financing in the new decade possibilities, …

TRANSCRIPT

FINANCING IN THE NEW DECADE –POSSIBILITIES, OPPORTUNITIES AND CHALLENGES

Bangkok Fintech Fair 2021

“FEEL THE RAIN,FEAR THE STORM”

(! or ?)

Copyright © 2021 Accenture. All rights reserved. 2

DISRUPTABILITY INDEX 2.0

Copyright © 2021 Accenture. All rights reserved. 3

Regional Banks

Diversified Banks

Consumer Finance

Investment Banking and Brokerage

Diversified Capital Markets

Asset Management and Custody Banks

Specialized Finance

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.20 0.30 0.40 0.50 0.60 0.70 0.80

CU

RR

EN

T L

EV

EL

OF

DIS

RU

PT

ION

SUSCEPTIBILITY TO FUTURE DISRUPTION

VOLATILITY

DURABILITY VULNERABILITY

WEIGHTED AVERAGE: 0.46

WE

IGH

TE

D

AV

ER

AG

E:

0.5

2

VIABILITY #1 Segments

Related segments

Banking

#2 Total EV of companiesin sample

Other segments

BANKING INDUSTRY DISRUPTION MATRIX LEGEND & NOTES

$6.7 trillion

$36 billion

THE BANKING SECTOR HAS BECOME HIGHLY DISRUPTED AND REMAINS SUSCEPTIBLE TO FUTURE DISRUPTION

Copyright © 2021 Accenture. All rights reserved. 4

EVIDENCED BY THE CHANGING STRUCTURE OF THE BANKING INDUSTRY

• 17% of global banking players entered the market since 2005

• Nearly 1 in every 5 players is new to market

• Regulation and technology facilitated a proliferation of new competitors, particularly in the payments market

17%3,200New players

Banks licensed

after 2005

Players in 2005

Players Today

Banking Leavers

83%

Subsidiaries of incumbent

banks

PaymentInstitutions

Fintechs

24.000

-8.300

7001.900 600 19.300

New Players (#)

17% of Global Banking players entered; 35% of Banks Have Disappeared Since 2005

Traditional banks

Payments players

FinTech BigTechNeobanks

Copyright © 2021 Accenture. All rights reserved. 5

% NEW PLAYERS IN BANKING INDUSTRY

NEO BANKS% OF INDUSTRY REV.

TAKEN BY NEW PLAYERSFINTECH

NEO PAYMENTS

19% 3.5%

7%

38%

7.1%

1.9%

11% 2.2%

23% 1.6%

19% 0.4%

1.2%

0.2%

0.1%

1.6%

1.0%

0%

1.7%

6.4%

1.3%

0.4%

0.5%

0.2%

0.5%

0.5%

0.5%

0.2%

0.1%

0.2%

63% 13.7% 0.6% 12.2% 0.9%

14% 4.1% 0.6% 3.4% 0.1%

COUNTRY

YET IN ASIA PACIFIC NEW PLAYERS ARE YET TO CAPTURE A MEANINGFUL SHARE OF INDUSTRY REVENUE

DID YOU KNOW, SINCE 2005…

Source: Accenture, #Berelevant (Accenture Research)

Copyright © 2021 Accenture. All rights reserved. 6

Copyright © 2021 Accenture. All rights reserved. 7

THE EARLY PANDEMIC HINTED AT FINTECH VULNERABILITIES

Operational

Performance(% change,

YoY H1 2020

External Risk

Indicators(% change,

YoY H1 2020

Financial

Implications(% respondents,

negative

Impact)

Operational

Costs(% change,

YoY H1 2020

• Onboarding Expenditure 8%

• Data Storage Expenditure 11%

• Platform downtime1%

• Agent/partner downtime 5%

• # Unsuccessful transactions 7%

• Liquidity risk17%

• Cybersecurity risk 17%

• Foreign currency exposure risk 12%

• Capital Reserve 51%

• Current Valuation41%

• Future fundraising outlook34%

Extracts from World Economic

Forum – “The Global Covid-19

Fintech Market Rapid

Assessment Study

“If the banks do not change, we will change the banks”Jack Ma, Co-founder and Executive Chairman of the Alibaba Group

AND IN SOME CASES THE OPTIMISM AND ROSE COLOURED GLASSES HAVE BEEN DISPENSED WITH

Copyright © 2021 Accenture. All rights reserved. 8

WHAT ABOUT THE CONSUMER?

Copyright © 2021 Accenture. All rights reserved. 9

ACCENTURE’S 2020 GLOBAL FINANCIAL SERVICES CONSUMER STUDY

Copyright © 2018 Accenture. All rights reserved. 10

Last year we built on the success of our 2018 study and assessed what customer trends are now apparent in the market.

ConsumersSurveyed Banking and Insurance consumers.

PersonasDeveloped distinct personas based on a detailed cluster analysis of how they perceive and engage with banks and insurers.

CountriesIncludes respondents from countries across North America, Asia Pacific, Europe, Latin America, Middle East and Africa.

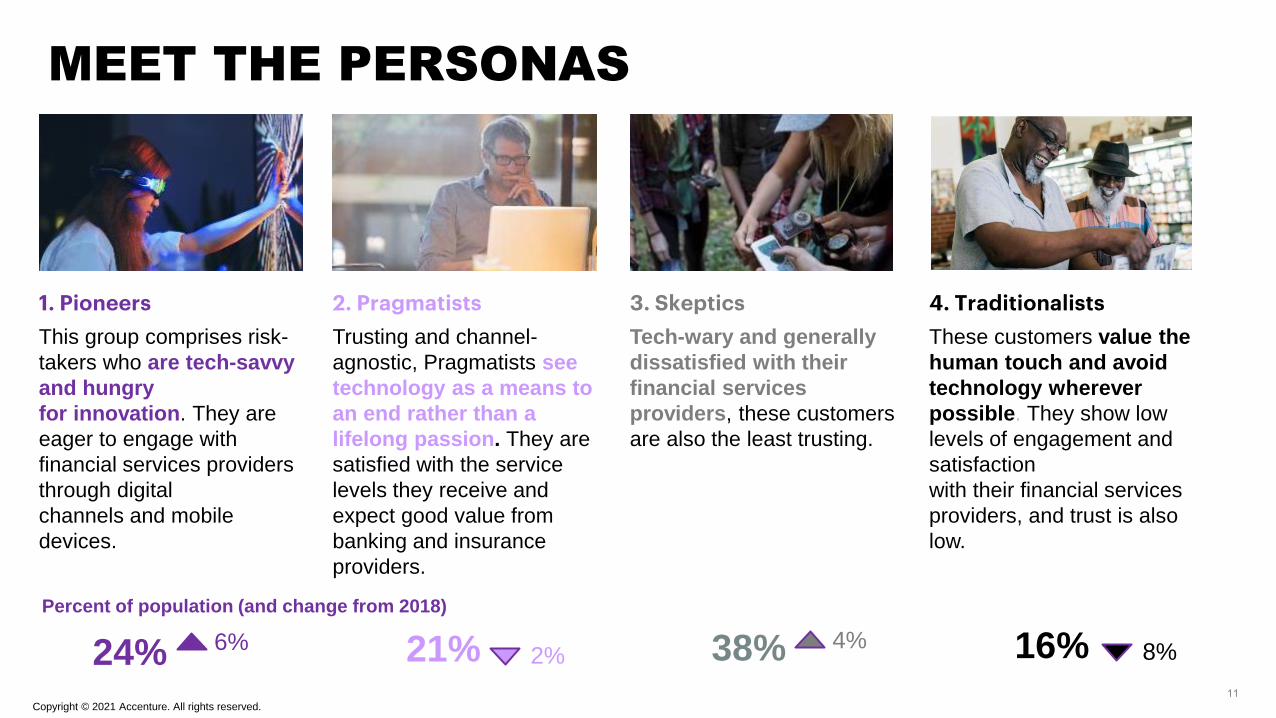

MEET THE PERSONAS

2. Pragmatists

Trusting and channel-

agnostic, Pragmatists see

technology as a means to

an end rather than a

lifelong passion. They are

satisfied with the service

levels they receive and

expect good value from

banking and insurance

providers.

4. Traditionalists

These customers value the

human touch and avoid

technology wherever

possible. They show low

levels of engagement and

satisfaction

with their financial services

providers, and trust is also

low.

1. Pioneers

This group comprises risk-

takers who are tech-savvy

and hungry

for innovation. They are

eager to engage with

financial services providers

through digital

channels and mobile

devices.

24% 21% 16%38%

3. Skeptics

Tech-wary and generally

dissatisfied with their

financial services

providers, these customers

are also the least trusting.

6%2%

4%8%

Percent of population (and change from 2018)

Copyright © 2021 Accenture. All rights reserved.

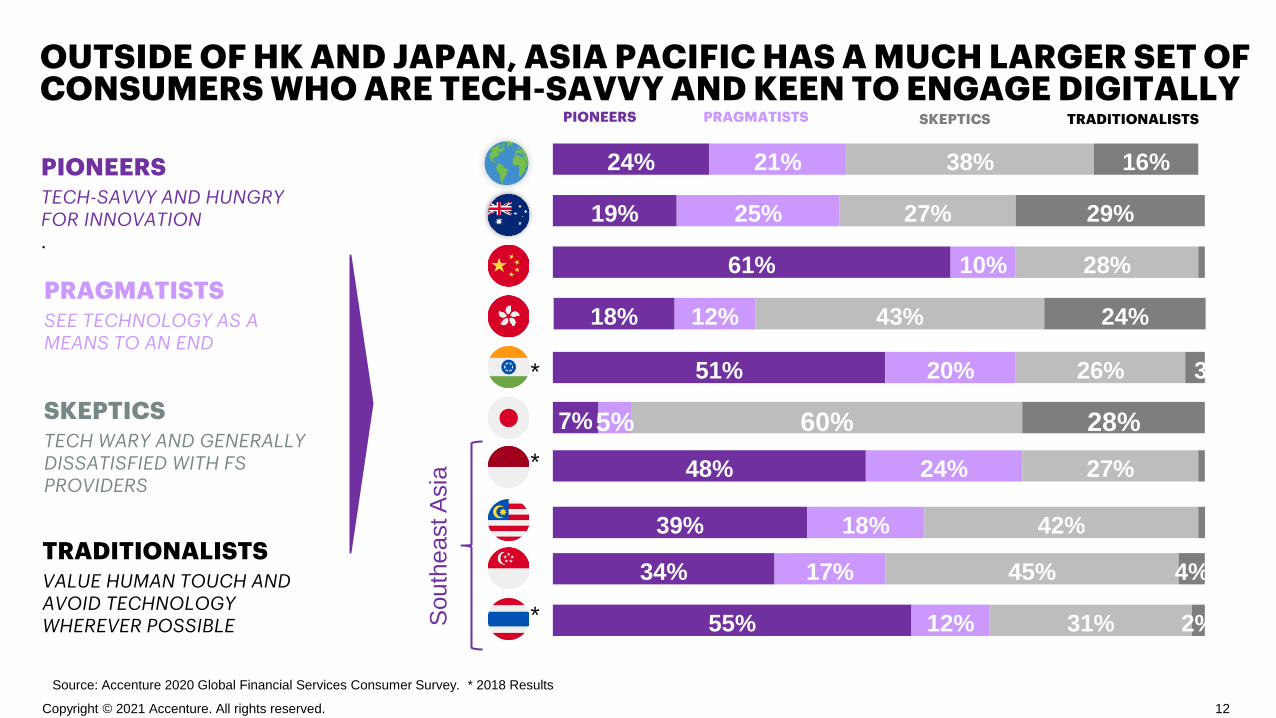

OUTSIDE OF HK AND JAPAN, ASIA PACIFIC HAS A MUCH LARGER SET OF CONSUMERS WHO ARE TECH-SAVVY AND KEEN TO ENGAGE DIGITALLY

TRADITIONALISTSVALUE HUMAN TOUCH AND AVOID TECHNOLOGY WHEREVER POSSIBLE

PRAGMATISTSSEE TECHNOLOGY AS A MEANS TO AN END

PIONEERSTECH-SAVVY AND HUNGRY FOR INNOVATION.

SKEPTICSTECH WARY AND GENERALLY DISSATISFIED WITH FS PROVIDERS

Copyright © 2021 Accenture. All rights reserved. 12

Source: Accenture 2020 Global Financial Services Consumer Survey. * 2018 Results

24% 21% 38% 16%

PIONEERS PRAGMATISTS TRADITIONALISTSSKEPTICS

19% 25% 27% 29%

61% 10% 28%

18% 12% 43% 24%

48% 24% 27%

34% 17% 45% 4%

55% 12% 31% 2%

51% 20% 26% 3%

39% 18% 42%

*

*

*

5% 60% 28%7%S

outh

east A

sia

COVID-19 ACCELERATED DIGITAL UPTAKE BY UP TO 5 YEARS

Source: Accenture 2020 Global Financial Services Consumer Survey.

VALUE AS OPPOSED TO EXPERIENCE IS NOW MOST IMPORTANT TO CONSUMERS

…

IS EXPERIENCE

BECOMING

UNDIFFERENTIATING?

Experience

Value

Copyright © 2021 Accenture. All rights reserved.

AND TRUST IN ALL INSTITUTIONS HAS FALLEN SIGNIFICANTLY – BUT MORESO FOR BANKS

Copyright © 2021 Accenture. All rights reserved.

Source: Accenture 2020 Global Financial Services Consumer Survey.

THE WAY FORWARD: A NEW ERA OF

“COOPETITION”?

Copyright © 2021 Accenture. All rights reserved.16

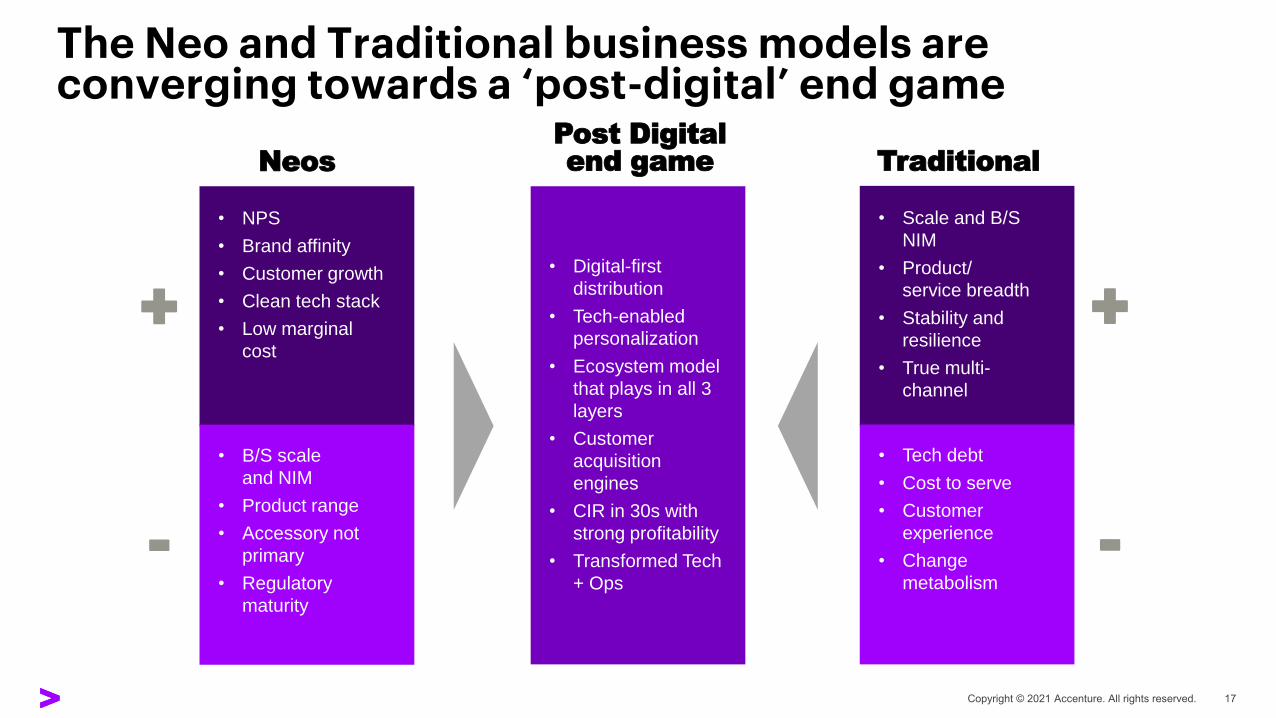

Neos

• NPS

• Brand affinity

• Customer growth

• Clean tech stack

• Low marginal

cost

• B/S scale

and NIM

• Product range

• Accessory not

primary

• Regulatory

maturity

+

-

Traditional

• Scale and B/S

NIM

• Product/

service breadth

• Stability and

resilience

• True multi-

channel

• Tech debt

• Cost to serve

• Customer

experience

• Change

metabolism

+

-

Post Digital end game

• Digital-first

distribution

• Tech-enabled

personalization

• Ecosystem model

that plays in all 3

layers

• Customer

acquisition

engines

• CIR in 30s with

strong profitability

• Transformed Tech

+ Ops

The Neo and Traditional business models are converging towards a ‘post-digital’ end game

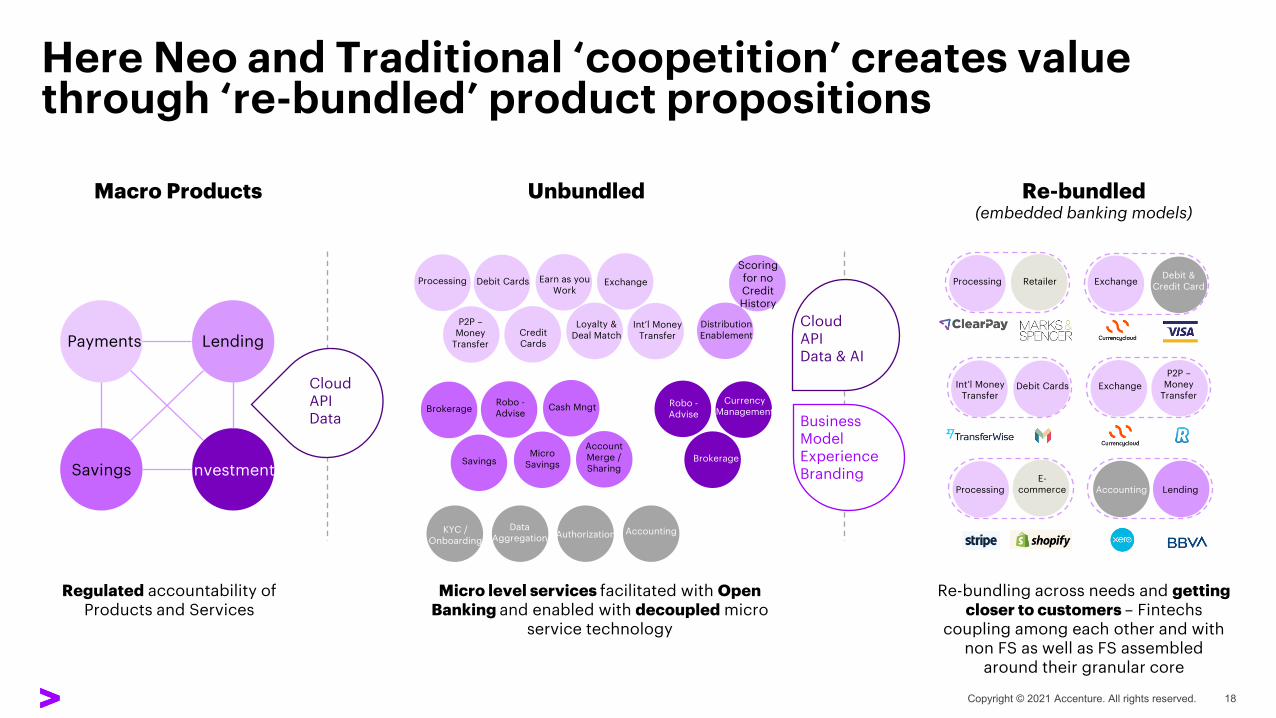

Here Neo and Traditional ‘coopetition’ creates value through ‘re-bundled’ product propositions

Macro Products Unbundled Re-bundled (embedded banking models)

Payments Lending

Savings Investment

Data Aggregation

KYC / Onboarding

Debit Cards

Credit Cards

P2P –Money

Transfer

Processing

BrokerageRobo -Advise

Micro SavingsSavings

Robo -Advise

Brokerage

Earn as you Work

Scoring for no Credit History

Loyalty & Deal Match

Distribution Enablement

Cash Mngt

Account Merge / Sharing

Processing Retailer

Authorization

Currency Management

Exchange Exchange

Business ModelExperienceBranding

Regulated accountability of Products and Services

Micro level services facilitated with Open Banking and enabled with decoupled micro

service technology

Re-bundling across needs and getting closer to customers – Fintechs

coupling among each other and with non FS as well as FS assembled

around their granular core

Cloud APIData & AI

Cloud APIData

Int’l Money Transfer

Int’l Money Transfer

Debit Cards Exchange

P2P –Money

Transfer

Data Aggregatio

n

Lending

Accounting

Accounting

Debit & Credit Card

E-commerceProcessing

Customer and revenue is shifting due to product componentization

Players who are emerging with niche product propositions are focusing on scale at speed

Product ‘unbundling’ happening at speed

Source: CBInsights

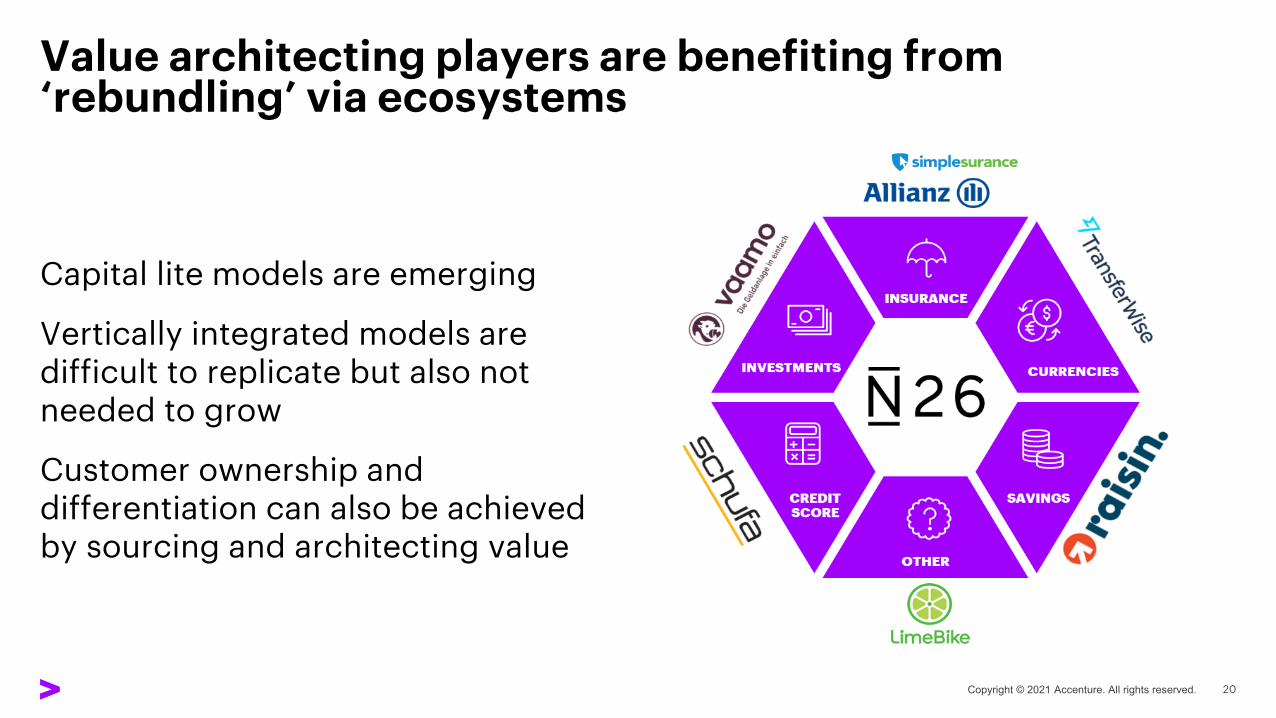

Capital lite models are emerging

Vertically integrated models are difficult to replicate but also not needed to grow

Customer ownership and differentiation can also be achieved by sourcing and architecting value

Value architecting players are benefiting from ‘rebundling’ via ecosystems

Digital Lending Market MapSMALL & MEDIUM BUSINESS

ANCILLARY TOOLSSERVICINGORIGINATIONPROSPECT& DATA

SERVICING ORIGINATIONPROSPECT & DATA

Non-Exhaustive

Prospecting & Intelligent Data: Vendors using data driven insights to identify prospects and/or make recommendations for next best product

Servicing: Vendors providing the system of record of loan data

Origination: Vendors improving the end-to-end loan cycle from initial credit application through underwriting and fulfillment of the loan

Ancillary Tools: Vendors offering tools that support digital loan origination

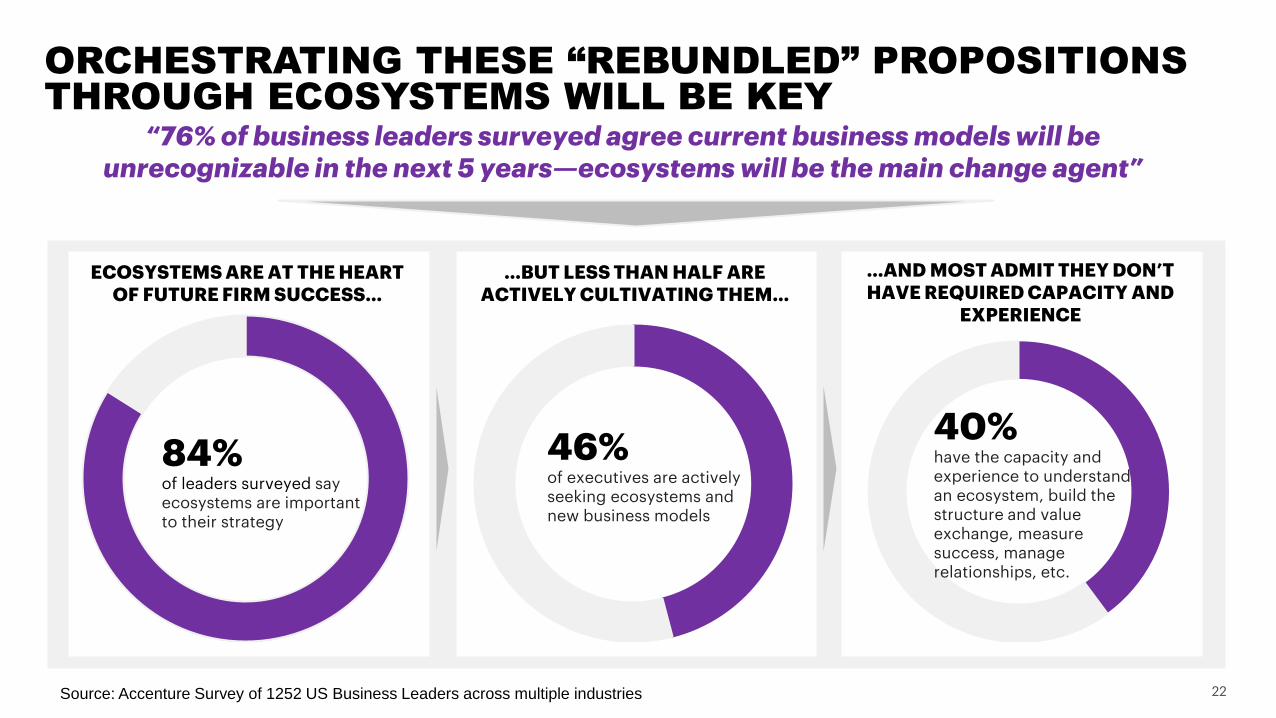

ORCHESTRATING THESE “REBUNDLED” PROPOSITIONS THROUGH ECOSYSTEMS WILL BE KEY

ECOSYSTEMS ARE AT THE HEART OF FUTURE FIRM SUCCESS…

84% of leaders surveyed say ecosystems are importantto their strategy

…BUT LESS THAN HALF ARE ACTIVELY CULTIVATING THEM…

46% of executives are activelyseeking ecosystems andnew business models

…AND MOST ADMIT THEY DON’T HAVE REQUIRED CAPACITY AND

EXPERIENCE

40% have the capacity and experience to understand an ecosystem, build thestructure and value exchange, measuresuccess, manage relationships, etc.

“76% of business leaders surveyed agree current business models will be unrecognizable in the next 5 years—ecosystems will be the main change agent”

Source: Accenture Survey of 1252 US Business Leaders across multiple industries

Some banks are already exploiting the opportunities driven by ‘rebundling’ product innovation

Current Product

From MACROproducts...

..to unbundling / componentization

...then to options of re-bundling / packaging

Re-bundled internally

Re-bundled internallywith externalcomponents

Provided for being re-bundled externally

Vertically bundled & sellable aaS to others

Own channels

Through others

VALUE:• Drivers of value and customer’s perceived value provider will be

different in each model

• Rebalance of componentization/commoditization vs specialized/differentiated

• Monetization of trust and trust intermediation leveraging brand promise and purpose

MODEL:

• 1to1 → XtoX for hyperpersonlization and real time bundling

• Impact on operating model and tech choices based on the model

• At scale execution of choices

external components internal components

Inputs to the PDB Intensity Index

Customers• Trusted• Empathetic• Personalized advice

Employees• Values and Culture• Fair treatment

Product Offering• Transparency• Best advice• Compliant

Source: Accenture Digital Maturity and PDB Index 2021. Sample of 70 Global Banks

Meanwhile winning requires purpose as well as digital leadership

1. Winners will need to be able to manage / execute across multiple business models at the same time

2. Traditional banking will shrink over time with value being created by consolidation, efficiency, and purpose

3. CX is becoming undifferentiated, and battleground is moving back toward ‘rebundled’ products

4. A key tech and ops decision is common enablement platform versus business portfolio approach

5. Technology excellence is critical, but it needs to be an enabler of strategy not an end in itself

We are entering a post-digital world

Copyright © 2018 Accenture. All rights reserved. Accenture Confidential Information | 26

THANK YOU