general agreement on - wto.org · general agreement on restricted spec ... i.e. d 469.7 million: -...

TRANSCRIPT

GENERAL AGREEMENT ON RESTRICTED

Spec(87)236 May 1987

TARIFFS AND TRADE

Original: French

WORKING PARTY ON ACCESSION OF TUNISIA

Communication from Tunisia

The following communication, dated 13 April 1987, has been receivedfrom the Permanent Mission of Tunisia.

The Permanent Mission of Tunisia at Geneva presents its compliments tothe GATT secretariat and has the honour to transmit herewith the TunisianGovernment's replies to questions put by certain contracting parties on theoccasion of the first meeting of the Working Party established to examineTunisia's request to become a contracting party in pursuance ofArticle XXXIII of the General Agreement.

Attached here is one copy of a document regarding the objectives ofthe VIIth Development Plan (1987-1991) , together with a notice amendingForeign Trade Notice No. 10.

Available in the secretariat for consultation (Development Division,Room 2010)

'The notice amending Foreign Trade and Currency Notice No. 10 has beencirculated in L/6075/Add.4.

87-0660

Spec(87)23Page 2

REPLIES TO QUESTIONS BY THE UNITED STATES OF AMERICA

Questions 1 and 16

Chapter I - Development of Trade

Concerning the import monopolies referred to, which are still inplace, what percentage of Tunisian imports is currently handled byeach of these monopolies?

What goods are currently State traded in Tunisia? What criteria areused in the selection of suppliers (domestic and import) in Tunisia'sState-trading monopolies? What methods are employed to assure thatthere is no discrimination among import suppliers?

Replies 1 and 16

The import monopolies still in place concern the following products:

- pharmaceutical products

- rice

- sugar, tea, coffee and cocoa beans

- pepper

- tobacco

- petroleum products- oils

- grains

- white cement

- alcohol

The share of these products in total imports in 1986 was 20.38 percent, i.e. D 469.7 million:

- petroleum

- grains

- pharmaceutical products

- oils

- sugar

- tea

- coffee

D 182.6 million

D 120.8 million

D 54.4 million

D 35.1 million

D 26.2 million

D 16.6 million

D 9.6 million

i.e.

i1

It

.i

it

I.

7.92%

5.24%

2.36%

1.52%

1.13%

0.72%

0.41%

Spec(87)23Page 3

- cocoa beans

- pepper

- white cement

- alcohol

- tobacco

- rice

D 1.5 million

D 3.1 million

D 6.1 million

D 1.1 million

D 11.7 million

D 0.9 million

The criteria used by the State monopolies in the selection of

suppliers guarantee equality of treatment and ensure the necessaryconditions for the fair operation of competition. These products are underthe authority of national purchase and sales boards which supervise theproper conduct of import operations and decide on the appropriateness ofeach operation. There is no discrimination in this respect.

The products subject to State trading on export are the following:

Products Value (D million)

- petroleum

- mf.ning products

- olive oil

- wine

% share in Tunisia'sExports

202

26.4

53.5

5.2

14.38%

1.88%

3.81%

0.37%

The share of these products in total exports in 1986 was 20.44 percent, i.e. D 287.1 million.

Question 2

Chapter II - Trade Agreements

Has Tunisia expanded the number of countries with which it haspreferential trade relations since the circulation of L/5566/Add.l?

Reply 2

Since the circulation of document L/5566/Add.1, Tunisia has extendedpreferential trade relations to one additional country - Guinea.

i.e.It

it

it

it

..

0.06%

0.12%

0.26%

0.04%

0.50%

0.03%

Spec(87)23Page 4

Question 3

Please list the current preferential trade arrangements applied toTunisian trade. What is the current scope and level of thepreferences granted?

Reply 3

The preferential trade arrangements currently applying in Tunisia'strade are those concluded with: Algeria, Morocco, Mauritania, Libya, SaudiArabia, Bahrain, the United Arab Emirates, Iraq, Jordan, Kuwait, Syria,Cote d'Ivoire, Nigeria, Senegal, Sudan and Guinea.

The preferences are of two types:

- tariff preferences (tariff reductions or duty-free treatment);- non-tariff preferences (principle of priority supply).

Question 4

Describe the non-tariff import instruments (e.g. quantitativerestrictions, licensing, border charges) that are not applied to tradewith preferential trading partners? What percentage of Tunisianimports/exports benefit from preferential arrangements?

Reply 4

The non-tariff import instruments (e.g. quantitative restrictions,import Licensing ...) are applicable without discrimination to tradingpartners eligible for preferences and to other partners.

The percentage of Tunisian trade covered by preferential arrangementsin 1986 was as follows:

- total trade of Tunisia: 8.6 per cent

- Tunisian imports: 6.7 per cent

- Tunisian exports: 9.5 per cent

Spec(87)23Page 5

Question 5

What is the current status of the Arab common market?

Reply.5

The Arab common market is one of the fundamental objectives of theLeague of Arab States. At the present time, the first phase for attainingthis objective is being implemented, since a trade and tariff conventionwas concluded on 17 February 1981 between the member countries of theLeague of Arab States:

- free movement of products of Arab origin;

- progressive reduction of customs duties and equivalent charges,ultimately leading to duty-free treatment;

- protection of Arab products vis-A-vis like or competing foreignproducts by the introduction of a minimum tariff which can beraised progressively.

Question 6

Chapter III - Foreign trade

L/6075/Add.1, Question 1. It is indicated that the import certificatedoes not require prior administrative authorization. What is thenecessary procedure for acquiring this certificate?

Reply 6

Goods imported under an import certificate are not subject to prioradministrative authorization.

Under this procedure, the importer makes a direct application to hisbank which releases the means of payment required for any import ofliberalized products (see Chapter II of the Foreign Trade and CurrencyNotice - document L/6075/Add.2 of 5 February 1987 as amended by Trade andCurrency Notice No. 10 (Official Gazette No. 63 of 4 November 1986)).

Spec(87)23Page 6

Question 7

L/6075fAdd.1, Questions 1, 2 and 9. Specifically, how does Tunisiaapply its criteria for issuance of an import licence? How much timeis normally necessary to secure an import licence? What agency of theTunisian Government makes the decision? How many agencies or officesmust approve and review each request for a licence? Is there anappeals process? What is the essential difference between the importauthorization and the import card?

Reply 7

Import licence applications are examined and licences issued by theMinistry of Industry and Trade, in accordance with the following criteriain particular:

- bai.ance-of-payments situation;

- market requirements;

- the time required for obtaining an import licence variesaccording to the nature of the product and the urgency ofimporting it;

- import licences are granted by the Ministry of Industry and Tradeand endorsed by the Central Bank of Tunisia;

- there is always the possibility of appealing to the Minister forIndustry and Trade.

The differences between the annual import authorization and the importcard are as follows:

Type of document:

Beneficiary:

Amount:

Period of validity:

Annual import authorization

Manufacturers

Authorities responsible fornational supply of parts, certainessential products, and productsintended for industry

Unlimited

One year, extendable by one yearfor non-utilized amount

Import card

Farmers

Craftsmen

Professional under-takings and smallindustries

D 1,000 per year andper importer

One year, non-extendable but thecard may be renewedonce yearly inrelation with needs.

Spec(87)23Page 7

Question 8

Are all agricultural imports subject to restricted licensingrequirements and quantitative restriction? Why are imports of barley,wheat and corn on the prohibited list? What non-tariff border chargesare applied to agricultural imports? Are these taxes also applied todomestic agricultural output?

Reply 8

Most agricultural imports are subject to licencing, because of theirstrategic character.

Imports of barley, wheat and maize are not prohibited but requireprior authorization from the Ministry of Industry and Trade. Theseproducts are under the authority of the National Purchase Board whichsupervises the proper conduct of import operations.

The non-tariff charges imposed on certain agricultural products arethe following:

- municipal slaughter charge on imported meat (specific toimports);

- import charge on vegetables and fruit (aC valorem on imports anddomestic regime);

- professional contribution on preserved foodstuffs (ad valorem onimports and domestic regime);

- veterinary sanitary charge (specific to imports and domesticregime);

- charge on eggs and poultry (ad valorem on imports);

- single charge on wine, beer and alcoholic beverages (ad valoremon imports and domestic regime).

Spec(87)23Page 8

Question 9

Please describe current Tunisian regulations concerning the ability ofenterprises to import. What type of enterprises are covered by theregulation? Are certain sectors, industries or products identifiedfor continued protection? If so, which ones, and based on whatcriteria?

Reply 9

The Tunisian regulations regarding imports are laid down in thefollowing texts:

1. Currency notice

- Foreign Trade and Currency Notice No. 10, as amended by theNotice of 4 November 1Sd6, constitutes not only a set ofregulations but also a practical guide for the use of importersand exporters.

- It codifies the principal rules governing the realization of andpayment for imports and exports of goods from and to thefollowing countries, with the exception of countries with whichTunisia does not maintain relations.

- It specifies the form and content of the foreign trade andcurrency document and the other documents to be annexed thereto,depending on the nature of the operations it covers, anddescribes the way it is prepared, used and issued as well as theconditions governing its domiciliation and period of validity.

2. Notices to importers

The goods that may be imported are listed in Notices to Importerspublished in the Official Gazette of the Republic of Tunisia indicating therelevant procedures.

The lists of products currently in force are:

- Annex 1 (new) listing the products liberalized for import -notice to importers and exports published in the annex toOfficial Gazette No. 13 of 20 February 1987.

- Annex 2 listing the products under import quota:

This list, which dates from 1981, is no longer applied and theproducts included in it are now subject to import licensing,without any quota restriction.

'Annex 1 listing the products liberalized for import has beencirculated in document L/6152.

Spec(87)23Page 9

It should be noted that products not included in Annex 1 areimported under an import licence.

- The right to import under the procedures laid down in CurrencyNotice No. 10 mentioned above is granted to any natural or legalperson whose occupation entails the use or sale of the product tobe imported and who possesses a customs code number.

- While there are no production sectors or branches nor specificproducts designated as eligible for permanent protection,protection can nevertheless be granted to nascent industries inaccordance with Article XVIII of the General Agreement.

Question 10

What level of export activity is required to permit an enterprise toimport? If an enterprise does not export, is it allowed to import?How long does Tunisia intend to maintain these restrictions?

Reply 10

All enterprises which fulfil the conditions laid down in theregulations in force can be authorized to import, regardless of whetherthey are exporters or are limited to the domestic market.

However, industrial undertakings, 15 per cent or more of whoseturnover is accounted for by exports, may import raw materials andsemi-manufactures used exclusively in their activities under the importcertificate procedure.

Question 11

L/6075/Add.1, Question 5. What portion of current Tunisian importsare covered by the items listed in Annex 1 (i.e. imported freely)?

Reply 11

The products included in Annex 1 (new list of products liberalized forimport, published in Official Gazette No. 13 of 20 February 1987) accountfor 23 per cent of Tunisia's imports in 1987.

1L/6152

Spec(87)23Page 10

Question 12

L/6075/Add.1, Questions 6 and 7. Please specify which GATT ArticlesTunisia intends to invoke to justify its quantitative importrestrictions and prohibitions (e.g. Article XI, XII, XVIII, XIX orXX)?

Reply 12

To justify its quantitative restrictions, Tunisia intends to invokethe relevant provisions of the General Agreement, in particular Part IVthereof.

Question 13

L/6075/Add.1, Question 10. Please answer Question 10. How manytariff lines (and what per cent of trade) are subject to importlicensing restrictions? What portion of Tunisian imports areaccounted for by the items listed in Annex 2 (items under importquota)? What percentage of tariff lines are associated with theproducts listed in Annexes 2 and 3 (items under import quota andprohibited)?

Reply 13

Evaluation of the degree of liberalization or restriction of Tunisia'sforeign trade regime in relation to tariff line criteria is not meaningful.

Tunisia's regulations lay down the following special provisions:

1. Manufacturing industries whose production is intended for export maybe authorized to import freely the goods needed for their producingactivities (Decree Law No. 85.14 of 11 October 1985, Official GazetteNo. 73 of 18 October 1985).

2. Parts and accessories intended for incorporation in articles used bymanufacturers, agricultural producers, hoteliers, hospital establishmentsand other undertakings which furnish services and likewise equipment goodsduly approved by the Investment Promotion Agency, the AgriculturalInvestment Promotion Agency or the Sub-Committee on Tourism Development,may be imported under an import certificate (Official Gazette No. 13 of20 February 1987).

3. Industrial undertakings, 15 per cent or more of whose turnover isaccounted for by exports, may import raw materials and semi-manufacturesused exclusively in their activities under the import certificate procedure(Official Gazette No. 13 of 20 February 1987).

Spec(87)23Page 11

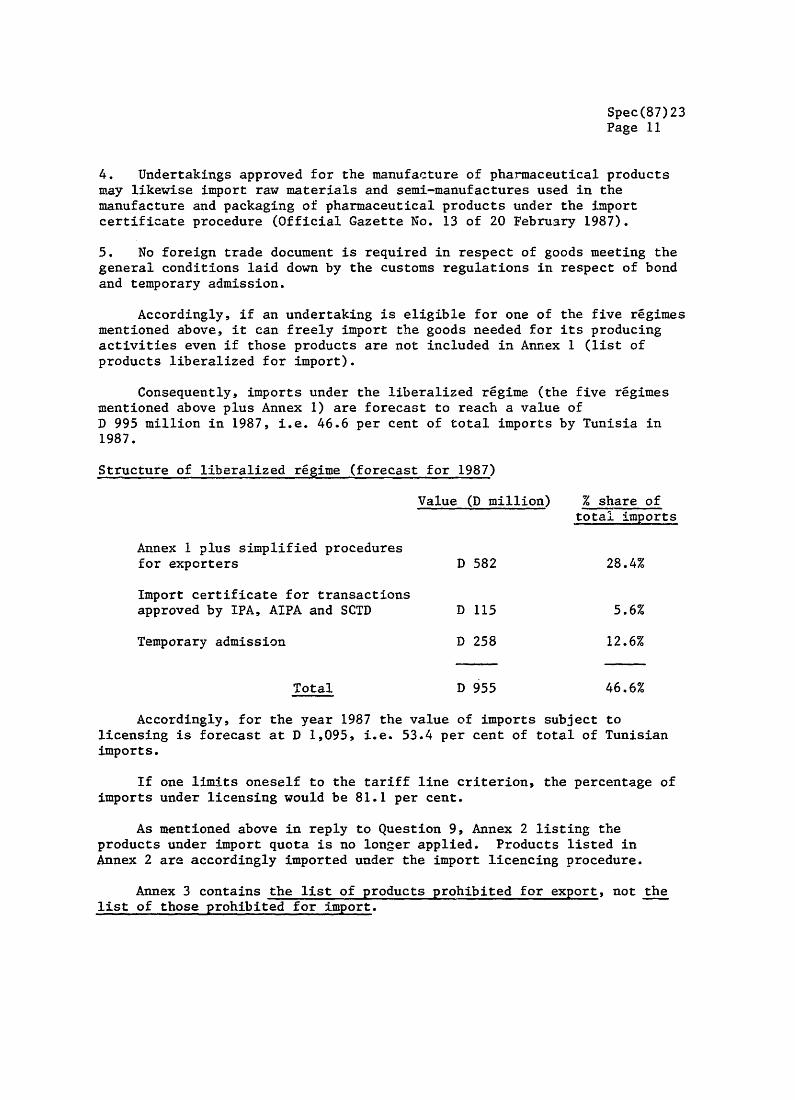

4. Undertakings approved for the manufacture of pharmaceutical productsmay likewise import raw materials and semi-manufactures used in themanufacture and packaging of pharmaceutical products under the importcertificate procedure (Official Gazette No. 13 of 20 February 1987).

5. No foreign trade document is required in respect of goods meeting thegeneral conditions laid down by the customs regulations in respect of bondand temporary admission.

Accordingly, if an undertaking is eligible for one of the five regimesmentioned above, it can freely import the goods needed for its producingactivities even if those products are not included in Annex 1 (list ofproducts liberalized for import).

Consequently, imports under the liberalized regime (the five regimesmentioned above plus Annex 1) are forecast to reach a value ofD 995 million in 1987, i.e. 46.6 per cent of total imports by Tunisia in1987.

Structure of liberalized regime (forecast for 1987)

Value (D million) % share oftotal imports

Annex 1 plus simplified proceduresfor exporters D 582 28.4%

Import certificate for transactionsapproved by IPA, AIPA and SCTD D 115 5.6%

Temporary admission D 258 12.6%

Total D 955 46.6%

Accordingly, for the year 1987 the value of imports subject tolicensing is forecast at D 1,095, i.e. 53.4 per cent of total of Tunisianimports.

If one limits oneself to the tariff line criterion, the percentage ofimports under licensing would be 81.1 per cent.

As mentioned above in reply to Question 9, Annex 2 listing theproducts under import quota is no longer applied. Products listed inAnnex 2 are accordingly imported under the import licencing procedure.

Annex 3 contains the list of products prohibited for export, not thelist of those prohibited for import.

Spec(87)23Page 12

Question 14

Does acquisition of an import licence guarantee availability offoreign exchange, or is a separate exchange licence procedurenecessary?

Reply 14

The import licence is a foreign trade and currency document necessaryfor carrying out import operations and the relevant financial settlements.The fact of obtaining an import licence entitles the importer to purchasethe necessary foreign exchange.

Question 15

Please describe the current Tunisian foreign-exchange allocationregime.

Reply 15

In accordance with the currency and foreign trade regulations, theforeign exchange needed for payment of various transactions with othercountries is obtained from the approved intermediary banks with which thefinancial document is domiciled or for which those banks have receiveddelegated authority from the Central Bank. The approved intermediarybanks, which are moreover obliged to transfer their foreign exchangereceipts to the Central Bank, purchase from the latter the foreign exchangeneeded for the transaction. The purchase and transfer of foreign exchangeis carried out by the approved intermediaries at the exchange rates fixedeach day by the Central Bank.

Question 17

What relationship is there between Tunisia's internal price controlsand import protection? Are import prices covered by Tunisia's pricecontrols?

Reply 17

The Tunisian authorities have embarked on a policy of progressiveliberalization of agricultural producer prices.

This policy is to be extended to the manufacturing sector. Inparticular, the intention is to eliminate price controls inwell-established industries.

For import prices, the normal price control system is applied at themarketing stage.

Spec(87)23Page 13

Question 18

Please describe the distribution of Tunisian tariff levels, by tariffline and by trade coverage.

Reply 18

Attached here are tables giving the breakdown of tariff levels bycustoms duty rates in respect of trade in 1986 (Table I, page 2).

Question 19

Does Tunisia still apply minimum and general tariffs according to theinformation supplied in L/5566/Add.1? What are intermediate tariffs?To whom might they be applied? What is the legal status of the threetypes of tariffs at the present time? What percentage of Tunisianimports is currently covered by each category of tariffs at thecurrent time? What percentage will be covered after Tunisianaccession to GATT? What percentage is currently covered by "generaltariffs"?

Reply 19

Tunisia still applies minimum and general tariffs, as indicated indocument L/5566/Add.l. Although the intermediate tariff is provided for inthe Customs Code, it has never been applied. It constitutes a lowering ofthe general tariff. Article 5 of the Customs Code stipulates that inrespect of imports, the customs tariff comprises the minimum tariff and thegeneral tariff. The general tariff is applicable to goods not eligible forthe minimum tariff. Certain goods may be subject to intermediate tariffs,at rates between those of the general tariff and the minimum tariff.

Tariff Laws No. 59-95 of 20'August 1959 and No. 73-45 of 23 July 1973fixed the general tariff at three times the rate of the minimum tariff, asindicated in document LI/5566/Add.1, page 20. At the present time, thegreat majority of imports are subject to the minimum tariff.

Question 20

What are Tunisia's future plans concerning the structure and level ofits tariff schedule?

Reply 20

On 24 June 1986 Tunisia signed the International Convention on theHarmonized Commodity Description and Coding System, concluded at Brusselson 14 June 1983. That Convention was ratified by Law No. 87-2 of6 February 1987. Accordingly Tunisia will apply that Convention on thedate stipulated therein.

Spec(87)23Page 14

Question 21

Are there any additional products exempted from customs duties?

Reply 21

The regime of temporary admission, bond and drawback (refund ofcustoms duties upon re-export) are at present the only ones under whichgoods can be imported with suspension of customs duties or duty free.There are no lists of products eligible for these advantages. In general,raw materials, semi-manufactures and equipment goods are imported underthese regimes.

Question 22

Please describe in more detail how Tunisian countervailing measuresand anti-dumping practices described in the answer to Questions 16 and17 are consistent with Article VI of the General Agreement. DoesTunisian law provide for granting the injury test in these cases? Howare margins calculated that will not exceed the level of the subsidyor margin of dumping?

Reply 22

Article 11 of the Customs Code will only be applied when inconsistentwith international treaties and agreements which Tunisia has signed or maysign in the future. This is the case of the General Agreement. In theevent that Tunisia accedes definitively to the General Agreement, theprovisions of Article VI will be applied.

Question 23

Does Tunisia have legal provisions that correspond to Article XIX ofthe General Agreement? Does Tunisian law provide for the injury testin such cases?

Reply 23

Tunisia has no legal provisions that correspond to Article XIX of theGeneral Agreement.

However, under Law No. 76-18 of 21 January 1976, the Minister for theNational Economy may prohibit or restrict the import of goods subject toconditions laid down in a decree.

Spec(87)23Page 15

Question 24

Please describe in more detail the method of customs valuation used.Does Tunisia apply levels of valuation for imports specified inofficial regulations?

Reply 24

At present, Tunisia applies the Brussels definition of value(convention of 15 December 1950). In regard to primary products,international prices are applied. Tunisia is preparing its accession tothe GATT Agreement on Customs Valuation.

Question 25

Is the customs formality tax an import fee related to customs costs(i.e. a customs user fee)? If so, why does the level of applicationvary on classes of products? Does Tunisia believe that an ad valoremcustoms fee is consistent with the provisions of Article VIII?

Reply 25

The customs formality tax is indeed a fee related to the cost ofservices rendered by the customs administration. It is charged in relationwith the final destination of the product, in an amount indexed to thevalue of the product so as to spread it equitably among all operators. Therate of the tax is lower on exports than on imports, in order to encourageexports.

Question 26

What products are exempted from the production tax? From theconsumption tax? Is the tax on services levied on all servicesperformed in Tunisia?

Reply 26

The tax on services is levied on commercial operations, other thansales, carried out in Tunisia. A service is considered to be performed inTunisia when the service rendered, the right assigned or the object rentedare used or worked in Tunisian territory.

Attached hereto is a list of products exempted from production tax(Tables II, II bis and II ter, pages 29-36) and a list of products subjectto consumption tax (Tables III, III bis and III ter, pages 37-64).

Spec(87)23Page 16

REPLIES TO QUESTIONS BY CANADA

Question 2

Under what provisions of the GATT does Tunisia justify importprohibition of over one hundred classes of resource-type commodities,including wood and wood-pulp products?

Reply 2

In general, there are no provisions prohibiting the import ofresource-type commodities.

As regards the products mentioned, logs and wood-pulp have beenliberalized for import (Notice to Importers and Exporters regarding Annex 1(new) listing the products liberalized for import, published in OfficialGazette No. 13 of 20 February 1987).

Question 3

Page 11 of document L/5566/Add.1 refers to the convention oninter-Arab co-operation which recommends "protection of Arab productsvis-A-vis similar competing foreign products by the introduction of aminimum tariff that can be gradually increased". How does Tunisiareconcile such a recommendation with the provisions of Articles I andII of the GATT?

Reply 3

The convention on inter-Arab co-operation concluded among the Arabcountries is a regional arrangement among less-developed contractingparties with a view to the elimination of customs duties and non-tariffmeasures on products originating in the member countries.

These provisions are consistent with the enabling clause (Decision ofthe CONTRACTING PARTIES) of 28 November 1979, paragraph 2(c)).

Question 4

The reply to Question 23 of document L/6075/Add.1 refers to non-tariffpreferences within Tunisia's preferential agreements. What kind ofnon-tariff preferences are incorporated in these agreements?

Reply 4

The non-tariff preferences concern the principle of priority supply.

IL/6152

Spec(87)23Page 17

Question 5

Is the 5 per cent customs formalities tax imposed on imports referredto in Question 21 of document L/6075/Add.1 related strictly to theadministrative cost of processing imports? Why does the rate of thistax differ between imports and exports?

Reply 5

The customs formality tax is indeed a fee related to the cost ofservices rendered by the customs administration. It Is charged in relationwith the final destination of the product, in an amount indexed to thevalue of the product so as to spread it equitably among all operators. Therate of the tax is lower on exports than on imports in order to encourageexports.

Question 6

What are the specific exceptions to the application of Article XIII tothe Tunisian system of import and export controls referred to in thereply to Question 4 of document L/6075/Add.l?

Reply 6

In principle, the Tunisian import regulations are consistent withArticle XIII of the General Agreement.

Question 7

How does the system of State trading relate to the import regime andimport documentation requirements? What specific products are subjectto State-trading monopoly? To what extent does the TunisianGovernment import goods and services on behalf of individuals,businesses and non-governmental organizations? Does the Governmentdetermine the price or tender system for such orders?

Reply 7

In Tunisia, State trading is under the authority of national purchaseand sales boards which supervise the proper conduct of import and exporttransactions and the free operation of competition.

Spec(87)23Page 18

The State monopolies apply to the following products:

1. Imports

Value (D million) % share of total imports

Coffee

Pharmaceutical products

Alcohol

Pepper

Oils

Tea

Sugar

Cocoa beans

Tobacco

Grains

Petroleum

Rice

White cement

2. Exports

Value (D million) % share of total imports

Petroleum

Mining products

Olive oil

Wine

202.0

26.4

53.5

5.2

14.38

1.88

3.81

0.37

Question 8

Does Tunisia intend to adhere to any of the GATT codes?

Reply 8

Tunisia is already a party to two of the Tokyo Round codes (the Code

on Technical Barriers to Trade and the Arrangement Regarding Bovine Meat).It is preparing its accession to the customs valuation code. Tunisia'saccession to the other codes will be examined case by case by the Tunisian

authorities w'hen the procedure for its full accession to the General

Agreement has been finalized.

9.6

54.4

1.1

3.1

35. 1

16.6

26.2

1.5

11.7

120.8

182.6

0.9

6.1

0.41

2.36

0.04

0.13

1.52

0.72

1.13

0.06

0.50

5.24

7.92

0.03

0.26

Spec(87)23Page 19

Question 9

With reference to page 24 of document L/5566/Add.1, under whatcircumstances is authorization for payment of invisible transactionsrefused by the Central Bank of Tunisia?

Reply 9

In order to ensure optimum allocation of foreign exchange resources,which are scarce, the Central Bank of Tunisia has responsibility forexamining files regarding payment of invisible transactions. Such paymentsare authorized when they are considered useful from the social and economicaspect in accordance with the objectives set by the authorities in thedevelopment programme. In the evp-nt that the service to be paid for is notconsidered justified in terms of social and economic priorities, or thatthe service could be furnished in Tunisia, the Central Bank can refuse toauthorize payment.

Question 10

In view of the products listed in Annex 2 of document L/6075/Add.1,does Tunisia intend to sign the MFA?

Reply 10

The list of products under import quota (Annex 2) is no longerapplied. Accordingly, the products included in that list are now importedunder licence.

Replies to questions put by Canada at the first meeting of the WorkingParty on the accession of Tunisia on GATT

Question

Do Tunisia's foreign trade regulations contain a list of productsprohibited for import? If so, can it be made available to us?

Reply

Tunisia's foreign trade regulations do not contain any list ofproducts prohibited for impart.

Nevertheless, the customs legislation stipulates that certain productsare absolutely prohibited for import, in particular the following:

- Narcotics- Orpiment- Saccharine- Counterfeit goods- Goods bearing false manufacturers' marks- Absinthe and similar liqueurs- Anethol or aniseed essence

Spec(87)23Page 20

Question

On what basis does the Administration grant an import licence?

Reply

Imports of goods fake place under trade agreements which Tunisia hasconcluded with foreign partners, Government import programmes, andliberalization measures or restrictions in respect of certain products.

The goods that may be imported are the subject of Notices to Importerspublished in the Official Gazette.

Question

Does the Tunisian Government publish quotas in respect of textiles andclothing?

Reply

Annex 2 to document L/6075/Add.1 listing products under import quotais no longer applied, and all the products mentioned in the list are nowsubject to import licensing without any quota restriction. Accordingly,there are no quotas to publish.

Spec(87)23Page 21

REPLIES TO QUESTIONS BY THE NORDIC COUNTRIES

Question 1, 2, 3 and 5

1. We understand that Tunisia has an eight-point programme with theIMF. It would be of great interest to receive detailedinformation on how the IMF programme affects the trade regimetoday and in the future.

2. The main document on Tunisia's trade regime is now more thanthree years old. We would welcome an update which points to anychanges introduced in 1983-86. Of particular interest arechanges in foreign exchange regulations, import licensingprocedures and countertrade practices. More general informationon Tunisia's agricultural and industrial policy would also beappreciated.

3. Tunisia's import administration appears somewhat complicated.Have changes been introduced in the past years? It seems that atpresent four different documents exist. Is any simplificationforeseen?

5. We would like to receive information on any planned changes inthe trade regime as a result of the economic reform programme.

Replies 1, 2, 3 and 5

.The economic recovery programme drawn up by the Tunisian Governmentprovides, inter alia, for progressive liberalization of foreign trade. Forachieving this the two principal measures will be the following:

- relaxation of quantitative import restrictions;

- rationalization of import duties.

As regards relaxation of quantitative restrictions, the measures takenin late 1986 and early 1987 are as follows:

A. Parts and accessories intended for incorporation in articles used bymanufacturers, agricultural producers, hoteliers, hospital establishmentsand other services undertakings may be imported under an import certificate(Official Gazette of 14-17 October 1986).

B. Industrial undertakings, 25 per cent or more of whose turnover isaccounted for by exports, may import raw materials and semi-manufacturesused exclusively in their activities under the import certificate procedure(Official Gazette of 14-17 October 1986).

C. Equipment goods approved by the Investment Promotion Agency, theAgricultural Investment Promotion Agency or the Sub-Committee on TourismDevelopment, are imported under an import certificate (Official GazetteNo. 63 of 4 November 1986).

Spec(87)23Page 22

D. Reduction from 25 per cent to 15 per cent of the level above whichindustrial undertakings that export part of their production may import rawmaterials and semi-manufactures used exclusively in their activities underthe import certificate procedure.

E. Liberalization of raw materials and semi-manufactures for undertakingsapproved to manufacture pharmaceutical products.

F, Inclusion of new products in Annex 1 listing products liberalized forimport (Official Gazette No. 13 of 20 February 1987).

As regards the currency regime, the principal changes made between1983 and 1986 are the following:

- Decree Law No. 85-14 of 11 October 1985 for the encouragement ofexport industries, which revoked and replaced Law No. 72-38. Theamounts in convertible dinars credited to the business travelaccounts of the resident undertakings referred to by theabove-mentioned Decree Law may be used freely for that purpose,subject to a maximum amount of D 6,000 annually for eachundertaking, with the possibility of carrying over to theensuing year any unused availabilities, subject to a maximum ofD 10,000.

- Law No. 86-85 of 1 September 1986 for the promotion of TourismInvestment.

- Law No. 85-108 authorizing the establishment in Tunisia, subjectto prior authorization by the Ministry of Finance and the CentralBank, of non-resident financial and banking institutionsoperating essentially with non-residents.

Question 4

At the Working Party's first meeting a discussion on "prohibitedproducts" (as specified in the annexes to Tunisia's tariff schedule)took place. We would welcome a comprehensive explanation of how theserules are implemented. It seems that products, for which a formalimport prohibition exists, nevertheless are imported.

Reply 4

Annex 1 to document L/6075/Add.1 listing the products liberalized forimport has been extended to additional products (Official Gazette No. 13 of20 February 1987).

Annex 2 regarding products under import quota is no longer applied andthe products listed therein are now subject to licensing.

As regards Annex 3, this concerns products prohibited for export, notfor import, as mentioned erroneously in the English version ofdocument L/6075/Add.l.

1L/6152

Spec(87)23Page 23

REPLIES TO QUESTIONS BY JAPAN

Question 1

The present criteria to grant import licences is lacking intransparency and the licensing system is not operated equally to allapplications (e.g. import quota for automobiles is allocatedpreferentially to the import from the special region).

If the Government of Tunisia intends to change the licensing system,how will it be improved?

Reply 1

The criteria used in issuing import licences are applied in the samemanner in respect of all requests.

Non-tariff import policy instruments are applied without anydiscrimination to trading partners enjoying preferential treatment as wellas to others.

The Government intends to liberalize its foreign trade gradually,mainly by reducing quantitative import restrictions.

Question 2

Normally, it takes a long time to get an import licence. Does theGovernment of Tunisia intend to improve the procedure of licensingsystem for simplification and efficiency of administration?

Reply 2

The procedure governing the issue of licences is described in ForeignTrade and Currency Notice No. 10 (document L/6075/Add.2 of 5 February 1987)as amended on 4 November 1986 (Official Gazette of the Republic of Tunisia,No. 63 of 4 November 1986).

This Foreign Trade and Currency Notice constitutes not only a set ofregulations governing import procedures but also a practical guide for theuse of importers.

ln practice, licences are issued in the light of foreign currencyavailability and the protection granted to domestic industry.

The procedures governing the issue of licences will be liberalized andsimplified in accordance with a programme that takes into accout foreignexchange availability and the gradual reduction of protection of theTunisian economy.

Spec(87)23Page 24

Question 3

Freely imported items are quite limited.

Is it the intention of the Government of Tunisia to enlarge the scopeof freely imported items?

Is it the intention of the Government of Tunisia to mitigate importquotas?

Reply 3

Products that may be freely imported (Annex 1) will account for over28.4 per cent of Tunisian imports in 1987.

The products that can be freely imported (Annex 1 + authorization +temporary admission + export procedures) will amount to 46.6 per cent oftotal Tunisian imports in 1987.

Questions 4 and 5

What items are subject to countertrade and offset?

What is the ratio (percentage) of offset?

Does the Government of Tunisia intend to reduce the number of theseitems subject to countertrade and offset?

Reply to 4 and 5

Countertrade is one of the many instruments used by the TunisianGovernment to expand trade with developing countries and States that callfor the establishment of a trade programme.

Countertrade has not been institutionalized as a system in Tunisia.

The Tunisian Government intends to reduce the number of productssubject to countertrade operations.

In any event, offset and countertrade operations account for only amodest proportion of Tunisia's total trade and their number is declining.

Such operations will in future be confined to:

- the automobile sector;

- countertrade with countries requesting such trade.

Spec(87)23Page 25

Question 6

The Government of Tunisia raised tariff rates substantially after itsapplication for accession to GATT.

What is the reason for this tariff rise?

Does the Government of Tunisia intend to proceed with bilateralnegotiations based upon the tariff rates at the time of itsapplication for accession?

Reply 6

On the contrary, Tunisia has reduced customs duties under itsFinance Law for the 1987 financial year. At the present time the maximumtariff rate is 45 per cent.

The Tunisian Government will embark upon bilateral negotiations on thebasis of the present customs tariff, namely, the 1987 tariff.

TABL

EI

IMPO

RTS

AMD

CUSTOMS

RECEIPTS

BYRA

TE-

1986

-0jCA

.TAR;.EF

...B

ATE,o........

..........

..............

................................

.9....s9.4MNC

.pAT.1TV.

....

..

........

Qm

.\,

.,,,

A/,D).

(.)

'M'

!.....

A...I)

,7%1n.6f

i~a9.t2.1...Q.

9i.^tp.g?6s~r.79.~

7^6iN

...

....

....

~.AR

??%:

2..

....

....

..A2^6s)

.4*

,,.,..9R:S7?

?1~s6

02W,6,

P1...

..592

Cr.

f..

.1.4

.1.?7.

.3.A

LJ0.........

..::........

...

....

4j

.

......

....P..

70AlP.

P.7<'§

.7A!MOA.Rt.9

23.9RR

.48^

A......

lell

.,P7^

.5.§f..5.

1.R.l

fM...Rm

9J~

~~~~

~~~~

~~A~...

.1§9.8..

.....

.9...

...M1Q.

4.7..,67*927

48*

...........I...t.t..I

P.Q@4.........

I.86AP9

97%..

V..1

,.K

.PQE59

n~,,2r

.~~~~.~~~

..?~~~~~~~

.I~~~~~

.~~~~

~~

~7.A51~

IV

12:

.........

'I.Q2

I............

.49.548..

..1@*.0?.i

..Q.f.i

g..

p397

7595

44

.8

.

,,,,

.,,,

14,,

,,......

.*..

?...

....

...Q

..'

....

...

....

..7

*,5.

?..p.Ct?9s'

.1i73

2...........

U..94

-.'.

6..1.1217

P.Q

....

......

.).?

723..,

,,,,^g

,,,2f3

S6,,,.4.?

,R..,,

ssq**,

,I.ps

;.7i83O5.

P68

1,73,

......................... 8P.7Q.5ff

........

19q0.

Q69........'

9..Q9....

ON

....

19:

f...13.7..

Uiq:

s1

742

:A

......

!.937P.45.Q§.39A.

R.

go..........

..............

....

....

..........1

A9P

..,Al

?.59

~~~~~

..~~~~~~....

.. ......

............

............4?...?...%..

?.l

%

:~~~~~~~~~~~~~~~~~~~~~~~M

..6P9

.~~~~........

,i1

^p

.5.

........

.......................

.....

..

.2f.7.2

.tRd

,...

9t13

t.60

^1s

«4~f

io-.

,,.1.

,,,2

4,e67

.4

2g,

~..'...

.'.P.Ap

',13,

4°

'Q

',,7

!..........N

O.........

A..

...

,, J.,1̂p,%,,,,,,.5n81

44,f,,,L

Mn.fi

..........

7.Q

.4%.:

...Z

Y.7.9

LAI

1.1Q71§0.1.

.?.

..?.,5

..?.

....

..1,

,'-.R,

,...

...A.M

5.73.0

..Q'

,372

....

...

..a7...

....

....

....

....

...

.!

40

V..

....

....

....

,,,,

.,.,

.,,,

.,.,

.o~

,,,,

,13?

R06E

~i,,

,,6,

@.2s

..... A..

28'

....

.',

L2g

.......IMAM...

...4.8.A

..1..

..,,64,

3,2,.A

..............

0....9....0....%

14456648

0*0

..

....,...

......

....

....

....

....

....

....

....

....

....

....

....

...

.449.

.a.,,A$',,,,gi86,.*

oos

.ww.!3R7,3s,

.,4^§,,

........

..+:.

r.....

~~~14.?70!..

82,AP

.A!

.I

.!.w.

6.i3

...

'53°

.'.

.t,,4,

p,,,,2

,'.........

t-,,,r4,,,,pA

IMPORTS

AND

CUSTOMS

RECE

IPTS

BYRATE

-1986

......n

**,*

.s.

....61

6*i.

...>.g.)

I~

1~s.e

~A~.......A

..44

....~jQPA

:79.

.....

.....

....?4

?.....

9C.......

.~.h

Q91.

~

..........

47..

.~~1

.407

.Q~.

~I7.~.~i

i.9.

1.t3

942'

i29-

Liff

:.

~.L..Q.Q.............4...........

.......7.

*.~~~~........-

IW.~....

.....i~...*...

MM9%

A1"AWI

4..91

,.,.........S

..'~

~4..

1.7~

~3?4

qi.1

.AQ%

:1.6

I237

.4-0

..94

4**..6

3658

223A?~1~~

.........

ft..:....1.7819AW?.:.14

0.~F

.........

9.O..

1.

?§4

p.

i7~16E..:

6,96

~..9....

IAl....?~IP5~5

~.~

......

..qQ1.

0......

1!9A09126

Q091

.~

1.64Q7.JA9-1

.IMW

49.~%.

.715K:....~

4

.fl~

~...?~~361

...~~~

.~~?P

9...

..47-~JA.7.~

....

.....

...

9"..AM

IP

798

,1:

:...

.60

7777

8.0

AQZA

.201.160483.K97

..........

..........

M8.

........I.1

~?.6~2

.~~~.1

k4.~~~

~~9~~.

P.AQ~~

~~~.1.

1f~

......

.657

82QAQ.O

?...~.

20.m

97..........

--

%z~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~~~~

~~~g

7..:.

%4qx~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~u...~

oa~7

....

....

L:.......Q

.1b

4~?

...

....

...6

2..:.

3:.

?.'.

.234

7l7)

.8.9

..1..4......

AL78

......

U8548...:.9Q9

?P4i

?1.7

..:.~~.,77%

.IS.Q

~9

64%29.OA

1....

...A'.

?.1

.1~~

......

~~9

...

9~57~*.

9986

%10

71....

....

2!?!8I83!.0-i.1P

~.........9..Q~..7~47..9.qAO87%.....:2

47..

.....9

QA'

.?0546

5.1-08

........A%

10.

94

3329

0Ai.

..?.

?P1

1~~~.

'~~~0.9.~~~qI31.iK

445J7

q%147O~~

.~~~~~.

1.4P~~~9-W-

J'0j.47P.

9%.Q796

2.....1...Q9

....99

77..Q.

........8J

999~

1.827AL:Q.

ON

517.

PR...j

A.....

.....

......

....

9%1033

0Ot

06640

000

.......AM

PL:.,goi

ng:.....

.....*791

-:.99.XA~~~

~~~~~~~~~~

~~~~~~~~~~

~~~~~~~~~r

%

XCA

CDCD'

(n

IMPORTS

AND

CUST

OMS

RECE

IPTS

BYRATE

-1986

tA

*...

....

....

.17

04884i::83.:

99A97%Ti:

,QgO

3..04

-U5

.....?41.........0Al

.O

..........

.9..

.7~

.3..

.^0b.. .74483.

.9.g

7...

Qo.

............

............

.........

26

24.5

.......

!pa

...

..

..

..

.

?3t:

533747

00oo

z:17

nm41

F;.3

Ori

noGood:

737:7Ap.

046,.

:0

o..................................

............

...........

........................

-;^

TA......

.1.7

OAI

WA.

3Q,O

Or1:

264,;9739

:10..

....

....

....

....

n...

...

.~

~~~~~~~~~~~~2

A

T.,o.1.~3~35

..

.~i

3.02

.............

I....................

.................................

...........

..................

...................

............

...............................

............

................................................................................

.............................................................

..............................................................

_

Spec(87)23Page 29

TABLE II

GOODS EXEMPTED FROM THE PRODUCTION TAX IN 1986IMPORTS

OGNP No.Tariff No. Description of goods From To

Printed books, brochures and similar printed matter.

Newspapers, journals and periodicals.

Newsprint

Cereals

Flour

Meal

Bread

Ships, boats and other vessels, other than pleasureand sports craft, intended for ocean navigation or

fishing and all materials for incorporation in such

ships, boats and vessels.

Fishing equipment and nets for ocean fishing.

Cinematographic films for projection in establish-ments to which the public is admitted againstpayment.

Flours obtained by evaporating a mixture of milkwith sugar and flour, not containing cocoa.

Medicinal milks

Milk, preserved or sweetened, specially treated tofacilitate its assimilation by babies or sickpersons.

Aircraft to be used for air transport and allmaterials for incorporation in such aircraft.

Plants and seeds (cf. Table 1).

Cinematcgraphic films of a cultural or social nature.

49-01 B

49-02

19-02 B

Ex 30-03

Ex 40-02

Spec(87)23Page 30

GNP No.Tariff No. Description of goods From To

Ex 73-21

Ex 84-21

Ex 84-24

84-25 A

84-25 ExB

84-26

84-27

84-28

87-01 Aa

Ex 88-02

Ex 88-03

87-10

87-11

Agricultural greenhouses

Mechanical appliances (whether or not hand operated)for projecting, dispersing or spraying liquids orpowders.

Agricultural and horticultural machinery for soilpreparation or cultivation, with the exception oflawn and sports ground rollers.

Winnowing and similar cleaning machines, egg-gradingand other grading machines for agricultural produce.

Other harvesting or threshing machinery, other thanlawnmowers.

Dairy machinery (including milking machines).

Presses, crushers and other machinery, of a kindused in wine-making, cider-making, fruit juicepreparation and the like.

Other agricultural, horticultural, poultry-keepingand bee-keeping machinery; germination plant fittedwith mechanical or thermal equipment; poultryincubators and brooders.

Agricultural tractors

Agricultural aircraft

Parts for the equipment of agricultural aircraft.

Cycles

Invalid carriages, whether or not motorized or other-wise mechanically propelled.

1This agricultural equipment is generally subject to a lower production taxof 11.11 per cent (10 per cent including all taxes)(Decree No. 77-1118 of31 December 1977) and is exempted from the production tax only if it is importedby duly constituted agricultural service co-operatives.

Spec(87)23Page 31

GNP No.Tariff No. Description of goods From To

90-19 Orthopaedic appliances, surgical belts, trusses andthe like, splints and other fracture appliances,artificial limbs, eyes, teeth and other artificialparts of the body, hearing aids and other applianceswhich are worn or carried, or implanted in the body,to compensate for a defect or disability, with theexception on artificial teeth and dental fittings ofprecious metal or rolled precious metal.

Baggage, whether accompanied or not, of travellersor immigrants.

Articles comprising the chattels of immigrants, aswell as trousseaux or inherited articles which, underthe regulations, are exempt from customs duty.

Articles sent to members of the consular corps whichare exempt from customs duty on an individual basis.

Original works of arts imported by their authors.

The crops of adjacent property owners.

Articles, not available commercially, imported inpostal packages or parcels.

Samples without commercial value.

Gold coin (72-01 A), gold and unworked gold alloysin I-locks, ingots and similar forms, native gold(71-07 A). Silver and unworked silver alloys inblocks, ingots and similar forms, native silver(71-05 A), gold and silver sweepings, waste andscrap (71-11), platinum and unwroixght platinum alloysin blocks, ingots and similar forms (Ex 71-09 Aa).

Consignments of funds, banknotes, lottery tickets,postage stamps imported by the State, revenuestamps, currency (legal tender), stocks and bonds.

Articles taken on by fishing boats or sea-goingvessels that can become part of the ship's suppliessubject to the conditions laid down by theadministration.

Drilling and sounding equipment, if admitted dutyfree.

Spec(87)23Page 32

GNP No.Tariff No. Description )f goods From I To

Tunisian fisheries products.

The production tax and consumption tax on goodsimported temporarily under a suspensory customsregime are suspended.

The following goods which are to be re-exportedwithin a period of six months after manufactureor further processing:

. Sponges of foreign origin, simply washedwith sea water, of the so-called "Venice","Zimogas", "Fine Syries", "Elephants' ears"qualities, imported and re-exported followingpreparation consisting of washing, dressing andcutting.

. Natural raw cork imported for processing intobottle corks, sheets and pieces.

Rutile imported for the production of titaniumdioxide.

. Woollen rags imported for carbonization or tobe taken apart, garnetted and washed.

Alcohol imported by the Alcohol Monopoly forauthorized bonded producers.

Wine imports by the Wines Office.

Imports by distribution enterprises that areproducers of the following petroleum products:27-10 (2710 A, B, C, D, E, F, G, H, I, J, K)

I.

Spec(87)23Page 33

TABLE II BIS

PRODUCTS EXEMPTED FROM THE PRODUCTION TAX IN 1986DOMESTIC REGIME

(1) The sale of printed books, brochures and leaflets as well asnewspapers, journals and periodicals;

(2) The sale of newsprint;

(3) The sale by the State of stamps and stamp-impressed paper;

(4) The sale of cereals, flour, meal and bread;

(5) The sale of fresh milk, not concentrated or sweetened, full-cream orskimmed;

(6) The sale of water under contract, subject to the special tax;

(7) The sale of ships, boats and other vessels, other than pleasure andsports craft, intended for ocean navigation or fishing and of allmaterials for incorporation in such ships, boats and vessels;

(8) The sale of fishing equipment and nets for ocean fishing;

(9) The production of cinematographic films;

(10) The sale of:

(a) flours obtained by evaporating a mixture of milk with sugar andflour, without cocoa

(b) medicinal milks

(c) milk, preserved or sweetened, specially treated to facilitate itsassimilation by babies or sick persons;

(11) The sale of aircraft to be used for air transport and all materialsfor incorporation in such aircraft;

(12) The activities of bodies whose work is recognized to be in thenational interest and authorized by the Minister of Finance;

(13) The sale of plants and seeds;

(14) The production of cinematographic films of a cultural or socialnature;

Spec(87)23Page 34

(15) The sale of agricultural equipment;

(16) The commercial presentation of agricultural products;

(17) The sale of cycles;

(18) The manufacture and sale of equipment and appliances for the use ofphysically handicapped persons.

Source: Handbook of Direct and Indirect Taxes, 1984 (updated on15 April 1984).

Spec(87)23Page 35

TABLE II TER

LIST OF PLANTS AND SEEDS EXEMPTED FROM THE PRODUCTION TAXIN 1986 (IMPORTS AND DOMESTIC REGIME)

1. Seeds of field crops

OatsDurum wheatCommon wheatFenugreekField beans

6. Broad beans7. Lentils8. Maize9. Barley10. Peas

I1. Chickpeas12. Grain sorghum13. Vetches

2. Seeds and seedlings of industrial crops:

Sugar beetBeetCarrhamesCottonCocksfoot

6.7.8.9.10.

Erhata calcinaHennaFlaxCanary grassPyrethrum

11.12.13.14.

Castor beansSesameTobaccoSunflowers

3. Seeds and seedlings of perennial fodder crops:

Canary grassAtriplexBrome grass

4.5.6.

Fescue grassLucerneNapier grass

4. Seeds and seedlings of annual fodder crops:

Fodder beetFodder carrotsFooder kale

4.5.6.

Fodder maizeFodder turnipsFodder peas

7.

8 .

Fodder sorghumClover

5. Seeds and seedlings of market garden crops:

GarlicGroundnutsArtichokes

AsparagusAuberginesGarden beets

Spinach beet

Chards and cardoonsCarrotsRibbed celeryCeleriac

Mushrooms

Chicory

CabbagesCauliflowers

Brussels sproutsCucumbers

18.19.20.21.22.23.24.25.26.27.28.29.30.31.32.33.34.

GherkinsMarrows

PumpkinsCressEndives

SpinachFennel

Broad beansStrawberriesGumboBeans

Lettuce

Corn saladMelons

TurnipsOnionsWatermelon

35.36.37.38.39.40.4.1.

42.43.44.45.46.47.48.49.50.Hi.

ParsleyPeasPimentsDandelion

LeeksWhite beetsSweet peppersPotatoesGiant pumpkinsRadishesHorseradish

RhubarbSalsifyScorzoneriaEndives

TetragoniaTomatoes

1 .

2.

3.4.

5 .

1 .

2.

3.4.5.

1.

2 .

3 .

1.

2.3 .

7.8.9.

OryzopsisRye grassSulla

1.2.3.4.5.6.7.8.9.10.11.12.13.14.15.16.17.

Spec(87)23Page 36

6. Seeds and seedlings of aromatic and other plants:

3. Coriander4. Cumin

5. Ginger

7. Seeds and seedlings of fruit trees:

Citrus fruit trees 5.Fig trees 6.

Pistachio trees 7.

Vines 8.

Quince treesApple treesPear treesPlum trees

9-

10.11.12.

Peach treesCherry treesNectarine treesMedlar trees

1.2 .

CamomileCaraway

1 .

2.3.4.

Spec(87)23Page 37

LIST OF GOODS SUBJECT TO THE CONSUMPTION TAX

TABLE III

Rate: 23%

Tariff Description of goodsheading

06-03

06-04

07-01 ClIa

09-05

13-02 D

13-02 E

16-04 A

18-04

18-06 C

19-08 Ex C

21-02 Aa

21-02 Ab

21-02 B

21-02 Ca

21-02 Ex Cb

22-03

22-05

22-05

B

C

*

Exempt frommedicaments.

Flowers and flower buds

Foliage and branches

Vegetables and plants not for sowing

Vanilla

Resins and gum-resins

Natural balsams

Caviar, caviar substitutes and botargo

Cocoa butter (fat or oil)

Cocoa and chocolate confectionery

Biscuit products containing 20% or more of cocoa

Extracts or essences of coffee

Other extracts, essences or concentrates of coffee

Roasted chicory

Extracts, essences and concentrates of tea

Preparations with a basis of extracts, essences orconcentrates of tea

Beer made from malt

Liqueur wines, mistelles

Sparkling wines

consumption tax when intended for the manufacture of

Spec(87)23Page 38

Tariff Description of goodsheading

22-06 Vermouths and other wines of fresh grapes flavouredwith aromatic extracts

22-09 B Liqueurs and other spirituous beverages

20-01 Unmanufactured tobacco, tobacco --ej.-;e

24-02 A Cigars (including those with cut ends)

24-02 B Cigarettes

24-02 C Other

33-01 Ex Cb Extracts (oleo-resins) of vanilla

33-06 Ex A Perfumes:

- Non-alcoholic liquid perfumes

- Alcoholic liquid perfumes except those containingnot more than 7070 alcohol

- Solid perfumes

33-06 B Products for dental hygiene

33-06 D Other

36-01 A Propellent powders, imported for the State

36-01 B Other propellent powders

36-04 A Percussion and detonating caps for hunting or target-shooting guns

36-05 A Fireworks for entertainment

39-07 B Hand fans and hand screens, including mountings andsheets therefor, imported separately

42-02 A Travel goods

42-02 Ex B { Covers and cases for arms, binoculars, cameras

44-28 Ca Mountings and parts of mountings, of wood, for fansand hand screens

Spec(87)23Page 39

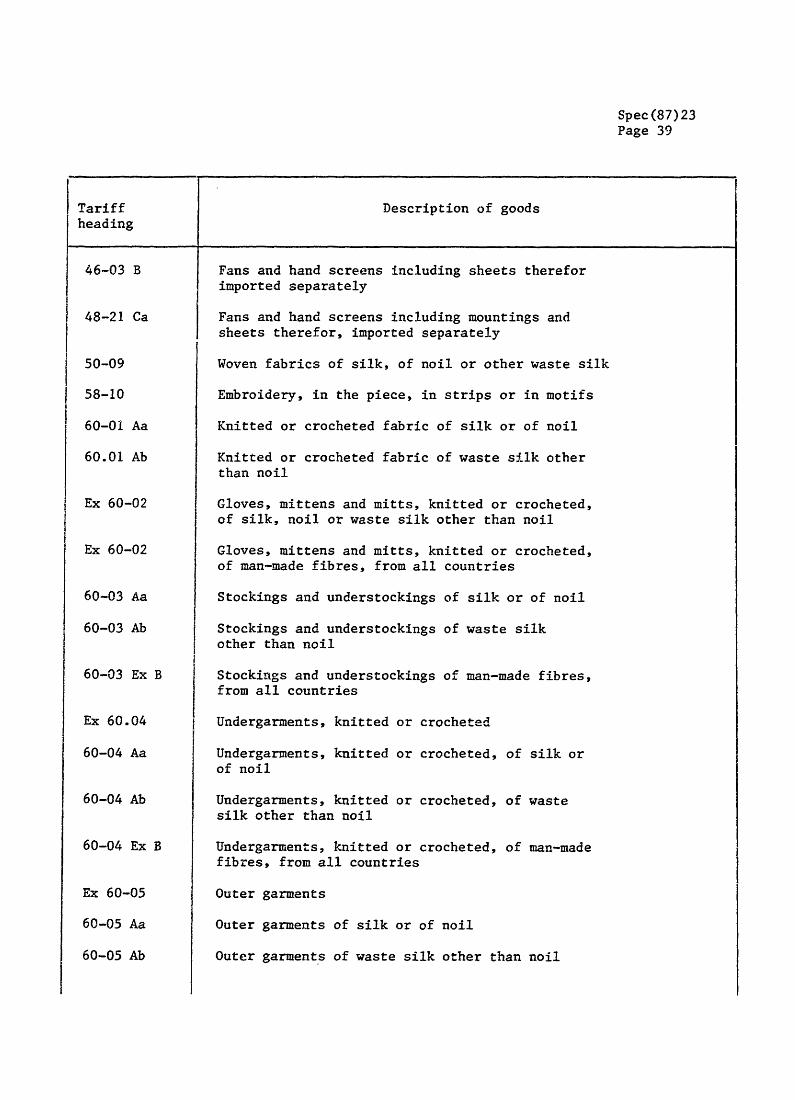

Tariff Description of goodsheading.~~~~~~~-

46-03 B

48-21 Ca

I50-09

58-10

60-01

60.01

Aa

Ab

Ex 60-02

Ex 60-02

60-03

60-03

Aa

Ab

60-03 Ex B

Ex 60.04

60-04 Aa

60-04 Ab

60-04 Ex B

Ex 60-05

60-05 Aa

60-05 Ab

Fans and hand screens including sheets thereforimported separately

Fans and hand screens including mountings andsheets therefor, imported separately

Woven fabrics of silk, of noil or other waste silk

Embroidery, in the piece, in strips or in motifs

Knitted or crocheted fabric of silk or of noil

Knitted or crocheted fabric of waste Silk otherthan noil

Gloves, mittens and mitts, knitted or crocheted,of silk, noil or waste silk other than noil

Gloves, mittens and mitts, knitted or crocheted,of man-made fibres, from all countries

Stockings and understockings of silk or of noil

Stockings and understockings of waste silkother than noil

Stockings and understockings of man-made fibres,from all countries

Undergarments, knitted or crocheted

Undergarments, knitted or crocheted, of silk orof noil

Undergarments, knitted or crocheted, of wastesilk other than noil

Undergarments, knitted or crocheted, of man-madefibres, from all countries

Outer garments

Outer garments of silk or of noil

Outer garments of waste silk other than noil

Spec(87)23Page 40

Tariff Description of goodsheading

60-05 Ex

Ex 60-06

Ex 60-06

60-01 Aa

60-01 Ab

B

61-01 Ex B

61-02 Aa

61-02 Ab

61-02 Ex B

61-03 Aa

61-03 Ab

61-03 Ex B

61-04 Aa

61-04 Ab

61-04 Ex B

61-05

61-05

61-05

Aa

Ab

Ex B

Outer garments of man-made fibres, from all countries

Fabrics of silk, of noil or of other waste silk

Fabrics of man-made fibres from all countries

Men's and boys' outer garments, of silk or of noil

Men's and boys' outer garments, of waste silk other thannoil

Men's and boys' outer garments of man-made fibres, fromall countries

Women's, girls' and infants' outer garments, of silk orof noil

Women's, girls' and infants' outer garments, of wastesilk other than noil

Women's, girls' and infants' outer garments of man-madefibres, from all countries

Men's and boys' under garments, of silk or of noil

Men's and boys' undergarments, of waste silk other thannoil

Men's and boys' undergarments of man-made fibres, fromall countries

Women's, girls' and infants' undergarments, of silk orof noil

Women's, girls' and infants undergarments, of waste silkother than noil

Women's, girls' and infants' undergarments of man-madefibres, from all countries

Handkerchiefs, of silk or of noil

Handkerchiefs, of waste silk other than noil

Handkerchiefs of man-made fibres, from all countries

Spec(87)23Page 41

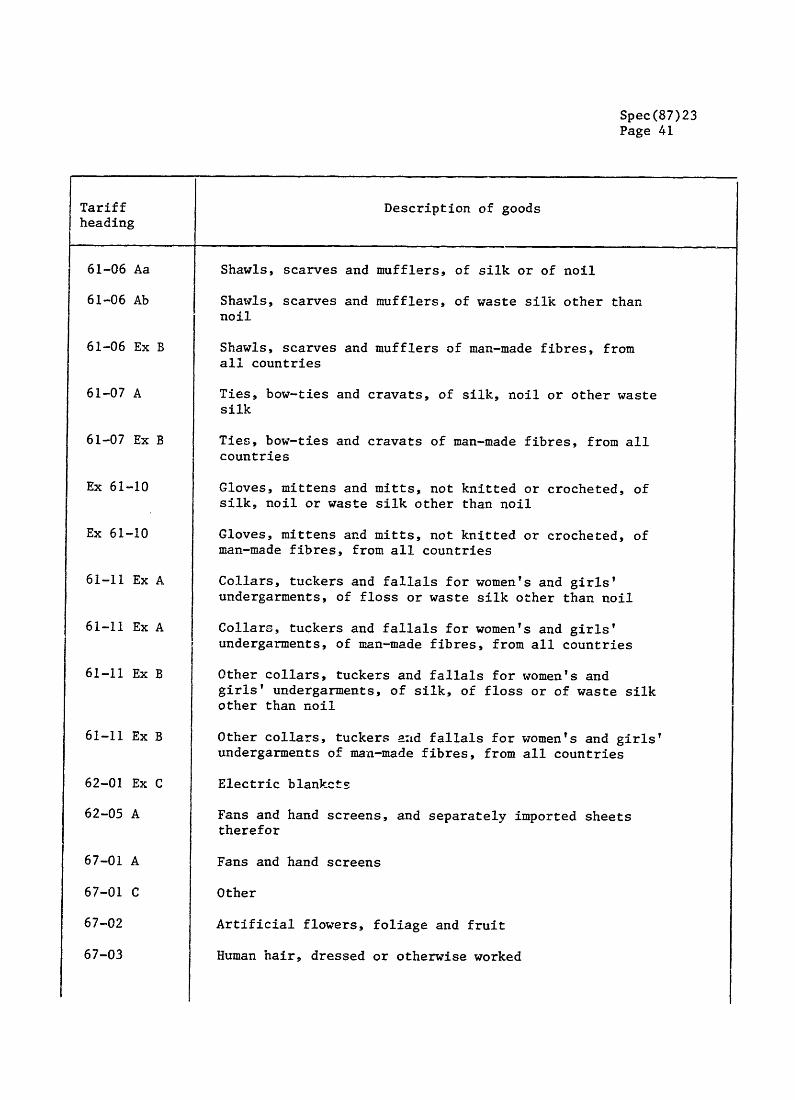

Tariff Description of goodsheading

61-06

61-06

Aa

Ab

61-06 Ex B

61-07 A

61-07 Ex B

Ex 61-10

Ex 61-10

61-11 Ex A

61-11 Ex A

61-11 Ex B

61-11 Ex B

62-01

62-05

67-01

67-01

67-02

67-03

Ex

A

C

A

C

Shawls, scarves and mufflers, of silk or of noil

Shawls, scarves and mufflers, of waste silk other thannoil

Shawls, scarves and mufflers of man-made fibres, fromall countries

Ties, bow-ties and cravats, of silk, noil or other wastesilk

Ties, bow-ties and cravats of man-made fibres, from allcountries

Gloves, mittens and mitts, not knitted or crocheted, ofsilk, noil or waste silk other than noil

Gloves, mittens and mitts, not knitted or crocheted, ofman-made fibres, from all countries

Collars, tuckers and fallals for women's and girls'undergarments, of floss or waste silk other than noil

Collars, tuckers and fallals for women's and girls'undergarments, of man-made fibres, from all countries

Other collars, tuckers and fallals for women's andgirls' undergarments, of silk, of floss or of waste silkother than noil

Other collars, tuckers aad fallals for women's and girls'undergarments of man-made fibres, from all countries

Electric blankets

Fans and hand screens, and separately imported sheetstherefor

Fans and hand screens

Other

Artificial flowers, foliage and fruit

Human hair, dressed or otherwise worked

Spec(87)23Page 42

Tariff Description of goodsheading

_ _ -~~~~~~~~~~~~~~~~~~~~~~

67-04 Wigs, false beards, eyebrows and eyelashes, switchesand the like

69-13 Statuettes and other ornaments, and articles of personaladornment; articles of furniture

70-13 B Crystal ware

70-19 Glass beads, imitation pearls, imitation precious andsemi-precious stones

Ex 71-01 Pearls, unworked or worked, except those for industrialuse

71-02 B Diamonds other than industrial diamonds

71-02 C Other precious stones, strung for convenience oftransport

71-03 B Other synthetic or reconstructed precious or semi-precious stones

Ex 71-04 Dust and powder of natural or synthetic precious orsemi-precious stones, except thatfor industrial use

71-12 Articles of jewellery and parts thereof, of preciousmetal or rolled precious metal

71-13 Articles of goldsmiths' or silversmiths' wares and partsthereof, of precious metal or rolled precious metal

71-14 Other articles of precious metal or rolled preciousmetal

71-15 Articles consisting of, or incorporating, pearls,precious or semi-precious stones (natural, synthetic orreconstructed)

71-16 Imitation jewellery

82-13 A Manicure and chiropody appliances

83-06 A Statuettes

Sports medals, except those made by stamping83-06 Ex B

Spec(87)23Page 43

Tariff Description of goodsheading

83-06

83-06

83-09

84-19

84-40

Ex Ca

Cb

A

Ex A I

A I a

84-40 Ab

84-40

85-06

85-06

85-06

85-06

85-06

85-06

85-07

A II

Ex A

B

Ca

D

E

F

85-15 Ex A I

85-15 Ex Bb

87-02 A I a

87-02 A I b

87-02 A II a

Medals other than for sports

Ornaments

Beads and spangles of base metal

Electrically-heated dishwashers

Washing machines, household type, having a dry linencapacity of less than 2.5 kg.

Washing machines, household type, having a dry linencapacity of 2.5 kg. to 6 kg.

Parts for household washing machines

Floor polishers

Vented hoods

Fans of a diameter of not more than 30 cm.

Food mixers and grinders; fruit-juice extractors

Other electro-mechanical domestic appliances

Parts for electromechanical domestic appliances

Shavers and hair clippers, with self-containedelectric motor

Television receivers, except those for use in thenational television and radio broadcasting system

Other radio-broadcasting receivers, except those for usein the national television and radio broadcasting system

Vehicles of all kinds, other than general purposevehicles with engines other than of the compression-ignition type, except those having a rated power of notnot more than five metric h.p.

Vehicles of ,all kinds, other than general purposevehicles with engines of the compression-ignition type

General purpose vehicles with four doors

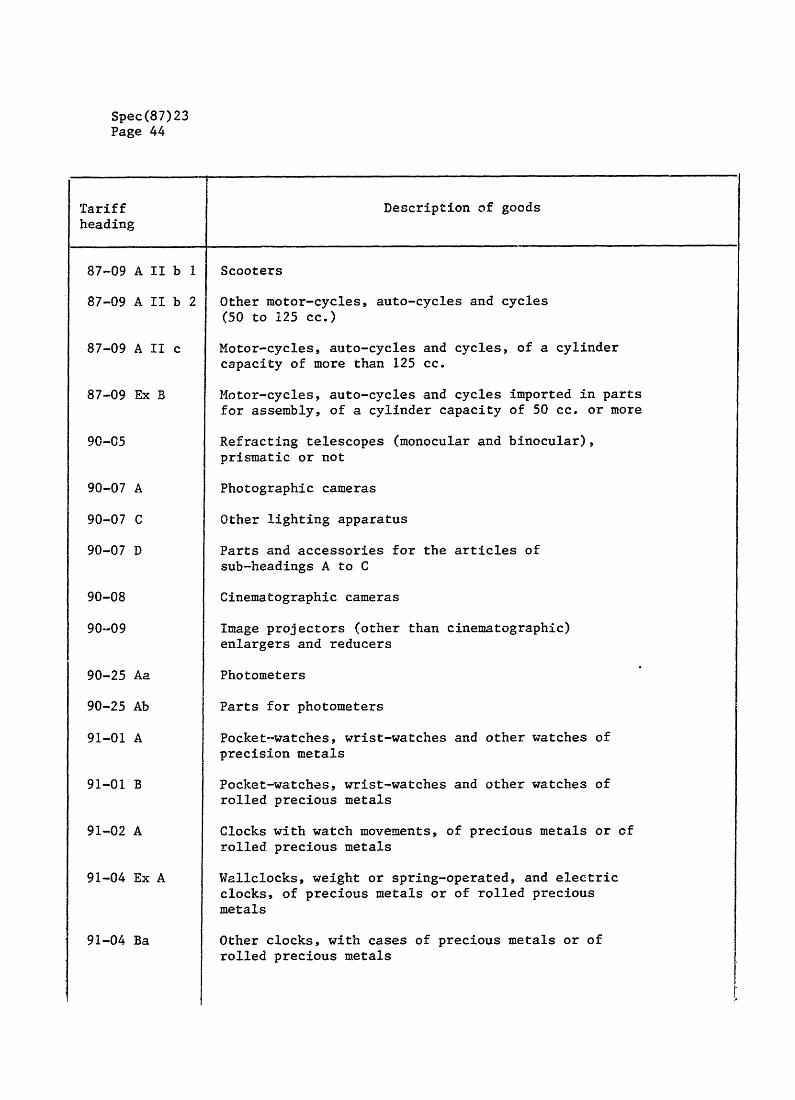

Spec(87)23Page 44

heariff Description of goodsheading

87-09 A II b

87-09 A II b

12

87-09 A II c

87-09 Ex B

90-C5

90-07 A

90-07 C

90-07 D

90-08

90--09

90-25 Aa

90-25 Ab

91-01 A

91-01 B

91-02 A

91-04 Ex A

91-04 Ba

Scooters

Other motor-cycles, auto-cycles and cycles(50 to 125 cc.)

Motor-cycles, auto-cycles and cycles, of a cylindercapacity of more than 125 cc.

Motor-cycles, auto-cycles and cycles imported in partsfor assembly, of a cylinder capacity of 50 cc. or more

Refracting telescopes (monocular and binocular),prismatic or not

Photographic cameras

Other lighting apparatus

Parts and accessories for the articles ofsub-headings A to C

Cinematographic cameras

Image projectors (other than cinematographic)enlargers and reducers

Photometers

Parts for photometers

Pocket-watches, wrist-watches and other watches ofprecision metals

Pocket-watches, wrist-watches and other watches ofrolled precious metals

Clocks with watch movements, of precious metals or ofrolled precious metals

Wallclocks, weight or spring-operated, and electricclocks, of precious metals or of rolled preciousmetals

Other clocks, with cases of precious metals or ofrolled precious metals

Spec(87)23Page 45

Description of goods

Watch cases and parts of watch cases of precious metals,for watches of 91-01

Watch cases and parts of watch cases of rolled preciousmetals, for watches of 91-01

Clock cases and cases of a similar type for othergoods of this Chapter, and parts thereof, of preciousmetals or of rolled precious metals

Other tortoise-shell, mother-of-pearl, ivory and bone

Worked vegetable and mineral carving material, exceptrosin

Tariffheading

91-09 A

91-09 B

91-10 A

95-05 B

Ex 95-08

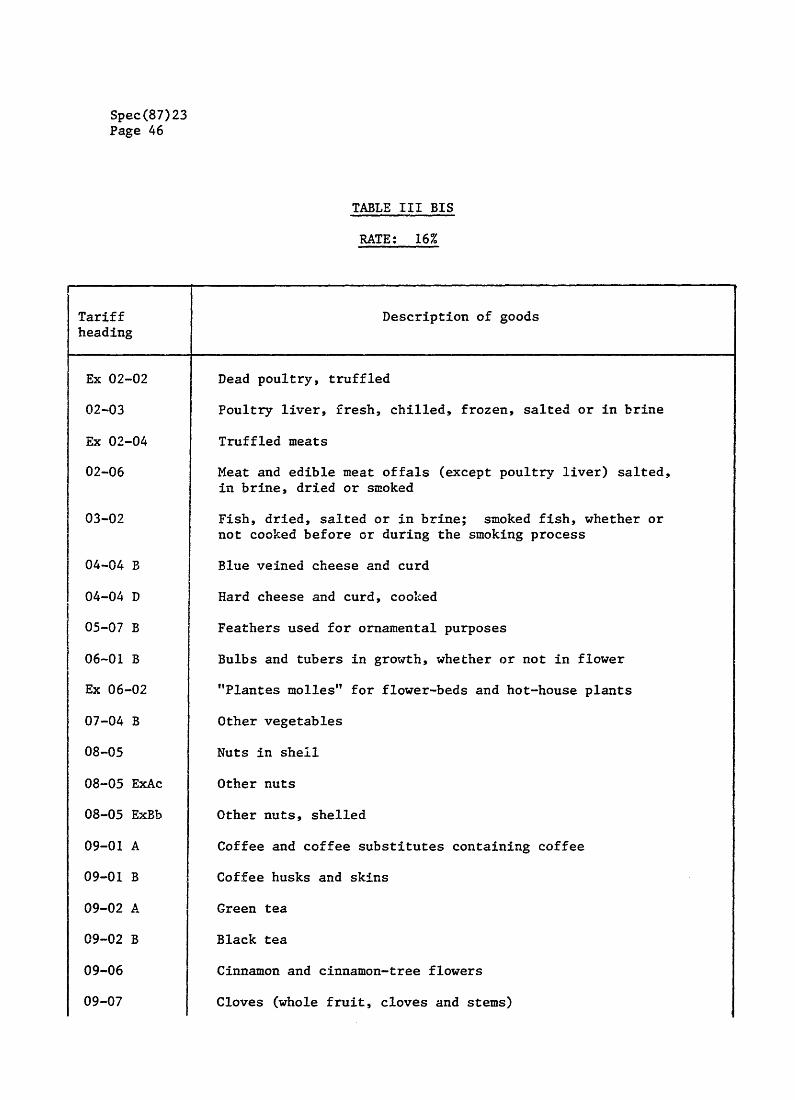

Spec(87)23Page 46

TABLE III BIS

RATE: 16%

I- -_

Tariffheading

Ex 02-02

02-03

Ex 02-04

02-06

03-02

04-04 B

04-04 D

05-07 B

06-01 B

Ex 06-02

07-04 B

08-05

08-05 ExAc

08-05 ExBb

09-01 A

09-01 B

09-02 A

09-02 B

09-06

09-07

Description of goods

Dead poultry, truffled

Poultry liver, fresh, chilled, frozen, salted or in brine

Truffled meats

Meat and edible meat offals (except poultry liver) salted,in brine, dried or smoked

Fish, dried, salted or in brine; smoked fish, whether ornot cooked before or during the smoking process

Blue veined cheese and curd

Hard cheese and curd, cooked

Feathers used for ornamental purposes

Bulbs and tubers in growth, whether or not in flower

"Plantes molles" for flower-beds and hot-house plants

Other vegetables

Nuts in shell

Other nuts

Other nuts, shelled

Coffee and coffee substitutes containing coffee

Coffee husks and skins

Green tea

Black tea

Cinnamon and cinnamon-tree flowers

Cloves (whole fruit, cloves and stems)

Spec(87)23Page 47

Tariff Description of goodsheading I~~~~~~~~~~~~~~~~~~~~09-08 Nutmeg, mace and cardamoms

09-10 A Saffron

09-10 B Other spices

11-07 Malt, roasted or not

12-03 C | Marrow seeds

13-02 C Other gums

13-03 Ex A Licquorice extracts

13-03 Ex B Other saps, except mucilages of carob and flours ofcarob-seed

14-02 A Vegetable hair

14-02 B Other vegetable materials

14-05 Ba Henna

15-13 B Vegetable semen

16-01 Sausages and the like, of meat, meat offal or animal blood

16-02 Other prepared or preserved meat or meat offal

Ex 16-03 Meat extracts and meat juices

16-05 Crustaceans and molluscs, prepared or preserved

17-04 A Chewing gum and the like

17-04 B Other sugar confectionery, not containing cocoa

18-02 Cocoa shells, husks, skins and waste

18-03 Cocoa paste (in bulk or in block) whether or not defatted

18-05 Cocoa powder, unsweetened

18-06 A Cocoa, in powder form, containing added sugar

Spec(87)23Page 48

Tariff Description of goodsheading

i I~~~~~~~~~~~~~~~~~~~~~~~~~~

18-06 B

19-02 B

19-02 Cb

19-02 Ex D

19-05

20-06 Ex B

21-02 Ex Cb

21-03 B

21-04

21-05

21-07 A

21-07 B

21-07 Ex C

22-02

22-05 A

Block chocolate (plates, slabs, tablets, pastilles,croquettes and various shapes), chocolate in powder formor granulated

Powders, sweetened or not, for the manufacture of creams,custards, desserts, etc.

Flours containing added milk, containing cocoa

Other malt extracts containing cocoa

Prepared foods obtained by the swelling or roasting ofcereals or cereal products (puffed rice, cornflakes andsimilar products)

Roasted groundnuts

Extracts, essences or concentrates of mate andpreparations with a basis of these extracts, essences orconcentrates

Prepared mustard

Sauces; mixed condiments and mixed seasonings

Soups and broths, in liquid, solid or powder form

Powders for the manufacture of creams, custards, puddings,desserts, etc.

Edible tablets and measured portions with a basis ofnatural or artificial fragrances, not containing addedsugar

Other food preparations, except yoghurts other than fruitflavoured

Lemonade, flavoured aerated waters and other non-alcoholicbeverages, not including fruit and vegetable juices fallingwithin heading No. 20-07

Wines obtained exclusively by the fermentation of freshgrapes or the juice of fresh grapes

Other fermented beverages (for example, cider perry and mead)22-07

Spec(87)23Page 49

Tariff Description of goodsheading

25-15

29-26

33-06

34-01

34-05

36-08

39-07

39-07

39-07

40-11

Ex A

A

Fa

Fc

Ex

Ex

Ff

A

40-11 Ex Ba

40-11 Ex Bb

40-11 Ex Ca

40-11

42-03

42-03

42-03

42-03

42-05

43-01

43-02

43-03

Cb

A

D

E

F

Marble, travertine, ecaussine and other calcareous stone

Carboxyimide-function compounds

Liquid perfumes of not more than 70° alcohol

toilet soap and perfumed soap

Polishes and creams for footwear, furniture or floors

Ferro-cerium and other pyrophoric alloys

Boot and shoe lasts

Discs for buttons

Other articles, except horns for olive picking

Solid or cushion tyres and tyre treads, weighing each morethan 2 kg.

Inner tubes weighing each more than 0.500 kg. and not morethan 2 kg., except inner tubes for aircraft

Inner tubes and flaps weighing more than 2 kg. each, exceptthose for aircraft

Pneumatic tyres, including tubeless tyres, weighing eachmore than 2 kg. and not more than 15 kg.

Pneumatic tyres weighing each more than 15 kg.

Articles of apparel of leather

Other gloves and mittens of leather

Belt-makers' wares of leather

Other clothing accessories of leather

Other articles of leather or composition leather

Raw furskins

Furskins, tanned or dressed

Articles of furskin

Spec(87)23Page 50

Tariff Description of goodsheading

43-04

44-27

Ex 48-10

Ex 48-21

48-21 Ex Cb

49-01 A

49-11 Ex B

49-11 C

49-11 Ex D

52-02

58-02 Bc

58-04 Ex A

58-04 Ex B

Artificial fur and articles made thereof

Fancy articles, of wood

Cigarette paper

Other articles of paper pulp, paper, paperboard orcellulose wadding

Other articles of paper pulp, paper, paperboard orcellulose wadding, except armatures for electric coilsor stereotyping blanks

Printed books, etc., bound in natural, artificial orcomposition leather

Technical handbooks, brochures, commercial cataloguesand other similar articles, whether or not includingincidental publicity

Technical handbooks, brochures, commercial cataloguesand other similar articles containing publicity

Printed matter used in data-processing machines

Other printed pictures, except those in leafletspublished as tourist advertising for hotels or printedpictures and other printed matter for use in schools

Woven fabrics of metal thread or of metallized yarnof a kind used in articles of apparel, as furnishingfabrics or the like

Other carpets

Furnishing pile fabrics of silk, silk floss or waste silk

Furnishing pile fabrics of other textiles, from allcountries

Clothing pile fabrics of silk, silk floss or waste silk

Clothing pile fabrics of other textiles, from allcountries

Spec(87)23Page 51

Tariff Description of goodsheading I

58-05

58-05

58-08

58-09

59-10

61-09

A

Ex B

Ex A

61-09 Ex A

61-09 Ex B

61-09 Ex B

61-09 Ex

61-09 Ex

Ex 62-02

C

C

Ex 62-02

62-05

62-05

62-05

62-05

62-05

62-05

Ex

Ex

Ex

Ex

Ex

Ex

B

C

D

E

F

&

Narrow woven fabrics consisting of warp and weft

Other narrow woven fabrics, except untreated tapes fortechnical uses

Tulle and other net fabrics, plain

Tulle and other net fabrics, figured

Linoleum for all uses

Combinations, corsets and girdles of silk, silk floss orwaste silk

Combinations, corsets and girdles of man-made fibres,from all countries

Brassieres and strapless brassieres, of silk, silk flossor waste silk

Brassieres and strapless brassieres, of man-made fibres,from all countries

Other corsets, of silk, silk floss or waste silk

Other corsets, of man-made fibres, from all countries

Sheets, table-cloths etc., of silk, silk floss or wastesilk