gaz de france exploration-production - engie · gaz de france exploration-production successful...

TRANSCRIPT

Gaz de France

Investor Day

22 May 2007

Gaz de France Exploration-Production

Successful track record and ambitious prospects

Gaz de France

Investor Day

22 May 2007

2

The objectives summarised above are based on data, assumptions and estimates deemed reasonable by Gaz de France. The said data, assumptions and estimates may evolve or be changed as a result of uncertainties due in particular to the economic, financial, competitive, regulatory or weather conditions. In addition, the materialisation of certain risks factors described in Chapter 4 of the Document de Référence filed with the Autorité des marchés financiers (“AMF”) under Number R07-046 on 27 April 2007 (hereinafter referred to as the “Document de Référence”) could have an impact on the group’s operations and its ability to achieve its objectives. In addition, achieving those objectives is dependent on the success of the commercial strategy described in Chapter 6.1.2 of the Document de Référence. Gaz de France consequently disclaims any undertaking and gives no representation as to the fact that it will achieve its objectives and does not undertake to publish or issue possible revisions or updates of such forward-looking statements or information, beyond what is required by the laws and regulations with which it must comply.

This communication does not constitute an offer to purchase or exchange or the solicitation of an offer to sell or exchange any securities of Suez or an offer to sell or exchange or the solicitation of an offer to buy or exchange any securities of Gaz de France, nor shall there be any sale or exchange of securities in any jurisdiction (including the United States, Germany, Italy and Japan) in which such offer, solicitation or sale or exchange would be unlawful prior to the registration or qualification under the laws of such jurisdiction. The distribution of this communication may, in some countries, be restricted by law or regulation. Accordingly, persons who come into possession of this document should inform themselves of and observe these restrictions. To the fullest extent permitted by applicable law, Gaz de France and Suez disclaim any responsibility or liability for the violation of such restrictions by any person.

The Gaz de France ordinary shares to be issued in connection with the proposed business combination to holders of Suez ordinary shares (including Suez ordinary shares represented by Suez American Depositary Shares) may not be offered or sold in the United States except pursuant to an effective registration statement under the United States Securities Act of 1933, as amended, or pursuant to a valid exemption from registration.

In connection with the proposed business combination, the required information document will be filed with the AMF and, to the extent Gaz de France is required or otherwise decides to register the Gaz de France ordinary shares to be issued in connection with the business combination in the United States, Gaz de France may file with the United States Securities and Exchange Commission (“SEC”), a registration statement on Form F-4, which will include a prospectus. Investors are strongly advised to read the information document filed with the AMF, the registration statement and the prospectus, if and when available, and any other relevant documents filed with the SEC and/or the AMF, as well as any amendments and supplements to those documents, because they will contain important information. If and when filed, investors may obtain free copies of the registration statement, the prospectus as well as other relevant documents filed with the SEC, at the SEC’s website at www.sec.gov and will receive information at an appropriate time on how to obtain these transaction-related documents for free from Gaz de France or its duly designated agent. Investors and holders of Gaz de France and Suez securities may obtain free copies of documents filed with the AMF at the AMF’s website at www.amf-france.org or directly from Gaz de France on its website at: www.gazdefrance.com or directly from Suez on its website at: www.suez.com, as the case may be.

Disclaimer

Gaz de France

Investor Day

22 May 2007

Introduction

Jean-Marie Dauger

Chief Operating OfficerHead of the "Supply & Production" Branch

Gaz de France

Investor Day

22 May 2007

4

Gaz de France Group

Energy Supply and Services

Exploration -

Production

Purchase

and Sale

of Energy

Services

Infrastructures

Transmission

and Storage

- France

Distribution

- France

Transmission

and Distribution

- International

Exploration-Production within Gaz de France

Division

Seg

men

t

Global Gas

+ LNG + Trading

Gaz de France

Investor Day

22 May 2007

5

1,270EBITDA

1,659Net sales

Operating income

Exploration-Production: Significant contribution to Group’s profitability and growth

935

726

1,139

2005

457

In million euros

625

968

2004

229

2006

25%

Contribution to Group 2006 EBITDA

26%

Contribution to Group 2006 Operating profit

Proportion of 2005-06 Group Capex*

* Investments excluding external growth 15% in 2004 10% in 2004

20%

Gaz de France

Investor Day

22 May 2007

6

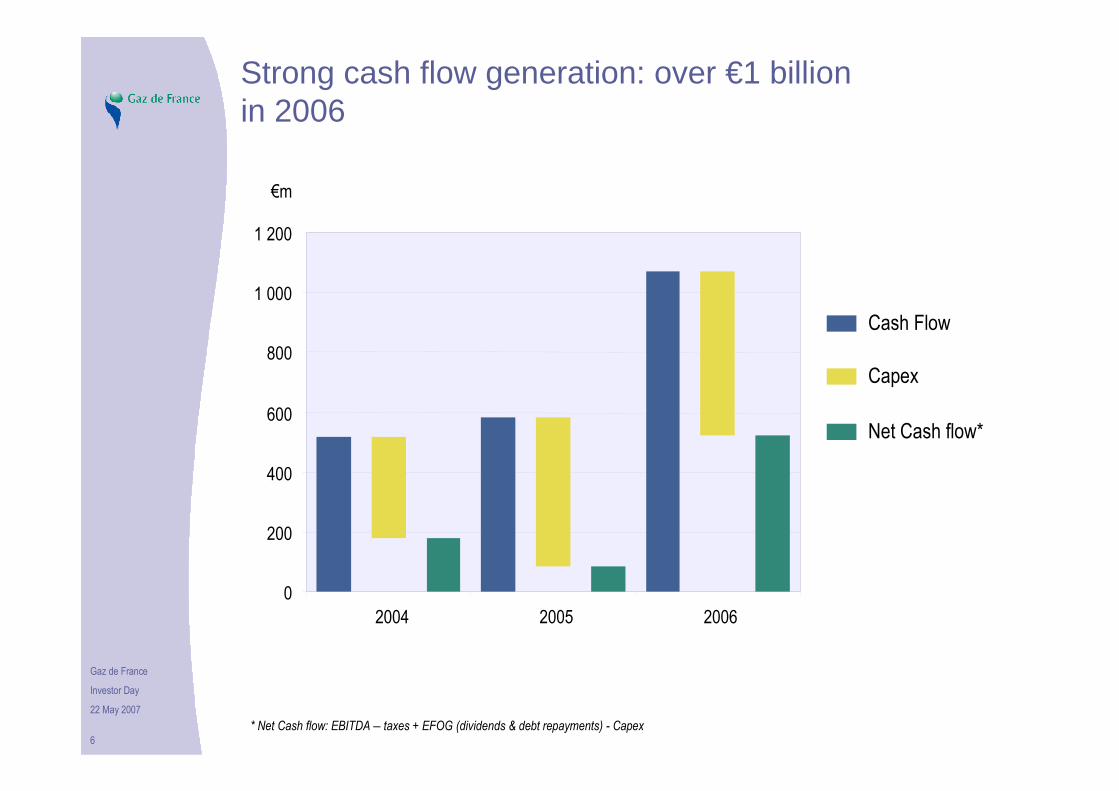

Strong cash flow generation: over €1 billion in 2006

* Net Cash flow: EBITDA – taxes + EFOG (dividends & debt repayments) - Capex

0

200

400

600

800

1 000

1 200

2004 2005 2006

Cash Flow

Capex

Net Cash flow*

€m

Gaz de France

Investor Day

22 May 2007

Exploration-Production

Didier Holleaux

Vice President Exploration-Production

Gaz de France

Investor Day

22 May 2007

8

Gaz de France Exploration-Production

Exploration-Production a fully established player

Successful track record

Growth driven strategy

Assets & projects portfolio

Ambitious prospects

Wrap up

Gaz de France

Investor Day

22 May 2007

9

Gaz de France Exploration-Production

Exploration-Production a fully established player

Successful track record

Growth driven strategy

Assets & projects portfolio

Ambitious prospects

Wrap up

Gaz de France

Investor Day

22 May 2007

10

Multi-country organisation E

xplo

ratio

n-P

rodu

ctio

n a

fully

est

ablis

hed

play

er1

Vice PresidentDidier Holleaux

Deputy Vice PresidentPhilippe Marcus

GDF BritainMark Hugues

Germany (PEG)Patrick Vannetzel

Albrecht Möhring

West Africa & Middle East Team(WAME)

René Montaz-Rosset

Norway (Gaz de France Norge)Bernard Ott

Germany (EEG)Jürgen Rückheim

North Africa Team (NAT)Gilbert Meunier

Subsurface expertiseHenri de Moegen

ExplorationPhilip Drijkoningen

OperationsMaqsood Sher

DevelopmentThierry Lefeuvre

Legal, commercial, human resources, communication …

Netherlands (ProNed)Jan Treffers

* Merger expected in 2007

*

1,115 employees

FinanceMonique Huet

Gaz de France

Investor Day

22 May 2007

11

316 exploration and production licenses

193 operator licenses

Total acreage (2006)

• 70 000 km2 (gross GdF)

• 31 500 km2 (net GdF)

Large portfolio of licenses

Exploration ProductionExploration

Exp

lora

tion-

Pro

duct

ion

a fu

lly e

stab

lishe

d pl

ayer

1

Gaz de France

Investor Day

22 May 2007

12

Producer in 5 countries, active in 9

Sources: WoodMackenzie, NPD, WEG, UKOOA.

Positions exclude state entities: Petoro/SDFI and EBN

UK

16th gas producer

21st liquid producer

19th for oil & gas reserves

Ivory Coast

Production dedicated

to a local power plant

Germany

3rd gas producer

5th liquid producer

Top 5 for oil & gas reserves

Netherlands

3 - 4th gas producer

Top 5 for oil & gas reserves

Norway

13th liquid producer

13th for oil & gas reserves

13th for gas

Exp

lora

tion-

Pro

duct

ion

a fu

lly e

stab

lishe

d pl

ayer

1

Gaz de France

Investor Day

22 May 2007

13

Strong skills in conventional projects

Exploration, development and production

• Onshore: Germany, Algeria

• Offshore: UK, Netherlands, Norway, Germany

• Gas and oil

Skills to operate some non-conventional fields

• Tight gas reservoirs

Synergies with Gaz de France’s LNG* and gas storage expertise

* Liquefied natural gas

Exp

lora

tion-

Pro

duct

ion

a fu

lly e

stab

lishe

d pl

ayer

1

Gaz de France

Investor Day

22 May 2007

14

National Oil Companies (NOC)

• Own major share of global oil & gas reserves

• Need less foreign investment & technology than in past

International Oil Companies (IOC)

• Focus on managing large projects

• Present in NOCs countries

Independents

• Competitive, tightly-run companies with focused expertise

• Competitive advantage in smaller fields

Utilities

• Very few utilities own significant E&P business units

• Focus on assets within easy reach of their markets

Gaz de France Exploration-Production ranks among the largest mid-sized Independent players. As a Utility, benefits from Group cross synergies

Excellent position in Exploration-Production market

Exp

lora

tion-

Pro

duct

ion

a fu

lly e

stab

lishe

d pl

ayer

1

Gaz de France

Investor Day

22 May 2007

15

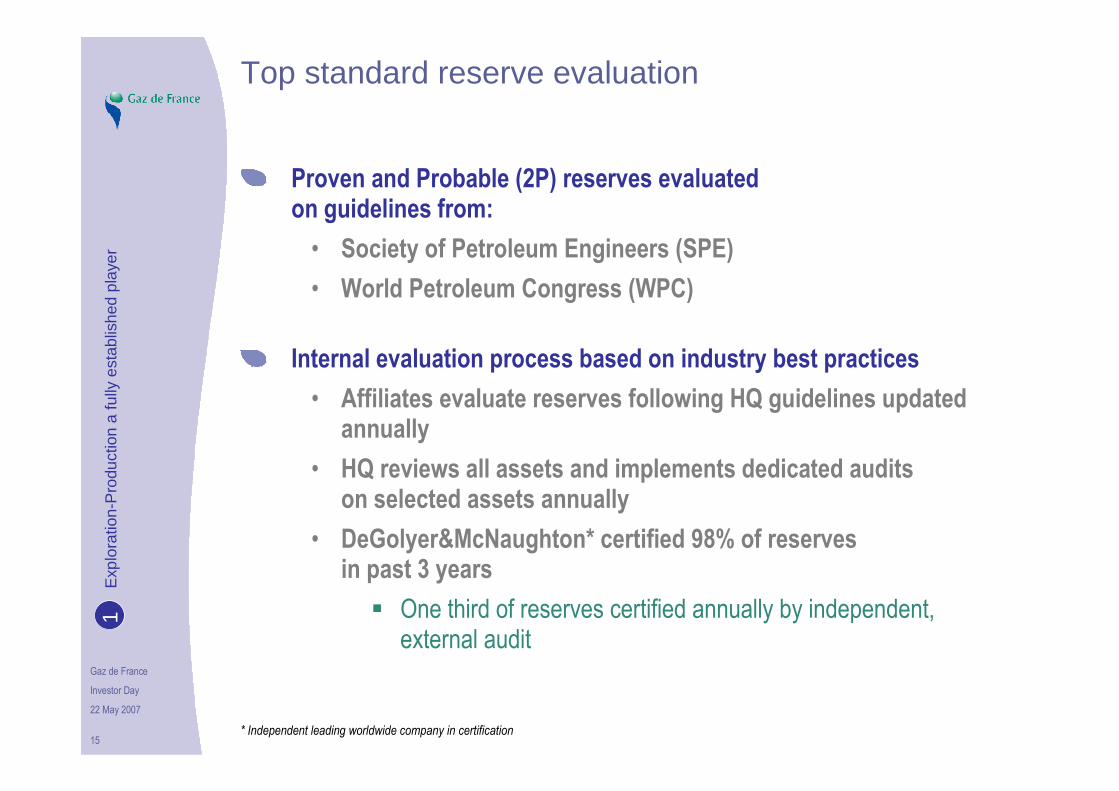

Top standard reserve evaluation

Proven and Probable (2P) reserves evaluated on guidelines from:

• Society of Petroleum Engineers (SPE)

• World Petroleum Congress (WPC)

Internal evaluation process based on industry best practices

• Affiliates evaluate reserves following HQ guidelines updated annually

• HQ reviews all assets and implements dedicated auditson selected assets annually

• DeGolyer&McNaughton* certified 98% of reserves in past 3 years

� One third of reserves certified annually by independent, external audit

* Independent leading worldwide company in certification

Exp

lora

tion-

Pro

duct

ion

a fu

lly e

stab

lishe

d pl

ayer

1

Gaz de France

Investor Day

22 May 2007

16

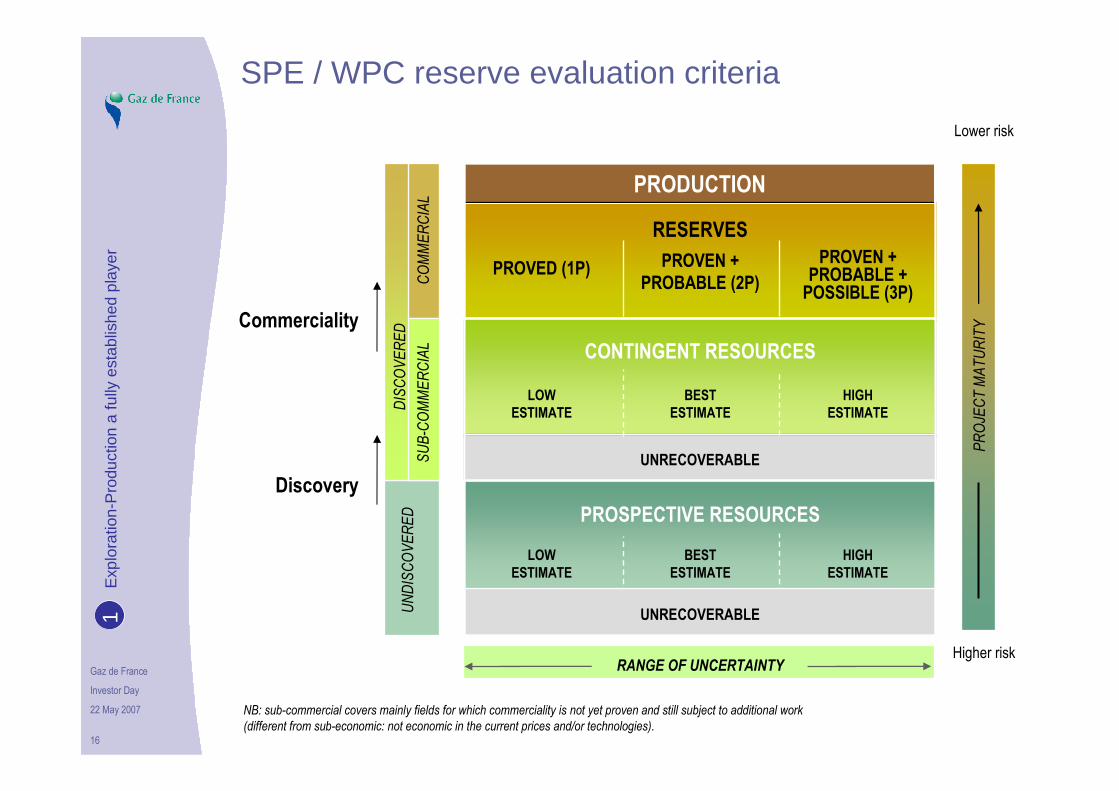

SPE / WPC reserve evaluation criteria

PROJECT MATURITY

RANGE OF UNCERTAINTY

UNRECOVERABLE

LOWESTIMATE

BESTESTIMATE

HIGHESTIMATE

LOWESTIMATE

BESTESTIMATE

HIGHESTIMATE

PROSPECTIVE RESOURCES

CONTINGENT RESOURCES

PROVED (1P) PROVEN +PROBABLE (2P)

RESERVES

PROVEN +PROBABLE +POSSIBLE (3P)

PRODUCTION

UNRECOVERABLE

UNRECOVERABLE

Lower risk

Higher risk

NB: sub-commercial covers mainly fields for which commerciality is not yet proven and still subject to additional work

(different from sub-economic: not economic in the current prices and/or technologies).

COMMERCIAL

DISCOVERED

SUB-COMMERCIAL

UNDISCOVERED

Commerciality

Discovery

Exp

lora

tion-

Pro

duct

ion

a fu

lly e

stab

lishe

d pl

ayer

1

Gaz de France

Investor Day

22 May 2007

17

Decreasing uncertainty for reserves evaluation

Phase Exploration Appraisal Development Production

High 3P

Medium2P

Low 1P

Seismic

Wells

Production Data

ClassificationProspective

Resources

Contingent

Resources

Uncertainty

Available Data

Method of

evaluation

Decline curve analysis

Reservess

Analogy

Static Calculation

Numerical Simulation

Material Balance

Time line and level of certainty

Exp

lora

tion-

Pro

duct

ion

a fu

lly e

stab

lishe

d pl

ayer

1

Gaz de France

Investor Day

22 May 2007

18

Gaz de France Exploration-Production

Exploration-Production a fully established player

Successful track record

Growth driven strategy

Assets & projects portfolio

Ambitious prospects

Wrap up

• Operation

• Finance

• Exploration

Gaz de France

Investor Day

22 May 2007

19

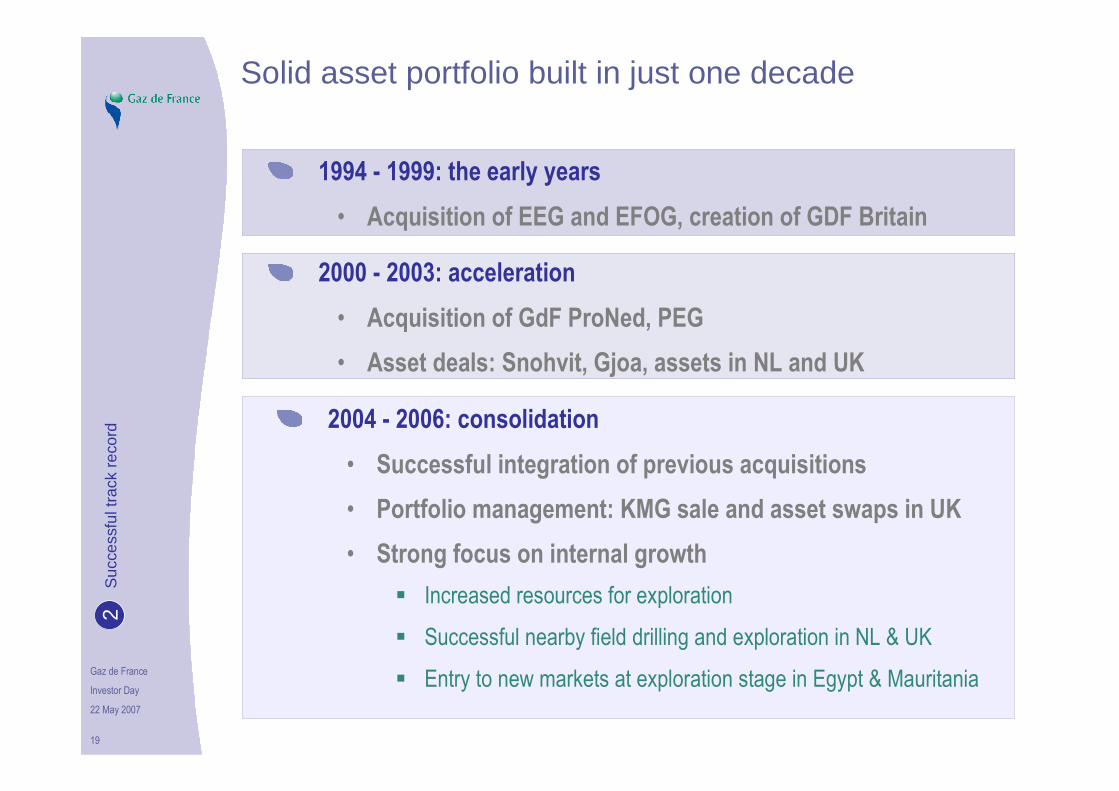

Solid asset portfolio built in just one decade

1994 - 1999: the early years

• Acquisition of EEG and EFOG, creation of GDF Britain

2000 - 2003: acceleration

• Acquisition of GdF ProNed, PEG

• Asset deals: Snohvit, Gjoa, assets in NL and UK

2004 - 2006: consolidation

• Successful integration of previous acquisitions

• Portfolio management: KMG sale and asset swaps in UK

• Strong focus on internal growth

� Increased resources for exploration

� Successful nearby field drilling and exploration in NL & UK

� Entry to new markets at exploration stage in Egypt & Mauritania

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

20

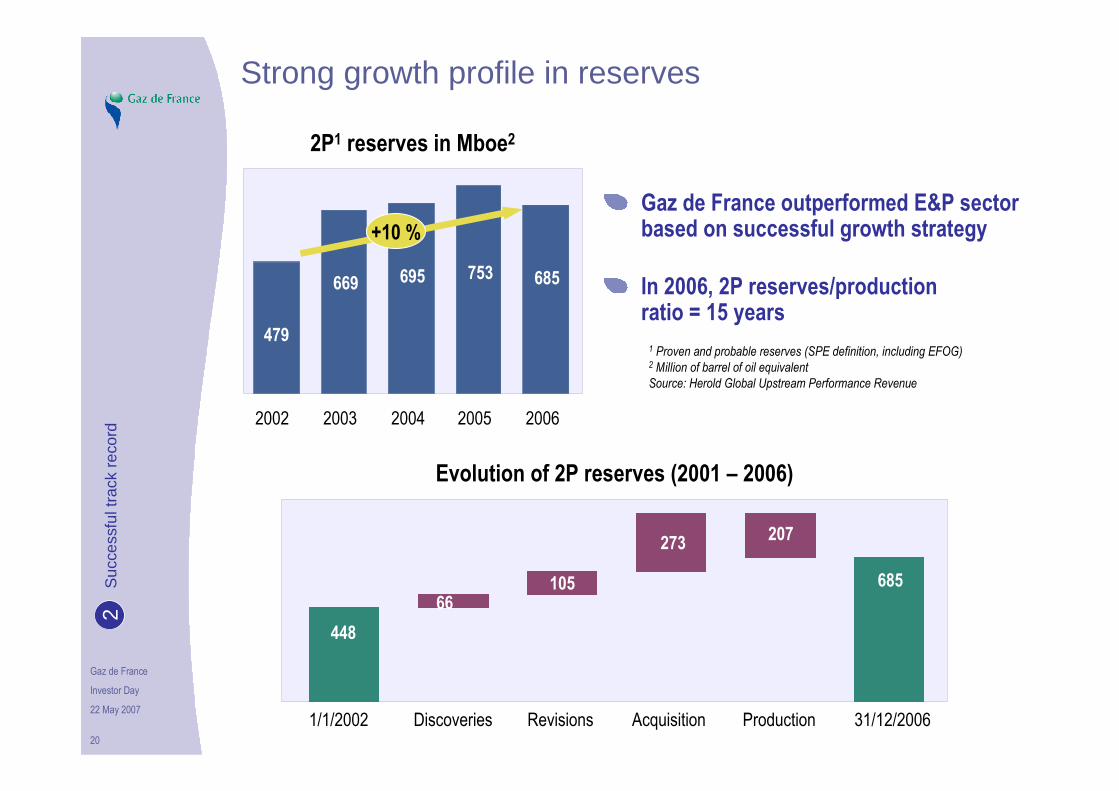

Strong growth profile in reserves

Gaz de France outperformed E&P sector based on successful growth strategy

In 2006, 2P reserves/production ratio = 15 years

Evolution of 2P reserves (2001 – 2006)

1 Proven and probable reserves (SPE definition, including EFOG)2 Million of barrel of oil equivalent

Source: Herold Global Upstream Performance Revenue

479

669 695 753 685

2002 2003 2004 2005 2006

2P1 reserves in Mboe2

+10 %

448

1/1/2002 Discoveries Revisions Acquisition Production 31/12/2006

448

685

207273

10566

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

21

Profitable growth

* Net sales, EBITDA and Operating Income do not account for EFOG consolidated under the Equity Method

2002 2003 2004 2005 2006

Net sales* EBITDA* Operating Income*

EFOG net results Oil & gas production incl. EFOG

0

300

600

900

1200

1500

1800

MEUR

15

20

25

30

35

40

45

50

55

Mboe

+42%

+53%

+112%

+13%

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

22

Gaz de France primarily operates concession contracts

• With the exception of Ivory Coast

PSC* accounts for < 1% of production and reserves

Sales portfolio breakdown (% production)

Diversified portfolio of commercial contracts

New production fields to modify sales portfolio breakdown

* PSC: Production Sharing Contract

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007 estimated

Long term contract(gas)

Market price(gas)

Brent related(oil)

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

23

Competitive technical costs

Technical costs very comparable to Peer Group2 composed of main license partners

In the context of rising cost for E&P sector 3, Gaz de France costs are remaining stable

1 For the definition of technical costs: see appendices2 Peer group includes european activities of Majors, Independants and Utilities (BG, Centrica, CoP, Dana, Dong, ENI, Hess,

Marathon, MOL, Norsk Hydro, OMV, Petro-Canada, RWE-Dea, Statoil, Talisman, Total, Wintershall)3 See appendix

Technical costs1 in eur/boe

13.6 12.9 12.8 12.7 13.3

Peer Group2 Europe (2 years average) GdF (2 years average)

2001-02 2002-03 2003-04 2004-05 2005-06

Source: Internal research

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

24

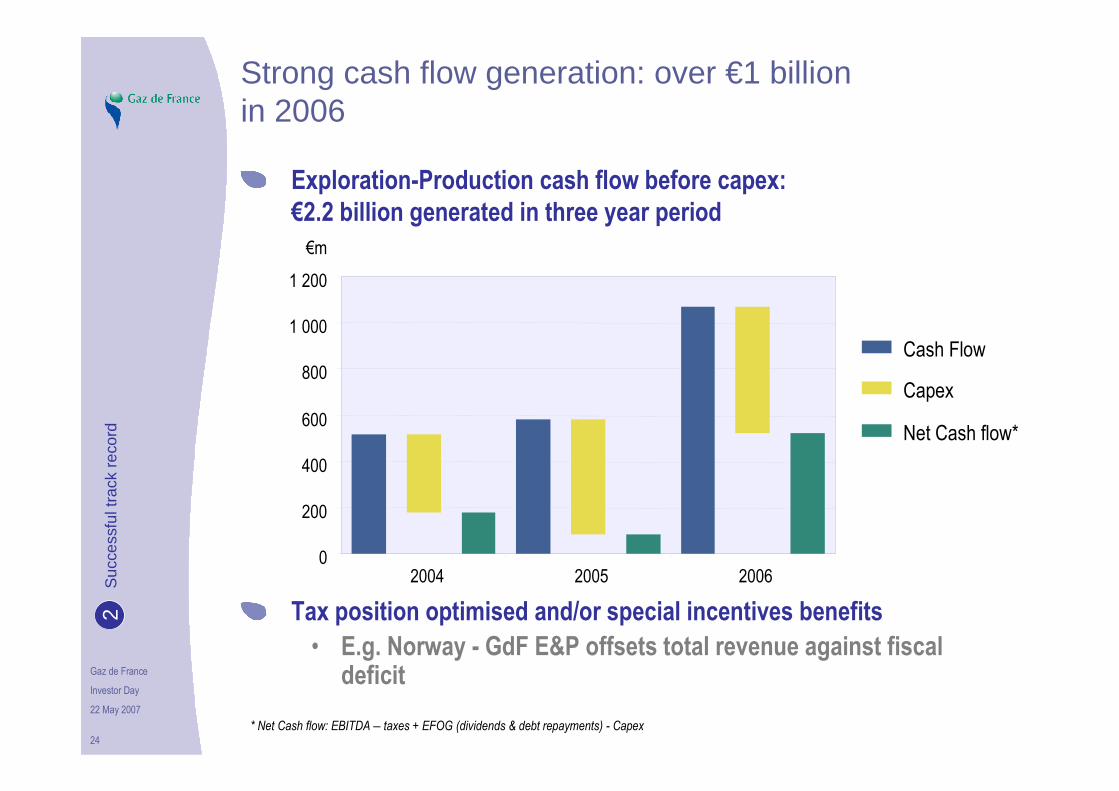

Strong cash flow generation: over €1 billion in 2006

Exploration-Production cash flow before capex: €2.2 billion generated in three year period

* Net Cash flow: EBITDA – taxes + EFOG (dividends & debt repayments) - Capex

0

200

400

600

800

1 000

1 200

2004 2005 2006

Cash Flow

Capex

Net Cash flow*

Tax position optimised and/or special incentives benefits

• E.g. Norway - GdF E&P offsets total revenue against fiscal deficit

Suc

cess

ful t

rack

rec

ord

2

€m

Gaz de France

Investor Day

22 May 2007

25

Sustained Upstream investments

Capex (acquisition, development, exploration)

Capex development Acquisition Exploration

0

250

500

750

1 000

1 250

1 500

2002 2003 2004 2005 2006

In MEUR

Exploration budget

CAGR +17%

0

50

100

150

200

2002 2003 2004 2005 2006

In MEUR

3 billion euros invested in past 5 years

• Acquisition of PEGin Germany

• Asset deals in UK and Netherlands

• Development projects in Norway and Netherlands

CAGR +17% 2002-2006

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

Exploration track record

Philip Drijkoningen

Head of Exploration

2S

ucce

ssfu

l tra

ck r

ecor

d

Gaz de France

Investor Day

22 May 2007

27

Reserve Replacement Ratio*

Reserve Replacement Ratio*

298%

112%

0%

100%

200%

300%

400%

2002-2004 2004-2006

Acquisition of PEG

Time between discovery and booking reserves

• Most discoveries are classified as Contingent Resources until they meet reserve definition criteria

Acquisitions and divesture significantly impact RRR*

• PEG acquisition in 2003, KGM sale in 2006

* RRR = ( Revisions + Discoveries + Acquisitions – Sales) / Production

Computed on a three years average based on 2P reserves

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

28

24 discoveries out of 42 exploration wells:

• 57% of success

+200 million barrels discovered:

• 2P reserves + unrisked contingent resources

57% success rate in exploration

0

2

4

6

8

10

12

14

2002 2003 2004 2005 2006

Number of exploration wells

Mauritania

Egypt

Algeria

Norway

Germany

Netherlands

UK

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

29

Competitive finding costs

Finding costs for 2P Reserves and Contingent Resources (unrisked)

• 1.8 Euro/boe

Finding costs limited to 2P Reserves

• 6.7 Euro/boe

Finding costs calculated as ratio of budget/volume over 5 years periodS

ucce

ssfu

l tra

ck r

ecor

d2

Gaz de France

Investor Day

22 May 2007

30

Industry benchmark confirms our solid performance

0%

10%

20%

30%

40%

IRR

0

5

10

15

20

Finding Cost US$/boe (2000-04)

0%

10%

20%

30%

40%

50%

60%

Success rate (2000-04)

* Peer Group: BG, Marathon, Apache, Repsol-YPF,

Wintershall, Norsk Hydro, Total, OMV, DONG, Woodside,

Occidental, Amerada, Kerr-McGee, Talisman, RWE-Dea,

ENI, ConocoPhilips, Encana.

Company results not disclosed for confidentiality reasons.

Peer Group*GDF

Peer Group*GDF

Peer Group*GDF

Source: Survey performed by WoodMackenzie early 2006

Suc

cess

ful t

rack

rec

ord

2

Gaz de France

Investor Day

22 May 2007

31

Gaz de France Exploration-Production

Exploration-Production a fully established player

Successful track record

Growth driven strategy

Assets & projects portfolio

Ambitious prospects

Wrap up

Gaz de France

Investor Day

22 May 2007

32

Our ambition: achieve double digit growth in production

Objective of 1,000Mboe for 2P reserves

Balance between oil and gas

Double digit growth for production

Gro

wth

driv

en s

trat

egy

3

Gaz de France

Investor Day

22 May 2007

33

Our growth strategy

Enlarge geographic coverage

Balance organic and external growth

Leverage value for other Group divisions

Gro

wth

driv

en s

trat

egy

3

Gaz de France

Investor Day

22 May 2007

34

Enlarge geographic coverage

Currently active in Europe and North Africa

Strong position built in a short period of time in mature countries, closed to our markets

Reinforce positions in "growth" countries

• Norway, Algeria

Enlarge geographic coverage to new growth regions

• West Africa, Middle East, Caspian SeaGro

wth

driv

en s

trat

egy

3

Gaz de France

Investor Day

22 May 2007

35

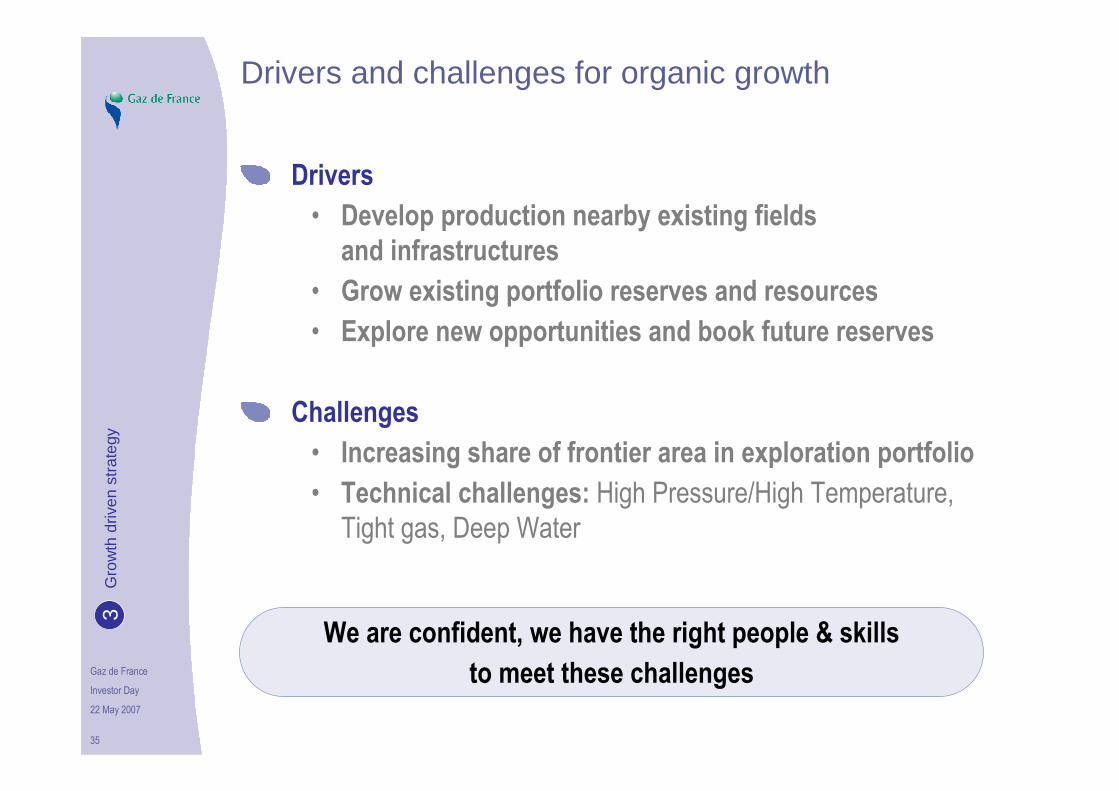

Drivers and challenges for organic growth

Drivers

• Develop production nearby existing fields and infrastructures

• Grow existing portfolio reserves and resources

• Explore new opportunities and book future reserves

Challenges

• Increasing share of frontier area in exploration portfolio

• Technical challenges: High Pressure/High Temperature, Tight gas, Deep Water

We are confident, we have the right people & skills

to meet these challenges

Gro

wth

driv

en s

trat

egy

3

Gaz de France

Investor Day

22 May 2007

36

External growth strategy

Boost operations and growth in new regions

• Initiate and sustain exploration efforts via bidding rounds, farm ins and acquisition of focused exploration portfolios

• Accelerate learning curve (subsurface expertise, etc)in a given basin

• Provide critical size in new areas

Balance asset portfolio across all stages (exploration, development, production) to sustain long term growth

Take advantage of value driven opportunistic acquisitions in line with capital discipline

Gro

wth

driv

en s

trat

egy

3

Gaz de France

Investor Day

22 May 2007

37

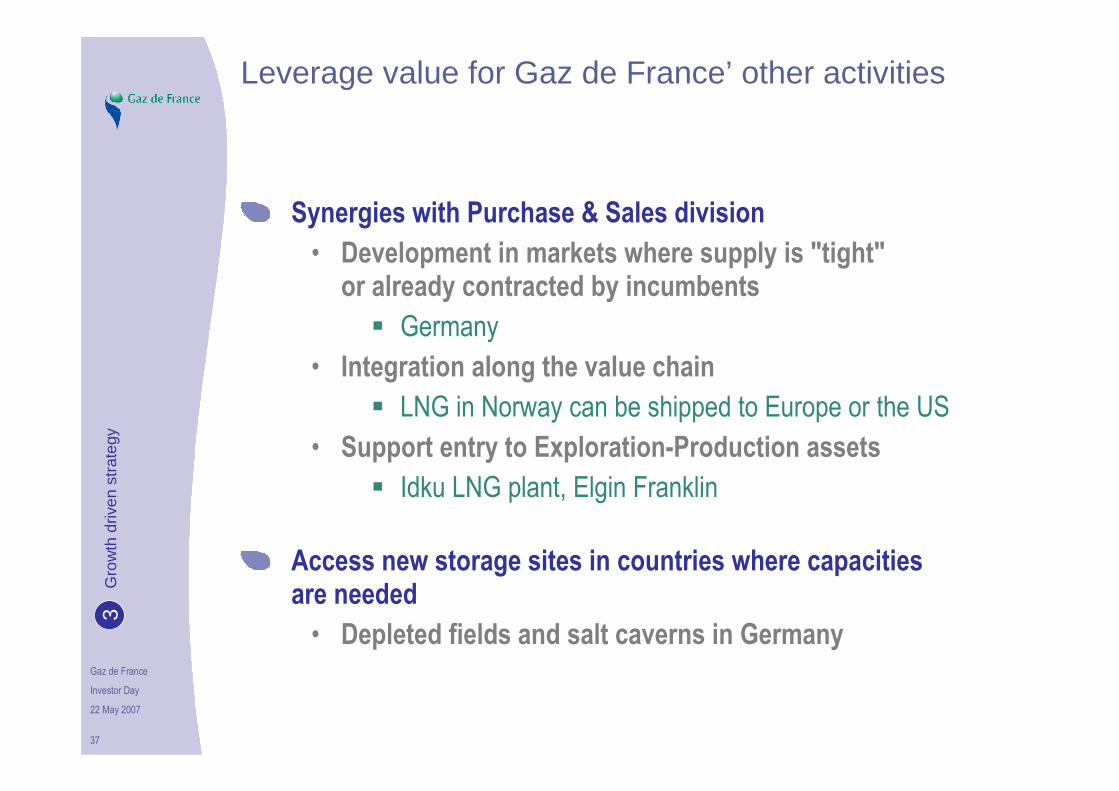

Leverage value for Gaz de France’ other activities

Synergies with Purchase & Sales division

• Development in markets where supply is "tight" or already contracted by incumbents

� Germany

• Integration along the value chain

� LNG in Norway can be shipped to Europe or the US

• Support entry to Exploration-Production assets

� Idku LNG plant, Elgin Franklin

Access new storage sites in countries where capacities are needed

• Depleted fields and salt caverns in Germany

Gro

wth

driv

en s

trat

egy

3

Gaz de France

Investor Day

22 May 2007

38

Gaz de France Exploration-Production

Exploration-Production a fully established player

Successful track record

Growth driven strategy

Assets & projects portfolio

Ambitious prospects

Wrap up

• Main producing countries

• Development projects

• Exploration portfolio

• Acquisition strategy

Gaz de France

Investor Day

22 May 2007

39

Balance between regions and maturity of projects

Production Development Exploration

Mature basins

On trend basins

Frontier areas

Southern gas basin (UK, NL, Germany)

Mauritania

Egypte(Nile Delta)

West of Shetland

Central North Sea

Barents Sea

Norvegian Sea

Algeria

Snohvit(Barents Sea)

GjoaTouat

Cash cows Medium to long term

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

40

2006 Production: 45.5 Mboe

Others include Kazakhstan (sold in 2006)

and Ivory Coast (not consolidated until 2007)

14.6

8.5 8.9

0.4

0.1

4.4 3.5

3.3 2.0

Netherlands UK Germany Norway Others

MBoe/year Liquids

Gas

14.6 12.8 12.4 3.3 2.4

2P Reserves: 685 Mboe

Current production coming mostly from asset portfolio in Netherlands, UK and Germany

Short term production growth will come mostly from Norway: 47% of 2P reserves

2006 production and reservesA

sset

s &

pro

ject

s po

rtfo

lio4

321.3

164.1

94.1

95.5

UK

NorwayNetherlands

Germany

Others

Gaz de France

Investor Day

22 May 2007

Video presentation

GdF ProNed

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

Netherlands and G block case study

Jan Treffers

President & General Manager GdF ProNed

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

43

Reserves (end 2006)

• 94 Mboe net GDF

Production planned 2007/2008

• 28 Mboe net GDF

Operate 30 platforms and 5 sub-sea wells

74 producing wells

• Capacity 15 M m3/day

670 km of pipeline

• Inclusive 480 km NGT

NGT* treating plant Uithuizen

Revenues 2006

• €545 million

220 employees (incl NGT)

Average 140 contractors

* Noordgastransport B.V.

GdF Proned: 3rd producer in the NetherlandsA

sset

s &

pro

ject

s po

rtfo

lio4

Gaz de France

Investor Day

22 May 2007

44

GdF Proned: competitive differentiation

Successful exploration results

• 57% average success ratio in last 5 years

Low cost operator (operating and investment) with high HSE standards

Innovative operator

• 1st in sub-sea development in Netherlands (1988)

• World’s largest offshore CO2 removal plant (1987)

• 1st to re-use platforms (5 platforms re-used, 1 planned in 2007)

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

45

G-BlocksG-Blocks

G block case study – success storyA

sset

s &

pro

ject

s po

rtfo

lio4

Gaz de France

Investor Day

22 May 2007

46

G block case study – success story A

sset

s &

pro

ject

s po

rtfo

lio4

Gaz de France

Investor Day

22 May 2007

47

1999/2000:G17-4 farm-in well discovered G17d-A field (2.3 BCM gross reserves)

G17-4

G block case study – success storyFirst discovery

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

48

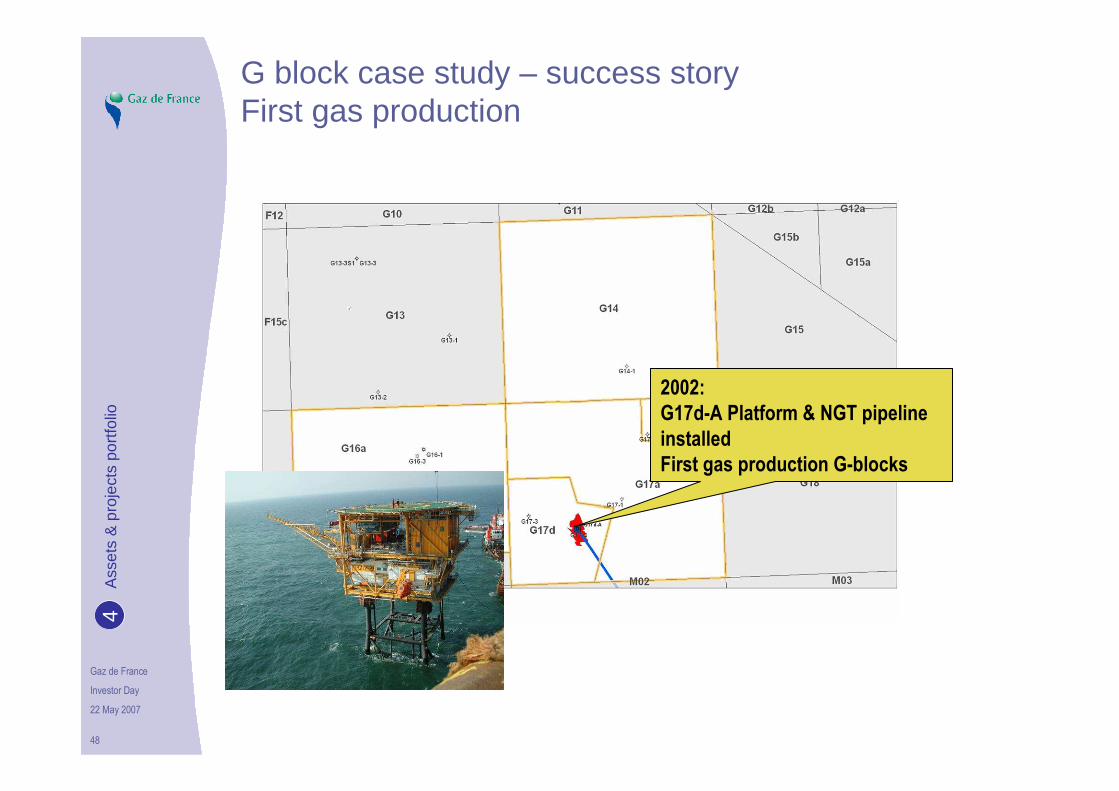

G17d-A

2002:G17d-A Platform & NGT pipeline installedFirst gas production G-blocks

G block case study – success storyFirst gas production

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

49

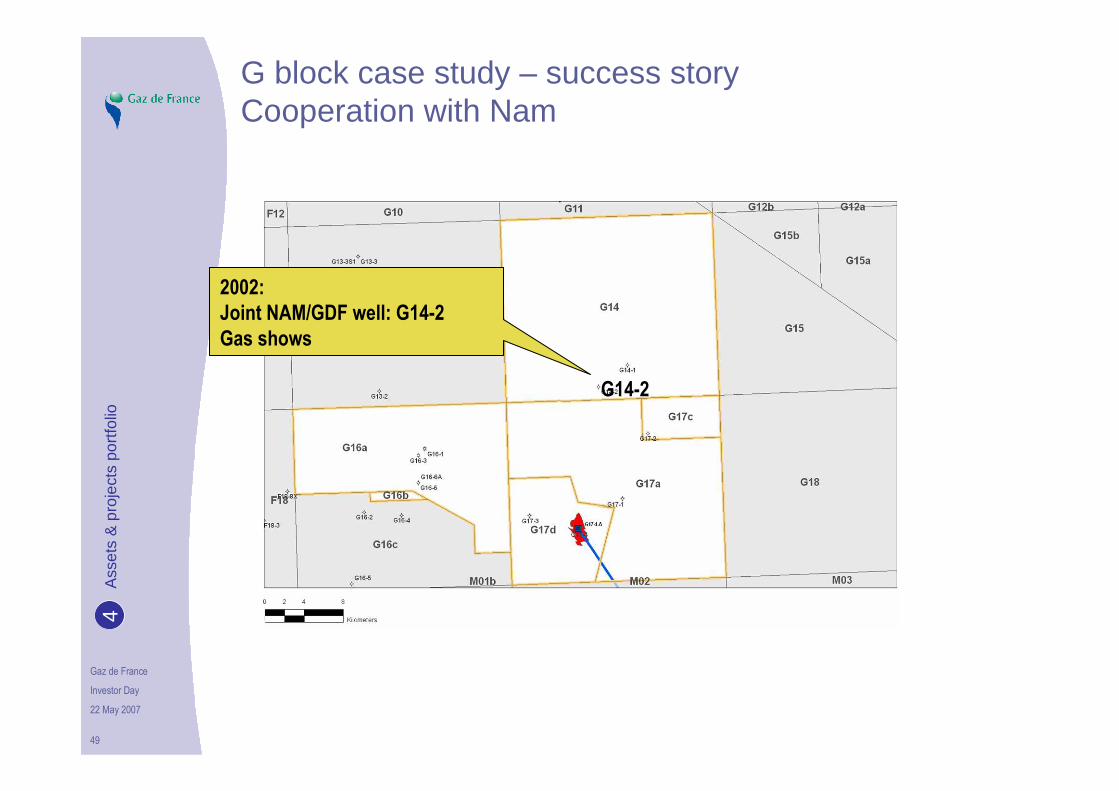

2002:Joint NAM/GDF well: G14-2Gas shows

G14-2

G block case study – success storyCooperation with Nam

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

50

2003:Sole risk GDF well: G14-2stDiscovered G14-A field(Reserves 6 BCM)

G14-2st

G block case study – success storySole risk GDF well

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

51

G16a-A field

2003:GDF Acquired blocks G16a&b with G16a-A field from NAM(1.7 BCM reserves)

G block case study – success storyGDF acquires blocks from Nam

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

52

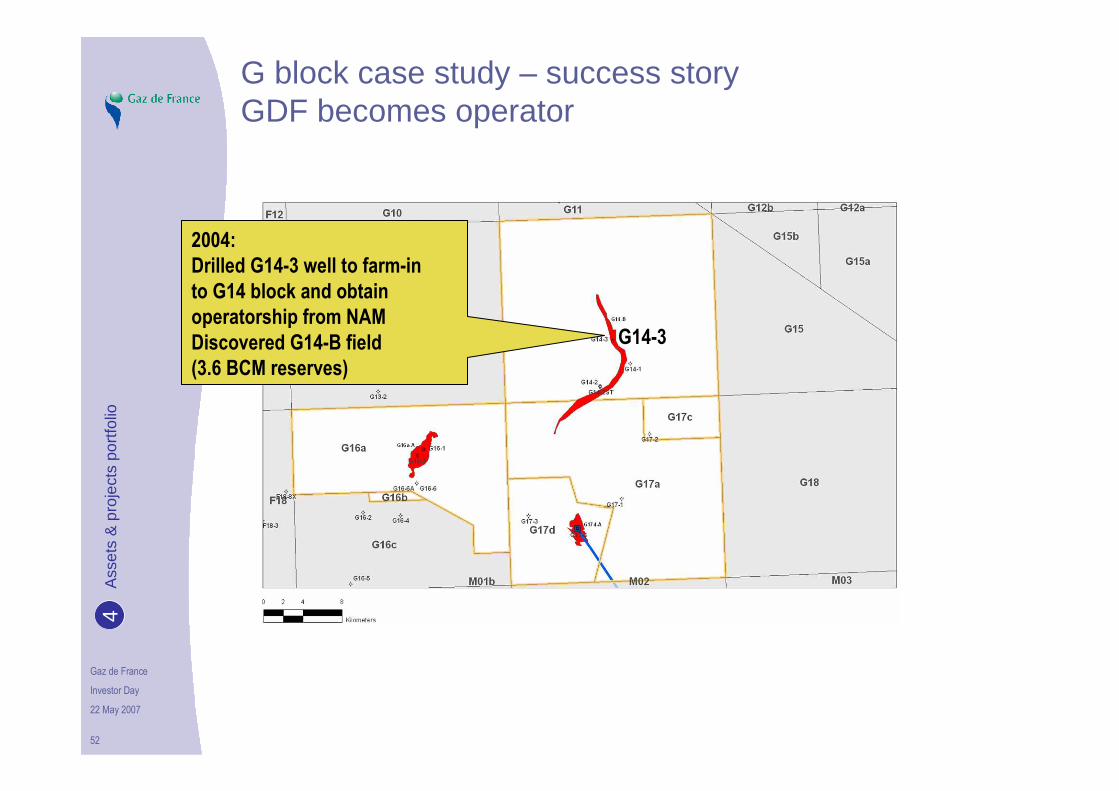

2004:Drilled G14-3 well to farm-in to G14 block and obtain operatorship from NAMDiscovered G14-B field(3.6 BCM reserves)

G14-3

G block case study – success storyGDF becomes operator

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

53

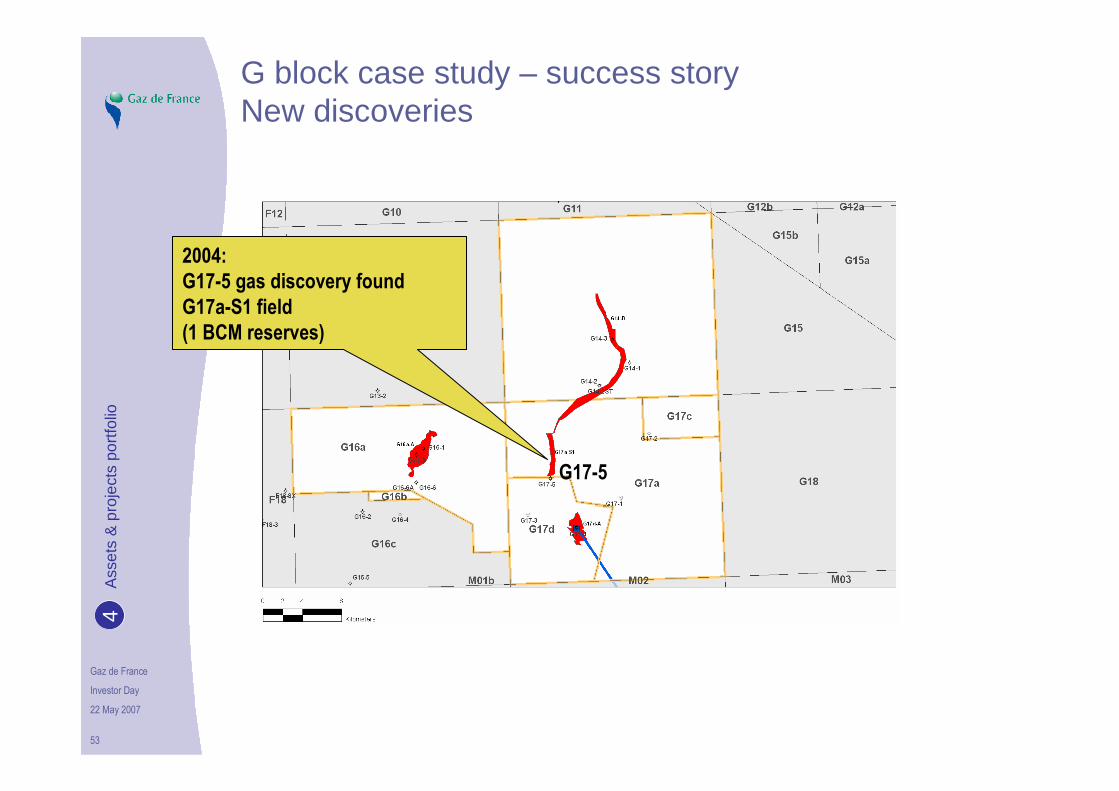

G17-5

2004:G17-5 gas discovery found G17a-S1 field(1 BCM reserves)

G block case study – success storyNew discoveries

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

54

2005:G14-A, G16a-A and G17d-AP platforms& G17a-S1 subsea installed

G17a-S1G16a-A

G14-A

G17d-AP

G block case study – success storyNew infrastructures

2005:Pipelines connecting G14-A, G16a-A and & G17a-S1 to G17d-AP platform installed

2005:G14-4 gas discovery found G14-C field(1.9 BCM reserves)

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

55

2005:G14-5 dry well

G14-5

G block case study – success storyNormal industry risks

2006:G17-6 dry well

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

56

2007:G16-7 exploration well

Future G14exploration well?

Future G16exploration well?

G block case study – success storyStill a prospective area

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

57

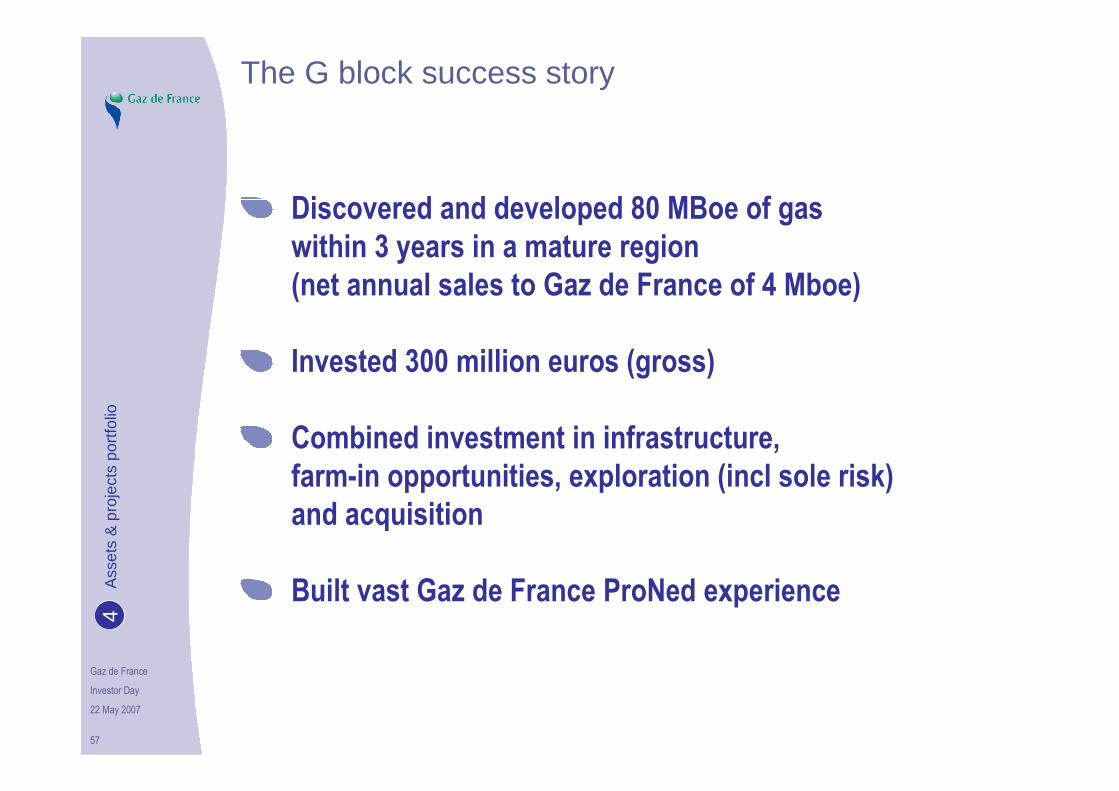

The G block success story

Discovered and developed 80 MBoe of gas within 3 years in a mature region(net annual sales to Gaz de France of 4 Mboe)

Invested 300 million euros (gross)

Combined investment in infrastructure,farm-in opportunities, exploration (incl sole risk) and acquisition

Built vast Gaz de France ProNed experienceAss

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

58

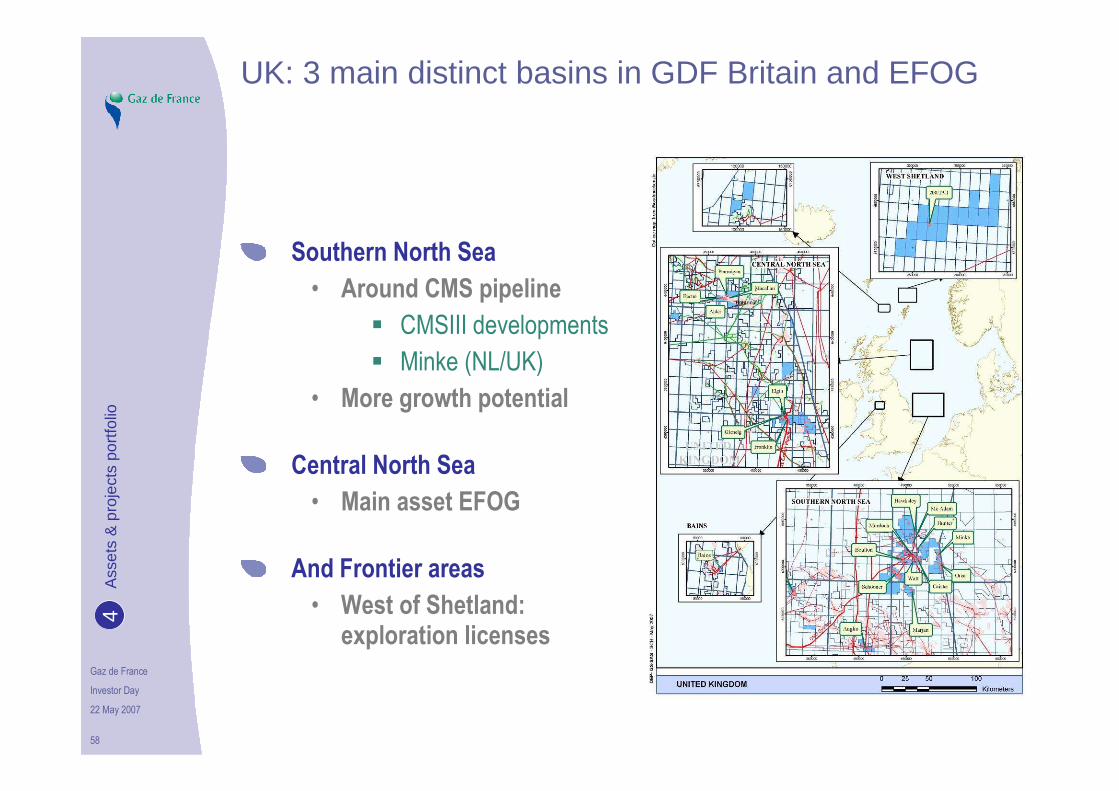

UK: 3 main distinct basins in GDF Britain and EFOG

Southern North Sea

• Around CMS pipeline

� CMSIII developments

� Minke (NL/UK)

• More growth potential

Central North Sea

• Main asset EFOG

And Frontier areas

• West of Shetland: exploration licenses

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

59

EFOG: e.g of downstream - upstream synergies

• High Pressure / High Temperature

• Operated by Total

• Gaz de France Purchase & Sale division as customer for gas

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

Exploration-Production in Germany

Albrecht Möhring

Managing Director, Technical AffairsGaz de France - PEG

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

61

Nearly 30 % of Gaz de France total production

Activity

• Oil & gas exploration

• Production

• Marketing

• Gas storage facilities

Key figures (2006)

• Reserves: 164 Mboe

• Gas Production: 8.85 Mboe

• Oil Production: 3.5 Mboe

• Revenues: €600 million

• Employees: 670

26% Oil

28% Gas

GDF-PEG Share of total GDF Production (2006)

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

62

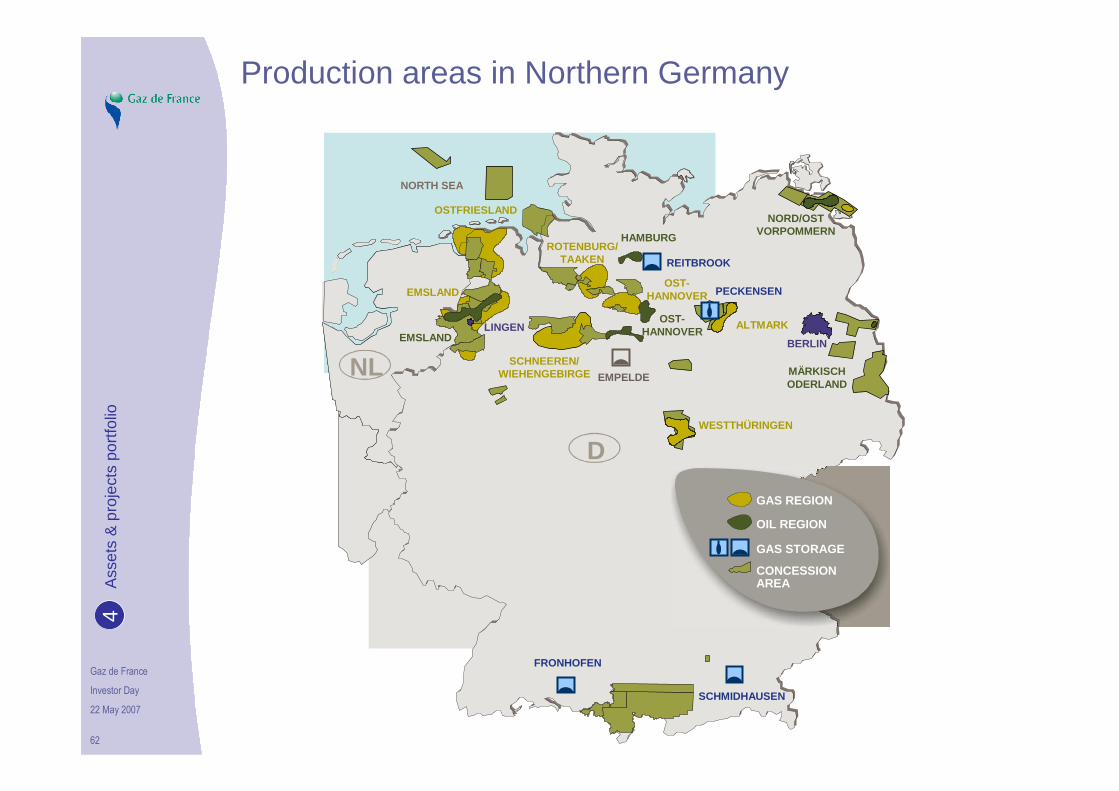

Production areas in Northern Germany

GAS REGION

OIL REGION

CONCESSIONAREA

GAS STORAGE

D

NL

ROTENBURG/TAAKEN

NORD/OSTVORPOMMERN

ALTMARK

MÄRKISCHODERLAND

WESTTHÜRINGEN

NORTH SEA

OST-HANNOVER

SCHNEEREN/WIEHENGEBIRGE

BERLIN

HAMBURG

EMSLAND

EMSLAND

OSTFRIESLAND

LINGEN

FRONHOFEN

SCHMIDHAUSEN

EMPELDE

OST-HANNOVER PECKENSEN

REITBROOK

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

63

Tight Gas Development: Innovative technology (1/9)

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

64

4km

Leer ExplorationDepth Structure Map

of the "Base Zechstein"

12 potential exploration targets are in the closer vicinity of the Leer Central Block

Exploration wells might enable us to tie a suitable rig to the project in a long term view

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (2/9)

Gaz de France

Investor Day

22 May 2007

65

604525OGIP (M boe)

P10MeanP90LEER Structure

Base Z - Depth Structure (Pre-well adjustment)

(3D Seismic, PreSDM Interpretation MARSKY 2003)

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (3/9)

Gaz de France

Investor Day

22 May 2007

66

Salzstock Rhaude

Oberkreide

Jura

Keuper

Muschelkalk

Buntsandstein

Zechstein

Karbon(Westfal C)

Tertiär500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

Leer Z4Teufe[m]

W E

Leer Block

Unterkreide

Heidberg-Dambeck-Member

Bahnsen-Wustrow-Member(gasführende Sandsteine)

Quartär

GWC ~4470m

0 500 1000 1500 2000 2500m

LEER Breinermoor

Rotliegend FWL ~ 4464 m

13 3/8“

9 5/8“

7“

4 1/2“

32“

W-E Geological Cross-Section through the Leer Block

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (4/9)

Gaz de France

Investor Day

22 May 2007

67

Salzstock Rhaude

Oberkreide

Jura

Keuper

Muschelkalk

Buntsandstein

Zechstein

Karbon(Westfal C)

Tertiär500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

Leer Z4Teufe[m]

W E

Leer Block

Unterkreide

Heidberg-Dambeck-Member

Bahnsen-Wustrow-Member(gasführende Sandsteine)

Quartär

GWC ~4470m

0 500 1000 1500 2000 2500m

LEER Breinermoor

Rotliegend FWL ~ 4464 m

13 3/8“

9 5/8“

7“

4 1/2“

32“

W-E Geological Cross-Section through the Leer Block

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (5/9)

Gaz de France

Investor Day

22 May 2007

68

Frac Technic

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (6/9)

Gaz de France

Investor Day

22 May 2007

69

Frac Technic

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (7/9)

Gaz de France

Investor Day

22 May 2007

70

Test Rate: 14,000 m³/h vs 4,000 m³/h without technology

Leer Z4 - Gas Test

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (8/9)

Gaz de France

Investor Day

22 May 2007

71

Leer Z4 - Facility

Ass

ets

& p

roje

cts

port

folio

4

Tight Gas Development: Innovative technology (9/9)

Gaz de France

Investor Day

22 May 2007

72

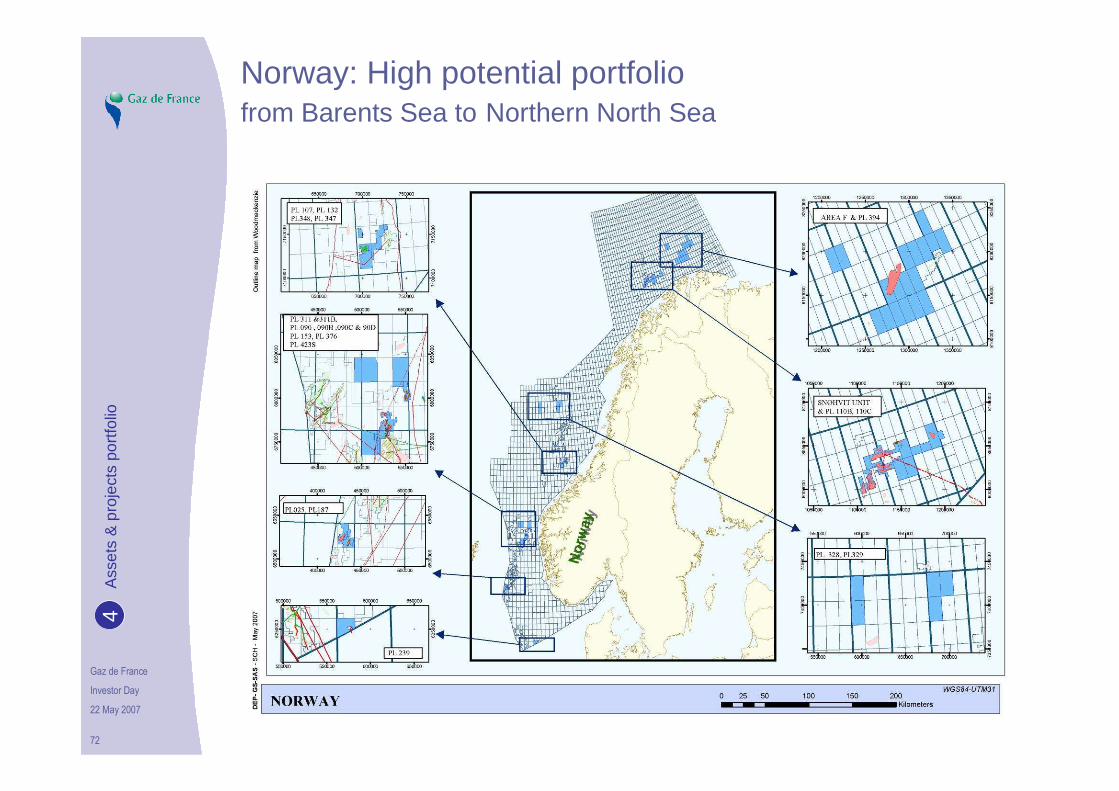

Norway: High potential portfoliofrom Barents Sea to Northern North Sea

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

Video presentation

Snøhvit

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

74

Snøhvit - challenging & innovative project

• Fields: Snøhvit, Albatross and Askeladd, discovered in 1981–84

• Water depth: 250 – 340 m

• Distance to shore: 140 km

• Gas in place (GIIP): 317 GSm3 / 11.2 TCF

• Condensate: 34 MSm3

• Annual LNG production : 5.7 GSm3

• Annual GPL production: 130000 to 330000t

• Annual Condensate prod. : 370000 to 630000t

• Consortium:

Statoil ASA (Operator) 33.53%

Petoro AS 30.00%

Total E&P Norge AS 18.40%

Gaz de France Norge AS 12.00%

Amerada Hess Norge AS 3.26%

RWE Dea Norge AS 2.81%

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

75

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

76

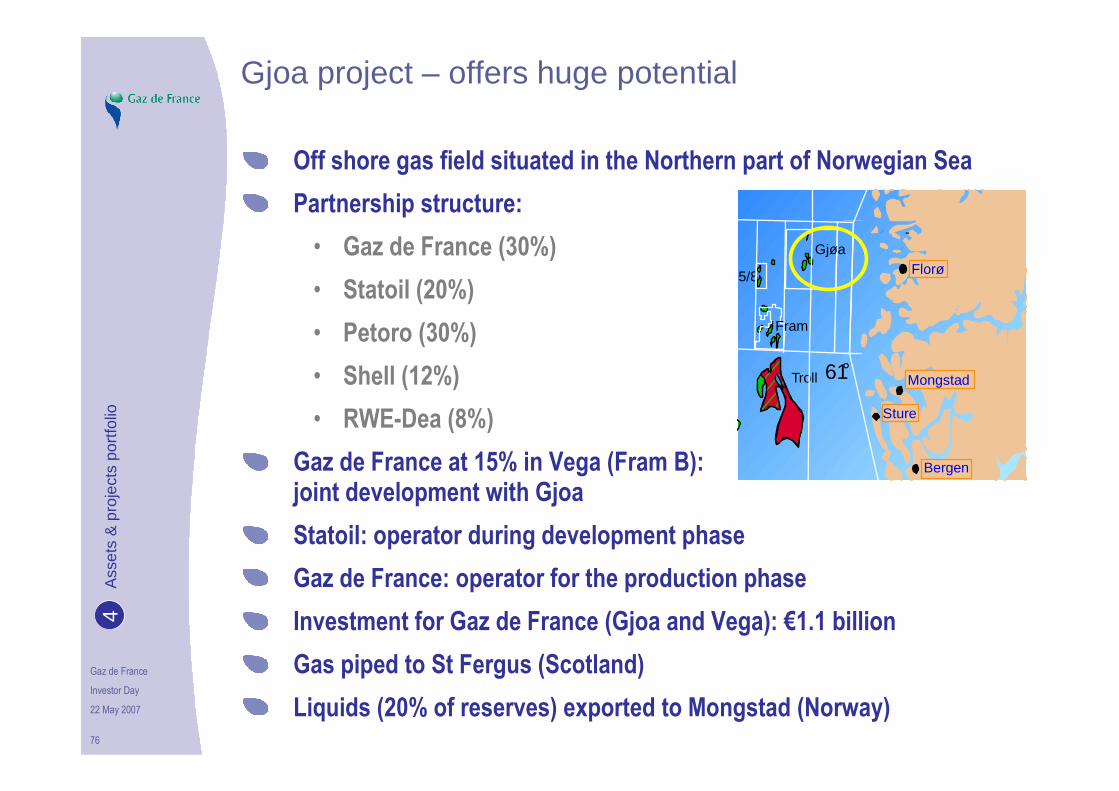

Gjoa project – offers huge potential

Off shore gas field situated in the Northern part of Norwegian Sea

Partnership structure:

• Gaz de France (30%)

• Statoil (20%)

• Petoro (30%)

• Shell (12%)

• RWE-Dea (8%)

Gaz de France at 15% in Vega (Fram B):joint development with Gjoa

Statoil: operator during development phase

Gaz de France: operator for the production phase

Investment for Gaz de France (Gjoa and Vega): €1.1 billion

Gas piped to St Fergus (Scotland)

Liquids (20% of reserves) exported to Mongstad (Norway)

Florø

Bergen

Mongstad

Sture

61 ° T roll

35/8 Gjøa

Fram

Camilla- Belinda

Fram B

Florø

Bergen

Mongstad

Sture

61 ° T roll

35/8 Gjøa

Fram

Camilla- Belinda

Fram B

Florø

Bergen

Mongstad

Sture

61 ° T roll

35/8 Gjøa

Fram

-

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

77

Gjoa: Development concept

Gas export El-power from shore Oil export

Vega

Gjøa

Gjøa – Vega: joint development

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

78

Algeria -Touat project

Production Sharing Contractsigned Jan 2003

Gaz de France 75% as operator, Sonatrach 25%

• Phase I: 2003-2005 4 wells/ 500 Km2 of 3D seismic

• Phase II: 2006-2007 4 wells/ 500 Km2 of 3D seismic

• Phase II ended successfully

First gas expected in 2011

Expected total upstream investment +/- $1 billion

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

Video presentation

Touat

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

Exploration strategy

Philip Drijkoningen

Head of Exploration

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

81

Exploration Strategy

Continue with value driven nearby field exploration in mature regions

• Benefit from short time-to-market, regional expertise and low risk acreage

Manage evolving portfolio mix of higher reward, higher risk opportunities in emerging countries

• Develop regional knowledge to identify new promising regions

• Ensure prospect profile meets strategic fit, competitive advantage and Gaz de France’ objectives

• Apply technical and risk assessment methods to measure opportunities

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

82

Exploration Budget

Long term target risk/reward balance

2006 and 2007 exploration budget: €150 million

* Probability of Success

Ass

ets

& p

roje

cts

port

folio

4

% of budgetType of exploration Standard POS*

Nearby Field Exploration- Lower Risk

- Smaller size fields40-60% 45%

Evolving Plays / On Trend - Moderate Risk/reward

20-40% 25%

Frontier Plays- Higher Risk/reward - Larger volumes

10-30% 15%

Gaz de France

Investor Day

22 May 2007

83

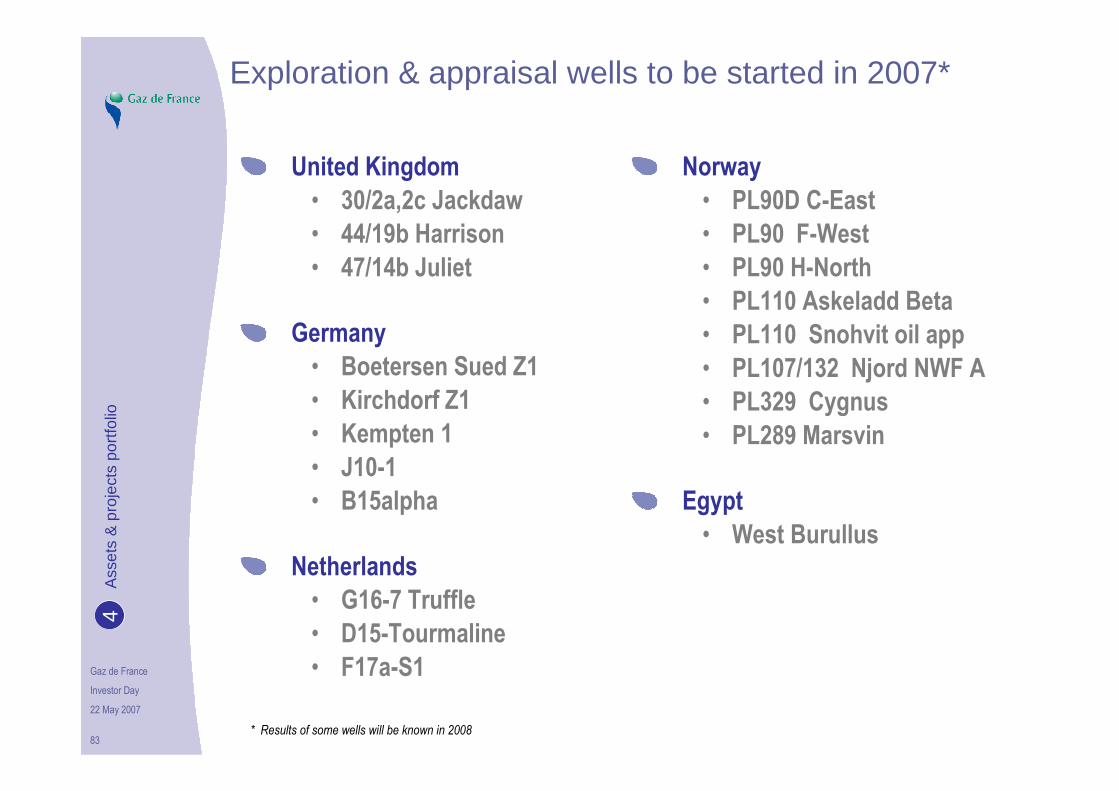

Exploration & appraisal wells to be started in 2007*

United Kingdom

• 30/2a,2c Jackdaw

• 44/19b Harrison

• 47/14b Juliet

Germany

• Boetersen Sued Z1

• Kirchdorf Z1

• Kempten 1

• J10-1

• B15alpha

Netherlands

• G16-7 Truffle

• D15-Tourmaline

• F17a-S1

Norway

• PL90D C-East

• PL90 F-West

• PL90 H-North

• PL110 Askeladd Beta

• PL110 Snohvit oil app

• PL107/132 Njord NWF A

• PL329 Cygnus

• PL289 Marsvin

Egypt

• West Burullus

* Results of some wells will be known in 2008

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

84

Southern Gas BasinUnited Kingdom

Netherlands

Germany offshore

Germany onshore

Central North SeaUnited Kingdom

Norvegian SeaNorway

Barents SeaNorway

Development in enlarged Europe

Eastern border

West of ShetlandUnited Kingdom

Norvegian North SeaNorway

Denmark

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

85

Nile Delta BasinEgypt

Mauritaniaoffshore

Ivory Coast offshore

Sbaa BasinAlgerie

North Africa, West Africa, Middle East, Caspian Sea

Exploration licenses currently held by GdF

Projects under analysis –focus for the area

Ass

ets

& p

roje

cts

port

folio

4

Gaz de France

Investor Day

22 May 2007

86

Gaz de France Exploration-Production

Exploration-Production a fully established player

Successful track record

Growth driven strategy

Assets & projects portfolio

Ambitious prospects

Wrap up

Gaz de France

Investor Day

22 May 2007

87

Boost organic growth

Organic Capex 2007-2011

• Budget €3-3.5 billion (Gjoa, Touat.., excl. acquisitions)

Production organic growth 2007-2011

Am

bitio

us p

rosp

ects

5

Estimated Production profile

MBoe/year

0

10

20

30

40

50

60

70

2006 2011

45

61+ 6%

Gaz de France

Investor Day

22 May 2007

88

Significant developments in near future, in addition to exploration to boost production

Targeted acquisitions to complete reserves and reach 1 billion barrels

100

200

300

400

500

600

700

800

900

1 000

2006

2007

2008

2009

2010

2011

2012

2013

Current reserves

Appraisal North Sea

Norway upside

Exploration

Reserve profile (Mboe)

Balance of organic and external growth

0

External growth

Am

bitio

us p

rosp

ects

5

Gaz de France

Investor Day

22 May 2007

89

Gaz de France Exploration-Production

Exploration-Production a fully established player

Successful track record

Growth driven strategy

Assets & projects portfolio

Ambitious prospects

Wrap up

Gaz de France

Investor Day

22 May 2007

90

Wrap up

Gaz de France is well positioned as an established Exploration-Production company

Our track record in generating growth is excellent

We aim to be a large Independent in terms of size and profitability

To achieve this, we will:

• Capitalise on existing positions

• Develop reserves and resources already in our portfolio

• Explore new opportunities and book future reserves

• Boost external growth and balance portfolio by acquiring profitable assets

Wra

p up

6

Gaz de France

Investor Day

22 May 2007

Thank you for your attention

It’s time for questions !

Gaz de France

Investor Day

22 May 2007

Appendices / Back-up

Gaz de France

Investor Day

22 May 2007

93

Booming upstream investments

Strong competition for assets and large number of "new entrants"such as NOCs outside their own countries and small exploration firms

Lead to very significant increase in E&P investments worldwide

E&P investments in billion USD

Source: IFP 2006

0

50

100

150

200

250

300

350

2004 2005 2006 2007e

North America Latin America North Sea Russia and China Others

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

94

Upstream costs on the rise for few years

• Increased investments in E&P and

• Higher commodity prices driven by overall economic growth

� Shortage of rigs and experienced people

� Rising drilling and construction costs

� Delays in developments

In such a context, know how of operating companies is key: management of drilling rigs, planning, control of investments … help minimize risks

Rising production and development costsA

ppen

dice

s7

Evolution of Upstream capital costs(index 100 in 2000)

90

110

130

150

170

190

2000 2001 2002 2003 2004 2005 2006

Source: les Echos / CERA

Gaz de France

Investor Day

22 May 2007

95

National Oil Companies (NOC)

Very different history and legal context

Largest part of oil and gas reserves in the world: more than 75% of oil reserves and 60% of gas reserves

Less in need of International Oil Companies for investment

Still in need for technologies ?

Tend to invest more and more outside their own backyard

Look for upstream to downstream integration

Source: James Baker Institute – Rice University

Based on Proven reserves figures – not exhaustive

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

96

International Oil Companies (IOC)

Successors of the Seven Sisters: Exxon Mobil, BP, Chevron, Shell

IOCs also include: Total, ENI, ConocoPhillips…

"Mega"mergers took place since the Seven Sisters, but decreasing share of the oil&gas reserves since mid 70s

Some companies are intermediate between IOCs and NOCs: Statoil, Petronas…

Competitive advantages in managing large projects and in technologies

Large projects tend to be located in countries with strong NOCs:

• Face growth difficulties along with the increasing political and financial strengths of NOCs

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

97

E&P Independents

Smaller size portfolios

Very specific risk profile with strong focus on:

• Limited number of countries

• Few type of projects/technologies

Comparative advantage in smaller fields:

• More reactive

• Lower fixed costs

• Increasing role as average field size declines ?

M&A market very active, smaller size producers tend to merge or acquire each other

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

98

Utilities companies

Few North American utilities developed upstream business (Calenergy …)

Limited number of European utilities have really invested in E&P: RWE-Dea, Eon Ruhrgas, Centrica

Generally looking for assets within reach of their markets

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

99

2002-04 Discoveries

2004 Development sanction

2006 Start of production

2019 Estimate of abandonment

From exploration to production

For historical reasons, time to market has been very long in E&P:

• The average for oil in the world is 12-15 years

• More than 30 years for gas: huge amount of stranded gas

Significant difference between mature areas with existing infrastructure and green field areas …

Elgin/ Franklin (UK) G14 (NL)

1986-91 Discoveries

1997 Development sanction

1997-2001 Platform Construction

2001 Start of production

2042 Estimate of abandonment

2004-06 Platform ConstructionApp

endi

ces

7

Gaz de France

Investor Day

22 May 2007

100

SNØHVIT : an integrated project from gas and condensate production to LNG shipping

CO2 Injection

well

Production well

Seabed

Reservoir

Albatross

Production wells

CDU

Plem

Production wells

Production wells

Snøhvit

CO2 Injection well

Slug catcher Inlet facilities

Pretreatment

Fractionation

Carbon dioxide

MEG recovery

Condensate production

LPG production

LNG production

Liquefaction cycle Subcooling cycle

Storage and loading:

LNG, LPG, condensate

Precooling cycle

Prepared by Petrolink as

Gaz de France

Investor Day

22 May 2007

101

Other countries positions

Ivory Coast: profitable gasproduction dedicatedto a power plant

Egypt: one exploration licence and looking for more assets

Mauritania: LNG or local electricity production ?

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

102

Commercial and fiscal aspects

Tax rates in concession regimes varies for Gaz de France affiliates, between 35-40% and 78% in Norway

• Investment incentives in Norway are such that Gaz de France offsets all its revenues against its fiscal deficit

Current gas and oil sales can be split between:

• Oil and liquids sold under contracts with a strong link to Brent (adjusted for quality and transportation costs)

• Gas sold under:

� Gas market indexes: NBP, Zeebrugge, TTF

� Typical continental gas contracts including various fuel

indexes and slipping averages

Although volumes sold under gas market indexes increased, long term contracts – continental type – remain dominant

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

103

The main fiscal regimes

Concession regimes: taxation applies mainly to income, there can be special tax rates for E&P activities and royalties

• UK, Netherlands, Germany, Norway…

• Most of the reserves and production of Gaz de France are under concession regimes, except Ivory Coast (PSC)

Production Sharing Contracts can be split into two subcategories where:

• E&P companies have rights to a portion of hydrocarbons: production and reserves are already net of tax ("entitlement")

• E&P companies have no (physical) rights on hydrocarbons, they receive the financial value of it

• Booking of reserves under PSC is less favorable as the entitlement is already net of tax

Service contracts (or Buy Backs): the E&P company is paid like a service provider and has no access to hydrocarbons: Iran…

• Booking of reserves requires a case by case analysis

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

104

Reserves - Definition and evaluation of reserves

Reserves are volumes of discovered hydrocarbons estimated to be technically and commercially recoverable

Oil and gas reserves are based on interpretation of geologic and engineering data available at the time of the estimate

Reserves are estimated under conditions of uncertainties, they are not counted for as a stock of goods

Different classification systems and definitions existApp

endi

ces

7

Gaz de France

Investor Day

22 May 2007

105

Evaluation according to SPE / WPC guidelines

Gaz de France evaluates its Proven and Probable (2P) reserves according to the guidelines of:

• The Society of Petroleum Engineers (SPE) and

• The World Petroleum Congress (WPC)

2P reserves are those quantities of hydrocarbons that are estimated to be recoverable more likely than not

• Commercially

• From known geologic accumulations

• From a given date forward

• With existing technologies

• Under the economic assumptions of the evaluator (evolution of prices, inflation and exchange rates)

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

106

Technical costs per barrel

A synthetic indicator calculated as follows:

• Opex : all expenses related to production, including treatment, transportation and G&A cost related to production

• Exploration costs expended (G&G expenses, seismic studies and G&A related cost as well as dry hole cost)

• And DD&A (Unit of production depreciation plus abandonment)

• Divided by the production of the year

How to understand it:

• Numerator includes all stages of projects from exploration to dismantling, it gives a fair view of upstream costs/investments

• Denominator reflects only the producing assets, a sudden increase or drop in production will affect it : pluriannualaverages are more significant

• Vary strongly according to the type of portfolio (large exploration base vs large producing base) and to the growth strategy (acquisition vs exploration)

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

107

Benchmark confirms performance

Comparison of GDF performance with peers, key metrics:

• Exploration well success rates

• Finding costs

• IRR

Survey performed by WoodMackenzie early 2006:

• Covers exploration activity of Gaz de France and Peer Group (2000-2004)

• Peer Group includes: BG, Marathon, Apache, Repsol-YPF, Wintershall, Norsk Hydro, Total, OMV, DONG, Woodside, Occidental, Amerada, Kerr-McGee, Talisman, RWE-Dea, ENI, ConocoPhilips, Encana

• Focus on Europe and North Africa

Definitions and methodology: WoodMackenzie

App

endi

ces

7

Gaz de France

Investor Day

22 May 2007

108

Build growth and create long term value

Cumulated value for the Group

Time line

2P reserves: "cash cows" and fields to be developed

Contingent resources: fields to be developed in coming years

Exploration portfolio: from mature to frontier areas

Projects matured internally

or integrated in portfolio

via acquisitionApp

endi

ces

7

CO2 sequestration: convert R&D project into profitable business model

Storage in depleted fields: new sites made available for the Group

Gaz de France

Investor Day

22 May 2007

109

CO2 sequestration projectsGaz de France involvment

CO2 injection on going

Gaz de France operator

CO2 injection pilot project

Gaz de France operator

CO2 injection project

Gaz de France partner

CO2 injection project

Gaz de France operator

Participation to various R&D

consortium on CO2

sequestration in depleted fields

and deep saline aquifersApp

endi

ces

7

TOUAT

SNØHVIT

K12B

ALTMARK