flexibility of wages and macroeconomic instability in an ... · pdf fileflexibility of wages...

TRANSCRIPT

Flexibility of wagesand macroeconomic instability

in an agent-based computational modelwith endogenous money

Pascal Seppecher∗

Workshop on Economic Heterogeneous Interacting AgentsESHIA/WEHIA 2010

We present a model of a dynamic and complex economy in which the cre-ation and the destruction of money result from interactions between multipleand heterogeneous agents. In the baseline scenario, we observe the stabiliza-tion of the income distribution between wages and profits. We then alter themodel by increasing the flexibility of wages. This change leads to the formationof a deflationary spiral. Aggregate activity decreases and the unemploymentincreases. The macroeconomic stability of the model is affected and eventuallya systemic crisis arises. Finally, we show that the introduction of a minimumwage would have allowed the aggregate demand to be boosted and to avoid thiscrisis.

JEL Codes: C63, E24, E27, E31

∗CEMAFI (Centre d’Etudes en Macroéconomie et Finance Internationale - Université deNice Sophia Antipolis). Email: [email protected]. The model presented is implemented asa Java application (Jamel: Java Agent-based MacroEconomic Laboratory). This application,together with the scenarios presented in this paper, is executable on the webpage http://p.seppecher.free.fr/jamel/.

1

1 IntroductionIn the General Theory, Keynes insists on the necessity of taking into account‘the complexities and interdependencies of the real world’ (Keynes, 1936). Hestrongly criticizes the methods which ‘expressly assume strict independence be-tween the factors involved’. For Keynes, it is ‘the nature of economic thinking’to ‘allow, as well as we can, for the probable interactions of the factors amongstthemselves.’

Among the complex problems approached by Keynes on the General Theory,we find the question of the effects of a decrease in nominal wages on the level ofunemployment, prices, and the equilibrium of the whole system. Keynes criti-cizes the view according to which unemployment would find its explanation inthe existence of ‘frictional resistances’ preventing wages to adapt to the aggre-gate demand of labor. For him, one can’t argue by supposing fixed the globaleffective demand:

(. . . ) whilst no one would wish to deny the proposition that a reduc-tion in money-wages accompanied by the same aggregate effectivedemand as before will be associated with an increase in employment,the precise question at issue is whether the reduction in money-wageswill or will not be accompanied by the same aggregate effective de-mand as before measured in money, or, at any rate, by an aggregateeffective demand which is not reduced in full proportion to the re-duction in money-wages (. . . ) (Keynes, 1936)

According to Keynes, the effects of a fall in nominal wages are not limitedto the labor market. Because the level of the effective demand can be modified,these effects can extend to prices of goods, and affect the stability of the wholeeconomy.

For if competition between unemployed workers always led to a verygreat reduction of the money-wage, there would be a violent insta-bility in the price-level. Moreover, there might be no position ofstable equilibrium except in conditions consistent with full employ-ment (Keynes, 1936)

Keynes paints the picture of the economy as a system in which the interac-tions between elements (households and firms) are real and monetary simulta-neously. Because in this system the interdependences are multiple, we cannotstudy the effects of the variation of one of its elements without examining theeffects on other elements and possibility of positive or negative feedback. Therepresentation of the economy that Keynes gives us corresponds to what we calla complex system today.

A complex system is a system composed of units interacting according tosimple rules, but which exhibits emergent properties, that is, macroscopic prop-erties arising from the interactions of the units that are not properties of theindividual units themselves (Tesfatsion 2006, Farmer and al. 2009a). If we

2

consider economic systems as complex systems, then agent-based modeling con-stitutes an essential tool to investigate their properties and study their dynamics(Arthur 2006, Leijonhufvud 2006, Howitt 2008).

In section 2, we describe the construction of an agent-based model of amonetary economy of production. In this model, real and monetary quantitiesare strictly distinguished. Money is endogenous: its flux and its reflux aredetermined by the interactions between the agents composing the system.

In section 3, we describe the behavior of the model. We observe the emer-gence of macroeconomic regularities characterized by the stability of the distri-bution of total income between wages and profits.

In section 4, we alter the model by increasing the flexibility of wages. We thenobserve a fall in aggregate demand. Firms react cutting prices and production.The development of the deflationary spiral leads to a systematic crisis. Finally,we show that the introduction of a minimum wage boosts demand and avoidsthe failure of the system.

2 The modelThe model presented follows the principles of the agent-based computationalapproach:

An agent-based model is a computerized simulation of a numberof decision-makers (agents) and institutions, which interact throughprescribed rules. (. . . ) Such models do not rely on the assumptionthat the economy will move towards a predetermined equilibriumstate, as other models do. Instead, at any given time, each agentacts according to its current situation, the state of the world aroundit and the rules governing its behavior. (Farmer and al. 2009b)

Seppecher (2009) gives a complete description of the model. However, in thisfirst version, the unique bank was perfectly accommodating. We abandon thishypothesis and instead assume that bankrupt firms do default. This assumptionopens the possibility of a bankruptcy of the banking system and thereby asystemic crisis.

2.1 General characteristicsThe model is formed by two coupled systems: the first one representing thereal sphere, the second the monetary sphere. The rules of functioning of thesetwo systems impose upon the agents. The model is implemented in an object-oriented language (Java) where the encapsulation of the real and monetary datawithin objects ensures:

• the respect of the physical constraints: rules of production, transfer anddestruction of the goods,

3

• the respect of the monetary constraints: rules of creation, transfer anddestruction of the money.

Figure 1 proposes a representation of the real and monetary interactionsprojected on two parallel plans.

Figure 1: The interactions of the agents at the real and monetary levels

The model contains three types of agents: firms (one hundred), households(one thousand) and banking sector (one single representative bank).

2.2 The bankIn its role of payment agent, the bank has no autonomy. It simply executesthe payment orders of the accounts holders, as long as accounts exhibit positivebalance.

In its role in production financing, the bank is accommodating: it acceptsall the applications for credit of firms.

When a firm is unable to pay off a credit in due terms, the bank grants itautomatically a new loan noted doubtful. The amount of this new loan is enoughto allow the firm to pay off at once the initial loan. On the other hand, whenone firm is unable to pay off a doubtful debt when due, the firm goes bankruptand disappears. The bank then has to absorb the defaulted debt.

4

For that purpose, the bank has a cash reserve (the bank’s capital) fromwhich it draws to erase the debt of the failing firm. The bank uses then itsresources (the payment of the interest by firms) to reconstitute its capital untilthe required level. The surplus of its resources is paid to its shareholders asdividends.

However, sometimes, the bank’s capital may be insufficient to face the bankruptcyof a debtor. The unique bank goes bankrupt itself and the simulation breaksoff.

2.3 FirmsAt the beginning of each period, every firm determines its objective of pro-duction. Firms do not observe exactly the condition of the goods market butinstead estimates it based on the level of their own stock of unsold goods. Whenits stocks are large, a firm lowers its levels of production and employment.

The firm then updates the wage offered on the labor market. There also, thereaction of the firm depends on its own estimate of the labor market situation.If during several consecutive periods the firm has experienced difficulties inrecruiting employees, then it increases its starting wage.

The firm can then calculate its payroll and determine its need for externalfinancing. The desired loan is automatically tuned by the bank. The firm postsits offer on the labor market. The households which answer this offer are paidand employed by the firm.

Once the phase of production is finished, the firm determines its price. Thenew price depends on the level of inventories after production. If the firm judgesthat the level of inventories is too high, it lowers the price, otherwise it increasesthe price. The firm posts then its offer on the goods market and satisfies thedemand of the households at that price.

The firm now must pay off the fallen debts. As we have already explained,if the firm has not enough money to pay off its doubtful debts, it immediatelygoes bankrupt and disappears. Its debt is erased, absorbed by the bank.

Each period, the profits of the firm are formed by its revenues from salesminus the costs of production (wages and interests on loans). When profits arepositive, the firm distributes a fraction to households through dividends andkeeps the rest to build up internal-financing for future production.

2.4 HouseholdsLike firms, households have only a limited knowledge of the labor market. Everyunemployed household makes a search: it consults the offers of a limited numberof employers chosen at random among all the offers posted on the labor market.The household holds the higher wage offer among the consulted offers. If thewage offer is higher than its reservation wage, the household accepts the joband it is hired at once by the firm. Otherwise, it remains unemployed for thisperiod. The level of the reservation wage depends on the number of periods

5

spent in unemployment. After a certain duration, the unemployed householdresigns to lower its reservation wage.

Once the labor market closed, the firms pay the employed households. Inexchange, these expend their labor power in the implementation of the processof production. The household income is the sum of the wage of the period andthe possible dividends paid by firms and bank. The households save a part oftheir income, and spend the other one on the goods market.

As on the labor market, the households have only a limited knowledge of thegoods market: each consults only a number limited of bids, and chooses amongthem the most interesting.

3 Baseline scenario

3.1 Emergence of a macroeconomic stabilityWe make a large number of simulations by varying one after the other each ofthe main parameters of the model. We find that the model is able to reproduceitself from one period to another, in a wide space of parameters, with strongregularities of behavior. Then we test these regularities by simulating an exoge-nous shock at given date by the rough variation of one of the parameters of themodel. Figures 2a and 2b show the consequences of two of these shocks on thedistribution of income between wages and profits.

(a) Productivity shock (b) Negative expenditure shock

Figure 2: Effects of an exogenous shock on the income distribution

At first, the macroeconomic stability of the model is deeply affected by theshock of productivity. This shock entails an increase of the profitability of firms,and thus an increase of the profits. But on the long term the effects of this shockease and disappear, the distribution of incomes finding its previous level.

In another scenario, to simulate the effects of a negative expenditure shock,we double the households saving propensity. Again, the shock entails in the shortterm a deep destabilization of the model. On the long term, the distributionof incomes is stabilised again, this time with a lower level for the share of theprofits. We can show that a new inverse shock, returning the households saving

6

propensity at its previous level, would allow to restore the previous levels of thedistribution.

Beyond these two examples, all the simulations we made show that there isa wide range of values in the space of the parameters of the model for which weobserve a long-term stability of the income distribution. The macroeconomicequilibrium of the model seems strongly connected to this stability.

Nothing in the behavior assigned to firms allowed to anticipate the stabilityof the distribution of incomes between wages and profits. We saw that firmsset the prices and the wages in a strictly independent way. In particular, everyfirm ignores its costs and can easily sell its production below its production cost(the latter being essentially formed by the payment of wages). Nevertheless, weobserve that the average price on the goods market settles above the productioncost at a level stabilising the average margin of firms and, thus, stabilising theshare of the profits in the total income.

The long-term stability of the income distribution between wages and profits,main appearance of the macroeconomic equilibrium of the model, is thus anemergent property of the model, testifying of the existence of a macroscopiccoordination between the price formation on the goods market and the wagesformation on the labor market.

This emergent property of the model illustrates the observation of Keynes,according to whom the stability of the income distribution constitutes a ‘well-known statistical phenomenon’:

The stability of the proportion of the national dividend accruing tolabour (...) is one of the most surprising, yet best-established, factsin the whole range of economic statistics, both for Great Britain andfor the United States. (. . . ) the result remains a bit of a miracle.(Keynes 1939)

3.2 Rigidity of wagesIn the baseline scenario, the resistance of the unemployed households to a de-crease of wages is fixed to 8 months on average (between 4 and 12 months). Forthese first months of unemployment, the reservation wage of each household isequal to the last wage earned by the household when it was employed. Afterthis laps, the household which did not find a job lowers its reservation wage of10 percent (figure 3a).

However, after the first five years of the simulation, the average durationof unemployment becomes established in approximately two and a half months(figure 3b). Most of the unemployed households thus find a job before loweringtheir reservation wage. In these circumstances, wages seem very sticky down-ward. This rigidity appears as responsible for the simultaneous presence ofvacancies and unemployed households (figure 3c). The orientation of the curveof Beveridge shows that the number of vacancies and the number of unemployedhouseholds varies in the same direction (figure 3d).

The households staying without a job in the baseline scenario appear to be

7

(a) (b)

(c) (d)

Figure 3: Rigidity of wages in the baseline scenario

responsible for their condition, because we notice simultaneously vacant jobs.The unemployment so observed is usually considered as ‘voluntary unemploy-ment’.

4 Experiments on the labor marketIn Seppecher (2010), we showed the essential role played by the banking systemin the emergence of the macroeconomic stability of the model. Here, we wonderif the rigidity of the labor market plays a role in this emergence.

By a first experiment, we test the stability of the model by increasing theflexibility of the nominal wages.

By a second experiment, on the contrary we strengthen the downward rigid-ity in nominal wages by introducing a minimum wage.

4.1 Flexibility of wagesWe modify the reference scenario by reducing, from 2030, the resistance of thehouseholds to a drop of wages. From this date the households agree to lowertheir reservation wage after 3 months of unemployment on average (between 2and 4 months).

At first sight, the results on the labor market are in accordance with theexpected effects. The unemployed households lower more quickly their reserva-tion wage (figure 4a). The average duration of unemployment is reduced (figure4b). The curves of the number of vacancies and the unemployment figures are

8

(a) (b)

(c) (d)

Figure 4: Flexibility of wages: effects on the labor market

disconnected (figure 4c). The curve of Beveridge takes a perpendicular directionto that observed in the baseline scenario (figure 4d).

However, the weakening of wages (figure 5a) affects the demand. The con-sumption passes under the production (figure 5b) and the inventory stocks offirms increase. Companies react by lowering their prices (figure 5c) but also byreducing the level of the production, what is translated into an increase of theunemployment (figure 5d).

This feedback on the labor market, by increasing the number of unemployedhouseholds, increases the competition between these, and leads them to acceptincessantly new reduction in wages. The deflation process, set off by the firstdrops of wages, grows and strengthens itself.

The curse of the Phillips curve illustrates the sinking of the economy inthe depression (figure 5e). The drop of nominal wages, faster than the drop ofprices, drives to a decline of the real wages (figure 5f). The income distributionis destabilised in favor of the share of the profits (figure 5g). Companies havemore and more difficulties to pay off the bank when due. Bad debts increase,bankruptcies grow, affecting the capital of the bank (figure 5h), until leadingthis one to failure.

Because the model is endowed with an unique bank representative of thewhole banking system, the bankruptcy of this bank translates the impossibilityto respect the reflux constraint of the money, imposed by the credit nature ofthe money. The crisis is systemic and the simulation breaks off.

9

(a) (b)

(c) (d)

(e) (f)

(g) (h)

Figure 5: Wages flexibility: effects on demand and activity

10

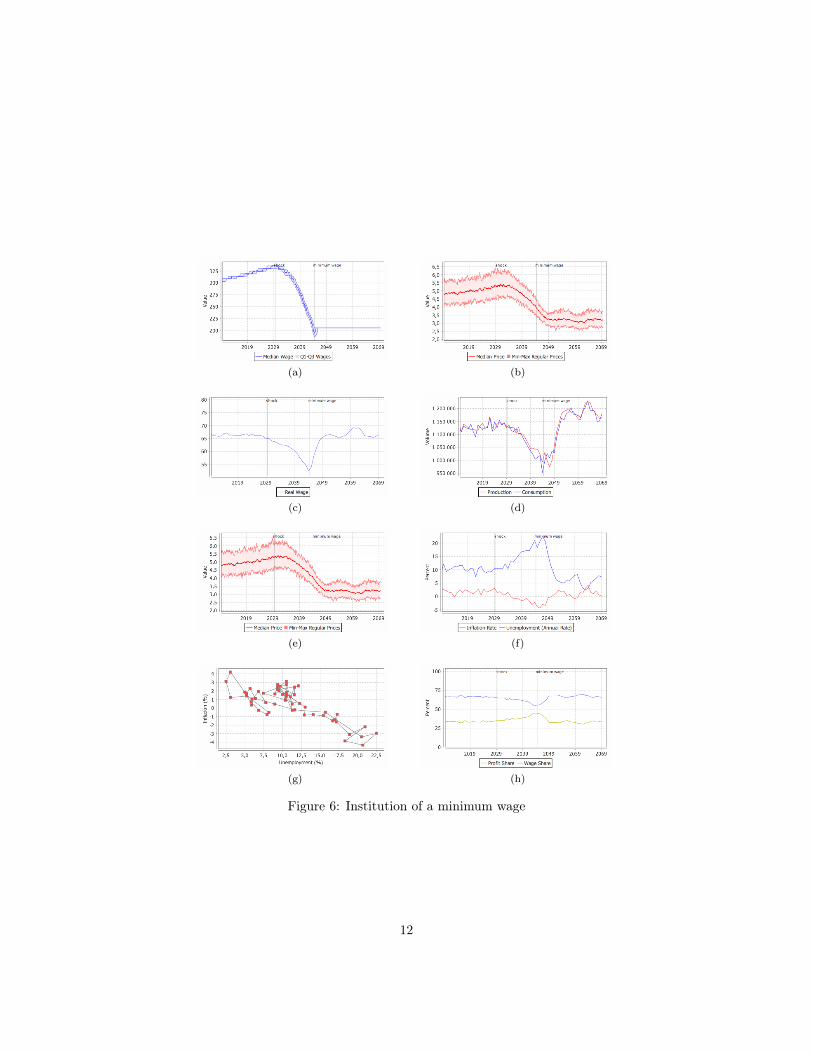

4.2 Institution of a minimum wageWe modify again the scenario. We keep the modification of the flexibility ofwages in 2030 but we introduce in 2045 a minimum wage.

The institution of the minimum wage interrupts the fall of wages (figure 6a).However, as at first the prices pursue their decline (figure 6b), the employedhouseholds see their real wage increasing (figure 6c). The consumption exceedsthe production (figure 6d) and the inventory stocks of firms fall. This demandrecovery leads firms to interrupt the drop of the prices (figure 6e) and to increasethe production.

The unemployment decreases (figure 6f) and the wage bill increases, feedingagain the demand. The economy goes up again along the Phillips curve (figure6g) and stabilises at levels of activity higher than those observed in the referencescenario. The distribution of incomes between wages and profits returns to levelsclose to those of the baseline scenario (figure 6h).

5 ConclusionAccording to Keynes,

Economics is a science of thinking in terms of models joined to theart of choosing models which are relevant to the contemporary world.(Keynes 1938)

The agent-based computational methods allow to model complex systemspopulated with a large number of autonomous and heterogeneous agents. Us-ing this approach, we built a computational model of a dynamic and complexeconomy in which the interactions between the agents are real and monetary.

We notice the emergence of a macroeconomic stability — characterized bythe long-term stability of the distribution of the total income between wagesand profits. In its basic version, this model contains a very rigid labor market.The unemployed households strongly resist against the fall in the nominal wagesthat firms try to impose. This resistance generates the simultaneous persistencyof a significant number of unemployed households and vacancies.

We have then modified the resistance to downward nominal wage flexibilityby forcing unemployed households to accept lower wages more easily. Whilehouseholds are more flexible to the demands of employers, we observed no sus-tained reduction in level of unemployment. In contrast, downward wage ad-justments lead to a weakening demand. This weakening of demand led firmsto lower commodity prices but also the level of production, with consequentincreases in unemployment. It sets up a self-feeding process of deflation thatonly the bankruptcy of the banking system will stop.

This scenario illustrates and confirms the reasoning of Keynes, which leadshim to assert that a fall of the nominal wages cannot assure the full employment,and could even destabilize prices and the whole economic system.

The following scenario, with institution of a minimum wage, confirms theimportance of wage rigidity for the emergence of the macroeconomic stability

11

(a) (b)

(c) (d)

(e) (f)

(g) (h)

Figure 6: Institution of a minimum wage

12

noticed in the baseline scenario. According to Keynes, it is the monetary char-acter of the considered economy that explains the importance of this rigidityfor the equilibrium of the system:

In fact we must have some factor, the value of which in terms ofmoney is, if not fixed, at least sticky, to give us any stability ofvalues in a monetary system. (Keynes 1936)

The model which we used remains still very simple with respect to the re-quirements expressed by Keynes in the General Theory. Nevertheless, no the-oretical obstacle seems to rule out extensions to the elements of the real worldwhich have been disregarded in this first version.

13

References• Arthur, W. Brian (2006) Out-of-Equilibrium Economics and Agent-Based

Modeling. In Leigh Tesfatsion & Kenneth L. Judd (ed.), Handbook ofComputational Economics, volume 2, chapter 32, pp. 1551-1564. Amster-dam: Elsevier/North-Holland.

• J. Doyne Farmer & John Geanakoplos (2009a) “The Virtues and Vices ofEquilibrium and the Future of Financial Economics”, Complexity, 14(3),pp. 11-38.

• J. Doyne Farmer & Duncan Foley (2009b) “The economy needs agent-based modelling”, Nature, Vol. 460, August 6, pp. 685-686.

• Peter Howitt (2008) Macroeconomics with intelligent autonomous agents.In Roger E.A. Farmer (ed.), The Small and the Large : Essays on Micro-foundations, Macroeconomic Applications and Economic History in Honorof Axel Leijonhufvud. Cheltenham: Edward Elgar.

• John Maynard Keynes (1936) The General Theory of Employment, Inter-est and Money. London: Macmillan.

• John Maynard Keynes (1938) Letter to Harrod. In Collected Writings ofJ.M. Keynes, volume XIV. London: Macmillan, 1973.

• John Maynard Keynes (1939) Relative Movements of Real Wages andOutput. The Economic Journal, Vol. 49, No. 193.

• Axel Leijonhufvud (2006) Agent-based macro. In Leigh Tesfatsion & Ken-neth L. Judd (ed.), Handbook of Computational Economics, volume 2,chapter 36, pp. 1625-1637. Amsterdam: Elsevier/North-Holland.

• Pascal Seppecher (2009) Un modèle macroéconomique multi-agents avecmonnaie endogène. Working Paper, 2009-11, Groupement de Rechercheen Economie Quantitative d’Aix-Marseille.

• Pascal Seppecher (2010) Dysfonctionnement bancaire, bulle du crédit etinstabilité macroéconomique dans une économie monétaire dynamique etcomplexe. La revue économique, Vol. 61, No. 3.

• Leigh Tesfatsion (2006) Agent-based computational economics: a con-structive approach to economic theory. In Leigh Tesfatsion & Kenneth L.Judd (ed.), Handbook of Computational Economics, volume 2, chapter 16,pp. 831-879. Amsterdam: Elsevier/North-Holland.

14