georgian economic trends -- 1998 no. 3 - georgian … · · 2013-08-05countries and the european...

TRANSCRIPT

GEORGIAN ECONOMIC TRENDS

GEORGIAN ECONOMIC TRENDS – 1998 NO.3 1

Contents

About Georgian Economic Trends 2 Introductory note 3 1. Summary and Short Economic Report 4 2. National Accounts and Economic Stability 9 3. Government Revenue and Expenditure 17 4. Money and Finance 32 5. Infrastructural Development and Regional News 39 6. International Trade 54 7. Privatisation and Production 67 8. Employment and Social Conditions 90 Calendar of Events 105 Statistical Appendix 113 Abbreviations 129

About Tacis and GEPLAC Georgian Economic Trends is a publication which is now funded by the Tacis Programme through the Georgian-European Policy and Legal Advice Centre. The Tacis Programme is a European Union Initiative for the New Independent States and Mongolia which fosters the development of harmonious and prosperous economic and political links between the European Union and these partner countries. Tacis does this by providing grant finance for know-how to support the process of transformation to market economies and democratic societies. Between 1991 and 1996 Tacis has committed more than ECU 2,807 million. Tacis works closely with its partner countries and provides know-how from a wide range of public and private organisations including advice and training, developing and reforming legal and regulatory frameworks, institutions and organisations, and setting up partnerships, networks, twinnings and pilot projects. Tacis also cultivates links and lasting relationships between organisations in the partner countries and the European Union to promote understanding of democracy and a market-oriented social and economic system. The Georgian-European Policy and Legal Advice Centre (GEPLAC) was established in 1998 by Tacis in order to support economic and legal reform in Georgia. Activities under GEPLAC’s programme include the production of Georgian Economic Trends and of the Georgian Legal Review, and the provision of economic policy and legal advice to the Georgian Government.

This publication is financed by the European Union’s Tacis Programme, which provides grants finance for know-how to foster the development of market economies and democratic societies in the New Independent States and Mongolia.

ABOUT GEORGIAN ECONOMIC TRENDS

2 GEORGIAN ECONOMIC TRENDS – 1998 No.3

This is the ninth quarterly edition of Georgian Economic Trends. GET was established in 1995 and is published in Georgian and English: it aims to provide all those interested in the progress of economic reform in Georgia with a review of developments. This and previous editions are available on the internet at:

www.sanet.ge/geplac/get This edition draws on information from a wide range of government and non-government sources including in particular the State Department for Statistics, the National Bank of Georgia, the United State Social Safety Fund, as well as other Government ministries and departments. Wherever possible every care is taken to ensure that data sources are fully acknowledged since without the full co-operation and support of information providers, including regular consultation, it would not be possible to produce this review. The purpose of GET is to offer an independent analytical account of economic trends drawing on information made publicly available. As part of this work, comments and advice are offered on policy and on the collection and dissemination of economic and other information. These are always intended to support the process of economic reform in Georgia and represent the view of the editors only and do not represent any official view of the European Commission, the Tacis Georgian-European Policy and Legal Advice Centre or the Government of Georgia. Readers may quote any information used provided it is properly acknowledged. For further information please contact Georgian Economic Trends at:

26, Gabriel Episkoposi Street, Tbilisi

Tel: Tbilisi (995 32) 93 91 61 / 77 67 64 Fax: Tbilisi (995 32) 93 91 60 / 77 65 14

e-mail: [email protected]

The following people worked on this edition: Mikheil Abramishvili, Andrew Barnard, Natalia Kakabadze, Daniel Linotte, Nikoloz Loladze, Veronica Schneider, Irakli Tsereteli. Printed by SMArt Ltd. 23, Bochorma St., Tbilisi, Georgia Tel: (995 32) 93 35 73 Mobile: 899 50 69 29 E-mail: [email protected]

INTRODUCTORY NOTE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 3

Distribution policy for GET As a TACIS-funded publication whose purpose is technical assistance, Georgian Economic Trends is written primarily for Georgian policy-makers and international donors of assistance. There are two additional groups of readers: actual and potential investors in Georgia, and people with an academic or personal interest in the Georgian economy. Copies of GET are still distributed free-of-charge to selected Georgian policy-makers and international donors of assistance; this policy is not expected to change. However, financial constraints and increasing demand now prevent us from distributing free copies to other people who want to read GET: unfortunately over the last few quarters we have run so short of copies that with great regret we have had to reject some requests. Therefore we are addressing the problem by introducing charges for printed copies: the idea is that the additional revenue will finance the printing of enough copies for all potential readers. In addition GET will continue to be available free-of-charge via the internet (both as Word documents and in html form) which people can read and from which they are also welcome to print off their own copies. Following last quarter's re-organisation of the chapters, we are continuing to develop GET in response to the needs of all our readers. The main change that we have introduced in this issue concerns our treatment of news about events that affect the Georgian economy. The aim is not only to be a statistical review but also to provide a reasonably up-to-date picture of the Georgian economy at the time of going to press. Therefore the calendar in this issue covers both the 2nd and 3rd Quarters, and the specialist chapters include updates on key events during the 3rd Quarter. (After all, it would have been unsatisfactory to wait until January before discussing the impact on Georgia of the Russian financial crisis.) This change seems to be the best way of making GET reasonably up-to-date while also ensuring that the statistical and economic analysis is as complete as it needs to be.

CHAPTER ONE: SUMMARY AND ECONOMIC REPORT

4 GEORGIAN ECONOMIC TRENDS – 1998 No.3

SUMMARY

• Georgia is now clearly in its "second phase" of economic reform, where macroeconomic stability

has been achieved but structural, institutional and legislative reforms are needed in order to sustain dynamic growth and to underpin Georgia’s application to join the WTO.

• The Georgian economy is continuing to grow strongly (11 per cent real growth per annum since

1996) following the restoration in the mid-1990s of political stability, macroeconomic stabilisation and progressive economic reform. Prices and trade are now largely liberalised, the most significant exception being electricity prices, which were raised to 6 Tetris (about 4.5 US cents) per kWh in 1998 Q3 but which remain well below the level required to cover long-term costs. Georgia’s prospects of joining the WTO in late-1999 look good.

• However, in 1998 the Government has failed to fulfil a number of conditions attached to its

Enhanced Structural Adjustment Facility loan from the IMF: this has put it in a position where it needs to achieve a dramatic improvement in tax revenue collection in the final quarter of 1998 in order to avert a serious budget crisis in the short term.

• The 1998 Q2 fiscal data shows that the Ministry of Finance kept the budget deficit at a

manageably small level (around 2 per cent of GDP) by tying expenditure to revenue. However this was achieved largely by delaying the payments of public sector salaries – accumulating expenditure arrears, in violation of Georgia’s agreements with the IMF. In the longer term the fiscal position seems basically sound, as tax revenue (although well below target) still seems to be rising at a trend rate of 15-20 per cent in real terms.

• External support for stabilisation is still required in order to prevent a spiral of devaluation and

inflation and to enable Georgia to continue to service and reschedule its debts; Georgia's debt to Turkmenistan still needs to be rescheduled.

• Numerous laws have been passed in an effort to develop an effective legal framework, but lack of

transparency (and associated corruption) remains a major problem which is not being tackled effectively. The government is still failing to make the business environment attractive enough to entice many small-scale entrepreneurs out of the shadow economy, and this is continuing to retard the development of small and medium-sized enterprises as well as playing havoc with public finance.

• Nevertheless, the government’s willingness to take account of commercial interests has made the

environment for major foreign investors substantially better than that in most of the former Soviet Union. Although there are few new major investments, there is now evidence of heavy re-investment by companies that have already established commercial operations here.

SUMMARY AND ECONOMIC REPORT

GEORGIAN ECONOMIC TRENDS – 1998 No.3 5

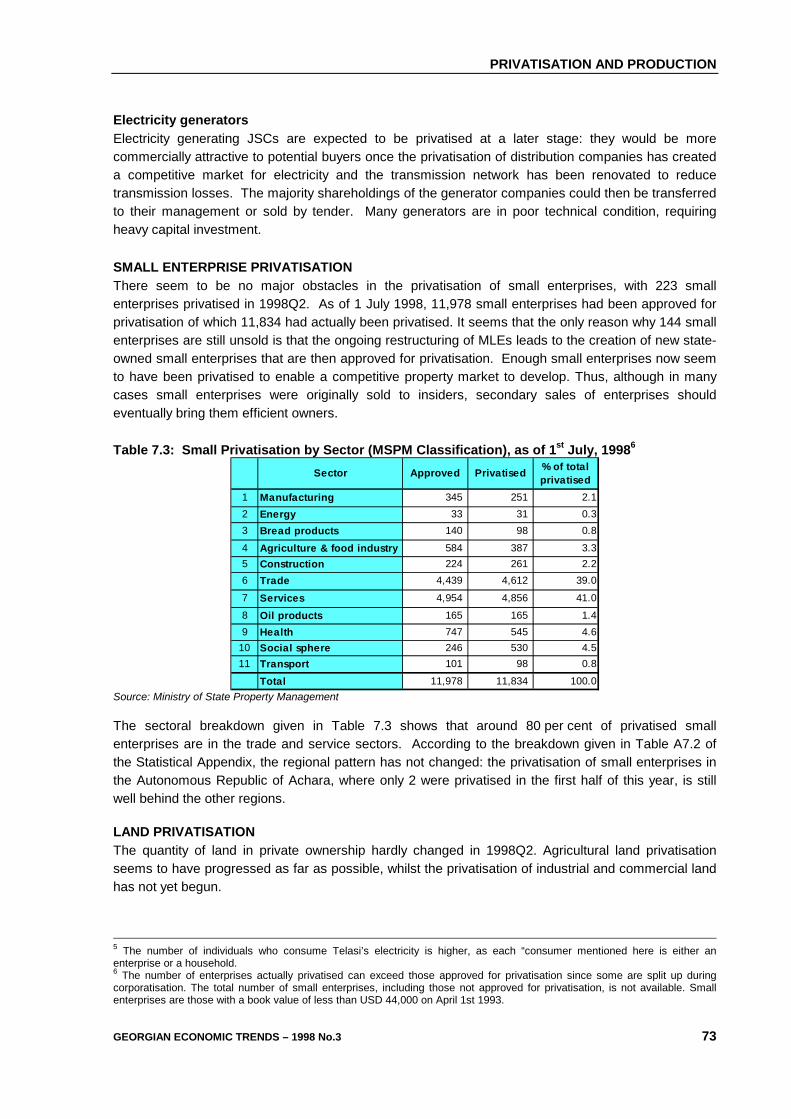

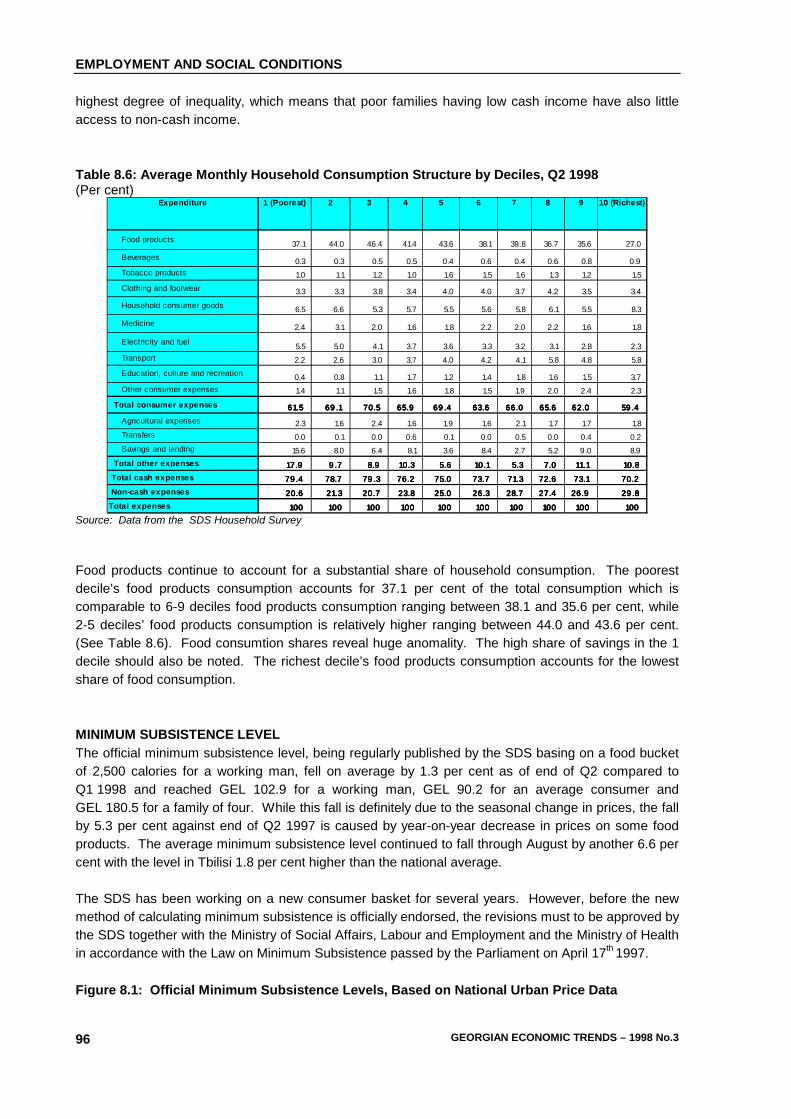

SHORT ECONOMIC REPORT NATIONAL ACCOUNTS AND ECONOMIC STABILITY GDP: Economic growth remains strong, with the Government reporting real growth of 11.4 per cent and 11.3 per cent in 1996 and 1997 respectively. The Government's most recent statistical report puts the first half of 1998's GDP 8.9 per cent higher in real terms than in the first half of 19971. Nevertheless, the underlying trend does not seem to have fallen; the prospects for economic growth remain reasonably good as far as supply-side factors are concerned. TRADE BALANCE: The trade deficit is continuing to widen. According to the Government's recorded trade statistics (which, although far from perfect, seem to be the most accurate source), registered imports in 1997 were USD 931 million compared with only USD 227 million exports. Imports have been increasing at an underlying rate of around 25 per cent a year, whilst exports have shown practically no increase. The statistics for the first half of 1998 tell much the same story, with import growth possibly accelerating. However, the deficit is largely a reflection of the amount of foreign participation in the economy: as in any country, it is normal for foreign investors and visitors to bring in foreign currency which directly or indirectly finances imports. Therefore the performance of Georgia's exports should be of much greater concern than the trade deficit. FOREIGN DIRECT INVESTMENT: Foreign direct investment during 1997 was officially recorded as USD 242 million, which is in line with survey evidence. Whilst there are few new foreign investors in Georgia (only two were registered during the first quarter of 1998), the foreign companies that have already made the biggest investments in Georgia are re-investing heavily. This pattern is basically encouraging for the longer term outlook, as "success stories" are likely to be the most effective way of promoting Georgia as an investment location. In addition the first half of 1998 has seen several foreign companies participating in Georgia's privatisation programme and in several cases committing themselves to significant industrial investments. FOREIGN DEBT: Debt repayments to Turkmenistan remain in arrears, with Georgia unable to find the USD 20 million that Turkmenistan is demanding as quarterly payments. ECONOMIC STABILITY: In the short term, failure to raise enough government revenue could result in serious economic instability. In the longer term the government’s finances look fundamentally sound, as general tax revenue still seems to be increasing at twice the rate of expenditure. GOVERNMENT REVENUE AND EXPENDITURE REVENUE: Tax revenue was 18 per cent below target in 1998 H1 because of shortfalls in the collection of excise duty and VAT revenue. Reports from 1998 Q3 suggest no improvement, with January-August revenue 26 per cent below target. A dramatic increase in revenue collection is required in 1998 Q4, with a commission headed by State Minister Lortkipanidze meeting twice a week to direct efforts to achieve this. EXPENDITURE: As a result of the shortfall in revenue, expenditure plans had to be scaled back in 1998 H1. This was basically achieved through cutbacks in a few major areas: expenditures on administration, health-care and education were all cut (presumably by delaying the payment of public-

1 All these figures remain approximate because of continuing uncertainty about factors such as the quality of data collection and the assumptions about the shadow economy (still officially estimated to be around 40 per cent of GDP).

SUMMARY AND ECONOMIC REPORT

6 GEORGIAN ECONOMIC TRENDS – 1998 No.3

sector salaries). The need to clear the backlog has created major financial problems for the government in the second half of the year. MONEY AND FINANCE EXCHANGE RATE: From a rate of 1.30 GEL/USD in late 1997, the GEL depreciated steadily against the dollar to around 1.35 GEL/USD in June, and remained at that level for most of the summer. The fall in the GEL's value is now understood to reflect the Central Bank’s exchange rate policy of keeping the GEL in an unspecified target range rather than fixing the rate rigidly to the USD. As the GEL (in line with the dollar) has appreciated against most other currencies, the fall against the dollar itself is unlikely to lead to inflation – the world market price of most European and Asian imports has fallen slightly. In September a speculative weekend attack on the GEL pushed its value down to 1.80 per USD, but this was reversed when the financial markets reopened. At the start of October the GEL’s value stood at about 1.36 per USD. INFLATION: The annual inflation rate (CPI compared with 12 months earlier) has fallen back after its recent peak of 7.3 per cent (December 1997) falling to 2.8 per cent in June. Goods price inflation is low, reflecting the stability both of the exchange rate and of world market prices. Services price inflation is higher, reflecting the growth of the economy: it is normal for services to become more expensive when general living standards rise. Fundamentally, this picture is not expected to change significantly unless there is substantial devaluation of the GEL. INTEREST RATES: The Treasury Bills market, which was established in August 1997, continued to develop with Georgian and foreign banks participating in the auctions. The volume of liquidity supplied on the T-Bills market increased significantly thanks to the larger number of participants. However growing uncertainty in August (related to the Russian crisis and also to Georgia’s own fiscal problems) forced the government to scale back its issue of T-Bills; sales seem to have been effectively suspended since mid-September. BANKING: The NBG is continuing to tighten up its regulation of the commercial banks, although the number of banks seems to have stabilised at around 50. 1998 has seen the award of a licence to the Black Sea Bank (in which the EBRD and Bank of Greece both have stakes), and the Turkish bank Emlak Bankasi opened a branch in Tbilisi in March 1998. INFRASTRUCTURE AND REGIONAL DEVELOPMENT INFRASTRUCTURE: The most important event in recent months was the Traceca conference held in Baku in September. The key development was the signature by 12 south-east European and Caspian countries of agreements to develop transport infrastructure and to streamline rules and procedures affecting transit along the “Silk Road” route between Europe and Asia. REGIONAL DEVELOPMENT: Recent studies seem to confirm the impression that the strongest growth is in Tbilisi and the south-east, with the highest levels of registered unemployment in industrial regions. INTERNATIONAL TRADE WTO ACCESSION: In March the first meeting of the working group on Georgia's accession agreed a preliminary scheme of action under which it might be possible for Georgia to accede to the WTO in 1999. The second working group in October 1998 concluded negotiations over trade in services. However Georgia is still pushing for relatively high bound tariffs on a few agricultural products (notably wheat), and there is a small risk that negotiations over these could delay Georgia’s accession. In

SUMMARY AND ECONOMIC REPORT

GEORGIAN ECONOMIC TRENDS – 1998 No.3 7

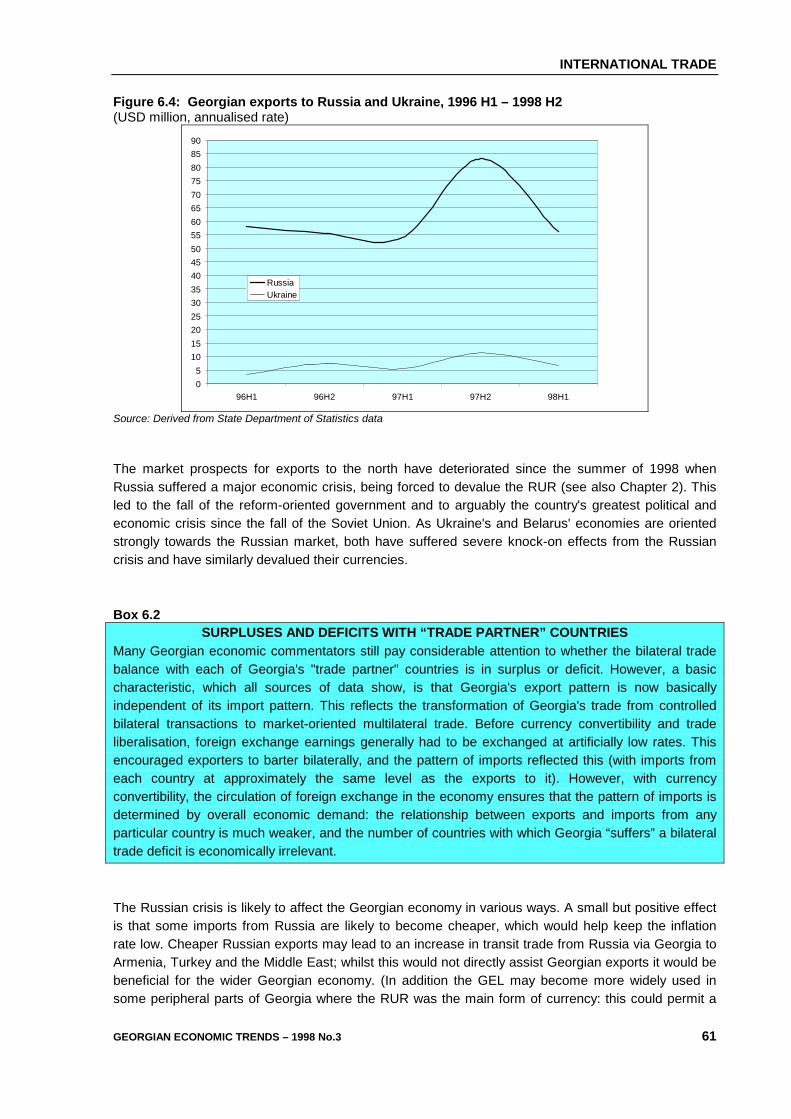

addition the legislative framework still needs to be strengthened further, with particular regard to trademarks, the protection of intellectual property, and government procurement. EXPORTS: Most of Georgia’s exports still go to its neighbouring countries, indicating the importance of proximity and of good transport links to Georgian exporters. The recorded statistics indicate little or no increase in Georgia's volume of exports to these markets, but there is significant growth in exports to more distant markets (the EU, Switzerland and the USA). In terms of the product mix, Georgia's underlying export performance also seems to be improving as exports from growth industries such as drinks and transport engineering (where Georgia appears to enjoy comparative advantages) become more important, offsetting falls in the exports of declining industries (which in any case the state can not afford to subsidise). This healthier composition of exports should lead to steady export growth in the future. IMPORTS: Georgia is continuing to import heavily from a large number of countries. Neighbouring countries all have significant shares of the Georgian market, a considerable share of imports (nearly half in 1998 Q1) also comes from south-east Europe, the European Union, the United States and Switzerland. U.S. data indicates that most American exports to Georgia are of chemicals and related products (SITC5) and machinery and transport equipment (SITC7), although exports of food and live animals (SITC1) are still important. PRIVATISATION AND PRODUCTION PROGRESS ON PRIVATISATION: Privatisation has made real progress in 1998, with the state selling its majority shareholdings in several major enterprises. There are also good signs of progress towards privatisation of the electricity sector. Two major privatisations may need to be aborted and repeated because of problems in finalising the sales, but these are both fairly unusual cases. Privatisation receipts in 1997 H1 were twice as high as expected. CAVEATS CONCERNING PRIVATISATION: In some cases the "privatisation" of an enterprise represents only a temporary transfer of the shareholding (typically for a ten-year period) and what happens when temporary transfers expire is unclear. Many of the direct sales are also subject to various commercial conditions concerning the levels of investment and employment, most of which are unnecessarily prescriptive and reduce the commercial value of enterprises. Nevertheless, the conditions set have not prevented deals of this nature from being concluded. INVESTMENT AND PRODUCTION: Despite the strong recovery (real growth of about 11 per cent) in the last two and a half years, GDP is still only around a third of what it was in the mid-1980s. Considering that an officially-estimated 45 per cent of industrial enterprises were idle in March 1998, and that agricultural yields are still very low, there still seems to be enough slack in the economy sustain the present strong growth in production. There are plenty of signs that systematic improvements are leading to more effective use of existing resources: these include the progress being made in industrial restructuring and privatisation, the wider availability of credit (and technical assistance) to farmers, and growing domestic competition in transport and communications. As expected, industrial output - which was hit badly by fuel shortages in 1998 Q1 - seems to have been much stronger in subsequent months. BUSINESS CONDITIONS: Arguably the most serious constraint on long-term development is the administrative burden - in particular the implementation of the over-complicated tax system - on small-scale entrepreneurs. The introduction in 1997 of the new Tax Code did not make the system of tax

SUMMARY AND ECONOMIC REPORT

8 GEORGIAN ECONOMIC TRENDS – 1998 No.3

collection more user-friendly for ordinary people, and continuing fears of heavy-handed and officious administration by tax inspectors are continuing to deter many entrepreneurs from joining the formal economy. As a result, many small-scale entrepreneurs prefer to develop their businesses in the shadow economy (or to seek alternative employment). This leads not only to low tax revenues for the state, but also disqualifies small-scale entrepreneurs from the credit lines that donors are trying to make available to SMEs.

CHAPTER TWO: NATIONAL ACCOUNTS AND ECONOMIC STABILITY

GEORGIAN ECONOMIC TRENDS – 1998 No.3 9

This chapter reviews official estimates of Georgia’s key macroeconomic indicators (GDP growth, the current and capital accounts, inflation and employment, and debt) and then interprets them in relation to the stability of the Georgian economy. The underlying factors that determine the longer-term trend in the key variables are discussed in various other chapters of GET. KEY MACROECONOMIC INDICATORS Economic Growth The strong trend in economic growth seems to have continued in the first half of 1998. 1998 H1 GDP is recorded as being only 8.9 per cent higher in real terms than in 1997 H1. However, on balance the underlying trend in recorded real output seems likely to remain at around 11 per cent. Output in 1998 H1 is estimated to be GEL 2.92 billion – equivalent to monthly income of about USD 70 per capita.1 Officially-estimated real GDP growth in the first quarter was 11.2 per cent higher than in 1997 Q1, and the SDS’ end-June report states that output accelerated in the second quarter. Thus, although the headline real growth figure for 1998 H1 was only 8.9 per cent, this apparent decline in growth was due to a major (and unexplained) upward revision of 1997 H1’s output.2 The IMF’s estimates for Georgian growth are in the same range, with real growth projected to be 10 per cent in 1998. Table 2.1: GDP, GNP and National Income 1995-1997 (GEL millions, current prices)

1995 1996 1997 Gross Domestic Product 3,694 5,300 6,431 Revenues from property abroad 5 7 89 Revenues transferred abroad 81 96 65 Gross National Product 3,617 5,211 6,455 Depreciation 413 616 750 Net National Income 3,204 4,596 5,705 Current transfers received from abroad 147 106 138 Current transfers sent abroad 0 0 4 National Disposable Income 3,351 4,701 5,839

Source: State Department for Statistics3 Because of continuing uncertainty about the production data, these figures should be treated as indicative rather than actual. Other evidence, including some of the recorded physical output data, seems more useful for assessing the underlying changes in the Georgian economy: this is done in the Production section of Chapter 7.

1 For seasonal reasons, output in the second half of the year tends to be considerably higher. 2 The methodology that the SDS uses for its calculation of GDP growth is still very different from that used in OECD countries – the 1998 Q1 edition of GET provided a fairly detailed discussion of some of the differences. However, the figures that the SDS arrives at seem plausible. 3 As provided in various SDS reports. The SDS’ revisions to its estimates of past GDP are difficult to keep track of, and these may not be the most recent estimates.

NATIONAL ACCOUNTS AND ECONOMIC STABILITY

10 GEORGIAN ECONOMIC TRENDS – 1998 No.3

Current Account The preliminary official figures for the balance of payments in 1997 and 1998 Q1 show that the trade deficit is widening: the official trade statistics for 1998 Q2 seem to confirm this and indicate that the rate of growth of imports may even be increasing: Figure 2.1: Balance of Trade in Goods 1995 Q1 –1998 Q2 (USD thousand per quarter)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

97Q1 97Q2 97Q3 97Q4 98Q1 98Q2

ImportsExportsDeficit

Source: State Department for Statistics The performance of Georgia's exports is of much greater concern than the trade deficit itself - see Chapter 6. Factor income from abroad, mostly earnings of short-term Georgian workers abroad, is estimated to be USD 189 million, whilst outgoings related to transportation services and travel are estimated to be USD 316 million. The share of services in total visible and invisible trade turnover increased from 15 per cent in 1996 to 25 per cent in 1997, with 1997’s registered factor payments turnover representing 10 per cent of all current transactions, compared with 5 per cent in 1996. Table 2.2: Current account in terms of GDP 1994-1997 (Per cent of GDP)

1995 1996 1997 Imports -24.8 -15.1 -21.4 Exports 10.1 8.2 7.7 Trade Balance -14.7 -6.9 -13.7 Factor Services -2.1 -1.6 2.6 Non-factor Services 0.2 0.1 -3.0 Transfers 4.0 1.9 4.0 Current Account -12.7 -6.5 -10.1

Source: State Department for Statistics - 1998 Q1 data. Capital and Financial Accounts The SDS now records estimates of portfolio investment in the Balance of Payments: USD 2.4 million of T-bills were held by foreigners at the end of 1997, with interest payments on T-bills included in the factor services account.

NATIONAL ACCOUNTS AND ECONOMIC STABILITY

GEORGIAN ECONOMIC TRENDS – 1998 No.3 11

An ongoing survey of foreign investors' activities has led to further upward revisions of the Foreign Direct Investment estimates, which were recorded as USD 242 million for 19974. Expectations for 1998 are very high, with the survey recording USD 81 million in 1998 Q1. Whilst there have been relatively few new foreign investors in Georgia, the privatisation of medium-sized and large enterprises has attracted several foreign buyers – see the Privatisation section of Chapter 7. In addition the foreign companies that have already made the biggest investments in Georgia are re-investing heavily. This pattern is basically encouraging for the longer term outlook, as "success stories" are likely to be the most effective way of promoting Georgia as an investment location. Inflation and Employment Consumer prices in June were recorded as being only 2.8 per cent higher than 12 months beforehand. This represents an impressive decrease in the 12-month rate from its recent peak of nearly 8 per cent in December 1997. The 12-month rate is likely to rise somewhat in the second half of the year, as the temporary fall in the exchange rate in September led many traders to mark up their prices and because of the 33 per cent rise in electricity tariffs. Estimates of employment and unemployment vary enormously according to the definitions used – see Chapter 8. However, as far as economic stability is concerned, the key characteristic is that in practice there are many people – both skilled and un-skilled – who are interested in new jobs because they are either unemployed or severely under-employed. This should enable the economy to continue to grow strongly without raising unit labour costs. Foreign Debt By 1st April 1998 the state's total outstanding debts had reached USD 1.815 billion. The full breakdown is given in Table 2.3. Turkey: Debt to Turkey has now been restructured. Turkmenistan: The problem concerning debt to Turkmenistan remains unresolved, with Georgia defaulting on its quarterly principal payments of USD 20 million which became payable in 1998 Q1. European Union: There is a problem concerning the payment of arrears to the EU. The EU was going to issue a ECU 55 million grant to be distributed over several years to help Georgia repay EU debt, but Georgia needed to find additional USD 6 million to finalise this. The finalisation of this agreement still seems to be in doubt because it is conditional on the Government meeting several targets which were set as conditions of the IMF’s Enhanced Structural Adjustment Facility loan: as discussed below, many of these conditions have not been met.

4 The 1997 FDI data is as provided in 1998 Q1 and may have been revised since.

NATIONAL ACCOUNTS AND ECONOMIC STABILITY

12 GEORGIAN ECONOMIC TRENDS – 1998 No.3

Table 2.3: Credits Contracted and Credits Disbursed by Creditor as of March 31, 1998 (USD million)

Creditor Total Credit Credit Disbursed

% of total

Turkmenistan 393.6 393.6 21.7 WB 352.8 233.8 19.4 IMF 252.9 252.9 13.9 EU 240.6 122.1 13.3 Russia 179.3 179.3 9.9 Austria 83.2 83.2 4.6 Turkey 54.3 54.3 3.0 Germany 51.4 34.5 2.8 EBRD 41.1 22.1 2.3 OECF* 40.3 0.0 2.2 USA 35.0 19.9 1.9 Kazakhstan 27.8 27.8 1.5 Armenia 19.6 19.6 1.1 Azerbaijan 16.2 16.2 0.9 Iran 12.8 12.8 0.7 IFAD 6.3 0.5 0.3 China 3.1 3.1 0.2 Uzbekistan 1.0 1.0 0.1 Ukraine 0.9 0.9 0.1 ATC** 2.5 2.5 0.1 Total 1,814.7 1,343.0 100.0

Source: Ministry of Finance *Japanese Overseas Economic Cooperation Fund ** Guarantee for USA Air-Traffic Control credit Armenia: Negotiations are underway on clearing Armenia’s liabilities to Georgian energy enterprises against Georgia’s state debt to Armenia; the sums concerned are roughly equal. Table 2.4: Foreign Debt Ratios (Per cent)

1995 1996 1997 Foreign debt / Exports 8.3 7.2 7.1 Foreign debt service / Exports 1.1 24.4 46.0 Foreign debt / GDP 44.0 34.0 33.0

Source: State Department for Statistics - 1998 Q1 data. ECONOMIC STABILITY Relations with the International Monetary Fund The IMF agreed to release the first tranche of a USD 74 million ESAF loan in July 1998. However, the Government’s failure to meet many of the conditions of this loan threatens to delay the release of the second tranche of the ESAF loan (which was originally scheduled for late 1998). Most, but not all, of the targets missed are interdependent: in other words, failure to meet some targets led to the failure to meet others. It appears that the Government found itself in a vicious circle and that its position has been deteriorating ever since. The failure to fulfil the conditions attached to the loan has been compounded by bad luck (notably the impact of the Russian crisis on confidence in Georgia). However it is clear that the problem began quite early in 1998 with poor collection of tax revenues – specifically, major shortfalls in revenue from excise duties and VAT on domestic production. These lower-than-expected revenues were too big to be offset by the positive impact on government finance of unexpectedly high privatisation receipts. The lack of government income forced the government to borrow excessively from the central bank. Despite this borrowing it also had to cut back on expenditure which led to other targets being missed –

NATIONAL ACCOUNTS AND ECONOMIC STABILITY

GEORGIAN ECONOMIC TRENDS – 1998 No.3 13

these include the failure to meet the minimum agreed level of health spending, and the accumulation rather than reduction in expenditure arrears (notably the backlog in the payment of salaries). June and July also saw the sale of an excessive number of T-Bills, which undermined Georgia’s financial credibility. In July the IMF approved the ESAF loan, but then bad luck struck with the impact of the Russian crisis: many people began to worry that Georgia would suffer a similar fate, and began to withdraw savings from bank deposits. As discussed below, there was a run on the GEL in early September but the central bank was able to use intervention to restore the exchange rate to its target level. However, this seems to have caused the central bank’s targets (concerning international reserves) to be missed. Apart from these interdependent targets being missed, a number of separate conditions have been violated. The Government decided to reduce the size of the Large Taxpayers’ Unit instead of increasing it as had been planned: this decision (apparently taken for internal political reasons) might not have mattered if enough tax revenue targets had been collected, but as things turned out it was evidently a big mistake. Tax arrears, which were supposed to fall, instead accumulated – this suggested lower efficiency in the system of tax collection. The Government also fell behind schedule with the implementation of its plan to introduce a new system of excise stamps for cigarettes, which has now been officially delayed by 5 months. With so many targets having been missed, it is most unlikely that the IMF’s strict internal procedures will permit it to release the second tranche of the ESAF loan before January 1999 at the earliest. Consequently it appears that the only way that the government finances can be stabilised in the meantime is through a major short-term improvement in tax revenue collection. In early October the President established a Commission, headed by the new State Minister, which is required to meet at least twice a week to “implement urgent measures to increase tax revenues of the budget and present proposals if necessary”. If successful this would enable Georgia to break out of the vicious circle, as it would have the additional benefit of meeting many of the conditions for the release of the second tranche. If unsuccessful, a further delay in the release of the tranche would seem inevitable; in that case the situation would be likely to deteriorate further. The measures that are most likely to work include the early adoption of tax changes to which Georgia is likely to have to adopt in the longer term anyway. These include the introduction of excise duty on petroleum products, heavier taxation of agriculture5, and the application of tariffs to trade in natural gas and electricity. The reduction of tax arrears would not only be directly beneficial to the budget, but would also meet one of the ESAF loan conditions. As discussed in Chapter 3, the adoption of an appropriate 1999 Budget will also be crucial as Georgia need to take specific measures restore international confidence in its commitment to fiscal reform. Parallels and differences between Russia and Georgia On 17-18 August 1998 the Russian government was forced to abandon its policy of maintaining the RUR's value against other currencies. The Russian crisis is seen by most economists as being part of a general currency crisis that so far has affected countries in south-east Asia and more recently has threatened the macroeconomic stability of countries in other regions, most notably Latin America. However, macroeconomic conditions in Georgia and most other countries along the "Silk Road”

5 The IMF has been pressing for VAT to be levied on agricultural goods. However, bearing in mind the poor operation of Georgia’s domestic VAT system, alternative measures such as an increase in land tax might be easier to implement.

NATIONAL ACCOUNTS AND ECONOMIC STABILITY

14 GEORGIAN ECONOMIC TRENDS – 1998 No.3

corridor have remained quite stable. This is largely thanks to structural differences between the various economies concerned, as well as because of their improving fiscal discipline6. The consumer imports equation described in Box 2.1 is a useful way of looking at currency stability in an emerging open market economy, because a currency crisis is normally the result of a major imbalance between consumer imports and the items on the right-hand side of the equation. Such an imbalance tends to be eliminated by an exchange rate adjustment which forces the demand for consumer imports to change: either by making imports cheaper if their level is too low or (more usually) by making them more expensive if their level is too high7. In Russia, the most important items on the right-hand side of the consumer imports equation are exports (notably energy exports) and the budget deficit (which was financed by the IMF and by sales of T-bills). One cause of instability was the fall in world energy prices, which cut Xp sharply. The large budget deficit and the government's inability to increase tax revenue were also important factors: they reduced monetary transfers from abroad because foreign investors lost confidence in Russian T-bills and therefore bought fewer of them. Consequently the level of consumer imports became unsustainable: when transfers from the IMF proved to be inadequate, the devaluation of the RUR became inevitable. More generally, emerging markets that have large budget deficits and whose exports depend on commodities such as energy or raw materials tend to be macroeconomically unstable. (Commodity prices are generally much less stable than prices of manufactured goods.) In Georgia, as in Russia, consumer imports are in part sustained as a result of IMF transfers (A); however in Georgia's case the items on the right-hand side of the equation are much more stable. As discussed in Chapter 5, Georgia's own-produced exports (Xp) seem to be quite diverse and are therefore unlikely to fall suddenly. Value-added through transit {Xx - Mx} is a stable item and is significant because of Georgia's location on the Silk Road. The item {I - Mi - S} is unlikely to fall dramatically unless the investment climate changes dramatically. This leaves the budget deficit {G - T}, which has been small in recent years because the government has systematically linked its expenditure to the collection of tax revenue. However, uncertainty about the deficit caused problems for Georgia in the second half of 1998 because of fears that the Ministry of Finance would allow expenditure to grow faster than revenue and would then have no choice but to adopt an austerity programme which would almost inevitably involve devaluation. Box 2.1

CURRENCY CRISES IN EMERGING MARKETS A currency crisis is likely to occur in any country if the government mismanage its finances (usually by running an unsustainably large budget deficit). Equally, some economic changes are so great that they make a currency crisis practically unavoidable - the collapse of the Soviet Union is an example. However, some economies are more sensitive to economic changes than others are. This is not simply a question of macroeconomic management, but also of economic structure. Currencies in "emerging markets" (transition countries and the more advanced developing countries) seem to be more sensitive to economic shocks compared with long-established market economies and the least developed countries. But emerging markets do not all have similar economic structures: this is the key to 6 At about 2 per cent of GDP, Georgia’s budget deficit is comparable to that of other countries in the region; in contrast, Russia’s budget deficit in summer 1998 was about 7 per cent of GDP.

NATIONAL ACCOUNTS AND ECONOMIC STABILITY

GEORGIAN ECONOMIC TRENDS – 1998 No.3 15

understanding why some are more stable than others, and in particular why Georgia has not followed Russia into macroeconomic chaos. Basic economic algebra can be used to consider what the key structural factors are and why they matter. In any economy, total income can be expressed by an equation representing expenditure and by another representing output: Y = C + S + T - A (expenditure) Y = C + I + G + X - M (output) where Y is income, S is domestic savings, T is taxation, A is net monetary transfers from abroad, I is investment, G is government expenditure, X is exports and M is imports. It is also sometimes useful to separate total exports (X) into own-produced exports (Xp) and re-exports (Xx), and to separate total imports (M) into components representing imports that are for consumption (Mc), those that are for investment (Mi) and those that are re-exported (Mx); X = Xx + Xp and M = Mc + Mi + Mx. By introducing these terms and then manipulating the expenditure and output equations, it can be shown that: Mc = Xp + {Xx - Mx} + {G - T} + A + {I - Mi - S} (consumer imports) The interpretation of this equation is that consumer imports are equivalent to the sum of own-produced exports, value-added in transit, the budget deficit, net monetary transfers from abroad and foreign investment expenditure on domestic output. Restoring the value of the Georgian Lari In contrast to the Russian crisis (when the president and government promised not to devalue the RUR but were eventually left with no choice), the Georgian authorities were able to revalue the GEL in response to a mini-crisis in September. During the weekend of 5/6 September (when the central bank was closed), rumours of devaluation pushed the GEL to a street exchange rate of around 1.80 per USD. However, the central bank's relatively modest market intervention on 7 September was sufficient to restore the GEL exchange rate to its previous level of 1.35 per USD. In terms of the consumer imports equation, this intervention corresponded to a minor short-term increase in government expenditure (since it involved the central bank "buying" GEL) and thus had the short-term effect of restoring the equilibrium level of consumer imports through (what was, in effect) an increase in G. Although this demonstrated the GEL's structural security under present policies, it also showed how risky a change in policy would be: just as a modest reduction in the money supply was sufficient to stabilise the GEL, a correspondingly modest increase could have the opposite effect. Thus Georgia seems to have practically no scope for monetary loosening in the short term. Moreover, the scope for further monetary tightening is limited because too tight a monetary policy would undermine Georgia’s financial credibility. Therefore - assuming no major increase in exports, monetary transfers from abroad or foreign investment - the only ways that the consumer imports equation can be balanced in the medium term8 is by cutting the level of consumer imports. This demands either major increases in tax collection (in order to reduce consumer demand) or else a major (and destabilising) fall in the exchange rate.

7 Alternatively this can be achieved by raising tariffs on imports or by raising consumption taxes (such as VAT and excise duties) that affect consumer exports. 8 The medium term in this context is the next few quarters.

NATIONAL ACCOUNTS AND ECONOMIC STABILITY

16 GEORGIAN ECONOMIC TRENDS – 1998 No.3

In the longer term, however, the prospects for economic stability look much healthier: the underlying trend in government finances still seems to be towards a progressive reduction in the budget deficit9; infrastructural and commercial foreign investment would tend to strengthen the capital account, and it also seems realistic to expect that the current account would eventually be strengthened by major increases in oil production10.

9 See Chapter 3. 10 See also the Production section of Chapter 7 concerning oil: even if oil prices remain low, 300,000 barrels/day domestic production would strengthen the current account by around USD 1.500 million per year.

CHAPTER THREE: GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 17

As explained in Chapter 2, the ineffective collection of tax revenue is one of the main threats to Georgia's continuing recovery and financial stability. In the second half of 1998 this has become a major issue. Although the budget deficit was reduced from 4.4 per cent in 1996 to 2 per cent of GDP in 1997, this was basically achieved by keeping expenditure very low. This meant very little public capital investment (resulting in the continued deterioration of much of the country's infrastructure) and tightly constrained payments of public employees’ salaries, which led to the accumulation of expenditure arrears, in violation of Georgia’s agreements with the IMF. The deficit was supposed to be reduced to about 1.8 per cent of GDP in 1998, but in the second half of 1998 this target seems to have been threatened by higher expenditure and by an apparent deterioration in the collection of excise duty and VAT. Issues relating to deficit financing are again covered elsewhere in this edition of GET: external debt is covered in Chapter 2, whilst the issue of Treasury bills is covered in Chapter 4. This chapter looks at the issues of revenue and expenditure; the focus of this issue of GET is mainly on revenue because a lot of new detailed information is already available concerning collection but relatively little on the details of expenditure. The chapter also discusses some of the key issues concerning the 1999 Budget, which is due to be debated in 1998 Q4. CONSOLIDATED TAX REVENUE Low government revenue collection remains the most pressing problem facing Georgia's public finance. From April 1998 onwards disturbing reports began to appear in the Georgian press about “catastrophic” shortfalls in tax collection1. The fiscal data for the first six months of 1998 indicates that total tax revenue in 1998 Q2 was 17 per cent higher in nominal terms than in the corresponding period of 1997. This represented a slowdown compared with 1997 (when, according to GET’s database, annual revenue was 58 per cent higher than in the previous year). Taking into account the Government’s and donors’ concerted efforts to improve methods of revenue collection, this slowdown could be considered disappointing. Nevertheless the 17 per cent rise in tax revenues was still a couple of percentage points higher than nominal GDP growth; as Chart 3.1 shows, revenue collection in 1998 H1 seems to have remained on an upward trend after allowing for the seasonal fall in activity between the fourth and first quarters. As the chart also shows, consolidated government income (excluding the Special State Funds, whose revenue is predicated) fell slightly during the second quarter, from GEL 165 million to GEL 157 million. This fall is explained by the drop in fees and non-tax income. A general pattern seems to be emerging this year: most revenue targets (including those for income tax, profits tax and customs) are being met or even exceeded but those for VAT and excise duty are being missed by wide margins. As VAT and excise duty are two of the most important sources of revenue, the result is that total revenue is well below target. In the first half of 1998, VAT and excise 1 For example, figures reported in the 24 April - 1 May issue of Georgian Business News indicated that the State Customs Department and State Tax Service had between them transferred only GEL 15.2 million to the Treasury compared with the planned GEL 36 million for April.

GOVERNMENT REVENUE AND EXPENDITURE

18 GEORGIAN ECONOMIC TRENDS – 1998 No.3

duty were planned to provide about three-quarters of the State’s tax revenue but in fact provided less than two-thirds: consequently its total tax revenue was some 18 per cent below target. Figure 3.1: Consolidated revenue and expenditure, 1996 Q1 to 1998 Q22 (GEL thousand per quarter)

0

50000

100000

150000

200000

250000

300000

96Q 2 97Q 2 98Q 2

C apita l receiptsTaxes on importsTaxes on businessIncome taxExpenditureC onsolidated income

Source: Ministry of Finance Note: revenue and expenditure from the Special State Funds is not included in this chart and is discussed in Chapter 8. THE EFFECTIVENESS OF TAX COLLECTION For most taxes, data on revenue in the second quarter of 1998 may be compared with the trend in 1996-97. The easiest historical comparison is with 1997 Q2: assuming that real output has grown by about 11 per cent and that 1998 Q2 prices were on average 4 per cent higher than in 1997 Q2, the increase in revenue should generally be more than 15 per cent in nominal terms if collection rates are improving. Evidence from the first quarter of 1998 also enables us to make a preliminary assessment of tax collection by local authorities in comparison with their planned revenue targets. 1. Personal income tax For Georgia as a whole, income tax collection in the first half of 1998 was GEL 39 million. This includes income tax revenue allocated to the central budget, which was GEL 16 million (8 per cent above target) and GEL 23 million retained by the local authorities (11 per cent below the aggregated regional targets). The aggregate shortfall for local authorities reflects large shortfalls in the more industrial regions of Georgia: most rural districts exceeded their targets. Considering that income tax revenue is still partly a reflection of salary-payments to public-sector employees, this regional pattern may indicate that there have been efforts to ensure salary-payments to public-sector employees in rural regions. Alternatively rural targets may have been set lower in anticipation of non-payment which has apparently been a particular problem for rural employees in the past. In either case, it seems unlikely that the regional pattern reflects an increase in revenue from the taxation of private incomes

2 Taxes on business include domestic VAT and excise duty, and regionally-retained taxes. Taxes on imports include VAT and excise duty. Contributions to the Special State Funds are excluded from this data.

GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 19

(which tend to be very low in rural areas: it is in Georgia’s urban areas that incomes tend to be highest and economic growth tends to be strongest). Figure 3.2: Personal income tax revenue, 1996 Q1 to 1998 Q2 (GEL thousand per quarter)

0

5000

10000

15000

20000

25000

96Q2 97Q2 98Q2

LocalState

Source: Ministry of Finance As Chart 3.2 shows, the collection of income tax has been rising steadily though with seasonal variations. Revenue in Q2 was 22 per cent higher in nominal terms than in the corresponding period in 1997 - comfortably above the 15 per cent "benchmark" mentioned above. Therefore the underlying trend continues to look satisfactory. 2. Corporate Profit Tax The application of profit tax rules and allowances tends to be especially arbitrary because accounting rules remain unclear and there is widespread distrust between tax collectors and taxpayers. Tax collectors tend not to trust the figures that business managers present them with, and few business managers trust tax collectors to implement the system correctly. Overall profit tax collection in the first half of 1998 was GEL 22 million. As Chart 3.3 shows, the collection of profit tax has been increasing rather slowly. However, consolidated profit tax revenue in Q2 was 21 per cent higher in nominal terms than in 1997 Q2: this indicates some improvement in collection rates, which might reflect the impact of technical assistance aimed at improving the system of business taxation. However, there still seems to be a long way to go in establishing a reasonable degree of mutual trust between taxpayers and the STS.

GOVERNMENT REVENUE AND EXPENDITURE

20 GEORGIAN ECONOMIC TRENDS – 1998 No.3

Figure 3.3: Profit Tax Revenue (GEL thousand per quarter)

0

5000

10000

15000

20000

25000

96Q2 97Q2 98Q2

LocalState

Source: Ministry of Finance As with income tax, the central target was exceeded by 8 per cent, whilst the aggregated regional revenue targets were 5 per cent below target. Again there were significant regional differences: Tbilisi and Achara both exceeded their targets, but revenue was much lower than planned in almost every other region. As far as local authorities are concerned, the incentive for collecting profit tax is the same as for income tax - in both cases 60 per cent of revenue is retained locally with the remainder transferred to the state budget. However, whereas most authorities met their income tax targets, almost every administrative district’s revenue collection was below the target set; this suggests that the regional profit tax targets may have been unrealistic. 3. Value-Added Tax VAT is the most important tax in Georgia, providing around 40 per cent of consolidated tax revenue. The total amount of VAT revenue collected in 1998 Q2 was about 17 per cent higher in nominal terms than in 1997 Q2. However this figure masks major differences between the respective collections of VAT on imports and VAT on domestic production. Revenue from VAT on imports is on a strong upward trend, albeit below target. However revenue from VAT on domestic goods and services is actually dropping; as Chart 3.4 shows, it has now fallen below that of VAT on imports.

GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 21

Figure 3.4: VAT revenue – imports and domestic (GEL thousand per quarter)

0

10000

20000

30000

40000

50000

60000

70000

96Q2 97Q2 98Q2

DomesticOn ImportsTotal VAT

Source: Ministry of Finance In most regions of Georgia all the VAT revenue collected is transferred to the central budget, giving local authorities little incentive to collect it. The two exceptions are Achara, which now retains 99 per cent of the VAT it collects from imports, and Tbilisi, which is now entitled to retain 15 per cent of VAT on domestic goods and services. The consolidated revenue from VAT on imports was slightly below target, with a surfeit of more than GEL 4 million in Achara not quite large enough to offset general shortfalls elsewhere. It is unclear why VAT on domestic goods and services is actually dropping, or why (outside Achara) the revenue target for VAT on imports was also missed. VAT is one of the taxes where technical assistance is evidently needed to improve the effectiveness of the system, and the advice that has been given does not yet seem to have resulted in any improvements. 4. Customs duty Revenue from customs duty continued to grow strongly, with 1998 Q2's figure 41% higher than that of 1997 Q2. A concerted effort has been underway over the past year to improve collection rates by the Customs Department, with the World Bank providing technical assistance to help push through organisational reform.

GOVERNMENT REVENUE AND EXPENDITURE

22 GEORGIAN ECONOMIC TRENDS – 1998 No.3

Figure 3.5: Customs Revenue (GEL thousand per quarter)

0

5000

10000

15000

20000

25000

96q1 97q1 98q1

LocalState

Source: Ministry of Finance 5. Excise duty In strong contrast to Customs duty, the revenue from Excise duty has been much lower than planned over the last 3 quarters and was some 30 per cent lower in nominal terms in 1998 Q2 than in 1997 Q2. The initial impression given by Chart 3.6 is that the relatively high levels of revenue collected in 1997 Q2 and 1997 Q3 were aberrations. However there is no practical reason why this should be so: with living standards rising in Georgia, the consumption of goods that are liable for Excise duty (notably alcohol and tobacco) would be expected to increase; this should have led to an increase in Excise revenue. The small amount of available data on alcohol and tobacco imports in the first quarter seems to confirm this: the US-Georgia bilateral statistics presented in the 1998 Q1 issue of GET show a marked rise in US exports of beverages and tobacco to Georgia. Figure 3.6: Excise Revenue (GEL thousand per quarter)

0

5000

10000

15000

20000

25000

96Q2 97Q2 98Q2

Excise duty on domestic suppliesExcise duty on imports

Source: Ministry of Finance

GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 23

The Government is now planning to introduce a new system of excise stamps to discourage smuggling; its implementation has been scheduled for 1998 Q4. COLLECTION OF REGIONAL TAXES Revenue from the regional taxes was about 8 per cent below target. In aggregate, the revenue from two of the three most important taxes (property tax and local tax) was on target. However, revenue from land tax and from the less important taxes was generally quite a long way below target. As in Q1 there were major regional variations; no district seems to be capable of meeting all of its revenue targets. Figure 3.7: Collection of the regional taxes in 1998 H1 (GEL thousand)

0

2000

4000

6000

8000

10000

12000

Land tax Naturalresources tax

Pollution tax Property tax Propertytransfer tax

Local tax

PlanOutcome

Source: Ministry of Finance a. Land tax As in Q1, Samegrelo and Zemo Svaneti’s collection of land tax revenue was above target; Imereti (whose collection was well below target in Q1) also met its target for H1.

GOVERNMENT REVENUE AND EXPENDITURE

24 GEORGIAN ECONOMIC TRENDS – 1998 No.3

Figure 3.8: Regional collection of land tax (GEL thousand per quarter)

0

500

1000

1500

2000

2500

Abkh

azia

Ajar

a

Tbilis

i

Kakh

eti

Imer

eti

Sam

egre

lo

Shid

a Ka

rtli

Kvem

o Ka

rtli

Gur

ia

Java

khet

i

Mts

khet

a

Rac

ha

PlanOutcome

Source: Ministry of Finance However, the rest of the regions were all below their revenue targets; this included Tbilisi, which had been above its target in Q1. In aggregate, land tax revenue was 9 per cent below target. b. Natural resources tax Collection of natural resources tax revenue remains a long way below target in the regions where most of it was expected to be collected. As in Q1, revenue targets were exceeded in the smaller regions of Guria, Samtskhe-Javakheti and Racha-Lechkhumi. Figure 3.9: Regional collection of natural resources tax (GEL thousand)

0

100

200

300

400

500

600

700

800

900

1000

Abkh

azia

Ajar

a

Tbilis

i

Kakh

eti

Imer

eti

Sam

egre

lo

Shid

a Ka

rtli

Kvem

o Ka

rtli

Gur

ia

Java

khet

i

Mts

khet

a

Rac

ha

P lanO utcom e

Source: Ministry of Finance

GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 25

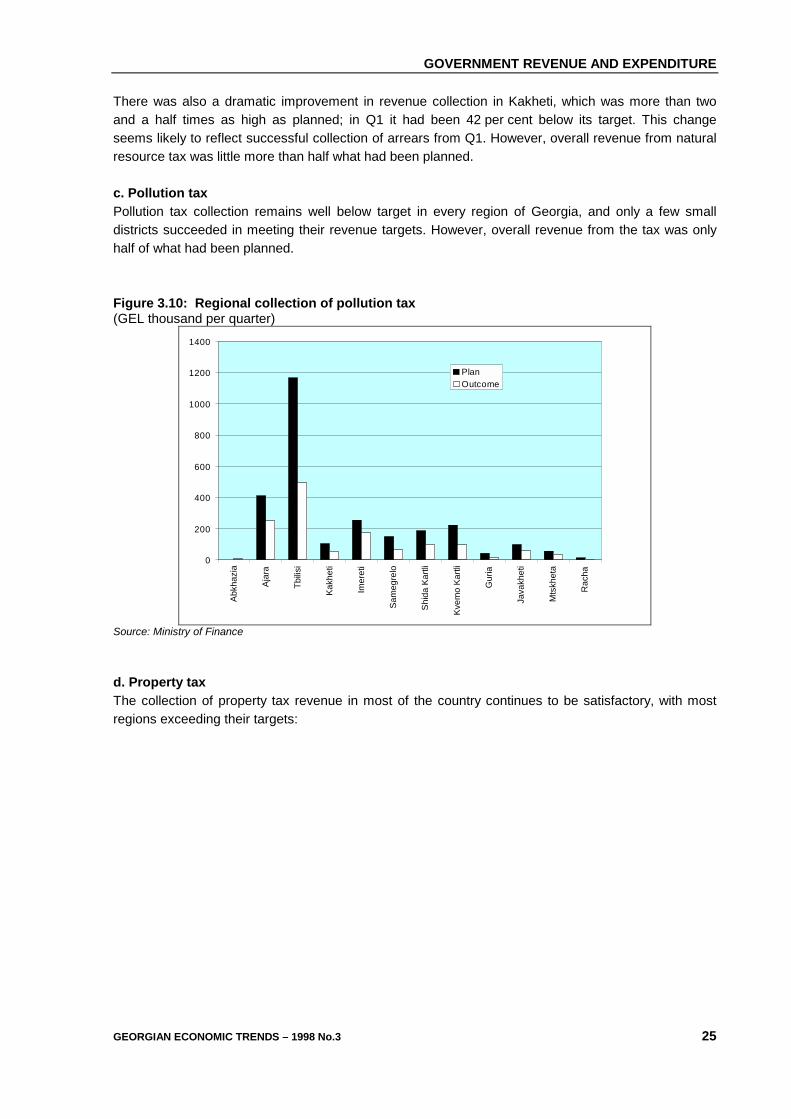

There was also a dramatic improvement in revenue collection in Kakheti, which was more than two and a half times as high as planned; in Q1 it had been 42 per cent below its target. This change seems likely to reflect successful collection of arrears from Q1. However, overall revenue from natural resource tax was little more than half what had been planned. c. Pollution tax Pollution tax collection remains well below target in every region of Georgia, and only a few small districts succeeded in meeting their revenue targets. However, overall revenue from the tax was only half of what had been planned. Figure 3.10: Regional collection of pollution tax (GEL thousand per quarter)

0

200

400

600

800

1000

1200

1400

Abkh

azia

Ajar

a

Tbilis

i

Kakh

eti

Imer

eti

Sam

egre

lo

Shid

a Ka

rtli

Kvem

o Ka

rtli

Gur

ia

Java

khet

i

Mts

khet

a

Rac

ha

PlanOutcome

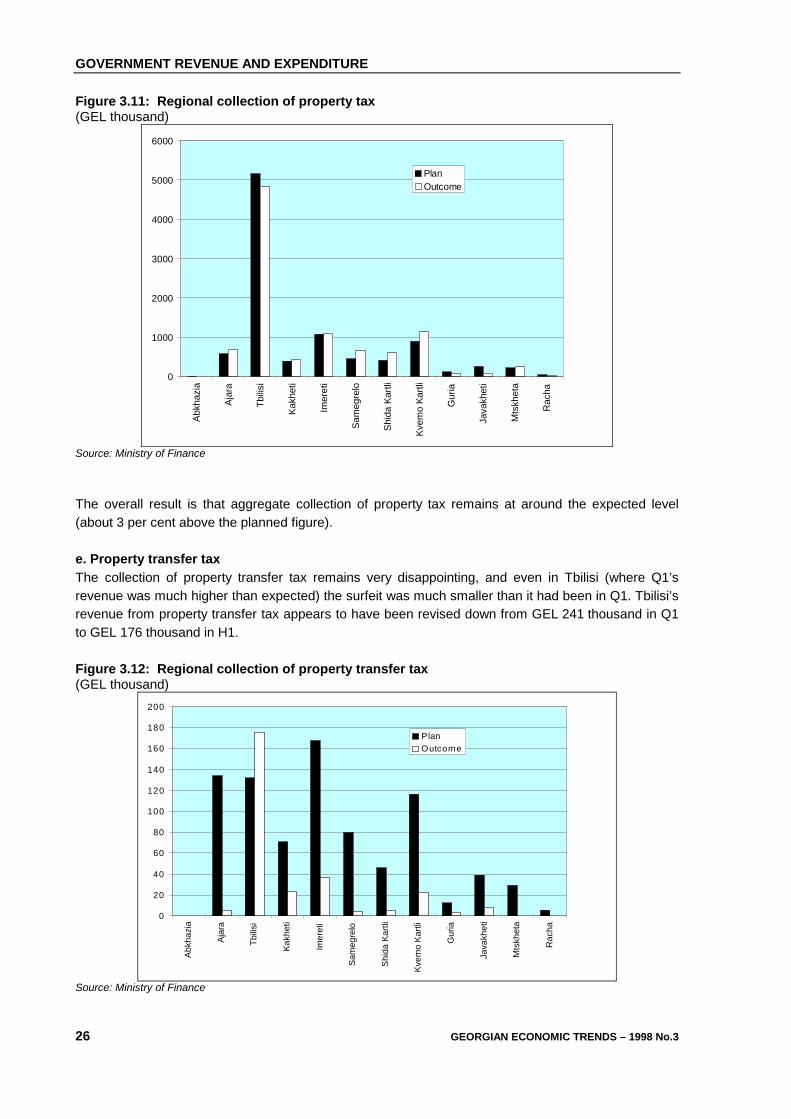

Source: Ministry of Finance d. Property tax The collection of property tax revenue in most of the country continues to be satisfactory, with most regions exceeding their targets:

GOVERNMENT REVENUE AND EXPENDITURE

26 GEORGIAN ECONOMIC TRENDS – 1998 No.3

Figure 3.11: Regional collection of property tax (GEL thousand)

0

1000

2000

3000

4000

5000

6000

Abkh

azia

Ajar

a

Tbilis

i

Kakh

eti

Imer

eti

Sam

egre

lo

Shid

a Ka

rtli

Kvem

o Ka

rtli

Gur

ia

Java

khet

i

Mts

khet

a

Rac

ha

PlanOutcome

Source: Ministry of Finance The overall result is that aggregate collection of property tax remains at around the expected level (about 3 per cent above the planned figure). e. Property transfer tax The collection of property transfer tax remains very disappointing, and even in Tbilisi (where Q1’s revenue was much higher than expected) the surfeit was much smaller than it had been in Q1. Tbilisi’s revenue from property transfer tax appears to have been revised down from GEL 241 thousand in Q1 to GEL 176 thousand in H1. Figure 3.12: Regional collection of property transfer tax (GEL thousand)

0

20

40

60

80

100

120

140

160

180

200

Abkh

azia

Ajar

a

Tbilis

i

Kakh

eti

Imer

eti

Sam

egre

lo

Shid

a Ka

rtli

Kvem

o Ka

rtli

Gur

ia

Java

khet

i

Mts

khet

a

Rac

ha

P lanOutcome

Source: Ministry of Finance

GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 27

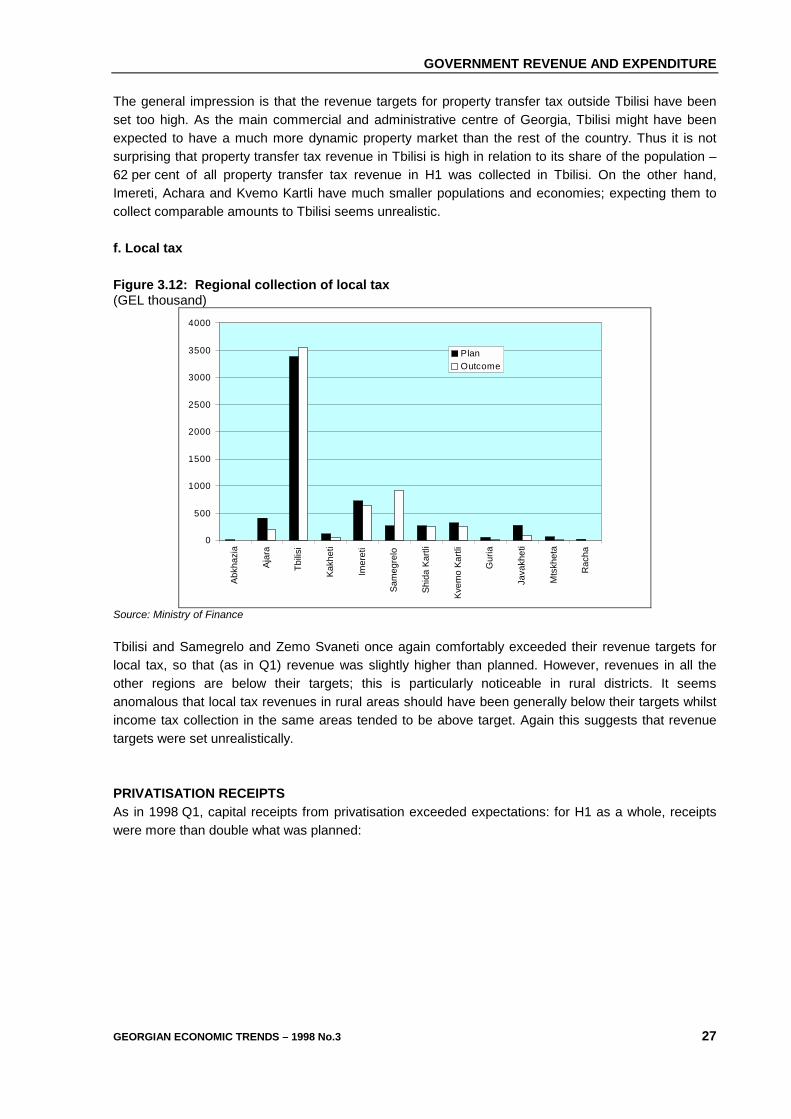

The general impression is that the revenue targets for property transfer tax outside Tbilisi have been set too high. As the main commercial and administrative centre of Georgia, Tbilisi might have been expected to have a much more dynamic property market than the rest of the country. Thus it is not surprising that property transfer tax revenue in Tbilisi is high in relation to its share of the population – 62 per cent of all property transfer tax revenue in H1 was collected in Tbilisi. On the other hand, Imereti, Achara and Kvemo Kartli have much smaller populations and economies; expecting them to collect comparable amounts to Tbilisi seems unrealistic. f. Local tax Figure 3.12: Regional collection of local tax (GEL thousand)

0

500

1000

1500

2000

2500

3000

3500

4000

Abkh

azia

Ajar

a

Tbilis

i

Kakh

eti

Imer

eti

Sam

egre

lo

Shid

a Ka

rtli

Kvem

o Ka

rtli

Gur

ia

Java

khet

i

Mts

khet

a

Rac

ha

PlanOutcome

Source: Ministry of Finance Tbilisi and Samegrelo and Zemo Svaneti once again comfortably exceeded their revenue targets for local tax, so that (as in Q1) revenue was slightly higher than planned. However, revenues in all the other regions are below their targets; this is particularly noticeable in rural districts. It seems anomalous that local tax revenues in rural areas should have been generally below their targets whilst income tax collection in the same areas tended to be above target. Again this suggests that revenue targets were set unrealistically. PRIVATISATION RECEIPTS As in 1998 Q1, capital receipts from privatisation exceeded expectations: for H1 as a whole, receipts were more than double what was planned:

GOVERNMENT REVENUE AND EXPENDITURE

28 GEORGIAN ECONOMIC TRENDS – 1998 No.3

Figure 3.13: Capital receipts (GEL thousand per quarter)

0

5000

10000

15000

20000

25000

96Q2 97Q2 98Q2

LocalState

Source: Ministry of Finance This is partly thanks to receipts from large privatisations, which seem to have brought windfalls to a small number of district authorities (notably Kvareli, Zestaphoni, Poti, Gori, Rustavi, Ozurgeti, Mtskheta and Ambrauli). However, the vast majority of districts also exceeded their planned receipts from privatisation: this suggests that the general pattern is also better than expected. OTHER GOVERNMENT RECEIPTS Fees and non-tax revenues fell back to their normal level in 1998 Q2. As in Q1, the state budget received no grants from donors. No grant income had been expected in Q2, but it appears that in Q1 the GEL 5.1 million that had been expected was in effect replaced by correspondingly higher net transfers to the budget from the central bank. This would have left less scope for central bank transfers in the rest of the year, resulting in recorded growth in the budget deficit in Q2. Figure 3.14: Quarterly Consolidated Miscellaneous Government Receipts (GEL thousand per quarter)

0

10000

20000

30000

40000

50000

60000

70000

96Q2 97Q2 98Q2

LocalState

Source: Ministry of Finance

GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 29

Thus it seems that the relatively healthy appearance of the government finances in Q1 masked a continuing structural deficit, and that subsequent government finance figures will seem worse because it has become practically to use central bank transfers to conceal the structural deficit.3 On the other hand, the underlying trend in the income side of government finances does not seem to have changed significantly in the first half of the year: tax revenues were still growing steadily. THE DIVISION BETWEEN STATE AND LOCAL EXPENDITURE At just under GEL 162 million, actual expenditure under the central budget was only 1 per cent higher than in 1997 Q2 - in other words, about 3 per cent lower in real terms. However, higher spending by local authorities pushed up consolidated government expenditure in 1998 Q2 to GEL 227 million, compared with GEL 209 million in 1197 Q2 – an increase of 9 per cent. Figure 3.15: State and local expenditure (GEL thousand per quarter)

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

97Q1 98Q1

StateLocalTOTAL

Source: Ministry of Finance As government in Georgia becomes less centralised (with the first local authority elections due to take place in mid-November 1998), expenditure and revenue at the local level is increasing at a rate of about 30 per cent a year. Education and national economy together account for most of this rise. In some countries the decentralisation of expenditure can threaten to fiscal discipline, as local authorities accumulate deficits which must then be funded by central government. However, Georgia’s local government finance rules seem to be effective in ensuring balanced budgets: therefore the trend towards decentralisation of expenditure does not seem to pose a risk to the stability of government finances. The composition of local government expenditure by category of expenditure does not fluctuate much, either over time or between one region and another (though there is some local variation within some regions). Most local government expenditure is on education and items categorised as “national economy” which range from minor infrastructural investment to the employment of specialist professionals such as veterinary surgeons. 3 “Income from the central bank” in 1998Q1 (GEL 36 million) inflated the consolidated income figure for that quarter. The item is not listed separately in the Ministry of Finance’s data, but the aggregate figure for non-tax income items in Q2 was less than GEL 14 million which suggests that the central bank income item was very low.

GOVERNMENT REVENUE AND EXPENDITURE

30 GEORGIAN ECONOMIC TRENDS – 1998 No.3

CONSOLIDATED EXPENDITURE The apparent composition of consolidated expenditure is derived by adding together similar categories of expenditure in the public accounts of central and local government provides: Figure 3.16: Detailed composition of consolidated expenditure in 1998H1 (GEL thousand per quarter)

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Education Administration Health Care Culture, Sportand Religion

Law and Order Social Security Defence Other

LocalState

Source: Ministry of Finance Consolidated expenditure on social services (law and order, education, health and cultural and sporting events) and on social security has stayed fairly constant over the past year. The main fluctuations have been in state expenditure on administration and in miscellaneous items of state expenditure (including public investment and debt servicing). Expenditure on social security and on health includes such items as central government "top-up" support for the United Social Security Fund, special centrally-funded programmes (such as assistance to disabled people) and local authority spending on social security including assistance to single mothers. As mentioned earlier, information about the Special State Funds is provided in Chapter 8. Figure 3.17: Changes in the composition of consolidated expenditure 1997 Q1 to 1998 Q2 (GEL thousand per quarter)

-

50,000

100,000

150,000

200,000

250,000

300,000

97Q1 98Q1

Administration & DefenceSocial ServicesSocial SecurityOther expenditure ex SSF

Source: Ministry of Finance

GOVERNMENT REVENUE AND EXPENDITURE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 31

As happened in 1997, state expenditure on administration was kept low in the first half of this year; this helped to constrain the rise in overall expenditure. However, this seems to have once again been achieved by postponing the payment of salaries to public servants. Therefore, as in 1997, a major increase in expenditure on administration to pay back the arrears seems unavoidable: Figure 3.18: Changes in expenditure on administration 1997 Q1 to 1998 Q2 (GEL thousand per quarter)

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

97Q1 98Q1

LocalState

Source: Ministry of Finance Judging from the other expenditure patterns (not re-produced here) most of the expenditure arrears that were accumulated in 1998 H1 were in administration. Chart 3.18 provides a rough indication of likely expenditure requirements in the second half of the year: if it is to follow the same pattern as in 1997, administrative expenditure in 1998 H2 seems likely to be some GEL 70 million higher than in 1998 H1. THE 1999 BUDGET With consolidated government income apparently still growing steadily at an annual rate of around 20 per cent, and with consolidated expenditure growing at only about half that rate, the fiscal position seems to be sustainable in the long term. However in the short term, as Chapter 2 explains, the failure to meet projected tax revenue targets in 1998 has led Georgia to a situation where it is struggling to fund the budget deficit. As the deficit is relatively small, the high-level Commission that has been established has a fair chance of averting the potential crisis. This could also enable Georgia to meet many of the conditions attached to the planned release of the second tranche of IMF credit. In addition to its efforts to meet the conditions that are presently being violated, Georgia must avoid violating other conditions. Apparently an early draft Budget envisages the establishment of new tax exemptions, which would violate the conditions of the ESAF loan. In addition the Budget would need to address the issue of applying tariffs to trade in natural gas and electricity.

CHAPTER FOUR: MONEY AND FINANCE

32 GEORGIAN ECONOMIC TRENDS – 1998 No.3

The controlled depreciation of GEL continued in 1998 Q2, standing at GEL USD 1.3478 at the end of June 1998). The GEL’s nominal exchange rate against the US dollar depreciated by 3 per cent during 1998 H1 and was 4 per cent lower than in June 1997. Nevertheless, the nominal exchange rate remained an anchor for domestic inflation and the year-on-year inflation rate (2.8 per cent annual in June) was still one of the lowest in the CIS region. Despite the low rate of inflation, the coefficient of deposit dollarisation was still high (about 60 per cent) but did not increase in 1998 Q2. Direct financing of the State budget remained significant. The NBG issued GEL 81 million for the MoF in 1998 H1, compared the revised annual target of GEL 110 million. The budget deficit was also financed by T-Bills emissions, of which GEL 18.9 million were outstanding at the end of June 1998. The last 28-day T-Bills auction was held in April, so that the market consisted only of 91-day T-Bills. MONETARY DEVELOPMENTS Figure 4.1: Money Supply

0

5 0 ,0 0 0

1 0 0 ,0 0 0

1 5 0 ,0 0 0

2 0 0 ,0 0 0

2 5 0 ,0 0 0

3 0 0 ,0 0 0

3 5 0 ,0 0 0

4 0 0 ,0 0 0

D e c95

J a n96

F e b M a r A pr M a y J un J ul A ug S e p O c t N o v D e c J a n97

F e b M a r A pr M a y J un J ul A ug S e p O c t N o v D e c J a n F eb M a r A pr M a y J un

GEL

thou

sand

s

F o re ig n C urre nc y D e p o s itsG E L D e p o s its

C urre nc y O uts id e C o m m e rc ia l B an ks

M 3

M 2

M 0

Source: Data provided by the National Bank of Georgia The money supply did not grown significantly in 1998 H1, with M3 increasing by only GEL 14 million and cash outside commercial banks increasing by GEL 1 million. GEL deposits grew by 5 million, whilst deposits in foreign currency increased by GEL 28 million. With direct budget financing running at GEL 81 million (plus GEL 3 million spent from Government deposits), it was only the tight monetary policy that prevented a rise in the inflation rate.

MONEY AND FINANCE

GEORGIAN ECONOMIC TRENDS – 1998 No.3 33

CREDIT TO THE GOVERNMENT Table 4.1: Central Government Loans and Deposits with the Banking System (GEL thousands)

1997 1998Mar Jun Sep Dec Jan Feb Mar Apr May Jun

Net Claim s on Central Governm ent 305,682 362,403 409,350 403,701 413,586 424,005 434,758 445,550 455,993 480,767

Central Government Borrow ing from NBG 333,418 372,818 424,759 412,725 424,925 436,583 446,100 460,600 466,700 493,650

Central Government Deposits 27,736 10,416 15,410 12,803 14,265 15,636 14,530 15,050 10,708 12,883 Central Government Deposits at NBG in GEL 6,821 3,172 10,368 11,929 10,959 11,725 9,883 11,511 6,361 8,931 Other Government accounts liab ilities 295,237 800,341 1,022,499 1,473,257 91,987 200,898 387,170 507,640 609,045 760,591 Other Government accounts assets 288,416 797,169 1,012,132 1,461,328 81,028 189,173 377,287 496,129 602,684 751,661 Central Government Deposits at NBG in foreign currency 10,745 1,666 465 1,264 2,494 2,086 3,130 1,942 2,393 2,286 Central Government Deposits at commercial banks 10,169 5,578 4,577 -390 812 1,824 1,517 1,597 1,954 1,666

Source: Data provided by the National Bank of Georgia Because of the growing difficulties in government finance, direct deficit financing became a major problem in 1998 H1. The upper limit for 1998 on deficit financing by the NBG credit was increased from GEL 54 million to GEL 110 million, but in 1998 H1 alone the NBG issued GEL 81 million. Consequently the NBG was forced to focus its attention on financing the state budget, the expense of at other key functions (improving the regulation of the banking system, developing the money markets, and strengthening the foreign exchange policy). In principle, the priority of the NBG should be to support a workable banking system; instead, it had to spend a high proportion of its international reserves on sterilising money emission. GOVERNMENT TREASURY BILLS In addition to direct NBG credit, the budget deficit was financed by the issue of T-Bills. This was an alternative way of financing the budget deficit that should in the long term completely replace NBG credit. However, that remained difficult because of the lack of market development. Figure 4.2: 91-day T-Bills Yields and Rate

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

11/6/

97

11/13/9

7

11/20

/97

11/27

/97

12/4/

97

12/11

/97

12/18

/97

12/25

/971/1

/981/8

/98

1/15/9

8

1/22/9

8

1/29/9

82/5

/98

2/12/9

8

2/19/9

8

2/26/9

83/5

/98

3/12/9

8

3/19/9

8

3/26/9

84/2

/984/9

/98

4/16/98

4/23/9

8

4/30/9

85/7

/98

5/14/9

8

5/21/9

8

5/28/9

86/4

/98

6/11/9

8

6/18/9

8

T-B i lls ra te (a ve ra g e )

Ye ld (a nnua l s im p le )

Ye ld (a nnua l co m p o und )

Source: GET calculation based on data provided by the National Bank of Georgia The last 28-day auction was held in April, so that at the end of H1 the market consisted entirely of three month (91-day) T-bills. The Ministry of Finance planned to issue six-month T-Bills later in the

MONEY AND FINANCE

34 GEORGIAN ECONOMIC TRENDS – 1998 No.3

year. At the end of June, there were GEL 19 million (USD 14 million) outstanding T-Bills. The Georgian T-Bills market was relatively small compared with some other CIS countries markets: for example, the Kyrgyz market includes 3-, 6- and 12-month maturities. The yield on Georgian T-Bills remained high despite a drop in the T-Bill rate during 1998 Q2. Figure 4.2 shows the T-Bill rate and the simple annual yield for 91-day T-Bills. COMMERCIAL BANKS AND INTEREST RATE DEVELOPMENTS Interest rates on GEL-denominated loans fell to 35 per cent in 1998 Q2, about 7 percentage points lower than in 1997 Q1. The average rate on term deposits increased to 20 per cent in June 1998 (10 percentage points higher than in June 1997). The overall deposit rate remained low, reflecting the high share of current accounts and demand deposits in the deposit structure; this situation showed no sign of changing. Figure 4.3: Average Commercial Banks Interest Rates in GEL Terms

0%

10%

20%

30%

40%

50%

60%

70%

Dec

-95

Jan-

96

Feb-

96

Mar

-96

Apr-

96

May

-96

Jun-

96

Jul-9

6

Aug-

96

Sep-

96

Oct

-96

Nov

-96

Dec

-96

Jan-

97

Feb-

97

Mar

-97

Apr-

97

May

-97

Jun-

97

Jul-9

7

Aug-

97

Sep-

97

Oct

-97

Nov

-97

Dec

-97

Jan-

98

Feb-

98

Mar

-98

Apr-

98

May

-98

Jun-

98

T im e depos it ra teLend ing ra teTB -s ra teO ve ra ll depos its ra teC red it A uc t ions

Source: Before October 1997, GET calculations from data provided by the National Bank of Georgia. Since October 1997,