future of canola - data.daff.gov.au

TRANSCRIPT

FUTURE OF

CANOLAPRODUCTIONin Australia

ABARE Research Report 01.6

Rohan Nelson

David Barrett

Max Foster

Scott Turner

Amy Beasley

Proudly supported by

© Commonwealth of Australia 2001

This work is copyright. The Copyright Act 1968 permits fair dealing for study,research, news reporting, criticism or review. Selected passages, tables ordiagrams may be reproduced for such purposes provided acknowledgmentof the source is included. Major extracts or the entire document may not bereproduced by any process without the written permission of the ExecutiveDirector, ABARE.

ISSN 1037–8286ISBN 0 642 76440 9

Nelson, R., Barrett, D., Foster, M., Turner, S. and Beasley, A. 2001, The Futureof Canola Production in Australia, ABARE Research Report 01.6, Canberra.

Australian Bureau of Agricultural and Resource EconomicsGPO Box 1563 Canberra 2601

Telephone +61 2 6272 2000 Facsimile +61 2 6272 2001Internet www.abareconomics.com

ABARE is a professionally independent government economic researchagency.

GRDC disclaimerAny recommendations, suggestions or opinions contained in this publica-tion do not necessarily represent the policy or views of the Grains Researchand Development Corporation. No person should act on the basis of thecontents of this publication without first obtaining specific, independentprofessional advice.

The Grains Research and Development Corporation will not be liable forany loss, damage, cost or expense incurred or arising by reason of any personusing or relying on the information in this publication.

ABARE project 1627

Foreword

The Australian canola industry expanded dramatically during the 1990s.Canola became profitable as a break crop because of favorable export pricesand internationally competitive production costs. Whether the industry cancontinue to expand at this rate depends on whether world prices remain favor-able, and the degree to which Australian production remains internationallycompetitive.

World consumption of canola is expected to rise strongly to 2010, creatinga good market outlook for the Australian canola industry. However, realcanola prices are unlikely to return to the high levels of the mid-1990s becauseof increasing world production of low cost soybean and palm oil. Competitionfrom low cost substitutes will be offset by growing consumer awareness ofthe health benefits of monounsaturated canola oil. The speed and extent oftrade liberalisation will significantly effect Australia’s access to these grow-ing world markets.

Although current international constraints on trade are significant, this reportconcludes that the Australian canola industry will recover from its recentdownturn, albeit at a slower rate than the expansion of the 1990s. ABARE’sprojections for the canola industry are likely to be influenced by a range ofissues surrounding genetically modified varieties and trade issues. Thesepotential influences are analysed in the report using the OECD’s Aglinkmodel.

BRIAN S. FISHER

Executive Director

June 2001

iiiFuture of canola production

Acknowledgments

This study was funded by the Grains Research and Development Corporation.The support of Mike Taverner from the GRDC is greatly appreciated.

The research involved consultation with researchers, farmers, consultantsand state department officers from around Australia, whose contributionsare gratefully acknowledged. The authors particularly wish to thank BobColton and Neil Wratten from New South Wales Agriculture; Ian Riley fromthe University of Adelaide; Adrian Cox, Ross Kingwell, Ian Pritchard andRob Loughman from Agriculture Western Australia; John Slee from JoyceIndustries at Pinjarra; Geoff Black from Cootamundra Oilseeds; Steve Brill,Justin Kudnig and John Lamont from the Canola Association of Australia;Peter Jones from AWB International; Phil Salisbury and Steve Marchantfrom the Victorian Institute of Dryland Agriculture; Tony Eyres and membersof the Birchip Cropping Group; Peter and Bob MacSmith from ‘Little Boree’of Cudal, New South Wales; Lloyd George from Cargill; and John Knoxfrom Australian Drilling Specialties.

The assistance in the preparation of earlier drafts of this report and with datagathering from Christine Byrnes, Stephen Hooper, Geoff Bailey and CatherineRees from ABARE’s Agriculture and Natural Resources Directorate is grate-fully acknowledged, as is the assistance of other ABARE staff, particularlyIan Shaw for his technical assistance with the Aglink model, Trish Gleesonfor assistance with the Aglink baseline, and Vince O’Donnell for projectoversight. Comments by Ahmed Hafi and Rhonda Treadwell on earlier draftsare also gratefully acknowledged.

iv ABARE research report 01.6

Contents

Summary 1

1 Australian and world oilseeds markets 5Expansion of the canola industry 5Australia’s role in world canola markets 7

2 Prospects for world oil markets 14Market outlook 14World supply 14World demand 17

3 Prospects for trade 23World canola trade 23Competing and trading nations 25

4 Prospects for Australian canola 39ABARE’s baseline projections 39Impact of potential developments 40Scenario 1: Adoption of GM canola in Australia 42Scenario 2: An increase in world wheat prices 47Scenario 3: Impact of Agenda 2000 51Scenario 4: A reduction in Chinese oilseed tariffs 54

AppendixA Agronomic performance of canola in Australia 61

References 68

vFuture of canola production

FiguresA Australian canola area, production and exports 5B Australian oilseeds production 6C Gross margins for Central East zone, New South Wales 6D Index of world oil consumption 9E Change in oil consumption per person, 1990-91 to

1999-2000 11F Australian vegetable oil consumption 11G Australian consumption of oilseeds meal 12H Australian canola exports as a percentage of production 12I Projected real world indicator prices for soybeans and canola14J World vegetable oil prices 15K Relationships between vegetable oil consumption and

income, selected countries 17L Volume of Australian oilseeds exports, by destination 25M Production costs and gross margins for canola, Australia

and Canada 26N Canadian plantings of genetically modified canola 28O Canola/rapeseed stocks and prices 28P Australian canola area, production and oilseeds exports 39Q World price indexes for wheat, coarse grains and oilseeds 40R Changes in key oilseeds market variables under two

scenarios 43S OECD field trials of genetically modified canola,

by category 65

Tables1 World production of oilseeds, by major producer 82 World consumption of vegetable oils 93 Major oilseeds processing nations in the world 134 World importers of oilseeds, excluding intra-European

Union trade 245 World exporters of oilseeds, excluding intra-European

Union trade 246 Production costs and gross margins for canola in Australia

and Canada, 2000 27

vi ABARE research report 01.6

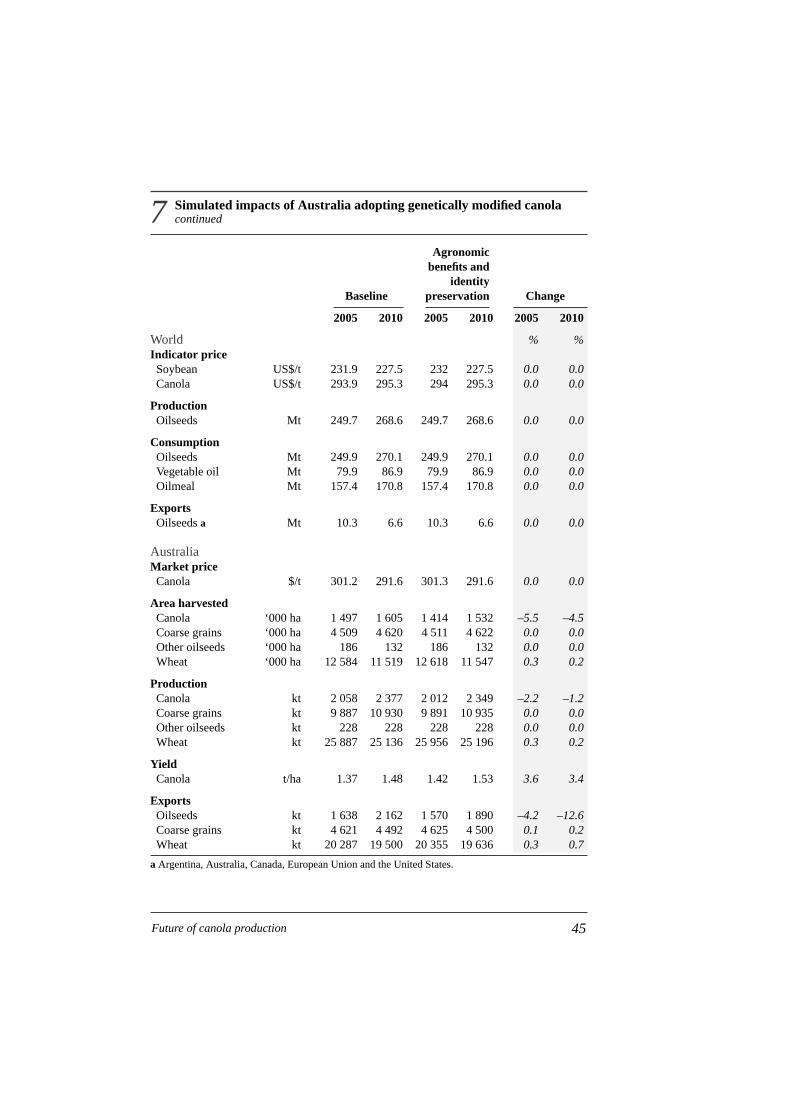

7 Simulated impacts of Australia adopting genetically modifiedcanola 44

8 Simulated impacts of a higher wheat price, 2001–03 489 Simulated impacts of a higher wheat price, 2001–10 50

10 Simulated impacts of Agenda 2000, using Aglink 5211 Simulated impacts of a reduction in China’s oilseeds tariffs,

using Aglink 5612 Simulated impacts of a reduction in China’s oilseeds,

oilseed meal and vegetable oil tariffs, using Aglink 5813 Key forms of genetically modified canola in the

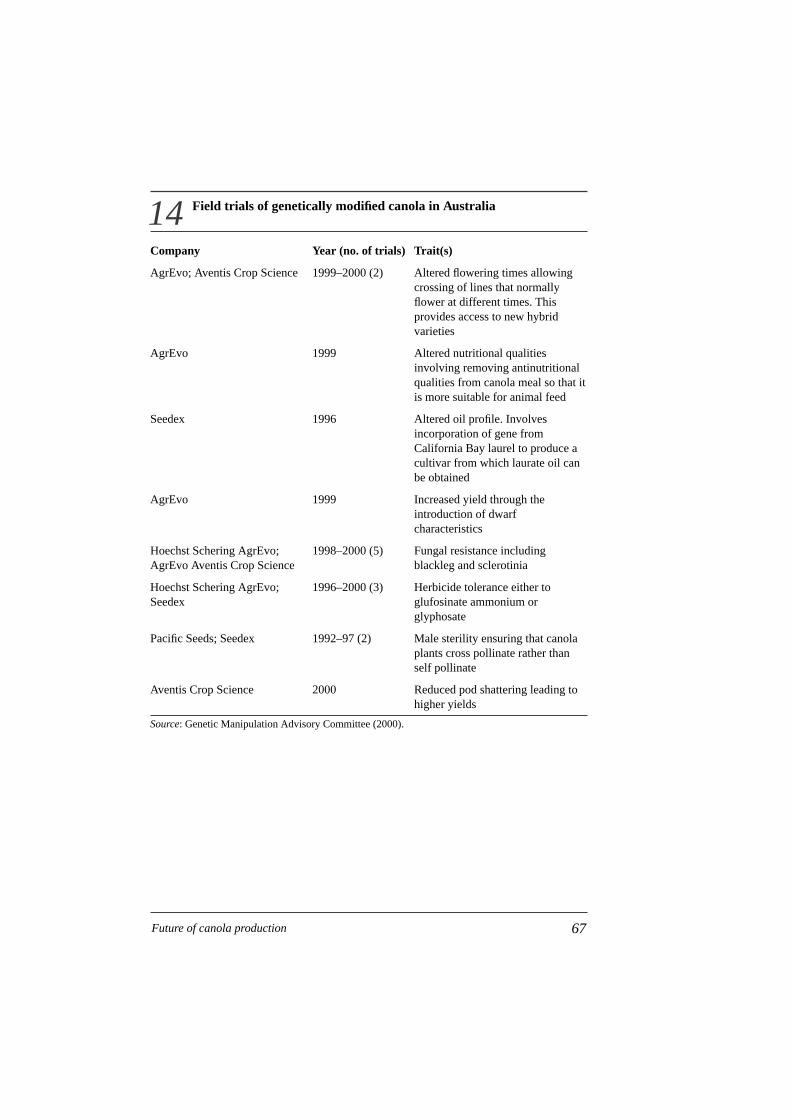

development pipeline 6614 Field trials of generically modified canola in Australia 67

viiFuture of canola production

Summary

Between 1992-93 and 1999-2000, the area planted to canola in Australiaincreased from 0.1 million hectares to an estimated 1.9 million hectares,while exports increased from just under half a million tonnes to 1.9 milliontonnes. The dramatic expansion of the Australian canola industry was drivenby favorable world prices for varieties with preferred oil characteristics, andthe international competitiveness of Australian canola production. Whetherthe Australian canola industry can continue to expand at the rate experiencedduring the 1990s depends on developments in world markets for oilseedsand derived products. An interaction of policy and market developments indomestic and world markets will shape the future of Australia’s canolaindustry.

World consumption of canola oilThe demand for Australian canola seed exports is driven by world demandfor canola oil. China and the European Union were the largest consumers ofcanola oil in 1999-2000. During the 1990s, canola oil comprised around 15per cent of total world vegetable oil consumption, which continues to bedominated by soybean and palm oil. The European Union, China, Canadaand India produced over 80 per cent of world canola production during the1990s.

World consumption of canola oil rose at a similar rate to that of soybean oilduring the 1990s, but at a slower rate than consumption of palm oil. Canolaoil’s share of total oil consumption per person rose in Australia, the EuropeanUnion, Pakistan and the United States, mostly at the expense of soybean oil.

With small domestic markets for oilseeds products, the Australian canolaindustry is reliant on export markets.

World consumption of canola is expected to rise strongly over the projec-tion period, creating a favorable outlook for the Australian canola industry.ABARE’s commodity research using the OECD’s Aglink model projectsthat world indicator prices for canola seed and soybeans will rise slightly inthe medium term, before falling slightly toward 2010. ABARE’s projectionof stable real prices for canola are based on strong expected world demand

1Future of canola production

for canola oil, and increasing world production of low cost soybean and palmoil.

Population growth in developing countries, particularly China and India, isexpected to be a major influence on world demand for oilseed products,including canola. The potential for increased per person consumption of oilsis highest in developing countries where low incomes have limited consump-tion to very low levels. In developed countries, increases in population areexpected to be only marginal, thus increases in the consumption of canolaoil are expected to be more closely related to changes in consumer prefer-ences.

Changing consumer preferences are expected to increase world demand forcanola oil. Growing consumer awareness of the health benefits of replacingsaturated oils with monounsaturated and polyunsaturated oils is expected toincrease canola oil’s share of world consumption. A consumer backlashagainst perceived health risks and genetic ‘contamination’ associated withgenetically modified (GM) crops has resulted in some countries imposingstrict labeling regulations on imports. Australia may face a growing demandfor non-GM canola, but only by incurring the substantial costs for identitypreservation if GM canola is adopted and forgoing its agronomic benefits ifit is not adopted.

Australian canola exportsThe prospects for the Australian canola industry will be influenced by devel-opments in the world vegetable oil markets, together with changes in poli-cies affecting world oilseed and vegetable oil trade. The European Unionand Japan have been significant importers of oilseeds, while China hasrecently become a major importer. The United States, Brazil and Argentinahave dominated world oilseed exports, while Canada has been by far thelargest exporter of canola. Australia is the next largest exporter of canola,contributing a quarter of total world exports in 1999-2000. Australian exportsof oilseeds, principally canola and cotton seed, are exported to Japan,Bangladesh, Mexico and, more recently, China.

The Australian canola industry’s ability to expand its share of world canolatrade depends, in part, on its comparative advantage relative to other worldproducers, particularly Canada. The value of the Australian dollar againstthe currencies of other exporting nations has a marked influence on thecompetitiveness of Australian canola on world markets. As a measure of

2 ABARE research report 01.6

Australia’s competitiveness in canola production estimated gross margins inCanada (at an exchange rate of A$1 = C$0.86) are roughly in the mid tolower range of estimates for Australia.

The speed and extent of trade liberalisation achieved through WTO negoti-ations will have a significant effect on access to growing world markets.Domestic support paid to producers in the United States and the EuropeanUnion reduces their import demand and increases world exportable supplies,depressing world canola prices. Similarly, import tariffs imposed by China,India, Japan and Pakistan to protect domestic oilseeds producers increasedomestic prices for commodities and reduce demand, lowering world prices.

Canola production in AustraliaDespite the constraints on trade, the market outlook for the Australia canolaindustry is positive but unlikely to support the dramatic rates of expansionof the 1990s. While Australian canola plantings fell from 1.8 million hectaresin 1999 to 1.2 million hectares in 2000, the area sown is projected to risegradually to 1.6 million hectares by 2010. Productivity gains will enableAustralian canola production to exceed the 1999 peak of 2.2 million tonnesby 2010, rising to an estimated 2.4 million tonnes from a low of 1.6 milliontonnes in 2000. Most of Australia’s canola production will continue to beexported, with exports estimated to rise gradually to 1.9 million tonnes follow-ing a fall to 1.1 million tonnes in 2000.

ABARE’s baseline estimates for the Australian canola industry assumeconservative productivity gains to 2010 because of emerging agronomiclimitations on the extent to which canola can be included in winter cerealrotations. In addition, strong world prices for wheat and coarse grains areprojected to provide an incentive for Australian producers to reduce the repre-sentation of canola in winter cereal rotations.

Several agronomic, market and policy influences have the potential to influ-ence ABARE’s baseline estimates for the Australian canola industry to 2010.The OECD Aglink model was used to analyse four alternative scenarios forthe Australian canola industry.

• The introduction of herbicide tolerant canola to Australia is unlikely tobe economically viable if identity preservation is required to overcomeconsumer acceptance problems. Alternatively, a significant premium fornongenetically modified over genetically modified canola is likely to benecessary to offset the additional costs of identity preservation.

3Future of canola production

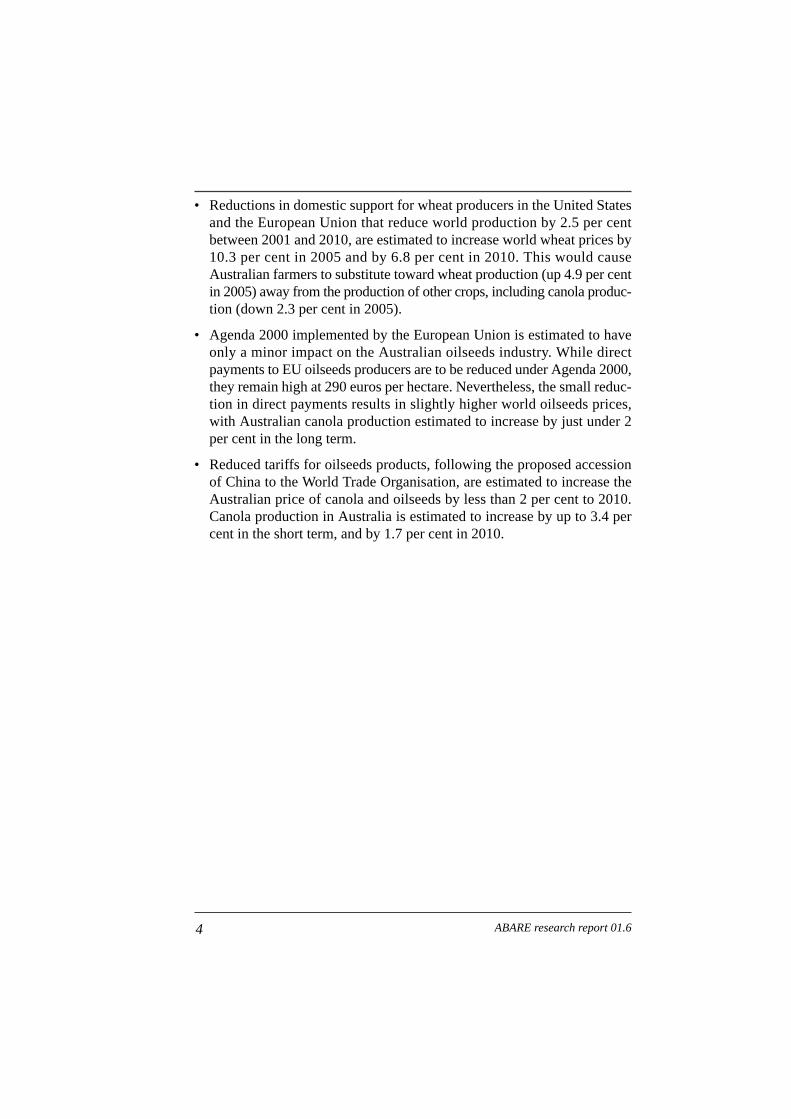

• Reductions in domestic support for wheat producers in the United Statesand the European Union that reduce world production by 2.5 per centbetween 2001 and 2010, are estimated to increase world wheat prices by10.3 per cent in 2005 and by 6.8 per cent in 2010. This would causeAustralian farmers to substitute toward wheat production (up 4.9 per centin 2005) away from the production of other crops, including canola produc-tion (down 2.3 per cent in 2005).

• Agenda 2000 implemented by the European Union is estimated to haveonly a minor impact on the Australian oilseeds industry. While directpayments to EU oilseeds producers are to be reduced under Agenda 2000,they remain high at 290 euros per hectare. Nevertheless, the small reduc-tion in direct payments results in slightly higher world oilseeds prices,with Australian canola production estimated to increase by just under 2per cent in the long term.

• Reduced tariffs for oilseeds products, following the proposed accessionof China to the World Trade Organisation, are estimated to increase theAustralian price of canola and oilseeds by less than 2 per cent to 2010.Canola production in Australia is estimated to increase by up to 3.4 percent in the short term, and by 1.7 per cent in 2010.

4 ABARE research report 01.6

Australian and world oilseed markets

Expansion of the canola industryBetween 1992-93 and 1999-2000, the area planted to canola in Australiaincreased from 0.1 million hectares to an estimated 1.9 million hectares,while seed production rose from 0.2 million tonnes to an estimated 2.4 milliontonnes (figure A). With small domestic oilseeds markets, the Australianoilseeds industry is reliant on exports. Australia’s canola exports increasedfrom 48 700 tonnes (27 per cent of production) to 1.9 million tonnes (78 percent of production) between 1992-93 and 1999-2000. The dramatic expan-sion of canola production has taken canola from less than 10 per cent ofAustralian oilseeds production in 1990-91, to nearly 65 per cent in 1999-2000 (figure B).

Canola’s introduction to Australia in the early 1960s met with limited successbecause demand for the low quality oil produced at that time was limited,and production was inhibited by agronomic problems. In the 1990s, favor-able world prices for varieties with preferred oil characteristics facilitated arapid expansion of Australia’s canola industry. The international competi-tiveness of the Australian canola industry (discussed in chapter 3) has enabledAustralia to become a major exporter of canola. Canola has been profitablerelative to winter cereal crops, and has proved to be a useful break crop inwinter cereal rotations (appendix A). For example, estimated gross margins

5

1

Future of canola production

0

500

1000

1500

2000

2500

1983-84

1981-82

1985-86

1987-88

1989-90

1991-92

1993-94

1995-95

199798

1999-2000

Production (kt)

Exports (kt)

Area (’000 ha)

Australian canola area, production and exportsA

for canola in the Central East zone of New South Wales reported by NewSouth Wales Agriculture (2001) indicate that canola provides relatively highreturns compared with wheat and barley when yields are high (figure C).

In marginal areas with a high probability of low yields, growing canola mayincrease the risk of low returns because of the high costs of cultivation,fertilisers, insecticides and harvesting relative to other winter crops. In suit-able regions, however, canola gross margins are attractive relative to barleyand wheat even when compared using yields from the lower end of theexpected range (figure C).

Can the Australian canola industry continue to expand at the rate experi-enced during the 1990s? The answer to this question depends on develop-

6 ABARE research report 01.6

Canola 9.5% Cotton 26.4%

Other 2.3%Soybean 2.8%

Sunflower 4.0%

Canola 64.5%

Sunflower 14.6%

Soybean6.0%

Other4.0%

Cotton 66.0%

Australian oilseeds productionB1990–91 1999–2000

Gross margins for Central East zone, New South WalesC

$/ha 100 200 300

Barley 1.5 to 3.0 t/ha1.5 to 3.0 t/ha

1.5 to 3.0 t/ha1.5 to 3.0 t/ha

1.2 to 2.1 t/ha1.2 to 2.1 t/ha

Wheat

Canola $300/t

$145/t

$112/t

Price

ments in world markets for oilseeds and derived products, and the positionof the Australian oilseeds industry in world markets. World demand foroilseeds is influenced by oilseeds prices and the price of substitutes, economicand population growth rates, and consumer preferences. Market access forAustralian canola exports, and their competitiveness in world markets, willcontinue to be influenced by policy and market developments in other oilseedsexporting nations, particularly Canada and the United States, as well ascurrent and potential importing nations such as China, India, Japan, theEuropean Union and Pakistan. An interaction of policy and market devel-opments in domestic and world markets will shape the future of Australia’scanola industry.

Australia’s role in world canola marketsDespite the rapid expansion of Australian canola production during the 1990s,by 1999-2000 Australian production contributed only 1 per cent of worldoilseeds production, and less than 6 per cent of world canola production(table 1). The European Union, China, Canada and India produced over 80per cent of world canola1 production during the 1990s. World canola produc-tion increased by 69 per cent over the decade, and accounted for 15 per centof world oilseeds production in 1999-2000. During the 1990s, around 80 percent of all oilseeds were produced in the United States, China, Brazil, India,Argentina and the European Union. World oilseeds production increased byaround 38 per cent during the 1990s, reaching almost 300 million tonnes in1999-2000, with soybeans and canola accounting for much of this growth.

The demand for Australian canola seed exports is driven by world demandfor canola oil. China and the European Union were the largest consumers ofcanola oil in 1999-2000, while India’s apparent high per person consump-tion of canola oil is mostly of domestically produced mustard and rapeseedoil (table 2). World canola oil consumption grew strongly during the 1990s,with the largest absolute growth in China, the European Union and the UnitedStates.

Canola oil comprised around 15 per cent of total world vegetable oil con-sumption during the 1990s (table 2). World vegetable oil consumption

7Future of canola production

1 Reflecting data availability, supply and disposal information for canola, rapeseed and mustard havebeen amalgamated throughout this report and are collectively referred to as canola. In some countriesthis can be misleading. For example, mustard is a significant oilseed in India and rapeseed still repre-sents a large proportion of ‘canola’ production.

8 ABARE research report 01.6

1 World production of oilseeds, by major producer

1990-91 1999-2000 Change inproduction

Share ShareProduction of world Production of world

Mt % Mt % %Canola aAustralia 0.1 0.4 2.4 6 96Canada 3.3 13 8.8 21 169China 7.0 28 10.1 24 45European Union 6.7 27 11.3 27 68India 5.2 21 5.5 13 5Other 2.8 11 4.5 9 –13World total 25.1 100 42.6 100 69

SoybeansArgentina 11.5 11 20.7 13 80Australia 0.06 0.1 0.1 0.1 41Brazil 15.8 15 32 20 99China 11.0 11 14.3 9 30United States 52.4 50 72.3 46 37Other 13.4 13 17.8 12 25World total 104.2 100 157.2 100 50

SunflowerArgentina 4.2 18 6.1 23 48Australia 0.2 0.7 0.1 0.6 –3China 1.3 6 1.3 5 –3Eastern Europe 2.1 9 3.0 11 45European Union 4.3 19 3.2 12 –26Former Soviet Union 3.4 15 7.3 27 112United States 1.0 5 2.0 7 91Other 6.5 27 3.3 15 –89World total 22.9 100 26.4 100 16

Total oilseeds bArgentina 16.5 8 27.5 8 50Australia 1.04 0.5 3.7 1 67Brazil 17.1 8 33.3 11 84China 33.3 15 45.2 15 32European Union 13.6 6 16.5 5 20India 20.5 10 23.6 9 26United States 60.6 28 82.3 31 50Other 52.9 25 65.8 20 –23World total 215.5 100 297.9 100 38

a Includes canola rapeseed and mustard seed. b Includes canola custard copra cottonseed soybeansunflower seed and peanuts.Source: US Department of Agriculture (2000a).

9Future of canola production

2 World consumption of vegetable oils

1990-91 1999-2000Change in

Consumption Share Consumption Share consumption

kt % kt % %Canola oilAustralia 40 0.5 126 1.0 215.0Canada 377 4.4 540 4.1 43.2China 2 490 28.9 4 225 32.2 69.7European Union 1 553 18.0 3 027 23.1 94.9India 1 620 18.8 1 560 11.9 –3.7Japan 785 9.1 895 6.8 14.0Pakistan 74 0.9 192 1.5 159.5United States 275 3.2 662 5.0 140.7Other 1 398 16.2 1 886 14.4 34.9

World total 8 612 100.0 13 113 100.0 52.3

Continued ➮

continues to be predominantly of soybean (30 per cent in 1999-2000 ) andpalm oil (24 per cent in 1999-2000).

World consumption of canola oil rose at a similar rate to that for soybean oilduring the 1990s, and at a slower rate than for palm oil (figure D). Canolaoil’s share of total per person oil consumption rose in Australia, the EuropeanUnion, Pakistan and the United States, mostly at the expense of soybean oil(figure E). The share of rapeseed and mustard oils in total consumption

200019981996199419921990

Index

50

100

150

200

PalmSoy

Canola

Index of world oil consumptionD

2 World consumption of vegetable oils continued

1990-91 1999-2000Change in

Consumption Share Consumption Share consumption

kt % kt % %Soybean oilAustralia 53 0.3 48 0.2 –9.4Canada 172 1.1 279 1.1 62.2China 1 055 6.8 2 841 11.6 169.3European Union 1 752 11.3 1 643 6.7 –6.2India 445 2.9 1 582 6.5 255.5Japan 624 4.0 684 2.8 9.6Pakistan 210 1.4 239 1.0 13.8United States 5 506 35.6 7 283 29.8 32.3Other 5 628 36.4 9 821 40.2 74.5

World total 15 445 100.0 24 420 100.0 58.1

Palm oilAustralia 130 1.2 185 0.9 42.3Canada 14 0.1 15 0.1 7.1China 1 194 10.7 1 200 6.0 0.5European Union 1 496 13.5 2 209 11.0 47.7India 259 2.3 3 300 16.5 1 174.1Japan 304 2.7 377 1.9 24.0Pakistan 800 7.2 1 108 5.5 38.5United States 116 1.0 152 0.8 31.0Other 7 992 71.9 12 704 63.4 59.0

World total 11 111 100.0 20 050 100.0 80.5

Total oilsAustralia 382 0.7 522 0.6 36.6Canada 649 1.2 942 1.1 45.1China 6 518 11.6 11 424 13.9 75.3European Union 9 168 16.3 12 017 14.6 31.1India 5 010 8.9 9 702 11.8 93.7Japan 1 861 3.3 2 080 2.5 11.8Pakistan 1 420 2.5 1 952 2.4 37.5United States 7 140 12.7 9 543 11.6 33.7Other 30 479 54.3 45 412 55.3 49.0

World total 56 109 100.0 82 170 100.0 46.4

Source: US Department of Agriculture (2000a).

10 ABARE research report 01.6

11Future of canola production

–20

–10

%

10

20

Australia

Euro

pean

Union

Pakista

n

Korea

United

State

s

Japan

Canada

ChinaIn

dia

CanolaSoybeanPalm

Change in oil consumption per person1990-91 to 1999-2000E

Canola 11% Canola 21%

Sunflower17% Sunflower

15%

Soybean14%

Soybean5%Olive

4%

Olive5%

Palm22%

Palm26%

Cotton23%

Cotton19%

Other 9% Other 9%

Australian vegetable oil consumptionF1990–91 1999–2000

declined in India (see footnote 1), where the consumption of palm oilincreased significantly.

Australian consumption of vegetable oils shifted significantly toward canolaoil in the 1990s. Over the decade, Australian demand for vegetable oilsincreased by 25 per cent to 24.5 kilograms per person, or 465 000 tonnes.Canola oil consumption increased twelvefold to 5.0 kilograms per personover the decade to 1999-2000, while the consumption of soybean oil fell byaround 46 per cent to 1.5 kilograms per person. The demand for palm oil(mostly palm olein) and olive oil has also grown over the decade and theirconsumption continues to be a significant proportion of the total fats and oilsin Australian diets (figure F).

Soybean meal remained an important source of protein for Australian live-stock throughout the 1990s, making up over 40 per cent of meal consump-tion throughout the decade (figure G). The consumption of oilseeds meal inAustralia expanded by 42 per cent to 768 000 tonnes between 1990-91 and1999-2000, as intensive livestock production expanded. Canola meal repre-sented 10 per cent of Australian consumption in 1990-91 and 25 per cent in1999-2000, displacing cotton seed meal in overall consumption (figure G).

With small domestic markets for oilseeds products, the Australian canolaindustry has become reliant on export markets. The proportion of Australiancanola production exported increased during the 1990s, to almost 80 per centin 1999-2000 (figure H).

12 ABARE research report 01.6

%

20

40

60

80

100OtherSoybean

CottonseedSunflower

Canola

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

Australian consumption of oilseeds mealG

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-2000

%

20

40

60

80

Australian canola exports as a percentage of productionH

Over the decade to 1999-2000 there was a 45 per cent increase in theAustralian oilseeds crush to 1.2 million tonnes in response to increaseddemand for both vegetable oil and oilseeds meal (table 3). In 1999-2000, 43per cent of the oilseeds crushed in Australia were cotton seed, 31 per centcanola, 13 per cent sunflower and 10 per cent soybean. Between 1990-91and 1999-2000, the global oilseeds crush increased by 33 per cent to around247 million tonnes. The United States, China and the European Union crushednearly 50 per cent of world production during the 1990s. Australian crush-ing of oilseeds to produce vegetable oil and protein meal represents a verysmall proportion (less than 1 per cent) of world production.

13Future of canola production

3 Major oilseeds processing nations in the world

1990-91 1999-2000Growth

Crush Share Crush Share in crush

Mt % Mt % %

Argentina 11.6 6 22.6 8 94Australia 0.8 .004 1.2 .006 33Brazil 14.1 8 21.7 9 54Canada 2.4 1 4.9 2 104China 20.2 11 40.9 16 102European Union 28.5 15 30.2 14 6Former Soviet Union 10.6 6 8.2 3 –23India 17.2 9 19.6 8 14Japan 5.3 3 6.0 2 12United States 36.4 20 47.9 18 32

World 185.7 100 247.3 100 40

Source: US Department of Agriculture (2000a).

Prospects for world oil markets

Market outlookWorld consumption of canola is expected to rise strongly over the projec-tion period, creating a favorable outlook for the Australian canola industry.Key factors that will influence world canola demand to 2010 include: theprice of canola and substitute vegetable oils, population growth and demo-graphic changes, economic growth, changing consumer preferences, anddomestic trade and food policies.

14

2

ABARE research report 01.6

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

$US/t

100

150

200

250

300

Canola

Soybeans

Projected real world indicator prices forsoybeans and canolaI

ABARE’s commodity research using the OECD’s Aglink model projectsthat world indicator prices for canola seed and soybeans will rise slightly inthe medium term, before falling slightly toward 2010 (figure I). Realcommodity prices tend to fall over time in response to increasing produc-tivity. Strong world demand for canola oil is expected to result in increasedcanola and soybean prices to 2002. After 2002, however, prices are projectedto fall in response to increasing world production of low cost soybean andpalm oil.

World supplyThese price projections are derived from a detailed analysis of influences onthe supply and demand of canola and other vegetable oils, as well as world

population and income growth. The potential for the Australian canolaindustry to continue to expand depends on the prospects for favorable worldcanola oil prices relative to the price of substitute vegetable oils. Mostvegetable oils have similar end uses in the food industry and, in many cases,food products are derived by blending vegetable oils. Manufacturers canalter the mix of vegetable oils depending on their relative prices. The rela-tively high degree of substitutability among vegetable oils means that theirprices in international markets are not likely to diverge greatly from eachother, at least in the long run (In and Inder 1997).

World prices, in real terms, for soybean oil, canola oil, sunflower oil andpalm oil for the period 1982-83 to 1999-2000 are shown in figure J. In andInder (1997) examined the relationship between the world prices of eightvegetable oils over the period October 1976 and March 1990. They concludedthat there was a long run relationship between sunflower and soybean, andsunflower and rapeseed, reflecting a high degree of substitution among them.

ABARE’s projections of stable rather than increasing real prices for canolaand soybeans, despite strong projected demand (discussed below), is basedon expected increases in world soybean and palm oil production. Worldproduction of vegetable oils is projected to expand by around 27 per cent to87 million tonnes by 2009-10. This supply outlook will be influenced bypolicy developments in the major producing countries, particularly in theUnited States and China, as well as expanded production in low cost export-ing countries. Palm oil production is expected to increase faster than theproduction of other vegetable oils.

15Future of canola production

1983-84

1985-86

1987-88

1989-90

1991-92

1993-94

1995-96

1997-98

1999-2000

$US/t 1999-2000

200

400

600

800

1000

1200

Sunflower

Soybean oil

Palm oilCanola oil

World vegetable oil pricesJ

In recent years there has been a significant expansion of soybean productionin South America. Between 1995-96 and 2000-01, soybean production inArgentina more than doubled to 25 million tonnes, while in Brazil, soybeanproduction increased by 25 per cent to 35 million tonnes. These recentincreases in South American oilseeds production are expected to be sustainedover the projection period. Investments in infrastructure developments suchas port facilities and privatisation of railways have improved the competi-tiveness of South American grain and oilseeds industries.

The yield of vegetable oil per hectare from palm is around 3.5 tonnes,compared with about one tonne for rapeseed and less than half a tonne forsoybeans. The high productivity for palm oil combined with its relativelylow cost of production (in US dollar terms) means that palm oil plays a signif-icant role in determining the overall price of vegetable oils. Therefore, inperiods when there are abundant supplies of palm oil and palm oil prices arelow, the prices of other vegetable oils are also likely to be low.

Palm oil production is forecast to increase by 36 per cent to 30 million tonnesover the next ten years in the two major producing countries, Malaysia andIndonesia. These two countries account for just over 80 per cent of worldproduction. Given the importance of palm oil to these two economies thegovernments in both countries have provided production incentives. Thevarious schemes used include direct investment by the government, grant-ing access to credit at concessionary rates for estate development, new cropplanting and crushing facilities, and further incentives to both domestic andinternational investors.

Most recently, the Malaysian government has provided a financial incentiveof 1000 ringgit per hectare for replanting palm trees. This is because a largeportion of oil palms in Malaysia are more than 25 years old, and new higheryielding varieties are now available. The government is aiming to have alarge percentage of these palms replanted by the end of 2001. However, theextent of the growth in palm oil production will be somewhat curbed byacreage limitations in west Malaysia and also by labor shortages and risingproduction costs relative to the prices received (Oil World 2001).

In the second half of the 1990s world palm oil production expanded at around7–9 per cent a year, leading to increased stocks and low prices. However,the growth in palm oil production, experienced in recent years, is expectedto slow over the next three or four years. As palms need four to five yearsgrowth before oil production becomes commercial, reduced palm plantings

16 ABARE research report 01.6

during the Asian financial downturn of 1997–99, particularly in Indonesia,will reduce medium term production. However, reduced Indonesian produc-tion in the medium term is expected to be offset by increased production inMalaysia and central America.

World demandABARE’s projection of strong demand for canola oil is based on an analy-sis of world production and prices, population growth, economic growth andchanging consumer preferences. Population growth in developing countriesis expected to result in an increase in the world demand for canola oil. Strongpopulation growth in China and India is expected to be a major influence onworld demand for oilseeds products, including canola. The population growthrate in China is expected to increase slightly in the short term, and besustained at an average of around 1 per cent to 2010. India’s population isexpected to continue increasing at around 1.8 per cent a year over this period.

In developed countries, increases in population are expected to be slow, thusincreases in the consumption of canola oil are expected to be more closelyrelated to changes in consumer preferences. For example, although the popu-lation of Australia is assumed to increase gradually to 2010, factors such ashealth awareness are likely to have a greater impact on the demand foroilseeds products.

Economic growthThere is a strong relationship between consumption of vegetable oil andincomes (figure K). The potential for increased consumption of oils per

17Future of canola production

K

0

5

10

15

20

25

30

0 5 10 15 20 25 30 35

Relationship between vegetable oil consumption and income, selected countries

GDP, purchasing power parity, per person (US$’000)

Co

nsu

mp

tion

pe

r pe

rso

n (

kg)

United States

Greece

Iraq

Nigeria

Pakistan

ThailandUruguay

SloveniaMexico

Saudi Arabia

Malaysia

MaltaKorea

Chile

Turkey

Vietnam

Indonesia

Papua New Guinea

Denmark

Norway

Australia

Japan

Netherlands

Ge

rma

ny

AustriaCanada

PhilippinesChinaIndiaEgypt

Egypt

Sweden

Russian Fed.

United Arab Emirates

NewZealand

Kuwait

Spain

PortugalCyprus

Czech Republic

Brazil

S Afric

a

Argentina

Iran

Italy

Belgium-Luxembourg

person is highest in developing countries where low incomes have limitedconsumption to very low levels. In contrast, per person consumption is highin developed countries, with less potential to increase as incomes increase.Economic growth, particularly in developing countries, is therefore likelyto have a strong influence on the world demand for canola oil.

World economic growth is assumed to average around 3.7 per cent a yearover the medium term to 2005. An easing of world economic growthcompared with the previous five years reflects an expected moderation ofstrong economic growth in the United States. The US economy is the largestin the world and its economic performance, and hence import demand, cansignificantly influence world markets. Over the medium term, economicgrowth in the United States is assumed to average around 3.0 per cent a year.

The economic prospects for non-OECD Asia (which excludes Japan andKorea) in the short term is largely dependent on movements in world crudeoil prices and economic developments in the United States. Economic growthin the region is expected to remain relatively robust, provided import demandin the United States does not decline sharply and oil prices do not increasesubstantially. For non-OECD Asia as a whole, economic growth is assumedto ease marginally from 6.8 per cent in 2000 to 6.2 per cent in 2001 and 6.0per cent a year over the medium to long term.

The economic recovery in east and south east Asia is expected to continuein the short term. In the Republic of Korea, recent indicators suggest thateconomic growth is likely to moderate to a lower but more sustainable ratein 2001. Economic growth in Korea is assumed to ease from an estimated9.2 per cent in 2000 to 5.0 per cent a year over the long term. For south eastAsia as a whole, economic growth is assumed to moderate from 5.7 per centin 2000 to 4.3 per cent in 2001. With economic conditions assumed toimprove in Indonesia, economic growth in south east Asia is assumed tostrengthen to around 5.0 per cent a year over the medium and long term.

In China, strong economic growth continues, with the economy recordinggrowth of around 8.0 per cent in 2000, compared with 7.1 per cent in 1999.Despite the recent improvement in China’s economic performance, consid-erable reforms, especially in the banking sector, are still required to sustainhigh economic growth. The expected entry of China into the World TradeOrganisation, which will increase external competition in many parts of theeconomy, underscores the need to accelerate structural reform in China.

18 ABARE research report 01.6

Economic growth in China is assumed to average 7.8 per cent in 2001 and7.0 per cent a year over the medium to long term.

In India, the domestic economy has been displaying signs of weakeningactivity. High oil prices have placed upward pressure on inflation, as well ason the current account deficit. Economic growth in India is assumed to aver-age around 6.0 per cent in 2001, compared with 6.0 per cent in 2000 and 6.4per cent in 1999. Over the medium and long term, economic growth isassumed to average 5.5 per cent a year.

In Latin America, economic prospects have improved over the past year.Higher oil prices have benefited a number of regional economies, such asVenezuela, Mexico and Colombia. Higher copper prices have providedeconomic support for Chile. For Latin America as a whole, economic growthis assumed to average around 3.5 per cent in 2001, compared with an esti-mated 3.5 per cent in 2000 and weak growth of 0.1 per cent in 1999. Beyond2001, economic growth in the region is assumed to average 3.7 per cent ayear.

Consumer preferencesWhile population growth, economic growth and exchange rates influenceoverall demand for oilseeds products, consumer preferences have a stronginfluence on the demand for canola products relative to those derived fromother oilseeds. Health considerations are expected to continue to have a stronginfluence on the demand for canola oil versus other vegetable oils. Otherinfluences on consumer preferences for oilseeds products include the use ofgenetically modified varieties and environmental benefits of vegetable oilsin industrial applications.

Health considerationsOne of the most important influences on world demand for canola oil hasbeen growing consumer awareness of the health benefits of replacing satu-rated vegetable oils and animal fats with monounsaturated and polyunsatu-rated oils. These oils have been found to help reduce cholesterol levels, whichhas been linked to reduced incidence of cardiovascular disease (Verheijenand Jimmink 1995). Animal fats (excluding fish oil), coconut oil, palm oiland palm kernel oil are high in saturated fats and are being replaced wherepossible by health conscious consumers with vegetable oils that are low insaturated fats. Relative to other vegetable oils, canola has the lowest levelof saturated fats and is a source of omega 3 fatty acids that have been demon-

19Future of canola production

strated to reduce blood cholesterol and cardiovascular disease levels (Morris2000).

The health benefits of canola oil have attracted more health consciousconsumers who have been able to pay premiums for vegetable oils that havea lower saturated fat content. The preference for monounsaturated oils hassignificantly increased the growth in demand for canola over other vegetableoils such as sunflower, soy and palm oils in developed countries, and thissubstitution is expected to continue. Research into differences in qualitybetween Australian and Canadian canola revealed that Australian canolaaveraged a higher level of omega 3 fatty acid (Adolphe 2000). High omega3 content could attract consumers to Australian canola until Canadian produc-ers select canola varieties that match these attributes.

In developing countries, the health benefits of canola oil are only beginningto be recognised and incorporated into the changing diets of their popula-tion. For example, canola oil is becoming popular among health consciousconsumers in Pakistan because of the high quality of the oil, leading to inter-est from within the private processing sector (Akhtar 1998). This interestmay lead to greater demand for canola imports into Pakistan over the mediumterm until local producers increase domestic production. However, pricecontinues to have a strong influence on demand in developing countries, andlower cost palm and soybean oils continue to be attractive to less wealthyconsumers.

Genetically modified canolaGenetically modified oilseeds varieties have emerged as another major influ-ence on world demand in the late 1990s. A consumer reaction against per-ceived health risks and genetic ‘contamination’ associated with GM cropshas resulted in some countries imposing strict labeling regulations on imports.The consumer reaction has already resulted in the European Union membercountries only importing canola seed that is GM free. EU imports of canolafrom Australia were substantial in 1998-99 and again in 2000-01, whileCanada has been unable to export to this market because of the GM statusof its canola. It is unclear whether consumer concerns about GM canola willfade or intensify toward 2010. Australia may face a growing demand fornon-GM canola, but only by incurring the substantial costs for identity preser-vation if GM canola is adopted and by forgoing its agronomic benefits if itis not adopted.

20 ABARE research report 01.6

Consumers in north America appear to have largely accepted products madefrom genetically modified inputs. However, as consumers have become moreaware of the existence of these products in the food chain, there has beengrowing demand for access to certified GM free foods. This has been partic-ularly so in Europe.

Consumer concerns are focused on the perceived safety of GM products infood, possible environmental consequences of releasing GM varieties, andthe extent of control that appears to be exercised by a few companies thatown key gene technologies. Some livestock feeders in Europe, Japan,Thailand and the Republic of Korea are now indicating that they will notfeed genetically modified feedstuffs to their animals because of possibleramifications for demand for their meat products.

In response to perceived safety concerns, a number of countries have imple-mented market access restrictions and conditions. The European Unionenforces the most significant trade restrictions. It does not allow the importof any genetically modified crops other than soybeans and some forms ofcorn. Moreover, there is a trend toward mandatory labeling of productscontaining genetically modified materials on the grounds that this enablesconsumers to make more informed decisions. Mandatory labeling can be asignificant barrier to trade because of the costs imposed on suppliers to sepa-rate GM and non-GM foods in handling and storage. While the EuropeanUnion already requires labeling, other key grain importers, Japan and Korea,intend to introduce labeling from mid-2001.

Some marketers are claiming that they are earning premiums for non-GMcanola in world markets. For example, it was reported in August 2000 thatEuropean buyers paid a premium of up to a US$5 a tonne on 150 000 tonnesof Australian non-GM canola (Reuters, 20 August 2000).

The developments to date in world grain markets are indicative of a pricediscovery phase in which marketers and processors are trying to determinewhether consumers are willing to pay premiums for grain and grain prod-ucts that are certified GM free. A clearer picture should emerge in the firsthalf of 2001 as the new season’s northern hemisphere grain crops — partic-ularly the US soybean and corn crops, both of which will include a substan-tial proportion of genetically modified product — are brought to market, andas the influence of mandatory labeling regimes scheduled to start in Asia inmid-2001 begin to exert an influence.

21Future of canola production

Environmental concernsConsumers appear to be placing increasing importance on environmentalissues affecting the products they consume. This could have an impact onfuture demand for oilseeds, particularly in developed countries. For exam-ple, research into the use of vegetable oil lubricants and fuels as a substitutefor mineral oils could lead to more widespread use of vegetable oils for indus-trial purposes (Verheijen and Jimmink 1995). Although there would be coststo the environment from producing industrial vegetable oil, the ‘green andclean’ perception may cause these biofuels to be preferred over mineral oilsby some consumers.

22 ABARE research report 01.6

Prospects for trade

Prospects for the Australian canola industry will be influenced by changesin its comparative advantage relative to major competitors, especially Canada,and policies affecting world oilseeds and vegetable oils trade. The potentialagronomic benefits of Canada’s adoption of genetically modified canola needto be assessed in the light of potential consumer reactions. Domestic supportpaid to producers in the United States and the European Union reduces theirimport demand and increases world exportable supplies of canola, depress-ing world prices. Import tariffs imposed by China, India, Japan and Pakistanto protect domestic oilseeds producers increase domestic prices for commodi-ties and reduce demand, lowering world prices. The speed and extent of tradeliberalisation achieved through WTO negotiations will have a significanteffect on access to growing world markets.

World canola tradeThe European Union and Japan have been significant importers of oilseeds,while China has recently become a major importer (table 4). China and Japanwere the world’s largest importers of canola seed in 1999-2000, with grow-ing markets in Mexico, Pakistan and Bangladesh.

The United States, Brazil and Argentina have dominated world exports ofoilseeds (table 5). Canada has been by far the largest exporter of canola,with Australia contributing nearly a quarter of total world exports in 1999-2000.

Australian oilseeds exports, principally canola and cotton seed, are exportedto Japan, Bangladesh and Mexico (figure L). In 1999-2000, China becamethe major destination for Australian canola exports, importing around 1.2million tonnes of seed.

The value of the Australian dollar against the currencies of other exportingnations has a marked influence on the competitiveness of Australian canolaon world markets. The rate at which the Australian dollar can be exchangedagainst the currencies of major importing countries, including China, theUnited States, the European Union and Japan, influences the relative cost ofAustralian exports to these markets.

23

3

Future of canola production

24 ABARE research report 01.6

4 World importers of oilseeds, excluding intra-European Union trade

1990-1991 1999-2000

Imports Share Imports Share

kt % kt %Total oilseedsChina 17 0.1 10 336 17.9Chinese Taipei 2 208 7.1 2 350 4.1European Union (net imports) 13 885 44.6 18 304 31.7Japan 6 593 21.2 7 169 12.4Korea, Rep. of 1 022 3.3 1 751 3.0Mexico 1 915 6.2 5 480 9.5Middle East 510 1.6 2 166 3.8Other 4 985 16.0 10 122 17.5

World 31 135 100.0 57 678 100.0

CanolaBangladesh 40 1.4 200 3.1China 15 0.5 2 500 38.8Japan 1 892 68.1 2 100 32.6Mexico 270 9.7 910 14.1Pakistan 0 0.0 350 5.4Other 562 20.2 377 5.9

World 2 779 100.0 6 437 100.0

5 World exporters of oilseeds, excluding intra-European Union trade

1990-1991 1999-2000

Exports Share Exports Share

kt % kt %Total seedsArgentina 4 849 16.6 5 225 8.9Australia 187 0.6 2 446 4.2Brazil 1 647 5.6 10 903 18.5Eastern Europe 382 1.3 803 1.4Former Soviet Union 404 1.4 2 147 3.6United States 15 640 53.6 27 460 46.7Other 6 073 20.8 9 868 16.8

World 29 182 100.0 58 852 100.0

CanolaAustralia 0 0.0 2 034 24.3Canada 1 859 84.0 4 350 52.0Eastern Europe 323 14.6 472 5.6United States 14 0.6 275 3.3Other 16 0.7 1 240 14.8

World 2 212 100.0 8 371 100.0

Over the short to medium term, the Australian dollar is assumed to appre-ciate gradually from below US50c in 2001, both against the US dollar andon a trade weighted basis. By 2005, the Australian dollar is assumed to aver-age around US67c and TWI 57, compared with an average of US58c andTWI 52 in 2000.

Over the past two years, the US dollar has appreciated significantly againstother major international currencies, especially the euro. The significantappreciation of the US dollar appears to have been supported by favorablefinancial market sentiment stemming from the strong growth achieved in theeconomy. As strong economic growth eases in the United States, the USdollar is assumed to depreciate gradually in the short term. A lower US dollaris expected to increase the competitiveness of US soybeans on world markets.Over the medium term, the US dollar is assumed to continue to depreciateagainst the euro, but remain relatively stable against the Japanese yen.

Competing and trading nations

Australia’s comparative advantage versus CanadaThe Australian canola industry’s ability to expand its share of world canolatrade depends in part on its comparative advantage relative to other worldproducers, particularly Canada. Gross margins can be used as a crude measureof comparative advantage between canola producing regions in Australiaand Canada. Gross margins are derived by subtracting variable costs fromthe gross income generated by each farm enterprise. The main shortcomingof gross margins is that they do not take account of capital costs associated

25Future of canola production

kt

200

400

600

800

1000

1989-90

1990-91

1988-89

1991-92

1992-93

1993-94

1994-95

1995-95

1996-97

199798

199899

1999-2000

Volume of Australian oilseeds exports, by destinationL

Pakistan

Mexico

Malaysia

Japan

China

Bangladesh

with land, plant and machinery, or labor costs other than those included incontracted operations. This comparison between Australian and Canadiancanola production assumes that labor and capital costs are similar betweenregions, which may not be true. It should also be noted that the gross marginestimates come from a number of different sources; where possible adjust-ments have been made to account for differences in estimation methods.

Some benchmarks of production costs and gross margins in the key produc-ing regions of Australia and Canada are shown in table 6 and illustrated infigure M. For the purposes of comparison, the same information for conven-tional and genetically modified (herbicide tolerant) canola in Canada hasbeen converted to Australian dollar terms. Genetically modified canola makesup around 55 per cent of total Canadian canola plantings.

On the basis of gross margins for Australian regions, canola production seemsto be most profitable in the Wimmera region of Victoria ($319 a hectare).The most marginal (and probably not profitable) region shown in the tableis the Victorian Mallee region ($47 a hectare). In Canada, genetically modi-fied varieties of canola are more profitable than conventional varieties —$152 a hectare compared with $115 a hectare. The Canadian estimates ofgross margins are roughly in the mid to lower range of the estimates for theAustralian regions.

26 ABARE research report 01.6

Production costs and gross margins for canola,Australia and CanadaM

Genetically modified

Conventional

Scaddan

Katanning

North Central

Mallee

Wimmera,

North east zone

East central zone

0 50 100 150 200 250 300

Gross marginVariable costs

New South Wales

Victoria

Western Australia

Canada

Canada is virtually the only producer of genetically modified canola; smallquantities are also grown in the United States. The other main canolaexporters — the European Union and Australia — are free of geneticallymodified canola, apart from production from field trials that does not enter

27Future of canola production

6 Production costs and gross margins for canola in Australia and Canada,2000

New South Wales Victoria

Central Northern Northzone, east a zone, west Wimmera Mallee central

A) Unit price $/t 250 250 250 250 250B) Average yield t/ha 1.80 1.20 2.00 1.00 2.00

C) Gross returns (A x B) $/ha 450 300 500 250 500

Variable costsSeed $/ha 12 1 15 30 15Herbicides $/ha 49 42 36 39 43Fertiliser $/ha 110 39 69 71 73Machinery operations $/ha 94 86 57 57 86Other $/ha 26 22 4 6 17

D) Total variable costs $/ha 290 189 181 203 234

Gross margin (C – D) $/ha 160 111 319 47 266

Canada b

Western Australia Conven-tional Genetically

Katanning Scaddan canola modified c

A) Unit price d $/t 250 250 233 238B) Average yield t/ha 1.45 1.40 1.79 1.97

C) Gross returns (A x B) $/ha 363 350 417 469

Variable costsSeed d $/ha 13 18 36 86Herbicides $/ha 26 45 65 39Fertiliser $/ha 69 62 76 81Machinery operations $/ha 53 54 120 106Other $/ha 5 4

D) Total variable costs $/ha 161 179 303 317

Gross margin (C – D) $/ha 201 171 115 152

a Short fallow. b Converted to A$ at an exchange rate of A$1=C$0.86. c With genetically modifiedcanola includes technology fee. d For Canada includes dockages for foreign material in grain samples.Sources: ABARE (1999); Serecon et al. (2001).

the market through bulk handling systems. Canada has developed a rangeof canola varieties that are resistant to herbicides (glyphosate, glufosinateammonium, bromoxynil and ioxynil). The adoption rate with these varietieshas been very strong and they are now estimated to make up around 60 percent of total Canadian canola area. Canada also has conventional varietiesof canola that have been bred to be herbicide tolerant. Plantings of canolain Canada declined in 2000 but the evidence to date is that the share of genet-ically modified varieties was maintained (figure N).

Canada does not, at any stage, segregate the crop into GM and non-GM cate-gories. From figure O it can be seen that Canadian canola appears to havenot incurred a discount in world markets in recent years compared withAustralia, despite the anecdotal evidence of increasing consumer concerns

28 ABARE research report 01.6

N

1995 1996 1997 1998 1999 2000

Canadian plantings of genetically modified canola

million ha

1

2

3

O

1997-98 1998-99 1999-2000

Canola/rapeseed stocks and prices

US$/t

100

150

200

250

Other

StocksEuropean Union

Canada

Mt

0.5

1.0

1.5

2.0Australian price

Canadian price

over genetically modified products. One possible explanation of this is thatthere are enough nongenetically modified supplies from Australia and theEuropean Union to meet requirements simply through adjustments in thepattern of world trade.

The United States

• The United States is the world’s largest soybean producer and in 1999exported an estimated 26 million tonnes.

• Depressed oilseeds prices since 1998 have led to an increase in supportpayments in the United States. Although these measures are onlytemporary, and do not directly intervene in trade, some of them arelinked to market prices and indirectly cause production and exportsupplies to be higher than would otherwise be expected.

The majority of agricultural support in the United States has been providedthrough domestic income support programs. Of particular interest to thecanola industry is the soybean loan program, which in the past provided asource of short term liquidity to producers until they sold their crop. However,strong US and global production in more recent times have led to buildingstocks and a reduction in market prices for soybeans to well below thesoybean loan rates.

In 1991 the introduction of marketing loan provisions to the commodity loanprogram for soybeans was designed to change the nature of domestic supportfor soybeans from the price supporting role of the earlier loan programs.Marketing loan provisions allow repayment of commodity loans at less thanthe original loan rate when market prices fall below the market loan rate.The difference between the original loan rate and the loan repayment rate isreferred to as the marketing loan gain and represents a program benefit toproducers, with US taxpayers covering the cost.

At the end of a loan period the farmer can choose to forfeit ownership of thecollateral (the crop) to the government and retain the loan money rather thanrepay the loan with interest. With market prices falling to levels lower thanthe loan rate, producers are better off financially to simply keep the loanpayment. Furthermore, the loan rate provides the incentive to plant the cropregardless of low prices because market receipts are augmented by the loanbenefits.

29Future of canola production

Therefore, marketing loans have and will continue to raise US soybeanproduction above otherwise expected levels and thus place downward pres-sure on world oilseeds prices. This system is supposed to decrease the loanprogram’s potential effect on support prices because stock accumulation bythe government through loan defaults is reduced. However, the marketingloan gain to producers means that production decisions are related to theloan rate rather than the market price and the area planted to supported cropsis higher than it would be without the support program. The net outlay fordomestic support payments for soybeans is estimated to be US$2.7 billionfor 2000 and US$3.3 billion for 2000.

Compounding the distorting effects of the marketing loan program was anagreement by the US government to provide additional support funds in theform of lump sum payments to reduce the impact of depressed commodityprices when agricultural prices fell in 1998 and 1999, reducing the risksfacing US producers (Turner et al. 2000). This year, a US$1.64 billion bailoutpackage has been earmarked for commodities not covered by market tran-sition contracts, including soybeans, peanuts, tobacco, fruit and vegetables.

In addition to these payments, a further US$8.2 billion will go to reducingpremiums on federally subsidised crop insurance over the next five years.

The effects of these various support payments are not offset by the acreagereduction programs, as was the case prior to 1996. Therefore, it is no longercertain whether the US reforms since the Uruguay Round have reducedmarket distortions arising from farm support programs (Roberts et al. 2000).The outlook for oilseeds exports from the United States is partly associatedwith farm programs that are due for reauthorisation in 2002 and partly withthe temporary assistance programs whose future is uncertain (OECD 2000c).

The European Union

• The European Union accounts for around a quarter of world canolaimports and in 1998-99 was Australia’s third largest export market.

• Reductions in producer payments for oilseeds production plannedunder Agenda 2000 are expected to result in a drop in EU canolaproduction.

After World War II, an underlying concern over food security influenced EU policy makers to implement a system that protected agriculture, while

30 ABARE research report 01.6

removing barriers to trade internally. This approach resulted in the EuropeanUnion changing from being a net importer of food to a large net exporter offood, and the Common Agricultural Policy (CAP) was soon used to managesurpluses.

In 1999, agreement on the reform of the CAP, referred to as Agenda 2000,was reached at the Berlin Summit (US Department of Agriculture 1999b).This covered a range of agricultural and other issues, including reform ofsupport policies for cereals and arable crops. These reforms were a contin-uation of those introduced in 1992 that reduced market support but largelycompensated producers by making direct payments (based on areas plantedfor cereals). The main components of the Agenda 2000 agreement directlyapplicable to oilseeds include:

• a reduction in direct payments for oilseeds of more than 30 per cent inthree equal steps to 63 euro a tonne by 2002-03;

• compulsory and voluntary set-asides maintained, with compensation beingset at 63 euro a tonne and payment commencing in 2001-02 — the nominalset-aside rate will be reduced from 17.5 per cent to 10 per cent in 2000-01 for arable crops, while the actual set-aside rate to be applied will beadministratively determined (Turner et al. 2000).

While the base compulsory set-aside rate will be 10 per cent, the actual rateapplied may vary from this. Historically, the actual set-aside rate has oftenbeen far lower than the base rate, particularly when world commodity marketprices were high. For example, in 1996-97 when the base set-aside rate was17 per cent, the actual rate was 10 per cent following high world prices in1995, and dropped further to 5 per cent in 1997-98. The result was greaterproduction from EU producers, which contributed to larger stocks anddepressed world prices in 1997-98. It is expected that actual set-aside rateswill again be lower than the base set-aside rates to 2010, resulting in increasedsupply and low world prices.

Other components of the agreement that, while not directly applicable tooilseeds, will have a significant impact on the area of oilseeds planted include:

• a reduction in the cereal intervention price of 15 per cent in two equalsteps as of 1 July 1999;

• the direct payments for cereals, fixed on an area basis, increased in twoannual steps from the current 54.34 euro a tonne to 63 euro a tonne forthe 2001-02 marketing year — the payment will be based on the area

31Future of canola production

actually planted to arable crops and fixed regional yields established underthe 1992 reforms; the increase in direct payments accounts for 50 per centof the intervention price cut (Turner et al. 2000); and

• supplementary aid for protein crops will be set at 9.5 euro a tonne, in addi-tion to the 63 euro a tonne area payment.

Overall, the change in support under Agenda 2000 means that the area plantedto cereals is likely to increase as farmers move away from oilseeds. As willbe discussed in chapter 4, oilseeds production is likely to fall under Agenda2000 relative to the level expected without the policy changes. The impactof lowering the base set-aside rate is expected to be minimal, because thebase rates were rarely, if ever, enforced under the CAP 1992 reforms.

Direct payments provide some incentive to at least maintain, if not increase,the area planted in order to maintain or increase the size of payments, as thepayments are based on current areas planted (Turner et al. 2000). Furthermore,this shift in production away from oilseeds toward cereals may lead to aslight fall in demand for oilseeds meal as the increased cereal supply isexpected to make the price of cereals for feed use more attractive to somelivestock producers (US Department of Agriculture 2000b).

As will be discussed in chapter 4, the Agenda 2000 reforms are expectedto have a small beneficial impact on world oilseeds trade, due to lower EUproduction and higher imports. Currently, oilseeds and oil meals can beimported duty free into the European Union while duties for vegetable oilare generally lower than 10 per cent. Since the implementation of theUruguay Round, the European Union has not used export subsidies forcanola although the WTO schedule of the European Union still includes asubsidy quantity and outlay commitment level for canola exports (USDepartment of Agriculture 2000d).

It is assumed therefore that total imports of both oilseeds and edible oilswill need to increase over the long term in order to meet the EuropeanUnion’s increasing vegetable oil demands if the expected shift away fromoilseeds production does occur. Furthermore, canola may be a more favor-able option to some crushers because of its high oil and low meal compo-nent compared with other substitutes, particularly soybeans, if a small shiftdoes occur away from oilseeds meals toward cereals for feed use in live-stock production.

32 ABARE research report 01.6

China

• Vegetable oil consumption in China increased from 6.5 million tonnesto an estimated 11.4 million tonnes between 1990-91 and 1999-2000,and now accounts for around 13 per cent of total world vegetable oilconsumption.

• Australia began exporting canola to China in 1997-98 with 132 600tonnes, increasing to an estimated 1.2 million tonnes in 1999.

• China’s planned accession to the World Trade Organisation isexpected to have a significant impact on demand for vegetable oil,increasing oil imports and dampening the recent growth in demandfor imported oilseeds.

China’s agricultural policies have a significant impact on the pattern of worldoilseeds trade. As Australia’s largest canola export market, changes in marketaccess have implications for the canola industry. An increase in market accessseems likely as China is currently in the process of trying to gradually reducetrade protection in order to become a member of the WTO.

The Chinese government still supports a policy of self sufficiency, the objec-tives of which arose for three main reasons. First, China has historicallysuffered from several food shortages that resulted in starvation, politicalturmoil and rural uprising. Second, during the 1950s to the 1970s, thirtyyears of isolation and frequent political conflict with the United States andother western countries made the Chinese government very cautious aboutrelying on international grain markets for its food supply. Third, Chinesepolicy makers have been concerned that the international grain market maynot be able to meet the demands of China’s increasing population if a foodshortage was to occur.

The policy of self sufficiency in food has had a number of significant impacts,such as extremely high pressure on natural resources, and the loss of compar-ative advantage through the increasing cost of grain production. It also hasa significant impact on international trade. However, markets for almost allnongrain products (soybean oil and cotton were exceptions) were liberalisedby the 1990s. China is now the largest world importer of oilseeds, whichhave partly replaced imports of soybean meal and oil.

This recent shift in policy is designed to promote and protect the domesticcrushing industry. The objective of expanding China’s oilseeds crushing

33Future of canola production

capacity has resulted in general tariffs on seed being reduced, in contrast tothe high tariffs imposed on imports of oil (OECD 2000c).

The recent increase in demand for vegetable oil, coupled with restricted oiland meal imports, has led to a greater emphasis on imports of canola seed(which has a high oil content) to satisfy oil needs. As a consequence,Australian canola producers have exported increasing quantities of canolaseed to China (US Department of Agriculture 1999a).

Currently, high in- and out-of-quota duties (US Department of Agriculture2000b) effectively eliminate the feasibility of exporting canola oil to Chinaand provide incentives for processors to smuggle vegetable oil, particularlycheap palm oil. The Chinese government began trying to stop smuggledvegetable oils during 1998 and 1999 and strictly regulated the allowablequota of imported vegetable oils. The result was a substantial increase inChinese imports of canola seed because of the higher percentage of oil contentrelative to other oilseeds (Doud 1999). Domestic processors have the addedincentive of crushing imported seed and then reexporting the meal and oil,after which they have the tariff refunded. Domestic production of canola oilhas increased in response to agricultural reforms that have resulted in a shiftout of grain production in favor of canola (US Department of Agriculture2000b).

Over the next decade vegetable oil consumption in China is expected tocontinue to rise as the population increases and incomes continue to grow.Domestic oilseeds production is expected to increase in response to higherdemand for oil. It is assumed that there will still be a deficit between thequantity of oilseeds demanded for crush consumption and the quantity ofoilseeds produced domestically. Thus imports of oilseeds are expected toincrease.

The current market situation is likely to change, however, if China’s progresstoward accession to the WTO gains pace. WTO membership is conditionalon agreed liberalisation of China’s oilseeds, vegetable oil and oil mealmarkets. This involves negotiations between China and other WTO membercountries. The timing of China’s accession to the WTO is currently uncer-tain, but is expected to be slow.

34 ABARE research report 01.6

Japan

• In 1999, Japan imported around 2.2 million tonnes of canola.

• Japan is Australia’s second largest export destination.

• The government of Japan introduced mandatory labeling require-ments for 24 foods containing genetically modified ingredients fromApril 2001.

Soybeans and peanuts are the two major oilseeds produced in Japan, andcanola is imported almost exclusively for crushing. Australia has become astable supplier of canola to Japan, securing about a 10 per cent share of thatmarket. Canada holds the largest market share (around 73 per cent in 1999).Demand for canola depends on its import price and the import price ofsoybeans, as these products are substitutes in the Japanese oil market.Therefore, the use and level of tariffs imposed on these two products havea significant impact on canola demand, and thus influence Australia’s accessto this market.

Japan follows a policy of maximising self-sufficiency, providing assistanceto the agricultural sector primarily through administered prices and tariffs.There are no tariffs on imports of canola and soybeans, or their respectivemeals. This encourages domestic crushing rather than importing vegetableoil products. The oil is used for human consumption and the canola andsoybean meal is the primary protein in animal feed production, and is alsoused as fertiliser. Japan maintains high tariffs on oil, with both canola crudeoil and soybean crude oil currently subject to an import duty of 10.90 yen akilogram, down from 11.92 yen a kilogram in 1999 (US Department ofAgriculture 2000c).

Prolonged weak economic growth may cause imports of canola to declineslightly in the short term. However, there is potential for Australia to lift itsmarket share as the government of Japan officially announced a mandatoryGM labeling policy on selected foods beginning April 2001 (US Departmentof Agriculture 2000c). Some manufacturers may start seeking non-GM canolaoil in reaction to this policy. This may result in a lift in imports of Australiannon-GM canola at the expense of GM canola from Canada, assuming thatAustralia either segregates GM canola through the production and exportchain, or opts not to adopt GM canola.

35Future of canola production

Over the longer term, pressure from the WTO process may reduce the tariffson vegetable oils. The government of Japan has repeatedly stated that anytariff reduction should be the subject of negotiation under WTO negotiations(US Department of Agriculture 2000c). Depending on this outcome, theremay be potential for Australia to export canola oil to Japan.

India

• Total vegetable oil consumption in India reached an estimated 10million tonnes in 1999-2000, with canola accounting for 17 per cent.Most of the canola oil consumed was sourced from domesticallyproduced canola.

• Canola and mustard oils are the dominant oils produced in India —around 1.6 million tonnes were produced in 1999 — with productiongreater than that of peanut and soybean oil.

• The potential for Australia to export to this large oil consumer willdepend on continued reductions in trade barriers negotiated inconjunction with the WTO.

Reflecting the low cost of palm oil, consumption of that oil has risen in India— to an estimated 3 million tonnes in 1999. Canola oil was the second largestedible oil consumed in India in the same year, with consumption estimatedat around 2 million tonnes. In contrast to palm oil, which is almost entirelyimported, around 85 per cent of canola oil was produced domestically. In1998-99 around 10 000 tonnes of Australian canola was exported to India.

Canola production in India increased rapidly in the late 1980s, reflecting theIndian government’s desire to attain self sufficiency and reduce large importsof edible oil (Chand and Jha 2000). Until 1994 the oilseeds sector wasprotected through volume restrictions on imports and exports, as well as highimport tariffs. Domestic prices of oilseeds were maintained at more thandouble the world price.

In 1995 import duties were increased following the removal of quantitativeimport restrictions in order to strengthen domestic oil prices and thus expanddomestic production. This was designed to provide better margins to localcrushers and refiners and to satisfy the considerable expansion in domesticvegetable oil demand.

36 ABARE research report 01.6

In July 1999, minimum support prices for oilseeds were raised. This wasaimed at boosting the production of oilseeds, which had remained stabledespite increasing vegetable oil demand, as relatively more attractive supportprices for other crops such as sugar and wheat discouraged oilseeds produc-tion (OECD 2000c).

Under WTO obligations, members are committed to phasing out many protec-tion measures, including trade restrictions on agricultural products, as theydistort world oilseeds markets. India, however, was allowed to maintainquantitative restrictions on some commodities to assist with the balance ofpayments. High tariff ceiling bindings for many agricultural products werealso negotiated. Quantity restrictions are scheduled to be abolished by 2003,although their tariff replacements will be relatively high (OECD 1999a). Forexample, from 1 January 2000, the import duty on refined edible oils wasraised from 16.5 per cent to 32.6 per cent.

Increased oilseeds production resulting from higher domestic support isexpected to increase production of canola in India to 2010. However, twostrong demand factors will have an impact on canola oil imports. First, India’spopulation is expected to continue to increase, with a resultant increase inthe demand for vegetable oils and, second, an income related trend towardhigher oil consumption levels per person is expected to continue.