friday, 01 june 2018 - … june morning... · 2 yr us 10 yr us 2yr de 10 yr de eur ... there was no...

TRANSCRIPT

Friday, 01 June 2018

P. 1

Rates: Focus on US eco data as Italian political deadlock ends?

The Italian political deadlock ended yesterday evening with a new government sworn in today. We don’t expect a strong relief rally as last week revealed vulnerabilities of (peripheral) government bond markets. Attention could shift to US eco data today with the June 13 FOMC meeting already in mind. The escalating trade conflict is a wildcard.

Currencies: Easiest part of euro rebound behind US?

Yesterday, EUR/USD rebounded temporary to 1.17, but the move stalled. We don’t expect much further support for the euro from the installation of a new government. US Payrolls might be mixed for the dollar. A further flaring up of the trade tensions might weigh slightly more on the euro than on the dollar.

Calendar

• US markets lost ground yesterday with the Dow Jones underperforming (-1%).

Asian stock markets are mixed overnight with China underperforming. The Caixin manufacturing PMI stabilized at 51.1 in May.

• Italy’s 5SM and the far-right Lega clinched the approval of president Mattarella for the launch of a populist government, all but ending a political crisis that has gripped the country for nearly 3 months and spooked investors. (FT)

• David Davis is devising a new Brexit plan to break a talks deadlock by giving Northern Ireland joint EU and UK status as well as a border buffer zone so it can trade freely with both. (The Sun)

• Spain's Socialists have enough votes to oust PM Rajoy in a no-confidence vote set for today and replace him with party leader Pedro Sanchez. Reports were denied that Rajoy will resign to avoid defeat, thereby triggering elections. (BB)

• Fed Brainard suggested a policy path that moves gradually from modestly accommodative to neutral and, afterwards, modestly beyond neutral, consistent with sustaining strong labor market conditions and inflation around target.

• Canada and Mexico retaliated against the US decision to impose tariffs on steel and aluminum imports and the EU had its own reprisals ready to go, reigniting investor fears of a global trade war. (Reuters)

• Today’s eco calendar contains US payrolls, unemployment rate, average hourly earnings and the manufacturing ISM (US) / PMI (UK). Fed Kaplan and Kashkari speak.

Headlines

S&PEurostoxx 50NikkeiOilCRB

Gold2 yr US10 yr US

2yr DE10 yr DEEUR/USDUSD/JPYEUR/GBP

Friday, 01 June 2018

P. 2

Focus on US payrolls as Italian deadlock ends

Investors tuned their trading behavior to the BTP market this week. Italian yields initially declined further yesterday with Bunds losing ground. Trading dynamics made a U-turn in the second half of the session without noticeable driver. EMU and US eco data were strong, but didn’t leave a trace on markets. Neither did the new developments in the trade conflict. The German yield curve bull flattened with yields 0.2 bps (2-yr) to 5.3 bps (30-yr) lower. Changes on the US yield curve varied between +1.6 bps (2-yr) and -0.2 bps (30-yr). 10-yr yield spread changes vs Germany ranged between -4 bps (Portugal) and +2 bps (Greece) with Italy (-9 bps) outperforming.

The anti-establishment 5SM and far right Lega reached a deal to form a new Italian government after the European close. Party leaders Di Maio and Salvini will be vice-premiers flanking PM Conte. Paolo Savona (previously proposed as FM, but vetoed by President Mattarella) returns as minister of European affairs. With the treat of snap elections gone, calm can return to markets. However, we don’t expect a strong relief rally. This week’s episode was a wake-up call for investors. The long overdue normalization of credit premiums in stretched government bond markets is likely to stay. We’ll now have to see whether the 5SM-Lega government picks up the gloves against E(M)U treaties with Savona as “Italian Varoufakis” or whether they want to “prove” themselves and stick to subjects like implementing fiscal stimulus.

Asian stock markets are mixed overnight with China underperforming because of technical reasons. The US Note future has a downward bias and we expect a slightly weaker opening for the Bund.

The eco calendar heats up in the US with payrolls and the manufacturing ISM. Risks for the ISM are on the upside of expectations. The bar for the payrolls (190k) could be too high. We think that we’re moving to a new normal (150k region) given tightness of the US labour market. The unemployment rate is expected to stabilize at 3.9% while consensus forecasts a muted 0.2% M/M & 2.6% Y/Y for average hourly earnings. Overall, US eco data should confirm the US economy’s momentum. The front end of the US curve will in that case underperform with the June 13 FOMC meeting coming in mind. The escalating trade conflict is a wildcard for trading which could support core bonds via deteriorating risk sentiment. Equity indices/futures currently suggest no panic though. Spanish PM Rajoy probably won’t survive tonight confidence vote, resulting in a caretaker government. With the 2018 budget already cleared, we don’t expect any short term adverse market impact.

Rates

0,00 US yield -1d2 2,43 0,025 2,70 0,0210 2,86 0,0030 3,02 0,00

DE yield -1d2 -0,66 0,005 -0,27 -0,0110 0,34 -0,0330 1,03 -0,05

German 10-yr yield (YTD): near term trading range between 0.2% and 0.5%

US 10-yr yield able to retake 2.9% if today’s US eco data confirm ongoing strength in the US economy

Af

Friday, 01 June 2018

P. 3

EUR/USD rebound slows ahead of first resistance

EUR/GBP:sterling fails to regain any ground against a soft euro.

Easiest part of EUR/USD rebound behind us

EUR/USD rebounded north of 1.17 yesterday as Italian-related tensions eased further, but the risk on trade petered out. A sharp rise in EMU inflation opened the door for the ECB to reduce its APP programme later this year. For now it didn’t help the euro. US data were good, but near expectations. Later, the US imposed tariffs on steel and aluminium from Canada, Mexico and the EU. There was no unequivocal reaction in global FX. EUR/USD settled in the upper half of 1.16. USD/JPY fell temporary, but closed the session little changed (108.82). The Canadian dollar reversed most of Wednesday’s post-BoC gains.

Asian markets are trading mixed this morning. The reaction to the rising trade tensions remain modest. The BOJ reduced buying of 5 and 10-y bonds in its regular operation (probably as it wants a slightly steeper yield curve). Interesting, the BOJ shift this time didn’t trigger any speculation on a more profound change in BOJ policy further down the road. The yen even declined slightly. USD/JPY rebounded north of 109. EUR/USD is losing a few ticks, indicating some cautious USD bid.

European investors will look for clues on what the policy of the new US government will mean for the budget and what position will take vis-à-vis the EU. After the recent relief rally, we expect investors to take some wait-and –see approach. It might be too soon for further euro gains on Italy. In the US, job growth is expected to rebound from 164K to 190K. A positive surprise might not be that evident. However, AHE (wages) might be at least as important as payrolls growth. For this indicator, consensus expectation (0.2% M/M) is not too high. Even so, it might not be that evident for the payrolls to raise market expectations on a more aggressive Fed at the June meeting. The impact of the trade tensions for global FX trading is diffuse. We hold the working hypothesis that it might be slightly negative for EUR/USD, but maybe also for USD/JPY. From a technical point of view, EUR/USD rebounded off the 1.1510/50 area, but didn’t regain any key technical level. We are not convinced on a protracted euro rebound yet. 1.1830 is first resistance ahead of the 1.1996/1.20 area which we consider not easy to break.

EUR/GBP drifted north yesterday, supported by the EUR/USD rebound. The manufacturing PMI is expected to ease slightly to 53.5 today. A big positive surprise is probably needed to support sterling. We expect sterling to remain relatively weak,

Currencies

R2 1,2155 -1dR1 1,1996EUR/USD 1,1693 0,0028S1 1,1554S2 1,1453

R2 0,9033 -1dR1 0,8968EUR/GBP 0,8794 0,0016S1 0,8628S2 0,8548

Friday, 01 June 2018

P. 4

Friday, 1 June Consensus Previous US 14:30 Change in Nonfarm Payrolls (May) 190k 164k 14:30 Change in Private Payrolls (May) 190k 168k 14:30 Change in Manufact. Payrolls (May) 20k 24k 14:30 Unemployment Rate (May) 3.9% 3.9% 14:30 Underemployment Rate (May) -- 7.8% 14:30 Average Hourly Earnings MoM/YoY (May) 0.3%/2.7% 0.1%/2.6% 14:30 Average Weekly Hours All Employees (May) 34.5 34.5 14:30 Labor Force Participation Rate (May) -- 62.8% 15:45 Markit US Manufacturing PMI (May F) 56.6 56.6 16:00 Construction Spending MoM (Apr) 0.8% -1.7% 16:00 ISM Manufacturing (May) 58.2 57.3 16:00 ISM Employment (May) -- 54.2 16:00 ISM Prices Paid (May) 78.0 79.3 16:00 ISM New Orders (May) -- 61.2 Japan 01:50 Capital Spending YoY (1Q) 3.4% A 4.3% 02:30 Nikkei Japan PMI Mfg (May F) 52.8 A 52.5 UK 10:30 Markit UK PMI Manufacturing SA (May) 53.5 53.9 EMU 10:00 Markit Eurozone Manufacturing PMI (May F) 55.5 55.5 Germany 09:55 Markit/BME Germany Manufacturing PMI (May F) 56.8 56.8 France 09:50 Markit France Manufacturing PMI (May F) 55.1 55.1 Italy 09:45 Markit/ADACI Italy Manufacturing PMI (May) 53.0 53.5 10:00 GDP WDA QoQ/WDA YoY (1Q F) 0.3%/1.4% 0.3%/1.4% China 03:45 Caixin China PMI Mfg (May) 51.1 A 51.1 Norway 10:00 Unemployment Rate (May) 2.2% 2.4% Spain 09:15 Markit Spain Manufacturing PMI (May) 54.0 54.4 Events 14:55 Fed’s Kashkari Speaks in Minneapolis 12:00 Riksbank's Ingves Gives Speech

Calendar

Friday, 01 June 2018

P. 5

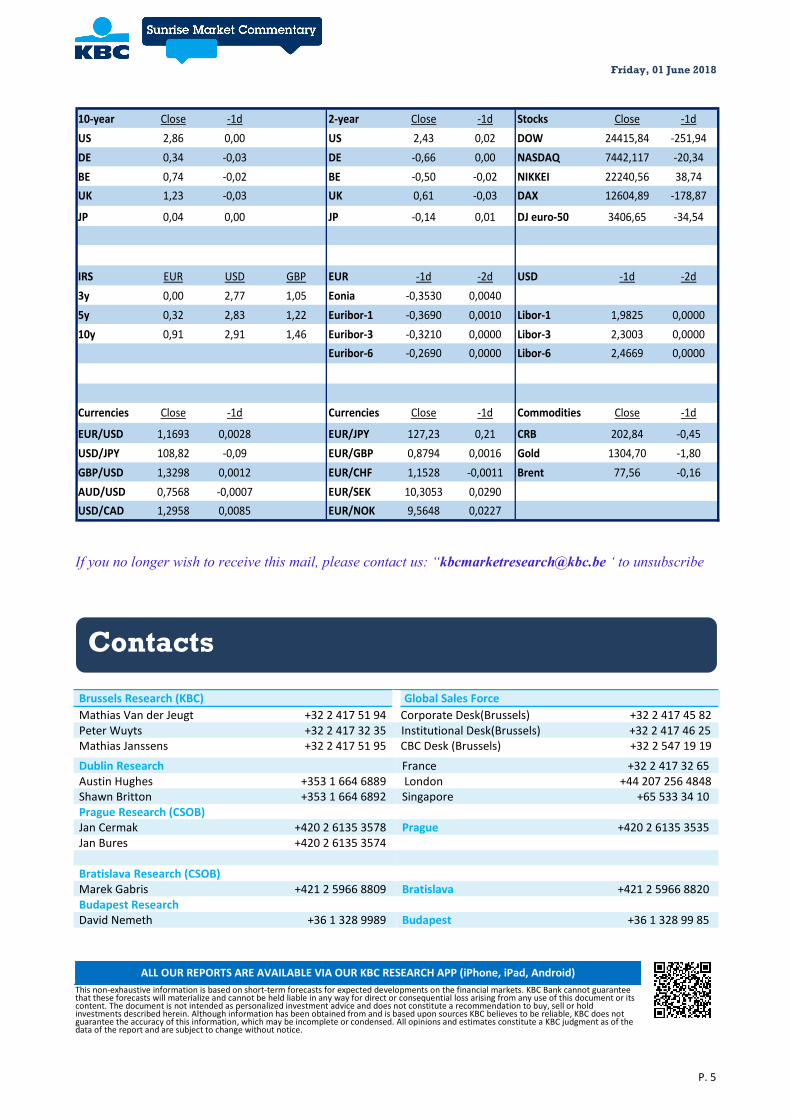

10-year Close -1d 2-year Close -1d Stocks Close -1dUS 2,86 0,00 US 2,43 0,02 DOW 24415,84 -251,94DE 0,34 -0,03 DE -0,66 0,00 NASDAQ 7442,117 -20,34BE 0,74 -0,02 BE -0,50 -0,02 NIKKEI 22240,56 38,74UK 1,23 -0,03 UK 0,61 -0,03 DAX 12604,89 -178,87

JP 0,04 0,00 JP -0,14 0,01 DJ euro-50 3406,65 -34,54

IRS EUR USD GBP EUR -1d -2d USD -1d -2d3y 0,00 2,77 1,05 Eonia -0,3530 0,00405y 0,32 2,83 1,22 Euribor-1 -0,3690 0,0010 Libor-1 1,9825 0,000010y 0,91 2,91 1,46 Euribor-3 -0,3210 0,0000 Libor-3 2,3003 0,0000

Euribor-6 -0,2690 0,0000 Libor-6 2,4669 0,0000

Currencies Close -1d Currencies Close -1d Commodities Close -1d

EUR/USD 1,1693 0,0028 EUR/JPY 127,23 0,21 CRB 202,84 -0,45USD/JPY 108,82 -0,09 EUR/GBP 0,8794 0,0016 Gold 1304,70 -1,80GBP/USD 1,3298 0,0012 EUR/CHF 1,1528 -0,0011 Brent 77,56 -0,16AUD/USD 0,7568 -0,0007 EUR/SEK 10,3053 0,0290USD/CAD 1,2958 0,0085 EUR/NOK 9,5648 0,0227

If you no longer wish to receive this mail, please contact us: “[email protected] ‘ to unsubscribe

Brussels Research (KBC) Global Sales Force Mathias Van der Jeugt +32 2 417 51 94 Corporate Desk(Brussels) +32 2 417 45 82 Peter Wuyts +32 2 417 32 35 Institutional Desk(Brussels) +32 2 417 46 25 Mathias Janssens +32 2 417 51 95 CBC Desk (Brussels) +32 2 547 19 19

Dublin Research France +32 2 417 32 65 Austin Hughes +353 1 664 6889 London +44 207 256 4848 Shawn Britton +353 1 664 6892 Singapore +65 533 34 10 Prague Research (CSOB) Jan Cermak +420 2 6135 3578 Prague +420 2 6135 3535 Jan Bures +420 2 6135 3574 Bratislava Research (CSOB) Marek Gabris +421 2 5966 8809 Bratislava +421 2 5966 8820 Budapest Research David Nemeth +36 1 328 9989 Budapest +36 1 328 99 85

ALL OUR REPORTS ARE AVAILABLE VIA OUR KBC RESEARCH APP (iPhone, iPad, Android) This non exhaustive information is based on short term forecasts for expected developments

This non-exhaustive information is based on short-term forecasts for expected developments on the financial markets. KBC Bank cannot guarantee that these forecasts will materialize and cannot be held liable in any way for direct or consequential loss arising from any use of this document or its content. The document is not intended as personalized investment advice and does not constitute a recommendation to buy, sell or hold investments described herein. Although information has been obtained from and is based upon sources KBC believes to be reliable, KBC does not guarantee the accuracy of this information, which may be incomplete or condensed. All opinions and estimates constitute a KBC judgment as of the data of the report and are subject to change without notice.

Contacts