for personal use only merger with tpg - · pdf filemerger with tpg creates one of...

TRANSCRIPT

Merger with TPG

Creates one of Australia’s largest DSLAM footprints and increases earnings per share and

cash flow

8 February 2008For

per

sona

l use

onl

y

2

Acquisition Rationale

• Acquisition of TPG Holdings Limited - a provider of ADSL, ADSL2+ and dial-up services to residential customers and SMEs.

• Immediately earnings per share accretive.

• Combines TPG’s 200,000 customers with Soul’s 500,000-strong customer base.

• TPG’s network adds 238 DSLAMs to Soul network.

• Significant opportunities for capital and operational cost savings.

• Improves cash flow.

• A highly complementary acquisition with substantial opportunities to increase margins through greater use of the SOUL network and the opportunity to take advantage of demand for ADSL2+.For

per

sona

l use

onl

y

3

Acquisition Price

• $150 million in cash

• 270 million shares in SOT

• Enterprise Value of $230 million as at 6 February 2008

• EV/EBITDA forecast multiple of 4.7x

• EV/EBIT forecast multiple of 5.4x

• PE forecast multiple of 8.5x

For

per

sona

l use

onl

y

4

About TPG - Group Structure

TPG Holdings Limited

TPG Network Pty Limited

TPG Internet Pty Limited

Orchid Cybertech Services Inc(Philippines)

Chariot Limited

100% 100% 100% 70%

For

per

sona

l use

onl

y

5

TPG Operations

• Established in 1986 by David Teoh.

• Initially sold computer equipment and network and internet services.

• Sale of computer equipment ceased in December 2005.

• TPG provides ADSL, ADSL2+ and dial-up internet solutions to residential customers and SMEs.

• The internet business, TPG Internet Pty Limited, is the cornerstone of the current business.

• TPG also offers network solutions to corporate customers through TPG Network Pty Limited.For

per

sona

l use

onl

y

6

TPG Operations (continued)

• Orchid Cybertech Services Inc, located in the Philippines, is the call centre operation for the group.

• Previously a reseller of ADSL services, TPG began a strategic investment in DSLAM infrastructure in 2005.

• TPG now owns 238 installed DSLAMs Australia-wide, enabling it to offer ADSL2+ services at reduced cost.

• ADSL2+ services are growing, driven by consumer demand and lower subscriber costs.

• In April 2007, TPG acquired a 70.25% shareholding in listed internet services provider (ISP), Chariot Limited (market capitalisation: $9 million). For

per

sona

l use

onl

y

7

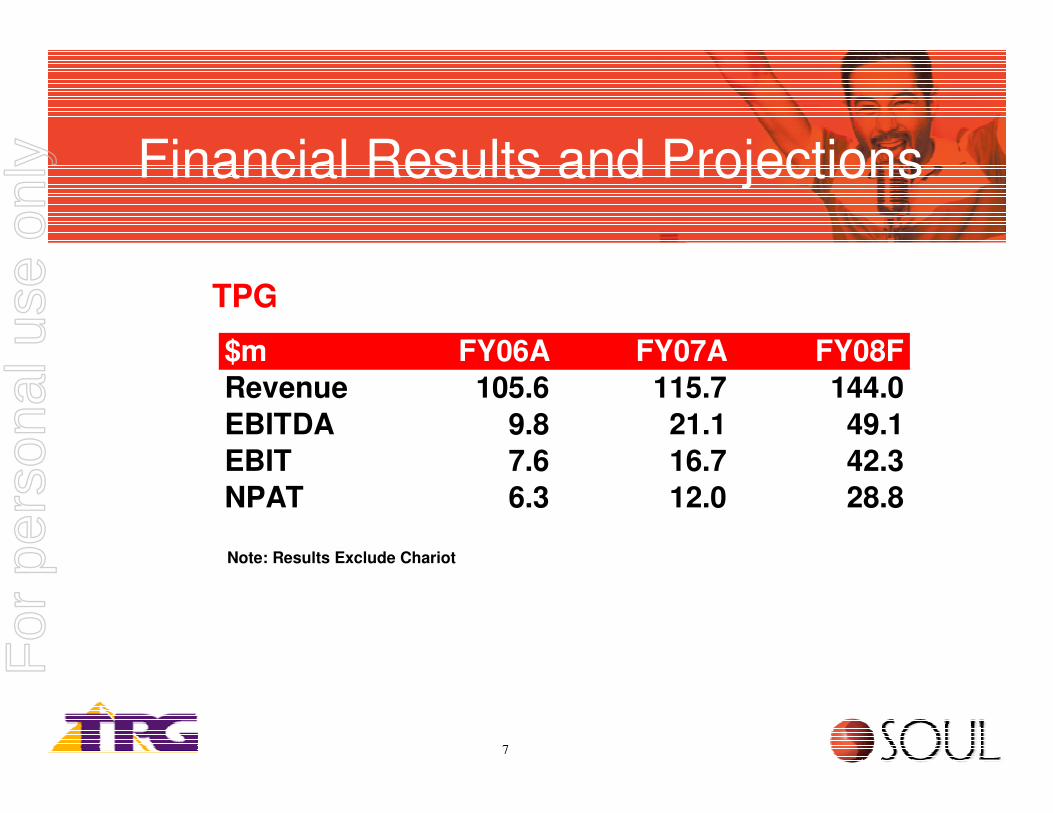

Financial Results and Projections

Note: Results Exclude Chariot

TPG

$m FY06A FY07A FY08F

Revenue 105.6 115.7 144.0

EBITDA 9.8 21.1 49.1

EBIT 7.6 16.7 42.3

NPAT 6.3 12.0 28.8

For

per

sona

l use

onl

y

8

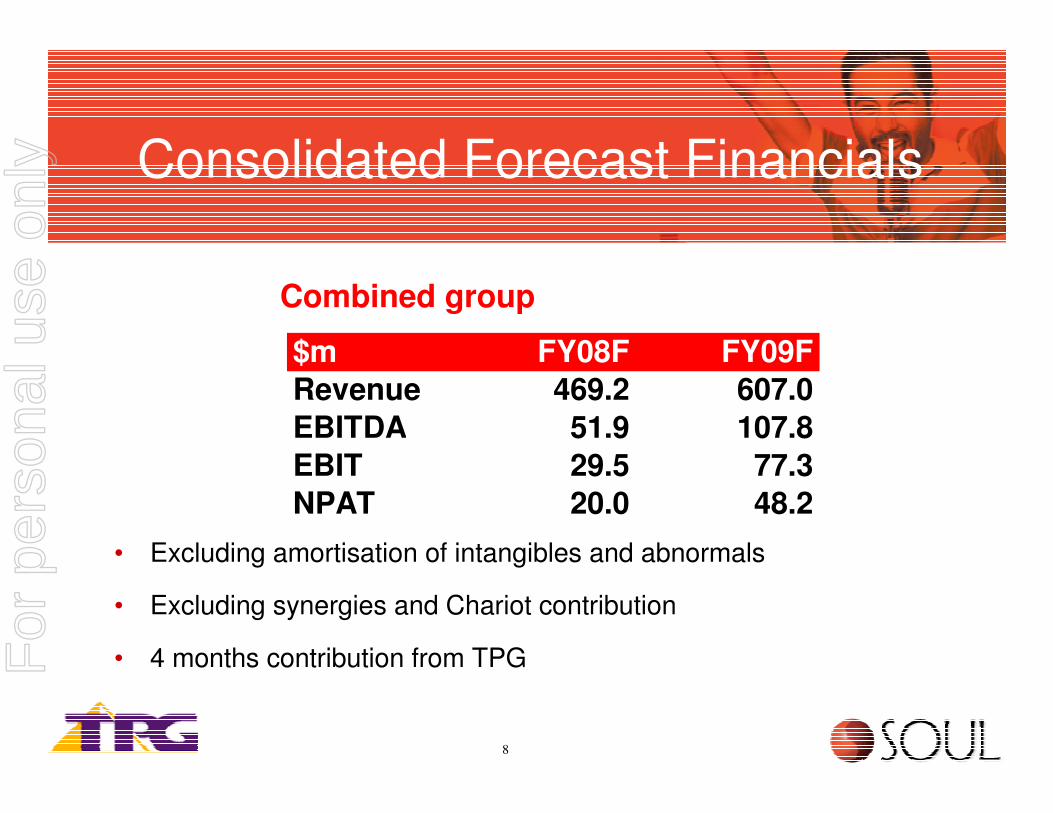

Consolidated Forecast Financials

• Excluding amortisation of intangibles and abnormals

• Excluding synergies and Chariot contribution

• 4 months contribution from TPG

Combined group

$m FY08F FY09F

Revenue 469.2 607.0

EBITDA 51.9 107.8

EBIT 29.5 77.3

NPAT 20.0 48.2

For

per

sona

l use

onl

y

9

Acquisition Accounting Adjustments

• Acquisition may give rise to an intangible asset representing the present value of TPG customer revenue contracts. The estimate used is:

• The final asset value and amortisation will be subject to acquisition accounting confirmation and completion date.

$m FY08F FY09F

Amortisation of customer contracts 9.0 23.7

For

per

sona

l use

onl

y

10

Potential Once-Off Accounting Adjustments

• There will be a number of potential once-off cash and non cash adjustments in FY08 arising from the acquisition:

• Synergy achievement costs.

• Loss of carried forward income tax losses.

• Asset impairment adjustments.

• Once-off transaction costs.

For

per

sona

l use

onl

y

11

Potential Synergies

• The potential to migrate some of the Australian based SOUL activities to the Orchid operations based in the Philippines.

• Rationalisation of rented premises.

• Reduction in overall headcount through elimination of duplicatedpersonnel.

• Migration of SOUL resold services to TPG DSLAM infrastructure. Both Consumer and Business customers.

• Migration of TPG purchased backhaul to SOUL owned or controlled backhaul.

• Consolidation of SOUL and TPG PoPs.

For

per

sona

l use

onl

y

12

Potential Synergies (continued)

• Consolidation of SOUL and TPG purchased backhaul services.

• Migration of SOUL internet bandwidth to TPG.

• The cross-selling of products to current customer base.

• Introduction of SOUL Voice and VoIP capability to the TPG DSLAM infrastructure and customers.

• The implementation of same OSS and BSS systems to provide improved efficiencies to both SOUL and TPG.

• Reduction in capital expenditure on duplicated DSLAM rollout.

• General administrative savings.For

per

sona

l use

onl

y

13

Anticipated Integration Costs

• Costs Arising:

• Universal service obligation applied to TPG revenue.

• Capital expenditure required to interconnect TPG and SOUL networks.

• Cost of achieving synergies.

For

per

sona

l use

onl

y

14

Leading DSLAM Network

• The table below shows competitive exchange coverage.

• The SOT/TPG DSLAM network will be amongst Australia’s largest, enabling the company to take advantage of demand for ADSL2+ services.

• Combining TPG’s DSL network and SOUL’s voice network allows significant bundling and VoIP growth opportunities and greater use of company-owned infrastructure.

95299315303Coverage

NEC/NextepAAPT/Powertel/iiNetOptusTPG/SOULCarrier

For

per

sona

l use

onl

y

15

Indicative Transaction Timetable

Note: timing subject to change

Action Timing

ASX Announcement 7 February

Announce intention to bid for Chariot 7 February

Send Notice of Meeting to SOT Shareholders 3 March

Shareholder Meeting 7 April

Record date for special dividend 17 April

Completion 21 April

Issue Bidder's statement for Chariot 24 April

For

per

sona

l use

onl

y

16

Shareholder Analysis

* Excludes impact of Chariot takeover

Shareholder Pre-transaction Post-transaction

TPG shareholders - 40.0%

WHSP 46.3% 27.7%

WIN television 12.7% 7.6%

Other 53.9% 32.3%

Shares on issue 405.2m 675.2m

For

per

sona

l use

onl

y

17

Management Structure

• At completion the board will comprise five Directors:

• two nominated by TPG

• one nominated by WHSP

• two independent Directors

• David Teoh will assume the role of Executive Chairman after completion.

• Directors will be named prior to completion.

• Overall management team and structure will be announced by the board prior to completion.For

per

sona

l use

onl

y

18

Proposed Chariot Offer

• SOT intends to offer to buy remaining Chariot shares using SOT scrip at a price to be determined by the Independent Expert, if the SOT shareholder vote is successful.

• ASIC has granted a waiver under section 606(1) of the Corporations Act, which stipulates a person must not acquire a relevant interest in a company if the acquisition would result in that person’s voting power in the company increasing from 20% or below to more than 20%.

For

per

sona

l use

onl

y

19

Chariot Synergies

• Synergies achievable from a full acquisition of CTI include:

• Listed company costs

• General administrative savings

• Interest savings on transferred debt

For

per

sona

l use

onl

y

20

Conclusion

• Strategically and financially compelling acquisition.

• SOT/TPG will become one of Australia’s most profitable telcos.

• Owned infrastructure enables provision of all telecommunication products to all sectors (excluding mobile) throughout Australia.

• Greater customer base with opportunities to increase network traffic, bundle and cross-sell products.

• Economies of scale and lower average cost of customer acquisition.

• Strong capacity to participate in further industry consolidation.

• Creates shareholder value - EPS accretive, improved cashflow.

For

per

sona

l use

onl

y