fubon financial holdings - mz asia-pacific fhc _2016 eu ndr... · emerging stock trading 2 17.27%...

TRANSCRIPT

Fubon Financial Holdings

2016.06

1

Disclaimer

This meeting may contain forward-looking statements with respect to the financial condition,

results of operations and business of the company. These forward-looking statements

represent the company’s expectations or beliefs concerning future events and involve known

and unknown risks and uncertainty that could cause actual results, performance or events to

differ materially from those expressed. Certain statements, such as those that include the

words “potential”, “estimated”, and similar expressions or variations on such expressions may

be considered “forward-looking statements”. Financial numbers in this report may include

preliminary unaudited numbers or management accounts.

2

Agenda

Fubon FHC overview

Taipei Fubon Bank

Fubon Life

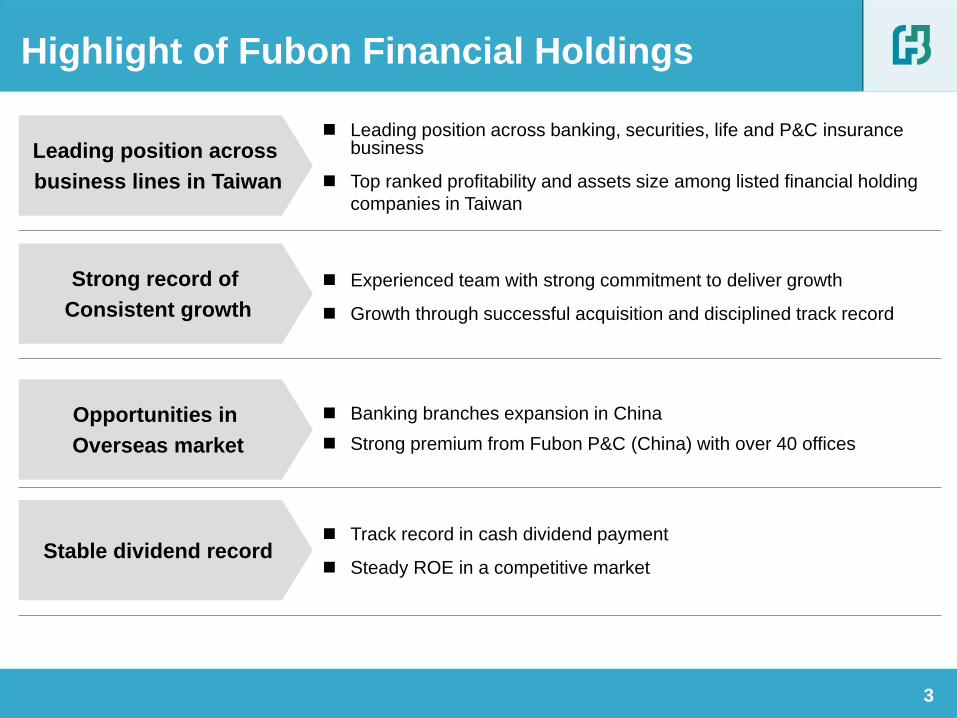

Highlight of Fubon Financial Holdings

Leading position across

business lines in Taiwan

Leading position across banking, securities, life and P&C insurance business

Top ranked profitability and assets size among listed financial holding

companies in Taiwan

Track record in cash dividend payment

Steady ROE in a competitive market

Banking branches expansion in China

Strong premium from Fubon P&C (China) with over 40 offices

Experienced team with strong commitment to deliver growth

Growth through successful acquisition and disciplined track record

Strong record of

Consistent growth

Opportunities in

Overseas market

Stable dividend record

3

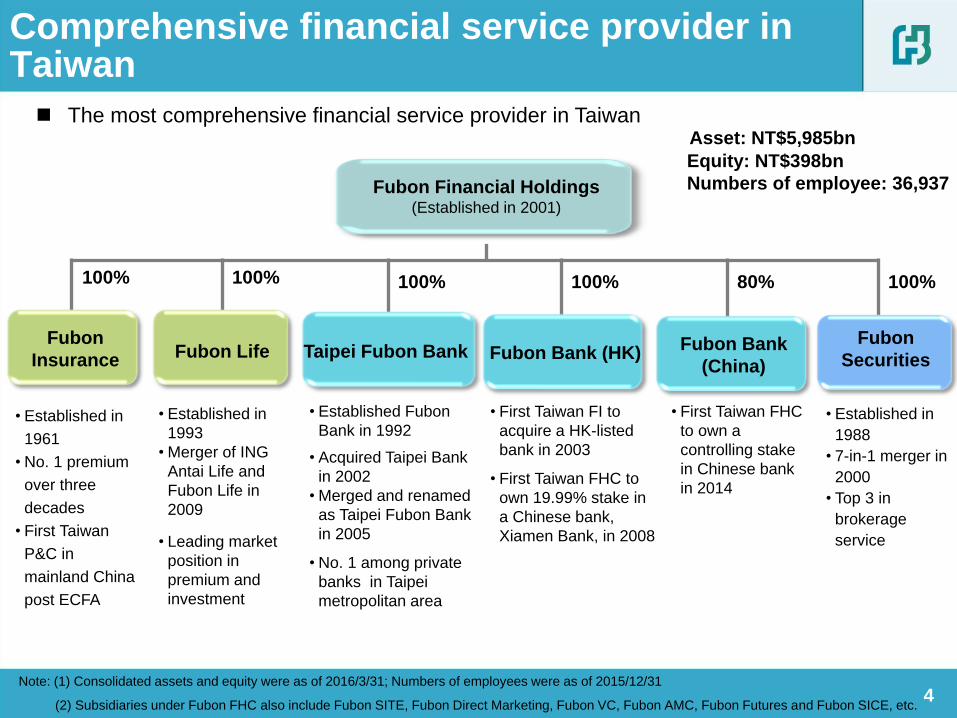

Note: (1) Consolidated assets and equity were as of 2016/3/31; Numbers of employees were as of 2015/12/31

(2) Subsidiaries under Fubon FHC also include Fubon SITE, Fubon Direct Marketing, Fubon VC, Fubon AMC, Fubon Futures and Fubon SICE, etc. 4

Comprehensive financial service provider in Taiwan

The most comprehensive financial service provider in Taiwan

• Established in

1961

• No. 1 premium

over three

decades

• First Taiwan

P&C in

mainland China

post ECFA

• Established in

1993

• Merger of ING

Antai Life and

Fubon Life in

2009

• Leading market

position in

premium and

investment

• Established Fubon

Bank in 1992 • Acquired Taipei Bank

in 2002

• Merged and renamed

as Taipei Fubon Bank

in 2005

• No. 1 among private

banks in Taipei

metropolitan area

• Established in

1988

• 7-in-1 merger in

2000

• Top 3 in

brokerage

service

Fubon Bank (HK)

Taipei Fubon Bank

Fubon

Securities

100% 80% 100% 100% 100%

Fubon Life

Fubon

Insurance

Fubon Bank

(China)

100%

• First Taiwan FHC

to own a

controlling stake

in Chinese bank

in 2014

• First Taiwan FI to

acquire a HK-listed

bank in 2003

• First Taiwan FHC to

own 19.99% stake in

a Chinese bank,

Xiamen Bank, in 2008

Fubon Financial Holdings (Established in 2001)

Asset: NT$5,985bn

Equity: NT$398bn

Numbers of employee: 36,937

Expansion Milestones

2002 2004 2000 2009

• US$2.4bn

• Acquired 100% of

Taipei Bank in

2002 through a

share swap

• First merger in

Taiwan between

private and

government owned

institution

• Strong distribution

network in Taipei

metropolitan area

2014 2008

• US$415mm

• Acquired 75% of

International

Bank of Asia in

2004

• First and only

Taiwan FHC to

operate a Hong

Kong-based bank

• Privatization with

100% stake in

June 2011

• US$345mn

• Fubon

Securities

acquired six

other domestic

securities firms

by shares

swap; the most

largest merger

in the history of

securities

industry in

Taiwan.

• US$1bn

• Acquired 80% of

First Sino Bank

in 2014

• Controlling stake

in a nationwide

licensed bank in

China

• US$600mm

• Acquired 100%

of ING Antai

Life (Taiwan) in

2009

• Became the 2nd

largest life

insurer in

Taiwan

• US$33mm

• Acquired 19.99%

of Xiamen City

Commercial

Bank in 2008

• First and only

Taiwan FHC to

own a stake in a

Chinese bank

Fubon Securities

7-in-1 merger

5

Business expansion through disciplined strategic M&A moves

Experienced management team

6

Daniel Tsai

Chairman

• 35 years of industry experience

• Master of Comparative Law, Georgetown University

Richard Tsai

Vice Chairman

• 35 years of industry experience

• MBA, New York University

Oliver Cheng

Chairman

• 43 years of industry

experience

• Joined Fubon in 1973

• BA of Law, National

Taiwan University

Fubon Life Insurance Fubon Financial Holdings

Jerry Harn

President

• 27 years of industry

experience

• Joined Fubon in

2005

• MBA, Ohio State

University

Taipei Fubon Bank

Steve Chen

Chairman

• 40 years of industry

experience

• Joined Fubon in 1976

• MBA, Roosevelt

University

Fubon P&C Insurance

Vivien Hsu

President

• 38 years of industry

experience

• Joined Fubon in 2013

• MBA, University of New

South Wales

Fubon Securities

Samuel Hsu

Chairman

• 35 years of industry

experience

• Joined Fubon in

2013

• MBA, Chinese

Culture University

Seasoned senior management team with an average of over 30 years of experience in

financial services industry

Howard Lin

Vice Chairman

• 36 years of industry

experience

• Joined Fubon in 1997

• Ph.D., Department of

Chemical Engineering,

National Taiwan

University

Fubon Life Insurance

Fubon Bank (HK)

Raymond Lee

Managing Director &

CEO

• 42 years of industry

experience

• Joined Fubon in

2012

• Fellow of ACCA,

Member of HK

institute of CPA

Fubon Bank (China)

Peili Hong

Chairman

• 32 years of industry

experience

• Joined Fubon in

2014

• Master of

Economics, East

China Normal

University

Fubon Bank (China)

Dennis Chan

President

• 27 years of industry

experience

• Joined Fubon in

2011

• MBA, Georgetown

University

7

Leading market position across major busineses

Banking Life insurance

Securities

Note: (1) Among top 6 card issuers; per active card basis; (2) Among private banks; (3) Among top 10 brokers

All data as of 2015

Market

ranking

Market

share/amount

Monthly per card spending (1) 1 NT$9,001

Loan Syndication (2) 1 6.0%

Mortgage loan(2) 2 5.49%

FX derivative 2 14.3%

Market

ranking

Market

share

FYP through broker 1 20.6%

FYP through bancassurance 1 19.2%

First year premium 2 17.3%

Total premium 2 16.2%

FYP through tied agents 3 14.3%

Market

ranking

Market

share

Emerging stock trading 2 17.27%

IPO amount 2 16.92%

SPO amount 2 15.31%

Brokerage per branch(3) 2 0.09%

Brokerage 3 5.19%

Market

ranking

Market

share

Direct written premium 1 22.48%

Personal line 1 21.85%

Commercial line 1 24.01%

Average premium per employee

(million) 1 NT$11.76

P&C

Subsidiary Service network

Bank

Taipei Fubon Bank 5 branches : HK, Hanoi, Binh Duong, Ho Chi Minh City,

Singapore

Fubob Bank (HK) 23 branches, 2 securities services centers and 1 personal

loan center

Xiamen Bank 49 branches & sub-branches: Xiamen, Fujian, Chong Qing

Fubon Bank (China)

22 branches & sub-branches: Shanghai, Suzhou, Tianjin,

Shenzhen, Kunshan, Beijing, Nanjing

Insurance

Fubon Insurance

(China) 42 offices: Xiamen, Fujian, Chong Qing, Dalian, Liaoning

Fubon Insurance -

Vietnam subsidiary

5 offices: Ho Chi Minh City, Hanoi, Binh Duong, Dong Nai,

Hai Phong

Fubon Insurance

Broker (Philippines) 1 office: Manila

Fubon Insurance

Broker (Thailand) 1 office: Bangkok

Fubon Life -

Vietnam subsidiary 2 offices: Hanoi, Ho Chi Minh City

Fubon Life -

Hong Kong subsidiary 1 office: Hong Kong

Securities

Fubon Securities HK subsidiary

Founder Fubon

Fund management Beijing

8

Note: Rep offices in Malaysia, Indonesia and China from subsidiaries under Fubon FHC.

Hong Kong

Chong Qing

Vietnam

Fujian

Taiwan

Liaoning

Thailand

Indonesia

Shanghai

Tianjin

Guangdong

Beijing

Jiangsu

Philippines

Vision: A leading financial institution in Asia

Singapore

9

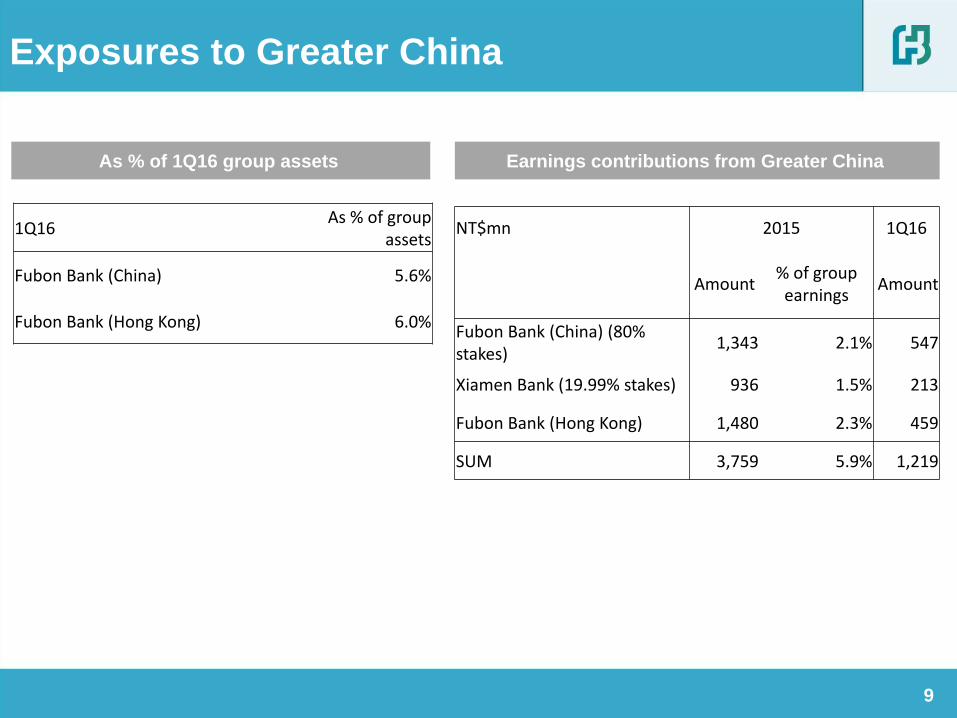

Exposures to Greater China

As % of 1Q16 group assets Earnings contributions from Greater China

1Q16 As % of group

assets

Fubon Bank (China) 5.6%

Fubon Bank (Hong Kong) 6.0%

NT$mn 2015 1Q16

Amount % of group

earnings Amount

Fubon Bank (China) (80% stakes)

1,343 2.1% 547

Xiamen Bank (19.99% stakes) 936 1.5% 213

Fubon Bank (Hong Kong) 1,480 2.3% 459

SUM 3,759 5.9% 1,219

10

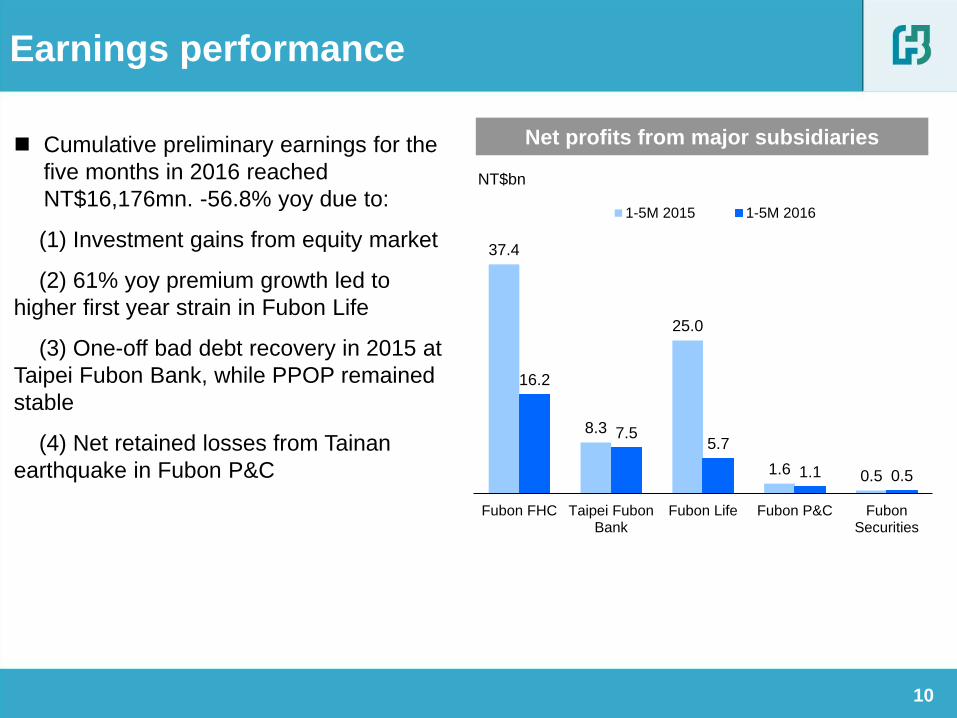

Earnings performance

Net profits from major subsidiaries

NT$bn

Cumulative preliminary earnings for the

five months in 2016 reached

NT$16,176mn. -56.8% yoy due to:

(1) Investment gains from equity market

(2) 61% yoy premium growth led to

higher first year strain in Fubon Life

(3) One-off bad debt recovery in 2015 at

Taipei Fubon Bank, while PPOP remained

stable

(4) Net retained losses from Tainan

earthquake in Fubon P&C

37.4

8.3

25.0

1.6 0.5

16.2

7.5 5.7

1.1 0.5

Fubon FHC Taipei FubonBank

Fubon Life Fubon P&C FubonSecurities

1-5M 2015 1-5M 2016

11

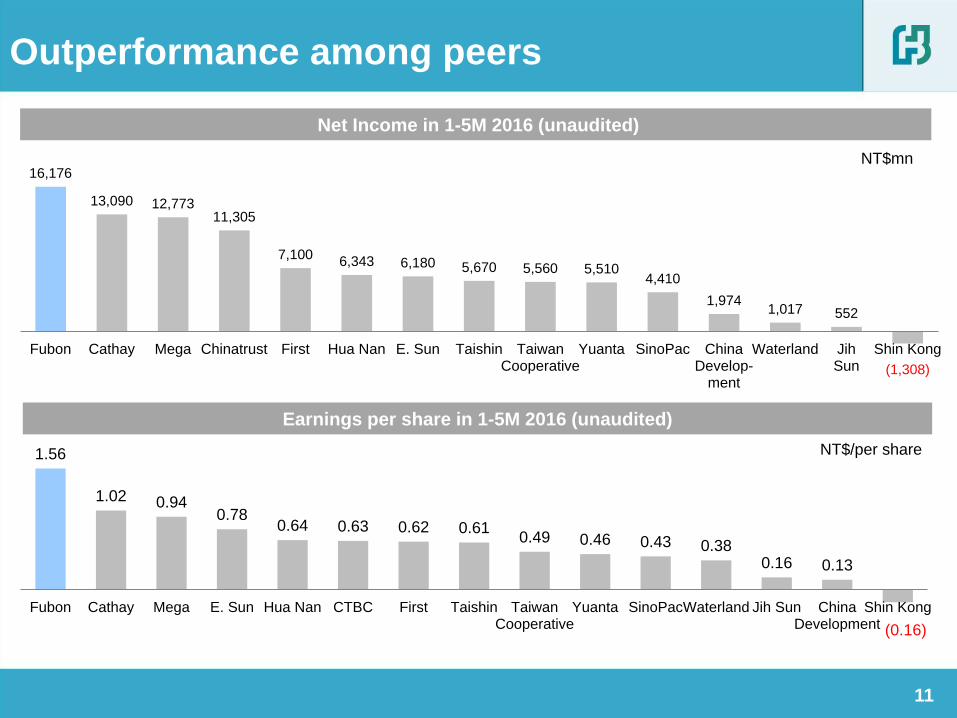

Net Income in 1-5M 2016 (unaudited)

Earnings per share in 1-5M 2016 (unaudited)

NT$mn

Outperformance among peers

NT$/per share

16,176

13,090 12,773 11,305

7,100 6,343 6,180 5,670 5,560 5,510

4,410

1,974 1,017 552

(1,308)

Fubon Cathay Mega Chinatrust First Hua Nan E. Sun Taishin TaiwanCooperative

Yuanta SinoPac ChinaDevelop-

ment

Waterland JihSun

Shin Kong

1.56

1.02 0.94 0.78

0.64 0.63 0.62 0.61 0.49 0.46 0.43 0.38

0.16 0.13

(0.16)

Fubon Cathay Mega E. Sun Hua Nan CTBC First Taishin TaiwanCooperative

Yuanta SinoPacWaterland Jih Sun ChinaDevelopment

Shin Kong

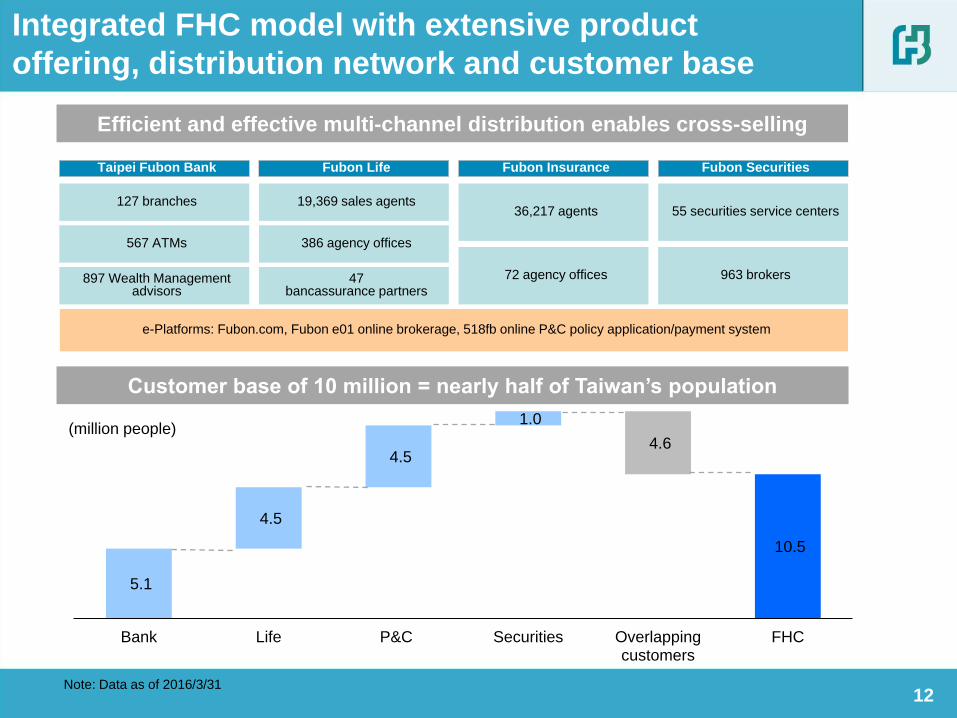

Efficient and effective multi-channel distribution enables cross-selling

Customer base of 10 million = nearly half of Taiwan’s population

Note: Data as of 2016/3/31

e-Platforms: Fubon.com, Fubon e01 online brokerage, 518fb online P&C policy application/payment system

(million people)

Taipei Fubon Bank Fubon Life Fubon Insurance Fubon Securities

386 agency offices

36,217 agents

72 agency offices

55 securities service centers

567 ATMs

897 Wealth Management advisors

127 branches

963 brokers 47 bancassurance partners

19,369 sales agents

12

Integrated FHC model with extensive product

offering, distribution network and customer base

5.1

10.5

4.5

4.5

1.0

4.6

Bank Life P&C Securities Overlappingcustomers

FHC

13 13

Taiwan macro/policy outlook

Opportunities Challenges

• Initiatives to promote five

targeted industries

• Social welfare improvement:

long term care and public

apartments

• Taiwan stock market stimulus

• Economic growth outlook

• Interest rate environment

• Cross-strait deregulation

• Tax reform: inheritance tax,

sales tax, and corporate tax

14

Channels

• Bank branch relocation & Life agency growth

• e-platforms for efficiency and business growth

• Cross-sale synergy

Opportunities

• Growth opportunities in life insurance and wealth

management business

• Portfolio management along with asset growth

Growth opportunities

Expansion

• Business contribution aim to diversify

• M&A and strategic alliance opportunities from domestic and

overseas

1.2

1.6 1.7

1.2 1.0

1.5

0.0

2.0

1.0 1.0 1.0

1.5

3.0

2.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Dividends & ROE

15 15

Cash dividends

NT$

ROE

6.3%

9.8% 9.9%

6.8% 5.3%

8.8% 7.0%

11.3%

9.3%

13.5%

10.8% 11.5%

16.1% 16.40%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

16

Agenda

Fubon FHC overview

Taipei Fubon Bank

Fubon Life

Growth momentum outperforming industry

Total loan growth (5 year CAGR)

Market share by loans among private banks

Leading commercial banking service

provider in Taiwan

Major product lines are corporate

banking, retail banking, credit card,

and wealth management services

Outperformance in greater China

franchise

17 Note: All data as of 2015/12/31

6.20%

4.99%

Fubon Industry Average

5.8%

4.6% 4.4% 4.0%

3.3%

CTBC TaipeiFubon Bank

CathayUnited Bank

E. SUN Taishin

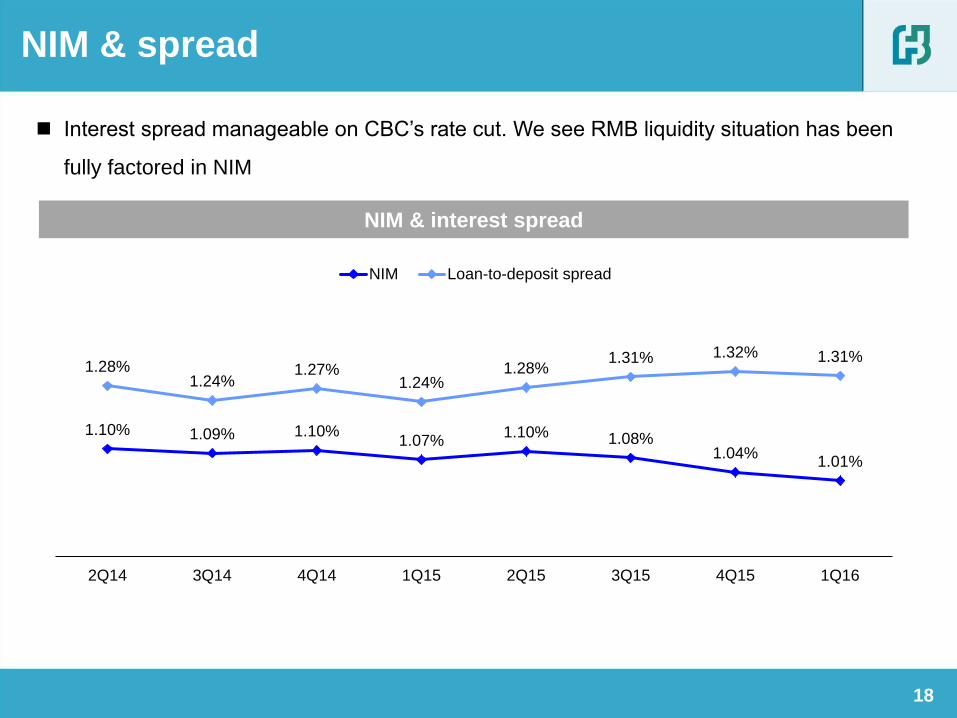

NIM & spread

Interest spread manageable on CBC’s rate cut. We see RMB liquidity situation has been

fully factored in NIM

18

1.10% 1.09% 1.10% 1.07%

1.10% 1.08% 1.04%

1.01%

1.28% 1.24%

1.27% 1.24%

1.28% 1.31% 1.32% 1.31%

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

NIM Loan-to-deposit spread

NIM & interest spread

Strong wealth management business

continues

Wealth management business growth momentum continues through client penetration rate

and financial consultant productivity enhancement

19

Wealth management fee

NT$mn

0

500

1,000

1,500

2,000

2,500

3,000

1Q15 1Q16

+16.5%

-0.7%

31.5%

7.7%

0

2,000

4,000

6,000

8,000

10,000

2013 2014 2015

Wealth management fee Growth rate

20

Agenda

Fubon FHC overview

Taipei Fubon Bank

Fubon Life

4.06%

4.97%

2009 2015

21

Growth momentum leading peers

Asset CAGR (2009~2015)

Investment return Cost of liability

Note: Peers group includes the top five life insurance companies by asset size. (Cathay, Nan Shan, Shin Kong, China Life, and Mercuries Life)

Asset growth outpacing industry average

and peers

Cost of liability improvement significant,

owing to premium growth

Investment spread turned positive

4.56%

3.84%

2009 2015

14.6%

11.2% 10.8%

Fubon Life Industry Peers*

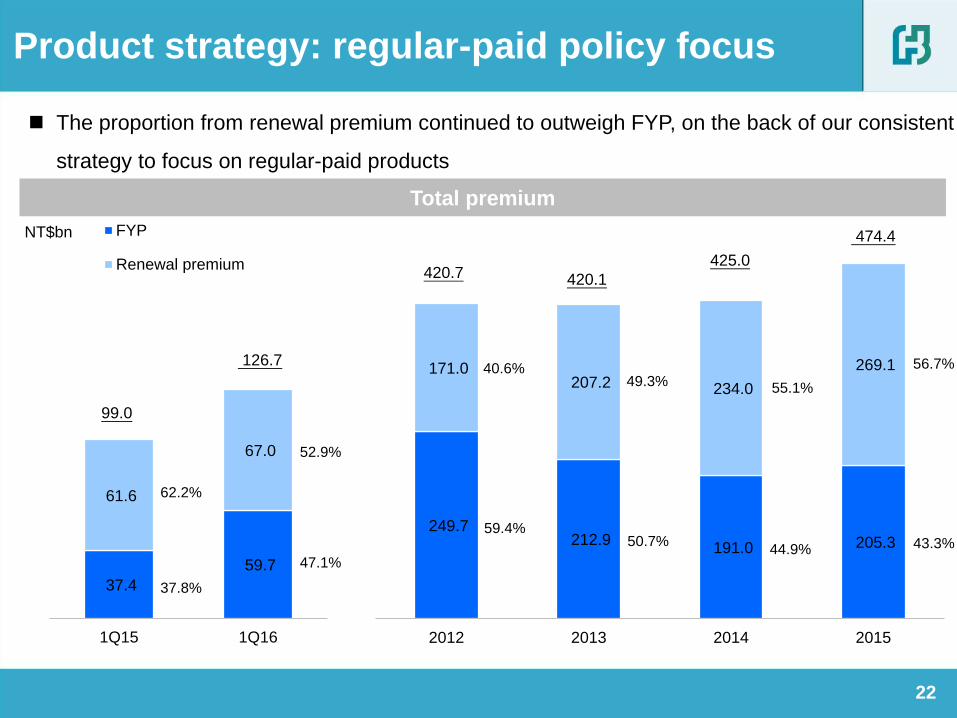

37.4

59.7

61.6

67.0

1Q15 1Q16

FYP

Renewal premium

249.7 212.9

191.0 205.3

171.0 207.2 234.0

269.1

2012 2013 2014 2015

420.7 420.1

425.0

474.4

56.7%

43.3%

55.1%

44.9%

49.3%

50.7%

40.6%

59.4%

99.0

126.7

52.9%

47.1%

62.2%

37.8%

The proportion from renewal premium continued to outweigh FYP, on the back of our consistent

strategy to focus on regular-paid products

22

NT$bn

Product strategy: regular-paid policy focus

Total premium

23 23

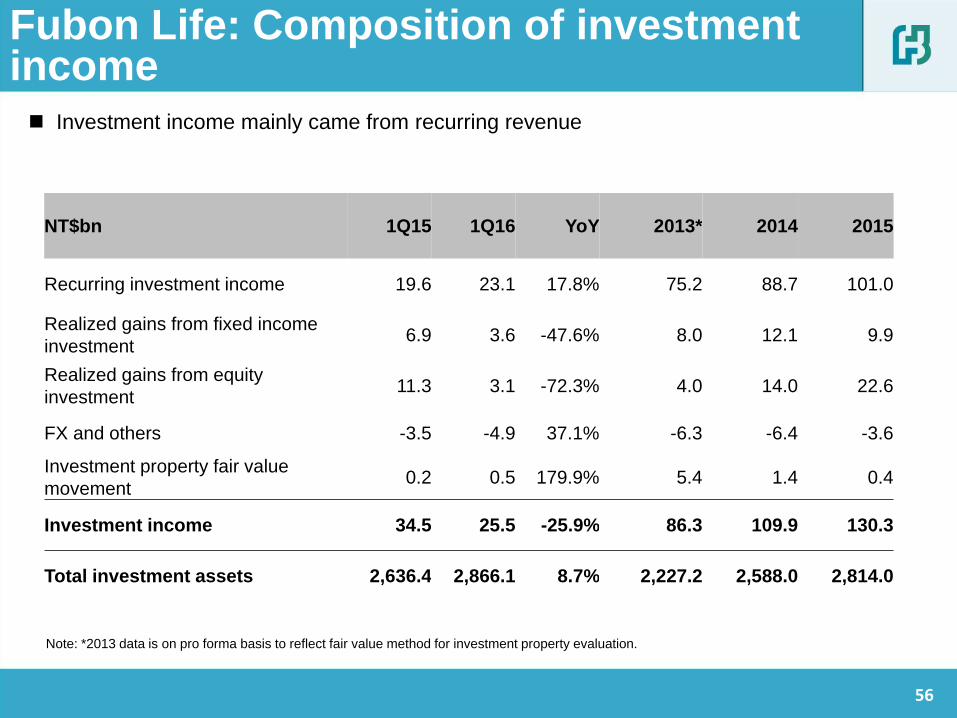

Investment income mainly came from recurring revenue

Sustainable positive spread

Temporary negative spread in 1Q16 due to strong FYP growth

Investment performance

Note: *2013 data is on pro forma basis to reflect fair value method for investment property evaluation.

NT$bn 2012 2013* 2014 2015 1Q16

Recurring investment income 62.7 75.2 88.7 101.0 23.1

Recurring investment income contributions 91% 87% 81% 78% 90%

Recurring yield (a) 3.43% 3.48% 3.57% 3.70% 3.14%

Capital gains 0.58% 0.95% 1.17% 1.27% 0.58%

Breakeven point (b) 3.18% 3.09% 2.91% 2.97% 3.24%

Spread (c)=(a)-(b) 0.25% 0.39% 0.66% 0.73% -0.10%

Investment income 68.6 86.3 109.9 130.3 25.5

Total investment assets 1,932.3 2,227.2 2,588.0 2,814.0 2,866.1

24 24

Deployment in overseas fixed income

Overseas fixed income investment strategy

Active deployment in overseas fixed income assets. Overseas fixed income recurring yield

remains intact despite reducing exposures to high yield bond funds

1.4

3.6 2.4 2.5

1.0

5.7

1.4

3.14%

3.75% 3.56%

3.12%

2.72%

2.96%

2.72%

1H13 2H13 1H14 2H14 1H15 2H15 1Q16

Overseas fixed income net change

US 30 year government bond yield

US$bn

Recurring yield maintained

3.17%

3.35%

1Q15 1Q16

Overall recurring yield (after hedge)

25 25

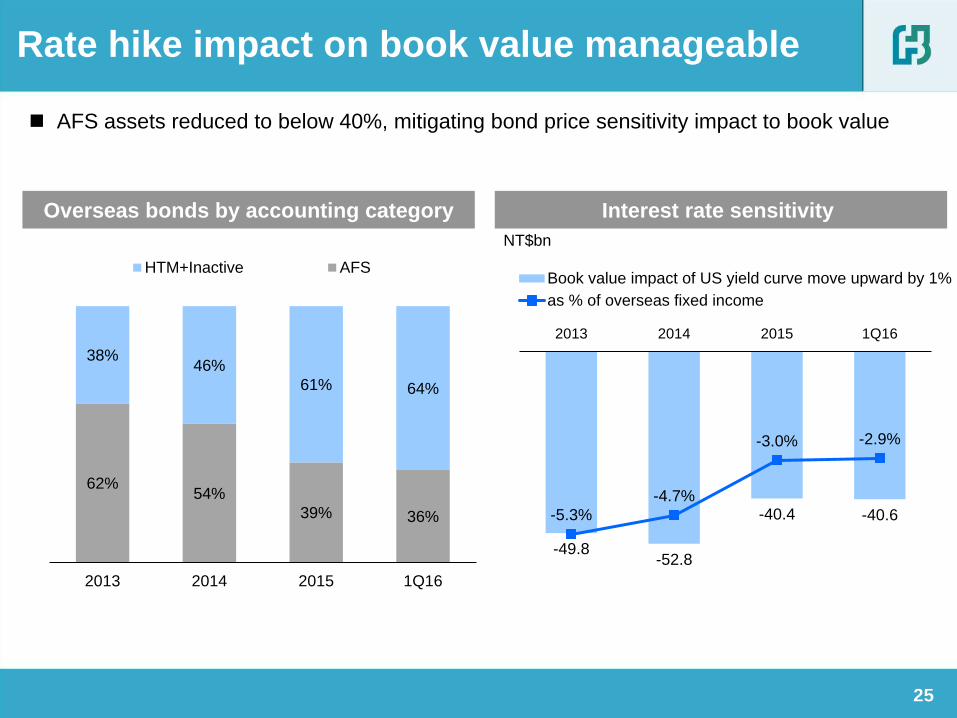

Overseas bonds by accounting category

Rate hike impact on book value manageable

AFS assets reduced to below 40%, mitigating bond price sensitivity impact to book value

Interest rate sensitivity

62% 54%

39% 36%

38% 46%

61% 64%

2013 2014 2015 1Q16

HTM+Inactive AFS

NT$bn

-49.8 -52.8

-40.4 -40.6 -5.3%

-4.7%

-3.0% -2.9%

2013 2014 2015 1Q16

Book value impact of US yield curve move upward by 1%

as % of overseas fixed income

26

Track record in consistent hedging strategies

0.75% 0.68% 0.58% 0.28% 1.01%

43.4% 45.5% 52.3% 57.9% 57.7%

Hedging costs (incl. FX gains/losses)

Overseas Investment

Hedging composition & costs

82.5% 81.4% 76.3% 75.6% 74.7%

2.7% 7.9% 10.8% 8.1%

5.4% 2.6% 2.0% 1.5% 4.3%

12.1% 13.2% 13.8% 12.1% 12.9%

2012 2013 2014 2015 1Q16

Equities/ mutualfunds

Other currencies

Naked USD

Currency swap &FX Policy

2016.06

Strategy and Performance of Fubon Life

Fubon Life’s financial goals

Short-term

Balanced

SoE

Long-term

Sustainable

Value

Creation

Ultimate

Maximized

Shareholders’

Value

Financial Goals

Mortality

Expense Interest

Source of Earnings

Reduce Cost of Liabilities

Maintain Mortality Gain

Enhance Expense Margin

Increase Investment

Return

Reduce Breakeven Points Increase Recurring

Yields and Return

Targets and Actions

28

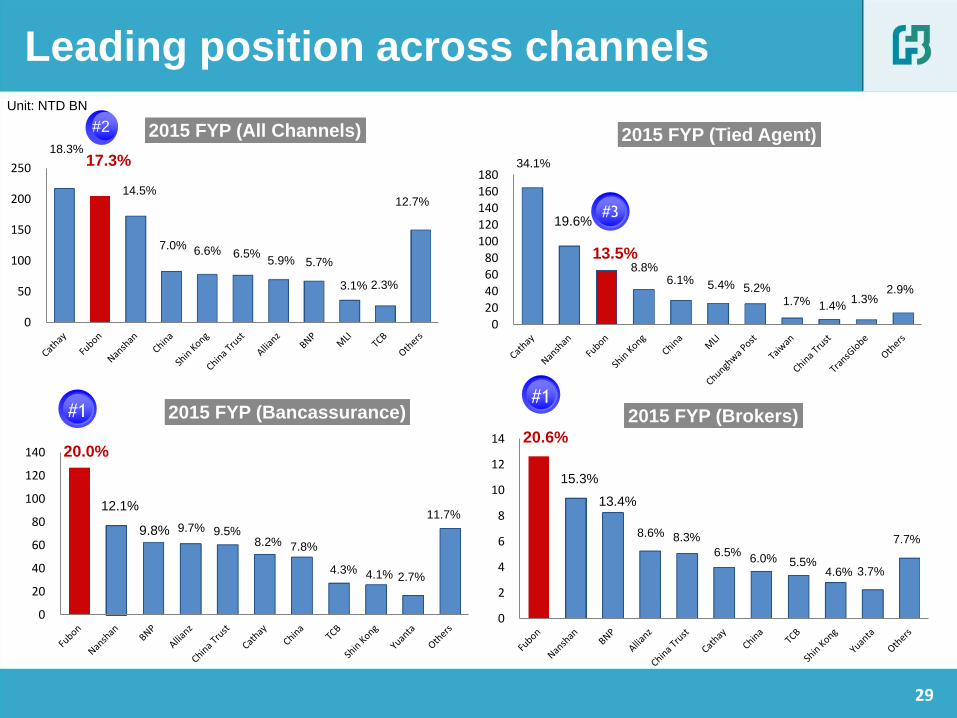

18.3% 17.3%

14.5%

7.0% 6.6% 6.5% 5.9% 5.7%

3.1% 2.3%

12.7%

0

50

100

150

200

250

2015 FYP (All Channels)

Leading position across channels Unit: NTD BN

#2

#3

#1 #1

34.1%

19.6%

13.5% 8.8%

6.1% 5.4% 5.2% 1.7% 1.4%

1.3% 2.9%

020406080

100120140160180

2015 FYP (Tied Agent)

20.0%

12.1%

9.8% 9.7% 9.5% 8.2% 7.8%

4.3% 4.1% 2.7%

11.7%

0

20

40

60

80

100

120

140

2015 FYP (Bancassurance)

20.6%

15.3%

13.4%

8.6% 8.3%

6.5% 6.0% 5.5%

4.6% 3.7%

7.7%

0

2

4

6

8

10

12

14

2015 FYP (Brokers)

29

Growing agency force

Number of Tied-Agents

Source: Taiwan Insurance Institution

Size of tied agents force is increasing, a CAGR of 9.3% from 2008 to 2015, while 0.1% for the industry.

Fubon’s tied-agent force grows from 11.6% to 21.5% of the industry agent force.

% of Industry Tied-Agents

30

3.36%

2.76%

3.03%2.97%

3.18%

3.09%

2.91%2.97%

3.27%3.30%

3.33%

3.43%3.48%

3.57%

3.70%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Breakeven Point

Recurring Return

5.17%

4.56%

4.16%4.16% 4.07%

3.98%

3.88% 3.84%

3.16%

4.06%

3.78%3.80%

4.01%

4.05%

4.74%

4.97%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Cost of Liabilities

Investment Return

Self sustainable growth strategy delivers

promising financial results

Note1:Recurring return of FY08 is unavailable.

Note2:Breakeven point = (Profit before tax – Investment income)/Average investment assets

Breakeven Point vs. Recurring Return Cost of Liability vs. Investment Return

31

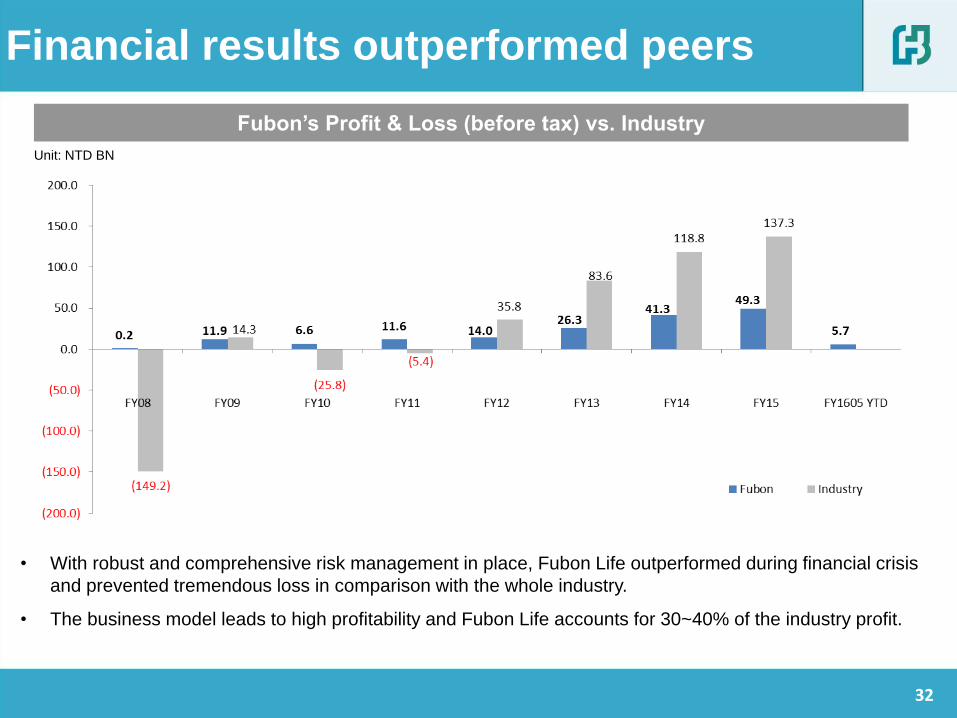

Fubon’s Profit & Loss (before tax) vs. Industry

Financial results outperformed peers

Unit: NTD BN

• With robust and comprehensive risk management in place, Fubon Life outperformed during financial crisis

and prevented tremendous loss in comparison with the whole industry.

• The business model leads to high profitability and Fubon Life accounts for 30~40% of the industry profit.

32

66

96 101 102

167 170

224

183 206

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16Q1

Net worth AUM

904 1,125

1,425 1,614

1,955 2,242

2,583 2,837 2,923

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16Q1

Unit: NTD BN

• ROE adjustment : excludes the release of special reserve from unrealized gains on property. Fubon released 2.6 NTD billion in 2013 and none for 2014 and 2015.

• Fubon 2008Y includes ex-Fubon and ex-ING Antai. Fubon 2015 dividend upstream 8,800m.

Source:TII、Company’s information

22

Financial performance

23

Impact from fair value method on investment property

Return on Equity

2.6%

13.4%

6.7%

9.9% 9.6%

14.8%

18.0%20.2%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Average ROE: 11.9%

33

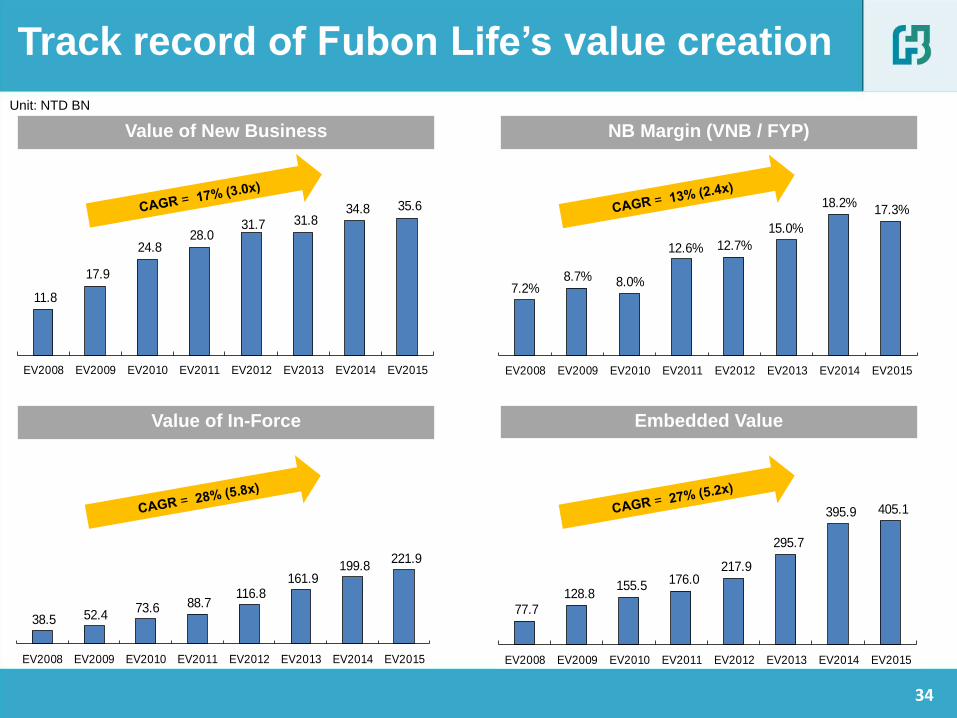

7.2%8.7% 8.0%

12.6% 12.7%

15.0%

18.2%17.3%

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

11.8

17.9

24.8 28.0

31.7 31.8 34.8 35.6

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

38.5 52.4 73.6 88.7

116.8 161.9

199.8 221.9

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

77.7 128.8

155.5 176.0 217.9

295.7

395.9 405.1

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

77.7 128.8

155.5 176.0 217.9

295.7

395.9 405.1

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

Unit: NTD BN

NB Margin (VNB / FYP) Value of New Business

Value of In-Force Embedded Value

Track record of Fubon Life’s value creation

34

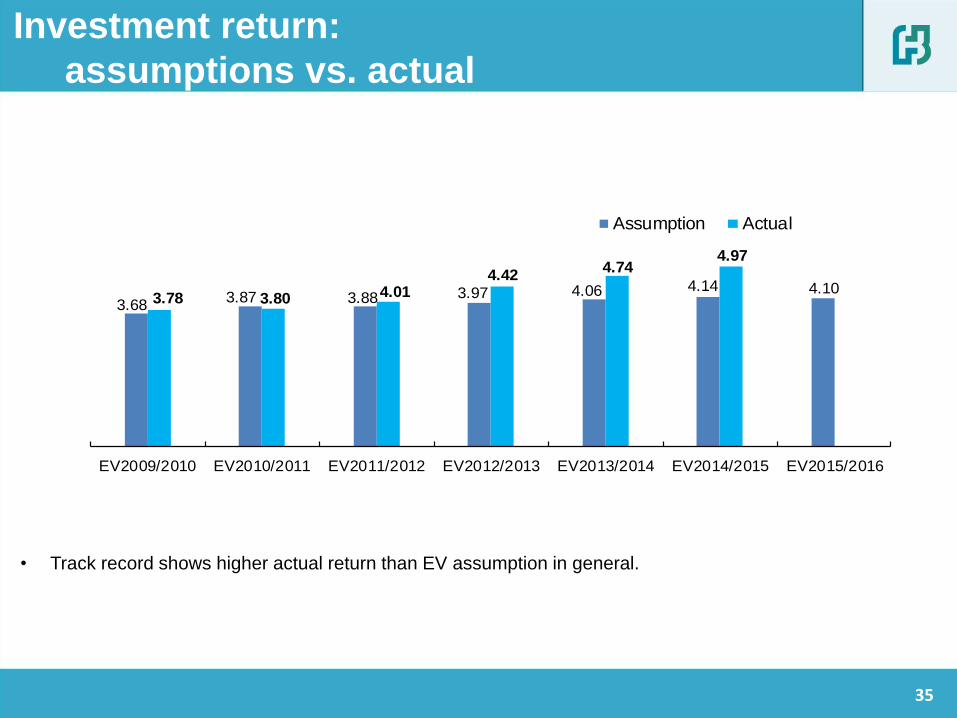

Investment return:

assumptions vs. actual

3.68 3.87 3.88 3.97 4.06 4.14 4.10

3.78 3.80 4.01 4.42

4.74 4.97

EV2009/2010 EV2010/2011 EV2011/2012 EV2012/2013 EV2013/2014 EV2014/2015 EV2015/2016

Assumption Actual

• Track record shows higher actual return than EV assumption in general.

35

2016.05.11

Fubon Financial 2016 Q1 Interim Results

and

2015 Embedded Value of Fubon Life

Disclaimer

This meeting may contain forward-looking statements with respect to the financial

condition, results of operations and business of the company. These forward-looking

statements represent the company’s expectations or beliefs concerning future events

and involve known and unknown risks and uncertainty that could cause actual

results, performance or events to differ materially from those expressed. Certain

statements, such as those that include the words “potential”, “estimated”, and similar

expressions or variations on such expressions may be considered “forward-looking

statements”. Financial numbers in this report may include preliminary unaudited

numbers or management accounts.

37

Performance review by subsidiary

• Fubon Life

• Fubon Securities

Performance highlights of Fubon Financial Holdings

• Fubon Insurance

Agenda

• Taipei Fubon Bank

• Fubon Bank (China)

• Fubon Bank (China)

2015 Embedded value of Fubon Life

38

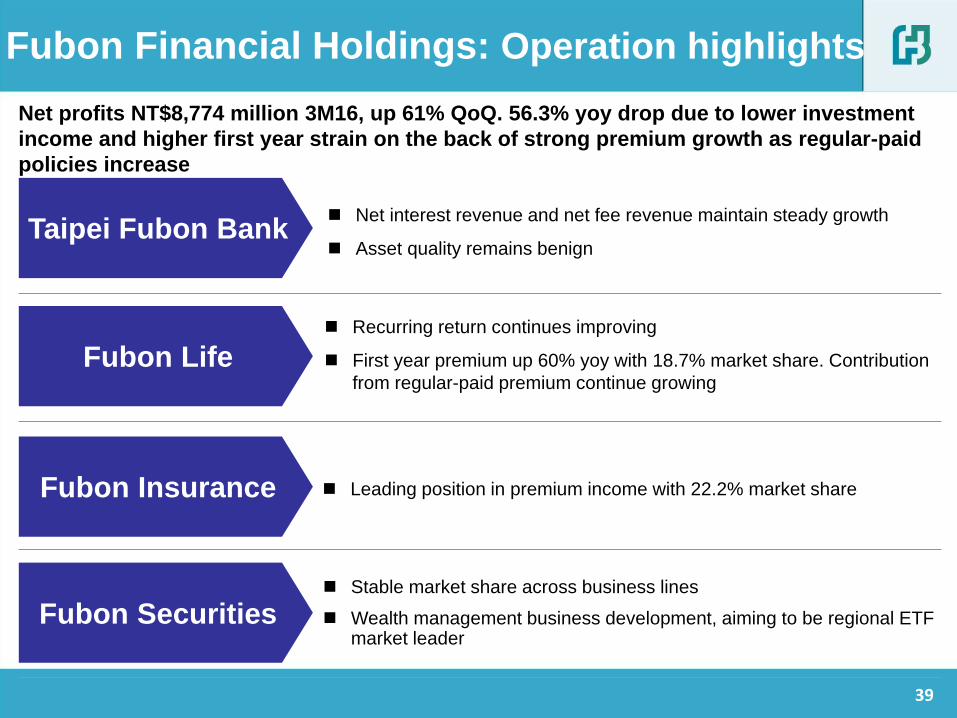

Fubon Financial Holdings: Operation highlights

Taipei Fubon Bank

Stable market share across business lines

Wealth management business development, aiming to be regional ETF market leader

Fubon Life

Fubon Insurance

Fubon Securities

Net profits NT$8,774 million 3M16, up 61% QoQ. 56.3% yoy drop due to lower investment

income and higher first year strain on the back of strong premium growth as regular-paid

policies increase

Recurring return continues improving

First year premium up 60% yoy with 18.7% market share. Contribution

from regular-paid premium continue growing

Net interest revenue and net fee revenue maintain steady growth

Asset quality remains benign

Leading position in premium income with 22.2% market share

39

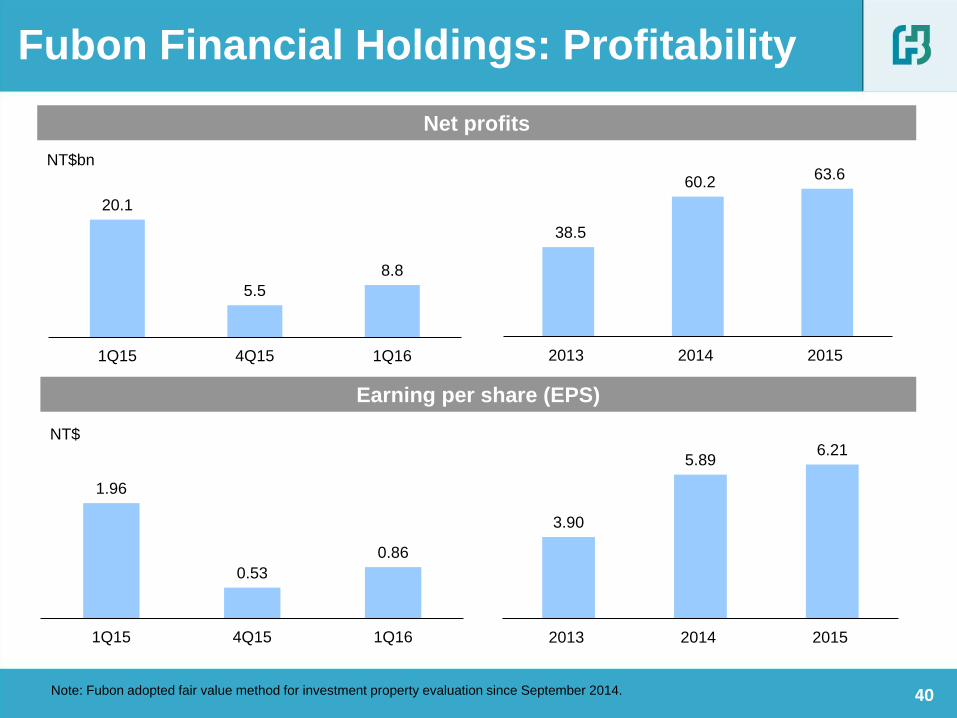

Net profits

Earning per share (EPS)

NT$

Note: Fubon adopted fair value method for investment property evaluation since September 2014.

NT$bn

Fubon Financial Holdings: Profitability

38.5

60.2 63.6

2013 2014 2015

20.1

5.5

8.8

1Q15 4Q15 1Q16

3.90

5.89 6.21

2013 2014 2015

1.96

0.53

0.86

1Q15 4Q15 1Q16

40

Fubon Financial Holdings: Net profits from major subsidiaries

Net profits from major subsidiaries Profit contribution from major subsidiaries

NT$bn NT$bn

Note:

(1) Profit contribution are based on the summation of five major

subsidiaries; (2) Fubon Bank (China) contributed NT$547 mn net

profits to the Company on the basis of 80% shareholding.

4.9

13.3

0.9 0.4

0.8

2.7 2.2

0.6 0.6 0.1

4.9

2.1

0.5 0.4 0.7

Taipei FubonBank

Fubon Life Fubon P&C FubonSecurities

Fubon Bank(HK)

1Q15 4Q15 1Q16

Taipei Fubon

Bank, 4.9 , 57.3%

Fubon Life, 2.1 , 24.8%

Fubon P&C, 0.5 ,

6.0%

Fubon Securities, 0.4 , 4.2%

Fubon Bank (HK), 0.7 ,

7.8%

41

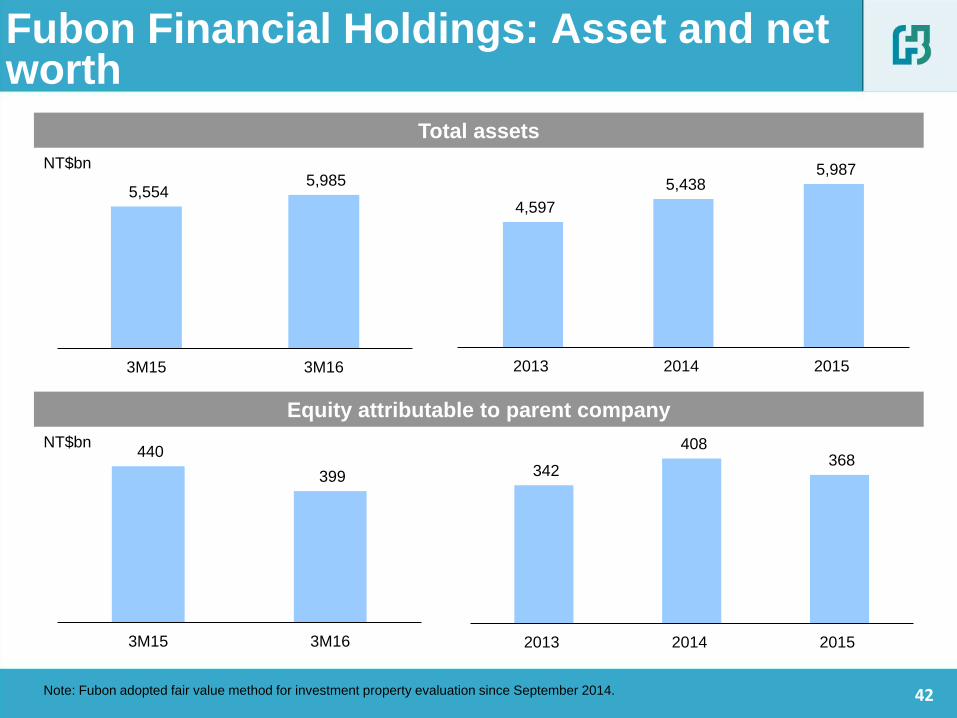

Total assets

Equity attributable to parent company

NT$bn

NT$bn

Fubon Financial Holdings: Asset and net worth

Note: Fubon adopted fair value method for investment property evaluation since September 2014.

4,597

5,438 5,987

2013 2014 2015

5,554 5,985

3M15 3M16

342

408 368

2013 2014 2015

440

399

3M15 3M16

42

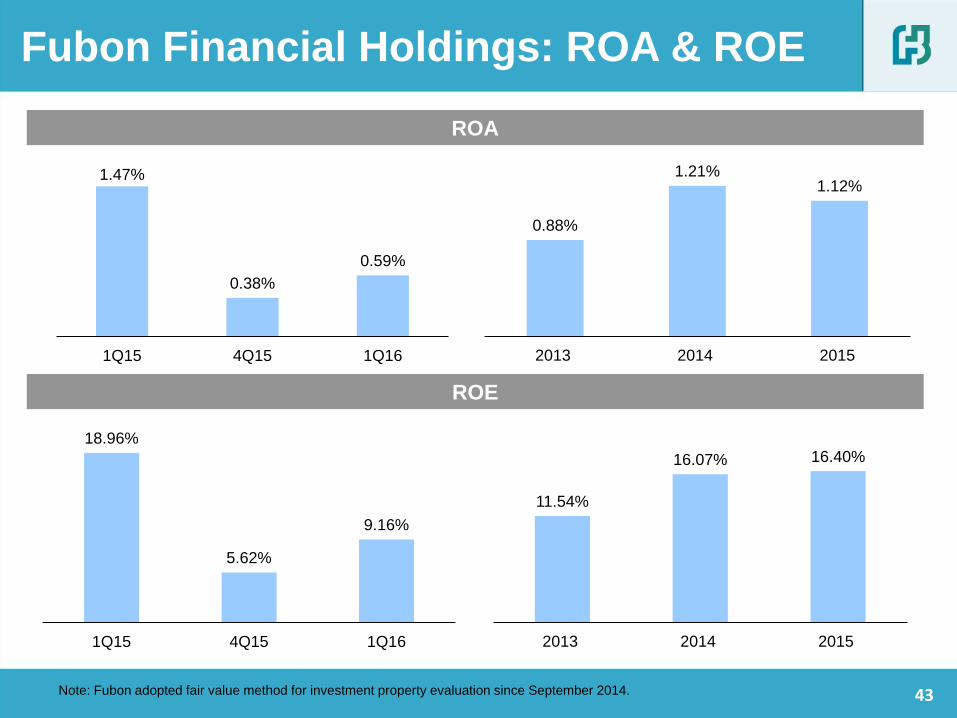

ROA

ROE

Fubon Financial Holdings: ROA & ROE

Note: Fubon adopted fair value method for investment property evaluation since September 2014.

0.88%

1.21% 1.12%

2013 2014 2015

1.47%

0.38%

0.59%

1Q15 4Q15 1Q16

11.54%

16.07% 16.40%

2013 2014 2015

18.96%

5.62%

9.16%

1Q15 4Q15 1Q16

43

Performance review by subsidiary

• Fubon Life

• Fubon Securities

Performance highlights of Fubon Financial Holdings

• Fubon Insurance

Agenda

• Taipei Fubon Bank

• Fubon Bank (China)

2015 Embedded value of Fubon Life

44

4.2 4.5

3.0 3.2

2.1 2.1

1.0 1.8

1Q15 1Q16

Fubon Bank (China)

Treasury & others

Net fee income

Net interest income

15.8 17.3 17.9

8.4 10.6 11.1

9.5

11.0 7.4

5.2 6.0

2013 2014 2015

Taipei Fubon Bank: Revenue

Revenue composition of Taipei Fubon Bank

NT$bn

Steadily growth from net interest income and net fees

33.7

Note: Consolidated basis; Fubon Bank (China) accounted starting from Jan. 7th, 2014

44.1 42.4

10.3

11.5

41.0%

28.1%

38.7%

10.1%

20.3%

28.6%

15.3%

17.9%

28.2%

42.2% 39.3%

24.0%

25.0%

11.7%

46.8%

25.0%

14.1%

17.5%

26.3%

45

40.6%

77.6% 7.3%

5.4%

40.3%

13.6%

11.8%

3.5%

1Q15 1Q16

SN and others

Mutual funds

Custodian andtrust

Insurancecommission

Taipei Fubon Bank: Fee and wealth

management revenue

Sources of fee revenue(1) Wealth management fee(2)

NT$mn NT$mn

Note: (1) Fee income including Taipei Fubon Bank standalone and Taipei Fubon Bank Life Insurance Agency

(2) Wealth management revenue includes fee in the chart and other income (1Q16: NT$93mn; 1Q15: NT$106mn)

(3) Data are stand-alone basis in page 11-16

2,957

3,239 2,690

2,309

+16.5%

78.1% 83.0%

10.3%

9.2% 7.3%

3.7% 4.3%

4.0%

1Q15 1Q16

Others

Syndicationloan

Credit card

Wealthmanagement

46

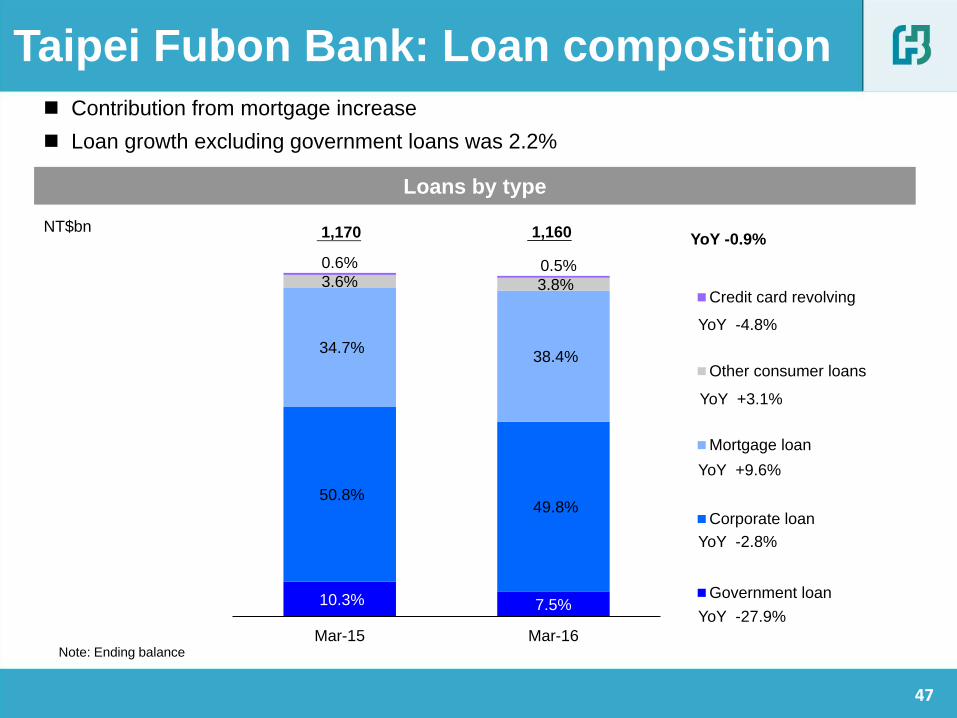

Loans by type

10.3% 7.5%

50.8% 49.8%

34.7% 38.4%

3.6% 3.8%

0.6% 0.5%

Mar-15 Mar-16

Credit card revolving

Other consumer loans

Mortgage loan

Corporate loan

Government loan

Taipei Fubon Bank: Loan composition

NT$bn 1,160 YoY -0.9%

YoY -4.8%

YoY +3.1%

YoY +9.6%

YoY -2.8%

YoY -27.9%

Contribution from mortgage increase

Loan growth excluding government loans was 2.2%

1,170

Note: Ending balance

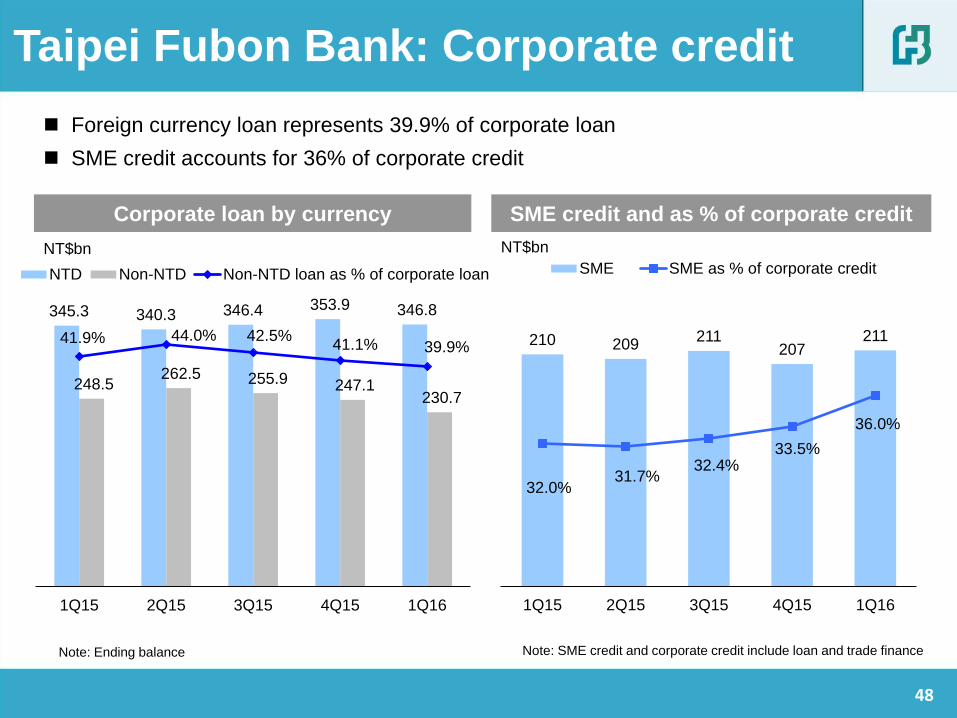

47

210 209 211

207 211

32.0% 31.7%

32.4% 33.5%

36.0%

1Q15 2Q15 3Q15 4Q15 1Q16

SME SME as % of corporate credit

345.3 340.3 346.4 353.9 346.8

248.5 262.5 255.9 247.1

230.7

41.9% 44.0% 42.5% 41.1% 39.9%

1Q15 2Q15 3Q15 4Q15 1Q16

NTD Non-NTD Non-NTD loan as % of corporate loan

Taipei Fubon Bank: Corporate credit

Corporate loan by currency SME credit and as % of corporate credit

NT$bn

Foreign currency loan represents 39.9% of corporate loan

SME credit accounts for 36% of corporate credit

NT$bn

Note: SME credit and corporate credit include loan and trade finance Note: Ending balance

48

Taipei Fubon Bank: Interest yield and margin

NIM and loan-to-deposit spread

Loan yield and deposit yield

Note: Loan rate calculation inclusive of credit card revolving

1.10% 1.09% 1.10% 1.07% 1.10% 1.08% 1.04% 1.01%

1.28% 1.24% 1.27%

1.24% 1.28% 1.31% 1.32% 1.31%

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

NIM Loan-to-deposit spread

2.08% 2.04% 2.08% 2.05% 2.05% 2.05% 2.03% 2.00%

0.80% 0.80% 0.81% 0.81% 0.77% 0.74% 0.70% 0.69%

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

Loan rate Deposit rate

49

41.7% 47.7%

58.3% 52.3%

Mar-15 Mar-16

Time

Demand

55.8% 52.9%

44.2% 47.1%

Mar-15 Mar-16

Time

Demand

Taipei Fubon Bank: Deposit mix and LDR

NTD loan-to-deposit ratio (LDR) Deposit mix in NTD

Deposit mix in foreign currency

NT$bn

NT$bn

Foreign currency LDR

1,039 1,103

382 438

Note: Ending balance

66.2%

53.5%

Mar-15 Mar-16

88.2% 83.8%

Mar-15 Mar-16

50

(118)

186

1Q15 1Q16

0.0%

0.2%

0.4%

0.6%

Mar-13 Mar-14 Mar-15 Mar-16

Corporate loan Mortgage loan

Taipei Fubon Bank: Asset quality

NPL ratio

NPL ratio by business Net provision

Coverage ratio

0.27%

0.03%

NT$mn

Net recovery

0.11% 0.11% 0.12%

0.15% 0.18%

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

0.26% Market

average 1095.99% 1113.09% 1033.47%

816.37% 716.80%

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

51

Performance review by subsidiary

• Fubon Life

• Fubon Securities

Performance highlights of Fubon Financial Holdings

• Fubon Insurance

Agenda

• Taipei Fubon Bank

• Fubon Bank (China)

2015 Embedded value of Fubon Life

52

37.4

59.7

61.6

67.0

1Q15 1Q16

212.9 191.0 205.3

207.2 234.0

269.1

2013 2014 2015

Renewal premium

FYP

28% yoy growth in total premium income

NT$bn

Fubon Life: Total premium

420.1 425.0

474.4

56.7%

43.3%

55.1%

44.9%

49.3%

50.7%

99.0

126.7

52.9%

47.1%

62.2%

37.8%

53

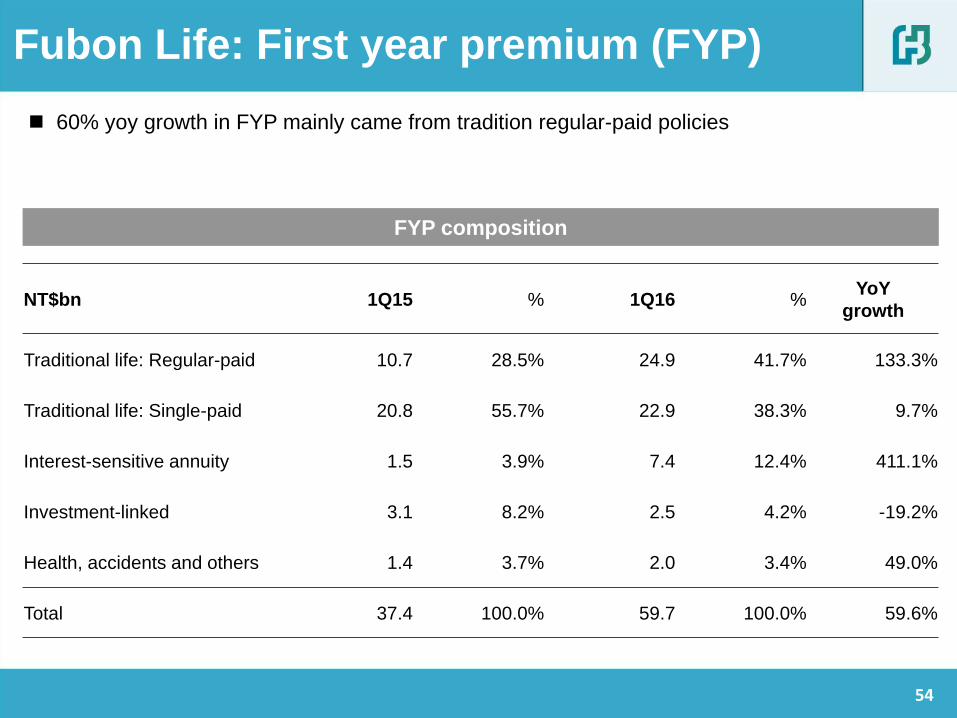

FYP composition

Fubon Life: First year premium (FYP)

60% yoy growth in FYP mainly came from tradition regular-paid policies

NT$bn 1Q15 % 1Q16 % YoY

growth

Traditional life: Regular-paid 10.7 28.5% 24.9 41.7% 133.3%

Traditional life: Single-paid 20.8 55.7% 22.9 38.3% 9.7%

Interest-sensitive annuity 1.5 3.9% 7.4 12.4% 411.1%

Investment-linked 3.1 8.2% 2.5 4.2% -19.2%

Health, accidents and others 1.4 3.7% 2.0 3.4% 49.0%

Total 37.4 100.0% 59.7 100.0% 59.6%

54

FYPE growth 139% yoy led to

improvement in FYPE/FYP ratio

VNB grew 133.5% in 1Q16 yoy

Fubon Life: Value of new business (VNB)

& First year premium equivalent (FYPE)

FYPE

/FYP

NT$bn

12.3

29.4

32.9% 49.3%

VNB

FYPE

NT$bn

Note: 1Q16 VNB is based on 2015 EV actuarial assumptions

FYPE by channel

36.8% 29.9%

30.0% 38.3%

18.2% 21.0%

15.0% 10.8%

1Q15 1Q16

Other

Bancassurance: throughTaipei Fubon bank

Bancassurance: throughexternal banks

Tied agents

10.8% 6.9% 1.3% 2.6% 2.7%

0.9% 17.0% 7.8%

68.3%

81.8%

1Q15 1Q16

Traditional life:Regular-paid

Traditional life:Single-paid

Investment-linked

Interest-sensitiveannuity

Health, accidentsand others

VNB/

FYP 16.8% 24.6%

6.3

14.7

1Q15 1Q16

55

Investment income mainly came from recurring revenue

Fubon Life: Composition of investment income

Note: *2013 data is on pro forma basis to reflect fair value method for investment property evaluation.

NT$bn 1Q15 1Q16 YoY 2013* 2014 2015

Recurring investment income 19.6 23.1 17.8% 75.2 88.7 101.0

Realized gains from fixed income

investment 6.9 3.6 -47.6% 8.0 12.1 9.9

Realized gains from equity

investment 11.3 3.1 -72.3% 4.0 14.0 22.6

FX and others -3.5 -4.9 37.1% -6.3 -6.4 -3.6

Investment property fair value

movement 0.2 0.5 179.9% 5.4 1.4 0.4

Investment income 34.5 25.5 -25.9% 86.3 109.9 130.3

Total investment assets 2,636.4 2,866.1 8.7% 2,227.2 2,588.0 2,814.0

56

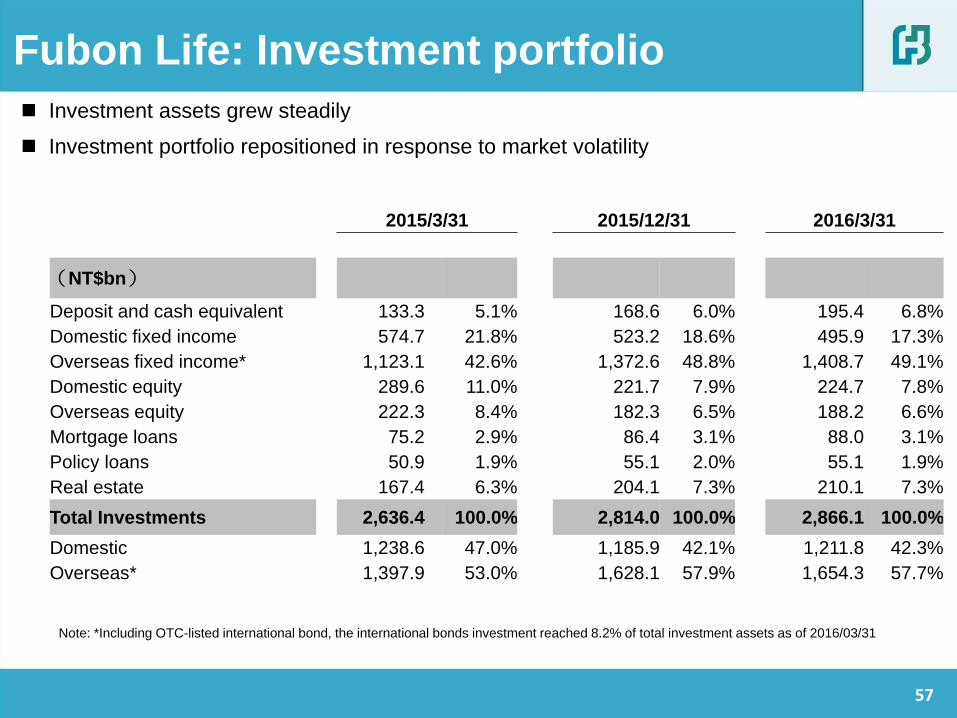

Investment assets grew steadily

Investment portfolio repositioned in response to market volatility

Fubon Life: Investment portfolio

Note: *Including OTC-listed international bond, the international bonds investment reached 8.2% of total investment assets as of 2016/03/31

2015/3/31 2015/12/31 2016/3/31

(NT$bn)

Deposit and cash equivalent 133.3 5.1% 168.6 6.0% 195.4 6.8%

Domestic fixed income 574.7 21.8% 523.2 18.6% 495.9 17.3%

Overseas fixed income* 1,123.1 42.6% 1,372.6 48.8% 1,408.7 49.1%

Domestic equity 289.6 11.0% 221.7 7.9% 224.7 7.8%

Overseas equity 222.3 8.4% 182.3 6.5% 188.2 6.6%

Mortgage loans 75.2 2.9% 86.4 3.1% 88.0 3.1%

Policy loans 50.9 1.9% 55.1 2.0% 55.1 1.9%

Real estate 167.4 6.3% 204.1 7.3% 210.1 7.3%

Total Investments 2,636.4 100.0% 2,814.0 100.0% 2,866.1 100.0%

Domestic 1,238.6 47.0% 1,185.9 42.1% 1,211.8 42.3%

Overseas* 1,397.9 53.0% 1,628.1 57.9% 1,654.3 57.7%

57

Fubon Life: Portfolio of overseas fixed

income

Overseas fixed income by region Overseas fixed income by asset type

4.0% 2.8%

45.7% 38.8%

45.9% 55.2%

4.4% 3.2%

Mar-15 Mar-16

Others

Corporatecredit

Financialbond

Governmentbond

21.6% 19.2%

52.4% 60.9%

26.0% 19.9%

Mar-15 Mar-16

Asia & Other

North America

Europe

58

-36 -36

-67 -65

1Q15 1Q16 CS cost

FX gain/loss & netprovision of FXreserve

Hedging cost & FX gain/loss FX position

Recurring return

Fubon Life: Hedging composition

Currency swap &

FX Policy, 74.7%

Naked USD, 8.1%

Other currencies

, 4.3% Equities/ mutual funds , 12.9%

3.17%

3.35%

2.98%

3.14%

1Q15 1Q16

Beforehedge

Afterhedge

-103bps -101bps

59

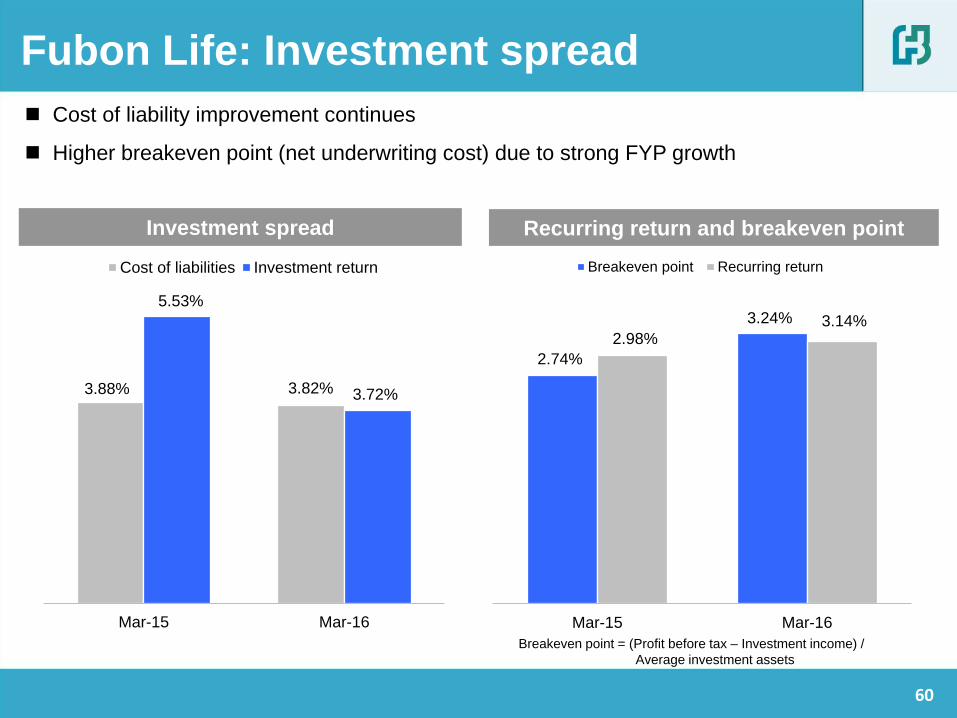

Fubon Life: Investment spread

Cost of liability improvement continues

Higher breakeven point (net underwriting cost) due to strong FYP growth

Breakeven point = (Profit before tax – Investment income) /

Average investment assets

Investment spread Recurring return and breakeven point

2.74%

3.24%

2.98% 3.14%

Mar-15 Mar-16

Breakeven point Recurring return

3.88% 3.82%

5.53%

3.72%

Mar-15 Mar-16

Cost of liabilities Investment return

60

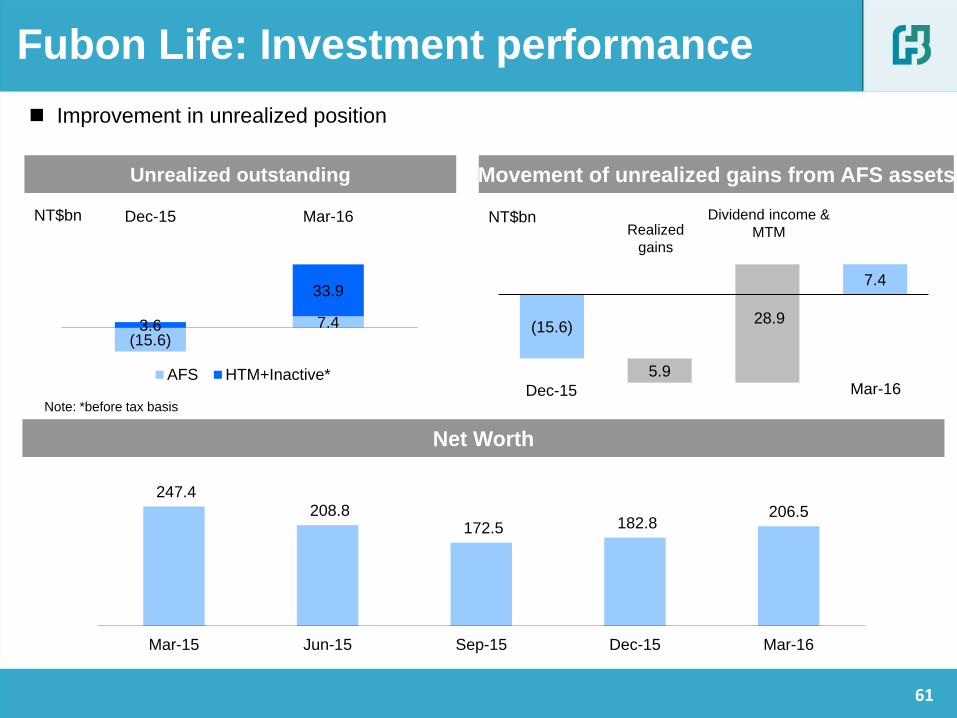

(15.6)

7.4

5.9

28.9

Net Worth

Unrealized outstanding

Fubon Life: Investment performance

Improvement in unrealized position

NT$bn NT$bn Realized

gains

Dividend income &

MTM

Dec-15 Mar-16

Movement of unrealized gains from AFS assets

247.4 208.8

172.5 182.8 206.5

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Note: *before tax basis

(15.6) 7.4 3.6

33.9

Dec-15 Mar-16

AFS HTM+Inactive*

61

Performance review by subsidiary

• Fubon Life

• Fubon Securities

Performance highlights of Fubon Financial Holdings

• Fubon Insurance

Agenda

• Taipei Fubon Bank

• Fubon Bank (China)

2015 Embedded value of Fubon Life

62

50.6% 52.1%

13.4%

13.7% 7.6%

5.7% 2.9%

3.3% 15.3%

15.2% 10.2%

10.0%

1Q15 1Q16

Others

Health/Injury

Engineering

Marine

Fire

Auto

Net combined ratio

NT$bn

Premium growth outperformed industry. Top 1 position in premium market share

Net claim ratio increase due to net retained losses from Tainan earthquake

Note: Standalone basis Note: Exclusive of auto compulsory due to the claims are reimbursed

Fubon Insurance: Operating snapshot

Direct written premium by product

7.1

8.1 97.4%

88.8%

54.1% 61.8%

34.7%

35.6%

1Q15 1Q16

Net expense ratio

Net claim ratio

63

Performance review by subsidiary

• Fubon Life

• Fubon Securities

Performance highlights of Fubon Financial Holdings

• Fubon Insurance

Agenda

• Taipei Fubon Bank

• Fubon Bank (China)

2015 Embedded value of Fubon Life

64

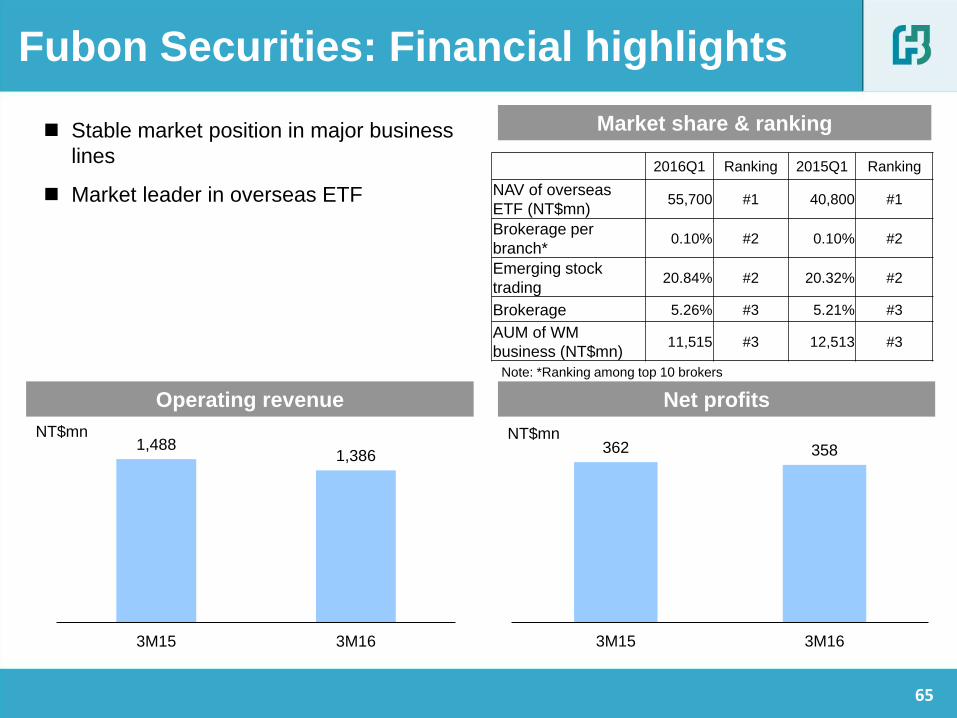

Fubon Securities: Financial highlights

Market share & ranking

Operating revenue

NT$mn

Stable market position in major business

lines

Market leader in overseas ETF

Net profits

NT$mn 1,488

1,386

3M15 3M16

362 358

3M15 3M16

2016Q1 Ranking 2015Q1 Ranking

NAV of overseas

ETF (NT$mn) 55,700 #1 40,800 #1

Brokerage per

branch* 0.10% #2 0.10% #2

Emerging stock

trading 20.84% #2 20.32% #2

Brokerage 5.26% #3 5.21% #3

AUM of WM

business (NT$mn) 11,515 #3 12,513 #3

Note: *Ranking among top 10 brokers

65

Performance review by subsidiary

• Fubon Life

• Fubon Securities

Performance highlights of Fubon Financial Holdings

• Fubon Insurance

Agenda

• Taipei Fubon Bank

• Fubon Bank (China)

2015 Embedded value of Fubon Life

66

20,670 23,522

7,567 4,867

Mar-15 Mar-16

Rediscount Loans (excluding rediscount)

Fubon Bank (China): Key balance sheet

items

Assets Net worth

Deposits Loans

RMB$m

28,388 28,237

RMB$m RMB$m

RMB$m

37,882

43,387

Mar-15 Mar-16

4,578

5,033

Mar-15 Mar-16

60,885 67,367

Mar-15 Mar-16

67

Fubon Bank (China): Financial highlight

ROAA & ROAE

NIM Net Profits

NPL ratio & Coverage ratio

RMB$m

84

152

1Q15 1Q16

0.55%

0.86% 7.39%

12.24%

1Q15 1Q16

ROAA ROAE

1.17%

1.91%

230.0% 157.5%

Mar-15 Mar-16

NPL Coverage ratio

1.36%

1.55%

1Q15 1Q16

68

Performance review by subsidiary

• Fubon Life

• Fubon Securities

Performance highlights of Fubon Financial Holdings

• Fubon Insurance

Agenda

• Taipei Fubon Bank

• Fubon Bank (China)

2015 Embedded value of Fubon Life

69

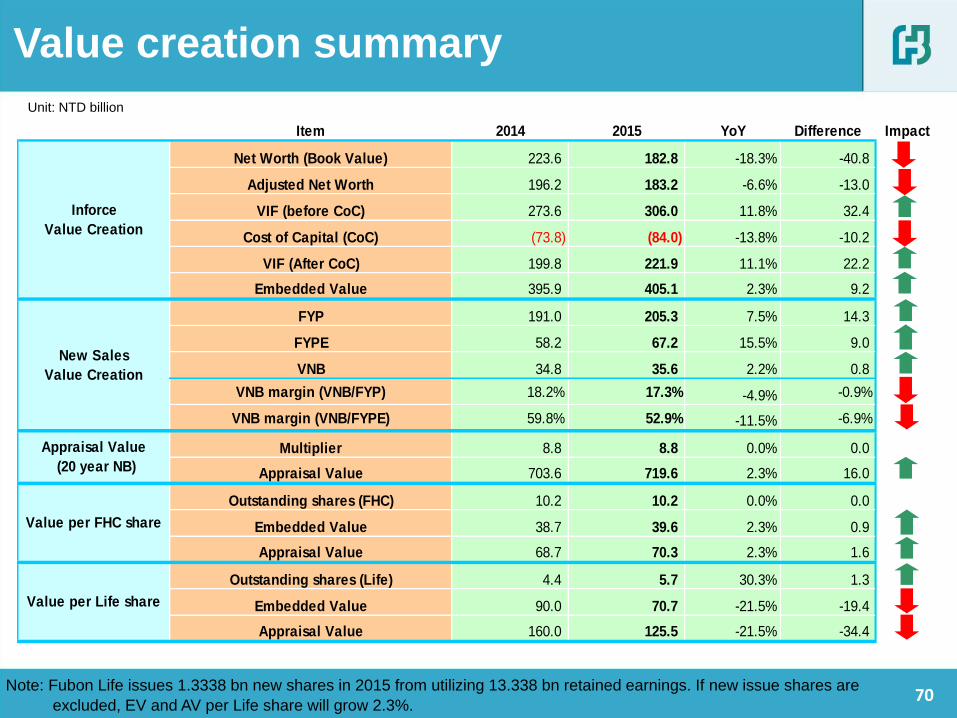

Unit: NTD billion

Item 2014 2015 YoY Difference Impact

Net Worth (Book Value) 223.6 182.8 -18.3% -40.8

Adjusted Net Worth 196.2 183.2 -6.6% -13.0

VIF (before CoC) 273.6 306.0 11.8% 32.4

Cost of Capital (CoC) (73.8) (84.0) -13.8% -10.2

VIF (After CoC) 199.8 221.9 11.1% 22.2

Embedded Value 395.9 405.1 2.3% 9.2

FYP 191.0 205.3 7.5% 14.3

FYPE 58.2 67.2 15.5% 9.0

VNB 34.8 35.6 2.2% 0.8

VNB margin (VNB/FYP) 18.2% 17.3% -4.9% -0.9%

VNB margin (VNB/FYPE) 59.8% 52.9% -11.5% -6.9%

Multiplier 8.8 8.8 0.0% 0.0

Appraisal Value 703.6 719.6 2.3% 16.0

Outstanding shares (FHC) 10.2 10.2 0.0% 0.0

Embedded Value 38.7 39.6 2.3% 0.9

Appraisal Value 68.7 70.3 2.3% 1.6

Outstanding shares (Life) 4.4 5.7 30.3% 1.3

Embedded Value 90.0 70.7 -21.5% -19.4

Appraisal Value 160.0 125.5 -21.5% -34.4

Value per FHC share

Value per Life share

Inforce

Value Creation

New Sales

Value Creation

Appraisal Value

(20 year NB)

Note: Fubon Life issues 1.3338 bn new shares in 2015 from utilizing 13.338 bn retained earnings. If new issue shares are

excluded, EV and AV per Life share will grow 2.3%.

Value creation summary

70

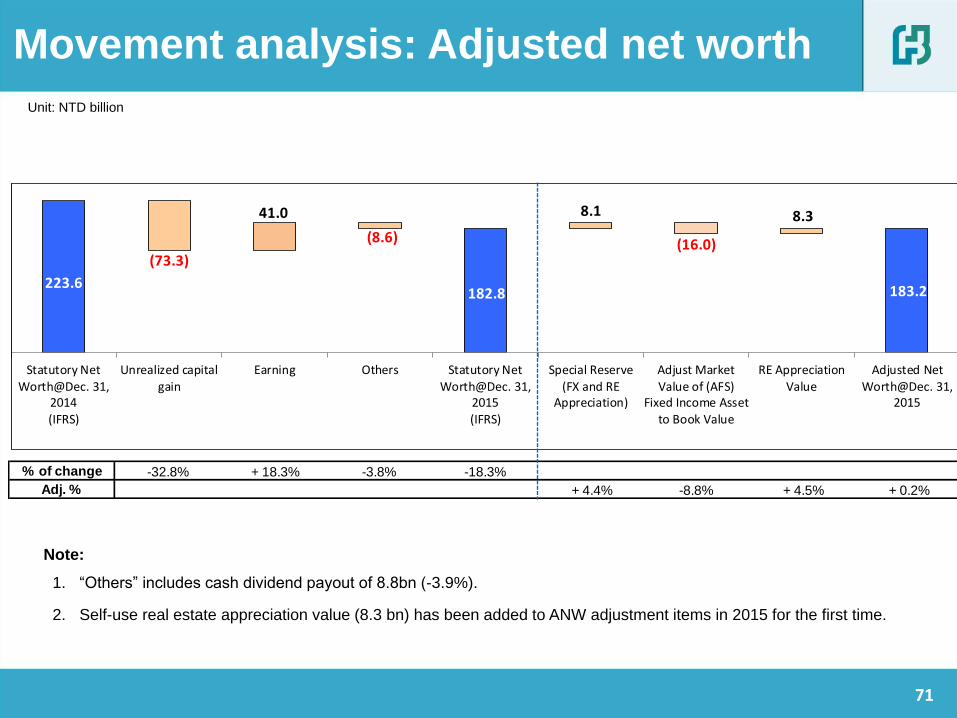

Graph

add

% of change -32.8% + 18.3% -3.8% -18.3%

Adj. % + 4.4% -8.8% + 4.5% + 0.2%

223.6

(73.3)

41.0

(8.6)

182.8

8.1

(16.0)

8.3

183.2

Statutory NetWorth@Dec. 31,

2014(IFRS)

Unrealized capitalgain

Earning Others Statutory NetWorth@Dec. 31,

2015(IFRS)

Special Reserve(FX and RE

Appreciation)

Adjust MarketValue of (AFS)

Fixed Income Assetto Book Value

RE AppreciationValue

Adjusted NetWorth@Dec. 31,

2015

Note:

1. “Others” includes cash dividend payout of 8.8bn (-3.9%).

2. Self-use real estate appreciation value (8.3 bn) has been added to ANW adjustment items in 2015 for the first time.

Movement analysis: Adjusted net worth

Unit: NTD billion

71

% of change -0.8% -9.3% + 11.7% + 1.0% -6.3% + 0.5% + 15.1% + 11.8%

273.6

(2.3)(25.4)

32.0 2.7

(17.2)

1.3 41.2

306.0

-80.0

-30.0

20.0

70.0

120. 0

170. 0

220. 0

270. 0

320. 0

2014 VIF(before CoC)

Model Change Existingbusiness -

transfer to networth

Required returnon existing

business

Data Change Eco.Assumption

Change

Non-eco.Assumption

Change

2015VNB(before

CoC)

2015 VIF(beforeCoC)

Note:

1. Economic assumption change includes changes of foreign exchange rate (+0.9%) and investment return (-7.2%).

2. The equivalent return of EV2014 reporting for VIF increased from 4.64% to 4.70% to reflect rolling over effect.

3. The equivalent return of EV2015 reporting for VIF is 4.58%.

4. 2015 VNB (after CoC) is 35.6 bn.

Unit: NTD billion

Movement analysis: Value of in-force

(before CoC)

72

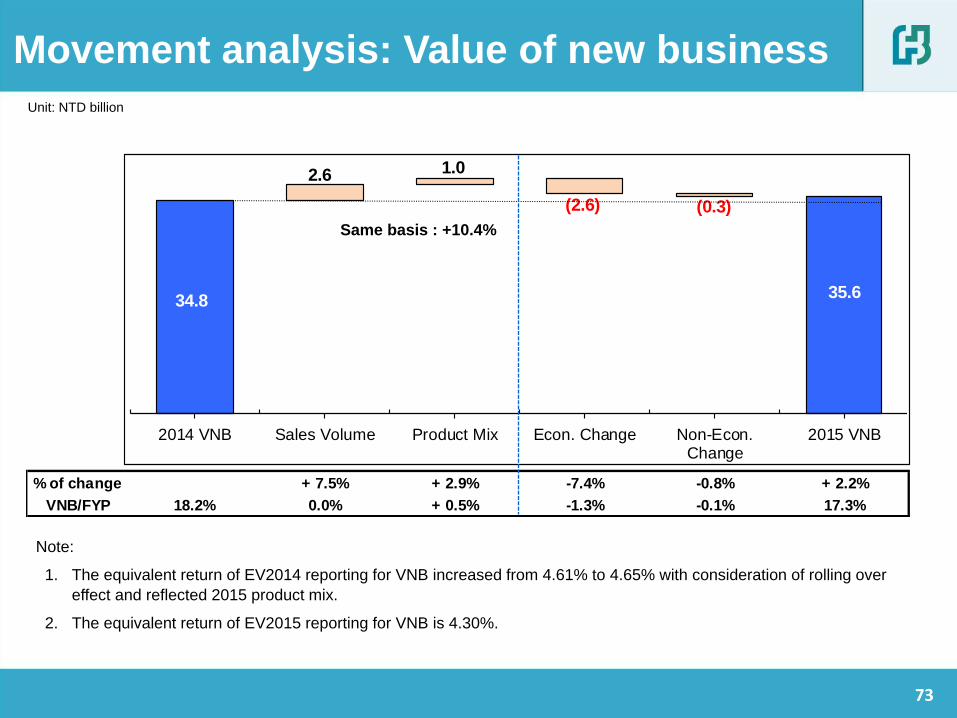

Same basis YoY +14%

% of change + 7.5% + 2.9% -7.4% -0.8% + 2.2%

VNB/FYP 18.2% 0.0% + 0.5% -1.3% -0.1% 17.3%

34.8

2.6 1.0

(2.6) (0.3)

35.6

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10. 0

12. 0

14. 0

16. 0

18. 0

20. 0

22. 0

24. 0

26. 0

28. 0

30. 0

32. 0

34. 0

36. 0

38. 0

40. 0

2014 VNB Sales Volume Product Mix Econ. Change Non-Econ.Change

2015 VNB

Same basis : +10.4%

Note:

1. The equivalent return of EV2014 reporting for VNB increased from 4.61% to 4.65% with consideration of rolling over

effect and reflected 2015 product mix.

2. The equivalent return of EV2015 reporting for VNB is 4.30%.

Movement analysis: Value of new business

Unit: NTD billion

73

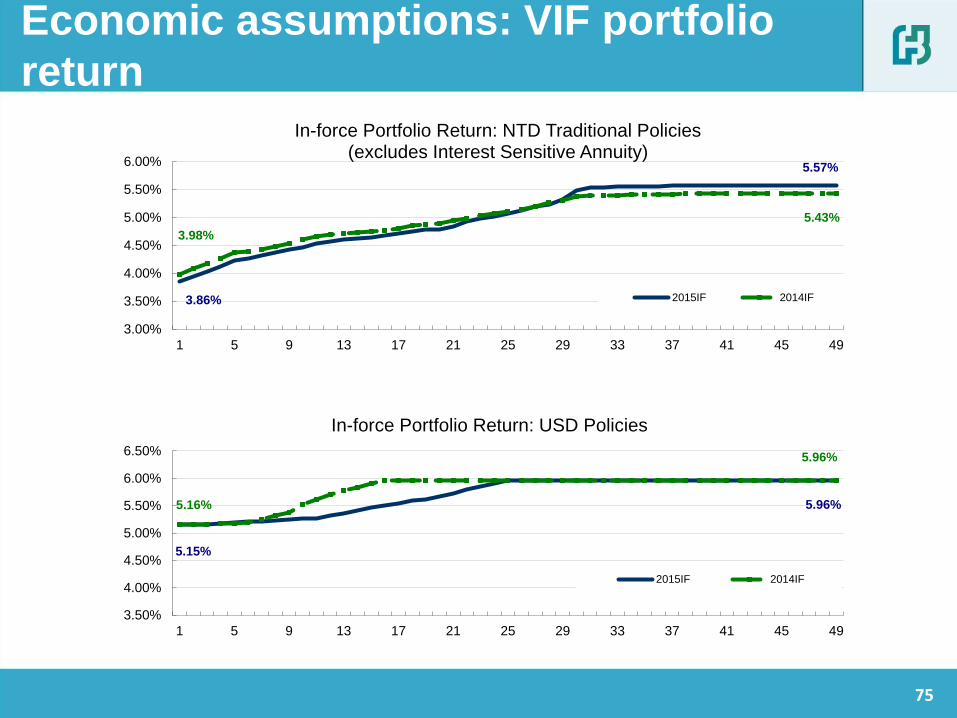

Year 2014 Year 2015

Investment

return

VIF

NTD Traditional Policies :

Year 2015 to Year 2052 at 3.98%~5.43%(2053+)

USD Policies :

Year 2015 to Year 2030 at 5.16%~5.96%(2031+)

V1NB

NTD Traditional Policies :

Year 2014 to Year 2047 at 3.89%~5.43%(2048+)

USD Policies :

Year 2014 to Year 2043 at 5.14%~5.96%(2044+)

ISA

Average retained spread for the Interest sensitive

business is around 100bps.

VIF

NTD Traditional Policies :

Year 2016 to Year 2052 at 3.86%~5.57%(2053+)

USD Policies :

Year 2016 to Year 2040 at 5.15%~5.96%(2041+)

V1NB

NTD Traditional Policies :

Year 2015 to Year 2050 at 3.46%~5.55%(2051+)

USD Policies:

Year 2015 to Year 2045 at 4.37%~5.96%(2046+)

ISA

Average retained spread for the Interest sensitive

business is around 50~100 bps.

Risk Discount

Rate

VIF: 11.0%

V1NB: 10.5%

VIF: 11.0%

V1NB: 10.5%

Equivalent

Return

VIF: 4.64% (rolling over to 2015: 4.70%)

V1NB: 4.61% (rolling over to 2015: 4.65%)

VIF: 4.58%

V1NB: 4.30%

YC (10 year)

Initial / ultimate

TWD: 1.64% / 3.50%

USD : 2.28% / 5.25%

TWD: 1.16% / 3.50%

USD: 2.19% / 5.25%

Note

• The FX reserve mechanism was stipulated from 2012, its respective cost is reflected in the derivation of portfolio return.

Economic assumptions

74

3.86%

5.57%

3.98%

5.43%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

1 5 9 13 17 21 25 29 33 37 41 45 49

In-force Portfolio Return: NTD Traditional Policies (excludes Interest Sensitive Annuity)

2015IF 2014IF

5.15%

5.96% 5.16%

5.96%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

1 5 9 13 17 21 25 29 33 37 41 45 49

In-force Portfolio Return: USD Policies

2015IF 2014IF

Economic assumptions: VIF portfolio

return

75

3.46%

5.55%

3.89%

5.43%

3.00%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

1 5 9 13 17 21 25 29 33 37 41 45 49

NB Portfolio Return: NTD Traditional Policies (excludes Interest Sensitive Annuity)

2015NB 2014NB

4.37%

5.96%

5.14% 5.96%

3.50%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

1 5 9 13 17 21 25 29 33 37 41 45 49

NB Portfolio Return: USD Policies

2015NB 2014NB

Economic assumptions: V1NB portfolio

return

76

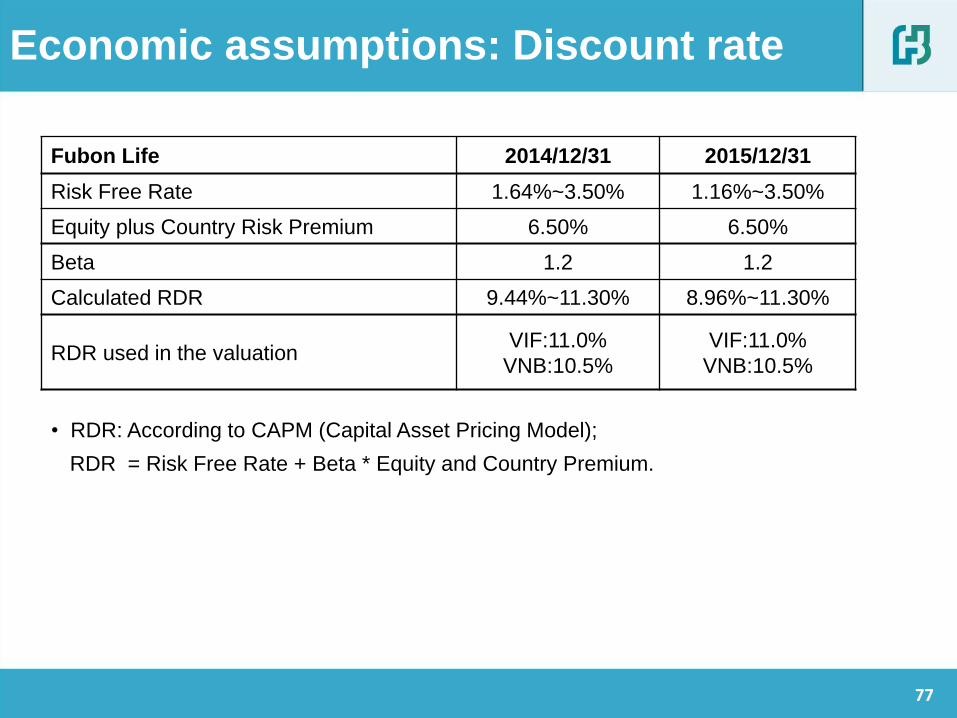

Economic assumptions: Discount rate

Fubon Life 2014/12/31 2015/12/31

Risk Free Rate 1.64%~3.50% 1.16%~3.50%

Equity plus Country Risk Premium 6.50% 6.50%

Beta 1.2 1.2

Calculated RDR 9.44%~11.30% 8.96%~11.30%

RDR used in the valuation VIF:11.0%

VNB:10.5%

VIF:11.0%

VNB:10.5%

• RDR: According to CAPM (Capital Asset Pricing Model);

RDR = Risk Free Rate + Beta * Equity and Country Premium.

77

Cost of capital

Cost of Capital projection

Maintain the regulatory minimum RBC level of 200% with consideration of following factors:

1) Add 30% C3 risk capital of previous year for all traditional products every year (excludes investment-linked product);

2) Reflect current business operation and future strategy.

Risk-based capital (RBC) regulation changes in 2015:

1) Lower risk factor of foreign real estate investment via SPV-loan in C0 (from 0.2608 to 0.1) to be the same as foreign real estate investment via SPV-equity investment;

2) Lower risk factor of domestic and foreign private equity fund investment in C1 (from 0.2950 to 0.2638);

3) Lower risk factor of domestic stock investment in C1 from 0.2411 to 0.2274;

4) Raise the extra charge percentage of previous year’s C3 risk for traditional products from 10% to 30%.

78

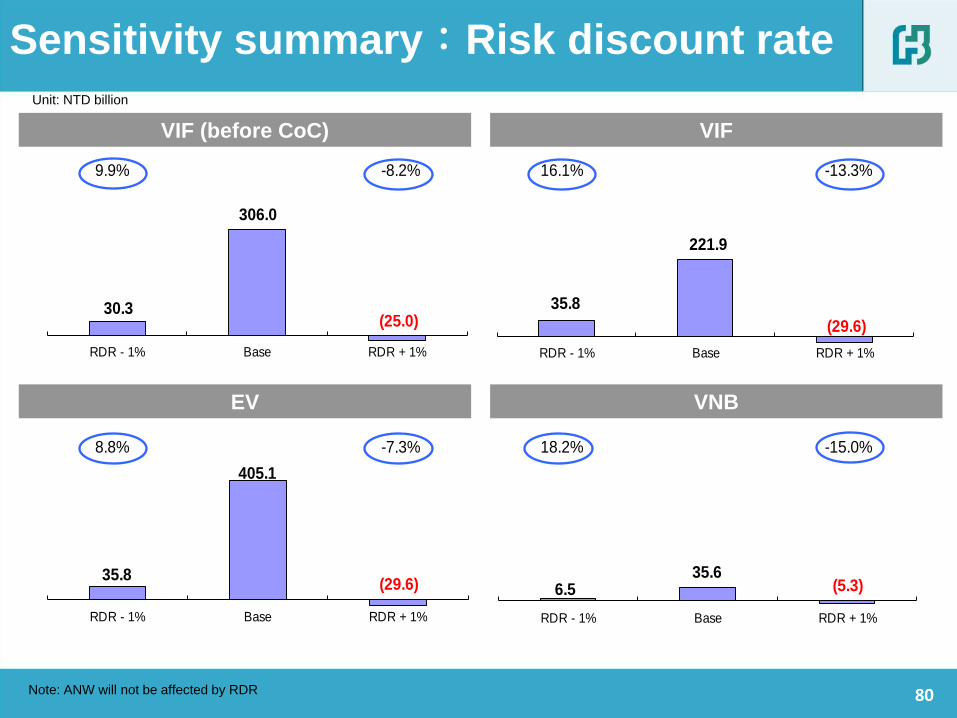

-17.8% 17.8% -25.6% 25.6%

-14.0% 14.0% -19.9% 19.9%

(54.4)

306.0

54.4

Return - 0.25% Base Return + 0.25%

(56.8)

405.1

56.8

Return - 0.25% Base Return + 0.25%

(56.8)

221.9

56.8

Return - 0.25% Base Return + 0.25%

(7.1)35.6

7.1

Return - 0.25% Base Return + 0.25%

Sensitivity summary:Portfolio return

Note: ANW will not be affected by portfolio return.

VIF (before CoC) VIF

EV VNB

Unit: NTD billion

79

9.9% -8.2% 16.1% -13.3%

8.8% -7.3% 18.2% -15.0%

30.3

306.0

(25.0)

RDR - 1% Base RDR + 1%

35.8

405.1

(29.6)

RDR - 1% Base RDR + 1%

35.8

221.9

(29.6)

RDR - 1% Base RDR + 1%

6.5 35.6

(5.3)

RDR - 1% Base RDR + 1%

VIF (before CoC) VIF

EV VNB

Sensitivity summary:Risk discount rate

Note: ANW will not be affected by RDR

Unit: NTD billion

80

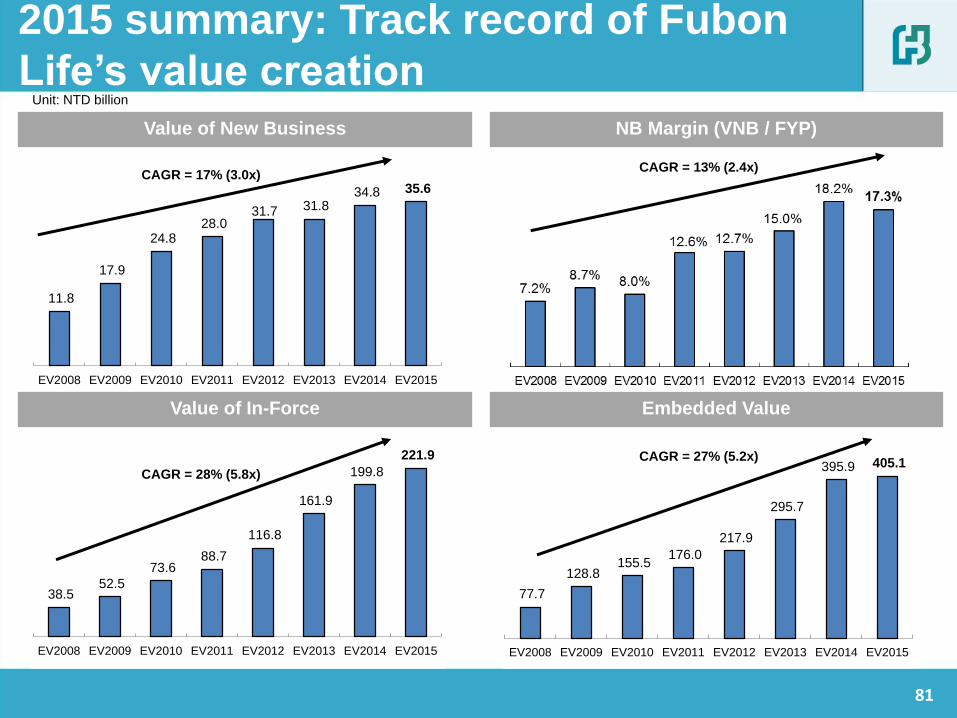

11.8

17.9

24.8 28.0

31.7 31.8 34.8 35.6

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

Value of New Business

單位: 新台幣十億元

38.5 52.5

73.6 88.7

116.8

161.9

199.8

221.9

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

77.7

128.8 155.5

176.0

217.9

295.7

395.9 405.1

EV2008 EV2009 EV2010 EV2011 EV2012 EV2013 EV2014 EV2015

CAGR = 17% (3.0x) CAGR = 13% (2.4x)

CAGR = 28% (5.8x)

CAGR = 27% (5.2x)

2015 summary: Track record of Fubon

Life’s value creation NB Margin (VNB / FYP)

Value of In-Force Embedded Value

Unit: NTD billion

81

3.68 3.87 3.88 3.97 4.06 4.14 4.10

3.78 3.80 4.01

4.42

4.74 4.97

EV2009/2010 EV2010/2011 EV2011/2012 EV2012/2013 EV2013/2014 EV2014/2015 EV2015/2016

Investment return: Assumption vs. Actual

Note:

1. Track record shows higher actual return than EV assumption in general.

2. The investment return for 2013 and 2014 includes fair value recognition of investment property, which is

+0.38% and +0.05% respectively.

82

The Engagement

• Deloitte Advisory (Hong Kong) Limited (“Deloitte Consulting”) were retained by Fubon Life to perform an

independent review of the Embedded Value (EV) as at 31 December 2015 and the Value of One Year’s New

Business (V1NB) written over the period of 1 January 2015 to 31 December 2015.

Scope of Deloitte Consulting’s Involvement

• Review and opine on the reasonableness of the EV and V1NB as calculated by the Company;

• Review of the reasonableness of the assumptions used in the calculations, taking into consideration both the

Company’s recent experience and the experience of the Taiwanese life insurance market;

• Review, at a high-level, model changes to the actuarial projection model since the previous valuation date;

• Review of the Company’s projection approach of the Cost of Capital;

• Review of the data put through the model compared to the policy data on the Company’s policy administration

systems to judge the extent to which the business has been valued in the financial model and to identify the

portion (if any) omitted and how that was valued;

• Review of the approach used to determine the Adjusted Net Worth (“ANW”), in particular, the adjustments

made in deriving the ANW, and any other adjustments made outside of the actuarial projection model;

• Review of the Company's analysis of change in the Value of In-Force Business (“VIF”) between 31 December

2014 and 31 December 2015.

Deloitte Consulting

The Engagement • Deloitte Advisory (Hong Kong) Limited (“Deloitte Consulting”) were retained by Fubon Life to perform an

independent review of the Embedded Value (EV) as at 31 December 2015 and the Value of One Year’s New

Business (V1NB) written over the period of 1 January 2015 to 31 December 2015.

Scope of Deloitte Consulting’s Involvement • Review and opine on the reasonableness of the EV and V1NB as calculated by the Company;

• Review of the reasonableness of the assumptions used in the calculations, taking into consideration both the

Company’s recent experience and the experience of the Taiwanese life insurance market;

• Review, at a high-level, model changes to the actuarial projection model since the previous valuation date;

• Review of the Company’s projection approach of the Cost of Capital;

• Review of the data put through the model compared to the policy data on the Company’s policy

administration systems to judge the extent to which the business has been valued in the financial model and

to identify the portion (if any) omitted and how that was valued;

• Review of the approach used to determine the Adjusted Net Worth (“ANW”), in particular, the adjustments

made in deriving the ANW, and any other adjustments made outside of the actuarial projection model;

• Review of the Company's analysis of change in the Value of In-Force Business (“VIF”) between 31 December

2014 and 31 December 2015.

Independent review by Deloitte Consulting

83

Fubon Life calculated the EV and V1NB at Risk Adjusted Discount Rates (“RDR”) of

11.0% and 10.5% respectively.

RFR based on current government

bond yield

RFR based on Company’s long-

term view

Equivalent RFR for New Business

Equivalent RFR for In-Force Business

Risk Free Rate (“RFR”) 1.16% 3.50% 2.59% 2.64%

Equity and Country Risk Premium 6.50% 6.50% 6.50% 6.50%

Beta 1.20 1.20 1.20 1.20

Calculated Risk Discount Rate 8.96% 11.30% 10.39% 10.44%

Risk Discount Rate used in the Valuation for VIF

11.00%

Risk Discount Rate used in the Valuation for V1NB

10.50%

Reference – RDR based on Capital Asset Pricing Model (CAPM):

RDR = RFR + Beta * Equity and Country Risk Premium

Deloitte Consulting

Risk adjusted discount rates

84

Deloitte Consulting independently derived a range of RDRs using the CAPM

approach:

The low end of the RDR is developed based on the current yield on 10-year Taiwan government bonds.

The high end of the RDR is developed based on the Company’s view of the 10-year Taiwan government bond in the future.

The equivalent RFR is the RFR equivalent to using a set of graded-up RFR from 1.16% to 3.50% that derives the same VIF and V1NB.

The Equity and Country Risk Premium was developed based on the Country Default Spreads and Risk Premiums research published by New York University.

The Beta of 1.2 was set using a risk profiling approach which considers risks related to the product range, distribution diversification/vulnerability, regulatory intervention and investments. Note that this beta value is consistent with that used in previous valuations.

The RDR assumption applied by Fubon Life in the valuation lies within the range of RDR that we derived.

In particular, we feel comfortable with different RDRs being used for the valuation of the in-force and new business, given the specific market conditions in Taiwan: it is well-known that the legacy business has a much riskier profile than the current new business, and hence it is reasonable for shareholders to be expecting a higher rate of return for the higher risk level. We feel that Fubon Life has taken a good approach in splitting up the RDR assumption for the two distinctively different blocks of business.

Deloitte Consulting

Comments: Risk adjusted discount rates

85

A set of rising investment return assumption has been used in this valuation

which is considered reasonable for the present market conditions.

Fubon Life’s derivation of the investment return assumption is featured by the following:

• Derivation methodology is consistent with that applied in previous valuations;

• The methodology involves:

For VIF, the investment return assumption was derived from a combination of the investment return

generated by the run-off of the existing asset portfolio and of that from future purchases of new

assets;

For V1NB, the new business is not supported by returns on existing assets and the investment

return was derived from future purchases of new assets;

• New assets are purchased at the prevailing new money rates, which are set to equal to the expected future

risk free rates plus a risk margin for each asset type;

• Future risk free rates are set starting off with the actual yield curves as at the valuation date and are

assumed to rise to a long-term level over a 10-year period. For New Taiwan Dollar and US Dollar

respectively, the initial risk free rates are 1.16% and 2.19% and a long-term risk free rate of 3.50% and

5.25% is assumed.

• Different assumptions were derived for different types of business, which were assumed to have a different

long-term asset allocation.

• For some business lines, the investment return assumption derived in the above-mentioned manner was

capped at a certain level for conservative reasons.

Deloitte Consulting

Comments: Investment return (1)

86

It is in Deloitte Consulting’s view that:

Methodology

• Fubon Life’s derivation methodology for the investment return assumption is reasonable

and consistent with the way that the ANW is calculated;

Economic Assumptions

• The expected long-term risk-free rate for New Taiwan Dollar yield and US Dollar yield are

maintained at 3.5% and 5.25% respectively.

• We note that taking a view on the future capital market is not uncommon under the

traditional Embedded Value methodology. On a macro-economic level the arguments put

forward for rising interest rates are plausible, and we note that the expected future rise in

yields is spread out over a reasonably long period of 10 years.

• Readers should be aware that capital market conditions are subject to the impact of

many forces. Yields and prices of financial instruments can move dramatically in a short

period of time. As a result, it is difficult to predict the interest rate level in the future with

great certainty. Readers should refer to the sensitivity tests to develop a broader

understanding of the impact of the investment return assumption on the assessment of

the economic value of Fubon Life.

• Overall, the economic assumptions appear to be reasonable.

Deloitte Consulting

Comments: Investment return (2)

87

Non - Economic Assumptions

• The non-economic assumptions reflect Fubon Life’s best estimate of future operating experience, and

are appropriately supported by the company’s historical operating experience.

Deloitte Consulting

Comments: Non-Economic assumptions

88

Deloitte Consulting have reviewed the Embedded Value and Value of

One Year’s New Business results at a high-level under the generally accepted method for

calculating traditional embedded values in Taiwan:

• Review of the changes in the VIF relative to the assumption changes and model changes

from 2014 to 2015;

• Review of the changes in the new business profit margin relative to that in 2014 based on

information on changes in sales mix, sales volume and valuation assumptions;

• Review of the sensitivities relative to the base case results.

The Embedded Value and Value of One Year’s New Business results appear to be

reasonable within the above context.

Deloitte Consulting’s detailed opinion can be found in their opinion letter.

Deloitte Consulting

Comments: EV and V1NB Results

89

Thank you

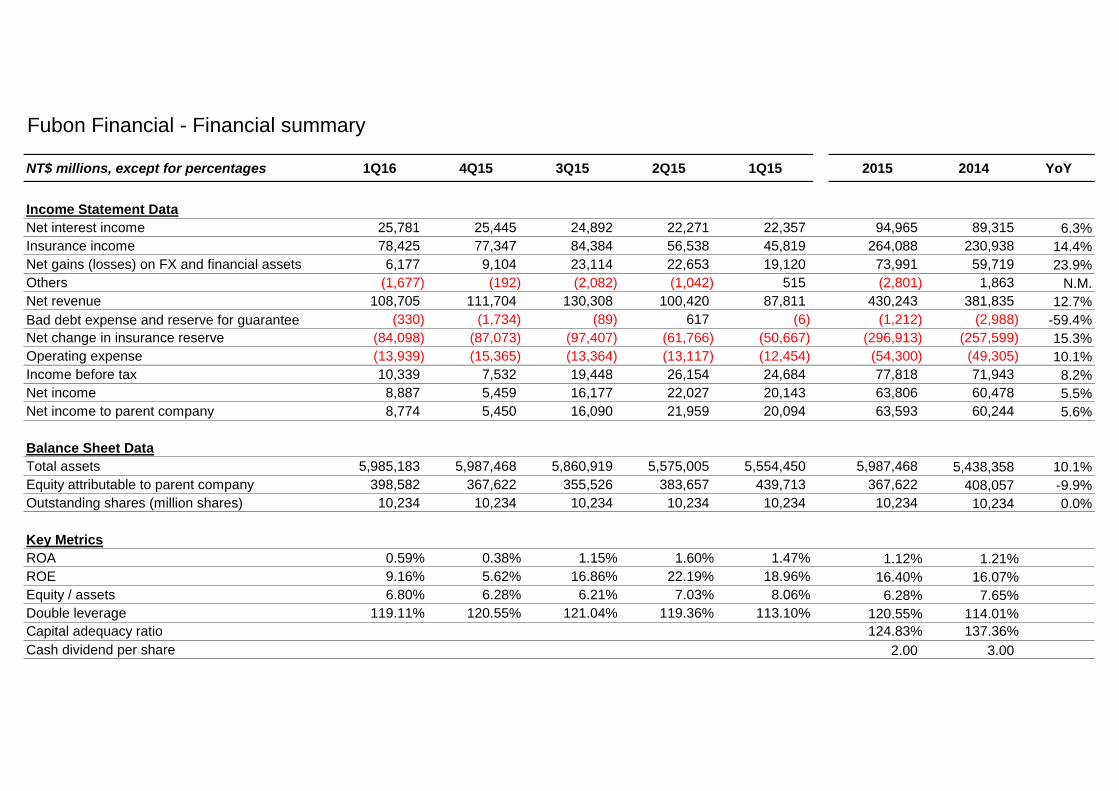

Fubon Financial - Financial summary

NT$ millions, except for percentages 1Q16 4Q15 3Q15 2Q15 1Q15 2015 2014 YoY

Income Statement Data

Net interest income 25,781 25,445 24,892 22,271 22,357 94,965 89,315 6.3%

Insurance income 78,425 77,347 84,384 56,538 45,819 264,088 230,938 14.4%

Net gains (losses) on FX and financial assets 6,177 9,104 23,114 22,653 19,120 73,991 59,719 23.9%

Others (1,677) (192) (2,082) (1,042) 515 (2,801) 1,863 N.M.

Net revenue 108,705 111,704 130,308 100,420 87,811 430,243 381,835 12.7%

Bad debt expense and reserve for guarantee (330) (1,734) (89) 617 (6) (1,212) (2,988) -59.4%

Net change in insurance reserve (84,098) (87,073) (97,407) (61,766) (50,667) (296,913) (257,599) 15.3%

Operating expense (13,939) (15,365) (13,364) (13,117) (12,454) (54,300) (49,305) 10.1%

Income before tax 10,339 7,532 19,448 26,154 24,684 77,818 71,943 8.2%

Net income 8,887 5,459 16,177 22,027 20,143 63,806 60,478 5.5%

Net income to parent company 8,774 5,450 16,090 21,959 20,094 63,593 60,244 5.6%

Balance Sheet Data

Total assets 5,985,183 5,987,468 5,860,919 5,575,005 5,554,450 5,987,468 5,438,358 10.1%

Equity attributable to parent company 398,582 367,622 355,526 383,657 439,713 367,622 408,057 -9.9%

Outstanding shares (million shares) 10,234 10,234 10,234 10,234 10,234 10,234 10,234 0.0%

Key Metrics

ROA 0.59% 0.38% 1.15% 1.60% 1.47% 1.12% 1.21%

ROE 9.16% 5.62% 16.86% 22.19% 18.96% 16.40% 16.07%

Equity / assets 6.80% 6.28% 6.21% 7.03% 8.06% 6.28% 7.65%

Double leverage 119.11% 120.55% 121.04% 119.36% 113.10% 120.55% 114.01%

Capital adequacy ratio 124.83% 137.36%

Cash dividend per share 2.00 3.00

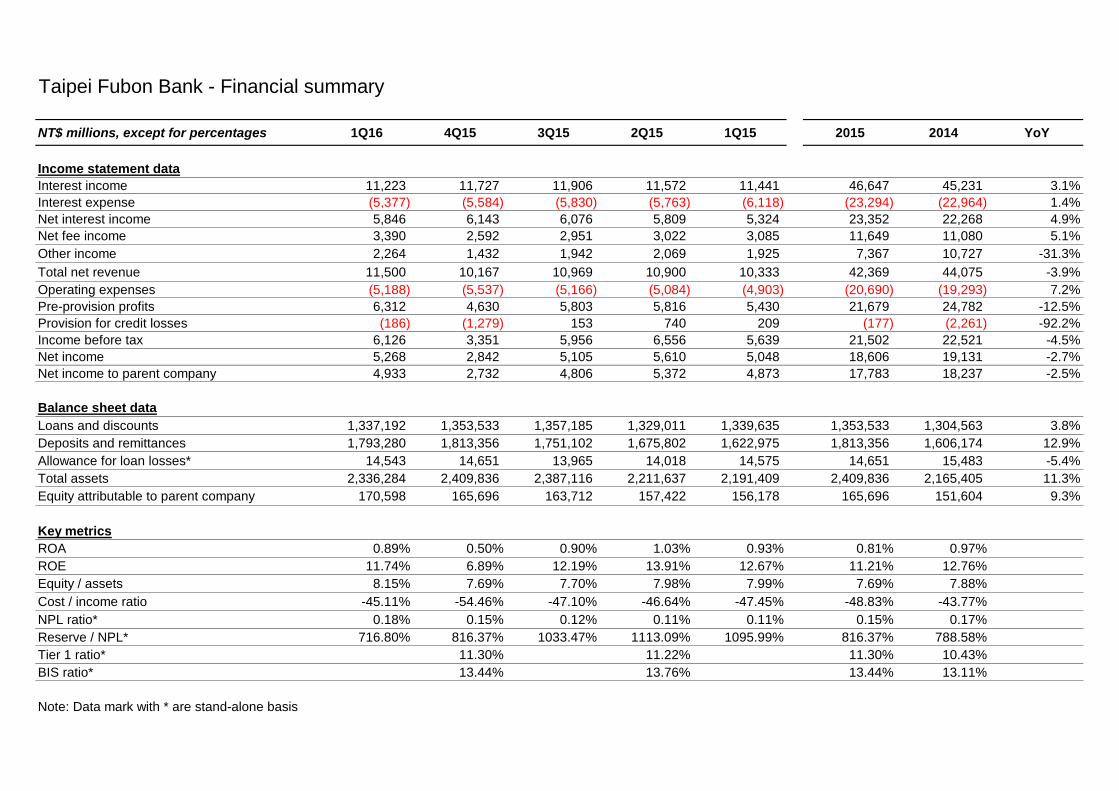

Taipei Fubon Bank - Financial summary

NT$ millions, except for percentages 1Q16 4Q15 3Q15 2Q15 1Q15 2015 2014 YoY

Income statement data

Interest income 11,223 11,727 11,906 11,572 11,441 46,647 45,231 3.1%

Interest expense (5,377) (5,584) (5,830) (5,763) (6,118) (23,294) (22,964) 1.4%

Net interest income 5,846 6,143 6,076 5,809 5,324 23,352 22,268 4.9%

Net fee income 3,390 2,592 2,951 3,022 3,085 11,649 11,080 5.1%

Other income 2,264 1,432 1,942 2,069 1,925 7,367 10,727 -31.3%

Total net revenue 11,500 10,167 10,969 10,900 10,333 42,369 44,075 -3.9%

Operating expenses (5,188) (5,537) (5,166) (5,084) (4,903) (20,690) (19,293) 7.2%

Pre-provision profits 6,312 4,630 5,803 5,816 5,430 21,679 24,782 -12.5%

Provision for credit losses (186) (1,279) 153 740 209 (177) (2,261) -92.2%

Income before tax 6,126 3,351 5,956 6,556 5,639 21,502 22,521 -4.5%

Net income 5,268 2,842 5,105 5,610 5,048 18,606 19,131 -2.7%

Net income to parent company 4,933 2,732 4,806 5,372 4,873 17,783 18,237 -2.5%

Balance sheet data

Loans and discounts 1,337,192 1,353,533 1,357,185 1,329,011 1,339,635 1,353,533 1,304,563 3.8%

Deposits and remittances 1,793,280 1,813,356 1,751,102 1,675,802 1,622,975 1,813,356 1,606,174 12.9%

Allowance for loan losses* 14,543 14,651 13,965 14,018 14,575 14,651 15,483 -5.4%

Total assets 2,336,284 2,409,836 2,387,116 2,211,637 2,191,409 2,409,836 2,165,405 11.3%

Equity attributable to parent company 170,598 165,696 163,712 157,422 156,178 165,696 151,604 9.3%

Key metrics

ROA 0.89% 0.50% 0.90% 1.03% 0.93% 0.81% 0.97%

ROE 11.74% 6.89% 12.19% 13.91% 12.67% 11.21% 12.76%

Equity / assets 8.15% 7.69% 7.70% 7.98% 7.99% 7.69% 7.88%

Cost / income ratio -45.11% -54.46% -47.10% -46.64% -47.45% -48.83% -43.77%

NPL ratio* 0.18% 0.15% 0.12% 0.11% 0.11% 0.15% 0.17%

Reserve / NPL* 716.80% 816.37% 1033.47% 1113.09% 1095.99% 816.37% 788.58%

Tier 1 ratio* 11.30% 11.22% 11.30% 10.43%

BIS ratio* 13.44% 13.76% 13.44% 13.11%

Note: Data mark with * are stand-alone basis

Fubon Life - Financial summary

NT$ millions, except for percentages 1Q16 4Q15 3Q15 2Q15 1Q15 2015 2014 YoY

Income statement data

First year premium 59,722 62,108 62,152 43,604 37,418 205,282 190,974 7.5%

Retained earned premium 120,845 122,879 125,791 99,205 92,422 440,297 390,077 12.9%

Total investment income 25,537 26,382 32,907 36,376 34,591 130,256 109,876 18.5%

Recurring investment income 23,110 25,326 33,093 22,885 19,736 101,040 88,695 13.9%

Other investment income 2,427 1,056 (186) 13,491 14,855 29,216 21,181 37.9%

Realized gains (losses) from fixed income 3,603 1,520 (2,633) 4,112 6,872 9,870 12,127 -18.6%

Realized gains (losses) from equity 3,138 (612) (368) 12,271 11,331 22,622 14,021 61.3%

FX and others (4,855) (420) 3,301 (2,969) (3,541) (3,629) (6,413) -43.4%

Investment property fair value movement 541 569 (486) 77 193 353 1,446 -75.6%

Other income 626 647 686 458 367 2,159 2,006 7.6%

Total operating revenue 147,008 149,908 159,383 136,038 127,381 572,711 501,960 14.1%

Retained claim payment 45,527 47,735 44,330 45,926 49,610 187,601 168,249 11.5%

Net commission expense 9,113 7,101 7,314 6,300 5,378 26,093 23,215 12.4%

Net change in insurance liability 85,625 86,518 91,860 62,329 51,957 292,665 254,691 14.9%

General and administrative expense 4,122 4,672 3,761 3,601 3,491 15,526 13,652 13.7%

Other operating costs 462 441 447 664 379 1,932 1,078 79.2%

Total operating costs and expenses 144,850 146,466 147,713 118,821 110,816 523,816 460,885 13.7%

Net non-operating income / (expenses) 106 141 141 91 144 518 222 133.7%

Income before tax 2,265 3,583 11,812 17,309 16,710 49,413 41,296 19.7%

Net income 2,137 2,169 9,770 15,827 13,252 41,018 35,367 16.0%

Net income to parent company 2,137 2,169 9,770 15,827 13,252 41,018 35,367 16.0%

Balance sheet data

Total assets 3,117,105 3,035,563 2,951,402 2,843,190 2,845,002 3,035,563 2,790,427 8.8%

Total assets (general account) 2,982,282 2,900,201 2,821,057 2,709,001 2,708,199 2,900,201 2,653,199 9.3%

Insurance liabilities 2,728,570 2,656,145 2,569,316 2,447,646 2,390,639 2,656,145 2,346,722 13.2%

Total liabilities 2,910,646 2,852,781 2,778,892 2,634,408 2,597,645 2,852,781 2,566,830 11.1%

Total liabilities (general account) 2,775,823 2,717,419 2,648,546 2,500,220 2,460,842 2,717,419 2,429,603 11.8%

Equity attributable to parent company 206,459 182,782 172,511 208,781 247,357 182,782 223,597 -18.3%

Key matrices

ROA 0.28% 0.30% 1.36% 2.25% 1.88% 1.41% 1.35%

ROE 4.39% 4.27% 19.73% 29.28% 22.51% 20.19% 17.96%

Equity / Assets 6.62% 6.02% 5.85% 7.34% 8.69% 6.02% 8.01%

Claims and benefits ratio 37.67% 38.85% 35.24% 46.29% 53.68% 42.61% 43.13%

Expense ratio 3.41% 3.80% 2.99% 3.63% 3.78% 3.53% 3.50%

Persistency ratio - 13th month 96.19% 96.66% 94.57% 95.22% 95.24% 96.66% 95.12%

Persistency ratio - 25th month 92.92% 92.07% 90.71% 90.43% 90.13% 92.07% 89.67%

Fubon Insurance - Financial summary

NT$ millions, except for percentages 1Q16 4Q15 3Q15 2Q15 1Q15 2015 2014 YoY

Income statement data

Direct written premiums 9,297 8,874 8,452 9,540 8,150 35,016 32,718 7.0%

Retention of earned premiums 7,230 6,833 7,024 6,833 6,450 27,139 24,653 10.1%

Net income from investment 497 485 739 852 735 2,811 2,498 12.5%

Other operating revenue 345 363 331 304 297 1,295 1,082 19.7%

Retained insurance payments 3,833 3,887 3,796 3,348 3,218 14,250 13,128 8.5%

Net change in liability reserve 358 (329) 377 256 352 656 626 4.7%

Commission and operating expenses 3,306 3,506 3,178 3,203 2,885 12,772 11,363 12.4%

Non-Operating Income (22) (9) (36) (29) (22) (96) (109) -12.2%

Income before tax 553 607 707 1,153 1,005 3,472 3,007 15.5%

Net income 444 485 566 962 826 2,839 2,420 17.3%

Net income to parent company 516 595 674 1,050 895 3,213 2,816 14.1%

Balance sheet data

Total assets 94,323 89,213 90,125 87,732 86,170 89,213 83,349 7.0%

Investment assets 65,752 64,689 64,278 61,978 63,377 64,689 60,362 7.2%

Policy reserve 51,580 47,470 48,059 47,350 45,445 47,470 44,930 5.7%

Equity attributable to parent company 30,281 28,677 28,099 28,829 30,057 28,677 27,665 3.7%

Summary ratios

ROA 1.94% 2.25% 2.61% 4.50% 3.90% 3.29% 2.99%

ROE 7.00% 8.44% 9.67% 14.87% 12.40% 11.41% 10.06%

Total investment return 3.05% 3.10% 4.74% 5.57% 4.83% 4.50% 4.21%

Solvency margin (NWP/equity) 99.48% 99.62% 97.27% 104.81% 87.28% 97.95% 94.11%

Retention ratio 75.19% 75.46% 75.13% 74.35% 76.42% 75.30% 76.11%

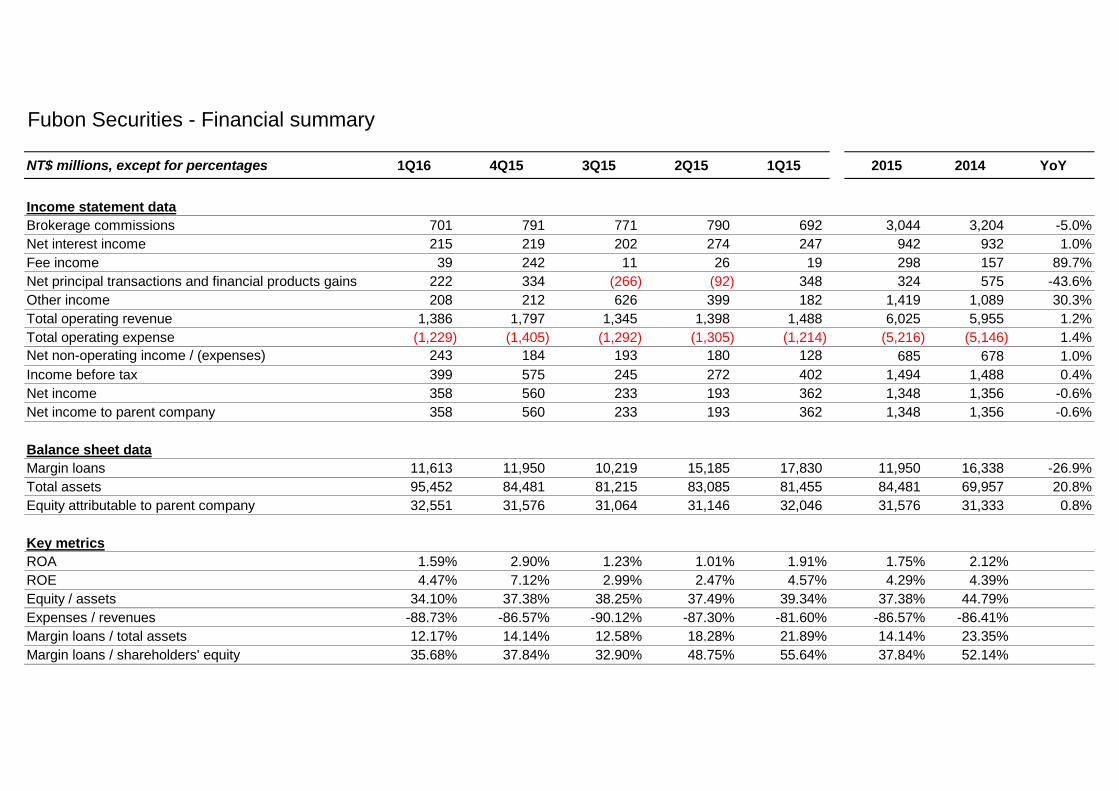

Fubon Securities - Financial summary

NT$ millions, except for percentages 1Q16 4Q15 3Q15 2Q15 1Q15 2015 2014 YoY

Income statement data

Brokerage commissions 701 791 771 790 692 3,044 3,204 -5.0%

Net interest income 215 219 202 274 247 942 932 1.0%

Fee income 39 242 11 26 19 298 157 89.7%

Net principal transactions and financial products gains 222 334 (266) (92) 348 324 575 -43.6%

Other income 208 212 626 399 182 1,419 1,089 30.3%

Total operating revenue 1,386 1,797 1,345 1,398 1,488 6,025 5,955 1.2%

Total operating expense (1,229) (1,405) (1,292) (1,305) (1,214) (5,216) (5,146) 1.4%

Net non-operating income / (expenses) 243 184 193 180 128 685 678 1.0%

Income before tax 399 575 245 272 402 1,494 1,488 0.4%

Net income 358 560 233 193 362 1,348 1,356 -0.6%

Net income to parent company 358 560 233 193 362 1,348 1,356 -0.6%

Balance sheet data

Margin loans 11,613 11,950 10,219 15,185 17,830 11,950 16,338 -26.9%

Total assets 95,452 84,481 81,215 83,085 81,455 84,481 69,957 20.8%

Equity attributable to parent company 32,551 31,576 31,064 31,146 32,046 31,576 31,333 0.8%

Key metrics

ROA 1.59% 2.90% 1.23% 1.01% 1.91% 1.75% 2.12%

ROE 4.47% 7.12% 2.99% 2.47% 4.57% 4.29% 4.39%

Equity / assets 34.10% 37.38% 38.25% 37.49% 39.34% 37.38% 44.79%

Expenses / revenues -88.73% -86.57% -90.12% -87.30% -81.60% -86.57% -86.41%

Margin loans / total assets 12.17% 14.14% 12.58% 18.28% 21.89% 14.14% 23.35%

Margin loans / shareholders' equity 35.68% 37.84% 32.90% 48.75% 55.64% 37.84% 52.14%

Fubon Bank (China) - Financial Summary

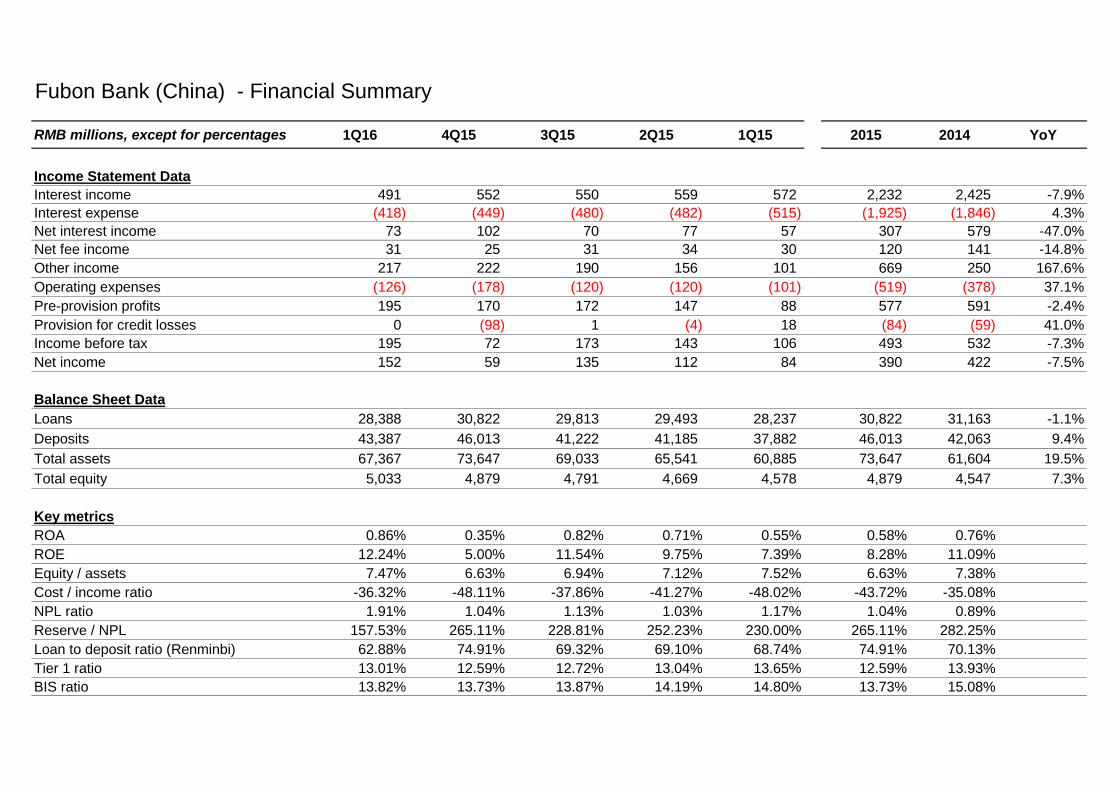

RMB millions, except for percentages 1Q16 4Q15 3Q15 2Q15 1Q15 2015 2014 YoY

Income Statement Data

Interest income 491 552 550 559 572 2,232 2,425 -7.9%

Interest expense (418) (449) (480) (482) (515) (1,925) (1,846) 4.3%

Net interest income 73 102 70 77 57 307 579 -47.0%

Net fee income 31 25 31 34 30 120 141 -14.8%

Other income 217 222 190 156 101 669 250 167.6%

Operating expenses (126) (178) (120) (120) (101) (519) (378) 37.1%

Pre-provision profits 195 170 172 147 88 577 591 -2.4%

Provision for credit losses 0 (98) 1 (4) 18 (84) (59) 41.0%

Income before tax 195 72 173 143 106 493 532 -7.3%

Net income 152 59 135 112 84 390 422 -7.5%

Balance Sheet Data

Loans 28,388 30,822 29,813 29,493 28,237 30,822 31,163 -1.1%

Deposits 43,387 46,013 41,222 41,185 37,882 46,013 42,063 9.4%

Total assets 67,367 73,647 69,033 65,541 60,885 73,647 61,604 19.5%

Total equity 5,033 4,879 4,791 4,669 4,578 4,879 4,547 7.3%

Key metrics

ROA 0.86% 0.35% 0.82% 0.71% 0.55% 0.58% 0.76%

ROE 12.24% 5.00% 11.54% 9.75% 7.39% 8.28% 11.09%

Equity / assets 7.47% 6.63% 6.94% 7.12% 7.52% 6.63% 7.38%

Cost / income ratio -36.32% -48.11% -37.86% -41.27% -48.02% -43.72% -35.08%

NPL ratio 1.91% 1.04% 1.13% 1.03% 1.17% 1.04% 0.89%

Reserve / NPL 157.53% 265.11% 228.81% 252.23% 230.00% 265.11% 282.25%

Loan to deposit ratio (Renminbi) 62.88% 74.91% 69.32% 69.10% 68.74% 74.91% 70.13%

Tier 1 ratio 13.01% 12.59% 12.72% 13.04% 13.65% 12.59% 13.93%

BIS ratio 13.82% 13.73% 13.87% 14.19% 14.80% 13.73% 15.08%