fy results 03 presentation final for pdf format - swisscom · wireline business – improved...

TRANSCRIPT

1

2003 results, conference call24 March 2004

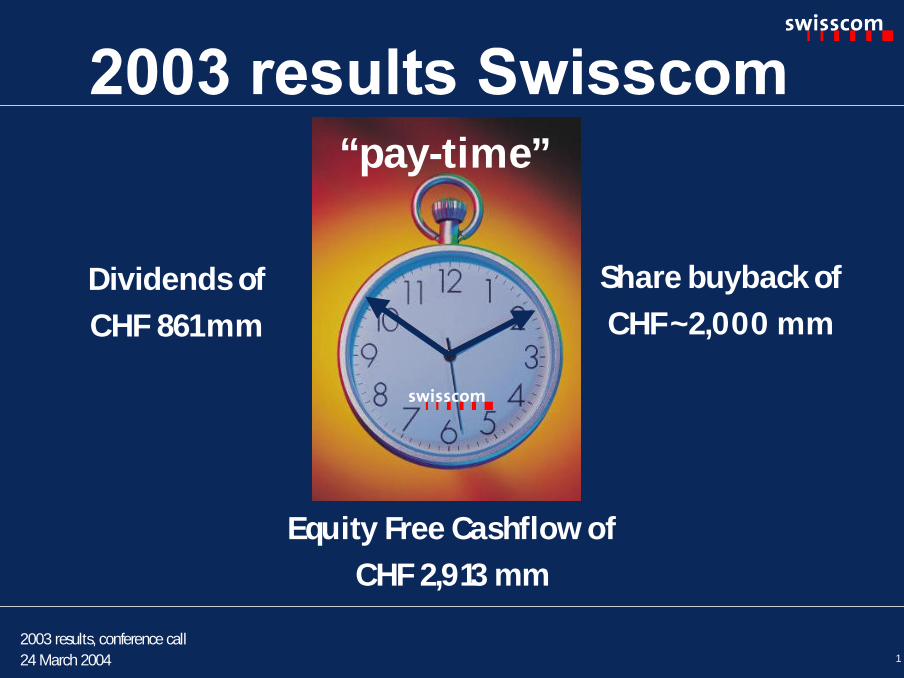

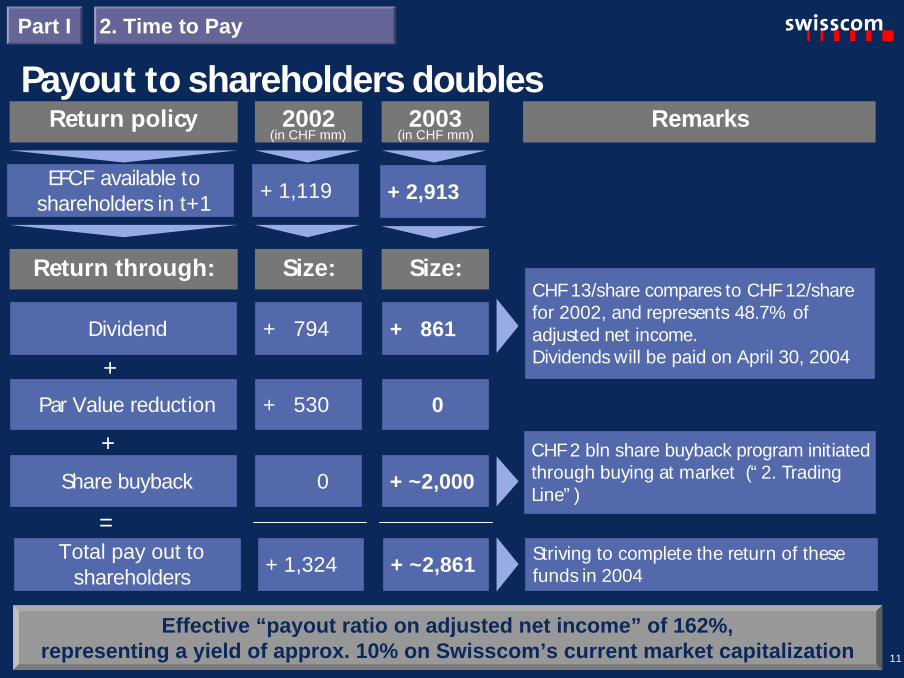

Dividends ofCHF 861 mm

Share buyback ofCHF~2,000 mm

Equity Free Cashflow ofCHF 2,913 mm

“pay-time”

2

Time division for this conference call:

The essentials & key messages

Supporting background information

Part I[presented]

Part II[not presented]

“pay-time”

3

Jens Alder, CEO

Jens Alder, CEO

Ueli Dietiker, CFO

Jens Alder, CEO

1. Time to Summarize 2003

2. Time to Pay

3. Time to Analyse

5. Time for Q&A

4

9

12

Content Slide

34

4. Time to Look Forward 29

Part I The essentials & key messages

“pay-time”

4

2003 results, conference call24 March 2004

“ pay-time ““pay-time”

5

1. Time to Summarize 2003

Strategic reviewA company committed to strong fundamentals and financial discipline

Leading Telco in CH Intelligent investor

Smallerinvestment

intoinnovative

“entry-ticket

options”

Largerinvestment

only ifacquisition

criteriasatisfied

Solid financial footing

Returningall equityfree cash

flow toshare-

holders.Every year

Optimize free cashflow from core

business

Create balancedrisk-reward growth

path

Combine strategicflexibility withgenerous yield

Success-fully

defendingstrongmarket

position

Focused onoperatingcost and

staffreductionsto sustainmargins

Preservingstrong

balancesheet tooptimizestrategicflexibility

Part I

What have we delivered?

6

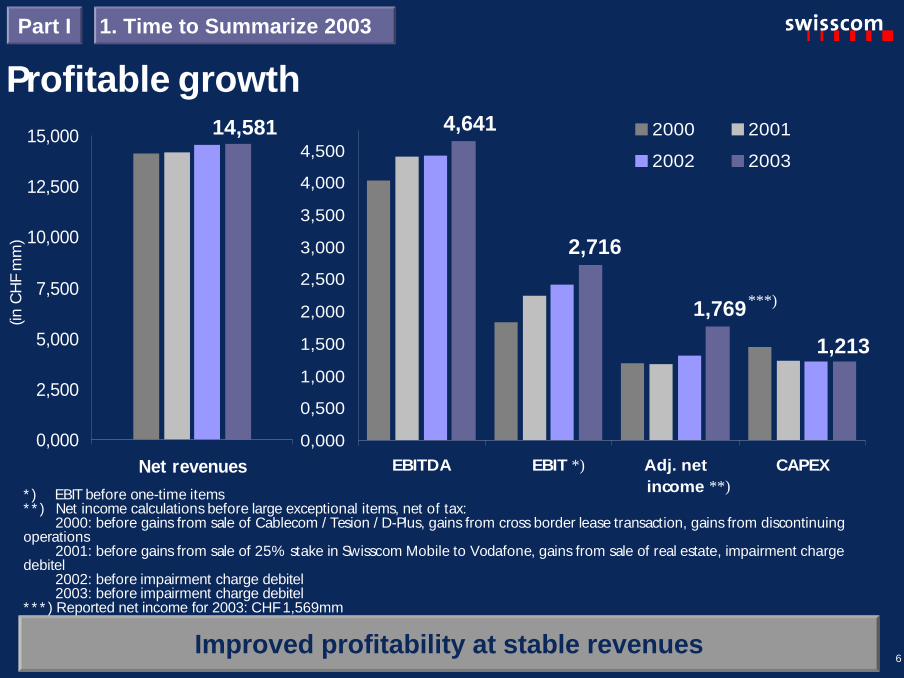

Profitable growth

Improved profitability at stable revenues

1. Time to Summarize 2003Part I

0,000

2,500

5,000

7,500

10,000

12,500

15,000

Net revenues

(inC

HF

mm

)

**)* ) EBIT before one-time items* * ) Net income calculations before large exceptional items, net of tax:

2000: before gains from sale of Cablecom / Tesion / D-Plus, gains from cross border lease transaction, gains from discontinuingoperations

2001: before gains from sale of 25% stake in Swisscom Mobile to Vodafone, gains from sale of real estate, impairment chargedebitel

2002: before impairment charge debitel2003: before impairment charge debitel

* * * ) Reported net income for 2003: CHF 1,569mm

0,000

0,500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

EBITDA EBIT Adj. netincome

CAPEX

2000 2001

2002 2003

14,581 4,641

2,716

1,213

1,769

*)

***)

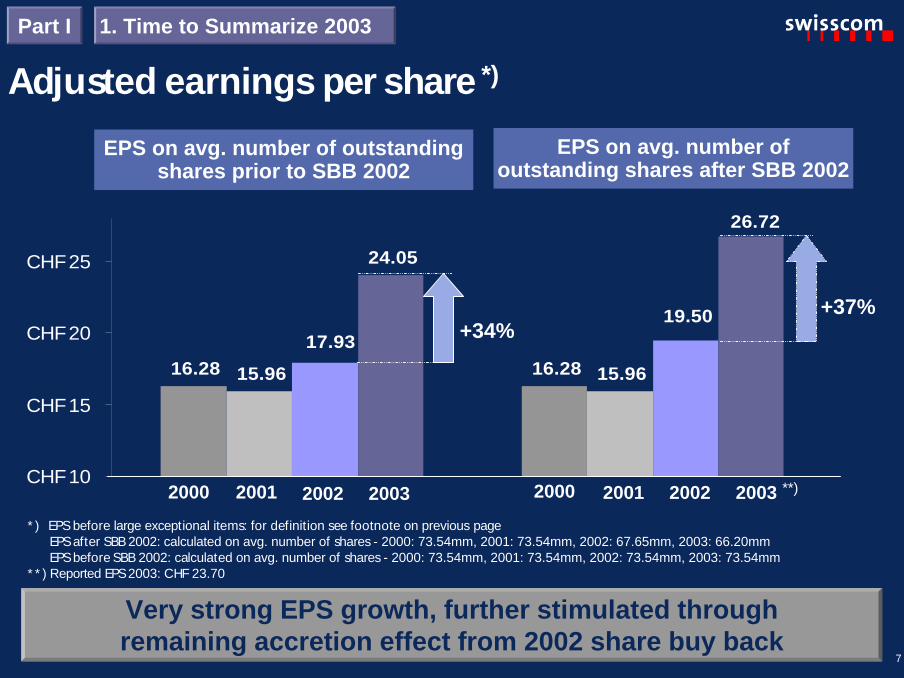

7

16.28 16.2815.96 15.96

24.05

19.5017.93

26.72

CHF 10

CHF 15

CHF 20

CHF 25

Adjusted earnings per share *)

* ) EPS before large exceptional items: for definition see footnote on previous pageEPS after SBB 2002: calculated on avg. number of shares - 2000: 73.54mm, 2001: 73.54mm, 2002: 67.65mm, 2003: 66.20mmEPS before SBB 2002: calculated on avg. number of shares - 2000: 73.54mm, 2001: 73.54mm, 2002: 73.54mm, 2003: 73.54mm

* * ) Reported EPS 2003: CHF 23.70

Very strong EPS growth, further stimulated throughremaining accretion effect from 2002 share buy back

+34%

EPS on avg. number ofoutstanding shares after SBB 2002

EPS on avg. number of outstandingshares prior to SBB 2002

+37%

2000 2001 2002 2003 2000 2001 2002 2003

1. Time to Summarize 2003Part I

**)

8

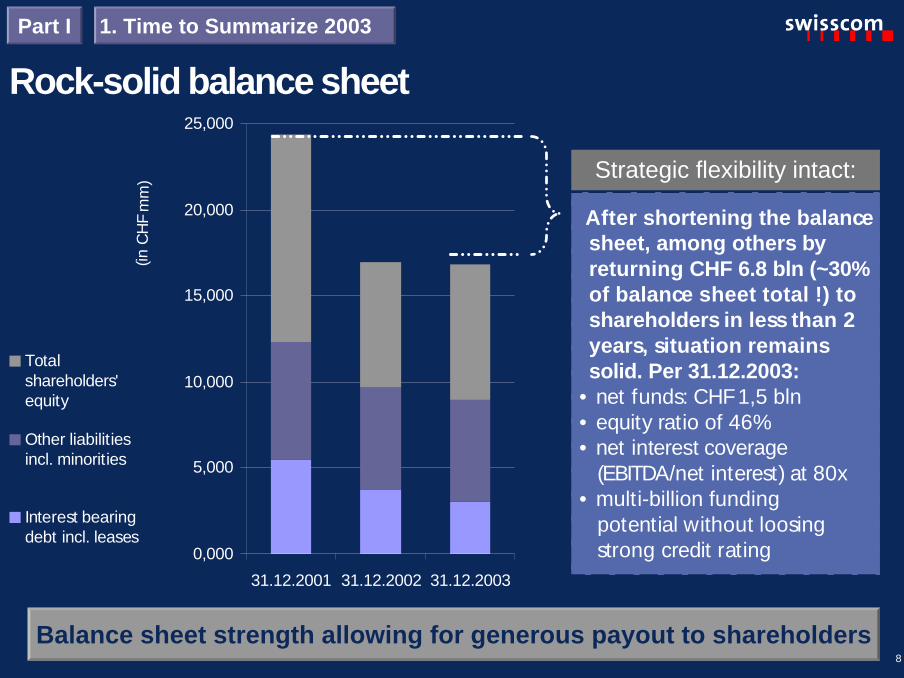

Balance sheet strength allowing for generous payout to shareholders

0,000

5,000

10,000

15,000

20,000

25,000

31.12.2001 31.12.2002 31.12.2003

Totalshareholders'equity

Other liabilitiesincl. minorities

Interest bearingdebt incl. leases

( inC

HF

mm

)

After shortening the balancesheet, among others byreturning CHF 6.8 bln (~30%of balance sheet total !) toshareholders in less than 2years, situation remainssolid. Per 31.12.2003:

• net funds: CHF 1,5 bln• equity ratio of 46%• net interest coverage

(EBITDA/net interest) at 80x• multi-billion funding

potential without loosingstrong credit rating

Strategic flexibility intact:

Rock-solid balance sheet1. Time to Summarize 2003Part I

9

2003 results, conference call24 March 2004

“pay-time”

10

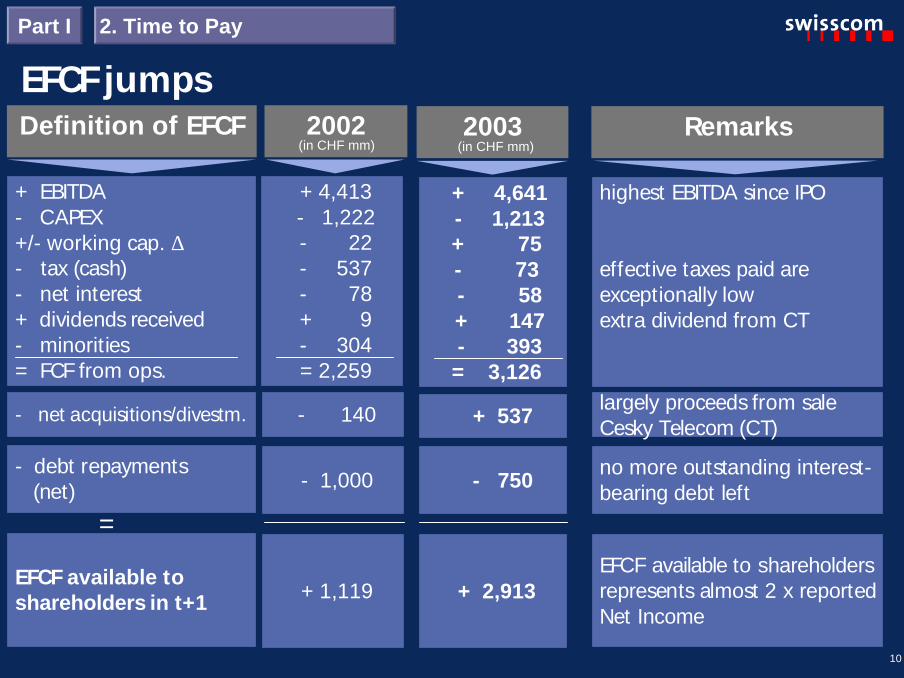

EFCF jumps2. Time to PayPart I

- net acquisitions/divestm.

- debt repayments(net)

EFCF available toshareholders in t+1

+ EBITDA- CAPEX+/- working cap. ∆- tax (cash)- net interest+ dividends received- minorities= FCF from ops.

Definition of EFCF

=

largely proceeds from saleCesky Telecom (CT)

no more outstanding interest-bearing debt left

EFCF available to shareholdersrepresents almost 2 x reportedNet Income

highest EBITDA since IPO

effective taxes paid areexceptionally lowextra dividend from CT

Remarks2003

+ 537

- 750

+ 2,913

+ 4,641- 1,213+ 75- 73- 58+ 147- 393

= 3,126

- 140

- 1,000

+ 1,119

+ 4,413- 1,222- 22- 537- 78+ 9- 304= 2,259

2002(in CHF mm) (in CHF mm)

11

EFCF available toshareholders in t+1 + 1,119

Return policy 2002 Remarks

Return through: Size:

Dividend + 794

Par Value reduction + 530

Total pay out toshareholders + 1,324

++

=

CHF 2 bln share buyback program initiatedthrough buying at market (“ 2. TradingLine” )

CHF 13/share compares to CHF 12/sharefor 2002, and represents 48.7% ofadjusted net income.Dividends will be paid on April 30, 2004

Striving to complete the return of thesefunds in 2004

Effective “payout ratio on adjusted net income” of 162%,representing a yield of approx. 10% on Swisscom’s current market capitalization

+ 2,913

2003

Size:

+ 861

0

+ ~2,861

Share buyback 0 + ~2,000

+

Payout to shareholders doubles(in CHF mm) (in CHF mm)

2. Time to PayPart I

12

2003 results, conference call24 March 2004

“pay-time”

13

Part I

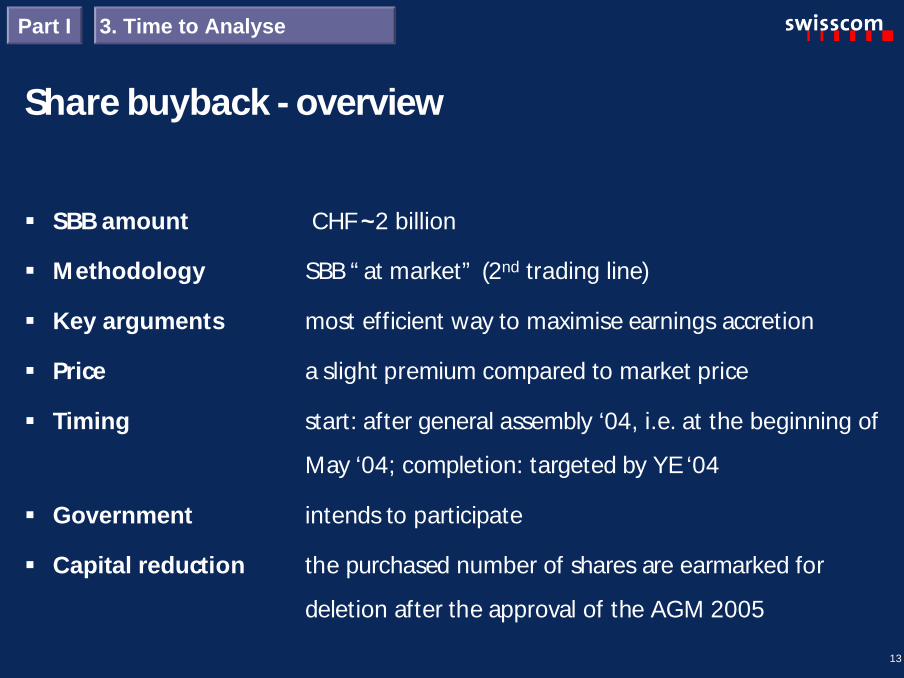

Share buyback - overview

§ SBB amount CHF~2 billion

§ Methodology SBB “ at market” (2nd trading line)

§ Key arguments most efficient way to maximise earnings accretion

§ Price a slight premium compared to market price

§ Timing start: after general assembly ‘04, i.e. at the beginning of

May ‘04; completion: targeted by YE ‘04

§ Government intends to participate

§ Capital reduction the purchased number of shares are earmarked for

deletion after the approval of the AGM 2005

3. Time to Analyse

14

Share buyback - taxes

Part I 3. Time to Analyse

Withholdingtax

Swissprivate investor

Incometax

§ 35% of purchaseprice minus nominalvalue of CHF 1/share

§ fully reclaimable

Swissinstitutional investor

Foreigninvestor

§ 35% of purchaseprice minus nominalvalue of CHF 1/share

§ fully reclaimable

§ 35% of purchaseprice minus nominalvalue of CHF 1/share

§ bilateral tax treatydetermines what canbe reclaimed

§ on purchase priceminus nominal valueof CHF 1/share

§ on purchase priceminus investor’sbook value

§ depending on localtax law

15

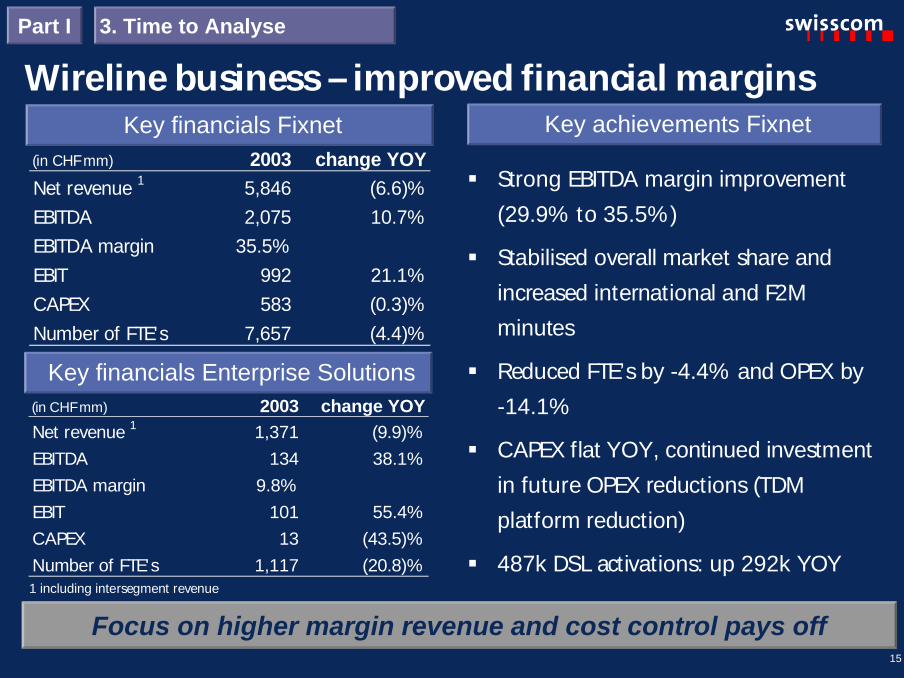

Wireline business – improved financial marginsKey achievements Fixnet

Focus on higher margin revenue and cost control pays off

§ Strong EBITDA margin improvement(29.9% to 35.5%)

§ Stabilised overall market share andincreased international and F2Mminutes

§ Reduced FTE’s by -4.4% and OPEX by-14.1%

§ CAPEX flat YOY, continued investmentin future OPEX reductions (TDMplatform reduction)

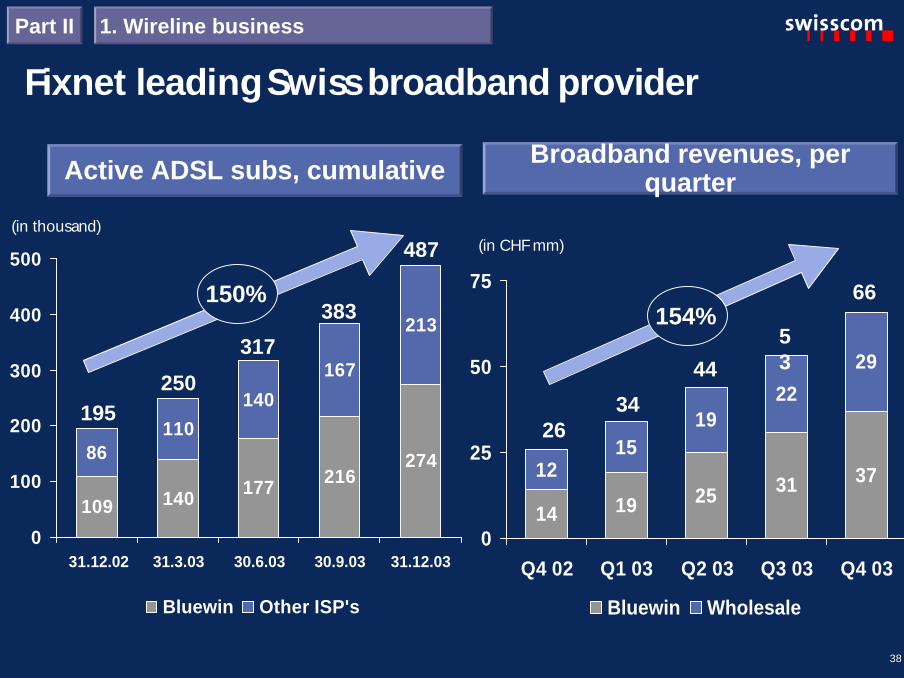

§ 487k DSL activations: up 292k YOY

Key financials Fixnet

Key financials Enterprise Solutions

(in CHF mm) 2003 change YOYNet revenue 1 5,846 (6.6)%EBITDA 2,075 10.7%EBITDA margin 35.5%EBIT 992 21.1%CAPEX 583 (0.3)%Number of FTE's 7,657 (4.4)%

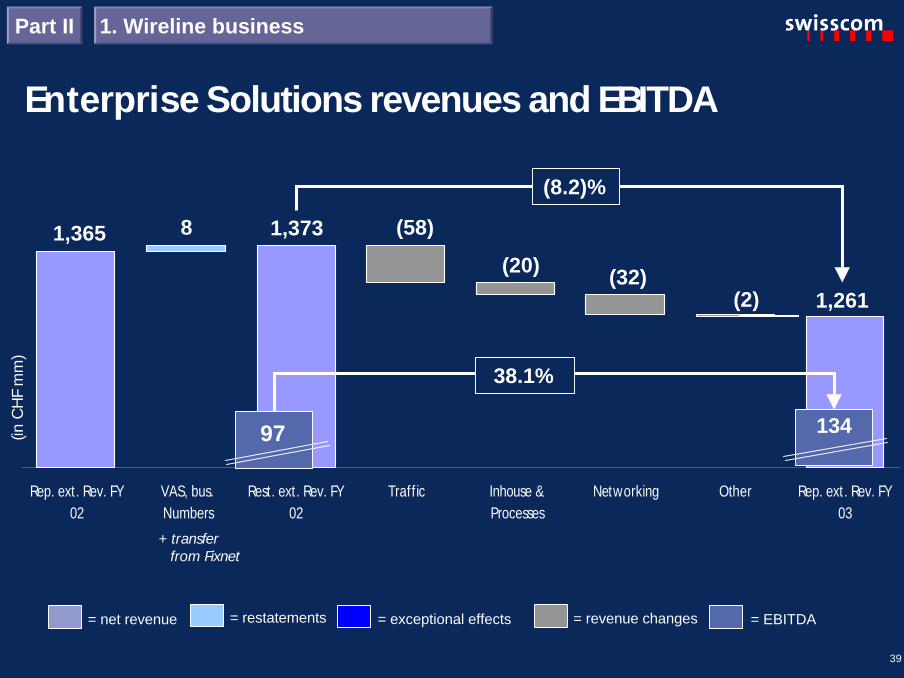

(in CHF mm) 2003 change YOYNet revenue 1 1,371 (9.9)%EBITDA 134 38.1%EBITDA margin 9.8%EBIT 101 55.4%CAPEX 13 (43.5)%Number of FTE's 1,117 (20.8)%1 including intersegment revenue

3. Time to AnalysePart I

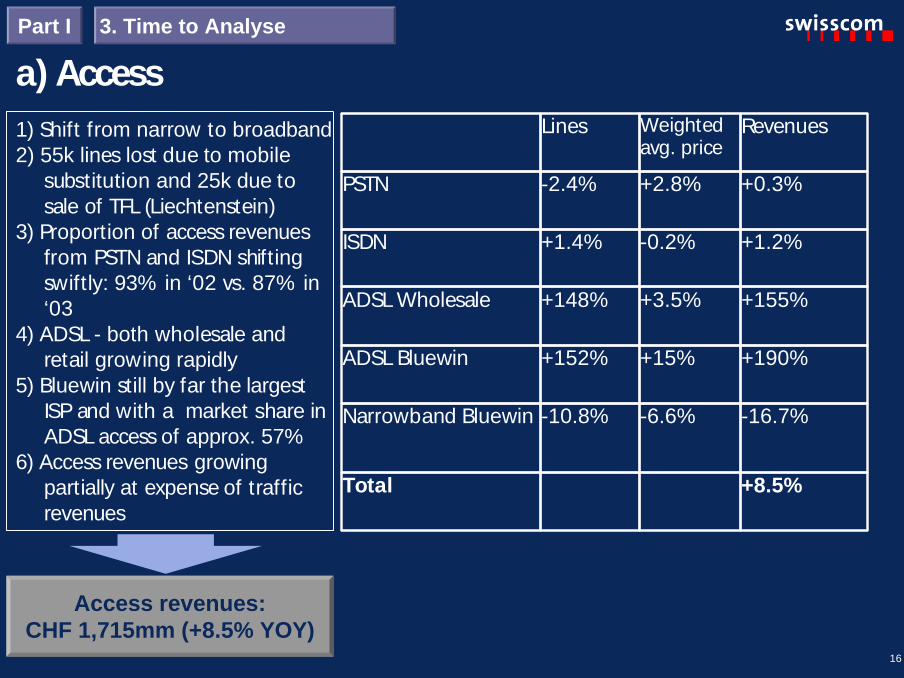

16

a) Access1) Shift from narrow to broadband2) 55k lines lost due to mobile

substitution and 25k due tosale of TFL (Liechtenstein)

3) Proportion of access revenuesfrom PSTN and ISDN shiftingswiftly: 93% in ‘02 vs. 87% in‘03

4) ADSL - both wholesale andretail growing rapidly

5) Bluewin still by far the largestISP and with a market share inADSL access of approx. 57%

6) Access revenues growingpartially at expense of trafficrevenues

Access revenues:CHF 1,715mm (+8.5% YOY)

+8.5%Total

-16.7%-6.6%-10.8%Narrowband Bluewin

+190%+15%+152%ADSL Bluewin

+155%+3.5%+148%ADSL Wholesale

+1.2%-0.2%+1.4%ISDN

+0.3%+2.8%-2.4%PSTN

RevenuesWeightedavg. price

Lines

3. Time to AnalysePart I

17

50

75

100

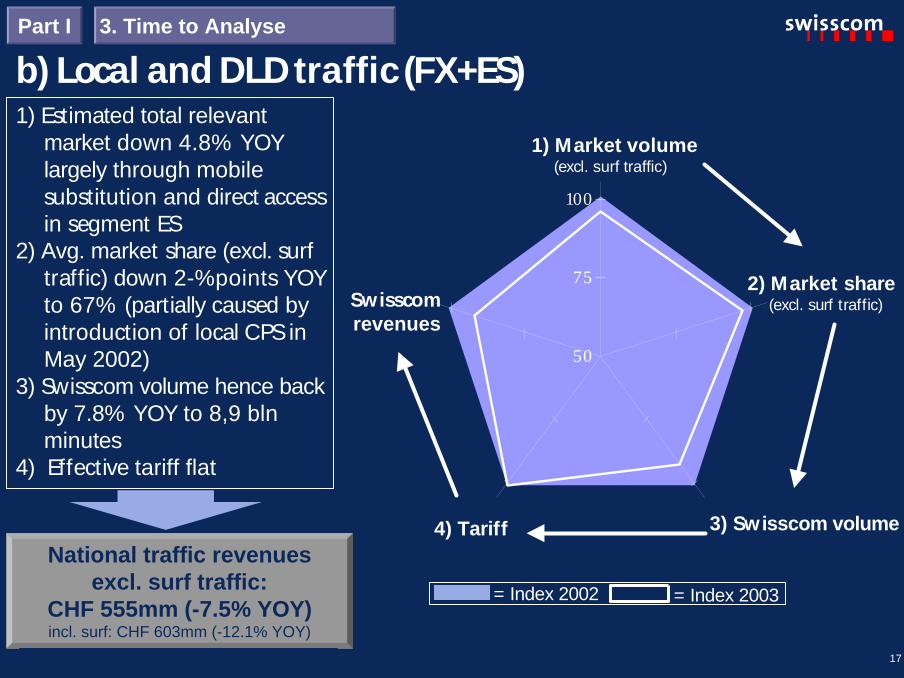

b) Local and DLD traffic (FX+ES)1) Estimated total relevant

market down 4.8% YOYlargely through mobilesubstitution and direct accessin segment ES

2) Avg. market share (excl. surftraffic) down 2-%points YOYto 67% (partially caused byintroduction of local CPS inMay 2002)

3) Swisscom volume hence backby 7.8% YOY to 8,9 blnminutes

4) Effective tariff flat

National traffic revenuesexcl. surf traffic:

CHF 555mm (-7.5% YOY)incl. surf: CHF 603mm (-12.1% YOY)

3. Time to AnalysePart I

Swisscomrevenues

3) Swisscom volume

2) Market share(excl. surf traffic)

1) Market volume(excl. surf traffic)

4) Tariff

= Index 2002 = Index 2003

18

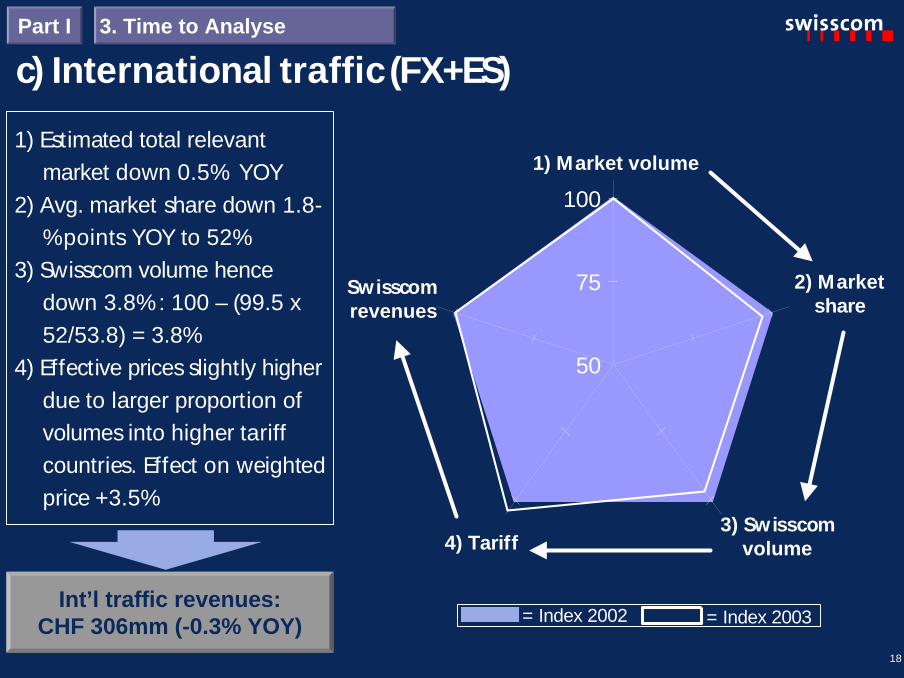

c) International traffic (FX+ES)1) Estimated total relevant

market down 0.5% YOY2) Avg. market share down 1.8-

%points YOY to 52%3) Swisscom volume hence

down 3.8%: 100 – (99.5 x52/53.8) = 3.8%

4) Effective prices slightly higherdue to larger proportion ofvolumes into higher tariffcountries. Effect on weightedprice +3.5%

Int’l traffic revenues:CHF 306mm (-0.3% YOY)

50

75

100

3. Time to AnalysePart I

Swisscomrevenues

3) Swisscomvolume

2) Marketshare

1) Market volume

4) Tariff

= Index 2002 = Index 2003

19

d) F2M traffic (FX+ES)1) Total market up 1% YOY

through higher penetrationMobile

2) Avg. market share up 0.5-%points YOY to 64%

3) Swisscom volume hence up1.5%

4) Avg. tariff 2% lower

F2M traffic revenues:CHF 600mm (-0.7% YOY)

50

75

100

3. Time to AnalysePart I

Swisscomrevenues

3) Swisscomvolume

2) Marketshare

1) Market volume

4) Tariff

= Index 2002 = Index 2003

20

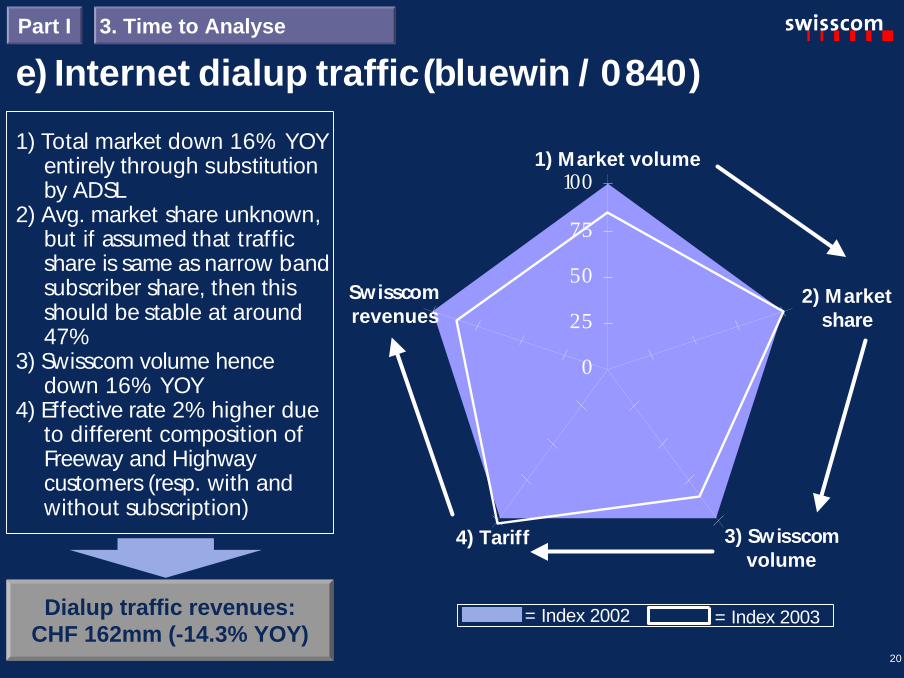

e) Internet dialup traffic (bluewin / 0840)1) Total market down 16% YOY

entirely through substitutionby ADSL

2) Avg. market share unknown,but if assumed that trafficshare is same as narrow bandsubscriber share, then thisshould be stable at around47%

3) Swisscom volume hencedown 16% YOY

4) Effective rate 2% higher dueto different composition ofFreeway and Highwaycustomers (resp. with andwithout subscription)

Dialup traffic revenues:CHF 162mm (-14.3% YOY)

0

25

50

75

100

3. Time to AnalysePart I

Swisscomrevenues

3) Swisscomvolume

2) Marketshare

1) Market volume

4) Tariff

= Index 2002 = Index 2003

21

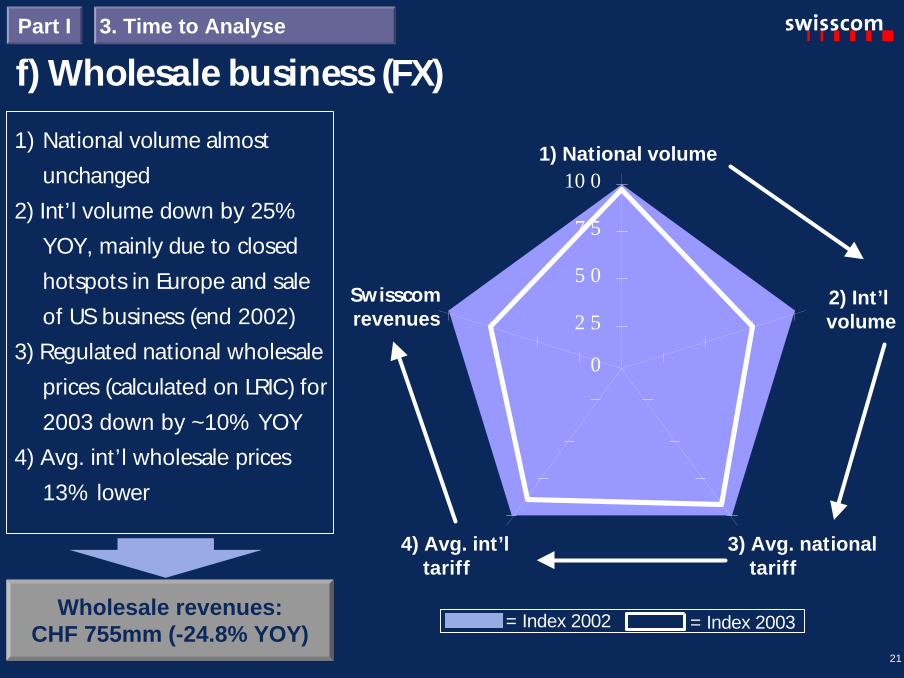

f) Wholesale business (FX)3. Time to AnalysePart I

1) National volume almostunchanged

2) Int’l volume down by 25%YOY, mainly due to closedhotspots in Europe and saleof US business (end 2002)

3) Regulated national wholesaleprices (calculated on LRIC) for2003 down by ~10% YOY

4) Avg. int’l wholesale prices13% lower

Wholesale revenues:CHF 755mm (-24.8% YOY)

Swisscomrevenues

3) Avg. nationaltariff

2) Int’lvolume

1) National volume

4) Avg. int’ltariff

0

2 5

5 0

7 5

10 0

= Index 2002 = Index 2003

22

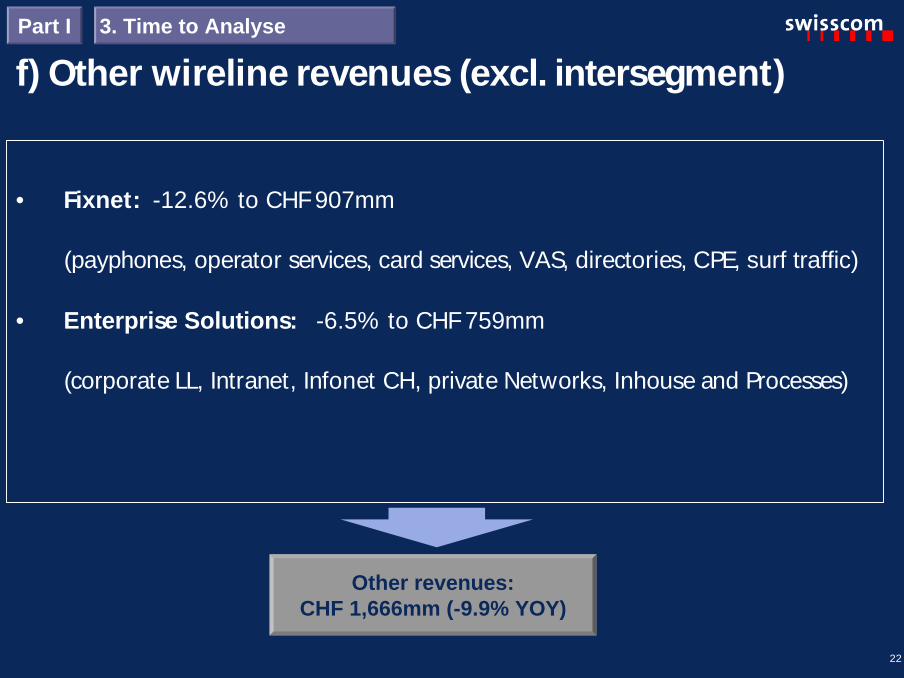

f) Other wireline revenues (excl. intersegment)

• Fixnet: -12.6% to CHF 907mm

(payphones, operator services, card services, VAS, directories, CPE, surf traffic)

• Enterprise Solutions: -6.5% to CHF 759mm

(corporate LL, Intranet, Infonet CH, private Networks, Inhouse and Processes)

Other revenues:CHF 1,666mm (-9.9% YOY)

3. Time to AnalysePart I

23

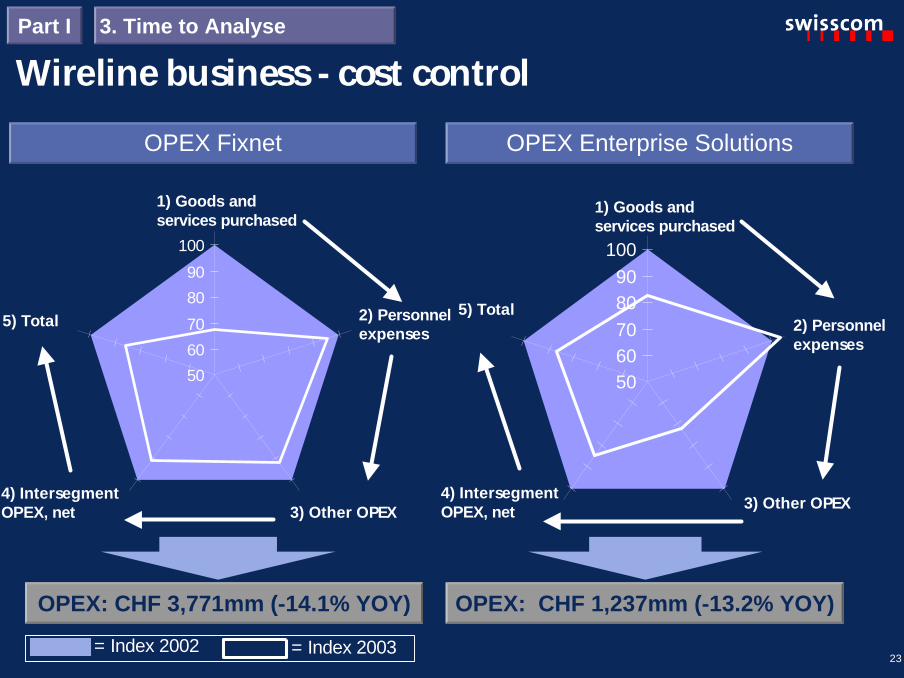

Wireline business - cost control

OPEX: CHF 3,771mm (-14.1% YOY)

OPEX Fixnet

50

60

70

80

90

100

1) Goods andservices purchased

2) Personnelexpenses

3) Other OPEX4) IntersegmentOPEX, net

5) Total

OPEX: CHF 1,237mm (-13.2% YOY)

OPEX Enterprise Solutions

5060708090

100

1) Goods andservices purchased

2) Personnelexpenses

3) Other OPEX4) IntersegmentOPEX, net

5) Total

3. Time to AnalysePart I

= Index 2002 = Index 2003

24

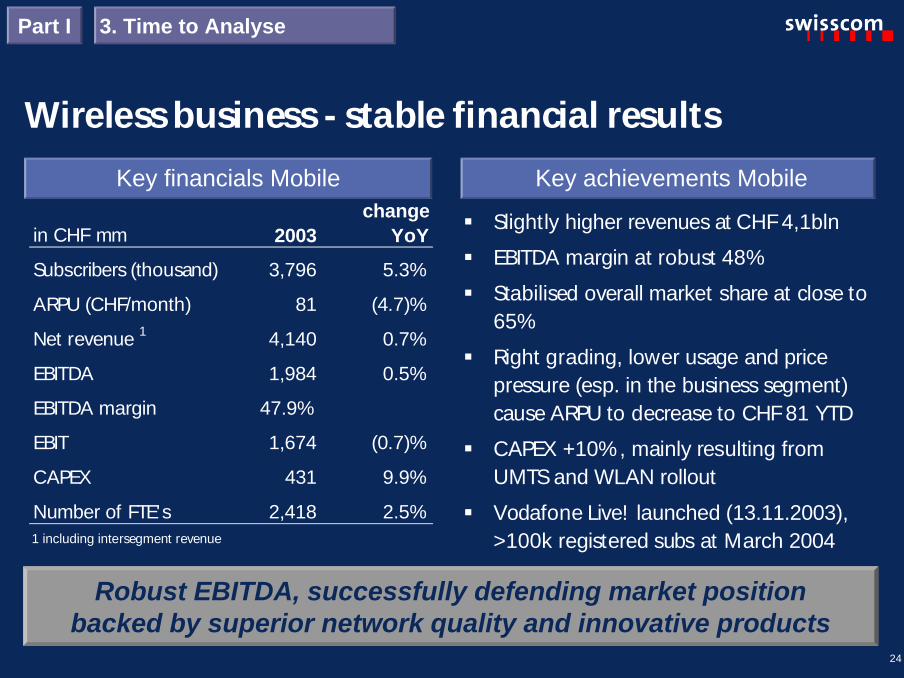

Wireless business - stable financial resultsKey achievements Mobile

Robust EBITDA, successfully defending market positionbacked by superior network quality and innovative products

§ Slightly higher revenues at CHF 4,1bln

§ EBITDA margin at robust 48%

§ Stabilised overall market share at close to65%

§ Right grading, lower usage and pricepressure (esp. in the business segment)cause ARPU to decrease to CHF 81 YTD

§ CAPEX +10%, mainly resulting fromUMTS and WLAN rollout

§ Vodafone Live! launched (13.11.2003),>100k registered subs at March 2004

Key financials Mobile

1 including intersegment revenue

in CHF mm 2003change

YoY

Subscribers (thousand) 3,796 5.3%

ARPU (CHF/month) 81 (4.7)%

Net revenue 1 4,140 0.7%

EBITDA 1,984 0.5%

EBITDA margin 47.9%

EBIT 1,674 (0.7)%

CAPEX 431 9.9%

Number of FTE's 2,418 2.5%

3. Time to AnalysePart I

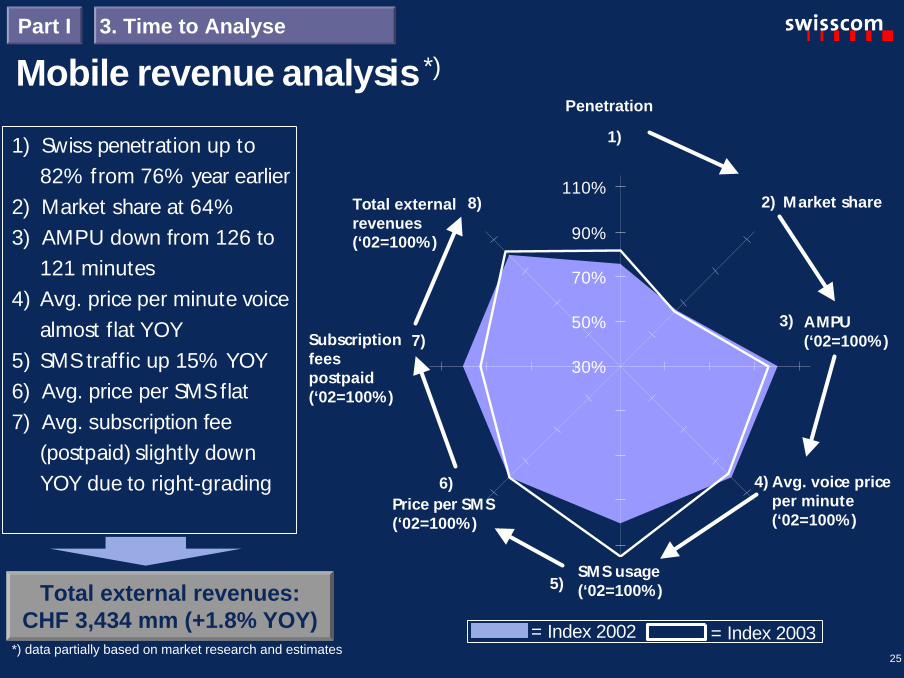

25

1) Swiss penetration up to82% from 76% year earlier

2) Market share at 64%3) AMPU down from 126 to

121 minutes4) Avg. price per minute voice

almost flat YOY5) SMS traffic up 15% YOY6) Avg. price per SMS flat7) Avg. subscription fee

(postpaid) slightly downYOY due to right-grading

Mobile revenue analysis *)

Total external revenues:CHF 3,434 mm (+1.8% YOY)

3. Time to AnalysePart I

30%

50%

70%

90%

110%

Subscriptionfeespostpaid(‘02=100%)

1)

6) 4)

3)

2)

5)

7)

Total externalrevenues(‘02=100%)

Price per SMS(‘02=100%)

8)

Penetration

Market share

AMPU(‘02=100%)

SMS usage(‘02=100%)

Avg. voice priceper minute(‘02=100%)

= Index 2002 = Index 2003*) data partially based on market research and estimates

26

3. Time to AnalysePart I

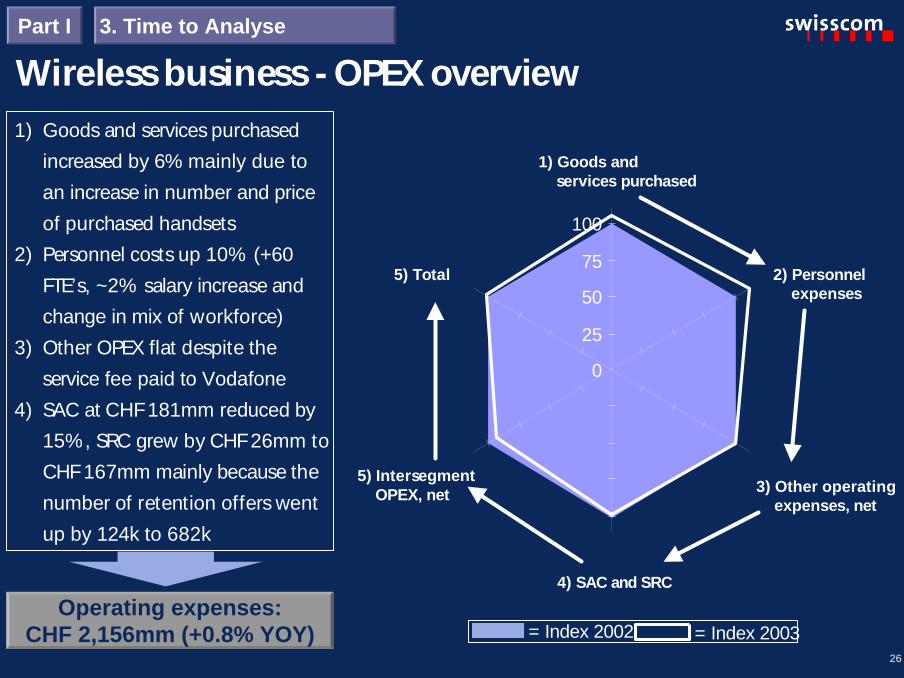

1) Goods and services purchasedincreased by 6% mainly due toan increase in number and priceof purchased handsets

2) Personnel costs up 10% (+60FTE’s, ~2% salary increase andchange in mix of workforce)

3) Other OPEX flat despite theservice fee paid to Vodafone

4) SAC at CHF 181mm reduced by15%, SRC grew by CHF 26mm toCHF 167mm mainly because thenumber of retention offers wentup by 124k to 682k

Operating expenses:CHF 2,156mm (+0.8% YOY)

Wireless business - OPEX overview

0

25

50

75

100

1) Goods andservices purchased

2) Personnelexpenses

3) Other operatingexpenses, net

5) IntersegmentOPEX, net

5) Total

4) SAC and SRC

= Index 2002 = Index 2003

27

Other businesses§ debitel - revenues up 10.8% YOY to CHF 4,555mm (+6.5% in EUR), backed by 571k

new subscribers (mainly postpaid) in Germany. EBITDA margin of 3.0%

§ Swisscom Systems - restructuring program progressing as planned. 510 FTE’s reducedin 2003 to 1,057 FTE’s per YE

§ Swisscom IT Services - restructuring steps led to extra costs and a lower operatingresult in 2003. Planned reduction of workforce by YE 2004: -300 FTE’s

§ Billag - revenues 2003 flat YOY, doubling in 2004 thanks to acquisition of T-Systems’Card Services as per YE 2003

§ SIMAG (real estate company) - restructuring announced, leading to 14% reduction ofworkforce by YE 2004 (-55 FTE’s). Related charges taken in 2003

§ Swisscom Eurospot - secured prime position in Europe’s P-WLAN business within1 year:n 2,000 contracted hotspots in 10 countries, of which 750 operational (March 2004)n operational hotspots are equipped with over 9,000 access pointsn additional coverage through roaming (~1,100 locations)

3. Time to AnalysePart I

28

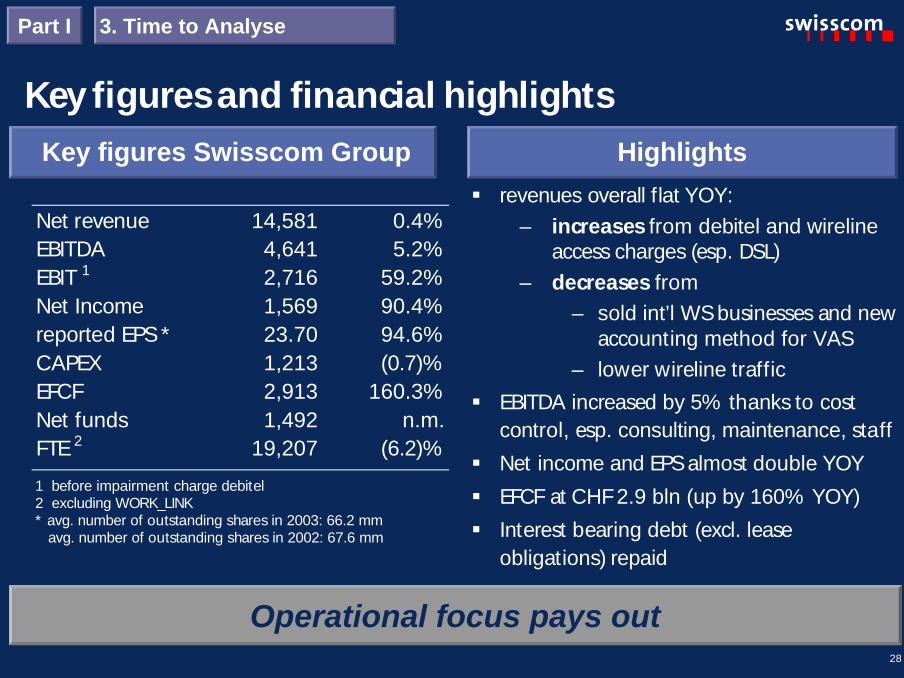

Key figures and financial highlightsKey figures Swisscom Group Highlights

Net revenue 14,581 0.4%EBITDA 4,641 5.2%EBIT 1 2,716 59.2%Net Income 1,569 90.4%reported EPS * 23.70 94.6%CAPEX 1,213 (0.7)%EFCF 2,913 160.3%Net funds 1,492 n.m.FTE2 19,207 (6.2)%

1 before impairment charge debitel2 excluding WORK_LINK* avg. number of outstanding shares in 2003: 66.2 mm

avg. number of outstanding shares in 2002: 67.6 mm

§ revenues overall flat YOY:– increases from debitel and wireline

access charges (esp. DSL)– decreases from

– sold int’l WS businesses and newaccounting method for VAS

– lower wireline traffic§ EBITDA increased by 5% thanks to cost

control, esp. consulting, maintenance, staff

§ Net income and EPS almost double YOY

§ EFCF at CHF 2.9 bln (up by 160% YOY)

§ Interest bearing debt (excl. leaseobligations) repaid

Operational focus pays out

3. Time to AnalysePart I

29

2003 results, conference call24 March 2004

“pay-time”

30

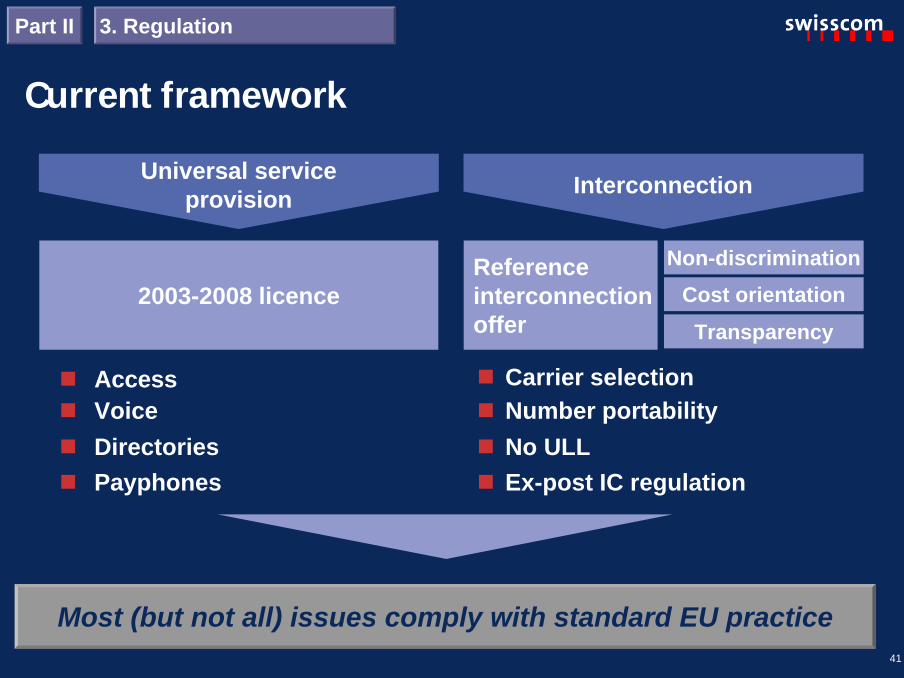

Regulation: update

Handling regulatory pressure remains core competence

Wireline

– LRIC: ComCom (6 November 2003) requiring to reduce IC prices in favourof 2 competitors by 25-35% retroactively for the years 2000-2003; finaldecision of Swiss Federal Court outstanding

– ULL: no final resolution to be expected until 2005/2006

– Access Reselling: obligation to offer access reselling is verified by SwissCompetition Commission

Wireless– Termination tariffs and SMS: are non-regulated tariffs, but are verified by

Swiss Competition Commission

Part I 4. Time to Look Forward

31

Potential sale debitel

§ debitel represents a financial investment

§ Swisscom is currently in discussions for a potential sale

§ debitel’s book value in 2003 further reduced by impairment charge of CHF

280mm, and stands at CHF 848mm as per year-end 2003 (of which CHF 710mm

goodwill)

§ Cumulative Translation Adjustments of CHF 221mm (non-cash) to be expected in

2004 accounts

§ Cash proceeds from a potential sale would add to the EFCF of 2004

4. Time to Look ForwardPart I

32

Telekom AustriaFact:

§ it appears that ÖIAG (representing the Austrian government as single largestshareholder of Telekom Austria) would prefer to sell its stake in the open marketand not in a block trade to a strategic investor

Opinion:§ Swisscom regrets that a deal with ÖIAG does not seem to be possible under

current circumstances§ Swisscom confirms it is still interested in a partnership with Telekom Austria§ Swisscom is of the opinion that a deal could make sense:

– it would represent an option to optimise the capital structure through anindustrial deal

– it would bring an option for further expansion (e.g. in mobile operations inEastern Europe)

– Telekom Austria would have a competent and stable majority partner withsimilar strategic views in a consolidating telecommunication environment

4. Time to Look ForwardPart I

33

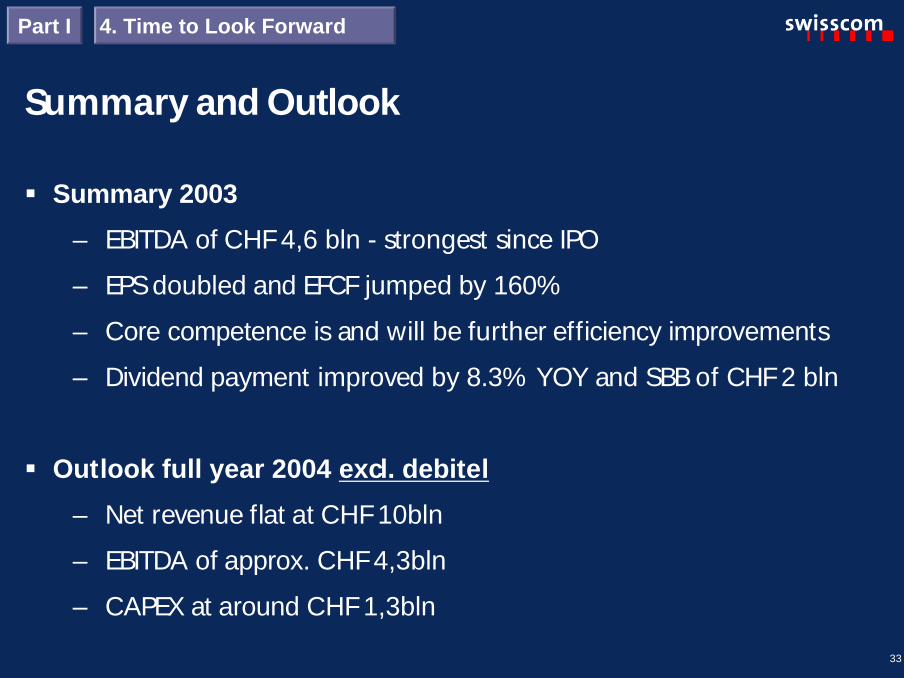

Summary and Outlook

§ Summary 2003

– EBITDA of CHF 4,6 bln - strongest since IPO

– EPS doubled and EFCF jumped by 160%

– Core competence is and will be further efficiency improvements

– Dividend payment improved by 8.3% YOY and SBB of CHF 2 bln

§ Outlook full year 2004 excl. debitel

– Net revenue flat at CHF 10bln

– EBITDA of approx. CHF 4,3bln

– CAPEX at around CHF 1,3bln

4. Time to Look ForwardPart I

34

2003 results, conference call24 March 2004

“pay-time”

35

Thank you for your attention!

Questions & Answers

Please also refer to separate background slidesdetailing the presentation of the key messagesFor further information, please contact:Phone : +41 31 342 6410Fax : +41 31 342 6411Email : [email protected] : www.swisscom.com/ir

5. Time for Q&APart I

36

1. Wireline business

2. Wireless business

3. Regulation

37

40

41

Content Slide

Part II Supporting background information

4. Group financials 42

“pay-time”

37

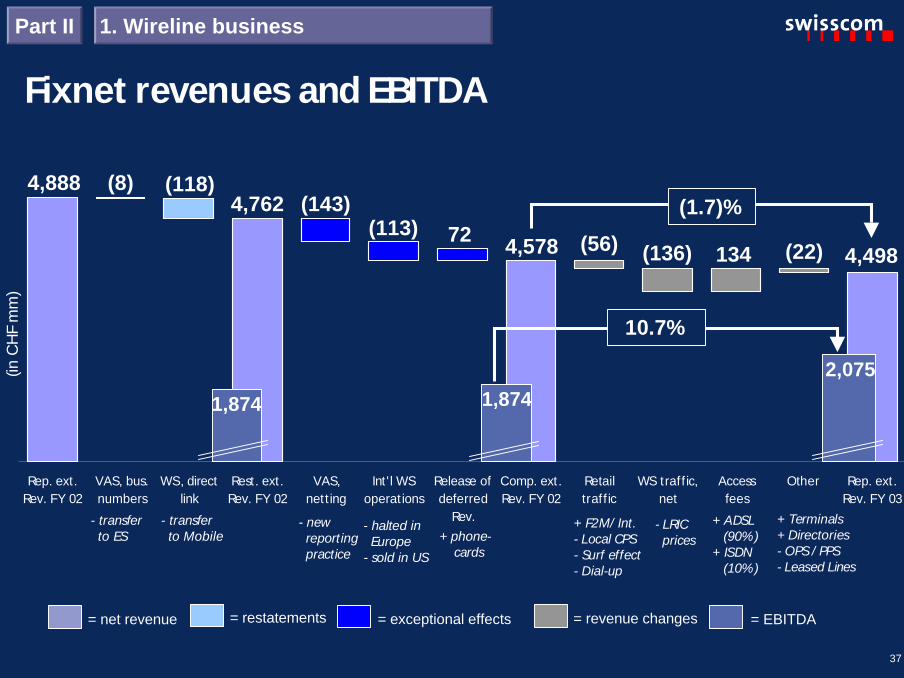

Fixnet revenues and EBITDA

Rep. ext.Rev. FY 02

VAS, bus.numbers

WS, directlink

Rest. ext.Rev. FY 02

VAS,nett ing

Int ' l WSoperat ions

Release ofdeferred

Rev.

Comp. ext.Rev. FY 02

Retailtraff ic

WS traff ic,net

Accessfees

Other Rep. ext.Rev. FY 03

+ ADSL(90%)

+ ISDN(10%)

+ F2M/ Int.- Local CPS- Surf effect- Dial-up

- halted inEurope

- sold in US

+ Terminals+ Directories- OPS / PPS- Leased Lines

- newreportingpractice

- transferto ES

= EBITDA= net revenue = exceptional effects = revenue changes= restatements

(inC

HF

mm

)

- transferto Mobile

1. Wireline businessPart II

- LRICprices+ phone-

cards

4,888 (8) (118)4,762 (143)

(113) 72 4,578 (56) (136) 134 (22) 4,498

(1.7)%

1,874

2,075

10.7%

1,874

38

Fixnet leading Swiss broadband provider

14 19 25 31 371215

1922

29

0

25

50

75

Q4 02 Q1 03 Q2 03 Q3 03 Q4 03

Bluewin Wholesale

Active ADSL subs, cumulativeBroadband revenues, per

quarter

109 140 177 21627486

110

140

167

213

0

100

200

300

400

500

31.12.02 31.3.03 30.6.03 30.9.03 31.12.03

Bluewin Other ISP's

(in CHF mm)(in thousand)

2634

4453

66154%

487

383

317

250195

150%

1. Wireline businessPart II

39

Enterprise Solutions revenues and EBITDA

Rep. ext. Rev. FY02

VAS, bus.Numbers

Rest. ext. Rev. FY02

Traff ic Inhouse &Processes

Networking Other Rep. ext. Rev. FY03

+ transferfrom Fixnet

1. Wireline businessPart II

= EBITDA= net revenue = exceptional effects = revenue changes= restatements

(inC

HF

mm

)

1,365 8 1,373 (58)

(20) (32)(2) 1,261

(8.2)%

97

38.1%

134

40

Mobile revenues and EBITDA

2. Wireless businessPart II

Rep. ext.Rev. FY 02

WS, directlink

Rest. ext.Rev. FY 02

VAS,netting

Release ofdeferred

Rev.

Comp. ext.Rev. FY 02

Voice Data andVAS

Base fees Other Rep. ext.Rev. FY 03

3,255

118 3,37363 (13) 20 3,434

(48)16

1,984

3,348

(inC

HF

mm

)

1,974

2.6%

+ transferfrom Fixnet

= EBITDA= net revenue = exceptional effects = revenue changes= restatements

23

0.5%

- newreportingpractice

1,974

41

n Access n Carrier selectionn Number portabilityn Voice

2003-2008 licence

n Directoriesn Payphones

Referenceinterconnectionoffer

Non-discrimination

Cost orientation

Transparency

n No ULLn Ex-post IC regulation

Most (but not all) issues comply with standard EU practice

Universal serviceprovision Interconnection

Current framework3. RegulationPart II

42

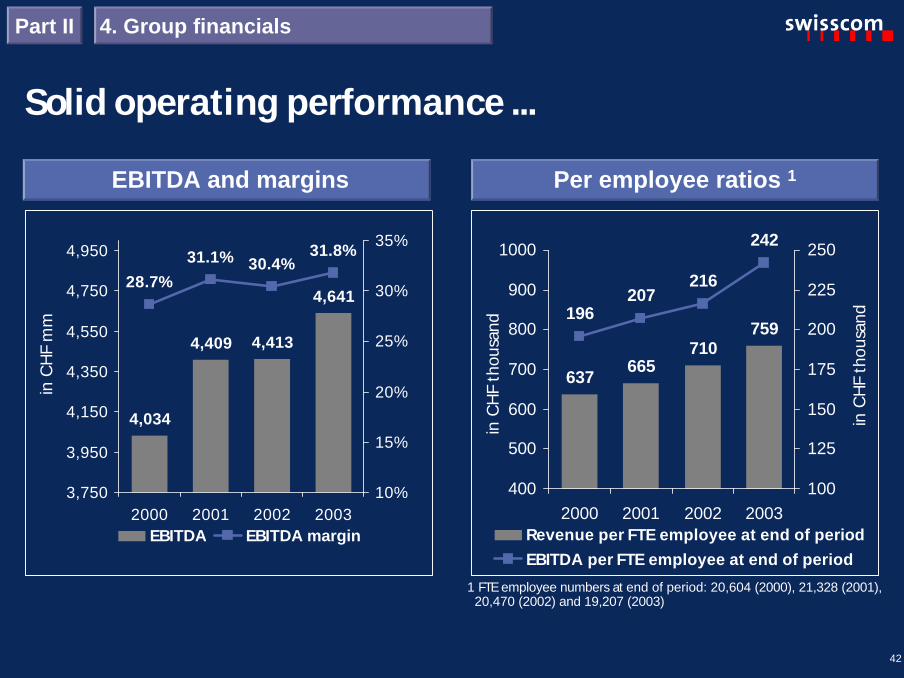

Solid operating performance ...

4,034

4,409 4,413

4,64128.7%

31.1% 30.4%31.8%

3,750

3,950

4,150

4,350

4,550

4,750

4,950

2000 2001 2002 2003

inC

HF

mm

10%

15%

20%

25%

30%

35%

EBITDA EBITDA margin

EBITDA and margins Per employee ratios 1

637665

710759

196207

216

242

400

500

600

700

800

900

1000

2000 2001 2002 2003in

CH

Fth

ousa

nd100

125

150

175

200

225

250

inC

HF

thou

sand

Revenue per FTE employee at end of periodEBITDA per FTE employee at end of period

1 FTE employee numbers at end of period: 20,604 (2000), 21,328 (2001),20,470 (2002) and 19,207 (2003)

Part II 4. Group financials

43

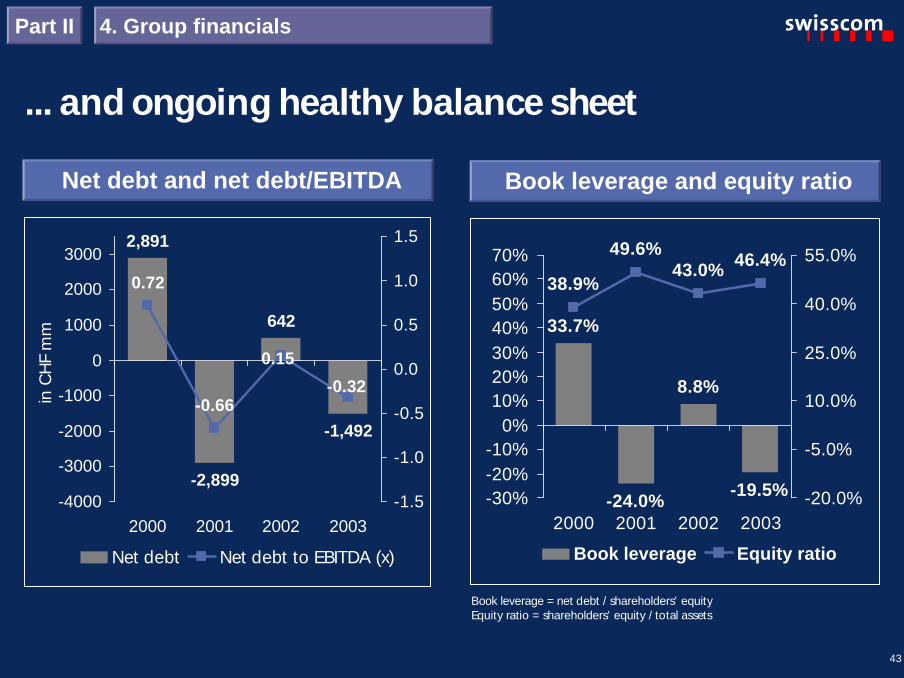

... and ongoing healthy balance sheet

33.7%

-24.0%

8.8%

-19.5%

38.9%

49.6%43.0% 46.4%

-30%-20%-10%

0%10%20%30%40%50%60%70%

2000 2001 2002 2003-20.0%

-5.0%

10.0%

25.0%

40.0%

55.0%

Book leverage Equity ratio

Book leverage and equity ratio

2,891

-2,899

642

-1,492

0.72

-0.66

0.15

-0.32

-4000

-3000

-2000

-1000

0

1000

2000

3000

2000 2001 2002 2003

inC

HF

mm

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Net debt Net debt to EBITDA (x)

Net debt and net debt/EBITDA

Book leverage = net debt / shareholders’ equityEquity ratio = shareholders’ equity / total assets

Part II 4. Group financials

44

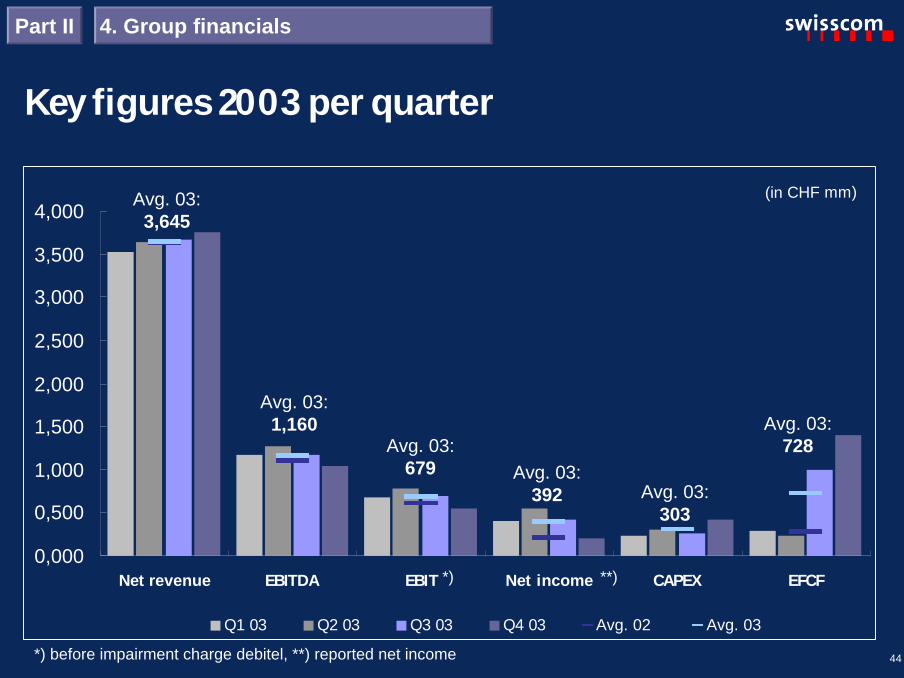

Key figures 2003 per quarter

4. Group financialsPart II

0,000

0,500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Net revenue EBITDA EBIT Net income CAPEX EFCF

Q1 03 Q2 03 Q3 03 Q4 03 Avg. 02 Avg. 03

(in CHF mm)

Avg. 03:1,160

Avg. 03:3,645

Avg. 03:679 Avg. 03:

392 Avg. 03:303

Avg. 03:728

*)

*) before impairment charge debitel, **) reported net income

**)

45

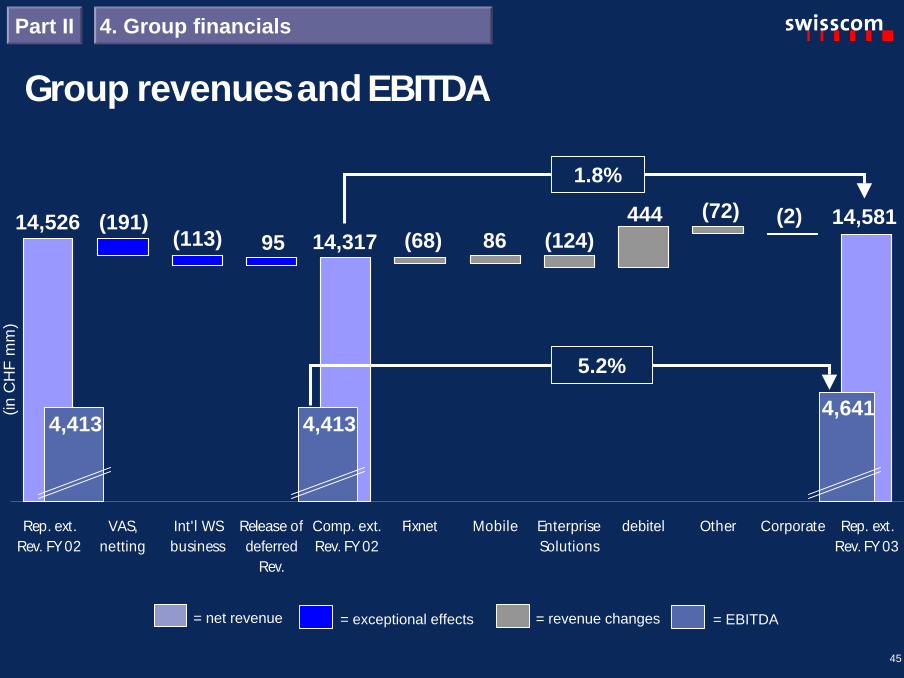

Group revenues and EBITDA

Rep. ext.Rev. FY 02

VAS,netting

Int'l WSbusiness

Release ofdeferred

Rev.

Comp. ext.Rev. FY 02

Fixnet Mobile EnterpriseSolutions

debitel Other Corporate Rep. ext.Rev. FY 03

14,526(113) (68) (124)

444 (72) (2) 14,581

4,4134,641

(191)14,317

4,413

1.8%

(inC

HF

mm

)

= EBITDA= net revenue = exceptional effects = revenue changes

5.2%

8695

4. Group financialsPart II

46

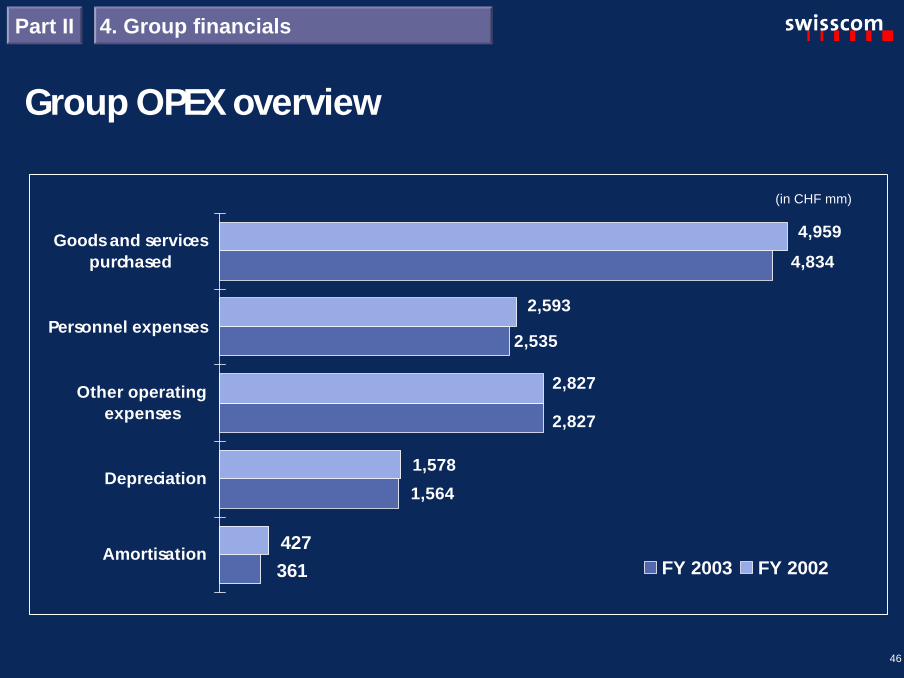

Group OPEX overview

2,535

4,834

2,827

1,564

4,959

2,827

2,593

1,578

Amortisation

Depreciation

Other operatingexpenses

Personnel expenses

Goods and servicespurchased

FY 2003 FY 2002

(in CHF mm)

Part II 4. Group financials

427361

47

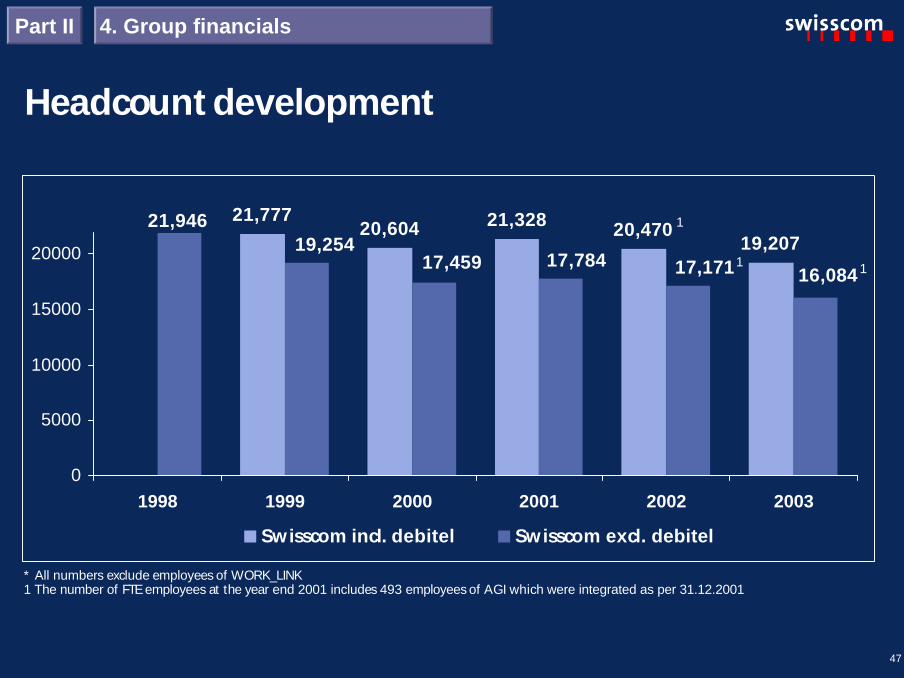

Headcount development

21,77720,604 21,328 20,470

19,207

16,084

21,946

17,17117,78417,45919,254

0

5000

10000

15000

20000

1998 1999 2000 2001 2002 2003

Swisscom incl. debitel Swisscom excl. debitel

1

1

* All numbers exclude employees of WORK_LINK1 The number of FTE employees at the year end 2001 includes 493 employees of AGI which were integrated as per 31.12.2001

Part II 4. Group financials

1

48

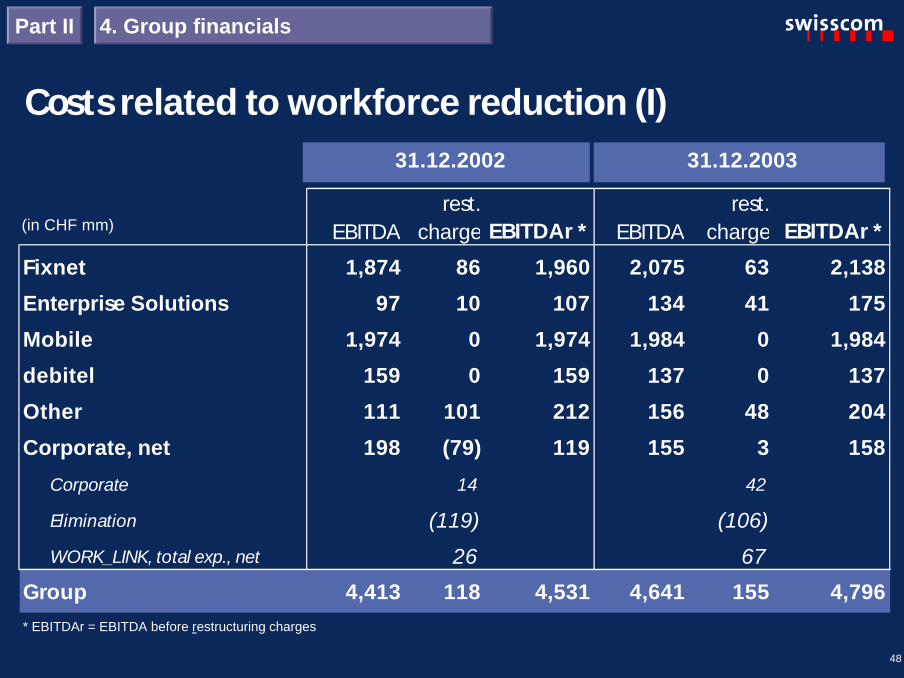

Costs related to workforce reduction (I)

EBITDArest.

charge EBITDAr * EBITDArest.

charge EBITDAr *

Fixnet 1,874 86 1,960 2,075 63 2,138

Enterprise Solutions 97 10 107 134 41 175

Mobile 1,974 0 1,974 1,984 0 1,984

debitel 159 0 159 137 0 137

Other 111 101 212 156 48 204

Corporate, net 198 (79) 119 155 3 158

Corporate 14 42

Elimination (119) (106)

WORK_LINK, total exp., net 26 67

Group 4,413 118 4,531 4,641 155 4,796

31.12.2002 31.12.2003

* EBITDAr = EBITDA before restructuring charges

(in CHF mm)

Part II 4. Group financials

49

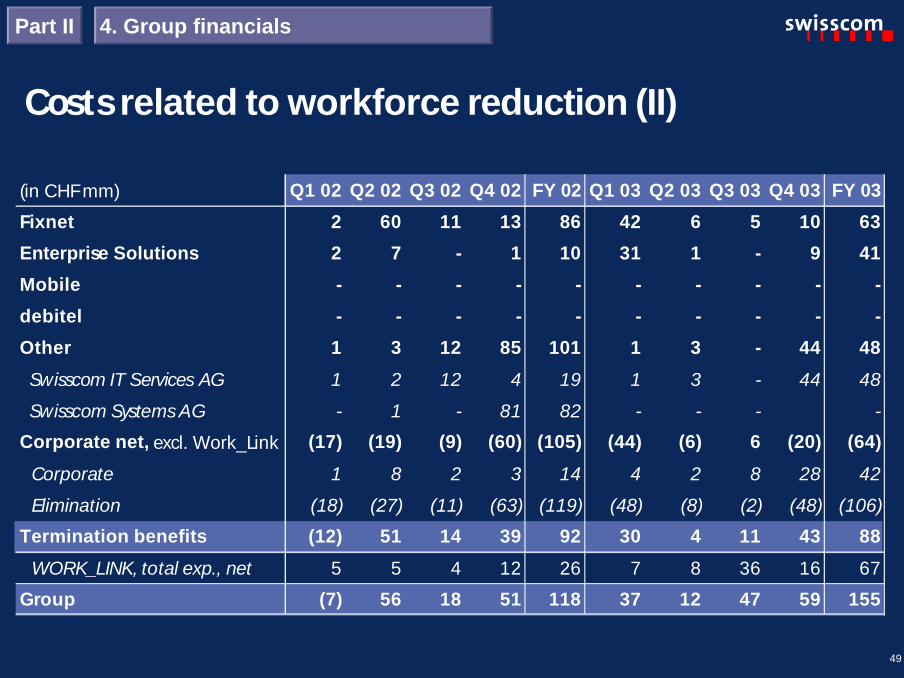

Costs related to workforce reduction (II)

Part II 4. Group financials

(in CHF mm) Q1 02 Q2 02 Q3 02 Q4 02 FY 02 Q1 03 Q2 03 Q3 03 Q4 03 FY 03

Fixnet 2 60 11 13 86 42 6 5 10 63

Enterprise Solutions 2 7 - 1 10 31 1 - 9 41

Mobile - - - - - - - - - -

debitel - - - - - - - - - -

Other 1 3 12 85 101 1 3 - 44 48

Swisscom IT Services AG 1 2 12 4 19 1 3 - 44 48

Swisscom Systems AG - 1 - 81 82 - - - -

Corporate net, excl. Work_Link (17) (19) (9) (60) (105) (44) (6) 6 (20) (64)

Corporate 1 8 2 3 14 4 2 8 28 42

Elimination (18) (27) (11) (63) (119) (48) (8) (2) (48) (106)

Termination benefits (12) 51 14 39 92 30 4 11 43 88

WORK_LINK, total exp., net 5 5 4 12 26 7 8 36 16 67

Group (7) 56 18 51 118 37 12 47 59 155

50

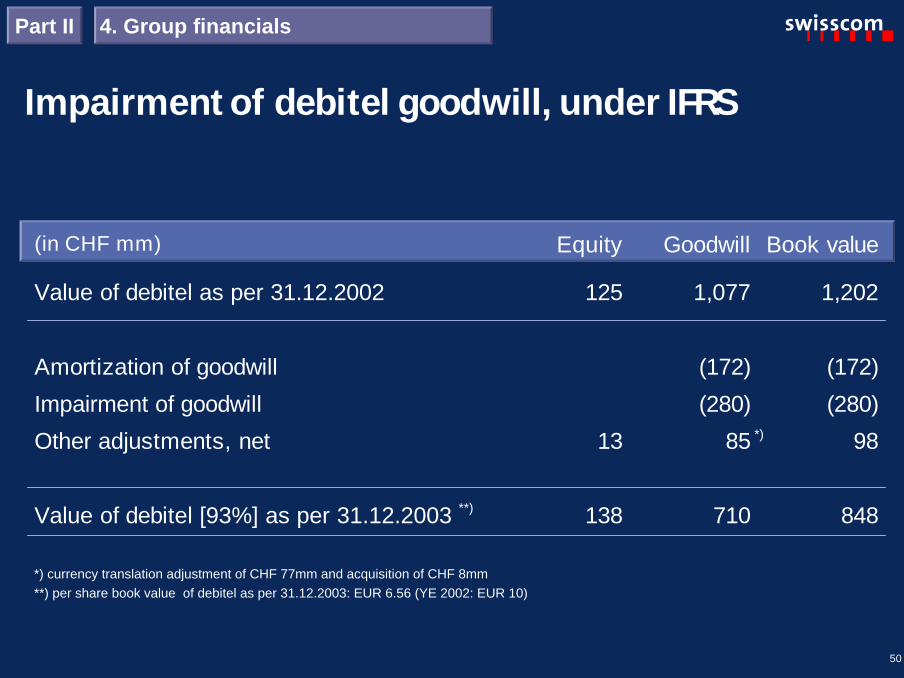

Impairment of debitel goodwill, under IFRS

(in CHF mm) Equity Goodwill Book value

Value of debitel as per 31.12.2002 125 1,077 1,202

Amortization of goodwill (172) (172)

Impairment of goodwill (280) (280)

Other adjustments, net 13 85 98

Value of debitel [93%] as per 31.12.2003 138 710 848

Part II 4. Group financials

*) currency translation adjustment of CHF 77mm and acquisition of CHF 8mm**) per share book value of debitel as per 31.12.2003: EUR 6.56 (YE 2002: EUR 10)

*)

**)

51

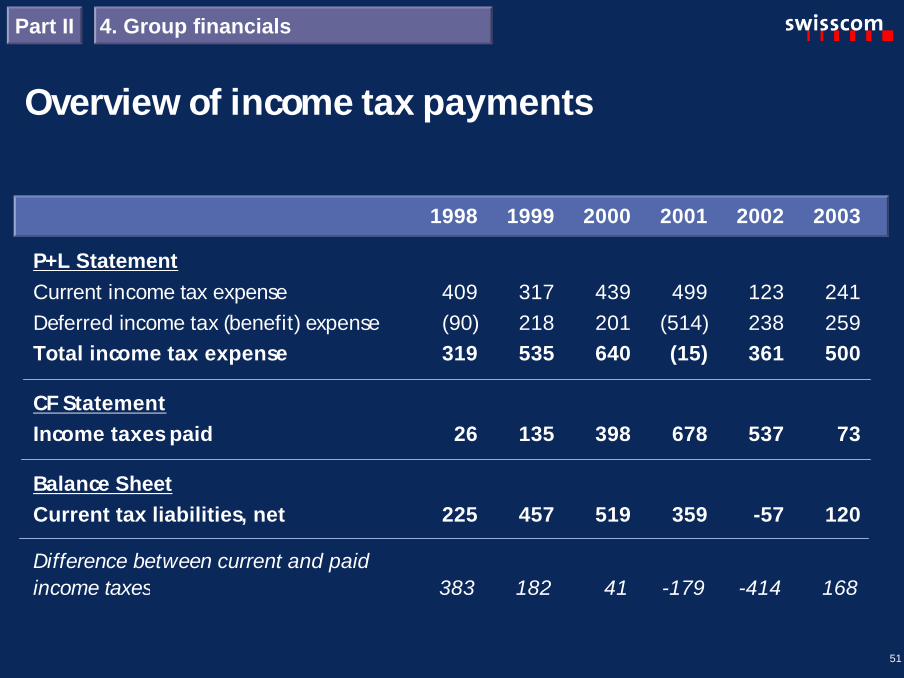

Overview of income tax payments

1998 1999 2000 2001 2002 2003

P+L StatementCurrent income tax expense 409 317 439 499 123 241Deferred income tax (benefit) expense (90) 218 201 (514) 238 259Total income tax expense 319 535 640 (15) 361 500

CF StatementIncome taxes paid 26 135 398 678 537 73

Balance SheetCurrent tax liabilities, net 225 457 519 359 -57 120

Difference between current and paidincome taxes 383 182 41 -179 -414 168

Part II 4. Group financials

52

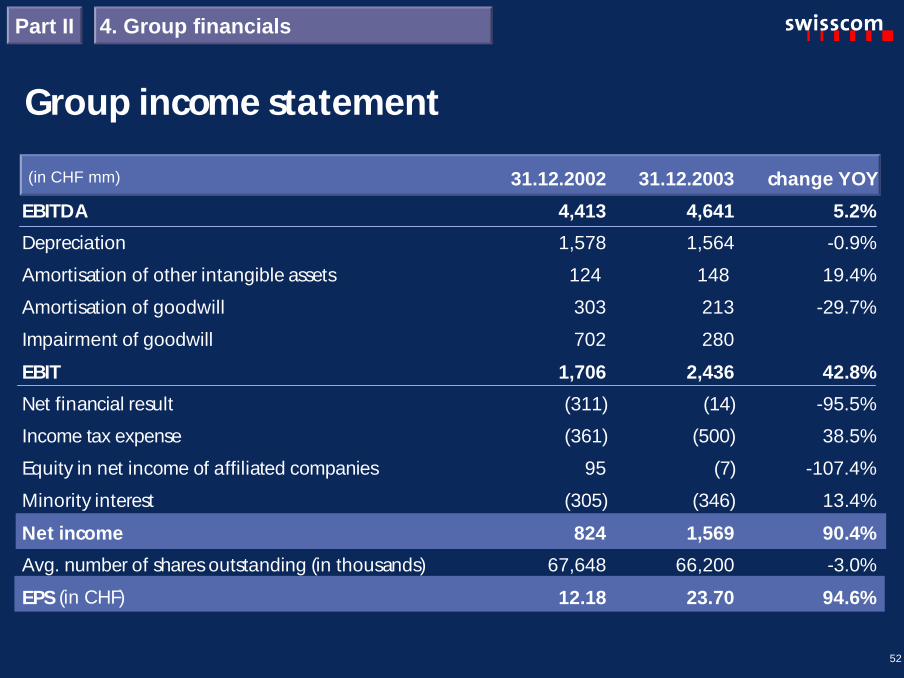

Group income statement31.12.2002 31.12.2003 change YOY

EBITDA 4,413 4,641 5.2%

Depreciation 1,578 1,564 -0.9%

Amortisation of other intangible assets 124 148 19.4%

Amortisation of goodwill 303 213 -29.7%

Impairment of goodwill 702 280

EBIT 1,706 2,436 42.8%

Net financial result (311) (14) -95.5%

Income tax expense (361) (500) 38.5%

Equity in net income of affiliated companies 95 (7) -107.4%

Minority interest (305) (346) 13.4%

Net income 824 1,569 90.4%

Avg. number of shares outstanding (in thousands) 67,648 66,200 -3.0%

EPS (in CHF) 12.18 23.70 94.6%

(in CHF mm)

Part II 4. Group financials

53

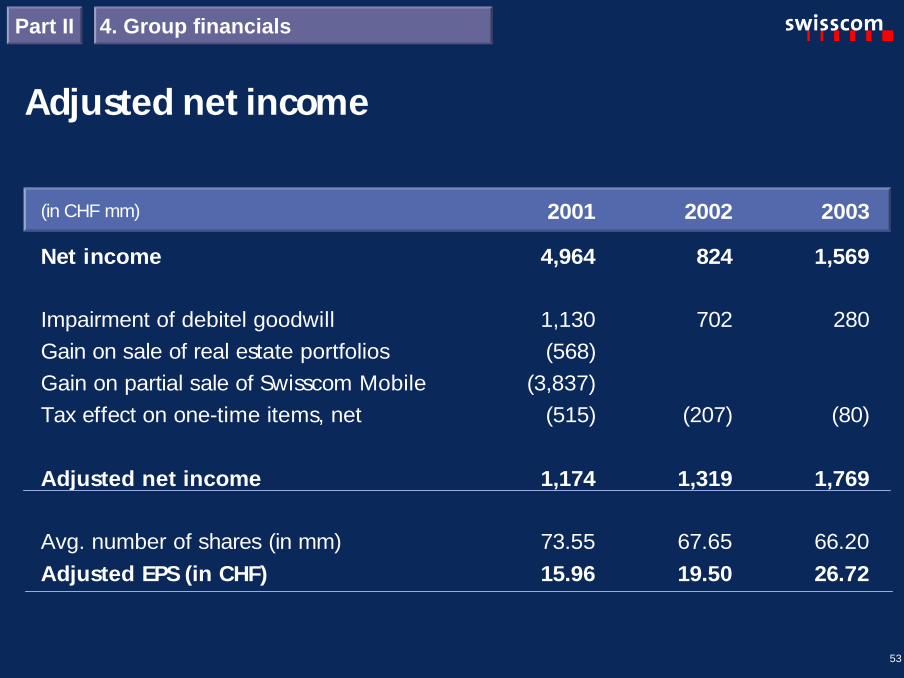

Adjusted net income

(in CHF mm) 2001 2002 2003

Net income 4,964 824 1,569

Impairment of debitel goodwill 1,130 702 280Gain on sale of real estate portfolios (568)Gain on partial sale of Swisscom Mobile (3,837)Tax effect on one-time items, net (515) (207) (80)

Adjusted net income 1,174 1,319 1,769

Avg. number of shares (in mm) 73.55 67.65 66.20Adjusted EPS (in CHF) 15.96 19.50 26.72

Part II 4. Group financials

54

CAPEX analysis

CAPEX developmentfor group without debitel

1,3911,168 1,154 1,165

13.8%

11.2% 11.5% 11.6%

0

500

1000

1500

2000

2500

2000 2001 2002 2003

inC

HF

mm

0%

3%

5%

8%

10%

13%

15%

CAPEX CAPEX/net revenue

1,213 1,165

583431

8.3%

11.6%10.4%10.0%

0

250

500

750

1000

1250

totalgroup

groupexcl.

debitel

Fixnet Mobilein

CH

Fm

m0.0%

2.0%

4.0%6.0%

8.0%

10.0%

12.0%14.0%

16.0%

CAPEXCAPEX/net revenueCAPEX/revenue incl. intersegment

CAPEX 2003

Part II 4. Group financials

55

Change of net debt / net funds

(1,213)CAPEX

Net cash providedby operating activities

4,732

Net debt31.12.02

642

(393)Dividendspaid to

minorities

Net funds31.12.03

1,492(794)Dividends

Par valuereduction

(530)

(in CHF mm)

Part II 4. Group financials

Proceedsfrom

CT sale510

Other(178)

56

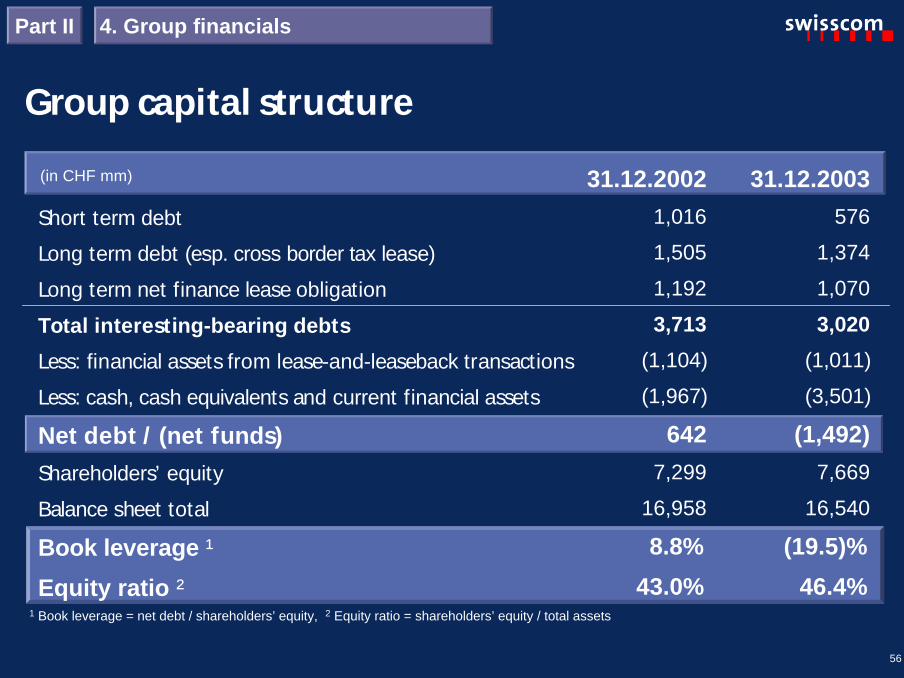

Group capital structure

Short term debt

Long term debt (esp. cross border tax lease)

Long term net finance lease obligation

Total interesting-bearing debts

Less: financial assets from lease-and-leaseback transactions

Less: cash, cash equivalents and current financial assets

Net debt / (net funds)Shareholders’ equity

Balance sheet total

Book leverage ¹

Equity ratio ²

31.12.20021,016

1,505

1,192

3,713

(1,104)

(1,967)

6427,299

16,958

8.8%

43.0%

31.12.2003576

1,374

1,070

3,020

(1,011)

(3,501)

(1,492)7,669

16,540

(19.5)%

46.4%1 Book leverage = net debt / shareholders’ equity, 2 Equity ratio = shareholders’ equity / total assets

(in CHF mm)

Part II 4. Group financials

57

(in CHF mm)Shareholders'

equitySwisscom AG

Sharecapital

non-distributable

reserves

distri- butablereserves

31.12.2002 before 2002 profit distribution 5,216 596 119 4,501Dividend in 2003 (794) (794)PVR paid in 2003 (530) (530) (106) 106Net income under Swiss GAAP 1,154 1,154

31.12.2003 before 2003 profit distribution 5,046 66 13 4,967Dividend in 2004 (861) (861)Share buyback in 2004 (2,000) (2,000)

After 2003 profit distribution, before 2004profits 2,185 66 13 2,106

Distributable reserves as per YE 2003Part II 4. Group financials

58

”This communication contains statements that constitute "forward-looking statements". In thiscommunication, such forward-looking statements include, without limitation, statements relating to ourfinancial condition, results of operations and business and certain of our strategic plans and objectives.

Because these forward-looking statements are subject to risks and uncertainties, actual future resultsmay differ materially from those expressed in or implied by the statements. Many of these risks anduncertainties relate to factors which are beyond Swisscom’s ability to control or estimate precisely, suchas future market conditions, currency fluctuations, the behaviour of other market participants, the actionsof governmental regulators and other risk factors detailed in Swisscom’s past and future filings andreports filed with SWX Swiss Exchange and the U.S. Securities and Exchange Commission and postedon our websites.

Readers are cautioned not to put undue reliance on forward-looking statements, which speak only of thedate of this communication.

Swisscom disclaims any intention or obligation to update and revise any forward-looking statements,whether as a result of new information, future events or otherwise.”

Cautionary statementregarding forward-looking statements

2003 results, conference call24 March 2004