gao february 1995 an overview

TRANSCRIPT

United States General Accounting Office

GAO High-Risk Series

February 1995 An Overview

GAO/HR-95-1

GAO United States

General Accounting Office

Washington, D.C. 20548

Comptroller General

of the United States

February 1995

The President of the SenateThe Speaker of the House of Representatives

In 1990, the General Accounting Office began a specialeffort to review and report on the federal program areaswe considered high risk because they were especiallyvulnerable to waste, fraud, abuse, and mismanagement.This effort, which has been strongly supported by theSenate Committee on Governmental Affairs and theHouse Committee on Government Reform and Oversight,brought much needed focus to problems that werecosting the government billions of dollars.

In December 1992, we issued a series of reports on thefundamental causes of problems in designated high-riskareas. We are updating the status of our high-riskprogram in this second series. In this Overview report, wediscuss the urgent need to continue addressing criticalhigh-risk problems, covering such areas as DefenseDepartment contract and inventory management, revenuecollection operations, major lending programs, andoversight of tens of billions of dollars in contracts. Wealso introduce newly designated high-risk areas, such asserious and long-standing financial managementweaknesses in Defense, growing fraudulent tax filings,and several critical information systems modernizationprojects that are plagued with problems.

Overall, legislative and agency actions in response to ourrecommendations have resulted in progress towardresolving many high-risk problems. In five areas, such asthe Pension Benefit Guaranty Corporation, improvementhas been significant enough for us to remove theirhigh-risk designation. In only three areas, Defenseweapons systems acquisition and inventory managementand the Internal Revenue Service’s collection ofdelinquent receivables, has there been little progress.

In addition to efforts to address individual high-risk areas,the Congress has moved to address critical problems on abroader basis by passing the 1993 GovernmentPerformance and Results Act and, in 1994, expanding theChief Financial Officers Act. These pieces of landmarklegislation establish the framework to better manage andmeasure results of federal operations.

In addition to this Overview, the series includes a QuickReference Guide (GAO/HR-95-2), which provides informationon the 18 high-risk areas we have tracked over the pastfew years. For each area, the Guide summarizes theproblems, root causes, progress, and outlook for thefuture; identifies a key GAO contact person; and provides alist of related GAO products. The series also includesseparate reports for 10 areas, detailing continuingsignificant problems and resolution actions needed.

Copies of this report series are being sent to thePresident and the Republican and Democratic leadershipof the Congress, committee chairs and ranking minority

GAO/HR-95-1 OverviewPage 2

members, all other members of the Congress, theDirector of the Office of Management and Budget, andthe heads of major departments and agencies.

Charles A. BowsherComptroller Generalof the United States

GAO/HR-95-1 OverviewPage 3

Contents

ExecutiveSummary

6

Calling Attentionto High-RiskAreas

20

The High-RiskProgramSuccesses

25

GAO’s High-RiskFocus

37

Implementing theLegislativeFramework forManagementReform

76

Key Contacts forNewly DesignatedHigh-Risk Areas

87

1995 High-RiskSeries

89

GAO/HR-95-1 OverviewPage 4

GAO/HR-95-1 OverviewPage 5

Executive Summary

Many critical government operations arehighly vulnerable to waste, fraud, abuse, andmismanagement. The government isneedlessly losing billions of dollars andmissing huge opportunities to achieve itsobjectives at less cost and with betterservice delivery. These vulnerabilitiesexpose the government to future losses.Mitigating these losses is especiallyimportant at a time when the governmentfaces large budget deficits. This report seriesupdates our efforts to address high-riskproblems and identifies further actionsneeded.

At the heart of high-risk situations is a lackof fundamental accountability, which has ledto hundreds of management weaknessesthroughout government, many persisting foryears. These weaknesses have fostered anenvironment with inefficient processes thatdo not provide reliable information and thaturgently need to be streamlined andimproved. Moreover, almost all of thegovernment’s major departments andagencies have not been able to pass the testof an independent financial statement audit.This situation justifiably reinforces thepublic’s low level of confidence in how thegovernment manages their tax dollars.

GAO/HR-95-1 OverviewPage 6

Executive Summary

This is not to say that no progress has beenmade. In fact, in 15 of the 18 high-risk areas,congressional and agency efforts haveprompted long-needed improvements. Insome areas, progress has been sufficient forus to remove the high-risk designation.

This report highlights:

• six broad current high-risk categories thatwill be the focus of our program over thenext 2 years;

• progress achieved in most of the high-riskareas we have emphasized since ourprogram’s inception in 1990; and

• recent legislation establishing the frameworkneeded to better manage and measureresults of federal operations.

Current HighRisks

Our focus over the next 2 years will be on sixbroad categories. Collectively, thesehigh-risk areas affect almost all of thegovernment’s $1.25 trillion revenuecollection efforts and hundreds of billions ofdollars of federal expenditures.

GAO/HR-95-1 OverviewPage 7

Executive Summary

Providing forAccountability andCost-EffectiveManagement ofDefense Programs

While our military capabilities areunparalleled in the world today, Defensecannot accurately account for its more than$250 billion annual budget and over $1trillion in assets worldwide. It also has beenunable to adequately fix well-known areas ofmajor vulnerability. These include

GAO/HR-95-1 OverviewPage 8

Executive Summary

• holding inventory, valued by Defense at$36 billion, that is no longer needed forcurrent operating requirements;

• disbursing $25 billion to vendors that cannotbe matched to supporting documentation todetermine if payments were proper;

• relying on contractors to voluntarily returnhundreds of millions of dollars inoverpayments; and

• paying billions of dollars in added costswhen acquiring weapons systems.

These poor practices are draining resourcesthat could be used to further enhancemilitary readiness. At the heart of theseproblems is a long-standing culture that hasnot valued good financial management. Nomilitary service or major Defensecomponent has been able to obtain afinancial audit opinion because of hundredsof billions of dollars in assets not accountedfor and countless failures in performing themost rudimentary bookkeeping tasks. TheSecretary of Defense said it well: “We needto reform our financial management. It is amess, and it is costing us money wedesperately need.”

Effective implementation of the landmarkChief Financial Officers Act throughout theDepartment of Defense is critical. We have

GAO/HR-95-1 OverviewPage 9

Executive Summary

made numerous recommendations tostrengthen Defense accountability andmanagement. While Defense hasacknowledged the severity of its financialmanagement problems and established goalsto correct them, it still lacks the realisticplans and expertise needed to accomplishthose goals. These issues are discussed inmore detail on pages 38 to 44.

Ensuring AllRevenues AreCollected andAccounted for

Although responsible for collecting98 percent of the government’srevenues—currently $1.25 trillionannually—the Internal Revenue Service (IRS)has not kept its own books and records withthe same degree of accuracy it expects oftaxpayers. For the last 2 years, we have beenunable to express an opinion on IRS’ financialstatements due to serious accounting andinternal control problems.

In response to our audit reports, IRS hasexpressed its commitment to developmeaningful and reliable financial informationand establish sound internal controls.However, IRS’ financial managementweaknesses are pervasive, have beenrepeatedly reported, and warrant promptattention. IRS’ financial systems are out ofdate, produce unreliable data on tax

GAO/HR-95-1 OverviewPage 10

Executive Summary

receivables, and do not adequately controlunauthorized access to taxpayerinformation. IRS’ financial operations fail toperform some of the most basic accountingpractices—reconciling collection deposits,assessing the collectibility of receivables,and ensuring that all transactions have beenproperly recorded to taxpayer accounts.

IRS is losing ground in collecting mountingtax receivables. Poor information systemsare a major barrier to making decisions.Also, IRS has had difficulty in coping withrapidly increasing filing fraud. Fraudulentpaper and electronic filings have flourishedand, unless brought under control, heavylosses will continue—tens of millions ofdollars annually. Problems related tocollecting and accounting for revenues arediscussed on pages 44 to 53.

Obtaining anAdequate Return onMultibillion DollarInvestments inInformationTechnology

Today’s information technology offersunprecedented opportunities to improve thedelivery of government services and reduceprogram costs. Using technology well iscentral to enhancing the informationavailable to federal managers and the public.Unfortunately, the government has not beenable to take full advantage of theseopportunities. The result is wasted

GAO/HR-95-1 OverviewPage 11

Executive Summary

resources, a frustrated public unable to getquality service, and a governmentill-prepared to measure results and manageits affairs in a businesslike manner.

Despite an estimated $200 billion investmentin the last 12 years, there is too littleevidence of promised capabilities beingdelivered on time and within budget. Forexample:

• The largest component of the FederalAviation Administration’s $36 billion airtraffic control modernization to improve airsafety has had to be dramatically revamped.

• IRS’ $8 billion Tax Systems Modernization,intended to overhaul the tax collectionprocess, has experienced continuing delaysand design difficulties.

• Defense’s Corporate InformationManagement initiative, estimated to savebillions of dollars by streamlining Defense’sbusiness operations in critical areas, hasfailed to meet program objectives.

• The National Weather Service effort toimprove its weather prediction systems hasexperienced cost growth for its radar andsatellite components and has lacked asystems architecture to guide thedevelopment and implementation of theseand other components.

GAO/HR-95-1 OverviewPage 12

Executive Summary

Problems in this area are discussed on pages54 to 59.

ControllingMedicare ClaimsFraud and Abuse

Medicare is undermined by flawed paymentpolicies, weak billing controls, andinconsistent program management.Instances of scams, abuses, and fraudabound in the $162 billion program. Insurershave owed Medicare millions of dollars formistaken payments. Moreover, to maximizeprofits, providers continue to exploitloopholes and billing control weaknesses.

Under current policy, the CongressionalBudget Office projects Medicare paymentswill reach $380 billion a year by 2003. TheHealth Care Financing Administration hasmoved to counteract the program’s abuses,but its overall management of theseactivities is not sufficient. Stronger controlsare essential to deter a drain on taxpayerfunds. See pages 60 to 63.

Minimizing LoanProgram Losses

The federal government provides thiscountry’s largest source of credit. Thegovernment managed direct loan portfoliosof $155 billion and had guaranteed loanstotaling $699 billion at the end of fiscal year

GAO/HR-95-1 OverviewPage 13

Executive Summary

1994. In fiscal year 1994 alone, lendingagencies wrote off about $2.8 billion ofdirect loans and terminated for default$16.4 billion of guaranteed loans. Futurecosts to the government of tens of billions ofdollars are anticipated.

This extraordinary exposure reinforces theneed to effectively manage credit programs.Oftentimes a lender of last resort, federalcredit programs will incur losses, but thesecosts can be reduced by overcomingmanagement control problems.

• Improvements have been made by theDepartment of Agriculture in the $18 billionfarm loan program, but the program incurredover $6 billion in losses from fiscal year 1991through fiscal year 1994 and still has nearly$5 billion on the books in outstanding loansto farmers who are behind on loanpayments. See pages 64 to 65.

• Between fiscal years 1991 and 1994, annualguaranteed student loan losses declinedfrom $3.6 billion to $2.4 billion, due in part toimprovements initiated by the EducationDepartment. However, problems with schooleligibility and the accuracy and availabilityof loan data could threaten the futuredelivery of Education’s student financial aid.See pages 66 to 67.

GAO/HR-95-1 OverviewPage 14

Executive Summary

• The Department of Housing and UrbanDevelopment (HUD), which insures some$400 billion in housing loans, guaranteesmore than $400 billion in outstandingsecurities, and spends $25 billion a year onhousing programs, is currently the subject ofnumerous “reinvention” proposals; however,the agency must address fundamentalinternal control, management, staffing, andsystems problems regardless of whatchanges are made. See pages 68 to 69.

ImprovingManagement ofFederal Contracts atCivilian Agencies

Civilian agencies rely on contractors toprovide goods and services costing tens ofbillions of dollars a year. It is critical toensure that the government gets what it paysfor and that contractors’ work is done atreasonable cost. But this has not alwaysbeen the case.

• The Department of Energy has allowed itsmanagement and operating contractorsextensive latitude in spending $15 billionannually, and it has not required contractorsto have financial audits despite continuingdisclosures of abuse and poor management.As a result, the government is not adequatelyprotected. See pages 70 to 72.

• Ineffective oversight by the NationalAeronautics and Space Administration

GAO/HR-95-1 OverviewPage 15

Executive Summary

(NASA), which spends about $13 billion a yearunder contract, has resulted in cost growthand schedule slippage in completing largespace projects. See pages 72 to 73.

• Contract management problems in theEnvironmental Protection Agency’s (EPA)multibillion dollar Superfund hazardouswaste cleanup program have providedcontractors too little incentive to controlcosts. See pages 74 to 75.

High-Risk ProgramSuccesses

In 15 of 18 high-risk areas we have followed,there has been progress in attacking rootcauses of problems. In 5 areas, enoughprogress has been made to remove theirhigh-risk designation, although we willcontinue to monitor their status.

GAO/HR-95-1 OverviewPage 16

Executive Summary

Progress in each of the 18 areas is discussedin the accompanying Quick Reference Guide(GAO/HR-95-2).

GAO/HR-95-1 OverviewPage 17

Executive Summary

Importance ofRecent LegislativeFramework forManagement Reform

While specific actions have been identifiedto fix individual high-risk areas, broader,more fundamental problems in governmentalso need to be addressed. Calls for civilservice reform, government reorganization,privatization, and devolution of functionsand programs to states and localgovernments are all areas worth exploring.Such changes may lessen the government’svulnerability, and we are working with theCongress on these and other broad reforms.

It is important to move toward a smaller,more efficient government that focuses onaccountability and managing for results. Tosuccessfully achieve these goals, accurateand reliable cost information andperformance data are absolutely essential.The Government Performance and ResultsAct (GPRA) and the Chief Financial Officers(CFO) Act help provide the critical impetusfor generating such managementinformation.

GPRA establishes pilot projects to defineexpected results up front and then measuretheir attainment. This is intended to movedecisionmakers from a focus on inputs andspending to one on outcomes and results.The CFO Act, as expanded by the 1994Government Management Reform Act,

GAO/HR-95-1 OverviewPage 18

Executive Summary

establishes a financial management leader ineach major department, requires annualaudited financial statements for all majordepartments and agencies for fiscal year1996, and mandates the development of costinformation and the modernization offinancial systems.

Effectively implementing such landmarklegislation should go a long way towardsolving high-risk problems and restoringcitizens’ confidence in government. It isessential that agencies adhere to thestatutory deadline for having auditedfinancial statements and that basicaccountability objectives are met. As part ofour continuing evaluation of high-risk areas,we will work with the Congress and theExecutive Branch to promote effectiveimplementation of the CFO Act and GPRA.

These issues are discussed in more detail onpages 76 to 86.

GAO/HR-95-1 OverviewPage 19

Calling Attention to High-Risk Areas

Over 12 years ago, in the face of seeminglyendless accounts of control breakdowns andprogram failures, the Congress passed theFederal Managers’ Financial Integrity Act of1982. The act required federal managers toevaluate their internal control andaccounting systems and to correct problems.

Since 1983, heads of the 18 largest federalagencies have identified well over 3,000weaknesses and reported progress inresolving them. Yet, our audits have shownthat similar problems surface over and over,and that the condition of controls andaccounting systems remains very poor.

In November 1989, we reported1 that fraud,waste, abuse, and mismanagementcontinued to cost the taxpayers billions ofdollars, rendered programs ineffective, andpainted a picture of federal agencies unableto manage their operations or fully accountfor their assets. It was during this time thatthe American public learned of a scandal atHUD, where serious deficiencies had goneunabated for many years.

1Financial Integrity Act: Inadequate Controls Result in IneffectiveFederal Programs and Billions in Losses (GAO/AFMD-90-10,Nov. 28, 1989).

GAO/HR-95-1 OverviewPage 20

Calling Attention to High-Risk Areas

In 1990, we established our high-riskprogram, placing special attention on 14areas considered to be especially vulnerable.

GAO/HR-95-1 OverviewPage 21

Calling Attention to High-Risk Areas

GAO/HR-95-1 OverviewPage 22

Calling Attention to High-Risk Areas

Since 1990, we have added four areas.

In December 1992, we issued a series ofreports on the designated areas. We reportedthat some agencies were openly recognizinghigh-risk problems and developing andimplementing corrective actions. We alsoreported that legislation needed to addresscertain individual high-risk areas had beenpassed, some agencies had developed soundplans for correcting problems, and a numberof financial management improvements hadbeen achieved.

GAO/HR-95-1 OverviewPage 23

Calling Attention to High-Risk Areas

Despite these advances, major problemspersisted and the danger of billions ofdollars in losses remained. Since the 1992series was issued, we have continued todevote substantial audit effort to high-riskareas to press for further improvements.

Since 1989, the Office of Management andBudget (OMB) also has had a high-riskprogram, which today encompasses 57areas. As reported in the President’s fiscalyear 1996 budget submission, OMB has alsofound that the concentrated attentionresulting from such an effort has helpedspark a number of important improvements.In our most recent review of OMB’s high-riskprogram,2 we agreed in most cases withOMB’s evaluation of the progress made byagencies to address identified problems.

2OMB’s High-Risk Program: Comments on the Status Reported inthe President’s Fiscal Year 1995 Budget (GAO/AIMD-94-136, Sept.20, 1994).

GAO/HR-95-1 OverviewPage 24

The High-Risk Program Successes

After 5 years, the high-risk programcontinues to demonstrate its value inprompting long-needed improvements.Significant efforts by agencies, coupled withlegislation and congressional oversight, haveaddressed many identified deficiencies.Congressional hearings have beenparticularly important in defining solutionsand bringing about changes. For some areas,we are removing the high-risk designation.Others are on the right path to resolution,while only three areas have shown littleimprovement.

Five Areas ShowSignificant Progress

In five areas, legislative and agency actionsin response to our recommendations haveresulted in improvements significant enoughfor us to remove their high-risk designation.

GAO/HR-95-1 OverviewPage 25

The High-Risk Program Successes

We will, however, continue to closelymonitor these areas. If significant problemsagain arise, we will consider returning thearea to the high-risk program. Additionalinformation on each of these areas isprovided in the Quick Reference Guide(GAO/HR-95-2).

We put the Bank Insurance Fund on ourhigh-risk list because unprecedentednumbers of bank failures and insurancelosses in the late 1980s and early 1990s haddepleted the Fund’s reserves. These failures

GAO/HR-95-1 OverviewPage 26

The High-Risk Program Successes

resulted from the banking industry’s shift toincreasingly risky lending activities inresponse to a shrinking customer base andincreased competition. Banks’ lending riskswere exacerbated by weak internal controls,flawed corporate governance systems, andlax regulatory supervision. By year-end 1991the Fund was in a deficit position.

In various reports and testimonies, werecommended that the Congress rebuild theFund and put safeguards in place to improveregulation and minimize future losses to theFund. These safeguards includedmanagement and auditor reporting on theeffectiveness of internal controls,independent audit committees, safety andsoundness standards, prompt correctiveactions to minimize Fund losses, andaccounting reforms to ensure reliablefinancial reports.

The Congress responded by passing severalpieces of legislation. The OmnibusReconciliation Act of 1990 removed caps onpremium increases and gave the FederalDeposit Insurance Corporation (FDIC)increased flexibility to set premium rates.The FDIC Improvement Act of 1991 providedfor rebuilding the depleted deposit insurancefund and required significant corporate

GAO/HR-95-1 OverviewPage 27

The High-Risk Program Successes

governance, regulatory, and accountingreforms. These reforms, which have largelybeen implemented by FDIC and others,address the serious weaknesses thatcontributed to earlier record bank failures.

The rapid rebuilding of the Fund’s reserves,which stood at $17.5 billion at June 30, 1994,has substantially reduced the Fund’s risks.We are currently performing the 1994financial audit of the Fund and will beissuing our report in March 1995.

The Resolution Trust Corporation (RTC)was created in August 1989 to resolvehundreds of failed savings and loaninstitutions and dispose of their assets.Although original estimates indicated thatRTC would need $50 billion to close knownfailed thrifts, cost estimates escalatedrapidly. By May 1990, the number of knownfailed thrifts had increased and RTC’s mostconservative cost estimates had grown tonearly $90 billion. In addition, RTC facedsignificant risks associated with contractingout the management and disposition of failedthrift assets worth hundreds of billions ofdollars. As a result, RTC was part of ourhigh-risk program almost from theCorporation’s inception.

GAO/HR-95-1 OverviewPage 28

The High-Risk Program Successes

We made numerous recommendations inreports and testimonies over the years aimedat reducing the total thrift cleanup costs. Wecalled for providing RTC with adequate andtimely funding for failed thrift closures andfor management reforms designed toimprove RTC’s asset disposition, contracting,and financial management activities. We alsopointed to the need for RTC to better estimatethe value of failed thrift assets so that theCongress would have the best possibleinformation on which to base its fundingdecisions.

In response, the Congress passed severallaws that provided RTC with additionalfunding, mandated that RTC implementspecific management reforms, and requiredthe establishment of an interagencytransition task force with specificresponsibilities to facilitate the transfer ofRTC’s workload, personnel, and operations toFDIC by January 1996. For its part, RTC madenumerous improvements in its estimatingprocesses, internal controls, and financialmanagement systems in order to providemore reliable, auditable cost data. As aresult, we have been able to attest to theaccuracy of RTC’s balance sheet beginning in1991 and its financial statements since thattime. RTC has also fully implemented most of

GAO/HR-95-1 OverviewPage 29

The High-Risk Program Successes

the congressionally mandated reforms andcontinues to work on the others. Finally, RTC

and FDIC have established a task force thathas begun to work on transition issues.

Although the transition remains an area ofconcern, RTC no longer poses the risk it oncedid. As of November 1994, RTC hadcompleted the resolution of 743 failed thrifts;disposed of $432 billion of the $463 billion inassets from those failed thrifts; and madenotable improvements in its disposition,contracting, and management activities. Weare currently performing the 1994 financialaudit of RTC and will report the results inmid-1995.

In December 1992, we reported that thePension Benefit Guaranty Corporation’s

(PBGC) weak financial condition threatenedthe program’s viability. In 1993, managementdeficiencies hindered PBGC’s ability toeffectively assess and monitor its financialcondition. Its single-employer fund had a$2.9 billion deficit, and it faced $71 billion inunderfunding in the ongoing plans it insured.

To reduce these threats, we recommended acombination of legislative actions andstrengthened oversight and enforcementefforts. In particular, we supported

GAO/HR-95-1 OverviewPage 30

The High-Risk Program Successes

legislation to strengthen funding standardsand make the variable rate premium morerisk related. We also recommended that PBGC

correct significant system and controlweaknesses in its liability estimation andpremium and accounting operations.

PBGC substantially improved its internalcontrols for estimating its liability for futurebenefits, enabling us for the first time toexpress an opinion on its 1992 balance sheet.Also on December 8, 1994, the Congresspassed the General Agreement on Tariffs andTrade (GATT) which contains provisions tostrengthen minimum funding standards andphase out the cap on variable rate premiumspaid by underfunded defined benefit pensionplans. We reported that most companieswith underfunded pension plans will putmore money into their plans. The agencyestimates that these provisions will lowerthe underfunding in plans it insures andreduce the deficit in its single-employerfund.

Congressional and agency actions shouldreduce PBGC’s exposure to losses and,correspondingly, the risk to the federalgovernment. We are currently working onthe 1994 financial audit and will issue ourreport in March 1995.

GAO/HR-95-1 OverviewPage 31

The High-Risk Program Successes

We put the State Department’s

management of overseas real property

on our high-risk list because of insufficientmaintenance of facilities, lax oversight ofoverseas post operations, inadequateinformation systems, and poor planning.These problems had resulted in deterioratedfacilities, increased costs, and questionablemanagerial decisionmaking.

In response, State’s actions includedestablishing priorities for constructionprojects based on specific criteria, betterevaluating contractors’ performance, hiringadditional qualified staff, surveying themaintenance conditions of posts,streamlining and updating housingstandards, and improving informationsystems. Related State initiatives underwayinclude:

• conducting global maintenance surveys atover 170 overseas posts and establishing 2regional maintenance assistance centers;

• implementing a facilities evaluation andassistance program;

• implementing an information resourcemanagement system and upgrading the realestate management system; and

• conducting financial audits at a number ofoverseas posts.

GAO/HR-95-1 OverviewPage 32

The High-Risk Program Successes

These initiatives significantly reduce theoverseas property management program’svulnerabilities.

The Federal Transit Administration’s

(FTA) grant management was on ourhigh-risk list because, until 1993, FTA focusedmore on awarding grants than on ensuringtheir proper use. Oversight was superficialand inconsistent, and FTA seldom used itsenforcement powers to compel grantrecipients to fix problems, even those thatwere long-standing.

We made numerous recommendations thatfocused on, among other things, ensuringthat grant recipients have adequatemanagement systems, strengthening reviewsof recipients, and linking awards of grantfunds to compliance with rules. In particular,we recommended that FTA withhold fundsfrom grantees that did not completecorrective actions or were not in compliancewith existing grant requirements.

Over the past few years, FTA has madesubstantial improvements in its process tooversee its $4.6 billion grants program,including organizational changes, increasedoversight staff levels, and better training. FTA

GAO/HR-95-1 OverviewPage 33

The High-Risk Program Successes

has made a concerted effort to change theattitudes of its oversight staff and granteestowards safeguarding federal funds. FTA hasgone from relying primarily on granteecertifications of compliance to implementingvarious initiatives and systems that, overtime, should instill a more proactiveapproach to its grant management,oversight, and enforcement responsibilities.Most importantly, FTA has recently used itsmost powerful enforcementtool—withholding funds—to sanctiongrantees found to be mismanaging theirprograms.

FTA is in the process of implementing itsimprovement plan, but we believe that asthese initiatives are carried out, the riskassociated with the FTA grant program willcontinue to decrease.

Remaining ProgramsShow Mixed Results

For the remaining 13 high-risk areas,1

agencies have made varying degrees ofprogress in designing corrective action plansand are in different stages of implementingthose plans. For 10 areas, we have seen agenuine commitment to improve.

1The titles of some of these high-risk areas have been changedslightly to reflect the current focus of coverage.

GAO/HR-95-1 OverviewPage 34

The High-Risk Program Successes

GAO/HR-95-1 OverviewPage 35

The High-Risk Program Successes

In the remaining three areas, agencies havemade little progress.

The high-risk program clearly has had avaluable impact and we will continue tofocus on all 13 of these areas in the future.The following section, which discusses ourfuture plans for the high-risk program,highlights problems remaining in the 13areas and introduces newly identified areas.

GAO/HR-95-1 OverviewPage 36

GAO’s High-Risk Focus

These 6 categories encompass the 13 areasbeing carried over and 7 newly added areas.All involve billions of dollars of taxpayers’money and will require a concerted effort toreduce significant risks.

GAO/HR-95-1 OverviewPage 37

GAO’s High-Risk Focus

Providing forAccountability andCost-EffectiveManagement ofDefense Programs

Defense is accountable for more than $1trillion in assets and, in fiscal year 1994,spent $272 billion—approximately50 percent of the government’s discretionaryspending in fiscal year 1994. However, manyof Defense’s management systems andpractices are inadequate for safeguarding itsassets or achieving its missions in the mostcost-effective manner.

Recently, concerns have been raised aboutthe current state of combat readiness. Whilethe link to accountability has not often beendrawn, funds lost through waste, fraud,abuse, and mismanagement are unavailablefor training and equipment repairs. Defensehas initiated actions to address most of itsmanagement problems, but the problems areall still far from being resolved. Defense’shigh-risk management problems fall in fourareas:

GAO/HR-95-1 OverviewPage 38

GAO’s High-Risk Focus

FinancialManagement

Defense’s financial management systems,practices, and procedures continue to behampered by significant weaknesses.1 Thissituation is the worst in government and isthe product of many years of neglect.According to former Secretary of DefenseLes Aspin:

“Accounting, business-type efficiency, andindirect support functions were secondaryconsiderations of top DOD leaders...The[DOD] financial management communityadapted to shortcomings and lacked a senseof urgency for correcting them.”

In presenting the fiscal year 1995 budget,Secretary of Defense William Perry said:

1Financial Management: Financial Control and System WeaknessesContinue to Waste DOD Resources and Undermine Operations(GAO/T-AIMD/NSIAD-94-154, Apr. 12, 1994).

GAO/HR-95-1 OverviewPage 39

GAO’s High-Risk Focus

“[O]ur financial management...is a mess, andit is costing us money we desperately need.”

Following are just a few examples ofDefense’s financial management problems.

• While over $400 billion in adjustments weremade to correct errors in Defense reportedfinancial data for fiscal years 1991 through1993, the resulting statements were still notreliable.

• Vendors were paid $25 billion that cannot bematched to supporting documentation todetermine if payments were proper.2

• An estimated $3 million in fraudulentpayments were made to a former Navysupply officer for over 100 false invoiceclaims, and approximately $8 million inArmy payroll payments were made tounauthorized persons, including 6 “ghost”soldiers and 76 deserters.3

While Defense has acknowledged theseverity of its financial managementproblems and established goals for theircorrection, it still lacks realistic plans andthe necessary expertise. A key contact forthis area is identified on page 87.

2Financial Management: Status of Defense Efforts to CorrectDisbursement Problems (GAO/AIMD-95-7, Oct. 5, 1994)

3GAO/T-AIMD/NSIAD-94-154.

GAO/HR-95-1 OverviewPage 40

GAO’s High-Risk Focus

ContractManagement

Despite reduced levels of reported defectivecontract pricing, long-standing contractorcost estimating problems continue, andother contract management problems haveemerged. As a result, significant risksremain.

• Serious control weaknesses continue toresult in numerous and large erroneous, andin some cases fraudulent, payments todefense contractors. During one 6-monthperiod in fiscal year 1993, contractorsreturned to the government $751 million, andin fiscal year 1994, they returned$957 million, most of which appears to havebeen overpayments detected by thecontractors.

• Contractors’ systems for charging costs tothe government continue to result incontractors’ billing for, and Defense payingfor, large unallowable amounts. From fiscalyears 1991 to 1993, Defense auditorsquestioned about $3 billion in contractoroverhead charges.

The recent emphasis on acquisition reform,including passage of the Federal AcquisitionStreamlining Act of 1994, is a positive steptoward strengthening the acquisition system.However, Defense must sustain efforts toensure the integrity and fairness of its

GAO/HR-95-1 OverviewPage 41

GAO’s High-Risk Focus

contracting and procurement processes.This must include eliminating sizable andnumerous overpayments to its contractorsand aggressively dealing with contractors toensure that long-standing deficiencies incost-estimating systems are corrected.

More information on these contractingissues is provided in Defense Contract

Management (GAO/HR-95-3).

Weapons SystemsAcquisition

Defense is committed to reforming its majorweapons acquisition process (involvingabout $80 billion a year) and has begun toreassess many of its most expensive weaponprograms for opportunities to cutback tomeet anticipated shortfalls in funding.Defense has also initiated reforms to addressweapons systems acquisition issues since theinception of our high-risk program.However, pervasive problems, including(1) unreliable cost data, (2) unrealisticschedule estimates, (3) unaffordableprogram plans, and (4) contracting forweapon systems before needed technologyis available, continue to add billions ofdollars to acquisition costs.

Both Defense and the Congress haveinitiated actions that attempt to address

GAO/HR-95-1 OverviewPage 42

GAO’s High-Risk Focus

these serious problems. Defense hasimplemented a number of long-standingrecommendations and has adopted anacquisition strategy that calls for provingtechnologies before incorporating them intothe procurement process. In October 1994,the Congress legislated changes in theacquisition process and has also directed areevaluation of the military services’ rolesand missions and the most cost-effective mixof weapons.

However, it is too early to assess theeffectiveness of these acquisition reformefforts. Defense must quickly provide theregulations needed for implementing therecently enacted acquisition reform law.Successful reform will also requirecontinuing strong congressional support.

As part of this high-risk series, we areissuing a separate report on Defense

Weapons Systems Acquisition problemsand additional needed improvements(GAO/HR-95-4).

InventoryManagement

Defense’s inventory management practicescontinue to result in billions of dollars inunneeded stock. Even after Defensedisposed of unneeded inventory costing

GAO/HR-95-1 OverviewPage 43

GAO’s High-Risk Focus

$43 billion4 over the last 3 years, it still holdsitems valued at $36 billion (or 47 percent ofits total current inventory) that are notneeded for current operating requirementsor war reserves. While Defense has donesome testing of new procedures in a fewareas, such as prime vendor delivery ofmedical supplies, overall it has made littleprogress. Defense must aggressively work tochange its inventory management culture sothat it can achieve higher levels of readinessin the future using fewer dollars. In addition,congressional oversight will be necessary tomaintain Defense’s focus on these problems.

A separate report on Defense Inventory

Management provides more information onthis problem and additional neededimprovements (GAO/HR-95-5).

Ensuring AllRevenues AreCollected andAccounted for

Fair and equitable administration of tax lawsdemands that the government collect what itis owed. Yet, with annual collectionscurrently at $1.25 trillion, IRS and Customs,the government’s principal revenuecollectors, continue to be unable toadequately account for and collect all that isdue the government. The result is the

4We estimate that this inventory had a value of $914 million.

GAO/HR-95-1 OverviewPage 44

GAO’s High-Risk Focus

potential loss of billions of dollars inrevenue.

High-risk revenue collection problems fall infour areas.

IRS FinancialManagement

IRS’ significant financial managementweaknesses cause errors in taxpayeraccounts and an inability to adequatelyaccount for collectionoperations—bookkeeping problems IRS

would not accept from taxpayers. IRS’systems are antiquated and were notdesigned to provide the meaningful andreliable financial information needed toeffectively manage and report on IRS’operations.

GAO/HR-95-1 OverviewPage 45

GAO’s High-Risk Focus

Our financial audits have highlighted a widerange of problems with the quality of IRS’revenue information, internal controls overbillions of dollars of assets, andunauthorized access to taxpayerinformation.5 Although efforts are under wayto address recommendations from our 1992financial audits, as of May 1994, IRS hadcompleted action on only 4 of the 44recommendations we made.

In our audit of IRS’ fiscal year 1993 financialstatements, we found

• unreliable data on its estimated $71 billion ofvalid accounts receivable (having anestimated collectable amount of $29 billion),which adversely impacted IRS’ collectionability;

• over $90 billion of transactions that had notbeen posted to taxpayer accounts; and

• the inability to identify the amount of exciseand social security taxes collected, resultingin billions of dollars of subsidies to recipienttrust funds.

IRS’ serious, long-standing, and pervasivefinancial management problems hamper the

5Financial Audit: Examination of IRS’ Fiscal Year 1992 FinancialStatements (GAO/AIMD-93-2, June 30, 1993) and Financial Audit:Examination of IRS’ Fiscal Year 1993 Financial Statements(GAO/AIMD-94-120, June 15, 1994).

GAO/HR-95-1 OverviewPage 46

GAO’s High-Risk Focus

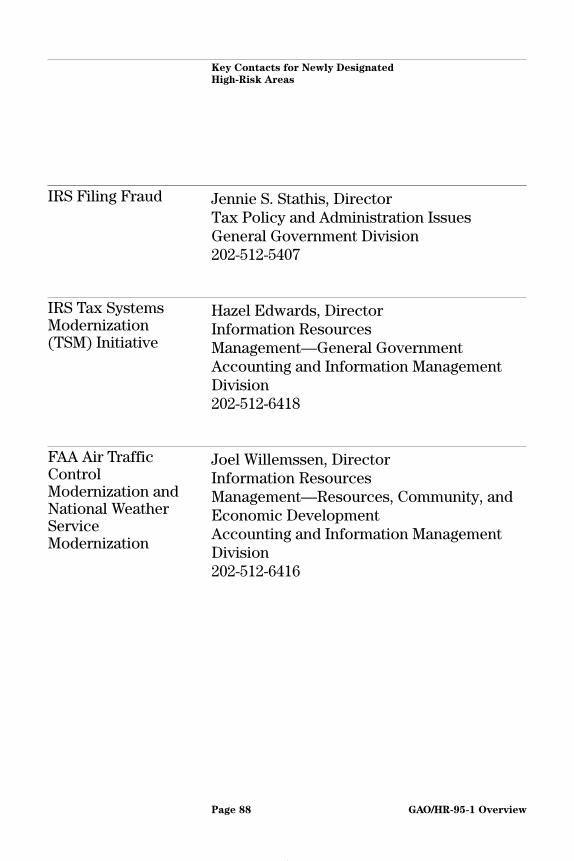

effective collection of revenues and precludethe preparation of auditable financialstatements. Without adequate, reliableinformation about noncompliant anddelinquent taxpayers, IRS cannot measure theeffectiveness of its enforcement andcollection programs. A key contact for thisarea is identified on page 87.

IRS Receivables Meanwhile, tax receivables continue togrow. In some respects, the problem ofcollecting IRS receivables is worse today thanit was 5 years ago when we designated thisas a high-risk area.

Between 1990 and 1994, the reportedinventory of tax debt increased from$87 billion to $156 billion. Coupled with thisgrowth is another troubling fact. By 1994,annual collections of delinquent taxes haddeclined from $25.5 billion to $23.5 billion.

IRS’ tax receivable collection is hampered byinaccuracies in records needed forstrategically planning and making decisionson collection cases and by a lack ofinformation to determine the optimum sizeand mix of staff for collection. Otherimpediments include a lengthy, antiquated,and rigid collection process and

GAO/HR-95-1 OverviewPage 47

GAO’s High-Risk Focus

decentralized lines of responsibility andaccountability. It is also difficult to balancecollection efforts with the need to protecttaxpayer rights.

Additional information on problems with IRS

Receivables is contained in a separatereport being issued as part of this high-riskseries (GAO/HR-95-6).

Filing Fraud Another high-risk area for IRS is filing fraud.In the past several years, detected filingfraud for both paper and electronic filingprograms has doubled or tripled annually asshown below in figure 1.6

6IRS Automation: Controlling Electronic Filing Fraud and ImproperAccess to Taxpayer Data (GAO/T-AIMD/GGD-94-182, July 19, 1994).

GAO/HR-95-1 OverviewPage 48

GAO’s High-Risk Focus

Figure 1: FradulentReturns Detected

During the first 6 months of 1994, IRS

identified about 34,700 fraudulent paperreturns and 24,000 fraudulent electronicreturns—increases of 151 percent and52 percent, respectively, over the sameperiod a year earlier. Thus, the upward trendcontinues.

GAO/HR-95-1 OverviewPage 49

GAO’s High-Risk Focus

Based on detected schemes alone, IRS hasacknowledged the government loses tens ofmillions of dollars to refund schemesannually. A key contact for this area isidentified on page 88.

Customs ServiceFinancialManagement and theAsset ForfeitureProgram

With responsibility for about $20 billion inrevenues, Customs is an important collectorfor the government. However, our 1992high-risk report pointed to majorweaknesses in Customs’ management andorganizational structure that diminished theagency’s ability to detect trade violations onimported cargo; collect applicable duties,taxes, fees, and penalties; control financialresources; and report on financialoperations.

Since that report, Customs has taken severalactions to address these problems, includingrevising its planning process, improvingcontrols over identification and collection ofrevenues owed, aggressively pursuingdelinquent receivables, and embarking on anagencywide reorganization plan. Althoughthese improvement efforts will requiresustained management attention, they areproperly focused and should reduceCustoms’ risks in the general managementarena. Therefore, we are narrowing the

GAO/HR-95-1 OverviewPage 50

GAO’s High-Risk Focus

scope of our high-risk work at Customs tofocus on its financial management problems.More information on Managing the

Customs Service can be found in the QuickReference Guide (GAO/HR-95-2).

Despite other improvements, Customs stillneeds to make significant additional effortsto correct its financial management andinternal control systems weaknesses. Ouraudits of Customs’ financial statements forfiscal years 1992 and 1993 disclosed that theagency had not yet fully resolved many ofthe financial management problems that wereported earlier.7 Although efforts areunderway to address recommendations fromour fiscal year 1992 financial statementsaudit, as of May 1994, Customs hadcompleted actions on only 11 of the 54recommendations we made. Our financialaudit for fiscal year 1993 found that Customshad not implemented controls, systems andprocesses to reasonably ensure that

• carriers, importers, and their agentscomplied with trade laws. As a result,revenue owed to the federal governmentmay not have been identified and quotas and

7Financial Audit: Examination of Customs’ Fiscal Year 1992Financial Statements (GAO/AIMD-93-3, June 30, 1993) andFinancial Audit: Examination of Customs’ Fiscal Year 1993Financial Statements (GAO/AIMD-94-119, June 15, 1994).

GAO/HR-95-1 OverviewPage 51

GAO’s High-Risk Focus

other legal restrictions may have beenviolated. Moreover, important trade statisticsmay not be reliable.

• sensitive data maintained in its automatedsystems, such as import inspection criteriaand law enforcement data, were adequatelyprotected from unauthorized access andmodification.

• full accountability for its assets and the useof its appropriated funds were provided, orthe costs of its programs and computermodernization efforts were reliablydetermined.

Customs also needs to address problems inits asset forfeiture program. We put bothCustoms’ and the Justice Department’s assetforfeiture programs on our original high-risklist because the programs—with inventoriesvalued at almost $2 billion in 1994—focusedmore on taking property away fromcriminals and less on managing propertytaken. Both agencies have since initiatedmanagement and systems changes toimprove program operations. However, ouraudits of Customs’ fiscal years 1993 and 1992financial statements have also revealedserious weaknesses in key internal controland systems that affected Customs’ ability tocontrol, manage, and report the results of itsseizure efforts, including accountability and

GAO/HR-95-1 OverviewPage 52

GAO’s High-Risk Focus

stewardship over property seized. As aresult, tons of illegal drugs and millions ofdollars in cash and other property have beenvulnerable to theft and misappropriation.For instance, in our fiscal year 1993 audit,we found that

• seized asset inventory records containedinformation on drugs that had beentransferred to other agencies as early as 2years before and did not show thousands ofpounds of drugs that Customs was stillholding; and

• physical security was weak at 20 of the 21facilities we visited. Over the past severalyears, drugs and property have occasionallybeen stolen from Customs storage facilities.For example, in fiscal year 1993, thievesbroke into a Customs facility and stole 356pounds of cocaine.

Customs is taking action to address theinternal control and systems problems;however, these efforts are in various stagesof development.

Additional information on Asset Forfeiture

Programs can be found in a separate reportissued as part of this series (GAO/HR-95-7).

GAO/HR-95-1 OverviewPage 53

GAO’s High-Risk Focus

Obtaining anAdequate Return onMultibillion DollarInvestments inInformationTechnology

Huge, complex, and expensive computermodernizations are under way across thefederal government to replace oldergeneration automated informationprocessing. Many of these long-term,multibillion dollar efforts are intended toharness information technology’s power toprovide agencies better capability toproduce higher quality services tailored tothe public’s changing needs and deliveredmore effectively, faster, and at lower cost.

Yet, after spending more than $200 billion oninformation management systems during thelast 12 years, project after project continuesto lag behind schedule, consistently fails toprovide intended mission benefits, andexceeds estimated costs by hundreds ofmillions of dollars.

Successful automation projects are moreoften the exception than the rule. As a result,critical financial, program, and managementinformation systems remain largelyincompatible, costly to operate andmaintain, and woefully inadequate inmeeting current users’ needs.

To reduce costs, increase service, and raiseproductivity, information systems projectsshould not simply automate existing

GAO/HR-95-1 OverviewPage 54

GAO’s High-Risk Focus

inefficient or ineffective processes. Rather,functional processes should first besimplified, redirected, and reengineered.Information technology, however, is oftenprocured as the fix to outdated, inefficientprocedures before new work processes andorganizational structures have beenadequately designed or decided on.

We are adding to our high-risk list fourmultibillion dollar information technologyinitiatives because they experienced pastfailure, involve complex technology, or arecritical to agencies’ missions. Key contactsfor these initiatives are identified on page 87and 88.

GAO/HR-95-1 OverviewPage 55

GAO’s High-Risk Focus

Air Traffic ControlModernization

The air traffic control (ATC) modernizationproject covers all parts of the $36 billionFederal Aviation Administration (FAA) effortto overhaul the nation’s air traffic controlsystem and includes the remainders of theAdvanced Automation System, componentsof which were canceled, replaced, and/orrestructured. That system failed because FAA

did not recognize the technical complexity ofthe effort, realistically estimate theresources required, adequately oversee itscontractors’ activities, or effectively controlsystem requirements.8

8Advanced Automation System: Implications of Problems andRecent Changes (GAO/T-RCED-94-188, Apr. 13, 1994).

GAO/HR-95-1 OverviewPage 56

GAO’s High-Risk Focus

IRS’ Tax SystemsModernization

Through fiscal year 1995, IRS will have spentor obligated over $2.5 billion on its $8 billionTax Systems Modernization (TSM) initiativeto automate selected tax processingfunctions. Yet, the overall design for TSM isstill incomplete and IRS is continuing toautomate existing problem-plaguedfunctions with limited understanding ofwhether or how different systems willeventually connect to improve taxprocessing overall.9 Given budget constraintsand the risks involved, the Congress reducedIRS’ fiscal year 1995 budget request by$339 million, and IRS has agreed to establishthe needed business and technicalfoundation to achieve TSM’s goals andobjectives.

Defense’s CorporateInformationManagementInitiative

The Corporate Information Management(CIM) initiative was estimated by Defense tosave billions by streamlining DefenseDepartment operations and managingresources more effectively; however, resultsto date have been mixed. Defense has largelybeen consumed with trying to pick the bestof its hundreds of existing automatedsystems and standardizing their use across

9Tax Systems Modernization: Status of Planning and TechnicalFoundation (GAO/T-AIMD-GGD-94-104, Mar. 2, 1994).

GAO/HR-95-1 OverviewPage 57

GAO’s High-Risk Focus

military components.10 As a result, Defenseis spending some $3 billion annually todevelop and modernize automatedinformation systems, while major Defensebusiness processes supported by thesesystems—such as personnel, payroll,inventory management, supply distribution,and contract administration—have not beenexamined for process reengineeringopportunities.

National WeatherServiceModernization

Although the National Weather Service’sprogram to modernize its weather observing,information processing, andcommunications systems was originallyexpected to be completed in 1994, it is nowestimated to not be completed until at least1999. Also, the system that is to be thecenterpiece of the modernization hasrecently experienced design problems and isbeing restructured. Additionally, the manysystems comprising the modernization havelong proceeded without the benefit of anoverall architecture to guide their design,development, and evolution. This hasnegatively affected the modernization’s cost

10Defense Management: Stronger Support Needed for CorporateInformation Management Initiative to Succeed(GAO/AIMD/NSIAD-94-101, April 1994); Defense ADP: CorporateInformation Management Must Overcome Major Problems(GAO/IMTEC-92-17, September 1992).

GAO/HR-95-1 OverviewPage 58

GAO’s High-Risk Focus

and performance by requiring additionalresources to acquire, interconnect, andmaintain hardware and software.11

In addition to focusing on these fourhigh-risk initiatives, we are working with(1) the Congress to amend the PaperworkReduction Act to provide a leadershipstructure for, and strengthen themanagement of, the government’sinformation technology resources and(2) the Executive Branch on new guidancedesigned to bring into the governmentstrategic information management “bestpractices” that successful organizations,public and private, have used to improvemission performance.12 These are importantsteps toward ensuring that the federalgovernment obtains an adequate return onits information technology investments.13

11Weather Forecasting: Systems Architecture Needed for NationalWeather Service Modernization (GAO/AIMD-94-28, Mar. 11, 1994).

12Executive Guide: Improving Mission Performance ThroughStrategic Information Management and Technology(GAO/AIMD-94-115, May 1994).

13Government Reform: Using Reengineering and Technology toImprove Government Performance (GAO/T-OCG-95-2, Feb. 2,1995) and Paperwork Reduction Act: Reauthorization CanStrengthen Government’s Management of Information andTechnology (GAO/T-AIMD/GGD-95-80, Feb. 7, 1995).

GAO/HR-95-1 OverviewPage 59

GAO’s High-Risk Focus

ControllingMedicare ClaimsFraud and Abuse

Medicare is one of the fastest growingprograms in the federal budget. In fiscal year1994 the government spent over $440 milliona day, or about $162 billion, on Medicare.CBO estimates that, under current policy,Medicare spending will reach about$380 billion a year by 2003. The portion ofMedicare spending attributable to waste,fraud, and abuse is difficult to quantify;however, health care experts have estimatedthat 10 percent of national health spending islost to these practices. Even a lesserpercentage, if applied to the $162 billionMedicare program, is a devastating amountand becomes even more devastating as theprogram grows.

The Health Care Financing Administration(HCFA) has made a number of regulatory andadministrative changes aimed at correctingflawed payment policies, weak billingcontrols, and deficient programmanagement. For example, in 1993, HCFA

raised the standards for contractorperformance regarding analyses of paymentdata to identify excessive spending. In 1994,the agency awarded a contract fordeveloping a national automated claimsprocessing system intended to replace themany systems currently operating. Throughthese efforts, using modern data analysis

GAO/HR-95-1 OverviewPage 60

GAO’s High-Risk Focus

techniques and greater uniformity in claimsprocessing, HCFA expects to reduceMedicare’s inappropriate payments.However, these improvements, whileworthwhile, are not sufficient to protectMedicare against continued program losses.

Although HCFA is aware that health carescams and abusive billing practices plagueMedicare, the exploitation continues. HCFA’scontrols against fraud and abuse have notkept pace with health care’s morecomplicated financial arrangements.Moreover, the broad discretion given toHCFA’s claims processing contractors hasresulted in uneven implementation of fraudand abuse controls. This problem has beencompounded by HCFA’s contractormanagement which, while improving,remains relatively weak.

As a result, HCFA does not have theinformation necessary to ensure thatcontractors are adequately protectingMedicare payments from providerexploitation or fraud. For example, HCFA

cannot explain why some contractors paymany more claims for certain proceduresthan do other contractors because HCFA doesnot know what criteria its contractors use toidentify claims ineligible for payment. In

GAO/HR-95-1 OverviewPage 61

GAO’s High-Risk Focus

addition, HCFA makes little use ofmanagement reports submitted bycontractors that describe their claims reviewactivities. For example, HCFA did not probe acontractor report that showed a 53 percentdrop (amounting to nearly $27 million) in theamount of savings achieved through claimsreview.

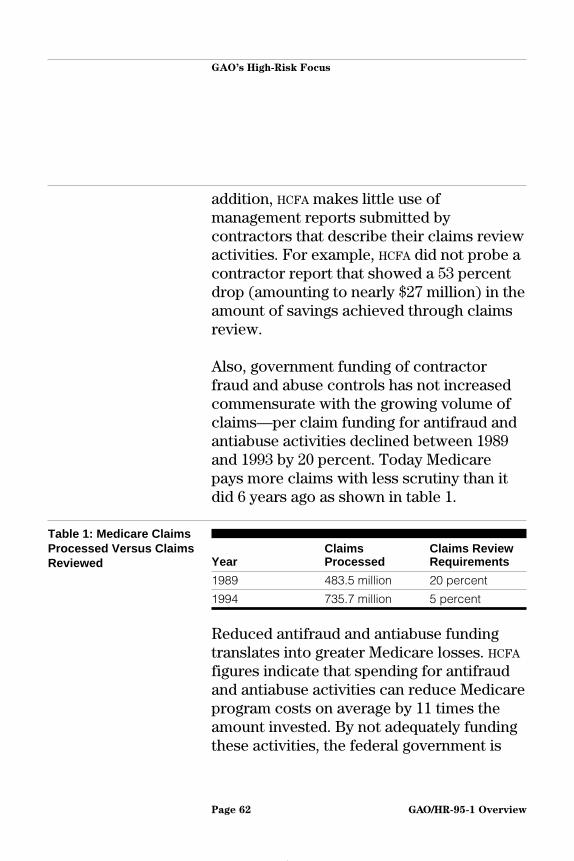

Also, government funding of contractorfraud and abuse controls has not increasedcommensurate with the growing volume ofclaims—per claim funding for antifraud andantiabuse activities declined between 1989and 1993 by 20 percent. Today Medicarepays more claims with less scrutiny than itdid 6 years ago as shown in table 1.

Table 1: Medicare ClaimsProcessed Versus ClaimsReviewed Year

ClaimsProcessed

Claims ReviewRequirements

1989 483.5 million 20 percent

1994 735.7 million 5 percent

Reduced antifraud and antiabuse fundingtranslates into greater Medicare losses. HCFA

figures indicate that spending for antifraudand antiabuse activities can reduce Medicareprogram costs on average by 11 times theamount invested. By not adequately fundingthese activities, the federal government is

GAO/HR-95-1 OverviewPage 62

GAO’s High-Risk Focus

missing a significant opportunity to controlMedicare program costs.

Medicare Claims high-risk issues arediscussed in more detail in a separate reportissued as part of this series (GAO/HR-95-8).

Minimizing LoanProgram Losses

The federal government continues to be thenation’s largest source of credit. In fiscal1994, the government reported that itobligated almost $23 billion in new directloans and guaranteed $204 billion in newnon-federal lending. As of September 30,1994, OMB estimated non-tax receivables,primarily direct loans and loans acquired asa result of claims paid on defaultedguaranteed loans, to be $241 billion. Of thatamount, $50 billion was delinquent. Thefollowing three loan programs present highrisks of losses.

GAO/HR-95-1 OverviewPage 63

GAO’s High-Risk Focus

Farm Loan Programs Farm loan programs have evolved into acontinuous source of credit for manyborrowers and have had a high rate of loandefaults, which resulted in the loss of over$6 billion of taxpayers’ money from fiscalyears 1991 through 1994.14 Although FarmersHome Administration (FmHA) has taken stepsto correct some problems, little progress hasbeen made in correcting other basicproblems with farm loan programs.

On the positive side, field office lendingofficials have been provided with extensivetraining in credit and financial analysis toimprove the quality of new loans beingmade. FmHA’s reviews show that most new

14Within the U.S. Department of Agriculture, farm loans have beenhistorically administered by FmHA. In October 1994, theresponsibility was transferred to the newly created ConsolidatedFarm Service Agency. Because of the general familiarity with theagency’s earlier name, we refer to FmHA in this report.

GAO/HR-95-1 OverviewPage 64

GAO’s High-Risk Focus

direct and guaranteed loans now meetlending standards. Also, compliance withstandards for servicing guaranteed loans hasrecently improved.

However, field officials still do not alwaysfollow established procedures for servicingoutstanding direct loans. In addition, neitherAgriculture nor the Congress have addressedproblems involving loan and propertymanagement policies; therefore, the agency,for example, continues to make loans toborrowers who either are delinquent or didnot repay their previous debts, and reduceand forgive the debts of borrowers who donot repay their loans.

Even though FmHA forgave about $6 billion inunpaid loans from fiscal year 1991 throughfiscal year 1994, its outstanding loanportfolio still contains nearly $5 billion indelinquent debt. We believe that FmHA needsfirm guidance from the Congress on theacceptable level of loan losses and the lengthof time borrowers may receive farm loanassistance.

A separate report on Farm Loan Programs

issued as part of this high-risk series offersadditional information on FmHA’simprovement efforts (GAO/HR-95-9).

GAO/HR-95-1 OverviewPage 65

GAO’s High-Risk Focus

Student FinancialAid Programs

Education’s loan programs have generallysucceeded in providing eligible studentsaccess to money for postsecondaryeducation. However, largely due tostructural problems, the programs have beencostly—$2.4 billion in losses in theguaranteed student loan program alone infiscal year 1994.

Education is taking action to address someof the guaranteed loan program’sweaknesses, including transferring some ofthe program’s risks and financial costs tolenders and guaranty agencies. As requiredby law, Education is also phasing down theguaranteed loan program and replacing itwith a new direct loan program.

Despite improvement efforts, many ofEducation’s problems with the guaranteedloan program continue. For example, we andthe Education Inspector General could notattest to the accuracy of the guaranteed loanprogram’s fiscal year 1992 or 1993 financialstatements because of unreliable loan data.15

Some of Education’s problems with theguaranteed loan program could also affect

15Financial Audit: Federal Family Education Loan Program’sFinancial Statements for Fiscal Years 1993 and 1992(GAO/AIMD-94-131, June 30, 1994).

GAO/HR-95-1 OverviewPage 66

GAO’s High-Risk Focus

the direct loan and other student financialaid programs. For example, Education’s loandata continue to be unreliable. Suchinformation is needed to determine ifineligible students received additionalfinancial aid or if the maximum allowableborrowing amount has been exceeded.Without this data, new financial assistance inthe form of guaranteed loans, direct loans, orgrants could be given to ineligible students.In addition, Education’s problems withpreventing unscrupulous schools fromparticipating in the guaranteed loan programcould surface in the new direct loan programas it is rapidly phased in—Education plansto go from just over 100 to about 1,400participating schools in a single year.Without a viable strategy to guide theDepartment during this period of rapidgrowth, Education has put the new directloan program at risk of not achieving itsobjectives efficiently and effectively.

Additional information on Education’simprovement actions and its new direct loanprogram is given in a separate report onStudent Financial Aid issued as part ofthis series (GAO/HR-95-10).

GAO/HR-95-1 OverviewPage 67

GAO’s High-Risk Focus

Department ofHousing and UrbanDevelopment

Effectively managing HUD, which insuressome $400 billion in housing loans,guarantees more than $400 billion inoutstanding securities, and spends$25 billion a year on housing programs, hasbeen hampered by four long-standingproblems: (1) weak internal controls, (2) anineffective organizational structure, (3) aninsufficient mix of staff with the properskills, and (4) inadequate information andfinancial management systems. Some ofthese problems were major factors leadingto incidents of fraud, waste, abuse, andmismanagement reported in the late 1980s.

Important HUD initiatives to address theselongstanding problems are either still in theplanning stage or in the process of beingimplemented. It is much too early to assesstheir effectiveness.

Recently, HUD’s Secretary announced aproposal to “reinvent” the agency over thenext 4 years by consolidating its housingassistance and community developmentprograms into three performance-basedblock grant funds, transforming publichousing to make it more competitive, andchanging the Federal HousingAdministration into an entrepreneurialgovernment-owned corporation. If

GAO/HR-95-1 OverviewPage 68

GAO’s High-Risk Focus

implemented, this proposal would shift manyprogram design and implementationresponsibilities to states and localities andwould change HUD’s primary role into that ofoverseer and information clearing house.

It is difficult to predict the impact of suchsweeping changes on the corrective actionsand plans that HUD already has under way.However, no matter what form HUD

eventually takes, its fundamentalweaknesses must be addressed. The currentdiscussion on how best to “reinvent” HUD

presents the agency, OMB, and the Congresswith an excellent opportunity to worktogether to eliminate internal control,management, staffing, and systemsproblems.

Additional information on the Department

of Housing and Urban Development

improvement efforts can be found in aseparate report being issued as part of thisreport series (GAO/HR-95-11).

ImprovingManagement ofFederal Contracts atCivilian Agencies

Civilian agencies spend tens of billions ofdollars per year on contracts and havebecome increasingly dependent oncontractors to help manage and carry outagency missions. However, once contracts

GAO/HR-95-1 OverviewPage 69

GAO’s High-Risk Focus

are awarded, federal agencies do not alwayseffectively control contractors’ costs andperformance. At the core of contractmanagement problems, we have found a lackof senior-level management attention toagencies’ contracting activities. Our high-riskefforts will focus on three areas.

Department ofEnergy

Energy spends about $15 billion annuallythrough management and operatingcontracts. But its use of cost-reimbursementcontracts, allowance of excessive contractorlatitude, and inadequate oversight ofcontractor activities and costs have failed toprotect the government from fraud, waste,abuse, and mismanagement. Energy did notrequire its contractors to prepare auditablefinancial statements, and the net

GAO/HR-95-1 OverviewPage 70

GAO’s High-Risk Focus

expenditures reports that contractors didprepare were not being audited every 5 yearsas required. Contractors were not able toprovide consistent and reliable detailed costinformation so that Energy managers couldevaluate whether costs were reasonable andcontractors were operating programseffectively. In addition, Energy’s managersand staff have not received the data neededto determine the nature and extent ofenvironmental contamination or to setpriorities and monitor the progress ofclean-up efforts.

In 1993, Energy began a comprehensivereform initiative. While Energy is still in theprocess of developing specificimplementation plans, actions planned todate include using alternatives tocost-reimbursement contracts, increasingcompetition for contracts, strengtheningfinancial information systems, andimproving management and control ofcertain costs. Policy changes can beimplemented almost immediately, butchanges in regulations and procedures willtake much longer. We are concerned,however, that staff training and informationsystems improvements are not scheduled totake place until most of the other contractreform initiatives have been implemented.

GAO/HR-95-1 OverviewPage 71

GAO’s High-Risk Focus

Energy’s practice of introducing policies andreforms before staff are fully trained andsystems fully developed has contributed toprevious contract reform failures.

Energy has plans to include contractoroperations in its agencywide financialstatement audits; however, we doubtEnergy’s ability to accomplish such auditswithin the near future. Although Energypublished its strategic plan for informationmanagement in July 1994, some actions willnot be completed before fiscal year 1997.

Additional information on Department of

Energy Contract Management problemsand improvement initiatives can be found inthe Quick Reference Guide (GAO/HR-95-2).

NASA Despite recent improvement initiatives, NASA

continues to struggle with the managementof its contracts, valued at between$12 billion and $13 billion and representingabout 90 percent of its funding.

Traditionally, NASA’s contract managementefforts have been hampered by

• procurements based on unrealistic fundingexpectations—its 1993 five-year budget

GAO/HR-95-1 OverviewPage 72

GAO’s High-Risk Focus

request totaled $90 billion, $20 billion morethan was likely to be appropriated;

• the lack of adequate systems andinformation with which to monitorcontractor activities; and

• field centers not adhering to contractmanagement requirements.

Compounding NASA’s inability to adequatelyoversee contractors has been its practice ofassuming virtually all risk related to contractcost and results. This practice hascontributed directly to frequent fundingincreases, schedule delays, and performanceproblems on many of NASA’s large spaceprojects.

NASA has been addressing its problems, but itis not yet clear whether its efforts will beeffective. Also, additional efforts are needed.For example, NASA’s new CFO must fill thefinancial leadership role and actively worktowards the goals laid out in the CFO Act.Further, NASA needs to aggressively use itsnew authority to penalize contractorsclaiming reimbursement of unallowablecosts.

Additional information on NASA Contract

Management can be found in the QuickReference Guide (GAO/HR-95-2).

GAO/HR-95-1 OverviewPage 73

GAO’s High-Risk Focus

Superfund Since the Environmental ProtectionAgency’s (EPA) Superfund program began in1980, thousands of waste sites have beendiscovered, and their cleanup has proven farmore complicated and costly thananticipated. Recent estimates indicate thatcleaning up the thousands of hazardouswaste sites—many of which are owned bythe federal government—could result in over$300 billion in federal costs and manybillions more in private expenditures.

Superfund relies heavily on contractors toperform cleanup work, but its extensive useof cost-reimbursable contracts givecontractors little incentive to control costs.A recent review of three contractors showedthat all three billed the government forentertainment, tickets for sporting events, oralcoholic beverage costs that either were notpermitted or appeared questionable underapplicable regulations. Furthermore, EPA’sproblems are compounded by backlogs ofrequests by procurement officials for auditsto verify the accuracy of contractors’charges.

After years of giving insufficient attention tocorrecting known contract managementproblems, EPA management has begunfocusing greater attention on better

GAO/HR-95-1 OverviewPage 74

GAO’s High-Risk Focus

controlling costs and other problems.However, little progress has been made inreducing the risk from insufficient oruntimely audits. As of August 1994, therewere 528 unfulfilled requests for audits ofEPA contractor costs.

Additional information on EPA’s Superfund

Program Management improvementinitiatives and remaining problems isprovided in a separate report issued as partof this high-risk series (GAO/HR-95-12).

GAO/HR-95-1 OverviewPage 75

Implementing the LegislativeFramework for Management Reform

A critical factor in resolving specifichigh-risk areas is addressing broader, morefundamental government managementproblems. A major breakthrough since theestablishment of our high-risk program is thepassage of legislation—the GovernmentPerformance and Results Act (GPRA) and theChief Financial Officers (CFO) Act—thatprovide the structure necessary to helpachieve improved government accountabilityand stewardship and to lower costs byfocusing on results.

The Congress framed it this way: Set goals,operate programs, and measure results usingreliable financial and managementinformation. Effectively implementing thisframework will require agencies to redirectthe focus of management, substantiallyimprove financial systems, and measureresults.

Managing for Results GPRA seeks to fundamentally change thefocus of federal management andaccountability from a preoccupation withinputs, such as program appropriations, toresults and outcomes of federal programs.With successful implementation, this changecan help address the question: What are the

GAO/HR-95-1 OverviewPage 76

Implementing the Legislative

Framework for Management Reform

American people getting for their investmentin the federal government?

The experiences of state governments andforeign countries that are leaders in publicmanagement show that GPRA’s three keyelements—strategic planning, performancemeasurement, and public reporting andaccountability—could influence the basicculture of government so that it is moreresults-oriented.1 The Congress intendsthrough GPRA to improve performance byproviding managers freedom to experimentand find innovative ways to improveprogram results, while increasing theiraccountability for achieving those results.

GPRA requires an agency to do the following.

• Develop a 5-year strategic plan for itsprogram activities by 1997, laying out theorganization’s fundamental mission andlong-term goals and objectives foraccomplishing that mission. To be updatedevery 3 years, this plan is to serve as thestarting point and basic underpinning of theagency’s goal-setting and performancemeasurement process.

1See, for example, Managing for Results: State Experiences ProvideInsights for Federal Management Reforms (GAO/GGD-95-22,Dec. 21, 1994).

GAO/HR-95-1 OverviewPage 77

Implementing the Legislative

Framework for Management Reform

• Submit, beginning in 1999, annual programperformance plans to OMB and subsequentprogram performance reports to thePresident and the Congress. OMB is todevelop an overall federal governmentperformance plan that is to be submittedannually to the Congress with the President’sbudget.

GPRA implementation began withperformance planning and reporting pilots atselected agencies. Already, more than 70programs and agencies have been designatedas pilots, ranging in size from smallprograms to entire agencies, including IRS,the Social Security Administration, and theDefense Logistics Agency.

GPRA’s vision of making major changes in theway federal agencies are managed and heldaccountable will require agencies to developthe capacity to manage for results. Currently,the lack of complete and reliable financialand other management informationprecludes many agencies from effectivelymeasuring performance. Strong financialmanagement systems and the aggressive useof information technology are preconditionsfor the success of GPRA.

GAO/HR-95-1 OverviewPage 78

Implementing the Legislative

Framework for Management Reform

This legislation requires us to report to theCongress on the implementation of the act,including the prospects that all federalagencies—even those not designated to dopilot projects—will comply with the act.Working with the Congress, we havedesigned a strategy for evaluating the pilots’implementation of results-orientedmanagement that will identify the lessonslearned from implementing GPRA as theyhappen.

Improving FinancialSystems and Reports

Reliable financial information is key tobetter managing government programs,providing accountability, and addressinghigh-risk problems. However, as highlightedearlier in our discussions of a number of riskareas, the government’s financial systemsare all too often unable to perform the mostrudimentary bookkeeping for organizations,many of which are oftentimes larger thanmany of the nation’s largest privatecorporations.

Further, the government’s financial systemsare fast aging. About 30 percent of themwere installed more than 5 years ago, andanother 34 percent have already passed the10-year mark. Agencies’ antiquated financialsystems simply do not adequately meet

GAO/HR-95-1 OverviewPage 79

Implementing the Legislative

Framework for Management Reform

critical requirements for comparable dataand users’ reporting needs. Also, OMB hasreported that only one-half of agencies’financial management systems meet existingagency automated data processing technicalstandards, and a mere 2 percent comply withagencies’ own targeted or plannedtechnology standards.

Today’s financial systems have no shortageof paper output but provide agencymanagers and the Congress little meaningfulfinancial information. Greatly improvedfinancial reporting is essential and wouldinclude

• financial information that is linked withprogram and budget data for use in bothmanagement control and planning,

• reports on program cost trends and otherperformance indicators from whichmanagers can make informed decisions onrunning government operations effectivelyand efficiently, and

• financial data that is consistent andcompatible and meets standard datarequirements so consolidated financialreports will be useful.

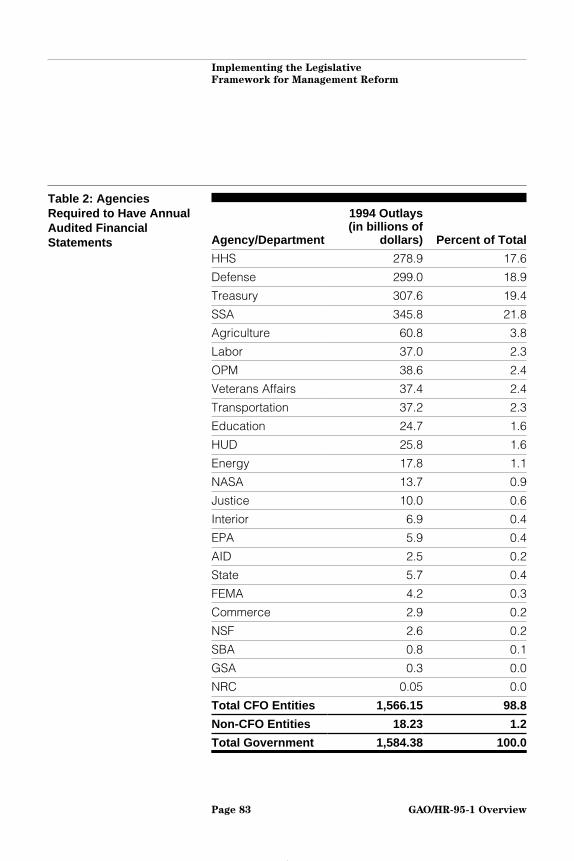

Before 1990, this information was notrequired and the reliability of financial

GAO/HR-95-1 OverviewPage 80

Implementing the Legislative

Framework for Management Reform

information for only a minor part of thegovernment’s $1.5 trillion annual spendingwas independently checked. With passage ofthe CFO Act in 1990, the Congress paved theway for the federal government to have thesame kind of financial statement reporting asrequired in the private sector and by stateand local governments.