gim uk loans s.a. - rns submit · gim uk loans s.a. 2 gim uk loans s.a. société anonyme de...

TRANSCRIPT

GIM UK Loans S.A.

2

GIM UK Loans S.A.

Société Anonyme de Titrisation R.C.S. Luxembourg N° B202528

60, avenue John F. Kennedy, L-1855 Luxembourg

Annual accounts for the period from December 9, 2015

(date of incorporation) to December 31, 2016

GIM UK Loans S.A.

2

Table of contents

Page

Audit report 3 – 4

Director’s report 5 - 8

Balance Sheet 9 - 10

Profit and Loss Account 11

Notes to the Annual Accounts 12 - 19

Ernst & YoungSociété anonyme

35E, Avenue John F. KennedyL-1855 Luxembourg

Tel: +352 42 124 1

www.ey.com/luxembourg

3

B.P. 780L-2017 Luxembourg

R.C.S. Luxembourg B 47 771TVA LU 16063074

Independent auditor’s report

To the Shareholders ofGIM UK Loans S.A.60, avenue John F. KennedyL-1855 Luxembourg

Report on the annual accounts

Following our appointment by the Board of Directors dated 18 December 2015, we have audited theaccompanying annual accounts of GIM UK Loans S.A., which comprise the balance sheet as at 31December 2016 and the profit and loss account for the period from 9 December 2015 (date ofincorporation) to 31 December 2016, and a summary of significant accounting policies and otherexplanatory information.

Board of Directors’ responsibility for the annual accounts

The Board of Directors is responsible for the preparation and fair presentation of these annual accountsin accordance with Luxembourg legal and regulatory requirements relating to the preparation andpresentation of the annual accounts and for such internal control as the Board of Directors determines isnecessary to enable the preparation and presentation of annual accounts that are free from materialmisstatement, whether due to fraud or error.

Responsibility of the “réviseur d’entreprises agréé”

Our responsibility is to express an opinion on these annual accounts based on our audit. We conductedour audit in accordance with International Standards on Auditing as adopted for Luxembourg by the“Commission de Surveillance du Secteur Financier”. Those standards require that we comply with ethicalrequirements and plan and perform the audit to obtain reasonable assurance about whether the annualaccounts are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures inthe annual accounts. The procedures selected depend on the judgment of the “réviseur d’entreprisesagréé”, including the assessment of the risks of material misstatement of the annual accounts, whetherdue to fraud or error. In making those risk assessments, the “réviseur d’entreprises agréé” considersinternal control relevant to the entity’s preparation and fair presentation of the annual accounts in order todesign audit procedures that are appropriate in the circumstances, but not for the purpose of expressingan opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating theappropriateness of accounting policies used and the reasonableness of accounting estimates made bythe Board of Directors, as well as evaluating the overall presentation of the annual accounts.

4

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour audit opinion.

Opinion

In our opinion, the annual accounts give a true and fair view of the financial position of GIM UK LoansS.A. as of 31 December 2016, and of the results of its operations for the period from 9 December 2015(date of incorporation) to 31 December 2016 in accordance with Luxembourg legal and regulatoryrequirements relating to the preparation and presentation of the annual accounts.

Report on other legal and regulatory requirements

The management report, which is the responsibility of the Board of Directors is consistent with theannual accounts and has been prepared in accordance with applicable legal requirements.

The corporate governance statement, which is included in the management report, contains theinformation required by the law with respect to the corporate governance statement.

Ernst & YoungSociété anonyme

Cabinet de révision agréé

Oliver CLOESS

Luxembourg, 2 June 2017

GIM UK Loans S.A.

5

Directors’ report

For the period ended December 31, 2016 The Board of Directors present the annual audited accounts for the period ended December 31, 2016. Statement of the Board of Directors' responsibilities The Board of Directors of the Company reaffirms their responsibility to ensure the maintenance of proper accounting records disclosing the financial position of the Company with reasonable accuracy at any time, and ensuring that an appropriate system of internal controls is in place to ensure the Company’s business operations are carried out efficiently and transparently. In accordance with the directive 2004/109/EC of the European Parliament and of the council of December 15, 2004 on the harmonisation of transparency requirements in relation to information about issuers whose securities are admitted to trading on a regulated market and amending directive 2001/34/EC (the "Transparency Directive"), the Company shall make public its annual financial report at the latest four months after the end of each financial year and shall ensure that it remains publicly available. This Transparency Directive establishes requirements in relation to the disclosure of periodic and ongoing information about issuers whose securities are admitted to trading on a regulated market situated or operating within EU member state. However, the Company is exempted from the reporting obligation as the minimum denomination of the notes issued and admitted to trading on the regulated market exceeds EUR 100,000, in line with an article 7 (b) of the Transparency Directive. We declare that, to the best of our knowledge, the Annual Accounts for the year ended 31 December 2016: (i) has been prepared in accordance with Luxembourg legal and regulatory requirements relating to the preparation and

presentation of the Annual Accounts;

(ii) give a true and fair view of the assets, liabilities, financial position and result for the year then ended.

In addition, the Directors’ report includes a fair review of the development and performance of the Company’s operations during the year and of the business risks, where appropriate, faced by the Company. Activities and review of the development of the business GIM UK Loans S.A. (the "Company") is a Luxembourg company, incorporated on December 9, 2015, for an unlimited period, as a «société anonyme» and subject to the law of 22 March 2004 on Securitisation (the "Securitisation Law"), as subsequently amended. The Company's principal activity is that of an acquisition and funding vehicle within the meaning of the Securitisation Law. The state of affairs of the Company at the closing of the financial year is adequately presented in the Balance Sheet and the Profit and Loss Account as published herewithin. In December 2015 the Company entered into certain agreements with BNP Paribas Securities Services Luxembourg S.A. for the performance of the day-to-day administrative activities. In December 2015 the Company entered also into an Investment Management Agreement with Ares Management Limited (“Investment Manager”) for the acquisition and administration of an portfolio of performing senior secured loans. During December 2015 the company has issued 2,050 Profit Participation Notes with a nominal value of EUR 200,000 each amounting to a total of EUR 410,000,000, entirely subscribed by institutional investors, to finance the acquisition of the above mentioned portfolio of senior secured loans, granted to fifteen different borrowers mainly located in the UK. Since the completion date of the loans portfolio acquisition, the Company implemented a currency hedging strategy for the loans denominated in currencies other than EURO. The Investment Manager is responsible for the continuous monitoring of the performance of the underlying portfolio on quarterly basis. As of December 31, 2016, based on Investment Manager’s analysis and in the opinion of the Board of Directors, all outstanding loans are performing as expected. Since the acquisition of the loan portfolio, the Company distributed to the Noteholders a total amount of EUR 138,719,250, out of which EUR 16,319,250 as profits and EUR 122,400,000 as capital repayment (due to both the contractual amortization of the loans and early repayments). The Company did not make any profit or loss during the period ended on December 31, 2016. Company future developments The Company acquired a loan portfolio which is managed by the Investment Manager until full repayments of the loans. The Company will operate in the future on similar basis.

GIM UK Loans S.A.

6

Directors’ report

For the period ended December 31, 2016 (continued)

Activities and review of the development of the business (continued) Research and development During the period ended 31 December 2016, the Company did not exercise any research and development activity, neither had a branch, nor did it acquire its own shares.

Principal risks and uncertainties The principal risks and uncertainties facing the Company relate to the other loans purchased. The Company has exposure to the following risks from its use of financial instruments and does not have any externally imposed capital requirements, except those of the Luxembourg commercial law on subscribed capital. Risk management objectives and policies and exposure to risk Credit risk

Credit risk is the risk of the financial loss to the Company if the counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from the Company’s loan portfolio. The Company’s principal financial assets are cash at bank and in hand, and other loans, which represent the Company’s maximum exposure to credit risk in relation to other loans.

The Company limits its exposure to credit risk by issuing limited recourse debt instruments. The credit risk on these principal financial assets is therefore ultimately borne by the holders of the issued limited recourse debt instruments (the "Noteholders") in accordance with their respective agreements.

Liquidity risk Liquidity risk is the risk that the Company will encounter difficulties in meeting obligations arising from its financial liabilities as they fall due. The Company’s obligation to the Noteholders is limited to the net proceed received from other loans in terms of principal and interest payments. Any deficit will ultimately be borne by the Noteholders of the issued limited recourse debt instruments. Foreign currency risk Currency risk is the risk which arises due to the assets and liabilities of the Company held in foreign currencies, which will be affected by fluctuations in foreign exchange rates. The Company is exposed to movement in exchange rates between Euro (''EUR''), its presentation currency, and British Pound (GBP) and Japanese Yen (JPY). The Company limits its exposure to currency risk by entering into Forward Exchange Agreements with BNP Paribas Securities Services, London Branch, in order to hedge its currency risk. Thus the Company does not face any major currency risk. Interest rate risk Interest rate risk is the risk that the Company does not receive adequate interests from the loans and dividends from the investments to secure interest payments on the Notes. The Company is not exposed to any interest risk as any deficit will ultimately be borne by the Noteholders of the issued limited recourse debt instruments.

GIM UK Loans S.A.

7

Directors’ report

For the period ended December 31, 2016 (continued)

Corporate Governance Statement The Company is subject to and complies with the law of 10 August 1915, as subsequently amended, on commercial companies and Listing Rules of the Irish Stock Exchange. The Company does not apply additional requirements in addition to those required by the above. All service providers engaged by the Company are subject to their own corporate governance requirements. Financial Reporting Process The Board of Directors (the "Board”) is responsible for establishing and maintaining adequate internal control and risk management systems of the Company in relation to the financial reporting process. Such systems are designed to manage rather than eliminate the risk of failure to achieve the Company’s financial reporting objectives and can only provide reasonable and not absolute assurance against material misstatement or loss. The Board has established processes regarding internal control and risk management systems to ensure its effective oversight of the financial reporting process. These include appointing the Corporate Administrator, BNP Paribas Securities Services Luxembourg S.A., to maintain the accounting records of the Company independently of the Paying Agent and the Custodian. The Corporate Administrator is contractually obliged to maintain proper books and records as required by the Corporate Administration agreement. To that end the Corporate Administrator performs reconciliations of its records to those of the Custodian. The Corporate Administrator is also contractually obliged to prepare for review and approval by the Board the Annual Accounts providing a true and fair view of the financial situation. The administrator is a Professional of the financial sector (PFS) and supervised as such by the CSSF. The Board evaluates and discusses significant accounting and reporting issues as the need arises. From time to time the Board also examines and evaluates the independent auditors’ performance, qualifications and independence. The Corporate Administrator has operating responsibility for internal control in relation to the financial reporting process and the Corporate Administrator’s report to the Board. Risk Assessment The Board is responsible for assessing the risk of irregularities whether caused by fraud or error in financial reporting and ensuring the processes are in place for the timely identification of internal and external matters with a potential effect on financial reporting. The Board has also put in place processes to identify changes in accounting rules and recommendations and to ensure that these changes are accurately reflected in the Company’s Annual Accounts. Control Activities The Board of Directors of the Company is responsible to ensure an appropriate system of internal controls is in place to ensure maintenance of proper accounting records and efficient and effective operations of the business. To achieve these objectives, Corporate Administrator has been contractually obliged to design and maintain control structures to manage the risks which are significant for internal control over financial reporting. These control structures include appropriate segregation of responsibilities and specific control activities aimed at detecting or preventing the risk of significant deficiencies in financial reporting for the Annual Accounts and the related notes to the Annual Accounts. Moreover the Investment Manager is contractually obliged to design and maintain control structures to monitor the credit risks in relation to loan portfolio. Monitoring The Board has an annual process to ensure that appropriate measures are taken to consider and address the shortcomings identified and measures recommended by the independent auditors. Given the contractual obligations of the Corporate Administrator, the Board has concluded that there is currently no need for the Company to have a separate internal audit function in order for the Board to perform effective monitoring and oversight of the internal control and risk management systems of the Company in relation to the financial reporting process. Capital Structure No person has a significant direct or indirect holding of shares in the Company. No person has any special rights of control over the Company’s share capital. With regard to the appointment and replacement of Directors, the Company is governed by its Articles of Association, and the law of 10 August 1915 on commercial companies, as subsequently amended. The Articles of Association themselves may be amended by special resolution of the shareholders.

GIM UK Loans S.A.

8

Directors’ report

For the period ended December 31, 2016 (continued)

Corporate Governance Statement (continued) Powers of Directors The Board is responsible for managing the business affairs of the Company in accordance with the Articles of Association. The Directors may delegate certain functions to other parties, subject to the supervision and direction by the Directors. Audit Committee Based on Article 20 of the Law of July 23, 2016, the Company is classified as public-interest entity and required to establish an audit committee. However, the Company's sole business is to act as issuer of asset-backed securities as defined in Article 52 5(c) Therefore, it is exempted from the audit committee obligation. The Company has concluded that the establishment of a dedicated audit committee is neither necessary nor appropriate for the nature and extend of the Company's business. The Board as a whole assumes these functions in order to ensure a proper governance of financial reporting, internal control and audit process.

June 2, 2017 The Board of Directors

Annual Accounts Helpdesk : RCSL Nr. : B 202528 Matricule :

Tel. : (+352) 247 88 494

Email : [email protected] BALANCE SHEET

Financial period from 01 09/12/2015 to 02 31/12/2016 (in 03 EUR )

GIM UK Loans S.A.60, avenue John F. KennedyL-1855 Luxembourg

ASSETS

Reference(s) Current period Previous year

A. Subscribed capital unpaid 1101 101 - 102 -

I. Subscribed capital not called 1103 103 - 104 -

II. Subscribed capital called but unpaid 1105 105 - 106 -

B. Formation expenses 1107 3 107 321 846 108 -

C. Fixed assets 1109 109 218 146 396 110 -

I. Intangible assets 1111 111 - 112 -1. Cost of development 1113 113 - 114 -2. Concessions, patents, licences, trade marks and similar rights and

assets, if they were 1115 115 - 116 -

a) acquired for valuable consideration and need not be shown under C.I.3 1117 117 - 118 -

b) created by the undertaking itself 1119 119 - 120 -3. Goodwill, to the extent that it was acquired for valuable

consideration 1121 121 - 122 -4. Payments on account and intangible fixed assets under

development 1123 123 - 124 -

II. Tangible assets 1125 125 - 126 -

1. Land and buildings 1127 127 - 128 -

2. Plant and machinery 1129 129 - 130 -

3. Other fixtures and fittings, tools and equipment 1131 131 - 132 -4. Payments on account and tangible assets in the course of

construction 1133 133 - 134 -

III. Financial assets 1135 135 218 146 396 136 -

1. Shares in affiliated undertakings 1137 137 - 138 -

2. Loans to affiliated undertakings 1139 139 - 140 -

3. Participating interests 1141 141 142 -4. Loans to undertakings with which the undertaking is linked by

virtue of participating interests 1143 143 - 144 -

5. Investments held as fixed assets 1145 145 - 146 -

6. Other loans 1147 4 147 218 146 396 148 -

D. Current assets 1151 151 83 160 785 152 -

I. Stocks 1153 153 - 154 -

1. Raw materials and consumables 1155 155 - 156 -

2. Work in progress 1157 157 - 158 -

3. Finished goods and goods for resale 1159 159 - 160 -

4. Payments on account 1161 161 - 162 -

II. Debtors 1163 163 1 081 603 164 -

1. Trade debtors 1165 165 - 166 -

a) becoming due and payable within one year 1167 167 - 168 -

b) becoming due and payable after more than one year 1169 169 - 170 -

2. Amounts owed by affiliated undertakings 1171 171 - 172 -

a) becoming due and payable within one year 1173 173 - 174 -

b) becoming due and payable after more than one year 1175 175 - 176 -3. Amounts owed by undertakings with which the undertaking is

linked by virtue of participating interests 1177 177 - 178 -

a) becoming due and payable within one year 1179 179 - 180 -

b) becoming due and payable after more than one year 1181 181 - 182 -

4. Other debtors 1183 183 - 184 -

a) becoming due and payable within one year 1185 5 185 1 081 603 186 -

b) becoming due and payable after more than one year 1187 187 - 188 -

III. Investments 1189 189 - 190 -

1. Shares in affiliated undertakings 1191 191 - 192 -

2. Own shares 1209 209 - 210 -

3. Other investments 1195 195 - 196 -

IV. Cash at bank and in hand 1197 197 82 079 182 198 -

E. Prepayments 1199 199 - 200 -

TOTAL (ASSETS) 201 301 629 027 202 -

9The accompanying notes form an integral part of these annual accounts

RCSL Nr. : B 202528 Matricule :

CAPITAL, RESERVES AND LIABILITIES

A. Capital and reserves 1301 301 31 000 302 -

I. Subscribed capital 1303 6 303 31 000 304 -

II. Share premium account 1305 305 - 306 -

III. Revaluation reserves 1307 307 - 308 -

IV. Reserves 1309 309 - 310 -

1. Legal reserve 1311 311 - 312 -

2. Reserve for own shares 1313 313 - 314 -

3. Reserves provided for by the articles of association 1315 315 - 316 -

4. Other reserves, including the fair value reserve 1429 429 - 430 -

a) other available reserves 1431 431 - 432 -

b) other non available reserves 1433 433 - 434 -

V. Profit or loss brought forward 1319 319 - 320 -

VI. Profit or loss for the financial period 1321 321 - 322 -

VII. Interim dividends 1323 323 - 324 -

VIII. Capital investment subsidies 1325 325 - 326 -

B. Provisions 1331 331 161 436 332 -1. Provisions for pensions and similar obligations 1333 333 - 334 -

2. Provisions for taxation 1335 335 - 336 -

2. Other provisions 1337 337 161 436 338 -

C. Creditors 1435 435 301 436 591 436 -1. Debenture loans 1437 437 285 781 122 438 -

a) Convertible loans 1439 439 - 440

i) becoming due and payable within one year 1441 441 - 442 -

ii) becoming due and payable after more than one year 1443 443 - 444 -

b) Non convertible loans 1445 8 445 285 781 122 446 -

i) becoming due and payable within one year 1447 447 - 448 -

ii) becoming due and payable after more than one year 1449 449 285 781 122 450 -

2. Amounts owed to credit institutions 1355 9 355 15 152 900 356 -

a) becoming due and payable within one year 1357 357 15 152 900 358 -

b) becoming due and payable after more than one year 1359 359 - 360 -3. Payments received on account of orders in so far as they are not

shown separately as deductions from stocks 1361 361 - 362 -

a) becoming due and payable within one year 1363 363 - 364 -

b) becoming due and payable after more than one year 1365 365 - 366 -

4. Trade creditors 1367 10 367 466 808 368 -

a) becoming due and payable within one year 1369 369 466 808 370 -

b) becoming due and payable after more than one year 1371 371 - 372 -

5. Bills of exchange payable 1373 373 - 374 -

a) becoming due and payable within one year 1375 375 - 376 -

b) becoming due and payable after more than one year 1377 377 - 378 -

6. Amounts owed to affiliated undertakings 1379 379 - 380 -

a) becoming due and payable within one year 1381 381 - 382 -

b) becoming due and payable after more than one year 1383 383 - 384 -7. Amounts owed to undertakings with which the undertaking is

linked by virtue of participating interests 1385 385 - 386 -

a) becoming due and payable within one year 1387 387 - 388 -

b) becoming due and payable after more than one year 1389 389 - 390 -

8. Other creditors 1451 451 35 761 452 -

a) Tax authorities 1393 393 35 761 394 -

b) Social security authorities 1395 395 - 396 -

c) Other creditors 1397 397 - 398 -

i) becoming due and payable within one year 1399 399 400 -

ii) becoming due and payable after more than one year 1401 401 402 -

E. Deferred income 1403 403 - 404 -

TOTAL (CAPITAL, RESERVE AND LIABILITIES) 405 301 629 027 406 -

10The accompanying notes form an integral part of these annual accounts

Annual Accounts Helpdesk : RCSL Nr. : B 202528 Matricule :

Tel. : (+352) 247 88 494

Email : [email protected] PROFIT AND LOSS ACCOUNT

Financial period from 01 09/12/2015 to 02 31/12/2016 (in 03 EUR )

GIM UK Loans S.A.60, avenue John F. KennedyL-1855 Luxembourg

PROFIT AND LOSS ACCOUNT

Reference(s) Current period Previous year

1. Net turnover 1701 701 - 702 -

2. Variation in stocks of finished goods and in work in progress 1703 703 - 704 -

3. Work performed by undertaking for its own purposes and capitalised 1705 705 - 706 -

4. Other operating income 1713 11 713 1 961 690 714 -

5. Raw materials and consumables and other external expenses 1671 671 (2 633 925) 672 -a) Raw materials and consumables 1601 601 - 602 -

b) Other external expenses 1603 12 603 (2 633 925) 604 -

6. Staff costs 1605 605 606 -a) Wages and salaries 1607 607 - 608 -

b) Social security costs 1609 609 - 610 -

i) relating to pensions 1653 653 - 654 -

ii) Other social securities costs 1655 655 - 656 -

c) Other staff cots 1613 613 - 614 -

7. Value adjustments 1657 657 (80 461) 658 -a) in respect of formation expenses and of tangible and intangible fixed assets 1659 659 (80 461) 660 -

b) in respct of current assets 1661 661 - 662

8. Other operating expenses 1621 621 - 622 -

9. Income from participating interests 1715 715 - 716 -a) derived from affiliated undertakings 1717 717 - 718 -

b) other income from participating interests 1719 719 - 720 -

10.1721 721 20 672 118 722 -

a) derived from affiliated undertakings 1723 723 - 724 -

b) other income not included under a) 13 723 20 672 118 724 -

11. Other interest receivable and similar income 1727 727 47 054 898 728 -a) derived from affiliated undertakings 1729 729 - 730 -

b) other interest and similar income 1731 14 731 47 054 898 732 -

12.1663 663 - 664 -

13.1665 665 - 666 -

14. Interest payable and similar expenses 1627 627 (66 970 121) 628 -a) concerning affiliated undertakings 1629 629 - 630 -

b) other interest and similar expenses 1631 15 631 (66 970 121) 632 -

15. Tax on profit or loss 1635 635 - 636 -

16. Profit or loss after taxation 1667 667 4 199 668 -

17. Other taxes not shown under items 1 to 16 1637 16 637 (4 199) 638 -

18. Profit for the financial period/year 1669 669 - 670 -

11

Income from other investments and loans forming part of thefixed assets

The accompanying notes form an integral part of these annual accounts

Share of profit or loss of undertakings accounted for under theequity method

Value adjustments in respect of financial assets and ofinvestments held as current assets

GIM UK Loans S.A.

12

Notes to the Annual Accounts as at December 31, 2016

Note 1. General comments

GIM UK Loans S.A. (the “Company”) was incorporated on December 9, 2015 in the form of a Société Anonyme de Titrisation which is governed by the laws of the Grand Duchy of Luxembourg, especially by the law of August 10, 1915 on commercial companies, as amended and, by the law of March 22, 2004 on securitisation companies. Its registered office is established at 60 avenue John F. Kennedy, L-1855 Luxembourg, Grand Duchy of Luxembourg and is registered at the Luxembourg Commercial Register under number Luxembourg B202528. The Company is incorporated for an unlimited duration.

The exclusive purpose of the Company is to enter into one or more securitisation transactions within the meaning of the Securitisation Law and the Company may, in this context, assume risks, existing or future, relating to the holding of assets, whether movable or immovable, tangible or intangible, as well as risks resulting from the obligations assumed by third parties or relating to all or part of the activities of third parties, in one or more transactions or on a continuous basis. The Company may assume those risks by acquiring the assets, guaranteeing the obligations or by committing itself in any other way. It may also, to the extent permitted by law and these articles of association, transfer or dispose of the claims and other assets it holds, whether existing or future, in one or more transactions or on a continuous basis. The acquisition or assumption of such risks by the Company will be financed by the issuance of securities (valeurs mobilières) by itself or by another securitisation entity, the value or return of which depend on the risks acquired or assumed by the Company. The Company will not be able to issue securities to the public on a continuous basis. Without prejudice to the generality of the foregoing, the Company may in particular issue any notes, bonds, certificates, warrants, and generally securities and financial instruments howsoever described the return or value of which shall depend on the risks acquired or assumed by the Company.

The Company may, in this same context, acquire, dispose and invest in loans, stocks, bonds, debentures, obligations, notes, advances, shares, warrants and other securities. The Company may, within the limits of the Securitisation Law, and in favor of its creditors only, grant pledges, other guarantees or security interests of any kind to Luxembourg or foreign entities and enter into securities lending activity on an ancillary basis.

In the context of its securitisation activities, the Company may, on an exceptional and limited basis, incur indebtedness for borrowed money, including through leverage facilities or other credit arrangement with one or more banks or other lenders within the limits of the Securitisation Law.

The Company may perform all transactions which are necessary or useful to fulfil and develop its purpose, as well as, all operations connected directly or indirectly to facilitating the accomplishment of its purpose in all areas described above, provided that the Company shall only perform activities permissible under the ECB Regulation concerning statistics on the assets and liabilities of financial vehicle corporations engaged in securitisation transactions (ECB/2013/40). The assets of the Company may only be assigned in accordance with the terms of the securities issued to finance the acquisition of such assets.

As at January 1, 2016 the Company address moved from 33, rue de Gasperich, L5826 Hesperange to 60, avenue J.F. Kennedy, L1855 Luxembourg.

The Company's financial year starts on the first of January and ends on the thirty-first of December of each year. The first financial year shall begin on the date of incorporation of the Company and terminate on December 31, 2016.

Note 2. Principal accounting policies and measurement basis

2.1. Basis of preparation

The Annual Accounts have been prepared in accordance with Luxembourg legal and regulatory requirements. The annual accounts are established in accordance with Luxembourg legal and regulatory requirements under the historical cost convention. The Annual Accounts of the Company are prepared under the provisions of the laws of 19 December 2002 as subsequently amended (the "Accounting Law") and the requirements of the Luxembourg commercial law dated 10 August 1915, as subsequently amended. Accounting policies and valuation rules are, besides the ones laid down by the Accounting Law, determined and applied by the Board of Directors.

GIM UK Loans S.A.

13

Notes to the Annual Accounts as at December 31, 2016 (continued) Note 2. Principal accounting methods and measurement basis (continued)

2.2. Principal valuation rules

The following are the principal valuation rules, in compliance with the principles described above:

Currency conversion

The accounts are expressed in Euro (“EUR”).

At the balance sheet date, the current assets and current liabilities denominated in currencies other than EUR are converted at the exchange rate at the end of the financial period. The unrealised exchange losses are recorded in the profit and loss account. The realised exchange gains and losses are recorded in the profit and loss account at the moment of their realisation.

Income and charges denominated in currencies other than EUR are translated at rates of exchange prevailing at the date of the relevant transaction. Financial assets and liabilities are translated at the exchange rate effective at the balance sheet date. Exchange losses and gains are recorded in the profit and loss account of the period. Other assets and liabilities are translated separately, respectively, at the lower or at higher of the value converted at the historic exchange rates, or the value determined on the basis of exchange rates effective at the Balance Sheet date. The realised and unrealised exchange losses are recorded in the Profit or Loss Account. Only realised exchange gains recorded in the Profit or Loss Account.

Financial fixed assets Other loans are initially recorded at purchase price. In the case of durable depreciation in value according to the opinion of the Board of Directors, value adjustments are made in respect of financial fixed assets, so that they are valued at the lower figure to be attributed to them at the balance sheet date. These value adjustments are not continued if the reasons for which the value adjustments were made have ceased to apply.

Formation expenses The formation expenses are written off on a straight-line basis over a period of 5 years.

Debtors Debtors are valued at their nominal value. They are subject to value adjustments where their recovery is compromised. These value adjustments are not continued if the reasons for which the value adjustments were made have ceased to apply.

Provisions Provisions are intended to cover losses or debts, the nature of which is clearly defined and which, at the date of the balance sheet, are either likely to be incurred or certain to be incurred but uncertain as to their amount or as to the date on which they will arise. Non convertible loans Non convertible loans are recognised at their repayable amount. The repayable amount of non convertible loans are subject to fluctuations in value calculated (i) based on fair value changes of the financial assets; (ii) based on realised results on disposals; (iii) based on all the fees attributable to these non convertible loans; and (iv) based on any foreign exchange impact attributable to the cash at bank and in hand. Any diminution in value will be credited to the Profit and Loss Account as an equalisation adjustment under the caption "Other operating income" and any increase in value will be recorded under the caption "Other operating expenses". On the applicable maturity or payment date, the profit will be provided to noteholders as profit participating rights as calculated by the paying agent.

GIM UK Loans S.A.

14

Notes to the Annual Accounts as at December 31, 2016 (continued)

Note 2. Principal accounting methods and measurement basis (continued)

2.2. Principal valuation rules (continued)

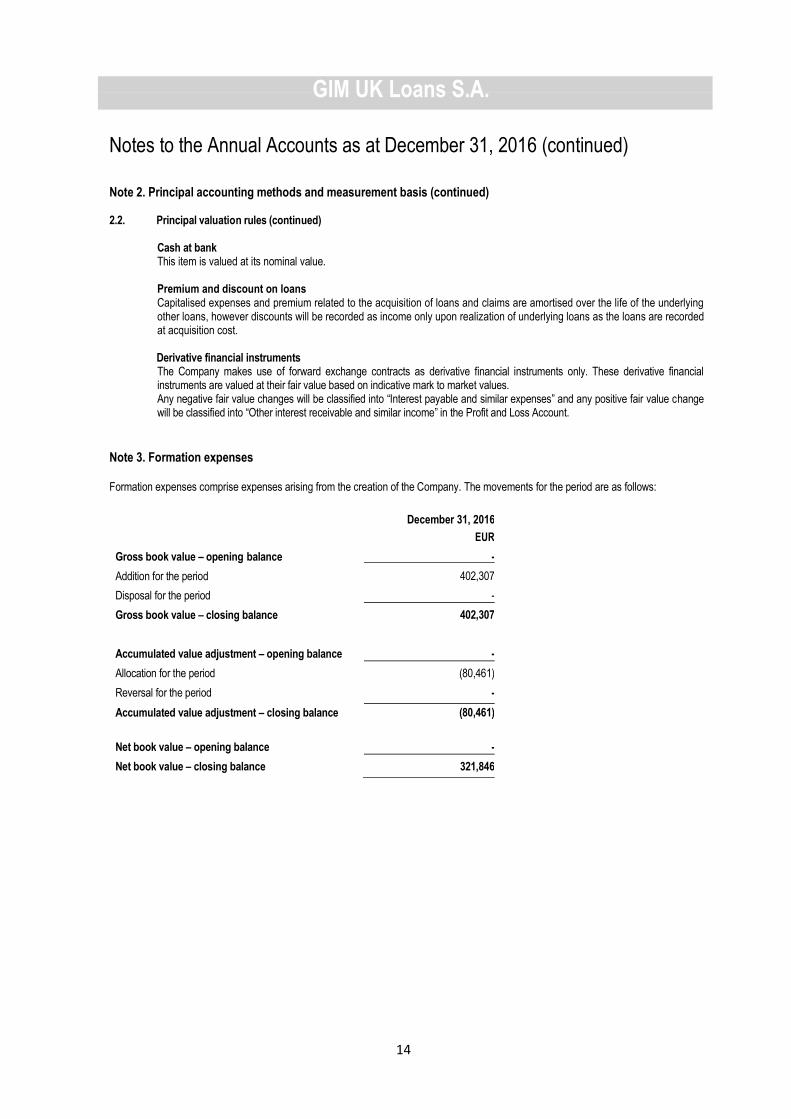

Cash at bank This item is valued at its nominal value. Premium and discount on loans Capitalised expenses and premium related to the acquisition of loans and claims are amortised over the life of the underlying other loans, however discounts will be recorded as income only upon realization of underlying loans as the loans are recorded at acquisition cost.

Derivative financial instruments The Company makes use of forward exchange contracts as derivative financial instruments only. These derivative financial instruments are valued at their fair value based on indicative mark to market values. Any negative fair value changes will be classified into “Interest payable and similar expenses” and any positive fair value change will be classified into “Other interest receivable and similar income” in the Profit and Loss Account.

Note 3. Formation expenses

Formation expenses comprise expenses arising from the creation of the Company. The movements for the period are as follows:

December 31, 2016 December 31, 2015

EUR USD

Gross book value – opening balance - 18,557,721

Addition for the period 402,307 1,146,050

Disposal for the period -

Gross book value – closing balance 402,307

Accumulated value adjustment – opening balance -

Allocation for the period (80,461)

Reversal for the period -

Accumulated value adjustment – closing balance (80,461) )

Net book value – opening balance -

Net book value – closing balance 321,846

GIM UK Loans S.A.

15

Notes to the Annual Accounts as at December 31, 2016 (continued)

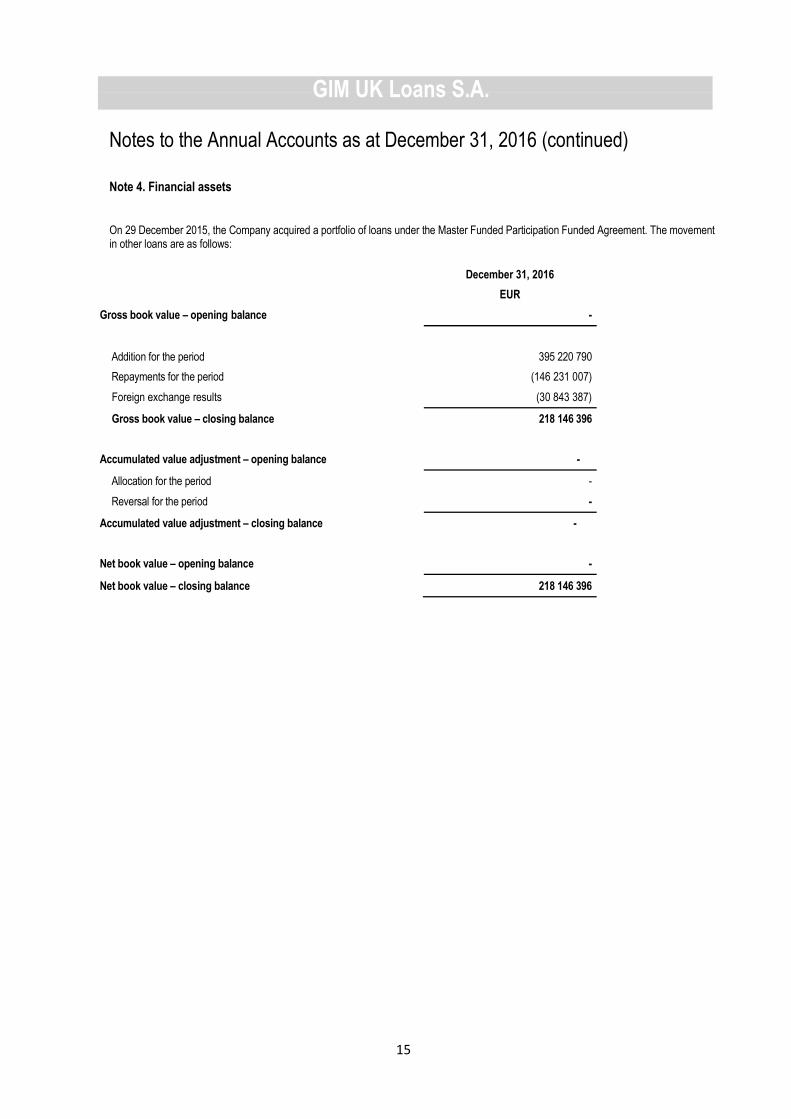

Note 4. Financial assets

On 29 December 2015, the Company acquired a portfolio of loans under the Master Funded Participation Funded Agreement. The movement in other loans are as follows:

December 31, 2016

EUR

Gross book value – opening balance -

Addition for the period 395 220 790

Repayments for the period (146 231 007)

Foreign exchange results (30 843 387)

Gross book value – closing balance 218 146 396

Accumulated value adjustment – opening balance -

Allocation for the period -

Reversal for the period -

Accumulated value adjustment – closing balance -

Net book value – opening balance -

Net book value – closing balance 218 146 396

GIM UK Loans S.A.

16

Notes to the Annual Accounts as at December 31, 2016 (continued)

Note 5. Other debtors becoming due and payable within one year

The details of debtors are as follows:

December 31, 2016 December 31, 2015

EUR USD

Interest accruals on loans 938,791 18,557,721

Other receivable 142,812 1,146,050

1,081,603 19,703,771

Note 6. Subscribed capital

The subscribed and fully paid-up capital of EUR 31,000 is represented by 31,000 ordinary shares with a par value of EUR 1 each.

Number of ordinary shares

December 31, 2015

Subscribed capital-opening balance -

Subscriptions for the period 31,000

Redemptions for the period -

Subscribed capital-closing balance 31,000

Note 7. Legal reserve

Under Luxembourg law, the company is obliged to transfer to a legal reserve 5% of its net profit each year until the reserve reaches 10% of the issued share capital. This reserve is not available for distribution.

During the period ended December 31, 2016, no allocation will be made to the legal reserve.

Note 8. Non - Convertible loans

As at December 31, 2016 the subscribed and fully paid issued Profit Participating Notes are amounting to EUR 287.600.000. Here below the movement during the period then ended December 31, 2016:

Gross book value – opening balance - Nominal value issued during the period 410,000,000 Less: redemption of notes (122,400,000)

Gross book value 287,600,000 Accumulated equalization provision - Addition during the period (1,818,878)

Gross book value – closing balance 285,781,122

The Notes, regardless of their date of issuance, shall have a maturity of seven (7) years starting on the date of the initial issuance of Notes (the “Maturity Date”). The Noteholders are entitled to receive a participation in the accrued and realised proceeds resulting from assets of the Company, after deduction of the expenses and retained Profit Amounts (the “Net Profits”) on the applicable Maturity Date or Payment Date.

GIM UK Loans S.A.

17

Notes to the Annual Accounts as at December 31, 2016 (continued)

Note 9. Amounts owed to credit institutions becoming due and payable within one year Amounts owed to credit institutions comprise of amount payable to BNP Paribas Securities Services, London Branch. This amount has been subsequently paid on January 4, 2017.

Note 10. Trade creditors becoming due and payable within one year

Non subordinated debts correspond to creditors as detailed below:

December 31, 2016 December 31, 2015

EUR USD

Management fees 338,062 18,557,721

Loan Administration fees 35,000 1,146,050

Accounting fees 28,246

Professional fees 3,000

Transfer agent fees 2,500

Audit fees 60,000

466,808 19,703,771

Note 11. Other operating income

December 31, 2016 December 31, 2015

EUR USD

Equalisation adjustment (note 8)

1,818,878 18,557,721

Other sundry income 142,812 1,146,050

1,961,690 19,703,771

Note 12. Other external expenses

December 31, 2016 December 31, 2015

EUR USD

Management fees 1,633,216 18,557,721

Loan Administration fees 73,144 1,146,050

Accounting fees 28,950

Transfer agent fees 10,000

Operating fees 386,172

Administration fees 49,795

Audit 60,000

Professional fees 3,000

Register fees 11,690

Transfer fee

372,532

Bank interest 1,304

Other expenses 4,122

2,633,925 19,703,771

GIM UK Loans S.A.

18

Notes to the Annual Accounts as at December 31, 2016 (continued) Note 12. Other external expenses (continued) Audit fees

No fees have been paid to the Company’s independent auditors during the period ended on December 31, 2016, however the provided audit fees will be paid subsequent to the period end December 31, 2016. Further the statutory auditor of the Company also provided corporate tax and VAT compliance services for a total fees of EUR 7,000.

Note 13. Income from other investments and loans forming part of the fixed assets

December 31, 2016 December 31, 2015

EUR USD

Interest income from financial assets

16,749,022 18,557,721

Realised portion of discount on loans portfolio 3,923,096 1,146,050

20,672,118 19,703,771

Note 14. Other interest receivable and similar income

December 31, 2016 December 31, 2015

EUR USD

Realised on forward foreign exchange contracts and spot transactions

46,928,930 18,557,721

Realized exchange profits on loans 125,968

47,054,898 19,703,771

Note 15. Interest payable and similar expenses

December 31, 2016 December 31, 2015

EUR USD

Net unrealised foreign exchange loss on loan portfolio 30,843,387

Realised foreign exchange loss on loan portfolio 12,856,986

Realised exchange loss on forward exchange contracts and spot transactions

3,022,293

Interest on Profit Participating Notes 16,319,250 18,557,721

Other foreign exchange losses 3,766,769 1,146,050

Net unrealised loss on forward exchange (note 17) 161,436

66,970,121 19,703,771

Note 16. Taxation

The Company is subject to all taxes applicable to securitisation companies in Luxembourg.

GIM UK Loans S.A.

19

Notes to the Annual Accounts as at December 31, 2016 (continued)

Note 17. Forward foreign exchange contracts

As of 31 December 2016, the Company entered into the following forward foreign exchange contracts with BNP Paribas, the Swap counterparty:

Purchase Sale Trade date Maturity date Fair value

EUR

EUR 209 177 388 GBP 179 202 268 29-Dec-2016 31-Mar-2017 (256 249)

EUR 15 134 570 JPY 1 851 684 429 29-Dec-2016 31-Mar-2017 94 813

(161 436)

Note 18. Personnel

During the year under review, the Company did not employ any personnel and, consequently, no payments for wages, salaries or social securities were made.

Note 19. Emoluments to be granted to the members of the administrative, managerial and supervisory bodies

No emoluments were granted to members of the Board of Directors and any other bodies during the period ended 31 December 2016.

Note 20. No loans or advances were granted to the management bodies during the year under review.

No loans or advances were granted to the management bodies during the year under review.

Note 21. Subsequent events

There are no material events after the reporting period that need to be reported in these Annual accounts.