frequently asked questions pertaining to tariff - nersa

TRANSCRIPT

Frequently Asked Questions (FAQ):

Tariff Methodology for the Setting and Approval of Tariffs in the

Petroleum Pipelines Industry

Version 4

Approved on

29 July 2013

FAQ Version 4: Approved on 29 July 2013.

Page 1 of 59

Frequently Asked Questions (FAQ):

Tariff Methodology for the Setting and Approval of Tariffs in the Petroleum Pipelines Industry

29 July 2013

Answers and guidance to Frequently Asked Questions are provided in this

document.

Glossary of Terms and Abbreviations ................................................................... 2

Regualtory Asset Base (RAB) ................................................................................. 3

WACC – General ...................................................................................................... 9

WACC – Beta .......................................................................................................... 14

WACC – The Market Return (MR) ......................................................................... 18

WACC – The Riskfree Rate (Rf) ............................................................................ 19

WACC – Cost of Equity (Ke).................................................................................. 21

WACC – Cost of Debt (Kd) .................................................................................... 25

DEPRECIATION ...................................................................................................... 29

EXPENSES – Land rehabilitation .......................................................................... 30

F-FACTOR .............................................................................................................. 35

CLAWBACK ............................................................................................................ 35

TAX .......................................................................................................................... 39

Tariff model on NERSA’s website ........................................................................ 45

Notes on multi-year tariff applications ................................................................. 46

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 2 of 59

GLOSSARY OF TERMS AND ABBREVIATIONS

ALSI - All share total return index on the Johannesburg stock exchange

C - Claw-back adjustments

CPI - Consumer price index

D - Depreciation. The charge (normal depreciation and amortisation on

the write-up) for the tariff period under review

E - Expenditure. Maintenance and operating expenses for the tariff

period under review.

F - Approved revenue addition to meet debt obligations

IRR - Internal rate of return

JSE - Johannesburg stock exchange

Kd - Cost of debt

Ke - Cost of equity

MR - Market return

RAB - Regulatory asset base

Rf - Riskfree rate of interest

ROE - Return on Equity

STC - Secondary tax on companies

T - Tax expense. Flow-through and notional tax options

TOC - Trended original cost

TRI - Total return index

PPE - Value of property, plant and equipment net of accumulated

depreciation

w - Net working capital

WACC - Weighted average cost of capital

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 3 of 59

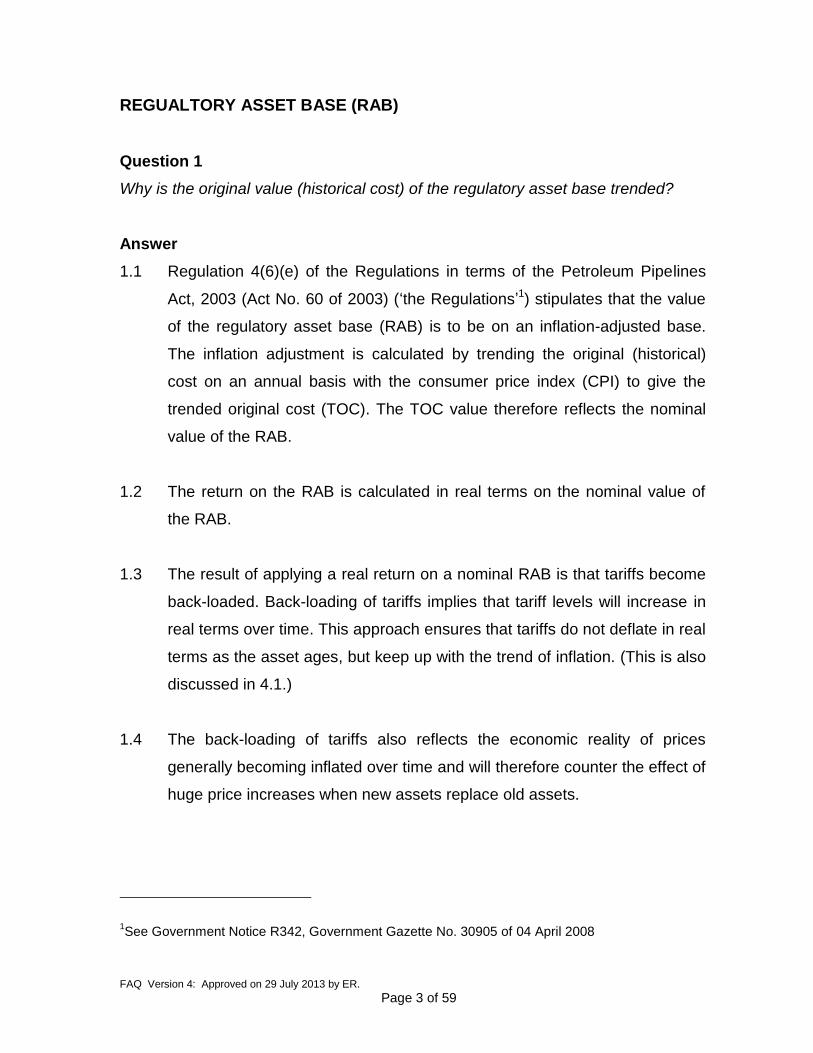

REGUALTORY ASSET BASE (RAB)

Question 1

Why is the original value (historical cost) of the regulatory asset base trended?

Answer

1.1 Regulation 4(6)(e) of the Regulations in terms of the Petroleum Pipelines

Act, 2003 (Act No. 60 of 2003) (‘the Regulations’1) stipulates that the value

of the regulatory asset base (RAB) is to be on an inflation-adjusted base.

The inflation adjustment is calculated by trending the original (historical)

cost on an annual basis with the consumer price index (CPI) to give the

trended original cost (TOC). The TOC value therefore reflects the nominal

value of the RAB.

1.2 The return on the RAB is calculated in real terms on the nominal value of

the RAB.

1.3 The result of applying a real return on a nominal RAB is that tariffs become

back-loaded. Back-loading of tariffs implies that tariff levels will increase in

real terms over time. This approach ensures that tariffs do not deflate in real

terms as the asset ages, but keep up with the trend of inflation. (This is also

discussed in 4.1.)

1.4 The back-loading of tariffs also reflects the economic reality of prices

generally becoming inflated over time and will therefore counter the effect of

huge price increases when new assets replace old assets.

1See Government Notice R342, Government Gazette No. 30905 of 04 April 2008

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 4 of 59

1.5 The way to calculate the TOC value of the RAB (inclusive of depreciation

and amortisation of the write-up) is demonstrated in Table 1 below. This

table is also published on the NERSA website.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 5 of 59

Table 1: Calculation of TOC value of RAB (inclusive of depreciation and amortisation of the write-up)

Trending of Asset Value (TOC) Formula for

year 2 (column "C")

A B C D E F G H I J K

1 Tariff Period 0 1 2 3 4 5 6 7 8 9 10

Remaining Asset Useful Life 10 9 8 7 6 5 4 3 2 1

3 Depreciated Original Cost b/f +B3-B4

100.00 90.00 80.00 70.00 60.00 50.00 40.00 30.00 20.00 10.00 4 Depreciation (historic) +$B$3/$B$2

10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00

5 Depreciated original cost (PPE--d) RAB Bal c/f +C3-C4

90.00 80.00 70.00 60.00 50.00 40.00 30.00 20.00 10.00 0.00

7 Inflation write-up balance

8 Inflation write-up bal b/f +B12

0.00 4.50 8.20 11.03 12.93 13.81 13.60 12.21 9.55 5.51

9 Current period inflation write-up +B13*$A$9 5.00% 5.00 4.73 4.41 4.05 3.65 3.19 2.68 2.11 1.48 0.78

10 Write up balance on which WACC should be earned =SUM(C8:C9)

5.00 9.23 12.61 15.09 16.58 17.00 16.28 14.32 11.03 6.29

11 Amortization of write-up +C10/C2

0.50 1.03 1.58 2.16 2.76 3.40 4.07 4.77 5.5

1 6.29

12

Write-up bal net of amortization carried forward =C10-C11

4.50 8.20 11.03 12.93 13.81 13.60 12.21 9.55 5.51 0.00

13 TOC Closing Balance (c/f) =C5+C12 100.00 94.50 88.20 81.03 72.93 63.81 53.60 42.21 29.55 15.5

1 0.00

TOC Opening Balance (b/f) balance to inflate +B13

100.00 94.50 88.20 81.03 72.93 63.81 53.60 42.21 29.55 15.51

Amount to be used Tariff application

15 Total amount on which WACC should be earned =+C3+C10

105.00 99.23 92.61 85.09 76.58 67.00 56.28 44.32 31.03 16.29

16 Historic Depreciation +C4

10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00 10.00

17 Amortization of write up +C11

0.50 1.03 1.58 2.16 2.76 3.40 4.07 4.77 5.51 6.29

18 Total [d] as per Allowable revenue Sum(C16:C17)

10.50 11.03 11.58 12.16 12.76 13.40 14.07 14.77 15.51 16.29

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 6 of 59

Note:

Further clarity on the meaning of non-current assets allowable in the RAB can be

obtained from the Regulatory Reporting Manual, Volume 4, which gives the following

classifications:

ASSETS AND OTHER DEBITS

Current Assets

100 Cash and Cash Equivalents

110 Accounts Receivable

110.003 Accounts Receivable – Trade

110.004 Accounts Receivable – Other

115 Accumulated Provision for Doubtful Debts

120 Inventory

120.001 Materials and Operating Supplies

120.003 Petroleum Inventory

125 Prepayments

135 Other Current Assets

Deferred Debits

142 Preliminary Surveys and Investigation Charges

147 Other Deferred Debits

Non-Current Assets

171.001 Plant in Service

171.002 Accumulated Depreciation – Plant in Service

172.001 Plant under capital leases and Improvements to leased facilities

172.002 Accumulated Depreciation – Leased Plant and Improvements

176 Line Fill

195.002 Other Intangible Assets

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 7 of 59

LIABILITIES AND OTHER CREDITS

Current Liabilities

200 Bank Overdraft

205 Accounts Payable

206 Account Payable to Affiliated Companies

212 Obligations under Capital Leases – Current Portion

216 Interest Payable and Accrued

220 Dividends Payable

230 Accrued Income Taxes Payable

235 Other Current Liabilities

Deferred Credits

238 Unamortized Debt Premium and Expenses

241 Other deferred credits

Non-Current Liabilities

245 Provision for Pension and Benefits

255 Long-Term Debt

256 Long-Term Debt-Advances from Affiliated Companies

265 Other Non-Current Liabilities

265.001 Obligations under capital lease – non-current

265.002 Accumulated provision for self insurance

Owners’ Equity

275 Equity Issued

275.001 Ordinary shares issued

275.002 Preference shares issued

280 Contributed Surplus

285 Reserves including excess of appraisal value over depreciated plant

cost

290 Retained Earnings

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 8 of 59

Question 2

Why is the Trended Original Cost not applied to the working capital component of the

RAB-formula?

Answer

2.1 Working capital resets itself each year and therefore there is an automatic

annual adjustment for inflation in the components of working capital.

2.2 If a multi-year tariff application is submitted, the working capital (W) should

be inflated with the CPI as at 12 months prior to the specific tariff period.

Question 3

What benchmarks are used for determining the allowable amounts for the respective

elements in the formula for determining the working capital?

Net working capital = inventory + linefill + receivables +

operating cash – trade payables

Answer

3.1 Inventory: Inventory is to be valued at the lower of cost or net realisable

value.

3.2 Llinefill: Linefill is to be valued at cost of product.

3.3 Receivables: Receivables is to be based on a maximum of 30 days of a

licensee’s allowable revenue.

3.4 Operating cash: Operating cash is to be based on a licensee’s standard

practice subject to a maximum of 45 days’ maintenance and operating

expenses, excluding depreciation and deferred taxes. Added to this amount

will be the minimum cash requirements of a licensee’s lender(s).

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 9 of 59

3.5 Trade payables: Trade payables is to be based on a maximum of 45 days

of a licensee’s allowable revenue.

3.6 If licensees have proof that their actual values for the above benchmarks

are higher, the higher values can be used.

Question 4

Why is a deferred tax liability deducted and a deferred tax asset added to the RAB in

the RAB formula?

Answer

4.1 A deferred tax liability represents a temporary return of capital on which no

return is allowed and therefore it is deducted from the RAB. As the licensee

starts repaying the deferred taxation to the Receiver of Revenue, the

deduction from the RAB reduces.

4.2 A deferred tax asset represents additional capital investment. The NERSA

tax formula (paragraph 4.5 of the Tariff Methodology for the setting of tariffs

in the petroleum pipelines industry – hereinafter ‘the Methodology’)

assumes the cash 'to be received' from the fiscus, but the actual cash flow

benefit from the fiscus materialises only in later years and therefore a return

would be allowed on this investment. Deferred tax assets arise mostly as a

result of assessed taxation losses not utilised and carried forward.

4.3 The deferred taxation liabilities and assets are not trended.

WACC – GENERAL

Question 5

Why is a real WACC and not a nominal WACC applied?

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 10 of 59

Answer

5.1 As explained under question 1, Regulation 4(6)(e) stipulates that the value of

the RAB has to reflect an inflation-adjusted value. Because the nominal value

of the RAB is used, a real rate of return is used [as reflected in the real

weighted average cost of capital (WACC)]. This requirement is also stipulated

in section 28(3)(c) of the Petroleum Pipelines Act, 2003 (Act No. 60 of 2003).

5.2 Inflation is added to the asset base (RAB) and is therefore 'taken out' of the

nominal return (WACC). Nominal returns on real assets would constitute a

double count of CPI and thus 'real returns' are used.

Question 6

What is to be understood by the following two statements?

i) Section 28(3)(c) of the Petroleum Pipelines Act 2003 (Act No. 60 of 2003) (the

Act):

(3) The tariffs set or approved by the Authority must enable the licensee to-

(c) make a profit commensurate with the risk;

ii) Section 4(6) of the Regulations made in terms of the Petroleum Pipelines Act

(see Government Notice R432, Government Gazette No. 30905 of 04 April

2008):

(6) The allowed revenue to be derived from tariffs contemplated in sub-

regulation (2) must include:

a) reasonable operating expenses

b) reasonable maintenance expenses

c) depreciation expenses

d) reasonable working capital

e) reasonable real return on the regulatory asset base which should

be determined on the assets’ inflation-adjusted cost less

accumulated depreciation; and

f) other applicable obligations.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 11 of 59

Answer

6.1 The reasonable return relates to the return earned by the licensee on the RAB

and not to the return earned by an equity investor on the RAB. Note that Sub-

regulation (2) refers to an ‘efficient licensee’ and not an equity holder as an

entity different from the licensee.

6.2 In view of the fact that Section 28(3) of the Act does not stipulate that the ‘profit

commensurate with risk’ is to be earned in each year, it is taken that the ‘profit’

(return) is to be earned over the total life of the asset. This profit relates to the

profit of the licensee on the RAB and not to the profit of an equity investor as a

separate construct.

6.3 The actual return that will be earned by the equity investor each year is a

function of the capital structure of the licensee. If the funding structure of the

licensee requires the debt funding to be repaid earlier or faster than the life of

the asset, it is viewed that the equity holder has chosen to become a 'patient

capital' investor. The ‘patient capital’ investor will therefore wait for the debt

capital to be repaid before the full return on equity can be earned.

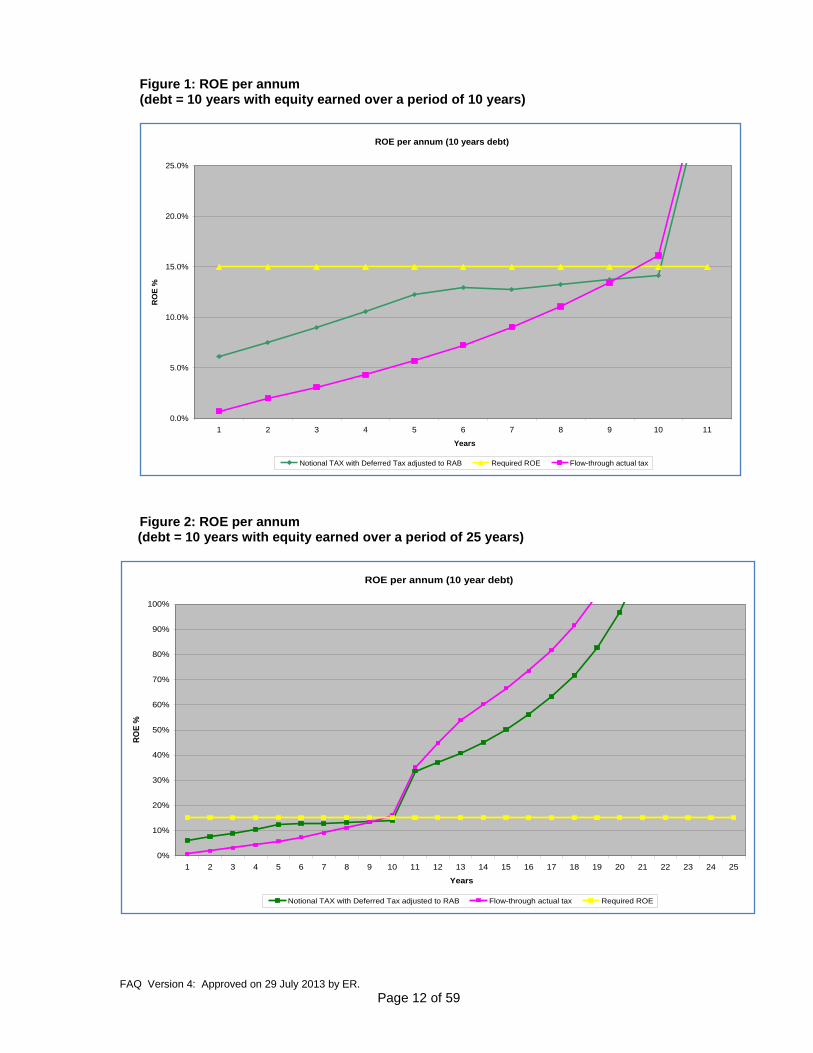

6.4 Figures 1, 2, 3 and 4 demonstrate the effect on the annual returns on equity

(ROE) under the following two scenarios (patient capital investor):

a) debt tenure of 10 years; and

b) debt tenure of 25 years.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 12 of 59

Figure 1: ROE per annum (debt = 10 years with equity earned over a period of 10 years)

Figure 2: ROE per annum (debt = 10 years with equity earned over a period of 25 years)

ROE per annum (10 years debt)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1 2 3 4 5 6 7 8 9 10 11

Years

RO

E %

Notional TAX with Deferred Tax adjusted to RAB Required ROE Flow-through actual tax

ROE per annum (10 year debt)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Years

RO

E %

Notional TAX with Deferred Tax adjusted to RAB Flow-through actual tax Required ROE

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 13 of 59

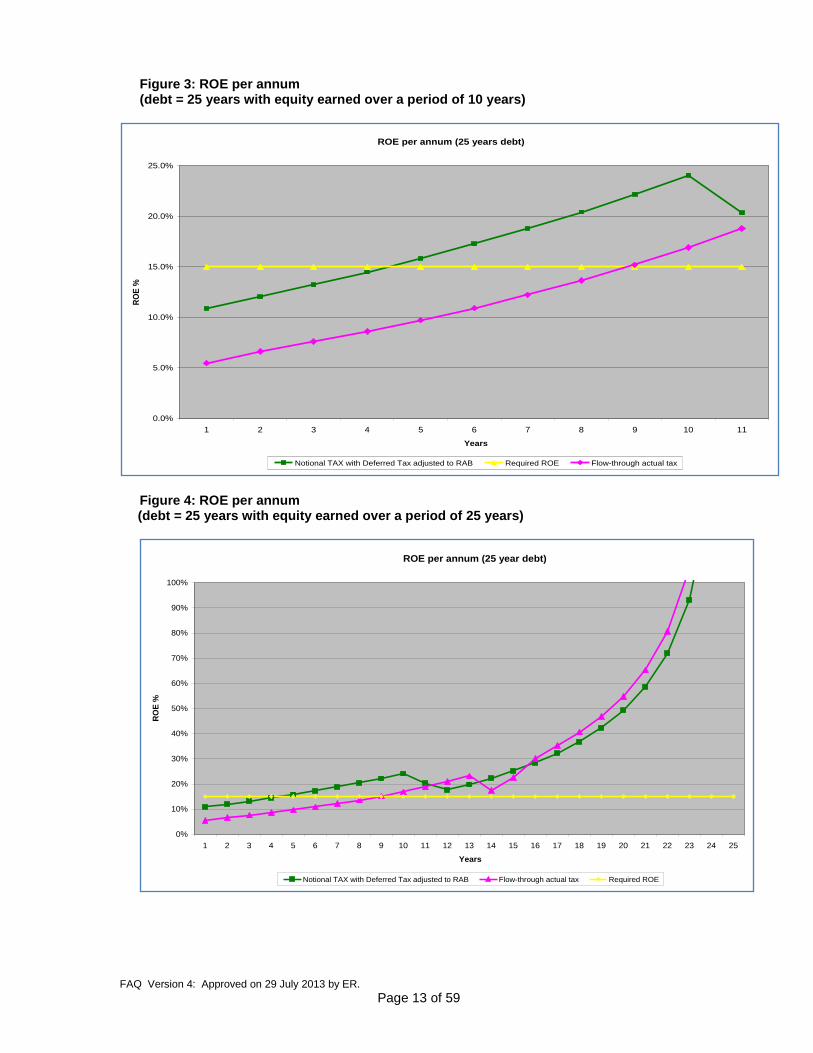

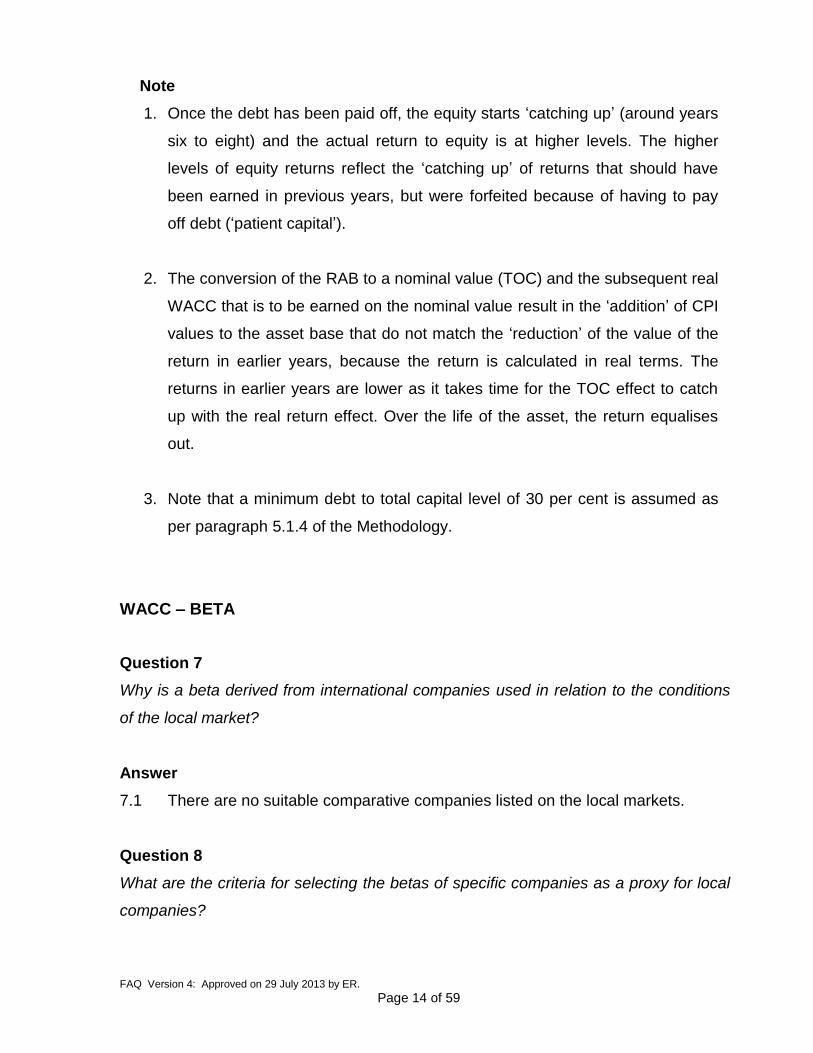

Figure 3: ROE per annum (debt = 25 years with equity earned over a period of 10 years)

Figure 4: ROE per annum (debt = 25 years with equity earned over a period of 25 years)

ROE per annum (25 years debt)

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1 2 3 4 5 6 7 8 9 10 11

Years

RO

E %

Notional TAX with Deferred Tax adjusted to RAB Required ROE Flow-through actual tax

ROE per annum (25 year debt)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Years

RO

E %

Notional TAX with Deferred Tax adjusted to RAB Flow-through actual tax Required ROE

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 14 of 59

Note

1. Once the debt has been paid off, the equity starts ‘catching up’ (around years

six to eight) and the actual return to equity is at higher levels. The higher

levels of equity returns reflect the ‘catching up’ of returns that should have

been earned in previous years, but were forfeited because of having to pay

off debt (‘patient capital’).

2. The conversion of the RAB to a nominal value (TOC) and the subsequent real

WACC that is to be earned on the nominal value result in the ‘addition’ of CPI

values to the asset base that do not match the ‘reduction’ of the value of the

return in earlier years, because the return is calculated in real terms. The

returns in earlier years are lower as it takes time for the TOC effect to catch

up with the real return effect. Over the life of the asset, the return equalises

out.

3. Note that a minimum debt to total capital level of 30 per cent is assumed as

per paragraph 5.1.4 of the Methodology.

WACC – BETA

Question 7

Why is a beta derived from international companies used in relation to the conditions

of the local market?

Answer

7.1 There are no suitable comparative companies listed on the local markets.

Question 8

What are the criteria for selecting the betas of specific companies as a proxy for local

companies?

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 15 of 59

Answer

8.1 The proxy companies must be listed on stock exchanges.

Question 9

Does NERSA publish beta values?

Answer

9.1 Yes, NERSA publishes the value of the unlevered beta applicable to the

petroleum industry. The names of the proxy companies utilised for determining

the beta value as well as quarterly updates on monthly beta values are

published on NERSA’s website.

Question 10

When are adjustments to the industry beta allowed?

Answer

10.1 No adjustments to the beta are allowed. The beta is a measure of systematic

risk. Company or project-specific risks should be accounted for separately from

the beta as explained in the tariff methodology.

Question 11

Which company is used as a supplier of data on beta values of proxy companies?

Answer

11.1 Data is collected monthly on the beta values of proxy companies and is based

on data provided by Bloomberg.

Question 12

At what frequency and over which period is data on the beta value of proxy companies

collected?

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 16 of 59

Answer

12.1 Monthly data for a period of five years is collected. The five-year period is the

period ending the year immediately preceding the date of publication, which is

at the end of March of every year.

Question 13

Is a statistical correction factor applied to the values of the beta?

Answer

13.1 NERSA does not apply any additional correction factor to data utilised for

calculating the beta.

Question 14

How is the beta calculated?

Answer

14.1 The following example demonstrates how the beta (β) is calculated.

For licensees that are not publicly listed and where there are insufficient

publicly listed competitors, the equity beta is derived from a proxy beta. To

make adjustments for differences in gearing between the proxy and the

licensee the process involves ‘un-levering’ and ‘re-levering’ as follows:

i. obtaining the equity beta for the proxy company;

ii. un-levering the beta of the proxy company by the gearing level of the

proxy company – this unlevered beta is known as the asset beta;

iii. calculating the weighted average of the asset betas for the chosen

proxy companies; and

iv. re-levering the average asset beta by the (approved) gearing of the

licensee.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 17 of 59

14.2 Further clarification

i. The Harris and Pringle formula, which excludes the tax shields in the

notation, will be used.

ii. The following steps must be followed when calculating the beta value:

Step 1 – Calculate asset beta (or un-levered beta) for proxy firms

The following formula must be used to determine the asset beta:

β a1 = β1 / [1 + Dt/Eq]

Where:

βa1 = Asset beta for proxy company 1

β1 = Beta of proxy company 1

Dt = Debt of proxy company 1

Eq = Equity of proxy company 1

Repeat Step 1 for each of the six (or more) chosen proxy firms.

Market values for proxy companies will be used where such

market values exists. Where no market values exist for proxy

companies, book values will be used.

Step 2 – Calculate weighted average asset beta of proxy firms

Weight each of the 6 (or more) proxy firm asset betas by their

proportion of the total debt plus equity of the 6 (or more) proxy firms

and sum the results using the following formula:

n

n

1nna

n

1nn

na )(*

EqDt

EqDtE

Where:

βaE = Weighted average asset beta of the proxy companies

nEqDt = Sum of the debt and equity for a specific proxy

company

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 18 of 59

na = Asset beta of the corresponding specific proxy

company

nn

1nEqDt

= Sum of debt and equity for all proxy companies

n = Number of proxy companies

Step 3 – Calculation of beta (β) for licensee (re-levering of beta)

The following formula must be used to determine the beta for the

licensee:

BL = βaE * [1 + Dt/Eq]

Where:

ΒL = Beta for the licensee

βaE = The weighted average β of the proxy firms asset betas

from Step 2. The Energy Regulator may adjust this

factor to take account of a difference in country risk

ratings between the host country of the proxy firms and

South Africa.

Dt = The interest bearing debt of the licensee subject to a

minimum gearing level of 30 per cent

Eq = The equity of the licensee

WACC – THE MARKET RETURN (MR)

Question 15

What market index will be used as a proxy for the performance of the South African

market?

Answer

15.1 The All Share Total Return Index (ALSI) is used as a proxy for the performance

of the South African market as it represents the widest possible spectrum of

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 19 of 59

industries trading in the South African market, as measured by the

Johannesburg Stock Exchange (JSE).

Question 16

Why is a post-tax market return (MR) used for determining the market risk premium

(MRP)?

Answer

16.1 The market returns, as represented by the various JSE indices, reflect earnings

after taxation has been provided for (i.e. data is presented on an after-tax

basis).

16.2 No adjustment for Capital Gains tax is made as it is assumed that the equity

return holders will hold the investment to maturity and therefore the total return

index (TRI) is used.

16.3 There are flaws and challenges inherent in using the ‘post-tax’ MR as a basis

and converting it to a ‘pre-tax’ MR by grossing it up with the tax rate. This

method is thus not used by NERSA.

16.4 As the Allowable Revenue formula treats Taxation as a separate ‘operational’

item (T), the WACC calculations are all performed on a post-tax basis.

WACC – THE RISKFREE RATE (RF)

Question 17

Why are government bonds with a maturity of ten years or longer used?

Answer

17.1 An investor in pipeline infrastructure normally has a long-term investment

horizon of at least ten years. A maturity of less than ten years is considered to

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 20 of 59

be subject to short-term fluctuations in the economic environment which could

impact on the volatility and validity of this measure for the industry.

17.2 Longer term investment instruments are also more in line with the 25-year MR

data used in calculating the WACC.

Question 18

What data sources does NERSA use and how frequently does NERSA publish

economic data for the purpose of tariff setting and approval?

Answer

18.1 The sources of the economic data utilised by NERSA and the frequency of

updating the economic data are provided in Table 2 below.

Table 2: Economic data sources and frequency of updates as provided by

NERSA for tariff setting and approval in the petroleum industry

Data Source Date & frequency of updating the

data on NERSA’s website

CPI-Historical

Statistics SA

Quarterly updates of monthly data

RSA 10-year Bonds

Reserve Bank of SA

Quarterly updates of monthly data

Market Return

ALL Share Total Return Index

(ALSI-TRI) on the JSE

Quarterly updates of monthly data

List of Beta proxy

companies as well as the

value of the beta applicable

for the tariff period

Quarterly updates of monthly data

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 21 of 59

WACC – COST OF EQUITY (KE)

Question 19

Are any adjustments to the cost of equity allowed?

Answer

19.1 The following adjustments to the Cost of Equity (Ke) will be considered on a

case-by-case basis:

CRA = Country risk adjustment.

(The real CRA will be added to the riskfree rate. The CRA is

for assets in another country outside South Africa that are an

integral part of the same asset/s within South Africa. The

adjustment is for the other country concerned)

SSP = Small stock premium. An adjustment to compensate for the

lack of specific qualitative abilities of a licensee if warranted

α = Project specific risk if the circumstances warrant such an

adjustment

LP = Liquidity premium to accommodate assets which are not

publicly traded if the circumstances warrant such an

adjustment.

Note

A small stock premium and project specific risk adjustment

will be considered in the following cases:

a) SSP adjustments:

If the answers to the following two questions are ‘No’,

then a SSP adjustment may be applied:

In running its business:

i. does the licensee have access to legal, financial and

operational/technical expertise within its own

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 22 of 59

structures/or can the licensee obtain this expertise

from its shareholders; and

ii. is there a history of the licensee having had access to

this expertise under its a previous shareholding

dispensation?

b) Project specific risk adjustments (if the circumstances

warrant such an adjustment)

The Energy Regulator needs to be provided with proof of

the following project specific risk factors:

- construction;

- management;

- technology;

- customer base;

- supplier chain; and

- other.

Question 20

How is the cost of equity calculated?

Answer

20.1 A practical example for calculating the Ke is presented below, making use of

assumed values for the respective elements in the formula for calculating Ke.

The formula for determining the Ke is:

Ke = Rf + (β *MRP)

Where:

Ke = Post-tax, real cost of equity

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 23 of 59

Rf = Riskfree rate of interest (real).

(This is the average of the real monthly marked-to-market

riskfree rate for the preceding 300 months for all Government

bonds with at least a 10 year maturity as at 12 months before

the commencement of the tariff period under review)

β = ‘Beta’ is the systematic risk parameter for regulated entities

providing pipeline, storage and loading facility services

(The beta must be determined by proxy. As a proxy the

average of at least six pipeline companies listed on stock

exchanges is used. The value of the proxy is as at 12 months

before the commencement of the tariff period under review).

MRP = Market risk premium (post-tax, real).

[The proxy used for the market is the Johannesburg Stock

Exchange (JSE) All Share Total Return Index (ALSI with JSE

Code J203T) for the preceding 300 months as at 12 months

before the commencement of the tariff period under review.

The arithmetic average for the 300 months is used.]

Note

Two scenarios are considered – the first where the cost of equity is adjusted for

liquidity by multiplying a factor, and the second where the cost of equity is

adjusted for liquidity by adding a factor. Examples to calculate these are

presented next.

Multiplying to adjust for liquidity:

In the practical example for calculating the Ke (and multiplying to adjust for

liquidity), the values for the elements in the Ke formula are assumed to be as

follows:

Rf = 4.5%

CRA = 0.2%

MRP = 7%

β = 0.5

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 24 of 59

SSP = 2.25%

α = 0.10%

LP = 5%

Based on the above assumed values, the value of the Ke is calculated to be:

Ke = [(Rf + CRA) + (MRP * beta) + SSP + α] * (1 + LP)

= [(4.5% + 0.2%) + (7% * 0.5) + 2.25% + 0.10 %] *(1 + 5%)

= (4.7% + 3.5% + 2.25% + 0.10%) *1.05%

= 11.08%

Adding to adjust for liquidity:

In the practical example for calculating the Ke (and adjust for liquidity through

adding), the values for the elements in the Ke formula are assumed to be as

follows:

Rf = 4.5%

CRA = 0.2%

MRP = 7%

β = 0.5

SSP = 2.25%

α = 0.10%

LP = 0.53%

Based on the above assumed values, the value of the Ke is calculated to be:

Ke = (Rf + CRA) + (MRP * beta) + SSP + α + LP

= (4.5% + 0.2%) + (7% * 0.5) + 2.25% + 0.10 % + 0.53%

= 4.7% + 3.5% + 2.25% + 0.10% + 0.53%

= 11.08%

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 25 of 59

WACC – COST OF DEBT (Kd)

Question 21

Why is the real cost of debt (Kd) used and not the nominal cost of debt?

Answer

21.1 The inflation adjustment in the cost of debt (Kd) is ‘taken out’ as this is

‘replaced’ with the trending of the full value (PPE-d) of the original cost to give

the nominal TOC of the RAB.

21.2 Nominal returns on real assets would constitute a double count of CPI and

therefore ‘real returns’ are used.

Question 22

Under what scenario will equity investors be in a position to earn their full return as

embedded in the Ke portion of the WACC?

Answer

22.1 The reasonable return relates to the return on the asset for the licensee and not

for the equity investors. The actual return that will be earned by the equity

investor is a function of the capital structure of the licensee as was explained

under question 5. If the funding structures of the licensee require the debt

funding to be repaid earlier or faster, it is viewed that the equity holder has

chosen to become a ‘patient capital’ investor. The ‘patient capital’ investor will

wait for the debt capital to be repaid before they receive their required return.

22.2 The conversion of the asset base (PPE-d) to a nominal value (TOC) and the

subsequent conversion of WACC into real WACC results in the ‘addition’ of CPI

to the asset that does not ‘match’ the ‘reduction’ of the rate in earlier years.

Therefore, the returns in earlier years are lower as it takes time for the TOC

effect to catch up with the real return effect. Once the catch up has taken place

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 26 of 59

(around years 6 to 8), the return will be superior. (See graphs in question 4

above.)

Question 23

Does the post-tax, real WACC not allow the entity enough allowable revenue to pay

back its debt which is payable in pre-tax nominal terms? [The WACC (Ke & Kd) is

provided for only on a post tax, real basis.]

Answer

23.1 No. The tax shield in the Kd is provided for in the tax formula where the post-tax

Kd is grossed up with the tax shield portion of the Kd. This ensures a pre-tax Kd

is provided for in the allowable return to match the payment of the financing

costs in nominal values. (See formula in paragraph 7.3 of Methodology.)

23.2 In tables 3 and 4 below, the calculation of tax (as per the tax formula in the tariff

Methodology) is demonstrated. For each component which is taxable, a gross-

up at the existing tax rate is performed. Tax allowances are therefore provided

for in these grossed-up balances and will be included in the total balance of the

allowable revenue.

23.3 As can be seen from tables 3 and 4, the grossing up of balances also applies to

the Kd to ensure the tax shield on the Kd is properly accounted and provided

for.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 27 of 59

Table 3: Treatment of WACC with Notional Tax

Allowable Revenue = (RAB x WACC) + E + T + D + F ± C.

RAB WACC E D (historic) D

(amortisation of write-up)

T taxation) Total

allowable revenue

WACC = [Rf + (MRP*beta)*Ke] + [Kd*debt] Ke Kd WACC

Gearing 51% 49%

NERSA decision (returns %) 9.52% 3.47% 6.56%

NERSA decision value (R million) 105.00 5.10 1.78 6.88 3.00 4.00 0.20 14.08

NRBTA = {(RAB*WACC) + D + E + F ±C} - {E + D(historic)}.

0.00 0.00 0.00 (3.00) (4.00) (7.00)

NRBTA 5.10 1.78 6.88 0.00 0.00 0.20 0.00 7.08

Taxation (gross up and notional tax) 1.98 0.69 2.68 0.00 0.00 0.08 2.75 2.75

Add back tax deductions 0.00 0.00 0.00 3.00 4.00 0.00 0.00 7.00

Total revenue including notional tax 7.08 2.48 9.56 3.00 4.00 0.28 2.75 16.84

All these WACC components are not deducted to arrive at a taxable income before tax allowance. They first become grossed up. By grossing up and then adding a notional tax allowance, they all effectively become pre-tax. The applicant therefore receives the tax which he is going to pay to the fiscus.

These components are tax deductible and there-fore do not need a tax shield.

The argument sometimes is that the amortisation of the write-up (effectively to counter for the "loss" of CPI in the conversion of nominal rates to real rates) is affecting the after-tax returns. This component is also awarded a tax shield in the calculation and the applicant receives the tax allowance it needs to pay the fiscus. There is obviously a time delay.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 28 of 59

Table 4: Treatment of WACC with flow-through tax

Allowable Revenue = (RAB x WACC) + E + T + D + F + C

RAB WACC E D & wear &

tear (historic)

D (amortisation of write-up)

T(taxation) Total

allowable revenue

WACC=[Rf+(MRP*beta)*Ke]+[Kd*debt] Ke Kd WACC

Gearing 51% 49%

Returns % 9.52% 3.47% 6.56%

Returns (R million)

105.00 5.10 1.78 6.88 3.00 4.00 0.20 14.08

NRBTA ={(RAB*WACC)+D(historic & write-up)+ E+F+-C}-{E+wear & tear allowance(historic) +Kd(nominal)} 0.00 (5.88) 0.00 (3.00) (10.00) (13.00)

NPBT excl tax allowance 5.10 (4.10) 6.88 0.00 (6.00) 0.20 0.00 1.08

Taxation (gross-up and notional tax) 1.98 (1.59) 0.39 0.00 (2.33) 0.08 (1.87) (1.87)

Add back tax deductions 0.00 5.88 0.00 3.00 10.00 0.00 0.00 13.00

Total revenue including flow- through tax with tax shield on Kd

7.08 0.19 7.27 3.00 1.67 0.28 (1.87) 12.22

All these WACC components (except Kd) are not deducted to arrive at a taxable income before tax

allowance. By grossing up and then adding a notional tax allowance, they all effectively

become pre-tax. The applicant therefore receives the tax which he is going to pay. Tax shield on

Kd not given.

These components are tax deductable and therefore do not need a tax shield.

The argument is sometimes that the amortisation of the write-up (effectively to counter for the "loss" of CPI in the conversion of nominal rates to real rates) is affecting the after-tax returns. This component is also awarded a tax shield in the calculation.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 29 of 59

Question 24

Why is Vanilla WACCreal (pre-tax Kd and post-tax Ke) not used instead of grossing up

the post-tax Kd to ensure that the tax shield of the Kd is provided for in the before tax

allowable revenue?

Answer

24.1 Vanilla WACC is a calculation where the Ke is post-tax and the Kd is pre-tax.

24.2 The taxation component for the cost of debt is ‘given’ to the investor by allowing

the ‘tax shield’ in the calculation of taxation allowance (T) as is demonstrated in

the above Table 3 and Table 4.

24.3 The Vanilla WACCreal results in a higher return relative to the notional or flow-

through (with tax shield) options and therefore it is not utilised by NERSA. This is

demonstrated in the published model in the TAB ‘flow-through Vanilla’ where the

return achieved is 15.5 per cent, which is higher than the 15 per cent required

return.

DEPRECIATION

Question 25

How is depreciation and amortisation of the write-up portion calculated?

Answer

25.1 See example in Table 1 of Question 1.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 30 of 59

EXPENSES – LAND REHABILITATION

Question 26

What is the legal and regulatory foundation for the recovery of land rehabilitation cost?

Answer

26.1 In terms of the Petroleum Pipelines Act, 2003 (Act No. 60 of 2003) the authority

may require a licensee to submit a financial security, or make such other

arrangements as may be acceptable to the Authority, to ensure compliance with

any licence condition relating to health, safety, security, or the environment, prior

to, during or after the period of validity of the licence. Regulation 9 (4) of the

regulations in terms of the Petroleum Pipelines Act, 2003 (Act No. 60 of 2003)

provides that the authority must require the licensee to provide financial security

for the purpose of rehabilitating land used in connection with a licensed activity

and the composition and amount of such security. Paragraph 6.4.7 of the

Methodology states ‘Provision for land rehabilitation costs are permitted, subject

to adequate justification. These funds must be kept in accordance with the

Petroleum Pipelines Act, 2003 (Act No. 60 of 2003) and sub-regulation 9 of

Regulations made in terms of the Act published under GN R342 in Government

Gazette 30905 of 4 April 2008’.

26.2 Paragraph 6.2 and 6.3 of the methodology refers to the classification and

calculation of the operating expenses (inclusive of the land rehabilitation costs as

per paragraph 6.4.7)

26.3 Sub-regulation 9 states:

(1) Licensees must, not less than six months prior to termination,

relinquishment or abandonment of licensed activities, submit to the

Authority a plan for approval for the closure, removal and disposal, as the

case may be, of all installations relating to such licensed activities.

(2) The plan contemplated in sub-regulation (1) must include information

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 31 of 59

regarding—

(a) alternatives investigated for further use and alternative disposal of

the installations;

(b) decommissioning activities;

(c) site cleanup, removal and disposal of dangerous material and

chemicals; and

(d) an environmental impact assessment of the termination and

abandonment of the licensed activity concerned.

(3) The Authority may approve the plan contemplated in sub-regulation (1)

subject to any condition or amendment that the Authority may determine.

(4) The Authority must require the licensee to provide financial security for

purposes of rehabilitating land used in connection with a licensed activity

and the composition and amount of such security.

(5) Financial security contemplated in sub-regulation (4) may be in any form

acceptable to the Authority and may only be used with the approval of

the Authority.

(6) The Authority may, in writing, at any time, require written confirmation

from a licensee that it is in compliance with the requirements of the

National Environmental Management Act, 1998 (Act No. 107 of 1998).

(7) The Authority may require written proof from the licensee that the

authority responsible for administering the Act referred to in sub-

regulation (6) has approved the environmental impact assessment

required by the Act in question.

(8) The Authority may not, before it is in receipt of a certificate from an

independent consultant competent to conduct environmental impact

assessments in accordance with the provisions of the National

Environmental Management Act, 1998 (Act No. 107 of 1998), stating that

the site has been rehabilitated, give consent to the termination of a

financial security arrangement contemplated in sub-regulations (4) and

(5).

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 32 of 59

26.4 The financial instrument must be in a form acceptable to the Energy Regulator as

required by section 9 (5) of the regulations. To ensure compliance in this regard it

would be the most practical for the financial security structure to be approved by

the Energy Regulator in advance. The guidelines the Energy Regulator would

apply when evaluating the financial security as referred to in regulation 9 (4) and

(5) are:

- a secure financial instrument with the objective of beating inflation; and

- a legal framework to ensure that such funds cannot be accessed by

normal operational funding needs or creditors. This would probably

require some sort of Trust structure.

Question 27

How should land rehabilitation costs be calculated and recovered trough the Allowable

Revenue?

Answer

27.1 Land rehabilitation costs are recovered as part of operating expenses.

27.2 Land rehabilitation cost can therefore NOT be included as part of Property, Plant

and Equipment (RAB) and therefore no return is earned thereon.

27.3 The mechanism to collect the land rehabilitation costs is the present value of the

future liability less the value of funds in the ‘decommissioning fund’ to arrive at a

balance still to be collected. The remaining balance is then divided by the

remaining years to decommission the asset. The formula for this is:

PMT=[PVfund value]/n

Where

N = the number of remaining years to decommission

PVfund value = the present value of decommissioning costs

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 33 of 59

Fund value = the current balance in the decommissioning fund, being historic

contributions (provision for decommissioning costs) plus net

returns on such contributions.

27.4 An example of how the land rehabilitation cost is to be calculated is presented in

Table 5.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 34 of 59

Table 5: An example on the calculation of land rehabilitation costs

Asset value

10,00

0 PV of expected

rehabilitation cost

6,000

Life of Asset

10yrs

1 2 3 4 5 6 7 8 9 10

CPI a 5% 6% 4% 4% 6% 7% 8% 5% 4% 5% Net returns [after tax] in the fund b 6% 7% 5% 4% 6% 7% 8% 4% 4% 5%

Remaining Life c 10 9 8 7 6 5 4 3 2 1

Present value of Land rehabilitation liability

d=opening* (1+a)

6,000

6,360

6,614

6,879

7,292 7,802

8,426

8,848 9,202 9,662

Fund value at beginning of the year e= 0 (618) (1,317) (2,061) (2,846) (3,780) (4,877) (6,190) (7,341) (8,584)

Still to be recovered over remaining life f=d+e

6,000

5,742

5,297

4,817

4,446 4,022

3,549

2,658 1,860 1,078

To be recovered "this" year g=f/c

600

638

662

688

741 804

887

886 930 1,078

Value of fund

Opening Balance h=j

-

618

1,317

2,061

2,846 3,780

4,877

6,190 7,341 8,584 Contribution from allowable revenue via the tariff g

600

638

662

688

741 804

887

886 930 1,078

Net returns [after tax] in the fund i=(h+g*50%)*b

18

61

82

96

193 293

426

265 312

Closing Balance of fund j=h+g+i

618

1,317

2,061

2,846

3,780 4,877

6,190

7,341 8,584 9,662

Liability less Fund value k=d-j

5,382

5,043

4,553

4,033

3,512 2,925

2,236

1,506 618 -

Note

The value of the land rehabilitation liability in year 10 (R9,662) is covered by the value

of the fund at the end of that year (R9,662) excluding the investment returns in that

year.

27.5 For the above example, the Depreciation in the Allowable Revenue formula

compared to the allowance of the land rehabilitation on an annual basis is

demonstrated in Figure 5 below. Note that the upward trend is similar to achieving

the goal of raising tariffs as intended by the nominal assets, real return principle

used in the methodology.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 35 of 59

Figure 5: Depreciation and TOC Amortisation vs Land Rehabilitation cots

F-FACTOR

Question 28

How is the F-factor calculated and how will it be recovered?

Answer

28.1 Details are provided in Section 4.2.14 of the Tariff Methodology. The F-factor will

be treated as a return of capital, i.e. deducted from/added to the RAB.

CLAWBACK

Question 29

When will clawbacks be applied?

-

200

400

600

800

1 000

1 200

1 400

1 600

1 800

1 2 3 4 5 6 7 8 9 10

Depreciation and TOC amortization vs Land rehabilitation costs

Depreciation and TOC amortization Land rehabiliatation cost

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 36 of 59

Answer

29.1 In the tariff period following the release of audited financial statements of the

applicant.

Question 30

Are there examples of specific clawback calculations?

Answer

30.1 The formula for clawback adjustments is as follows:

Clawback adjustments = ARA +(PPE-d)A + DA + KdA + EA + OeA + + + GA

Where:

ARA = Allowable revenue adjustment

(PPE-d)A = Allowable revenue adjustment on (PPE-d)updates

DA = Depreciation and amortisation of inflation write-up adjustment

KdA = Cost of debt adjustment

EA = Expenses adjustment

GA = General adjustment for any remaining differences between

projected allowable revenue and actual allowable revenue not

resulting from efficiency gains, for example:

i. debt ratio and the effect thereof on beta, cost of equity,

WACC and the taxation effect of these adjustments

ii. taxation adjustments

iii. other

OeA = Operating efficiency adjustment (Only if more efficient)

Note: Operating efficiency could result in clawbacks to or from a

licensee.

30.2 More detail on the formulas to determine clawbacks is presented below.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 37 of 59

30.2.1 Allowable Revenue adjustment (ARA)

The allowable revenue adjustment compensates the licensee and customers for

differences between allowable revenue planned and allowable revenue realised

in a specific tariff period. The following formula applies:

ARA = ARa - ARr

Where

ARA = Allowable revenue adjustment

ARa = Allowable revenue approved

ARr = Allowable revenue realised

30.2.2 Value of new operating property, plant and equipment adjustment (PPE-d)

The net value adjustment for operating property, plant and equipment (PPE-d)A

compensates licensees and customers for differences in operating assets

estimated to be in use and operating assets actually in use in the tariff period

under review. This pertains to changes arising from additions, decommissioning

and disposals of operating assets – as well as to the timing of implementing

these changes. Timing refers to the difference between the projected date and

the actual date when the changes were implemented.

Adjustments to the net value of the operating assets (PPE-d)A is determined by

applying the formula below:

(PPE-d)A = Allowable revenue adjustment on (PPE-d)updates

= [(PPE-d)updates x (Dya – Dyp)/365] x WACC

Where:

(PPE-d)updates = Net value of the operating assets that will be

commissioned, decommissioned or disposed of during the

tariff period under review.

Dya = Actual number of days from the date when the operating

asset(s) was commissioned, decommissioned or disposed of

to the end of the tariff period.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 38 of 59

Dyp = Projected number of days from the date when the operating

asset(s) was planned to be put into use, decommissioned

or disposed of to the end of the tariff period.

30.2.3 Depreciation and amortisation of inflation write-up adjustment (DA)

The depreciation and amortisation of inflation write-up adjustment provides for

the differences between the projected depreciation made at the time the

allowable revenue was determined and the actual depreciation for the specific

tariff period. The following formula must be applied:

DA = Da – Dp

Where:

DA = Depreciation and amortisation of inflation write-up adjustment

Da = Depreciation and amortisation of inflation write-up actual

Dp = Depreciation and amortisation of inflation write-up approved

30.2.4 Cost of Debt Adjustment (KdA)

If there is a difference between the estimated cost of debt in the allowable

revenue and the actual cost of debt for that tariff period, then the allowable

revenue must be recalculated using the actual cost of debt and the difference

added to or subtracted from the clawback adjustment. The following formula must

be used to determine the KdA:

KdA = Allowable Revenue recalculated using actual cost of debt –

Allowable Revenue calculated using approved cost of debt2

30.2.5 Expense adjustment – Operating and Maintenance Adjustment (EA)

Adjustments on operating and maintenance expenditure provides for differences

between expenditure projected at the time of setting the tariffs and the actual

2 All other factors and quantum in estimated Allowable Revenue remain the same.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 39 of 59

expenditure for the tariff period and is calculated by applying the following

formula:

EA = Ep – Ea

Where:

EA = Operating and maintenance expense adjustment

Ep = Operating and maintenance expense projected

Ea = Operating and maintenance expense actual

30.2.6 General adjustment (GA)

Provision is made for a general adjustment. This adjustment is for any

remaining differences between projected allowable revenue and actual

allowable revenue not resulting from efficiency gains, for example:

i. debt ratio and the effect thereof on beta, cost of equity, WACC and the

taxation effect of these adjustments;

ii. taxation adjustments; and

iii. other.

TAX

Choice between two different tax approaches

Question 31

What is the difference between flow-through tax and notional tax?

Answer

31.1 Section 10.2 of the Methodology states that the flow-through tax is the actual tax

paid by the entity and this is allowed as a tax allowance. Notional tax expense is

the tax due according to accounting requirements. Flow-through tax neither

awards the tax shield nor the benefits of accelerated wear and tear (or deferred

taxation).

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 40 of 59

Question 32

How is the tax calculated under the following scenarios?

Flow-through tax

Notional tax

Answer

32.1 Examples on the calculation of tax under the two scenarios are provided in tables

6, 7, 8 and 9.

32.2 Calculation of the flow-through tax.

Tax = {(NRBTA) / (1-t)}*t

Where:

NRBTA = Net revenue before tax allowance

= {(RAB*WACC)+E+D(historic & write up)+F± C} -

{E+D(historic) +Kd(nominal)}.

t = prevailing corporate tax rate of the licensee

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 41 of 59

Table 6: Example of the calculation of flow-through taxes

Ke a 5.10

Kd b 1.78

WACC c=a+b 6.88

E d 3.00

D (historic) e 4.00

D (write-up) ee 0.20

Wear and tear allowance eee 10.00

F f -

C [Claw back Excluding Tax claw back] g -

NRBTA=Allowable revenue before tax allowance h=c+d+e+ee+f+g 14.08

t j 28%

Kd (nominal) n 5.88

NRBTA={(RAB*WACC)+E+D(historic & write up)+F+-C}-{E+D(historic)

+Kd(nominal)} Note that interest is deducted as an actual tax

calculation is performed k=h-d-e-n (4.80)

Tax={(NRBTA excl tax allowance)/(1-t)}*t l={k/(1-j)}*j (1.87)

Total Allowable revenue m=h+l 12.22

Test tax rate l/(k+l) 28%

Note that no other non-taxable income or non-deductible expenses have been

included above. These will form part of the actual calculation when detail is

available.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 42 of 59

Table 7: The effect of using flow-through tax

Allowable Revenue = (RAB x WACC) + E + T + D + F + C

RAB WACC E D & wear and tear (historic)

D (amortisation of write-up)

T(taxation) Total

allowable revenue

WACC=[Rf+(MRP*beta)*Ke]+[Kd*debt] Ke Kd WACC

Gearing 51% 49%

Returns % 9.52% 3.47% 6.56%

Returns (R million)

105.00 5.10 1.78 6.88 3.00 4.00 0.20 14.08

NPBT excl tax allowance={(RAB*WACC)+E+D(historic & write-up)+F+-C}-{E+wear & tear allowance (historic) +Kd(nominal)} 0.00 (5.88) 0.00 (3.00) (10.00) (13.00)

NPBT excl tax allowance 5.10 (4.10) 6.88 0.00 (6.00) 0.20 0.00 1.08

Taxation (gross-up & notional tax) 1.98 (1.59) 0.39 0.00 (2.33) 0.08 (1.87) (1.87)

Add back tax deductions 0.00 5.88 0.00 3.00 10.00 0.00 0.00 13.00

Total revenue including flow-through tax with tax shield on Kd

7.08 0.19 7.27 3.00 1.67 0.28 (1.87) 12.22

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 43 of 59

Table 8: Example on the calculation of notional tax

Tax = {(NRBTA) / (1-t)}*t Where NRBTA = Net revenue before tax allowance

= {(RAB*WACC) +E+D(historic & write-up) +F ± C} - {E+D(historic)}.

t = prevailing corporate tax rate of the licensee

Ke a

5.10

Kd b

1.78

WACC c=a+b

6.88

E d

3.00

D (historic) e

4.00

D (write-up) ee

0.20

Wear and tear allowance eee

10.00

F f -

C [Claw back Excluding Tax claw back] g -

NRBTA=Net revenue before tax allowance h=c+d+e+

ee+f+g

14.08

t j 28%

Kd (nominal) n

5.88

NRBTA={(RAB*WACC)+E+D(historic & write up)+F+-C}-{E+D (historic) } Note that interest is not deducted to allow for the tax shield on after tax real Kd. k=h-d-e 7.08

Tax={(NRBTA)/(1-t)}*t l={k/(1-

j)}*j 2.75

Total Allowable revenue m=h+l

16.83

Test tax rate l/(k+l) 28%

FAQ Version 4: Approved on 29 July 2013.

Page 44 of 59

Table 9: The impact of the ‘tax shield’ when notional tax is used

Allowable Revenue = (RAB x WACC) + E + T + D + F + C

RAB WACC E D

(historic)

D (amortisation of write-up)

T(taxation) Total

allowable revenue

WACC=[Rf+(MRP*beta)*Ke]+[Kd*debt] Ke Kd WACC

Gearing 51% 49%

Returns % 9.52% 3.47% 6.56%

Returns (R million)

105.00 5.10 1.78 6.88 3.00 4.00 0.20 14.08

NPBT excl tax allowance={(RAB*WACC)+E+D+F+-C}-{E+D(historic)}

0.00 0.00 0.00 (3.00) (4.00) (7.00)

NPBT excl tax allowance 5.10 1.78 6.88 0.00 0.00 0.20 0.00 7.08

Taxation (gross-up and notional tax) 1.98 0.69 2.68 0.00 0.00 0.08 2.75 2.75

Add back tax deductions 0.00 0.00 0.00 3.00 4.00 0.00 0.00 7.00

Total revenue including notional tax 7.08 2.48 9.56 3.00 4.00 0.28 2.75 16.84

Tax – deferred tax (dtax)

Question 33

Why is the deferred tax asset/liability not included in the RAB formula when the flow-

through tax option is chosen?

Answer

33.1 Deferred tax liabilities do not arise relative to the allowable revenue awarded

when the flow-through approach is taken because it is merely a timing issue of

when the tax will be paid and therefore it is not deducted in the RAB formula.

33.2 Deferred tax assets arising from tax losses in earlier years are not added in the

RAB formula to counteract the previous ‘competitive advantage’ enjoyed by the

entity because of this asset class.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 45 of 59

TARIFF MODEL ON NERSA’S WEBSITE

Question 34

Is there a practical example of how to incorporate all the elements of the tariff

methodology into one template?

Answer

34.1 NERSA has published a model on its website with the intention of

demonstrating the various options and scenarios by way of testing the target

cost of equity by the outcome of the internal rate of return (IRR) of cash flows to

investors.

34.2 Some general notes on the model as published on NERSA’s website are:

i. Base case – The model presents a base case scenario using the

notional tax option where no adjustments are made for deferred taxation

to the RAB.

ii. F-Factor – The model demonstrates the treatment of the F-factor as a

return of capital, i.e. the full value of the F-factor is deducted from/or

added to the RAB.

iii. Notional tax – This is the notional tax option with the deferred taxation

adjusted in RAB. Note that IRR is higher than targeted as the actual tax

and deferred tax cash flows practically lag one year.

iv. Tax formula notional – The model demonstrates the tax formula for

year 1 and also demonstrates the tax shield for each component of

allowable revenue.

v. Flow-through using Vanilla WACC – This represents a flow-through

option but with the Kd pre-tax. This means that the tax shield on the Kd

is not allowed in the tax calculation as the tax is already included in the

pre-tax rate. Also note that the ‘achieved IRR’ in this option is higher

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 46 of 59

(15.50 per cent) than the targeted 15 per cent, which is why this option

is not followed.

vi. Flow-through actual – Flow-through tax is defined in the Methodology

(paragraph 10.2) as actual tax payments. As can be seen, the resultant

IRR is below the target IRR of 15 per cent, which is a result of the tax

shield on cost of debt not being allowed. For this reason, NERSA uses

the tax flow-through formula to calculate the tax allowance in the model.

vii. Graphs – The model also has ‘worksheet tabs’ comparing, by way of

data or graphs, the differences between the various tax options (flow-

through and notional tax) and tenures of debt (10 years versus 25

years).

NOTES ON MULTI-YEAR TARIFF APPLICATIONS

Question 35

How will NERSA treat multi-year tariff applications?

Answer

The treatment of multi-year tariffs is presented in the section that follows.

FAQ Version 4: Approved on 29 July 2013.

Page 47 of 59

Notes on multi-year tariffs in terms of the Petroleum Pipelines Act

Approved on 18 September 2012

1. Purpose

1.1 Regulating the tariffs charged for pipelines, storage and loading facilities within

the petroleum pipelines industry is a function of the National Energy Regulator

of South Africa (NERSA or ‘the Energy Regulator’). In doing so, NERSA applies

its tariff methodologies3. Throughout this paper, these methodologies are

referred to as ‘the Methodologies’. These Methodologies meet all the

requirements of the Petroleum Pipelines Act, 2003 (Act No. 60 of 2003) (‘the

Act’) and the Regulations in terms of this Act (‘the Regulations’).

1.2 Regulation 4(9)(a) of the Regulations provides licensees with the option to

follow a multi-year tariff dispensation when applying for tariff increases. Some

licensees have indicated that they intend to follow this approach and this

document serves to provide clarifying notes on implementing multi-year tariffs

within the petroleum pipelines industry.

3 Methodologies:

1. Tariff methodology for the setting of tariffs in the petroleum pipelines industry. 6th Edition.

Approved on 31 March 2011.

2. Tariff methodology for the approval of loading facilities and storage facilities. 2nd

Edition.

Approved on 31 March 2011.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 48 of 59

2. Summary

2.1 Tariffs are typically set for periods of one year, however in the case of multi-

year decisions, tariffs are set for a period of two to five years. Tariffs for the

years ahead are necessarily based on forecasts for various parameters. As a

general rule, the longer the forecast period is, the less accurate the forecasts

towards the end of the period are likely to be.

2.2 With the passing of time forecasts can be replaced with actual data for those

parameters. When sufficient actual data is available for a tariff year, the tariff

will be recalculated. If there is a difference, as is often the case, clawbacks or

give backs will be calculated. This will be done each year during a multi-year

tariff decision. Because actual data for tariff year one will only become available

in tariff year two, any clawback or giveback will only be implemented in tariff

year three

2.3 To lessen the impact of the uncertainty brought about with having to work with

estimated, forecasted and proxy values in a multi-year tariff determination, there

will be instances where NERSA will have to update such values with more

recent values. When the update needs to be done, it may require the opening of

the public participation process in order to amend the multi-year tariffs set or

approved. (See paragraph 6.2 for more detail.)

3. Definition of multi-year tariffs

3.1 The term ‘multi-year’ tariff determination means that tariffs for multiple

years/periods are being determined at one point in time.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 49 of 59

3.2 The Methodologies define a tariff period as a period of one year (12 months) –

which is the financial year of the licensee.

3.3 A multi-year tariff application implies that each of the components in the formula

for determining the allowable revenue (AR) for each of the years/periods will

have different values that need to be brought into consideration when setting

the allowable revenue for each of these years.

3.4 The adjustments to the values of the components are brought into account by

applying clawbacks (to and from the licensee). Guidance on how and when

these clawbacks will be done, as well as the terms and conditions for revising

the decision and therefore the re-opening of the public consultation process

pertaining to a specific multi-year tariff determination, are presented in the rest

of this document.

4. Components

The values of the components referred to above, are the values of specifically

identified components as contained in the following formulas:

4.1 Formula to calculate the allowable revenue (AR):

AR = (RAB x WACC) + D + E +F ± C + T

Where:

AR = Allowable revenue

WACC = Weighted average cost of capital

D = Depreciation and amortisation of inflation write-up for the tariff

period under review

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 50 of 59

E = Expenses: actual and accrued operating and maintenance

expenses, including provisions for land rehabilitation costs, for

the tariff period under review

F = Projected revenue addition to meet debt obligations for the tariff

period under review

C = Clawback adjustments in all elements of clawback formula to

correct for differences between actuals and approved for a

preceding tariff period or periods.

T = Tax expense: estimated notional or flow through tax expense for

the tariff period under review

4.2 Formula pertaining to the composition of the RAB:

RAB = (PPE – d) + w ± dtax

Where:

PPE = Value of original and inflation write-up of operating assets

(property, plant and equipment)

d = Accumulated depreciation and accumulated amortisation of

inflation write-up for the period up to the commencement of the

tariff period under review

w = Net working capital

dtax = Deferred tax

4.3 Formula to calculate the weighted average cost of capital (WACC):

Kd*

EqDt

DtKe*

EqDt

Eq WACC

Where:

Eq = Shareholders equity

Dt = Interest bearing debt

Ke = Post-tax, real cost of equity derived from the capital asset pricing

model (CAPM)

Kd = Post-tax, real cost of debt

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 51 of 59

4.4 Components in the formula to determine the cost of equity (Ke):

− Riskfree rate (Rf)*

− Market risk premium (MRP)* and

− Beta ( )*

Note:

The * indicates that as per these Methodologies, these values are to be

determined as at 12 months prior to the commencement of a specific tariff

year/period.

In a multi-year tariff determination, this means as at 12 months prior to the

commencement of each of the respective tariff years/periods. The application,

however, will reflect the value of these components only as at 12 months prior

to the first tariff year/period because only these are available.

4.5 Formula to determine the cost of debt(Kd):

1 - CPI 1

t)]-(1*[Kd1 Kd

nomtax,prenominaltax,-post

Where:

Kdpre-tax,nominal = Projected cost of debt, pre-tax, nominal, for the tariff period

under review

t = Prevailing corporate tax rate of the licensee.

CPI = Actual annual consumer price index (CPI) as at 12 months

prior to the commencement of the current tariff period under

review.

Note

This annual CPI is the same actual annual CPI included in the

calculation of the average used for converting year 25 in the

market risk premium (MRP) formula from its nominal to real

value.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 52 of 59

5. Categories of values

The values of the components can broadly be classified into the following three

categories:

5.1 Estimated Values

i. These are the estimated values of the components as at the time of

applying for the tariff determination. These values are then later updated

with the actual values. The differences between the estimated and actual

values for a particular year will be clawed back (to or from the licensee).

The clawback will be calculated once a particular tariff year/period has

expired and the actual values are available.

ii. The following components are included in this category:

- the regulated asset base [RAB];

- operational expenditure [E];

- depreciation [D];

- nominal cost of debt [Kdnom];

- debt ratio;

- tax rate [t]; and

- volumes shipped [Vol].

5.2 Proxy Values

i. The value of these components is 'proxies' based on actual data 12

months prior to the commencement of the tariff period. In a single year

tariff application, these values will always be known at the time of the

application and no adjustments need be made.

ii. In a multi-year/period tariff application, the value for the first year (Y1) is

to be determined in the same way as for a single year tariff application:

as at 12 months prior to the commencement of Y1. The final values for

the remaining years (Y2, Y3, Y4 and Y5) can only be determined in

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 53 of 59

future and therefore the values for Y1 will also be used as the value for

these years until such time that the proxy values for these years can be

determined with certainty as at 12 months prior to the start of each of

these years.

iii. The value of Y2, Y3, Y4 and Y5 will then be corrected by performing a

clawback calculation once that particular year has passed and clawback

calculations on the actual values for that particular year are being

implemented.

Note:

The tariffs for these remaining years (Y2, Y3, Y4 and Y5) will not be

updated at the beginning of each of these respective years as this will be

done in the year when the clawbacks for each of these particular years

are being implemented.

iv. The components falling into this category are mainly the components for

determining the cost of equity [Ke]:

- the risk free rate [Rf]

- the market risk premium [MRP]; and

- the beta [ ].

5.3 Forecasted Values

i. The only component in this category is the forecast for the consumer

price index [CPI]. The CPIf for Y1 will be the forecast which is

determined by using the actual forecast for CPI as at 12 months prior to

the commencement of the tariff period as proposed in paragraph 4.5.

ii. The components affected by the CPIf are:

- the RAB: to calculate the trended original cost (TOC) addition to

property, plant and equipment (PPE-d); and

- cost of debt: to convert the nominal cost of debt (Kd) to real cost of

debt.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 54 of 59

iii. The CPIf will be set at the actual forecasts as at 12 months prior to the

commencement of Y1.

iv. The CPIf will not necessarily be the same as was determined for Y1

throughout the multi-year tariff period, as the inflation outlook will be

different looking further into the future. However, this outlook will not be

updated for the remaining years (Y2, Y3, Y4, and Y5) at the beginning of

these years but rather ‘corrected’ by way of clawbacks in the year when

the clawbacks applicable to each of these respective remaining years

are being implemented. The reason for this is because the effect of the

CPIf on the RAB, as a result of the trending of the RAB (TOC), is

complicated and we propose the final TOC be done once the final

forecasted value to be used in the clawback is known.

v. In this document, the forecasts on volumes are also done at the

beginning of the multi-year tariff period.

6. Terms and conditions for the amendment to a multi-year tariff decision

6.1 NERSA may, during the course of a multi-year tariff period, adjust the multi-year

tariff. The legal basis for this is Regulation 4(9) of the Regulations:

4(9) The Authority must as appropriate-

(a) for a period between 3 and 5 years, adjust pipeline tariffs in a

manner that seeks to-

i. take into account rising operating and maintenance costs; and

ii. increase efficiency of the operation of the pipeline; and

(b) at the end of period contemplated in sub-regulation (a), or any other

time if the need arises, conduct a comprehensive tariff setting exercise in

the manner contemplated in sub-regulation (2).

6.2 After a multi-year tariff decision has been made, NERSA will monitor the trends

in the variables listed below to decide whether or not changes in these variables

since the start of the multi-year tariff period would result in a new tariff that

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 55 of 59

exceeds the threshold as per paragraph 6.3 below. If the threshold is exceeded,

NERSA will:

a) publish a draft amendment to the multi-year tariff decision; and

b) consult the public in this regard.

Variables

i. regulated asset base (RAB);

ii. operational expenses;

iii. volumes;

iv. debt ratio; and

v. values of the estimated, forecasted and proxy components listed above

under number 5 in order to determine the WACC.

6.3 Should changes in the values of the above listed variables and the relevant

clawbacks for each 12-month period have an impact of 20 per cent or more

(increase or decrease) on the tariff level(s) as per the original multi-year tariff

decision, it would signal the need for NERSA to open the public consultation

process in order to amend the multi-year tariffs set or approved.

6.4 For NERSA to be able to monitor the trend in the values of the variables listed

above in 6.2, a licensee will have to submit data to NERSA on an annual basis

throughout the multi-year tariff period.

6.5 It is important to note that a licensee can, in terms of Section 28(5) of the Act,

request NERSA to review its tariffs from time to time. Section 28(5) is also

applicable to a multi-year tariff decision.

7. Conclusion

i. A matrix of the different categories of values and the timing thereof are

presented in Table 1 on the pages 57 to 72.

ii. It should be noted that clawbacks from previous tariff determinations

(single or multi-year) will still be implemented as required.

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 56 of 59

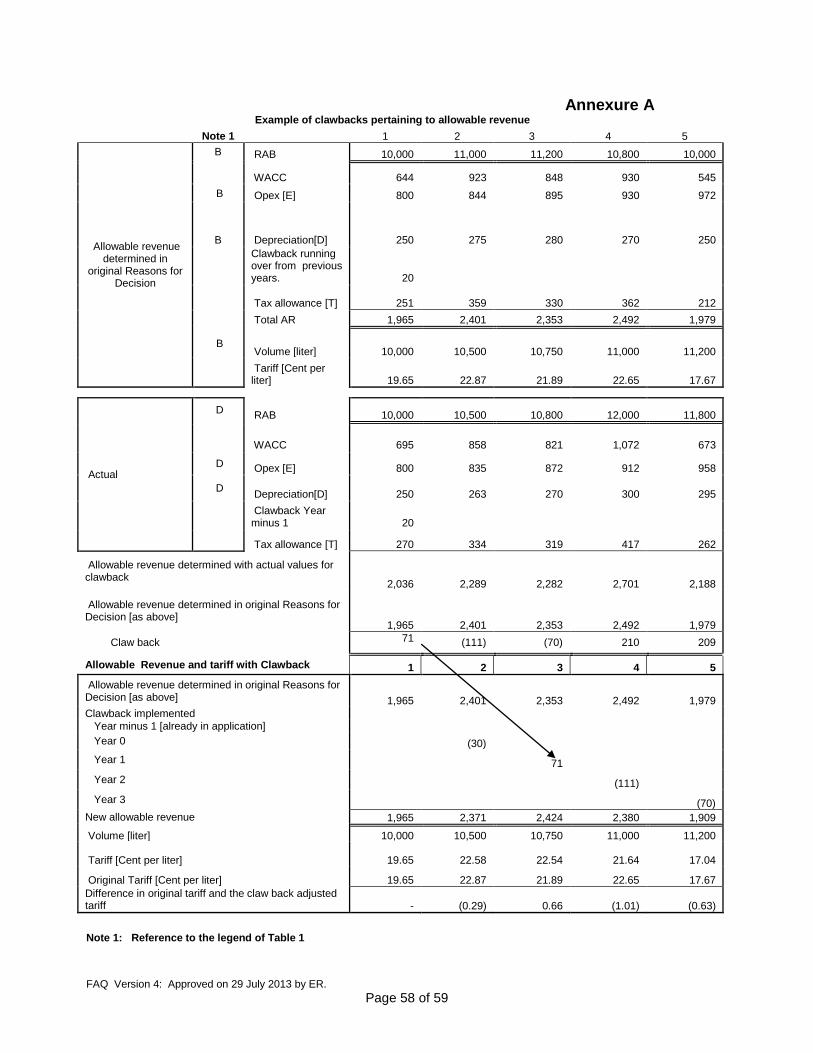

8. Annexures

Annexure A:

Practical example reflecting the treatment of claw backs in a multi-year tariff

determination

FAQ Version 4: Approved on 29 July 2013 by ER.

Page 57 of 59

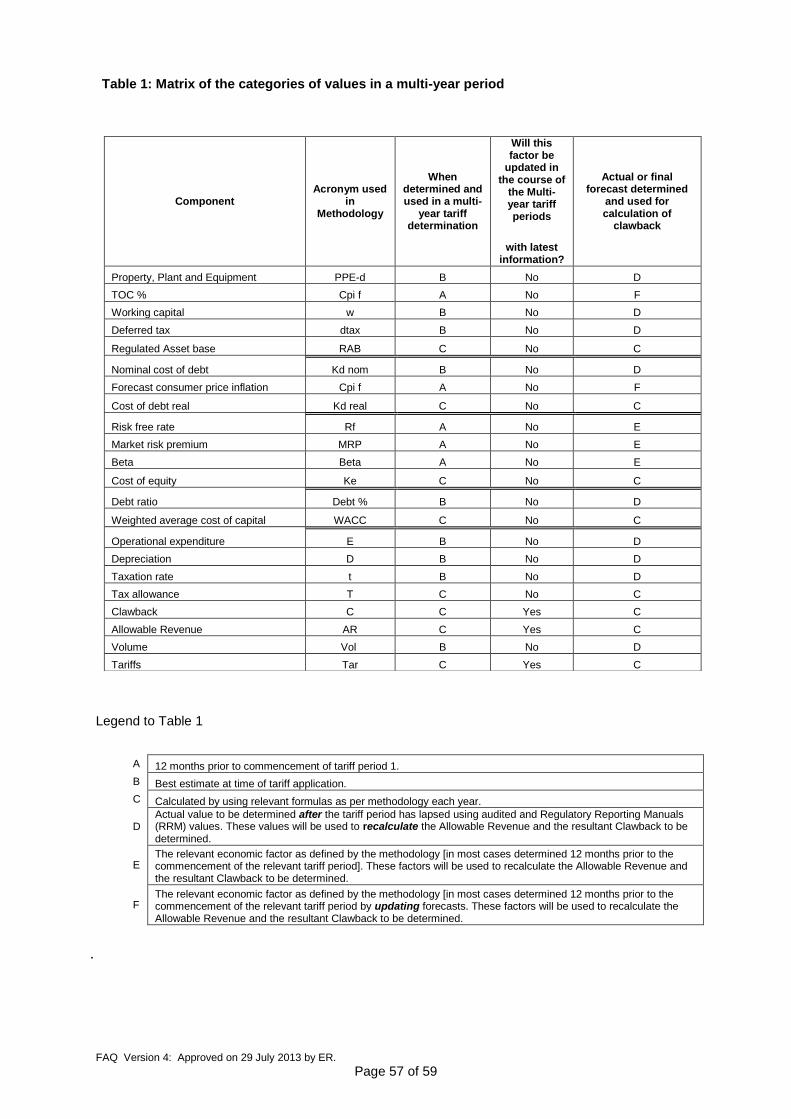

Table 1: Matrix of the categories of values in a multi-year period

Legend to Table 1

A 12 months prior to commencement of tariff period 1.

B Best estimate at time of tariff application.

C Calculated by using relevant formulas as per methodology each year.

D Actual value to be determined after the tariff period has lapsed using audited and Regulatory Reporting Manuals (RRM) values. These values will be used to recalculate the Allowable Revenue and the resultant Clawback to be determined.

E The relevant economic factor as defined by the methodology [in most cases determined 12 months prior to the commencement of the relevant tariff period]. These factors will be used to recalculate the Allowable Revenue and the resultant Clawback to be determined.

F The relevant economic factor as defined by the methodology [in most cases determined 12 months prior to the commencement of the relevant tariff period by updating forecasts. These factors will be used to recalculate the Allowable Revenue and the resultant Clawback to be determined.

.

Component

Acronym used in

Methodology

When determined and used in a multi-

year tariff determination

Will this factor be

updated in the course of

the Multi-year tariff periods

with latest information?

Actual or final forecast determined

and used for calculation of

clawback

Property, Plant and Equipment PPE-d B No D

TOC % Cpi f A No F

Working capital w B No D

Deferred tax dtax B No D

Regulated Asset base RAB C No C

Nominal cost of debt Kd nom B No D

Forecast consumer price inflation Cpi f A No F

Cost of debt real Kd real C No C

Risk free rate Rf A No E

Market risk premium MRP A No E

Beta Beta A No E

Cost of equity Ke C No C

Debt ratio Debt % B No D