gabelli & company’s 2017 pump, valve & water systems symposium · gabelli &...

TRANSCRIPT

1 1

Gabelli & Company’s 2017 Pump, Valve & Water

Systems Symposium

EnPro Industries, Inc.

Presented by Milt Childress, CFO & SVP March 1, 2017

2 2

Forward-Looking Statements

Statements in presentation that express a belief, expectation or intention, as well as those that are not historical fact, are forward-looking statements under the Private Securities Litigation Reform Act of 1995. They involve a number of risks and uncertainties that may cause actual events and results to differ materially from such forward-looking statements. These risks and uncertainties include, but are not limited to: general economic conditions in the markets served by our businesses, some of which are cyclical and experience periodic downturns; the effect of changes in currency exchange rates, expected volumes of purchases of parts denominated in euros used for engines to be sold in U.S. dollars; prices and availability of raw materials; and the amount of any payments required to satisfy contingent liabilities related to discontinued operations of our predecessors, including liabilities for certain products, environmental matters, employee benefit obligations and other matters. In addition, adverse developments could arise in regard to voluntary petitions filed by certain of our subsidiaries in U.S. Bankruptcy Court to establish a trust that would resolve all current and future asbestos claims. Our filings with the Securities and Exchange Commission, including the Form 10-K for the year ended December 31, 2016, describe these and other risks and uncertainties in more detail. We do not undertake to update any forward-looking statement made in this presentation to reflect any change in management's expectations or any change in the assumptions or circumstances on which such statements are based. We own a number of direct and indirect subsidiaries and, from time to time, we may refer collectively to EnPro and one or more of our subsidiaries as “we” or to the businesses, assets, debts or affairs of EnPro or a subsidiary as “ours.” These and similar references are for convenience only and should not be construed to change the fact that EnPro and each subsidiary is an independent entity with separate management, operations, obligations and affairs. This presentation also contains certain non-GAAP financial measures as defined by the Securities Exchange Commission. A reconciliation of these measures to the most directly comparable GAAP equivalents is included as an appendix to this presentation. We will also be referencing certain pro forma unaudited condensed consolidated financials. Please refer to our earnings releases for important information regarding how pro forma financial information is derived, as well as related risks and uncertainties.

3 3

EnPro Industries Snapshot

Pro Forma Sales(2)

Pro Forma Adjusted EBITDA & Margin(3)

$ in millions

$ in millions

$1,378 $1,338 $1,404 $1,371 $1,338

2012A 2013A 2014A 2015A 2016A

$225 $216 $208 $200 $186

16.3% 16.2% 14.8% 14.6% 13.9%

2012A 2013A 2014A 2015A 2016A

Key EnPro Highlights: • NYSE Stock Ticker: NPO • Market Cap: ~$1.4 billion • Shares Outstanding: ~21.4 million • Dividend: $0.88/share(1)

• Dividend Yield: ~1.4% • # of Employees: ~6,000 • History:

― Founded June 1, 2002 ― Spin-off from Goodrich Corp. ― Several brands >100 years old

EnPro Segments: • Reports in 3 Segments

― Sealing Products ― Engineered Products ― Power Systems

• Garlock Sealing Technologies (GST) ― Deconsolidated business ― Chapter 11 bankruptcy protection from asbestos-

related claims ― A profitable business

(1) Quarterly dividend increased to $0.22/share that will be payable starting in March 2017. (2) See appendix for reconciliations. (3) Represents pro forma adjusted EBITDA per reconciliations in appendix.

4 4

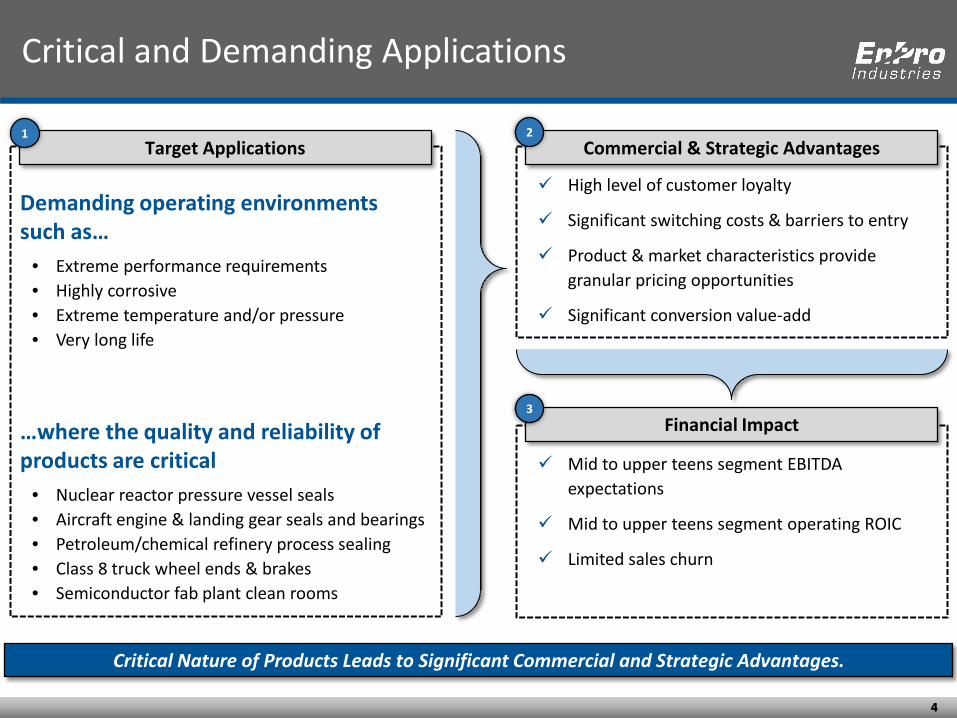

Critical and Demanding Applications

Critical Nature of Products Leads to Significant Commercial and Strategic Advantages.

Demanding operating environments such as…

• Extreme performance requirements • Highly corrosive • Extreme temperature and/or pressure • Very long life

…where the quality and reliability of products are critical

• Nuclear reactor pressure vessel seals • Aircraft engine & landing gear seals and bearings • Petroleum/chemical refinery process sealing • Class 8 truck wheel ends & brakes • Semiconductor fab plant clean rooms

Target Applications

High level of customer loyalty

Significant switching costs & barriers to entry

Product & market characteristics provide granular pricing opportunities

Significant conversion value-add

Commercial & Strategic Advantages

Mid to upper teens segment EBITDA expectations

Mid to upper teens segment operating ROIC

Limited sales churn

Financial Impact

1 2

3

5 5

Leading Brands Drive Recurring Business

Core Brands Select Supporting Brands Flagship Products

• Gylon • Klozure • Lubrikup

• Pikotek • PSI • Gar-Seal

• PTFE-based gasket material for high pressure, high temperature applications

• Pro-Torq • STEMCO Duroline

• STEMCO Kaiser • Aeris • Class 8 truck wheel-end seals, bearings and accessories

• Helicoflex • Cefil‘Air • Origraf

• Bio-Guardian • Feltmetal

• Spring energized seals, advanced polymer seals, abradable seals, and edge welded bellows seals

• DU • DX

• DP-4 • GAR-MAX

• Metal and polymer-backed, self-lubricating plain bearings

• Hi-Flo • Twin Ring • Valvealert • High flow valves, piston and rider rings, and monitoring

devices

• FM/Alco • FM OP Engines

• FM-MAN • Colt-Pielstick

• Medium-speed diesel engines for marine and stationary power applications

6 6

Highly Diversified Business Leads to Stable Cash Flows

58% 22%

7%

6% 5% 3%

United States

Europe

Asia Pacific

Canada Latin America

Other

(1) FCF defined as pro forma adjusted EBITDA less pro forma capital expenditures. (2) Refer to appendix for reconciliations.

Pro Forma Free Cash Flow(1)(2)

$ in millions

$177 $166

$147 $147 $134

2012A 2013A 2014A 2015A 2016A

Diversified Geographic and End Market Mix Leads to Stable Cash Flow Generation.

2016 Pro Forma Sales by Market

2016 Pro Forma Sales by Geography

24%

16%

13% 13%

10%

7%

6% 5%

3% 2% Medium/Heavy-Duty Truck

General Industrial

Navy & Marine

Chemical & Material Processing

Power Generation

Oil & Gas

Automotive

Semiconductor Aerospace

Avg. = $154

Other

7 7

Overview of EnPro

Sealing Products(1) Engineered Products(1) Power Systems(1)

Pro Forma Sales:

$211.1

Pro Forma Segment Adjusted

EBITDA:

$22.6

Pro Forma

Segment Adjusted EBITDA Margin:

10.7%

Pro Forma Sales:

$278.0

Pro Forma Segment Adjusted

EBITDA:

$37.5

Pro Forma

Segment Adjusted EBITDA Margin:

13.5%

Pro Forma Sales:

$852.3

Pro Forma Segment Adjusted

EBITDA:

$156.4

Pro Forma

Segment Adjusted EBITDA Margin:

18.4%

• Gaskets & Packing • Oil Seals • Pipeline Insulating

Products

• High Performance Metal Seals

• Brush Seals • Bellows • Turbine Hot Gas Path

Section Components • Polymer Products

• Wheel End • Suspension • Brake Products • Intelligent

Transportation Systems

• Plain Bearings • Bushing Blocks • Bearing

Assemblies

• Sealing Components, Valves, and Lubrication Systems for Reciprocating Compressors

• Medium-Speed Diesel Engines

• Parts & Service • Systems Packager

Products:

• General Industry • Oil & Gas • Basic Materials • Chemical Processing • Power Generation • Water

• Electronics & Semiconductors

• Aerospace • Power Generation • General Industry • Oil & Gas • Food & Beverage

• Class 8 Heavy Duty Truck

• Medium Duty Vocational Truck

• Auto • Construction &

Agriculture • Fluid Power • General Industry

• Oil & Gas • Compressors • Services • Chemical Processing • Other Industries

• Commercial • Government

Markets:

(1) Financial information based on pro forma 2016 results; pro forma sales and pro forma segment adjusted EBITDA reconciliations located in appendix.

$ in millions

8 8

Sealing Products

Pro Forma Sales & Pro Forma Segment Adjusted EBITDA Margin(1)

$ in millions

2016 Pro Forma Sales Mix As % of Pro Forma Sales

$801 $811 $844 $868 $852

21.7% 23.0% 20.1% 19.0% 18.4%

2012A 2013A 2014A 2015A 2016A

55%

45%

Aftermarket

62% 14%

8%

7% 6% 3%

Sales by Channel Sales by Geography

OEM

United States

Europe

Asia Pacific

Latin America

Canada Other

Secular Market Trends: • Aging global infrastructure of pipelines • Low oil and gas prices driving demand for

petro-chem • Stable durable goods shipments by trucking • Global growth of distributed power • Growth in global aerospace production

Organic Growth Strategies: • Leverage commercial synergies from

acquisitions • New product development

― Food & pharma sealing ― Aerospace applications and sub-systems ― Aeris mileage and safety systems

Inorganic Growth Strategies: • Increase size of addressable market • Gain scale in sanitary sealing markets • Grow presence in aerospace and industrial

turbine

(1) See appendix for pro forma sales and pro forma segment adjusted EBITDA reconciliations.

9 9

Engineered Products

$ in millions

2016 Pro Forma Sales Mix As % of Pro Forma Sales

33%

67%

Aftermarket

52%

28%

8%

4% 4% 4%

Sales by Channel Sales by Geography

OEM Europe

United States

Asia Pacific

Canada Latin America

Other

$365 $358 $360

$299 $278

13.4% 13.0% 14.3% 11.1%

13.5%

2012A 2013A 2014A 2015A 2016A

Secular Market Trends: • Industrial activity in Europe and North

America: slow growth • Automotive markets have been steady • Low oil and gas prices affecting demand for

compressor parts

Organic Growth Strategies: • Focus on core refinery and petro-chem

markets at CPI • Convert more of U.S. industrial market to

plain bearings • Leverage global manufacturing and service

presence

Strategic Focus: • Right size for demand levels • Improve operational performance • Tightly manage SG&A costs

Pro Forma Sales & Pro Forma Segment Adjusted EBITDA Margin(1)

(1) See appendix for pro forma sales and pro forma segment adjusted EBITDA reconciliations.

10 10

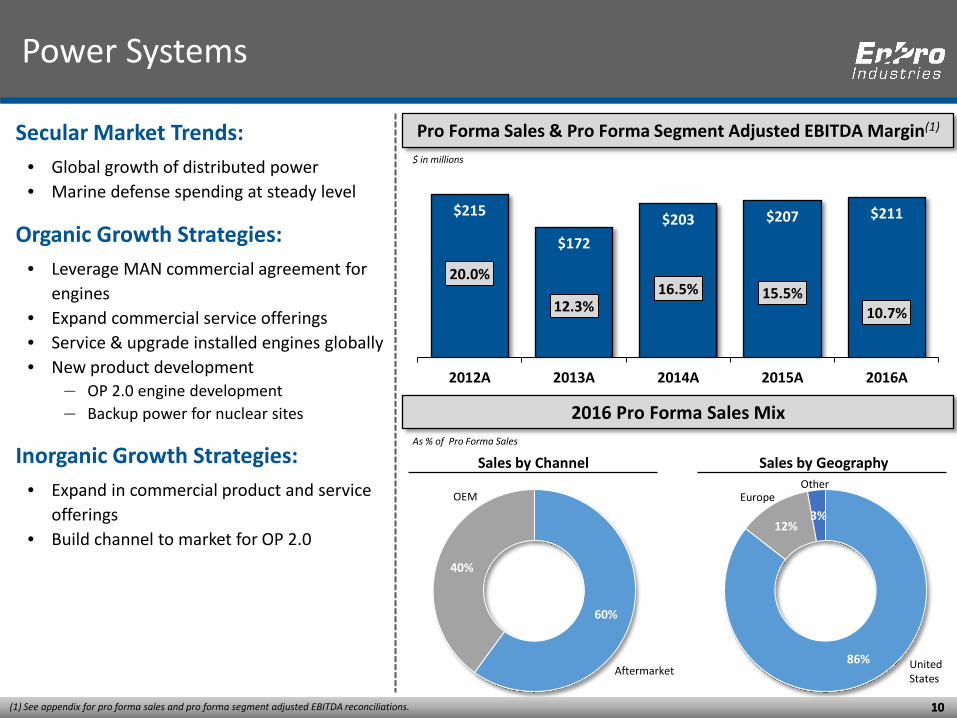

Power Systems

$ in millions

2016 Pro Forma Sales Mix As % of Pro Forma Sales

60%

40%

Aftermarket 86%

12% 3%

Sales by Channel Sales by Geography

OEM

United States

Europe Other

$215

$172 $203 $207 $211

20.0%

12.3% 16.5% 15.5%

10.7%

2012A 2013A 2014A 2015A 2016A

Secular Market Trends: • Global growth of distributed power • Marine defense spending at steady level

Organic Growth Strategies: • Leverage MAN commercial agreement for

engines • Expand commercial service offerings • Service & upgrade installed engines globally • New product development

― OP 2.0 engine development ― Backup power for nuclear sites

Inorganic Growth Strategies: • Expand in commercial product and service

offerings • Build channel to market for OP 2.0

Pro Forma Sales & Pro Forma Segment Adjusted EBITDA Margin(1)

(1) See appendix for pro forma sales and pro forma segment adjusted EBITDA reconciliations.

11 11

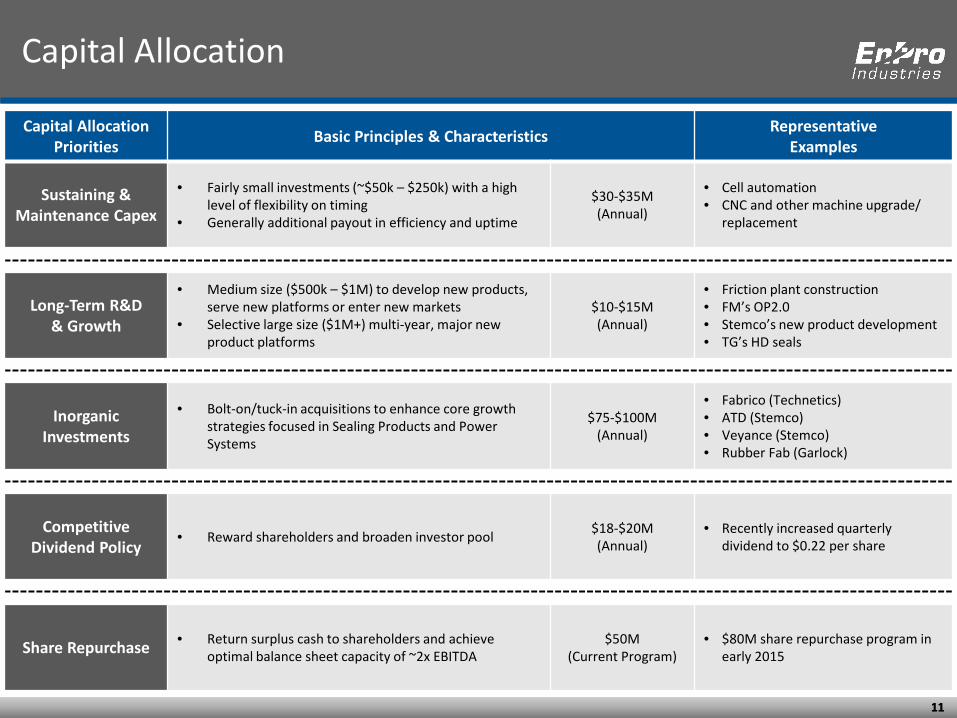

Capital Allocation

Capital Allocation Priorities Basic Principles & Characteristics Representative

Examples

Sustaining & Maintenance Capex

• Fairly small investments (~$50k – $250k) with a high level of flexibility on timing

• Generally additional payout in efficiency and uptime

$30-$35M (Annual)

• Cell automation • CNC and other machine upgrade/

replacement

Long-Term R&D & Growth

• Medium size ($500k – $1M) to develop new products, serve new platforms or enter new markets

• Selective large size ($1M+) multi-year, major new product platforms

$10-$15M (Annual)

• Friction plant construction • FM’s OP2.0 • Stemco’s new product development • TG’s HD seals

Inorganic Investments

• Bolt-on/tuck-in acquisitions to enhance core growth strategies focused in Sealing Products and Power Systems

$75-$100M (Annual)

• Fabrico (Technetics) • ATD (Stemco) • Veyance (Stemco) • Rubber Fab (Garlock)

Competitive Dividend Policy

• Reward shareholders and broaden investor pool $18-$20M (Annual)

• Recently increased quarterly dividend to $0.22 per share

Share Repurchase • Return surplus cash to shareholders and achieve optimal balance sheet capacity of ~2x EBITDA

$50M (Current Program)

• $80M share repurchase program in early 2015

12 12

Understanding the Asbestos Claims Resolution Process (ACRP)

ACRP Summary Background ACRP Settlement Agreement

GST sought protection from asbestos claims on June 5, 2010 via voluntary bankruptcy protection

• Fully operational wholly-owned subsidiary of EnPro • Deconsolidated from EnPro financial results

Court also enjoined affiliate asbestos claims • Preserved remaining common insurance for GST • Protects EnPro and other EnPro businesses during case

Liability estimate was volatile • Assumptions challenged by tort system abuses,

concealment of 524g trust claims on other companies • Insurance was diminishing

Presiding judge endorsed GST’s liability estimate on January 10, 2014

• Scientific evidence showed product did not contribute to asbestos-related diseases

• $125M versus claimants’ estimates of $970M - $1.26B for mesothelioma liability

• Sets path to permanent resolution of asbestos claims

Settlement Agreement reached March 17, 2016

Comprehensive settlement • Resolves claims against GST, its affiliates and Coltec;

protecting all of EnPro

Plan follows 524(g) safe harbor provision of asbestos bankruptcy law

• Proven path to resolution performed by previous asbestos bankruptcies

• Preserves equity in GST for Coltec • Significantly reduces appellate risk

GST and Coltec (EnPro’s sub) have the means to fund the Trust

• $400M cash contribution would be made upon consummation of the plan

• Additional $80M contribution would be made no later than the first anniversary of plan consummation

• Additional $20M cash payment for Canadian claims would be payable on the fourth anniversary of plan consummation

• Above amounts all deductible against taxable income

13 13

ACRP Path Toward Reconsolidation

Next Steps and Path toward Reconsolidation

We continue to progress on the ACRP timeline towards plan confirmation and reconsolidation.

# Activity 2016 2017

Status Q2 Q3 Q4 Q1 Q2 Q3 Q4

1 Parties file all plan documents including plan and disclosure statement. Complete

2 Court hears motion to approve disclosure statement & claimant solicitation process; issues approval. Complete

3 Solicitation begins for GST & Coltec claimants. Complete

4 4-month notice period ends. Votes are tabulated and certified within a month thereafter. Complete

5 Assuming successful vote, Coltec reorganization accomplished (operating businesses moved outside of Coltec corp. family; Coltec merges into newly formed “OldCo”. Complete

6 OldCo files the claimant-approved prepackaged chapter 11 & Bankruptcy Court agrees to jointly administer the cases. Complete

7 Bankruptcy Court holds confirmation hearing for all debtors (GST, Garrison & OldCo); issues positive confirmation decision shortly thereafter, assuming no objection. On-Track

8 District Court affirms BC decision; issues confirmation orders & 524(g) channeling injunction, directing all current and future claims to Trust, assuming no objection. On-Track

9 Confirmation orders become final 30 days later, assuming no appeal. On-Track

10 Plan of Reorganization is consummated & becomes effective; GST and OldCo reconsolidated into EnPro. On-Track

14 14

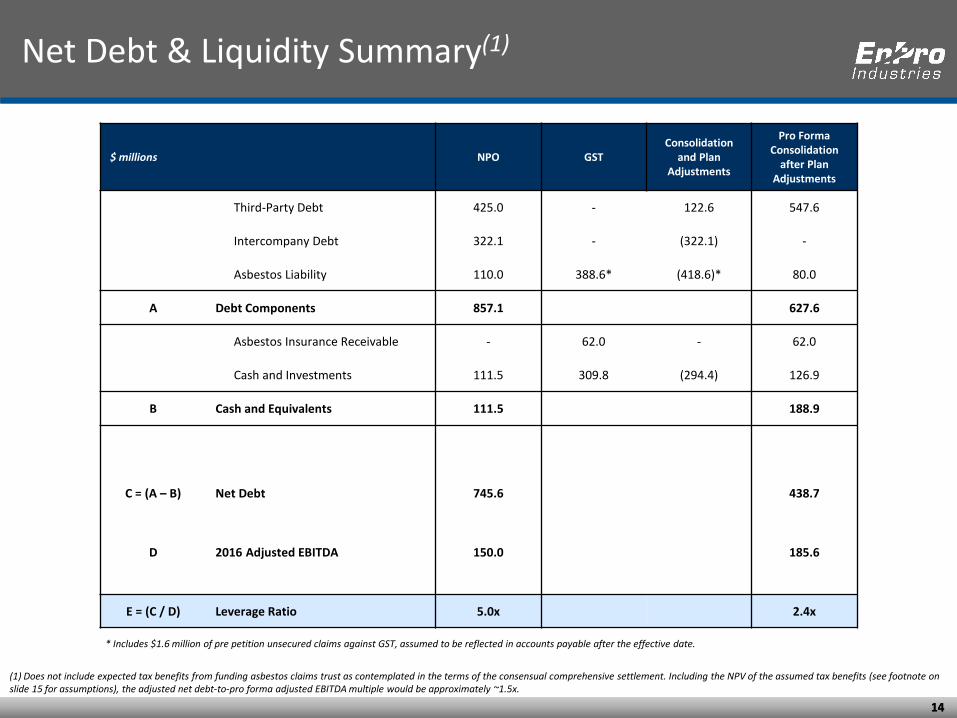

Net Debt & Liquidity Summary(1)

(1) Does not include expected tax benefits from funding asbestos claims trust as contemplated in the terms of the consensual comprehensive settlement. Including the NPV of the assumed tax benefits (see footnote on slide 15 for assumptions), the adjusted net debt-to-pro forma adjusted EBITDA multiple would be approximately ~1.5x.

$ millions NPO GST Consolidation

and Plan Adjustments

Pro Forma Consolidation

after Plan Adjustments

Third-Party Debt 425.0 - 122.6 547.6

Intercompany Debt 322.1 - (322.1) -

Asbestos Liability 110.0 388.6* (418.6)* 80.0

A Debt Components 857.1 627.6

Asbestos Insurance Receivable - 62.0 - 62.0

Cash and Investments 111.5 309.8 (294.4) 126.9

B Cash and Equivalents 111.5 188.9

C = (A – B) Net Debt 745.6 438.7

D 2016 Adjusted EBITDA 150.0 185.6

E = (C / D) Leverage Ratio 5.0x 2.4x

* Includes $1.6 million of pre petition unsecured claims against GST, assumed to be reflected in accounts payable after the effective date.

15 15

NPO Valuation Considerations

Internal Valuation Summary: • On a pro forma basis, taking into account

ACRP settlement plan and reconsolidation of GST, EnPro trades at ~9.0x

• Peer median is ~13.8x

Peer Enterprise Value/TTM EBITDA Multiples(3)

9.0x

9.6x

9.8x

11.5x

11.8x

12.6x

13.7x

13.8x

13.8x

13.8x

14.8x

15.0x

15.3x

15.8x

20.7x

EnPro (Pro Forma)

Regal Beloit

Crane

Barnes Group

Curtiss-Wright

Mueller Water

Colfax

TriMas

EnPro (NPO)

Actuant

IDEX

Woodward

Graco

Nordson

CIRCOR

$ in millions

Market Cap(1) $1,392

Pro Forma Net Debt (Per Slide 14) $439

(A) Enterprise Value $1,831

(B) Estimated Trust Funding Tax Benefits (NPV)(2) $154

(C) Adjusted Enterprise Value (A - B) $1,677

(D) Pro Forma Adjusted 2016 EBITDA $186

Pro Forma EV/TTM EBITDA Multiple (C / D) 9.0x

Peer Median: 13.8x

(1) Market capitalization for NPO per CapitalIQ as of 2/22/17. (2) Estimated Trust Funding Tax Benefit of $154 million assumes that 1/3 of benefit will be realized based on two-year carryback and 2/3 will be realized equally over four years. Detailed tax evaluation underway. (3) EV/TTM EBITDA multiples per CapitalIQ as of 2/22/17. Peer median EV/TTM EBITDA multiple excludes NPO and EnPro (Pro Forma) from calculation. TTM = “Trailing Twelve Months”.

16 16

Why Invest in EnPro?

Critical Nature of Products Leads to Commercial

& Strategic Advantages Leading Brands

Drive a Portfolio of Attractive,

Recurring Business

Highly Diversified

Business Leads to Stable Cash

Flows

Growth Focus Includes

Multiple Levers

Disciplined Investment

Strategy

Favorable ACRP Developments

Attractive Share Price Relative to

Peers

17 17

Appendix

18 18

EnPro Adjusted EBITDA & FCF Reconciliation

($ in millions) 2012 2013 2014 2015 2016

Net Income (Loss) $41.0 $27.4 $22.0 $(20.9) $(40.1)

Plus:

Interest Expense, net 42.8 44.3 44.1 52.1 55.1

Income Tax Expense (Benefit) 22.5 8.4 10.6 2.3 (28.6)

Depreciation and Amortization 55.5 56.6 57.5 58.1 57.1

Restructuring Costs 5.0 6.7 2.3 6.6 13.4

Environmental Reserve Adjustment 1.2 6.3 4.5 1.4 8.6

Asbestos-Related Expenses - - 30.0 - 80.0

Goodwill and Intangible Impairment - - - 47.0 -

Loss on Debt Exchange - - 10.0 2.8 -

Gain on Sale of Business - - (27.7) - -

Other 4.2 5.1 3.0 7.0 4.5

Adjusted EBITDA $172.2 $154.8 $156.3 $156.4 $150.0

Less: Capital Expenditures(1)(2) (40.9) (39.9) (54.7) (47.2) (45.3)

Free Cash Flow(3) $131.3 $114.9 $101.6 $109.2 $104.7

(1) Includes PP&E and software capex. (2) For each period, amount includes capex which EnPro had purchased during the period but for which cash payments had not yet been made. See footnote 1 in the “Notes to Consolidated Financial Statements” of the 2016 Form 10-K for reference. (3) FCF defined as adjusted EBITDA less capex.

19 19

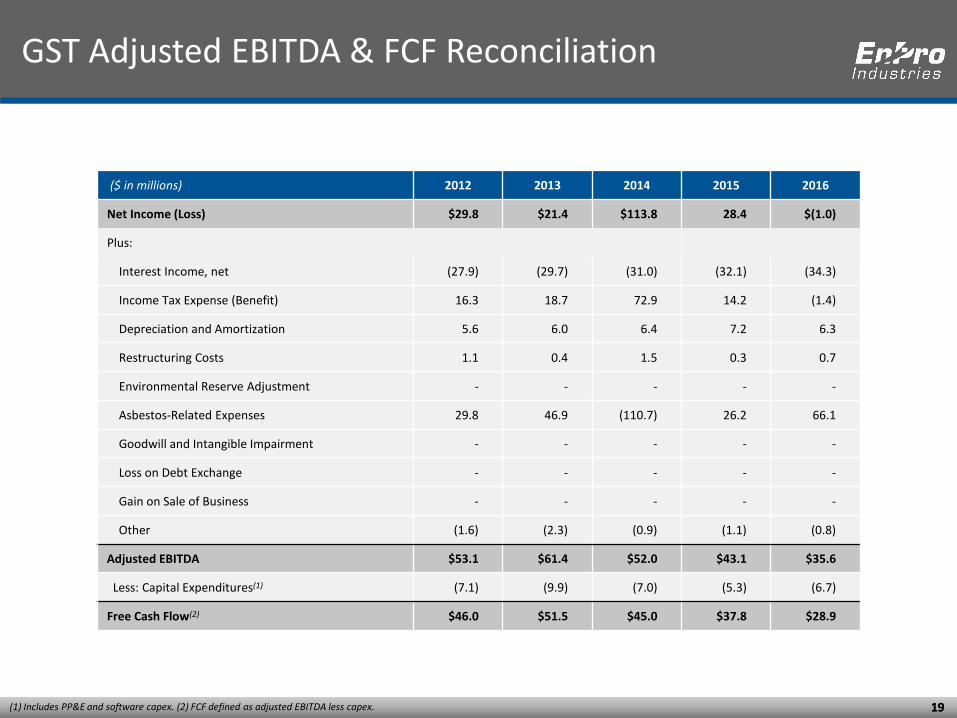

GST Adjusted EBITDA & FCF Reconciliation

($ in millions) 2012 2013 2014 2015 2016

Net Income (Loss) $29.8 $21.4 $113.8 28.4 $(1.0)

Plus:

Interest Income, net (27.9) (29.7) (31.0) (32.1) (34.3)

Income Tax Expense (Benefit) 16.3 18.7 72.9 14.2 (1.4)

Depreciation and Amortization 5.6 6.0 6.4 7.2 6.3

Restructuring Costs 1.1 0.4 1.5 0.3 0.7

Environmental Reserve Adjustment - - - - -

Asbestos-Related Expenses 29.8 46.9 (110.7) 26.2 66.1

Goodwill and Intangible Impairment - - - - -

Loss on Debt Exchange - - - - -

Gain on Sale of Business - - - - -

Other (1.6) (2.3) (0.9) (1.1) (0.8)

Adjusted EBITDA $53.1 $61.4 $52.0 $43.1 $35.6

Less: Capital Expenditures(1) (7.1) (9.9) (7.0) (5.3) (6.7)

Free Cash Flow(2) $46.0 $51.5 $45.0 $37.8 $28.9

(1) Includes PP&E and software capex. (2) FCF defined as adjusted EBITDA less capex.

20 20

GST Adjusted EBITDA & FCF Reconciliation

($ in millions) 2012 2013 2014 2015 2016

Adjusted EBITDA

EnPro $172.2 $154.8 $156.3 $156.4 $150.0

GST 53.1 61.4 52.0 43.1 35.6

Pro Forma Adjusted EBITDA(1) $225.3 $216.2 $208.3 $199.5 $185.6

Capex

EnPro $40.9 $39.9 $54.7 $47.2 $45.3

GST 7.1 9.9 7.0 5.3 6.7

Pro Forma Capex(2) $48.0 $49.8 $61.7 $52.5 $52.0

Pro Forma FCF(3) $177.3 $166.4 $146.6 $147.0 $133.6

(1) See adjusted EBITDA reconciliations for EnPro and GST in appendix. (2) “Pro Forma Capex” defined as sum of total EnPro capex and total GST capex. (3) “Pro Forma FCF” defined as pro forma adjusted EBITDA less pro forma capex.

21 21

Reconciliation of Net Sales to Pro Forma Net Sales

Sealing Products 2012 2013 2014 2015 2016 Net Sales $609.1 $622.9 $664.3 $705.6 $705.6 Adjustments:

Sales of Unconsolidated Entities 230.4 232.7 230.3 210.4 189.2 Intercompany Sales (38.3) (44.2) (50.3) (47.6) (42.5)

Pro Forma Net Sales $801.2 $811.4 $844.3 $868.4 $852.3

Engineered Products 2012 2013 2014 2015 2016 Net Sales $363.0 $356.4 $357.6 $297.8 $277.1 Adjustments:

Sales of Unconsolidated Entities 5.3 4.8 4.5 3.0 2.4 Intercompany Sales (3.3) (3.3) (2.4) (1.7) (1.5)

Pro Forma Net Sales $365.0 $357.9 $359.7 $299.1 $278.0

Power Systems 2012 2013 2014 2015 2016 Net Sales $214.6 167.6 $200.1 $204.6 $208.3 Adjustments:

Sales of Unconsolidated Entities 4.4 7.3 5.8 4.2 4.2 Intercompany Sales (4.3) (3.2) (2.9) (1.8) (1.4)

Pro Forma Net Sales $214.7 $171.7 $203.0 $207.0 $211.1

EnPro 2012 2013 2014 2015 2016 Net Sales $1,184.2 $1,144.2 $1,219.3 $1,204.4 $1,187.7 Adjustments:

Sales of Unconsolidated Entities 240.1 244.8 240.6 217.6 195.8 Intercompany Sales (46.3) (50.9) (55.8) (51.4) (45.8)

Pro Forma Net Sales $1,378.0 $1,338.1 $1,404.1 $1,370.6 $1,337.7

22 22

Reconciliation of Segment Profit to Pro Forma Adjusted Segment EBITDA

Sealing Products 2012 2013 2014 2015 2016 Segment Profit $88.8 $97.1 $85.6 $84.3 $81.8 Adjustments:

Segment Profit of Unconsolidated Entities 44.4 51.5 42.5 34.5 28.3 Pro Forma D&A Adjustments (6.6) (6.6) (6.6) (6.6) (6.6)

Pro Forma Segment Profit $126.6 $142.0 $121.5 $112.2 $103.5 Acquisition Expenses 2.6 0.3 0.2 3.8 1.0 Restructuring Costs 2.4 1.3 3.8 0.6 4.0 Depreciation and Amortization Expenses 42.4 42.9 43.9 48.1 47.9

Pro Forma Adjusted Segment EBITDA $174.0 $186.5 $169.4 $164.7 $156.4

Engineered Products 2012 2013 2014 2015 2016 Segment Profit $20.5 $17.6 $26.8 $6.4 $12.4 Adjustments:

Segment Profit of Unconsolidated Entities 2.0 2.4 1.9 1.0 0.6 Pro Forma D&A Adjustments - - - - -

Pro Forma Segment Profit $22.5 $20.0 $28.7 $7.4 $13.0 Acquisition Expenses 1.0 0.2 0.1 - 0.1 Restructuring Costs 3.7 3.7 - 6.2 6.8 Depreciation and Amortization Expenses 21.8 22.5 22.5 19.5 17.6

Pro Forma Adjusted Segment EBITDA $49.0 $46.4 $51.3 $33.1 $37.5

Power Systems 2012 2013 2014 2015 2016 Segment Profit $39.2 $14.0 $28.5 $27.1 $17.0 Adjustments:

Segment Profit of Unconsolidated Entities 0.8 1.5 1.1 0.8 0.7 Pro Forma D&A Adjustments - - - - -

Pro Forma Segment Profit $40.0 $15.5 $29.6 $27.9 $17.7 Acquisition Expenses - - - - - Restructuring Costs - 2.0 - - 0.4 Depreciation and Amortization Expenses 3.1 3.6 3.8 4.1 4.5

Pro Forma Adjusted Segment EBITDA $43.1 $21.1 $33.4 $32.0 $22.6