global cloud infrastructure as a service market outlook

TRANSCRIPT

Global Cloud Infrastructure as a Service Market Outlook,

Forecast to 2023

An Executive Summary

2 CC 9-2

Executive Summary

3 CC 9-2

Executive Summary

The Infrastructure as a Service (IaaS) market remains highly active worldwide, having reached an astounding U$45.6 Billion

in revenues in 2018. While adoption pace and patterns vary, all regions—North America, Europe, Latin America, and Asia-

Pacific—are firmly on the path toward the cloud.

This study analyzes the current global IaaS market, and forecasts revenue growth from

2019–2023. The analysis is segmented by multi-tenant and single-tenant cloud services.

Companies have Become

Increasingly Hybrid and/or

Multi-cloud

Regions More Mature in Cloud

Adoption are Experiencing a

Repatriation Trend

The Competitive Landscape has

Two Top Providers

Single-tenant services Will

Gain Share

Asia Pacific and Latin America are

Lagging in Terms of Adoption Those regions hold tremendous opportunity for cloud vendors, and potentially

the greatest compound annual growth rates

Frost & Sullivan expects that single-tenant services will gain share over the

forecast period, precisely As a result of the hybrid and multi-cloud trends.

AWS and Microsoft now control 74% of the global market share. Microsoft

holds second place behind AWS in all regions except for Asia Pacific, where

Alibaba is the second largest.

Network latency, migration challenges, and challenges with backup/recovery of

cloud workloads are reasons enterprises in North America and certain parts of

Europe are taking cloud-based workloads back to their premises

Hybrid environment allows businesses to choose a mix of deployment models

and manage them as a single pool of resources. A multi-cloud environment

comprises more than one cloud provider. Cloud brokerage and cloud

management platforms are boosting this trend, making managed cloud

services providers key in supporting enterprises, while also challenging IaaS

providers to constantly innovate to meet their customers’ needs.

4 CC 9-2

Executive Summary—CEO’s Perspective

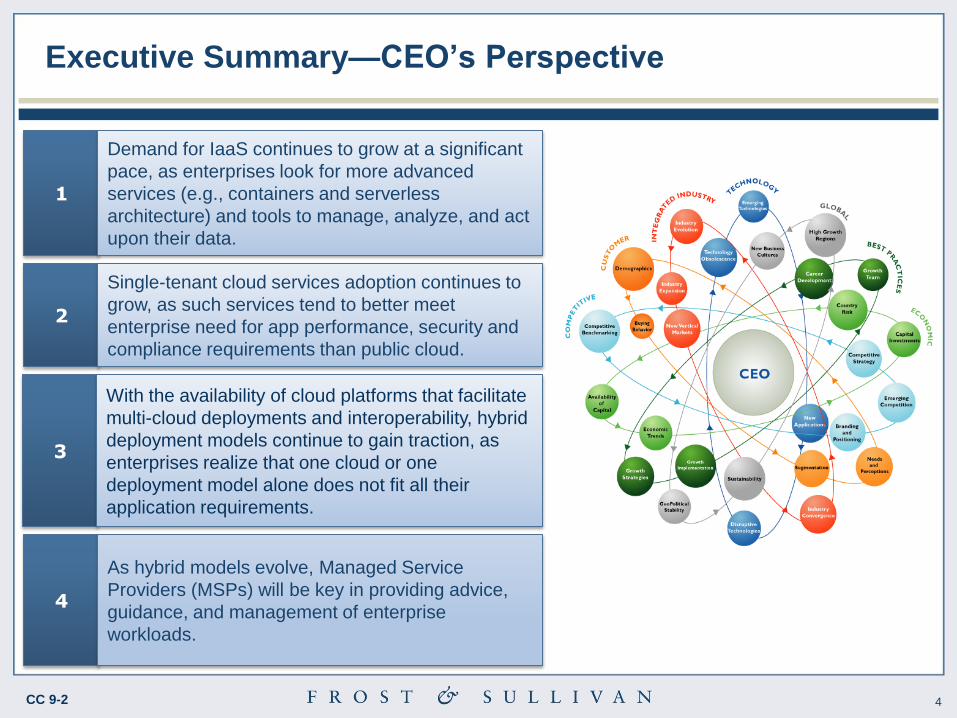

2

Single-tenant cloud services adoption continues to

grow, as such services tend to better meet

enterprise need for app performance, security and

compliance requirements than public cloud.

3

With the availability of cloud platforms that facilitate

multi-cloud deployments and interoperability, hybrid

deployment models continue to gain traction, as

enterprises realize that one cloud or one

deployment model alone does not fit all their

application requirements.

4

As hybrid models evolve, Managed Service

Providers (MSPs) will be key in providing advice,

guidance, and management of enterprise

workloads.

1

Demand for IaaS continues to grow at a significant

pace, as enterprises look for more advanced

services (e.g., containers and serverless

architecture) and tools to manage, analyze, and act

upon their data.

5 CC 9-2

Market Overview

6 CC 9-2

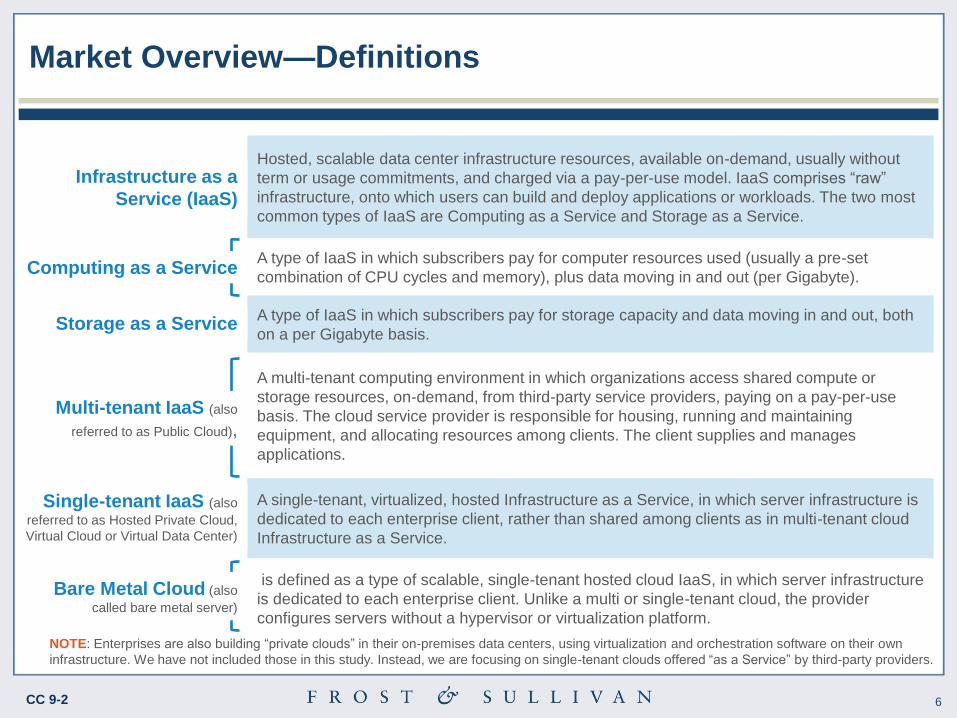

Hosted, scalable data center infrastructure resources, available on-demand, usually without

term or usage commitments, and charged via a pay-per-use model. IaaS comprises “raw”

infrastructure, onto which users can build and deploy applications or workloads. The two most

common types of IaaS are Computing as a Service and Storage as a Service.

A type of IaaS in which subscribers pay for computer resources used (usually a pre-set

combination of CPU cycles and memory), plus data moving in and out (per Gigabyte).

A type of IaaS in which subscribers pay for storage capacity and data moving in and out, both

on a per Gigabyte basis.

A multi-tenant computing environment in which organizations access shared compute or

storage resources, on-demand, from third-party service providers, paying on a pay-per-use

basis. The cloud service provider is responsible for housing, running and maintaining

equipment, and allocating resources among clients. The client supplies and manages

applications.

A single-tenant, virtualized, hosted Infrastructure as a Service, in which server infrastructure is

dedicated to each enterprise client, rather than shared among clients as in multi-tenant cloud

Infrastructure as a Service.

is defined as a type of scalable, single-tenant hosted cloud IaaS, in which server infrastructure

is dedicated to each enterprise client. Unlike a multi or single-tenant cloud, the provider

configures servers without a hypervisor or virtualization platform.

Market Overview—Definitions

NOTE: Enterprises are also building “private clouds” in their on-premises data centers, using virtualization and orchestration software on their own

infrastructure. We have not included those in this study. Instead, we are focusing on single-tenant clouds offered “as a Service” by third-party providers.

Infrastructure as a

Service (IaaS)

Storage as a Service

Single-tenant IaaS (also

referred to as Hosted Private Cloud,

Virtual Cloud or Virtual Data Center)

Computing as a Service

Multi-tenant IaaS (also

referred to as Public Cloud),

Bare Metal Cloud (also

called bare metal server)

7 CC 9-2

Market Overview—Definitions (continued)

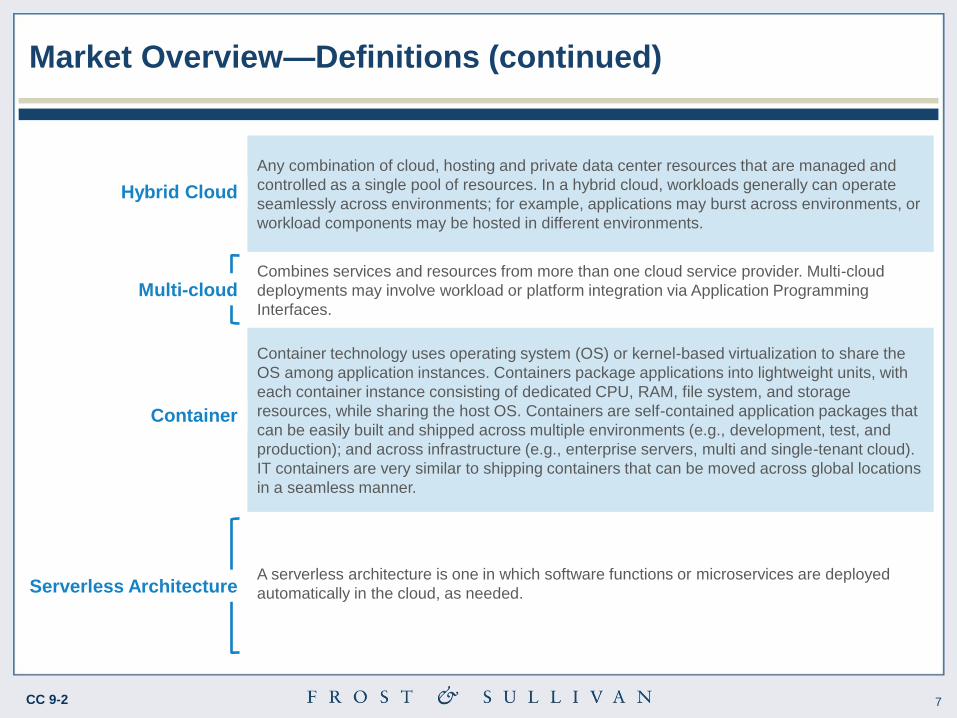

Any combination of cloud, hosting and private data center resources that are managed and

controlled as a single pool of resources. In a hybrid cloud, workloads generally can operate

seamlessly across environments; for example, applications may burst across environments, or

workload components may be hosted in different environments.

Combines services and resources from more than one cloud service provider. Multi-cloud

deployments may involve workload or platform integration via Application Programming

Interfaces.

Container technology uses operating system (OS) or kernel-based virtualization to share the

OS among application instances. Containers package applications into lightweight units, with

each container instance consisting of dedicated CPU, RAM, file system, and storage

resources, while sharing the host OS. Containers are self-contained application packages that

can be easily built and shipped across multiple environments (e.g., development, test, and

production); and across infrastructure (e.g., enterprise servers, multi and single-tenant cloud).

IT containers are very similar to shipping containers that can be moved across global locations

in a seamless manner.

A serverless architecture is one in which software functions or microservices are deployed

automatically in the cloud, as needed.

Hybrid Cloud

Multi-cloud

Container

Serverless Architecture

8 CC 9-2

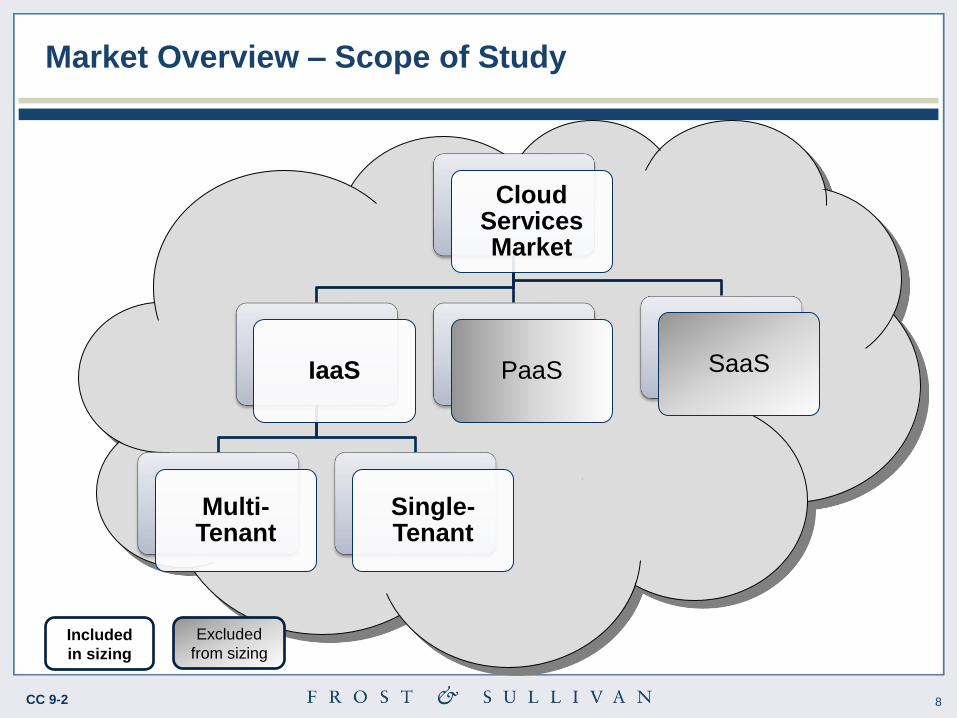

Market Overview – Scope of Study

Cloud Services Market

IaaS

Multi-Tenant

Single-Tenant

PaaS SaaS

Included

in sizing

Excluded

from sizing

9 CC 9-2

Market Overview—Scope of Study (continued)

In our market sizing, Frost & Sullivan has included IaaS services, as defined—comprising both multi-tenant

and single-tenant cloud.

Whenever possible, we have excluded revenue from value-added services that providers may offer to their

cloud customers, including fee-based managed and professional services. However, many providers in the

market do not split their IaaS revenues based on self-service and managed services. Inconsistencies in

reporting may have led to inclusion of some revenues from managed portions in our total market estimate. We

will revise this estimate as providers clarify their definitions and start to record revenues separately.

Bare metal cloud, which is a type of IaaS, is gaining some traction in the market, with companies like IBM and

CenturyLink offering the service. AWS and Azure have also begun rolling out bare metal options in the past

year. Revenue from bare metal is counted in the single-tenant cloud category in this report.

We have excluded hosted services that are not available on-demand, such as co-location and managed

hosting services. We have also excluded “pull through” IaaS, in which a provider offers elastic storage or

computing resources as part of a different service offering, such as PaaS or SaaS. Our reasoning is that this

type of service constrains users to a specific platform, rather than providing raw infrastructure. Furthermore, in

most cases, the provider defines the computing or storage resources as an element of the primary service

(SaaS or PaaS), rather than standalone IaaS.

Some value-added services, such as Database as a Service (DBaaS) can be considered a “pull through” IaaS;

but due to lack of sufficient data on the revenue breakdowns from the providers, we are counting such services

within the IaaS revenue market size.

10 CC 9-2

Market Overview—Scope of Study (continued)

Throughout the report, statistics from the Frost & Sullivan Cloud User Survey are mentioned. The Frost &

Sullivan Cloud User Survey, conducted annually since 2010, tracks perceptions and behaviors related to

business cloud decisions. It covers not only cloud services, but adjacent infrastructure areas, including

managed services, premises data center infrastructure, security, and communications services.

In this report, we review key findings from the 2018 Cloud User Survey related specifically to cloud

Infrastructure as a Service (IaaS). The survey was conducted via web in June 2018, garnering responses from

401 US-based IT decision makers responsible for purchases of IT infrastructure, software, or services for their

firms.

11 CC 9-2

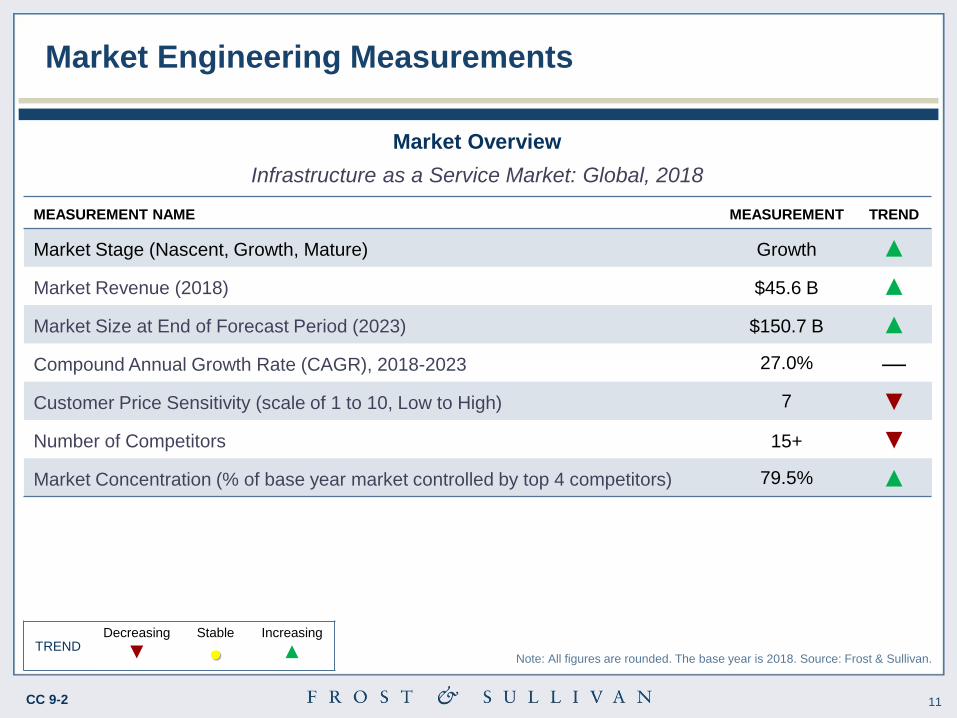

MEASUREMENT NAME MEASUREMENT TREND

Market Stage (Nascent, Growth, Mature) Growth ▲

Market Revenue (2018) $45.6 B ▲

Market Size at End of Forecast Period (2023) $150.7 B ▲

Compound Annual Growth Rate (CAGR), 2018-2023 27.0% —

Customer Price Sensitivity (scale of 1 to 10, Low to High) 7 ▼

Number of Competitors 15+ ▼

Market Concentration (% of base year market controlled by top 4 competitors) 79.5% ▲

Market Engineering Measurements

TREND Decreasing Stable Increasing

▼ ● ▲

Market Overview

Infrastructure as a Service Market: Global, 2018

Note: All figures are rounded. The base year is 2018. Source: Frost & Sullivan.

12 CC 9-2

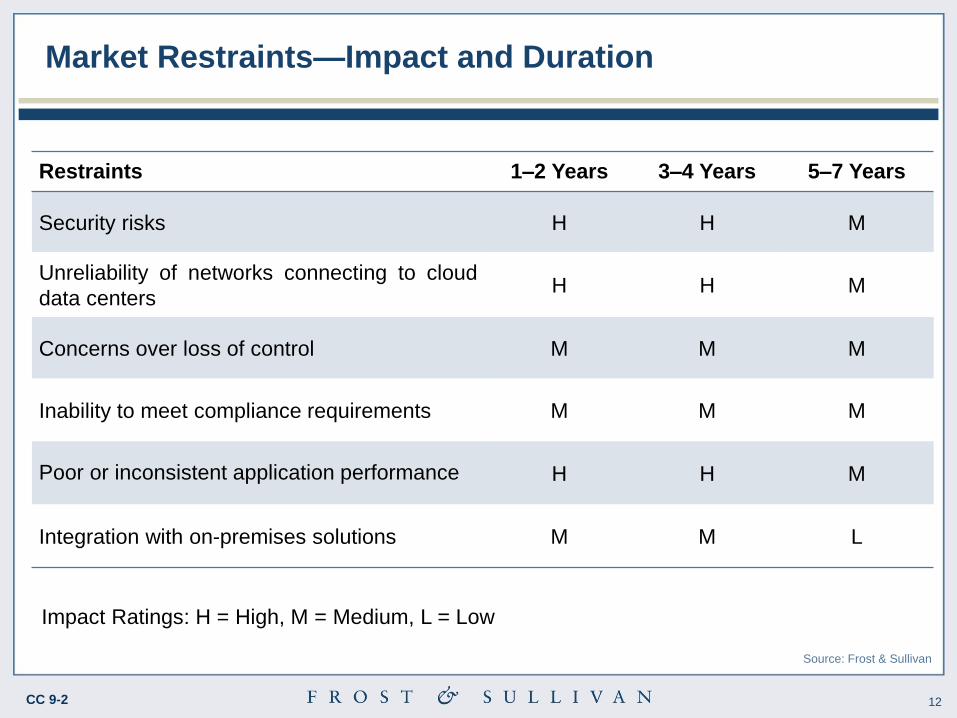

Restraints 1–2 Years 3–4 Years 5–7 Years

Security risks H H M

Unreliability of networks connecting to cloud

data centers H H M

Concerns over loss of control M M M

Inability to meet compliance requirements M M M

Poor or inconsistent application performance H H M

Integration with on-premises solutions M M L

Impact Ratings: H = High, M = Medium, L = Low

Market Restraints—Impact and Duration

Source: Frost & Sullivan

13 CC 9-2

Restraints Explained

Security risks – Sixty-one percent of survey respondents cited concerns about unauthorized access to

data as the top restraint to cloud IaaS adoption in 2018. Security concerns mainly surround unauthorized

access to apps and leakage of data, particularly in a shared cloud environment; as well as the need to

have globally consistent cybersecurity protections. Regions that are later adopters of cloud, such as

Latin America, as well as countries with a higher level of conservatism, such as Germany and some

parts of Asia, are more impacted by this restraint. However, interviews with leading cloud service

providers indicate that, while data security remains a concern for cloud users, it is driving enterprises to

adopt a hybrid cloud strategy that places each workload in the optimal deployment model—multi-tenant

cloud, single-tenant cloud, on-premises—based on security and other needs.

Unreliability of networks connecting to cloud data centers – A majority of cloud users connect to the

cloud over public internet, which offers best-effort connectivity. Any disruption to the access network

leaves the users without access to applications hosted in the cloud. Fifty-five percent of survey

respondents cited unreliable networks as a deterrent to cloud adoption.

14 CC 9-2

Concerns over loss of control – This is the third biggest concern about IaaS adoption, with 54% of

survey respondents citing it as a top concern. IT leaders are still not one-hundred percent confident that a

multi-tenant environment is well-suited to keep their apps running consistently in the face of contention for

shared resources. Furthermore, with the cloud model, the enterprise IT no longer owns the hardware; and

hence, has no control over addressing application-affecting system failures. Over time, as the cloud

market continues to evolve, and providers earn the trust of customers, this restraint is being mitigated.

Inability to meet compliance requirements – Enterprises’ requirement to ensure regulatory compliance

of data storage continues to be a market restraint for multi-tenant IaaS. Fifty-three percent of the

respondents cited this as a reason for not choosing cloud IaaS. This concern has been further enhanced

by the European Union General Data Protection Regulation (GDPR), which has strict requirements for

handling and storage of personally identifiable information; the General Law of Data Protection (LGPD) in

Brazil, Latin America; and strict data sovereignty laws in Germany, France and Russia, which require

citizens’ data to be stored in physical servers inside each countries’ borders. Compliance concerns are

leading cloud providers to expand their data centers to more countries and regions; but it is also driving

enterprises to keep their sensitive data on-premises or in co-location facilities.

Restraints Explained (continued)

15 CC 9-2

Restraints Explained (continued)

Application performance and downtime – While evaluating cloud IaaS services, enterprises are very

concerned about reliable performance and uptime. Fifty-three percent of the respondents cite inconsistent

application performance as a deterrent to cloud adoption. Concerns are fueled by the cloud outages that

leading IaaS vendors have experienced, including: a power outage at AWS-East Region (Ashburn), which

is one of the company’s largest regions and comprises six availability zones, in March 2018; and Microsoft

Azure’s outage in September 2018, due to a power voltage increase caused by a storm, which impacted

the cooling systems in its datacenter near San Antonio, Texas. In addition, the shared environment can

create contention for resources, which can negatively impact application performance. Any downtime to

critical applications can cost sales, impact the direct bottom line, and also have a longer-term impact on

the enterprises’ brand reputation.

Integration with on-premises solutions – Businesses may want to keep some workloads on-premises

due to network latency or for disaster recovery reasons. However, because leading cloud services are

largely built on proprietary platforms, it can be really difficult to integrate and orchestrate under a common

management platform. That is why hybrid cloud platforms have gained increasing acceptance across

enterprises, as well as offerings such as AWS Outposts and Google’s GKE On-prem, which offer

premises-based extensions of the cloud environment.

16 CC 9-2

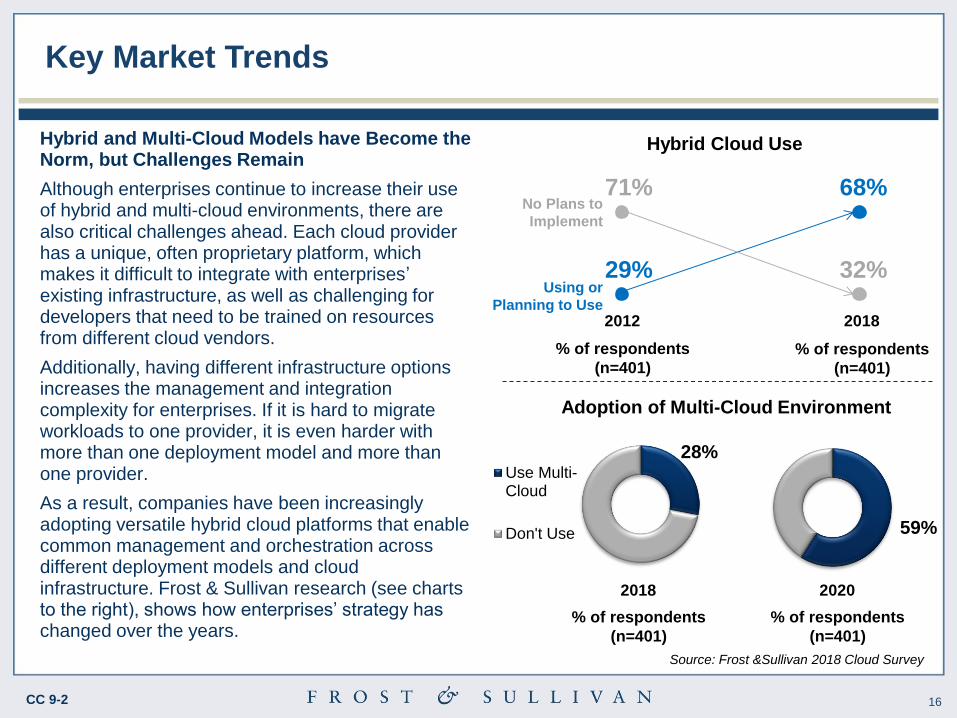

Hybrid and Multi-Cloud Models have Become the Norm, but Challenges Remain

Although enterprises continue to increase their use of hybrid and multi-cloud environments, there are also critical challenges ahead. Each cloud provider has a unique, often proprietary platform, which makes it difficult to integrate with enterprises’ existing infrastructure, as well as challenging for developers that need to be trained on resources from different cloud vendors.

Additionally, having different infrastructure options increases the management and integration complexity for enterprises. If it is hard to migrate workloads to one provider, it is even harder with more than one deployment model and more than one provider.

As a result, companies have been increasingly adopting versatile hybrid cloud platforms that enable common management and orchestration across different deployment models and cloud infrastructure. Frost & Sullivan research (see charts to the right), shows how enterprises’ strategy has changed over the years.

Hybrid Cloud Use

Source: Frost &Sullivan 2018 Cloud Survey

2012 2018

No Plans to

Implement

Using or

Planning to Use

71%

32% 29%

68%

Adoption of Multi-Cloud Environment

28% Use Multi-Cloud

Don't Use 59%

2018 2020

% of respondents

(n=401)

% of respondents

(n=401)

% of respondents

(n=401)

% of respondents

(n=401)

Key Market Trends

17 CC 9-2

Source: Frost &Sullivan 2018 Cloud Survey

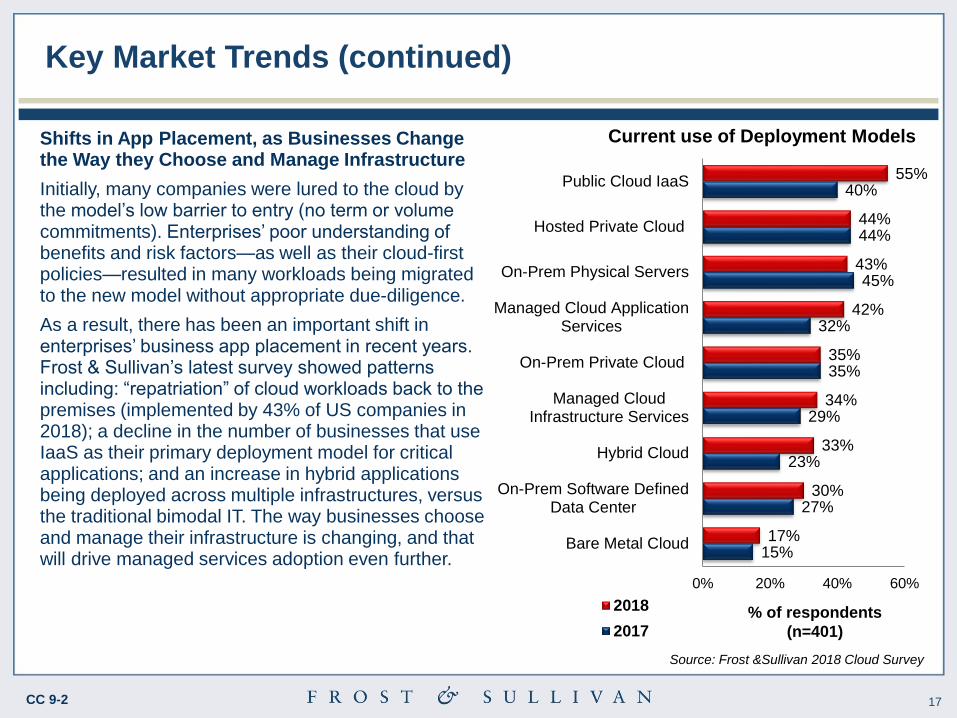

Shifts in App Placement, as Businesses Change the Way they Choose and Manage Infrastructure

Initially, many companies were lured to the cloud by the model’s low barrier to entry (no term or volume commitments). Enterprises’ poor understanding of benefits and risk factors—as well as their cloud-first policies—resulted in many workloads being migrated to the new model without appropriate due-diligence.

As a result, there has been an important shift in enterprises’ business app placement in recent years. Frost & Sullivan’s latest survey showed patterns including: “repatriation” of cloud workloads back to the premises (implemented by 43% of US companies in 2018); a decline in the number of businesses that use IaaS as their primary deployment model for critical applications; and an increase in hybrid applications being deployed across multiple infrastructures, versus the traditional bimodal IT. The way businesses choose and manage their infrastructure is changing, and that will drive managed services adoption even further.

Current use of Deployment Models

15%

27%

23%

29%

35%

32%

45%

44%

40%

17%

30%

33%

34%

35%

42%

43%

44%

55%

0% 20% 40% 60%

Bare Metal Cloud

On-Prem Software DefinedData Center

Hybrid Cloud

Managed CloudInfrastructure Services

On-Prem Private Cloud

Managed Cloud ApplicationServices

On-Prem Physical Servers

Hosted Private Cloud

Public Cloud IaaS

2018

2017% of respondents

(n=401)

Key Market Trends (continued)

18 CC 9-2

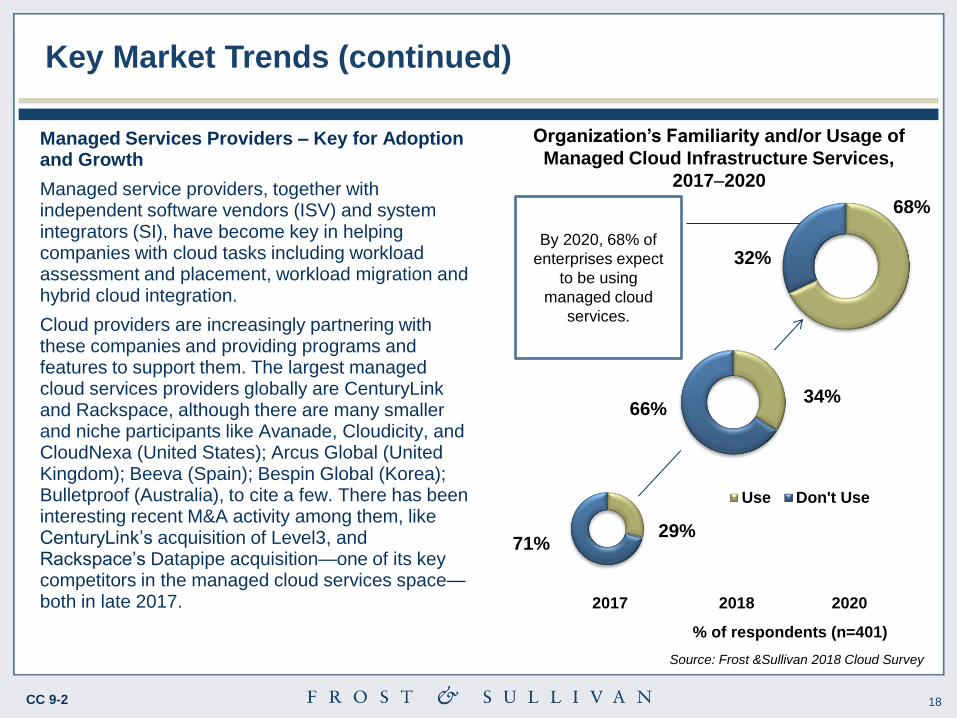

Managed Services Providers – Key for Adoption and Growth

Managed service providers, together with independent software vendors (ISV) and system integrators (SI), have become key in helping companies with cloud tasks including workload assessment and placement, workload migration and hybrid cloud integration.

Cloud providers are increasingly partnering with these companies and providing programs and features to support them. The largest managed cloud services providers globally are CenturyLink and Rackspace, although there are many smaller and niche participants like Avanade, Cloudicity, and CloudNexa (United States); Arcus Global (United Kingdom); Beeva (Spain); Bespin Global (Korea); Bulletproof (Australia), to cite a few. There has been interesting recent M&A activity among them, like CenturyLink’s acquisition of Level3, and Rackspace’s Datapipe acquisition—one of its key competitors in the managed cloud services space—both in late 2017.

Source: Frost &Sullivan 2018 Cloud Survey

Organization’s Familiarity and/or Usage of

Managed Cloud Infrastructure Services,

2017–2020

34% 66%

Use Don't Use

29% 71%

By 2020, 68% of

enterprises expect

to be using

managed cloud

services.

68%

32%

% of respondents (n=401)

2018 2020 2017

Key Market Trends (continued)

19 CC 9-2

IBM continues to be very strong in enterprise-grade environments and in its AI and machine learning

portfolio. It is also the leading provider of bare metal (non-virtualized) cloud. In Fiscal Year (FY) 2018, IBM

reached 12% growth in total cloud revenues, and approximately 18% in cloud as-a-service revenues,

according to Frost & Sullivan estimates and IBM’s quarterly reports.

In 2018, IBM made several moves to accelerate its pace and strengthen its position in hybrid and multi-cloud

environments. In October 2018, IBM announced its intention to acquire Red Hat, an enterprise open source

technology provider; giving the company a strong edge in open source architectures, management

platforms, and hybrid cloud solutions. Also in October 2018, IBM launched IBM Multicloud Manager, an

open technology solution for managing Kubernetes clusters across a variety of infrastructures, both public

and private; enabling visibility, governance and security, and consistent application management via a single

platform. The platform is optimized on IBM Cloud, but also manages workloads from AWS, Red Hat, and

Microsoft.

IBM is investing globally with increased footprint/multi-zone regions in Tokyo, Frankfurt, London and now

Sydney, which support its global footprint. IBM also has a strong competitive presence in Latin America. The

company reports that Brazil is its second biggest market for Watson, globally—second only to the United

States; and it claims that its Cloud Kubernetes Service (IKS) is the only Kubernetes service available in a

data center in Brazil.

In February 2019, IBM announced that Watson is now available on other cloud platforms such as Microsoft,

AWS, and Google Cloud Platform.

Competitor Profiles – IBM

20 CC 9-2

The Last Word

21 CC 9-2

The Last Word

The global cloud IaaS market has evolved. Enterprises are frequently choosing cloud for strategic benefits—

like supporting digital transformation initiatives and enabling them to take advantage of new technologies;

rather than tactical ones—like reducing IT infrastructure costs and hardware/software maintenance burden.

That shift is also changing the way they choose and manage their infrastructure, leading them to deploy

applications across multiple infrastructures—from on-premises to cloud, and between different cloud

vendors.

As the mix of deployment models and best-of-breed cloud IaaS vendors becomes increasingly diverse, two

key outcomes are expected: single-tenant IaaS will continue to gain revenue share over multi-tenant; and

MSPs will continue to be key in supporting companies with workload assessment and placement, workload

migration, and hybrid cloud integration. Cloud brokerage and cloud management platforms will be strategic

tools during this process.

While AWS continues to be the market leader with great leverage, Microsoft is growing at a rapid pace, and

so is Alibaba. All three vendors are expected to continue to invest in expanding their territories and market

reach. 2019 should be key for IBM, after the Red Hat acquisition; and also for Google Cloud, under new

leadership. Frost & Sullivan believes that, looking forward, it will be essential for cloud IaaS vendors to

continue to invest in integrated services, on-prem and cloud; and in the support of MSPs to help enterprises

shift to the hybrid and multi-cloud models.

22 CC 9-2

Legal Disclaimer

Frost & Sullivan takes no responsibility for any incorrect information supplied to us by

manufacturers or users. Quantitative market information is based primarily on interviews

and, therefore, is subject to fluctuation. Frost & Sullivan research services are limited

edition publications containing valuable market information provided to a select group of

customers. Our customers acknowledge, when ordering or downloading, that Frost &

Sullivan research services are for customers’ internal use and not for general publication or

disclosure to third parties. No part of this research service may be given, lent, resold or

disclosed to noncustomers without written permission. Furthermore, no part may be

reproduced, stored in a retrieval system, or transmitted in any form or by any means,

electronic, mechanical, photocopying, recording or otherwise, without the permission of the

publisher.

For information regarding permission, write to:

Frost & Sullivan

3211 Scott Blvd

Santa Clara CA 95054