for producer use only. not for distribution to the public. estate planning for foreign nationals–a...

TRANSCRIPT

For producer use only. Not for distribution to the public.

Estate Planning for Foreign Nationals–A World of Opportunity

OLA 2026 0314

For producer use only. Not for distribution to the public.

Key Trends

Glocalization

For producer use only. Not for distribution to the public.

Why Consider the Foreign National Market?

• Large, growing population• Foreign Nationals face unique

U.S. planning challenges• Significant need for

information on strategies and planning

For producer use only. Not for distribution to the public.

Where are Foreign Nationals?

New York

West Palm Beach

Washington, DC

Seattle

Los Angeles

Sacramento

Las Vegas

Phoenix

Dallas – Fort Worth

Boston

Colorado Springs

Denver

Minneapolis

Houston

Detroit

Sarasota

Tampa

Orlando

Miami

Atlanta

Philadelphia

For producer use only. Not for distribution to the public.

Understanding Needs

Foreign Nationals fall into two categories:• Resident Aliens• Non-Resident Aliens

For producer use only. Not for distribution to the public.

Resident Aliens

• Foreign National with permanent U.S. home• Worldwide assets subject

to U.S. estate and gift tax• Denied certain tax

advantages available to U.S. citizens

For producer use only. Not for distribution to the public.

Non-Resident Aliens

• Foreign National with permanent home in another country

• Only U.S. assets subject to U.S. estate and gift tax

For producer use only. Not for distribution to the public.

Residency Factors

• What is your immigration status?

• Where do you spend most of your time?

• Where do you consider home to be?

• Do you own a home in the United States?

For producer use only. Not for distribution to the public.

Planning Issues

• Resident Aliens with significant worldwide assets

• Non-Resident Aliens with U.S.-based assets

• Married couples with a Foreign National spouse

For producer use only. Not for distribution to the public.

U.S. Estate Tax Comparison

*Intangible property includes stock in a U.S. corporation and interest in a U.S. partnership

Resident Alien (RA)

Non-Resident Alien (NRA)

Lifetime estatetax exemption

$5,340,000 $60,000

Estate tax rate 40% top tax rate 40% top tax rate

Unlimitedmarital deduction

Only if inherited assets are transferred

to QDOT

Only if inherited assets are transferred

to QDOT

Assets subjectto U.S. estate taxes

All worldwide assets

U.S. properties,

including most intangible properties*

For producer use only. Not for distribution to the public.

Resident Aliens

Worldwide assets subject to U.S. estate tax• Property in the United States• Property outside the United States

For producer use only. Not for distribution to the public.

What they don’t know…

A survey of immigrants to the U.S. with a net worth of $10 million or more found:

Source: “Clueless,” Trusts and Estates, December 2003

Survey Question Asked% Who

Answered Yes

Before emigrating to the U.S. those who sought advice as to the consequences of acquiring a U.S. residency for U.S. gift and estate taxes

34.5%

Obtained advice for making gifts of non-U.S. property prior to coming to the U.S.

10.9%

After emigrating to the U.S., those who sought tax advice 49.6%

Of the above group, those who sought advice on U.S. estate planning that could minimize estate taxes

6.8%

For producer use only. Not for distribution to the public.

Why Is Planning Important?

Meet Carlos, a Peruvian national, U.S. resident• $15 million in U.S. assets• $20 million in Peruvian assets

For producer use only. Not for distribution to the public.

Estate Erosion

Gross Estate $35,000,000

Estate Tax $11,845,800

Net Estate $23,154,200

Estate Shrinkage 33.85%

For producer use only. Not for distribution to the public.

Solution: Trust owned life insurance

• Create irrevocable life insurance trust• Trust provides liquidity for estate taxes and

other needs

For producer use only. Not for distribution to the public.

Non-Residents Purchasing U.S. Real Estate

For producer use only. Not for distribution to the public.

What They Don’t Know

$60,000

Non-Resident AlienResident Alien

$5.34M

For producer use only. Not for distribution to the public.

Why Planning Is Important

Niran• Thai resident and national• Purchased ski getaway

in Colorado

For producer use only. Not for distribution to the public.

U.S. Estate Tax Exposure

home in Telluride, CO

estate tax liability in 2014$1.1M

$3M

For producer use only. Not for distribution to the public.

Nonresident AliensU.S. Gift and Estate Situs Rules

*A gift of a life insurance policy on oneself may be subject to the IRC §2035 look back rule, and therefore may be subject to estate taxes if included within the decedent’s estate.

Type of property transferred

Subject to U.S. Gift tax

Subject toU.S. Estate tax

Real property located in U.S. Yes Yes

U.S. tangible personal property (i.e., cash, jewelry, paintings, automobiles) Yes Yes

U.S. intangible personal property (i.e., stocks in U.S. corp., interest in U.S. partnership)

No Yes

Ownership interest in a U.S. life insurance policy on oneself No* No

For producer use only. Not for distribution to the public.

Estate Erosion

Death in 2014

Tentative TaxLess Credit

($1,145,800) $13,000

Net Taxes ($1,132,800)

Net U.S. Assets $1,867,200

Estate Erosion = 38%

For producer use only. Not for distribution to the public.

Alternative 1

Tangible Property Intangible Property

Gift to Heirs

For producer use only. Not for distribution to the public.

Alternative 2

For producer use only. Not for distribution to the public.

Alternative 2

For producer use only. Not for distribution to the public.

Alternative 2

For producer use only. Not for distribution to the public.

Alternative 2

For producer use only. Not for distribution to the public.

Alternative 3

Life Insurance

For producer use only. Not for distribution to the public.

Married Couple with Foreign National

No unlimited marital estate deduction

For producer use only. Not for distribution to the public.

Love knows no boundaries

CANADA / 69,887

MEXICO / 390,950

PUERTO RICO / 54,551

CUBA / 14,430

ENGLAND / 33,877

SPAIN / 12,653

ITALY / 19,080

GERMANY / 92,997

CHINA / 29,532

INDIA / 35,092

THAILAND / 13,368

VIETNAM / 20,951

PHILIPPINES / 74,180

JAPAN / 28,964

KOREA / 39,846

TOP COUNTRIES FOR CROSS-BORDER MARRIAGES TO A U.S. CITIZEN(TOTAL NUMBER OF COUPLES IN 2010)

Source: "Legal Hassles of Global Love Affairs” Wall Street Journal, Summer 2013

For producer use only. Not for distribution to the public.

The Issue

Foreign NationalU.S. Citizen

For producer use only. Not for distribution to the public.

The Issue

Foreign NationalU.S. Citizen

No Deduction

For producer use only. Not for distribution to the public.

The Issue

Foreign NationalU.S. Citizen

For producer use only. Not for distribution to the public.

The Issue

Foreign NationalU.S. Citizen

Unlimited Marital Deduction

For producer use only. Not for distribution to the public.

Why Planning Is Important

• Mark, a U.S. citizen• Anna, a Philippine citizen

and U.S. Resident Alien • $15 million net worth

For producer use only. Not for distribution to the public.

Alternative One: QDOT

MarkU.S. Citizen

Unlimited Marital Deduction

AnnaPhilippine Citizen

Resident Alien

For producer use only. Not for distribution to the public.

QDOT

• No immediate estate taxation• Assets “stuck” in U.S.• Distributions limited to income and hardship

OR immediate estate taxation• Need U.S. trustee, may require bond

For producer use only. Not for distribution to the public.

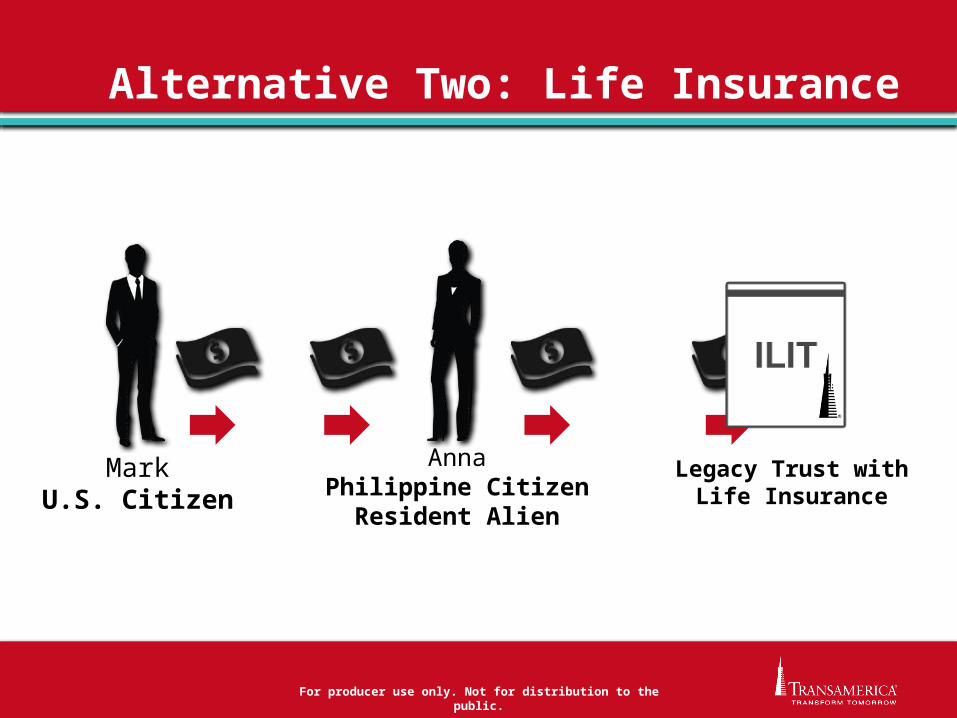

Alternative Two: Life Insurance

Legacy Trust withLife Insurance

MarkU.S. Citizen

AnnaPhilippine Citizen

Resident Alien

For producer use only. Not for distribution to the public.

Why Plan for Foreign Nationals?

• Large, growing demographic• Special financial planning needs• Resident Aliens–

worldwide estate• Non-resident Aliens–

U.S. estate • No unlimited marital

estate deduction

For producer use only. Not for distribution to the public.

Life Insurance

• A simple solution• Internationally competitive

For producer use only. Not for distribution to the public.

Next Steps

• Review your book of business

• Reach out to contacts that match the client profile

• Strengthen and build your referral network

For producer use only. Not for distribution to the public.

Look at your existing business

• Immigrant clients?• Clients with

immigrant spouses?• Develop a

champion client

For producer use only. Not for distribution to the public.

Look at your neighborhood

• Nearby colleges/universities?• Nearby hospitals?• Nearby military bases?• Talk to realty firms for leads• Align with immigration and/or

international tax attorneys and real estate agents catering to foreign national home sales

• Network with ethnic business associations

For producer use only. Not for distribution to the public.

Why Transamerica?

• Dedicated international underwriting team• Established in 1998 – deep understanding of landscape

• Access to experts & marketing materials:• Attorneys and Certified Financial Planners providing

consultative support and case design• Chinese and Spanish language materials

• Foreign Nationals Connection: • Hub for information, sales ideas, and materials & forms • Viewable across mobile, tablet, laptop, and desktop

For producer use only. Not for distribution to the public.

Why Transamerica?

• iPad App• Clear and engaging animations

• Expand market• No product limitations• Guaranteed products available• Very competitive premiums

• Close more business• Best underwriting risk class

generally available

For producer use only. Not for distribution to the public.

Transamerica’s Available Resources

Dedicated International Underwriting Team

iPad App

Foreign National Connection web site

Contact Advanced Marketing

(877) 238-6758

Foreign Nationals Team

Marketing Tools Support

For producer use only. Not for distribution to the public.

This material was not intended or written to be used, and cannot be used, to avoid penalties imposed under the Internal Revenue Code. This material was written to support the promotion or marketing of the products, services, and/or concepts addressed in this material. Anyone to whom this material is promoted, marketed, or recommended should consult with and rely solely on their own independent advisors regarding their particular situation and the concepts presented here.

Transamerica Life Insurance Company (“Transamerica”) and its representatives do not give tax or legal advice. This material is provided for informational purposes only and should not be construed as tax or legal advice. Clients and other interested parties must be urged to consult with and rely solely upon their own independent advisors regarding their particular situation and the concepts presented here.

Discussions of the various planning strategies and issues are based on our understanding of the applicable federal tax laws in effect at the time of presentation. However, tax laws are subject to interpretation and change, and there is no guarantee that the relevant tax authorities will accept Transamerica’s interpretations. Additionally, this material does not consider the impact of applicable state or foreign laws and regulations or income or estate tax treaties between the U.S. and other countries upon clients and prospects. Clients should consult with and rely on their own legal and/or tax advisor to determine the consequences, if any, of owning or receiving proceeds from a Transamerica policy.

Although care is taken in preparing this material and presenting it accurately, Transamerica disclaims any express or implied warranty as to the accuracy of any material contained herein and any liability with respect to it. This information is current as of March 2014.

OLA 2026 0314