future of mobility: corporate carsharing

TRANSCRIPT

Future of Mobility: Corporate CarsharingFuture of Mobility: Corporate Carsharing

Continued Growth in Traditional Carsharing & Fleet Markets Leading to Continued Growth in Traditional Carsharing & Fleet Markets Leading to Convergence & New Mobility Business Models such as Corporate Convergence & New Mobility Business Models such as Corporate

CarsharingCarsharing

Martyn BriggsProgramme Manager, MobilityAutomotive & Transportation

18th March 2014

© 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

2

Today’s Presenter

Bio: Experienced Automotive & Transportation consultant and Project Manager, responsible for Frost & Sullivan’s Mobility Research & Consulting initiatives. I have over 8 years of relevant experience in urban mobility, transportation policy, strategy and evaluation in particular.

Specialties: Urban Mobility & New Mobility Business Models, Smarter Transport, Intelligent Transport Services, Transport Economics

Particular expertise in: Carsharing, Mobility Integration, Demand Responsive Mobility, Transport & Mobility Policies, Transport Planning, Behavioural Changeand Transport Scheme Appraisal

Martyn Briggs, Programme Manager – Mobility Frost & Sullivan

http://www.linkedin.com/pub/martyn-briggs/24/346/76b

http://twitter.com/BriggsMartyn

http://twitter.com/frost_sullivanhttp://twitter.com/FS_Automotive

3

Poll Question

What do you think was the highest growing carsharing market 2012-2013?

A.Germany

B.France

C.USA

D.UK

E.Italy

4

Focus Points of Our Presentation Today

1. Growth in the Global Carsharing Market

2. Convergence of Carsharing, car rental, and fleet leasing

3. Definition of Corporate Carsharing – What’s included & Excluded

4. Key Drivers & Challenges Impacting Corporate Carsharing Growth

5. Key Corporate Carsharing Players

6. Industry Convergence Opportunity

7. Key Growth Forecasts

8. Corporate Carsharing Outlook 2014

9. Annual Urban Mobility Workshop

5

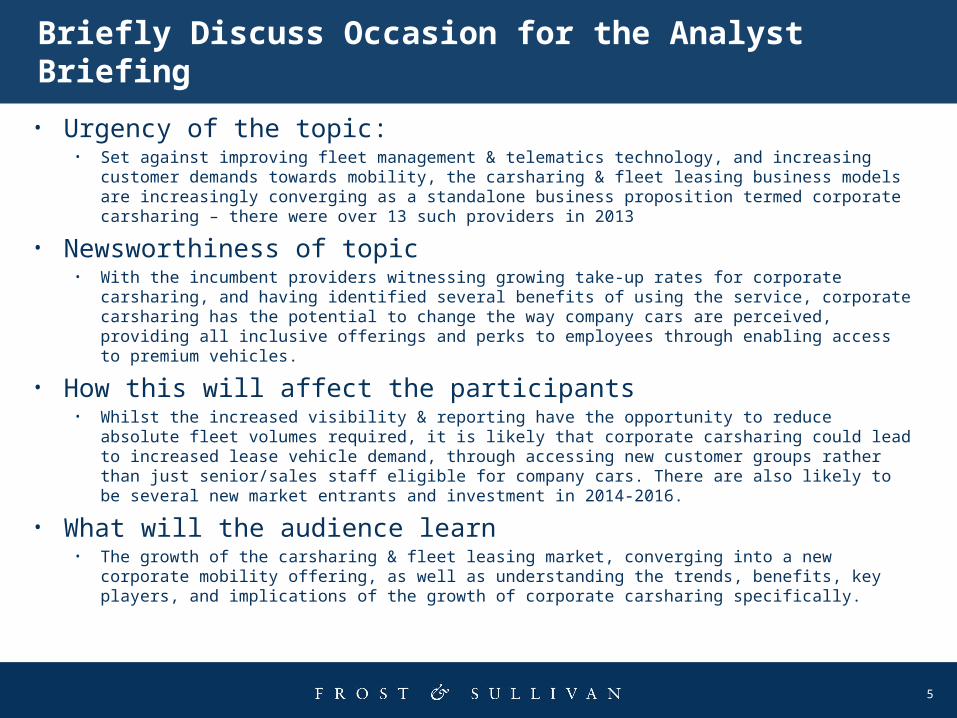

Briefly Discuss Occasion for the Analyst Briefing

• Urgency of the topic: • Set against improving fleet management & telematics technology, and increasing customer demands

towards mobility, the carsharing & fleet leasing business models are increasingly converging as a standalone business proposition termed corporate carsharing – there were over 13 such providers in 2013

• Newsworthiness of topic• With the incumbent providers witnessing growing take-up rates for corporate carsharing, and having

identified several benefits of using the service, corporate carsharing has the potential to change the way company cars are perceived, providing all inclusive offerings and perks to employees through enabling access to premium vehicles.

• How this will affect the participants• Whilst the increased visibility & reporting have the opportunity to reduce absolute fleet volumes

required, it is likely that corporate carsharing could lead to increased lease vehicle demand, through accessing new customer groups rather than just senior/sales staff eligible for company cars. There are also likely to be several new market entrants and investment in 2014-2016.

• What will the audience learn• The growth of the carsharing & fleet leasing market, converging into a new corporate mobility

offering, as well as understanding the trends, benefits, key players, and implications of the growth of corporate carsharing specifically.

6

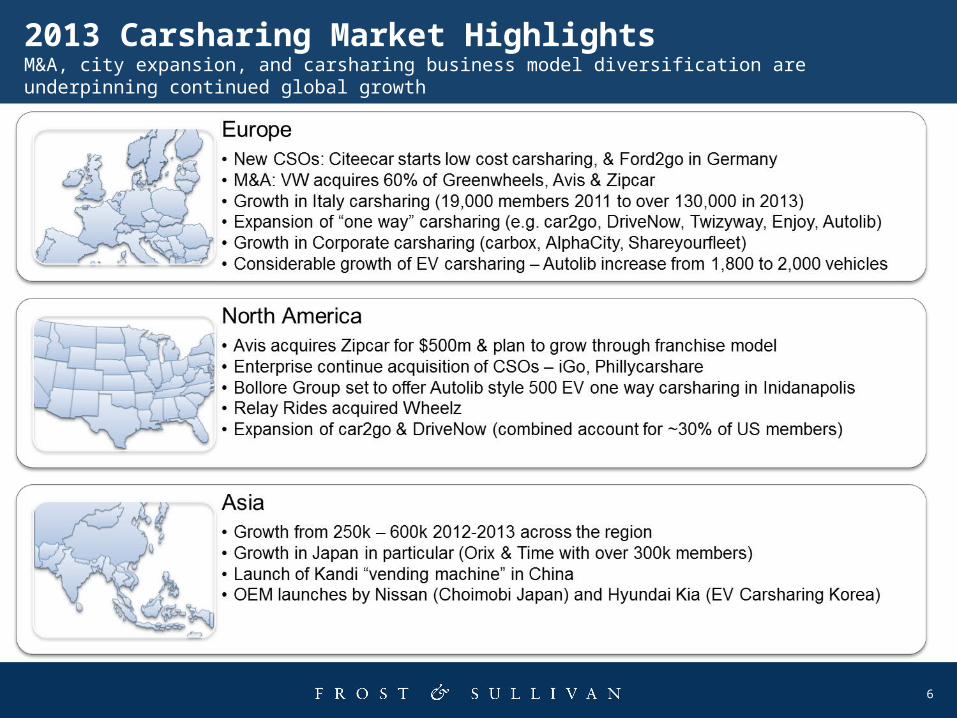

2013 Carsharing Market HighlightsM&A, city expansion, and carsharing business model diversification are underpinning continued global growth

7

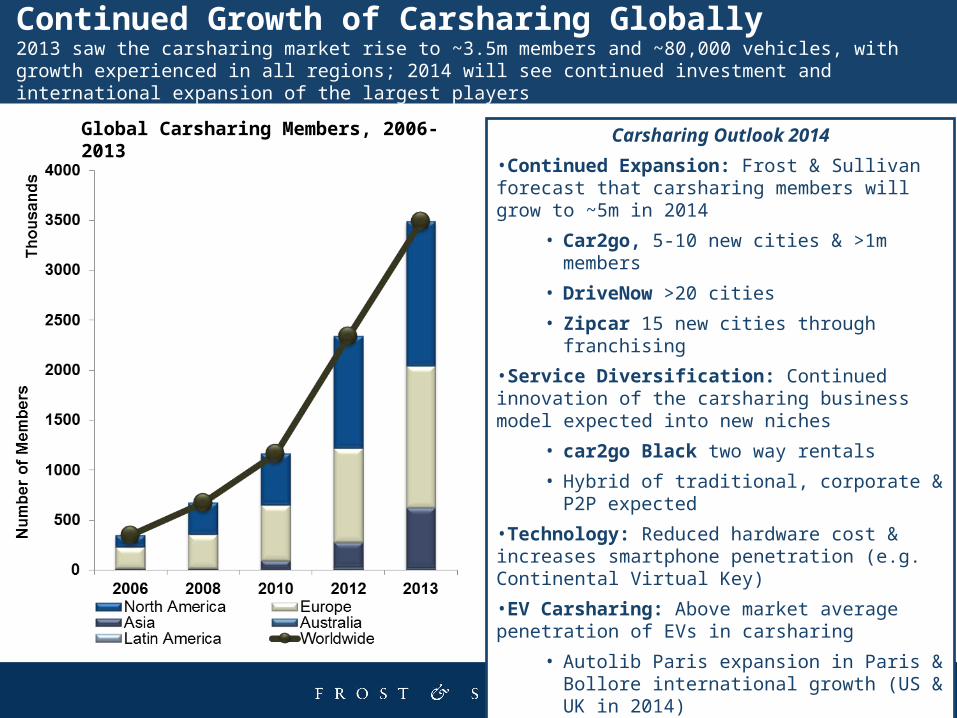

Continued Growth of Carsharing Globally2013 saw the carsharing market rise to ~3.5m members and ~80,000 vehicles, with growth experienced in all regions; 2014 will see continued investment and international expansion of the largest players

Global Carsharing Members, 2006-2013 Carsharing Outlook 2014

•Continued Expansion: Frost & Sullivan forecast that carsharing members will grow to ~5m in 2014

• Car2go, 5-10 new cities & >1m members

• DriveNow >20 cities

• Zipcar 15 new cities through franchising

•Service Diversification: Continued innovation of the carsharing business model expected into new niches

• car2go Black two way rentals

• Hybrid of traditional, corporate & P2P expected

•Technology: Reduced hardware cost & increases smartphone penetration (e.g. Continental Virtual Key)

•EV Carsharing: Above market average penetration of EVs in carsharing

• Autolib Paris expansion in Paris & Bollore international growth (US & UK in 2014)

8

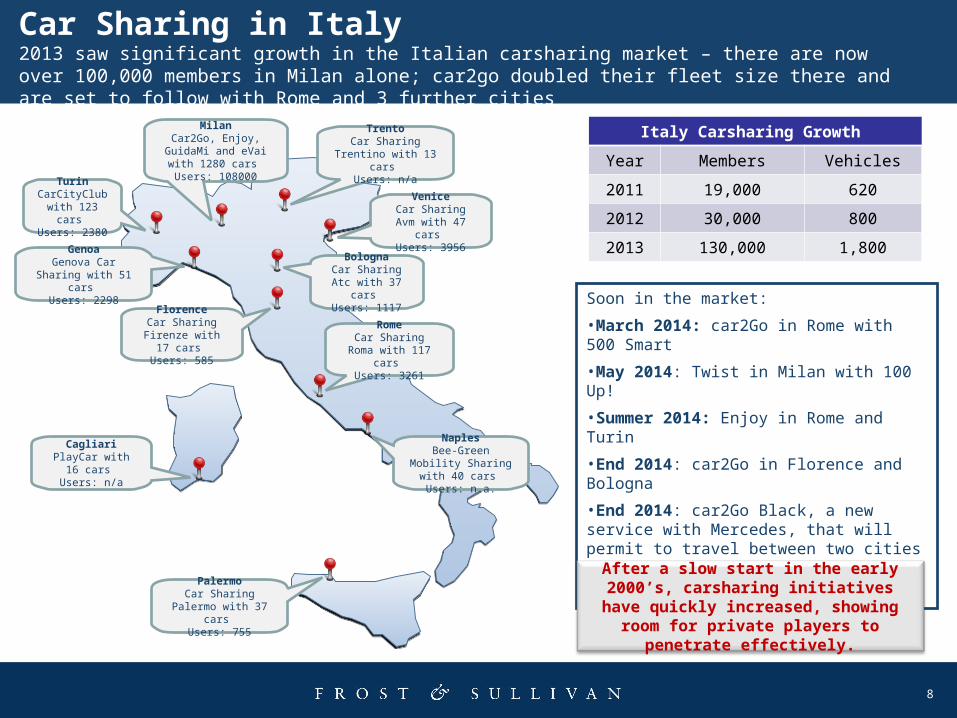

Car Sharing in Italy2013 saw significant growth in the Italian carsharing market – there are now over 100,000 members in Milan alone; car2go doubled their fleet size there and are set to follow with Rome and 3 further cities

TurinCarCityClub

with 123 cars Users: 2380

VeniceCar Sharing Avm

with 47 cars Users: 3956

BolognaCar Sharing Atc

with 37 cars Users: 1117

GenoaGenova Car Sharing

with 51 cars Users: 2298

RomeCar Sharing Roma

with 117 cars Users: 3261

NaplesBee-Green Mobility

Sharing with 40 cars Users: n.a.

PalermoCar Sharing Palermo

with 37 cars Users: 755

MilanCar2Go, Enjoy,

GuidaMi and eVai with 1280 cars

Users: 108000

Soon in the market:

•March 2014: car2Go in Rome with 500 Smart

•May 2014: Twist in Milan with 100 Up!

•Summer 2014: Enjoy in Rome and Turin

•End 2014: car2Go in Florence and Bologna

•End 2014: car2Go Black, a new service with Mercedes, that will permit to travel between two cities where car2Go is present

•Late2014/2015: car2Go in Genoa

After a slow start in the early 2000’s, carsharing initiatives have quickly

increased, showing room for private players to penetrate effectively.

TrentoCar Sharing Trentino

with 13 cars Users: n/a

CagliariPlayCar with 16

cars Users: n/a

FlorenceCar Sharing

Firenze with 17 cars

Users: 585

Italy Carsharing Growth

Year Members Vehicles

2011 19,000 620

2012 30,000 800

2013 130,000 1,800

9

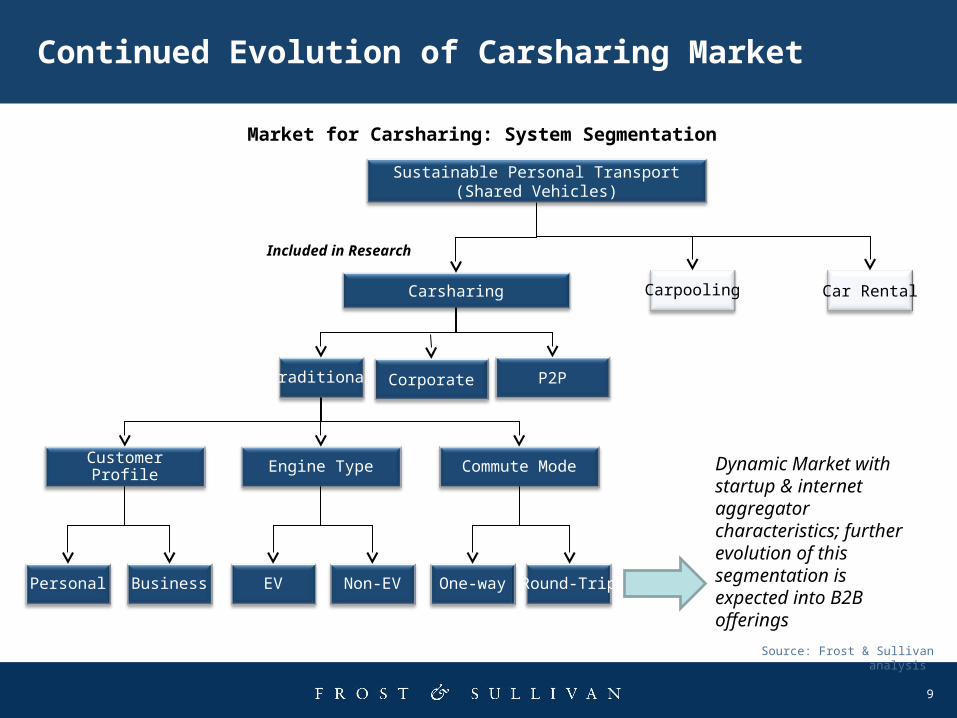

Continued Evolution of Carsharing Market

Source: Frost & Sullivan analysis

Traditional

Carsharing

Customer Profile Engine Type

P2P

Personal Business EV Non-EV

Commute Mode

One-way Round-Trip

Carpooling Car Rental

Sustainable Personal Transport(Shared Vehicles)

Market for Carsharing: System Segmentation

Included in Research

Dynamic Market with startup & internet aggregator characteristics; further evolution of this segmentation is expected into B2B offerings

Corporate

10

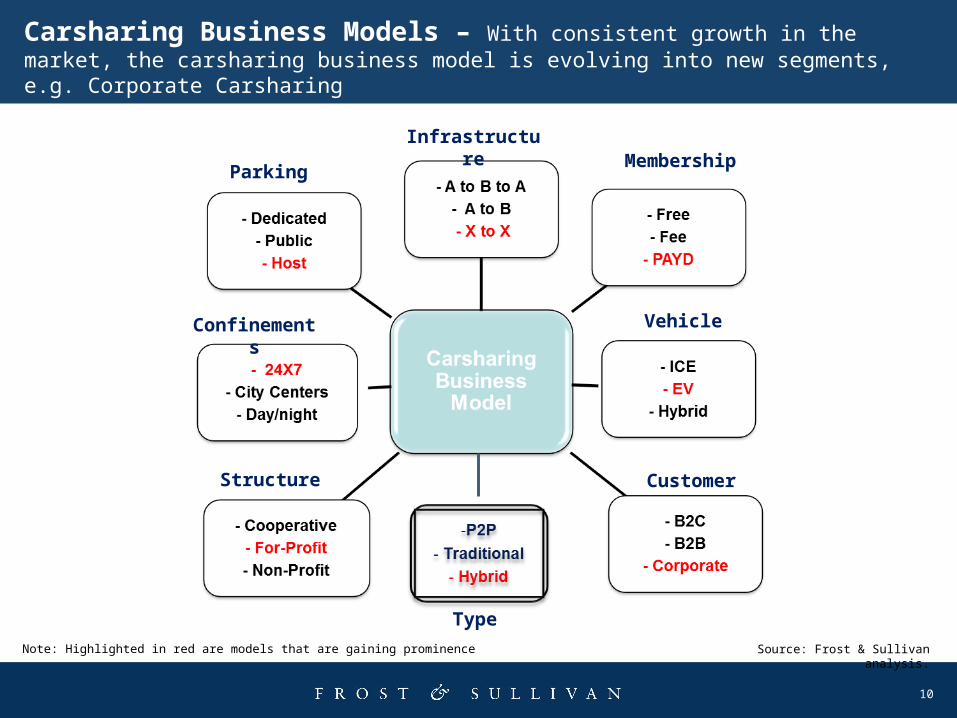

Carsharing Business Models – With consistent growth in the market, the carsharing business model is evolving into new segments, e.g. Corporate Carsharing

Vehicle

Infrastructure

Parking

Structure

Membership

Customer

Confinements

Type

Source: Frost & Sullivan analysis.Note: Highlighted in red are models that are gaining prominence

11

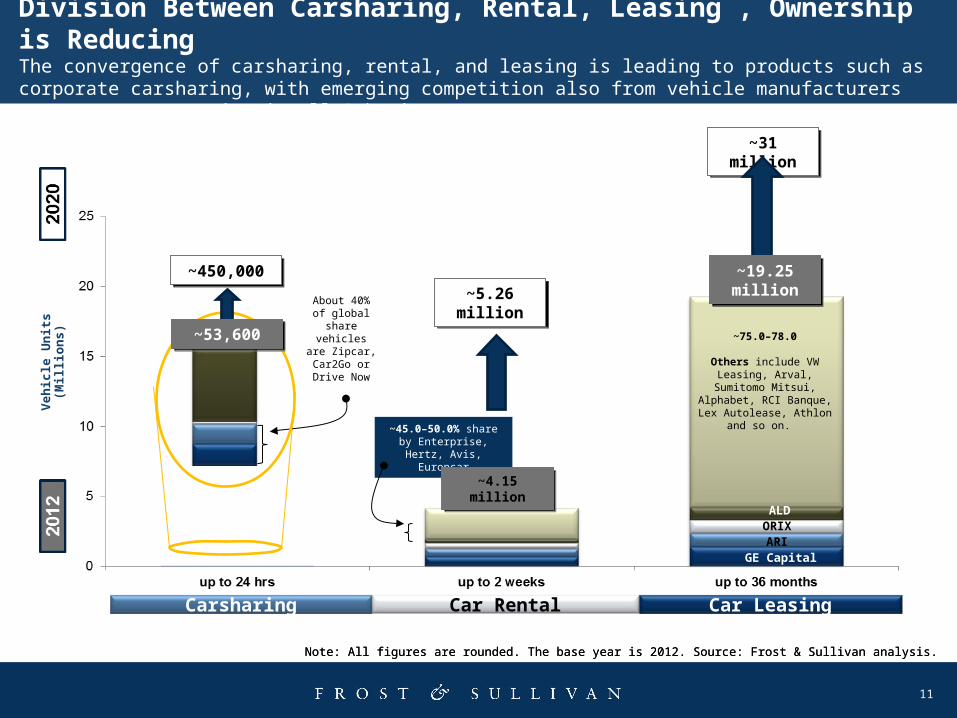

Division Between Carsharing, Rental, Leasing , Ownership is Reducing The convergence of carsharing, rental, and leasing is leading to products such as corporate carsharing, with emerging competition also from vehicle manufacturers present or partnering in all 3 business groups

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

~45.0–50.0% share by Enterprise, Hertz, Avis,

Europcar

ALD

~75.0–78.0

Others include VW Leasing, Arval, Sumitomo Mitsui,

Alphabet, RCI Banque, Lex Autolease, Athlon and so on.

Carsharing Car Rental Car Leasing

About 40% of global share vehicles are

Zipcar, Car2Go or Drive Now

GE CapitalARI

ORIX

Veh

icle

Un

its

(Mil

lio

ns)

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

~5.26 million~5.26

million

~31 million~31 million

~450,000~450,000

~53,600~53,600

~4.15 million~4.15 million

~19.25 million~19.25 million

12

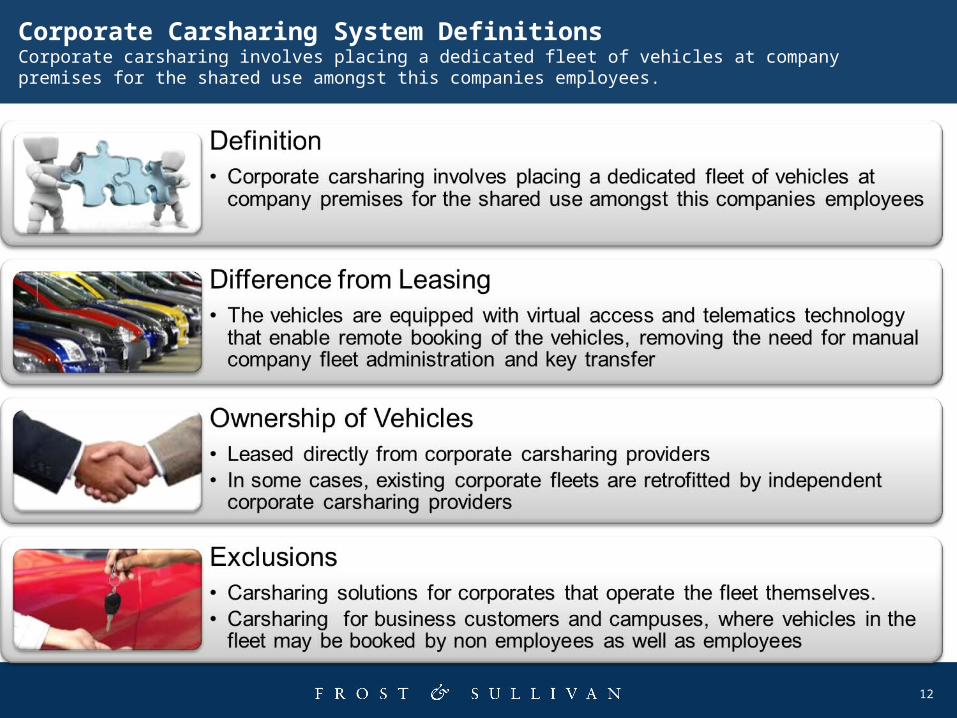

Corporate Carsharing System DefinitionsCorporate carsharing involves placing a dedicated fleet of vehicles at company premises for the shared use amongst this companies employees.

13

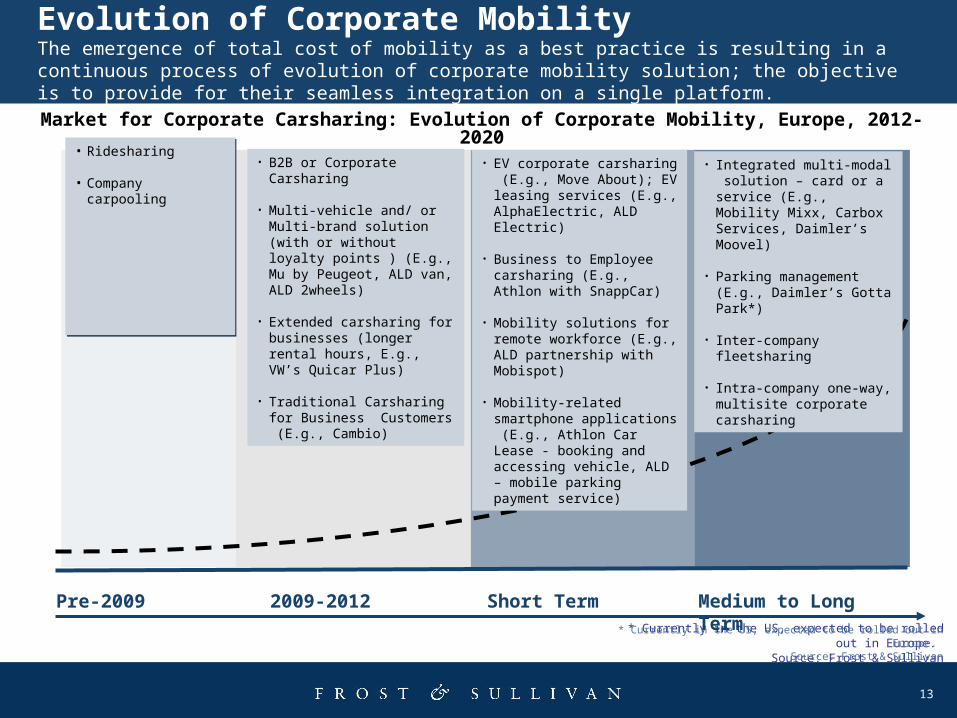

Evolution of Corporate Mobility The emergence of total cost of mobility as a best practice is resulting in a continuous process of evolution of corporate mobility solution; the objective is to provide for their seamless integration on a single platform.

* Currently in the US, expected to be rolled out in Europe. Source: Frost & Sullivan

Pre-2009 2009-2012 Short Term

* Currently in the US, expected to be rolled out in Europe. Source: Frost & Sullivan

• B2B or Corporate Carsharing

• Multi-vehicle and/ or Multi-brand solution (with or without loyalty points ) (E.g., Mu by Peugeot, ALD van, ALD 2wheels)

• Extended carsharing for businesses (longer rental hours, E.g., VW’s Quicar Plus)

• Traditional Carsharing for Business Customers (E.g., Cambio)

• Ridesharing

• Company carpooling

• Ridesharing

• Company carpooling

• EV corporate carsharing (E.g., Move About); EV leasing services (E.g., AlphaElectric, ALD Electric)

• Business to Employee carsharing (E.g., Athlon with SnappCar)

• Mobility solutions for remote workforce (E.g., ALD partnership with Mobispot)

• Mobility-related smartphone applications (E.g., Athlon Car Lease - booking and accessing vehicle, ALD – mobile parking payment service)

Medium to Long Term

• Integrated multi-modal solution – card or a service (E.g., Mobility Mixx, Carbox Services, Daimler’s Moovel)

• Parking management (E.g., Daimler’s Gotta Park*)

• Inter-company fleetsharing

• Intra-company one-way, multisite corporate carsharing

Market for Corporate Carsharing: Evolution of Corporate Mobility, Europe, 2012-2020

14

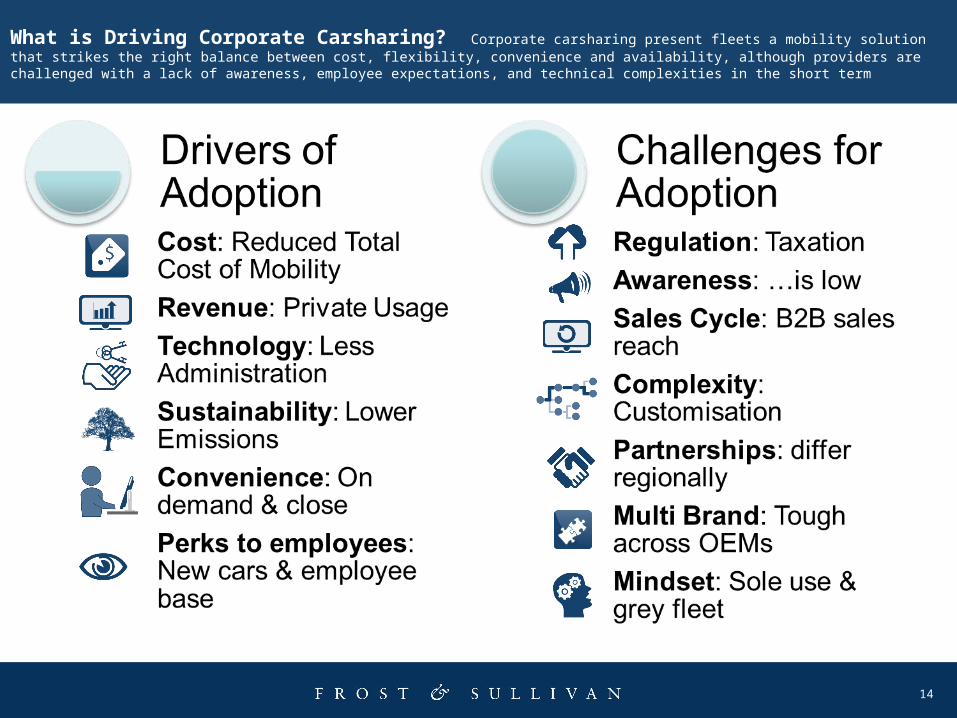

What is Driving Corporate Carsharing? Corporate carsharing present fleets a mobility solution that strikes the right balance between cost, flexibility, convenience and availability, although providers are challenged with a lack of awareness, employee expectations, and technical complexities in the short term

15

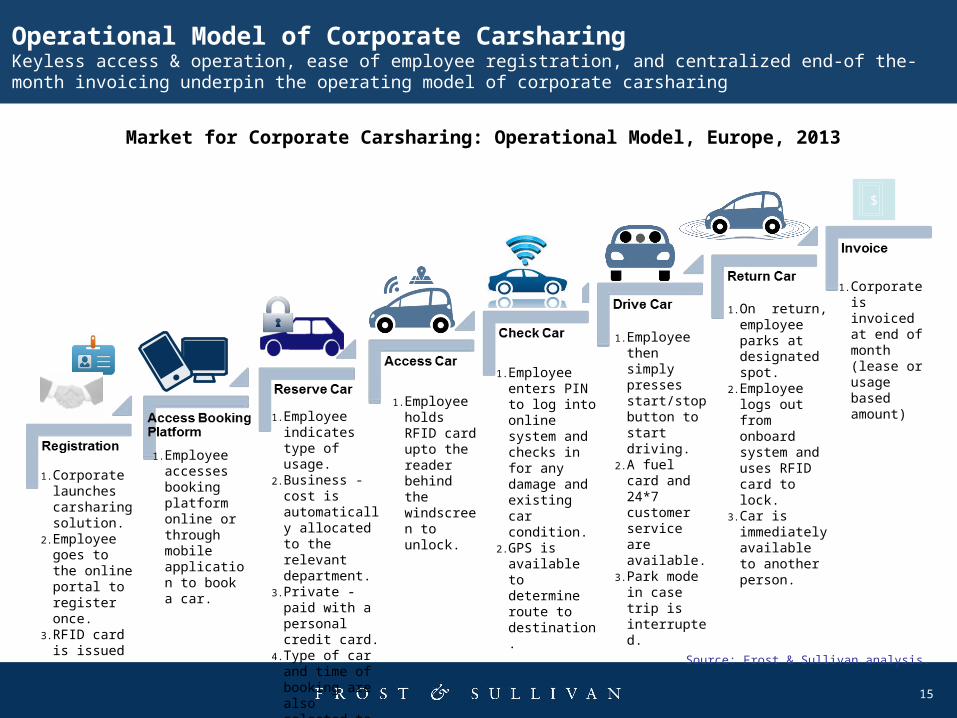

Operational Model of Corporate CarsharingKeyless access & operation, ease of employee registration, and centralized end-of the-month invoicing underpin the operating model of corporate carsharing

Source: Frost & Sullivan analysis.

1. Corporate launches carsharing solution.

2. Employee goes to the online portal to register once.

3. RFID card is issued

1. Employee accesses booking platform online or through mobile application to book a car.

1. Employee indicates type of usage.

2. Business - cost is automatically allocated to the relevant department.

3. Private - paid with a personal credit card.

4. Type of car and time of booking are also selected to reserve the car immediately.

1. Employee holds RFID card upto the reader behind the windscreen to unlock.

1. Employee enters PIN to log into online system and checks in for any damage and existing car condition.

2. GPS is available to determine route to destination.

1. Employee then simply presses start/stop button to start driving.

2. A fuel card and 24*7 customer service are available.

3. Park mode in case trip is interrupted.

1. On return, employee parks at designated spot.

2. Employee logs out from onboard system and uses RFID card to lock.

3. Car is immediately available to another person.

1. Corporate is invoiced at end of month (lease or usage based amount)

Market for Corporate Carsharing: Operational Model, Europe, 2013

$

16

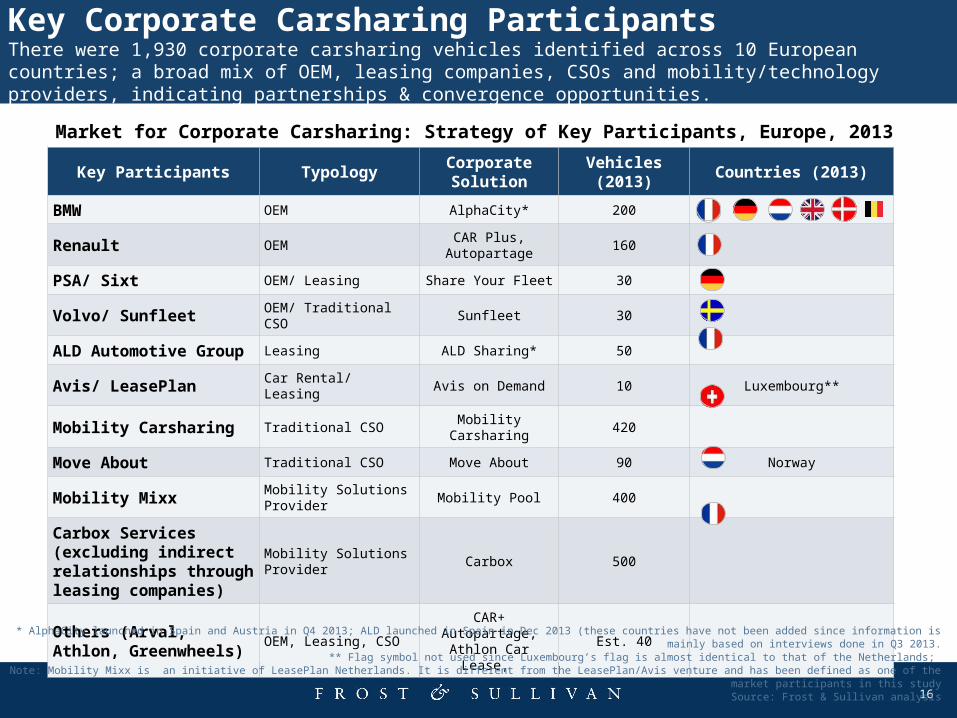

Key Corporate Carsharing Participants There were 1,930 corporate carsharing vehicles identified across 10 European countries; a broad mix of OEM, leasing companies, CSOs and mobility/technology providers, indicating partnerships & convergence opportunities.

Key Participants TypologyCorporate Solution

Vehicles (2013)

Countries (2013)

BMW OEM AlphaCity* 200

Renault OEMCAR Plus,

Autopartage160

PSA/ Sixt OEM/ Leasing Share Your Fleet 30

Volvo/ Sunfleet OEM/ Traditional CSO Sunfleet 30

ALD Automotive Group Leasing ALD Sharing* 50

Avis/ LeasePlan Car Rental/ Leasing Avis on Demand 10 Luxembourg**

Mobility Carsharing Traditional CSO Mobility Carsharing 420

Move About Traditional CSO Move About 90 Norway

Mobility MixxMobility Solutions Provider

Mobility Pool 400

Carbox Services (excluding indirect relationships through leasing companies)

Mobility Solutions Provider

Carbox 500

Others (Arval, Athlon, Greenwheels)

OEM, Leasing, CSOCAR+ Autopartage, Athlon Car Lease,

Est. 40

Market for Corporate Carsharing: Strategy of Key Participants, Europe, 2013

* AlphaCity launched in Spain and Austria in Q4 2013; ALD launched in Spain in Dec 2013 (these countries have not been added since information is mainly based on interviews done in Q3 2013.** Flag symbol not used since Luxembourg’s flag is almost identical to that of the Netherlands;

Note: Mobility Mixx is an initiative of LeasePlan Netherlands. It is different from the LeasePlan/Avis venture and has been defined as one of the market participants in this studySource: Frost & Sullivan analysis

17

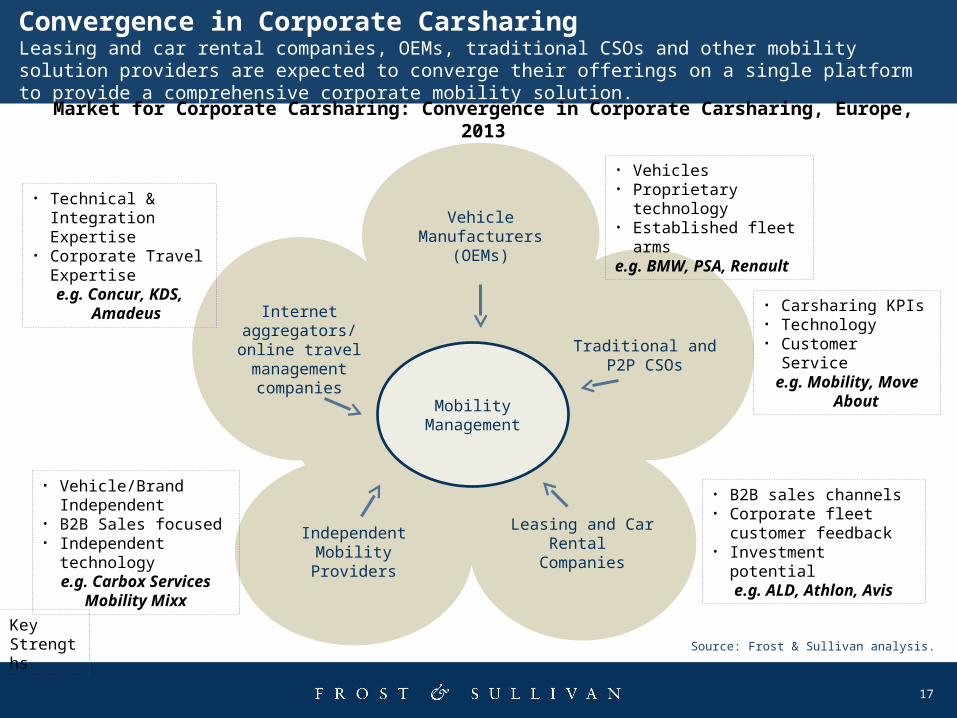

Convergence in Corporate CarsharingLeasing and car rental companies, OEMs, traditional CSOs and other mobility solution providers are expected to converge their offerings on a single platform to provide a comprehensive corporate mobility solution.

Market for Corporate Carsharing: Convergence in Corporate Carsharing, Europe, 2013

Source: Frost & Sullivan analysis.

Independent Mobility Providers

Internet aggregators/ online travel management

companies

Leasing and Car Rental

Companies

Traditional and P2P CSOs

Mobility Management

Vehicle Manufacturers (OEMs)

• Vehicles• Proprietary technology• Established fleet armse.g. BMW, PSA, Renault

• Carsharing KPIs• Technology• Customer Service

e.g. Mobility, Move About

• B2B sales channels• Corporate fleet customer

feedback• Investment potential

e.g. ALD, Athlon, Avis

• Vehicle/Brand Independent

• B2B Sales focused• Independent

technologye.g. Carbox Services

Mobility Mixx

• Technical & Integration Expertise

• Corporate Travel Expertisee.g. Concur, KDS,

Amadeus

Key Strengths

18

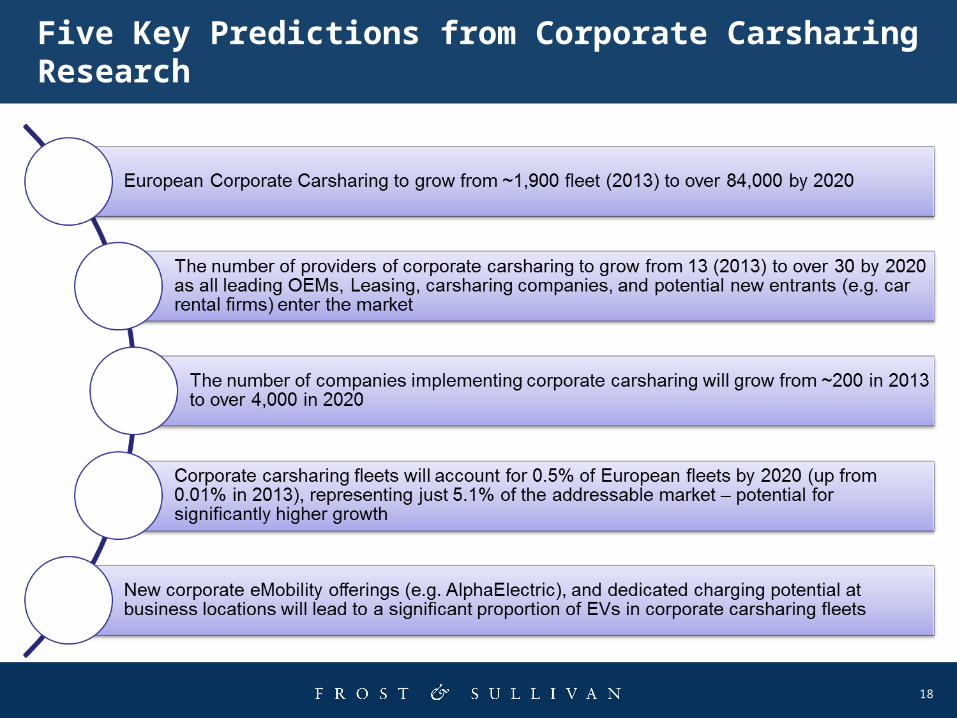

Five Key Predictions from Corporate Carsharing Research

19

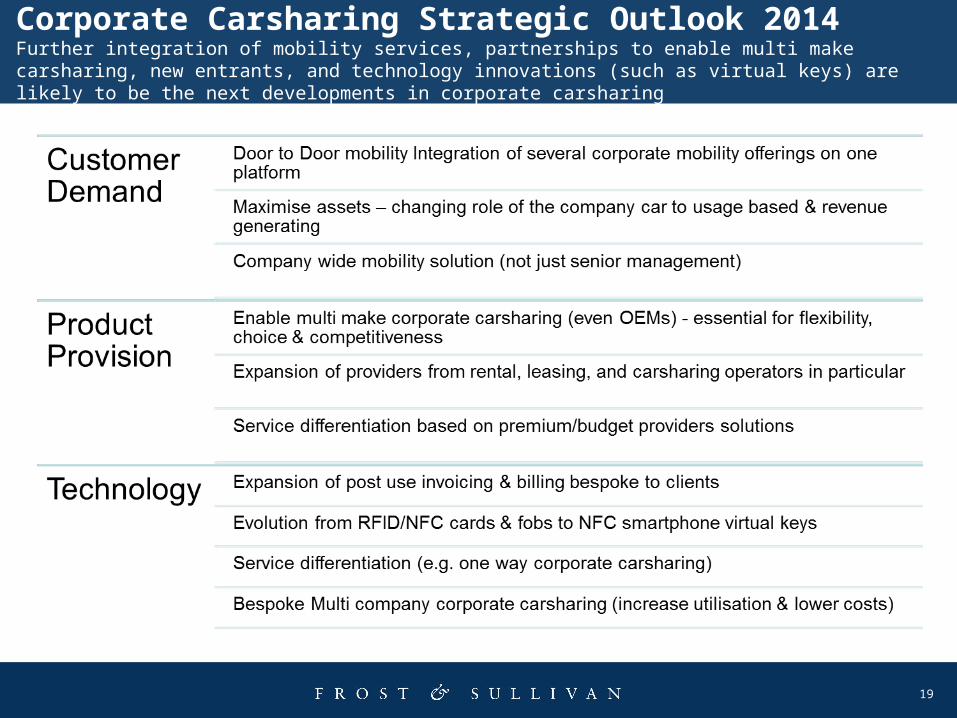

Corporate Carsharing Strategic Outlook 2014Further integration of mobility services, partnerships to enable multi make carsharing, new entrants, and technology innovations (such as virtual keys) are likely to be the next developments in corporate carsharing

20

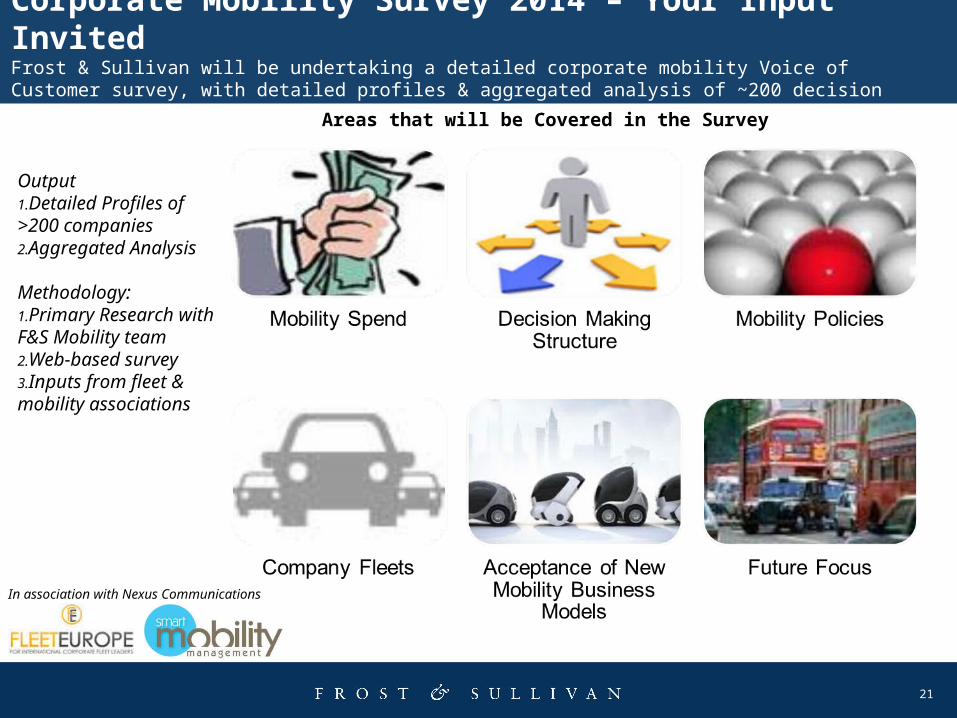

Corporate Mobility Survey 2014 – Your Input InvitedFrost & Sullivan will be undertaking a detailed corporate mobility Voice of Customer survey, with detailed profiles & aggregated analysis of ~200 decision makers to understand companies future mobility requirements

21

Corporate Mobility Survey 2014 – Your Input InvitedFrost & Sullivan will be undertaking a detailed corporate mobility Voice of Customer survey, with detailed profiles & aggregated analysis of ~200 decision makers to understand companies future mobility requirements

Output1.Detailed Profiles of >200 companies2.Aggregated Analysis

Methodology: 1.Primary Research with F&S Mobility team2.Web-based survey3.Inputs from fleet & mobility associations

Areas that will be Covered in the Survey

In association with Nexus Communications

22

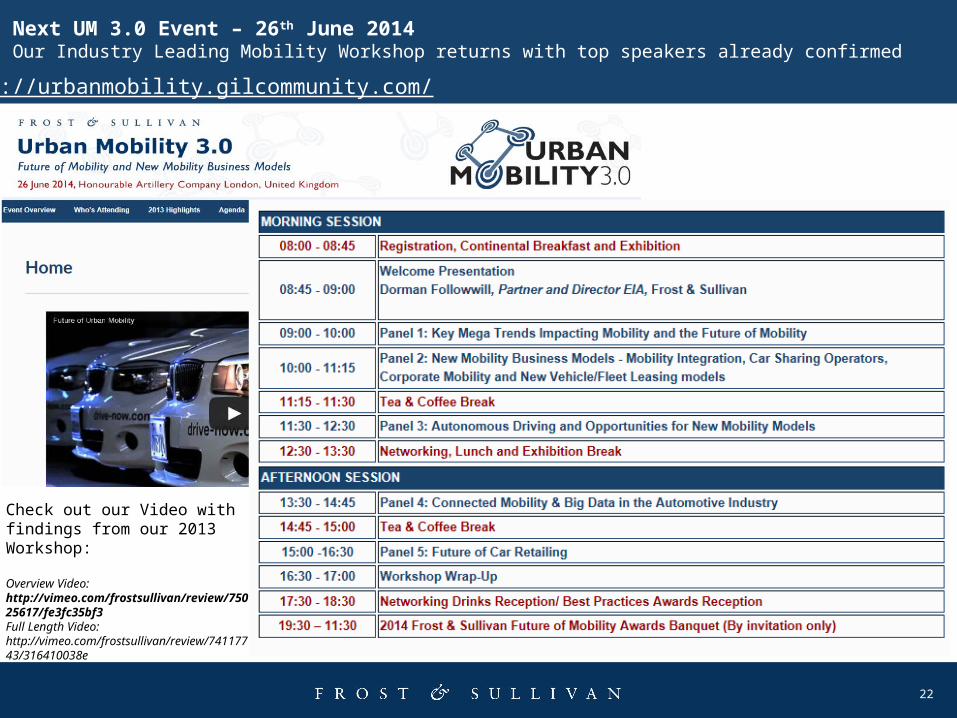

Next UM 3.0 Event – 26th June 2014Our Industry Leading Mobility Workshop returns with top speakers already confirmed http://urbanmobility.gilcommunity.com/

Check out our Video with findings from our 2013 Workshop:

Overview Video: http://vimeo.com/frostsullivan/review/75025617/fe3fc35bf3Full Length Video: http://vimeo.com/frostsullivan/review/74117743/316410038e

23

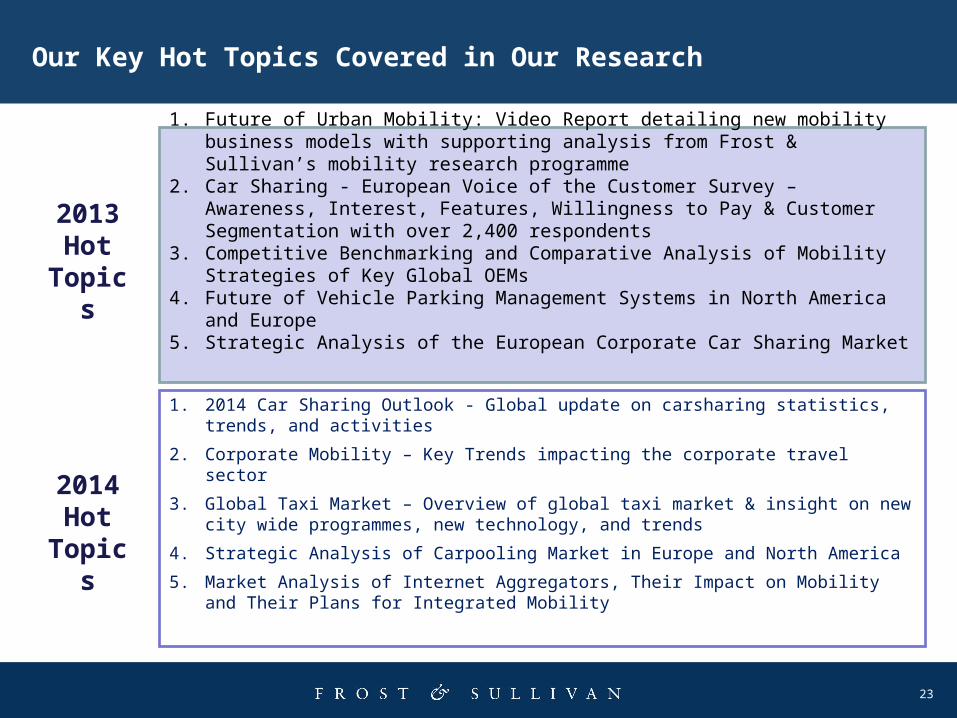

Our Key Hot Topics Covered in Our Research

1. Future of Urban Mobility: Video Report detailing new mobility business models with supporting analysis from Frost & Sullivan’s mobility research programme

2. Car Sharing - European Voice of the Customer Survey – Awareness, Interest, Features, Willingness to Pay & Customer Segmentation with over 2,400 respondents

3. Competitive Benchmarking and Comparative Analysis of Mobility Strategies of Key Global OEMs

4. Future of Vehicle Parking Management Systems in North America and Europe5. Strategic Analysis of the European Corporate Car Sharing Market

1. 2014 Car Sharing Outlook - Global update on carsharing statistics, trends, and activities

2. Corporate Mobility – Key Trends impacting the corporate travel sector

3. Global Taxi Market – Overview of global taxi market & insight on new city wide programmes, new technology, and trends

4. Strategic Analysis of Carpooling Market in Europe and North America

5. Market Analysis of Internet Aggregators, Their Impact on Mobility and Their Plans for Integrated Mobility

2013 Hot

Topics

2014 Hot

Topics

24

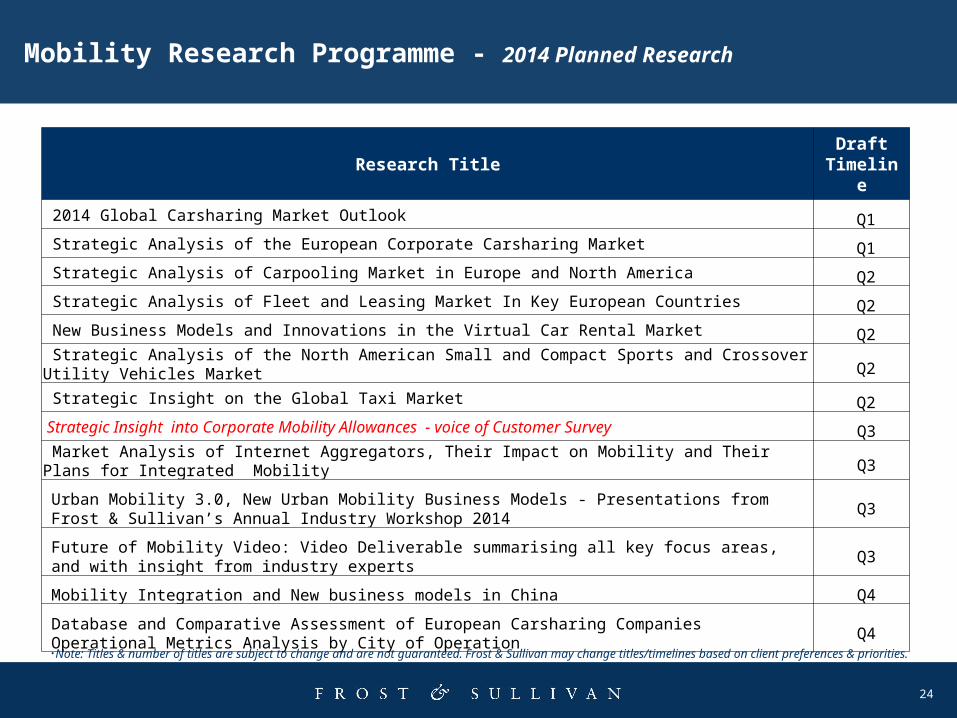

Mobility Research Programme - 2014 Planned Research

Research TitleDraft

Timeline

2014 Global Carsharing Market Outlook Q1

Strategic Analysis of the European Corporate Carsharing Market Q1

Strategic Analysis of Carpooling Market in Europe and North America Q2

Strategic Analysis of Fleet and Leasing Market In Key European Countries Q2

New Business Models and Innovations in the Virtual Car Rental Market Q2

Strategic Analysis of the North American Small and Compact Sports and Crossover Utility Vehicles Market Q2

Strategic Insight on the Global Taxi Market Q2

Strategic Insight into Corporate Mobility Allowances - voice of Customer Survey Q3

Market Analysis of Internet Aggregators, Their Impact on Mobility and Their Plans for Integrated Mobility Q3

Urban Mobility 3.0, New Urban Mobility Business Models - Presentations from Frost & Sullivan’s Annual Industry Workshop 2014

Q3

Future of Mobility Video: Video Deliverable summarising all key focus areas, and with insight from industry experts

Q3

Mobility Integration and New business models in China Q4

Database and Comparative Assessment of European Carsharing Companies Operational Metrics Analysis by City of Operation

Q4

•Note: Titles & number of titles are subject to change and are not guaranteed. Frost & Sullivan may change titles/timelines based on client preferences & priorities.

25

Next Steps

Develop Your Visionary and Innovative SkillsGrowth Partnership Service Share your growth thought leadership and ideas or

join our GIL Global Community

Join our GIL Community Newsletter Keep abreast of innovative growth opportunities

26

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

What would you like to see from Frost & Sullivan?

27

http://twitter.com/frost_sullivanhttp://twitter.com/FS_Automotivehttp://twitter.com/BriggsMartyn

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter, & Watch our Urban Mobility 2013 Video

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506& join our “Future of Mobility” Group

http://www.slideshare.net/FrostandSullivan

http://www.urbanmobility.gilcommunity.com

Overview Video:http://vimeo.com/frostsullivan/review/75025617/fe3fc35bf3

Full Length Video:http://vimeo.com/frostsullivan/review/74117743/316410038e

1. Check out our Future of Mobility Video on Youtube / Vimeo

2. Join our LinkedIn group3. Join us at Urban Mobility 3.0 in

London, 26th June 2014

28

For Additional Information

Katja FeickCorporate CommunicationsAutomotive & Transportation+49 (0) 69 [email protected]

Mohamed Mubarak Programme ManagerAutomotive & Transportation+90 212 709 8804 Extn: [email protected]

Martyn BriggsProgramme Manager – MobilityAutomotive & Transportation 0044 (0)207 915 [email protected]

Cyril CromierVP SalesAutomotive & Transportation +33 1 4281 2244 [email protected]