for plan sponsor use only. saving : investing : planning for plan sponsor use only advantage october...

TRANSCRIPT

For plan sponsor use only

SAVING : INVESTING : PLANNING

For plan sponsor use only

ADVANTAGE

October 4, 2010

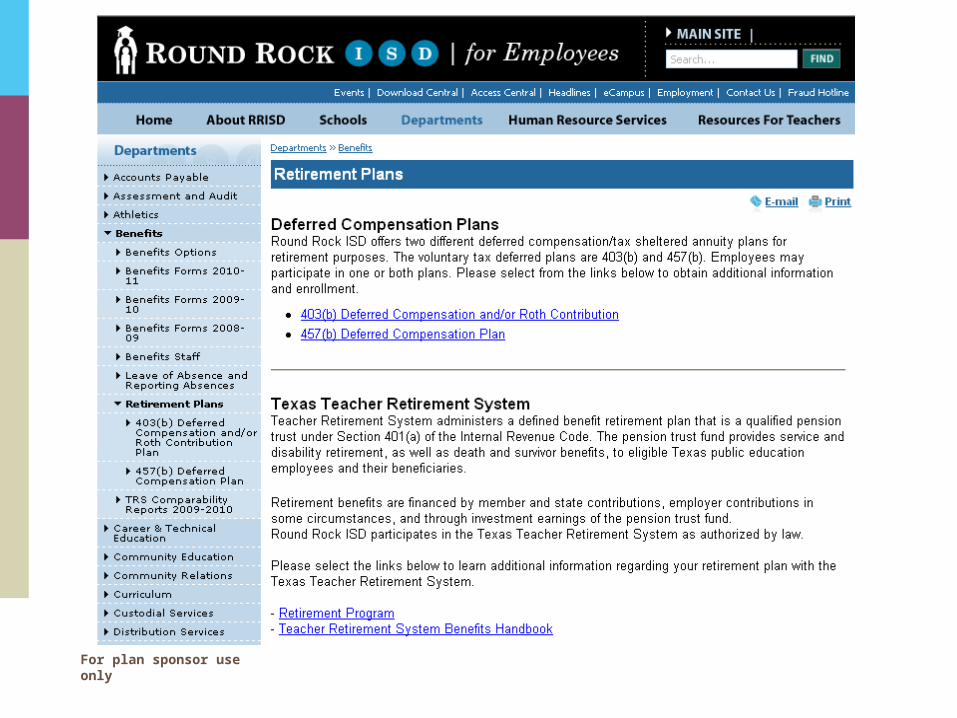

RRISD 457(b) & 403(b) Retirement Plans

For plan sponsor use only

Who can participate in RRISD 403(b) or 457(b) plans?

All Round Rock Employees

No Exceptions

3

For plan sponsor use only

Round Rock ISD employees have a special opportunity – 403(b) or 457(b)>Convenient and smart way to prepare for retirement

>Tax-advantaged plans−Contribute money through pretax payroll deduction−Lowers your taxable income−Might reduce current income taxes

>You decide how to invest contributions

>Taxes on your account’s earnings are deferred until withdrawal−Can accelerate account growth−Taxes must be paid at withdrawal, and federal withdrawal

restrictions apply. You might incur a 10% federal tax penalty if you withdraw funds from your 403(b) account before age 59½.

4

For plan sponsor use only

Important IRS Timelines

>59 ½ - Early Distribution

>70 ½ - RMD

For plan sponsor use only

Employee benefits of a 457(b) & 403(b) tax-qualified accounts> Investment flexibility

>Tax-free loan provisions

>Easy access or convenience

>Go to RRISD Website

6

For plan sponsor use only

How to enroll in RRISD Retirement Plans?

Go to RRISD Website

403(b) – 32 Approved Providers

457(b) – VALIC is RRISD’s Exclusive Provider

For plan sponsor use only

For plan sponsor use only

RRISD 403(b) & 457(b)

>Key Features/Benefits−Accepts External Rollovers−Voluntary−No Open Enrollment−Contributions – Monthly−Pre-Tax−Grows Tax Deferred

For plan sponsor use only

You can participate in the 403(b)/457(b) plans

> Each plan was established to encourage long-term savings

−Vesting — The ownership of money in your account. You are always 100% vested in:• Your own contributions

• Rollover contributions

• Earnings generated by contributions

−Account statement — Active participants receive a quarterly report from your plan provider that documents account activity like contributions and transfers among investment options

−Account consolidation —Transferring vested balances from other retirement plans can simplify personal finances• Promotes suitable diversification among investments

• Could improve consistency with investment preferences

• Important—determine if your other provider’s plan imposes surrender fees

10

For plan sponsor use only

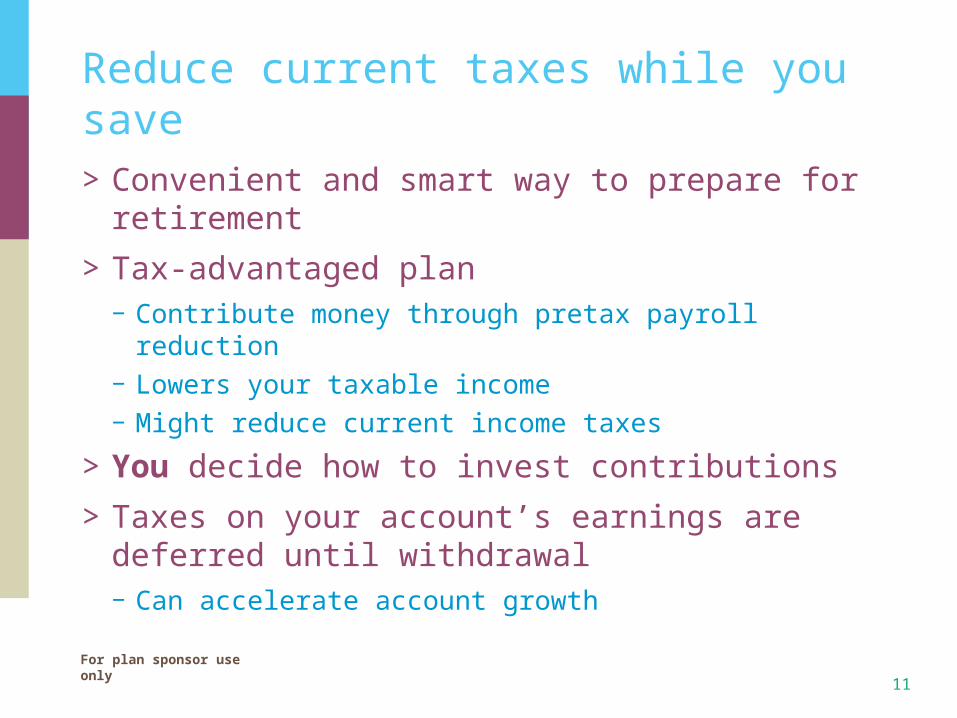

Reduce current taxes while you save

>Convenient and smart way to prepare for retirement

>Tax-advantaged plan−Contribute money through pretax payroll reduction−Lowers your taxable income−Might reduce current income taxes

>You decide how to invest contributions

>Taxes on your account’s earnings are deferred until withdrawal−Can accelerate account growth

11

For plan sponsor use only

RRISD > Comparison: Effect on Paycheck

Without Deferred Contribution

With Deferred Contribution

Monthly Gross Income

Deferred Contribution$500.00

$0.00

$500.00

($25.00)

Taxable Income

Income Taxes Due

$500.00

$125.00

$475.00

$118.75

Net Income $375.00

Difference

$356.25

$18.75

Contribution of $25 only costs individual $18.75

Assumption: Individual is in the 25% tax bracket.

For plan sponsor use only

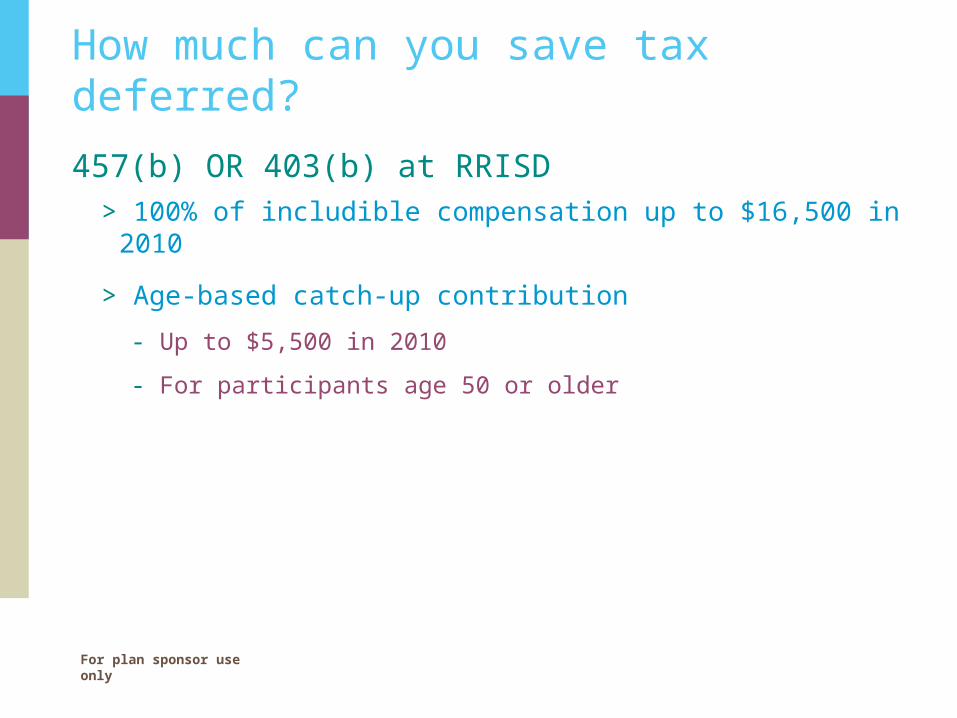

How much can you save tax deferred?

457(b) OR 403(b) at RRISD> 100% of includible compensation up to $16,500 in 2010

> Age-based catch-up contribution

- Up to $5,500 in 2010

- For participants age 50 or older

For plan sponsor use only

Why should I invest in the RRISD 403(b) or 457(b) Retirement Plans?

> Monthly pretax contributions of $100 could grow to more than $95,000 in 25 years!− But your out-of-pocket cost could be just $75 each month

Monthly Contribution

Reduce current tax withholding by

Your out-of-pocket cost

Account Value

5 years 15 years 25 years

$25.00 $6.25 $18.75 $1,850 $8,710 $23,930

$50.00 $12.50 $37.50 $3,698 $17,420 $47,870

$75.00 $18.75 $56.25 $5,550 $26,120 $71,800

$100.00 $25.00 $75.00 $7,395 $34,830 $95,700

Assumptions: (1) 8% Growth

(2) 25% tax bracket

For plan sponsor use only

Enrolling in the RRISD plan is simple

>Go to the RRISD Website

>457(b) OR 403(b)−Just decide your monthly contribution and your portfolio

allocation.−Minimum contribution - $25 monthly

15

For plan sponsor use only

RRISD 457(b) or 403(b) withdrawal provisions

> You can withdraw your vested account balance in the following circumstances:

− Retirement or separation from service

− Your death

− Unforeseeable emergencies

− RMD

For plan sponsor use only

$18,128$24,170

$57,266

$76,352

$141,760

$189,009

This chart compares the hypothetical results of contributing (1) $100 each month to a taxable account and (2) $136.99 (since contributions are pretax) to a tax-qualified retirement investment plan. The chart assumes a 25% federal marginal income tax rate and an 8% annual rate of return. Fees and charges, if applicable, are not reflected in this example and would reduce the amount shown. Income taxes are payable upon withdrawal. Federal restrictions and tax penalties may apply to early withdrawals. This information is hypothetical and only an example. It does not reflect the return of any investment and is not a guarantee of future income.

17

The advantages of a tax-deferred retirement plan

For plan sponsor use only

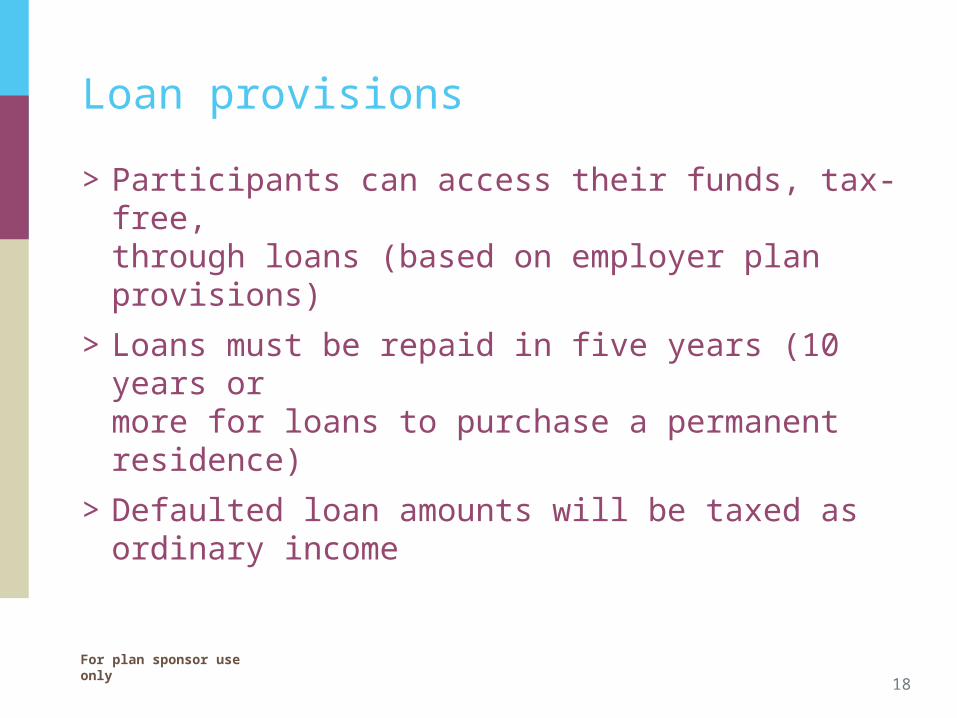

Loan provisions

>Participants can access their funds, tax-free, through loans (based on employer plan provisions)

>Loans must be repaid in five years (10 years or more for loans to purchase a permanent residence)

>Defaulted loan amounts will be taxed as ordinary income

18

For plan sponsor use only

Rollover provisions

>Direct rollovers to or from other tax-qualified plans or an IRA are not taxed

> Indirect rollovers are subject to 20% federal withholding−Rollover must be completed within 60 days−Participant must repay the 20% withholding from

other funds to avoid taxation on the amount withheld−Withdrawals from money rolled in from non-457(b) plans may be

subject to 10% federal early withdrawal penalty if withdrawn from the 457(b) plan prior to attainment of age 59 1/2.

19

For plan sponsor use only

20

Do my investments support all my life goals?

Managing investments in retirement

>Cash

>Bonds

>Stocks

>Mutual funds

>CD’s

>Money Markets

For plan sponsor use only

Diversification

>Stocks

>Bonds

>Cash

For plan sponsor use only

22

Time horizon

>Liquidity

>Distribution method

>Certainty of time to distribution

>Capital preservation or spend down

For plan sponsor use only

23

Neither asset allocation nor diversification ensure a profit or protect against market loss.Source: Markowitz, H. The Journal of Finance, Vol. 7, No. 1. (Mar., 1952), pp. 77-91.

Strategic asset allocation

For plan sponsor use only

Investment Tools

>Reallocation

>Rebalance

>Suitability Factors−Risk−Time Horizon−Age− Investment Experience

For plan sponsor use only

RRISD Retirement Fair

Monday

October 18, 2010

All approved vendors will be present

For plan sponsor use only

For plan sponsor use only

27

Action items Next Steps

Determine risk tolerance and time horizon

Develop an investment strategy

Review annually

RRISD Retirement Fair

>Monday- 10/18/2010

For plan sponsor use only

For plan sponsor use only

Questions and Answers

For plan sponsor use only

Securities and investment advisory services are offered by VALIC Financial Advisors, Inc., member FINRA and an SEC-registered investment advisor.

The information in this presentation is general in nature and may be subject to change. Neither VALIC nor its financial advisors or other representatives give legal or tax advice. Applicable laws and regulations are complex and subject to change. Any tax statements in this material are not intended to suggest the avoidance of U.S. federal, state or local tax penalties. For legal or tax advice concerning your situation consult your attorney or professional tax advisor.

VALIC represents The Variable Annuity Life Insurance Company and its subsidiaries, VALIC Financial Advisors, Inc. and VALIC Retirement Services Company.

Copyright © The Variable Annuity Life Insurance Company.All rights reserved. VC 13847 (12/2009) J75837 ER

SAVING : INVESTING : PLANNING

For plan sponsor use only

THANK YOURRISD 403(b) & 457(b) Retirement Plans