florida orange juice outlook - uf/ifas oci | home · florida orange juice outlook: factors that...

TRANSCRIPT

FLORIDA ORANGEFLORIDA ORANGEJUICE OUTLOOK:JUICE OUTLOOK:

Factors that ImpactFactors that ImpactSustainability of Florida CitrusSustainability of Florida Citrus

www.floridajuice.comwww.floridajuice.com

48th Annual Short Course for the Food IndustryInternational Citrus & Beverage Conference (ICBC)

Sheraton Sand Key ResortClearwater Beach, FL - September 16-19, 2008

Robert P. NorbergDeputy Executive Director of Research & Operations

FLORIDA DEPARTMENT OF CITRUSLakeland, Florida, USA

22

AGENDAAGENDA1. Introduction

2. Sustainability Concepts

3. Factors Impacting Supply-Side

4. Factors Impacting Demand-Side

5. Intersection of Supply & Demand Scenarios

6. Summary & Conclusions

33

INTRODUCTIONINTRODUCTION

4

Production and Tree Losses

► Hurricanes

► Diseases► Canker► Greening► Tristeza

► Development4

CURRENT FLORIDA CURRENT FLORIDA CITRUS SITUATIONCITRUS SITUATION

55

Intent of Presentation isIntent of Presentation isto Understand Factors thatto Understand Factors that

Impact Sustainability ofImpact Sustainability ofthe Florida Citrus Industrythe Florida Citrus Industry

66

SUSTAINABILITYSUSTAINABILITYCONCEPTSCONCEPTS

7

Definition of Definition of ““SustainableSustainable””

A characteristic of a process or state that can be maintained at a certain level indefinitely.

To keep from yielding or failing during stress or difficulty.

Widely used term to describe humans’interaction with earth’s natural ecosystem.

However, can also be used to assess an industry’s struggle to survive challenging times.

7

8

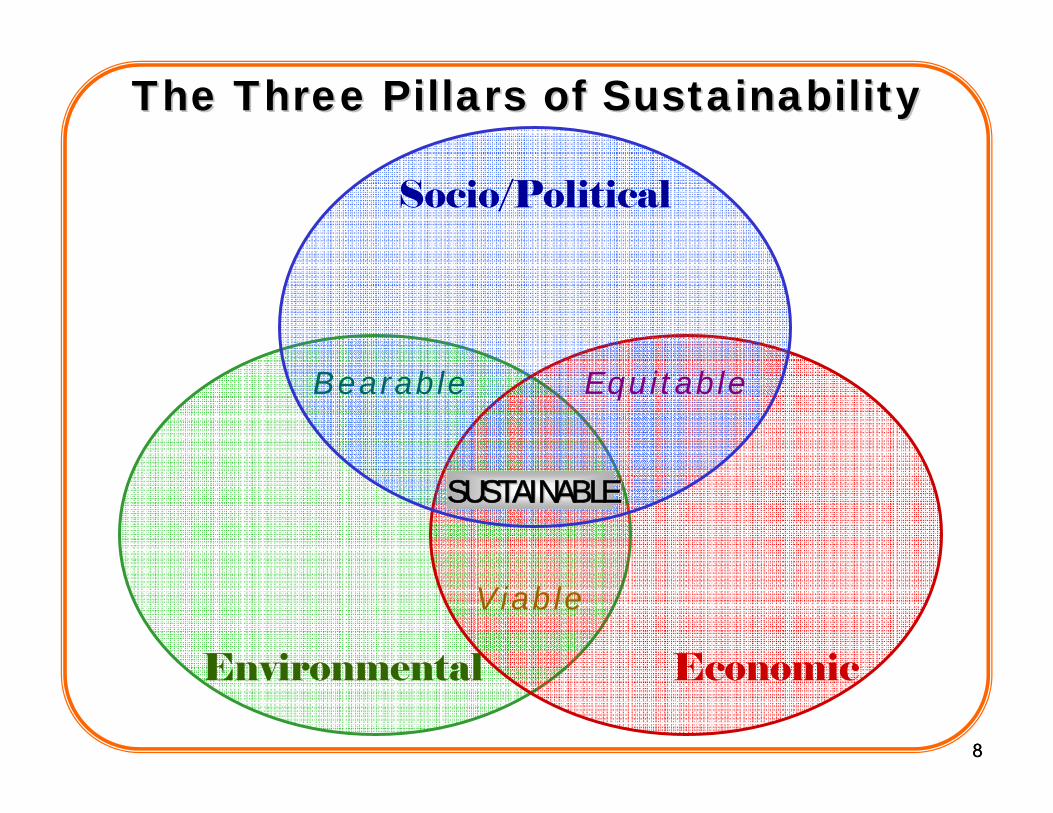

The Three Pillars of SustainabilityThe Three Pillars of Sustainability

8

Environmental Economic

Socio/Political

Bearable

Viable

Equitable

SUSTAINABLESUSTAINABLE

9

Socio/Political SustainabilitySocio/Political Sustainability

PEACE AND SECURITY► Diversions of Resources

POPULATION GROWTH► Migrations► Urbanization► Developed vs. Undeveloped

AFFLUENCE & POVERTY► Inequalities & Disparities

GOVERNANCE► Freedom & Equity

9

10

Environmental SustainabilityEnvironmental Sustainability

PROTECTION OF ECOSYSTEM ► Land, Water, Atmosphere

BIOLOGICAL PRESERVATION & DIVERSITY

PRESERVATION OF VITAL ELEMENTS► Oxygen, Water, Nitrogen, Carbon

TERMINOLOGY► Conservation & Preservation► Pollution Control► Deforestation► Extinction

10

11

Economic SustainabilityEconomic SustainabilityMACRO DEFINITION

► Market Allocation of Diminishing Resources

MICRO DEFINITION► Firm or Industry Level Profitability► Easy Entry or Exit► Transparent Knowledge

EQUILIBRIUM OF LONG-RUN SUPPLY & DEMAND CURVES ABOVE BREAK-EVEN COSTS

11

12

Economic SustainabilityEconomic SustainabilityAgricultural CommoditiesAgricultural Commodities

Quantity

RetailPrice

P1

Sustainable

12

Short-TermSupply Curve

Ps= Break-Even Cost

Unsustainable

Q0

Ps

P2

13

ShortShort--Run Supply & DemandRun Supply & Demand

Quantity

PriceS1 withoutGreening

S2 withGreening

D1

D2

Q2 Q1

14

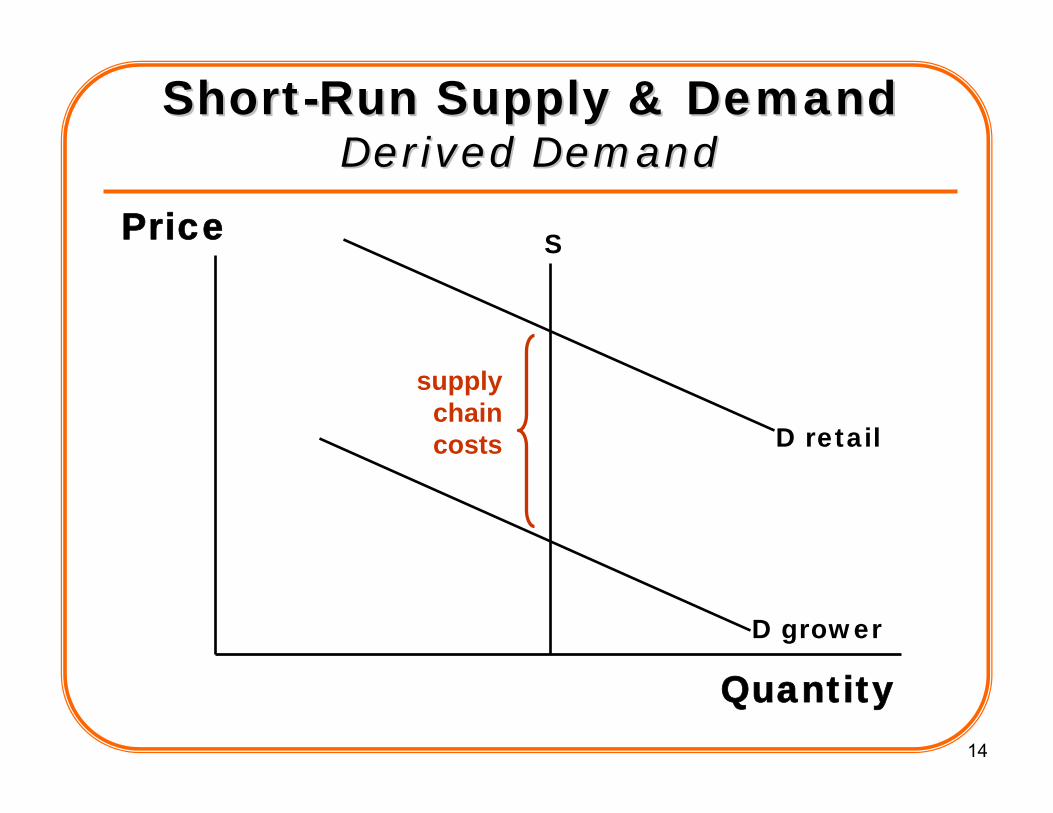

ShortShort--Run Supply & Demand Run Supply & Demand Derived DemandDerived Demand

Quantity

Price S

D retail

D grower

supplychaincosts

15

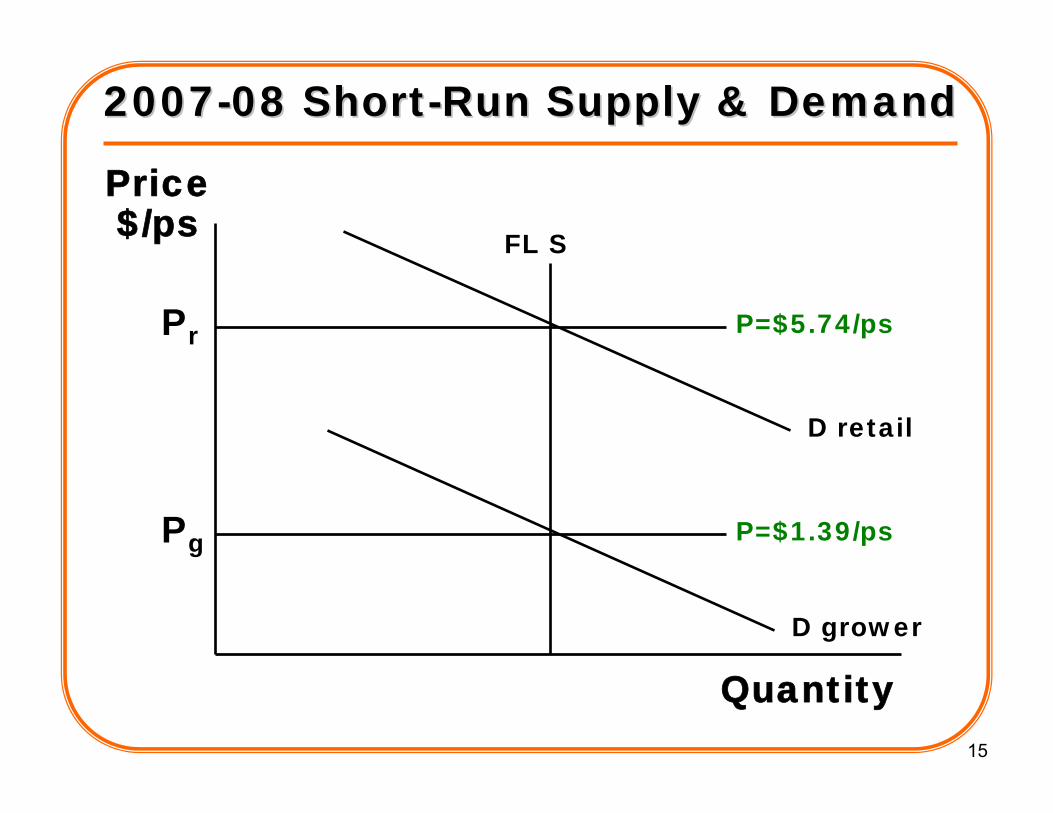

20072007--08 Short08 Short--Run Supply & DemandRun Supply & Demand

Quantity

Price$/ps FL S

D retail

D grower

P=$5.74/ps

P=$1.39/ps

Pr

Pg

16

Quantity

Price$/ps

Theoretical LongTheoretical Long--RunRunOJ Supply CurveOJ Supply Curve

Changes in Inputs

New PlantingsExisting Lands

New PlantingsNew Land

17

Quantity

Price$/ps

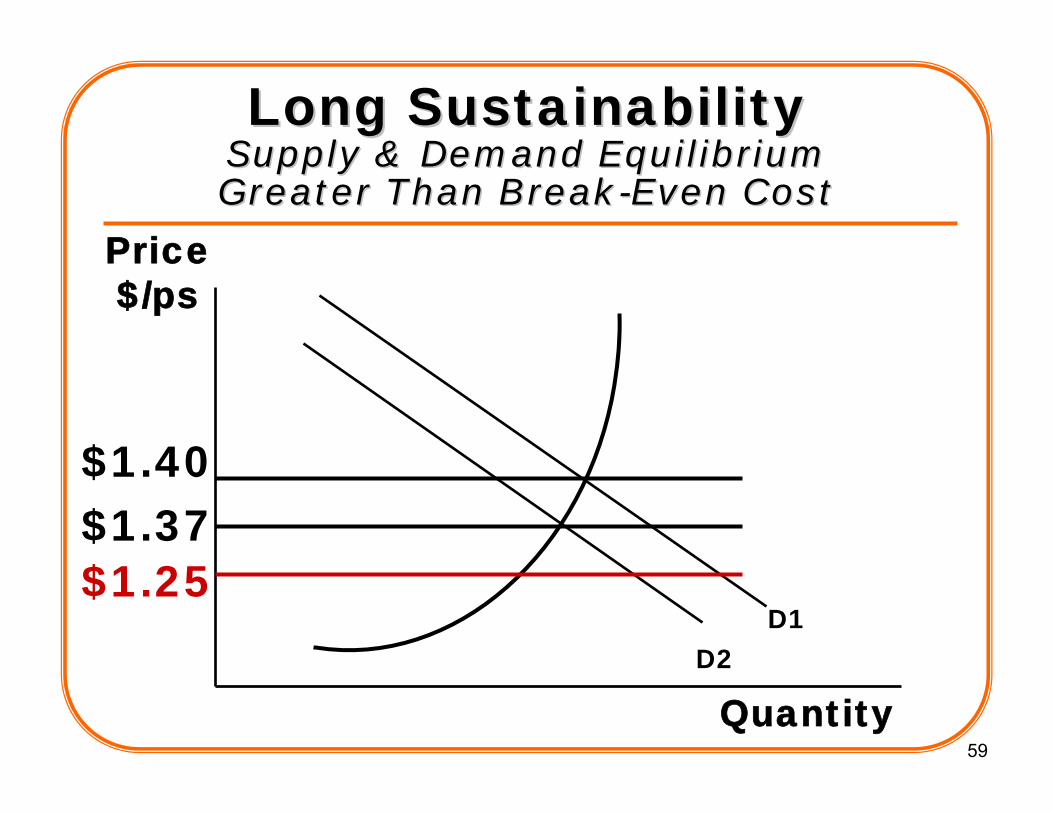

Long SustainabilityLong SustainabilitySupply & Demand EquilibriumSupply & Demand EquilibriumGreater Than BreakGreater Than Break--Even CostEven Cost

D1

Pg

Ps

1818

HistoricalHistoricalSustainabilitySustainability

IndicatorsIndicators

19

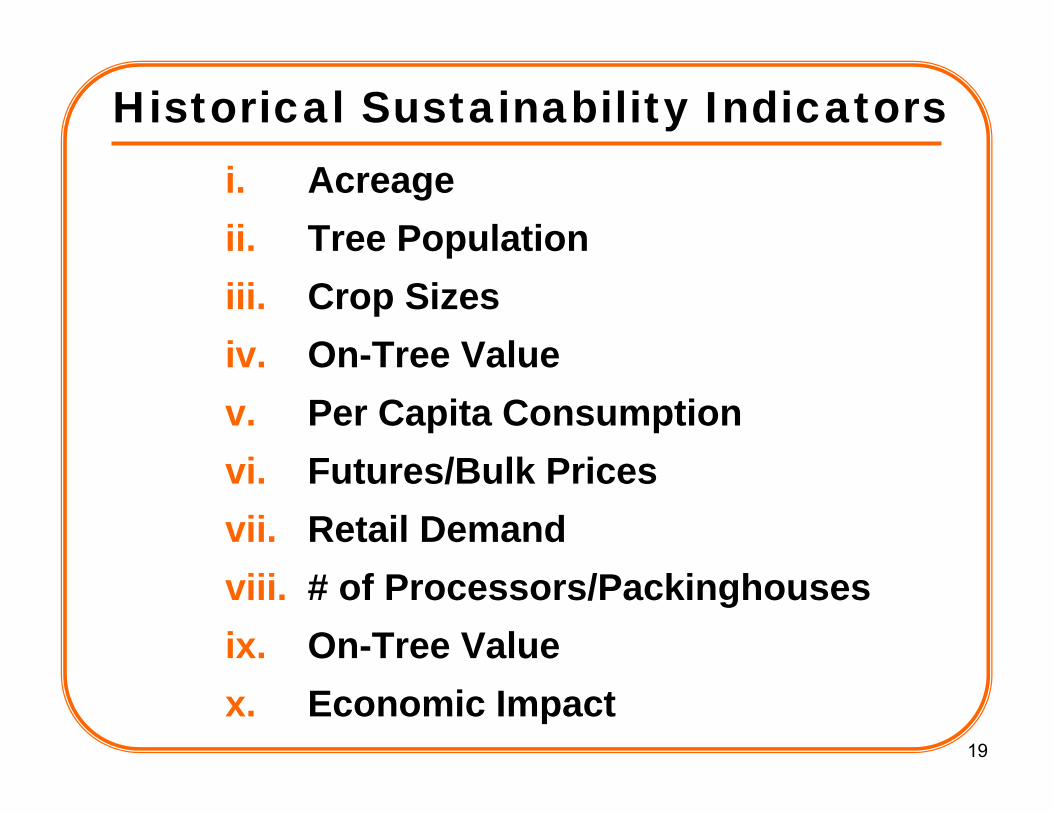

Historical Sustainability Indicatorsi. Acreageii. Tree Populationiii. Crop Sizesiv. On-Tree Valuev. Per Capita Consumptionvi. Futures/Bulk Pricesvii. Retail Demandviii. # of Processors/Packinghousesix. On-Tree Valuex. Economic Impact

Notes and Assumptions

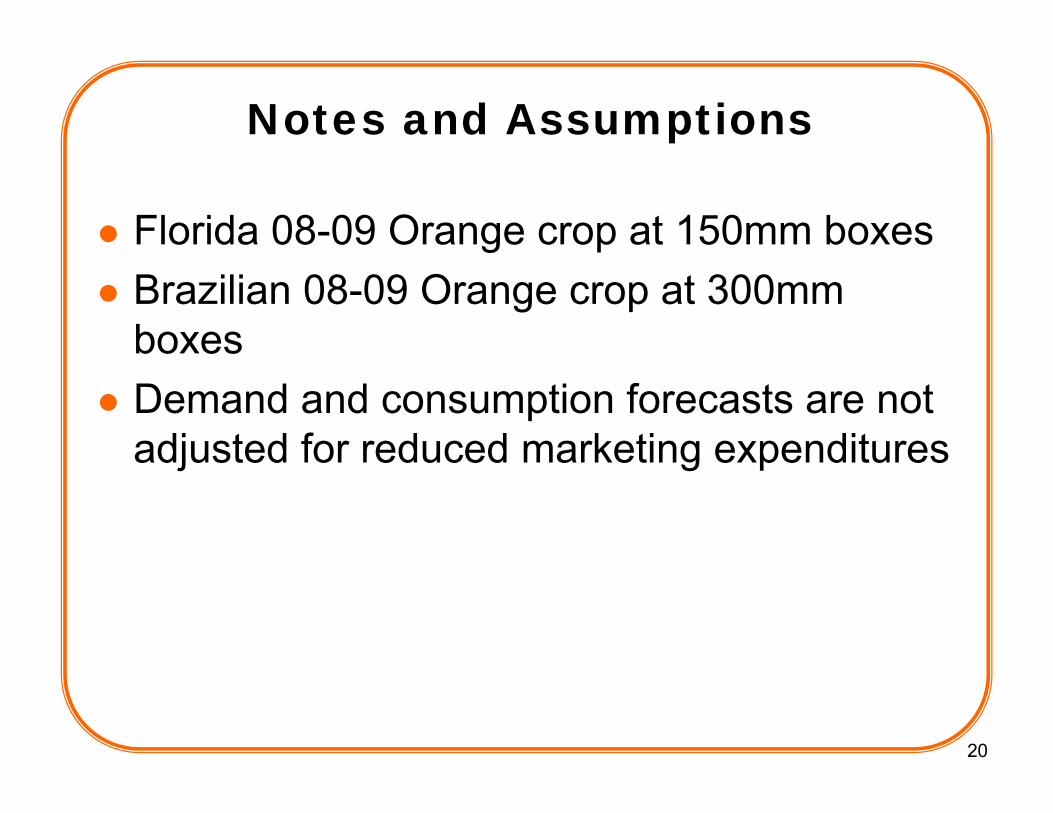

Florida 08-09 Orange crop at 150mm boxes Brazilian 08-09 Orange crop at 300mm boxesDemand and consumption forecasts are not adjusted for reduced marketing expenditures

20

2121

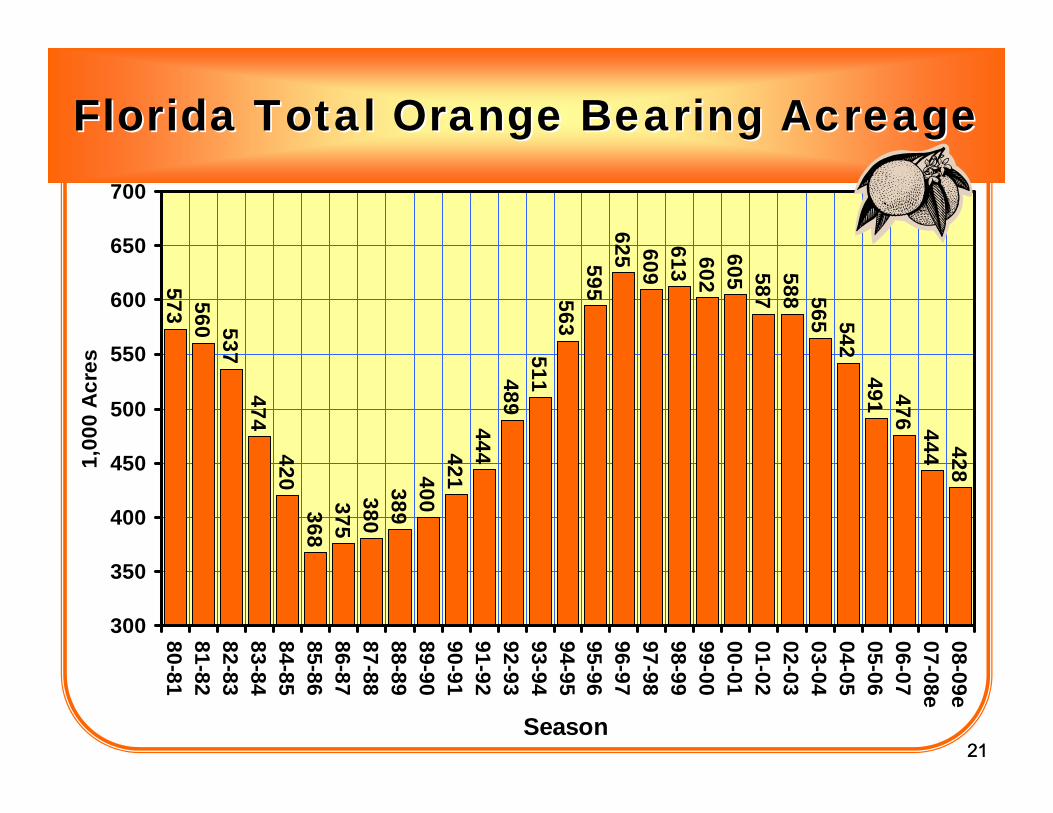

Florida Total Orange Bearing AcreageFlorida Total Orange Bearing Acreage

573 560 537474

420368

375380

389400

421444

489511

563595

625 609613 602605 587

588 565 542491 476 444 428

300

350

400

450

500

550

600

650

700

80-8181-8282-8383-8484-8585-8686-8787-8888-8989-9090-9191-9292-9393-9494-9595-9696-9797-9898-9999-0000-0101-0202-0303-0404-0505-0606-0707-08e08-09e

Season

1,00

0 A

cres

22

53.8

43.5

87.2

64

35

45

55

65

75

85

95

19661968

1970

1972

1974

1976

19781980

1982

1984

1986

1988

19901992

1994

1996

1998

2000

20022004

2006

2008eM

illio

n Tr

ees

Census Year22

SOURCE: USDA-FASS.

Florida Orange Tree PopulationFlorida Orange Tree Population

2323

Florida Total Orange Crop SizesFlorida Total Orange Crop Sizes

172126

140117 104119120

138147

110152 140

187 174206203

226244

186233 223230

203242

150148 129

170150

75

100

125

150

175

200

225

250

275

80-8181-8282-8383-8484-8585-8686-8787-8888-8989-9090-9191-9292-9393-9494-9595-9696-9797-9898-9999-0000-0101-0202-0303-0404-0505-0606-0707-08e08-09e

Season

Mill

ion

Box

es

24

World OJ Per Capita Consumption(SSE Gallons)

Country 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08Estimate

Israel 6.33 7.39 8.54 8.31 8.21 8.19 8.17U.S. 5.12 4.98 5.04 4.76 4.53 4.22 3.96Canada 4.32 4.35 4.18 4.20 4.00 3.79 3.56Australia 3.53 3.28 3.46 3.43 2.91 2.85 2.79E.U. 2.94 3.11 3.41 3.16 2.89 2.40 2.28S. Korea 1.44 1.63 1.40 1.32 1.34 1.19 1.21Japan 1.06 1.06 1.00 1.00 1.01 .98 .98Russia* .26 .36 .44 .45 .54 .55 .55Hong Kong* .36 .38 .32 .31 .31 .32 .32Turkey .30 .30 .32 .32 .31 .31 .30Brazil .12 .14 .15 .17 .21 .23 .25S. Africa .29 .38 .41 .33 .31 .16 .13Morocco .07 .08 .11 .11 .10 .10 .09Mexico .08 .06 .06 .08 .07 .08 .08China .04 .04 .05 .05 .06 .07 .07TOTAL .85 .87 .91 .86 .81 .73 .70

24

Sources: FAS; USDA; FDOC estimates for U.S., Canada & the E.U.; Global Trade Information Services, Inc. (GTI) for other countries.*NOTE: E.U. OJ consumption estimated as (Brazil) ABECitrus exports to the E.U. plus U.S. Dept. of Commerce exports to the E.U. plus USDA estimates of OJ production in Greece, Italy & Spain, plus GTI based estimates of OJ imports from other countries besides Brazil and the U.S.

minus GTI based estimates of E.U. exports.

25

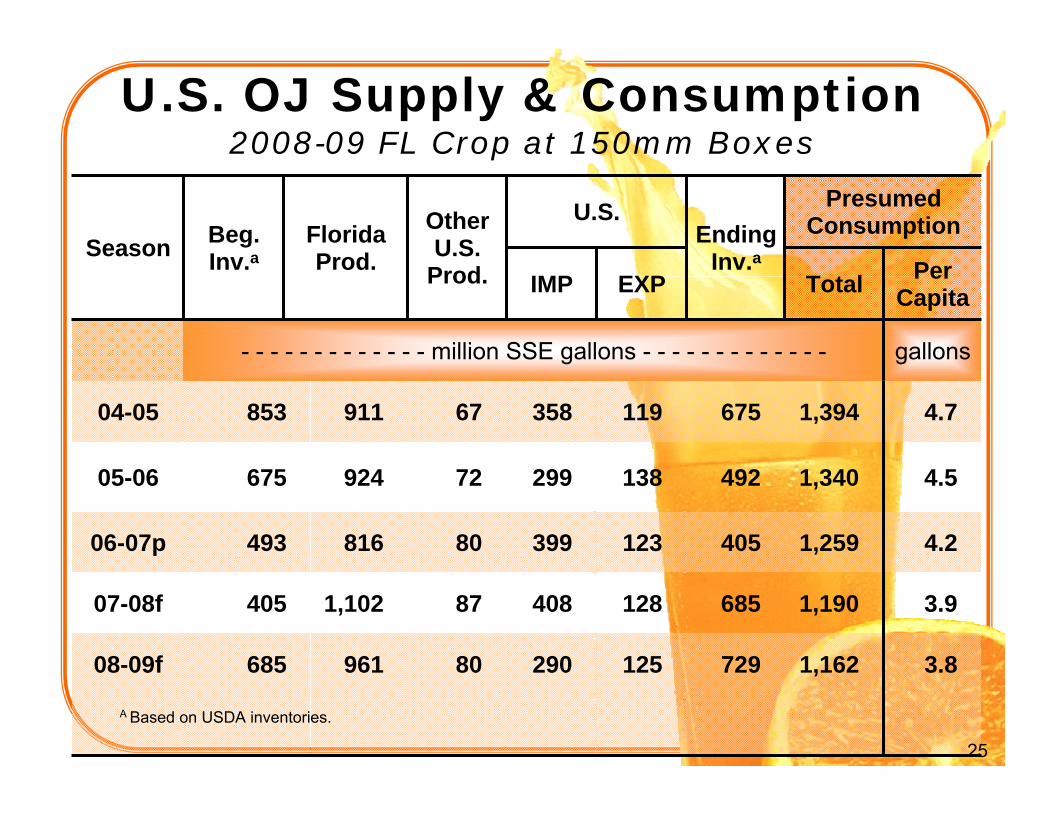

U.S. OJ Supply & Consumption2008-09 FL Crop at 150mm Boxes

Season Beg.Inv.a

FloridaProd.

OtherU.S.

Prod.

U.S.Ending

Inv.a

PresumedConsumption

IMP EXP Total PerCapita

- - - - - - - - - - - - - million SSE gallons - - - - - - - - - - - - - gallons

04-05 853 911 67 358 119 675 1,394 4.7

05-06 675 924 72 299 138 492 1,340 4.5

06-07p 493 816 80 399 123 405 1,259 4.2

07-08f 405 1,102 87 408 128 685 1,190 3.9

08-09f 685 961 80 290 125 729 1,162 3.8

25

A Based on USDA inventories.

2626

0.50

0.70

0.90

1.10

1.30

1.50

1.70

1.90

2.10

2.30

350

650

950

1,250

1,550

1,850

2,150

2,450

2,750

3,050A

ug

-99

Dec

-99

Ap

r-0

0A

ug

-00

Dec

-00

Ap

r-0

1A

ug

-01

Dec

-01

Ap

r-0

2A

ug

-02

Dec

-02

Ap

r-0

3A

ug

-03

Dec

-03

Ap

r-0

4A

ug

-04

Dec

-04

Ap

r-0

5A

ug

-05

Dec

-05

Ap

r-0

6A

ug

-06

Dec

-06

Ap

r-0

7A

ug

-07

Dec

-07

Ap

r-0

8A

ug

-08

$/PS (Futures &

Bulk)

$/M

T (R

ott

erda

m)

Month Average

Rotterdam Futures Bulk FOB

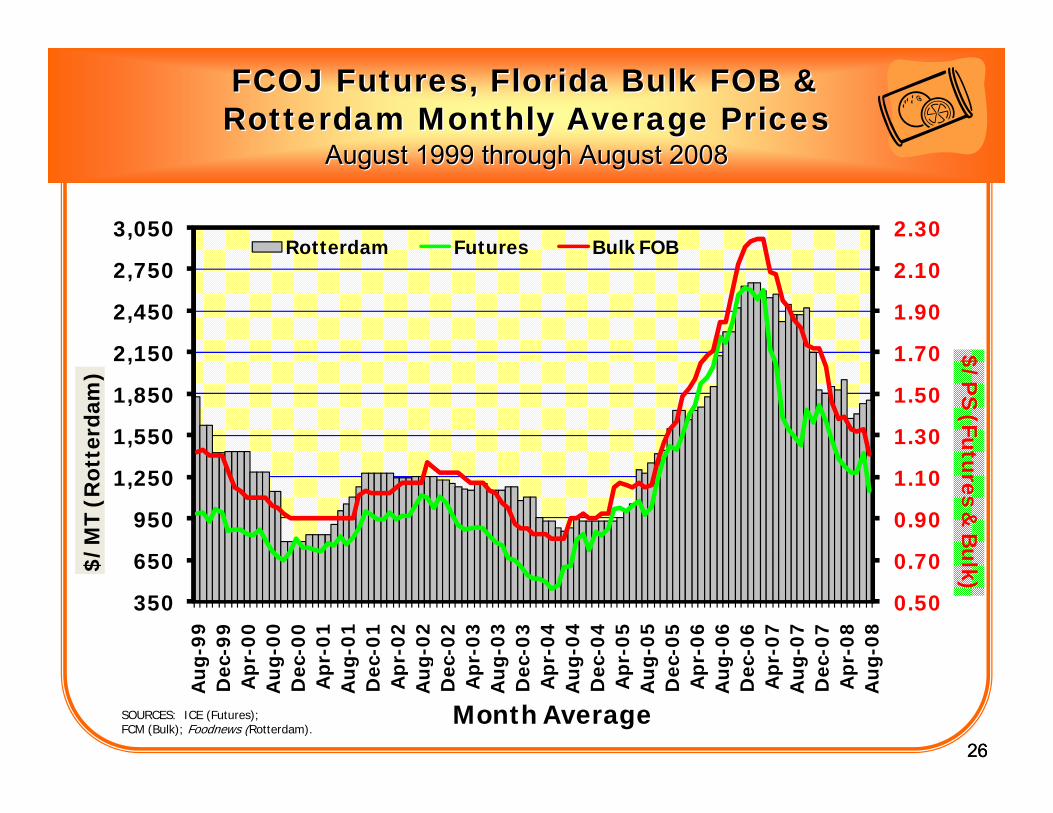

SOURCES: ICE (Futures);FCM (Bulk); Foodnews (Rotterdam).

FCOJ Futures, Florida Bulk FOB &FCOJ Futures, Florida Bulk FOB &Rotterdam Monthly Average PricesRotterdam Monthly Average Prices

August 1999 through August 2008August 1999 through August 2008

27

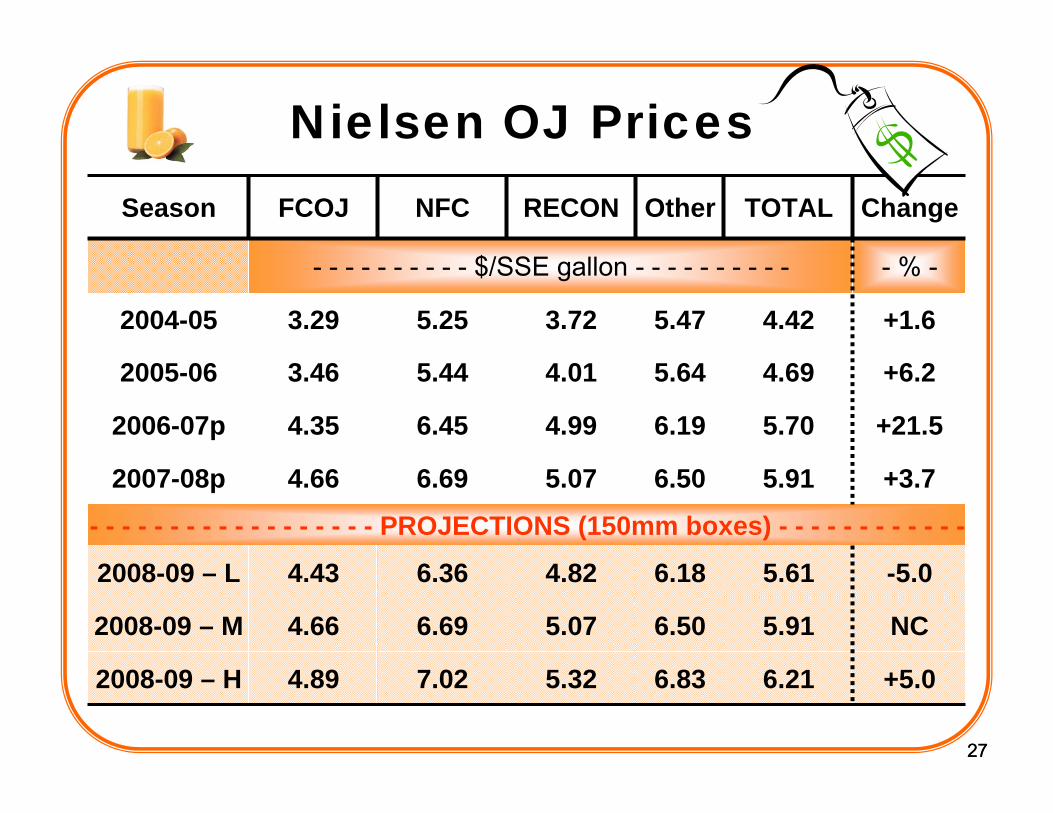

Nielsen OJ PricesSeason FCOJ NFC RECON Other TOTAL Change

- - - - - - - - - - $/SSE gallon - - - - - - - - - - - % -

2004-05 3.29 5.25 3.72 5.47 4.42 +1.6

2005-06 3.46 5.44 4.01 5.64 4.69 +6.2

2006-07p 4.35 6.45 4.99 6.19 5.70 +21.5

2007-08p 4.66 6.69 5.07 6.50 5.91 +3.7

- - - - - - - - - - - - - - - - - - PROJECTIONS (150mm boxes) - - - - - - - - - - - -

2008-09 – L 4.43 6.36 4.82 6.18 5.61 -5.0

2008-09 – M 4.66 6.69 5.07 6.50 5.91 NC

2008-09 – H 4.89 7.02 5.32 6.83 6.21 +5.0

27

28

Nielsen OJ VolumeSeason FCOJ NFC RECON Other TOTAL Change

- - - - - - - - - - million SSE gallons - - - - - - - - - - - % -

2004-05 70.1 374.7 343.8 6.7 795.3 -1.5

2005-06 62.3 373.5 303.6 5.9 745.3 -6.3

2006-07p 54.8 337.9 252.7 5.5 650.8 -12.7

2007-08p 49.4 328.0 240.0 5.5 623.0 -4.3

- - - - - - - - - - - - - - - - - - PROJECTIONS (150mm boxes) - - - - - - - - - - - -

2008-09 – L 44.9 311.5 223.1 5.2 586.7 -5.8

2008-09 – M 46.5 322.3 232.9 5.4 607.1 -2.6

2008-09 – H 48.2 334.1 241.4 5.6 629.3 +1.0

28

29

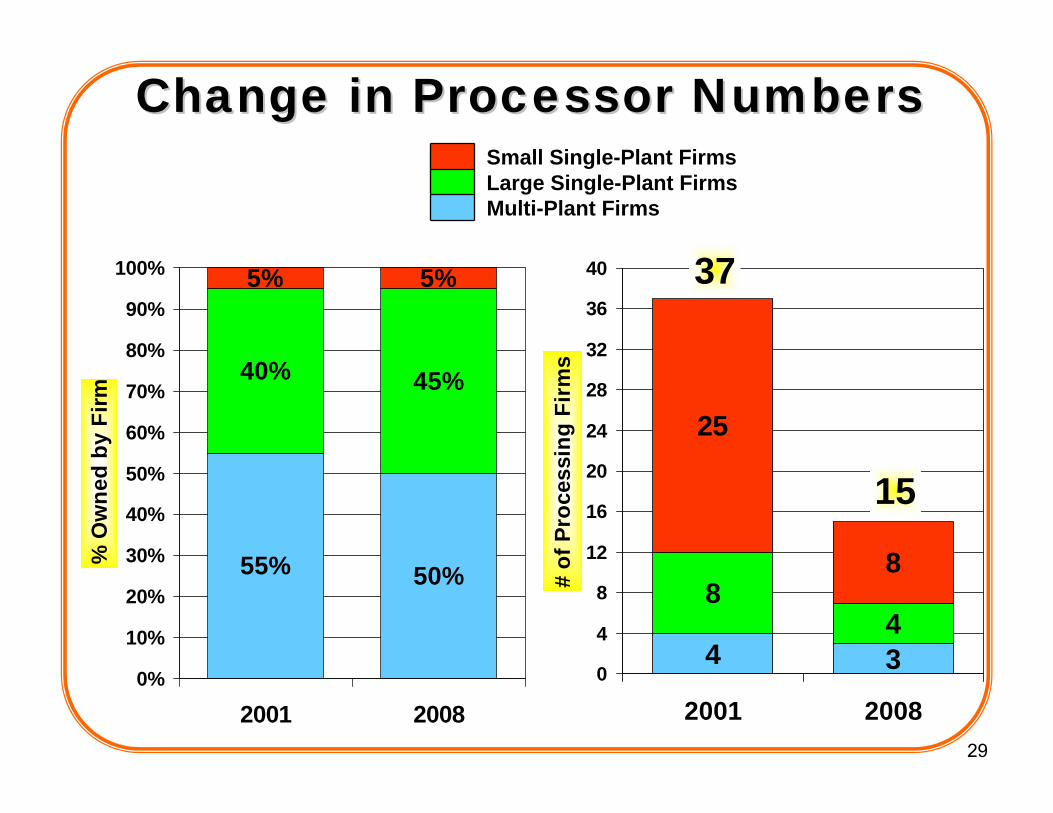

Change in Processor NumbersChange in Processor Numbers

55% 50%

40% 45%

5% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2008

% O

wne

d by

Firm

4 3

84

25

8

0

4

8

12

16

20

24

28

32

36

40

2001 2008

# of

Pro

cess

ing

Firm

s

Small Single-Plant FirmsLarge Single-Plant FirmsMulti-Plant Firms

37

15

30

Change in Packinghouse NumbersChange in Packinghouse Numbers

19%9%

76%86%

5% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2008

% O

wne

d by

Firm

6 1

4030

51

19

0

10

20

30

40

50

60

70

80

90

100

2001 2008

# of

Pac

king

hous

e Fi

rms

Small Single-Plant FirmsLarge Single-Plant FirmsMulti-Plant Firms

97

50

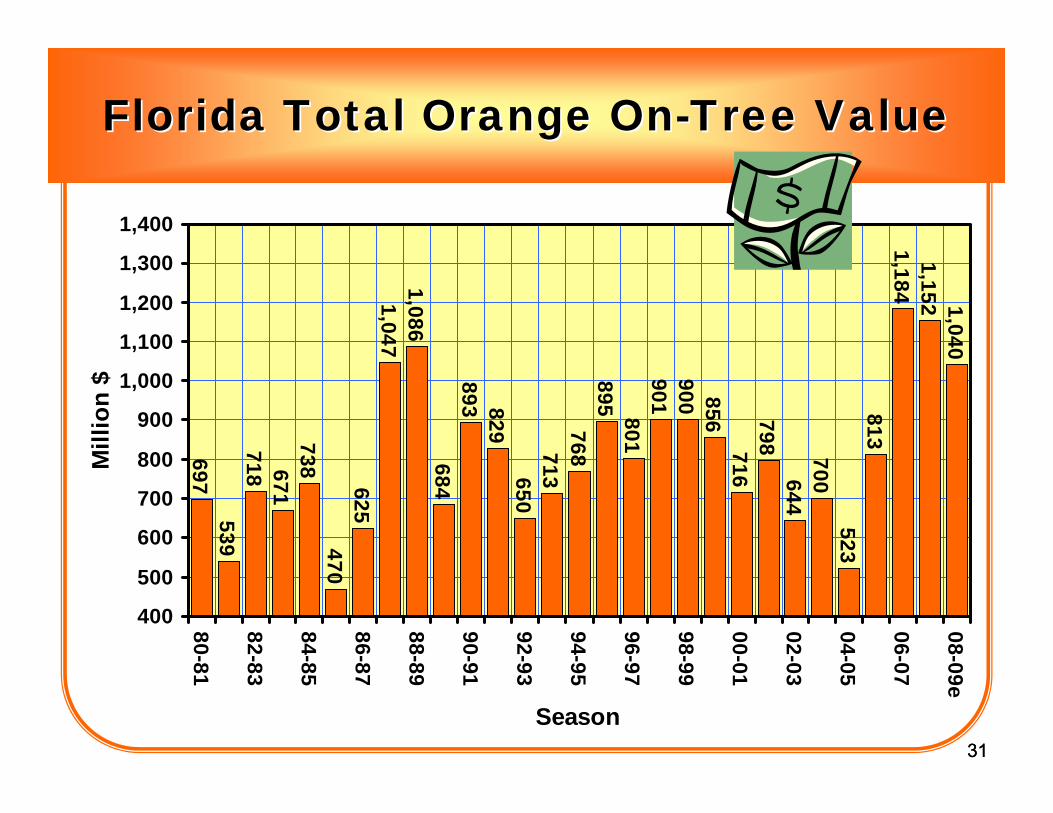

3131

Florida Total Orange OnFlorida Total Orange On--Tree ValueTree Value

697539

718 671738

470625

1,0471,086

684893 829

650713

768895 801901900 856

716798

644700

523813

1,1841,152 1,040

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

80-81

82-83

84-85

86-87

88-89

90-91

92-93

94-95

96-97

98-99

00-01

02-03

04-05

06-07

08-09e

Season

Mill

ion

$

2006 Economic Impact2006 Economic Impact

$9.3+ Billion$9.3+ BillionOver 500,000 Acres

Nearly 80,000 Jobs

3333

What factors willWhat factors willinfluence theseinfluence these

indicators inindicators inthe future?the future?

3434

FACTORSFACTORSIMPACTINGIMPACTING

SUPPLYSUPPLY--SIDESIDE

35

Quantity

Price$/ps

LongLong--Run Supply CurveRun Supply Curve

3636

FACTORSFACTORSIMPACTINGIMPACTING

DEMANDDEMAND--SIDESIDE

37

Factors That Impact OJ DemandFactors That Impact OJ DemandPRICING

► Own- & Cross-Price Effects

PROMOTION► Features, Display & TPR

ADVERTISING► Generic & Branded

INCOMES► Real Per Capita Incomes

INFLATION37

38

Shifts in Demand CurvesShifts in Demand Curves

Quantity

Price

D1

D2

39

20072007--08 Supply and Demand Equilibrium08 Supply and Demand EquilibriumDerived Demand for FruitDerived Demand for Fruit

Quantity

Price$/ps FL S

D retail

D grower

P=$5.74/ps

P=$1.39/ps

Pr

Pg

supplychaincosts

4040

PricingPricing

41

4.33 4.37 4.39 4.40 4.35 4.424.69

5.705.91

5.615.91

6.21

4.00

4.50

5.00

5.50

6.00

6.50

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09e

Season

$ pe

r SS

E ga

llon

Retail OJ Price

4242

Per CapitaPer CapitaIncomeIncome

43

Per Capita DisposablePersonal Income

Year Nominal Real(2008 dollars)

Change- - - - - $1,000 - - - - - - - % - -

2000 25.5 31.9 2.82001 26.3 31.9 .22002 27.2 32.5 2.02003 28.1 32.9 1.02004 29.6 33.7 2.62005 30.7 33.9 .42006 32.2 34.4 1.62007 33.7 35.0 1.82008e 35.3 35.3 .82009e 36.1 34.3 -2.0

4444

InflationInflation

45

3.4%

2.8%2.3%

2.7%

3.4%3.2%

3.8%

2.8%

1.6%

5.0%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

2000 2001 2002 2003 2004 2005 2006 2007 2008e 2009e

Year

% C

hang

eConsumer Price Index

4646

Competitive /Competitive /SubstituteSubstituteProductsProducts

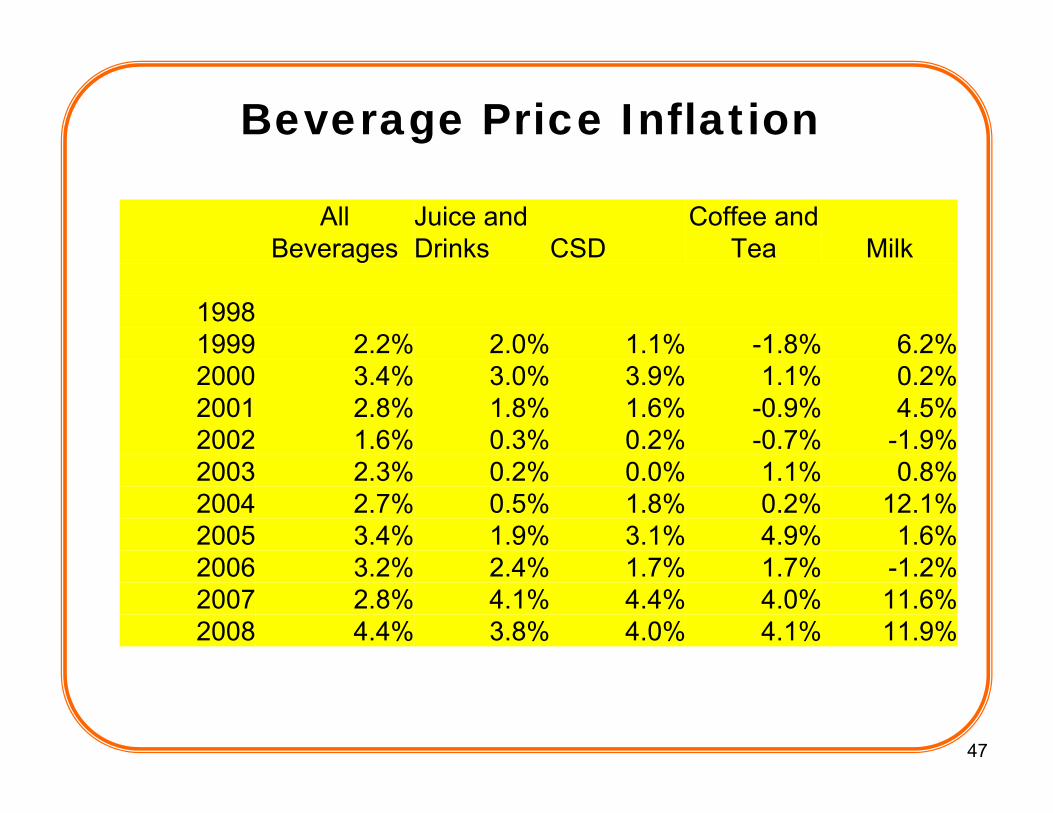

Beverage Price Inflation

47

All Beverages

Juice and Drinks CSD

Coffee and Tea Milk

19981999 2.2% 2.0% 1.1% -1.8% 6.2%2000 3.4% 3.0% 3.9% 1.1% 0.2%2001 2.8% 1.8% 1.6% -0.9% 4.5%2002 1.6% 0.3% 0.2% -0.7% -1.9%2003 2.3% 0.2% 0.0% 1.1% 0.8%2004 2.7% 0.5% 1.8% 0.2% 12.1%2005 3.4% 1.9% 3.1% 4.9% 1.6%2006 3.2% 2.4% 1.7% 1.7% -1.2%2007 2.8% 4.1% 4.4% 4.0% 11.6%2008 4.4% 3.8% 4.0% 4.1% 11.9%

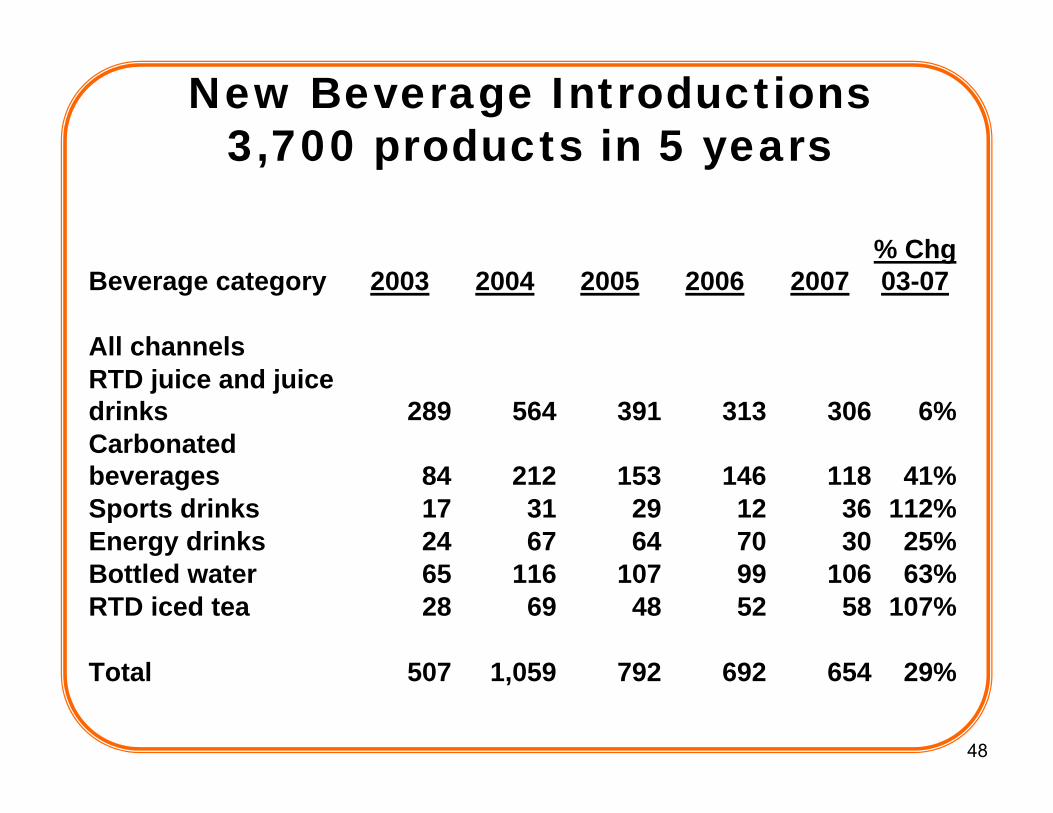

New Beverage Introductions3,700 products in 5 years

48

Beverage category 2003 2004 2005 2006 2007% Chg 03-07

All channelsRTD juice and juice drinks 289 564 391 313 306 6%Carbonated beverages 84 212 153 146 118 41%Sports drinks 17 31 29 12 36 112%Energy drinks 24 67 64 70 30 25%Bottled water 65 116 107 99 106 63%RTD iced tea 28 69 48 52 58 107%

Total 507 1,059 792 692 654 29%

4949

PromotionPromotion

50

Percent ACV with A/B Ad ActivityPercent ACV with A/B Ad ActivityTotal OJTotal OJ

50

5151

MARKETINGMARKETINGGenericGenericBrandBrand

52

Total FDOC vs. BrandTelevision Advertising

17.8 18.2 19.122.1

15.812.0 13.3

9.0

37.632.9

14.517.0

14.5

47.6

55.055.0

$0

$10

$20

$30

$40

$50

$60

01-02 02-03 03-04 04-05 05-06 06-07 07-08 08-09f

Fiscal Year

Mill

ion

Dol

lars

FDOC Brand

5353

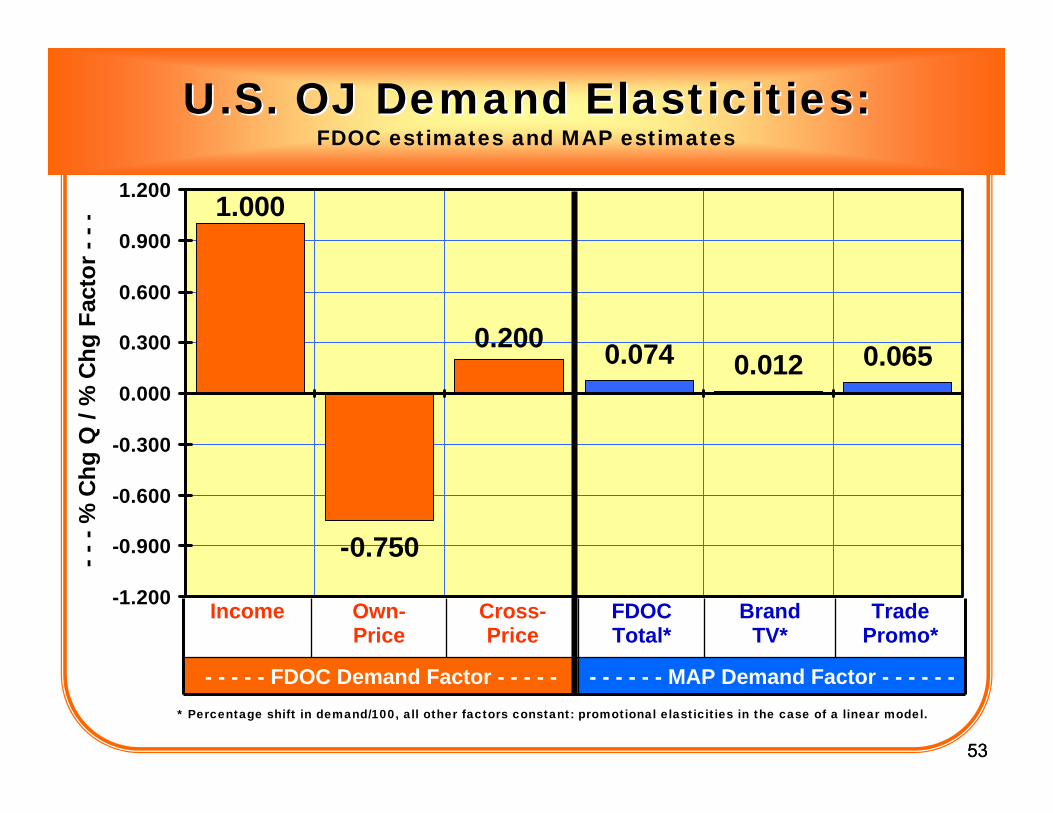

-0.750

0.074 0.012 0.065

1.000

0.200

-1.200

-0.900

-0.600

-0.300

0.000

0.300

0.600

0.900

1.200

Income Ow n-Price Cross-Price FDOC Total (3) Generic Brand TV (3) Brand Trade Promo (3)

- - -

% C

hg Q

/ %

Chg

Fac

tor -

- -

* Percentage shift in demand/100, all other factors constant: promotional elasticities in the case of a linear model.

U.S. OJ Demand Elasticities:U.S. OJ Demand Elasticities:FDOC estimates and MAP estimates

Income Own-Price

Cross-Price

FDOCTotal*

BrandTV*

TradePromo*

- - - - - FDOC Demand Factor - - - - - - - - - - - MAP Demand Factor - - - - - -

5454

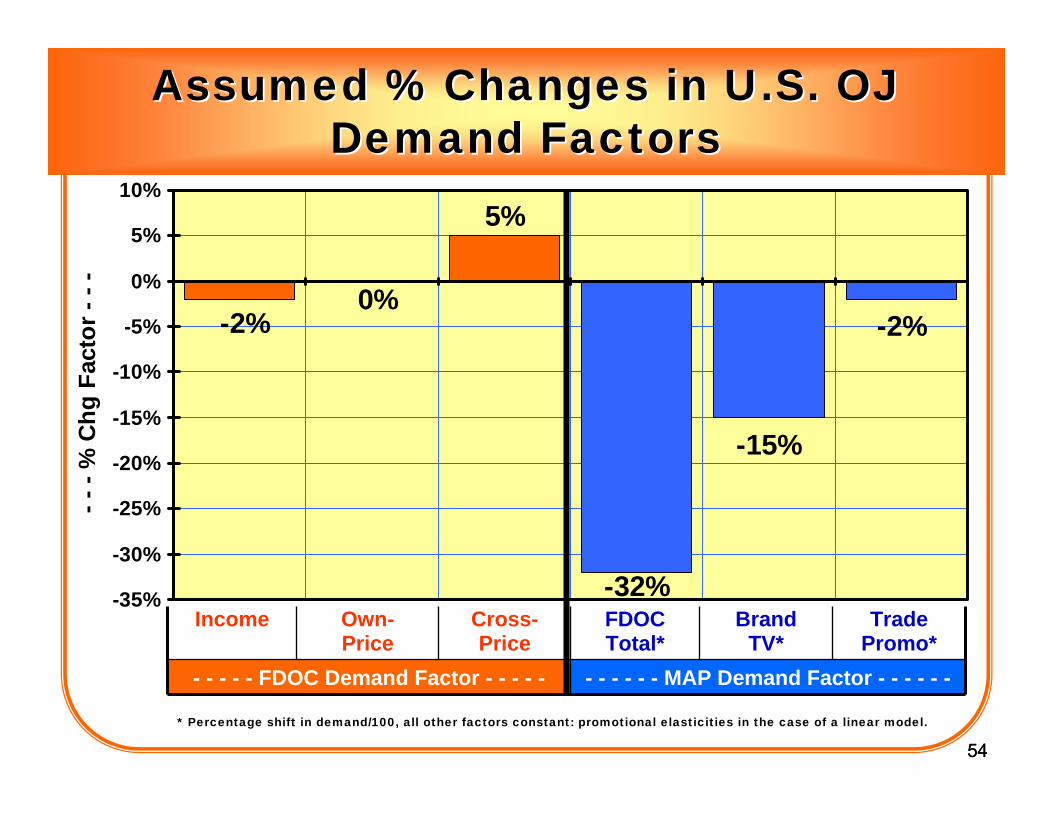

-15%

-2%

-32%

-2%0%

5%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Income Ow n-Price Cross-Price FDOC Total (3) Generic Brand TV (3) Brand Trade Promo (3)

- - -

% C

hg F

acto

r - -

-Assumed % Changes in U.S. OJ Assumed % Changes in U.S. OJ

Demand FactorsDemand Factors

Income Own-Price

Cross-Price

FDOCTotal*

BrandTV*

TradePromo*

- - - - - FDOC Demand Factor - - - - - - - - - - - MAP Demand Factor - - - - - -

* Percentage shift in demand/100, all other factors constant: promotional elasticities in the case of a linear model.

5555

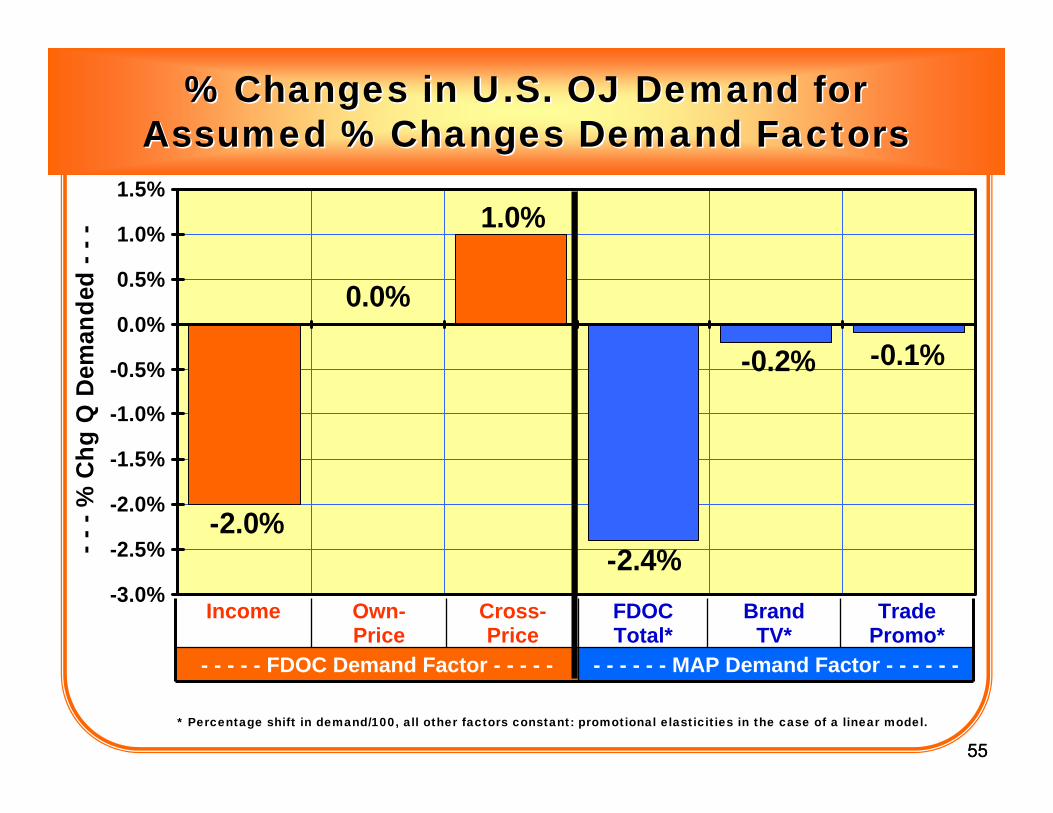

0.0%

-0.1%-0.2%

-2.4%-2.0%

1.0%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

Income Ow n-Price Cross-Price FDOC Total (3) Generic Brand TV (3) Brand Trade Promo (3)

- - -

% C

hg Q

Dem

ande

d - -

-% Changes in U.S. OJ Demand for% Changes in U.S. OJ Demand for

Assumed % Changes Demand FactorsAssumed % Changes Demand Factors

Income Own-Price

Cross-Price

FDOCTotal*

BrandTV*

TradePromo*

- - - - - FDOC Demand Factor - - - - - - - - - - - MAP Demand Factor - - - - - -

* Percentage shift in demand/100, all other factors constant: promotional elasticities in the case of a linear model.

5656

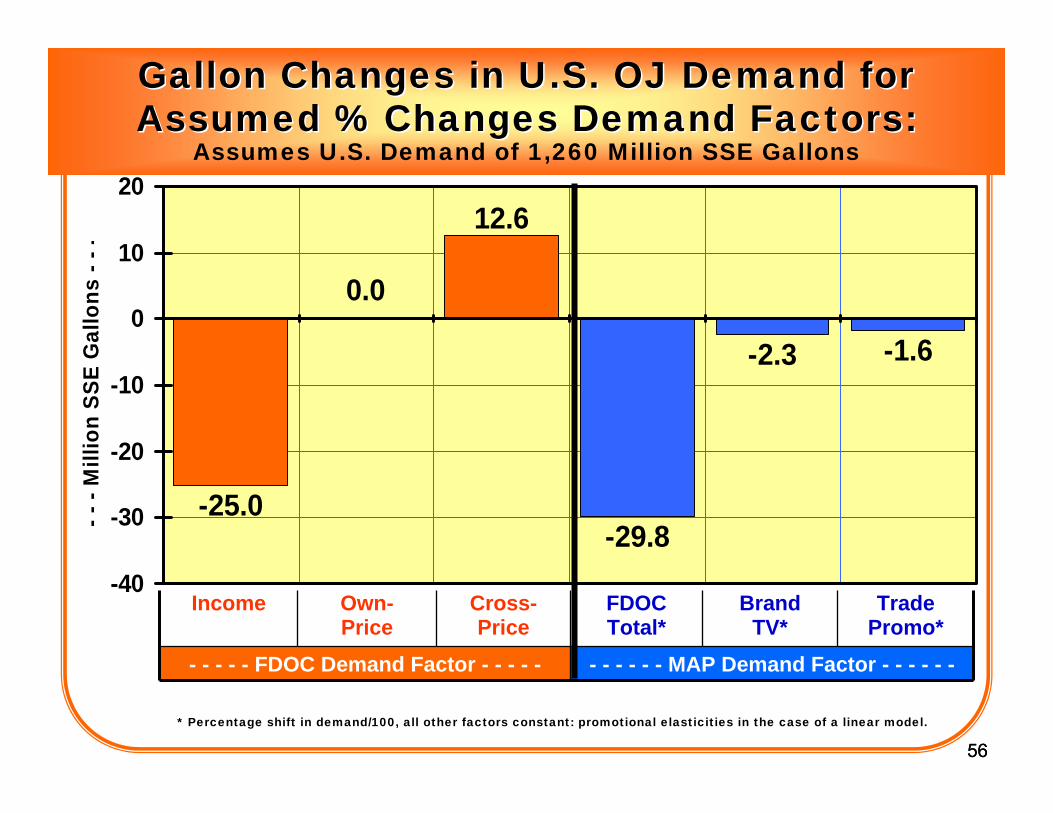

0.0

-1.6-2.3

-29.8-25.0

12.6

-40

-30

-20

-10

0

10

20

Income Ow n-Price Cross-Price FDOC Total (3) Generic Brand TV (3) Brand Trade Promo (3)

- - -

Mill

ion

SSE

Gal

lons

- - -

Gallon Changes in U.S. OJ Demand forGallon Changes in U.S. OJ Demand forAssumed % Changes Demand Factors:Assumed % Changes Demand Factors:

Assumes U.S. Demand of 1,260 Million SSE Gallons

Income Own-Price

Cross-Price

FDOCTotal*

BrandTV*

TradePromo*

- - - - - FDOC Demand Factor - - - - - - - - - - - MAP Demand Factor - - - - - -

* Percentage shift in demand/100, all other factors constant: promotional elasticities in the case of a linear model.

5757

20082008--09 INTERSECTION OF09 INTERSECTION OFSUPPLY & DEMANDSUPPLY & DEMAND

SCENARIOSSCENARIOS

58

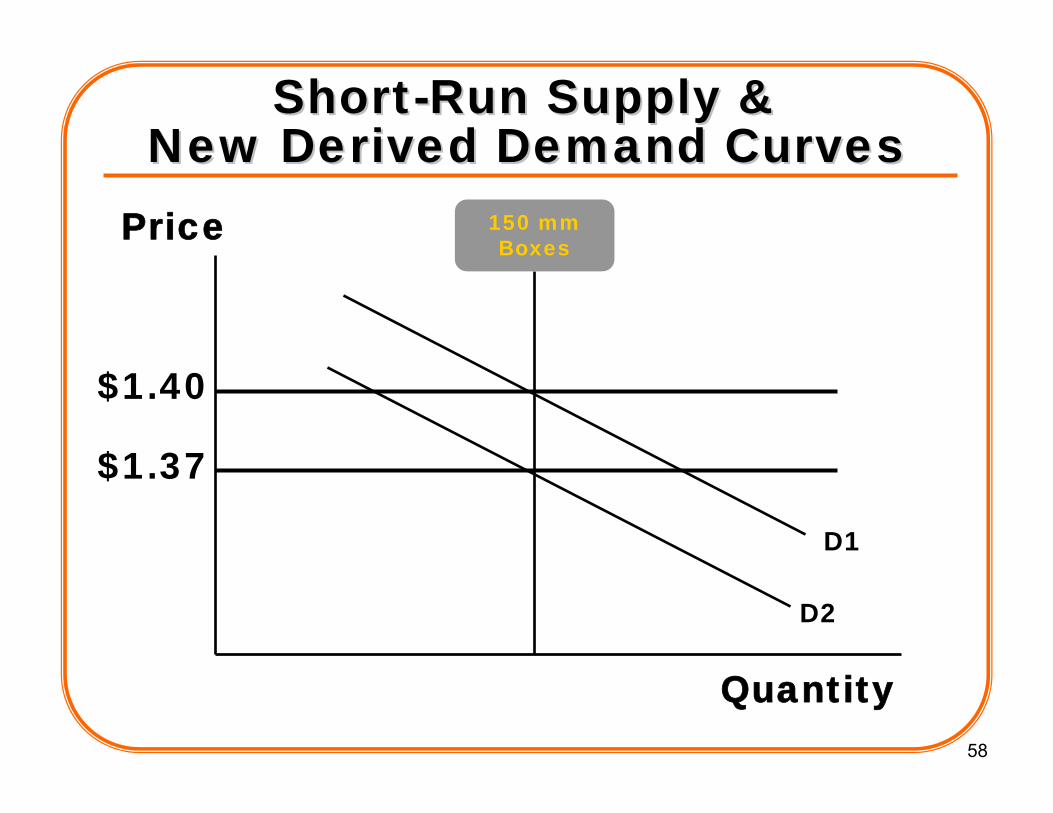

ShortShort--Run Supply & Run Supply & New Derived Demand CurvesNew Derived Demand Curves

Quantity

Price 150 mmBoxes

D1

$1.40

D2

$1.37

59

Quantity

Price$/ps

Long SustainabilityLong SustainabilitySupply & Demand EquilibriumSupply & Demand EquilibriumGreater Than BreakGreater Than Break--Even CostEven Cost

D1D2

$1.37$1.40

$1.25

6060

SUMMARYSUMMARY&&

CONCLUSIONSCONCLUSIONS

61

Florida OJ Sustainability:Florida OJ Sustainability:Economic ConsiderationsEconomic Considerations

61

Pest and Disease issues, along with weather disasters, impact the viability of Florida Growers

Costs are increasing and per-acre yields are decreasing rapidly

Shifts in demand are also impacting long-term sustainability

Today the intersection of supply and demand is slightly higher than break-even costs. Tomorrow??

Future studies can help the Industry determine the right levels of demand and supply enhancements

6262

Thank You!Thank You!