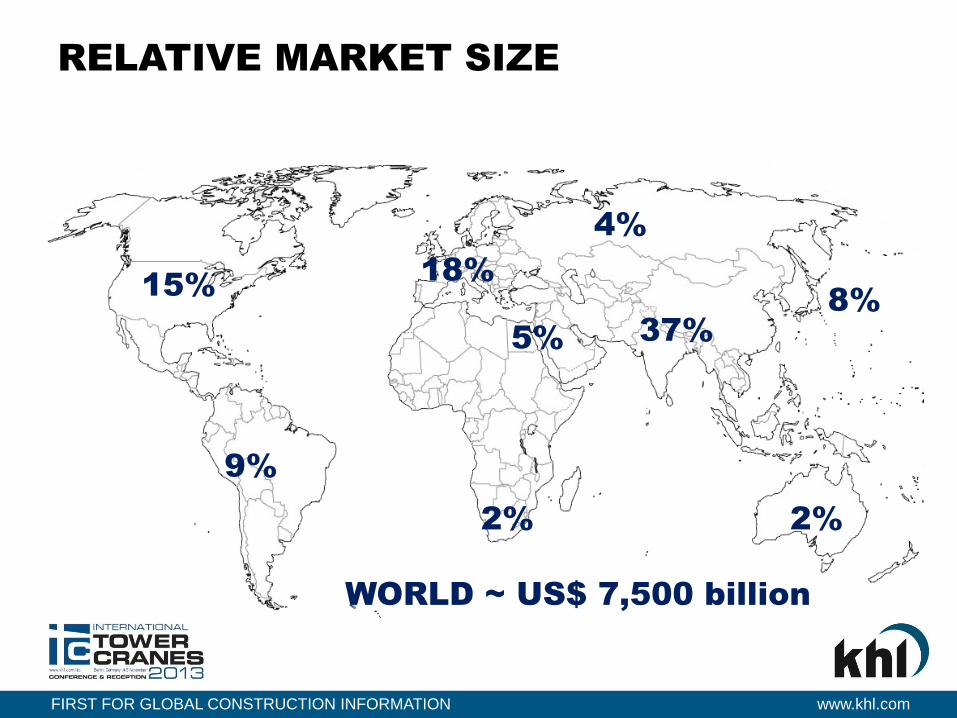

RELATIVE MARKET SIZE

18% 15%

9%

5%

2%

4%

8%

37%

WORLD ~ US$ 7,500 billion

2%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

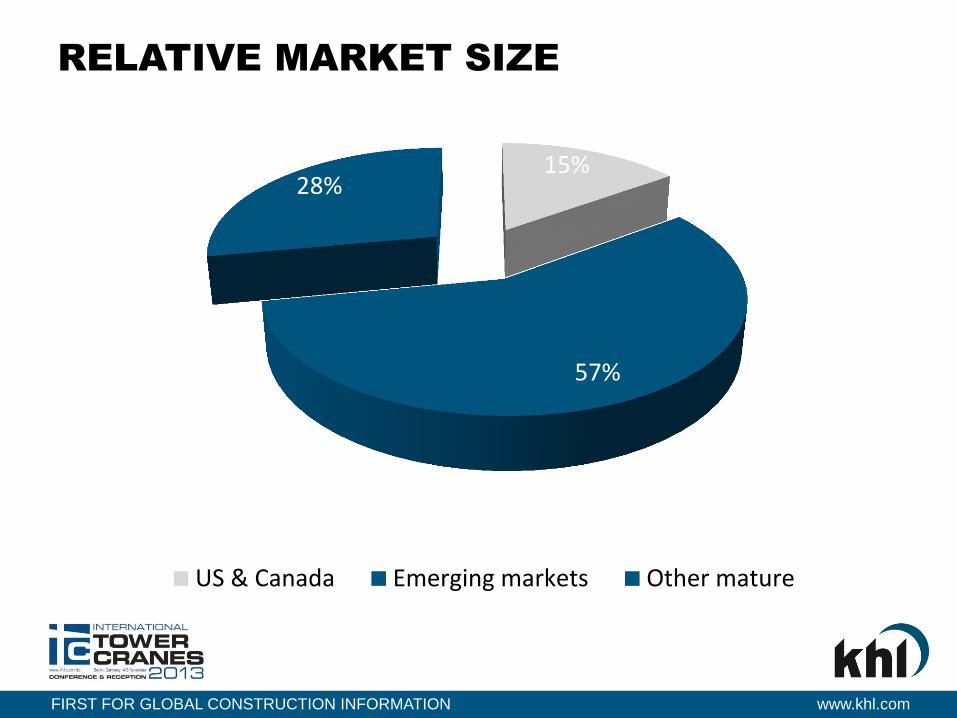

RELATIVE MARKET SIZE

15%

57%

28%

US & Canada Emerging markets Other mature

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

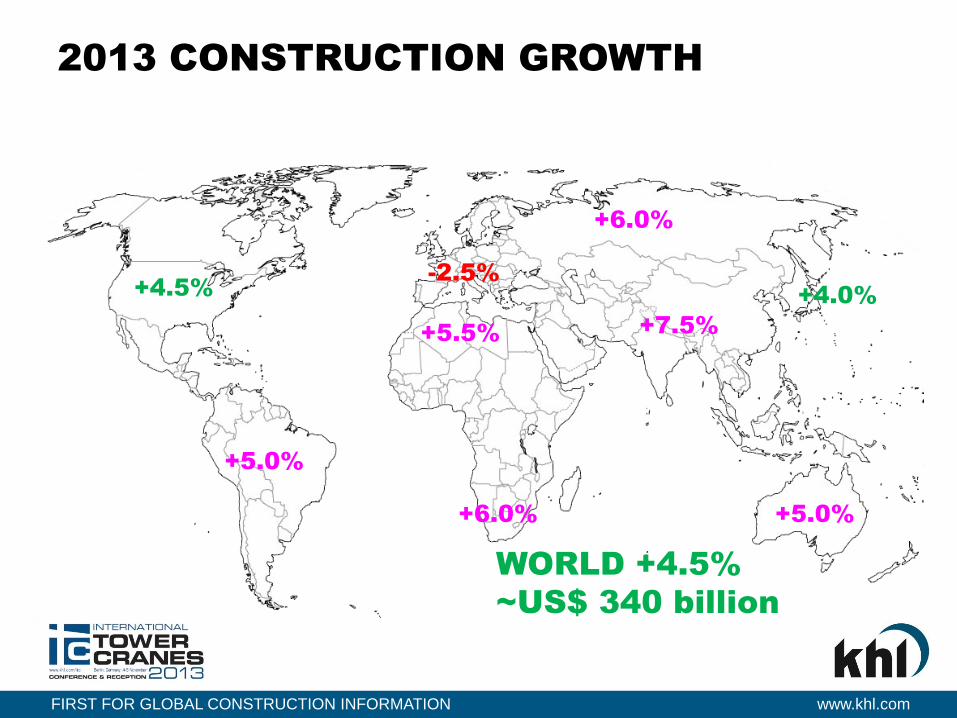

2013 CONSTRUCTION GROWTH

-2.5% +4.5%

+5.0%

+5.5%

+6.0%

+6.0%

+4.0%

+7.5%

WORLD +4.5%

~US$ 340 billion

+5.0%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

ECONOMIC SUMMARY

• Construction growing faster than GDP

• Recovery not a boom

• Infrastructure particularly strong

• Greatest growth in emerging markets

– Average +6.8%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

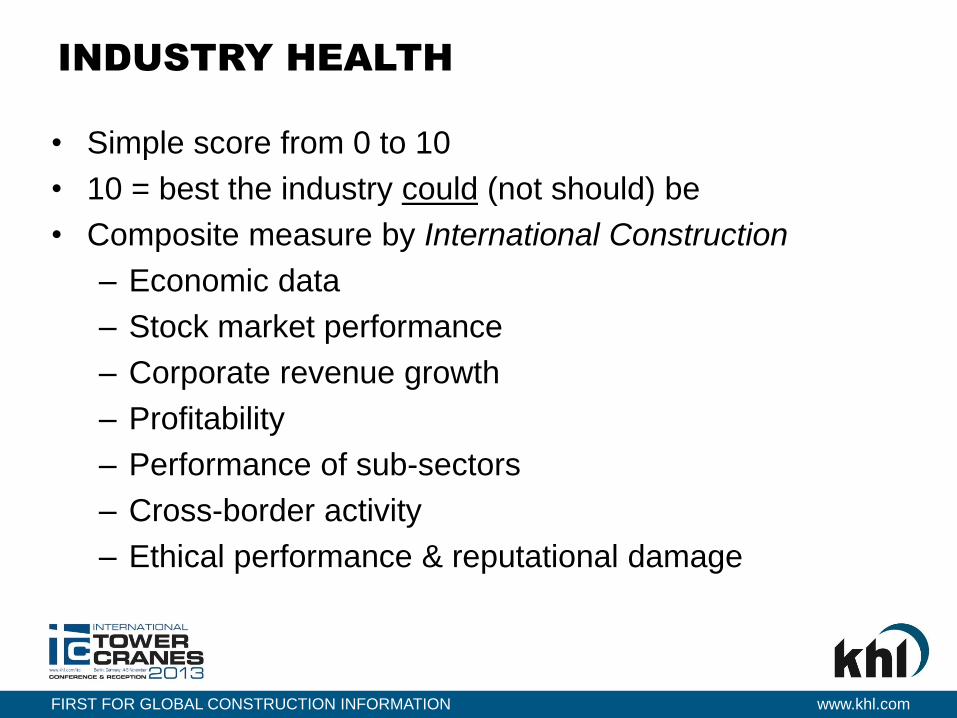

INDUSTRY HEALTH

• Simple score from 0 to 10

• 10 = best the industry could (not should) be

• Composite measure by International Construction

– Economic data

– Stock market performance

– Corporate revenue growth

– Profitability

– Performance of sub-sectors

– Cross-border activity

– Ethical performance & reputational damage

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

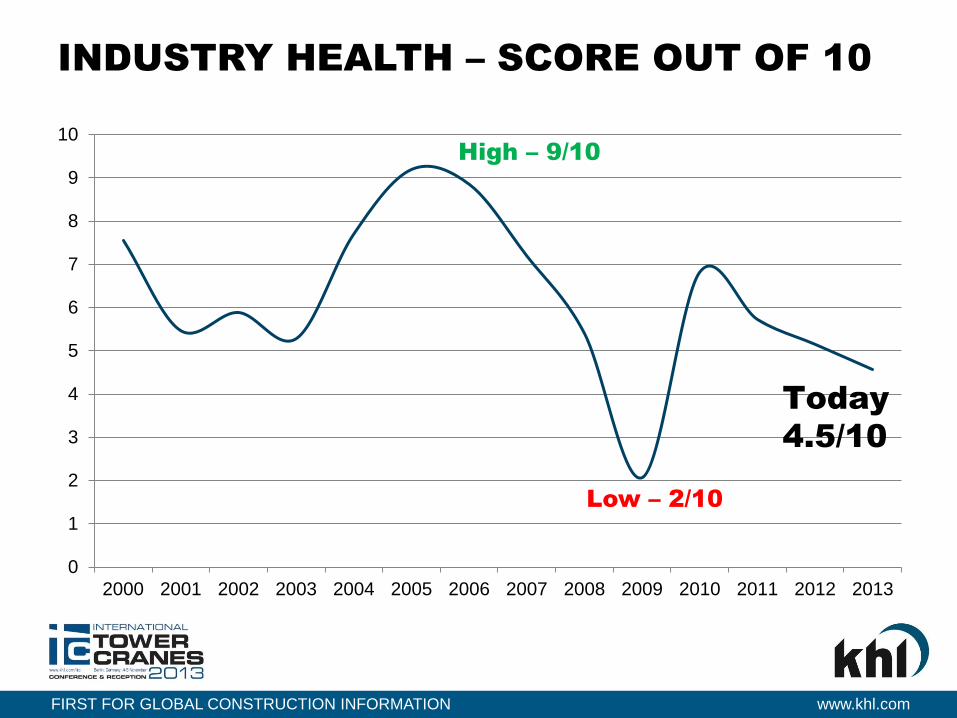

INDUSTRY HEALTH – SCORE OUT OF 10

0

1

2

3

4

5

6

7

8

9

10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Low – 2/10

Today

4.5/10

High – 9/10

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

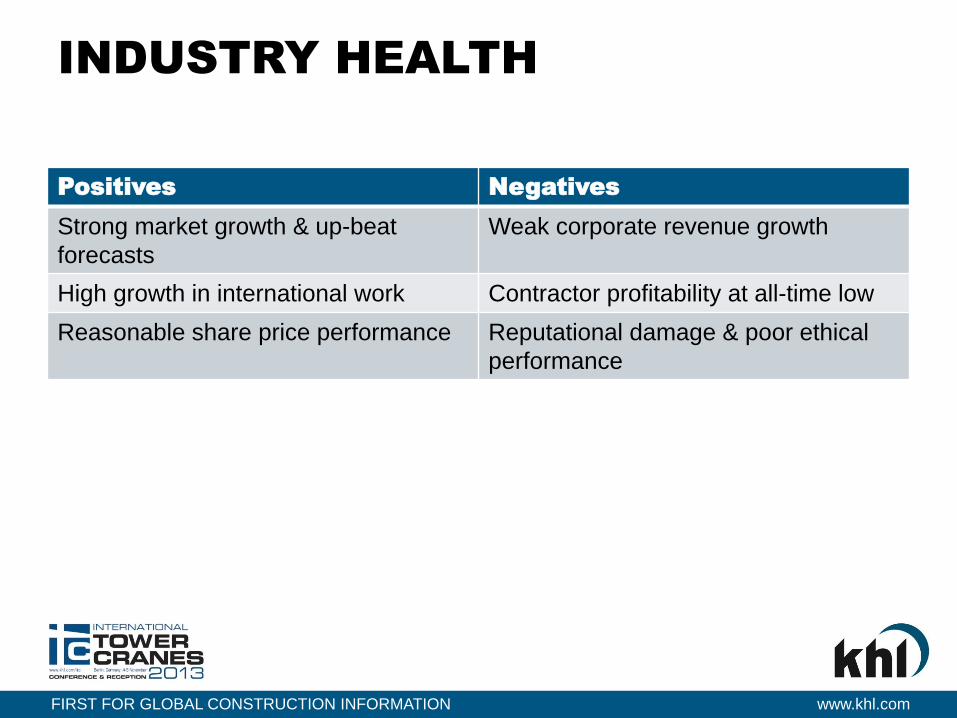

INDUSTRY HEALTH

Positives Negatives

Strong market growth & up-beat

forecasts

Weak corporate revenue growth

High growth in international work Contractor profitability at all-time low

Reasonable share price performance Reputational damage & poor ethical

performance

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

EUROPEAN MARKETS IN DEPTH

• Many sources & forecasts (FIEC, Euroconstruct, IHS

Global Insight, Oxford Economics++)

– Exact numbers may differ

– Some specific differences of opinion

– Trends & outlook similar

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

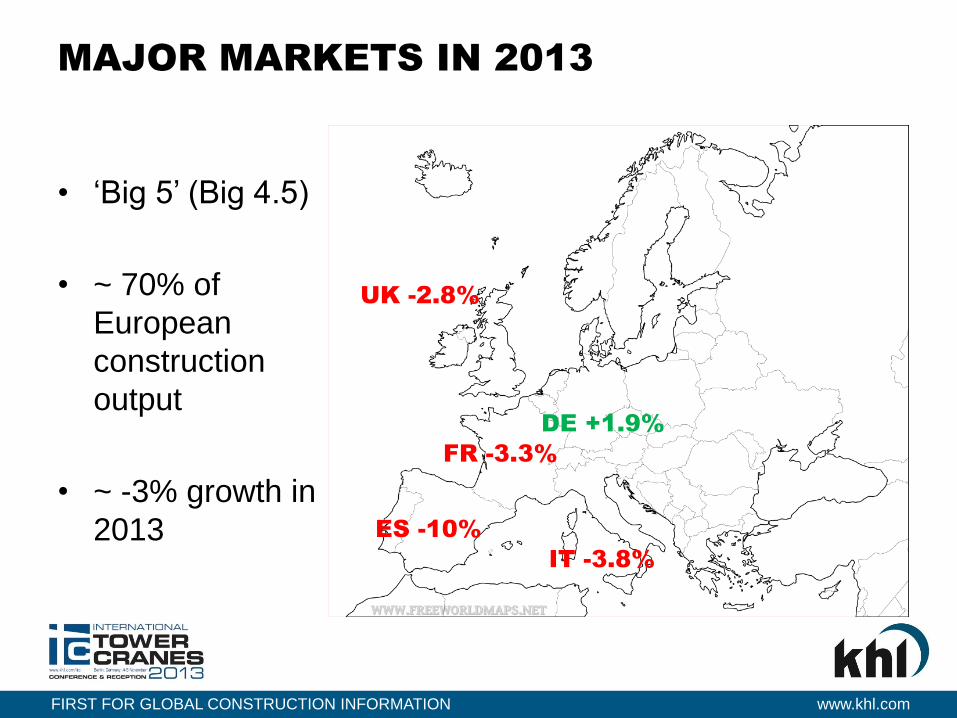

MAJOR MARKETS IN 2013

UK -2.8%

IT -3.8%

FR -3.3%

ES -10%

• ‘Big 5’ (Big 4.5)

• ~ 70% of

European

construction

output

• ~ -3% growth in

2013

DE +1.9%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

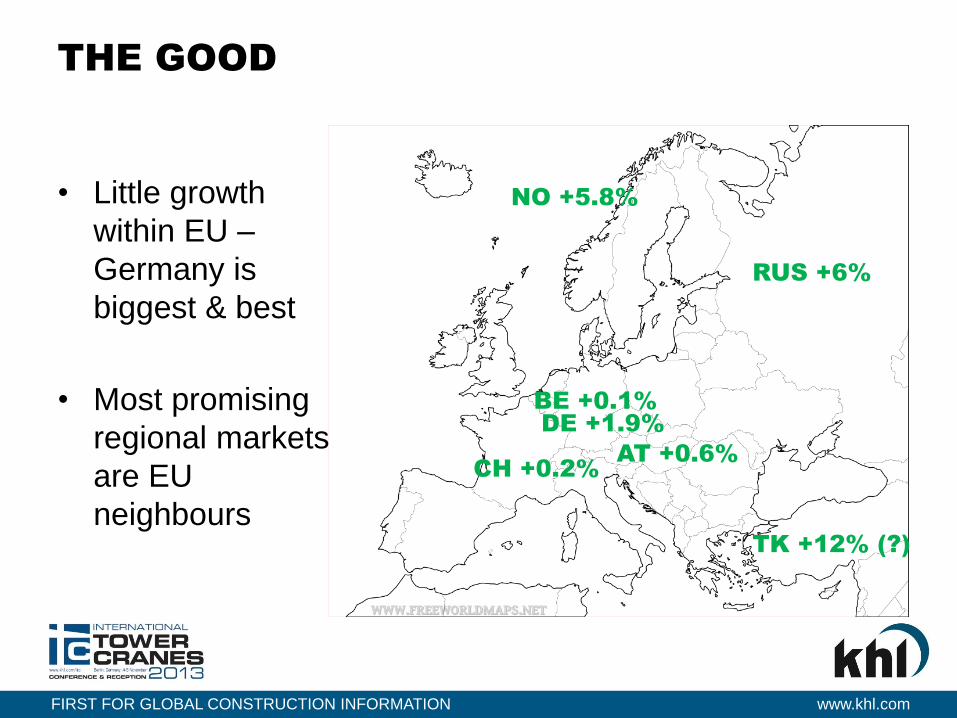

THE GOOD

DE +1.9%

• Little growth

within EU –

Germany is

biggest & best

• Most promising

regional markets

are EU

neighbours

NO +5.8%

AT +0.6%

TK +12% (?)

RUS +6%

BE +0.1%

CH +0.2%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

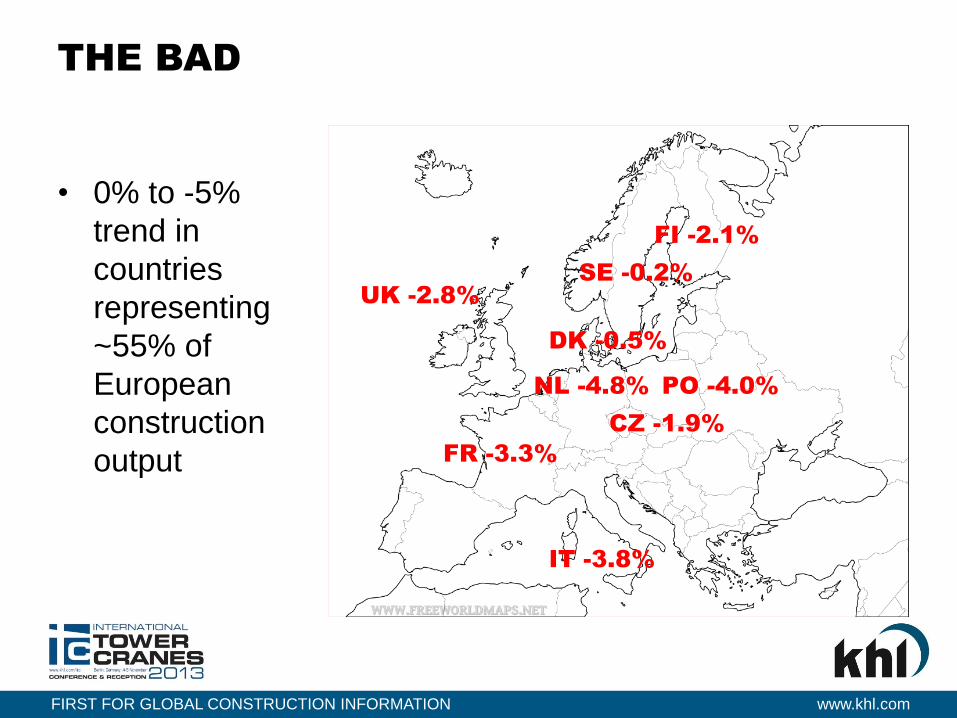

THE BAD

UK -2.8%

IT -3.8%

FR -3.3%

• 0% to -5%

trend in

countries

representing

~55% of

European

construction

output

SE -0.2%

FI -2.1%

PO -4.0%

CZ -1.9%

NL -4.8%

DK -0.5%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

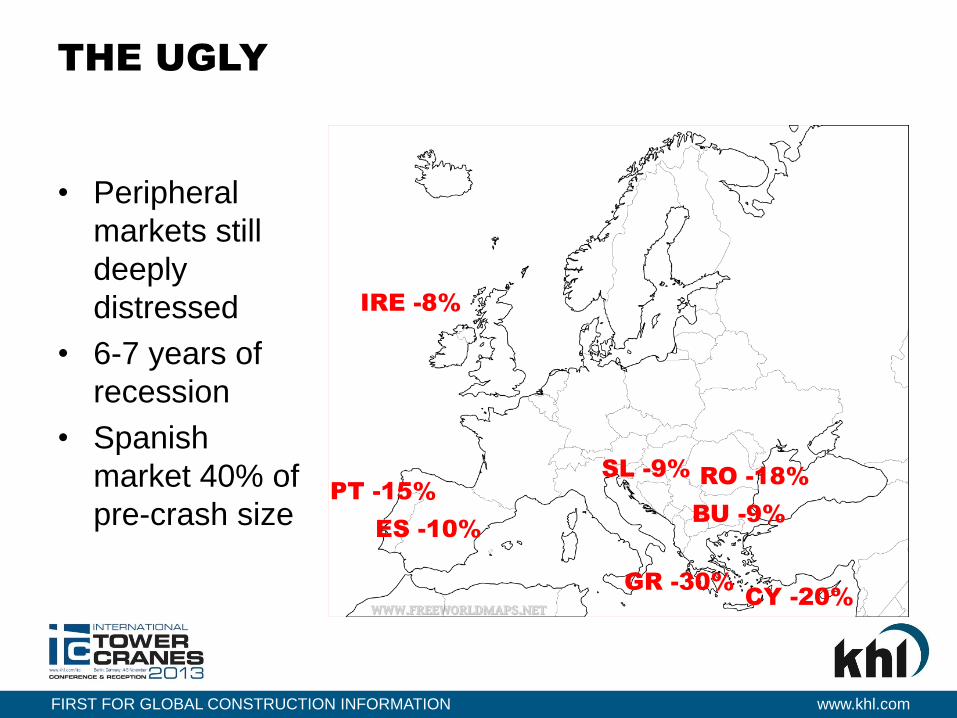

THE UGLY

IRE -8%

ES -10%

• Peripheral

markets still

deeply

distressed

• 6-7 years of

recession

• Spanish

market 40% of

pre-crash size

CY -20%

PT -15%

GR -30%

RO -18%

BU -9%

SL -9%

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

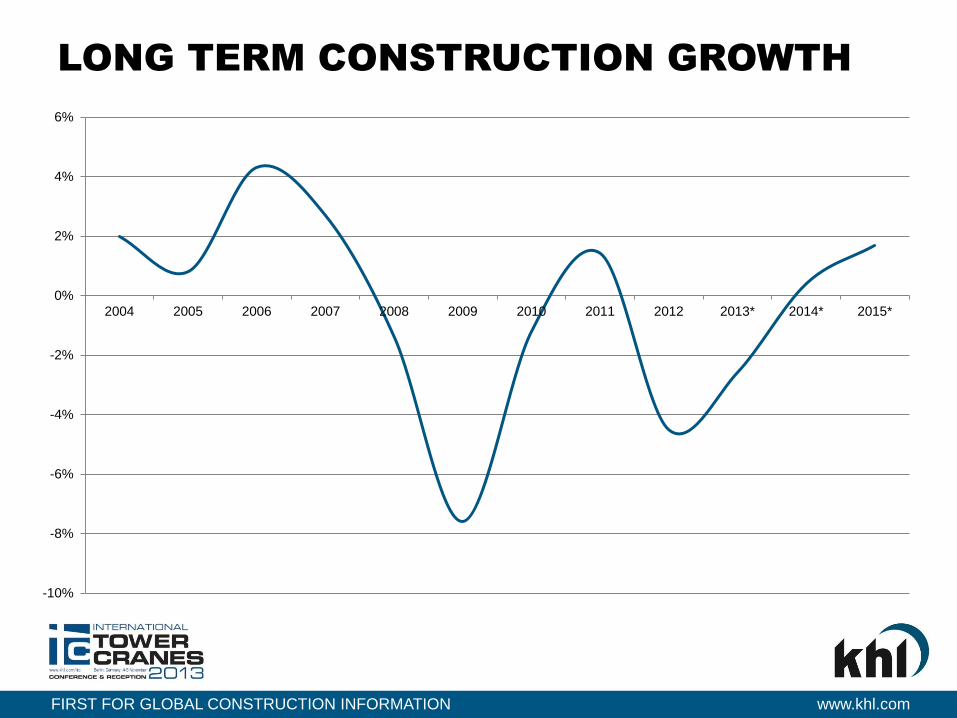

LONG TERM CONSTRUCTION GROWTH

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013* 2014* 2015*

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

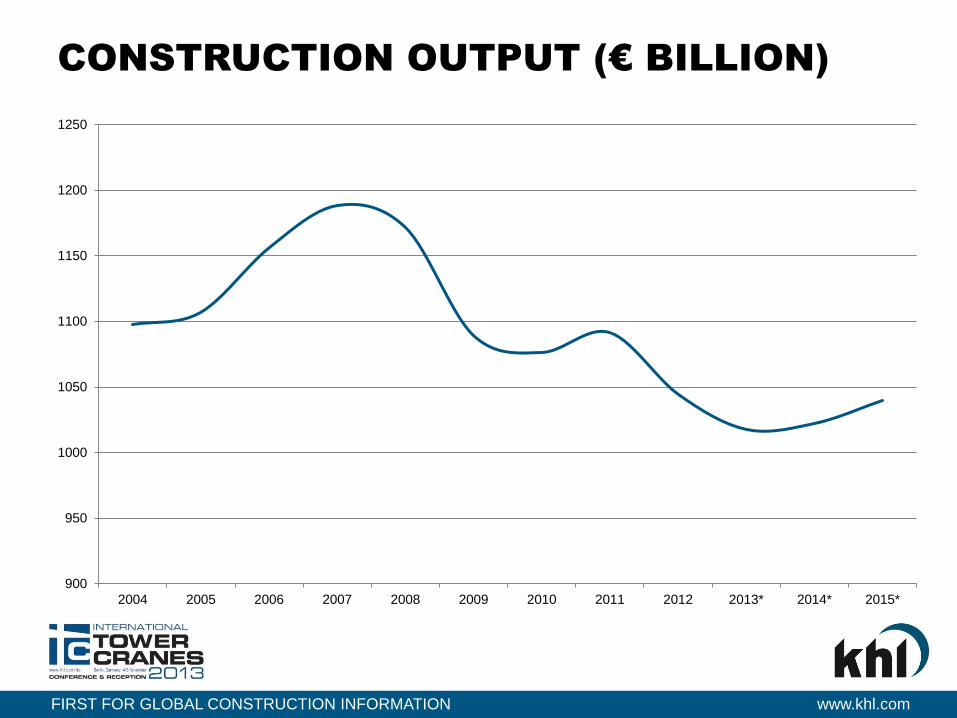

CONSTRUCTION OUTPUT (€ BILLION)

900

950

1000

1050

1100

1150

1200

1250

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013* 2014* 2015*

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

LONG TERM GROWTH TRENDS

• 2011 recovery stalled – now in second dip

– Triggered by threat of Greek default

• Recovery in 2014(?)

• Market value has fallen back to late-1990s levels

• When it returns, growth will be weak in global terms

– The ‘boom year’ of 2006 saw +4.5% growth

• Europe is still a big market ~20% of global output

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

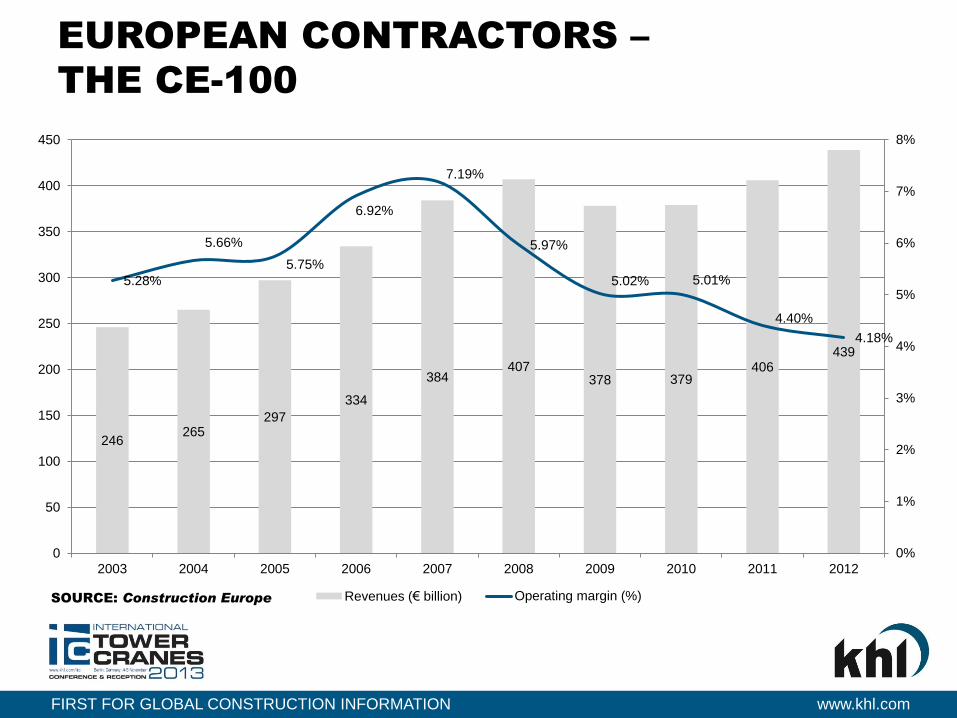

EUROPEAN CONTRACTORS –

THE CE-100

246 265

297

334

384 407

378 379 406

439

5.28%

5.66%

5.75%

6.92%

7.19%

5.97%

5.02% 5.01%

4.40%

4.18%

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

50

100

150

200

250

300

350

400

450

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Revenues (€ billion) Operating margin (%)SOURCE: Construction Europe

FIRST FOR GLOBAL CONSTRUCTION INFORMATION www.khl.com

SUMMARY

• Industry in recovery

• Era of moderate global growth

– Hard to predict

• Greatest growth in emerging markets

– Risk vs reward