fy15 results presentation - adairs

TRANSCRIPT

FY15 resultspresentation

25 August 2015

1

Pro Forma Results highlights

Variances refer to pro-forma FY15 highlights compared to pro-forma FY14 highlights

$210.9mup 25.6%

Sales

Up 51.8%

$33.1mEBIT

margin

21.6%

LFL salesgrowth

Gross profit

62.0% down from 46.5%

44.1% of salesCODB

$22.0mNPAT

1. Operational highlights – Strong gains and milestones achieved

2. Financial performance – FY15 ahead of Prospectus Forecast

3. Outlook – Well positioned for continued growth and achievementof FY16 Prospectus Forecast

Agenda

3

FY15 operational highlights

Continued focus on product and range differentiation• Strong performance from fashion bedlinen and home furnishings• Improved performance of Adairs Kids category

Continued focus on product and range differentiation• Strong performance from fashion bedlinen and home furnishings• Improved performance of Adairs Kids category

Four net new stores opened with ongoing store refurbishments• Three Adairs, two Adairs Homemaker (one closure - underperforming)• Fully refurbished seven stores (four Adairs, three Adairs Homemakers)

Four net new stores opened with ongoing store refurbishments• Three Adairs, two Adairs Homemaker (one closure - underperforming)• Fully refurbished seven stores (four Adairs, three Adairs Homemakers)

First Urban Home Republic concession stores opened in Myer• Sydney CBD, Geelong, HighpointFirst Urban Home Republic concession stores opened in Myer• Sydney CBD, Geelong, Highpoint

Online continues to grow significantly above market• 35.2% sales growth (second half 48.3% growth)Online continues to grow significantly above market• 35.2% sales growth (second half 48.3% growth)

New ERP implemented enabling opportunities for the future• Warehouse, Product and Finance implemented successfully• POS roll out on track for second half FY16

New ERP implemented enabling opportunities for the future• Warehouse, Product and Finance implemented successfully• POS roll out on track for second half FY16

Keysborough DC opened building capacity for growth• New 6700m facility for store replenishment and online operational January

2015

Keysborough DC opened building capacity for growth• New 6700m facility for store replenishment and online operational January

2015

Successful ASX listing Successful ASX listing

All store formats delivering strong LFL sales growth

31 consecutive months of LFL sales growth

Second half delivered 24.1% growth

Growth in transaction numbers driving sales

Core formats performance driven by expansion indecorator categories and growth of fashion &decorator product categories

Emerging formats driven by continued productimprovement

LFL sales growth

4

LFL sales momentum strong +21.6%

* Three of the 135 stores represent concession stores within Myer

Adairs Stores (incl. Outlet)

Homemaker Stores

Adairs Kids Stores

UHR Stores (inc. Myer concessions)DC and HQ

11 5

1

44

27

12

2214 1

18 6 2

5 1

1

1

Number of stores

5

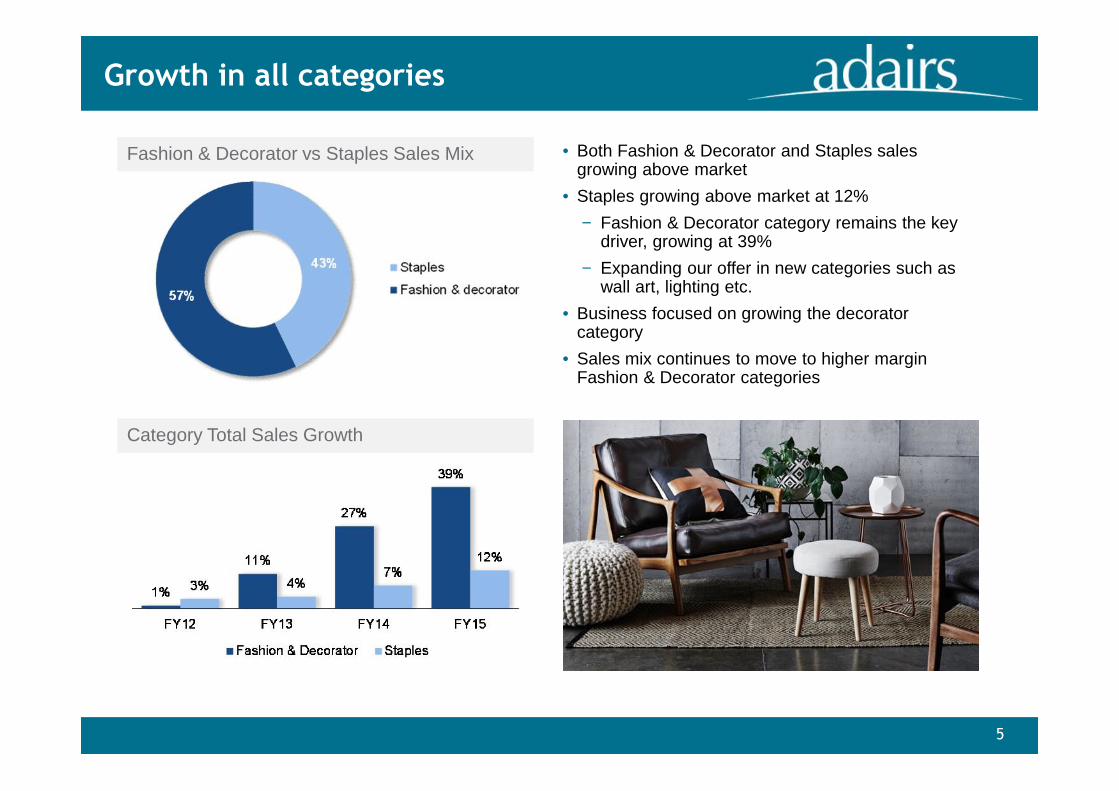

Growth in all categories

Fashion & Decorator vs Staples Sales Mix Both Fashion & Decorator and Staples salesgrowing above market

Staples growing above market at 12% Fashion & Decorator category remains the key

driver, growing at 39% Expanding our offer in new categories such as

wall art, lighting etc. Business focused on growing the decorator

category Sales mix continues to move to higher margin

Fashion & Decorator categories

Category Total Sales Growth

1. Operational highlights – Strong gains and milestones achieved

2. Financial performance – FY15 ahead of Prospectus Forecast

3. Outlook – Well positioned for continued growth and achievementof FY16 Prospectus Forecast

Agenda

7

FY15 above Prospectus Forecast

$ million Statutory FY15 Pro-forma FY15

Pro-forma FY15Prospectus

forecast Variance

Sales 210.9 210.9 203.4 3.7%

Gross Profit 130.7 130.7 127.5 2.5%

EBITDA 23.0 37.7 35.8 5.2%

EBIT 18.4 33.1 31.4 5.7%

NPAT (continuing operations) 2.9 22.0 20.7 6.3%

EPS (cents per share)* 0.5 14.5 n/a

Net Debt 32.2 39.4 40.0

Note: Variance measures pro-forma FY15 vs pro-forma FY15 Prospectus forecast

Adairs has successfully executed it’s strategy to deliver pro-formaFY15 results above Prospectus Forecast

* EPS based on 165.9m shares on issue is 13 cents (Prospectus forecast 12.5 cents)

8

8

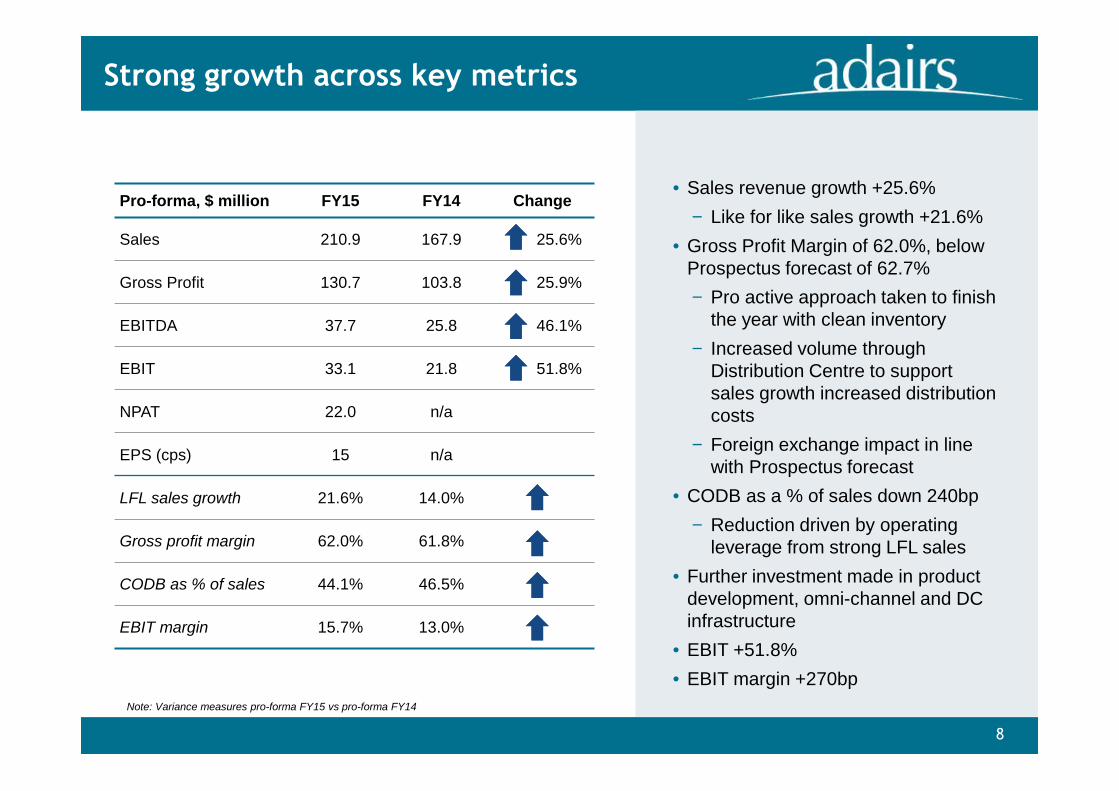

Pro-forma, $ million FY15 FY14 Change

Sales 210.9 167.9 25.6%

Gross Profit 130.7 103.8 25.9%

EBITDA 37.7 25.8 46.1%

EBIT 33.1 21.8 51.8%

NPAT 22.0 n/a

EPS (cps) 15 n/a

LFL sales growth 21.6% 14.0%

Gross profit margin 62.0% 61.8%

CODB as % of sales 44.1% 46.5%

EBIT margin 15.7% 13.0%

Sales revenue growth +25.6% Like for like sales growth +21.6%

Gross Profit Margin of 62.0%, belowProspectus forecast of 62.7% Pro active approach taken to finish

the year with clean inventory Increased volume through

Distribution Centre to supportsales growth increased distributioncosts

Foreign exchange impact in linewith Prospectus forecast

CODB as a % of sales down 240bp Reduction driven by operating

leverage from strong LFL sales Further investment made in product

development, omni-channel and DCinfrastructure

EBIT +51.8% EBIT margin +270bp

Strong growth across key metrics

Note: Variance measures pro-forma FY15 vs pro-forma FY14

9

Continued operational improvement

Cost of doing business down to 44.1%, from46.5% prior year

Lower than FY15 pro-forma ProspectusForecast of 45.0%

Significant investment in recent years haspositioned the business to leverage the teamand infrastructure for future growth

Key infrastructure projects in final stages ofimplementation

Focus on operational improvements within theDistribution Centre

Focus on optimising ERP

Rollout of POS on track for second half FY16

Cost of doing business (CODB)

10

10

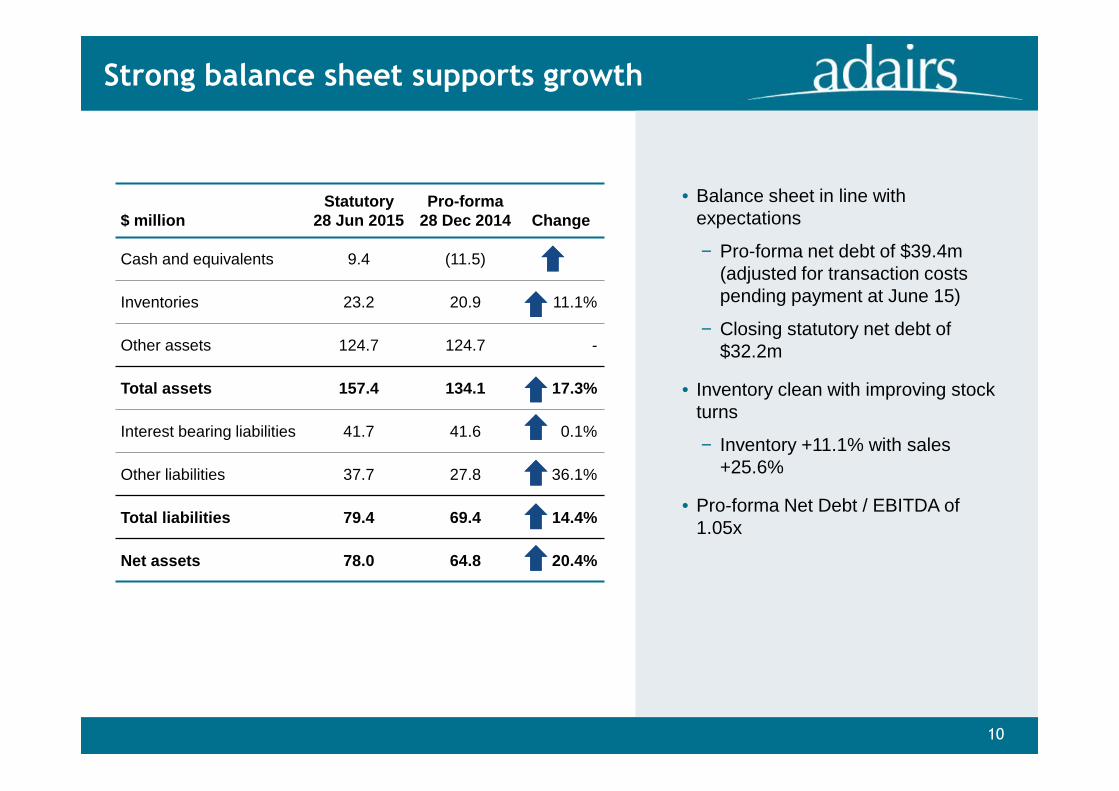

Strong balance sheet supports growth

$ millionStatutory

28 Jun 2015Pro-forma

28 Dec 2014 Change

Cash and equivalents 9.4 (11.5)

Inventories 23.2 20.9 11.1%

Other assets 124.7 124.7 -

Total assets 157.4 134.1 17.3%

Interest bearing liabilities 41.7 41.6 0.1%

Other liabilities 37.7 27.8 36.1%

Total liabilities 79.4 69.4 14.4%

Net assets 78.0 64.8 20.4%

Balance sheet in line withexpectations

Pro-forma net debt of $39.4m(adjusted for transaction costspending payment at June 15)

Closing statutory net debt of$32.2m

Inventory clean with improving stockturns

Inventory +11.1% with sales+25.6%

Pro-forma Net Debt / EBITDA of1.05x

11

11

Strong cash flow from operations

$ millionPro-forma

FY15

FY14(continuingoperations) Change

Net cash flows fromoperating activities 26.2 21.8 20.3%

Net cash flows frominvesting activities (6.9) (6.3) 10.0%

Net cash flows fromfinancing activities - (2.6)

Net cash (decrease) /increase in cash 19.3 12.9 49.2%

• $26.2 million cash from operatingactivities

Strong operating cash flow due toimprovement in working capitalmanagement (i.e. stock turns) andincrease in profitability

• $6.9 million cash used for investingactivities

5 new stores plus 3 concessionstores, 9 refurbs/relocations and anumber of LED upgrades

Other major capital expenditureincluded the ERP implementation

• $0 cash from financing activities There is no requirement to make

annual repayments under the newdebt facility

All prior year financing activityrelates to the company restructureand IPO

• No dividends paid since IPO as perProspectus

Pro-forma excludes all cash flows from IPO, refinancing anddivestment of Dusk.

12

Investing for growth

Capital expenditure Continued focus on opening new stores

Pleasing results from stores refurbished inFY15

Remain committed to ongoing investmentin existing stores

Continue to seek opportunities to expand inhigh performing homemaker centres

Majority of ERP expenditure completed asplanned

Trial of 3 Myer Urban Home Republicconcessions commenced. Continue to assesstrading performance

Capex above Prospectus forecast ($6.2m)due to UHR concessions, store expansionsand ERP capex brought forward

1. Operational highlights – Strong gains and milestones achieved

2. Financial performance – FY15 ahead of Prospectus Forecast

3. Outlook – Well positioned for continued growth and achievementof FY16 Prospectus Forecast

Agenda

14

Positioned for category growth

Adairs has the structure to support continued product andrange differentiation and expansion.

Leverage product design, development and sourcingcapabilities to drive:

On trend fashionable merchandise

Speed to market

Product quality

Coordinated ranging

Expanded range

Superior value for customers

The business has proven the capability of this strategy todrive like for like sales growth

15

Core store format provides proven growth path

Roll out of core store formats remains the largest driver of growth of our store network

7 – 10 of the new stores to be opened annually for the next 5 years expected to be Adairs and

Adairs Homemaker

Majority of new sites are expected to be in New South Wales and Queensland

Where possible, up-size selected existing Adairs Homemaker stores (nine potential stores identified)

FY16 store roll out on track with Prospectus forecast

16

Emerging formats offer growth opportunity

Adairs Kids

Improving performance metrics will see more stores open inFY16

New store format developed and will be progressively rolled out

Urban Home Republic

Currently trialing concession format in three Myer stores

Looking to add standalone stores in key markets

Medium term focus to open 2 – 4 stores per annum and faster ifthese formats continue to perform

Adairs will recommence the roll-out of Adairs Kids andUrban Home Republic

17

Leveraging investments to support growth

Excellence in retail execution supportsAdairs’ future growth

Enhance online customer experience and omni-channelmarketing

Growing online email database

More product available online

Continue to switch marketing dollars from mass marketingto higher performing omni-channels (EDM / Social etc.)

Increased focus on social media and brand ambassadors

Leverage ERP to improve customer experience

New POS will enable improved customer delivery channelse.g. click and collect CY16

Faster transaction speeds and superior data integrity

Enhances execution of loyalty program in store

Reduces administrative tasks in store providing moreselling hours

18

International expansion opportunity

A disciplined and selective international expansion may offer an additional pathwayto growth

Adairs is evaluating the potential to commence international expansion trial stores in New Zealand orSouth Africa

Further diligence on these two markets is currently being undertaken by management

Reaffirm the prospectus dividend expectation of11 cents per share fully franked in FY16Reaffirm the prospectus dividend expectation of11 cents per share fully franked in FY16

19

Well positioned for continued growth

Attractive growth opportunities – new products, new stores, new marketsAttractive growth opportunities – new products, new stores, new markets

Successfully listed on ASX in JuneSuccessfully listed on ASX in June

FY15 result ahead of Prospectus forecastFY15 result ahead of Prospectus forecast

Well positioned to achieve FY16 Prospectus forecastWell positioned to achieve FY16 Prospectus forecast

20

Questions?

Appendix

22

Leading Australian home furnishings retailer

Adairs has a long history in Australia and now supplies home furnishings across fivedifferent formats nationwide, plus an online store

Strong sales and profitability growth across allformats

“Core” formats key to growth over next fiveyears (bias to new homemaker stores)

“Emerging” formats support growth

Medium term focus to open 2 – 4 storesover next five years and faster if theseformats continue to perform

“Online” fastest growing channel

Critical to optimising and growing customerexperience

23

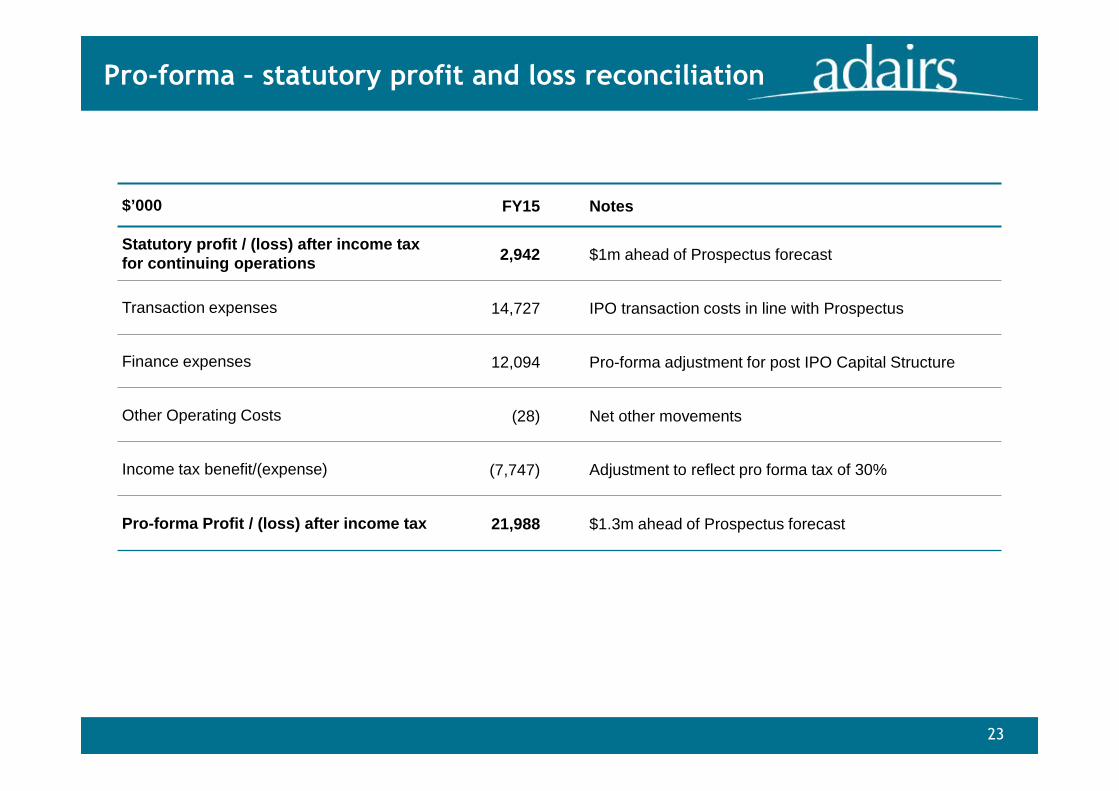

Pro-forma – statutory profit and loss reconciliation

$’000 FY15 Notes

Statutory profit / (loss) after income taxfor continuing operations 2,942 $1m ahead of Prospectus forecast

Transaction expenses 14,727 IPO transaction costs in line with Prospectus

Finance expenses 12,094 Pro-forma adjustment for post IPO Capital Structure

Other Operating Costs (28) Net other movements

Income tax benefit/(expense) (7,747) Adjustment to reflect pro forma tax of 30%

Pro-forma Profit / (loss) after income tax 21,988 $1.3m ahead of Prospectus forecast

24

Pro-forma – statutory cash flow reconciliation

$’000 FY15 NotesStatutory net increase in cash and cashequivalents (7,896)

Income tax (paid)/refunded (9,355) Difference between income tax paid and pro formaassumed tax paid at 30% of profit before tax.

Net incremental costs as a public company (144)

Operating cash flow from discontinuedoperations (4,692) Dusk net operating cash flow

Investing cash flows from discontinuedoperations 1,374 Dusk capex pre divestment

IPO Transaction costs 10,165 Cash Transaction costs paid – $7.1m will be paid in FY16

Pre IPO restructure costs expensed 309 Transaction and adviser fees relating to pre IPOdivestment and refinancing activities

Proceeds from share issue (35,645) IPO related

Net proceeds from borrowings (Bank Debt) (5,808) Impact of refinancing activity excluded from pro forma

Repayment of RPS including interest 71,477

Cash retained on divestment (500) Dusk dividend received as part of divestment

Pro-forma net increase in cash and cashequivalents 19,285

25

Disclaimer

Some of the information contained in this presentation contains “forward-looking statements” which may not directly orexclusively relate to historical facts. These forward-looking statements reflect Adairs Limited current intentions, plans,expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors, many ofwhich are outside the control of Adairs Limited.Important factors that could cause actual results to differ materially from the expectations expressed or implied in theforward-looking statements include known and unknown risks. Because actual results could differ materially from AdairsLimited current intentions, plans, expectations, assumptions and beliefs about the future, you are urged to view all forward-looking statements contained herein with caution.