gift accounting presentation acso 2014

TRANSCRIPT

“Ask an Expert” Webinar Series

Gift Accounting and Budgets: Bridging the Gap Between

Development & Finance

Michael Costa, Executive Director, Philharmonia Baroque OrchestraKate Akos, Principal, Katherine Akos Consulting

What You Will Learn

1. Basic principles of gift accounting2. How development and finance can

work together

3. Special cases for gift accounting

4. Budgeting Best Practices

Tug of War

Development vs. Finance

It all comes down to…

•Donor intent

•Accuracy matters

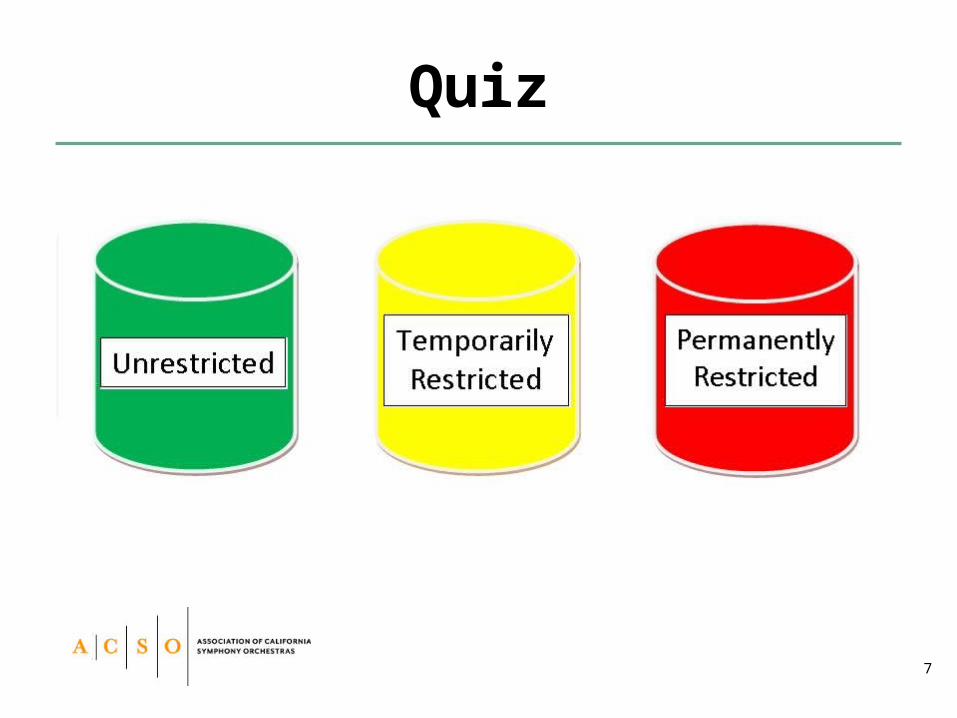

Restrictions, Restrictions

Three asset classes:• Unrestricted• Temporarily restricted• Permanently restricted

Restrictions, Restrictions

• Permanently restricted– Principal cannot be invaded

• Temporarily restricted– Time or purpose restriction

• Unrestricted– No external restriction

Quiz

Endowments

• Donor restricted = permanently restricted

• Board designated = unrestricted Quiz:

$1M Donor restricted endowment$250k = Board designated endowment

Why isn’t the money showing up?

• Matching Principle– match expenses and revenue

• Accrual vs. Cash basis accounting– when revenue earned; when expense incurred

So where is the money?

• Statement of activities (a.k.a. Income statement)

• Statement of Position (a.k.a. Balance sheet)

When Can I Record a Gift?

• Cash

• Pledges + Documentation =

• Multi-year pledges

Getting It Right

• Who receives the gift?• Accurately identifying the gift

– Restrictions / Installments– Coding– Cover sheet

• Regular reconciliation

Gift Acceptance Policies

• Types of gifts accepted• Procedures for review and

acknowledgement• Resource

-http://www.councilofnonprofits.org/nonprofit-gift-acceptance-policy

Budgeting

• Development + Finance• History• Attrition and growth• Litmus test – rationale & strategy

Budgeting (continued)

• Big fish vs. little fish

• Board involvement in planning

• Operating vs. Special Initiatives

Re-Projecting

• New Information

• Major milestone

• Time of year – six months+

Tug of War

Development vs. Finance

A New Paradigm

Fundraising + Finance