financial statements 20 12 - regional … statements 20 12 ... conducted our audits in accordance...

TRANSCRIPT

FINANCIAL STATEMENTS

2012

HALTON COMMUNITY HOUSING CORPORATION

1151 Bronte Road,Oakville, Ontario L6M 3L1

(905) 825-60001-866-442-5866

www.halton.ca

Approved by the Board on May 21, 2013

KPMG LLP Chartered Accountants Box 976 21 King Street West Suite 700 Hamilton ON L8N 3R1

Telephone (905) 523-8200 Telefax (905) 523-2222 www.kpmg.ca

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. KPMG Canada provides services to KPMG LLP. KPMG Confidential

INDEPENDENT AUDITORS' REPORT

To the Members of Board of Directors Halton Community Housing Corporation We have audited the accompanying financial statements of Halton Community Housing Corporation, which comprise the statement of financial position as at December 31, 2012, December 31, 2011, and January 1, 2011, the statements of operations, changes in net financial assets and cash flows for the years then ended, and notes, comprising a summary of significant accounting policies and other explanatory information. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of Halton Community Housing Corporation as at December 31, 2012, December 31, 2011, and January 1, 2011, the statements of operations, changes in net financial assets and cash flows for the years then ended, in accordance with Canadian public sector accounting standards.

Chartered Accountants, Licensed Public Accountants May 21, 2013 Hamilton, Canada

HALTON COMMUNITY HOUSING CORPORATION

STATEMENT OF OPERATIONSfor the year ended December 31, 2012(with comparative figures for the year ended December 31, 2011)

2012 2011

REVENUES Restated

Rental revenues 11,872,607$ 11,021,535$

Operating subsidies 6,153,276 5,789,484

Capital revenues 8,320,135 16,135,975

Other 331,861 350,531

Total Revenues 26,677,879 33,297,525

EXPENSES

Non-Profit Housing (Note 13) 10,849,541 10,340,448

Public Housing (Note 13) 12,732,676 11,867,954

Affordable Housing Program (Note 13) 2,329,649 262,947

Total Expenses 25,911,866 22,471,349

NET REVENUES 766,013 10,826,176

ACCUMULATED SURPLUS, BEGINNING OF YEAR 89,407,187 78,581,011

ACCUMULATED SURPLUS, END OF YEAR 90,173,200$ 89,407,187$

See accompanying notes to financial statements.

HALTON COMMUNITY HOUSING CORPORATION

for the year ended December 31, 2012(with comparative figures for the year ended December 31, 2011)

2012 2011

Restated

Net revenues 766,013$ 10,826,176$

Acquisition of tangible capital assets (2,465,203) (16,226,927)

Amortization of tangible capital assets 6,524,084 5,253,178

Change in prepaid expenses 29,462 (2,990)

Change in net debt 4,854,356 (150,563)

NET DEBT, BEGINNING OF YEAR (64,956,631) (64,806,068)

NET DEBT, END OF YEAR (60,102,275)$ (64,956,631)$

See accompanying notes to financial statements.

STATEMENT OF CHANGE IN NET DEBT

HALTON COMMUNITY HOUSING CORPORATION

as at December 31, 2012(with comparative figures as at December 31, 2011)

Cash provided by (used in): 2012 2011

OPERATING ACTIVITIES Restated

Net revenues 766,013$ 10,826,176$

Items not involving cash:

Amortization 6,524,084 5,253,178

Change in non-cash assets and liabilities:

Accounts receivable 1,758,075 (1,507,001)

Government subsidy receivable 739,846 (94,220)

Accounts payable and accrued liabilities (3,251,669) 2,957,096

Government subsidy payable (869,872) 12,610

Deferred revenue (435,510) (357,031)

Prepaid expenses 29,462 (2,990)

Net change in cash from operating activities 5,260,429 17,087,818

CAPITAL ACTIVITIES

Cash used to acquire tangible capital assets (2,465,203) (16,226,927)

Net change in cash from capital activities (2,465,203) (16,226,927)

INVESTING ACTIVITIES

Investments (309,062) (353,067)

Net change in cash from investing activities (309,062) (353,067)

FINANCING ACTIVITIES

Debt issued and assumed (1,877,807) 2,736,713

Long-term debt repaid (2,652,710) (2,497,611)

Net change in cash from financing activities (4,530,517) 239,102

NET CHANGE IN CASH (2,044,353) 746,926

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 3,694,931 2,948,005

CASH AND CASH EQUIVALENTS, END OF YEAR 1,650,578$ 3,694,931$

See accompanying notes to financial statements.

STATEMENT OF CASH FLOWS

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

1. AUTHORITY AND PURPOSE The Halton Community Housing Corporation (the “Corporation”) is incorporated with share capital under the Ontario Business Corporations Act to provide, operate and construct housing accommodation primarily for persons of low and moderate income.

The Corporation operates the following non-profit properties under Parts VI and VII of the Housing Services Act

(HSA): Walkers Fields, The Abbeyview, Sheridan Woods, Golden Briar Heights, Walkers Landing, Bray’s Lane, Maple Crossing, Donaghey Square, Glen Valley Place, Wellington Terrace.

Part VI of the HSA governs the following public housing, 100% rent geared to income properties: Holmesway Place, John Armstrong Terrace, Margaret Drive, Sargent Court, The Bruce Apartment, Longmoor Avenue, John R. Rhodes Residence, Harmony Court, Maurice Drive, Burloak Drive, Braeside, Pinedale, Lakeview Villa, Elm Road, Kin Court. Financing of these properties is held by the Province and are not reflected in the Corporation’s financial statements. The HSA is not applicable to the Brant Court, Martin House Seniors’ Residence and Aldershot Village Residence properties. The Martin House Seniors’ Residence and the Aldershot Village Residence are governed by contribution agreements with The Regional Municipality of Halton (the “Region”) and are subject to the requirements of the provincial Affordable Housing Program. The Corporation’s shares are 100% owned by the Region. The Region is also the Service Manager for the Corporation. The Corporation is exempt from tax under the Federal Income Tax Act. 2. CONVERSION TO PUBLIC SECTOR ACCOUNTING STANDARDS The Housing Services Act (HSA) was proclaimed into law on January 1, 2012 replacing and repealing the Social Housing and Reform Act (SHRA). A control assessment was performed and it was determined that due to the changes in legislation the Corporation is controlled by the Region for reporting purposes under the Canadian Public Sector Accounting (PSA) standards recommended by the Canadian Institute of Chartered Accountants (CICA). As an entity controlled by a local government, the Corporation is required to follow PSA standards. Beginning with the 2012 fiscal year, the Corporation has adopted the PSA standards without non-profit provisions in sections PS 4200 to PS 4270. These financial statements are the first financial statements for which the Corporation has applied PSA standards. Relating accounting changes have been applied retroactively with restatement of prior period results. Key adjustments on the Corporation’s financial statements resulting from the adoption of the PSA standards are as follows: (a) Investments Previously, the Corporation recorded its investments at fair value because they were classified as “held-for-trading” financial instruments. Unrealized gains and losses on investments and interest received were recorded in the related fund statement. PSA standards require that investments be recorded at cost with interest earnings recognized when received or receivable. Gains and losses on investments are recorded at the time of sale. (b) Deferred Revenue

Under the Canadian generally accepted accounting principles for non-profit organizations the Corporation was required to defer revenue recognition for the funding received for the construction of the Aldershot Village Residence and Martin House Seniors’ Residence and recognize the revenue over the useful life of the assets. PSA standards require revenue recognition for government transfers at the point in time when eligibility criteria are met and

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

2. CONVERSION TO PUBLIC SECTOR ACCOUNTING STANDARDS (continued) construction is complete. A portion of the funding received from the Service Manager for this purpose was recognized as revenue as a result of this change. (c) Tangible Capital Assets Prior to the adoption of PSA standards, the Corporation accounted for tangible capital assets in accordance with provisions of the SHRA. These practices are materially different from Canadian generally accepted accounting principles. Non-profit properties previously governed by Section 103 of the SHRA were recorded at historical cost with amortization for buildings provided at a rate equal to the annual principal repayments on the related mortgages. Under PSA standards the amortization of these properties is calculated based on the useful life of the building components. Public housing properties previously governed by Section 106 of the SHRA are financed by the Province of Ontario and these capital assets were not recorded on the Corporation’s financial statements. The Brant Court property transferred to the Corporation from the City of Burlington was not recorded in the Corporation’s financial statements. Under PSA standards these properties are recognized in the financial statements at their fair value at the time of contribution to the Corporation with amortization calculated based on the useful life of the building components. The Martin House Seniors’ Residence and Aldershot Village Residence properties, constructed in 2011, were recorded at cost with amortization reported based on the useful life of the building components in accordance with Canadian generally accepted accounting principles for non-profit organizations. This accounting treatment is substantially the same as the provisions under PSA standards. (d) Reserves and Reserve Funds

Under the Canadian generally accepted accounting principles for non-profit organizations the Corporation was required to present reserves and reserve funds as part of the Net Assets section on the Statement of Financial Position below assets and liabilities. Under PSA standards, funds transferred to the Corporation from the Service Manager for expenses relating to capital projects meet the definition of government transfers and are reported as part of deferred revenue until the funds are expended for the designated purpose. Operating and capital reserves funded from the annual surplus form part of accumulated surplus.

The impact of the conversion to PSA standards on the accumulated surplus at the date of transition on January 1, 2011

and the 2011 annual surplus is presented below. These accounting changes have been applied retroactively with

restatement of prior periods.

January 1, 2011

Accumulated surplus as originally reported, beginning of year $12,244,565

Adjustments to accumulated surplus:

Investments (228,727)

Deferred revenue 9,124,904

Tangible Capital Assets 67,177,690

Capital reserve balance reclassification (9,737,421)

Accumulated surplus as restated, beginning of year $78,581,011

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

2. CONVERSION TO PUBLIC SECTOR ACCOUNTING STANDARDS (continued)

December 31, 2011

Annual surplus (deficit) for the year as originally reported $(206,300)

Adjustments to annual surplus for the year:

Re-valuation of Investments (39,428)

Deferred revenue 12,524,276

Tangible Capital Assets (1,789,629)

Capital reserve balance reclassification 337,257

Annual surplus for the year as restated 10,826,176

Accumulated surplus, end of year as restated $89,407,187

The impact on the Statement of Cash Flows is as follows:

Previously stated

December 31, 2011

Adjustment

December 31, 2011

Restated

December 31, 2011

Amortization of capital costs $2,497,611 $2,755,567 $5,253,178

Unrealized gain on investment (39,427) 39,427 -

Government subsidy receivable (1,063,757) 969,537 (94,220)

Deferred revenue 13,474,039 (13,831,070) (357,031)

Tangible Capital Assets (15,260,989) (965,938) (16,226,927)

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The financial statements of the Corporation have been prepared in accordance with accounting standards issued by

the Public Sector Accounting Board (PSAB) of the Canadian Institute of Chartered Accountants (CICA). Significant

accounting policies adopted by the Corporation are as follows: (a) Basis of Accounting

The Corporation follows the accrual method of accounting for revenues and expenses. Revenues are normally recognized in the year in which they are earned. Expenses are recognized as they are incurred and are measurable as a result of receipt of goods or services.

(b) Deferred Revenue

Deferred revenue represents revenues which have been collected but for which the related services have yet to be performed or eligible expenses incurred. Deferred revenue is comprised of general and capital deferred revenue. Government transfers such as funds for capital projects are recognized when the transfer can be reasonably estimated, is authorized and eligibility criteria have been met.

(c) Amortization Methods

The cost, less residual value, of tangible capital assets is amortized on a straight-line basis over their estimated useful lives. Estimated useful lives for major categories of tangible capital assets are as follows: Buildings and Building Improvements 15 to 60 years Land Not Amortized Land Improvements 15 to 70 years

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

3. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Machinery and Equipment 5 to 60 years Land tangible capital assets are not amortized. For all other tangible capital assets, amortization commences in the year following acquisition, with a full year’s amortization charged in the final year of useful life. No amortization is calculated for assets not in service or under construction until they are available to be put into service.

(d) Contributed Assets

All assets contributed to the Corporation are recorded at their fair value at the time of contribution. Revenue at an equal amount is recognized at the time of contribution.

(e) Reserves and Reserve Funds

Under Provincial policy and as part of the funding agreements with the Service Manager, the Corporation is mandated to transfer annual surplus amounts up to a cumulative maximum of $300 per unit to the operating reserves. Remaining surplus amounts are transferred to reserves designated for capital expenditures. Withdrawals from the reserves must have Board of Directors approval.

(f) Government Transfers

Government transfers are received from the Service Manager and the Province for the provision of social housing services, building construction and other capital expenditures. The Corporation recognizes the transfer of government funding when the transfer can be reasonably estimated, is authorized and eligibility criteria have been met. Revenue is recorded on the Statement of Operations when the relating services are performed or eligible expenses incurred.

(g) Rental revenue

Rental and other revenue is recognized at the time the services are provided. (h) Investments

Investments consist of money market bond funds and are stated at the lower of cost and market value. Gains and losses on investments are recorded when incurred and interest is recorded when received or receivable.

(i) Cash and cash equivalents

Cash and cash equivalents include short-term investments with a term to maturity of 90 days or less at acquisition.

(j) Use of estimates

The preparation of financial statements, in conformity with Canadian Public Sector Accounting Standards, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the financial statements, and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

4. OAKVILLE SENIOR CITIZENS RESIDENCES (OSCR) OSCR is a non-profit corporation that operates subsidized senior citizens housing projects in the Town of Oakville. The operations of OSCR are governed by an independent Board of Directors and it is funded independently through rental income and subsidies from the Province. The OSCR property is owned by the Corporation and is included as part of tangible capital assets. Capital maintenance and improvements to OSCR’s buildings are the responsibility of the Corporation and such expenditures on behalf of OSCR are included in the Statement of Operations. As a result of this responsibility, OSCR is required to remit any net surplus it has for the year to the Corporation. The net surplus for the year is recorded as revenue on the Statement of Operations. The surplus remitted for the current year is $ nil (2011 - $ nil). 5. INVESTMENTS The Corporation’s investments include money market bond funds with a cost value of $11,156,369 (2011 - $10,847,307) and a market value of $11,317,808 (2011 - $11,115,462) at the end of the year. The market value represents the realizable value of the investments if they were to be sold at December 31, 2012. The investments are managed by Phillips, Hager & North Investment Funds Ltd. as per the provisions of the HSA. The Corporation’s discretion regarding the management of the funds is limited by the investment pooling provision contained in the HSA. 6. ACCOUNTS RECEIVABLE Accounts receivable recorded on the balance sheet are composed of the following:

2012 2011 GST/HST Receivable $431,898 $2,026,498 Other Receivables 84,916 299,381

Rents 324,840 273,850

Allowance for doubtful accounts (135,000) (135,000)

Total accounts receivable $706,654 $2,464,729

7. DEFERRED REVENUE The Corporation’s deferred revenue is comprised of general and capital deferred revenue. General deferred revenue consists of funding designated for specific operating expenditures that will occur in future periods. Funding for capital projects has been provided by the Service Manager under Provincial policy to ensure funds are available to maintain the housing stock in a state of good repair. The use of these funds is governed by Provincial policy and the Service Manager and requires the approval of the Board of Directors. These funds will be used for capital projects in conjunction with the capital reserve which forms part of the accumulated surplus.

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

Deferred revenue reported on the Statement of Financial Position is made up of the following:

2012 2011 Emergency shelter $18,318 $18,318 Capital deferred revenue 8,964,654 9,400,164

Total deferred revenue $8,982,972 $9,418,482

8. MORTGAGES PAYABLE Mortgages are secured by properties of the Corporation. The mortgages principal amount repaid this period was $2,652,710 (2011- $2,497,611) and mortgages interest paid and payable was $2,642,425 (2011- $2,789,083).

As at December 31, 2012, the unpaid balances of the mortgages are as follows:

Non Profit Properties:

2012

2011

Walkers Fields CMHC amortized over 20 years with a renewal date of June 1, 2015, at 4.39% per annum with blended monthly payments of $31,289, retires January 2025.

$3,524,130

$3,741,096

The Abbeyview CMHC amortized over 15 years with a renewal date of February 1, 2016, at 2.75% per annum with blended monthly payments of $31,521, retires December 2025.

4,133,994

4,395,294

Sheridan Woods CMHC amortized over 20 years with a renewal date of March 1, 2017, at 4.42% per annum with blended monthly payments of $30,372, retires April 2027. Golden Briar Heights Bank of Nova Scotia amortized over 22 years with a renewal date of September 1, 2015, at 4.318% per annum with blended monthly payments of $53,299, retires September 2027.

3,875,473

6,986,052

4,065,609

7,318,867

Walkers Landing Royal Bank amortized over 20 years with a renewal date of March 1, 2018, at 4.6872% per annum with blended monthly payments of $82,088, retires March 2028.

10,751,313

11,225,279

Bray’s Lane Toronto Dominion amortized over 30 years with a renewal date of July 1, 2028, at 5.94% per annum with blended monthly payments of $39,535, retires July 2028.

4,839,616

5,024,149

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

8. MORTGAGES PAYABLE (continued)

Non Profit Properties:

2012

2011

Maple Crossing Toronto Dominion amortized over 17 years with a renewal date of September 1, 2017 at 2.442% per annum with blended monthly payments of $47,487, retires September 2029.

7,834,725

8,154,072

Donaghey Square Bank of Nova Scotia amortized over 24 years with a renewal date of September 1, 2015, at 4.3184% per annum with blended monthly payments of $19,329, retires September 2029.

2,769,715

2,880,532

Glen Valley Place CMHC amortized over 22 years with a renewal date of June 1, 2018, at 3.65% per annum with blended monthly payments of $28,898, retires May 2030.

4,474,220

4,655,300

Wellington Terrace Toronto Dominion amortized over 22 years with a renewal date of January 1, 2018, at 4.726% per annum with blended monthly payments of $68,417, retires January 2030.

9,642,871

10,003,397

AHP Properties: Martin House Seniors’ Residence Halton Region amortized over 20 years at 4.5% per annum with blended monthly payments of $8,292, retires September 2032 Aldershot Village Residence Halton Region amortized over 20 years at 4.5% per annum with blended monthly payments of $6,087, retires November 2032

1,301,663

958,113

2,307,781

1,851,026

Total mortgages payable $ 61,091,885 $ 65,622,402

The annual principal repayments, assuming refinancing at the end of the term, for each of the five years subsequent to December 31, 2012 are as follows: 2013 - $ 2,871,699 2014 - 2,991,266 2015 - 3,112,844 2016 - 3,215,295 2017 - 3,344,636 2018+ 45,556,145 Total $ 61,091,885

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

9. TANGIBLE CAPITAL ASSETS Tangible capital assets are recorded at cost on the Statement of Financial Position. Contributed tangible capital assets are recorded at their fair value at the time of contribution. There were no contributed tangible capital assets during the year (2011 - $nil). During the year there were no write-downs of assets (2011 - $nil). The Corporation has no tangible capital

assets recognized at a nominal value. There was no interest capitalized in the year (2011 - $nil). There were no assets

under construction at the end of the current year (2011 - $295). The use of the tangible capital assets owned by the

Corporation is governed by the provisions of the HSA. As such, these assets must be used in the provision of social

housing and cannot be divested without prior consent of the Service Manager and the Minister.

The public housing properties held by the former Halton Housing Corporation and passed through to the

Corporation were originally financed by the Province of Ontario through general obligation provincial debentures.

At the time of the transfer of ownership of the Halton Housing Corporation to the Region, the Province did not

transfer the responsibility for the repayment of these debentures. Accordingly, the value of the provincial debentures

has not been recorded on the Corporation’s financial statements. The value of the debentures at the end of the year is

$10.9 million (2011 - $11.7).

The Martin House Seniors’ Residence property has been constructed on the land leased from the Region. The lease is

for a term of twenty (20) years. HCHC shall pay to the Region a nominal base rent of Two Dollars ($2.00) for the term.

The following charts summarize tangible capital asset balances by category for the years 2012 and 2011:

Opening

Balance Additions Disposals

Ending

Balance

Opening

Accumulated

Amortization

Balance Amortization Disposals

Ending

Accumulated

Amortization

Balance

Ending Net

Book Value

1-Jan-12 31-Dec-12 1-Jan-12 31-Dec-12 31-Dec-12

General

Buildings and Building Improvements $116,979 $1,296 $68 $118,207 $38,290 $3,466 $68 $41,688 $76,519

Land 50,573 - - 50,573 - - - - 50,573

Land Improvements 8,601 606 - 9,207 5,327 519 5,846 3,361

Machinery and Equipment 45,198 858 - 46,056 23,909 2,539 - 26,448 19,608

Total General Capital 221,351 2,760 68 224,043 67,526 6,524 68 73,982 150,061

Assets Under Construction 295 (295) - - - - - - -

Total Tangible Capital Assets $221,646 $2,465 $68 $224,043 $67,526 $6,524 $68 $73,982 $150,061

Opening

Balance Additions Disposals

Ending

Balance

Opening

Accumulated

Amortization

Balance Amortization Disposals

Ending

Accumulated

Amortization

Balance

Ending Net

Book Value

1-Jan-11 31-Dec-11 1-Jan-11 31-Dec-11 31-Dec-11

General

Buildings and Building Improvements $99,940 $17,117 $78 $116,979 $35,373 $2,995 $78 $38,290 $78,689

Land 50,573 - - 50,573 - - - - 50,573

Land Improvements 7,783 818 - 8,601 4,953 374 - 5,327 3,274

Machinery and Equipment 36,654 8,544 - 45,198 22,025 1,884 - 23,909 21,289

Total General Capital 194,950 26,479 78 221,351 62,351 5,253 78 67,526 153,825

Assets Under Construction 10,547 (10,252) - 295 - - - - 295

Total Tangible Capital Assets $205,497 $16,227 $78 $221,646 $62,351 $5,253 $78 $67,526 $154,120

Asset Type

(Dollars in Thousands)

(Dollars in Thousands)

Asset Type

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

10. ACCUMULATED SURPLUS Accumulated Surplus consists of the following:

2012 2011 Difference Public and Non-Profit Housing operating reserve $691,871 $691,871 $- Affordable Housing Program operating reserve 43,500 - 43,500 Affordable Housing Program capital reserve 342,405 91,528 250,877 Tangible Capital Assets 150,061,478 154,120,359 (4,058,881) Contributed capital 1,074 1,074 - Mortgages payable (61,091,885) (65,622,402) 4,530,517 Other 124,757 124,757 -

Total Accumulated Surplus $90,173,200 $89,407,187 $766,013

Capital and operating reserves have been established through Service Manager policy. The Corporation is mandated to place a cumulative amount of $300 per unit into the operating reserve. Remaining accumulated surplus is allocated to the capital reserve. As at December 31, 2012 the operating reserve was fully funded for all programs. Contributions to and withdrawals from the funds are governed by Service Manager policy and must have approval from the Board of Directors. Additional funds from the Service Manager designated specifically for capital projects are accounted for in accordance with PS 3410 Government Transfers. As such, these funds are recorded as deferred revenue until the funds are expended for the specified purposes as directed by the Board of Directors and the Service Manager. 11. PROVINCIAL CAPITAL GRANT In 2012 the Provincial Social Housing Capital Repairs (SHRRP) Fund has provided a grant for the following capital projects:

2012 Revenues

2012 Expenses

Abbeyview – Machine guarding of elevators $353 $353

Wellington Terrace - Machine guarding of elevators 6,350 6,350

Bruce Apartments - Machine guarding of elevators 5,957 5,957

Longmoor Avenue - Machine guarding of elevators 706 706

John R. Rhodes Residence - Machine guarding of elevators 1,412 1,412

Longmoor Avenue – Lighting replacement 16,332 16,332

Total provincial capital grant $31,110 $31,110

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

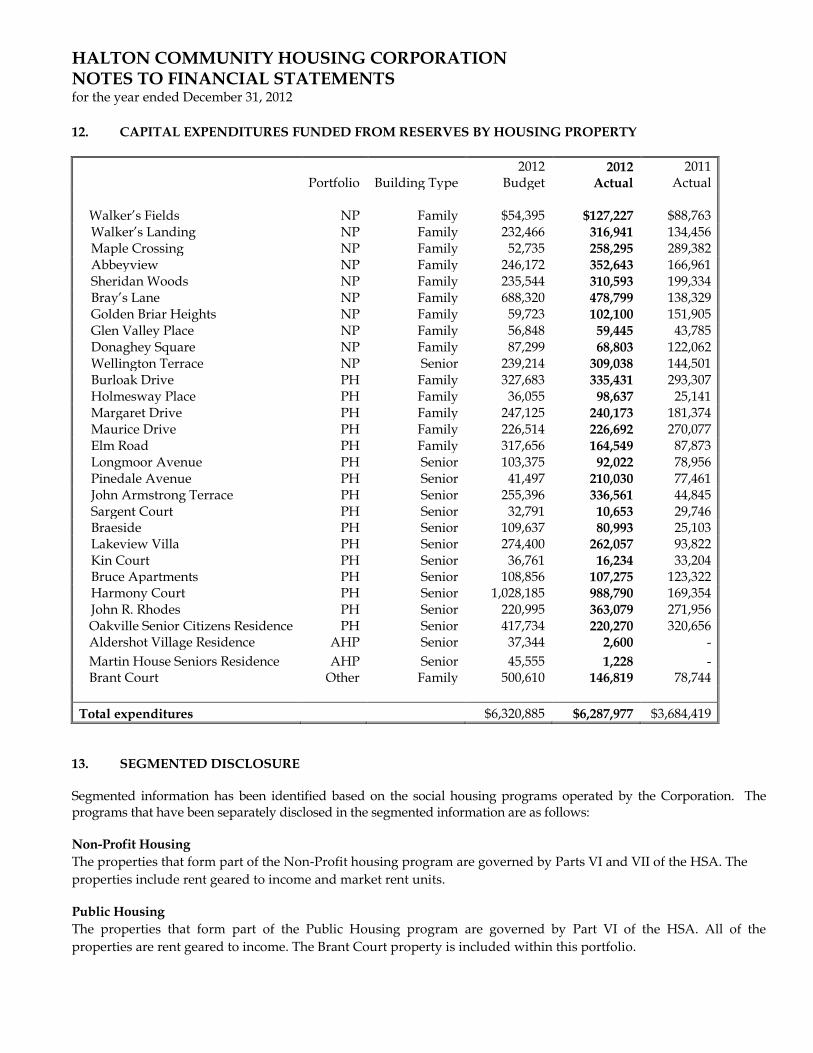

12. CAPITAL EXPENDITURES FUNDED FROM RESERVES BY HOUSING PROPERTY

Portfolio Building Type

2012 Budget

2012 Actual

2011 Actual

Walker’s Fields NP Family $54,395 $127,227 $88,763

Walker’s Landing NP Family 232,466 316,941 134,456 Maple Crossing NP Family 52,735 258,295 289,382 Abbeyview NP Family 246,172 352,643 166,961 Sheridan Woods NP Family 235,544 310,593 199,334 Bray’s Lane NP Family 688,320 478,799 138,329 Golden Briar Heights NP Family 59,723 102,100 151,905 Glen Valley Place NP Family 56,848 59,445 43,785 Donaghey Square NP Family 87,299 68,803 122,062 Wellington Terrace NP Senior 239,214 309,038 144,501 Burloak Drive PH Family 327,683 335,431 293,307 Holmesway Place PH Family 36,055 98,637 25,141 Margaret Drive PH Family 247,125 240,173 181,374 Maurice Drive PH Family 226,514 226,692 270,077 Elm Road PH Family 317,656 164,549 87,873 Longmoor Avenue PH Senior 103,375 92,022 78,956 Pinedale Avenue PH Senior 41,497 210,030 77,461 John Armstrong Terrace PH Senior 255,396 336,561 44,845 Sargent Court PH Senior 32,791 10,653 29,746 Braeside PH Senior 109,637 80,993 25,103 Lakeview Villa PH Senior 274,400 262,057 93,822 Kin Court PH Senior 36,761 16,234 33,204 Bruce Apartments PH Senior 108,856 107,275 123,322 Harmony Court PH Senior 1,028,185 988,790 169,354 John R. Rhodes PH Senior 220,995 363,079 271,956

Oakville Senior Citizens Residence PH Senior 417,734 220,270 320,656 Aldershot Village Residence AHP Senior 37,344 2,600 -

Martin House Seniors Residence AHP Senior 45,555 1,228 - Brant Court Other Family 500,610 146,819 78,744

Total expenditures $6,320,885 $6,287,977 $3,684,419

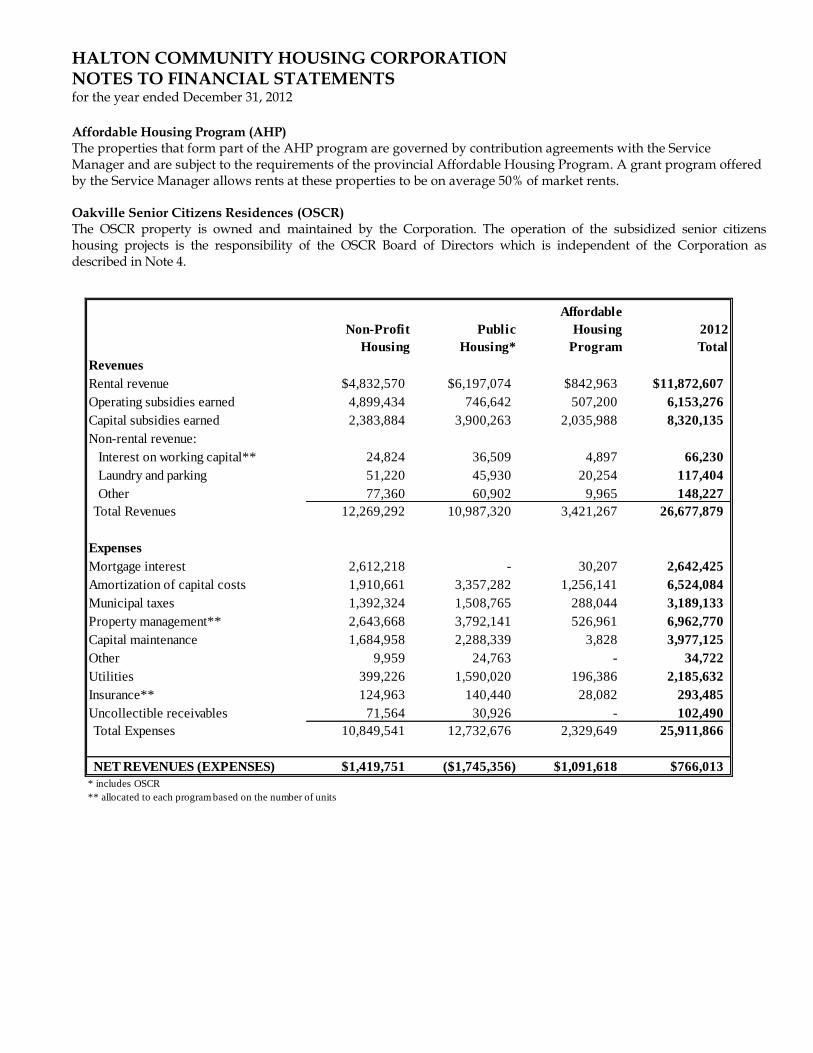

13. SEGMENTED DISCLOSURE Segmented information has been identified based on the social housing programs operated by the Corporation. The programs that have been separately disclosed in the segmented information are as follows: Non-Profit Housing

The properties that form part of the Non-Profit housing program are governed by Parts VI and VII of the HSA. The

properties include rent geared to income and market rent units. Public Housing

The properties that form part of the Public Housing program are governed by Part VI of the HSA. All of the

properties are rent geared to income. The Brant Court property is included within this portfolio.

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

Affordable Housing Program (AHP) The properties that form part of the AHP program are governed by contribution agreements with the Service Manager and are subject to the requirements of the provincial Affordable Housing Program. A grant program offered by the Service Manager allows rents at these properties to be on average 50% of market rents. Oakville Senior Citizens Residences (OSCR) The OSCR property is owned and maintained by the Corporation. The operation of the subsidized senior citizens housing projects is the responsibility of the OSCR Board of Directors which is independent of the Corporation as described in Note 4.

Non-Profit

Housing

Public

Housing*

Affordable

Housing

Program

2012

Total

Revenues

Rental revenue $4,832,570 $6,197,074 $842,963 $11,872,607

Operating subsidies earned 4,899,434 746,642 507,200 6,153,276

Capital subsidies earned 2,383,884 3,900,263 2,035,988 8,320,135

Non-rental revenue:

Interest on working capital** 24,824 36,509 4,897 66,230

Laundry and parking 51,220 45,930 20,254 117,404

Other 77,360 60,902 9,965 148,227

Total Revenues 12,269,292 10,987,320 3,421,267 26,677,879

Expenses

Mortgage interest 2,612,218 - 30,207 2,642,425

Amortization of capital costs 1,910,661 3,357,282 1,256,141 6,524,084

Municipal taxes 1,392,324 1,508,765 288,044 3,189,133

Property management** 2,643,668 3,792,141 526,961 6,962,770

Capital maintenance 1,684,958 2,288,339 3,828 3,977,125

Other 9,959 24,763 - 34,722

Utilities 399,226 1,590,020 196,386 2,185,632

Insurance** 124,963 140,440 28,082 293,485

Uncollectible receivables 71,564 30,926 - 102,490

Total Expenses 10,849,541 12,732,676 2,329,649 25,911,866

NET REVENUES (EXPENSES) $1,419,751 ($1,745,356) $1,091,618 $766,013

* includes OSCR

** allocated to each program based on the number of units

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

13. SEGMENTED DISCLOSURE (continued)

Non-Profit

Housing

Public

Housing*

Affordable

Housing

Program

2011

Total

Revenues

Rental revenue $4,730,676 $6,225,925 $64,934 $11,021,535

Operating subsidies earned 4,893,691 630,425 265,368 5,789,484

Capital subsidies earned 1,462,430 2,149,268 12,524,277 16,135,975

Non-rental revenue:

Interest on working capital** 26,153 38,463 - 64,616

Laundry and parking 51,308 16,247 586 68,141

Other 84,897 109,287 23,590 217,774

Total Revenues 11,249,155 9,169,615 12,878,755 33,297,525

Expenses

Mortgage interest 2,789,083 - - 2,789,083

Amortization of capital costs 1,898,588 3,354,590 - 5,253,178

Municipal taxes 1,416,632 1,514,474 25,865 2,956,971

Property management** 2,497,642 3,607,247 213,233 6,318,122

Capital maintenance 1,152,745 1,493,016 - 2,645,761

Other 17,047 55,675 - 72,722

Utilities 387,690 1,664,268 18,321 2,070,279

Insurance** 118,840 159,793 5,528 284,161

Uncollectible receivables 62,181 18,891 - 81,072

Total Expenses 10,340,448 11,867,954 262,947 22,471,349

NET REVENUES (EXPENSES) $908,707 ($2,698,339) $12,615,808 $10,826,176

* includes OSCR

** allocated to each program based on the number of units

HALTON COMMUNITY HOUSING CORPORATION NOTES TO FINANCIAL STATEMENTS for the year ended December 31, 2012

14. BUDGET COMPARISON The Board approves HCHC’s operating and capital budgets each year on a cash basis. Since the audited financial statements are prepared on a full accrual basis, reconciliation must be performed in order to present the annual budget. A summary of that reconiciliation for 2012 is as follows :

2012

Approved

Budget Adjustments*

2012

Full Accrual

Budget

2012

Actuals

Statement of Operations

Revenues

Rental revenues $11,747,458 $- $11,747,458 $11,872,607

Operating subsidies 9,637,537 (3,462,611) 6,174,926 6,153,276

Capital subsidies - 8,320,135 8,320,135 8,320,135

Other 184,122 - 184,122 331,861

Total Revenues 21,569,117 4,857,524 26,426,641 26,677,879

Expenses

Non-Profit Housing 10,577,677 212,373 10,790,050 10,849,541

Public Housing 9,497,180 3,690,897 13,188,077 12,732,676

Affordable Housing Program 1,494,260 1,035,565 2,529,825 2,329,649

Total Expenses 21,569,117 4,938,835 26,507,952 25,911,866

Net Revenues - (81,311) (81,311) 766,013

Statement of Changes in Net Debt

Net Revenues (81,311) 766,013

Acquisition of tangible capital assets (2,465,203) (2,465,203)

Amortization of tangible capital assets 6,524,084 6,524,084

Change in prepaid expenses 29,462 29,462

Change in Net Debt $4,007,032 $4,854,356

*Adjustments include revenue and expenses which were not budgeted (amortization) or included in capital budget (unit turnover). Given that certain budget information is not available in full accrual format, the assumption of using budget adjustments that equal the actual full accrual adjustments was used. These full accrual budget estimates are unaudited and for financial statement presentation only.