g:casc bulletin book jobcasc bulletin …casconline.org/images/november month web file 2016.pdf ·...

TRANSCRIPT

+91 9940680500 +91 9900093129+91 9940680500 +91 9900093129

in CCH iFirmin CCH iFirmin CCH iFirm

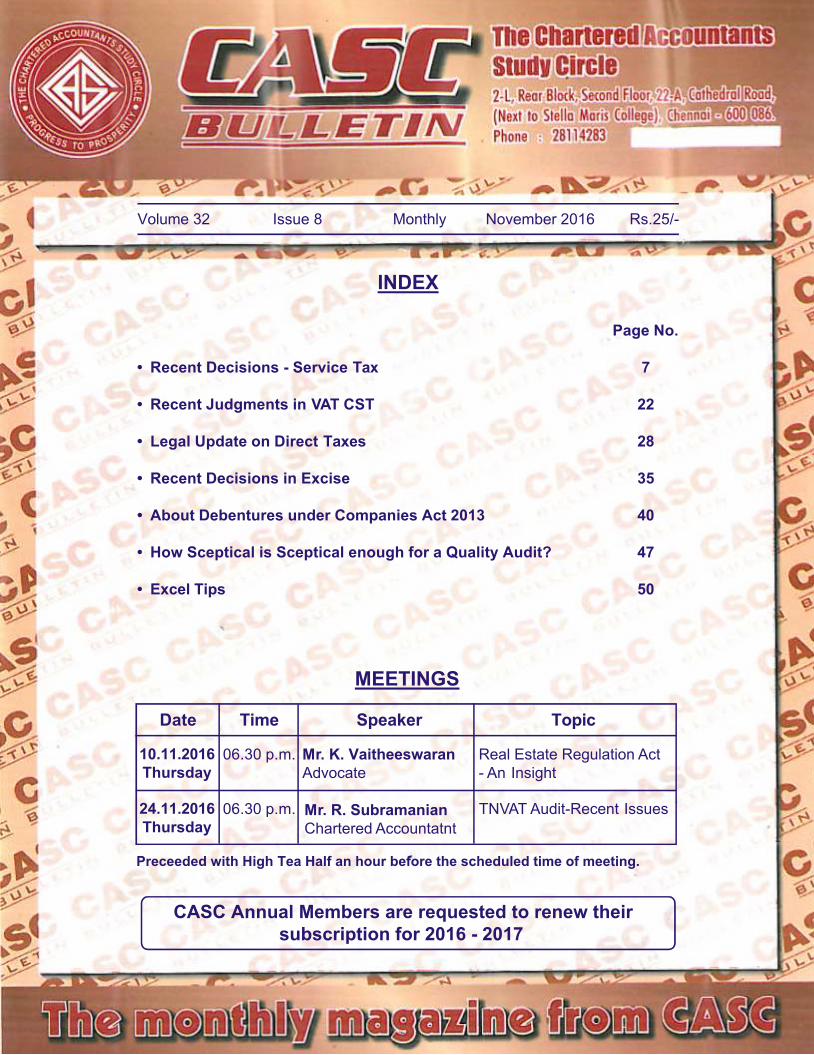

3CASC BULLETIN, NOVEMBER 2016

EDITORIALIDS – Last Minute Approach – NeverHeard about before?

There was almost a different facet of theDepartment to be seen in the last fewmonths particularly September, 2016, theultimate month to finish of the race to reachthe so called “No Target” set goal for theCountry as a whole but “Target” for theAssessing Officer’s. The Departmentofficials were put before with a challengeto see the success of the Scheme and theworld was turned upside down by theAssessing Officer’s approach for many ofthe assessees. The last 24 hours were hecticbut had brought a huge sense of relief fortax officials. The methodology adoptedincluded from persuasion to threat and forthe same the Assessing Officer used /misused the machinery as well asprovisions of the Act. In some cases theAssessing Officer are struggling to find theway out in the provisions of the Act, toclose the act carried out by them. Forexample the Assessing Officer hasconducted a survey in a business premiseswhich comes under his / her jurisdictionbut the assessee is assessed by a differentofficer.

The Finance Ministry had initially claimedin the press release dated 1st October, 2016,as under

“In order to facilitate the taxpayers and tospread awareness about the Scheme, the

CBDT issued a number of FAQs to addressvarious queries received. Major issuesclarified included manner of declaration offictitious liability, allowance of costindexation and holding period benefit forregistered immovable property, sanctity ofvaluation report etc. Difficultieswith respect to payment of taxes in a shortspan were removed by permitting paymentof tax in 3 instalments, the last being inSeptember 2017. Absolute confidentialityof the declarations made was promisedunder the scheme to reassure thedeclarants.” [Emphasis Supplied]

The modus operandi of the Departmentwas exactly in the opposite direction as theAssessing Officer are aware of thedeclaration, though many times not onrecord, as the said declarations wereobtained based on the enquiry or surveyconducted by them. Be that as it may theScheme is claimed to be successful by totaldeclaration of over Rs. 65000 crores asagainst the Rs. 33000 Crores in the 1997VDIS Scheme.

In one of news items on the website this iswhat was stated “The disclosures lastedfour months starting June 1, 2016. Thegovernment knows this is not a clean-upexercise. All those who have black moneyaren’t going to jump forward and comeclean. Nation is by no yardstick going tobe free of black money. But yes many are

4CASC BULLETIN, NOVEMBER 2016

Finance Act, 2016, one for IncomeDisclosure and another for DisputeResolution. Sensing the chance of failureof the scheme for Income Disclosure, theGovernment has pressed into promotionmode. In this process the departmentalpeople were asked to conductpromotional meetings and all of asudden the Assessing Officer were madeto do certain activities which they havenever done. The CBDT came out withFAQs in 4 sets to clarify and convincethe stakeholders to opt for the scheme.All kinds of methods like threatening aswell as convincing, are used to makethe scheme successful. The AssessingOfficer are now made to behave like asalesman who has to achieve the targetof making the scheme successful andalso document the same by updatingthe higher authorities with pictures andvisuals. The Assessing Officer have beenprovided with all materials likestandees, banners, pamphlets, etc. Themajor controversy was created witheffective rate of tax and secondcontroversy related to reopening of theassessment. The effective rate of tax hasbeen put to rest after requirement ofclarification was forced upon CBDT byrepresentation from professionalassociations and others. However, the

other controversy continues with thestatement from CBDT confirming thatSection 197(C) of Income Disclosure Act,2016, will prevail over the reopeningscheme under Income Tax Act. TheCBDT seems to ignore the fact that theSection 197 starts with the words “Forthe removal of doubts ….” and thus arenot able to explain how these words canbe ignored. However, the CBDT istrying its level best to make the schemesuccessful and let’s hope it succeeds.

Appeal

Members are requested to attend theprograms conducted by CASC and arealso requested to send their suggestionsand / or value additions to the servicesprovided by CASC including thisBulletin. The same can be sent by hardcopy to the office of the CASC oremailed to [email protected] or anyof the Members on the ManagementCommittee.

For and on behalf of Editorial Board

Editor

going to declare part of their stash,” a topfinance ministry official.” Source: ndtv.com

The need of the hour is that the AssessingOfficers as well as the assessee and or theirauthorised representative have to learn –“Be a Sceptic, not being a Cynic”.

“A cynic distrusts most information they see,particularly when it challenges their own beliefsystem. Thus, they often become intolerant ofother people’s ideas. It’s not difficult to findcynics everywhere in our society, from livedebate on TV to our own family dinner tables.People who are driven by inflexible beliefs rarelythink like Galileo or Jobs.

Scepticism, on the other hand, is a key part ofcritical thinking – a meaning “to inquire” or“look around.” A Sceptic requires additionalevidence before accepting someone’s claims astrue. They are willing to challenge the statusquo with open-minded, deep questioning ofauthority. In today’s complex world, scepticsand cynics are often hard to differentiate.

And herein lays the dilemma of our modernday quest for certainty. When we can no longerbe objective “inquirers” because we havealready decided the truth, then we create aculture of cynicism instead of scepticism.

Be Scepticism but Be Positive. Thisapplies for quality audit as well asQuality audit is a relative term, difficultto quantify. Moreover it may vary fromperson to person, case to case. Similarlyhow and how much sceptical should be

auditor in particular scenario, verydifficult to summarize. However therealways exist a scope for process, reprocess,re-engineering, and innovation to improveand make auditing relevant with changingtime.”

An interesting article on the topic – “Howsceptical is sceptical enough for a qualityaudit?” is carried somewhere else in thisbulletin which is worth reading

Judgements – The After Effects?

The Honourable Madras High Court hadin one of its Judgement held by stating that“we are of the view that this aspect wouldbrook no delay till the governmentdevelops some thought process for plansand brings into force Section 22A ofRegistration (Tamil Nadu Amendment)Act 2008”. Accordingly the bench haddirected that no registering authority shallregister any sale deed in respect of anybuilding constructed on plots inunauthorised layouts. The judges said,“We are concerned with the absence of anyprovision for the Act/Rules/Regulationsat present describing any wetland lying formore than three years to be converted intoresidential or other use applied for. Thiswas noticed in our order dated March 24,2016 while simultaneously noticing thatonly 5 per cent of land area was understatutory planning process and for theremaining 95 per cent plans are yet to bedeveloped. ”We thus hereby direct that no

5CASC BULLETIN, NOVEMBER 2016

registering authority shall register any saledeed in respect of any building constructedon such plots or unauthorised layouts. Thisorder becomes necessary in order toprevent unauthorised and haphazarddevelopment/sale of agricultural areas foragricultural use, and giving governmenttime to come forthwith with a broad policydocument to save ecology and preventflooding”, the judges said. This had its ownimpact and the registering authoritywithout understanding the context underwhich such a direction was issued, hadstarted rejected any building from beingregistered unless it is on an approved plot.The process of approval has got modifiedover a period of time. Panchayats are nomore authorised to approve any layout. Inother words though the order was somecategories of registration but it was takenas a blanket ban by the registeringauthority. Now what happens to the publicwho have already acquired and got itregistered in their names? This isirrespective of the time frame when it wasacquired. Literally there seems to be noescape for buyers as their property hasturned into a ‘zero-return’ asset with thepassage of the order by the High Court.

An interesting fact to note is that the saidsection 22A of the Registration (TamilnaduAmendment) Act, 2008, though amendedway back but the same has not beennotified till date. Though according to anews report the same is now notified on20th October, 2016.

Accomplishments

One of our life Member, an eminent taxcounsel, a leading and highly respectedadvocate, has been elevated to theprestigious post of a Judge of High Courtof Madras. She is none other than Dr. AnitaSumanth, daughter of highly respectedSenior advocate Late Mr. V.Ramachandran. She has represented andargued in many landmark judgements inillustrious career as an advocate. We wishher all the best in her new responsibility.

Annual Residential Refresher Seminar

The next Residential seminar will beconducted in the month of January, 2017.The entire details about the same is carriedsomewhere in this bulletin. We humblyrequest you to register at the earliest toenable the committee in charge to carry outseamless arrangement for the same.

Appeal

Members are requested to attendthe programs conducted by CASC and arealso requested to send their suggestionsand / or value additions to the servicesprovided by CASC including this Bulletin.The same can be sent by hard copy tothe office of the CASC or emailed [email protected] or any of theMembers on the Management Committee.

For and on behalf of Editorial Board

Editor

6CASC BULLETIN, NOVEMBER 2016

DISCLAIMER :

The contents of this Monthly Bulletin are solely for informational purpose. Itneither constitutes professional advice nor a formal recommendation. Whiledue care has been taken in assimilating the write-ups of all the authors. Neitherthe respective authors nor the Chartered Accountants Study Circle acceptsany liabilities for any loss or damage of any kind. No part of this MonthlyBulletin should be distributed or copied (except for personal, non-commercialuse) without express written permission of Chartered Accountants Study Circle.

COPYRIGHT NOTICE :

All information and material printed in this Bulletin (including but notflowcharts or graphs), are subject to copyrights of Chartered Accountants StudyCircle and its contributors. Any reproduction, retransmission, republication,or other use of all or part of this document is expressly prohibited, unlessprior permission has been granted by Chartered Accountants Study Circle.All other rights reserved.

ANNOUNCEMENTS :

1. The copies of the material used by the speakers for the regular meetings heldtwice in a month is available on the website and is freely downloadable.

2. Earlier issues of the bulletin is also available on the website in the “News” column.

The soft copy of this bulletin will be hosted on the website shortly.

READER’S ATTENTION

You may please send your Feedback Contributions / Queries on Direct Taxes, IndirectTaxes, Company Law, FEMA, Accounting and Auditing Standards, Allied Laws orany other subject of professional interest at [email protected]

For Further Details contact :“The Chartered Accountants Study Circle”

“Prince Arcade”, 2-L, Rear Block, 2nd Floor, 22-A, Cathedral Road,Chennai - 600 086. Phone 91-44-28114283

Log on to our Website :www.casconline.org

for updates on monthly meetings and professional news.Please email your suggestions / feedback to [email protected]

7CASC BULLETIN, NOVEMBER 2016

RECENT DECISIONS - SERVICE TAX

1. Exclusion of writ jurisdiction byavailability of an alternative remedy is arule of discretion not one of compulsion.Income from writing articles inmagazines, anchoring TV shows brandendorsements & from playing cricket inIPL – not covered under businessauxiliary services / business supportservices – income – rule of exclusion ofwrit jurisdiction by availability of analternative remedy is a rule of discretionand not one of compulsion :

In Sourav Ganguly v. UOI 2016 (43) STR482 (Cal.), the petitioner is a cricketer andis a former captain of the Indian CricketTeam who has participated in the IPLCricket tournament held in India as amember of the Kolkata Knight Rider Teamand was acting as a brand ambassador forvarious products. He also acted as anchorin television shows and was also engagedin writing articles for Sports Magazines.CBEC, vide instruction/circular dated 26July, 2010, viewed as under:-

a. Sponsorship received by a player or aTeam would be independent of sportevent and hence taxable assponsorship of IPL is not sponsorshipof any sports event, since IPL in itselfis not a sports event but an entity offranchisee teams and therefore it istaxable and the activity of thefranchisee sub serves the business of

CA. VIJAY ANAND

BCCI IPL and would fall within thescope of ‘Business Support Services’which is a taxable service under theservice tax law.

b. The players provide taxable servicewhen they wear apparel provided bythe franchisee that are embossed withcommercial endorsements or whenthey participated in endorsementevent and the service provided by theplayers for promoting or marketing ofthe logos/brands/marks of thefranchisee/sponsors would fall underthe ‘Business Support Services’ andchargeable to service tax.

c. Fee charged for playing the matcheswill fall outside the purview of taxableservice.

d. In case the players are paid compositefee for playing the matches and forparticipating in promotional activitiesthe component of promotionalactivities should be segregated for

8CASC BULLETIN, NOVEMBER 2016

charging service tax and if it cannot bedone then service tax should beleviable on the total compositeamount.

e. The Commissionerate havingjurisdiction on the address of theplayers should issue show cause noticeto the players for rendering service tothe franchisee.

f. In case, the address of the players isout of India, the liability to pay servicetax would fall on the franchisee underthe reverse charge mechanism.”

Thereafter, the office of the AdditionalDirector General, Directorate General ofCentral Excise Intelligence, Calcutta Zonal(respondent no. 4) initiated investigationagainst the petitioner. Thereafter theCommissioner confirmed the demand ofthe following:-

a. Writing articles in magazines,anchoring TV shows and BrandEndorsement.

b. On receipt of fee from KKR for playingcricket in IPL under business supportservice.

Thereafter, the assessee filed a writ petitionbefore the High Court for quashing of theSCN, Order and Instruction/Circulardated 26.07.2010 which observed asunder:-

1. It is a rule of self-imposed restraint thatthe courts have developed in theinterest of judicial discipline that writjurisdiction does not intervene whenan efficacious alternative remedy isavailable to the aggrieved person.However, where the vires of a statuteor a statutory rule is challenged orbreach of a fundamental right iscomplained of or an order or action ofan authority is challenged on theground of lack of jurisdiction or on theground of violation of the principlesof natural justice, the Writ Courts haveinterfered in spite of an alternativeremedy being available to the writpetitioner. The discretion should be leftto the court to be exercised inaccordance with sound principles oflaw and judicial conscience in a givenfactual matrix. The rule of exclusion ofwrit jurisdiction by availability of analternative remedy is a rule ofdiscretion and not one of compulsion.

2. If it is finally decided that the extendedperiod of limitation was wronglyinvoked by the authority in issuing theimpugned show cause notice, thelogical conclusion that would followis that the show cause notice wasissued without jurisdiction. In thatevent, the court would be justified ininterfering with the show cause noticeand the order in which it culminatedin the exercise of jurisdiction underArt. 226 of the Constitution of India.

9CASC BULLETIN, NOVEMBER 2016

An authority cannot clothe itself withjurisdiction by erroneously deciding apoint of fact or law. An authoritycannot confer on itself jurisdiction todo a particular thing by wronglyassuming the existence of a factualmatrix, existence whereof is a pre-condition for exercise of jurisdiction bysuch authority.

3. The question is whether theDepartment was justified in invokingthe extended period of limitation forthe purpose of issuing the impugnedshow cause notice. A mere ipse dixitthat fraud has been committed orsomething has been done or permittedto be done with fraudulent motivecannot be taken note of and cannotform the basis of any action on the partof the authorities. Even if, suchparticulars are not included in thenotice, the Department should be in aposition to justify and/or substantiateits allegation of suppression ofmaterial facts on the part of the noticee.The Department initiated the enquiryby issuing the letter dated 5November, 2009. The petitioner dulyresponded to the said letter by hisletter dated 24 November, 2009wherein he categorically stated that hewas not rendering any businessauxiliary services and had earnedincome by playing cricket forthe country. Thereafter, under coverof letters dated 14 December, 2009 and

15 March, 2010, the petitioner suppliedall documents called for by the officeof the respondent no. 4 includingcopies of agreements entered into withvarious companies and corporateentities and, in compliance of summondated 12 January, 2011, the petitionerthrough his authorised representative,appeared before the respondent no. 4for making statements and producingdocuments. Furthermore, by letterdated 20 August, 2011, the petitionersupplied the information sought for bythe Department by its letter dated 4August, 2011.

4. From the aforesaid it would appearthat the petitioner was prompt anddiligent in responding to all the noticesissued by the Department and in hisreplies, the petitioner clearly explainedthe nature and scope of his activities.Subsequently, copies of contractsentered into by the petitioner with thecorporate entities were also madeavailable to the Department. There wasfull and sufficient disclosure of thenature of the petitioner’s activities tothe Department and it cannot be saidthat the petitioner suppressed materialfacts to deceive the Department withintent to evade payment of service tax.

5. In the following cases, the Hon’bleSupreme Court held that a mere failureto disclose a transaction or activity andpay tax thereon or a mere

10CASC BULLETIN, NOVEMBER 2016

misstatement or mere contravention ofthe Central Excise Act or the FinanceAct, 1994 as amended, or of any Rulesframed thereunder, is not sufficient forinvocation of the extended period oflimitation.

i. CCE, Chandigarh v. PunjabLaminates Pvt. Ltd., 2006 (202) ELT578 (S.C.)

ii. CCE, Chennai v. Chennai PetroleumCorporation Ltd., 2007 (211) ELT 193(S.C.)

iii. CCE, Hyderabad v. Chemphar Drugsand Liniments, Hyderabad, (1989) 2SCC 127 = 1989 (40) ELT 276 (S.C.)

iv. Anand Nishikawa Co. Ltd. V. CCE,Meerut (2005) 188 ELT 149 (S.C.)

v. CCE, Aurangabad v. Bajaj Auto Ltd.2010 (260) ELT 17 (S.C.).

6. There has to be a positive, consciousand deliberate action on the part of theassessee intended to evade tax, forexample, a deliberate misstatement orsuppression pursuant to a query, inorder to evade tax. A clear fraudulentmotive or an element of men’s rea onthe part of the assessee has to beestablished before the Department cantake recourse to the extended periodof limitation.

7. Consequently, there was no ground orjustification whatsoever for issuing the

SCN by invoking the extended periodwhen no precondition for invoking theextended period existed.

8. With respect to the taxability of writingof articles in magazines, the samecannot, by any stretch of imagination,be said to be amounting to renderingbusiness auxiliary service within themeaning of Sec. 65(19) or businesssupport service under Sec. 65(104c) ofthe Finance Act, 1994. Writing articlefor publication in a media is for thebenefit of the readers who haveinterest in the concerned topic. Thepetitioner wrote articles for media,primarily for the sports lovers and itwould be preposterous to suggest thatin writing such articles the object of thepetitioner was to advance any businessor commercial venture. The articleswere meant for information and evenentertainment of the general publicinterested in sports. An article writtenby a celebrity in an issue of a magazinemay to some extent boost the sale ofthat issue but cannot be said that theobject of the author in writing thearticle or permitting publicationthereof was to promote circulation ofthe concerned magazine which mightbe an incidental effect but the samecannot foist service tax liability on theauthor of the article. Hence, suchremuneration received for writingarticles would not attract service tax.

11CASC BULLETIN, NOVEMBER 2016

9. With respect to the taxability of theremuneration received by thepetitioner for anchoring TV shows,such shows are meant forentertainment of the viewers. Incontemporary world watchingtelevision is a primary form ofrecreation. It would be absurd to saythat anchoring TV shows amounts torendering business auxiliary service orbusiness support service. By anchoringa TV show, a celebrity or for thatmatter any other person does notrender service with the object ofenhancing any business or commercialinterest. No reasonable authority withproper application of mind couldclassify anchoring of TV show asbusiness auxiliary service or businesssupport service. Hence, suchremuneration received by thepetitioner for anchoring TV showsdoes not attract service tax.

10. As regards the claim on brandendorsement, under the heading‘Business Auxiliary Service’, byamendment of the Finance, Act, 1994,a new taxable service category of‘Brand Promotion’ was introducedwith effect from 1 July, 2010, the logicalcorollary and inevitable inference isthat such category of service was nottaxable prior to 1 July, 2010. Reliancewas sought on the decision in the caseof CST, Delhi-vs.-Shriya Saran 2014(36) STR 641 (Tri.-Del.) and in the case

of Indian National Shipowners’Association-vs.-UOI 2009 (14) STR289 (Bom.). Business auxiliary serviceand brand promotion are distinctservice heads as admitted by theDepartment in the show cause noticeunder challenge. Since brandendorsement was not a taxable serviceduring the period of time for which thetax demand has been raised, suchdemand cannot be sustained. Suchservice rendered by the petitionercould not be taxed under the head ofbusiness auxiliary service as has beensought to be done.

11. As regards the remuneration receivedby the petitioner for playing IPLcricket, in my opinion, the service taxdemand raised on such amount underthe head of ‘Business Support Service’,is not legally tenable. As per the facts,the terms of the contract that thepetitioner entered into with M/s.Knight Riders Sports Pvt. Ltd. wouldreveal that the petitioner’s obligationwas not limited to displaying hiscricket skills in a cricket match and healso lent himself to businesspromotional activities. Thus heprovided taxable service when hewore apparel provided by thefranchisee that was embossed withcommercial endorsements or when heparticipated in endorsement event.The Department admits that the feecharged for playing the matches will

12CASC BULLETIN, NOVEMBER 2016

fall outside the purview of taxableservice. However, the Departmentcontends that the petitioner has beenpaid composite fee for playing matchesand for participating in promotionalactivities but the component ofpromotional activities could not besegregated for charging service tax.Accordingly, service tax is chargeableon the composite amount. For thiscontention, the Department relied onthe letter dated 26 July, 2010 issued bythe Central Board of Excise andCustoms which is also under challengein this writ petition.

12. The adjudicating authority held thatsuch fees/remuneration have beenpaid to the petitioner by the franchiseein addition to his playing skills andthus the services rendered by thepetitioner are classifiable under thetaxable service head of ‘BusinessSupport Services’ as per the provisionsof Sec. 65(104c) read with Sec. 65(105)(zzzzq) of the Finance Act, 1994. Thereappears to be inherent inconsistencyin such as Sec. 65(105) (zzzzq) pertainsto Brand Promotion whereas Sec.65(104c) pertains to Business AuxillaryServices. They are two distinct andseparate categories. The taxable headof Brand Promotion was not inexistence prior to 1 July, 2010, hence,reliance on that head for levying taxon the amount received by thepetitioner from the IPL franchisee is

misplaced and misconceived. This issufficient to vitiate the order.

13. The petitioner was under full controlof the franchisee and had to act in themanner instructed by the franchisee.The apparel that he had to wear wasteam clothing and the same could notexhibit any badge, logo, mark, tradename etc. The petitioner was notproviding any service as anindependent individual worker. Hisstatus was that of an employee ratherthan an independent worker orcontractor or consultant. It cannot besaid that the petitioner was renderingany service which could be classifiedas business support service as he wassimply a purchased member of a teamserving and performing under KKRand was not providing any service toKKR as an individual.

14. Insofar the letter/instruction dated 26July, 2010 issued by the CBEC isconcerned, the petitioner is aggrievedby the instruction in the said letter tothe effect that in case the players (inIPL) are paid composite fee for playingmatches and for participating inpromotional activities, the componentof promotional activities should besegregated for charging service tax andif it cannot be done then service taxshould be leviable on the totalcomposite amount. CBEC in itsadministrative capacity is not entitled

13CASC BULLETIN, NOVEMBER 2016

to impose its views on its varioussubordinate authorities exercisingquasi-judicial functions to interpret aparticular provision of a statute in aparticular manner. A circular/instruction/letter cannot create taxliability. The statutory provisionsrelating to service tax do not providethat the fee received by an IPL playerwould attract service tax. This isadmitted by the Department even inthe said circular which states, inter alia,that charges for playing matches willfall outside the purview of taxableservice. If the statute does not providefor levying service tax on fee receivedfor playing matches, such a liabilitycannot be created by issuing a letter/instruction/circular. A circular cannottravel beyond the statute. The statutedoes not provide that if a playerreceives a composite amount forplaying matches and promotionalactivities and the segregation of thetwo elements is not possible, then thecomposite entire amount may betaxed. Such an act on the part of theDepartment will be de hors the statuteand without jurisdiction or authorityof law. It will also be in contraventionof Art. 265 of the Constitution of India.CBEC cannot seek to legislate byissuing circulars/instructions. If suchcirculars/instructions/clarificationsare contrary to or inconsistent with thestatutory provision in question or seekto create a liability which the statute

does not contemplate, such circular/instruction is liable to be struck down.A misconceived and legally untenableinterpretation of a statutory provisionand/or an erroneous understandingthereof, which if applied by the quasi-judicial authorities will undulyprejudice the citizens of the country,cannot be allowed to stand. Hencesuch circular/instruction dated 26July, 2010 was quashed to the extent itstates that if composite fee received forplaying matches and for participatingin promotional activities cannot besegregated, then service tax should belevied on the total composite amount.Hence, the remuneration received bythe petitioner from the IPL franchiseecould not be taxed under businesssupport service.

Hence, the court set aside the SCN, theconsequential order and instruction/circular dated 26.07.2010.

2. Repair of roads and airports –exclusion under commercial orindustrial construction does notmean that it could form part of othertaxable services - retrospectiveexemption to the activity ofmanagement, maintenance and repaircannot be extended to runways onwhich aircrafts takes off and land -:

In D.P. Jain & Co. v. UOI, [2016] 43 STR5072 (Mum.), the appellant was engagedin:-

14CASC BULLETIN, NOVEMBER 2016

(i) Construction of roads for NHAI(National Highway Authority ofIndia), CPWD (Central Public WorksDepartment) and NMC (NagpurMunicipal Corporation).

(ii) Construction of runways for AirportAuthority of India Ltd.

(iii) Strengthening renewal of roads.

(iv) Improving and surfacing of runways.

(v) Site preparation, excavation for furtherconstruction of roads either on its ownbehalf or for the clients havingcontracts for construction of roads.

The adjudicating authority, after dueinvestigations, confirmed the demands onthe services of (i) repair and maintenanceof roads; (ii) repair and maintenance ofairport runways; (iii) site formation activityundertaken at roads. On de novo appeal(after remand by the High Court), theTribunal set aside the demand on repairand maintenance of roads, but upheld theother demands, against which theappellant preferred an appeal before theHigh Court which observed as under:-

1. Merely because repair of road andairports is specifically excluded fromthe definition of commercial orindustrial construction does not meanthat it cannot form part of other taxableservice. If one carefully analysessection 65(25b) of the Finance Act,1994, it would be apparent that itdefines the words or expression‘

'Commercial or IndustrialConstruction’ which means, repair,alteration, renovation, restoration of orsimilar services in relation to buildingor civil structure, pipe line or conduit,but that ought to be used or to be usedprimarily for or occupied or to beoccupied primarily with or engaged orto be engaged primarily in commerceor industry, or work intended forcommerce or industry. From thatservice, the legislature excludedservices provided in respect of roads,airports, transport terminals etc. Thereason is obvious because the sectioncontains a definition. The serviceprovided could be for maintenance ofutilities. Such maintenance may alsoinclude repairs. Therefore, thelegislature thought it fit to bring itwithin maintenance or repair serviceunder section 65(64) and while doingso, it firstly defined “management,maintenance or repair service” tomean any service provided by anyperson under a contract or anagreement for a manufacturer or anyperson authorised by him in relationto management of properties, whetherimmovable or not, maintenance orrepair of properties, whetherimmovable or not or maintenance orrepair including reconditioning onrestoration, or servicing of any goods,excluding a motor vehicle and alsosubstituted it by the Finance Act, 2006

15CASC BULLETIN, NOVEMBER 2016

with effect from 1-5-2006. It alsosubstituted the Explanation belowsection 65(64) with effect from 15-5-2008 to state that for the purpose ofsection 65(64) “goods” includescomputer software and “properties”includes information technologysoftware.

2. However, when the Legislaturebrought in the concept of 'TaxableService' by section 65(105) and definedit to mean any service provided or tobe provided to person by any personin relation to management,maintenance or repair, its aim wasspecific and clear. The definitionscontained in section 65 and by priorclauses would act as and provide aguideline.

3. Merely because repairs of roads andairports is specifically excluded fromthe definition of ' Commercial orIndustrial Construction' it could stillbe brought in under the category of‘management, maintenance or repairservice’. Ultimately, management,maintenance or repair is defined tomean any service provided by anyperson under a contract or anagreement for a manufacturer or anyperson authorised by him in relationto management of properties, whetherimmovable or not, maintenance orrepair of properties, whetherimmovable or not or maintenance or

repair including reconditioning onrestoration, or servicing of any goods,excluding a motor vehicle. It is noturged that roads and airports are notproperties. It is the management ofproperties as also their maintenance orrepairs, irrespective of whether theyare immovable or not, which is amanagement, maintenance or repairservice. Once it is taxable, then,whether it is in relation to road orairport is hardly relevant and material.

4. Commercial or industrial constructionservice is defined in section 65(25b)and in its wisdom, the Legislaturethought the services provided inrespect of roads, airports, railways,transport terminals, bridges, tunnelsand dam would not be necessarilycommercial or industrial constructionand in any event repair, alteration,renovation, restoration of such utilityshould be excluded from the purviewof the definition of the term 'Commercial or Industrial ConstructionService'. By this, there is no prohibitionfor bringing it in another category. Thedefinitions as carved out do not makeany provision of the Act redundant.Once management, maintenance orrepair is a service and, in it, provisionof such service in relation to anyproperty immovable or otherwisecould be brought, then, Court cannotuphold the argument of assessee thatexclusion from one service wouldimply exclusion from service tax itself.

16CASC BULLETIN, NOVEMBER 2016

5. In matter of taxation, when thelanguage of the section or provision isclear and unambiguous, then, the courtmust give effect to it. There is noquestion of then interpreting theprovision and by finding out thesupposed intention of the Legislature.It is only when the language is not clearbut ambiguous or obscure, then, thereis scope for interpretation. In thepresent case, principles ofinterpretation cannot be pressed intoservice more so when there is noredundancy nor absurdity. Eventually,in inserting and incorporatingdefinitions so as to understand taxableservice if management, maintenance orrepair is taken to be a distinct serviceand that aspect is excluded from thedefinition of the term ' Commercial orIndustrial Construction Service', then,it is not a case of redundancy orrendering any provision nugatory, butbeing specific and clear.

6. The principle that ‘When there is a lawgenerally dealing with a subject andanother dealing with one of the topicscomprised therein, then, General lawis to be construed as yielding to thespecial in respect of matters comprisedtherein’ cannot be applied in thispresent case. Here, we have twodefinitions which are to be found tounderstand the whole gamut ofservices brought to tax. To encompass

almost all the services for bringingthem in the tax net, their definitionsare worded accordingly, one cannotignore the plain words by applying theabove principle.

7. What could be brought to tax alone canbe exempted from it or the levy. If thatwas not taxable at all or from inception,then, there is no question of grant ofany exemption therefrom.

8. There is a difference even incommercial parlance between twowords and terms viz. ‘roads’ and‘runways’ as when these terms beingnot defined in the Finance Act, 1994,they must take their color from theircommon parlance meaning and beunderstood and interpreted as knownto the commercial world. ‘Runway’ isa specially prepared surface alongwhich an aircraft takes off and land.Thus, it is a path for aircraft to take offfrom. Whereas, ‘road’ may be a pathor way with a specially preparedsurface, but it is used by vehicles/pedestrians etc. Ordinarily road isunderstood as a passageway, tracksuitable for wheeled vehicles. That isnot how runway is construed andunderstood. Runway is made orspecifically prepared along which anaircraft takes off and lands. Eventually,it is not how it is made and surfaced,but what it is utilized for which isrelevant. Therefore, the premise or

17CASC BULLETIN, NOVEMBER 2016

foundation that road is a genus ofwhich runway is species is not correctand proper. It cannot be agreed thatroad is a wide term and included in itis a runway. Mere fact that on someportions adjacent to a runway, motorvehicles ply or to tow or bring backstranded aircraft specialized recoveryvehicles are brought on runway doesnot mean that runways are roads.

9. With respect to the submissionpertaining to section 98 of the FinanceAct, 1994, which grants retrospectiveexemption to repair/maintenanceservices provided to non-commercialGovernment buildings and assesseehas argued that airports arenon-commercial Governmentbuildings and maintenance/repairthereof is exempt u/s 98, the exclusionis clear as section 98 refers to buildingservices relating to management etc.of non-commercial Governmentbuildings.

Consequent to the above, the High Courtdid not find any merit in the appeal anddismissed the same.

3. Export of software to SEZ – refund ofaccumulated credit under rule 5 of theCENVAT Credit Rules, 2004 – not tobe denied - CENVAT Credit onGoods transport agent’s services uptothe port which is the place of removal– not to be denied – when value ofSEZ turnover is included in the value

of total turnover, the same should beincluded in the value of exportturnover.

In Cognizant Technology Solutions v.CCE & ST (LTU), Chennai [2016] 43 STR576, the appellants were renderingsoftware services and the services areexported and also to the domestic clientsand obtained centralized registration forservice tax with the Commissioner of LTU,Chennai and also registered with STPI/SEZ as well. The Appellant claimed refundof CENVAT credit on the credit relating toinput services used in the output servicesexported outside India under Rule 5 ofCCR read with Notification No. 05/2006dated 14 March 2006 as amended. Theoriginal adjudicating authorities as well asthe Commissioner (Appeals) rejected/restricted the refund claims of theAppellant on the following grounds:-

a. Services related to development ofinformation technology software andmaintenance of such software werespecifically included as taxable serviceonly from 16.05.2008.

b. Appellant was engaged in provisionof software maintenance service whichwas not covered under the ambit ofManagement, maintenance, and repairservice (MMRS) upto 16.05.2008) andhence the same was not taxable up to16.05.2008.

18CASC BULLETIN, NOVEMBER 2016

c. The appellants are not eligible forrefund of CENVAT credit of inputservices availed on the softwaremaintenance service.

d. The export turnover portion in theformula prescribed under Rule 5 ofCCR, does not include the value ofexports made from SEZ.

e. In the numerator the total exportturnover the adjudicating authoritytaken only STPI turnover andexcluded the SEZ exports and whiletaking the total turnover(denominator) the adjudicatingauthority has computed including SEZexports and accordingly rejected therefund.

f. The adjudicating authority alsoexcluded the quantum of amount fromthe refund claim which are otherwiseineligible for which separate showbecause notices were issued underCCRs.

Aggrieved by these orders, the appellantsand the departments preferred appealsbefore the Tribunal which observed asunder:-

1. The short issue involved in this caserelates to rejection of refund on inputservice credit utilized in the export ofservices and refund claimed underRule 5 of CCR. The adjudicatingauthority and the lower appellate

authority in the appellant assesseesappeals rejected or restricted therefund on the ground as under:-

a. The software maintenance serviceunder the category of ManagementMaintenance and Repair Service(MMRS) is not taxable/exempted.

b. Restricted their refund claim byadopting different value forcomputation in respect of totalturnover vis-‘-vis export turnoverprovided in the formula prescribedunder Notification No. 5/2006-CE(NT) dated 14.03.2006.

2. With respect to the first issue, theappellant is a software firm engagedin the business of softwaredevelopment and obtained centralizedservice tax registration under LTUCommissionerate and dischargingservice tax on the software servicesrendered to local customers and alsoexported software services. There isno dispute on the payment of servicetax by the appellant on the MMRSduring the period 2007-2008. Theappellant has furnished the details ofthe taxable service i.e., MMRS and ithas been clearly mentioned that theappellant has paid the service tax bothby cash as well as by debit in theirCENVAT credit and the appellant hasclaimed refund of service tax paid oninput service which was used in

19CASC BULLETIN, NOVEMBER 2016

output service. Revenue cannot adopttwo standards, when the appellantpaid service tax under MMRS the samewas accepted by the Revenue whereaswhile claiming the refund under Rule5 of CCR, they choose to arguedifferently, stating that the saidservices are exempted. The issue ofgranting refund of unutilized inputcredit/input service tax credit used inthe export of services under Rule 5 ofCCR has been settled by variousHonble High Courts and Tribunal.The decision of the Tribunal atMumbai Bench in the case of KPITCummins Info systems Ltd. Vs. CCE,Pune-I - 2013 (32) STR 356 (Tri.-Mum.) has dealt the identical issue onthe software consultancy serviceexported during the relevant periodand allowed the appeal by followingthe decision in mPortal India WirelessSolutions Pvt. Ltd. Vs. CST,Bangalore 2012 (27) STR 134 (Kar.).

3. The ratio of the above Tribunaldecision is squarely applicable to thepresent case as the Tribunal in theabove case has held that the softwaremaintenance service is classifiableunder the category of Managementand Maintenance or Repair Service(MMRS) during the relevant periodand in the present case it is clearlyestablished that the appellants havepaid the service tax on MMRS andavailed credit.

4. Further the Tribunal Mumbai Bench inthe case of CCE, Pune Vs. BarclaysTechnology Centre (I) Pvt. Ltd 2014TIOL-2641-CESTAT-MUM by relyingthe decision in the case of TataConsultancy services Ltd. Vs. CST,LTU, Mumbai, - 2013 (29) STR 393(Tri.-Mum.), rejected the revenueappeal and allowed the refund of inputservices utilized in the export ofsoftware services to SEZ.

5. Hence, the appellants are eligible forrefund under Rule 5 of CCR on theinput services used in the export ofservice.

6. On the issue relating to thecomputation of total turnover vis-‘-Visexport turnover for determining therefund amount as per the formulaprescribed under Notification No, =.05/2006-CE (NT) dated 14.03.2006.While calculating the quantum ofrefund eligible as per the formulaprescribed under Rule 5 of CCR, theappellant claimed the refund on theexport turnover of both SEZ and STPIunits. For the purpose of totalturnover, the appellants havecomputed total turnover of both SEZand STPI units as the appellants beingone entity whereas the adjudicatingauthority, while computing the value,has deducted the value of SEZ exportsfrom the export turn over (numerator)but retained the SEZ export turn over

20CASC BULLETIN, NOVEMBER 2016

in the total turnover (Denominator).The appellants contended that theadjudicating authority whendeducting the value of SEZ exportsfrom the turnover, ought to havededucted the same from the totalturnover or, if he has included it in theturn over, he should have alsoincluded it in the export turn over.

7. In an identical issue in CCE, Pune Vs.Computer Land UK Ltd., - 2015 (10)TMI 517 CESTAT-MUMBAI, theTribunal discussed the correct methodof computation of total turnover vis-‘-Vis export turnover and upheld theimpugned order and rejected therevenue appeal.

8. Further, in CIT & Others vs. Tata ElxsiLtd. & Others 247 CTR- 334, in respectof computation of deduction underSection 10 (A) of IT Act, dealt theidentical issue of computation ofexport turn over and total turnover,High Court dismissed the revenueappeal and upheld the Tribunal order.

9. The above decision are squarelyapplicable to the facts of the presentcase in so far as the computation of theexport turnover and total turnover forcomputing the export value as per theformula prescribed under Clause5 of Notification No. 5/2006 dated

14.03.2006. In the present case, thelower authorities while computing theturn over deducted the value of SEZexports from the export turn over(numerator) and retained the same inthe total turnover (denominator)which has resulted in the anomaly andthe reduction in the quantum of refundwhen Clause 5 of the Notification No.5/06 dated 14.3.2006, clearly stipulatesthat the formula has to be applied onlyfor the activity to which the claimrelates and it is for the entity as awhole.

10. Hence, when the revenue proceededto include the value of SEZ exports incomputing the total turnover, the sameshould also have been included incomputing export turnover. The orderof the Learned adjudicating authorityin rejecting the refund claim byadopting the wrong method ofcomputation is not justified and liableto be set aside to that extent ofrestriction of the refund claim.

Hence, the assessee’s appeals were allowedwith consequential relief and thedepartment’s appeal rejected.

(The author is a Chennai based CharteredAccountant. He can be reached at reached [email protected])

21CASC BULLETIN, NOVEMBER 2016

CASC CHENNAI, MEMBERSHIP FEE

Corporate MembershipCorporate Annual Membership 3,000.00Corporate Life Membership (20 Years) 20,000.00

Individual MembershipAnnual Membership 750.00Life Membership 7,500.00

CASC - HALL RENTHALL RENT FOR 2 HOURS 1,000.00HALL RENT FOR 2-4 HOURS 1,500.00HALL RENT FOR FULL DAY 2,500.00LCD RENT FOR 2 HOURS 600.00LCD RENT FOR 2-4 HOURS 800.00LCD RENT FOR FULL DAY 1,200.00

The above amounts are EXCLUSIVE of Service Tax. Applicable Taxes will beadded.

CASC BULLETIN - ADVERTISEMENT TARIFF - PER MONTH

Full Page Back Cover 2,500.00Full Page Inside Cover 2,000.00Half Page Back Cover 1,500.00Half Page Inside Cover 1,250.00Full Page Inside 1,200.00Half Page Inside 750.00Strip Advertisement Inside 500.00

Minimum 6 months advertisement is required.If advertisement is 12 months or above, special discount of 15% is available

Your demand draft / cheque at par should be drawn in the name of“The Chartered Accountants Study Circle” payable at Chennai.

Kindly contact [email protected] for the updates.

Rs.

22CASC BULLETIN, NOVEMBER 2016

RECENT JUDGMENTS IN VAT CST

Levy of tax by State:

The standard adopted as a measure of thelevy may be indicative of the nature of thetax but it does not necessarily determineit. The nature of the mechanism by whichthe tax is to be assessed is not decisive ofthe essential characteristic of the particulartax charged, though it may throw light onthe general character of the tax. Whendeciding an issue of legislative competencein relation to a taxing statute, the court isrequired to determine whether the natureof the tax is such that it does not fall withinthe fields of legislation that are earmarkedfor the Legislature concerned. While theremay have been an express understandingbetween the various State Governmentsthat the provisions of the value added taxlegislations in the respective States wouldhave some common features, a legislativeprovision that is introduced by one of theStates cannot be struck down on theground that it goes against the StateGovernment’s commitment to anempowered committee. One cannotattribute mala fides to a Legislature whileconsidering the validity of a legislativeprovision. Once it is found that the StateLegislature has the legislative competenceto introduce the levy in question, the merefact that other State Legislatures have not

CA. V.V. SAMPATHKUMAR

introduced a similar levy cannot be citedas an instance of discrimination. StateLegislatures have a greater freedom whenit comes to economic legislations and theycan pick and choose the subjects of taxationreasonably. Other than increasing the rateof tax on specified textile articles, when theturnover in respect of the articles crosses aspecified threshold level in the hands ofsome dealers, the levy does not meet outdiscrimination in the matter of taxation toany specified class of dealers. [2016] 90VST 267 (Ker) KERALA TEXTILE ANDGARMENTS DEALERS WELFAREASSOCIATION AND OTHERS v.STATE OF KERALA AND OTHERS (andother cases)

Statutory forms:

Even though, the petitioner had availed ofthe concessional rate of tax, it failed tofurnish the requisite statutory forms,

23CASC BULLETIN, NOVEMBER 2016

within the stipulated period as prescribedin the Puducherry Value Added Tax Rules.However, it could not be lost sight that theCentral Sales Tax Rules did not provide forany time-limit. Furnishing of the statutoryforms was not within the control of thepetitioner and was dependent on the otherState dealers’ co-operation. If on sufficientcause, the petitioner satisfied therequirements of law, then the claim couldnot be rejected unjustifiably merely on theground of belated submissions of statutoryforms. The petitioner also maderectification applications. Therefore thepetitioner could be given an opportunityto produce all the statutory forms formaking appropriate assessment orders.[2016] 90 VST 297 (Mad) PANDI DEVIOIL PRIVATE LIMITED v.ADDITIONAL DEPUTYCOMMERCIAL TAX OFFICER (lAC),PONDICHERRY AND ANOTHER

Remand orders:

Where an order of remand lays down limitsfor the enquiry to be made by the lowercourt that court ought to confine itself toquestions which fall within those limits. Itis not open to any of the parties or to thecourt below to enlarge the scope of theremand order. Even when a matter isremitted to High Court by the SupremeCourt, the High Court cannot assume a

wider field of jurisdiction than one whichhas been permitted by the Supreme Courtthrough the order of remand, and enterinto examining the whole controversyafresh and as if all contentions of all partiesare open before it. When evidence ofexperts is tendered and when the expertiseof the persons tendering such evidence isestablished, such materials can be rebuttedonly through such contra evidence as couldbe held to be of more evidentiary value incomparison by competitive evaluation bya duly informed adjudicator. The scope ofenquiry following of an order of remandwould necessarily stand guided by thedirections contained in the order ofremand. [2016] 90 VST 304 (Ker) STATEOF KERALA v. M. R. F. LIMITED

Authorisation:

Where there was no order in writing byany Commissioner authorising the SalesTax Officer, Siliguri to discharge functionsof the Commissioner or a SpecialCommissioner or an AdditionalCommissioner under section 67 of the Act,the order of seizure conducted by the SalesTax Officer, Siliguri Range was liable to beset aside and such was to be directed toreturn immediately all seized items. As aconsequence no penal or other action maybe taken against the dealer in respectseizure conducted without jurisdiction.

24CASC BULLETIN, NOVEMBER 2016

[2016] 90 VST 326 (Cal) SAPTRISHIINFRATRADE PRIVATE LIMITED v.SALES TAX OFFICER, SILIGURIRANGE, SILIGURI AND OTHERS

Jurisdiction:

The petitioner had submitted itsapplication for amendment of certificate ofregistration, furnishing the information asrequired under the Act, whereupon thecompetent authority issued amendedcertificate of registration, in favour of thepetitioner on February 5, 2015, wherein theK branch was also mentioned. Theinspection report on record mentioned thatthe person in charge of the businesspremises informed that the dealer wascentralised registered. Thus in that view ofthe matter the Assistant Commissioner, KCircle, exceeded his jurisdiction andillegally passed the order dated January 23,2015. Moreover, the third proviso to section19 of the Act, which is a deeming Clause,says that if the dealer applies for grant ofcertificate of registration in the prescribedmanner and that the application is dulyfilled in, he shall be deemed to be inpossession of a valid certificate ofregistration from the date of application forthe purpose of exercising all rights andperforming all duties or bearing allliabilities under the Act or the Rules madethere under. Thus, once the dealer applied

for amendment of certificate under the Actfurnishing the information required underthe Act, it could not be treated as a dealerevading registration. Therefore, the orderpassed by the Assistant Commissioner, KCircle, was without jurisdiction as well asbased on wrong notion of law. The Courtalso held that since there was complete lackof jurisdiction in the officer or authority totake the action in question, the jurisdictionunder article 226 of the Constitution ofIndia needed to be invoked. [2016] 90 VST356 (Patna) V MART RETAIL LIMITEDv. STATE OF BIHAR AND ANOTHER

Revision:

The scope of judicial scrutiny in a revisionpetition is limited to a question of law andnot a question of fact. The Tribunal, for thepurpose of a question of fact is the ultimatefact-finding authority. The court mayinterfere with such finding of fact if it is amixed question of law and fact or the viewtaken by the Tribunal on the basis of thefacts available on record is an impossibleview and not the possible view. If it is apossible view, this court may not sit in anappeal over such finding of fact. The firstappellate authority after examining thecontentions of the dealer had come to thecategorical finding that the benefit ofcircular was not available to the dealer. TheTribunal after re appreciation of whole

25CASC BULLETIN, NOVEMBER 2016

material had reiterated the finding of factconcurring with the view of the firstappellate authority. The contention that theTribunal had not properly considered theother clauses of the circular or that theTribunal had not considered that theformula was applied by the petitioner butwas found to be erroneous by the assessingofficer was not tenable for two reasons: thatthe first appellate authority after havingconsidered all aspects did find that theaction was not unintentional and that theTribunal had found that there was noconfusion about applicability of theformula and it was clear. When the formulawas clear as found by the Tribunal, and ifit was not applied, the view taken by theTribunal that the action was notunintentional was not an impossible view,which may call for interference by thecourt. [2016} 90 VST 220 (Karn)BHARATH EARTH MOVERS LTD. V.STATE OF KARNATAKA

Input tax credit:

The word “business” is defined in aninclusive manner. If a manufacturer-dealersets up a research centre for undertakingthe research of a product or may be a newproduct in which he is dealing, it can besaid to have a direct nexus to the principalactivity of manufacture. It is out of variousresearches undertaken one may possibly

decide to manufacture a particular productor of a particular quality having betterprospects in the business. When the dealerwas not running an independent researchinstitute, but was also dealing in themanufacturing or sale of the products andthat the principal activity of the dealer wasmanufacturing of the product and researchwas limited to the variety of productswhich may be manufactured by the Dealerand if dealer is manufacturing a particularproduct and is also undertaking researchactivity pertaining thereto for itself, suchcan be said to be an incidental activity tothe manufacturing activity and hencewould fall within the definition of the word“business”. The dealer was entitled toinput tax credit on the purchases made forresearch unit as claimed. [2016] 90 VST 236(Karn) HINDUSTAN UNILEVER LTD.V.STATE OF KARNATAKA

Constitutional validity of Section 19(20)of TNVAT Act:

As per section 19(20) of TNVAT Act 2006,made retrospectively, there is need for thereversal of the amount of the input taxcredit over and above the output tax ofthose credit when dealer has sold goods ata price lesser than the price of the goodspurchased by him. When the question ofthe validity of this enactment and that toomade retrospectively came into questionthe Court held that whenever concession

26CASC BULLETIN, NOVEMBER 2016

is given by statute or notification etc. theconditions thereof are to be strictlycomplied with in order to avail suchconcession. Under the scheme of the VATAct, it is not permissible for the dealers toargue that the price as indicated in the taxinvoice should not have been taken intoconsideration but the net purchase priceafter discount is to be the basis. When aconcession is given by a statute, theLegislature has power to make theprovision stating the form and manner inwhich such concession is to be allowed.Sub-section (20) seeks to achieve that.There was no right, inherent or otherwise,vested with dealers to claim the benefit ofITC but for Section 19 of the VAT Act. Thatapart, there were valid and cogent reasonsfor inserting Section 19(20) to protect theRevenue against clandestine transactionsresulting in evasion of tax. The challengeto constitutional validity of sub-section (20)of Section 19 of VAT Act has to fail. Withrespect to the retrospective effect sub-section (20) of Section 19 of the TNVATAct it was held that sub-section (20) ofSection 19 is altogether new provisionintroduced for determining the input taxin specified situation, i.e., where goods aresold at a lesser price than the purchaseprice of goods. The manner of calculationof the ITC was entirely different before thisamendment. This is clearly a provisionwhich is made for the first time to the

detriment of the dealers. Such a provision,therefore, cannot have retrospective effect,more so, when vested right had accruedin favour of these dealers in respect ofpurchases and sales made betweenJanuary 01, 2007 to August 19, 2010. Thus,while upholding the vires of sub-section(20) of Section 19, the Court set aside andstrike down Amendment Act 22 of 2010whereby this amendment was givenretrospective effect from January 01, 2007.JAYAM & CO. Vs ASSISTANTCOMMISSIONER & ANR [2016] (SC)CIVIL APPEAL NOS. 8070-8073 OF 2016etc. (SC) Dated: 05.08.2016

Accounts:

The Assessing Officer who is enjoined withthe statutory duty to complete theassessment, inadequacy or adequacy ofinformation gathered by the enforcementwing is of no consequence, when theAssessing Officer takes up the case forassessment to tax. The Assessing Officercannot be bowed down by theobservations of the enforcement wing andin several cases that appears to be so andthis malady is on account of the fact thatthe enforcement officers are superiorofficers to the Assessing Officer. It is truethat the Rules stipulate the manner inwhich the accounts have to be maintained.However, it is not the case of the firstrespondent that the data available with the

27CASC BULLETIN, NOVEMBER 2016

petitioner does not confirm to the Rules.The petitioner’s justification is that theaccounts are maintained in that particularformat, which is a specially designedsoftware and this helps them in monitoringthe business throughout the country. TheAssessing Officer is a statutory authoritywho plays a very vital role in assessingdealers to tax. Therefore, the endeavour ofthe officer should be to ensure that not arupee of revenue payable to theGovernment is missed out in collection thatis why financial experts have said that anassessment proceedings is an outcome ofdialogue and deliberations. In certain casesto understand the nature of activity, doneby a dealer/assessee, the Assessing Officermust equip himself to the nuances of theparticular trade, so as to ensure that thedisclosure made by the Assessee in theirreturn is full and true. There is no reasonas to why the respondent should fight shyof visiting the place of business of thepetitioner or in the alternative, the entiredata in the format maintained by thepetitioner can be made available in theoffice of the first respondent with theinfrastructure being set up at the cost ofthe petitioner. HINDUSTAN UNILEVERLIMITED Vs THE DEPUTYCOMMISSIONER (CT)-II, LTU,CHENNAI etc., [2016] (Mad)W.P.Nos.28818 & 28819 of 2014 Dated29.08.2016

Penalty:

Levy of penalty is not justifiable if at thetime of assessment turnover has beenrecorded as per the books of accounts andverified by the department, in suchcircumstances, suppression cannot beattributed. Transaction giving rise totaxable turnover, has been categoricallydeclared by the assessee as compositeworks contract and at the concessional rateof 4%, tax has been paid. Though penaltyis leviable under the provisions of the Act,while exercising discretion, the AO isrequired to take note of the bona fides ofthe assessee. In view of the explanationsto Section 12(3) of the Act the contentionof the department that levy of penaltyunder Section 12(3) is automatic, cannotbe accepted. Tribunal is not right inapplying explanation (iii) to Section 12(3)(b) of the Act, to sustain the levy of penalty,despite the fact that the petitioner hadopted for compounding of tax underSection 7C of the Act. SHYAM AIRFRIDGE Vs THE STATE OF TAMILNADU REP. BY THE DEPUTYCOMMISSIONER (CT), VELLORE[2016] (Mad) Tax Case (Revision) No.186of 2009 Dated: 28.07.2016

(The author is a Chennai based CharteredAccountant. He can be reached [email protected])

28CASC BULLETIN, NOVEMBER 2016

LEGAL UPDATE ON DIRECT TAXES

CA. G. PARI & CA. P. PRADEEP KUMAR

I. Whether interest on partners’ capitalis an expenditure envisagingdisallowance under rule 8D read withsection 14A of Income tax Act [ITA],if the partnership firm has investedin shares and mutual funds?

The issue came up for consideration in thecase of QUALITY INDUSTRIES v. JCIT,Range-2, NASHIK, [2016] 73taxmann.com 363 (Pune - Trib.),SEPTEMBER 9, 2016

FACTS:

1. The assessee is a partnership firmengaged in the business of chemicalsand for the assessment year 2010-11has earned and claimed exemption ofdividend income derived out ofinvestment in mutual funds made bythe firm in earlier years and also in theyear of assessment out of capitalintroduced by its partners. Whilecompleting assessment u/s 143(3), theAO observed and completed theassessment that investment in mutualfunds has been made out of interestbearing funds, which includespartners’ capital also; thus invokedrule 8D read with section 14A of ITAon interest on partners’ capital as anexpenditure incurred in relation toearning of exempted income viz.dividends by rejecting the assessee’splea that interest on partners’ capital

is not an expenditure and the firm andpartners are not different persons inthe eye of Indian Partnership Act 1932.

2. CIT(A) confirmed the order of AO;aggrieved and further appeal toTribunal;

ITAT DECISION:

3. Section 40(b) of ITA, by virtue of theFinance Act 1992, enable a firm to claimdeduction of interest on partners’capital subject to some upper limitswith effect from the assessment year1993-94, which in turn is taxable asbusiness income in the hands ofpartners. Further, disallowance ofinterest has been spelt out only insection 40(b) and not in section 36 and37 of ITA.

4. It is noted that there is no consequentamendment in Indian Partnership Acton this aspect and partnership is not aseparate legal entity. Consequently

29CASC BULLETIN, NOVEMBER 2016

interest and salary to partners remainas distribution of business income andpartnership and partners are nottreated as distinct persons underPartnership Act, although treated asseparate persons for the purpose of taxassessment. Therefore no relationshipof lender of funds (by partners) andborrower of funds (by firm) can beinferred for the application of section36(1) (iii).

5. Finally, the matter has been remandedback for fresh assessment by holdingthat interest paid to its partners cannotbe treated at par with the other interestpayable to outside parties.

BUTTRESSES/GROUNDS for theDECISION:

Firm and partners are not distinct personsunder Indian Partnership Act:

6. As per the scheme of taxation, section28(v) of ITA interest on partners’capital and salary is chargeable to taxin the hands of partners as businessincome. This taxation is line with theapex court’s ruling in the case of CITv. R.M. CHIDAMBARAM PILLAIreported in [1977] 106 ITR 292 (SC)wherein it has been ruled that ‘paymentof salary to partners represent as specialshare of profits and therefore taxable asbusiness income’ as under:

“A firm is not a legal person, eventhough it has some attributes of

personality. In Income-tax law, a firmis a unit of assessment, by specialprovisions, but it is not a full person.Since a contract of employmentrequires two distinct persons, viz., theemployer and the employee, therecannot be a contract of service, in strictlaw, between a firm and one of itspartners. Payment of salary to apartner represents a special share ofthe profits. Salary paid to a partnerretains the same character of theincome of the firm.”

Salary, interest and profits received bypartners are business income even priorto 01.04.1992:

7. The business of the firm is business ofthe partners of the firm and, hence,salary, interest and profits received bythe partner from the firm is businessincome and, therefore, expensesincurred by the partners for thepurpose of earning this income fromthe firm are admissible as deductionfrom such share income from the firmin which he is partner - CIT v.RAMNIKLAL KOTHARI [1969] 74ITR 57 (SC).

II. Whether rule 8D read with section14A would be applicable even whenthe assessee claimed that he has notincurred any expenditure? Orwhether rule 8D is automatic or canbe resorted to as a measure of lastresort?

30CASC BULLETIN, NOVEMBER 2016

The issue came up for consideration in thecase of RANIGANJ CO-OPERATIVEBANK LTD. v. DCIT [2016] 73taxmann.com 90 (Kolkata - Trib.)SEPTEMBER 2, 2016

FACTS:

1. The assessee, being a co-operativebank, for assessment year 2008-09 hasreceived dividend income out of UTIinvestments made in earlier years andalso partly invested in the year underassessment. The AO, whilecompleting assessment u/s 143(3)invoked rule 8D read with section 14Aof ITA and disallowed interest underrule 8D(2)(ii) and administrative andother expenses under rule 8D (2)(iii).The claim of the assessee that it has notincurred any expenditure for thepurpose of earning dividend incomeand the capital is adequate to cover theinvestment in mutual funds werenegated by the AO.

2. CIT(A) confirmed the order of AOrejecting the contention of the assesseethat i) AO has not recorded anysatisfaction while invoking rule 8Dread with section 14A of ITA ii) noexpenditure has been incurred forearning dividend income and iii) itsreliance on GODREJ & BOYCE 328ITR 81 (Bom.) that no disallowance oninterest u/s 14A where the capital ofthe assessee is adequate to cover the

investments or where there is no nexusfor the investments made out of theborrowed funds.

3. Aggrieved appeal has been filedbefore ITAT and decision has beenrendered for the assessment year 2008-09 and also for the assessment year2009-10, wherein disallowance hasalso been made u/s 14A even wherethere was no receipt of dividend(exempted) income in that year.

ITAT DECISION:

The expression ‘shall’ in section 14A (2)shall be read as ‘may’:

4. Sec. 14A(2) of ITA reads that “TheAssessing Officer shall determine theamount of expenditure incurred inrelation to such income which doesnot form part of the total income underthis Act in accordance with suchmethod as may be prescribed”; a plainreading of the expression enunciatesthat when the claim of expenditure hasnot been accepted by AO, it is notmandatory for him to invoke themethod of calculation prescribed byRule 8D(2) of the Rules, but he is freeto make the disallowance on anyreasonable basis. In other words, Rule8D is not automatic and the methodsprescribed thereunder ought to betaken as a measure of last resort. Theexpression `shall’ used in section 14A(2) shall be read as `may’.

31CASC BULLETIN, NOVEMBER 2016

No disallowance on interest; however theclaim that no expenses were incurred notaccepted by ITAT:

5. Considering the availability of fundsfor investment, it is held thatdisallowance of interest will not arise;however ITAT negated the claim thatno expenditure were incurred duringthe year for earning the exemptedincome and recomputed thedisallowance for administrative andother expenses under rule 8D(20(iii)being 0.5% on average of UTIinvestments.

Sec 14A cannot be invoked in a yearwhere there was no exempted income:

6. For the assessment year 2009-10 it hasbeen held that no disallowance ofexpenses u/s. 14A of ITA since noincome was earned during the year.

III. Whether income from licensing ofproperty is taxable under the head‘income from business’ or incomefrom house property?

The issue came up for consideration in thecase of BOMBAY PLAZA (P.) LTD. v.ACIT, Circle-5, Kolkata [2016] 73taxmann.com 91 (Kolkata - Trib.)SEPTEMBER 2, 2016

FACTS:

1. The main objects of the assessee, beinga private limited, envisages ‘acquiringproperties by way of purchase, lease

and license and further leasing or sub-leasing, licensing or sub-licensing ofthese properties’; on 16.04.1991 itentered into a leave and licenseagreement with M/s. East India HotelsLimited to acquire under a license anarea of 9000 sq. in Hotel OberoiTowers, Mumbai, for a tenure of 50years at an agreed monthly license fees,for the purpose of using the same asshopping centre.

2. The assessee, intern, licensed the areato various licensees with a conditionthat each licensee shall subscribespecific number shares in the licensorcompany apart from paying monthlycharges, which termed as ‘contributionfrom shops’. The assessee alsoprovided various services like air-conditioning, telephone services,maintenance, electricity, water,sanitary, security etc. the considerationfor such services are also included inthe monthly contribution charges asdetermined by its Board of Directors.These contributions have been offeredas business income and the license feespaid by the company has been claimedas an expenditure of business.

3. While making assessment U/s 143(3)for the assessment year 2007-08, theAO by relying on the decision of apexcourt in the case of CIT v. PODDARCEMENT LTD.226 ITR 625 assessedthe income as ‘Income from Property’on the premise that the assessee has an

32CASC BULLETIN, NOVEMBER 2016

irrevocable right of 50 years over theshopping space, which in view ofsection 27(iiib) deemed the assessee tobe owner of space licensed and,therefore, income accrued over thisproperty rights are property income.

4. CIT (A) confirmed the order of AO andon further appeal to ITAT;

ITAT DECISION:

5. Considering the objects of the assesseeand the facts and circumstances of thecase, it is concluded that the assesseecarried on a systematic and regularactivity in the nature of business andtherefore the income from granting thepremises on sub-license was to beassessed under the head income frombusiness. The concept of deemedowner u/s.22 read with Sec.27 (iiib) ofthe Act, no longer assumes importancefor this purpose.

BUTTRESSES/GROUNDS for theDECISION:

If the main objects of the assessee isleasing or licensing of properties, incometherefrom is taxable as business income:

6. Where rent is the main source ofincome or the purpose for which thecompany is incorporated should be toearn income from rent, then suchrental income shall be taxable underthe head ‘Profits and Gains of Business

or Profession’. - Civil Appeal No.6437of 2016 dated 11.08.2016. RAYALACORPORATION PVT. LTD. v. ACIT[SC] by referring the case of CHENNAIPROPERTIES AND INVESTMENTSLTD. V CIT 373 ITR 673(SC)

7. Where the main object of the assesseewas acquiring on license propertiesand giving them on sub-license andderiving income therefrom, suchincome from sub-licensing has to beregarded as income under the head'Income from Business' - SHAMBURLAP CO. LTD v. CIT 380 ITR 151(Cal).

AUTHORS’ NOTE:

Lease Vs License:

8. A lease is a transaction with respect toimmovable property and creates aright to enjoy such property for acertain term and for consideration onthe conditions mentioned in it,whereas a license is a mere permissionto do something without transfer of aninterest.

9. In case of lease, the right to possess andenjoy the property is transferred infavour of the lessee and he acquiresinterest through the conveyance oflease, whereas in the case of license,the licensee is not having any propertyrights and further he cannot defend thepossession in his own name.

33CASC BULLETIN, NOVEMBER 2016

10. The lease does not come to an endeither on the death of lessor or lessee,whereas a license comes to an end withthe death of either grantor or thegrantee.

Leasing right, whether construed as‘property’ for the purpose of capital gains:

11. The expression ' Property of any kind'used in section 2(14) of ITA has widerimplications. A right to obtainconveyance of immovable property isalso a ‘property’ contemplated bysection 2(14) of ITA - CIT v. TATASERVICES LTD. [1980] 122 ITR 594(Bom.). The word ‘property’ does notmean merely physical property, butalso means the right, title or interest init - CIT v. DAKSHA RAMANLAL[1992] 197 ITR 123 (Guj.).Interestingly for the purpose ofinvoking section 50C whether leaserights are included in the expression ‘'Capital asset being land or buildingor both' it has been held that leaserights are not applicable in a land -ATUL G. PURANIK v. ITO [2011] 132ITD 499 (Mum.)

12. Giving up of the right to claim specificperformance by conveyance in animmovable property amounts torelinquishment of a right in ' Capitalasset', accordingly, it is a transfer ofcapital asset within the meaning of the

Act - CIT v. VIJAY FLEXIBLECONTAINERS [1990] 48 Taxman 86& CIT v. Smt. LAXMIDEVI RATANI[2008] 296 ITR 363 (MP).

13. A lease consists of a right of possessioncum use of property owned by someother person. The leasing out of acapital asset for exploitation by thelessee like mining lease amounts totransfer of capital asset - A.R.KRISHNAMURTHY &A.R.RAJAGOPALAN v. CIT [1982]133 ITR 922 (Mad.); RAJENDRAMINING SYNDICATE v. CIT [1961]43 ITR 460 (AP)

14. Leased out of plots carved out for aperiod of 99 years for a considerationof ‘salami’ or `premium’ is subject tocapital gains as it amounts to transferof property - R.K. PALSHIKAR (HUF)v. CIT [1988] 172 ITR 311 (SC)

15. Where lease right was surrendered bythe lessee and compensation wasreceived for premature termination ofthe lease, it is capital gains taxable - CITv. PRAMIA ENGG. (P.) LTD. [1992]63 Taxman 579 (Cal.).

IV. Whether clause (c) to section 200Asubstituted by the Finance Act, 2015with effect from 1-6- 2015 empowersthe AO to charge/collect fees undersection 234E prospectively and notprior to 01.06.2015?

The issue came up for consideration in the

34CASC BULLETIN, NOVEMBER 2016

case of GAJANAN CONSTRUCTIONSv. DCIT, GHAZIABAD [2016] 73taxmann.com 380 (Pune - Trib.),SEPTEMBER 23, 2016

FACTS:

1. Bunch of appeals filed by differentassessee’s against the orders of CIT (A)relating to different assessment yearson the common issue whetherintimation issued under section 200Aof the Act and / or order passed undersection 154 of the Act in charging feespayable under section 234E of the Actis valid?

2. In all the appeals CIT (A) held that theappeal of assessee was notmaintainable, in view of the ratio laiddown by the Hon’ble Bombay HighCourt in RASHMIKANTKUNDALIA v. UNION OF INDIA[2015] 54 Taxman.com 200 (Bom), inwhich case by upholding theconstitutionality of section 234E, it isheld that the delay on the part of thedeductor in furnishing the TDSstatement causes delay in issue ofrefund to the deductees and puts extraburden on all concerned.

ITAT DECISION:

3. The amendment to section 200A (1) ofITA is procedural in nature and shallbe applied prospectively; therefore

intimations issued by AO prior to01.06.2015 by way of raising demandu/s 234E of ITA are not valid.

4. It is further held that intimation issuedby the AO after processing the TDSreturns is appealable under section246A(1)(a) and (c) of ITA since thedemand raised by way of charging offees under section 234E of the Act isequivalent to the demand raised u/s156, which is generally appealable.

SCHEME OF TDS PROVISIONS:

5. As per 200 of ITA the deductor has toprepare a statement in such form andverified in such manner and shalldeliver statement within such time asmay be prescribed. Rule 31A of theRules provided the time limit for thefurnishing of statement for taxdeduction at source on quarterlybasis. in addition to interest u/s200(1A) of ITA both these amounts,clause (c) to section 200A (1) (b) ofITA, there is a levy in the form ofadditional fees u/s 234E of ITA, witheffect from 01.07.2012, for the defaultin furnishing the statements of taxdeducted at source.

(The authors are Chennai based CharteredAccountants and they can be reachedat [email protected] &[email protected] respectively)

35CASC BULLETIN, NOVEMBER 2016

RECENT DECISIONS IN EXCISE

CA. B.DEBASIS NAYAK & CA. SRIHARI V.K.

Debit notes raised for excess amount ofmaterial used – excise duty not payableprior to 1st July 2000 but payablethereafter as valuation is based onTransaction value

In the case of CCE vs Hyundai UnitechElectrical Transmission Ltd 2016-TIOL-2749-CESTAT-MUM, the Taxpayermanufactured Electrical TransmissionTowers (ETT) of a specified weight anddischarged Central Excise duty as per theinvoices value. Subsequently, they raiseddebit note on the purchaser for excessamount of material used by them inmanufacturing of such ETT and recordedthe same in the account books as amountreceivable from purchaser.

Revenue authorities demanded excise dutyon the said amount during the scrutiny ofthe balance sheet and ledger account. Thedemand was confirmed for the periodApril 1999 to March 2003. However,Commissioner (A) set aside the order andthe Revenue has filed an appeal beforeTribunal